the way ahead - financial services compensation … way ahead annual report 2001/02 of the financial...

TRANSCRIPT

Financial Services Compensation Scheme

7th Floor, Lloyds Chambers, 1 Portsoken Street, London E1 8BN

Telephone +44 (0)20 7892 7300 Facsimile +44 (0)20 7892 7301

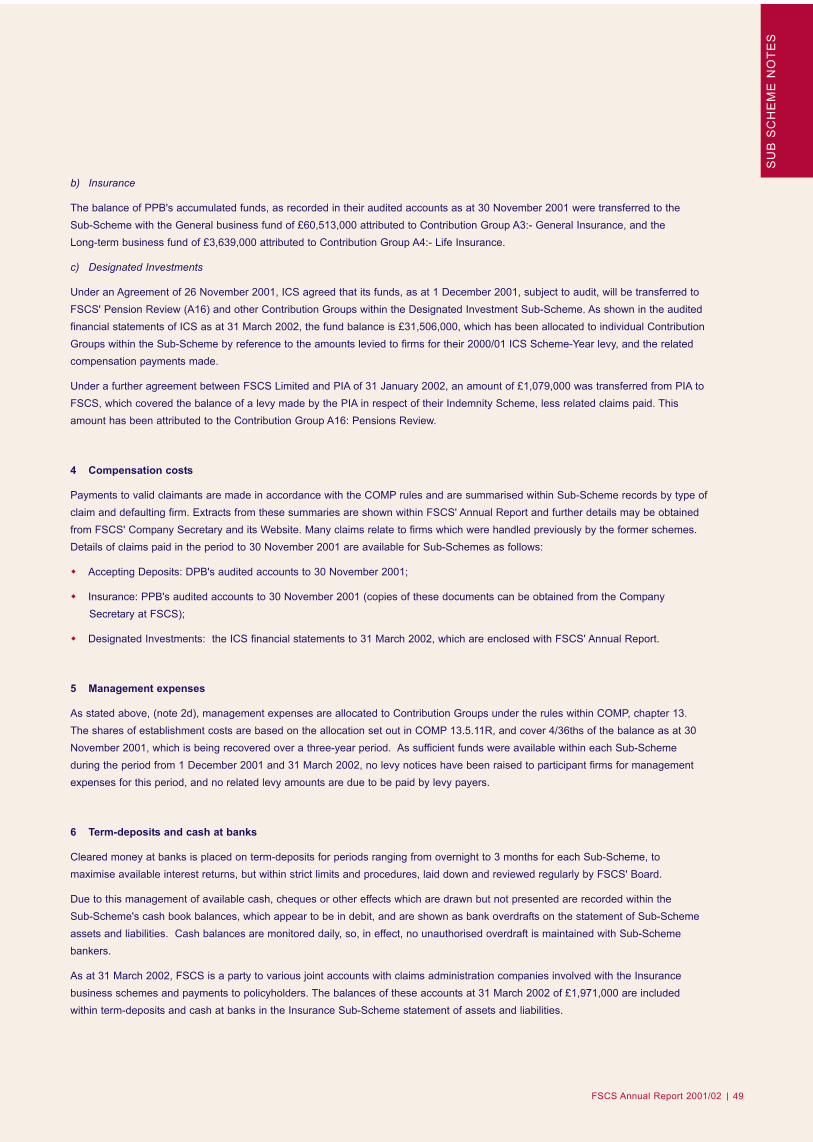

www.fscs.org.uk

design: orbital www.orbital-web.co.uk

The Way Ahead

Annual Report 2001/02 of the Financial Services Compensation Scheme

Financial Services Compensation Scheme

Financial Services Compensation Scheme

Annual Report and Accounts

2001/02

Photography: Grantly Lynch Photography Ltd

Design: Orbital Print: Newnorth Print Ltd

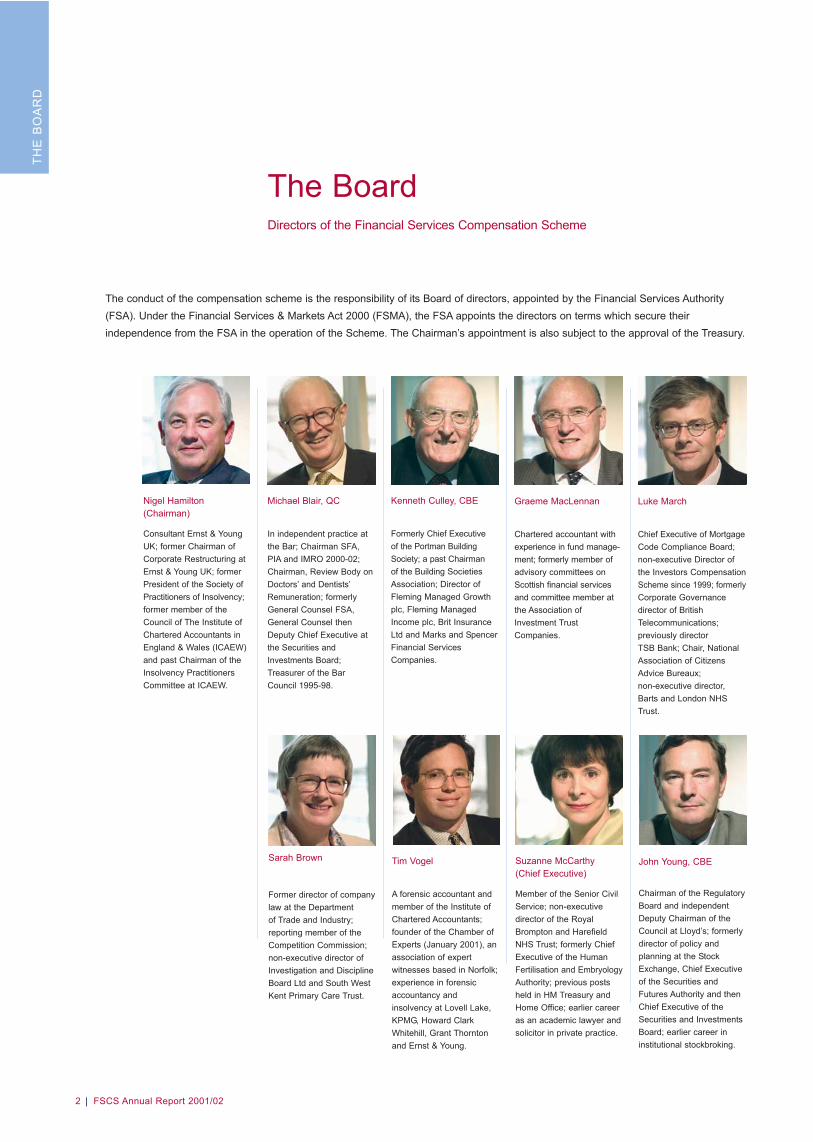

Graeme MacLennan

Chartered accountant withexperience in fund manage-ment; formerly member ofadvisory committees onScottish financial servicesand committee member atthe Association ofInvestment TrustCompanies.

Suzanne McCarthy (Chief Executive)

Member of the Senior CivilService; non-executivedirector of the RoyalBrompton and HarefieldNHS Trust; formerly ChiefExecutive of the HumanFertilisation and EmbryologyAuthority; previous postsheld in HM Treasury andHome Office; earlier careeras an academic lawyer andsolicitor in private practice.

Luke March

Chief Executive of MortgageCode Compliance Board;non-executive Director ofthe Investors CompensationScheme since 1999; formerlyCorporate Governancedirector of BritishTelecommunications; previously director TSB Bank; Chair, NationalAssociation of CitizensAdvice Bureaux;non-executive director,Barts and London NHSTrust.

John Young, CBE

Chairman of the RegulatoryBoard and independentDeputy Chairman of theCouncil at Lloyd’s; formerlydirector of policy and planning at the StockExchange, Chief Executiveof the Securities andFutures Authority and thenChief Executive of theSecurities and InvestmentsBoard; earlier career ininstitutional stockbroking.

Michael Blair, QC

In independent practice atthe Bar; Chairman SFA,PIA and IMRO 2000-02;Chairman, Review Body onDoctors’ and Dentists’Remuneration; formerlyGeneral Counsel FSA,General Counsel thenDeputy Chief Executive atthe Securities andInvestments Board;Treasurer of the BarCouncil 1995-98.

Sarah Brown

Former director of companylaw at the Department of Trade and Industry; reporting member of theCompetition Commission;non-executive director ofInvestigation and DisciplineBoard Ltd and South WestKent Primary Care Trust.

Kenneth Culley, CBE

Formerly Chief Executive of the Portman BuildingSociety; a past Chairman of the Building SocietiesAssociation; Director ofFleming Managed Growthplc, Fleming ManagedIncome plc, Brit InsuranceLtd and Marks and SpencerFinancial ServicesCompanies.

Tim Vogel

A forensic accountant andmember of the Institute ofChartered Accountants;founder of the Chamber ofExperts (January 2001), anassociation of expertwitnesses based in Norfolk;experience in forensicaccountancy andinsolvency at Lovell Lake,KPMG, Howard ClarkWhitehill, Grant Thorntonand Ernst & Young.

The BoardDirectors of the Financial Services Compensation Scheme

The conduct of the compensation scheme is the responsibility of its Board of directors, appointed by the Financial Services Authority(FSA). Under the Financial Services & Markets Act 2000 (FSMA), the FSA appoints the directors on terms which secure their independence from the FSA in the operation of the Scheme. The Chairman’s appointment is also subject to the approval of the Treasury.

Nigel Hamilton(Chairman)

Consultant Ernst & YoungUK; former Chairman ofCorporate Restructuring atErnst & Young UK; formerPresident of the Society ofPractitioners of Insolvency;former member of theCouncil of The Institute ofChartered Accountants inEngland & Wales (ICAEW)and past Chairman of theInsolvency PractitionersCommittee at ICAEW.

THE

BO

AR

D

FSCS Annual Report 2001/022

contentsThe Board 2

What is the Financial Services Compensation Scheme? 4

Chairman’s statement 6

Key facts and figures 8

Chief Executive’s statement 10

The work of the Industry Committees 12

Organisation chart 13

The work of our departments 14

Corporate Governance 20

Report & AccountsDirectors’ Report 24Report of the Auditors 26Financial Statements 27Notes to the Financial Statements 30Sub-Schemes and Contribution Groups 40

What is the Financial Services Compensation Scheme?

The Financial Services Compensation Scheme (FSCS) acts as a 'safety net' for customers of finance sector firms. The primary aim ofthe Scheme is to provide protection for private individuals and small businesses. FSCS compensates consumers if an authorised firm isunable or likely to be unable to pay claims against it, usually because it has gone out of business or is insolvent. The Scheme coversinvestments, deposits and insurance.

The Scheme is funded by the financial servicesindustry. Its existence promotes financialstability and lessens the risk of a single failuretriggering a wider loss of confidence in thatsector.

Deposit protectionFSCS provides protection for customers ofdeposit-taking firms, for example, banks andbuilding societies. Credit unions will be includedin the Scheme from July 2002.

The Scheme is triggered when an authorisedfirm goes out of business, for example, if it issubject to an insolvency action, such asliquidation or administration, or when the FSAconsiders that it is unable to repay its depositorsor is likely to be unable to do so.

InsurancePolicyholders are eligible for protection if theyare insured by an authorised insurance firmunder a contract of insurance issued in the UK,or, in some cases, within the EuropeanEconomic Area (EEA), Channel Islands or theIsle of Man. Re-insurance, marine, aviation,transport business, credit insurance and Lloydspolicies are excluded, as are risks outside theEEA.

Policyholder protection is triggered if anauthorised firm is unable or likely to be unableto meet claims against it, for example, if it has

been placed in liquidation or provisional liquida-tion. If this should happen the Scheme will seekto take measures to safeguard policyholders, forinstance, by trying to ensure that policies aretransferred to another firm. If this is not possi-ble, compensation may be payable.

The level of protection depends on the type ofinsurance policy.

InvestmentsThe Scheme covers losses should anauthorised investment firm be unable or likely tobe unable to pay claims made against it:

� when it cannot return its customer's invest-ments or money; or

� for loss arising from bad investment adviceor poor investment management.

FSCS can only pay compensation for the latterif such advice was given or the investmentmanagement took place only after the date ofthe firm's authorisation which, in any event,must be on or after 28 August 1988.

Eligibility for compensationNotwithstanding FSCS' existence, consumersstill have responsibility to take care of theirmoney. There are limits to the amount ofcompensation that FSCS can pay, depending onthe basis of the claim.

1 The eight schemes are the Building Societies Investor Protection Scheme, the Deposit Protection

Scheme, the Friendly Societies Protection Scheme, the Investors Compensation Scheme, the PIA

Indemnity Scheme, the Policyholders Protection Scheme, the Section 43 Scheme and the arrangement

between the Association of British Insurers and the Investors Compensation Scheme Ltd for paying

Pension Review compensation to widows, widowers and dependents of deceased persons.

FSCS Annual Report 2001/02

FSCS was createdunder the Financial

Services and MarketsAct 2000 (FSMA), andbecame operational on

1 December 2001.

At that time it replacedeight existing compen-

sation schemes1 and theassets and liabilities of

the pre-existingschemes were

transferred to FSCS.

FSCS also assumedresponsibility for any

outstanding claims thathad been made to those

schemes before 1December 2001.

FSCS Annual Report 2001/024

WH

ATIS

FS

CS

?

To qualify for compensation claimants need tobe eligible under the Scheme's rules. Theseform part of the FSA's Handbook.

Compensation limitsThe maximum levels of compensation payable are2 :

Claims against deposit takers:

£31,700 (100% of £2,000 and 90% of the next£33,000).

Deposits in all currencies are covered.

Claims against investment firms:

£48,000 (100% of £30,000 and 90% of the next£20,000).

Claims against insurance firms:

� Long-term insurance (such as pensions and life assurance): 100% of the first £2,000plus 90% of the rest of the claim.

� General insurance: 100% of the first £2,000 plus 90% of the rest of the claim.

� Compulsory insurance: 100% of claim.

When we can help - a fewexamplesMr X was advised that he would be better off ifhe transferred his pension from an occupationalpension scheme to a personal pension.

When he discovers that the advice had beeninappropriate and he has lost money as a result,he finds that the independent financial adviserhe dealt with is no longer in business.

Mrs Y's car was damaged in an accident andshe wishes to make a claim against an insurerthat goes into provisional liquidation. Her policystill has six months cover left on it.

Mr & Mrs Z have a current and savings accountwith a bank that goes out of business.

Mr B was advised to buy an investment productthat was inappropriate for his needs. The investment firm that sold it to him is nolonger in business.

Mrs K has a claim for flood damage on herhome insurance policy, but the insurer has goneinto liquidation.

2 These limits apply to claims against firms declared in default after 1 December 2001. For claims against

firms declared in default before this date the rules (and compensation limits) of the pre-existing

compensation schemes apply, although FSCS will still handle the claim.

FSCS Annual Report 2001/02

For further informationabout FSCS, visit ourwebsite atwww.fscs.org.uk, telephone our Helplineon 020 7892 7300 [email protected]

AB

OU

TFS

CS

FSCS Annual Report 2001/02 5

At that time we also started providing opera-tional resources to the Deposit ProtectionBoard, and throughout 2001/02 we workedclosely with the Policyholders Protection Board.

I would especially like to thank the Chairmen,the Boards and staff of those schemes not onlyfor their past work, but also for their support andco-operation during the building of FSCS.

On 1 December 2001 FSCS was officially born.I am delighted to confirm that the transition wentsmoothly.

I am further pleased to report that at the end ofFSCS' first year our management costs weresome 23% less expensive than if the separatecompensation schemes had continued tooperate. Rationalisation does make excellentfinancial and operational sense!

Operational controlsImportant to the creation of a thriving FSCS wasthe design during the year of strong operationalcontrols, not only to ensure that our servicescontinue to be robust during periods of normaloperations, but also for those times whenbusiness continuity may be threatened byunforeseen events. FSCS takes risk manage-ment extremely seriously, and will work with itsinternal auditors to make certain that itsprocedures are tight and sufficient for theirpurposes.

During the coming year we will continue toconcentrate on improving our processes andprocedures for the benefit of all ourstakeholders.

Prime objectivesOur prime objectives are to ensure that eligibleconsumers, be they protected depositors,investors or policyholders, have access toappropriate compensation in a timely fashion,and to provide our services as efficiently andeffectively as possible.

Having a single scheme promotes cost efficien-cies, and provides a single point of contact forboth consumers and levy payers. It also enablesus to pursue operational improvements that theprevious, smaller schemes found difficult tointroduce.

Raising awarenessRaising awareness about the work of theScheme has also been a key aim during thepast year.

During November we published the first issue ofour bi-annual newsletter, Outlook, speciallywritten for the financial industry.

In addition, we have been working closely withprofessional trade bodies to ensure that theirmembers understand the Scheme's role, and toensure that we are aware of issues that mayimpact on FSCS.

Developing these relationships has proved valu-able, and I look forward to their continuation.

We also commissioned MORI to conductresearch into consumer attitudes towards thesafety of their money and investments, and theirgeneral awareness of compensation.

Chairman’s statementNigel Hamilton

This is our second Annual Report, and our first as the UK's single financial services compensation scheme. Our first report, On our way,explained how we were preparing to take over responsibility for financial services compensation. We anticipated that changeover whenwe made our "early start" on 1 February 2001 when the Investors Compensation Scheme (ICS) became our subsidiary.

FSCS Annual Report 2001/026

“You dealt with adifficult matter and

have had manyothers to deal with atthe same time. Your

service dealt with meas an individual.”

- FSCS CustomerSatisfaction Survey

2001-2002

FSCS Annual Report 2001/02

Nigel Hamilton

The results of the survey prompted theproduction of our consumer guide and theimplementation of several awareness-raisingstrategies that include working closely withconsumer advice centres.

Maintaining good linksMaintaining good links with the FSA is extremelyimportant to us. Although independent from theFSA, we are accountable to it. I would particu-larly like to thank Sir Howard Davies and hiscolleagues for working with us so constructively.

We recognise that our most valuable asset isour staff. We are committed to being a goodemployer, and to ensuring that our staff workwithin a positive environment. Our ChiefExecutive in her statement refers to the work weare doing to deliver and sustain our commit-ments to our staff.

As a single scheme we have had an interestingfirst few months, and, I believe, a successfulstart.

I would like to thank my Board members, ourChief Executive, Suzanne McCarthy, and all thestaff for all their hard work and commitmentduring the past 12 months.

I would also like to send a particular vote ofthanks to Kit Jebens, who retired as a memberof the FSCS Board in February 2002. Kit gavemany years of valuable service, first as adirector of ICS, and later on the FSCS Boardand as Chairman of our Investment IndustryCommittee. I would like to wish him a long andhappy retirement.

I am delighted to welcome Tim Vogel, a forensicaccountant, to the Board. I also look forward towelcoming Bernard Day OBE, a CharteredInsurer, who joins the Board in June.

I would also like to thank Keith Woodley, whoacted as ICS' Independent Investigator for overten years and then on FSCS' behalf during itsearly months. I am sure that Rear AdmiralRichard Irwin, who has assumed this role, willcontinue to provide us with the same level ofexcellent service.

This reportThis report focuses on our achievements so far,and our aims for the future. I hope you find itinteresting and informative.

FSCS Annual Report 2001/02 7

“I, like most people,find pensions very

hard to follow.I am therefore very

grateful for thisservice which was

carried out efficiently,despite my lack of

knowledge.”

- Pension Review claim

CH

AIR

MA

N’S

S

TATE

ME

NT

CH

AIR

MA

N

FSCS Annual Report 2001/02

FSCS Annual Report 2001/028

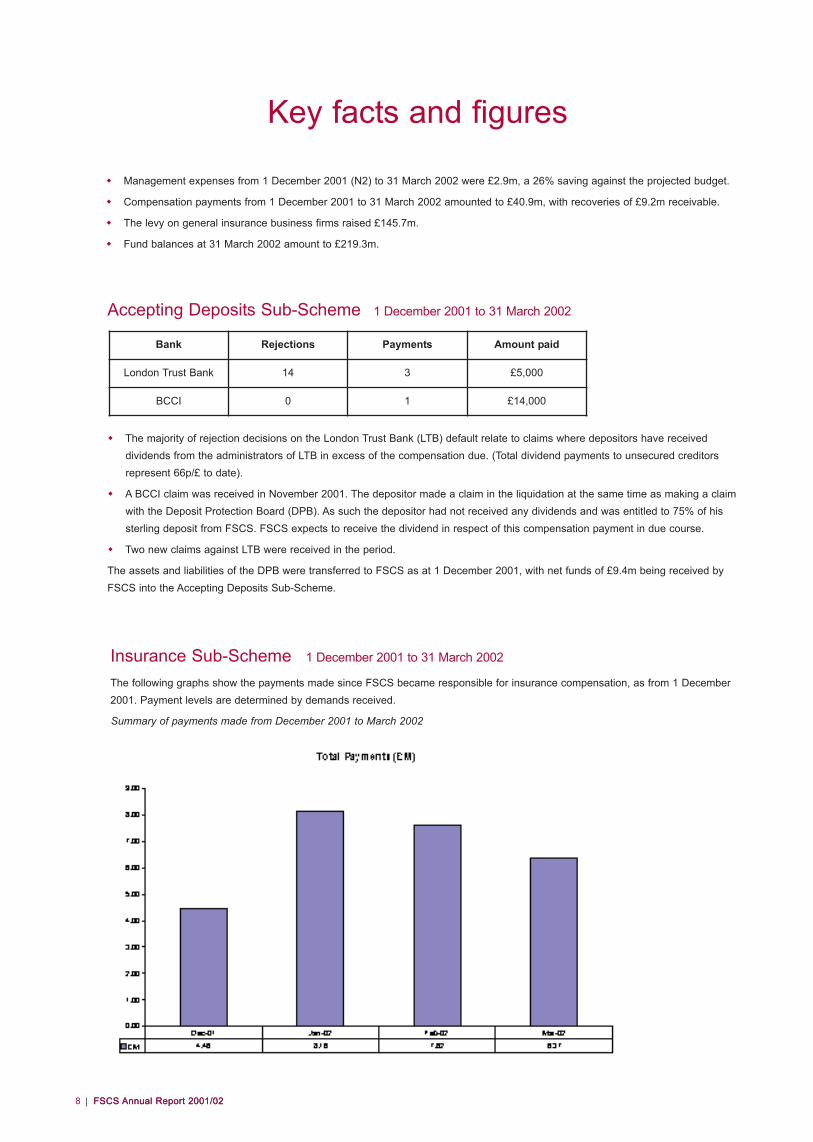

Accepting Deposits Sub-Scheme 1 December 2001 to 31 March 2002

� The majority of rejection decisions on the London Trust Bank (LTB) default relate to claims where depositors have receiveddividends from the administrators of LTB in excess of the compensation due. (Total dividend payments to unsecured creditors represent 66p/£ to date).

� A BCCI claim was received in November 2001. The depositor made a claim in the liquidation at the same time as making a claim with the Deposit Protection Board (DPB). As such the depositor had not received any dividends and was entitled to 75% of his sterling deposit from FSCS. FSCS expects to receive the dividend in respect of this compensation payment in due course.

� Two new claims against LTB were received in the period.

The assets and liabilities of the DPB were transferred to FSCS as at 1 December 2001, with net funds of £9.4m being received byFSCS into the Accepting Deposits Sub-Scheme.

Key facts and figures

FSCS Annual Report 2001/02

Bank Rejections Payments Amount paid

London Trust Bank 14 3 £5,000

BCCI 0 1 £14,000

Summary of payments made from December 2001 to March 2002

Insurance Sub-Scheme 1 December 2001 to 31 March 2002

The following graphs show the payments made since FSCS became responsible for insurance compensation, as from 1 December2001. Payment levels are determined by demands received.

� Management expenses from 1 December 2001 (N2) to 31 March 2002 were £2.9m, a 26% saving against the projected budget.

� Compensation payments from 1 December 2001 to 31 March 2002 amounted to £40.9m, with recoveries of £9.2m receivable.

� The levy on general insurance business firms raised £145.7m.

� Fund balances at 31 March 2002 amount to £219.3m.

FSCS Annual Report 2001/02 9

NO

TE

SFA

CTS

AN

D F

IGU

RE

S

FSCS Annual Report 2001/02

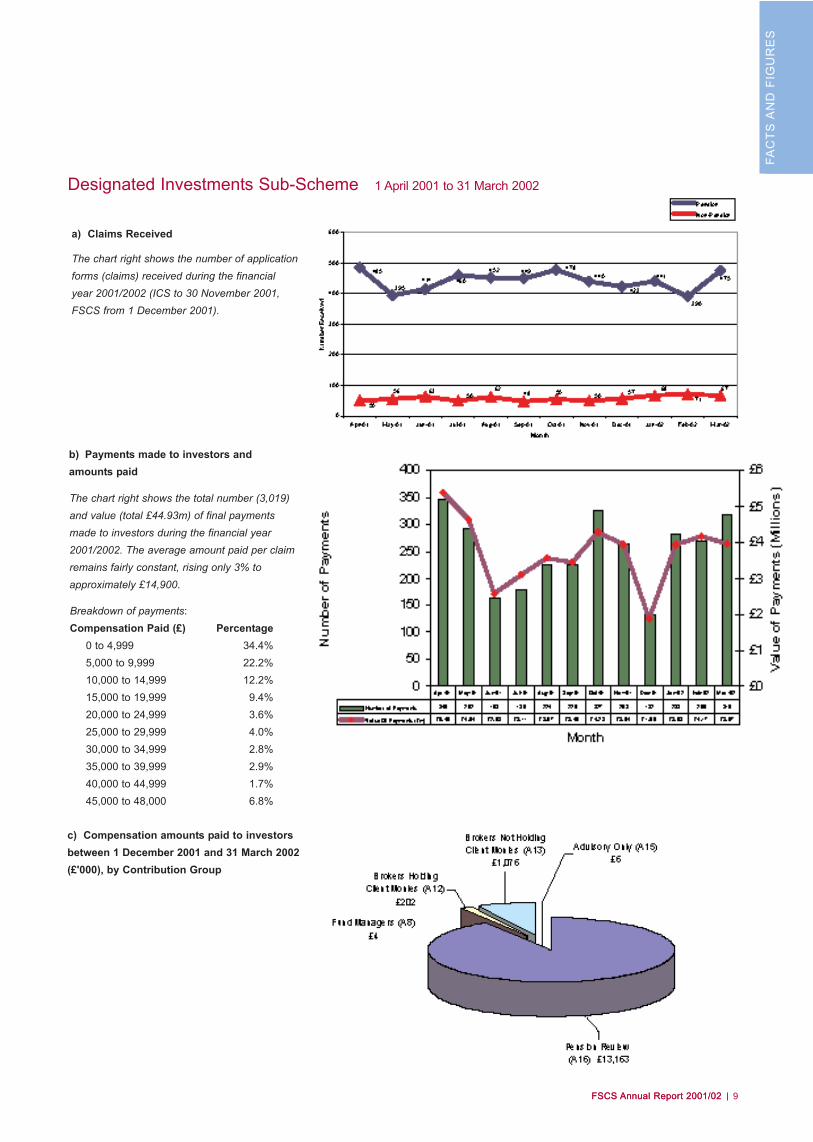

c) Compensation amounts paid to investorsbetween 1 December 2001 and 31 March 2002(£'000), by Contribution Group

b) Payments made to investors andamounts paid

The chart right shows the total number (3,019)and value (total £44.93m) of final paymentsmade to investors during the financial year2001/2002. The average amount paid per claimremains fairly constant, rising only 3% toapproximately £14,900.

a) Claims Received

The chart right shows the number of applicationforms (claims) received during the financialyear 2001/2002 (ICS to 30 November 2001,FSCS from 1 December 2001).

Designated Investments Sub-Scheme 1 April 2001 to 31 March 2002

Breakdown of payments:Compensation Paid (£) Percentage

0 to 4,999 34.4%5,000 to 9,999 22.2%10,000 to 14,999 12.2%15,000 to 19,999 9.4%20,000 to 24,999 3.6%25,000 to 29,999 4.0%30,000 to 34,999 2.8%35,000 to 39,999 2.9%40,000 to 44,999 1.7%45,000 to 48,000 6.8%

FSCS Annual Report 2001/0210

During 2001/2002 FSCS progressed throughvarious stages following on from its "early start"on 1 February 2001. Our work towards mould-ing the different compensation schemes intoone continued throughout the year.

An important stage was taken towards achievingthis objective when the Scheme moved to itsnew offices at Lloyds Chambers in June. Withthe co-operation of the Policyholders ProtectionBoard, their staff joined us in October.

These various steps contributed to ensuring thatall was ready for the change-over, and itssuccess is testament to the intensive planningdone by both the Scheme's Board and its staff.

Our Chairman has mentioned in his statementthe economic value that has flowed fromcombining the various schemes.

We are determined to demonstrate that we canprovide first-rate value for money, and, to thatend, we are putting in place mechanisms thatwill facilitate the measurement of ourperformance.

Novel issues2001/02 produced novel issues and newproblems, to which we have taken a pragmaticapproach.

In the investment sector FSCS (through itssubsidiary ICS) negotiated an agreement withTowry Law plc and AMP plc to secure recover-ies for the levy payer of up to £20m to helpmeet the cost of claims flowing from the defaultof Advizas Limited and minimise disruption toinvestors' claims.

The failures of Chester Street and IndependentInsurance produced not just a large volume of

claims, but also several difficult and sensitiveissues, as is often the case with complexinsurance insolvencies. We are pleased that,working with the provisional liquidators, theAssociation of British Insurers and others, wewere able to overcome these obstacles.

Recognising the volume of claims that wouldflow into the Scheme principally as a result ofthese failures, FSCS successfully raised its firstlevy in January 2002 of some £150m on thegeneral insurance contribution group.

New challengesWhat of the coming year? New challengescontinue to face us.

From July 2002 depositors with credit unionswill come under our protection, the first time thatcustomers of these financial institutions havehad the benefit of a compensation scheme.

Further, our insurance team will be workingthroughout the year to refine the 'tools' that theyneed.

Much of the work of the investment group willcontinue to be the processing of PensionReview cases. Working in partnership with theFSA, we have identified significant improve-ments to the processing of these claims. We,like the FSA, are determined to complete thedeparted firms Pension Review as quickly aspossible, but without sacrificing quality or cost-effectiveness. Our two organisations will bemaintaining our efforts to achieve this goal.

Our ability to realise our objectives for this yearand in the future depends fundamentally on ourstaff. FSCS is committed to being an employerthat provides a supportive, modern working

Chief Executive’s statementSuzanne McCarthy

If 2001/02 was a year of transition for the Financial Services Compensation Scheme, 2002/03 will be one of consolidation. Over thenext 12 months the changes inaugurated at midnight 1 December 2001 will be bedded down. This financial year will be a testing time forthe new Scheme, giving us our first opportunity to assess the workability of our rules, policies and procedures as we take decisions onclaims, seek recoveries, assess our funding requirements and raise any necessary levies.

“It was a bolt from theblue, I was jollying

along and thought myfinances wererelatively safe.

I didn't even knowthat the investment

company had stoppedtrading.”

- Pension Review claim

"We always felt that wewere pressured into it,

that it was wrong. Just bytelling us that it was

wrong gave usconfidence really. You

certainly helped us andwe are very pleased.”

- Bad investment adviceclaim

environment based on equal opportunities,visible leadership, open communication,teamwork and well targeted staff developmentwith rewards linked to achievements.

Several special initiatives aimed particularly atpromoting good management behaviour andtraining and development are being takenforward this year to make certain our practicesreflect our goals.

Relevant to achieving many of our business andemployment aims is the use we make of our ITsystems. 2002/2003 should see the firstproducts of the IT strategy we commissionedlast year.

The results should create an office that is ableto communicate with greater speed andefficiency both internally and externally, toprocess claims more quickly and to providegreater IT support to all its functions.

We recognise that there is a need to raise thelevel of public awareness of the Scheme notonly amongst our levy payers, but also with thepublic generally.

We will continue to work with levy payers, tradeassociations and consumer groups throughoutthe coming year to make sure our message isheard. Complementing this is our website whichis currently being improved to make it evenmore user-friendly.

This report explains our recent achievementsand our expectations for the year ahead. Butthis is only part of the story, for FSCS iscommitted to ensuring the long-term provisionof a secure, effective and cost-efficientcompensation scheme for the UK.

The groundwork we are laying now is focusedon obtaining this objective, and, in so doing,delivering a service that is innovative,pragmatic, responsive and accountable.

Our commitment to ourstakeholdersFSCS is committed to meeting its responsibili-ties to its various stakeholders.

To claimants: to provide a high qualitycompensation scheme that is efficient, fair,approachable and responsive and, whereappropriate, to work proactively with insolvencypractitioners and other persons and organisa-tions in securing cost-effective redress forclaimants and delivering compensation.

To our industry stakeholders: to provide anaccountable and cost-efficient compensationservice funded to the correct level, and to workproactively to secure recoveries from firms indefault.

To the Financial Services Authority (FSA):while acknowledging our independence, to beaccountable to the FSA as required bylegislation, and generally to work together inpartnership for the benefit of the UK's regulatorysystem.

To FSCS staff: to provide a supportive, modernworking environment based on equal opportuni-ties, visible leadership, open communication,teamwork and well targeted staff developmentwith rewards being linked to achievement.

To the general public: to provide timely,relevant, accurate and accessible informationabout FSCS and its activities.

CH

IEF

EX

EC

UTI

VE

FSCS Annual Report 2001/02 11

Deposit-taking IndustryCommitteeIn addition to receiving reports from theco-opted members, Gordon Pell of Royal Bankof Scotland, and Matthew Wyles of PortmanBuilding Society, about their respective sectors,this Committee kept under general review thework of the Accepting Deposits Sub-Scheme.

This included noting the activities of the DepositProtection Board to which FSCS was providingoperational support until 1 December 2001 andthe Scheme's operations thereafter.

During the year the Committee has beenparticularly interested in the preparations beingmade for the inclusion of credit unions withinFSCS' remit.

The Committee was also concerned withensuring that good communication links existedbetween FSCS and the relevant tradeassociations.

As a result, meetings were arranged withrepresentatives of both the British BankersAssociation and the Building SocietiesAssociation.

Insurance IndustryCommitteeAs with the Deposit-taking Industry Committee,this Committee's co-opted members, IainLumsden of Standard Life, and Stephan Pater ofRoyal & Sun Alliance, gave presentations.

The Committee was especially committed tomaking certain that all necessary actions weretaken to ensure a smooth transition of responsi-bilities from the Policyholders Protection Boardto FSCS.

Regarding FSCS' own activities, the Committeewas kept aware of the flow of work andestimates of activity, the outcome of FSCS'insurance levy and discussions held betweenFSCS and the Association of British Insurers onvarious matters.

Other issues considered included the subject ofclosures of schemes of arrangement.

Investment IndustryCommitteeThe co-opted members, Allan Daffern, formerdirector of Willis National Ltd, and ChrisLyttelton of NCL Investments Ltd, updated theCommittee on developments within this sector.

In addition to reviewing the Scheme'sInvestment Sub-Scheme work, (both pensionand non-pensions), the Committee alsoconsidered the FSA's consultation paper on thehandling of Endowment Mortgage Complaints inthe context of the Scheme's practices and thecontent and style of FSCS' quarterly reports tothe FSA on ICS/FSCS business activities.

The work of the IndustryCommittees

The FSCS Board recognises the importance of keeping abreast with developments and events taking place within the different financialsectors. To that end it created three Industry Committees, to cover each of the three main sectors - deposit-taking, insurance and invest-ment. Their specific remit is to look generally at FSCS' flow of work within their respective area, likely future workloads and industrytrends. The Committees consist of several non-executive directors together with the Chief Executive and experienced practitioners. Thefollowing summarises the work that each Committee did during 2001/02.

FSCS Annual Report 2001/0212

Details of IndustryCommittee members

can be found in theCorporate Governance

section of this AnnualReport (see page 20).

CustomerServices

Assistant ManagerTom Sheffield

FSCS Annual Report 2001/02 13

OR

GA

NIS

ATIO

N

FSCS Annual Report 2001/02

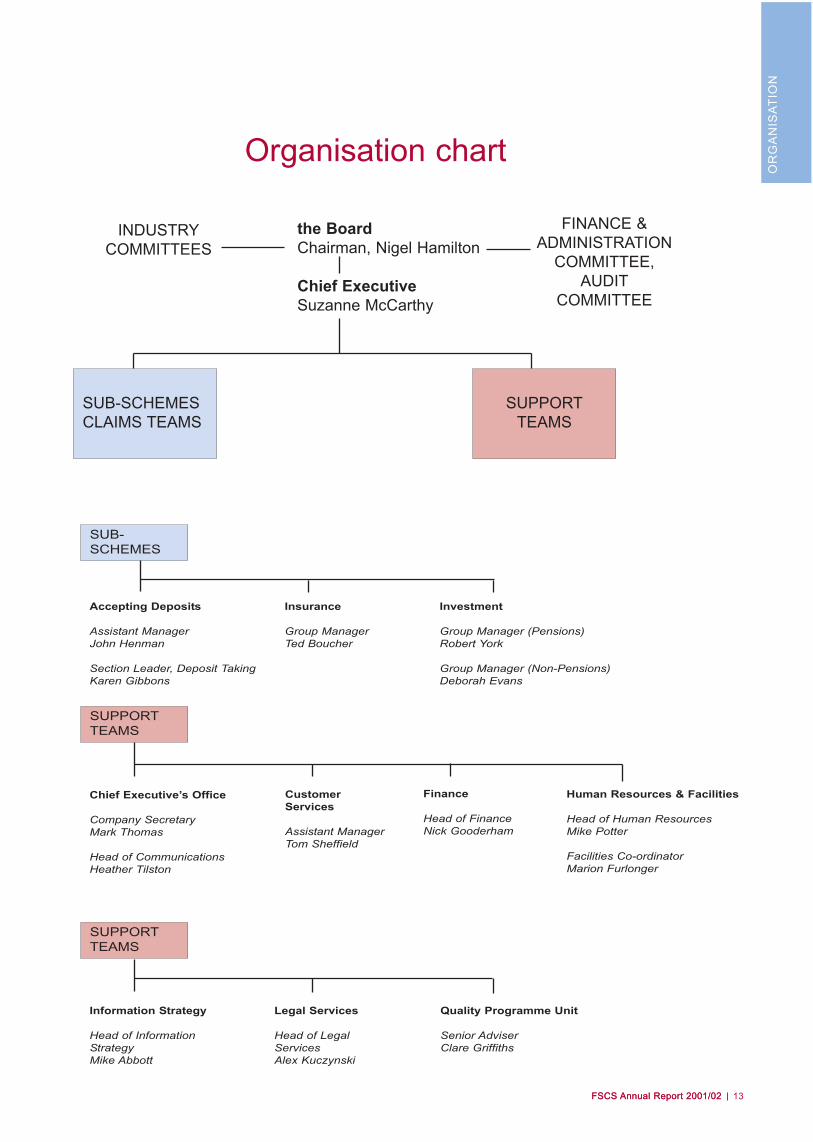

the BoardChairman, Nigel Hamilton

Chief ExecutiveSuzanne McCarthy

Investment

Group Manager (Pensions)Robert York

Group Manager (Non-Pensions)Deborah Evans

SUB-SCHEMES

Accepting Deposits

Assistant ManagerJohn Henman

Section Leader, Deposit TakingKaren Gibbons

Insurance

Group ManagerTed Boucher

SUPPORTTEAMS

SUB-SCHEMESCLAIMS TEAMS

INDUSTRYCOMMITTEES

FINANCE &ADMINISTRATION

COMMITTEE,AUDIT

COMMITTEE

SUPPORTTEAMS

SUPPORTTEAMS

Information Strategy

Head of InformationStrategy Mike Abbott

Legal Services

Head of LegalServicesAlex Kuczynski

Quality Programme Unit

Senior AdviserClare Griffiths

Chief Executive’s Office

Company Secretary Mark Thomas

Head of CommunicationsHeather Tilston

Human Resources & Facilities

Head of Human Resources Mike Potter

Facilities Co-ordinator Marion Furlonger

Finance

Head of FinanceNick Gooderham

Organisation chart

The work of our departments:

Claims teamsFSCS' achievements are very much dependent on its staff. This section briefly explains how each team contributed towards deliveringFSCS as a fully operational organisation on 1 December 2001, and how they continue to contribute to FSCS' success.

Accepting DepositsThe Accepting Deposits Sub-Scheme deals withclaims made against failed banks and buildingsocieties. From 1 February 2001, under theterms of a Service Level Agreement with theDeposit Protection Board (DPB), which wasthen responsible for handling such compensa-tion, FSCS began providing the necessaryoperational resources to that Board.

On 1 December 2001 the DPB's assets andliabilities were transferred to FSCS. The prepa-rations made by the Accepting Deposits teamfor this transition ensured a seamless transfer ofresponsibility from DPB to FSCS.

No new failures were reported during 2001/02,and the team continued to process claimsagainst London Trust Bank and BCCI. Duringthe period 1 December 2001 to 31 March 2002these totaled £19,482. Further, FSCS received£455,000 in recoveries (the bulk of this moneyhaving been passed to it from DPB).

During 2001/02 FSCS representatives attendedtwo deposit insurance conferences in Europe todiscuss developments. These meetings gaveFSCS an important opportunity to makeinternational colleagues aware of the changesthat were taking place in deposit insurancewithin the UK.

During the year FSCS has also had opportuni-ties to share information and experiences withother deposit insurers, with visits fromrepresentatives of Slovakia, Korea and theJersey Financial Services Commission.

From July 2002 credit unions will join thescheme and become part of the Accepting

Deposits Sub-Scheme. From that time creditunion members will be entitled to the same levelof compensation currently only available to bankand building society depositors. This team hasbeen working, together with the FSA, to ensurewe are ready for their inclusion.

InsuranceThe Insurance team is responsible for dealingwith claims for compensation that arise followingthe failure of an authorised insurance firm. It iscurrently dealing with claims resulting from thefailure of 20 general insurers and two lifeassurance companies. During the period 1December 2001 to 31 March 2002 compensa-tion payments were made totaling £26,627,735.

During 2001/02 FSCS faced two key challengesin relation to the Insurance Sub-Scheme. Thefirst was the creation of the Scheme's owninsurance team, and the second was to ensurea smooth transfer of work from thePolicyholders Protection Board (PPB), thebody previously responsible for insurancecompensation.

Throughout 2001 FSCS worked closely withthe PPB to ensure a smooth transfer ofresponsibility. We were pleased that all theexisting PPB staff as at 1 December 2001chose to join FSCS until at least the end of thefinancial year. This allowed us to continue tobenefit from their experience.

During 2002/03 the Insurance team will moveahead in a number of areas. It will continue thereview started in the previous year of theprocesses needed to handle existing insolventestates.

“Thank you verymuch for the serviceprovided. Without it Iwould have had little

or no chance ofachieving an

outcome.”

- FSCS CustomerSatisfaction Survey

2001-2002

FSCS Annual Report 2001/0214

Already the team has made certain changes tospeed up the delivery of compensationmonies. In line with this the team will also becreating and putting in place an improved auditregime.

The team will also carry on developing acloser relationship with InsolvencyPractitioners and their claims handling agentsto ensure a good appreciation and understand-ing of the issues particular to any individualestate, and play a full role in delivering aquality service. In addition, we will be workingwith Insolvency Practitioners to examine theissues surrounding closure of schemes ofarrangement. FSCS has a particular interest inthis area given its need to deliver serviceefficiently, but also reflecting that our doorscan never close to protected policyholders.

We will be continuing our dialogue with variouskey stakeholders, including the FSA and theAssocation of British Insurers, to ensure thatwe understand the important issues and trendsfacing them that may impact on our insuranceactivities.

InvestmentFSCS made an "early start" on 1 February2001 when the Investment CompensationScheme (ICS) became its subsidiary.

Full details of ICS' activities (pension and non-pension work) carried out during the period 1April 2001 to 30 November 2001 are containedin the enclosed ICS Annual Report. FSCS tookover full responsibility for this work on 1December 2001.

a) Pensions Group

The Pensions Group, together with the FSA'sPension Unit, processes the departed firm partof the Pension Review into the sales of per-sonal pensions. (A departed firm is one that is

no longer authorised to conduct investmentbusiness.) This work accounts for around 90%of the Sub-Scheme's activities, and this is like-ly to continue to be the case during 2002/03.

The Pensions Group is split into a number ofteams, each with its own specialism.

The Insolvency team assesses the ability ofthe relevant departed Independent FinancialAdviser (IFA) firm to meet the claims against it,while the Eligibility team establishes whetherthe advice given to the claimants, by the firm,was responsible for any loss suffered and alsowhether the claims are eligible under our rules.

The Redress team makes sure that losscalculations are updated where necessary andthat the appropriate form of offer is issued toeach eligible claimant.

Finally, the Payment team coordinates thereceipt of accepted offers of compensation andany necessary third party documentationbefore completing the redress (compensation)process by issuing payments to occupationalpension schemes, personal pension providersand claimants.

During 2001/02 several issues concerningwindfall benefits affected both the industry andthe Scheme's efforts to process pensionreview claims. Recognising this obstacle, theGroup took steps to ensure that it should notunduly affect FSCS' ability to process theseclaims.

Further, in order to enhance overall efficiency,the Group worked with the FSA's Pension Unitduring the year to identify improvements in theway cases are handled. The resulting recom-mendations have been implemented. During2002/03 FSCS in general, and the pensionsgroup in particular, will continue to work withthe FSA in seeking ways to speed up theprocessing of these claims.

DE

PAR

TME

NTS

FSCS Annual Report 2001/02 15

“I found the serviceprovided very helpfulindeed. I would alsolike to point out thatwere it not for thisinvestigation I wouldhave lost out on mypension rights.”

- FSCS CustomerSatisfaction Survey2001-2002

FSCS Annual Report 2001/0216

Investmentb) Non-Pensions Group

The Non-Pensions Group covers those claimsarising from investment business that do not fallwithin the FSA Pensions Review. During2001/02 this group made 654 decisionsresulting in around 300 payments.

In recent years the number of non-pensiondefaults resulting in large numbers of claimantshas decreased, and during 2001/02 the teamdealt with just one large default with around 300claimants.

Various investments might give rise to a rangeof claims, from assurance based savingsproducts to futures and options.

Negligent advice that encouraged an investor toenter into an unsuitable product is the mostcommon reason for such claims being received,but the team has also investigated claims forother reasons, such as misappropriation offunds.

During 2001/02 this team has seen an increasein the number of claims relating to endowmentpolicies connected with mortgage loans.

c) Central Processing Claims (CPC)

The CPC team is responsible for administeringthe weekly download received from the FSAPension Unit (Pension Review), sendingapplication forms to all Investment Sub-Schemeclaimants and ensuring the forms are correctlycompleted and entered on our systems on theirreturn. In 2001/2002 the team dealt with over4,000 new applications.

This team also deals with all commission-checkqueries, sends chaser and closure letters,re-allocates and re-opens claims, and isresponsible for the setting up of 'new' firms(those against which we have not had previousclaims) by entering their details on oursystems.

“Excellent service byall members of your

team.”

“I would like to thankeverybody for all thehelp and assistanceyou have given. So

once again, thanks.”

- FSCS CustomerSatisfaction Survey

2001-2002

The work of our departments:Claims teams

The work of our departments:Support teamsCommunicationsThis team's principal focus has been raisingawareness of the Scheme amongst its stake-holders.

For levy payers this work has included thepublication of the first issue of our bi-annualindustry newsletter, Outlook, several specialevents and various presentations.

As the starting point of our awareness-raisingstrategy amongst consumers we commissioneda MORI research poll aimed at discovering theirattitudes towards the safety and security of theirmoney and investments and their awareness ofthe availability of compensation.

Not surprisingly awareness of FSCS was low,but one key factor to emerge was that the firstpoint of call for consumers when they need helpis often advice centres.

As a result we are working with a number ofthese organisations. We also were able tosupply input for FSA publications and fact-sheetsoffering advice for consumers who need to claimcompensation.

Publication of the MORI research, and thelaunch of our consumer guide generated mediacoverage at both national and local levels, andwe will continue to build on this during the year.

DE

PAR

TME

NTS

FSCS Annual Report 2001/02 17

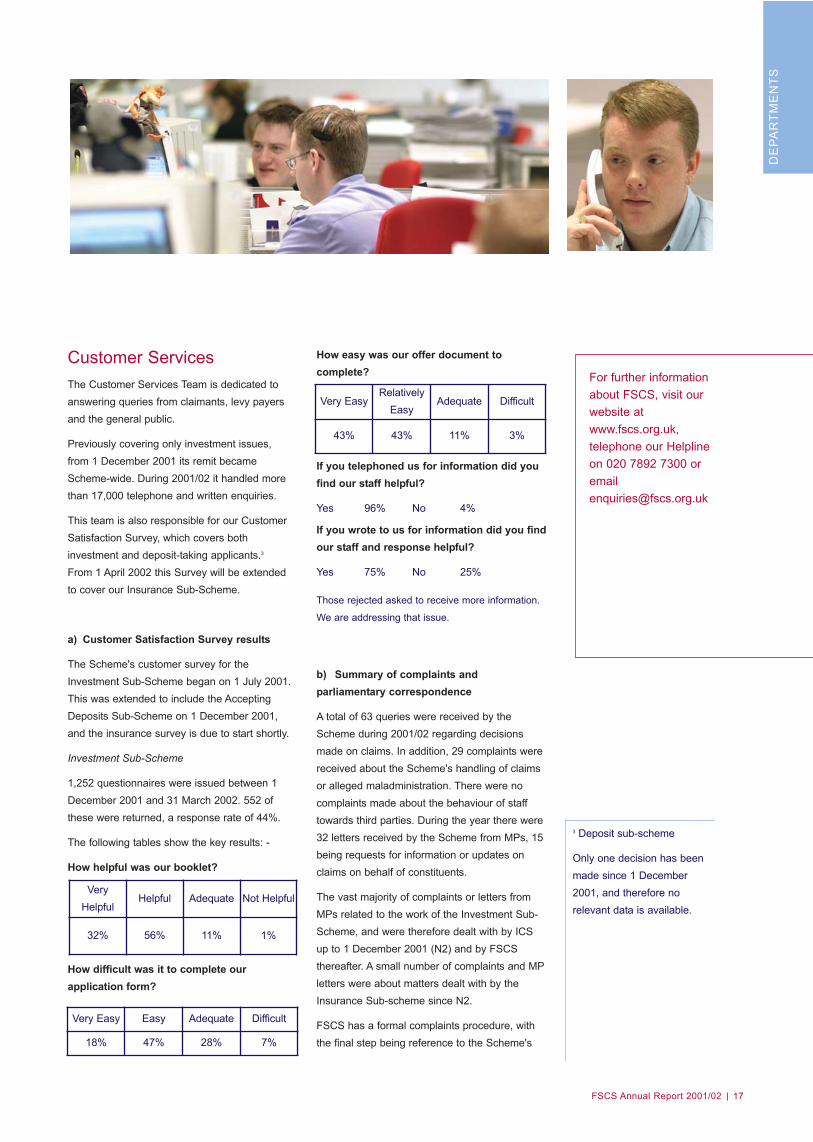

Customer ServicesThe Customer Services Team is dedicated toanswering queries from claimants, levy payersand the general public.

Previously covering only investment issues,from 1 December 2001 its remit becameScheme-wide. During 2001/02 it handled morethan 17,000 telephone and written enquiries.

This team is also responsible for our CustomerSatisfaction Survey, which covers bothinvestment and deposit-taking applicants.3

From 1 April 2002 this Survey will be extendedto cover our Insurance Sub-Scheme.

a) Customer Satisfaction Survey results

The Scheme's customer survey for theInvestment Sub-Scheme began on 1 July 2001.This was extended to include the AcceptingDeposits Sub-Scheme on 1 December 2001,and the insurance survey is due to start shortly.

Investment Sub-Scheme

1,252 questionnaires were issued between 1December 2001 and 31 March 2002. 552 ofthese were returned, a response rate of 44%.

The following tables show the key results: -

How helpful was our booklet?

How difficult was it to complete our application form?

How easy was our offer document to complete?

If you telephoned us for information did youfind our staff helpful?

Yes 96% No 4%

If you wrote to us for information did you findour staff and response helpful?

Yes 75% No 25%

Those rejected asked to receive more information.

We are addressing that issue.

b) Summary of complaints and parliamentary correspondence

A total of 63 queries were received by theScheme during 2001/02 regarding decisionsmade on claims. In addition, 29 complaints werereceived about the Scheme's handling of claimsor alleged maladministration. There were nocomplaints made about the behaviour of stafftowards third parties. During the year there were32 letters received by the Scheme from MPs, 15being requests for information or updates onclaims on behalf of constituents.

The vast majority of complaints or letters fromMPs related to the work of the Investment Sub-Scheme, and were therefore dealt with by ICSup to 1 December 2001 (N2) and by FSCSthereafter. A small number of complaints and MPletters were about matters dealt with by theInsurance Sub-scheme since N2.

FSCS has a formal complaints procedure, withthe final step being reference to the Scheme's

For further informationabout FSCS, visit ourwebsite atwww.fscs.org.uk, telephone our Helplineon 020 7892 7300 [email protected]

3 Deposit sub-scheme

Only one decision has beenmade since 1 December2001, and therefore norelevant data is available.

VeryHelpful

Helpful Adequate Not Helpful

32% 56% 11% 1%

Very Easy Easy Adequate Difficult

18% 47% 28% 7%

Very EasyRelatively

EasyAdequate Difficult

43% 43% 11% 3%

FSCS Annual Report 2001/0218

Independent Investigator. One referral,concerning an ICS case, was made by FSCS tohim in 2001/02. This matter is still beinginvestigated.

Another ICS case was reported in last year'sAnnual Report as having been referred to theIndependent Investigator. His report wasreceived by the FSCS Board during 2001/02.He concluded generally that, whilst there weredelays in the processing of that particular claim,they were unavoidable in the circumstances.

It was, however, recommended that the Schemeshould continually review its procedures toensure that compensation calculations weredone at the earliest possible date.

FacilitiesFacilities has responsibility to ensure that FSCSstaff work in a healthy and safe environment.During 2001/02 this team had primaryresponsibility for the Scheme's move to its newoffices at Lloyds Chambers. In addition, theteam worked with the other support servicesteams generally to deliver FSCS' smooth start.

FinanceThe finance team ensures timely and accuratesettlement of agreed compensation claims, andmanages our internal financial information, pro-cedures and controls and our treasury function.

In January 2002 the finance team issued andcollected FSCS' first levy raised on the GeneralInsurance Contribution Group. In future the teamwill be responsible for raising levies for thescheme using the FSA as its collection agent.

In addition to its usual day-to-day business, theteam this year undertook the changes necessaryto cover FSCS' new financial requirements after1 December 2001, principally the handling ofclaims for the Insurance and Accepting DepositSub-Schemes, and work related to the variouscontribution groups within FSCS' three separateSub-Schemes.

HRA new HR Team was recruited over the summerof 2001. It fell to them to tackle the crucialpersonnel issues associated with the creation ofa new organisation, particularly remuneration,pension provision, an appraisal process andperformance measurement.

In addition, this team was instrumental inorganising a special Staff Event aimed atengendering a "one Scheme" ethos.

That in turn has produced a number of specialprojects focused on the induction, training andmentoring of employees, communication withinand between teams and general managementphilosophy and corporate behaviour.

The results of these initiatives will be rolled outduring 2002/03.

“Very impressed withthe speed with which

my claim was dealt10 out of 10!”

- FSCS CustomerSatisfaction Survey

2001-2002

The work of our departments:

Support teams

DE

PAR

TME

NTS

FSCS Annual Report 2001/02 19

Information SystemsWorking closely with Facilities, the IT teamensured that, during the move to new premises,the transfer of the Scheme's functions wassuccessful, with no interruption in FSCS'services.

Recognising the important contribution IT canmake to an organisation's efficiency, the FSCSBoard authorised a major review of all FSCS'systems during the past year and approved thedevelopment of a new FSCS InformationSystems strategy.

Work towards implementing this strategy beganin earnest during the latter half of the year.

The strategy's objectives are to create a systemthat will:

� enhance the interface between the Scheme and its customers;

� improve responsiveness to queries and generally accelerate the claims processes;

� be easily expandable to cope with additional Sub-Schemes should they be needed in the future;

� provide the IT capability to handle a major failure (of an authorised firm) if one occurred;

� a document management system that can improve the flow of information both within FSCS and externally;

� provide a secure repository of all files and correspondence.

LegalThe Scheme's legal department was closelyinvolved in preparing for the assumption ofFSCS' powers, and, in particular, the introduc-tion of the new rules and associated policies.

This team continues to monitor the practicalapplication of the Scheme's rules and to adviseon novel issues when received.

In addition, the team has continued its advisorywork on individual claims (or classes of ) forcompensation, and the management of theScheme's recovery function, relying on the rightsassigned to it by compensated claimants.

Recovery work covers all three Sub-Schemes.Where possible recoveries are pursued bothagainst firms that have been declared in defaultand third parties. In some cases the Scheme isable to make further payments to claimants withoutstanding losses from amounts recovered.

Quality Programme Unit (QPU)QPU's main function is to perform qualityassurance reviews of work done by claimsprocessing teams. During 2001/02 the team wasable to assure the Board that the quality targetsset had been met.

Together with the legal team, QPU was heavilyinvolved in preparing the Scheme for its newrole. During the year this team was particularlyinstrumental in developing FSCS' approach torisk assessment, and it continues to beresponsible for overseeing the ongoing reviewand management of the Scheme's businesscontingency plans.

“The service receivedwas excellent,professional andcourteous fromeveryone we dealtwith at FSCS - thankyou.”

- FSCS CustomerSatisfaction Survey2001-2002

FSCS Annual Report 2001/0220

The Board1. Composition of the Board

The Combined Code indicates that there shouldbe an effective Board to lead and control thecompany, and that there should be a balance ofexecutive and non-executive directors.

The FSCS Board currently comprises ninedirectors, eight of whom are non-executivedirectors, including the Chairman. The oneexecutive director is the Chief Executive.

All directors are appointed by the FinancialServices Authority (the FSA) using appropriateNolan principles, transparent recruitmentprocesses and public advertisement. Theappointment (and removal) of the Chairman isalso approved by HM Treasury.

This appointment mechanism means that thereis no need for FSCS to have a separatenomination committee to advise the Board onprospective new directors.

Biographical details of the directors are given onpage 2 of the Annual Report.

2. Operation of the Board

The Board usually meets once a month, and aformal schedule of matters reserved to theBoard for decision has been documented andagreed. Directors are subject to a conflict ofinterest policy to prevent any potentialinterference with the independence of theirjudgement on Board matters.

The Company Secretary, appointed by theBoard, attends all Board and Committeemeetings, and is responsible for ensuring thatBoard procedures are followed and thatappropriate records are kept.

Directors are permitted to obtain independentprofessional advice, as required, on any matterthat might assist them in the furtherance of theirduties.

Committees of the Board 1. Finance and Administration Committee

The Finance and Administration Committeeaims to meet approximately four times a year,and comprises four non-executive directors andthe Chief Executive.

The Committee:

� monitors and oversees all operational areas of FSCS;

� reports to the Board on key strategic, financial and operational issues; and

� makes recommendations to the Board on areas such as remuneration policy, the Business Plan and Budget, the annual financial statements and levies.

2. Audit Committee

The Audit Committee aims to meet approxi-mately three times a year, and comprises fournon-executive directors (with the ChiefExecutive normally in attendance at meetingsby invitation). The Committee is responsible forreviewing, and reporting to the Board on, thefollowing:

� the annual accounts;

� the accounting policies;

� the financial reporting system;

� the system of internal control;

� risk management;

� the audit processes.

Corporate Governance

The FSCS Board is committed to high standards of Corporate Governance. Accordingly, the Board has agreed to follow the provisionsof the Combined Code produced by the Hampel Committee on Corporate Governance in June 1998. Whilst recognising that only UKlisted companies are required to report on their compliance with the Combined Code, the Board decided that FSCS should report onthe extent to which it complies with the Code's provisions.

GO

VE

RN

AN

CE

FSCS Annual Report 2001/02 21

3. The Industry Committees

The Board recognises the importance not only ofconsidering the operational performance ofFSCS, but also of being aware of significantdevelopments, trends or events in the financialservices industry.

To assist the Board in this, it has set up threeIndustry Committees, one for each of the threemain sectors of the industry, covering invest-ment, insurance and deposit-taking.

These Committees aim to meet two to threetimes a year, to look generally at the flow ofwork and likely future workloads for FSCS intheir respective sectors, and to discuss relevantissues.

In order to assist the Committees in theirdiscussions, and as a means of fostering,developing and monitoring FSCS' relationshipwith the financial services' sectors, experiencedpractitioners have been co-opted.

Aside from these members, each IndustryCommittee comprises three non-executivedirectors plus the Chief Executive.

COMMITTEE MEMBERSHIP Audit Finance & Admin Deposit Insurance Investment

Non-executive directors:

Nigel Hamilton � �

Michael Blair QC � �

Sarah Brown � �

Kenneth Culley CBE � �

Kit Jebens CBE4 � � �

Graeme MacLennan � �

Luke March � �

Tim Vogel 5 �

John Young CBE � �

Executive director:

Suzanne McCarthy � � � �

*Co-opted members:

Gordon Pell �

Matthew Wyles �

Stephan Pater �

Iain Lumsden �

The Hon Chris Lyttelton �

Allan Daffern �

4. Composition of the Board Committees

4 Until February 2002

5 From April 2002

* Each Industry Committeehas two co-opted members.These are experiencedpractitioners, invited to jointhe respective Committee toassist in their discussions.

FSCS Annual Report 2001/0222

Corporate Governance(continued)

Internal ControlsAs with the Combined Code, the requirementsof Internal Control: guidance for Directors on thecombined code (the Turnbull Report) aremandatory only for UK listed companies.

However, recognising its commitment to main-taining a sound system of internal control, theBoard has decided that it would be appropriateto follow the provisions of the Turnbull Report.

A sound system of internal control is designedto manage rather than eliminate the risk of fail-ure to achieve business objectives, and canonly provide reasonable and not absolute assur-ance against material misstatement or loss.

In the period covered by this Report, theBoard's principal tasks, in addition to operatingthe various schemes, have been preparing forN2 and creating a unified organisation.

The Board has received regular reports onthese issues as well as on the performance andfinancial position of each of the Sub-Schemesand on its own financial position.

It receives regular reports from the threeIndustry Committees and the Finance andAdministration Committee. The Board alsoreceives reports from the Audit Committee on,amongst other things, the following:

� the quality, reliability and effectiveness of the internal and external audit functions;

� the procedures for the assessment and management of risks; and

� FSCS' internal controls (which include financial, operational and compliance controls).

The arrangements for internal control have beenin place throughout the year.

These arrangements are kept under regularreview by the Board and were further developed

during the year in readiness for FSCS assumingresponsibility for the new Scheme as from 1December 2001.

The Board also undertakes an annual review ofthe appropriateness and effectiveness of theinternal controls, drawing on reports frommanagement and advice from the AuditCommittee where required.

The following are examples of the work thatFSCS has carried out in order to satisfy itselfthat there are appropriate controls throughoutthe organisation:

1 FSCS has developed a risk register, whichidentifies, analyses and prioritises key risks tothe organisation and highlights the relevantcontrols for each risk area. This register isreviewed and updated regularly by managementand is also considered by the Audit Committee,which reports to the Board after eachCommittee meeting.

2 The Board has reviewed the operatingpolicies for each of the three Sub-Schemes forwhich it is responsible since N2.

3 The Audit Committee considers, at each ofits meetings, a report on the quality assurance(QA) reviews of certain claims processes.These QA reviews are carried out by FSCS'internal Quality Programme Unit (QPU), a teamthat performs a quasi-internal audit function inrespect of claims processes.

4 FSCS has decided that a full internal auditfunction should be set up, utilising the servicesof an outside firm to act as FSCS' internalauditors. Deloitte and Touche were appointed asFSCS' internal auditors from April 2002onwards.

5 During the year FSCS has given priority toreviewing and revising its arrangements forensuring business continuity in the event ofsome kind of disaster. This might be due to

GO

VE

RN

AN

CE

FSCS Annual Report 2001/02 23

For further informationabout FSCS, visit ourwebsite atwww.fscs.org.uk, telephone our Helplineon 020 7892 7300 [email protected]

either business interruption as a result of asudden loss of FSCS' premises and equipmentor to a large or novel business failure resultingin a significant rise in the number of claims forcompensation.

6 FSCS has also developed its treasurymanagement policy and the processes formanaging resources and budgets to ensure thatthere are appropriate controls in place.

7 In addition, attention has been given to theway in which the Board has delegated some ofits decision-making powers to the ChiefExecutive, and, through the use of a set ofpolicies, to management.

During the coming year, the Board will continueto prioritise its review of risk management andthe internal control arrangements in the light ofexperience of operating the Scheme since N2,and will also consider the work of the newinternal audit function.

Directors' Remuneration All remuneration matters, including the fullremuneration package for the Chief Executive,are considered initially by the Finance &Administration Committee with recommenda-tions made to the Board for its approval (in bothcases the Chief Executive is not present whenher remuneration package is being considered).

Remuneration details of directors are given inthe Directors' Report on page 24, and in note 5to the financial statements.

Non-executive directors' fees are reviewedannually by the Board as a whole andrecommendations are made to the FSA, whichsets the fees.

Board/ManagementRelationshipSome specific areas of Board responsibility aredelegated to Committees of the Board or to theChief Executive, as appropriate. The Boardreceives and considers reports on all relevantareas of activity to satisfy itself that FSCS isperforming its functions satisfactorily and isusing its resources efficiently and economically.The Board regularly reviews the supply ofinformation from management to ensure thatsuch information is timely and appropriate.

Compliance with theCombined CodeFSCS complied throughout the year with theCode provisions set out in Section 1 of theCombined Code on Corporate Governance,except the following:

� A.5.1 (Nomination Committee)

� A.6.2 (length of directors' appointments)

� B.1.7 to B.1.10 (Service Contracts and Compensation)

� B.2.2 (composition of Remuneration Committee)

� B.2.4 (remuneration of non-executive directors)

� B.3.2 to B.3.5 (report on directors' remuneration policy)

As explained earlier, all appointments to theFSCS Board are made by the FSA, with theChairman's appointment (and removal) alsobeing approved by HM Treasury.

Accordingly, there is no need for FSCS to havea nominations committee, and the remunerationof the non-executive directors is determined bythe FSA.

The remuneration package of the ChiefExecutive, being the only executivedirector on the Board, is considered bythe Finance & Administration Committee,whose terms of reference includeconsideration of all remuneration matters,and approved by the Board (in bothcases, without the Chief Executive beingpresent).

The Memorandum of Association statesthat directors' appointments are to bemade for periods not exceeding fouryears, at which time directors may besubmitted for re-appointment, althoughthe Combined Code recommends thatdirectors submit themselves forre-election at least every three years.

Initial appointments to the FSCS Boardare usually staggered between two andfour years. The existing four-yearprovision, however, may be reviewedfrom time to time.

The directorsDetails of the directors for the year to 31 March 2002 are shown on page 2 of the FSCS Annual Report.

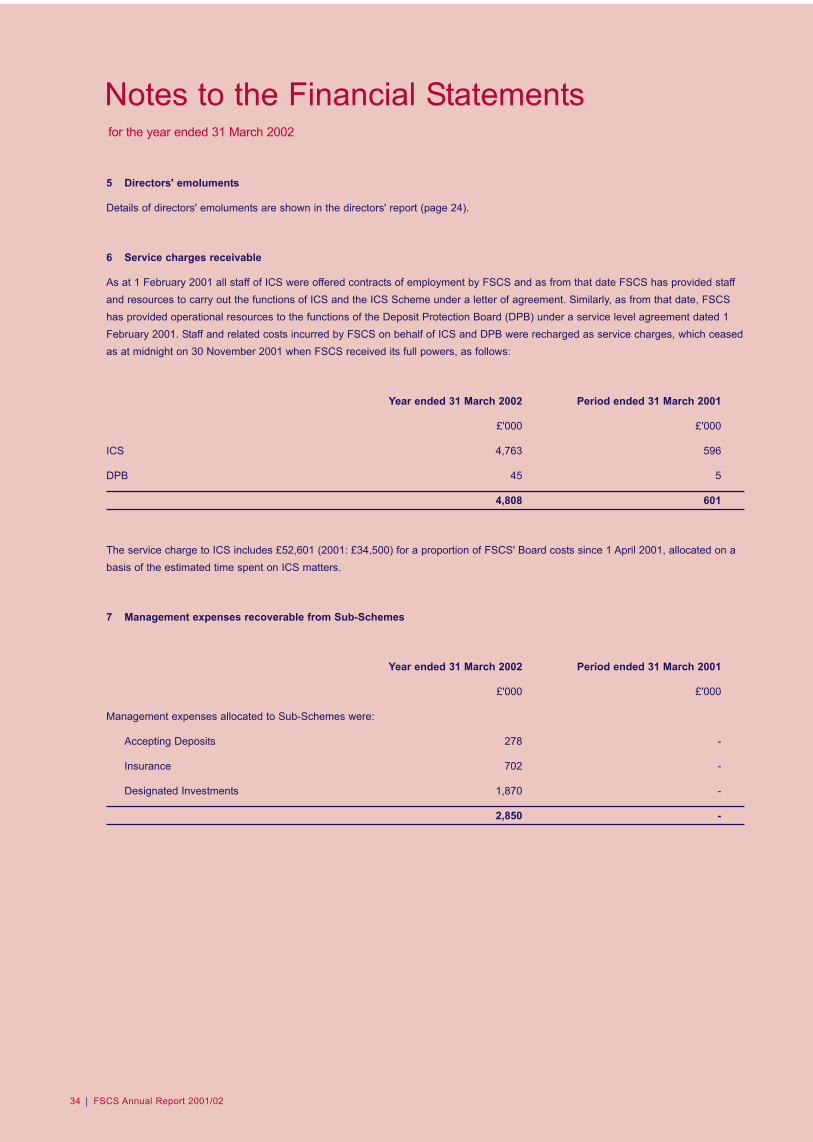

Directors' emolumentsTotal emoluments paid to directors are as follows:

Year ended Period ended31 March 2002 31 March 2001

£'000 £'000

Aggregate emoluments 246 166

Pension contributions 23 8

269 174

FSCS Annual Report 2001/0224

Principal activitiesFSCS was formed as the Scheme Manager designate under s212 of the Financial Services and Markets Act 2000 (FSMA) toadminister a single compensation scheme for consumers in respect of deposits, contracts of insurance and investment business,should a financial services firm be unable to meet its liabilities, and it assumed its responsibilities at midnight on 30 November 2001when FSMA was fully enacted.

Review of activitiesSince its incorporation and the appointment of directors, the company has made preparations in anticipation of receiving its powersunder FSMA at a date referred to as N2, and integrating the former compensation schemes. As a part of this process, on 1 February2001 FSCS became the sole member of Investors Compensation Scheme Limited (ICS), the Scheme Manager responsible for theInvestors Compensation Scheme (the ICS Scheme). At that date, the FSCS directors also became directors of ICS.

As a further part of the "early start" process, staff of both ICS and the Deposit Protection Board (DPB), were offered contracts ofemployment with FSCS as from 1 February 2001, and FSCS assumed, under a Service Level Agreement, the provision of operationalresources to DPB, and under an agreement, as from 20 August 2001, certain activities of the Policyholders Protection Board (PPB).

Financial positionThe company's results show neither a surplus nor deficit as its net costs to 30 November 2001 are treated as recoverable from futureparticipating firms from that date as costs of establishing the scheme, under s213 of FSMA. After that date management expenses andcorporate costs are recoverable from and allocated fully to the three Sub-Schemes of Accepting Deposits, Insurance and DesignatedInvestments, as shown on pages 40 to 50.

The financial statements of ICS as at 31 March 2002, show net assets of £Nil and the company did not trade during the year to thatdate although it continued to act in its capacity as Scheme Manager of the ICS Scheme until 30 November 2001. In accordance withs229(2) of the Companies Act, consolidated financial statements have not been prepared in view of the immateriality of the amountsinvolved. Financial statements of the ICS Scheme for the year to 31 March 2002 are included with FSCS’ Annual Report andAccounts, or available from the Company Secretary at 7th Floor, Lloyds Chambers, 1 Portsoken Street, London E1 8BN.

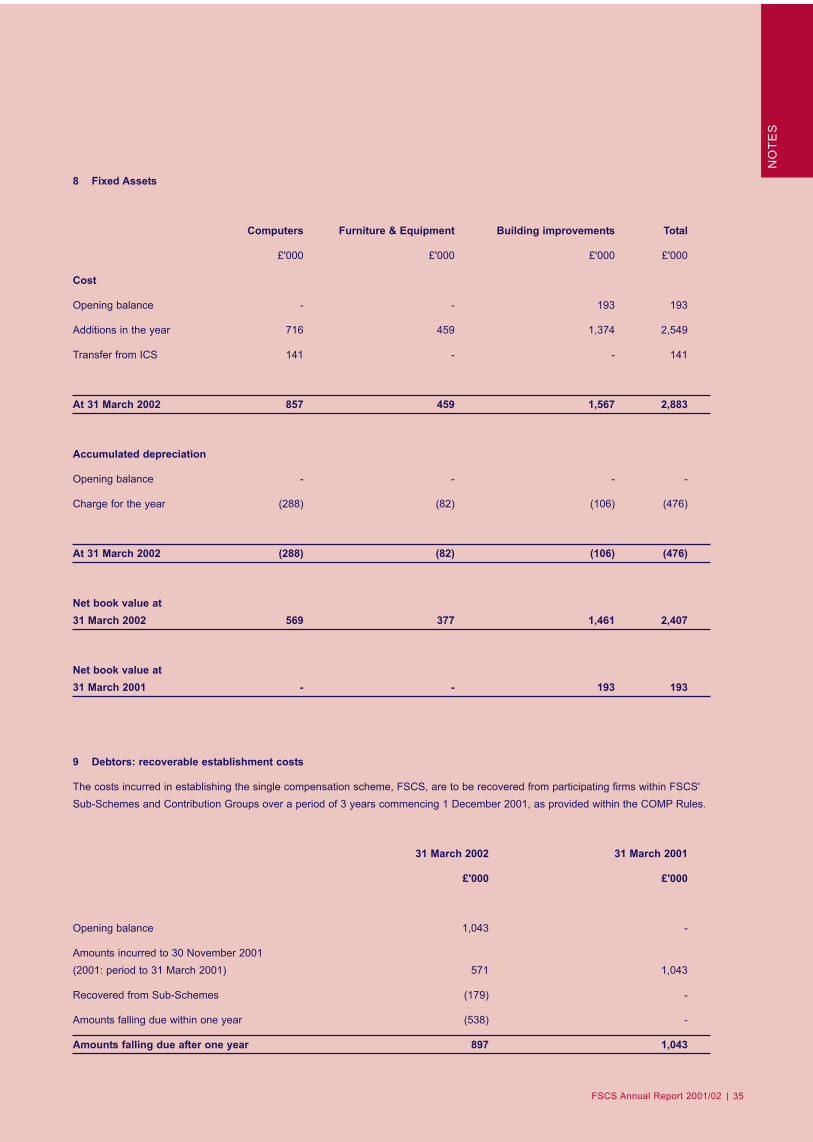

Fixed assetsThe movements in fixed assets during the year are set out in note 8 to the financial statements.

Directors’ ReportReports and Accounts of Financial Services Compensation Scheme Limited for the year ended 31 March 2002

The directors of Financial Services Compensation Scheme Limited (FSCS) present their second report, together with the auditedfinancial statements of the company for the year ended 31 March 2002. The comparatives cover a 13 month period from incorporationon 3 March 2000 to 31 March 2001.

The highest paid director, the Chief Executive, receivedaggregate emoluments in the year of £136,043(comprising basic salary of £128,000 and other emolu-ments of £8,043 (2001: period from October 2000 to 31March 2001, £62,317)) and contributions to a definedbenefit arrangement under the company's pensionscheme have been made of £23,091 (2001: £7,563).

The Chief Executive received no additional remunerationin respect of her role as director.

DE

PAR

TM

EN

TS

FSCS Annual Report 2001/02 25

DE

PAR

TM

EN

TS

At the end of the year retirement benefits were accruing for the Chief Executive as a result of participation in the defined benefitscheme as follows:

Accrued Pension Accrued Pension Increase in Transferat 1 April 2001 at 31 March 2002 Accrued Pension value of

(in excess of inflation) increase

(£ pa) (£ pa) (£ pa) £

S McCarthy 638 2,253 1,604 19,888

The pension entitlement is that which would have been paid annually on retirement based on service to the end of the year on theassumption that the director left service on that date and this excludes any increase for inflation.

The fees paid to the Chairman were set at £40,000 from October 2001 (2001: to September previously £25,000 per annum) and thefees paid to the non-executive directors were set at £10,000 per annum with effect from 17 February 2000. The Chairman anddirectors, other than the Chief Executive, are not entitled to a pension funded by the company.

Liability insuranceFSCS maintains insurance to indemnify itself, its directors and its officers against claims arising from the operations of itself and itssubsidiary, ICS.

Statement of the directors' responsibilities in respect of the financial statementsCompany law requires the directors to prepare financial statements for each financial year which give a true and fair view of the stateof affairs of the company and of the income and expenditure for that period. In preparing these financial statements, the directors arerequired to:

� select suitable accounting policies and then apply them consistently;

� make judgements and estimates that are reasonable and prudent;

� state whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the financial statements; and

� prepare the financial statements on the going concern basis unless it is inappropriate to presume that the company will continue in business.

The directors confirm that the financial statements comply with these requirements.

The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financialposition of the company and to enable it to ensure that the financial statements comply with the Companies Act 1985. They are alsoresponsible for safeguarding the assets of the company and hence for taking reasonable steps for the prevention and detection offraud and other irregularities.

The maintenance and integrity of the FSCS website is the responsibility of the directors. The directors recognise that uncertaintyregarding legal requirements may be compounded as information published on the internet is accessible in many countries withdifferent legal requirements relating to the preparation and dissemination of financial statements.

Corporate GovernanceA statement of corporate governance is contained in FSCS' Annual Report.

AuditorsA resolution proposing the re-appointment of PricewaterhouseCoopers as auditors will be put to members at the Annual GeneralMeeting.

By order of the BoardM Thomas, Secretary30 May 2002

AC

CO

UN

TS

FSCS Annual Report 2001/0226

Respective responsibilities of directors and auditorsThe directors' responsibilities for preparing the annual report and the financial statements in accordance with applicable UnitedKingdom law and accounting standards are set out in the statement of directors' responsibilities.

Our responsibility is to audit the financial statements in accordance with relevant legal and regulatory requirements and UnitedKingdom Auditing Standards issued by the Auditing Practices Board.

We report to you our opinion as to whether the financial statements give a true and fair view and are properly prepared inaccordance with the Companies Act 1985. We also report to you if, in our opinion, the directors' report is not consistent with thefinancial statements, if the company has not kept proper accounting records, if we have not received all the information andexplanations we require for our audit, or if information specified by law regarding directors' remuneration and transactions is notdisclosed.

We read the other information contained in the annual report and consider the implications for our report if we become aware ofany apparent misstatements or material inconsistencies with the financial statements. The other information comprises only thedirectors' report.

Basis of audit opinionWe conducted our audit in accordance with auditing standards issued by the Auditing Practices Board. An audit includesexamination, on a test basis, of evidence relevant to the amounts and disclosures in the financial statements. It also includes anassessment of the significant estimates and judgements made by the directors in the preparation of the financial statements, and ofwhether the accounting policies are appropriate to the company's circumstances, consistently applied and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in orderto provide us with sufficient evidence to give reasonable assurance that the financial statements are free from material misstate-ment, whether caused by fraud or other irregularity or error. In forming our opinion we also evaluated the overall adequacy of thepresentation of information in the financial statements.

OpinionIn our opinion the financial statements give a true and fair view of the state of the affairs of the company at 31 March 2002 and ofits result and cash flows for the year then ended and have been properly prepared in accordance with the Companies Act 1985.

PricewaterhouseCoopersChartered Accountants and Registered AuditorsLondon30 May 2002

Report of the AuditorsIndependent auditors’ report to the members of Financial Services Compensation Scheme Limited for the yearended 31 March 2002

We have audited the financial statements which comprise the income and expenditure account, the balance sheet, the statement ofcash flow and the related notes.

FSCS Annual Report 2001/02 27

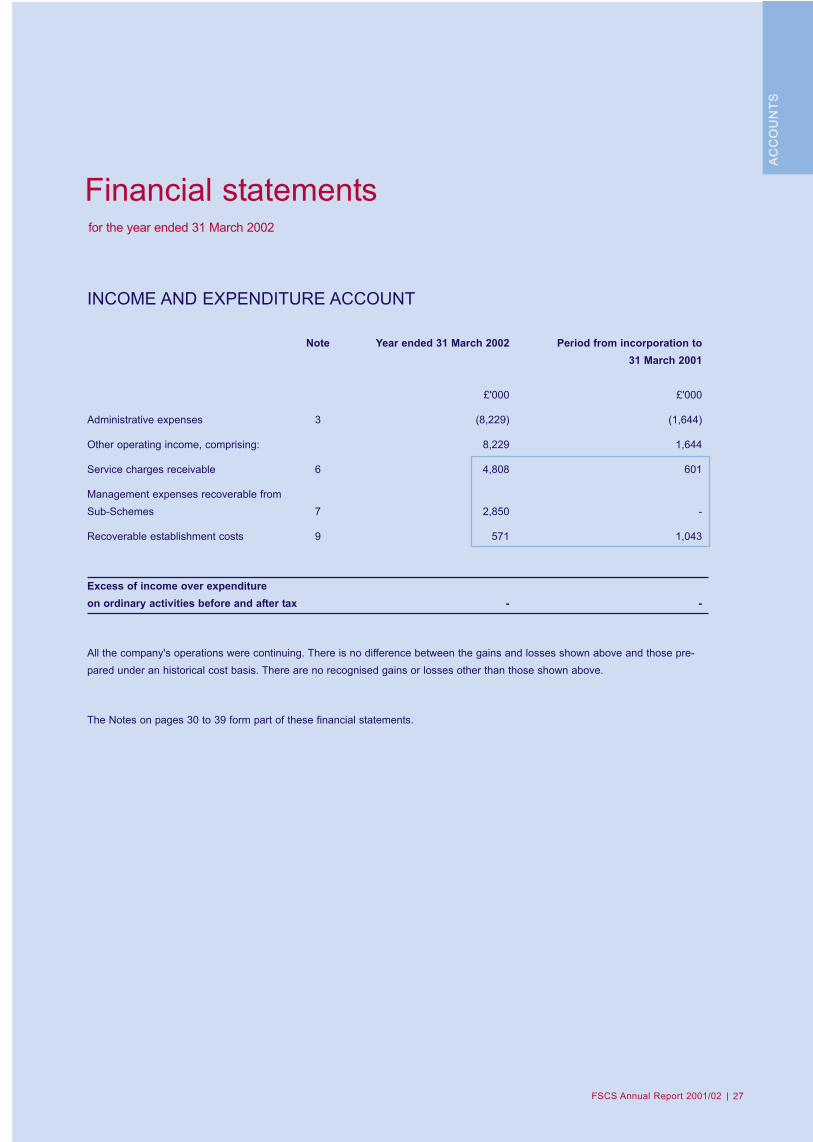

INCOME AND EXPENDITURE ACCOUNT

Note Year ended 31 March 2002 Period from incorporation to 31 March 2001

£'000 £'000

Administrative expenses 3 (8,229) (1,644)

Other operating income, comprising: 8,229 1,644

Service charges receivable 6 4,808 601

Management expenses recoverable from Sub-Schemes 7 2,850 -

Recoverable establishment costs 9 571 1,043

Excess of income over expenditure on ordinary activities before and after tax - -

All the company's operations were continuing. There is no difference between the gains and losses shown above and those pre-pared under an historical cost basis. There are no recognised gains or losses other than those shown above.

The Notes on pages 30 to 39 form part of these financial statements.

Financial statementsfor the year ended 31 March 2002

AC

CO

UN

TS

FSCS Annual Report 2001/0228

Financial Statementsfor the year ended 31 March 2002

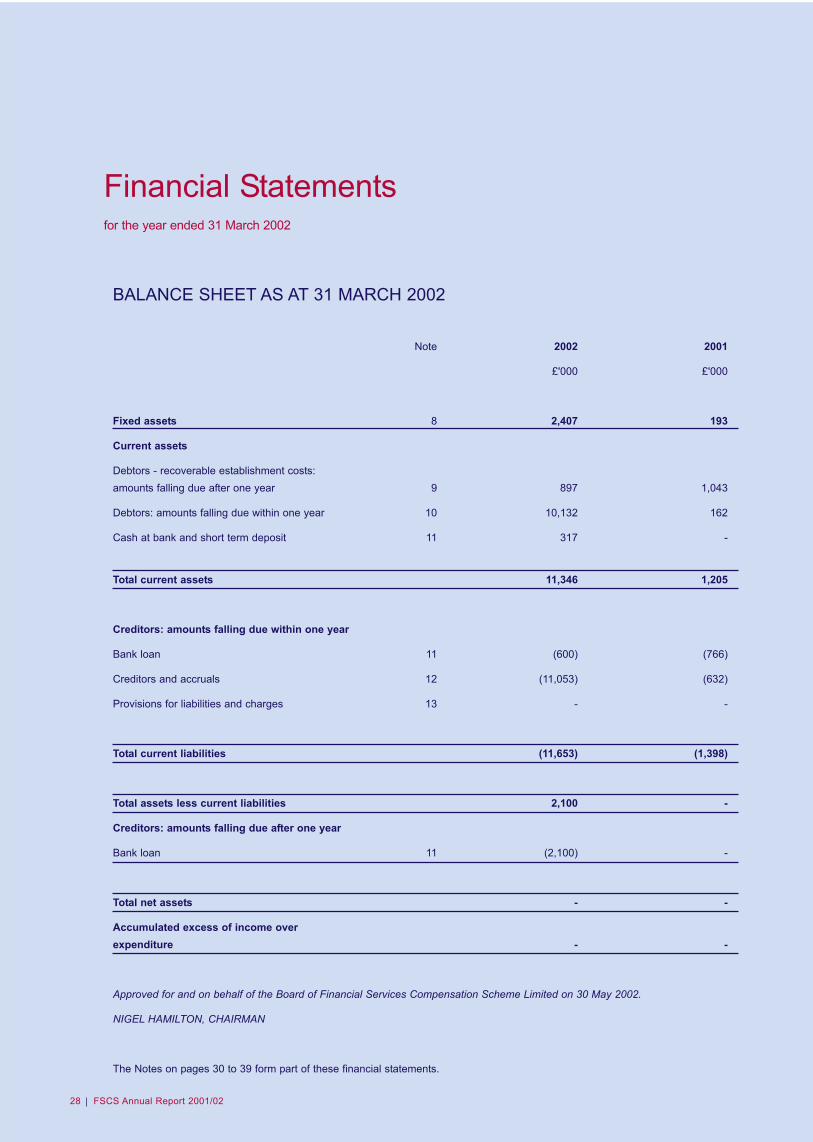

BALANCE SHEET AS AT 31 MARCH 2002

Note 2002 2001

£'000 £'000

Fixed assets 8 2,407 193

Current assets

Debtors - recoverable establishment costs: amounts falling due after one year 9 897 1,043

Debtors: amounts falling due within one year 10 10,132 162

Cash at bank and short term deposit 11 317 -

Total current assets 11,346 1,205

Creditors: amounts falling due within one year

Bank loan 11 (600) (766)

Creditors and accruals 12 (11,053) (632)

Provisions for liabilities and charges 13 - -

Total current liabilities (11,653) (1,398)

Total assets less current liabilities 2,100 -

Creditors: amounts falling due after one year

Bank loan 11 (2,100) -

Total net assets - -

Accumulated excess of income over expenditure - -

Approved for and on behalf of the Board of Financial Services Compensation Scheme Limited on 30 May 2002.

NIGEL HAMILTON, CHAIRMAN

The Notes on pages 30 to 39 form part of these financial statements.

AC

CO

UN

TS

FSCS Annual Report 2001/02 29

Financial Statementsfor the year ended 31 March 2002

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 MARCH 2002

Note 2002 2001

£'000 £'000

Net cash inflow / (outflow) from operating activities 15 1,202 (573)

Returns on investment and servicing of finance 16 (129) -

1,073 (573)

Capital expenditure and financial investments

Payments to acquire tangible fixed assets (2,690) (193)

Net cash outflow from investing activities (2,690) (193)

Acquisitions and allocations

Transfer of cash and term deposits at N2 17 108,605 -

Allocation of fund to Accepting Deposits (9,529) -

Allocation of fund to Insurance (66,217) -

Allocation of fund to Designated Investments (32,859) -

Net cash movement from acquisitions and allocations - -

Financing activities

Loan received 3,000 -

Loan repaid (300) -

Net cash inflow from financing activities 2,700 -

Increase/(decrease) in cash 18 1,083 (766)

FSCS Annual Report 2001/0230

Notes to the Financial Statementsfor the year ended 31 March 2002

1 Constitution, accounting period and subsidiary

Financial Services Compensation Scheme Limited (FSCS) was incorporated on 3 March 2000 and is a company limited by guarantee.The members of the company are the directors of the company, and liability is limited to an amount not exceeding £1 for eachmember.

FSCS was formed as the designated Scheme Manager under s212 of the Financial Services and Markets Act 2000 (FSMA). Its fullpowers were assumed following the coming into force of powers of the Financial Services Authority (FSA), under FSMA, at midnighton 30 November 2001. In anticipation of its powers, FSCS acquired Investors Compensation Scheme Limited (ICS) on 1 February2001 for £Nil consideration. ICS was the current Scheme Manager under the Financial Services Act 1986 with responsibility forcompensation for private clients of UK authorised investment firms that have gone out of business, and is a company registered inEngland.

Financial statements to 31 March 2001 were prepared for the period from incorporation on 3 March 2000 to that date. FSCS assumedits full powers as at midnight on 30 November 2001, before which date its expenses were either recovered as service charges ordeferred as recoverable establishment costs. As from 1 December 2001, management expenses are recoverable from Sub-Schemes.

The company has one subsidiary, ICS, the financial statements of which show net assets of £Nil. ICS did not trade during the period to31 March 2002 although it continued to act in its capacity as Scheme Manager and agent to the ICS Scheme until 30 November 2001.In accordance with s229(2) of the Companies Act, consolidated financial statements have not been prepared in view of theimmateriality of the amounts involved. Financial statements of the ICS Scheme for the year to 31 March 2002 are available from thecompany secretary.

2 Accounting policies

The financial statements have been prepared under the historical cost convention and in accordance with applicable FSMA provisions,COMP Rules and United Kingdom accounting standards.

a) Administrative expenses

These costs are included in the income and expenditure account on an accruals basis.

b) Pension scheme payments

FSCS operates both a defined benefit pension scheme and a money purchase scheme. The costs of the money purchase scheme arecharged to the income and expenditure account as incurred. The costs of the defined benefit scheme are recognised so as to spreadthe cost of pensions over the expected remaining service lives of current employees in the Scheme.

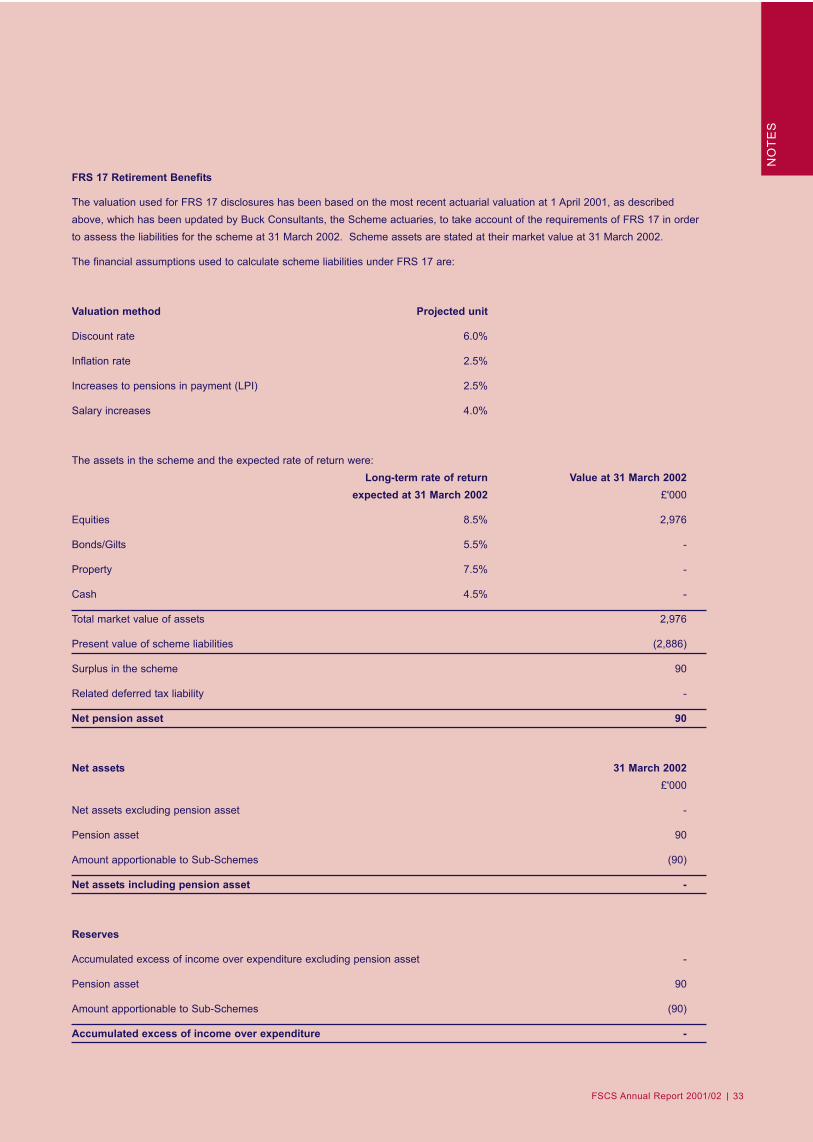

FSCS continues to account for pensions in accordance with the Statement of Standard Accounting Practice No 24 Accounting forPension Costs. A new standard (Financial Reporting Standard No 17 Retirement Benefits ('FRS 17')) which changes the basis ofaccounting for pensions and other post-retirement benefits will be mandatory for the year ended 31 March 2004. This new standardrequires certain additional disclosures in accounting periods prior to its implementation. The additional disclosures for the year ended31 March 2002 are set out in Note 4.

FSCS Annual Report 2001/02 31

c) Fixed assets

Fixed assets are capitalised and depreciated over their estimated useful lives at the following rate:

� Computers: 60% per annum (reducing balance basis)

� Furniture & equipment: 33 1/3% per annum (reducing balance basis)

� Building improvements: straight-line basis over the period of the lease, commencing on occupancy.

Computer software is expensed when incurred.

d) Levies, compensation costs and other items handled on behalf of Sub-Schemes

The Scheme Manager raises levies which are reflected as amounts due to the relevant Sub-Schemes, and receivable from theirContribution Groups. Compensation offers made, accepted, and, for re-instatement cases, fully valued, but not paid at the year-endand any recoveries notified before the year-end, but not received by that date, are accrued by the Scheme Manager and reflected asamounts payable to or receivable from the relevant Sub-Scheme and their Contribution Group(s) in accordance with FSMA and theCOMP Rules.

Management expenses comprise base costs, being the costs of running the Scheme, specific costs, which are the remaining costswhich cover the handling and payment of compensation and establishment costs, which relate to the set-up costs of FSCS prior to 1December 2001. These expenses are allocated by the Scheme Manager to each Sub-Scheme and Contribution Group in accordancewith the levy principles contained within COMP rules 13.5.5, 13.5.6 and 13.5.11.

e) Foreign currencies

Transactions in foreign currencies are recorded at the rate ruling at the date of the transaction. Monetary assets and liabilitiesdenominated in foreign currencies are re-translated at the rate of exchange ruling at the balance sheet date. All differences are takento the income and expenditure account.

3 Administrative expenses

The following amounts are included within administrative expenses:

Year ended 31 March 2002 Period ended 31 March 2001

£'000 £'000

Auditor's fees:

Audit work 40 18

Non-audit work: Due diligence reviews 7 76

Operating lease rentals (see note 14) 672 -

NO

TES

FSCS Annual Report 2001/0232

Notes to the Financial Statementsfor the year ended 31 March 2002

4 Staff costs and FRS 17 disclosure

As from 1 February 2001, 91 former staff of ICS accepted FSCS' contracts of employment. The average number of employees duringthe year was 106 (2001: 16). At the year end the company had 112 staff comprising 84 permanent and 28 contract and temporarystaff.

Employment costs comprise:

Year ended 31 March 2002 Period ended 31 March 2001

£'000 £'000

Aggregate gross salaries together with costs of seconded, contract and long term temporary staff 3,126 1,116