the world that changed the machine - gerpisagerpisa.org/ancien-gerpisa/actes/31/31-3.pdf · the...

TRANSCRIPT

THE WORLD THAT CHANGED THE MACHINE

Synthesis of GERPISA Research Programs

1993-1999

Robert Boyer, Michel Freyssenet

Once again, and over a ten-year span, theworldwide automobile industrial environmenthas changed. The expansion of Japanesecarmakers, at the pinnacle of their success atthe start of 1990’s, only seemed capable ofbeing stopped by American and Europeancompetitors if the latter rapidly adoptedJapanese management methods. Both workersand suppliers had to submit to new productionnorms established in Japan, or else witness theruin of their employer or command source.

This common opinion was corroborated byan MIT research group, IMVP (InternationalMotor Vehicle Program), that published thebook - The Machine that Changed the World(Womack, Jones and Roos). Relying on asystematic comparative study, the authorsattempted to demonstrate the decidedlysuperior productivity level of Japanesecarmaker assembly plants no matter whichcountry they had been implanted in. Theyexplained this superiority by the adaptation ofthe Japanese production system to the demandsof an increasingly varied, variable, andcompetitive international market. According tothe authors, this system was characterizedby thesystematic elimination of waste and lack ofquality by providing an automobile supply thatclosely followed evolutions in demand,directing production in function of commands,and through active participation by workersand suppliers in achieving performanceimprovment objectives. They named the main

principle of this system lean production.In both professional and academic circles,

the subject thus appeared to be finalized: a newproductive model had been born. It wasdestined to replace the old "Taylorian-Fordian"model that had proven its incapacity torespond to new market and societal demandsdue to its organizational rigidity and socialrejection. The acceleration of globalizedcompetition and the liberalization of exchangein the 1990s seemed to confirm the necessityfor firms to become very reactive to themarket, as well as frugal in means thanks toparticipation by all. American and Europeancarmakers had no other choice but to adoptlean production, just like changes after theSecond World War had lead to thegeneralization of the "Taylorian-Fordian"model, according to many analysts. Leanproduction was certainly now going to changethe world.

A System that Failed to Prevent theJapanese Crisis

And yet, a short decade later, this quasi-unanimous conviction seems to have lost itszest. How come the system that was going tochange the world was not able to prevent thecountry that gave birth to it from plunging intoa long period of economic crisis, a period notyet over? How come firms such as Nissan,Mazda, and Mitsubishi, considered up to nowas representative of the Japanese productionmodel as well as other firms, were required at

2

the end of the 1990s to seek out capitalisticalliances or become totally absorbed in orderto avoid bankruptcy? How can one account forToyota and Honda's diminished expansionwhile simultaneously American and Europeanfirms are recovering to the point of leading theacquisitions-mergers-alliance dancethroughout the world?

Drunk with their success, did Japanese firmsneglect the principles of the model they hadinvented? In adopting the Japanese model, didAmerican and European firms perform betterthan their "master"? Is lean production noneother than a step towards a new modelcombining a certain number of its elementswith the principles of modular production thatcarmakers, especially European ones, were thefirst to implement?

Turned more pragmatic, firm managersadmit today that they are seeking to adopt andapply the best practices of their competitors nomatter what they are. Will this less dogmaticapproach, correctly recognizing that nothing isacquired, allow firms to achieve long lastingcompetitiveness? Does it suffice to simply addup the best practices in order to achieve highperformance levels?

GERPISA believes that it can respond to allof these questions with new insight, one basedon a more rigorous scientific and practicalfoundation thanks to research projects carriedout by its members during the 1990s. In 1992,social science researchers who established theinternational GERPSIA group (Grouped'Etudes et de Recherche Permanent surl'Industrie et les Salariés de l'Automobile/ThePermanent Research Group on the AutomobileIndustry and Workers) expressed theirambivalence with MIT's hypothesis. Some ofthem questioned the characterization of leanproduction and its possible adoption withoutimportant local adaptation measures, all thewhile conceding to its general pertinence. Theothers simply rejected the ideal that a universalone best way could even exist. These doubtswere fed by a number of observations.

Some Japanese GERPISA membersunderlined that important differences existedbetween firms in Japan as in any country, and

thus it was dangerous to generalize. They alsoimpressed upon other GERPISA members,unaware of certain facts, that a firm asemblematic as Toyota had experienced animportant labor crisis in 1990 and had beenobliged to implement substantialtransformations in its production system.

Economists members of GERPISA outlinedparticularly difficult conditions required for aglobal homogenization of markets, andconsequently insisted on the probability that atleast a minimum of several variants on themodel would emerge. Historians recalled thefailure of transplanting the Ford system outsideof the United States during the interwar period,and the superior profitability of localcarmakers, thus suggesting that a model hasconditions for feasibility that limit its diffusion.Sociologists questioned whether leanproduction could inaugurate a long lastinginversion of the division of labor betweenconception and execution, and/or radicallychange the content of work. All noted thatessential methodological rules had not beenrespected in comparisons made between firms.Hence, a formally identical component oforganization, such as teamwork, can in factfulfill different functions and target a varietyof objectives in function of the firm.Consequently, this prevented one fromconcluding that lean production, meant to berepresented by teamwork, could be easilydiffused. In short, GERPISA membersconsidered that the plurality of models was asmuch a plausible hypothesis deserving testingas that of the diffusion of a unique model asbeing solely capable of guaranteeing a firm'sprofitability.

This is why the international researchprogram entitled "Emergence of NewIndustrial Models" was launched. It was rapidlyfollowed by a second international researchprogram, "The Automobile Industry: BetweenGlobalization and Regionalization", whichserved as the complement to and expansion ofthe first program. What ensued was a longprocess of identifying successive problems thatprincipal automobile firms, and a certainnumber of their foreign subsidiaries, had

3

encountered since the end of the 1960s, bothin the market and labor fields, as well assolutions they had attempted to implement tosolve these problems. This became the meansby which analyses of shared or differentconditions leading towards profitability couldbe carried out, as well as improvedunderstanding of the meaning attributed tochanges underway, be it in the field of productpolicy, productive organization, and/oremployment relationships.

The main and commonly shared conclusionof this international research project underlinesthe renewed and long lasting diversity ofmacro-economic and societal conditionswherein firms evolve, and the variety in theirstrategic choices and production systemsdespite a certain number apparent or transitoryconvergences.

This contextual, strategic, and socio-productive diversity does not necessarly rendereach firm unique unto itself, thus rejecting theidea of a general model. On the contrary,processes that allowed certain firms to adopt orinvent a coherent and pertinent productionsystem characterize it, but also evolutions thatinversely prevented other carmakers to obtainlong lasting profitability, due to both internaland external reasons leading to one crisis afteranother.

At the end of the first research program,scientific coordinators Robert Boyer andMichel Freyssenet pursued this analysis andextended research to take deeply in accountearlier periods of the automobile industry,other carmakers, and numerous host countriesfor transplants. The objective was to succeed inclear characterization of previously existingproductive models, to conceptualize conditionsfor their emergence, crisis, and disappearance,and from a more extensive standpoint, to becapable of enumerating conditions forprofitability. The analysis scheme thusobtained was tested and developed during thesecond international research program, underthe scientific direction of Michel Freyssenetand Yannick Lung, the goal being to improveunderstanding of the new internationalizationprocesses implemented by firms in the

automobile industry since the second half ofthe 1990s. What follows are the results bothfrom of the first and the second internationalGERPISA reserch programs1.

A Single Productive Model Has NeverExisted

The "received wisdom" of the history of theautomobile industry divided up into threephases has become common to those whostudy it and those who work in it. Following aprimarily "craft"- based phase thatcorresponded to elitist demand, carmakers aresaid to have adopted the mass productionsystem, which - thanks to obtained economiesof scale - allowed the market to be extended tothe population at large. Because of thissystem's inherent rigidity, it is said to have beentrown into crisis by the transition to a morevariable, renewed, and diversified demand aswell as to a far too competitive and globalmarket. Lean production was meant to be themodel adapted to this new configuration.However,_the three supposedly successivesystems are actually the result of historicamalgams and conceptual ambiguities.

From the start of the 20th century,automobile firms were industrial enterprisesusing tool-machines and interchangeable partseven if they assembled their vehicles on a fixedstation or on non-mechanized short assemblylines. These did not disappear in the UnitedStates because of a lack of competitiveness with"mass producers", but rather due to a lack ofliquid assets following the Great Depression.Elsewhere, not only were they maintained andeven developed, but they also competedefficiently with Ford's subsidiaries that, in theabsence of mass consumption, could not beprofitable in the long run. Contrary to Ford,and through supply diversity and productionflexibility, they were able to answer in aprofitable manner to limited and diversifiedmarkets. Several productive models wereelaborated to achieve this. At least two havebeen identified and characterized : the"Woollardian model" and the "Taylorianmodel". The latter was not in fact itselfconceived for "mass production", contrary to

4

many beliefs.Thus the "mass production" model -

erroneously called "Taylorian-Fordian" - infact mixes two models, the "Fordian" and the"Sloanian" models, whose conditions forviability as well as specific characteristics aredifferent despite the fact that they share theprinciple of the mechanized assembly lineamongst themselves and with others. The"Fordian model" implemented a volumestrategy by mass producing a standard vehiclewhereas the "Sloanian" model implementedboth a volume and diversity strategy bydiversifying its models "on the surface"through body, saddlery, and equipment, andby commonalizing the invisible parts andplatforms. While the first model experienced atransitory and geographically limited existence,the second appeared from the 1950s on tohave become the universal model, given thedevelopment of a finely hierarchized demandranging from bottom-of-the-line to top-of-the-line products. Indeed, a decidedly visibleconvergence was observed.

However, the diffusion of the "Sloanianmodel" was slowed down, first by the laborcrisis at the end of the 1960s, then by themonetary and petrol crises spanning 1971 to1974. These crises even seemed to strip awayany viability whatsoever of the "Sloanianmodel". In fact, it met some difficulties in theUnited States during the 1960s, paradoxicallydue to its success at the very moment when itwas being celebrated as the one best way for

the second half of the 20th century. Inaddition, it had not been as widely adopted asmanagerial discourse, and hasty conclusions,had reported at the time. Indeed, it had beenadopted only by a certain number of firms inonly a few industrialized countries wherenational income distribution was carried out ina coordinated and moderately hierarchizedmanner.

Two new industrial models weresimultaneously being developed in theJapanese automobile industry: the "Toyotanmodel" privileging "permanent reduction ofcosts at constant volume", and the "Hondianmodel" implementing a totally different profit

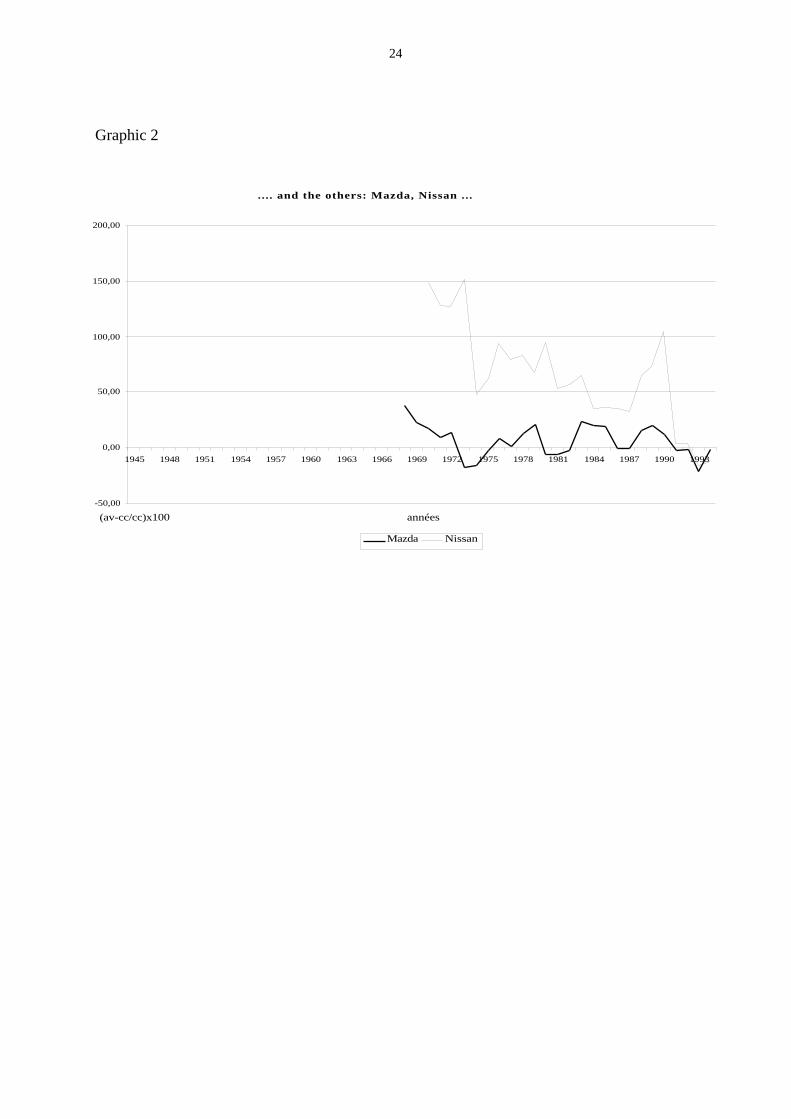

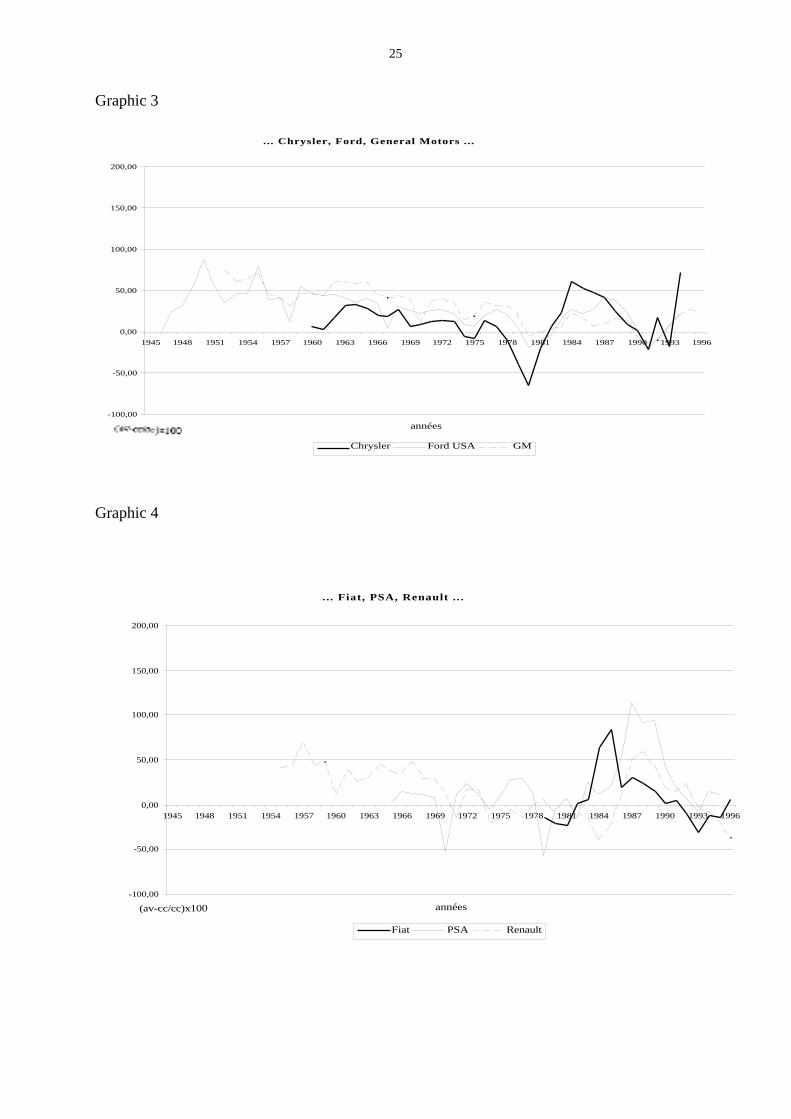

strategy of "innovation and flexibility". Thesetwo models were erroneously placed under thesame heading of lean production despite thefact that they differ significantly on essentialpoints. The remarkable performances of thefirms which embodied these models (Toyotanand Hondian) did not chase however the"Sloanian model" away, Volkswagen adopted itas of 1974, and was able to exploit it profitablyin the context of a renewed market. Thesethree firms Toyota, Honda, and Volswagenwere in fact the only ones to have a "break-even point" that was constantly andsignificantly above their value added, whereasall other carmakers had experienced periods ofnon-profitabilit. (see graphic 1 to 5, appendix)

It is not the intrinsic and non-temporalqualities of their productive models thatachieved the performance levels of these threefirms. The first reason of their profitability wasthe relevance of their profit strategies to theircountry's "national income distribution andgrowth mode" that the international contextprivileged after 1974. Floating exchange ratesand oil crises, by cutting back on worldwidegrowth, provoked in fact confrontationbetween industrial economies. In that context,countries which had a growth that relied onexports, and whose national incomedistribution was already a function of externalcompetitiviness, such as was the case for Japanand Western Germany were in a favorableposition. Firms that were particularly favoredwere those that had a profit strategy basedeither on "permanent reduction of costs atconstant volume" such as Toyota or on"innovation and flexibility" notably destinedfor exportation, such as Honda, or yet again aprofit strategy based on "volume and diversity"thanks to internationalization, the buying outof other carmakers and the commonalizationof car models platforms such as Volkswagen.

Apart from fulfilling this first criterion forprofitability, the aforementioned three firmshad also fulfilled the second one, it is anadequate "enterprise government compromise"between the main protagonists of the firmconcerning "product policy", "productiveorganization", and "employment relationships",

5

allowing for implementation of the chosenstrategy in a coherent manner. The othersJapanese and German carmakers that did notfulfill one or the other of the two criteria beganto experience difficulties (that no one wantedto recognize at the time due to widespreadshared perception of the superiority of the"Japanese model", and to a lesser degree, the"German model"), thus well before the turningpoint of the 1990s that fully revealed thesedifficulties.

On the contrary, countries whose growthbefore 1974 had relied on domesticconsumption and whose national incomedistribution was regulated by domesticproductivity gains were destabilized. Theseinclude the United States, France, and Italy, aswell as free market countries having littleregulation such as Great Britain. It isinteresting to note that all carmakers in thesecountries, without exception, underwent at leastone serious crisis between 1974 and 1990 andwere not able to reconstruct or invent a newproductive model. (see Table 1, appendix)

The international context changed onceagain in the 1990s. The "speculative bubble"had already carried the three aforementionedmodels to their limits among those carmakersembodying them, at the very moment when atleast two of them, mixed together under thesame lean production definition, were beingpresented as the future of the world, a scenarioidentical to the "Sloanian model" mise en scènein the 1960s. In 1990, Toyota underwent asevere labor crisis that forced it to change its"enterprise government compromise" andsubstantially transform its productive model.Honda at the same time made an errorevaluating emerging demands, andVolkswagen, swept up by growth levels, hadproblems controlling its costs. Simultaneously,carmakers previously in difficulty hadproceeded to drastically reorganize andimplement some major strategic reorientations.The bursting of the "speculative bubble",restrictive budgetary policies, the "emergence"of a certain number of countries, and above allthe transformation of "national incomedistribution and growth mode" were to change

relationships between countries, automobiledemand, mobilizable labor, and automobilegeography.

Most industrialized countries abandonednational income distribution based on internalproductivity. Some of them had adopted a"competitive" national income distribution, thatis to say, one based on local and categorialagreements. Directly or indirectly theydestabilized the countries that have beenprivileged by the previous international context(notably Germany and Japan) and thatmaintained a largely coordinated andmoderately hierarchized distribution. Thenature and meaning of confrontation betweencountries thus changed. It is within this contextthat differents tendancies to recomposition ofthe world were to occur: general liberalizationof exchange, constitution of regional spaces,reaffirmation of somes nations. In addition,"competitive" income distribution mode,through the economic and social differencesthus created, gave birth to a second automobilemarket, that of pick-ups, minivans, recreationalvehicles, and other conceptually innovativevehicles. This second market, which now hasbecome as important as that of sedans in theUnited States, has attributed a new andexpanded degree of pertinence to the"innovation and flexibility" strategy that Hondaand other firms such as Chrysler and Renaultsubsequently adopted.

Today, automobile firms must bet on theworld's recomposition type as well as thenational income distribution and growth modethat will prevail in the next ten years, to choosea pertinent profit strategy and to constructstrong "enterprise government compromises".

This new representation of the automobileindustry history resulting from GERPISAresearches does not offer the same simplicity asthe three successive models of IMVP, that wereeasy to remember and apparently even easierto apply! Should this be regretted? Though itcontinues to prevail to this day, it presents theunfortunate inconvenience of simply being afairy tale.

Are actors of the firms (stockholders, banks,directors, workers, unions, suppliers, etc.) now

6

deprived of a convenient compass due to therelative complexity inherent to the newproposed representation of automobileindustry history? If a number of possibilitiesexist, how can choose an productive modelwhich is economically pertinent and sociallyacceptable? Why have some firms notsucceeded in embodiing or inventing a model,and have experienced long periods ofoscillating between loss and profit, some evendisappearing altogether?

Contrary to appearances, a more complexand long term vision of the history of theautomobile sector allows one to highlightgeneral and valid rules for all periods andareas. These consist in more operational rulesfrom a practical and scientific standpoint thanthose affirming the existence of a singleperformant model for each important periodaccompanied by naïve encouragement of itsgeneral adoption. The analysis of firms andsubsidiaries trajectories, as carried out byGERPISA, allows to bring two essentialconditions for profitability in light and todefine the possibilities of action for firm'sactors to invent or adopt production forms thatcan become the object of acceptablecompromise by all.

These conditions and possibilities will bediscussed in the next two sections, followed bya detailed presentation of profit strategies andidentified productive models.

Two essential conditions for profitabilityThese two conditions can be summed up in

two sentences:1. The pertinence of "profit strategy" in

relationship to "national incomedistribution and growth modes" in thosecountries where the firm evolves;

2. The solidity of the "enterprise governmentcompromise" that allows the firm's actors tofind and implement the means ("productpolicy", "productive organization", and

"employment relationships") that are bothcoherent in light of the adopted profitstrategy and acceptable by all these actors,in other words, the invention or adoptionof a productive model.

3. Hence, productive models can be definedas "enterprise government compromises"that allow "profit strategies" to beimplemented, and that are viable within the" national income distribution and growthmode" of the countries wherein firms areactive, through coherent means acceptedby all the actors.

Inversely, firms that have not succeeded ininventing or adopting a productive model, arefirms that have not fulfilled at least one of thetwo conditions required for profitability. Eithertheir profit strategy was not pertinent relative tothe national income distribution and growthmode or else became non-viable followingchanges in growth modes, or a "enterprisegovernment compromise" was never elaboratedamong the firm's actors or else was rejected byone or several protagonists (see figure 1,appendix).

What is the meaning of "profit strategy","income distribution and growth mode","enterprise government compromise", "productpolicy", "productive organization", and"employment relationships"? Historical studieshave shown that carmakers have not privilegedthe same profit sources. Two reasons canexplain this phenomenon. First, profit sourcescan not all be exploitable at any time andanywhere. Second, they are not all compatibleamong themselves due to their contradictoryrequirements. This is why above all firmsdistinguish themselves by their differentcombinations of profit sources, in other words,by what we have defined as their "profitstrategies". Profit source combinations do notnecessarily nor always result from a consciousand/or deliberate choice, but from anprogressive ajustment process.

7

Figure 1

PRODUCTIVE MODELand its context

international regime

national incomedistribution and growth

mode

market labor

profitstrategy

productpolicy

enterprisegovernmentcompromise

productiveorganization

employmentrelationships

GERPISA, Robert Boyer, Michel Freyssenet, 06.05.2000

The number of profit sources directly linked to automobile industrial activity comes

8

to six: economies of scale, supply diversity,product quality, pertinent commercialinnovation, productive flexibility, andpermanent reduction of costs at a constantvolume. During the first century of automobileproduction, carmakers implemented at least sixdifferent profit strategies that we havementionned by name of privileged profitsources: the "diversity and flexibility" strategy,the "volume" strategy, the "volume anddiversity" strategy, the "quality" strategy, the"permanent reduction of costs at constantvolume" strategy, and the "innovation andflexibility" strategy.

These "profit strategies" were not all equallypertinent at all times and everywhere. In orderto be so, they each require specific types ofmarkets and labor that only certain Nationalincome distribution and growth modesprovide. To briefly illustrate this, one can sayfor example that the "volume" strategy -consisting in massively producing a uniqueproduct - requires (in order to be viable in thelong term) continued and sociallyundifferentiated progressive buying power ofthe population as well as a labor force thataccepts work conditions associated withhomogenous production. On the contrary, the"quality" strategy - consisting in offeringexecutive range models that symbolize theprestigious economic and social status of thebuyer - prospers in countries where asubstantially proportion of stabilized highrevenues exist, and where one may also find arelatively more skilled work force.

"National income distribution and growthmodes" are not numerous and several countriescan implement the same mode simultaneouslyor at different times. This is why certain profitstrategies can simultaneously be found inseveral areas or during several historicalperiods. Inversely, the same "national incomedistribution and growth mode" can guaranteefor the viability of several "profit strategies".This is why there is neither universalproductive model, nor national productivemodels.

"National income distribution and growthmodes" are differentiated by the major source

of growth (investment, consumption, orexportation) and by the form of incomedistribution ("competitive", "regulated" infunction of internal productivity or externalcompetitiveness, etc.). For example, the modecalled "competitive and competed", because thegrowth depend on competitiviness of each firmin national and international market andbecause the national income distribution modedepends on local and professional agreementswas that of most of the European countriesbefore World War I and of some of themduring the inter war period. The mode called"consumer-oriented and coordinated", becausethe growth is based on the internalconsumption, the national market is protectedand the income distribution is coordinated atnational level in function of internalproductivity gains, was that of the UnitedStates, France, and Italy from 1950's to1970's.The mode called "specialized exporter andcoordinated", because the growth is pushed byexporation of specialized products, the marketis protected by the quality of products, and theincome distribution is coordinated in functionof external exchange gains, still present inGermany to day, and was employed bySweden. The mode called "price-exporter andcoordinated", because the growth is based onprice competitiveness of exported goods, theinternal market is protected, and the incomedistribution is coordinated in function ofexternal exchange gains" is that of Japan,South Korea, etc.

"Profit strategies" can not be implementedusing any means. The "product policy","productive organization", and "employmentrelationships" must correspond to preciserequirements that are specific to each profitstrategy. However, in reality, they are often thefruit of successive contradictory choices,tensions between actors and the firm, orexternal constraints. Rendering means coherentwith the adopted "profit strategy" can only beaccomplished and maintained if the firm'smain actors first agree on the strategy itself,and then on the means. This agreement can notbe concluded unless it allows each protagonistthe perspective of attaining his/her own goals in

9

the mid or long term. No coherence is possible,no profit can be a long lasting one without theconstruction of a solid "enterprise governmentcompromise".

Fortunatelly, "profit strategy" requirementscan be fulfilled in many ways. Nothing obligesa firm to submit to the means supposedlyimposed by the "profit strategy" selected. Infact, we have been able to observe, for example,that the "diversity and flexibility" strategy wasimplemented not by a single productive model,but by two different models at the same periodand in the same country, that is to say the"Taylorian model" and the Woollardianmodel". Likewise, Toyota was obliged tochange its "enterprise governmentcompromise" during the 1990s in order tocontinue implementing its "permanentreduction of costs at constant volume" profitstrategy following the labor crisis that it hadundergone.

The emergence or adoption of a productivemodel that is not based on an intellectualconversion and/or application of firmlyestablished dispositions. These are in partunintentional processes. They imply thesynchronization of conditions that render theprofit strategy feasible as well as means toimplement it. This synchronization oftenescapes control by enterprise players, fromboth a cognitive and practical standpoint. It isoften only after the fact that they realize thatconditions and means joined together in asystem, and thus they proceed to theorize this.Inversely, when they want to adopt a modelthat has born fruit elsewhere, they are neverguaranteed that their decisions will indeedallow for the synchronization of conditionsand means, due to the fact that interveningsocial processes are numerous and the effectsof their intersection difficult to predict.

Here lies precisely the practical utility ofsocial science research, that of identifyingsocial processes, dissecting them, andsubsequently highlighting the possibility to actso as to facilitate actions undertaken bydifferent enterprise players in conformity withtheir specific perspectives.

The possibilities and limits of action forenterprise players

Just what exactly are the possibilities andlimits for enterprise players? Profit within thecapitalist system is the essential condition forthe firm's viability. If what we have presentedthusfar is valid, theoretically, therefore, actorsmay act upon the "national income distributionand growth mode", the "profit strategy", and/orthe content of the "enterprise governmentcompromise". Naturally, their capacity to acton these three levels is unequal.

Countries are not free to choose their"national income distribution and growthmode". Apart from their resources and history,the choice depends on internationalrelationships they have among themselves,especially with the most powerful country atthat particular period. A growth based oninternal consumption and coordinated andmoderately hierarchized national incomedistribution are only possible if customsbarriers or a structural advantage protect thecountry from more competitive foreignproducts. However, a country is required todeal with others in order to establish itscustoms tariff regime. The determination of a"national income distribution and growthmode", the latter shaping the pertinence ofdifferent "profit strategies" (in other words thefirst condition for profitability for firms) thuslargely escapes control by the enterpriseplayers. The latter may indeed have moredifficulty in maintaining or changing the"national income distribution and growthmode" so that it remain or become favorable tothe firm's "profit strategy", than in finding anew pertinent "profit strategy".

In any case, firm actors can not just remainpassive. Indeed, they may hope that one modeor another be maintained or adopted inaccordance with the conception they have ofboth national independence and thedistribution of produced wealth for example.History has shown that their action is not onlypossible but also necessary. This was the caseafter World War II, between 1974 and 1980,and most probably at the present time.

Hence, theoretically, enterprise players can

10

choose among "profit strategies" that "Nationalincome distribution and growth modes"authorize within the areas the firm evolves in.But frequently they don't realize that a choiceis possible, due to the fact that each individualis persuaded that there are not a million waysto make a profit. Naturally, the choice is notentirely free from constraints. It thus dependson the "profit strategy" already undertaken inthe firm, and on other carmakers' "profitstrategies". Indeed, changing a "profit strategy"is easier said than done. It first requires thereconstruction of an "enterprise governmentcompromise" about the means to employ,therefore the necessity to engage in a long-term and potentially conflictual process havinguncertain results. It also depends on thechoices of competitors. It can be riskyadopting the same strategy as one'scompetitor(s), since it(they) have already beenthere for awhile and have constructed a solid"enterprise government compromise" that hasput means into synergy. What remains to bechosen is a no-used "profit strategy" amongthose authorized by the "national incomedistribution and growth mode".

However, some circumstances have shownthat the invention of a new strategy is possible,even necessary, by rendering compatible profitsources considered up to now as beingcontradictory. This was the case with volumeand diversity rendered compatible by GeneralMotors during the interwar period, when theirvehicle platforms were put to common use soas to generate economies of scale but also bydiversifying them "on the surface" throughbody, saddlery, and different equipment so asto respond to demanded diversity.

Of course, the possibilities of choice inconstructing of "enterprise governmentcompromise" are more large. It is important tobe conscious of that to attenuate the impatientof firm's directors, who generally insists thatthe only solution possible is the one theypropose. An analysis of automobile firmtrajectories over the past century allowseveryone to conclude that this impatience is theworst way to achieve lasting profitability. All"enterprise government compromises" that

have allowed for the invention or adoption of aproductive model required at least ten years tobe built and a large degree of intelligence onthe part of all partners so that each one did notfeel he/she gave up on his/her principles andgoals. In fact, the range of possible means islarger than what appears to be the case,including means that appear intrinsic toindustrial activity such as the assembly line.Without delving into details here, we can say -by looking at a very extreme example - thatthe mass production of a unique car modelassembled in a fixed station by two to fourworkers is technically possible andeconomically profitable under the conditionthat employment relationships in practicerender this viable. Now the time has come topresent the "profit strategies" and "productivemodels" identified and to illustrate thepreceding comments.

Profit Strategies and Productive ModelsThe "diversity and flexibility" strategy and

the "Taylorian" and "Woollardian" modelsThe "diversity and flexibility" strategy

consists in offering specific automobile modelscorresponding to demands by economicallyand socially distinct customers who expressmarkedly distinguished identity criteria. It alsoinvolves rapidly adapting to quantitative andqualitative variations in these demands infunction of the irregular revenue evolutions ofthis category of customers.

This type of simultaneously "Balkanized"and unstable market is essentially found in a"national income distribution and growthmode" wherein revenue and salary formation,instead of being regulated in function ofproductivity or exterior competitiveness, issubmitted to "competition" in function of localand categorial power relations. The harshnessof social relations leads each social andprofessional group to defend their acquiredpositions and consolidate them. In such asocial and economic context, mass demand hasdifficulty in forming due to highly irregularrevenue evolutions. This mode, which we havecalled "competitive-competed", was found in anumber of countries before World War II, and

11

continued to be the case in Great Britain. The"diversity and flexibility" strategy was logicallyadopted by most European carmakers in theinterwar period as well as British firms beforethe British Leyland was created at the end ofthe 1960s. Is this strategy now part of the past?Things are not so sure. The return to systemsof "competitive" salary and revenue formationseems to be attributing new pertinence to it.

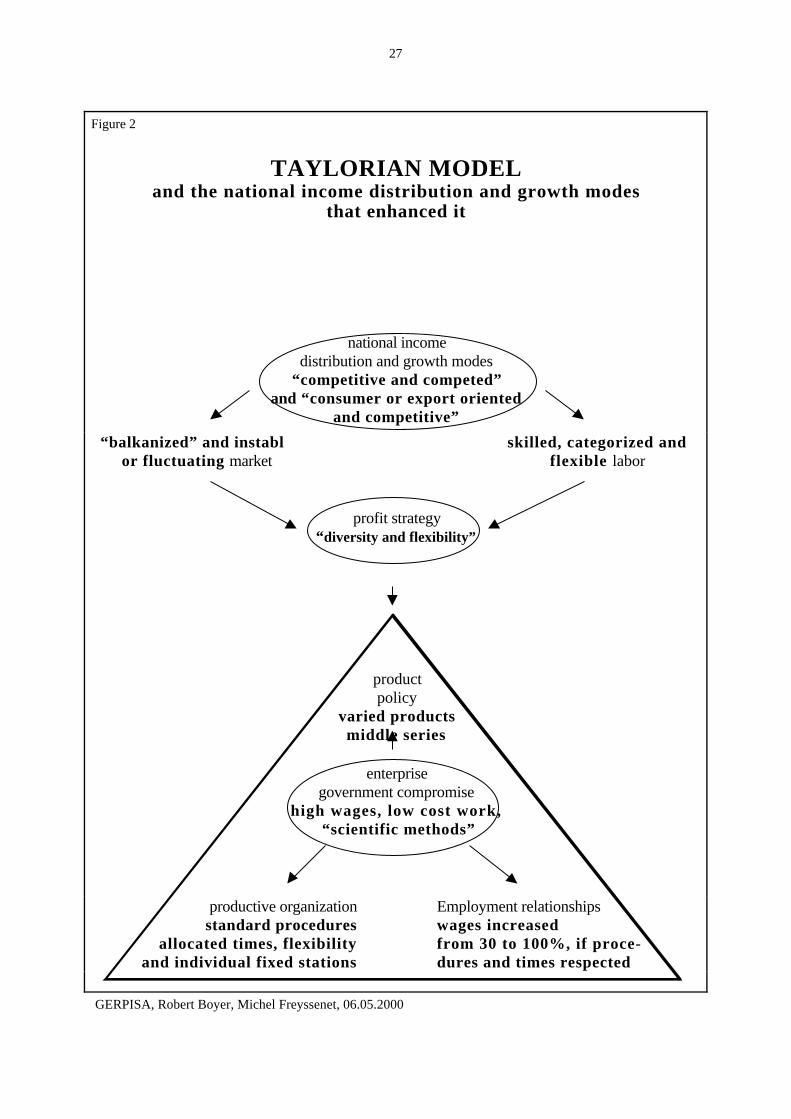

To be implemented, the "diversity andflexibility" strategy requires a product policymade up of coherent models, sharing a limitingnumber of common parts with other car-models, responsive to each demand category,and profitable unto themselves. The productiveorganization must allow the firm to rapidlyconceive of new models at the lowest cost, andchange product as often as necessary infunction of demand variations. Employmentrelationships must offer compensation for therequired level of flexibility and competence.At least two productive models haveimplemented the "diversity and flexibility"strategy: the "Taylorian" and the "Woollardian"models. However, they differ in their"enterprise government compromises" as wellas by the means employed (see figures 2 and 3,appendix).

What is called "Taylorism" today has little todo with its historical specificity. Indeed, the"Taylor method" can not be reduced to one orthe other of its techniques - for example,timekeeping - nor expanded to the separationbetween conception and execution. of which itwas but one historical form and certainly notthe most important. In fact, Taylor had calledfor a complete production system in order tosolve one of the most typical problems ofdiversified production, in small and average-sized series, fixed stations, or non-mechanicalshort assembly lines, that is to say what hecalled "worker idleness". It is typical of thiskind of production, since it no longer is aproblem once the assembly line is adopted.Everyone recalls that Taylor mainly defined"worker idleness" as a function of managementpractice consisting in decreasing the wage paidby produced part and reducing the work forcewhenever an increase in hourly wages was

obtained one way or the other. Hence, heproposed to conciliate high salaries andinexpensive labor by increasing the valueadded instead of negotiating its distribution.He confirmed that daily production could thusbe doubled or even quadrupled. He guaranteedthat workers would be ready and willing towork more efficiently in accordance with asequence of operations and in "scientifically" -thus impartial - established time framesdesigned by a special team in charge ofanalyzing and timing both skilled andunskilled tasks. The condition was thatemployers pay those workers accepting thenew rules from 30 to 100% more than theaverage. The establishment of a standardsequence of operations for each task did notquestion its intellectual logic; as the assemblyline soon would in its dispersal of operationsamong different work stations solely for thepurpose of "saturating" the cycle time at eachwork station. Taylor often repeated that the"optimal" sequence and the time required forits execution could only be correctlydetermined with more experienced andefficient workers, and not by a single serviceisolated from fabrication, as has been endlesslyreiterated over the past thirty years.

The "Taylor method" became the"Taylorian model" when firms pursuing a"diversity and flexibility" strategy adopted it,and when it was adapted to become sociallyacceptable. The "Taylorian model" wascharacterized by an "enterprise governmentcompromise" mainly established betweenmanagers, organizational engineers, andworkers. It is built around the following: 1° acompetitive, varied, and average-size seriesproduct policy; 2° skilled and unskilled taskorganization simultaneously applied inconception, fabrication, and administration, onthe one hand founded on procedures andrequired operational modes, and on the otherhand, allotted time defined by those involvedand in accordance with a specialized service; 3°employment relationships wherein the wage issignificantly increased if procedures andallotted time are respected or improved. This"compromise" gave firm managers increased

12

productivity and flexibility. Meanwhile,organizational engineers were attributed alarger scope of power, and those workers whoaccepted the new work rules received highersalaries. Thus, the "Taylorian" model wasprofitably adopted where series weresufficiently long enough to obtain a benefitfrom preparing and normalizing tasks. Thiswas to be the case for several American andFrench carmakers in the interwar period.

British carmakers in the interwar periodgenerally chose another "enterprisegovernment compromise" so as to produce avariety of distinct cars destined for a"Balkanized" and limited market, and to avoidconfronting a skilled and categoricallyorganized labor force. This method consistedfirst in relying on individual and collectiveknow-how as well as the autonomy of thisworkforce in order to dispose of requiredlevels of flexibility; second in mechanizing andsynchronizing supply to fixed workstations orshort, non-mechanized assembly lines toreduce intermediate stocks and handling.Demands in volume and delays were obtainedby a salary system qualified as "incentive" or"inductive" characterized by a piece rate, whichcould be highly increased by individual orgroup bonuses attributed in function ofproduced volume and the time used toaccomplish this. This original productivemodel, which we have called the "Woollardianmodel" (named after Frank Woollard,fabrication engineer at Morris, main theoristand craftsman of the method), guaranteed tofirm owners and managers a regular return oninvested capital, offered required quantitativeand qualitative flexibility to fabricationengineers, and attributed the requested level ofautonomy and work qualificationcorresponding to workers' demands.

As one may easily observe, the "Taylorian"and "Woollardian" models were completelydifferent yet implemented the same profitstrategy. These models encountered a crisiswhen the profit strategy they implemented lostits pertinence, for example when thedistribution of national income becames morecoordinated, predictable, and moderately

hierarchized. The firms that progressivelymade up British Leyland in the 1960s and1970s failed to become again profitable tryingto make the transition from the "Woollardian"model to the "Taylorian" model that theyhoped would bring about a greater degree ofdiscipline among workers. The reason was theTaylorian model was also ill-adapted to thenew British national income distribution andgrowth mode.

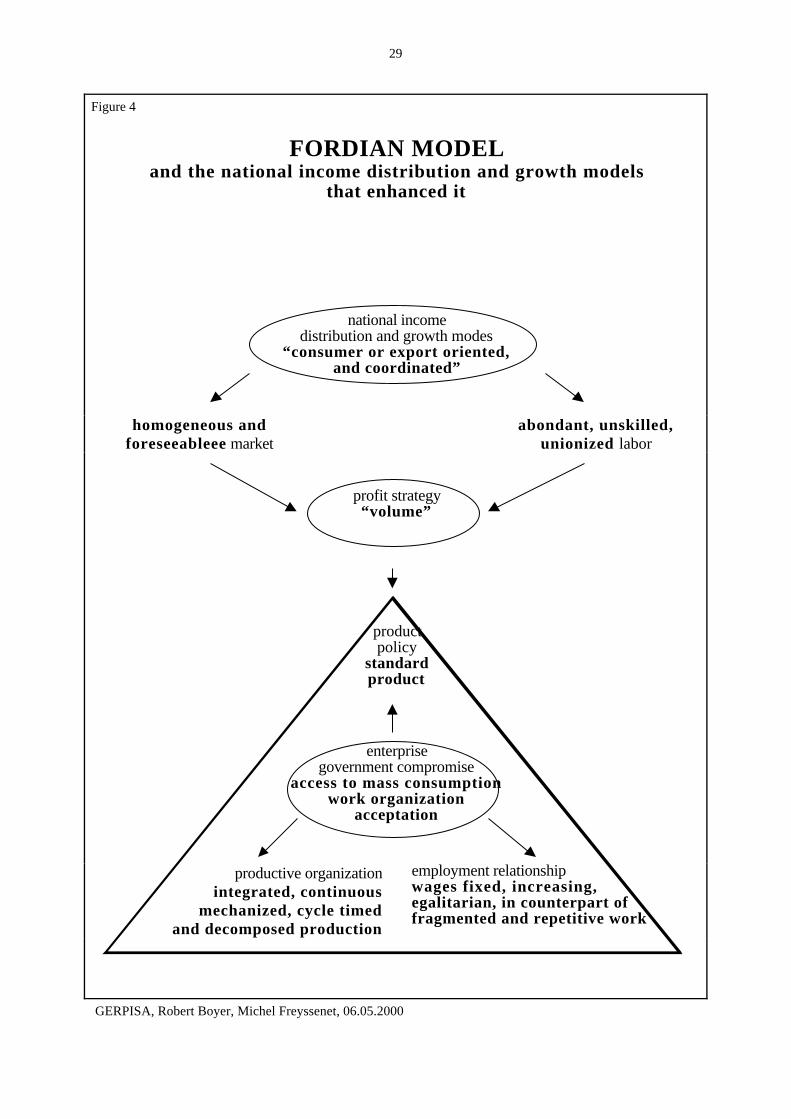

The "volume" strategy and the Fordianmodel

The "volume" strategy consists ofdistributing costs among the largest numberpossible of vehicles, costs that are notimmediately adjustable to demand. The bestimplementation of this strategy is the massiveproduction of a unique model for as long aspossible. It demands a growing andhomogeneous market that is satisfied with oneor a few standardized models, and also requiresa sufficient quantity of workforce that acceptsan undifferentiated production and work.

This explains why the "volume" strategy"was only temporarily viable during very shortphases of mass automobile market take-offs,such as Henry Ford's Model T andVolkswagen's Beetle. Only egalitarian regimesbased on a centralized and/or administratedeconomic system could, in theory, guarantee"volume" strategy conditions over the longterm. However, the latter generally do notprovide the means to efficiently implementthis. An example is the Avtovaz experience inthe case of the Soviet economy. Irregularity ofsupply and the impossibility of makinginvestment, salary, and workforce volumedecisions did not allow Avtovaz to obtain thesame results as Fiat's Mirafiori plant for itsTogliattigrad plant, even though the formerwas its direct transposition. Indeed, a technicaltool only is efficient when the employmentrelations are coherent with it.

Hence, the "volume" strategy requires thefollowing in order to be implemented:conceiving a product that responds to basicdemands for individual transportation of thepopulation at large, a stabilized productive

13

organization allowing for standardizedproduction in regularly increased andcontinuous flow, and sufficiently attractiveemployment relationships so the firm maybenefit from an increasing volume of workers,but sufficiently constraining so that they acceptrepeating similar tasks (see figure 4, appendix).

The "Fordian" model has responded tothese demands with a product policy consistingin offering a unique, "integrated", reliable, andinexpensive car model to the population atlarge or to an average clientele within eachlarge segment of the market; a standardized,continuous, and strongly integrated productiveorganization based on mechanizeddisplacement of the product, task breakdowninto elementary operations redistributedamong work stations with the sole purpose ofsaturating cycle time periods; and employmentrelationships guaranteeing workers lackingrequired skills a fixed salary that is notdependent on profits, and whose buying powerregularly progresses. Volkswagen was able todevelop the most robust Fordian "enterprisegovernment compromise" and proved to beprofitable for almost twenty-five years.

The "Fordian" model experienced a crisislong before the market become a renewedmarket in countries where it had been applied.Indeed, national differentiation in revenues andautomobile demand rapidly reduced theviability of a "volume" strategy and "enterprisegovernment compromise" based on rigidorganization and uniform and high wages.

The "volume and diversity" strategy and the"Sloanian" model

This strategy combines two profit sources,volume and diversity, have long beenconsidered as incompatible. In the 1920s and1930s, General Motors found the solution toovercoming this contradiction by havingdifferent models share a maximum number ofinvisible parts among them, thus reducingdiversity to one only perceptible by thecustomer, in other words, body, sadlery andequipment.

This strategy is only possible if "surface"

diversity is commercially acceptable. For this,demand must be moderately differentiatedfrom an economic, social, and geographicstandpoint. This can only be found incountries where national income distribution isnationally coordinated and moderatlyhierarchized. The "volume and diversity"strategy also implies having an abundantworkforce at one's disposal that acceptspolyvalence in order to face variations andvariety in production. These conditions werefully satisfied in a certain number ofindustrialized countries beginning in the 1940sin the United States and Sweden, the 1950s inWest Germany, France, and Italy, the 1960s inJapan and Spain, and the secont part of 1980sin South Korea. Since the 1980s, generallyspeaking, these conditions have become lesssatisfied. The introduction of more"competitive" income distribution, notably inthe private sector whereas public sector wagesremain coordinated and moderatelyhierarchized, contributed to the emergence of amore dispersed second automobile market(four-wheel drive, pick-ups, recreationalvehicles, monospaces, etc.) for which the"volume and diversity" strategy is lesspertinent.

The product policy of a "volume anddiversity" strategy must therefore consist in afinely hierarchized range covering theprinciple segments of the market, andgenerally excluding both very low and highquality models as well as "niches" vehiclescorresponding to only a small number ofcustomers. Productive organization must allowfor diversity and variations in demand amongvehicles, versions, and options, so that bothover and under capacities will be avoided, andso that complexity in supply, conception,fabrication, and distribution be fullycontrolled. Insofar as employmentrelationships are concerned, they must fulfilltwo requirements: attract an abundant numberof workers while valorizing polyvalence, andremain coherent within a moderatelyhierarchized national income distributionmode.

The "Sloanian" model (named after Alfred

14

Sloan, under whose presidency this model wastheorized and constructed at General Motors)is the model that implemented the "volume anddiversity" strategy. It relies on an "enterprisegovernment compromise" essentiallyestablished between managers and one orseveral powerful and professionalized unions.It thus takes on the form of a "socialcompromise" wherein accepting workorganization and promoting social peace iscompensated by programmed growth inworker's buying power, promotions in theworkplace, and the expansion of both socialprotection and union rights (see figure 5,appendix). The "Sloanian" product policy ismulti-brand, offering parallel ranges whosemodels of same market segment share the sameplatform while offering a number of versionsand options. Productive organization ischaracterized by the centralization of strategicchoices and the decentralization of theirimplementation within divisions; relying onsubsidiaries or sub-contractors for numerouscomponents so as to displace a part of diversityto them and to benefit lower prices due to theireconomies of scale obtained thanks the ordersfrom other clients; machine polyvalence(multi-specialized) and mechanical assemblylines with buffers to saturate the productiontool despite vehicle variety. Employmentrelationships consist of applying the "enterprisegovernment compromise" under the union'scontrol, and in the name of polyvalent workerspaid in function of job evaluation of workstations they successively have. (see figure 5,appendix)

Product policy and productive organizationwere clearly defined as of the 1930s byGeneral Motors. But the "Sloanian" model wasonly genuinely formed in the 1940s. To obtainthe synchronization of the "volume anddiversity" strategy and sloanian employmentrelationships with the American "nationalincome distribution and growth mode", onehad to await that income distribution becomescoordinated and moderatly hierarchized. Thissynchronization strarted spectacularly by theagreement concluded at General Motors after a113-day strike in 1946, and then served as a

matrix for wage policy nationwide. It was at theorigin of the "abundant years" period, latercalled the "Fordist" period, an erroneouslabeling and quite unjust for Sloan. Ford andChrysler also adhered to the Sloanian model.The progressive adoption by mostindustrialized countries in the 1950s and 1960sof the same income distribution as that of theUnited States, even if the origin of gains wasdifferent, led several carmakers to try to adopt"Sloanian" model: Peugeot, Renault and Simcain France, Fiat in Italy, Nissan in Japan. A "onebest way" seemed to have been found, andduring the 1960s many experts announced thenecessary convergence of all productivesystems towards this productive model.

The "Sloanian" model began to encountersome difficulties at the end of the 1960s. As weall know, it can only last if its profit strategycan be continued and all concluding partiesrespect the "enterprise governmentcompromise". While being presented as the"machine" generating the society of abundanceand leisure, productivity gains it had generatedbegan to decline in the United States followingstagnation in economies of scale. TheAmerican market began a renewal market andexportations and commonalization wereunsuffisant to growth the volume. In Franceand Italy, the difficulties of "Sloanian" modelcame from the rejection by youngergenerations of "enterprise governmentcompromise" These difficulties could havebeen surmounted if monetary policy enactedby the United States to readjust theirprogressively degrading trade balance had not,through a series of domino effects, led to theoil crisis and interruption of world growthrates. Countries whose "National incomedistribution and growth modes" were« consumer oriented and coordinated » weredestabilized by countries whose modes were"exporting oriented and coordinated". Fromthis moment, the "Sloanian" modelencountered in these latter countries betterconditions for long life due to economies ofscale brought on by exportation and to incomedistribution based on exterior competitiveness.From 1974 on, Volkswagen successfully

15

applied the "Sloanian" model through a policyof growth outside of the European arena, thesystematic commonalization of platforms forpurchased brand car models, and exportation.

The "quality" strategy, seeking a model forlong-lasting profitability

The term "quality" signifies not onlyreliability and the vehicle's performance level,but also - and perhaps even moreso - the socialdistinction of a particular style, the use ofcertain materials, refined finishing touches, ahigh price and the prestige of a brand thatreflects the aspirations of wealthy anddistinguished customers ready to pay the price.This strategy leads firms adopting it tospecialize in luxury range products, or morerecently, to respond to the superior portion ofeach market's segment. This is why firms areoften called "specialists" as opposed to"generalist" firms that produce for the largemass of consumers. Profits are essentiallygenerated from price margins authorized bythe product and executive range orientedcustomers.

The "quality" strategy has the largest degreeof pertinence in both space and time. Only afew societies lack a wealthy populationcategory ready to pay a high price so as topossess products that represent their high-ranking economic and social position. This iswhy the luxury and executive range marketwas first and foremost an international one, andstill remains so today. But the « specializedexpoter and coordinated mode » is in favour to« quality » strategy.

For the period more particularly studied byGERPISA, that is to say, particularly since the1960s, no firm having adopted the "quality"strategy (BMW, Mercedes, Saab, and Volvo)experienced a break-even point constantlyabove added value. Though their profitstrategy was pertinent, their "enterprisegovernment compromise" was not sufficientlyrobust - despite a socially favorableenvironment - to overcome the labor crisis allthese firms encountered, not only in the 1960slike so many other carmakers, but also in the

1970s and 1980s. Nor did it allow them tocontrol supplier costs. All these firmsattempted to apply "socio-technical" solutionsto the labor crisis, for example, byconsiderably enlarging cycle times,introducing modular work, and/orsystematically improving work stationergonomics. In addition, the image of qualityitself, essential to maintain for obviouscommercial reasons, could be reinforced bypublicity concerning new production methods.They were presented more dignified than"mass production" methods for the demandingcustomer who wanted "his/her car" to be theobject of special attention. Volvo went thefurthest along the path of "work reform" byradically splitting from the assembly line,replacing it with assembling in fixed parallelstations, notably in its new Uddevalla plant. Butboth at Volvo and other firms, employmentrelationships and product policy were notcoherently conceived of in relation to the newproductive organization so as to generate asmuch benefit as possible in terms ofpersonalization of response to demand (be it inthe realm of delays, costs, productimprovement and adaptation, and service).

The derivation of costs, unfavorableexchange rates, unemployment growth, andprice wars brought about a limitation andfinally the abandon of this chosen path.However, a new "enterprise governmentcompromise" concerning new product policy,productive organization, and employmentrelationships was not established. GeneralMotor's and Ford's take over of Saab andVolvo, respectively, most probably hails aradical trajectory change for both Swedishcarmakers.

The "permanent cost reductions at aconstant volume" strategy and the "Toyotan"model

With this strategy, cost reductions at aconstant volume occurs continuously and in allcircumstances. Other profit sources areadditionally exploited only if they do notinhibit the main priority, that of reducing costsat a constant volume. The goal is to be

16

prepared for any eventuality so as to remainprofitable since nothing is really ever sure.This consists in reducing cost prices bothinternally and vis-a-vis suppliers throughcontinuous savings.

This has been Toyota's strategy since the1950s. It is particularly adapted to a "nationalincome distribution and growth mode" basedon the exportation of competitive productsthrough pricing and to an income distributionmode determined by exterior competitiveness(the « price-exporter and coordinated mode »).

To be implemented, it requires a productpolicy that chooses to ignore innovativemodels because of their high financial risk. Italso requires a constantly evolving productiveorganization that is not based on technologicaltake-offs so as to eliminate "waste" of all sorts,as well as employment relationships thattolerate continued reduction in the number ofworkers at constant volume.

The Toyotan model answers to thesedemands with a product policy that aims atsatisfying average demand in each largesegment of the market. This is accomplishedby offering models whose commercialcharacteristics are well grounded, have littleexcess in diversity (such as options), and areplanified quantitatively so as to grow regularly.The method consists in applying a "just-in-time" productive organization both internallyand with suppliers, the goal being to revealproblems inhibiting a continuous and regularflow at the origin of waste in time,workmanship, materials, energy, tools, andspace. In addition, employment relationshipsmotivate workers to reduce standard time spentwithin each workstation by making wages andpromotion dependent on the accomplishmentof cost reduction management goals.

Managers, workers, and suppliers essentiallyagree upon the "enterprise governmentcompromise". It is based on large-scaleworkers and suppliers implication. In exchangeworkers obtain job security, wages increase,and promotions, and suppliers guarantees for avolume of production and profits (see figure 6,appendix).

Up to the 1990s, the Toyotan model

conferred an exceptional degree of expansionand profitability upon the firm. It thusappeared to be the "optimal" model since itguaranteed for a firm's competitiveness, workerparticipation and job security, as well asgeneral satisfaction on the part of all buyers.However, competitiveness is not guaranteed inall circumstances. When a demand forinnovative models develops, the firmincarnating the Toyotan model can notrespond. It has no other choice but to copyand improve upon innovative models alreadyon the market as quickly as possible. That iswhy a firm like Honda was able to develop andbecome profitable alongside Toyota. TheToyotan model is shaken by brutal changes, bethey in exchange rates or currency paritylevels, that can strike down with one blow allthe patient and continual efforts demanded ofboth workers and suppliers. Pushed to its limitsin a tense labor market coupled with explosivedemand, it is then criticized by workers, as wasthe case in Toyota. At the beginning of the1990s, Toyota had to substantially change itsmodel to the point where, in all exactness, itwill soon have to be called by another nameonce a new "enterprise governmentcompromise" has been elaborated.

The "innovation and flexibility" strategyand the Hondian model

This strategy consists of designingconceptually innovative models that respond toemerging expectations and demands, producethem massively and immediately if commandsconfirm this anticipation, so as to make a profitfrom the risk taken before competitors thenchoose to invest in the newly created marketsegment; or, on the other hand, to abandon theinnovative model(s) rapidly and at the leastcost in the event of commercial failure. Thiswas Honda's strategy from the moment itentered the automobile industry. It also hasbecome Chrysler's strategy that, since the endof the 1980s, has reunited with its formerconceptually innovative model policy. Last butnot least, it has been Renault's strategy since thebeginning of the 1990s.

This strategy presupposes "National income

17

distribution and growth modes" where by theneeds and lifestyles of social categories evolveperiodically or where economically andsocially distinctive population categoriesemerge. This is particularly the case for"National income distribution and growthmodes" wherein income distribution is more"competitive". Different social or professionalcategories of the population are periodicallyprivileged by this form of distribution and seekto translate their new and favorable economicposition through an automobile demand thatdistinguishes them from others and/or respondsto their very specific demands.

However, the history of the automobileindustry is made up of firms pursuing the"innovation and flexibility" strategy that havefailed whereas demand for innovative cars stillremained present due to adequate incomedistribution mode. Indeed the risks of thisstrategy are apparent. Among them: aninnovation that does not (or poorly) find itspublic, over or underestimation of thedemand's latent volume, loss of capacity tosuccessfully innovate over the long term,refusal by investors, the temptation to follow inthe footsteps of the "big generalist firms"following an initial success. To beimplemented, the "innovation and flexibility"strategy requires that the firm takes necessaryfinancial risks and be capable of regularlyoffering commercially pertinent innovativevehicles. It requires a very reactive productiveorganization, be it in the realm of conception,fabrication, and/or distribution, so as torespond to and saturate demand beforecompetition copies the model. The productiveorganization must likewise be capable ofwithdrawing the model rapidly and at thelowest cost if it does not find a public. It mustestablish employment relationships thatencourage useful innovation and the capacityto completely change production projects at alllevels of the firm.

Today, of the three carmakers pursuing thisstrategy, only Honda has genuinelyconstructed a productive model that respondsto all these demands. It did so even though itwas still producing motorcycles, then

consolidated and completed it when it becamea carmaker. The model that one may now call"Hondian" answers to the "innovation andflexibility" strategy demands through aconceptually innovative product policy, eachmodel having their own platform, yet formingan entirely coherent technical and stylisticstructure. It is also based on productiveorganization characterized by a low integrationrate to limit negative financial impact in theevent of failure, and inversely, to respond moreeasily to success. In addition, the productionstructure is easily convertible without having torely on large-scale engineering efforts. Thismeans low automation level, and innovatorsallowed to express themselves in conception, tocreate their teams and accomplish their chosenprojects. Employment relationships favor theemergence within the firm of technically andcommercially competent innovators found atall levels thanks to recruitment, salary, andpromotion policies that value expertise andindividual initiative more than a diploma, age,or seniority, and in same way more thanhierarchical responsibilities. Last but not least,the firm boasts good working conditions,offering the lowest annual, weekly, and dailywork periods of the sector.

The "enterprise government compromise"that founded the Hondian model was agreedupon by managers (legitimized by their ownpersonal innovative qualities and/or theircapacity to value those of others for the benefitof the firm and its employees) and employeesthemselves who where called upon to expresstheir personal ideas and experiences regardingthe product and its process. It thereforeexcludes banks, shareholders, and supplierswho generally refuse the indispensablenecessity of taking risks. The firm is self-financed and has not established a singleassociation with suppliers (see figure 7,appendix).

However, Honda has also experienceddifficulties with the "speculative bubble". Itbelieved that demands within the context oflong lasting growth were for increasinglyluxurious and executive range vehicles andsports cars, and thus completely neglected the

18

emerging demand for monospaces andrecreational vehicles. Only recently has it(successfully) rectified this approach inproduct policy by launching the muchappreciated leisure vehicles.

Again the world changes the machine:new income growth and distribution modes,new confrontations between countries, andthe recomposition of the world

How can the preceeding analysis approachallow phenomena observed during the 1990sto be interpreted, such as the decrease incompetitiveness gaps between carmakers,turnaround of European and American firms,difficulties encountered by certain Japanesefirms, the new globalization wave, theemergence of newly industrialized countriesaccompanied by implantations of newcarmakers, regional or worldwide organizationof firms, mergers-acquisitions-alliances, theexplosion in demand for recreational, semi-utilitarian and "niches" vehicles, the newimportance of shareholders, etc..

The two world confrontations and theiroutcomes

Indeed, the beginning of the 1990srepresents a major turning point, notablyconcerning the consequences emanating froma double confrontation: one between capitalistand communist countries, and the otherbetween countries consumer-oriented,protected and having a nationally coordinatedand moderately hierarchized incomedistribution based on internal productivitygains, and countries exporting-oriented,protected, also having a nationally coordinatedand moderately hierarchized incomedistribution, but based on exteriorcompetitiveness.

As a surprise to many, the firstconfrontation led to the implosion of the vastmajority of communist countries as well as theaccess to new areas for capitalist firms,particularly in the automobile industry. Theconfrontation with the "Socialist camp" hadlargely contributed to the emergence of newly

industrialized countries, particularly in Asia,with the design of protecting them fromcoming under Communist regime. Notablythanks to access to the United States market,these countries were able to adopt anindustrialization way based on the exportationof manufactured products, first at low valueadded cost, and after with higher value added,all the while protecting their domestic market.

The second confrontation did not culminatein the convergence of all countries towards the"winner" income growth and distribution mode,that is "exporting oriented, protected andcoordinated distribution in function of externalcompetitiveness gains" mode. During theeigties, the countries applying it wereconsidered as a model (the Japanese model, theGerman model, the Swedish model). ThoughFrance and Italy moved closer to this model,the United States chose another path. Theyconserved their "consumer-oriented" growth,but adopted a new national income distributionbased on "competition". Revenue structure anddemand were modified as well as employmentconditions and mobilizable labor. Massiveinjection of public financing during the 1980s,the oil "counter-shock", changes in theequivalence of monetary exchange , newfacilities to create a firm, adjustingemployment and wages and mobilizing capital,all these factors contributed to a growth cyclethat, since the 1990s, has made the UnitedStates the country upon which the rest of theworld's growth depends. In addition, theliberalization of capital circulation andinvestment has significantly enhanced theposition of one actor in the firm, theshareholder. Beginning in the United Statesthen spreading to other countries, shareholdershave been demanding increasing amounts ofreturn on their invested capital.

From that point on, countries with anationally coordinated and moderatelyhierarchized income distribution weredestabilized. This first occurred in Japan,Germany and Sweden, but also in France andItaly, the latters having extroverted themselvessomewhat, all the while limiting deregulation ofwages. European countries and Japan had

19

difficulty reacting, the former due to theirrestrictive budgetary policy, the latter due tofinancial uncertainty increasingly slumpingdomestic demand. European countries alwayshad - and still have - one alternative; theregionalization of growth and exchange, inother words, the European Union, whosegrowth can still be self-centered and whoseincome distribution can be regionallycoordinated while not being too dissimilar.Japan's historical and political isolation withinits own region deprives it of this perspective,unless the crisis of emerging Asian countries,and pressure from the United States to furtheropen up their borders (the Communist threat -or supposed - having disappeared) succeed inconvincing Japan's neighbors to regionallygroup together with Japan.

Effects of the worldwide doubleconfrontation on the automobile industry

The change in "National incomedistribution and growth modes" in certaincountries belonging to the Triad, theintroduction of some limited "competitive"modalities in wage and revenue formation inothers, the liberalization of capital circulation,the emergence of new industrialized countriesand their ensuing crisis, the transition towards acapitalist economy by former Communist-regime countries in Eastern Europe and Asia,contradictory trends in the world'srecomposition between globalization andregionalization, and the reaffirmation of acertain number of very important nations, allthese factors have had numerous effects on theworldwide automobile industry:Ø a change in power relations between

carmakers as well as between actors withinthe firm;

Ø strong growth followed by a drop inautomobile demand in emerging or formerCommunist countries;

Ø the creation of a second automobilemarket, that of semi-utilitarian, recreational,and "niches" vehicles corresponding to newcategories of the population engenderedby their more or less fortunate income in

the competition for share of internalproductivity gains or externalcompetitiveness;

Ø renewed heterogenization of demandamong the world's regions or even amongcountries in function of specific trajectoriesof different areas.

Changes in power relations betweencarmakers as well as between actors within thefirm

This initial effect was observed in thedifficulties experienced by Japanese, Koreanand East-european carmakers during the1990s, while simultaneously witnessing therecovery of American and Europeancarmakers. Tensions provoked by thespeculative bubble, a slump in the Japanesedomestic market, the yen's valuation, effectsbrought about by American and Europeanrestructuring on Japanese competitiveness, allthese factors revealed the limits of Japanesecarmakers and even the high degree offragility among some of them. Notably, Nissan,Mazda, and Mitsubishi, firms that had notconstructed a solid "enterprise governmentcompromise" and had gone into considerabledebt, could not resist. Only Toyota and Honda,which had been self-financing theirdevelopment for quite some time inconformity with their own "profit strategy",could not only preserve their independence butalso pursue their growth. Nevertheless they didnot entirely preserve its dominant position, inrelation to American and European carmakers.Once again, it was the "world" that changed the"machine" by modifying conditions andpossibilities for the implementation of profitstrategies and productive models.

This reversal of the world conditions wasseized upon by a certain number of Europeanand American firms that perceived themselvesas being too regionalized. They consideredtheir globalization as a necessity for theirprofitability in the future. They took control ofJapanese, Korean or East-european firms: Fordof Mazda, Renault of Nissan, Dacia andSamsung, Daimler-Chrysler of Mitsubishi.Many American and European automobile

20

firms competed to take control of Daewoo andto form an alliance with Hyundaï, and may beAvtovaz.

Among the various measures employed bycertain American, European firms, and nowJapanese firms, to lower their break-even point,to improve control variety, and to adjust moreeasely their production capacity tocircumstantial variations in demand, there isone that stands out due both to its long termand worldwide ramifications: the outsourcingof a number of activities in conception andfabrication to (already or recent) independentfirst-rank suppliers. These suppliers have infact been put in a position to structure andmanage automobile activity in their area ofcompetence. They have acquired greatimportance, and only the future will tell ifcarmakers will be able to control them.

The liberalization of capital circulation,designed to facilitate new investment, has alsomodified power relations between the firm'sactors. It has allowed shareholders to havemobile capital to demand improved returns.They push managers to reorientate the firmtowards potentially more profitable activity,notably services linked to the automobile. Anew player in the construction of "enterprisegovernment compromise" obligates a changein the productive model. However, it isimportant to recall that many carmakers havestrived to maintain their financialindependence, notably the three mostprofitable firms: Toyota, Honda, andVolkswagen.

Just what is emerging?The development of automobile markets in

emerging countries and in former Communistcountries has encouraged the quasi-totality ofcarmakers to go there, searching a volumegrowth that they can no longer obtain from theTriad countries. They thought that eventualupsets in the development of some of thesecountries or in transition for the others wouldnot affect the irreversible trend towards growth.Long before the Asian crisis and ensuingshock waves, GERPISA analytical approach

had led to express some doubts about thesepredictions for several reasons. The so-called"emerging countries" owed their growth to theexportation of manufactured products at agrowing added value to those industrializedcountries who did not oppose this type ofgrowth, for geo-political, economic, or socialreasons. However, since the disappearance ofthe "Socialist camp" and success in exporting athigher value added by these countries, onecould observe increasing pressure placed onthem, to open their markets. Hence, theirgrowth rate was not guaranteed to evolve at thesame rhythm. The 1997 financial crisis alsorevealed that development in these countrieshad relied on debt, and that local deficient andblind international institutions had allowed thisto reach an intolerable level, at least from along-term perspective. Did this Asian crisisprovoke the painful but beneficial rectificationallowing emerging countries to start again on amore healthy and solid basis? This is possiblebut not entirely certain.

These countries will now have less controlof their development since American andEuropean firms have taken over certainimportant local firms that have gone bankrupt,notably in South Korea. They will also have torely more on domestic consumption. Yet (withthe exception of South Korea), nationalincome distribution remains highly unequal inthis area since the 1980s, inequalities evenincreasing considerably since the crisis. Theconstitution or consolidation of a middle classsusceptible to generating mass automobiledemand is constantly put off by periodicalfinancial or political crises. In addition, there islittle chance that these countries will adopt anationally coordinated and moderatelyhierarchized distribution mode in the nearfuture. Automobile demand will certainlydevelop, however it will revolve more arounddemand for luxurious and executive-range carsand light trucks, and extremely low pricedvehicles that remain to be designed, rather thandemand for wisely hierarchized sedans.

Insofar as former Communist countries areconcerned - beginning with the foremostamong them, i.e. Russia - it was obvious that in

21

the absence of institutions allowing for amarket to function, these countries were notable to make a rapid transition to capitalism,one that is profitable to firms offeringequipment products to the population at large,such as the automobile.

Anticipation made by firms for the futureof these countries were probably bothquantitatively and qualitatively erroneous. Asof now, capacities installed seem too extensivein relation to mid-term demand previsionswithin this new context. Fiat is certainly thecarmaker that has the most harshlyexperienced the turn around of markets inemerging countries, due to its massive financialand human resource investment there, to thedetriment of the European market. Recordedlosses most probably explain its alliance withGeneral Motors.

The two automobile marketsSince the mid 1980s in the United States

and the 1990s in Japan and Europe, a demandfor conceptually innovative vehicles from apractical and symbolic standpoint has emerged,especially in industrialized countries: lighttrucks, sports utilitarian vehicles, monospaces,recreational vehicles, urban four-wheel drives,"niches" cars, mini-cars, etc. Today thisdemand represents between a quarter to a halfof the automobile market, according to thecountry. Its concomitance with thederegulation of revenue formation is striking.Thus, it appears that the second marketemanates from new categories of thepopulation that express through automobiledemand their own economic and socialtrajectory. This radical change in the marketstructure has had several consequences.

It has rendered the "innovation andflexibility" strategy (adopted by Chrysler andRenault, following Honda) much moreprofitable than before. It has allowed Ford andGeneral Motors, imitating Chrysler, toencounter less competition from Japanesecarmakers and their transplants, and togenerate substantial profits. On the other hand,it has created harsh mid-term dilemmas thatneed solving.

If the second automobile market isconsolidated and even extends from a volumestandpoint, it will destabilize carmakerspursuing a "volume and diversity" and"reduction of costs at a constant volume"strategies. Indeed, it requires that firmsregularly offer innovative vehicles to new andrenewed population categories. However, as wehave seen, the risk involved with conceptuallyinnovative vehicles is in contradicts thesestrategies. The firms that implement them willbe obliged to imitate the innovative car models.But will they obtain the required level ofvolume to make profit? Indeed the "innovativeand flexible" firms will always know how toquickly saturate new demand once the markethas validated proposed innovative models.Likewise, the "innovative" vehicle supposes thatit differs from classical models, and not onlyon the surface. If the market becomes moreand more balkanized, and due to a nationalincome distribution more "competitive", thecommonalization of classic and innovative carplatforms will be less acceptable to thecustomers.