thecoldchain, acruciallinktotrade … ter16 thecoldchain, acruciallinktotrade andfoodsecurity...

TRANSCRIPT

CHAPTER 16

THE COLD CHAIN,

A CRUCIAL LINK TO TRADE

AND FOOD SECURITYGérald Cavalier

Cemafroid-Tecnea, FranceSoumia El Hadji

Veterinary Doctor, ONSSA, MoroccoIbrahim Sani Özdemir

Tübitak MRC Food Institute, Turkey

Mediterranean populations have developed the first equipment of the cold chain

since antiquity. The remains of coolers used in Roman times reveal their remarkable

mastery in maintaining the cold chain, unequalled for centuries until the arrival of

industrial refrigeration in the mid nineteenth century. However, it was not until a

century later that modern tools as we know them today appeared. The first ventilated

reefer truck making use of an independent group for vapour compression appeared

in 1937 in the United States, and only in 1947 in Europe. The use of existing current

insulators was only widespread and industrialised in the 1970’s, paving the way for

large-scale development of cold chain quality (Cavalier, 2011).

The Mediterranean is the cradle of the cold chain, and with Southern Europe, it has

remained a centre of excellence in this field. With the development of trade in the

region and the growing expectations of the populations in terms of quality and food

safety, the area needs to be equipped with a quality temperature-controlled logistics

service (allowing each product to be stored at the right temperature throughout its

lifespan) worthy of its ambitions.

The current situation does not meet needs and expectations. However, even if some

links in the cold chain are still lacking, both in terms of equipment, facilities and

service, the situation is progressing rapidly, and projects are being developed. A

network of players in the cold chain is being formed around the Mediterranean and

governments have undertaken, and indeed have in part already achieved, the creation

of a suitable regulatory and normative framework.

The growing needs of the cold chainin the Mediterranean

The cold chain is necessary to ensure food safety for Mediterranean populations,

but also to allow for the development of food industries and trade, as well as devel-

opments in tourism.

The development of trade and industrial needs

Trade is developing rapidly around the Mediterranean and food exchanges between

the European Union and Mediterranean countries are expected to double in

number between 2000 and 2025 (De Rijk et al., 2008). The trade of fruits and

vegetables and processed food is increasing rapidly. Tunisia or Morocco export

dates or citrus and import potatoes or bananas. The share of fishery in these trade

exchanges is also significant. It represents more than 50% of food temperature

controlled commodities exported by Tunisia. This also applies to pharmaceutical

products which are often sensitive to changes in temperature. Whether in the case

of fresh products, to be stored between + 2oC and + 8oC, such as vaccines, insulins

or anticancer drugs, or the range of products to be maintained at ambient tem-

peratures between + 15oC and + 25oC, as well as frozen products stored below – 20o

C, and all the other ranges need to be maintained at specific temperatures. Their

production, particularly that of generic medicines, has developed all around the

Mediterranean, and their trade has not only increased enormously, but they have

also completely changed over the last years. One should not forget the importance

of veterinary vaccines for the production and for the sanitary quality of meat.

Veterinary medicine needs the cold chain, and both the quality of meat and the

reduction of production losses depend on good quality veterinary medicine. For

instance, poultry vaccination campaigns against the H5N1 virus have undoubtedly

helped prevent a global pandemic and a high mortality rate. This is also the case

of many other animal vaccinations.

Exchange agreements with the European Union require the application of Euro-

pean safety regulations, in particular, requirements of the food hygiene package

which among other things impose compliance with product temperatures

throughout the cold chain. Mediterranean countries must therefore set up suc-

cessful cold chain logistics in order to conquer European export markets, both

for food products and pharmaceutical products that they are producing in greater

amounts. It is to be noted that in Southern and Eastern Mediterranean countries

(SEMCs), it is those firms or groups of players essentially focused on lucrative

but demanding markets that have established the main elements of cold chain

logistics. On the other hand, logistics are often less efficient when it comes to

domestic markets, deemed “captive”, but may be tempted to prefer imported

products due to their superior image, as is often the case of middle or high income

consumers.

304 MEDITERRA 2014

Box 1: The cold chain in Turkey

The Turkish economy has experienced considerable growth rates over the pastdecade, which has had a major impact on the purchasing power and economicactivity in the country. In the food and beverage sector, both production and con-sumption rates have increased significantly during the same period. Similarly, therewas a rise in the consumption of frozen and chilled foodstuffs. However, domesticconsumption was limited due to the high price of frozen foods which remains unaf-fordable for a large number of Turks, and an overall reluctance to consume frozenand chilled prepared foods. Nevertheless, in recent years, consumer behaviour andawareness on prepared foods have changed due to increased income levels, morewomen joining the work force and more time spent on leisure activities than home-cooking. Similar to earlier observations made in other European countries, thenumber of fast-food restaurants and pastry shops has increased dramatically duringthe last decade, along with changing consumer habits. Another noticeable changeseen during the last two decades is the proliferation of modern retail outlets chainsthroughout the country. They are considered as the driving force leading to theimplementation of modern domestic cold chain systems.

Trends in the consumption of frozen and chilled food

The improvements in cold chain both in terms of quality and cost have also led tothe emergence of various frozen and chilled foods in the retail market where thereis a clear tendency to choose chilled ready-to-eat traditional foods (i.e. kebab, meze,dolma, etc.).

It should be noted that the above-mentioned trends in frozen and chilled foodconsumption are not identical in all regions of the country. In highly populatedcities like Istanbul, Ankara and Izmir, consumers are more likely to eat frozen andchilled foods and more reluctant to prepare meals because more time is spent atwork and in public transportation. Heavily dependant on cold chain systems, theexpansion of the catering sector is primarily due to the increase in industrial activitywhere catering services are needed.

All these economic and social changes have had a significant impact on the coldchain system in Turkey. The most important impact was the one on the qualitystandards of logistic companies specialised in the cold chain. In the last decade coldchain logistic companies have modernised their structures and increased theircapacity in order to meet the domestic demand for goods transported via reliablecold chains. As a result, the number of reefer trucks and large cold storage hubs hasincreased.

Progress to be made

As for the export market, modern cold chain systems were adopted much earlier.Turkey is a major fruit and vegetable producing country where traditional produceis foremost among frozen food products. Despite the striking change observed incold chain quality throughout the past decade, there is still a lot of progress to bemade in the domestic market where transport of fresh goods is mainly done withouttemperature control. Consequently, significant amounts of fruits and vegetables arelost due to inadequate temperature control during transport and storage while theremaining fresh produce reaching market shelves is of poor organoleptic quality.The lack of a reliable cold chain for milk collection in remote areas is still one ofthe major problems of the Turkish food industry. However, in recent years, someimprovements have been made thanks to government subsidies allocated to milkproducers applying cold chain practices. The logistics of fishery products is anotherproblematic issue of the Turkish food industry in terms of cold chain

305The cold chain, a crucial link to trade and food security

practices. Mainly artisanal fisheries suffer from the lack of proper refrigeration equip-ment due to the fishermen’s lack of knowledge about the benefits of cold chainsystem and existing infrastructure. In contrast, industrial fisheries fully enjoy thelatest technology in cold chain systems.

Perspectives and challenges in the years to come

Further improvements in the use of the cold chain in the various sectors of theTurkish food industry are expected in the coming years. One of the most importantdrivers that will shape the Turkish cold chain is undoubtedly the prospect of joiningthe European Union. The adoption of the ATP agreement by Turkey in 2012 isanother important step that will gradually lead to a better cold chain. Among thepriorities of the Ministry of Food and Agriculture, developments in the cold chainfor fresh products are expected in the coming years. Comparable advances are alsoplanned for fishery and dairy cold chain systems. All these improvements will requireconsiderable public and private investment in the construction of cold chain infra-structure. Meanwhile, a major growth is also expected in the number and quality ofservices provided by companies in the field of cold chain logistics.

Ibrahim Sani Özdemir, Ph.D. Chief senior scientist, Food Institute, Tübitak MRC (Turkey).

Reduction of losses

The establishement of a quality cold chain also provides opportunities to reduce

food losses. Such a reduction is all the more necessary since the needs of populations

and industries will continue to grow in the future. Globally, today, the losses due to

the lack of a cold chain amount to more than 30% and can even reach 40% in some

developing countries, especially for fruit and vegetables. Yet, these losses represent

a major source of savings and food to feed 9 billion people in 2050 and develop

food industries and exchanges.

If the report of International Institute of Refrigeration (IIR, 2009) on cold and

hunger in the world, published in 2009, unfortunately continues to be topical, it has

contributed to raising political awareness. The French government has prioritised

the reduction of food losses, and for several years, southern European countries have

been requesting, within the framework of the Agreement on the International Car-

riage of Perishable Foodstuffs and on the Special Equipment to be used for such

Carriage (ATP)1, an extension of the regulations on the transport of perishable food-

stuffs to include the transport of fruits and vegetables. Their demand is also

expanding to the enforcement of the regulations not only to international transport

but also to national transport (a proposal has been submitted by France in this

direction since the drafting of this chapter). At the same time, North African and

Middle-Eastern countries are joining the ATP and implementing national regulations

to develop a cold chain worthy of the name.

For the first time, the economic motivation for the regulation of the cold chain

could be even stronger than the sanitary motivation. Even if the cost may be impor-

tant, the savings achieved would largely compensate for the investment.

1 - United Nations Economic Commission for Europe Agreement (CEEONU or UNECE) signed in Geneva in 1970.

306 MEDITERRA 2014

Evolution of consumption

Strong demographic growth and urban development accompany changes in life-

style, consumption and distribution. Local distribution networks are no longer suf-

ficient to feed cities, and short lifespan products are not appropriate to urban

consumption. At the same time, supermarkets are developing in new areas. Their

supply flow requires products with a longer lifespan and temperature-controlled

logistics. No cold chain, no supermarkets.

Health of populations and tourists

All the studies carried out in countries that have set up a quality cold chain show a

significant improvement in the health of populations, which remains the top priority

for all governments and the main concern of the populations themselves. Mediter-

ranean countries have the same demands, and a significant leeway.

Safety levels also have an impact on tourism, a major economic activity in all Med-

iterranean countries to the extent that their attractiveness depends in part on the

safety that they are able to offer their visitors. Food poisoning due to a lack of or a

breakdown in the cold chain is the most common annoyances, the most unpleasant

and most unfortunate inconvenience for tourists visiting hot countries. The cold

chain is therefore a crucial tool for the development of tourism across the

Mediterranean.

The current situation for temperaturecontrolled transport

Mediterranean countries share similar climatic conditions and face high tempera-

tures, particularly in summer. These temperatures have a significant impact on

product lifespan as well as on the storage or transport possibilities for certain fresh

products. If the requirements in terms of temperature-controlled logistics are similar

from one Mediterranean country to another, the current situations in the cold chain

are highly variable.

Low levels of equipment

Cold-chain logistics around the Mediterranean suffer from a lack of equipment,

starting with agriculture, for purposes of rapid storage at harvest time (see Mon-

voisin’s cold tripod), right through to the consumer, via temperature-controlled

storage, refrigerated transport, distribution and food factories. According to the

United Nations Refrigeration, Air conditioning and Heat Pumps Technical Options

Committee (RTOC) Report of 20102, with 4 million temperature-controlled land

transport systems, the rate of global equipment was of 1 per 1750 inhabitants in

2010. However, this rate varies greatly from one country to another, and from one

region to another. With 6,000 equipment vehicles in 2012, India only has one tem-

perature-controlled transport vehicle per 200,000 inhabitants. With some

2 - UNEP, Refrigeration, Air conditioning and Heat Pumps Technical Options Committee (RTOC) Reports, Nairobi, UNEP

(four-year United Nations report on the evolution of the ozone layer and carbon).

307The cold chain, a crucial link to trade and food security

150,000 vehicles in 2012, France is within the European average with 1 vehicle per

450 inhabitants (The European fleet is estimated at 1,100,000 vehicles). If southern

European countries are well equipped, southern and eastern Mediterranean countries

are generally under-equipped. With only 5 to 6,000 vehicles in service in 2007,

Tunisia has only one vehicle per 1,750 inhabitants, thus remaining within the global

average.

The level of equipment in warehouses is also insufficient to meet the demands of

temperature-controlled logistics both for the domestic markets of the countries con-

cerned and for the development of trade between Mediterranean countries. IIR data

show a strong heterogeneity for refrigerated storage facilities in the world including

Mediterranean countries. For example Tunisia has tripled its refrigerated storage

capacity over a period of 15 years, between 1996 and 2010, 70% of which is used

for fruit and vegetables. With a park of approximately 1,500,000 m3, of which 17%

is used for frozen products, the country has about 140 m3 per thousand inhabitants

and approaches developed countries that have 200. However, this park’s facilities are

not very efficient in terms of energy as they consume more than 120 kWh per m3

per annum and remain under-utilised with occupancy rates of 50 to 60%.

Box 2: Metrological tools: indicators, thermometers, recorders

There can be no cold chain without temperature traceability, and traceability requiresthe right tools. These have evolved considerably in recent years, integrating, in par-ticular, new technologies, including biotechnologies and information technologies.Recorders using paper bands or disks have almost disappeared, giving way to elec-tronic recorders or indicators.

Temperature recorders have become an indispensable accessory for cold rooms,warehouses and reefer trucks. The European regulation 37/2005 requires the use oftemperature recorders througout the entire cold chain for frozen products, whichmust, since 2010, comply with the standard NF EN 12830, currently under review,and regularly checked according to standard NF EN 13486. In practice, checking iscarried out before using the machinery and then every two or three years. Properlyused, these recorders can demonstrate compliance with the performance require-ments but also to prevent trade disputes. For the benefit of users, some countriesoffer a list of recorders (the one established by France is available on the website ofthe Ministry of Agriculture). Today, these recorders are integrated into devicestracking transport, the vehicle’s position, the data of the refrigeration unit, energyconsumption or the opening of doors. These systems provide a centralised way, notonly to access the data’s history, but also receive alarms allowing for preventiveaction.

Probe thermometers to measure product temperature are just as necessary in casesof doubt or disagreements during destructive product controls. Their legal metro-logical version is the tool of control services, but it is also that of controls at theinterfaces between professionals. Even though probe thermometer technology haslittle evolved, methods of control have undergone important changes within theEuropean Union. Their use still needs to be developed in all countries. Thermom-eters must conform with the standard NF EN 13485 and be checked regularly, liketemperature recorders, according to standard NF EN 13486.

308 MEDITERRA 2014

Finally, indicators and integrators of temperature, which allow for simple monitoringof compliance with the cold chain by operators, have evolved and developed greatlyover the last years. Their price has fallen dramatically, allowing for a wider use ofthese tools, particularly in the cold chain of health products. Electronic indicatorsderived from recorders are now used alongside chemical, biological, microbiologicalor mechanical indicators. They are simple to use and their cost is low enough toenvisage, in the mid-term, their use on all products, for example on vaccines. Theiruse should become more widespread in the coming years.

Gérald Cavalier, President of the Section storage and transport of the IIR, Cemafroid-Tecnea (France).

The cold chain is not only limited to warehouses and means of transport. Product

quality is primarily guaranteed, according to the principles of Monvoisin’s cold

tripod, by early cold. Agricultural stocking equipment is just as important as efficient

equipment in industrial or traditional processing units

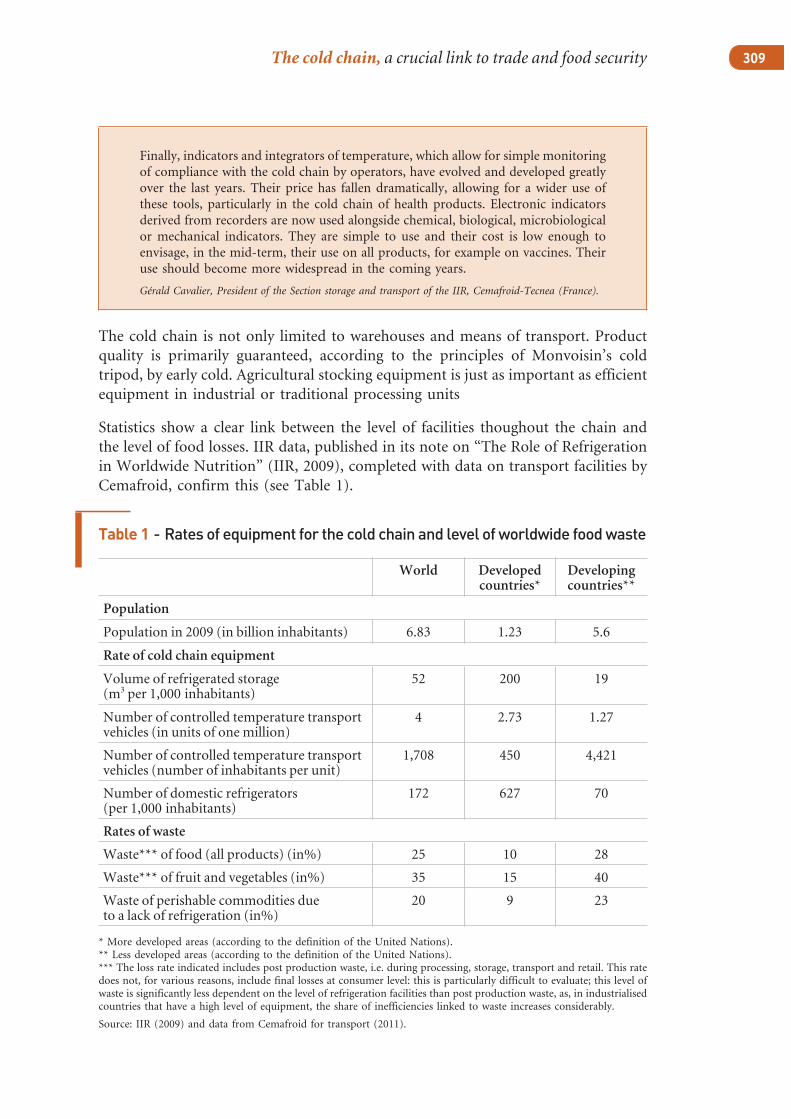

Statistics show a clear link between the level of facilities thoughout the chain and

the level of food losses. IIR data, published in its note on “The Role of Refrigeration

in Worldwide Nutrition” (IIR, 2009), completed with data on transport facilities by

Cemafroid, confirm this (see Table 1).

Table 1 - Rates of equipment for the cold chain and level ofworldwide foodwaste

World Developedcountries*

Developingcountries**

Population

Population in 2009 (in billion inhabitants) 6.83 1.23 5.6

Rate of cold chain equipment

Volume of refrigerated storage(m3 per 1,000 inhabitants)

52 200 19

Number of controlled temperature transportvehicles (in units of one million)

4 2.73 1.27

Number of controlled temperature transportvehicles (number of inhabitants per unit)

1,708 450 4,421

Number of domestic refrigerators(per 1,000 inhabitants)

172 627 70

Rates of waste

Waste*** of food (all products) (in%) 25 10 28

Waste*** of fruit and vegetables (in%) 35 15 40

Waste of perishable commodities dueto a lack of refrigeration (in%)

20 9 23

* More developed areas (according to the definition of the United Nations).** Less developed areas (according to the definition of the United Nations).*** The loss rate indicated includes post production waste, i.e. during processing, storage, transport and retail. This ratedoes not, for various reasons, include final losses at consumer level: this is particularly difficult to evaluate; this level ofwaste is significantly less dependent on the level of refrigeration facilities than post production waste, as, in industrialisedcountries that have a high level of equipment, the share of inefficiencies linked to waste increases considerably.

Source: IIR (2009) and data from Cemafroid for transport (2011).

309The cold chain, a crucial link to trade and food security

Cold chain quality and practice

The climactic conditions around the Mediterranean require the use of quality equip-

ment. However, the sanitary control authorities and users alike have commented on

the lack of certain materials and equipment whose performance levels have unfortu-

nately been sacrificed for price considerations. This is the case for both transport

equipment and storage capacity.

These levels of performance are not enough to guarantee cold chain quality. Equip-

ment requires proper maintenance and therefore a follow-up by competent and

committed personnel. On the one hand, equipment reliability has improved enor-

mously over the last sixty years, whereas on the other hand, the professional com-

petence and personal conscience of the personnel have become the weak link in the

cold chain at all levels. The regular maintenance of these facilities is still inadequate.

However, the best solutions and best equipment, even well-maintened, are not

enough to guarantee cold chain quality if they are not used wisely. Their operation

requires fully trained and skilled personnel throughout the chain. Bad habits are

numerous: poor product loading, problems in temperature setting regulations, over-

loading of equipment, deficient closing doors, obstruction of blowing devices or

extract air vents, non-ceasing refrigeration during the delivery to avoid icing... and

so on. These are the poor practices that are the main cause for the failure of the

cold chain, in particular during loading, unloading, delivery, stocking, etc.

Perspectives for logistics andfor temperature-controlled transport

The establishment of a cold chain concerns all the links. Agro-food factories as well

as logisticians must develop the necessary tools and solutions. As we have seen, it is

not enough to build warehouses, to buy and use trucks and to develop maintenance

services. The implementation of logistics must also be accompanied by appropriate

regulations and the training and awareness of personnel. Finally, monitoring and

certification systems and services are necessary for the enforcement of the regulations

are applied and to win the trust of consumers, operators and stakeholders, without

whom the cold chain is difficult to develop.

Development of temperature-controlled logistics

Aware of the issues and the current situation of the cold chain, Mediterranean coun-

tries have started to develop networks of warehouses and transport logistics including

temperature-controlled logistics. This is the case in Morocco, Algeria or Tunisia.

Improving the cold chain for fresh products is also a priority for the Turkish Ministry

of Food and Agriculture. Morocco has initiated an important project in this field:

by creating logistics platforms across the territory, including temperature-controlled

warehouses with positive and negative cold allowing the supply of the whole area

and providing essential infrastructure upon which private, national or foreign oper-

ators can rely.

310 MEDITERRA 2014

Like Tunisia, Morocco has also taken steps to implement the ATP in its territory

and transform the provision of international transport to improve the quality of

national transport (see Box 3). Both public and private providers specialised in cold

chain logistics are being developed to meet the growing demand for temperature-

controlled logistics for e.g. Polytrans or Guanter in Morocco. The main European

players have also expanded their networks to other Mediterranean countries like

STEF, the European leader in temperature-controlled logistics, which provides reg-

ular refrigerated links between Mediterranean countries.

Box 3: The ATP and its application in Morocco

The United Nations Agreement of 1 September 1970 relating to the InternationalCarriage of Perishable Foodstuffs and on the Special Equipment to be Used for SuchCarriage (ATP) came into force on the 21 November 1976. It sets the minimumrequirements for temperature-controlled transport vehicles used for internationaltransports in signatory countries. It specifies the testing procedures, sizing and clas-sification of the insulation and refrigeration performance of new vehicles, but alsothe verification of the performance of vehicles in service. The terms of this agreementstate that all temperature-controlled vehicles ensuring the international transport ofperishable goods within contracting states must have a technical compliance certif-icate (ATP certificate), and associated marking issued by the competent authorityof the country where the vehicule is registered. The certificates are valid for six yearsand can then be renewed for periods of three years. The agreement also establishesa list of the perishable goods concerned.

The agreement is governed by the United Nations Economic Commission for Europe(UNECE, www.unece.org). Each country designates a competent authority in chargeof delivering ATP certificates. The lists are available on the UNECE site. In France,this authority has been delegated to Cemafroid by the Ministry of Agriculture(www.autoritecompetenteATP.cemafroid.fr). Each country can also designate atesting station, a laboratory whose task is specifically to test new equipment andcontrol the testing of equipment in service. Cemafroid is currently the official testingstation in France. Not all countries have such a laboratory given the investmentrequired to build it. The countries have also established a network of ATP expertsor test centres for the re-certification of vehicles in service. In France there are morethan two hundred such centres (Cavalier, 2008).

Originally created to ensure food safety, the ATP now also controls environmentalperformance (Cavalier, 2009). Its consumption measurements allow the user to com-pare the energy performances of different solutions, and its requirements in termsof insulation for energy saving.

After the ratification and signature of the ATP in 1981, Morocco integrated it intoits national legislation by enacting the Dahir of 6 May 1982. Pending the publicationof specific legislation, an interministerial circular (Ministry of Agriculture andAgrarian Reform, Ministry of Transport, Ministry of Public Works, of Vocationaland Management Training) was published on 2 July 1993 for the implementationof the agreement.

Thereafter, pursuant to the Dahir of 6 May 1982, the decree of 5 January 1999 andthe joint order of 30 April 2004 were published. These texts have established anational commission to review the applications of ATP certificate under the chair-manship of the former Department of Livestock (veterinary services), which from 1January 2010 has become the National Agency for the Sanitary Safety of Food Prod-ucts (ONSSA), the competent ATP authority. The ATP is payable on Moroccan

311The cold chain, a crucial link to trade and food security

territory for all temperature-controlled transport vehicles unless there are specificderogations. The ONSSA delivers ATP agreements for new imported vehicles andrenews ATP certificates for vehicles in service destined for international transport.For national transport, the office issues certificates of sanitary agreements during thetransitional period.

Morocco is currently revising its national regulations and will soon establish anagreement or designation procedure for a test station and for test centres requiredfor performance verification of the park in terms of temperature-controlled transportof perishable goods. The national park currently has about 2,520 vehicles in service,mainly trucks and vans. The park reserved for temperature-controlled transport forperishable goods has nearly 443 vehicles in service, belonging to 236 internationalroad transport companies: 26% of these vehicles are less than 6 years old, 29% arebetween 6 and 9 years old, and 44% are older than 9 years. Most are semi-articulatedtrucks, classed FRC (class C mechanically refrigerated equipment with heavy insu-lation adapted to the transport of frozen or chilled products) in 95% of cases, andFNA (normal class A refrigerated equipment adapted only to the transport of freshproducts) in 5% of cases.

Regarding cold warehouses, in accordance with the law 28-07 of 11 February 2010on food product safety (“SSA Act”), in mid-2013, ONSSA has approved 24 temper-ature-controlled warehouses specifically for, among other products, butter, cold-cuts, imported frozen meat and gave 9 favourable opinions for the storage of fisheryproducts.

Dr Soumia El Hadji, ONSSA/DSV/DVHA (Morocco).

Regulatory changes

The development of cold chain logistics also requires appropriate and applied reg-

ulations, backed up by technical standards. Exchange agreements with the European

Union require the application of European regulations that set performance require-

ments in terms of temperatures for the cold chain. These performance requirements

will be even easier to keep if they are backed up by obligations of means. They will

allow for the setting of simple objectives for minimum performance level of equip-

ment easier to use by professionals.

In the transport sector, the ATP international regulations for cross-border transport

sets requirements for easily satisfiable means both for new equipment and for equip-

ment in use. Southern European countries have expanded (or are currently seeking

to do so) the application of the ATP regulations to their national transport in order

to ensure a quality cold chain suited to their climate conditions. This is the case of

Morocco, that signed the agreement in 1981. The country is trying to develop its

own regulations. Tunisia has also signed the agreement in 2005 and Turkey in 2012.

Other Mediterranean countries, such as Algeria, are thinking of adopting it.

Draft regulations are being prepared or published to harmonise and improve other

cold chain equipment. An example is the generalisation of the use of existing stand-

ards on recorders or thermometers.

312 MEDITERRA 2014

The development of suppliers of suitable equipment

and services

There can be no cold chain logistics without suitable equipment and services. The

supply of local constructors’ equipment or of imported material distribution net-

works has increased considerably over the last years. However, the insufficient

enforcement of regulations, of their shortcomings, sometimes give way to cheap

equipment but with poor performance. It is essential that the authorities provide

control (Cavalier, 2008) and ensure that quality solutions, whether constructed on

site or imported, are adapted to local needs. Although quality solutions are also

sometimes more expensive, they should not be eliminated.

In recent years, manufacturers of equipment have developed all around the Medi-

terranean, e.g. SAFKAR, manufacturer of refrigerated transport groups in Turkey,

COLDEQ and SIMPATIC, manufacturers of equipment for isothermal cells in

Tunisia, or CECI in Morocco. Market leaders have also established networks of

agents or agencies. Carrier Transicold or Thermoking, via their representatives, cover

the whole world with their refrigerator group maintenance service point networks.

Equipment rental facilities, service included, are also on the increase. The Petit-

Forestier group, world leader in this field, specialised in temperature-controlled

transport vehicles and refrigerated display cabinets, recently established itself in

Morocco.

To respond to the development of the cold chain in Mediterranean countries, the

range of solutions, equipment and services have yet to expand and mesh the entire

region. It must also integrate the specific needs of certain regions, in particular

remote, mountainous or desert regions, which require special conditions (taking into

account the climate, transport time or road quality): refrigerator groups adapted to

working conditions that are more extreme than the standard versions, with tropic-

alisation options; bodies adapted to greater insulation requirements for lower thermal

losses, particularly on long haul routes; greater mechanical constraints on poor road

surfaces.

Training and awareness-raising

The development of solutions will only be effective if it is accompanied by proper

training of both professional and individual users. The consumer will always be the

weakest link of the chain. He must constantly be aware of the need to respect the

cold chain. Surveys carried out on the state of domestic refrigerators in French

households show that this effort must always be stressed. It is even more important

to raise this awareness in countries where the inhabitants are less well equipped, or

not equipped at all, for it is at the beginning that habits, good or bad, are adopted.

In turn, professionals must know and understand the issues related to the cold chain,

in order to incorporate them. Maintaining the cold chain’s continuity must be con-

sidered as an opportunity and not as a constraint. This implies that the benefits

incurred by a quality cold chain are shared between the various players and that

cold chain logistics provide tangible added value for all players. The only savings

313The cold chain, a crucial link to trade and food security

generated by the reduction of losses are a huge economic pool, but the benefits also

have a bearing on product quality, which must be sought in order to lengthen sales

time and therefore reduce distribution costs.

Finally, operators and personnel must all be trained to the proper use of equipment

and good practices of the cold chain, ranging from the handlers to the site manager

via quality control, technical and maintenance services, drivers, farmers, pharma-

cists... The cold chain is not only the domain of refrigeration technicians whose

interventions are always limited to the installations and equipment. In both the

health and food sectors, personnel involved in the cold chain must be well informed

on this subject that is often forgotten in their basic training.

Clients must also be aware of the savings made possible by a careful choice of

materials, the cost of using skilled professionals, both for the choice and the man-

agement of equipment. This effort is small when compared to the potential savings,

a possibility that is too often under-estimated.

Box 4: Presentation of the International Institute

of Refrigeration (IIR)

The IIR is the only intergovernmental organisation that gathers all scientific andtechnical expertise and independently disseminates all aspects of cold chain facts andinformation, from cryogenics to air-conditioning, through the liquefaction of gases,the cold chain, procedures and equipment for refrigeration, refrigerants and heatpumps. Member states, including most Mediterranean countries represent 60% ofthe global population. The main issues are food security, health, energy efficiency,global warming and the ozone layer. In this regard, the IIR has signed cooperationagreements with the United Nations Food and Agriculture Organisation (FAO), theUnited Nations Industrial Development Organisation (UNIDO), the World HealthOrganisation (WHO), the United Nations Framework Convention on ClimateChange (UNFCCC), the United Nations Environment Programme (UNEP), and itis an observer member of the Codex Alimentarius. The dissemination of knowledgeis carried out by various means (meetings and congresses, guides and technical notes,a documentary database with about 100,000 references).

For further information: www.iifiir.org

Conclusion

A quality cold chain is essential for the development of Mediterranean countries and

their food and health product trade, but also for the improvement of the living

conditions of inhabitants, as well as the support of the evolution of their life-styles

and consumer habits.

Apart from a few successful export-orientated industries, existing services and equip-

ment are insufficient. Only investments made by many countries and the develop-

ment of regulatory and technical requirements will lead to a functional cold chain

in the short and medium term. They must be accompanied by the development of

training and awareness-raising of staff and consumers, and also the establishment

314 MEDITERRA 2014

of a reassuring regulatory and normative framework for cold chain operators. All

Mediterranean countries should be assured of rapid returns on their investments

thanks to the savings achieved on the products and the improved quality thus

generated.

Working towards the establishment of a quality Mediterranean cold chain is not and

will not represent sunk costs investments, quite the contrary. Its implementation

will help to support the development of agriculture, the food industry, distribution,

tourism and the industries and services necessary for construction, management,

maintenance and safeguarding of the cold chain. It will provide the Mediterranean

with an opportunity to add value to its products and services and to create new

employment possibilities3.

Bibliography

Cavalier (G.) (2008), “La qualité totale du maillon transport sous température dirigée”,Paris, Conseil national du froid (CNF), 8 December.

Cavalier (G.) (2009), “ATP Regulation: How a Food Safety Standard Can Become anEnvironmental Protection Driver”, European Conference, Milan, Politecnico, June.

Cavalier (G.) (2011), “From A to Z: 26 Challenges Facing Refrigerated Trucks for Sus-tainable Development”, 23rd IIR International Congress of Refrigeration, Prague,21-26 August.

Cavalier (G.) and Tassou (S. A.) (2011), “Sustainable Refrigerated Road Transport”,Informatory Note on Refrigerating Technologies (International Institute of Refrigeration).

Cavalier (G.) and Viart (D.) (ed.) (2007), “Chaîne du froid: les outils pour maîtriser tousles maillons”, Revue pratique du froid et du conditionnement d’air, 950.

De Rijk (J.), Cavalier (G.) and Saline (P.) (2008), “L’économie européenne de la logis-tique du froid”, Université du froid et de la logistique agroalimentaire, STEF-TFE, Paris,Stade de France, 11 March.

International Institute of Refrigeration (IIR) (2009), “Le rôle du froid dans l’alimentationmondiale”, Note of the International Institute of Refrigeration.

3 - This chapter was coordinated by the IIR.

315The cold chain, a crucial link to trade and food security