through the looking glass - wsata)...

TRANSCRIPT

State Taxation and Pass-Through EntitiesBruce Ely—Bradley ArantBoult Cummings LLP

Nikki Dobay—Council on State Taxation

Tracee Abel, CPA-Montana Department of Revenue

Through the Looking Glass

Agenda• Down the Rabbit Hole – history and rise in use of pass-through

entities

• The Queen's Croquet Ground – how states tax and audit pass-through entities

• A Mad Tea-Party – changes in federal audit procedures for partnerships and LLCs

• Who Stole the Tarts? – Federal tax reform and state pass-through entity taxation

• Advice from a Caterpillar – Final Thoughts

2

- history and rise in use of pass-through entities

Snap shot of current use of pass-through entities• Sub K entities (general partnerships, LLCs and limited/LLP/LLLPs)

surpassed individuals and C/S corporations as the “top income recipients for the second consecutive year” (2014)

• Sub K entities filed more than 3.61 million returns- a 4.4% increase over 2013—covering 27.71 million partners (but rising only 0.8% compared to the 8.5% increase last year)

• Domestic (U.S.) LLCs make up two-thirds of all Sub K entities

• Real estate and rental/leasing accounted for almost 50% of all Sub K entities

4

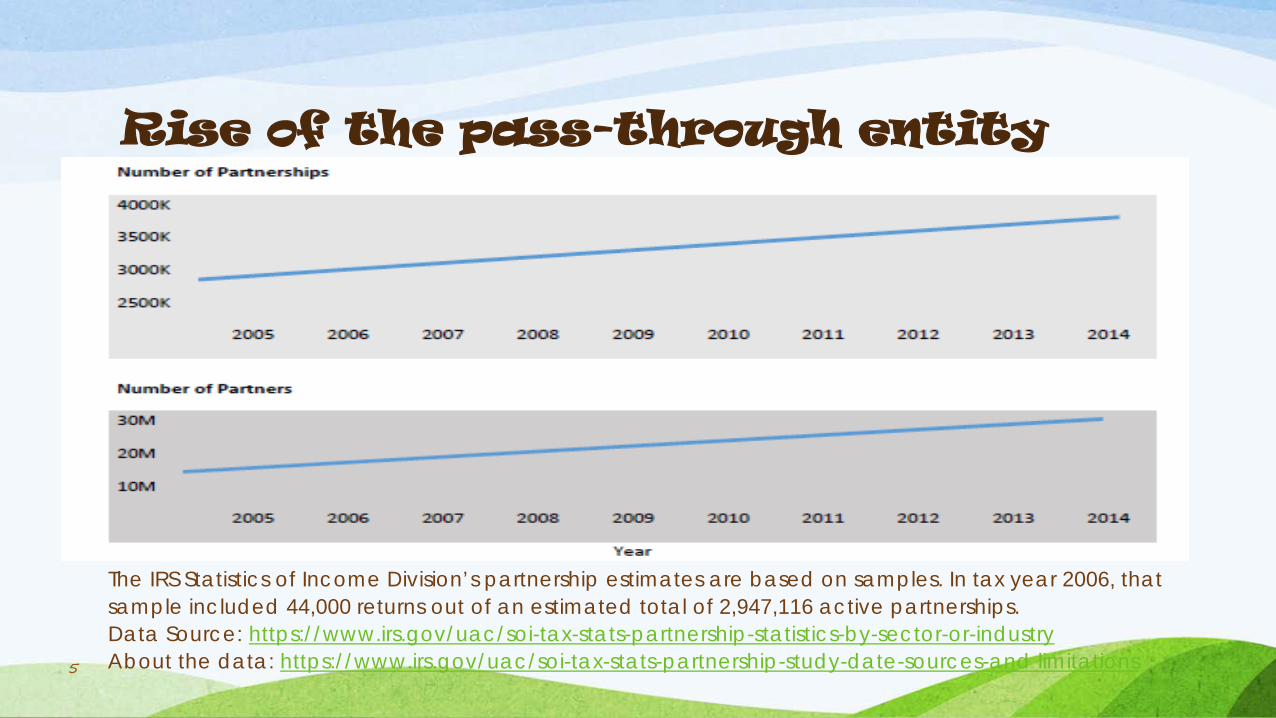

Rise of the pass-through entity

The IRS Statistics of Income Division’s partnership estimates are based on samples. In tax year 2006, that sample included 44,000 returns out of an estimated total of 2,947,116 active partnerships.Data Source: https://www.irs.gov/uac/soi-tax-stats-partnership-statistics-by-sector-or-industryAbout the data: https://www.irs.gov/uac/soi-tax-stats-partnership-study-date-sources-and limitations5

Effective tax rates of pass-through entities v. corporate entities• The State Tax Research Institute (STRI) working with PwC examined the share of corporate

and pass-through business income using state tax definitions and to compare the state-level effective tax rates (ETRs) of both types of businesses taking into consideration taxes paid at the entity level and by their individual owners. This report is the first to undertake these measures and comparisons at the state level.

• This report finds that the corporate share of aggregate state-level business income has declined from 53 percent in 1993 to 42 percent in 2013. This is consistent with other studies that find the federal-level corporate share of business income has declined over this time period.

• The Study’s primary finding is that the aggregate state-level effective business income tax rate for corporations (6.1%) is 30 percent higher than the aggregate rate for pass-through businesses (4.7%). This finding and the detailed analysis in the Study should be increasingly valuable to state policymakers as they struggle to maintain consistency and fairness in state tax structures while balancing current budgets and considering conformity to potential federal tax reform.

6

The Queen's Croquet Ground—how states tax and audit pass-through entities

State Conformity with Federal Rules

• Most states recognize the federal tax classification of business entities.

• Most state pass-through entity information or composite returns begin with the federal Forms 1065/1120S and/or Schedule K.

8

Nexus Issues• Does owning an interest in a pass-through entity create nexus

for an owner?

• Does ownership of a general partnership vs. limited partnership interest make a difference?

• Does an active or limited membership interest in the LLC make a difference?

9

Apportionment Issues• Partner/Shareholder Level v. Entity Level

• Individual vs. Corporate owners

• Are transactions between the partners and the partnership required to be eliminated?

• Sale of a partnership interest – Is it business or nonbusiness income?

10

Withholding/Composite Return Requirements

• Most states require a pass-through entity to withhold on behalf of a nonresident owners distributive share of state source income.

• Some states require a composite return.

• Some states offer a waiver from withholding/composite requirements if the owner agrees to file and pay taxes in the state.

• Owners claim their share of withholding (or composite tax) as a credit against their personal tax liability.

11

Withholding/Composite Return Requirements

• Owners claim their share of withholding as a credit against their personal tax liability.

• See Bloomberg BNA “Pass-through Entity Navigator” Chart (handout)

12

Tax at the Pass-through Entity Level- State Audit Procedures

Pennsylvania 72 P.S. §7306.2• Applies to underreporting of income by more than $1 million

• Applies to partnerships with 11 or more individual partners or partnerships that have at least one partner that is a corporation, LLC, partnership or trust

• Does not apply to publicly traded partnerships

• Only the partnership may appeal the adjustment

• Final adjustment is binding on all partners

• Assessment is made for thetax year being adjusted

13

A Mad Tea-Party—changes in federal audit procedures for partnerships and LLCs

Federal partnership audit reform

• HR 1314 – Bipartisan Budget Act of 2015 (“BBA”) (P.L. 114-74 signed by Pres. Obama Nov. 2, 2015)

• Includes federal partnership audit “reform”• Generally applies to partnership taxable years beginning

after December 31, 2017• Confusing, complex body of law imposing administrative burdens

for the IRS and for taxpayers• Amendments are intended to streamline and simplify the

partnership audit rules, and …raise over $9.3 billion in revenue.• And that’s just at the federal level …

15

Why was reform necessary?

• In 2012, the IRS audited 0.8% of large partnerships, but 27% of large C corporations

• No change rate for audits closed in 2012:• 42% for partnerships; 66.7% for large partnerships

• 29% for C corporations; 27.2% for large corporations

• Oh … and $9.3 billion of revenue (without raising taxes)!

16

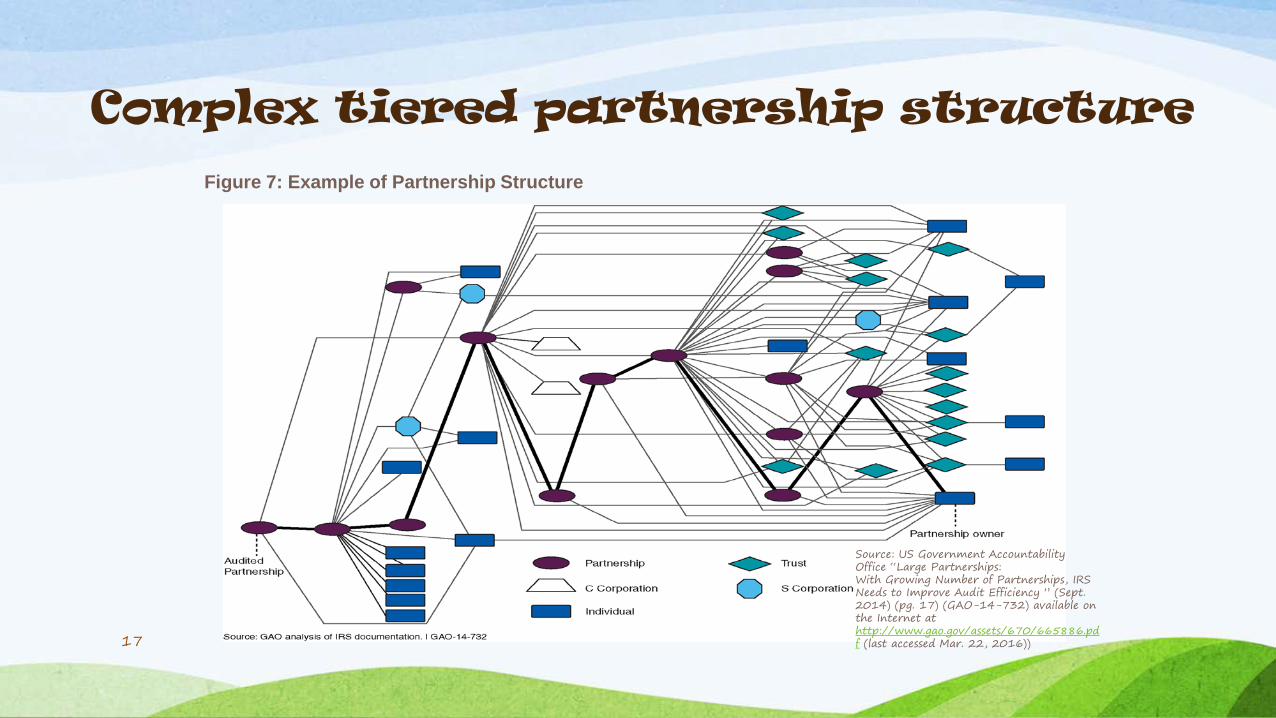

Complex tiered partnership structureFigure 7: Example of Partnership Structure

Source: US Government Accountability Office “Large Partnerships: With Growing Number of Partnerships, IRS Needs to Improve Audit Efficiency ” (Sept. 2014) (pg. 17) (GAO-14-732) available on the Internet at http://www.gao.gov/assets/670/665886.pdf (last accessed Mar. 22, 2016))17

High-level: Old law v. New lawPre-TEFRA

(before 1982)

• Audit, assess and collect ONLY at partnerlevel (large or small partnerships)

BBA (New law)2018

(but 2015 - 2017 elections)

• ≤100 eligible partners (elective) – audit, assess and collect at partnerlevel

• All others – audit, assess and collect at the partnershiplevel (subject to “push-out” elections)

TEFRA1982-2017

• Audit at partner -ship level if >10 partners

• Assess and collect ONLY at partnerlevel

• Electing “large partnerships” procedure (rarely used)

18

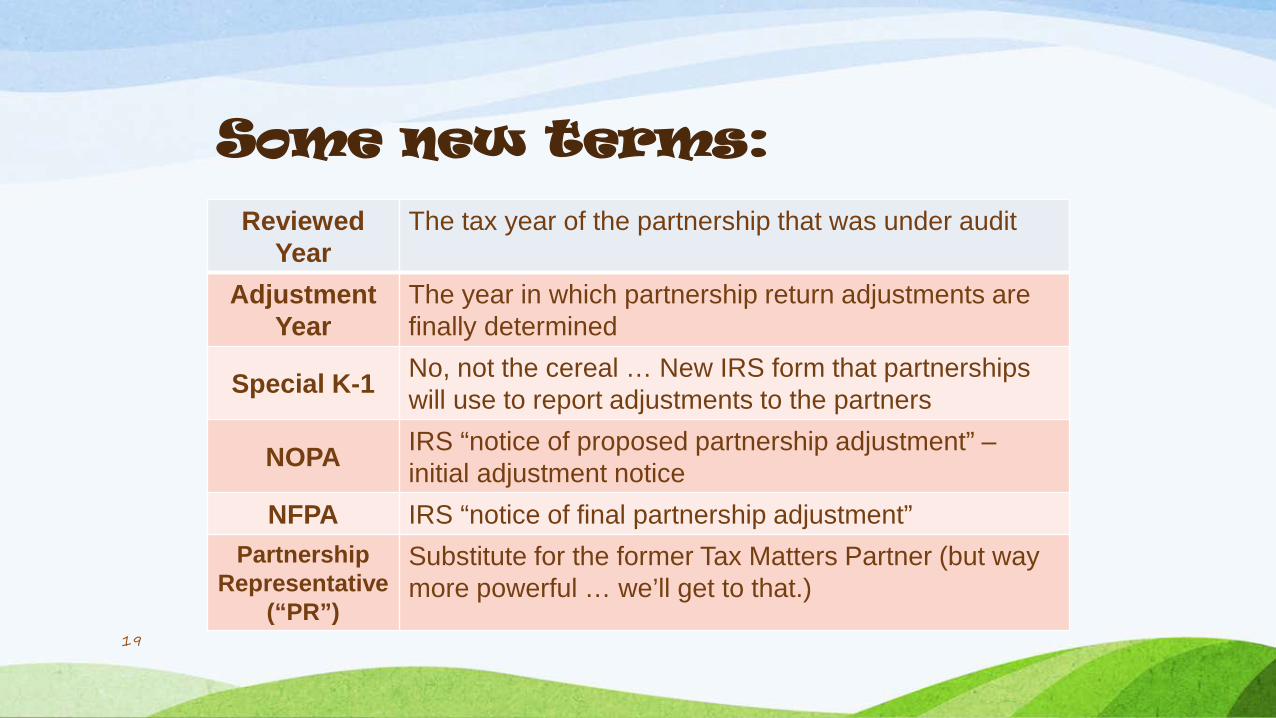

Some new terms:Reviewed

YearThe tax year of the partnership that was under audit

Adjustment Year

The year in which partnership return adjustments are finally determined

Special K-1 No, not the cereal … New IRS form that partnerships will use to report adjustments to the partners

NOPA IRS “notice of proposed partnership adjustment” –initial adjustment notice

NFPA IRS “notice of final partnership adjustment”Partnership

Representative (“PR”)

Substitute for the former Tax Matters Partner (but way more powerful … we’ll get to that.)

19

General overview of the new federal rules

Option #1Election Out

• Pre-TEFRA rules apply• Audit, assess and

collect at partnerlevel

• Strict eligibility requirements• 100 or fewer partners

• Count by K-1s• No partnerships, LLCs

(including SMLLCs) or trusts as partners

• Annual election “in” or “out” of regime on timely filed return (do not expect much IRS grace)

Option #2Partnership Pays

•Partnership taxed at highest IRC §§ 1 or 11 rate in current year

•Current partners bear economic burden

•“Imputed underpayment” reduced if reviewed year partners file amended returns, pay tax or demonstrate lower rate or tax-exempt partners

•“Overpayments” taken into account by partnership in adjustment year as change in non-separately stated income or loss

•Interest and penalties determined at the partnership level

Option #3 Partnership Pushes Out

• Reviewed year partners increase IRC ch. 1 taxes in “current year” based on “as if amended” formula for the reviewed year through the current year.

• Partners pay interest at increased rate and any penalties

• Alternative rule does not apply to “overpayments”

20

Issues for states to consider• Conformity is not automatic

• Most states conform to the IRC but only for the determination of taxable income, not for its administrative procedures –states usually have their own

• State statutes don’t treat partnership as “taxpayer” (except for nonresident partner composite return and withholding)

• Few states have their own partnership audit procedures

• Information sharing between IRS and states is unclear21

More issues…• Will states accept the federal partnership representative?

• How will the partnership report federal changes to the states?

• Elections – should partnerships and states be bound by federal elections?

• Unique state partnership issues• Multistate income apportionment factor - Reviewed vs. Adjustment year

• Unitary partnership – apportion/allocate at the partner level or partnership level

• Partners that move between reviewed years and adjustment year

• Credit for taxes paid to other states22

And still more Issues…• Statutes of limitation and notices to partners

• Relationship to existing state RAR statutes.

• Adjustments that affect one partner vs. multiple partners

• Adjustments that affect multiple partners

• Adjustments that affect other years

• Adjustments resulting in refunds

• Penalties and interest, collection of liabilities, due process?

…just to name a few23

The Organizations working on this Draft Model Statute (see handout) are:• ABA Section of Taxation SALT Committee Task Force• American Institute of CPAs (AICPA)• Council On State Taxation (COST)• Institute for Professionals in Taxation (IPT)• Tax Executives Institute (TEI)• Multistate Tax Commission (MTC)

• Note: This Draft Model Statute has not yet been formally endorsed by the Interested Parties - it is a draft for discussion purposes only

Organizations going down the rabbit hole. . .

24

Draft Model Statute - Reporting Federal Partnership Level Audits

• Make an election as to whether the partnership or its partners will pay the tax:

• Option 1: Partnership pays the tax (entity level tax)• Option 2: Reviewed year partners pay the tax (partnership

issues “state” K-1 forms)• Option 3: Hybrid approach, partnership pays the tax on

behalf of all non-resident partners but resident partners pay their own tax

• Election is irrevocable unless the State, in its discretion, otherwise allows

25

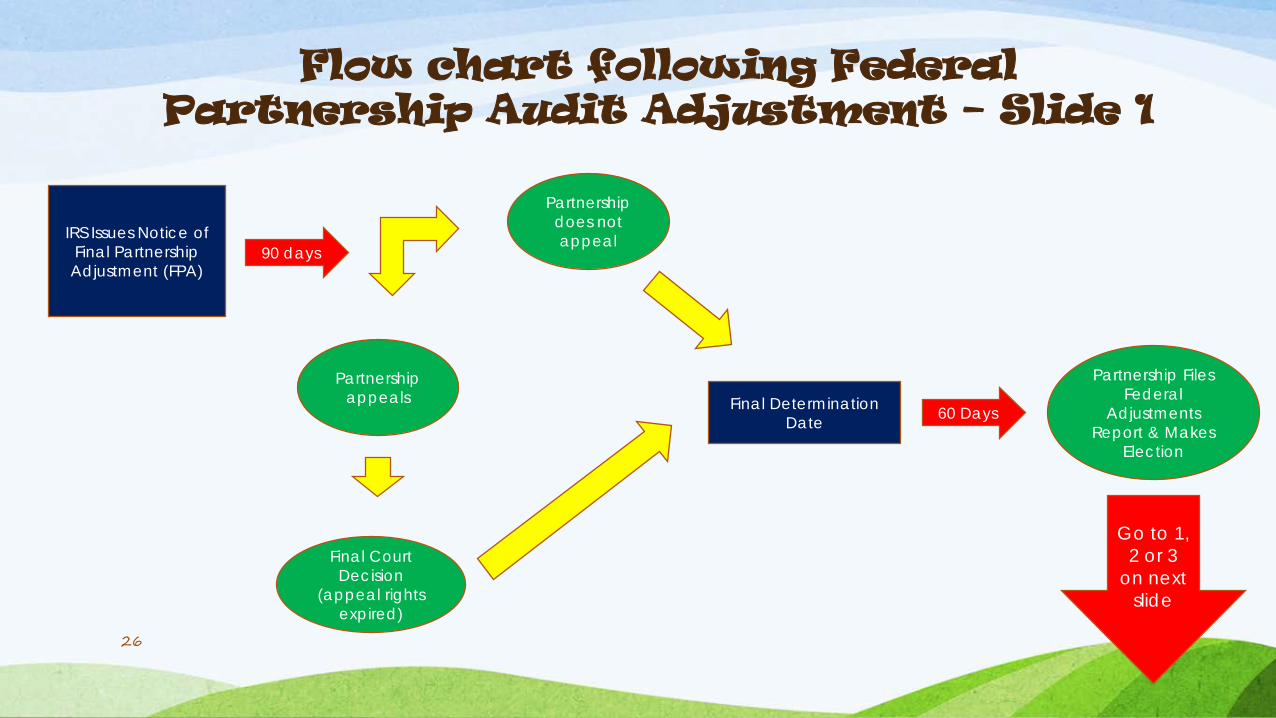

IRS Issues Notice of Final Partnership Adjustment (FPA)

Final Determination Date 60 Days

Partnership Files Federal

Adjustments Report & Makes

Election

Go to 1, 2 or 3

on next slide

90 days

Partnership does not appeal

Partnership appeals

Flow chart following Federal Partnership Audit Adjustment – Slide 1

Final Court Decision

(appeal rights expired)

26

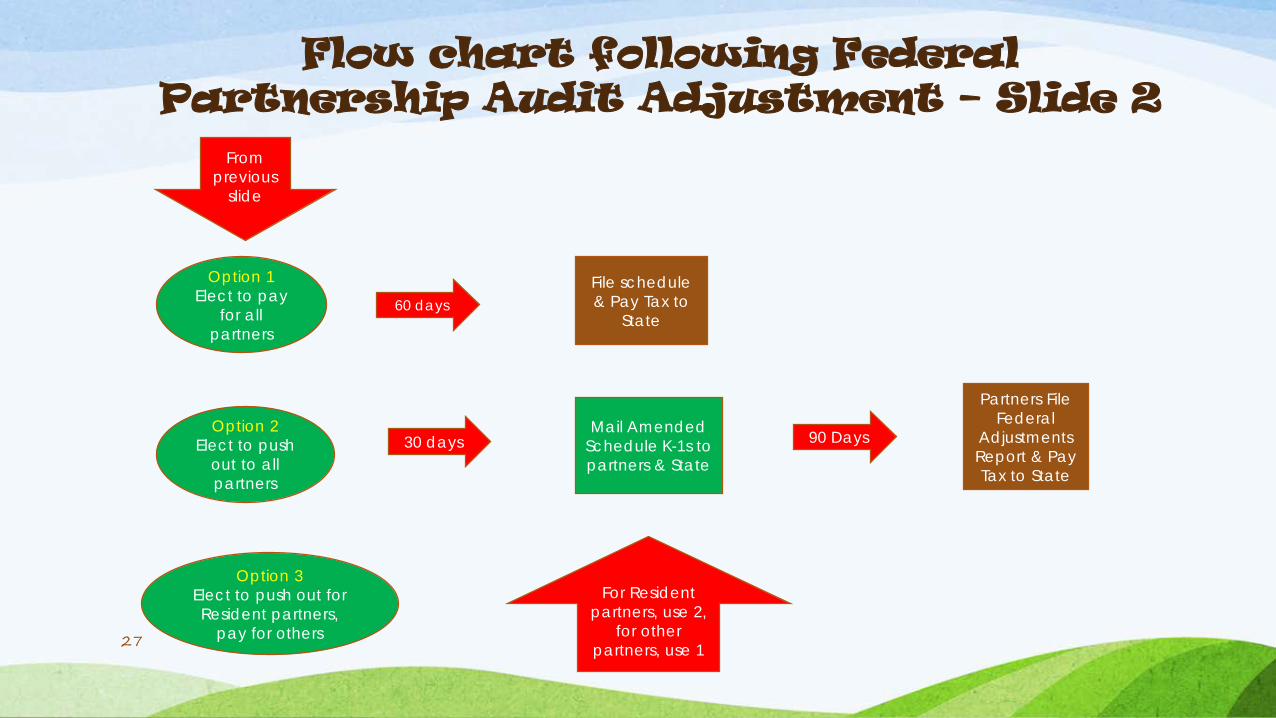

Option 1Elect to pay

for all partners

Option 2Elect to push

out to all partners

Option 3Elect to push out for Resident partners,

pay for others

60 daysFile schedule & Pay Tax to

State

30 daysMail Amended

Schedule K-1s to partners & State

90 Days

Partners File Federal

Adjustments Report & Pay Tax to State

For Resident partners, use 2,

for other partners, use 1

Flow chart following Federal Partnership Audit Adjustment – Slide 2

From previous

slide

27

Draft Model Statute –Other Considerations

• Composite Income Tax Returns

• Federal Partnership Representative acts on behalf of the partnership unless the Partnership delegates such authority to another person

• Model Statute requires partners to pay or file for refund if:• The federal audit does not result in an Imputed Underpayment to the

State; or

• The partnership has dissolved or becomes insolvent

• The States’ tax agencies can promulgate regulations to address adjustments to special partner allocations28

Who Stole the Tarts?Federal tax reform and state pass-through entity taxation

Tax Reform Framework• Tax relief for middle-class families.

• The simplicity of “postcard” tax filing for the vast majority of Americans.

• Tax relief for businesses, especially small businesses.

• Ending incentives to ship jobs, capital, and tax revenue overseas.

• Broadening the tax base and providing greater fairness for all Americans by closing by closing special interest tax breads and loopholes.

https://waysandmeansforms.house.gov/uploadedfiles/tax_framework.pdf30

Tax Rates• Lowering the Corporate Tax Rate

• Framework proposes a 20% tax rate on corporate income.

• Corporate integration – several options

• Special Rate on Pass-Through Income• Framework proposes a 25% maximum rate on business income for pass-

through entities (includes sole proprietorships)• Limited to “small and family owned businesses”?

• Recall the Kansas experiment (failed)

• Re-characterization Issues

31

Cost Recovery

• Full and immediate expensing of machinery and other capital assets (but not buildings)• State budgeting could prove difficult• May result in a significant revenue reduction in year of

purchase• Potential “smoothing” period for tax years thereafter • States that allow Bonus Depreciation may be less

impacted. (More than half do not conform to Bonus Depreciation rules)

32

Other Considerations

• Territorial Taxation• Will this apply to pass-through entities?• If so, what will that look like?• Does it impact Apportionment Factors?

• One-time Repatriation Holiday

• Rules for Specific Industry – Still a mystery

33

Other Considerations

• Repeal of Most Deductions & Credits• 199 deduction repealed• R&D and Low Income Housing Credits retained

• Elimination of AMT• Will separately stated items on Schedule K-1 be

necessary?

34

Advice from a Caterpillar

Final Thoughts

“Sometimes I have believed six impossible things before breakfast”

QUESTIONS?

THANK YOU!Bruce Ely – PartnerBradley Arant Boult Cummings [email protected]

Nikki Dobay – Senior Tax CounselCouncil On State [email protected]

Tracee Abel, CPA – Tax SpecialistMontana Department of [email protected]

37