tilaknagar industries ltd. - latest news | india...

TRANSCRIPT

1

TILAKNAGAR INDUSTRIES LTD.

HOLD Target Price: Rs.110.00

CMP: Rs.90.00 Market Cap.:Rs.2726.10 mn.

Date: December 29, 2009

Key Ratios:

Particulars FY09A FY10E FY11E

OPM (%) 19.35 19.89 19.30

NPM (%) 8.90 6.03 5.70

ROE (%) 39.50 16.35 15.43

ROCE (%) 24.3 24.53 25.12

P/BV(x) 0.74 2.91 2.46

P/E(x) 1.89 17.79 15.94

EV/EBDITA(x) 0.86 6.89 6.54

Debt-Equity(x) 2.33 1.47 1.37

Key Data:

Sector Breweries &Distilleries

Face Value Rs.10.00

52 wk. High/Low Rs.236.00/57.00

Volume (2 wk. Avg.) 79267

BSE Code 507205

SYNOPSIS

• Tilaknagar Industries (TI) is a leading player in the

liquor industry and manufactures Indian Made

Foreign Liquor (IMFL).

• The company remains committed to expand profit

margins, achieve robust growth going forward and

increase its footprints globally.

• Rapid induction of new consumers along with

increasing urbanization will accelerate the company’s

future growth.

• The company is setting up a Rs 800 million grain-

based distillery at Ahmednagar in Maharashtra.

• The company has given a bonus issue of Equity Share

in the ratio of two Equity Shares of the Company of Rs

10/- each for every one Equity Share of the Company.

• Net sales and PAT of the Company are expected to

grow at a CAGR of 27.25% & 1.78% over FY08 to

FY11E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Company Profile 06

3. Peer Group Comparison 15

4. Key Concerns 15

5. Financials 16

6. Charts & Graph 19

7. Outlook and Conclusion 21

8. Industry Overview 23

3

Investment Highlights

• Results Update (Q2FY10)

For the quarter ended on September 30, 2009 (Standalone) the company has registered a 28.32

% (YOY) growth in the net sales and stood at Rs.586.83 mn from Rs.457.33 mn of the

corresponding period of the previous year.The operating profit margins for the quarter stood at

22.23%.The operating profit stood at Rs.130.46 mn.During the Q2FY10 the net profit of the

company stood at Rs.40.62 mn. EPS for the quarter stood at Rs.1.34 per equity share of Rs.10.00.

Quarterly Results –Standalone (Rs in mn)

As at Q2FY09 Q2FY10 %Change

Net Sales 457.33 586.83 28.32

Net Profit 51.73 40.62 (21.48)

Basic EPS(Rs)* 9.03 1.34 (85.46)

4

• Margins (%):

Operating Profit Margins (OPM %)

Net Profit Margins (NPM %)

5

• Bonus issued

The company has given a bonus issue of Equity Share in the ratio of two Equity Shares of the

Company of Rs 10/- each for every one Equity Share of the Company.

• Open Offer

D & A Financial Services (P) Ltd, ("Manager to the Offer"), on behalf of the promoters ("Persons

Acting in Concert(s)/ "PACs") has issued this Public Announcement ("PA") to the Equity

Shareholders of Tilaknagar Industries Ltd ("Target Company").The Acquirers along with PACs

intend to make an Open Offer in terms of the SEBI (SAST) Regulations, 1997 to the shareholders

of the Target Company to acquire 2,019,014 Equity Shares of Rs. 10/- each representing 20% of

post-conversion capital/voting capital of the target Company at a price of Rs. 94.00 (Rupees

Ninety Four Only) per fully paid-up Equity Shares ("Offer Price"), payable in cash subject to the

terms and conditions mentioned in PA.

• Expansion plans

The company plans to continue with its proven strategy of expanding both its manufacturing

presence and its marketing and distribution network, backed by strong, established brands and a

consistent introduction of strategic brands in the overall product matrix.

• Build Rs 800 mn distillery in Ahmednagar

Tilaknagar Industries is setting up a Rs 800 million grain-based distillery at Ahmednagar in

Maharashtra. The company has already secured the license for the grain-based distillery from the

state government.

6

• Dividend declared

For the the financial year 2008-09 the company has declared a dividend of 25% (Rs.2.50 per

share) on the face value of equity share Rs.10 each. Recently the company has hiked its equity

capital to Rs.302.85mn from Rs.57.25 mn.

Company Profile

Tilaknagar Industries (TI) is a leading player in the liquor industry and manufactures Indian Made

Foreign Liquor (IMFL). Established in 1933 as Maharashtra Sugar Mills Ltd. (MSM), the company

transitioned to the liquor business in 1987. Over its 75 year existence, TI has grown to be an

organisation committed to quality, excellence and integrity

Tilaknagar Distilleries & Industries Ltd. was promoted as a 100 per cent subsidiary of The

Maharashtra Sugar Mills Ltd. The year 1973 saw TI diversify into the businesses of Industrial

Alcohol, Indian Made Foreign Liquor (IMFL) and Sugar Cubes. Both Maharashtra Sugar Mills Ltd.

and Tilaknagar Distilleries & Industries Ltd have been merged to form Tilaknagar Industries Ltd. (TI)

with effect from August 6, 1993.Since then TI has been engaged in the business of manufacture and

distribution of spirit and Indian Made Foreign Liquor (IMFL).

There has been no change in the promoter of the company. The ‘Dahanukar family’ continues to be

the promoter of Tilaknagar Industries, sharing the same vision and values of the founders.Due to its

core competency in alcoholic beverages and conscious efforts, TI swiftly established its distinct

identity in the liquor industry. Today TI’s brand portfolio consists of unique and diverse brands that

enjoy excellent consumer preference solely due to their quality and value for money.

7

Tilaknagar Industries (TI) is driven by its long term vision of emerging as a formidable brand in the

global alcoholic beverages industry. TI plans to continue with its proven strategy of expanding both

its manufacturing presence and its marketing and distribution network, backed by strong,

established brands and a consistent introduction of strategic brands in the overall product matrix.

Business areas

The current business of the Company is manufacturing, marketing and selling of Indian Made

Foreign Liquor comprising of Brandy, Whisky, Gin, Vodka and Rum.

8

Manufacturing

The mainstay manufacturing hub of TI is located at Shrirampur, Maharashtra. The plant is an ISO

9001:2000 certified plant. A new 50,000 litres per day, state of the art, multipressure distillation

plant will be in operation by September 2009. TI had acquired manufacturing locations last year in

Karnataka and Andhra Pradesh and in addition, TI has 8 lease arrangements and 13 tie-up

arrangements across the country for carrying out manufacturing and bottling activities. Hence, TI

has in all 24 units in 18 States in the country.

Strategic Initiatives

To meet the growing demands of the IMFL segment, TI has planned to invest in expanding the

manufacturing capacity of its main plant together with investing in cost saving equipment.

• The Company has successfully commissioned its Malt Spirit plant at its factory at Shrirampur. It

has capacity to produce 3000 litres per day.

• The Company has successfully commissioned MEE plant to reduce effluent quantity and recover

usable water.

• The Company has successfully commissioned Gas engine for generation of electricity of 700 KW

per hour.

• The Company is expected to commission its 50 KLPD wash to ENA Plant by end of 2009

• The Company is also planning to commission grain based ENA Plant with the capacity of 100 KLPD

by end of the calendar year.

9

Marketing & Selling

During the year 2008-09, TI achieved a sales volume of 5.54 Million cases as against 4.21 Million

cases in the previous year. The remarkable growth of over 30 per cent in adverse economic

conditions was rendered even more impressive by higher sales in the premium categories, which

has resulted in a 70 per cent growth in turnover. A drive to increase national presence, increasing

dominance in their traditional markets and a cohesive marketing strategy were instrumental in

achieving this growth. Senate Royale, which was launched as a flagship brand, has achieved a

national presence including new markets such as Punjab, Haryana, Chandigarh, HP, Delhi, Orissa,

Madhya Pradesh and Chattisgarh. Their Mansion House brand has been the fastest growing brand

in the Canteen Stores Department, also contributing handsomely to the growth in turnover.

TI has invested heavily in communication and customer engagement. In their various efforts to

reach out to the target audience for the entire basket of brands, and create a pan-India impact,

they have planned various consumer centric programs, which are aimed at engaging the

consumers, intercepting with their lives, creating multiple occasions of consumption and ultimately

converting them to loyal consumers of their brands. They have planned various below the line

outlet level activities in addition to a visibility campaign across electronic and digital media. TI will

continue to heavily focus on these key brands and expects to maintain the same momentum in the

future.

10

Products

The company is a leading manufacturer of liquor across the major categories - Whisky, Brandy,

Rum, Vodka and Gin. TI has a market leading position in the southern and western parts of India

Whisky:

TI has eight brands under the 'Whisky' category of liquor

1. Senate Royale Whisk

It manufactured from a blend of the finest Scotch malts from Spey and highland regions and the

finest Indian spirits.

11

2. Mansion House Whisky

It is perfected from Indian malts and select Scotch whisky to create a refined taste for the

discerning palate.

3. Senate Whisky

A unique blend of the finest Scotch malts and Indian neutral spirits

4. Shot Whisky

A blend of barley matured into a drink with notable flavour and smooth taste

5. Classic Whisky

A light, smooth flavoured Scotch blend made with the finest alcohol.

6. Royal Choice Whisky

A blend of first generation barley matured into a drink with notable flavour and smooth taste.

7. Hottt Silk Whisky

A refined peat flavoured blend of high quality ENA matured into a drink with notable flavour and

smooth taste.

12

8. Castle Club Whisky

A unique blend perfected from Indian malts and select Scotch whisky.

Brandy:

TI manufactures two leading brands of Brandy

1. Mansion House Brandy

A blend of finest quality alcohol produced and blended with matured grape spirit.

2. Courrier Napoleon Brandy

A blend made from select grapes, distilled in the Cognac pot stills of France

Rum:

TI holds three strong contenders in Rum brands

1. Savoy Club Rum

It is full-bodied and dark, blended to perfection and matured in old oak casks.

13

3. Royal Choice Rum

A blend made of first generation sugarcane juice spirit and matured to a product with a distinct

flavour and smooth taste.

4. Madira Rum

A blend made of first-generation sugarcane juice spirit and matured to a product with notable

flavour and smooth taste.

Vodka:

TI manufactures two leading brands of Vodka

1. Classic Vodka

It is a blend of the finest triple distilled alcohol with natural ingredients to give a crisp, smooth

flavor.

2. Castle Club

It is a blend of the finest triple distilled alcohol with natural ingredients.

Gin:

TI also manufactures two brands of Gin

1. Savoy Club Dry Gin

14

A blend of natural flavoured dry gin distilled with herbs for a pleasant taste.

2. Royal Choice Duet Gin

A blend of natural flavoured gin distilled with herbs for a pleasant taste.

Exports

With a heritage of 75 years of success, and our long term relationships with local partners in Indian

and offshore markets, they have responded innovatively to changing customer demands to capture

new territories and forayed into uncharted markets.

The distillery has the capacity to produce more than 60,000 liters of alcohol per day. In addition to

TI’s own distilleries and factory at Tilaknagar (Maharashtra), India, the Company also has lease/tie

up with 24 more factories which cater to expanding demand in both domestic and export markets.

The exports are catered from TI’s main factory in Tilaknagar (Maharashtra) to ensure impeccable

quality control and supervision. TI is exporting to many overseas markets in Africa, Caribbean

Islands and Asia.

Their brands continue to find favor with our growing customer base due to their taste, flavours,

quality and competitive markets.

Subsidiary companies

• Surya Organic Chemicals ( P) Ltd

• Prag Distillery (P) Ltd

15

Peer Group Comparison

Name of the company CMP(R.s)

(As on Dec

29.2009)

Market

Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E (x) P/BV

(x)

Dividend

(%)

Tilaknagar Industries 90.00 2726.10 37.12 2.42 0.95 25.00

Empee Distilleries 132.50 2518.70 - - 1.07 50.00

Khoday India 59.00 2217.9 - - 2.28 0.00

Pioneer Distilleries 43.85 552.00 6.37 9.57 1.66 20.00

Key Concerns

• Ban on Advertising, Surrogate Advertisement and Word-of-Mouth publicity

• Strict Distribution Regulation

• Complex Logistics Framework

• Heavy taxes, duties and levies

• Tough competition

• Availability of raw material

• Adequate availability of power risk

16

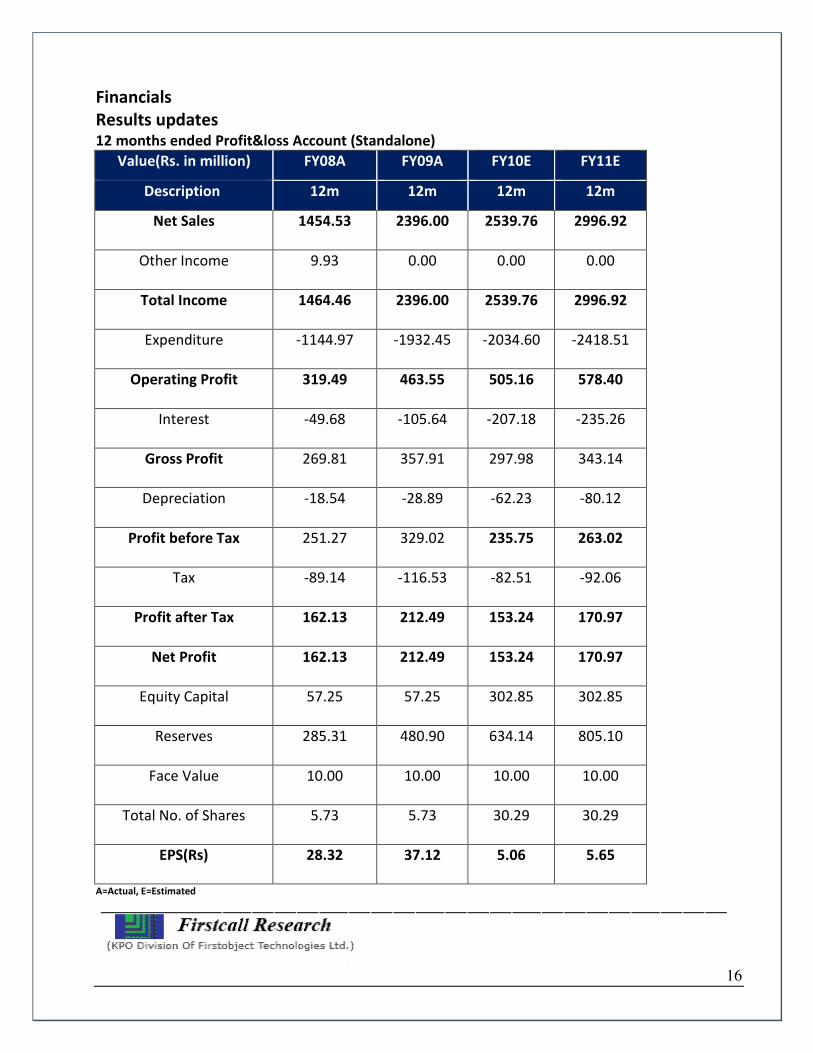

Financials

Results updates 12 months ended Profit&loss Account (Standalone)

Value(Rs. in million) FY08A FY09A FY10E FY11E

Description 12m 12m 12m 12m

Net Sales 1454.53 2396.00 2539.76 2996.92

Other Income 9.93 0.00 0.00 0.00

Total Income 1464.46 2396.00 2539.76 2996.92

Expenditure -1144.97 -1932.45 -2034.60 -2418.51

Operating Profit 319.49 463.55 505.16 578.40

Interest -49.68 -105.64 -207.18 -235.26

Gross Profit 269.81 357.91 297.98 343.14

Depreciation -18.54 -28.89 -62.23 -80.12

Profit before Tax 251.27 329.02 235.75 263.02

Tax -89.14 -116.53 -82.51 -92.06

Profit after Tax 162.13 212.49 153.24 170.97

Net Profit 162.13 212.49 153.24 170.97

Equity Capital 57.25 57.25 302.85 302.85

Reserves 285.31 480.90 634.14 805.10

Face Value 10.00 10.00 10.00 10.00

Total No. of Shares 5.73 5.73 30.29 30.29

EPS(Rs) 28.32 37.12 5.06 5.65

A=Actual, E=Estimated

17

Quarterly ended Profit & Loss Account (Standalone)

Value(Rs. in million) 31-Mar-09 30-Jun-09 30-Sep-09 30-Dec-09E

Description 3m 3m 3m 3m

Net Sales 859.72 528.38 586.83 674.85

Other Income 0.00 0.00 0.00 0.00

Total Income 859.72 528.38 586.83 674.85

Expenditure -683.85 -451.65 -456.37 -526.39

Operating Profit 175.87 76.73 130.46 148.47

Interest -38.33 -25.42 -59.46 -61.15

Gross Profit 137.54 51.31 71.00 87.32

Depreciation -10.21 -9.76 -15.48 -18.15

Profit before Tax 127.33 41.55 55.52 69.17

Tax -57.03 -13.00 -14.90 -20.75

Profit after Tax 70.30 28.55 40.62 48.42

Net Profit 70.30 28.55 40.62 48.42

Equity Capital 57.25 57.25 302.85 302.85

Face Value 10.00 10.00 10.00 10.00

Total No. of Shares 5.73 5.73 30.29 30.29

EPS(Rs) 12.28 4.99 1.34 1.60

18

Key Ratios:

Particulars FY09A FY10E FY11E

Equity Capital (Rs.mn.) 57.25 302.85 302.85

EBDITA Margin (%) 19.35% 19.89% 19.30%

Net Profit Margin (%) 8.87% 6.03% 5.70%

P/E (x) 1.82 17.79 15.94

ROE (%) 39.49% 16.35% 15.43%

ROCE (%) 27.52% 24.53% 25.12%

EV/EBDITA(x) 0.84 6.89 6.54

Book Value (Rs.) 93.92 30.94 36.58

P/BV (x) 0.72 2.91 2.46

Debt-Equity ratio(x) 2.33 1.47 1.37

19

Charts

A) Net sales & PAT Chart

B) EV/EBITDA (x) chart

20

C) P/E(X) Chart

D) Debt-Equity ratio(X) chart

21

1 Year Comparative Graph

TIL BSE SENSEX

Outlook and Conclusion

• At the current market price of the stock Rs.90.00, the stock trades at a P/E of 17.79 x and 15.94x

for FY10E and FY11E respectively.

• The EPS of the stock is expected to be at Rs.5.06 and Rs.5.65 for the earnings of FY10E and FY11E

respectively.

• The top line and bottom line of the company are expected to growth a CAGR of 27.25% and

1.78% over FY08 to FY11E.

• On the basis of EV/EBDITA, the stock trades at 6.89 x and 6.54 x for FY10E and FY11E

respectively.

• Price to Book Value of the stock is expected to be at 2.91 x for FY10E and 2.46 x for FY11E.

• Rapid induction of new consumers along with increasing urbanization will accelerate the

company’s future growth.

• The company focused on not just growing volumes, but increasingly positioning itself in the

higher priced segments of the market.

22

• The company is strongly positioned in the Indian alcoholic beverages market, as a result of its

impressive performance for the last couple of years and the consistent quality and acceptability

of its brands, most of which are segment leaders.

• Investments in equipments, expanding capacities, product diversification and line extensions are

part of their constant drive to push the benchmarks.

• The Indian Made Foreign Liquor Segment is a 125 million cases industry that is worth US$ 2

billion. The IMFL segment constitutes 31 % of the total liquor market. The IMFL is expected to

grow at a CAGR of 9.7%.

• The Company is also planning to commission grain based ENA Plant with the capacity of 100

KLPD by end of the calendar year.

• The company offers a strong outlook for the coming years, based on its multi-pronged strategy

of increased manufacturing bandwidth, greater geographical reach, supplemented by

introduction of new products and a strong marketing focus on its existing brands.

• Today TI’s brand portfolio consists of unique and diverse brands that enjoy excellent consumer

preference solely due to their quality and value for money.

• The company remains committed to expand profit margins, achieve robust growth going

forward and increase its footprints globally.

• We recommend ‘HOLD in this particular scrip with a target price of Rs.110.00 for Medium to

Long term investment.

23

Industry Overview

The Indian alcoholic beverages industry is poised for a rapid growth in both value and volume

terms in the times to come. The Indian alcoholic beverages industry is at its tipping point now, with

high growth rates, across the entire spectrum of price points and categories. With more and more

consumers (men and women) getting added into the alcohol consumption base every year, and

with the rising disposable income of these consumers, the premium brands are doing exceedingly

well and consequently, the Industry as a whole has begun to take strategic marketing of alcoholic

beverage and its distribution much more seriously.

The Indian alcoholic drinks market generated total revenues of $12.9 billion in 2008, representing a

compound annual growth rate (CAGR) of 11.1% for the period spanning 2004-2008. In comparison,

the Chinese and South Korean markets grew with CAGRs of 7.5% and 2.6%, respectively, over the

same period, to reach respective values of $49.2 billion and $14.4 billion in 2008.

Market consumption volumes increased with a CAGR of 8.6% between 2004-2008, to reach a total

of 2.2 billion litres in 2008. The market’s volume is expected to rise to 3.4 billion litres by the end of

2013, representing a CAGR of 8.6% for the 2008-2013 period. Spirits sales proved the most

lucrative for the Indian alcoholic drinks market in 2008, generating total revenues of $9.6 billion,

equivalent to 74.6% of the market’s overall value. In comparison, sales of beer, cider and flavored

alcoholic beverages generated revenues of $3.1 billion in 2008, equating to 23.7% of the market’s

aggregate revenues.

24

Constitution and product segments

However, the optimism stems from the following factors:

• Rapid induction of new consumers along with increasing urbanization will accelerate growth

• Spending on non basic discretionary items and personal consumption to grow at 9-10 % p.a.

• Disposable income to increase at an average of 8.5% p.a. up to 2015

• Working population to rise by 30% by 2013

• 150 million new customers likely to be added totarget consumer group in this decade

Growth Drivers

The Indian Alcoholic Beverages Industry is witnessing high growth traction owing to the following

reasons:

The Favorable Indian Demography

India is best placed demographically, with nearly 485million people in the age group of 20-59 years

in 2001, expected to increase to 636 million by 2011. Greater exposure to western media, lower

inhibitions about consuming alcoholic beverages coupled with the lowest per capita global alcohol

consumption clearly indicates huge potential in the market. These factors are likely to add another

150 million new consumers to the Indian alcoholic beverages industry in the coming years.

25

Rising Disposable Incomes

Economic growth is leading to higher per capita income and the proportion of the ‘consuming class’

is increasing. The average per capita income has increased from US$450 in FY01 to an estimated

US$790 in FY07. It is expected that the growing per capita income will increase disposable incomes

which is expected to outperform the GDP growth and this will lead to an increased consumption of

lifestyle products such as alcoholic beverages.

Improving Regulatory Framework

There has been significant number of changes in the regulatory framework, each of them forward

looking – that of further reforms. Several States have moved away from the practice of auctioning

distribution rights to state controlled distribution to free market, reducing prices by 20-25%

together with improved product quality. Thus boosting demand significantly and increasing the

profit margins of existing players.

___________________________________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation for the purchase

or sale of any financial instrument or as an official confirmation of any transaction. The information

contained herein is from publicly available data or other sources believed to be reliable but we do not

represent that it is accurate or complete and it should not be relied on as such. Firstcall India Equity Advisors

Pvt. Ltd. or any of it’s affiliates shall not be in any way responsible for any loss or damage that may arise to

any person from any inadvertent error in the information contained in this report. This document is provide

for assistance only and is not intended to be and must not alone be taken as the basis for an investment

decision.

26

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

Other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com