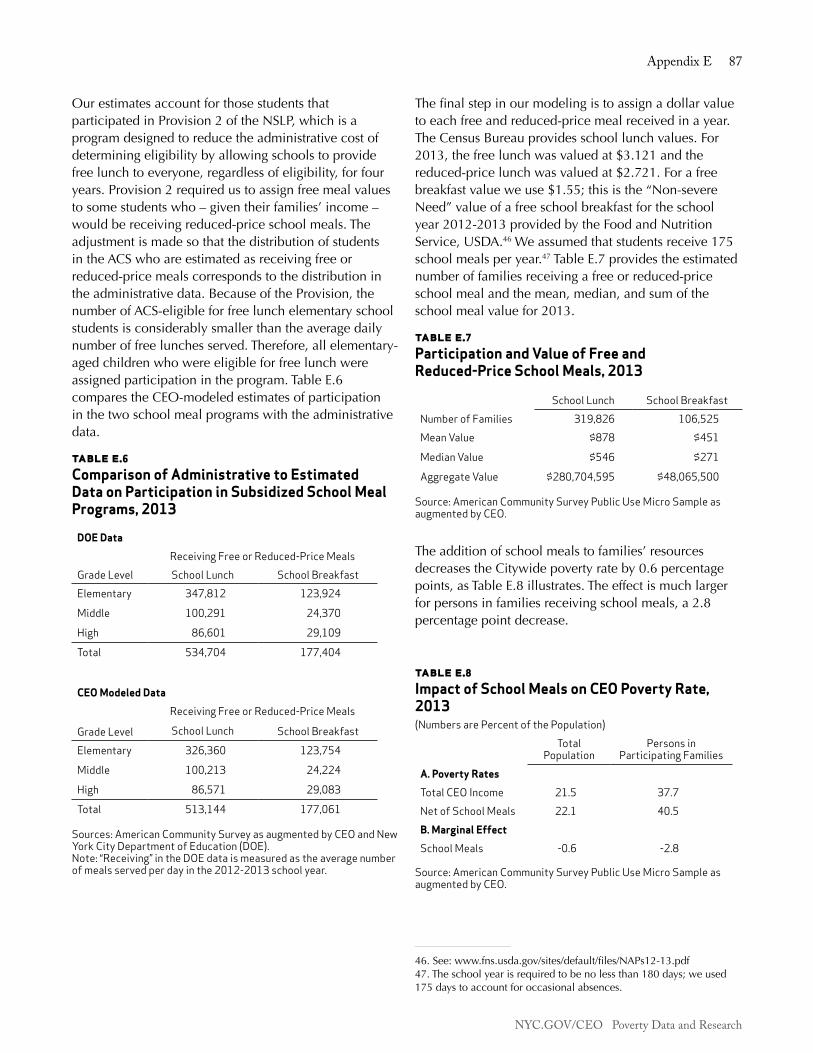

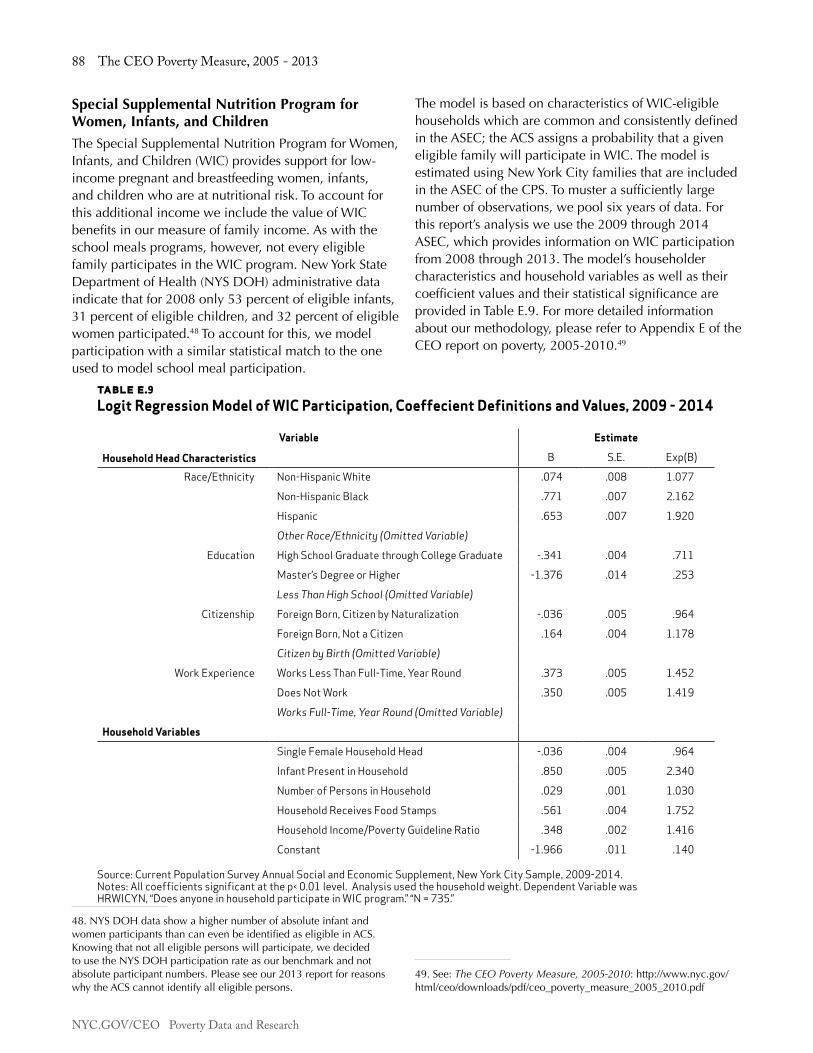

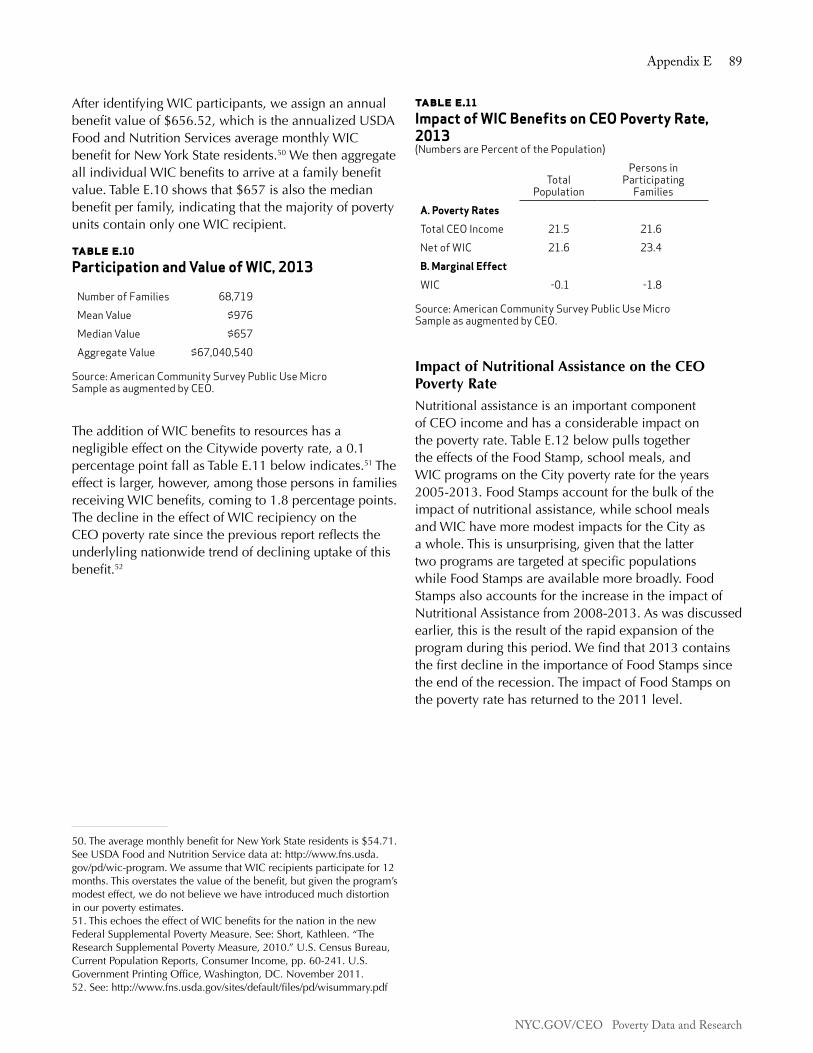

· memorandum to: melissa mark-viverito, speaker, new york city council from: mindy tarlow,...

TRANSCRIPT

MeMoranduM

TO: Melissa Mark-Viverito, Speaker, New York City Council FROM: Mindy Tarlow, Director, Mayor’s Office of Operations DATE: April 22, 2015 SUBJECT: The CEO Poverty Report, 2005 - 2013

I am pleased to submit the annual poverty report on behalf of Mayor de Blasio in accordance with Section 16, Chapter 1 of the New York City Charter.

The report covers the years 2005-2013. The latest data available are from calendar year 2013, representing a two-year lag from present conditions.

The City used methodology that is now mandated by the Charter. The City’s methodology provides an alternative to the official U.S. poverty measure that more fully reflects New York City conditions. The analysis was carried out by the New York City Center for Economic Opportunity (CEO), a part of the Mayor’s Office.

The report finds that CEO poverty rates in New York City rose from 19.0 percent in 2008 to 21.5 percent in 2013. The rate remains statistically unchanged since 2011. By comparison, the official poverty rate rose from 16.8 percent in 2008 to 18.8 percent in 2010, and continued to climb, reaching 19.9 percent in 2013, statistically the same as the 2012 official poverty rate. Although the CEO poverty rate exceeds the official rate, this report finds that a smaller proportion of the City’s population was living in extreme poverty - below 50 percent of the poverty threshold - in 2013. The CEO method estimates this figure at 5.7 percent in 2013 compared to 7.9 percent according to the official method. Conversely, however, our measure finds a larger share of the population was living near poverty – below 150 percent of the respective poverty thresholds - compared to the official measure. The CEO measure puts this figure at 41.1 percent in 2008 and 45.1 percent in 2013 compared to the respective 26.6 percent and 30.6 percent of the official method.

The increase in poverty continues to be notable among workers and working families. The poverty rate for working age adults (persons 18 through 64 years of age) who were employed full-time, year-round, rose by 2.2 percentage points from 2008 to 2013, reaching 8.5 percent in 2013.

This year, concurrent with the publication of this report, the City is releasing One New York: The Plan for a Strong and Just City, or OneNYC, an update of the City’s long-term planning document. For the first time, our long-term plan contains an explicit focus on equity, and a vision for a city with an inclusive, equitable economy that offers well-paying jobs and opportunity for all to live with dignity and security. In both this report and OneNYC we have set a goal of moving 800,000 New Yorkers out of poverty or near poverty in the next ten years. As we describe, one of the most powerful ways to reach this goal is to raise the minimum wage. In his 2015 State of the City address, Mayor de Blasio called for raising the City’s minimum wage to more than $13 an hour next year, and indexing it to inflation to reach $15 an hour in 2019. The City’s own living wage law, signed last year by Mayor de Blasio building on the law previously passed by the City Council, already sets an example at $13.30 per hour without benefits, or $11.90 with benefits, and adjusted to match the Consumer Price Index. Raising the floor on wages is critical for low-income New Yorkers and central to achieving our long-term poverty reduction goal.

Increasing the minimum wage will lower the poverty rate immediately upon implementation. But over the next ten years we need to make the minimum wage only one important step in improving the economic conditions of New Yorkers. The broad set of anti-poverty initiatives described in this report and in OneNYC will also have a significant impact. Workforce development programs that will better train and place New Yorkers in available jobs, educational programs that prepare students for college and career success, affordable and supportive housing programs, social services and broad-based economic growth strategies will lift tens of thousands of New Yorkers out of poverty and near poverty. The Administration is taking a comprehensive approach, from programs that create the fundamental opportunities we aspire to for all residents - high quality early education, access to the internet, municipal identification that opens doors to critical civic services - to those that make living in New York City more affordable.

In all of this work, the City will be promoting evidence-based, data-driven approaches to reducing poverty and income inequality. We are committed to designing initiatives based on solid research, conducting rigorous evaluations – and only continuing those with proven records of success.

We look forward to working in partnership with the City Council on reducing poverty and increasing opportunity for all New Yorkers.

The CEO Poverty Measure, 2005 - 2013

An Annual Report from the Office of the Mayor

April 2015

Table of ConTenTs

PREFACE AND ACKNOWLEDGMENTS ............................................................................................. i

EXECUTIVE SUMMARY ................................................................................................................... iii

1. INTRODUCTION ......................................................................................................................... 1 1.1 The Need for an Alternative to the Official Poverty Measure .............................................. 1 1.2 The National Academy of Sciences’ Alternative ................................................................. 2 1.3 The Supplemental Poverty Measure ................................................................................... 2 1.4 CEO’s Adoption of the NAS/SPM Method .......................................................................... 3 1.5 Comparing Poverty Rates ................................................................................................... 5 1.6 The New York City Labor Market ........................................................................................ 6 1.7 Key Findings in This Report ................................................................................................ 9

2. POVERTY IN NEW YORK CITY, 2005 - 2013 .............................................................................. 11 2.1 New York City Poverty Rates, 2005 - 2013 ....................................................................... 11 2.2 The Depth of Poverty and Extent of Near Poverty ............................................................. 16 2.3 The Effect of Non-Cash Resources on the CEO Poverty Rate............................................. 18

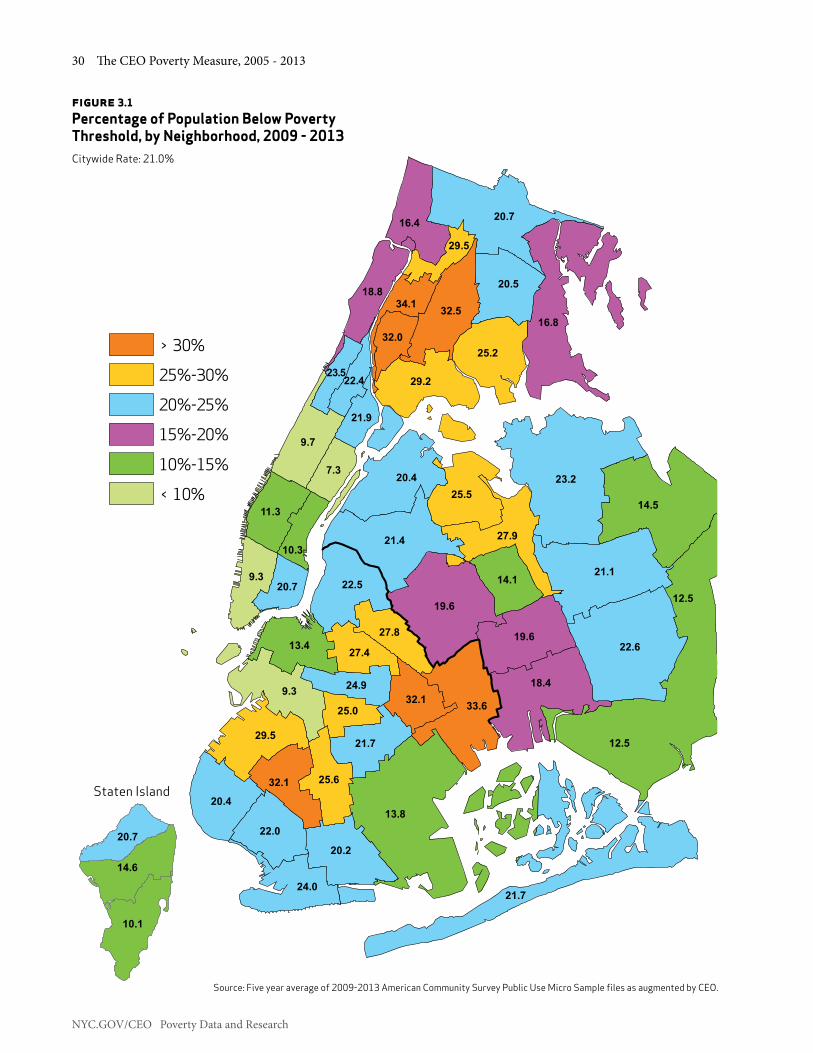

3. CEO POVERTY RATES IN DEMOGRAPHIC DETAIL, 2005 - 2013 .............................................. 23 3.1 Poverty Rates by Demographic Characteristic of the Individual ........................................ 23 3.2 Poverty Rates by Family Characteristic ............................................................................. 26 3.3 Poverty Rates by Borough ................................................................................................ 29 3.4 Poverty Rates by Neighborhood ....................................................................................... 29 3.5 A Closer Look at Some Patterns in the Data ..................................................................... 32

4. ALTERNATIVE POVERTY MEASURES IN THE U.S. AND NEW YORK CITY ................................. 37 4.1 Poverty Rates by Age Group ............................................................................................ 37 4.2 Extreme Poverty and Near Poverty ................................................................................... 38 4.3 Changes in the SPM and CEO Poverty Rates, 2009 - 2013 ............................................... 39

5. POLICY AFFECTS POVERTY, ADDITIONAL DATA AND FUTURE DIRECTIONS ......................... 41 5.1 Lifting 800,000 New Yorkers Out of Poverty in the Next 10 Years ..................................... 41 5.2 The City’s Approach to Poverty ......................................................................................... 42 5.3 Looking Forward .............................................................................................................. 43 5.4 Ongoing Programs ........................................................................................................... 47 5.5 In Conclusion .................................................................................................................. 51

APPENDIX A: THE POVERTY UNIVERSE AND UNIT OF ANALYSIS ............................................... 55 APPENDIX B: DERIVING A POVERTY THRESHOLD FOR NEW YORK CITY .................................. 58 APPENDIX C: ADJUSTMENT FOR HOUSING STATUS .................................................................. 63 APPENDIX D: THE CEO TAX MODEL ............................................................................................. 73 APPENDIX E: ESTIMATING THE VALUE OF NUTRITIONAL ASSISTANCE ...................................... 81 APPENDIX F: ESTIMATING THE VALUE OF HEAP BENEFITS ......................................................... 91 APPENDIX G: WORK-RELATED EXPENSES .................................................................................... 93 APPENDIX H: MEDICAL OUT-OF-POCKET EXPENDITURES .......................................................... 99 APPENDIX I: THE EFFECT OF A MINIMUM WAGE INCREASE ON THE POVERTY RATE ............. 104 APPENDIX J: ACCURACY OF THE DATA AND CHANGES TO THE CEO MODEL ........................ 107

Preface and Acknowledgments i

NYC.GOV/CEO Poverty Data and Research

PrefaCe and aCknowledgMenTs

This is the second issue of the New York City Poverty Report since the New York City Charter was revised in December 2013, requiring the Mayor to issue an annual report on poverty in the City. It is also the second report on poverty issued by Mayor Bill de Blasio. The Charter mandates that the report contain data describing the city’s strategy and resources aimed at alleviating poverty. This year we continue that narrative and link our poverty strategy to programs described in One New York: The Plan for a Strong and Just City (OneNYC), an update to the City’s long-term plan, released concurrent with this report.

The poverty measure has its origins in 2006, when a Commission on Economic Opportunity was convened to craft innovative approaches to reducing poverty in the City. The Commissioners soon learned what social scientists have known for decades: the nation’s fifty-year-old measure of poverty no longer provides useful information. In the 1960s, the poverty measure was a focal point for the nation’s growing concern about poverty. Over the decades, society evolved and policies have shifted, but the official poverty measure remains frozen in time. As a result, it has steadily lost credibility and usefulness as a social indicator. The Commissioners concluded that, along with new programs, the City needed to develop a new measure of poverty. The development of an improved measure of poverty became a goal of the New York City Center for Economic Opportunity (CEO), tasked with implementing the Commission’s recommendations.

There has been no shortage of proposals for improving the way America counts its poor. The most influential of these was developed, at the request of Congress, by the National Academy of Sciences (NAS). Although the NAS’s proposal was issued in 1995, neither the Federal nor any other branch of government had adopted this approach until 2008 when we released our first working paper on poverty in New York City. This study – our seventh – continues our practice of issuing annual updates of our measure.

The CEO poverty measure has become an important resource for how we think about poverty in New York City. We have gained a better estimate of the rate of poverty - what portion of the city is poor and near poor; the extent to which some anti-poverty programs lower the poverty rate; and a demographic and economic profile of New Yorkers in poverty. This data-backed understanding of the nature of poverty is now the first

step in a progressive framework for addressing poverty as initiated by the de Blasio administration. We identify and implement solutions based on the growing body of evaluation data and then continue to monitor and measure the effectiveness of these solutions. Successful outcomes will be judged as those that address income inequality and inequality in access to critical services.

The need for an alternative poverty measure is seen in the increasing interest in a new measure. In recent years, New York City has been joined by other state and local poverty measurement initiatives. To date, NAS-style, state-level poverty measures have been developed for New York, Connecticut, Georgia, Illinois, Massachusetts, Minnesota, Wisconsin, California, and the city (and metro area) of Philadelphia. In addition, longitudinal estimates for the U.S. have been developed by the Population Research Center at Columbia University. All these projects have been enormously helpful to our work. We have benefited from the wisdom of many: Linda Giannarelli, Laura Wheaton, and Sheila Zedlewski at the Urban Institute; Julia Isaacs and Timothy Smeeding at the University of Wisconsin’s Institute for Research on Poverty.

In 2011, the U.S. Bureau of the Census began releasing annual reports on poverty in the United States using a new Supplemental Poverty Measure, which is also based on the NAS recommendations. To enhance the commensurability of our work with the new Federal measure, CEO revised some elements of our approach. Our colleagues at the Census Bureau, David Johnson, Kathleen Short, and Trudi Renwick, as well as Thesia Garner at the Bureau of Labor Statistics – friends of the CEO project since its inception – have been particularly helpful in this work.

From the earliest stages of our effort, we have benefited from opportunities to present our work to other scholars and policy practitioners. The Brookings Institute’s Center on Children and Families hosted a number of meetings, some at CEO’s request, where many of the nation’s leading poverty experts not only shared their work, but offered us advice for improving our measure. We need to recognize the generosity of Ron Haskins, the Center’s Co-Director, as well as the wisdom of those who have attended these events. CEO has also presented our work at a number of conferences, including annual meetings of the Association for Public Policy and Management, the National Association for Welfare Research and Statistics, the American Statistical Association, the International Association for Research in Income and Wealth, and the Administration for Children and Families’ Welfare

NYC.GOV/CEO Poverty Data and Research

ii The CEO Poverty Measure, 2005 - 2013

Research and Evaluation Conference. Thanks to a grant from the RIDGE Center for National Food and Nutrition Assistance Research at the University of Wisconsin’s Institute for Research on Poverty, we were able to present our work on valuing Food Stamp benefits to experts in this field. In the course of all this we have amassed a considerable debt. In addition to those mentioned above, we wish to acknowledge Jessica Banthin, Richard Bavier, David Betson, Rebecca Blank, Gary Burtless, Constance Citro, Sharon O’Donnell, Rachel Garfield, Irv Garfinkel, Mark Greenberg, Amy O’Hara, Nathan Hutto, John Iceland, Dottie Rosenbaum, Isabelle Sawhill, Karl Scholz, Arloc Sherman, Sharon Stern, Jane Waldfogel, Christopher Wimer and James Ziliak.

Closer to home, Dr. Joseph Salvo, Director of the Population Division at New York City Department of City Planning has made several important contributions. Many other colleagues in City government have shared their expertise about public policy, the City’s administration of benefit programs, and agency-level data: Adam Hartke at MTA; Jay Fiegerman, Metro North Railroad; Patricia Yang, Director of Health Policy, NYC Mayor’s Office; Kent Cherny, NYC Office of Management and Budget; Tracey Thorne, Kevin Fellner, Audrey Diop, and Joanne Bailey at the City’s Human Resources Administration helped us understand several benefits programs, and also to Hildy Dworkin, librarian at the Human Resources Administration, for her continuing support. Thanks are due to Dave Hall and the staff at the HRA print shop; Erin Shigaki at Purple Gate Design; and Eileen Salzig for their help in producing this document.

Staff at other government agencies that also assisted us include: Grace Forte-Fitzgibbon, Long Island Railroad; Robert Hickey, Office of Management and Budget; Jessica Semega, Housing and Household Economic Statistics Division, U.S. Bureau of the Census; Mahdi Sundukchi, Demographic Statistical Methods Division, U.S. Bureau of the Census; and Lynda Laughlin, Social, Economic and Housing Statistics Division, U.S. Bureau of the Census.

Over the years we have also amassed a considerable debt to past and present CEO colleagues, including Mark Levitan, Daniel Scheer and Todd Seidel original members of the Poverty Research Unit; Carson Hicks, Deputy Executive Director of CEO, Emily Apple, Diego Benitez, Sarah Bennett, David Berman, Brigit Beyea, Jean-Marie Callan, Kate Dempsey, Emily Firgens, Patrick Hart, Blair Hewes, Sinead Keegan, Minden Koopmans, Parker Krasney, Ada Rehnberg-Campos, and Shammara Wright

were especially generous in sharing their time, space, and able assistance this year.

Adam Cohen, Tina Chiu and Stephanie Puzo of the Mayor’s Office of Operations helped bring this document to completion. Matthew Klein, Executive Director of CEO and Senior Advisor in the Office of Operations, was indispensable in his guidance.

The Center for Economic Opportunity since 2014 has operated as a unit within the Mayor’s Office of Operations. Mindy Tarlow, Director of Operations, provides both visionary leadership and engaged support on the details of our work, and we are grateful for her expertise and commitment to our research.

This report was authored by John Krampner, Danny Silitonga, Jihyun Shin, and Vicky Virgin, along with myself.

Christine D’Onofrio, Ph.D. Director, CEO Poverty Research Unit On behalf of the New York City Center for Economic Opportunity and the Mayor’s Office of Operations.

CEO POVERTY RESEARCH UNIT 253 Broadway, 14th floor New York, NY 10038 Christine D’Onofrio: [email protected] John Krampner: [email protected] Danny Silitonga: [email protected] Jihyun Shin: [email protected] Vicky Virgin: [email protected]

desi

gn: w

ww.

pur

pleg

ated

esig

n.co

m

Executive Summary iii

NYC.GOV/CEO Poverty Data and Research

exeCuTive suMMary

In December 2013, the New York City Charter was revised, requiring the Mayor to issue an annual report on poverty in the City. The Charter specifically requires that the report be based on the poverty measure developed by the New York City Center for Economic Opportunity (CEO). The purpose is to provide policymakers and the public with a more informative alternative to the 50-year-old official U.S. poverty measure and present current anti-poverty initiatives. This is the second report released under the new mandate. It includes data from 2005 to 2013, the most recent years for which data are available. The report finds that there has been no significant change in the poverty rate since 2011, when the City first began to recover from the Great Recession. Lowering the poverty rate is central to new initiatives across the policy spectrum.

In 2013, 21.5 percent of the New York City population was living below the CEO poverty line. This rate is statistically unchanged from the two prior years. The poverty rates for 2011, 2012 and 2013 are 21.5, 21.4 and 21.5 percent, respectively. In 2013, 45.1 percent of the New York City population was living below 150 percent of the CEO poverty line, meaning they were in poverty or near poverty.

Changes in the CEO poverty rate have closely matched trends in employment and earned income in the City. The poverty rate fell from 2005 to 2008, to 19.0 percent, when the local economy was expanding. The

Great Recession began in 2008. By 2010 the poverty rate rose to 21.0 percent and reached a cyclical peak of 21.5 percent in 2011. The post-recession growth in employment and earnings stopped any further increases in the poverty rate, but the recovery has yet to gather sufficient strength to move the poverty rate towards its pre-recession level.

Figure 1 illustrates the trend in the CEO poverty rate. It is paralleled by the movement in the official poverty rate. This on-the-surface similarity, however, masks many important differences between the two poverty measures. The first part of this Executive Summary reviews those differences.

We then turn to the economic and public policy context that has shaped recent trends in the poverty rate. The next section identifies the report’s key findings. In the final section we describe the current policy framework and initiatives for addressing poverty as defined in this report.

The Official Poverty MeasureThe official U.S. poverty measure was developed in the early 1960s. Its threshold was based on the cost of the U.S. Department of Agriculture’s Economy Food Plan, a diet designed for “temporary or emergency use when funds are low.” Because the survey data available at the time indicated that families typically spent a third of their income on food, the cost of the plan was simply multiplied by three to account for other needs. Since the threshold’s 1963 base year, it has been updated annually

figure 1Official and CEO Poverty Rates, 2005 - 2013

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Note: Official poverty rates are based on the CEO poverty universe and unit of analysis.

Perc

ent o

f the

Pop

ulat

ion

2005 2006 2007 2008 2009 2010 2011 2012 2013

Official CEO

12

14

16

18

20

22

24

18.317.9

16.8 16.8 17.3

18.819.3 19.9

21.021.5 21.5

20.0

21.4

19.819.0

19.819.820.4

NYC.GOV/CEO Poverty Data and Research

iv The CEO Poverty Measure, 2005 - 2013

by the change in the Consumer Price Index.1

A half century later, this poverty line has little justification. The threshold does not represent contemporary spending patterns; food now accounts for less than one-seventh of family expenditures, and housing is the largest item in the typical family’s budget. The official threshold also ignores differences in the cost of living across the nation, an issue of obvious importance to measuring poverty in New York City. A final shortcoming of the threshold is that it is frozen in time. Since it only rises with the cost of living, it assumes that a standard of living that defined poverty in the early 1960s remains appropriate, despite advances in the nation’s standard of living since that time.

The official measure’s definition of the resources that are compared against the threshold is pre-tax cash income. This includes wages, salaries, and earnings from self-employment; income from interest, dividends, and rents; and some of what families receive from public programs if they take the form of cash. Thus, payments from Unemployment Insurance, Social Security, Supplemental Security Income, and public assistance are included in the official resource measure.

Given the data available and the policies in place at the time, this was not an unreasonable definition. But over the decades an increasing share of what government programs do to support low-income families takes the form of tax credits (such as the Earned Income Tax Credit) and in-kind benefits (such as Food Stamps). If policymakers or the public want to know how these programs affect poverty, the official measure cannot provide an answer.

1. Fisher, Gordon M. “The Development and History of the Poverty Thresholds.” Social Security Bulletin, Vol. 55, No. 4, Winter 1992.

Measures of Poverty

Official: The current official poverty measure was de-veloped in the early 1960s. It consists of a set of thresh-olds that were based on the cost of a minimum diet at that time. A family’s pre-tax cash income is compared against the threshold to determine whether its mem-bers are poor.

NAS: At the request of Congress, the National Academy of Sciences issued a set of recommendations for an improved poverty measure in 1995. The NAS threshold represents the need for clothing, shelter, and utilities, as well as food. The NAS income measure accounts for taxation and the value of in-kind benefits.

SPM: In March 2010 the Obama Administration an-nounced that the Census Bureau, in cooperation with the Bureau of Labor Statistics, would create a Supple-mental Poverty Measure based on the NAS recommen-dations, subsequent research, and a set of guidelines proposed by an Interagency Working Group. The first report on poverty using this measure was issued by the Census Bureau in November 2011.

CEO: The Center for Economic Opportunity released its first report on poverty in New York City in August 2008. CEO’s poverty measure is largely based on the NAS recommendations, with modifications based on the guidelines from the Interagency Working Group.

The National Academy of Sciences’ AlternativeDissatisfaction with the official measure prompted Congress to request a study by the National Academy of Sciences (NAS). The NAS’s recommendations for an improved measure were issued in 1995.2 The NAS took a considerably different approach to both the threshold and resource side of the poverty measure. Its poverty threshold reflects the need for clothing, shelter, and utilities, as well as food. It is established by selecting a sub-group of families as reference families,3 calculating their spending on these items and then choosing a point in the resulting expenditure distribution.4 A small multiplier is applied to account for miscellaneous

2. Citro, Constance F. and Robert T. Michael (eds). Measuring Poverty: A New Approach. Washington, DC: National Academy Press. 1995.3. The NAS reference families are those composed of two adults and two children. The threshold for this family is then scaled for families of different sizes and compositions. See Appendix B.4. The NAS suggested that this point lie between the 30th and 35th percentile. Citro and Michael, p.106.

Executive Summary v

NYC.GOV/CEO Poverty Data and Research

expenses such as personal care, household supplies, and non-work-related transportation. The threshold is updated each year by the change in the level of this spending. This connects the threshold to the growth in living standards. In further contrast to the official measure, the NAS proposed that the poverty line be adjusted to reflect geographic differences in housing costs.

On the resource side, the NAS measure is designed to account for the flow of income and in-kind benefits that a family can use to meet the needs represented in the threshold. This creates a much more inclusive measure of income than pre-tax cash. The tax system and the cash-equivalent value of in-kind benefits for food and housing create important additions to family resources. But families also have non-discretionary expenses that reduce the income available to meet their other needs. These include the cost of childcare, commuting to work, and medical care that must be paid for out of pocket. This non-discretionary spending is accounted for as deductions from income.

The NAS report sparked further research and garnered widespread support among poverty experts.5 However, neither the Federal nor any state or local government had adopted the NAS approach until CEO’s initial report on poverty in New York City in August 2008.6

More recently the U.S. Bureau of the Census has issued annual reports on poverty using a Supplemental Poverty Measure (SPM). Like CEO’s measure, the Census Bureau’s SPM – first issued in November 2011 – is also shaped by the NAS recommendations, along with a set of guidelines provided by an Interagency Technical Working Group in March 2010.7 Subsequent to the original NAS report, the guidelines incorporated work by researchers at the Census Bureau, the Bureau of Labor Statistics, and others. Many of these recommendations are reflected in our measure.

5. Much of the research inspired by the NAS report is available at: www.census.gov/hhes povmeas/methodology/nas/index.html6. New York City Center for Economic Opportunity. The CEO Poverty Measure: A Working Paper by the New York City Center for Economic Opportunity. August 2008. Available at: www.nyc.gov/html/ceo/ downloads/pdf/final_poverty_report.pdf7. Observations from the Interagency Technical Working Group on Developing a Supplemental Poverty Measure. March 2010. Available at: www.census.gov/hhes/www/poverty/SPM_TWGObservations.pdf

Poverty Thresholds

Official: The official threshold was developed in the early 1960s and was based on the cost of a minimum diet at that time. It is updated each year by the change in consumer prices. It is uniform across the United States.

CEO: The CEO poverty threshold is a New York City-specific threshold derived from the U.S.-wide thresh-old developed for the Federal Supplemental Poverty Measure. The threshold is based on what families spend on basic necessities: food, clothing, shelter, and utilities. It is adjusted to reflect the variation in housing costs across the United States.

Measuring Income

Official Income: The official poverty measure’s defini-tion of family resources is pre-tax cash. This includes income from sources such as wages and salaries, as well as government transfer payments, provided that they take the form of cash. Thus, Social Security benefits are included in this measure, but the value of in-kind ben-efits, like Food Stamps or tax credits such as the Earned Income Tax Credit, are not counted.

CEO Income: Based on the NAS recommendations, CEO income includes all the elements of pre-tax cash plus the effect of income and payroll taxes, as well as the value of in-kind nutritional and housing assistance. Non-discretionary spending for commuting to work, childcare, and out-of-pocket medical care are deduc-tions from income.

CEO’s Adoption of the NAS/SPM MethodCEO bases our New York City-specific poverty threshold on the U.S.-wide threshold developed for the SPM. We adjust the national-level threshold to account for the relatively high cost of housing in New York City by applying the ratio of the New York City to the U.S.-wide Fair Market Rent for a two-bedroom apartment to the housing portion of the threshold.8 In 2013, our poverty line for the two-adult, two-child family comes to $31,156. We refer to this New York City-specific threshold as the CEO poverty threshold. The 2013 official U.S. poverty threshold for the corresponding family was $23,624.

8. Details of the calculation are given in Appendix B.

NYC.GOV/CEO Poverty Data and Research

vi The CEO Poverty Measure, 2005 - 2013

Obviously, if this were the only change CEO had made to the poverty measure, it would lead to a poverty rate higher than the official rate. But, as described above, CEO also uses a far different measure of income to compare against the poverty threshold. Although our measure includes subtractions as well as additions to resources, CEO income is higher than pre-tax cash income at the lower rungs of the income ladder. At the 20th percentile, for example, CEO income was $30,254 in 2013. The corresponding official income figure for pre-tax cash was only $23,364. Thus, if a more complete account of resources had been the only change we had made to the poverty measure, the CEO poverty rate would fall below the official measure. Figure 2 illustrates official and CEO thresholds, incomes, and poverty rates for 2013. The effect of the higher CEO threshold (31.9 percent above the official) outweighs the effect of CEO’s more complete definition of resources (which is 29.5 percent higher, at the 20th percentile, than the official resource measure), resulting in a higher poverty rate. In 2013, the CEO poverty rate stood at 21.5 percent while the official rate was 19.9 percent, a 1.6 percentage point difference.9

To measure the resources available to a family to meet the needs represented by the threshold, our poverty measure employs the Public Use Micro Sample (PUMS) from the Census Bureau’s American Community Survey (ACS) as its principal data set. The advantages of this

9. Differences are taken from unrounded numbers.

survey for local poverty measurement are numerous. The ACS is designed to provide measures of socioeconomic conditions on an annual basis in states and larger localities. It offers a robust sample for New York City (roughly 26,000 households) and contains essential information about household composition, family relationships, and cash income from a variety of sources.

But, as noted earlier, the NAS-recommended poverty measure greatly expands the scope of resources that must be measured in order to determine whether a family is poor. Unfortunately, the ACS provides only some of the information needed to estimate these additional resources. CEO has developed a variety of models that estimate the effect of taxation, nutritional and housing assistance, work-related expenses, and medical out-of-pocket expenditures on total family resources and poverty status. We reference the resulting data set in this report as the “American Community Survey Public Use Micro Sample as augmented by CEO” and we refer to our estimate of family resources as “CEO income.”

This ReportThis report incorporates data through 2013. The focus of this year’s report is on poverty in New York City during the continuing recovery from the Great Recession. From 2008 to 2010, labor market indicators for City residents showed that a declining proportion of the working age population was employed. As Figure 3 illustrates, the share of New Yorkers 18 through 64 years of age who were holding a job at the time they were surveyed peaked in 2008 at 70.8 percent. That proportion declined to 66.4 percent in 2010. By 2013 it had edged back up to 68.4 percent. The trend is positive, but has not reached the pre-recession peak.

Because poverty status is determined by annual income, employment over the course of a year is a particularly useful labor market indicator for understanding trends in the poverty rate. Figure 4 shows that the share of the working age population with steady work, defined as 50 or more weeks in the prior 12 months, declined from 59.8 percent in 2008 to 56.3 percent in 2010, while the proportion of the population that had no work at all grew from 23.5 percent in 2008 to 27.3 percent in 2010. This indicator improved somewhat by 2013. The share of the working age population with year-round work was 57.5 percent, statistically unchanged from 2012. The share of the population with no work fell to 26.0 percent by 2013. The largest change from 2012 to 2013 occurred in

$23,624

OfficialThresholds Incomes Poverty Rates

$23,364

$31,156

CEO Official CEO Official CEO

$30,254

19.9% 21.5%

figure 2 Thresholds, Incomes and Poverty Rates, 2013

Source: U.S. Bureau of the Census and American Community Survey Public Use Micro Sample as augmented by CEO.Notes: Incomes are measured at the 20th percentile and stated in family size and composition-adjusted dollars. Official poverty rates are based on the CEO poverty universe and unit of analysis.

Executive Summary vii

NYC.GOV/CEO Poverty Data and Research

the share of the population with less than full time work, from 15.9 to 16.4 percent.

The decline and then slow increase in weeks worked is reflected in measures of annual earnings. Table 1 reports cost of living (COL) adjusted per family earnings. We focus on those families whose earnings put them near the CEO poverty threshold (between the 25th and 40th percentile of the earnings distribution).10 Table 1 shows that the decline in earnings continued into 2011, even as employment stabilized. The declines range from 20.2 percent to 18.8 percent from 2008 to 2011. The 2013 data indicate an improvement from the prior year, with gains for the 25th percentile greater than gains for groups just above them in the income distribution. But the

10. These earnings data are stated in 2013 dollars using the CEO threshold as a price index.

combined gains from 2011 to 2013 fall short of the earnings lost in the recession.

The job market, we have seen, plays an important role in year-to-year changes in the CEO poverty rate. But its effect takes place within the broader scope of our measure of family resources and the context of public policies intended to bolster family incomes. In addition to earnings, low-income families’ ability to meet their needs is determined by public benefit programs. Over the last several decades there has been an important shift in the composition of these programs, especially for the non-elderly population. As noted above, a smaller proportion of means-tested assistance takes the form of cash payments such as public assistance, while a larger proportion is composed of tax credits and in-kind benefits. The trend has been reinforced by the Bush and

Perc

ent o

f 18-

thro

ugh

64-Y

ear-

Olds

2005 2006 2007 2008 2009 2010

67.068.7 69.3

70.868.2

2012 2013

68.0 68.466.4

2011

67.0

50

55

60

65

70

75

figure 3Employment/Population Ratios, 2005 - 2013

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

0

20

40

60

80

100

Perc

ent o

f 18-

thro

ugh

64-Y

ear-

Olds 23.5

2008

59.8

16.7

2009 2010

24.6 27.3

16.5

56.3

2011

27.0

16.6

56.3

2012 2013

26.4

15.9

57.8

26.0

16.4

57.5

17.1

58.3

At Least 50 Less Than 50 No Weeks

figure 4Weeks Worked in Prior 12 Months, 2008 - 2013

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

NYC.GOV/CEO Poverty Data and Research

viii The CEO Poverty Measure, 2005 - 2013

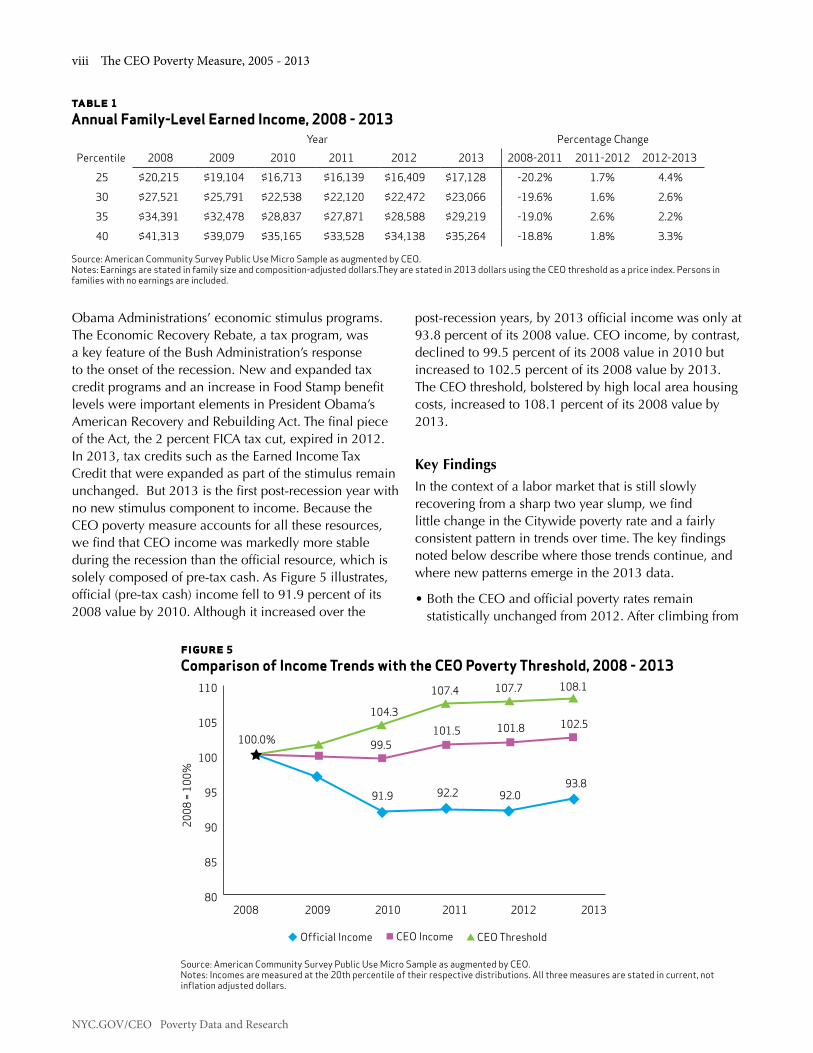

Obama Administrations’ economic stimulus programs. The Economic Recovery Rebate, a tax program, was a key feature of the Bush Administration’s response to the onset of the recession. New and expanded tax credit programs and an increase in Food Stamp benefit levels were important elements in President Obama’s American Recovery and Rebuilding Act. The final piece of the Act, the 2 percent FICA tax cut, expired in 2012. In 2013, tax credits such as the Earned Income Tax Credit that were expanded as part of the stimulus remain unchanged. But 2013 is the first post-recession year with no new stimulus component to income. Because the CEO poverty measure accounts for all these resources, we find that CEO income was markedly more stable during the recession than the official resource, which is solely composed of pre-tax cash. As Figure 5 illustrates, official (pre-tax cash) income fell to 91.9 percent of its 2008 value by 2010. Although it increased over the

post-recession years, by 2013 official income was only at 93.8 percent of its 2008 value. CEO income, by contrast, declined to 99.5 percent of its 2008 value in 2010 but increased to 102.5 percent of its 2008 value by 2013. The CEO threshold, bolstered by high local area housing costs, increased to 108.1 percent of its 2008 value by 2013.

Key FindingsIn the context of a labor market that is still slowly recovering from a sharp two year slump, we find little change in the Citywide poverty rate and a fairly consistent pattern in trends over time. The key findings noted below describe where those trends continue, and where new patterns emerge in the 2013 data.

• Both the CEO and official poverty rates remain statistically unchanged from 2012. After climbing from

table 1Annual Family-Level Earned Income, 2008 - 2013

Year Percentage ChangePercentile 2008 2009 2010 2011 2012 2013 2008-2011 2011-2012 2012-2013

25 $20,215 $19,104 $16,713 $16,139 $16,409 $17,128 -20.2% 1.7% 4.4%

30 $27,521 $25,791 $22,538 $22,120 $22,472 $23,066 -19.6% 1.6% 2.6%

35 $34,391 $32,478 $28,837 $27,871 $28,588 $29,219 -19.0% 2.6% 2.2%

40 $41,313 $39,079 $35,165 $33,528 $34,138 $35,264 -18.8% 1.8% 3.3% Source: American Community Survey Public Use Micro Sample as augmented by CEO. Notes: Earnings are stated in family size and composition-adjusted dollars.They are stated in 2013 dollars using the CEO threshold as a price index. Persons in families with no earnings are included.

104.3

99.5

2008

= 10

0%

2008 2009 2010 2011 2012 2013

Official Income CEO Income CEO Threshold

107.4

101.5

107.7

101.8

108.1

102.5

80

85

90

95

100

105

110

100.0%

91.9 92.2 92.093.8

figure 5Comparison of Income Trends with the CEO Poverty Threshold, 2008 - 2013

Source: American Community Survey Public Use Micro Sample as augmented by CEO. Notes: Incomes are measured at the 20th percentile of their respective distributions. All three measures are stated in current, not inflation adjusted dollars.

Executive Summary ix

NYC.GOV/CEO Poverty Data and Research

0

1

2

3

4

5

6

7

8

9

6.9

7.78.1

Official CEO

5.15.5

7.9

5.75.4

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2012 2013

19.0 percent in 2008 to 21.5 percent in 2011, the CEO poverty rate remained at 21.5 percent in 2013, statistically unchanged from its 2012 level. The official poverty rate rose from 16.8 percent in 2008 to 19.3 percent in 2011 and continued to climb, reaching 19.9 percent in 2013, statistically unchanged from 2012. (See Figure 1.)

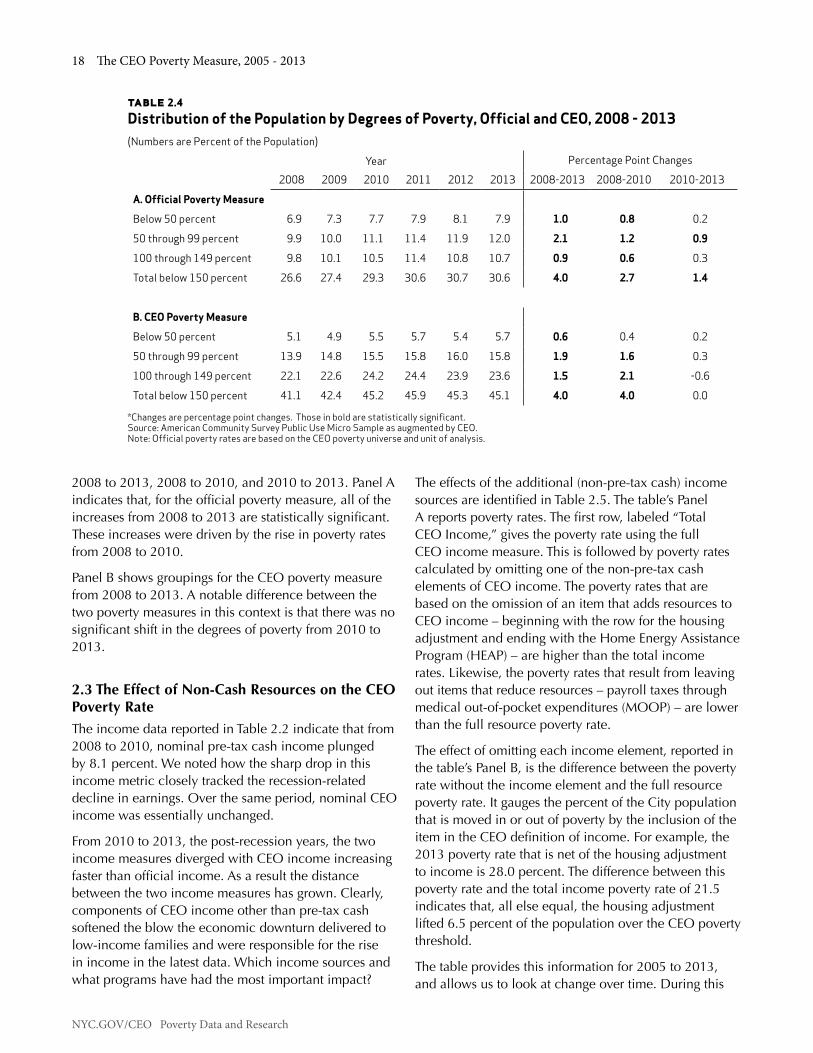

• Although the CEO poverty rate exceeds the official rate in each year for which we have data, the CEO methodology finds that a smaller proportion of the City’s population is living in extreme poverty – below 50 percent of the poverty threshold – than the official method (5.7 percent compared to 7.9 percent in 2013). The CEO extreme poverty rate rose from 5.1 percent in 2008 to 5.7 percent in 2013. The official extreme poverty rate increased from 6.9 percent in 2008 to 7.9 percent in 2013. (See Figure 6.)

figure 6 Share of the Population in Extreme Poverty

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

• The CEO measure categorizes a much larger share of the population as living in “near poverty” – above, but uncomfortably close to the poverty threshold – than the official measure. This is reflected in comparisons of the share of the population that is living below 150 percent of the respective poverty thresholds. In 2013, 45.1 percent of New York City residents were living below 150 percent of the CEO poverty threshold, up from 41.1 percent in 2008. The corresponding shares

for the official measure were 30.6 percent in 2013 and 26.6 percent in 2008. (See Figure 7.)

figure 7 Share of the Population below 150 Percent of the Poverty Threshold

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

• The trend in CEO poverty rates by demographic characteristics such as age, race/ethnicity, nativity/citizenship, and family type generally follows the rise in the Citywide poverty rate from 2008 to 2010 and its statistical stability from 2010 to 2013, with a few exceptions. Looking over the 2008 to 2013 time period, there are statistically significant increases in the poverty rate across nearly every demographic group. Increases in poverty were particularly pronounced for Asians (by 3.6 percentage points to 25.9 percent). Poverty for Asian New Yorkers hit a high of 29.0 percent in 2012, but abated somewhat by 2013. The poverty rate for non-citizens continued to increase (by 6.3 percentage points to 30.7 percent). (See Figures 8 and 9.) There is considerable overlap between these two demographic groups; nearly one-third (30.5 percent) of the City’s Asian population falls into the non-citizen category.

26.629.3 30.7

41.1

45.2 45.3

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2012 2013

Official CEO0

5

10

15

20

25

30

35

40

45

50

30.6

45.1

NYC.GOV/CEO Poverty Data and Research

x The CEO Poverty Measure, 2005 - 2013

figure 8CEO Poverty Rates by Race/Ethnicity

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

figure 9CEO Poverty Rates by Nativity/Citizenship

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

13.215.3

13.8

Non-Hispanic White

Non-Hispanic Black

Non-Hispanic Asian

Hispanic, Any Race

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2012 2013

0

5

10

15

20

25

30

20.8 22.4 22.3 22.4

26.0

29.0

23.5 24.425.8

15.0

22.4

25.9 25.8

0

5

10

15

20

25

30

17.7

Citizen by Birth

20.0 19.3 19.6

Naturalized Citizen Not a Citizen

18.4 18.220.2 19.4

24.4

30.2 30.727.2

Perc

ent o

f the

Pop

ulat

ion

2008 2010 2012 2013

Executive Summary xi

NYC.GOV/CEO Poverty Data and Research

• From 2008 to 2013, poverty rates increased in three of the City’s boroughs. More recent data show different trajectories in the recovery. In some boroughs, 2013 marks a decline from post-recession peaks, in others the poverty rate remains relatively unchanged or is increasing. Brooklyn, with a 22.9 percent poverty rate, saw a decline from its 2010 peak of 24.5 percent; Manhattan, in 2013, reached a post-recession peak of 15.8 percent; the Bronx saw relatively small movements in its poverty rate, from 26.5 percent in 2008 to 27.1 percent in 2013; Queens rose 4.7 percentage points from 16.4 percent in 2008 to 21.1 percent in 2013 (although this represents a full percentage point decline from the peak rate of 22.1 percent in 2012, it was not a statistically significant change); Staten Island, with an increase of 6.7 percentage points from 2008 to 2013 (11.5 percent to 18.2 percent) shows an upward trend in the poverty rate, even when year-to-year comparisons are numerically large but statistically insignificant. (See Figure 10.)

• The relatively large jump in the Queens poverty rate is consistent with its demographic composition. One-half of the City’s Asian population (49.7 percent) lives in Queens and the borough is home to just over one-third (33.8 percent) of New York’s non-citizens. This does represent a small decline from 2012 when Queens was home to 50.2 percent of the City’s Asian population and 32.8 percent of its non-citizens.

• In Staten Island, we find the upward trend in poverty is due to a confluence of factors. The borough, when compared to the rest of the City, has a population that is older on average with lower earnings among full-time workers and more post-recession job loss. The data from 2013 also cover the time period of the aftermath of Hurricane Sandy in late 2012. In the ACS data we cannot directly identify job loss or dislocation due to the hurricane, but consider it a potential contributing factor to the poverty rate. Finally, the Staten Island data consist of a smaller sample than other boroughs. This contributes to large margins of error in the data such that even the difference in the poverty rate from 15.5 percent to 18.2 percent from 2012 to 2013 is not statistically significant.

• The 2008 to 2013 increase in poverty remains particularly pronounced for workers and working families. The poverty rate for working age adults (persons 18 through 64 years of age) who were employed full time, year round rose by 2.2 percentage points from 2008, reaching 8.5 percent in 2013. (See Figure 11.) Over the same time period, poverty rates increased for persons living in families with the equivalent of two full-time, year-round workers, 2.3 percentage points (to 6.1 percent); and one full-time, year-round worker, 2.7 percentage points (to 18.6 percent), respectively. (See Figure 12.) The only statistically significant difference from 2012 was for families with one full-time, year-round worker.

figure 10CEO Poverty Rates by Borough

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

26.5 25.3 26.0 27.1

22.3 22.924.5 23.4

13.515.2 14.9 15.8 16.4

19.9 18.222.1 21.1

11.513.7

15.5

Bronx Brooklyn Manhattan Queens Staten Island

Perc

ent o

f the

Pop

ulat

ion

0

5

10

15

20

25

30

2008 2010 2012 2013

NYC.GOV/CEO Poverty Data and Research

xii The CEO Poverty Measure, 2005 - 2013

• The pattern in poverty rates for the United States based on the new Federal Supplemental Poverty Measure resembles the CEO pattern for New York City. In both the nation and the City, the two NAS-based poverty measures find a higher incidence of poverty than do the official measures. In the U.S., the SPM rate in 2013 was 15.5 percent as opposed to the official rate of 14.6 percent. In New York City, the respective poverty rates

were 21.5 percent (CEO) and 19.9 percent (official) in that year. Because they count the value of non-cash assistance, however, both the SPM and CEO measures of poverty among children are lower than child poverty rates based on the official method: 16.4 percent compared to 20.4 percent for the nation and 24.8 percent rather than 29.1 percent for the City. (See Figures 13 and 14.)

figure 11CEO Poverty Rates by Individual Work Experience

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

6.2 7.1 8.1

22.6 23.6 24.4

36.638.1 39.0

Perc

ent o

f the

Pop

ulat

ion

Full-Time,Year-Round

Some Work No Work0

5

10

15

20

25

30

35

40

4539.1

25.2

8.5

2008 2010 2012 2013

Executive Summary xiii

NYC.GOV/CEO Poverty Data and Research

figure 13 Official and SPM Poverty Rates for the U.S., by Age, 2013

Source: U.S. Bureau of the Census.

figure 12CEO Poverty Rates by Family’s Work Experience

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

3.8 5.0 5.4

12.413.7 14.9 16.0 16.3 17.2

44.4 45.243.4

51.3 51.751.9

Perc

ent o

f the

Pop

ulat

ion

2 Full TimeWorkers

1 Full Time, 1 Part Time

Worker

1 Full TimeWorker

Less than 1 Full Time Worker

No Work0

10

20

30

40

50

60

51.1

44.8

18.613.0

6.1

2008 2010 2012 2013

Total Under 18 18 through 64 65 and Older

Perc

ent o

f the

Pop

ulat

ion

14.615.5

20.4

16.4

13.615.4

9.5

14.6

0

5

10

15

20

25

Official SPM

NYC.GOV/CEO Poverty Data and Research

xiv The CEO Poverty Measure, 2005 - 2013

Perc

ent o

f the

Pop

ulat

ion

19.921.5

29.1

24.8

17.1

20.418.6

21.6

Total Under 18 18 through 64 65 and Older

Official CEO

0

5

10

15

20

25

30

35

figure 14 Official and CEO Poverty Rates for New York City, by Age, 2013

Source: American Community Survey Public Use Micro Sample as augmented by CEO.

Executive Summary xv

NYC.GOV/CEO Poverty Data and Research

Poverty and Policy: Lifting 800,000 New Yorkers Out of Poverty in the Next 10 YearsMayor de Blasio came into office with a commitment to reducing poverty. This year’s poverty report shows that there is considerable work to do. It finds that fully 45.1 percent of New Yorkers lived in poverty or near poverty (below 150 percent of the poverty threshold) in 2013. It also finds that there was no significant change in the official or CEO poverty rate from 2012 to 2013 – and that earnings remain below pre-recession levels.

This year, the City is stating a significant commitment to address poverty. This report is being published concurrently with the City’s release of One New York: The Plan for a Strong and Just City, or OneNYC, an update of the City’s long-term planning document. In both this report and OneNYC we set a target of moving 800,000 New Yorkers out of poverty or near poverty in the next ten years.

Raising the floor on wages is central to achieving our poverty reduction goal. In his 2015 State of the City address, Mayor de Blasio called for raising the City’s minimum wage to more than $13 an hour next year, and indexing it to inflation to reach $15 an hour by 2019. To model the effect if the minimum wage were $15 an hour in 2013, we simulated a $15 wage on 2013 minimum wage earners, and find that approximately 748,000 fewer people would be poor or near poor.11 This, combined with the City’s ongoing anti-poverty initiatives, establishes our goal to move 800,000 people out of poverty or near poverty.

Nearly half of the goal can be reached through steps that are within the City’s control or have been proposed by others. The minimum wage is already scheduled to rise to $9 an hour on January 1, 2016. A further increase to $11.50 has been proposed by New York’s Governor. These increases would move over 310,000 people out of poverty or near poverty in our estimates.

Increasing the minimum wage will lower the poverty rate immediately upon implementation. But over the next ten years we need to make the minimum wage only one important step in building economic opportunity. Concrete initiatives described in this report and in OneNYC will also have a significant impact. Workforce development programs that will create career pathways for New Yorkers at all skill levels, educational programs that prepare students for college and career success, affordable and supportive housing programs, social

11. For the methodology and assumptions of this model, and other calculations in this section, see Chapter 5 and Appendix I.

services, and broad-based economic growth strategies will lift tens of thousands more New Yorkers out of poverty or near poverty.

As we fight to raise the minimum wage we are also implementing other anti-poverty strategies that create the foundation to enable opportunities we aspire to for all residents: from high-quality early education, access to the internet, identification that opens doors to critical civic services, to those that make living in New York more affordable.

The effect of these three steps – the existing increase in the minimum wage to $9 an hour, the enactment of the Governor’s proposed further minimum wage increase, and the agenda set forth in the OneNYC plan – would together lift 400,000 New Yorkers out of poverty or near poverty, halfway to our goal.

The City is committed to using evidence-based, data-driven, cost-effective methods. Our framework calls for examining the relevant data closely, adopting evidence-based solutions, and rigorously evaluating the performance of our own initiatives.

This approach has guided our work over the past year. Our prior poverty report highlighted two notable findings: high and rising poverty rates among noncitizens and rising poverty among New Yorkers working full time. This administration took a significant step in addressing the first finding by launching IDNYC, the nation’s largest municipal ID program. IDNYC is a program for all New Yorkers that particularly helps unauthorized City residents by providing access to important government and private services. We addressed the second with a focus on workforce activities, including launching the Jobs for New Yorkers Task Force, which produced evidence-based recommendations in the Career Pathways report that are now being put into practice. The City’s new workforce development approach will complement the programmatic and policy changes already made by the Human Resources Administration and Department of Small Business Services to help New Yorkers prepare for and find higher-paying jobs.

Efforts to address poverty and increase opportunity extend throughout the administration. They include the historic expansion of pre-kindergarten, preserving and building affordable housing, working to connect more people to benefits for which they are eligible, and continuing to enhance the City’s health and human services, including those for our most senior residents, to name just a few.

NYC.GOV/CEO Poverty Data and Research

xvi The CEO Poverty Measure, 2005 - 2013

We will build on this work in the coming year. The City is working to make affordable or free high-speed internet – a critical service in this digital age – available to low-income New Yorkers, with a variety of cutting-edge programs, including LinkNYC, which will replace the City’s payphones with up to 10,000 kiosks with free, high-speed internet service.

The City is putting a particular emphasis on initiatives that help low-income New Yorkers to graduate from college. As one example, we have increased funding to the City University of New York’s Accelerated Study in Associate Programs (CUNY ASAP), which has a proven track record of significantly increasing student graduation rates.

We expect “Pre-K for All” to make full-day, high quality pre-K available to every four-year-old in the City. There is robust evidence that children in pre-K have better employment and life outcomes, and the availability of pre-K helps parents to reenter the workforce to support their families.

Looking forward, the commitment to addressing poverty and inequality will continue to be central to the City’s work. The goals and initiatives set out in OneNYC’s long-term plan include broad-based economic development, public health efforts, inclusive workforce strategies, targeted hiring connected with our investments, and an ongoing pledge to strengthen our neighborhoods and help all New Yorkers access services that provide gateways to opportunity. With the release of OneNYC, the City has entered a new era in fighting poverty and inequality. We have committed to making equity issues a key part of all of our planning – and to lifting 800,000 New Yorkers out of poverty or near poverty. Our goal is an inclusive, equitable City, with opportunity, dignity, and security for all.

Chapter 1: Introduction 1

NYC.GOV/CEO Poverty Data and Research

ChaPTer 1: inTroduCTion

This is the sixth release of CEO’s alternative poverty measure for New York City. We now have data covering the time span of 2005-2013, dating back to the inception of the American Community Survey, our primary data source. Over the economic expansion and subsequent Great Recession we have provided a unique perspective on poverty as incomes rose and then fell. During the recession we measured the impact of income support programs. Since the recession’s official end in 2010 and the ensuing modest recovery, we have measured poverty amid growing employment but stagnant wages.

This chapter establishes the context for our findings. It begins with an overview of the reasons why CEO developed a new measure of poverty and a description of our alternative measure. Because trends in poverty are so closely associated with economic conditions, the second part of the Introduction moves the discussion from methodology to trends in the local labor market. The Introduction’s final section summarizes the report’s principal findings.

1.1 The Need for an Alternative to the Official Poverty MeasureIt has been over a half century since the development of the current official measure of poverty. In the early 1960s the measure represented an important advance, serving as a focal point for the public’s growing concern about poverty in America. But over the decades, discussions about poverty have increasingly included criticism of how poorly it was being measured. Society has evolved and public policy has shifted, yet the Census Bureau has been measuring poverty as if nothing had changed. This still widely used indicator is now sorely out of date.

The official poverty measure is income-based. All such measures must answer two key questions. First, how much is enough? The answer to this question gives us the income threshold (the poverty line) that separates the poor from the non-poor. The second question is, how much of what? Which resources available to families should be counted as income to meet their needs and compared against the poverty thresholds?

The official measure’s threshold, developed in the early 1960s, was based on the cost of the U.S. Department of Agriculture’s Economy Food Plan, a diet designed for “temporary or emergency use when funds are low.” Because the survey data available at the time indicated that families typically spent a third of their income on food, the cost of the plan was simply multiplied by three to account for other needs. Since the threshold’s 1963 base year, it has been updated annually by the change in the Consumer Price Index.12

A half century later, this poverty line has little justifi–cation. The threshold does not represent contemporary spending patterns. Food now accounts for less than one-seventh of family expenditures. Housing is the largest item in the typical family’s budget. The official threshold also ignores differences in the cost of living across the nation, an issue of obvious importance when measuring poverty in New York City. A final shortcoming of the threshold is that it is frozen in time. Since it only rises with the cost of living, it assumes that a standard of living that defined poverty in the early 1960s remains appropriate, despite advances in living standards since that time.

The official measure’s definition of the resources that are compared against the threshold is pre-tax cash. This includes wages, salaries, and earnings from self-employment; income from interest, dividends, and rents; and some of what families receive from public programs, if they take the form of cash. Thus, payments from Unemployment Insurance, Social Security, Supplemental Security Income (SSI), and public assistance are included in the official resource measure.

Given the data available and the policies in place at the time, this was not an unreasonable definition. But in recent years an increasing share of what government does to support low-income families takes the form of tax credits (such as the Earned Income Tax Credit) and in-kind benefits (such as Food Stamps). If policymakers or the public want to know how these programs affect poverty, the official measure cannot provide an answer.

12. Fisher, Gordon M. “The Development and History of the Poverty Thresholds.” Social Security Bulletin, Vol. 55, No. 4. Winter 1992.

NYC.GOV/CEO Poverty Data and Research

2 The CEO Poverty Measure, 2005 - 2013

1.2 The National Academy of Sciences’ AlternativeDissatisfaction with the official measure prompted Congress to request a study by the National Academy of Sciences (NAS). The NAS’s recommendations, issued in 1995, sparked further research and garnered widespread support among poverty experts.13 However, neither the Federal nor any state or local government had adopted the NAS approach until CEO’s initial report on poverty in New York City in August 2008.14

The NAS-based methodology is also income based, but takes a considerably different approach to both the threshold and resource sides of the poverty measure. The poverty threshold reflects the need for clothing, shelter, and utilities, as well as food. It is established by selecting a sub-group of families as reference families,15 calculating their spending on these items, and then choosing a point in the resulting expenditure distribution.16 A small multiplier is applied to account for miscellaneous expenses such as personal care, household supplies, and non-work-related transportation. The threshold is updated each year by the change in the level of this spending. This connects the threshold to the growth in living standards. In further contrast to the official measure, the NAS-style poverty line is also adjusted to reflect geographic differences in housing costs.

On the resource side, the NAS-based measure is designed to account for the flow of income and in-kind benefits that a family can use to meet the needs represented in the threshold. This creates a much more inclusive measure of income than pre-tax cash. The tax system and the cash-equivalent value of in-kind benefits for food and housing are important additions to family resources. But families also have non-discretionary expenses that reduce the income available to meet their other needs. These include the cost of commuting to work, childcare, and medical care that must be paid for out of pocket. This spending is accounted for as deductions from income.

13. Citro, Constance F. and Robert T. Michael (eds). Measuring Poverty: A New Approach. Washington, DC: National Academy Press. 1995. Much of the research inspired by the NAS report is available at: www. census.gov/hhes/povmeas/methodology/nas/index.html14. New York City Center for Economic Opportunity. The CEO Poverty Measure: A Working Paper by the New York City Center for Economic Opportunity. August 2008. Available at: www.nyc.gov/html/ceo/ downloads/pdf/final_poverty_report.pdf15. The reference family proposed by the NAS is composed of two adults and two children. The threshold for this family is then scaled for families of different sizes and compositions. See Appendix B.16. The NAS suggested that this point lie between the 30th and 35th percentile of the distribution. Citro and Michael, p.106.

Measures of Poverty

Official: The current official poverty measure was de-veloped in the early 1960s. It consists of a set of thresh-olds that were based on the cost of a minimum diet at that time. A family’s pre-tax cash income is compared against the threshold to determine whether its mem-bers are poor.

NAS: At the request of Congress, the National Academy of Sciences issued a set of recommendations for an improved poverty measure in 1995. The NAS threshold represents the need for clothing, shelter, and utilities, as well as food. The NAS income measure accounts for taxation and the value of in-kind benefits.

SPM: In March 2010 the Obama Administration an-nounced that the Census Bureau, in cooperation with the Bureau of Labor Statistics, would create a Supple-mental Poverty Measure based on the NAS recommen-dations, subsequent research, and a set of guidelines proposed by an Interagency Working Group. The first report on poverty using this measure was issued by the Census Bureau in November 2011.

CEO: The Center for Economic Opportunity released its first report on poverty in New York City in August 2008. CEO’s poverty measure is largely based on the NAS recommendations, with modifications based on the guidelines from the Interagency Working Group.

1.3 The Supplemental Poverty MeasureSince November 2011, the U.S. Bureau of the Census has been issuing a Supplemental Poverty Measure (SPM).17 The new Federal measure is shaped by the NAS recommendations and an additional set of guidelines provided by an Interagency Technical Working Group (ITWG) in March 2010.18 The guidelines made several revisions to the 1995 NAS recommendations. The most important of these are:

17. U.S. Bureau of the Census. The Research Supplemental Poverty Measure: 2010. November 2011. Available at: www.census. gov/hhes/povmeas/methodology/supplemental/research/ Short_ ResearchSPM2010.pdf18. Observations from the Interagency Technical Working Group on Developing a Supplemental Poverty Measure. March 2010. Available at: www.census.gov/hhes/www/poverty/SPM_TWGObservations.pdf

Chapter 1: Introduction 3

NYC.GOV/CEO Poverty Data and Research

1. An expansion of the type of family unit whose expenditures determine the poverty threshold from two-adult families with two children to all families with two children.

2. Use of a five-year, rather than three-year, moving average of expenditure data to update the poverty threshold over time.

3. Creation of separate thresholds based on housing status: whether the family owns its home with a mortgage; owns, but is free and clear of a mortgage; or rents.

1.4 CEO’s Adoption of the NAS/SPM MethodCEO has followed the first two of these three revisions to the NAS recommendations in our poverty measure. However, we do not utilize the SPM’s development of thresholds that vary by housing status. We account for all differences in housing status – including residence in rent-regulated apartments and participation in means-tested housing assistance programs – on the income side of the poverty measure.19 By applying the ratio of New York City to U.S.-wide Fair Market Rent for a two-bedroom apartment to the housing portion of the SPM poverty line, we adjust the national-level threshold (before its adjustment for housing status) to account for the relatively high cost of housing in New York City. In 2013, our poverty line for the two-adult, two-child family comes to $31,156, some 25.0 percent above the U.S.-wide SPM threshold of $24,931. We refer to this New York City-specific threshold as the CEO poverty threshold. (See Appendix B.)

19. The rationale for this decision is provided in Appendix B of an earlier report. See: The CEO Poverty Measure, 2005 – 2010: A Working Paper by the NYC Center for Economic Opportunity. Available at: www.nyc.gov/html/ceo/downloads/pdf/CEO_Poverty_Measure_ April_16.pdf

Poverty Thresholds

Official: The official threshold was developed in the early 1960s and was based on the cost of a minimum diet at that time. It is updated each year by the change in consumer prices. It is uniform across the United States.

CEO: The CEO poverty threshold is a New York City-specific threshold derived from the U.S.-wide thresh-old developed for the Federal Supplemental Poverty Measure. The threshold is based on what families spend on basic necessities: food, clothing, shelter, and utilities. It is adjusted to reflect the variation in housing costs across the United States.

To measure the resources available to a family to meet the needs represented by the threshold, we employ the Public Use Micro Sample from the Census Bureau’s American Community Survey (ACS) as our principal data set. The advantages of this survey for local poverty measurement are numerous. The ACS is designed to provide measures of socioeconomic conditions on an annual basis in states and larger localities. It offers a robust sample for New York City (roughly 26,000 households) and contains essential information about household composition, family relationships, and cash income from a variety of sources.

But, as noted earlier, the NAS-recommended poverty measure greatly expands the scope of resources that must be measured in order to determine whether a family is poor. Unfortunately, the ACS provides only some of the information needed to estimate the additional resources required by the NAS measure. Therefore, CEO has developed a variety of models that estimate the effect of taxation, nutritional and housing assistance, work-related expenses, and medical out-of-pocket expenditures on total family resources and poverty status. We reference the resulting data set as the “American Community Survey Public Use Micro Sample as augmented by CEO” and we refer to our estimate of family resources as “CEO income.”

NYC.GOV/CEO Poverty Data and Research

4 The CEO Poverty Measure, 2005 - 2013

Measuring Income

Official Income: The official poverty measure’s defini-tion of family resources is pre-tax cash. This includes income from sources such as wages and salaries, as well as government transfer payments, provided that they take the form of cash. Thus, Social Security benefits are included in this measure, but the value of in-kind ben-efits, like Food Stamps or tax credits such as the Earned Income Tax Credit, are not counted.

CEO Income: Based on the NAS recommendations, CEO income includes all the elements of pre-tax cash plus the effect of income and payroll taxes, as well as the value of in-kind nutritional and housing assistance. Non-discretionary spending for commuting to work, childcare, and out-of-pocket medical care are deduc-tions from income.

Below is a brief description of how the non-pre-tax-cash income items are estimated. More details on these procedures can be found in the report’s technical appendices.

Housing Adjustment: The high cost of housing makes New York City an expensive place to live. The CEO poverty threshold, we noted above, is adjusted to reflect that reality. But some New Yorkers do not need to spend as much to secure adequate housing as the higher threshold implies. Many of the City’s low-income families live in public housing or receive a housing subsidy, such as a Section 8 housing voucher. A large proportion of New York’s renters live in rent-regulated apartments. Some homeowners have paid off their mortgages and own their homes free and clear. We make an upward adjustment to these families’ incomes to reflect these advantages. The adjustment equals the difference between what they would be paying for their housing if it were market rate and what they are actually paying out of pocket. The adjustment is capped so that it cannot exceed the housing portion of the CEO threshold.

The ACS does not provide data on housing program participation. To determine which households in the ACS could be participants in rental subsidy or regulation programs, we match households in the Census Bureau’s New York City Housing and Vacancy Survey with household-level records in the ACS. (See Appendix C.)

Taxation: CEO has developed a tax model that creates tax filing units within the ACS households; computes their adjusted gross income, taxable income, and tax liability; and then estimates net income taxes after non-refundable and refundable credits are applied. The model takes account of Federal, State, and City income tax programs, including all the credits that are designed to aid low-income filers. The model also includes the effect of the Federal payroll tax for Social Security and Medicare (FICA). (See Appendix D.)

Nutritional Assistance: We estimate the effect of Food Stamps,20 the National School Lunch program, the School Breakfast Program, and the Supplementary Nutrition Program for Women, Infants, and Children (WIC). To estimate Food Stamp benefits, we make use of New York City Human Resources Administration Food Stamp records, imputing Food Stamp cases to the “Food Stamp Units” we construct in the ACS data. We count each dollar of Food Stamp benefits as a dollar added to family income.

The likelihood of participation in the school meals programs is calculated by a probability model. Participation is assigned to eligible families to replicate administrative data on meals served provided to us by the City’s Department of Education. We follow the Census Bureau’s method for valuing the income from the programs by using the per-meal cost of the subsidy. We identify participants in the WIC program in a similar manner, matching enrollment in the program to participation rate estimates from the New York State Department of Health. Benefits are calculated using the average benefit level per participant calculated by the U.S. Department of Agriculture. (See Appendix E.)

Home Energy Assistance Program: The Home Energy Assistance Program (HEAP) provides assistance to low-income households that offsets their utility costs. In New York City, households that receive cash assistance, Food Stamps, or are composed of a single person receiving SSI benefits are automatically enrolled in the program. Other low-income households can apply for HEAP, but administrative data from the City’s Human Resources Administration indicate that nearly all HEAP households come into the program through their participation in these other benefit programs. We identify HEAP-receiving households by their participation in public assistance, Food Stamps, or SSI, and then add

20. The Food Stamp program has been renamed the Supplemental Nutritional Assistance Program (SNAP). Since the program is more widely recognized by its former name, we continue to use it.

Chapter 1: Introduction 5

NYC.GOV/CEO Poverty Data and Research

the appropriate benefit to their income. Beginning in 2011, we also make use of HEAP receipt reported in the Housing and Vacancy Survey. (See Appendix F.)

Work-Related Expenses: Workers must travel to and from their jobs, and we treat the cost of that travel as a non-discretionary expense. We estimate the number of trips a worker will make per week based on their usual weekly hours. We then calculate the cost per trip using information in the ACS about their mode of transportation and administrative data (such as subway fares). Weekly commuting costs are computed by multiplying the cost per trip by the number of trips per week. Annual commuting costs equal weekly costs times the number of weeks worked over the past 12 months.

Families in which the parents are working must often pay for the care of their young children. Like the cost

of commuting, the CEO poverty measure treats these childcare expenses as a non-discretionary reduction in income. Because the American Community Survey provides no information on childcare spending, we have created an imputation model that matches the weekly childcare expenditures reported in the Census Bureau’s Survey of Income and Program Participation (SIPP) to working families with children in the ACS data set. Childcare costs are only counted if they are incurred in a week in which the parents (or the single parent) are at work. They are capped by the earned income of the lowest earning parent. (See Appendix G.)