tod finance summit12_6_12

DESCRIPTION

Presentations from the MAPC TOD Finance Summit on December 12, 2012TRANSCRIPT

Transit-Oriented Development

Finance Summit• December 6, 2012 •

Executive DirectorMetropolitan Area Planning

Council

Marc D. Draisen

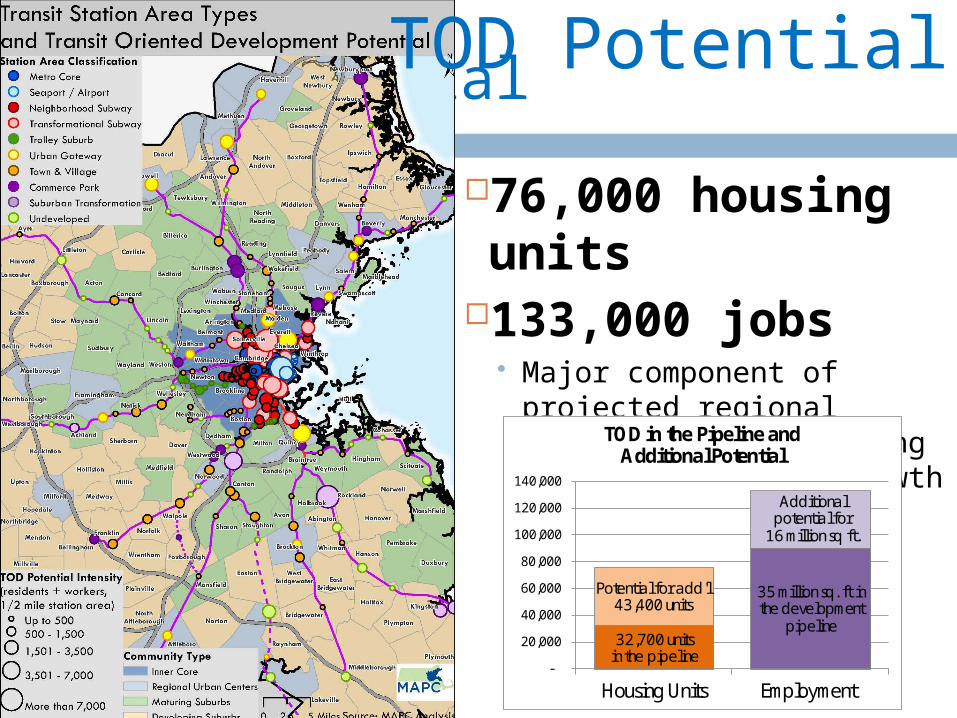

GROWING STATION AREASTHE VARIETY AND POTENTIAL OF TRANSIT ORIENTED DEVELOPMENT IN METRO BOSTON

Transit Station Area Types

Metro Core Metro Core NeighborhoNeighborhood Subway od Subway

Urban Urban Gateway Gateway

Commerce Commerce Park Park

Trolley Trolley Suburb Suburb

Seaport / Seaport / Airport Airport

TransformaTransformational tional

SubwaySubwayTown & Town & Village Village

Suburban Suburban TransformaTransforma

tion tion UndevelopeUndevelope

d d

TOD Potential

76,000 housing units

133,000 jobs Major component of

projected regional growth - 31% of housing demand 56% of job growth

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Housing Units Employment

TOD in the Pipeline and Additional Potential

Additional potential for

16 million sq ft.

32,700units in the pipeline

Potentialfor add'l 43,400 units

35million sq. ft in the development

pipeline

TOD Potential

Executive DirectorLocal Initiatives Support

CorporationBoston

Bob Van Meter

Creating an “Equitable Transit Oriented

Developmment Accelerator Fund (ETODAF)”

Bob Van Meter, Executive DirectorKristin Blum, Senior Program Officer

December 6, 20127

Boston LISCLocal Initiatives Support Corporation (LISC)’smission is to help neighbors build community.We believe that everyone should have theright to live in a SAFE, HEALTHY,PROSPEROUS NEIGHBORHOOD FULL OFOPPORTUNITIES.

Boston LISC * December 6, 2012 8

LISC is an Established Community Development Lender• Invested over $400 million

in loan capital nationally since 2004

• Boston LISC has a 30-year track record

• Over $45 million in loans in greater Boston with a loss rate of about 1%.

• LISC lends to non profit and for profit borrowers for affordable and mixed income housing, commercial and retail and other community development needs

Boston LISC * December 6, 2012 9

LISC’s TOD Background

Boston LISC * December 6, 2012 10

In the past 4 years, LISC has invested:

• $20 million in equity investments (New Markets and Low Income Housing credits) • $5.7 million in loan capital• $500,000 in grant funding

Supporting a range of TOD projects and locations totaling:

•625 units of affordable and mixed income housing; and •150,000 square feet of commercial space

Boston LISC * March 14, 2012

TOD as part of Building Healthy Communities of Choice LISC’s approach includes

economic development, public safety, active transportation options, access to food

Resilient Communities/ Resilient Families

TOD can bring economic diversity in stronger market communities with access to transit

Boston LISC * December 6, 2012 11

Benefits of EquitableTransit-Oriented DevelopmentFor HouseholdsHouseholds have

increased access to jobs and services

Combined cost of housing and transportation is reduced

Low income families have access to affordable housing in gentrifying transit communities

Boston LISC * December 6, 2012 12

For CommunitiesLess dependence on automobile use Reduce pollutionPedestrian friendly environments with services in walking/biking distanceCommunities serve a range of incomes in mixed-use settings

The Market is Demanding More TOD

Boston LISC * December 6, 2012 13

• Today, about 6 million households live within ½ mile of transit

• Demand for transit accessible housing is projected to reach 16 million by 2030!

• Meeting this demand means building 10 million housing units within a 10-minute walk of transit, or 2,000 units near every

station in the U.S. “This movement toward denser, mixed-use forms of development presents a golden opportunity

to create mixed-income transit villages, providing healthier environments, especially for low-income families.” –Convergence Partnership

The case for Equitable TOD “Equitable TOD” prioritizes investments that:

Support production and preservation of affordable housing near transit

provides other transit-accessible community services such as schools, health clinics, and food stores; and

enhances access for transit-dependent populations through connecting bicycle and pedestrian facilities.

Equitable TOD is about creating equal opportunities for people of all incomes to capture the benefits of transit oriented locations.

Market pressures often target new development to higher incomes; but lower income households are the highest users of transit.

Boston LISC * December 6, 2012 14

Distinct roles for equitable TOD in three different locations

Stronger markets Emerging/gentrifying markets Weaker markets

Boston LISC * December 6, 2012 15

Strong Market Neighborhoods Market-rate TOD is happening in many suburban

and stronger market urban locations Affordable housing needs to be part of the

housing mix in these locations; Equitable TOD is an opportunity to provide this.

Housing near transit provides better connections to jobs and services, and lowers housing/ transportation costs for low- and moderate-income families

Boston LISC * December 6, 2012 16

Gentrifying Neighborhoods = Affordability at Risk Those who rely on transit the most or who stand to

gain the most quality-of-life benefits from new transit also face the greatest risk of being displaced by the rising property values associated with new and expanded transit

Equitable TOD in these neighborhoods can reduce displacement and preserve affordability

Boston LISC * December 6, 2012 17

Weaker Market Neighborhoods: Catalyzing Revitalization TOD can be part of a revitalization strategy

that improves the neighborhood and attracts private investment;

Additional development, with increased density and foot traffic, can attract investment and improve property values; and

Increasing connections to jobs and services for neighborhood residents can result in equitable outcomes

Boston LISC * December 6, 2012 18

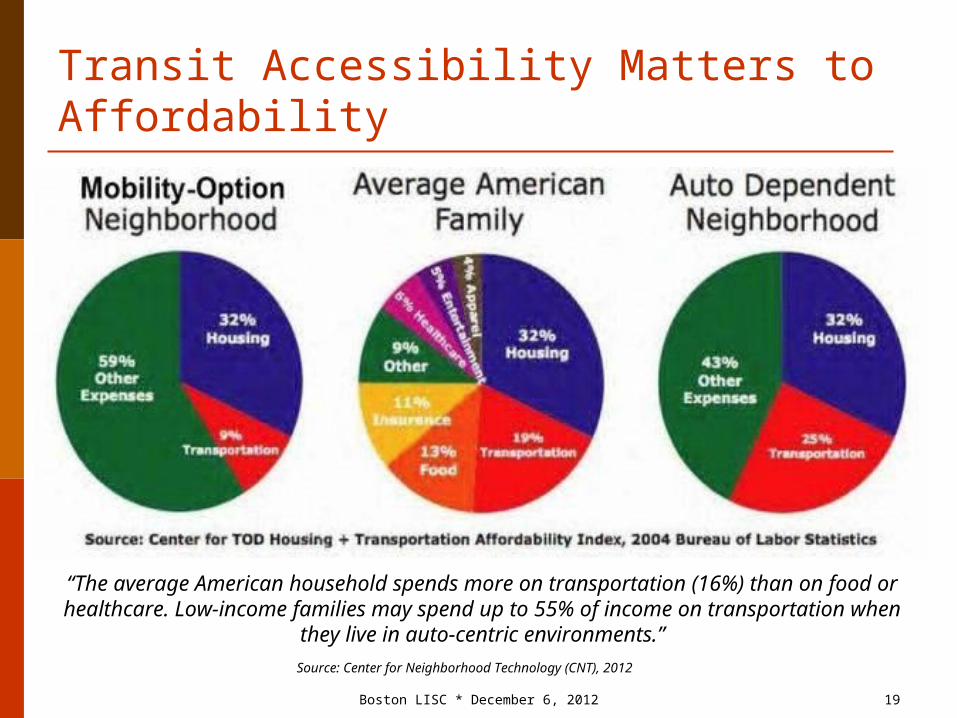

Transit Accessibility Matters to Affordability

Boston LISC * December 6, 2012 19

“The average American household spends more on transportation (16%) than on food or healthcare. Low-income families may spend up to 55% of income on

transportation when they live in auto-centric environments.”Source: Center for Neighborhood Technology (CNT), 2012

Why ETOD: Low-Income Households Most Burdened by Rising H+T Costs

Boston LISC * December 6, 2012 20

Working families making $20,000-50,000/yr pay 10% more of their income on transportation costs (~30%) than average households (~20%)

Source: “A Heavy Load”, Center for Housing Policy, 2006

While median-income households in the largest 25 U.S. metros have paid 44% more for housing and transportation over the last decade, they have earned only 25% more in income

Source: “Losing Ground”, Center for Housing Policy, 2012

Why ETOD: Low-Income and Minority Populations Most Burdened by Long, Burdensome Commutes

Boston LISC * December 6, 2012 21

A recent Northeastern University study found that, in Boston:

• White commuters who drive have the shortest commutes (27 min), and black commuters who bus have the longest (46 min)

• Black commuters spend an extra 66 hours/year waiting, riding, and transferring than white bus riders

“…affordable housing is scarce and often far from desireable

subway and rail stations.”Source: NEU Dukakis Center for Urban and Regional Policy, 2012

Strategies to Create ETOD

Policy changes in public funding allocation mechanisms to prioritize TOD (underway)

Land disposition to include equitable development

Transit system improvements and expansion Develop financing tools to facilitate and

prioritize TOD such as LISC’s proposed fund and the Healthy Neighborhoods Equity Fund to provide capital

Boston LISC * December 6, 2012 22

Development of Fund ConceptLISC started looking at the feasibility of a TOD fund at the request of philanthropic

partners and our CDC partners with active projects in TOD corridors

Identified Needs: Low interest, patient, flexible capital Higher loan to value limits Help with carrying costs Early planning reinforced by TOD Gap

Finance Analysis findingsBoston LISC * December 6, 2012 23

Boston LISC * March 14, 2012

Financing Challenges to TODSmall scale, strategic land assembly is

critical to creating larger parcels but is perceived as risky by lenders.

The competitive funding environment means projects must demonstrate high readiness. Holding periods are growing.

Non-profit TOD borrowers have difficulty meeting the LTV requirements of existing lenders.

Boston LISC * December 6, 2012 24

Boston LISC * March 14, 2012

Financing ChallengesLack of financing available for carrying

costs strains community based and nonprofit developers

Developers need to access multiple sources of predevelopment capital for the same deal

Alternative site control arrangements (option payments, rights of first refusal) are not always pursued

Boston LISC * December 6, 2012 25

Boston LISC * March 14, 2012

ETODAF: Addressing the Challenges Provides access to

streamlined, lower cost capital to close the LTV gap and unlock existing lender network funds;

Allows efficient acquisition of strategic TOD parcels;

Provides predevelopment capital to advance critical projects efficiently;

Reduces risks by offering recoverable grants for early feasibility expenses and for option payments.

Boston LISC * December 6, 2012 26

Boston LISC * March 14, 2012

Fund Overview (ETODAF) *The ETODAF- managed by Boston LISC- will

provide critical early stage capital and streamline access to capital to acquire and jump start equitable TOD developments.

Key funders are: State Government - EOHED is considering a

MassWorks grant through MassDevelopment for top loss reserve.

PRI requests are currently being considered by the Hyams Foundation and The Boston Foundation

LISC intends to seek PRIs from additional local and national funders interested in participating

Grant funders: LISC has secured start up funding from Hyams Foundation and Barr Foundation.

Boston LISC * December 6, 2012 27

Fund StructureBoston LISC will manage the fund as a local financing tool:Fund will provide credit enhancement to allow a higher Loan to Value ratio (LTV) in the form of subordinate loans behind acquisition loans.

Acquisition/first lenders will provide a loan at 80-90% LTV; Fund will provide a second loan to allow a total LTV from 110-120% to allow financing for carrying costs and other predevelopment expenses.

Boston LISC * December 6, 2012 28Boston LISC * March 14, 2012

Eligible ProjectsEligible uses of the fund:

Affordable housing, mixed-income housing, mixed-use development, and neighborhood retail, commercial or community space (non-housing investments to be limited to 10-15% of fund).

Projects will need to meet Fund definitions:

PROXIMIITY to transit; CONNECTIVITY and orientation to transit; and AFFORDABILITY.

Boston LISC * December 6, 2012 29

Proposed Terms Rate: Fund second loan 3-4%; community development

lenders: 4.5% to 6% Term: up to 3 years Types of Loans

Acquisition of strategic properties Predevelopment Holding Costs Lines of credit for multiple TOD activities and uses Bridge loans and other loans based on project needs to move

advance TOD projects Recoverable grants for option payments and early feasibility

expenses Loan to Value: up to 110-120% on secured loans

Boston LISC * December 6, 2012 30Boston LISC * March 14, 2012

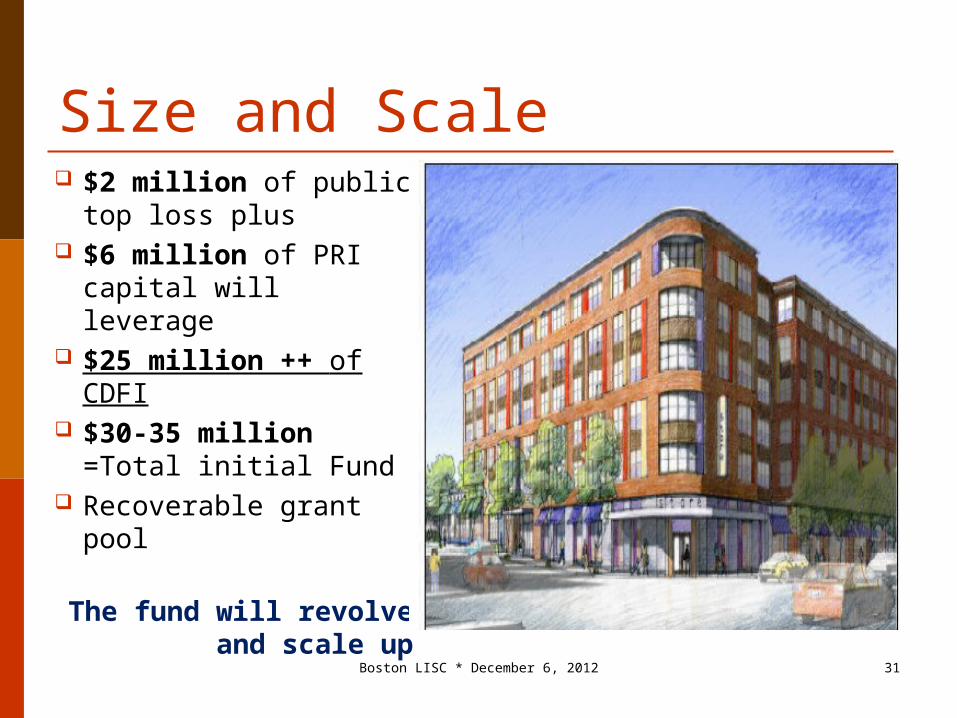

Size and Scale $2 million of public

top loss plus $6 million of PRI

capital will leverage $25 million ++ of

CDFI $30-35 million

=Total initial Fund Recoverable grant

pool

The fund will revolve and scale up

Boston LISC * December 6, 2012 31

How the Fund Makes a Difference Fills equity and loan to value (LTV) gap

Covers holding and interest costs

Encourages alternative site control arrangements by providing recoverable grants for this purpose

Systems change in predevelopment

systemBoston LISC * December 6, 2012 32

What would the TOD Fund do? Leverage capital,

underwriting expertise, and technical assistance of the existing network of funders

Streamline the process of raising early stage capital

Leverage public investment and private capital to respond to financing challenges

Reduce the need for multiple predevelopment sources for one project

Mitigate risks that prevent existing lenders from participating in TOD projects

Provide PRI investments for LTV gap at low cost

Utilize recoverable grants for the riskiest components and encourage alternative site control arrangements

Manage the pipeline by teeing up compelling projects that respond to State priorities.

Engage public partners as stakeholders

Boston LISC * December 6, 2012 33

Streamline ProcessStreamline Process Manage RiskManage Risk

Boston LISC * March 14, 2012

Implementation Schedule1. Secure investments for fund: 1st quarter 2013

2. Close fund: May 2013

3. Available for loans: Beginning May 2013

Boston LISC * December 6, 2012 34

Anticipated outcomes

Competitive, well funded non-profit sector able to advance equitable TOD transactions efficiently;

Affordable and revitalizing TOD in Fairmount Corridor and Gateway Cities to lead the market;

Mixed use, affordable urban village development to complement transit improvements;

Preservation of affordable housing in key urban transit corridors to avoid displacement as the market heats up; and

Creation of new affordable housing in gentrifying and stronger markets.

Boston LISC * December 6, 2012 35

Boston LISC * March 14, 2012

EDOTAF Aligned with Other Important Initiatives for Greater Impact Supports 13 of the 65 MetroFuture goals for

TOD, Smart Growth, Development of Affordable Housing Throughout the Region, particularly: Increasing affordable housing for working families Providing housing choices throughout the region without

displacement. Mass. Smart Growth Alliance’s Great

Neighborhoods Initiative Commonwealth’s new production goals and

Compact Neighborhoods initiative

Boston LISC * December 6, 2012 36

Complements CLF’s Healthy Neighborhoods Equity Fund Conservation Law Foundation Ventures

(CLFV) and Mass Housing Investment Corporation (MHIC) are working to develop Healthy Neighborhoods Equity Fund

The funds will be complementary (LISC: early stage capital; CLFV/MHIC: permanent equity)

Boston LISC * December 6, 2012 37

Thank you!Bob Van Meter, Executive Director, Boston LISC

Kristin Blum, Senior Program Officer, Boston LISC

[email protected] [email protected] www.bostonlisc.org

@LISC_Boston

Boston LISC * December 6, 2012 38

Conservation Law Foundation Ventures

Massachusetts Housing Investment Corporation

Bill ColemanMaggie ChurchJoe Flatley

Healthy Neighborhoods Equity Fund

TOD Summit PresentationDecember 6, 2012

What is the Healthy Neighborhoods Equity Fund?

$100M “blended” private equity fund – Transformative mixed-income, mixed-use projects in selected transit corridors– “Blended” structure of PRIs, mezzanine debt, and traditional PE – Innovative mix of institutional and social impact investors– Staged capitalization commencing 3rd quarter 2013 with $30MM first phase

CLFV/MHIC collaborative response to TOD funding gaps and opportunities for TBL outcomes– Leverage/finance upside not valued by underwriters– First bottom line: attractive risk-adjusted market returns– Second and third bottom lines: avoided VMTs, local economic development, improvements in

public health

The Fund conceived and managed as part of an integrated overall capital program– Capital program design informed by findings from GLC gap analysis– Coordinated synergy with LISC– Addresses multiple regional MetroFuture goals – Leverage state resources with new private capital– Managed by MHIC, a proven institutional fund manager

• CLF/CLFV mission “wheelhouse”

• History with “Big Dig” mitigation

• Private markets as part of social/environmental solutions

• Sponsor transformative projects by eliminating chronic

funding gaps

Why CLF / CLF Ventures?

What is CLF’s Role?

• Promote re-emerging interest in TBL outcomes

• Apply research linking TOD and health outcomes to investor strategies

• Collaborate with MHIC to capitalize the Fund

• Define/design metrics and participate in governance through formal committee or 501©3

• “Chancellor of Metrics” – guardian of project selection criteria and outcome metrics

Role of Private Equity

• Leverage other sources of public/private financing• Recognize longer term upside of market rate housing/retail/

C&I in unproven markets• Accelerate larger scale mixed use projects in transitional

markets• Unlock projects which might otherwise be infeasible

(e.g. complex infrastructure/brownfield issues)

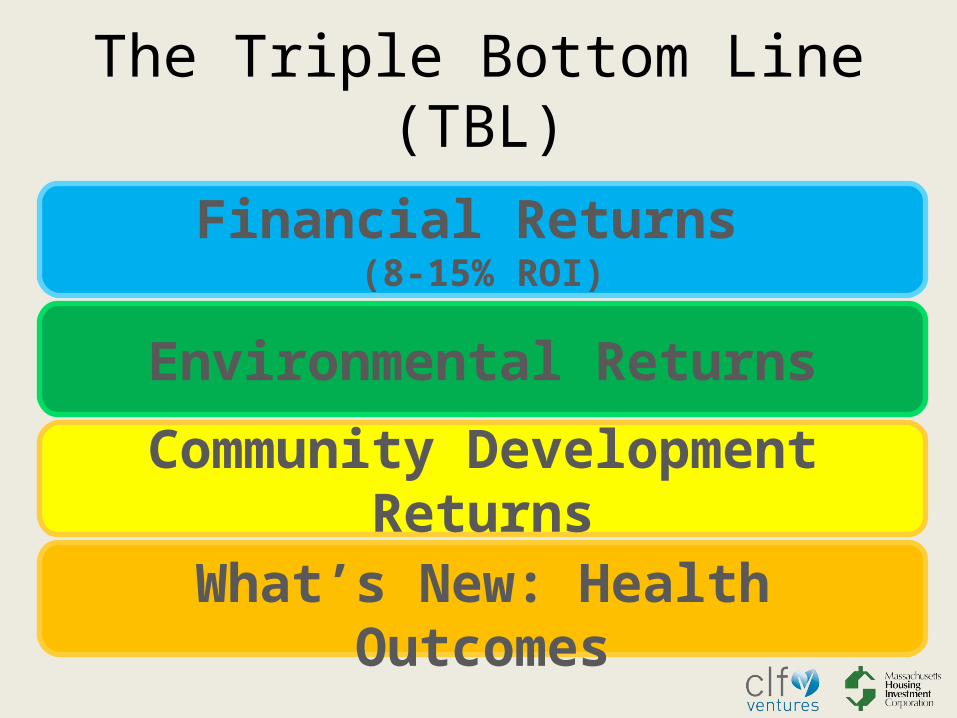

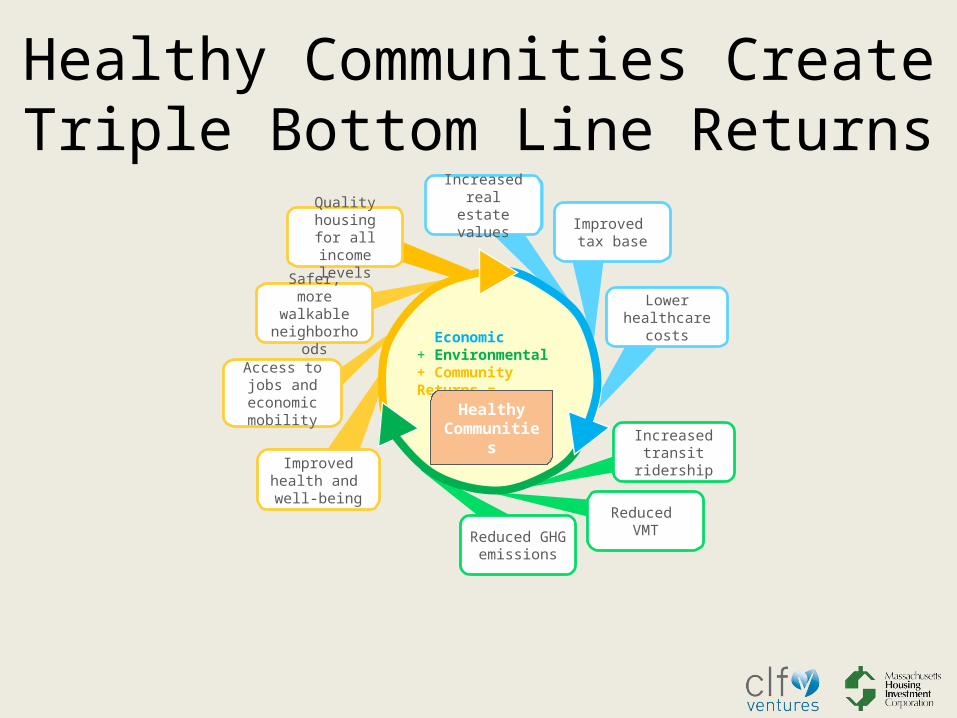

Community Development Returns

The Triple Bottom Line (TBL)

Financial Returns (8-15% ROI)

Environmental Returns

What’s New: Health Outcomes

Access to jobs and economic

mobility

Safer, more walkable

neighborhoods

Improved health and well-being

Increased real estate values

Improved tax base

Lower healthcare

costs

Reduced GHG emissions

Reduced VMT

Increased transit ridership

+ Economic+ Environmental+ Community Returns =

Healthy Communities

Quality housing for all income levels

Healthy Communities CreateTriple Bottom Line Returns

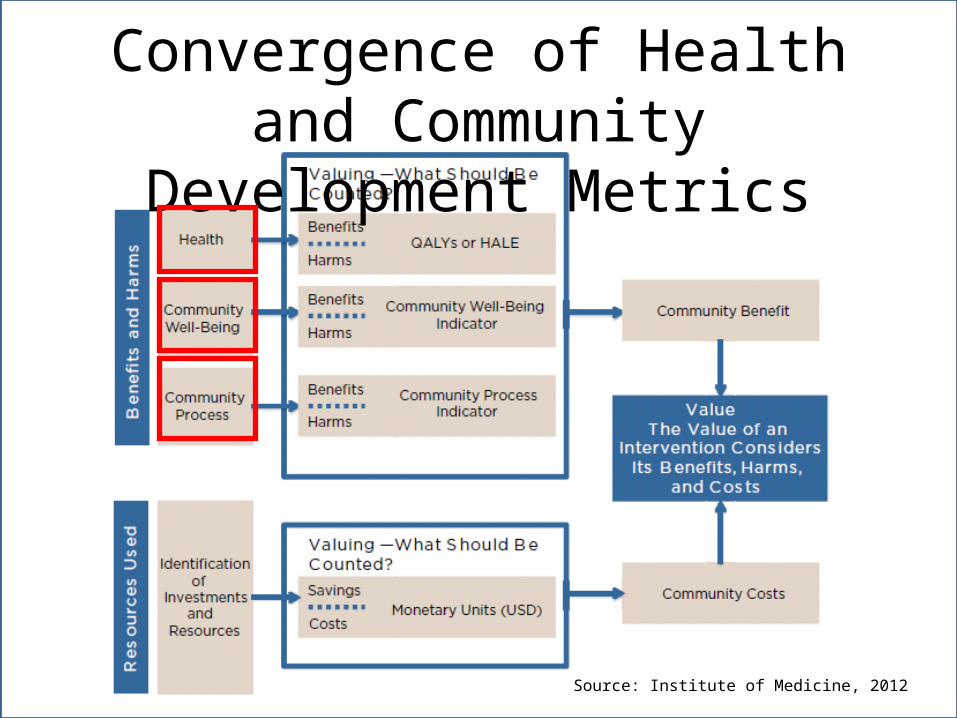

Convergence of Health and Community Development Metrics

Source: Institute of Medicine, 2012

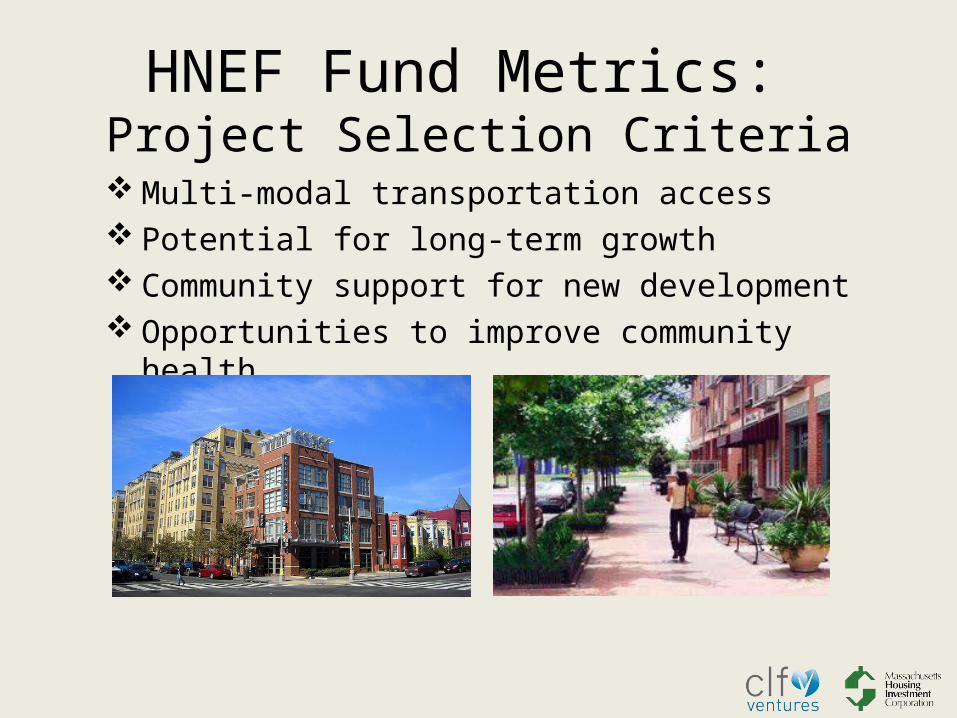

HNEF Fund Metrics: Project Selection Criteria

Multi-modal transportation access Potential for long-term growth Community support for new development Opportunities to improve community health

HNEF Fund Metrics: Project Outcomes

Increasing walkability and health/wellness opportunities Reducing VMTs; increased mode share for walking, biking, and

transit Improving energy and environmental performance Implementing community vision/ goals

AND…. Creating jobs and economic activity Expanding access to healthy food Increasing the range of quality housing options

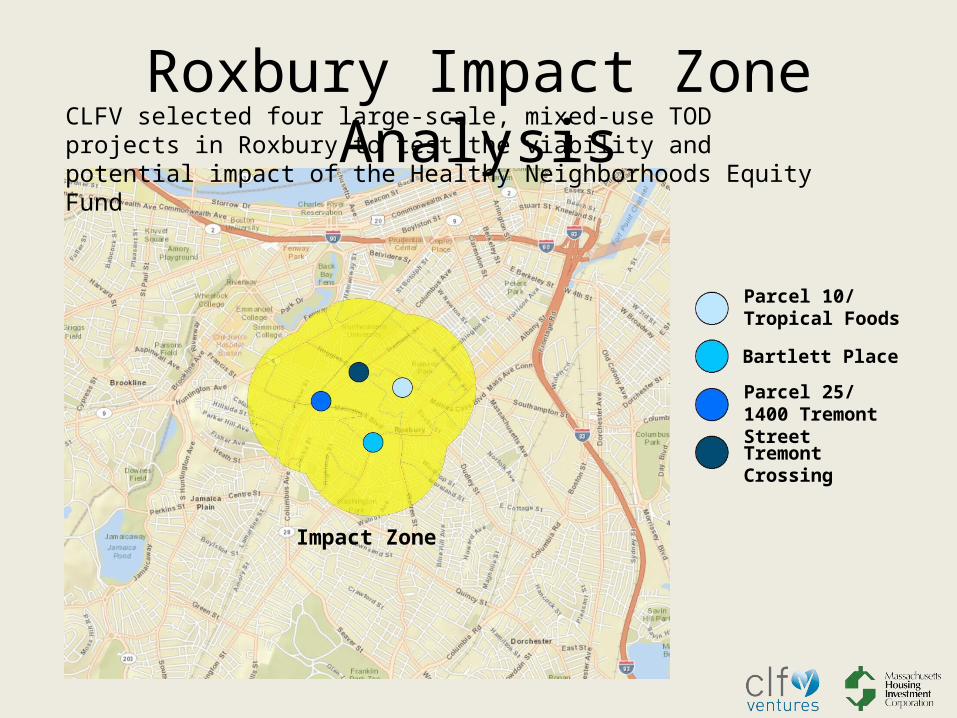

Roxbury Impact Zone Analysis

Bartlett Place

Parcel 25/1400 Tremont Street

Tremont Crossing

Parcel 10/Tropical Foods

CLFV selected four large-scale, mixed-use TOD projects in Roxbury to test the viability and potential impact of the Healthy Neighborhoods Equity Fund

Impact Zone

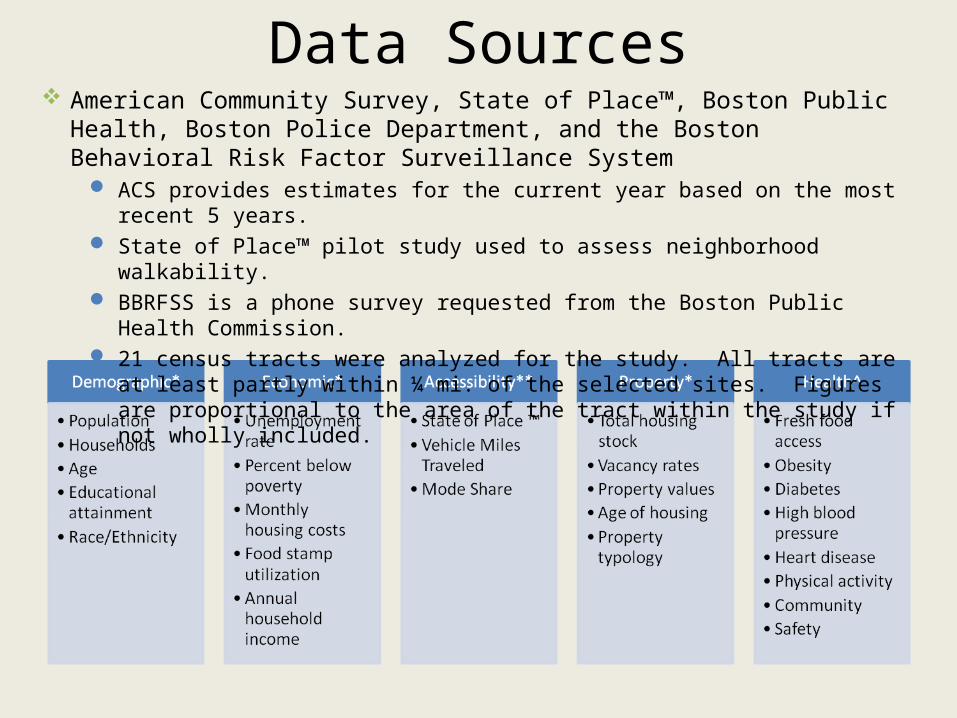

American Community Survey, State of Place™, Boston Public Health, Boston Police Department, and the Boston Behavioral Risk Factor Surveillance System

ACS provides estimates for the current year based on the most recent 5 years. State of Place™ pilot study used to assess neighborhood walkability. BBRFSS is a phone survey requested from the Boston Public Health Commission. 21 census tracts were analyzed for the study. All tracts are at least partly within ¼ mi. of

the selected sites. Figures are proportional to the area of the tract within the study if not wholly included.

Data Sources

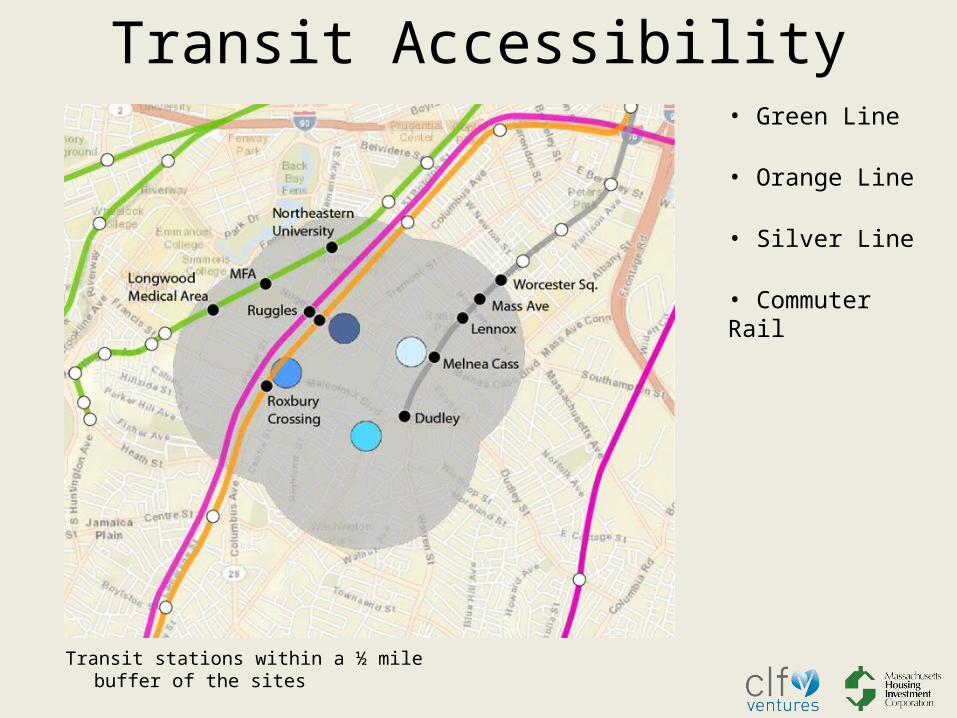

Transit stations within a ½ mile buffer of the sites

• Green Line

• Orange Line

• Silver Line

• Commuter Rail

Transit Accessibility

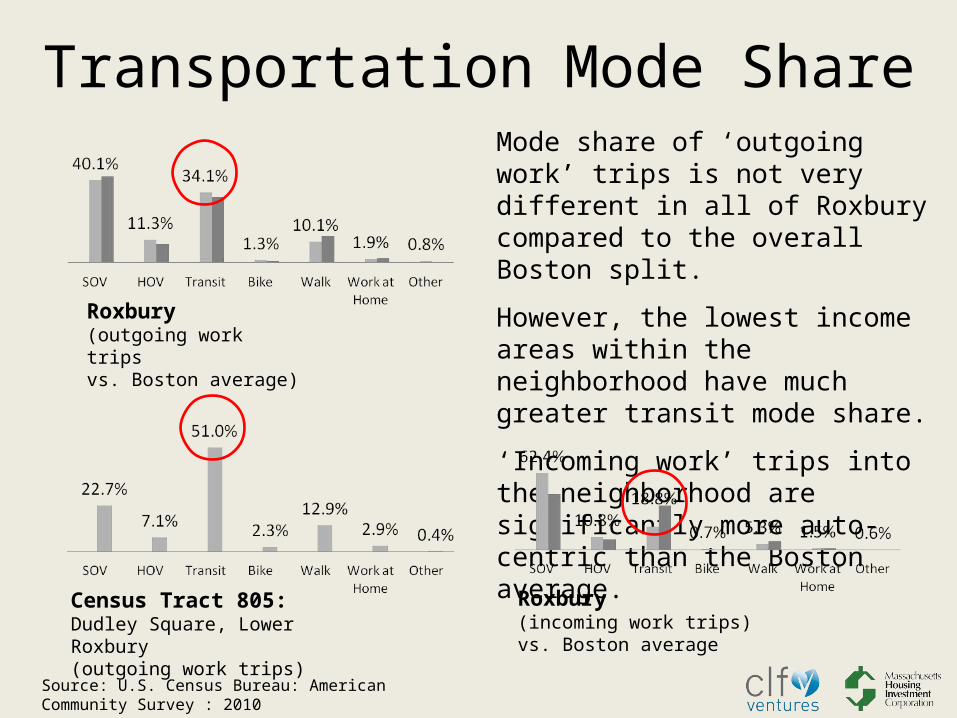

Census Tract 805: Dudley Square, Lower Roxbury(outgoing work trips)

Roxbury(outgoing work tripsvs. Boston average)

Mode share of ‘outgoing work’ trips is not very different in all of Roxbury compared to the overall Boston split.

However, the lowest income areas within the neighborhood have much greater transit mode share.

‘Incoming work’ trips into the neighborhood are significantly more auto-centric than the Boston average.

Roxbury(incoming work trips)vs. Boston average

Transportation Mode Share

Source: U.S. Census Bureau: American Community Survey : 2010

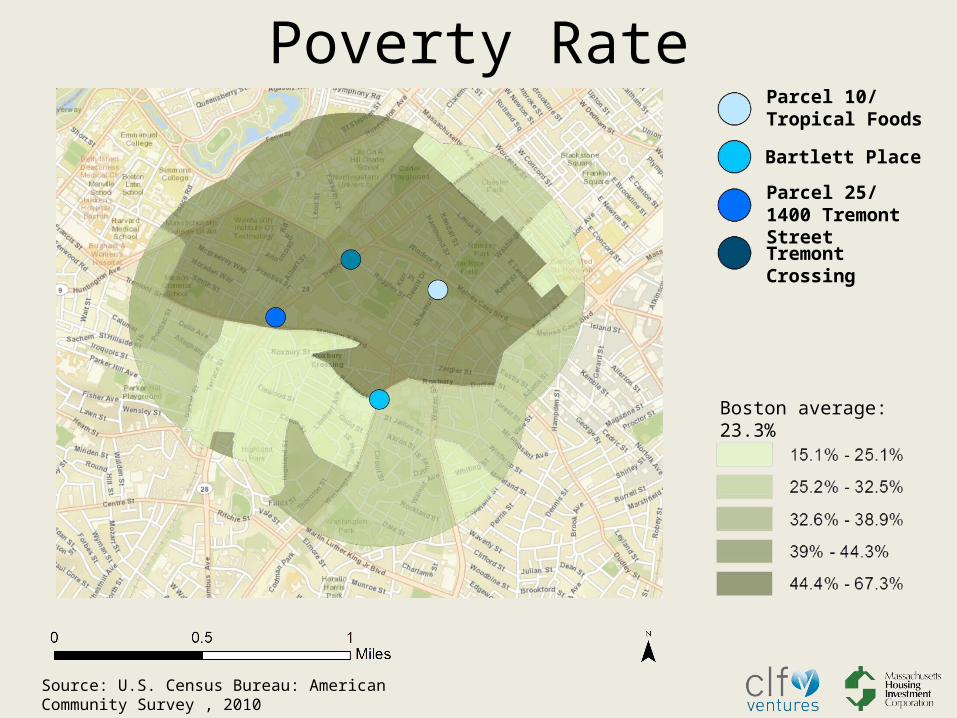

Boston average: 23.3%

Source: U.S. Census Bureau: American Community Survey , 2010

Poverty Rate

Bartlett Place

Parcel 25/1400 Tremont Street

Tremont Crossing

Parcel 10/Tropical Foods

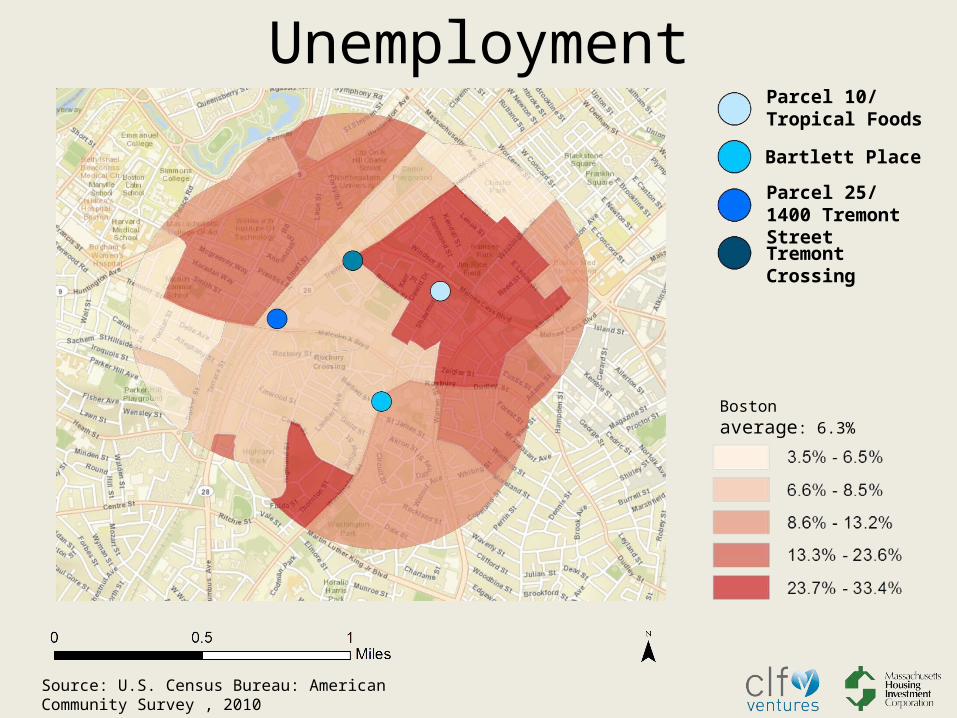

Boston average: 6.3%

Unemployment

Bartlett Place

Parcel 25/1400 Tremont Street

Tremont Crossing

Parcel 10/Tropical Foods

Source: U.S. Census Bureau: American Community Survey , 2010

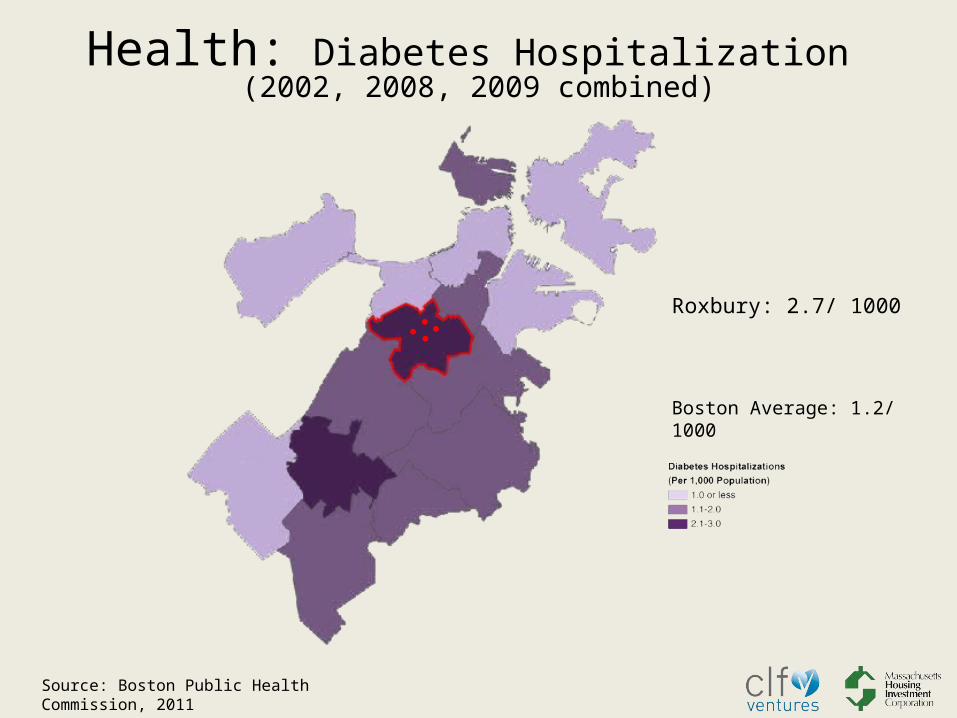

Health: Diabetes Hospitalization (2002, 2008, 2009 combined)

Boston Average: 1.2/ 1000

Roxbury: 2.7/ 1000

Source: Boston Public Health Commission, 2011

Boston Average: 19.4 / 1000

Health: Heart Disease Hospitalization (2007,2008,2009 combined)

Roxbury: 30.3/ 1000

Source: Boston Public Health Commission, 2011

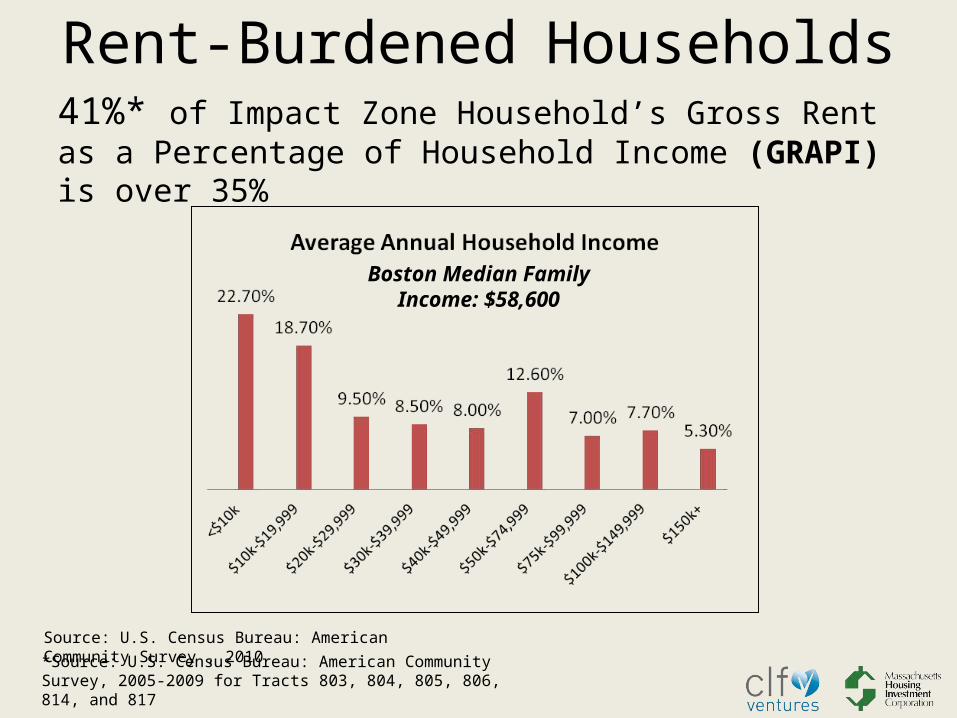

Boston Median Family Income: $58,600

Rent-Burdened Households

*Source: U.S. Census Bureau: American Community Survey, 2005-2009 for Tracts 803, 804, 805, 806, 814, and 817

41%* of Impact Zone Household’s Gross Rent as a Percentage of Household Income (GRAPI) is over 35%

Source: U.S. Census Bureau: American Community Survey , 2010

Bartlett Place2556 Washington Street

Developer: Bartlett Place Land Inc.(partnership between Nuestra Comunidad Dev. Corp. and Windale Developers)

Proposed Uses:• 56,000 SF of• Commercial/Retail • 300 residential units:• mix of rental and homeownership units • 60% affordable and • 40% market rate

Total Investment: $137 m

Cumulative Project ImpactNew Jobs

Affordable/Workforce Housing

Market -Rate Housing

Office and retail(SF)

Arts/ cultural (SF)

Total Investment

Bartlett Place

142 120 180

56,000 $137,000,000

Parcel 10/Tropical Foods

145 48 18

50,500

$44,000,000

Parcel 25

500* 65

200,000

$95,000,000

Tremont Crossing

1,738 240

700,000

58,000

$300,000,000

TOTAL 2,525 233 438

1,006,500

58,000

$576,000,000

Building Out a Community VisionRoxbury Community Master Plan: Boston Redevelopment AuthorityArts & Cultural HeritageEconomic Development & Job CreationTransportationHousingCommunity-Wide Urban Design Recommendations

Resilient Communities/ Resilient Families: Mission 180 - LISCCommunity Vision: Addressing community development through a public health lens, and working with residents to improve health outcomes.

Connecting the MetricsHealth Impact Assessments (three of four projects):

Awaiting funding decision from Mass. Dept. of Public Health

HIAs to be completed over 6 months (January - August 2013)

Will help inform health and wellness metrics for the Fund

State of Place™ Walkability Analysis Build on baseline walkability rating for

the neighborhood Examine most promising opportunities to

increase walkability Benchmark economic benefits of

increased walkability

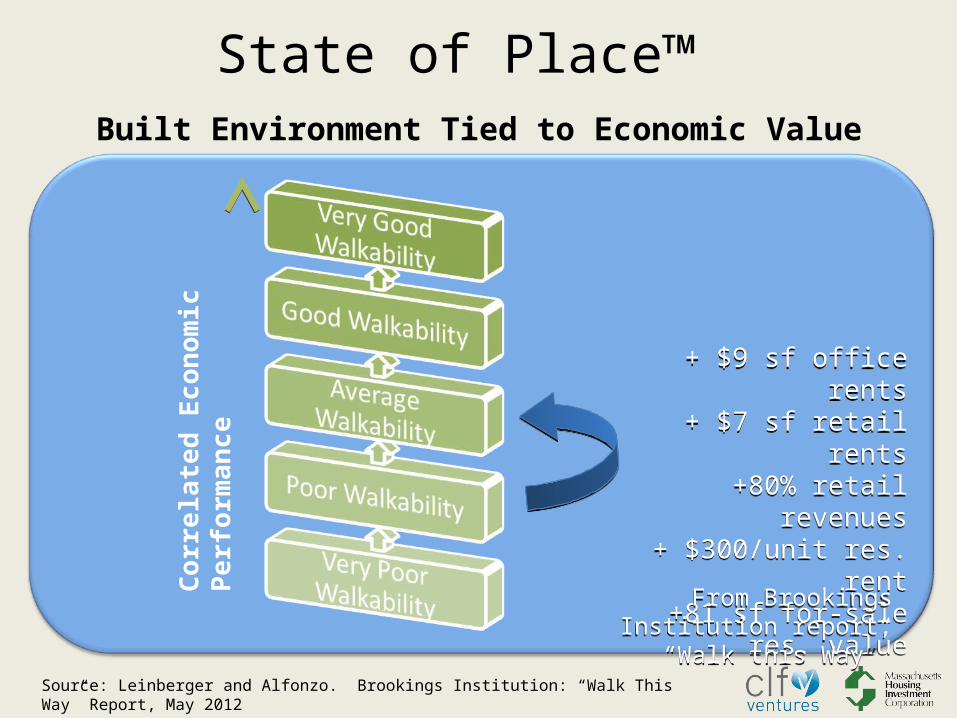

State of Place™ Built Environment Tied to Economic Value

Corr

ela

ted

Econ

om

ic

Perf

orm

an

ce

+ $9 sf office rents+ $7 sf retail rents

+80% retail revenues+ $300/unit res. rent

+81 sf for-sale res. value

+ $9 sf office rents+ $7 sf retail rents

+80% retail revenues+ $300/unit res. rent

+81 sf for-sale res. value

From Brookings Institution report, “Walk this Way”

From Brookings Institution report, “Walk this Way”

Source: Leinberger and Alfonzo. Brookings Institution: “Walk This Way” Report, May 2012

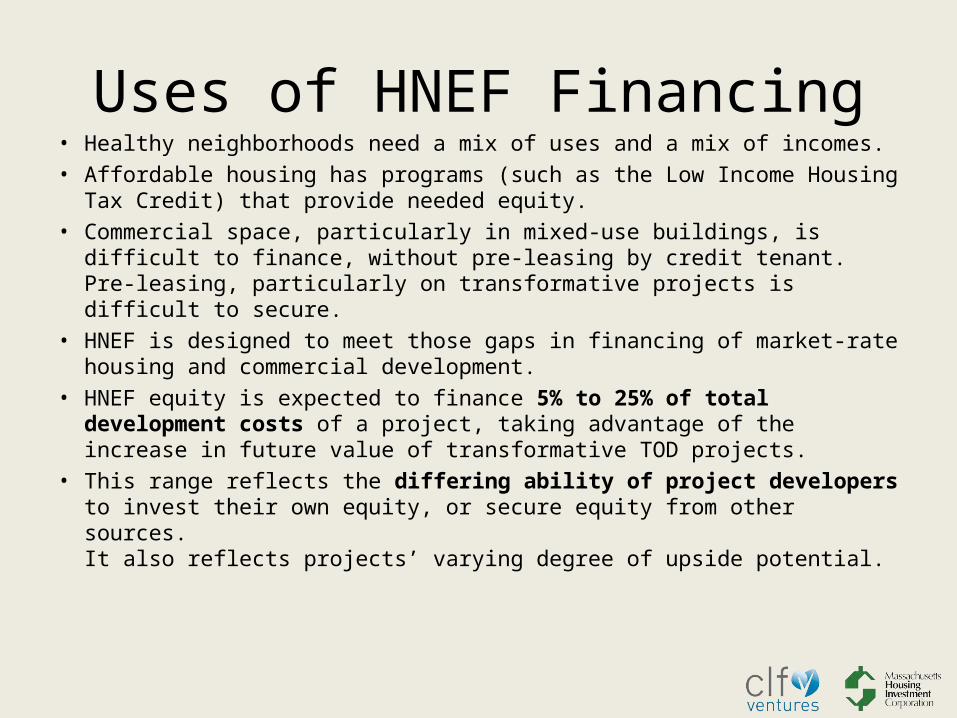

Uses of HNEF Financing• Healthy neighborhoods need a mix of uses and a mix of incomes.• Affordable housing has programs (such as the Low Income Housing Tax

Credit) that provide needed equity.• Commercial space, particularly in mixed-use buildings, is difficult to

finance, without pre-leasing by credit tenant. Pre-leasing, particularly on transformative projects is difficult to secure.

• HNEF is designed to meet those gaps in financing of market-rate housing and commercial development.

• HNEF equity is expected to finance 5% to 25% of total development costs of a project, taking advantage of the increase in future value of transformative TOD projects.

• This range reflects the differing ability of project developers to invest their own equity, or secure equity from other sources. It also reflects projects’ varying degree of upside potential.

HNEF Financing Terms• Projects will deliver return to investors over a 7 to 12 year period. Investor

returns will be generated via a share of project cash flow, along with priority distributions from refinancing or equity take-outs, and is expected to be in the range of 8-15%.

• While HNEF improves project feasibility, the trade-off is that it also requires the developer to share future upside with the HNEF investors.

• Terms for individual projects will depend on the degree of risk as well as the potential for upside returns.

• Sample terms (illustrative only): HNEF will receive an annual preferred return of 4% HNEF will receive 50% share of cash flow after preferred return For a project with substantial lease-up (or similar) reserves, 75% of release of

reserves will go to HNEF Payout from refinancing in 7-10 years to achieve target return of 15%, plus share

of equity upside above that

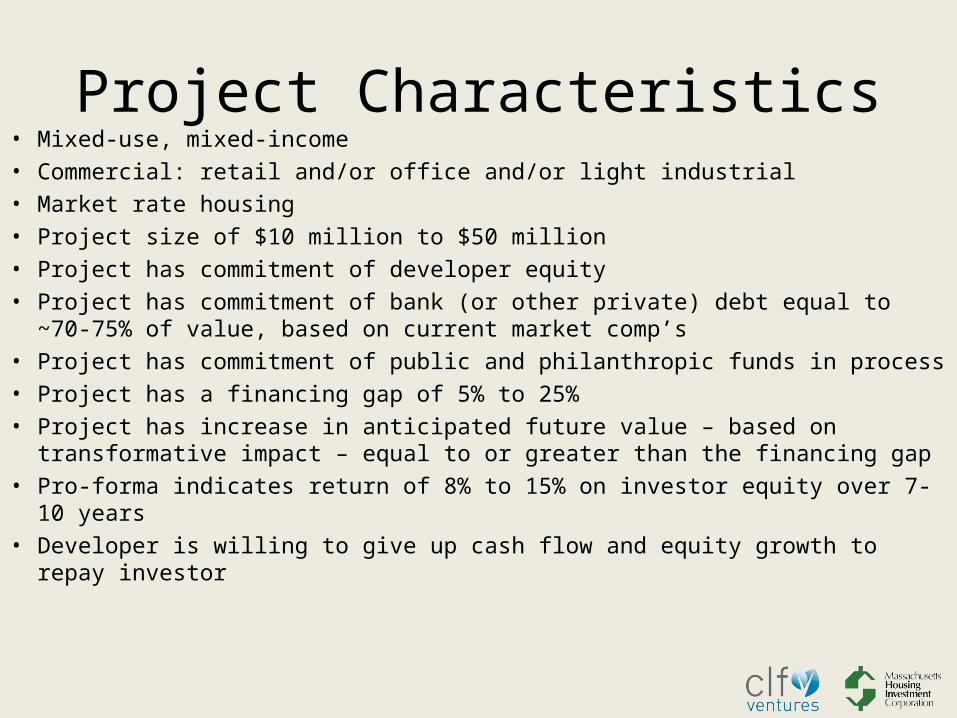

Project Characteristics• Mixed-use, mixed-income• Commercial: retail and/or office and/or light industrial• Market rate housing • Project size of $10 million to $50 million• Project has commitment of developer equity• Project has commitment of bank (or other private) debt equal to ~70-75% of

value, based on current market comp’s• Project has commitment of public and philanthropic funds in process• Project has a financing gap of 5% to 25%• Project has increase in anticipated future value – based on transformative

impact – equal to or greater than the financing gap• Pro-forma indicates return of 8% to 15% on investor equity over 7-10 years• Developer is willing to give up cash flow and equity growth to repay investor

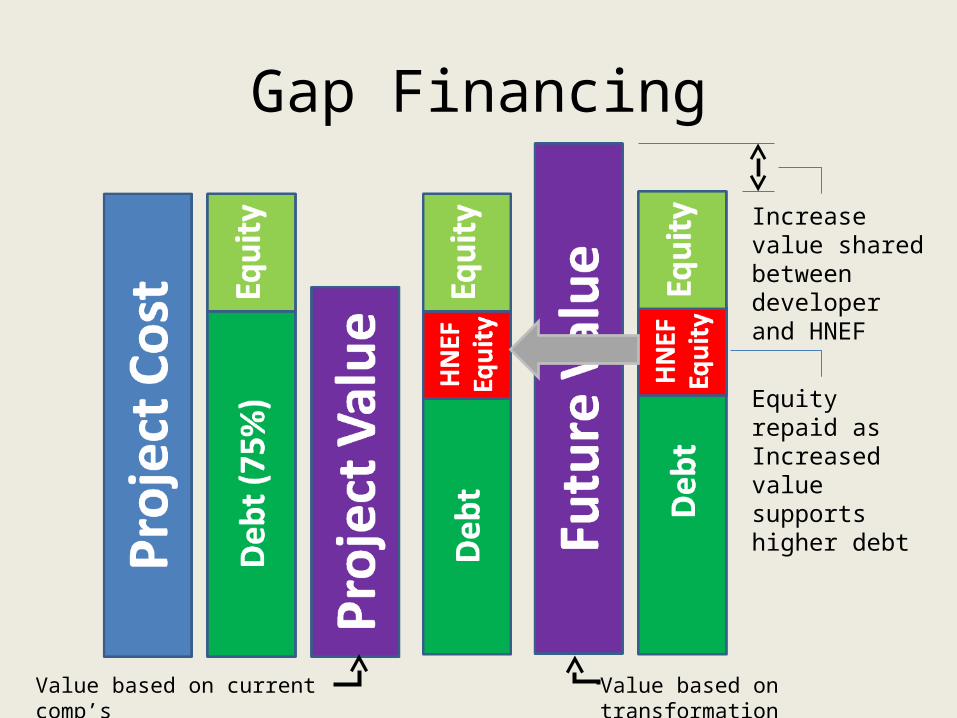

Assumes Value = Cost

• Debt = 75% of Value• Value based on current comp’s

Gap Financing

Gap Financing

Value based on current comp’s Value based on transformation

Increase value shared between developer and HNEF

Equity repaid asIncreased value supports higher debt

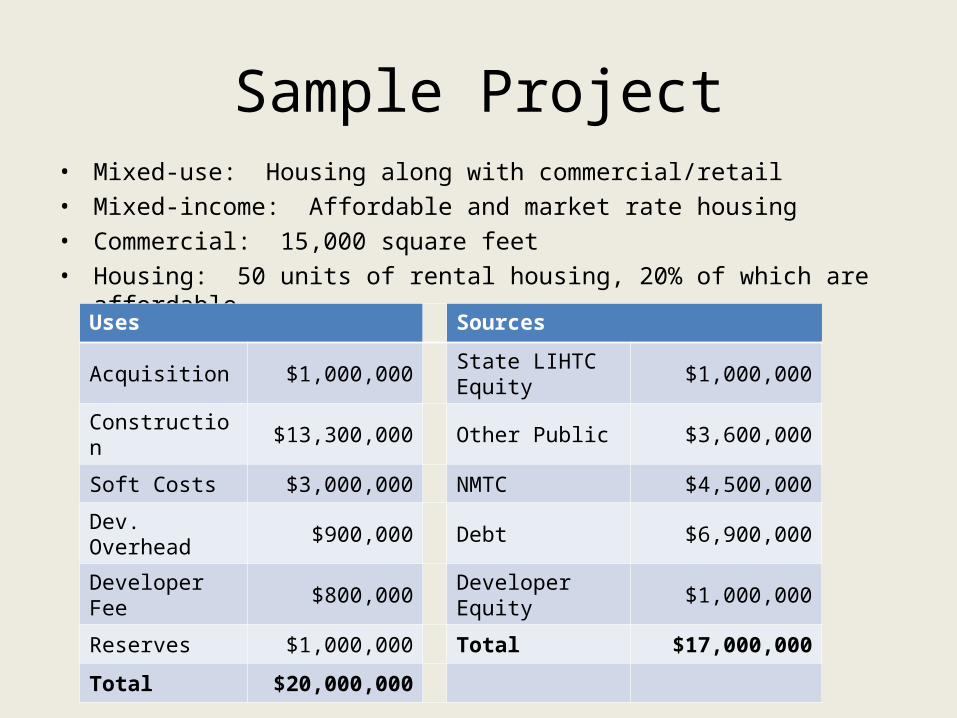

Sample Project• Mixed-use: Housing along with commercial/retail• Mixed-income: Affordable and market rate housing• Commercial: 15,000 square feet• Housing: 50 units of rental housing, 20% of which are affordable

Uses Sources

Acquisition $1,000,000 State LIHTC Equity $1,000,000

Construction $13,300,000 Other Public $3,600,000

Soft Costs $3,000,000 NMTC $4,500,000

Dev. Overhead $900,000 Debt $6,900,000

Developer Fee $800,000 Developer Equity $1,000,000

Reserves $1,000,000 Total $17,000,000

Total $20,000,000

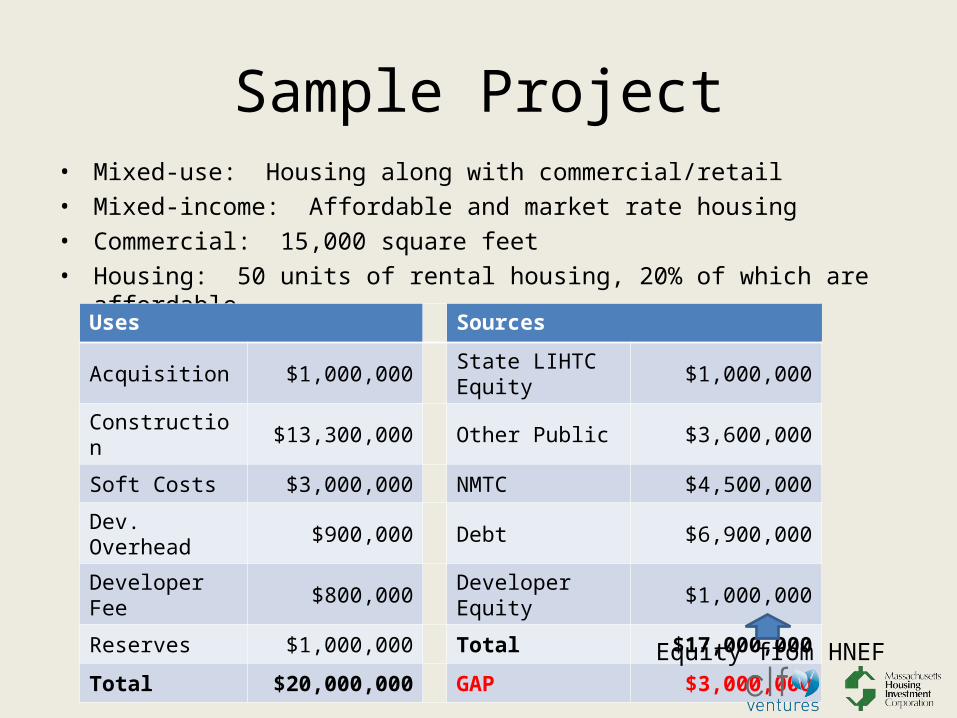

Sample Project• Mixed-use: Housing along with commercial/retail • Mixed-income: Affordable and market rate housing• Commercial: 15,000 square feet• Housing: 50 units of rental housing, 20% of which are affordable

Uses Sources

Acquisition $1,000,000 State LIHTC Equity $1,000,000

Construction $13,300,000 Other Public $3,600,000

Soft Costs $3,000,000 NMTC $4,500,000

Dev. Overhead $900,000 Debt $6,900,000

Developer Fee $800,000 Developer Equity $1,000,000

Reserves $1,000,000 Total $17,000,000

Total $20,000,000 GAP $3,000,000

Equity from HNEF

Fund Structure and Capitalization• The HNEF will be a structured fund with a capital stack aimed at ensuring the fund

can make transformative investments while meeting institutional investors return expectations.

• There will be a “top loss” investor with a tolerance for absorbing risk and lower return expectations, which will offset the return expectations of other investors.

• Program related investments from foundations and social impact investors will form the second tier, who can be expected to moderate their return expectations depending on the strength of the other bottom lines.

• Private (institutional) investors will make up the balance of the fund. • The overall goal of capital development will be to attract investors that will tolerate

a 8-15% blended return. Another objective of the Fund will be to create a blended equity structure with different timing and risk requirements to meet the complex needs of various TOD projects.

• Projects will be underwritten for financial feasibility by MHIC, while CLFV will review for conformance with HNEF’s healthy community goals.

Public Funds

PRI Investor PRI Investor PRI Investor

PrivateInvestor

Sub

ordi

nate

Ret

urn

Sen

ior

Ret

urn

Pari-passu

PrivateInvestor

PrivateInvestor

PrivateInvestor

PrivateInvestor

Capital Structure

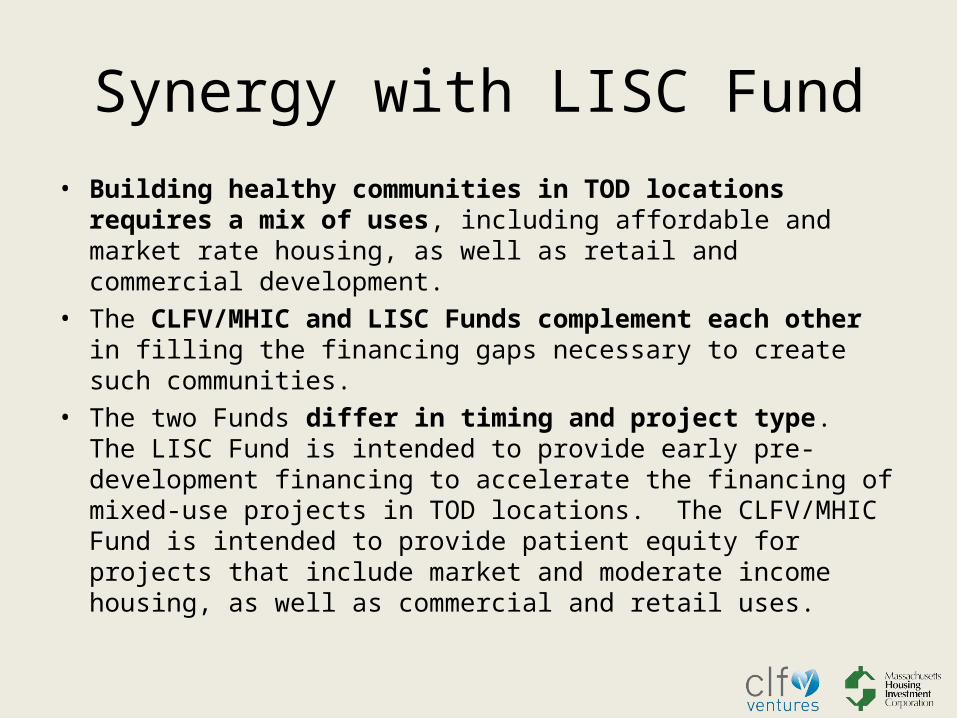

Synergy with LISC Fund• Building healthy communities in TOD locations requires a mix of

uses, including affordable and market rate housing, as well as retail and commercial development.

• The CLFV/MHIC and LISC Funds complement each other in filling the financing gaps necessary to create such communities.

• The two Funds differ in timing and project type. The LISC Fund is intended to provide early pre-development financing to accelerate the financing of mixed-use projects in TOD locations. The CLFV/MHIC Fund is intended to provide patient equity for projects that include market and moderate income housing, as well as commercial and retail uses.

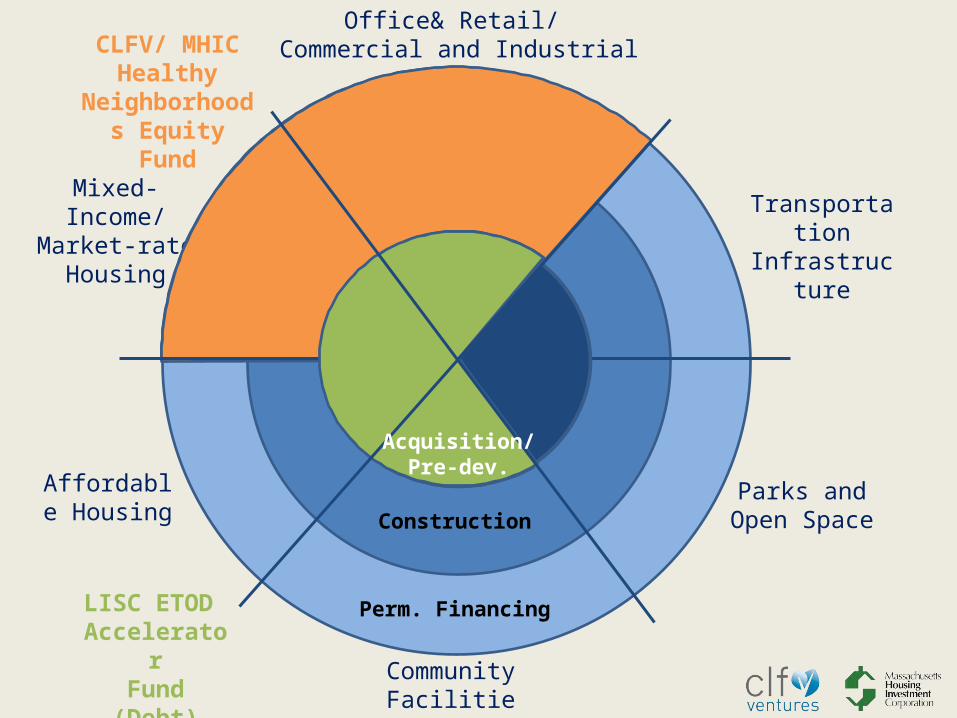

Transit-Oriented Development: Closing

the Financing Gap

Affordable Housing

Mixed-Income/ Market-rate

Housing

Office& Retail/ Commercial and Industrial

CommunityFacilities

Transportation Infrastructure

Parks and Open SpaceConstruction

Perm. FinancingLISC ETOD AcceleratorFund (Debt)

CLFV/ MHIC Healthy

Neighborhoods Equity Fund

Acquisition/Pre-dev.

Achieving Regional and Statewide Goals

• Statewide Goals:• Commonwealth of MA: 10,000 new MF units/ year• HNEF project criteria are consistent with

Commonwealth of Massachusetts “Compact Neighborhoods” principles

• MetroFuture Goals:• TOD neighborhoods in greater Boston have the

potential to accommodate 76,000 new housing units and 133,000 new jobs over the next 25 years

Clarifying questions about Equitable TOD Accelerator Fund

or Healthy Neighborhoods Equity Fund

Questions?

BREAK

SecretaryExecutive Office of Housing and Economic Development

Commonwealth of Massachusetts

Gregory Bialecki

President, LOCUSResponsible Real Estate

Developers and Investors

Christopher B. Leinberger

Thank you for attending today!