today’s international tax landscape global and americas … conference israel_jds...

TRANSCRIPT

Today’s International Tax landscape – global and Americas trends

International Tax Conference

Israel, 9 May 2017

9 May 2017 | International Tax Conference Israel Page 1

Presenters

Jeffrey MichalakEY Americas Director,

International Tax Services

Peter GriffinEY Global and Americas TP Leader,

International Tax Services

Simon Moore

EY Americas Deputy Director,

International Tax Services

9 May 2017 | International Tax Conference Israel Page 2

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst &

Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-

serving member firm of Ernst & Young Global Limited operating in the U.S.

► This presentation is © 2016 Ernst & Young LLP. All rights reserved. No part of this document may

be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or

mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using

any information storage and retrieval system, without written permission from Ernst & Young

LLP. Any reproduction, transmission or distribution of this form or any of the material herein is

prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims

any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent

the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It

does not provide tax advice to any taxpayer because it does not take into account any specific

taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied

upon, as accounting advice.

Tax Policy Trends

9 May 2017 | International Tax Conference Israel Page 4

Key tax and investment issues affecting business

State Aid and Tax Transparency

E-government &Tax Technology

US tax reform

OECD and Tax Policy: BEPS

9 May 2017 | International Tax Conference Israel Page 5

Tax policy trends: the United States

Pre-Trump administration:

► New US Model Treaty

► Taking a hardline on intellectual property (IP) migration

► Increase in transfer pricing court cases

► New regulations issued on contributions of IP to foreign

corporations

► New regulations announced regarding treatment of transfer of IP to

certain partnerships

► Aggressive anti-inversion regulations issued

► Debt vs equity characterization rules issued for foreign investors

9 May 2017 | International Tax Conference Israel Page 6

Tax policy trends: the United States

Post-Trump administration:

► Comprehensive US tax reform

► Significant corporate tax rate reduction

► GOP blueprint vs Trump campaign plan

► Territorial taxation regime vs worldwide taxation without deferral

► Reduction in regulatory activity

► IRS budget reduction

9 May 2017 | International Tax Conference Israel Page 7

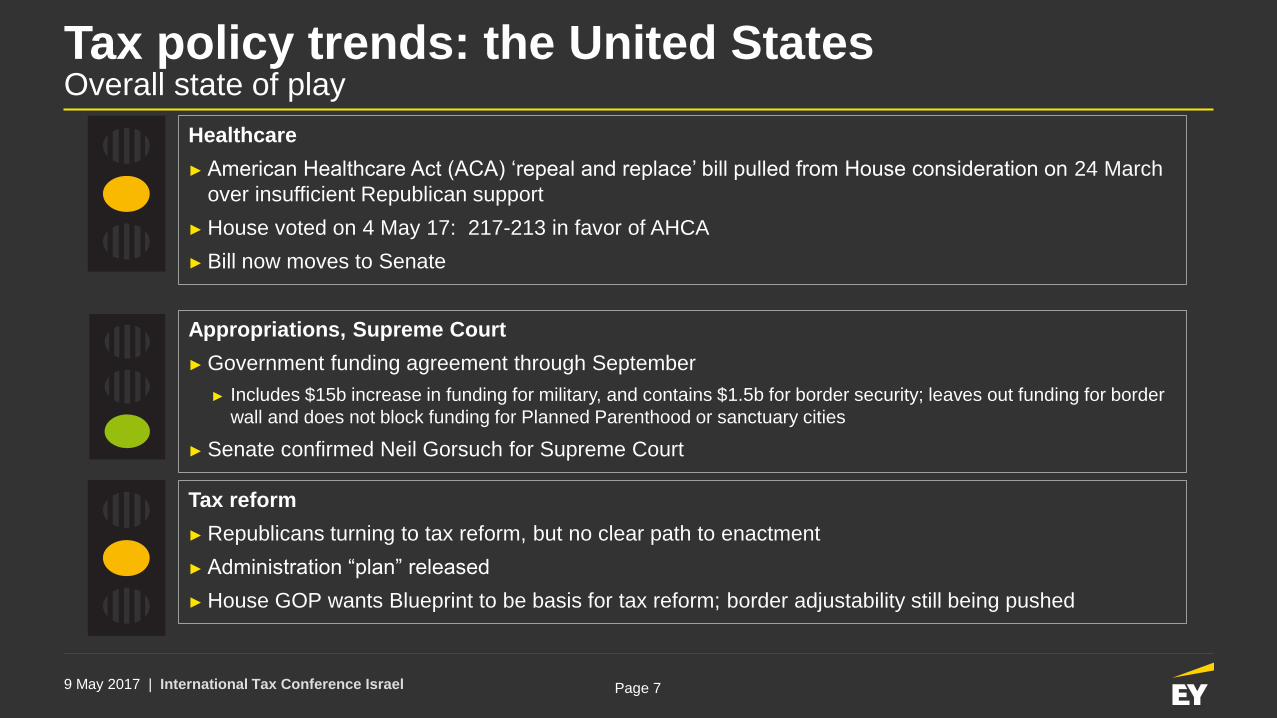

Tax policy trends: the United StatesOverall state of play

Healthcare

► American Healthcare Act (ACA) ‘repeal and replace’ bill pulled from House consideration on 24 March

over insufficient Republican support

► House voted on 4 May 17: 217-213 in favor of AHCA

► Bill now moves to Senate

Appropriations, Supreme Court

► Government funding agreement through September

► Includes $15b increase in funding for military, and contains $1.5b for border security; leaves out funding for border

wall and does not block funding for Planned Parenthood or sanctuary cities

► Senate confirmed Neil Gorsuch for Supreme Court

Tax reform

► Republicans turning to tax reform, but no clear path to enactment

► Administration “plan” released

► House GOP wants Blueprint to be basis for tax reform; border adjustability still being pushed

9 May 2017 | International Tax Conference Israel Page 8

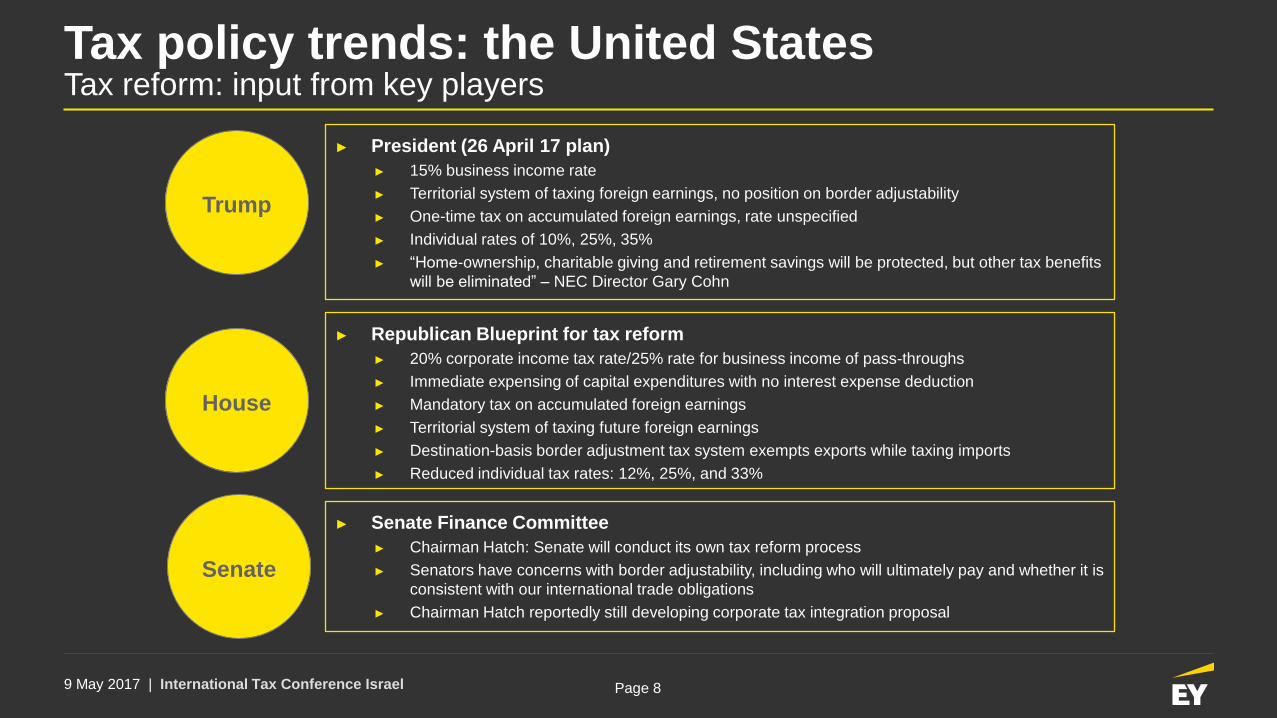

Tax policy trends: the United StatesTax reform: input from key players

► Republican Blueprint for tax reform

► 20% corporate income tax rate/25% rate for business income of pass-throughs

► Immediate expensing of capital expenditures with no interest expense deduction

► Mandatory tax on accumulated foreign earnings

► Territorial system of taxing future foreign earnings

► Destination-basis border adjustment tax system exempts exports while taxing imports

► Reduced individual tax rates: 12%, 25%, and 33%

House

Senate

► Senate Finance Committee

► Chairman Hatch: Senate will conduct its own tax reform process

► Senators have concerns with border adjustability, including who will ultimately pay and whether it is

consistent with our international trade obligations

► Chairman Hatch reportedly still developing corporate tax integration proposal

Trump

► President (26 April 17 plan)

► 15% business income rate

► Territorial system of taxing foreign earnings, no position on border adjustability

► One-time tax on accumulated foreign earnings, rate unspecified

► Individual rates of 10%, 25%, 35%

► “Home-ownership, charitable giving and retirement savings will be protected, but other tax benefits

will be eliminated” – NEC Director Gary Cohn

9 May 2017 | International Tax Conference Israel Page 9

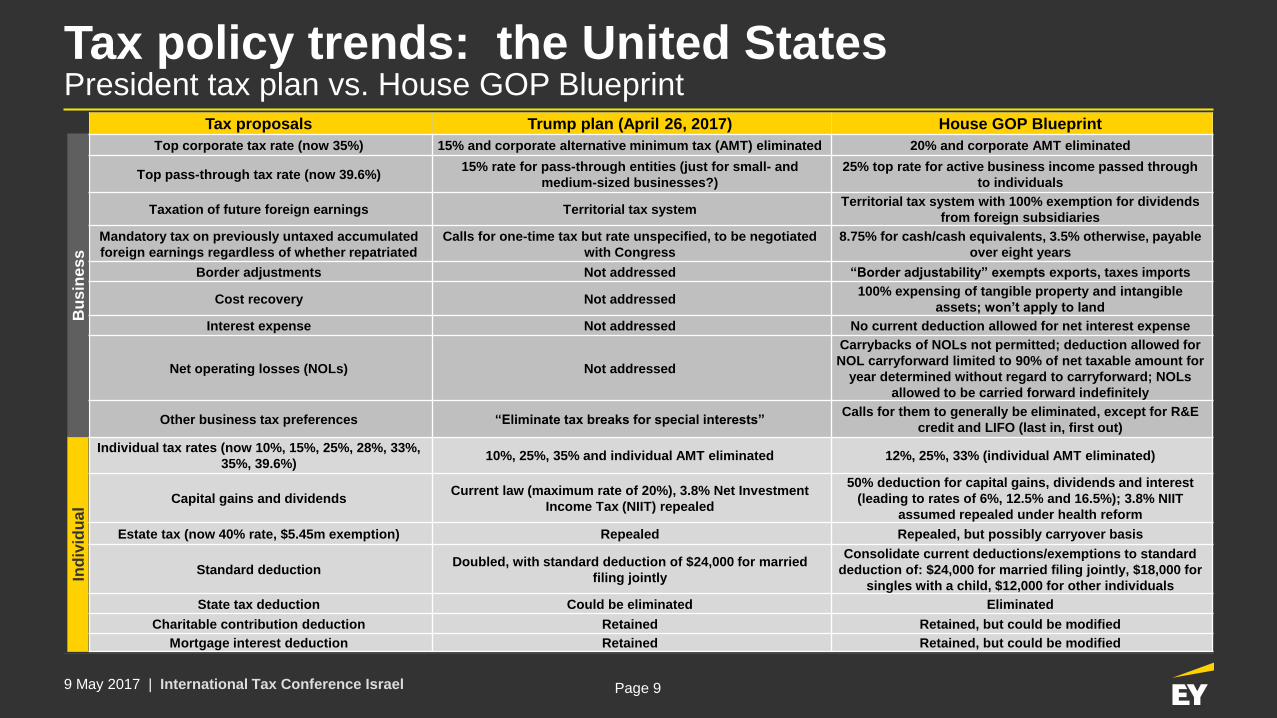

Tax policy trends: the United States President tax plan vs. House GOP Blueprint

Ind

ivid

ua

lB

us

ine

ss

Tax proposals Trump plan (April 26, 2017) House GOP Blueprint

Top corporate tax rate (now 35%) 15% and corporate alternative minimum tax (AMT) eliminated 20% and corporate AMT eliminated

Top pass-through tax rate (now 39.6%)15% rate for pass-through entities (just for small- and

medium-sized businesses?)

25% top rate for active business income passed through

to individuals

Taxation of future foreign earnings Territorial tax systemTerritorial tax system with 100% exemption for dividends

from foreign subsidiaries

Mandatory tax on previously untaxed accumulated

foreign earnings regardless of whether repatriated

Calls for one-time tax but rate unspecified, to be negotiated

with Congress

8.75% for cash/cash equivalents, 3.5% otherwise, payable

over eight years

Border adjustments Not addressed “Border adjustability” exempts exports, taxes imports

Cost recovery Not addressed100% expensing of tangible property and intangible

assets; won’t apply to land

Interest expense Not addressed No current deduction allowed for net interest expense

Net operating losses (NOLs) Not addressed

Carrybacks of NOLs not permitted; deduction allowed for

NOL carryforward limited to 90% of net taxable amount for

year determined without regard to carryforward; NOLs

allowed to be carried forward indefinitely

Other business tax preferences “Eliminate tax breaks for special interests”Calls for them to generally be eliminated, except for R&E

credit and LIFO (last in, first out)

Individual tax rates (now 10%, 15%, 25%, 28%, 33%,

35%, 39.6%)10%, 25%, 35% and individual AMT eliminated 12%, 25%, 33% (individual AMT eliminated)

Capital gains and dividendsCurrent law (maximum rate of 20%), 3.8% Net Investment

Income Tax (NIIT) repealed

50% deduction for capital gains, dividends and interest

(leading to rates of 6%, 12.5% and 16.5%); 3.8% NIIT

assumed repealed under health reform

Estate tax (now 40% rate, $5.45m exemption) Repealed Repealed, but possibly carryover basis

Standard deductionDoubled, with standard deduction of $24,000 for married

filing jointly

Consolidate current deductions/exemptions to standard

deduction of: $24,000 for married filing jointly, $18,000 for

singles with a child, $12,000 for other individuals

State tax deduction Could be eliminated Eliminated

Charitable contribution deduction Retained Retained, but could be modified

Mortgage interest deduction Retained Retained, but could be modified

9 May 2017 | International Tax Conference Israel Page 10

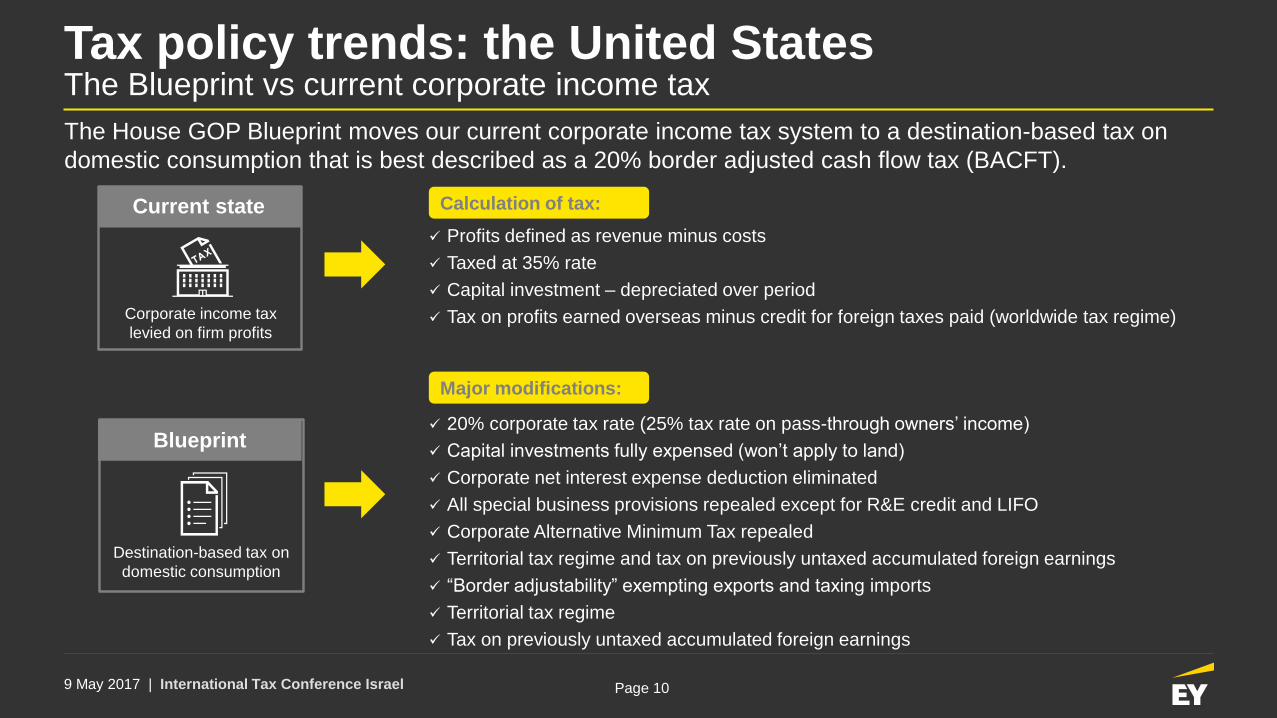

Tax policy trends: the United StatesThe Blueprint vs current corporate income tax

Calculation of tax:

Major modifications:

20% corporate tax rate (25% tax rate on pass-through owners’ income)

Capital investments fully expensed (won’t apply to land)

Corporate net interest expense deduction eliminated

All special business provisions repealed except for R&E credit and LIFO

Corporate Alternative Minimum Tax repealed

Territorial tax regime and tax on previously untaxed accumulated foreign earnings

“Border adjustability” exempting exports and taxing imports

Territorial tax regime

Tax on previously untaxed accumulated foreign earnings

Profits defined as revenue minus costs

Taxed at 35% rate

Capital investment – depreciated over period

Tax on profits earned overseas minus credit for foreign taxes paid (worldwide tax regime)

The House GOP Blueprint moves our current corporate income tax system to a destination-based tax on

domestic consumption that is best described as a 20% border adjusted cash flow tax (BACFT).

Current state

Corporate income tax

levied on firm profits

Blueprint

Destination-based tax on

domestic consumption

9 May 2017 | International Tax Conference Israel Page 11

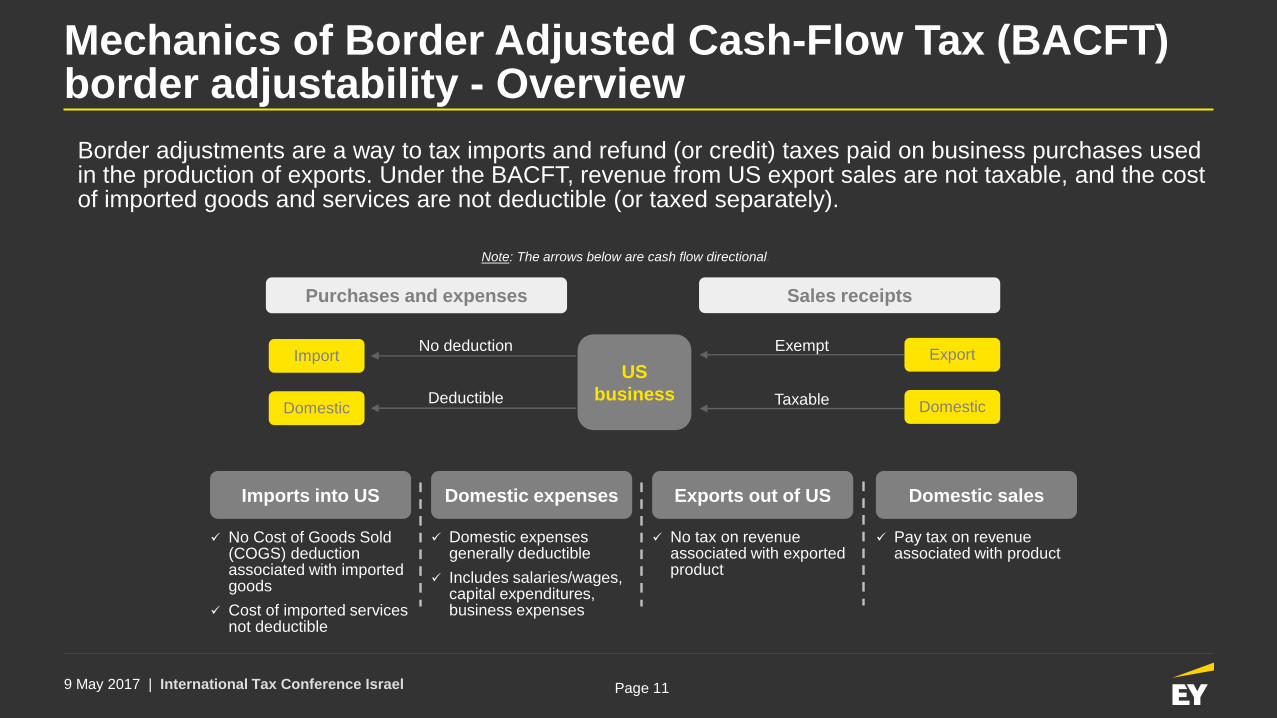

Mechanics of Border Adjusted Cash-Flow Tax (BACFT) border adjustability - Overview

Imports into US Exports out of US Domestic sales

No tax on revenue associated with exported product

No Cost of Goods Sold (COGS) deduction associated with imported goods

Cost of imported services not deductible

Pay tax on revenue associated with product

Border adjustments are a way to tax imports and refund (or credit) taxes paid on business purchases used in the production of exports. Under the BACFT, revenue from US export sales are not taxable, and the cost of imported goods and services are not deductible (or taxed separately).

No deduction Exempt

US

business

Import

Purchases and expenses

DeductibleDomestic

Taxable

Export

Domestic

Sales receipts

Domestic expenses

Domestic expenses generally deductible

Includes salaries/wages, capital expenditures, business expenses

Note: The arrows below are cash flow directional.

9 May 2017 | International Tax Conference Israel Page 12

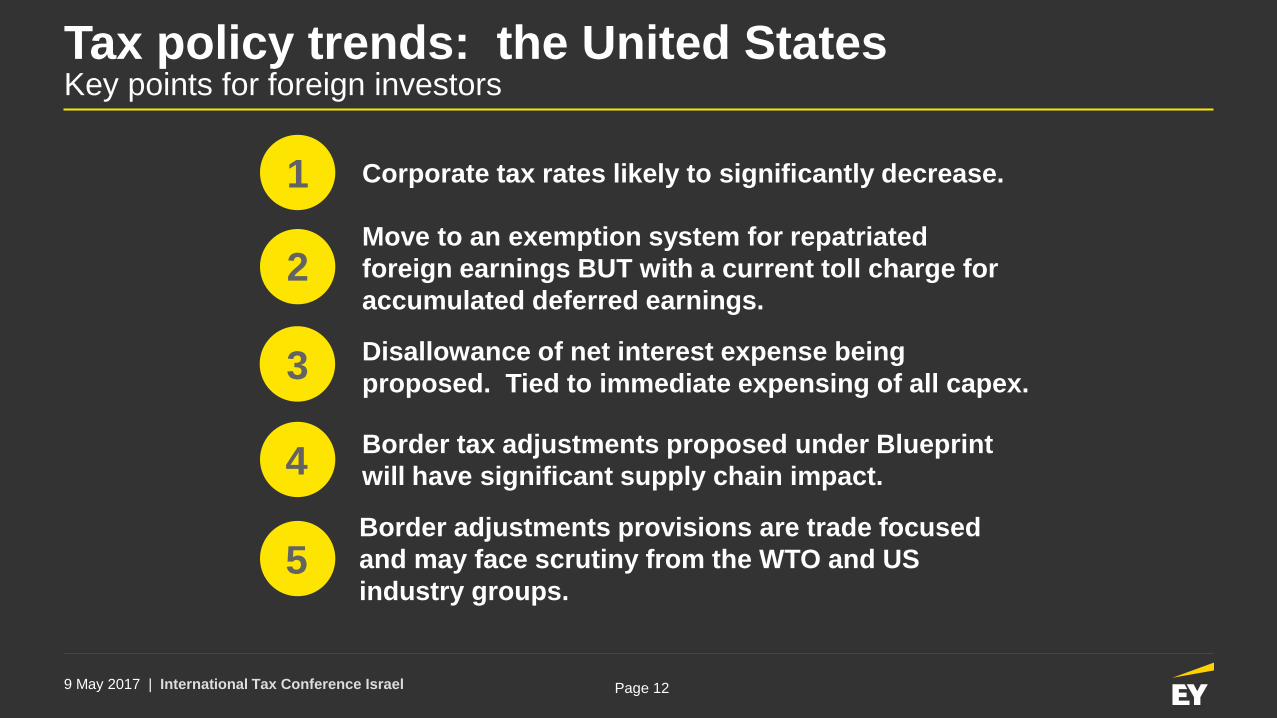

Tax policy trends: the United States Key points for foreign investors

Corporate tax rates likely to significantly decrease.1

2

3

4

Border adjustments provisions are trade focused

and may face scrutiny from the WTO and US

industry groups.5

Move to an exemption system for repatriated

foreign earnings BUT with a current toll charge for

accumulated deferred earnings.

Disallowance of net interest expense being

proposed. Tied to immediate expensing of all capex.

Border tax adjustments proposed under Blueprint

will have significant supply chain impact.

9 May 2017 | International Tax Conference Israel Page 13

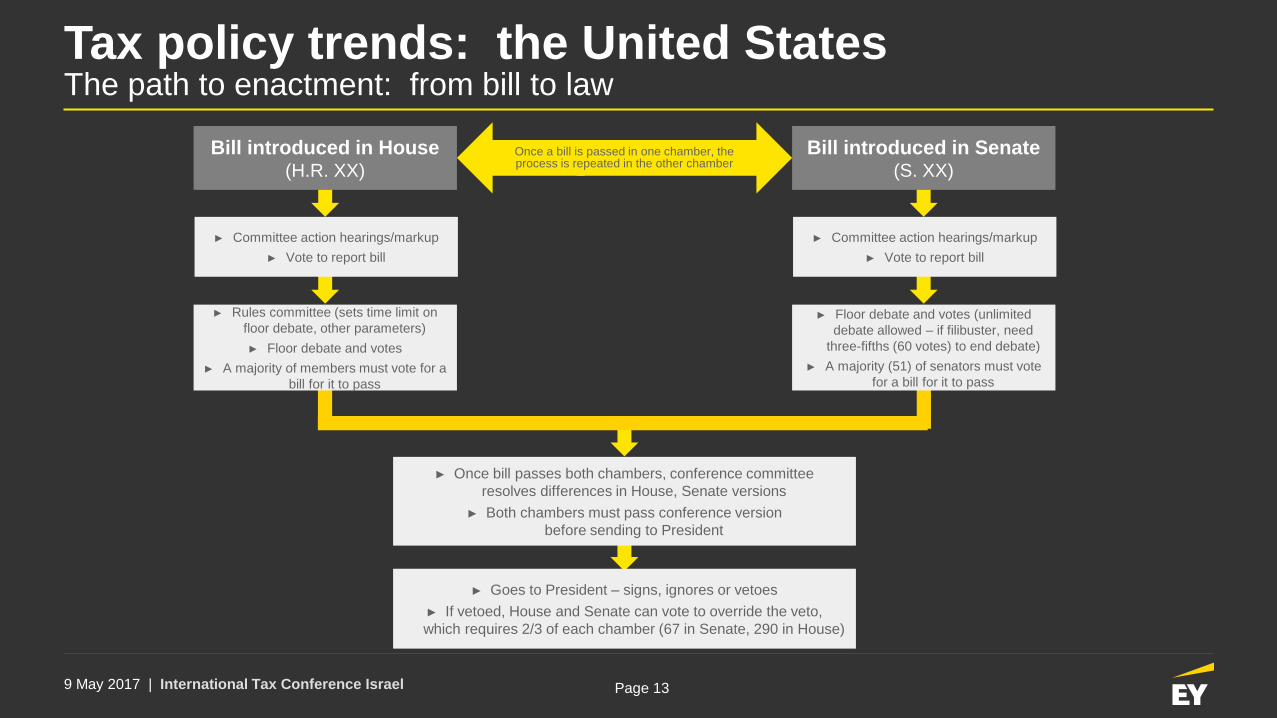

Tax policy trends: the United States The path to enactment: from bill to law

► Goes to President – signs, ignores or vetoes

► If vetoed, House and Senate can vote to override the veto,

which requires 2/3 of each chamber (67 in Senate, 290 in House)

► Once bill passes both chambers, conference committee

resolves differences in House, Senate versions

► Both chambers must pass conference version

before sending to President

► Rules committee (sets time limit on

floor debate, other parameters)

► Floor debate and votes

► A majority of members must vote for a

bill for it to pass

► Floor debate and votes (unlimited

debate allowed – if filibuster, need

three-fifths (60 votes) to end debate)

► A majority (51) of senators must vote

for a bill for it to pass

► Committee action hearings/markup

► Vote to report bill

► Committee action hearings/markup

► Vote to report bill

Bill introduced in House(H.R. XX)

Bill introduced in Senate(S. XX)

Once a bill is passed in one chamber, the process is repeated in the other chamber

9 May 2017 | International Tax Conference Israel Page 14

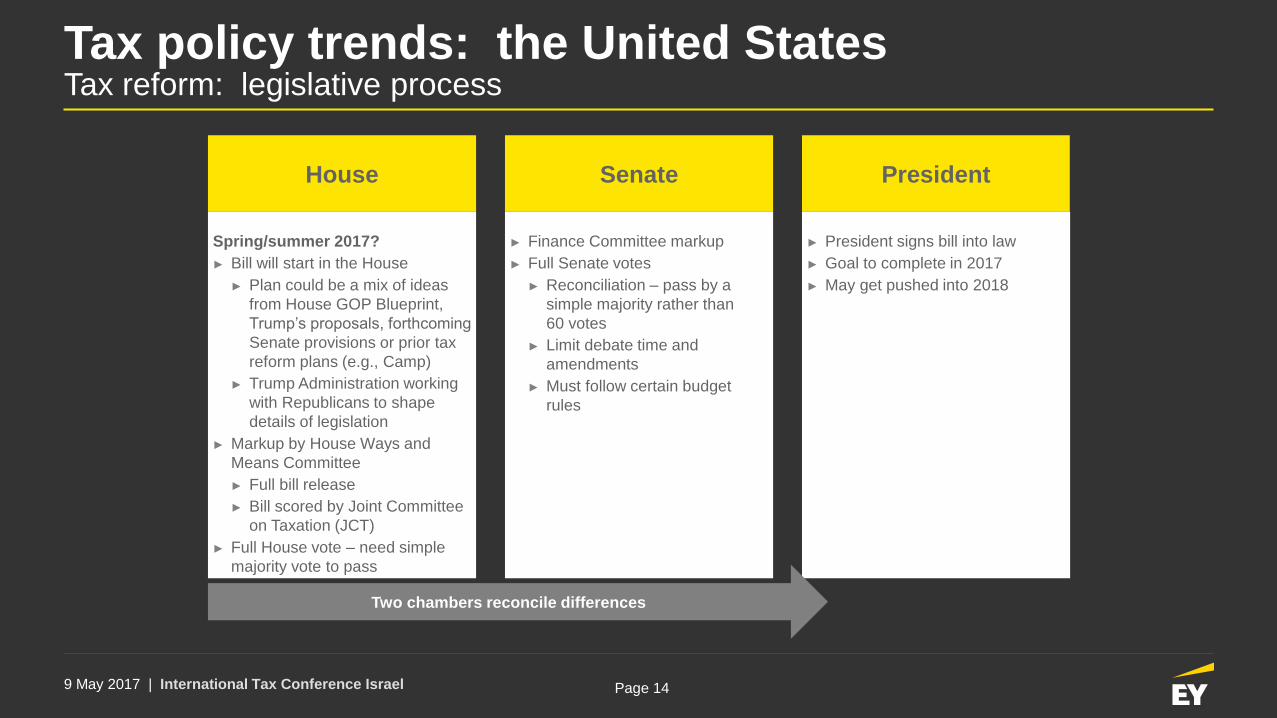

Tax policy trends: the United States Tax reform: legislative process

Spring/summer 2017?

► Bill will start in the House

► Plan could be a mix of ideas

from House GOP Blueprint,

Trump’s proposals, forthcoming

Senate provisions or prior tax

reform plans (e.g., Camp)

► Trump Administration working

with Republicans to shape

details of legislation

► Markup by House Ways and

Means Committee

► Full bill release

► Bill scored by Joint Committee

on Taxation (JCT)

► Full House vote – need simple

majority vote to pass

► Finance Committee markup

► Full Senate votes

► Reconciliation – pass by a

simple majority rather than

60 votes

► Limit debate time and

amendments

► Must follow certain budget

rules

► President signs bill into law

► Goal to complete in 2017

► May get pushed into 2018

Two chambers reconcile differences

House Senate President

9 May 2017 | International Tax Conference Israel Page 15

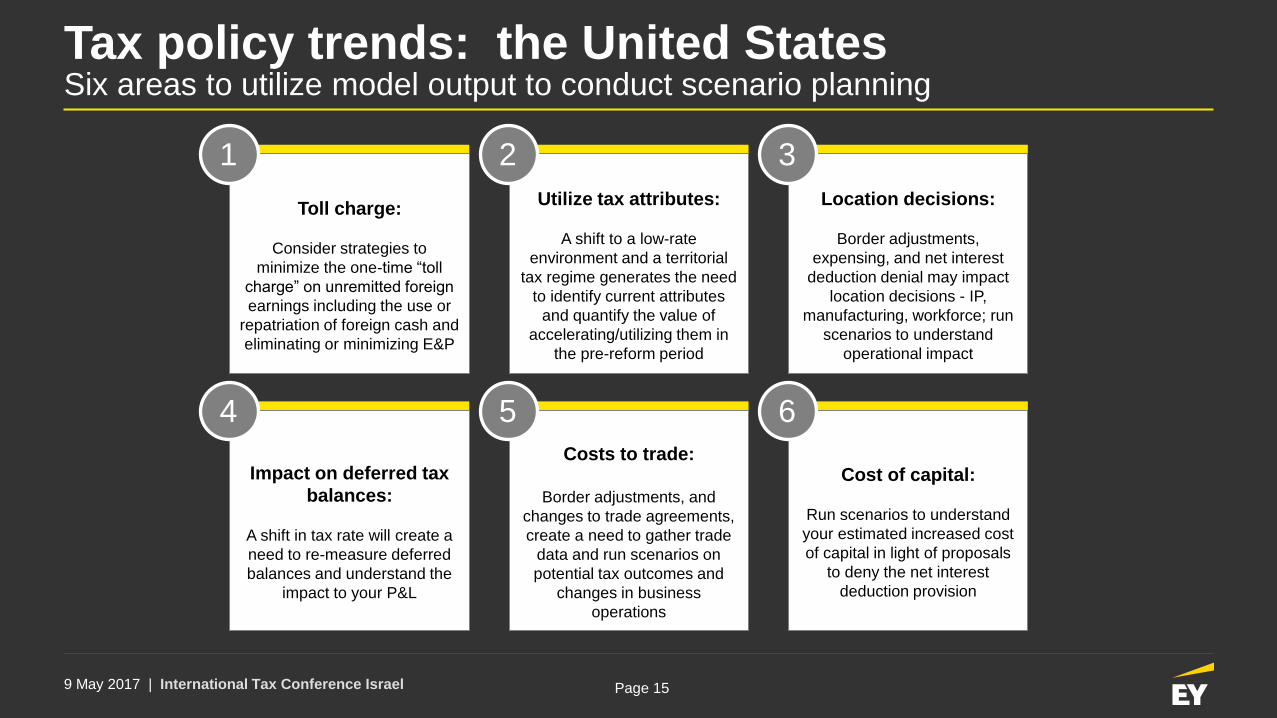

Tax policy trends: the United States Six areas to utilize model output to conduct scenario planning

Toll charge:

Consider strategies to

minimize the one-time “toll

charge” on unremitted foreign

earnings including the use or

repatriation of foreign cash and

eliminating or minimizing E&P

1

Utilize tax attributes:

A shift to a low-rate

environment and a territorial

tax regime generates the need

to identify current attributes

and quantify the value of

accelerating/utilizing them in

the pre-reform period

2

Location decisions:

Border adjustments,

expensing, and net interest

deduction denial may impact

location decisions - IP,

manufacturing, workforce; run

scenarios to understand

operational impact

3

Impact on deferred tax

balances:

A shift in tax rate will create a

need to re-measure deferred

balances and understand the

impact to your P&L

4

Costs to trade:

Border adjustments, and

changes to trade agreements,

create a need to gather trade

data and run scenarios on

potential tax outcomes and

changes in business

operations

5

Cost of capital:

Run scenarios to understand

your estimated increased cost

of capital in light of proposals

to deny the net interest

deduction provision

6

9 May 2017 | International Tax Conference Israel Page 16

Global focus intensifying on corporate taxes

► Economic and revenue needs driving tax policy

► Increasing focus on compliance and enforcement, information sharing,

transparency, analysis of company data

► Taxpayers facing greater tax and reputational risk:

► Globally: Political and economic volatility resulting from “Brexit,” “State aid”

investigations, new or strengthened anti-avoidance rules, data leaks

► Organisation for Economic Co-operation and Development (OECD) Base Erosion

and Profit Shifting (BEPS) project: continuing implementation at country level

► United States: scrutiny of tax dealings, including mergers and overseas

reincorporations (inversions), regulatory activity, calls for tax reform

9 May 2017 | International Tax Conference Israel Page 17

Global snapshot: tax reform

► More than 40% of countries are engaged in significant tax reform activity

► Drivers include:

► Deficits

► Moves to increase competitiveness

► Responses to growing inequality

► Responses to changing capital flows

► Statutory corporate income tax rates are declining

► Organisation for Economic Co-operation and Development (OECD) average dropped from

32.6% in 2000 to 25.2% in 2014

► Many countries deriving more revenue from consumption taxes

► Many countries are moving to more territorial taxation systems

► One goal is to attract investment

9 May 2017 | International Tax Conference Israel Page 18

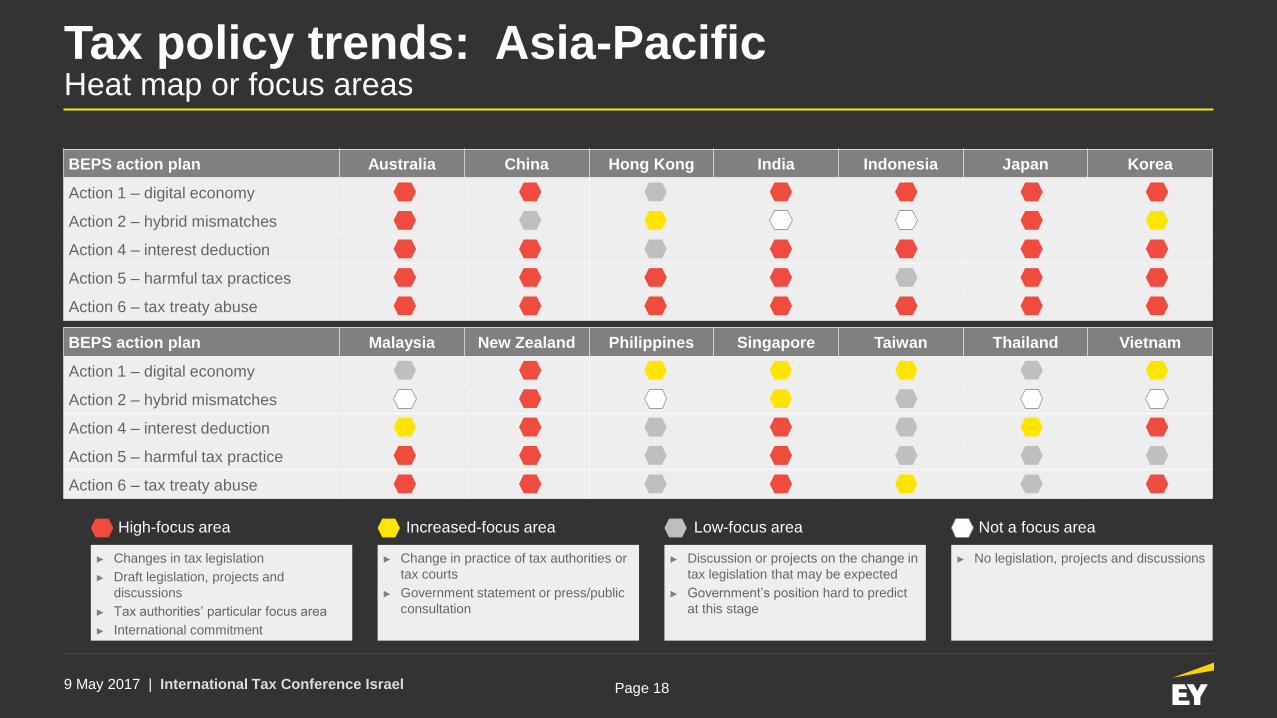

Tax policy trends: Asia-Pacific Heat map or focus areas

BEPS action plan Australia China Hong Kong India Indonesia Japan Korea

Action 1 – digital economy

Action 2 – hybrid mismatches

Action 4 – interest deduction

Action 5 – harmful tax practices

Action 6 – tax treaty abuse

BEPS action plan Malaysia New Zealand Philippines Singapore Taiwan Thailand Vietnam

Action 1 – digital economy

Action 2 – hybrid mismatches

Action 4 – interest deduction

Action 5 – harmful tax practice

Action 6 – tax treaty abuse

► Changes in tax legislation

► Draft legislation, projects and

discussions

► Tax authorities’ particular focus area

► International commitment

► Change in practice of tax authorities or

tax courts

► Government statement or press/public

consultation

► Discussion or projects on the change in

tax legislation that may be expected

► Government’s position hard to predict

at this stage

► No legislation, projects and discussions

High-focus area Increased-focus area Low-focus area Not a focus area

9 May 2017 | International Tax Conference Israel Page 19

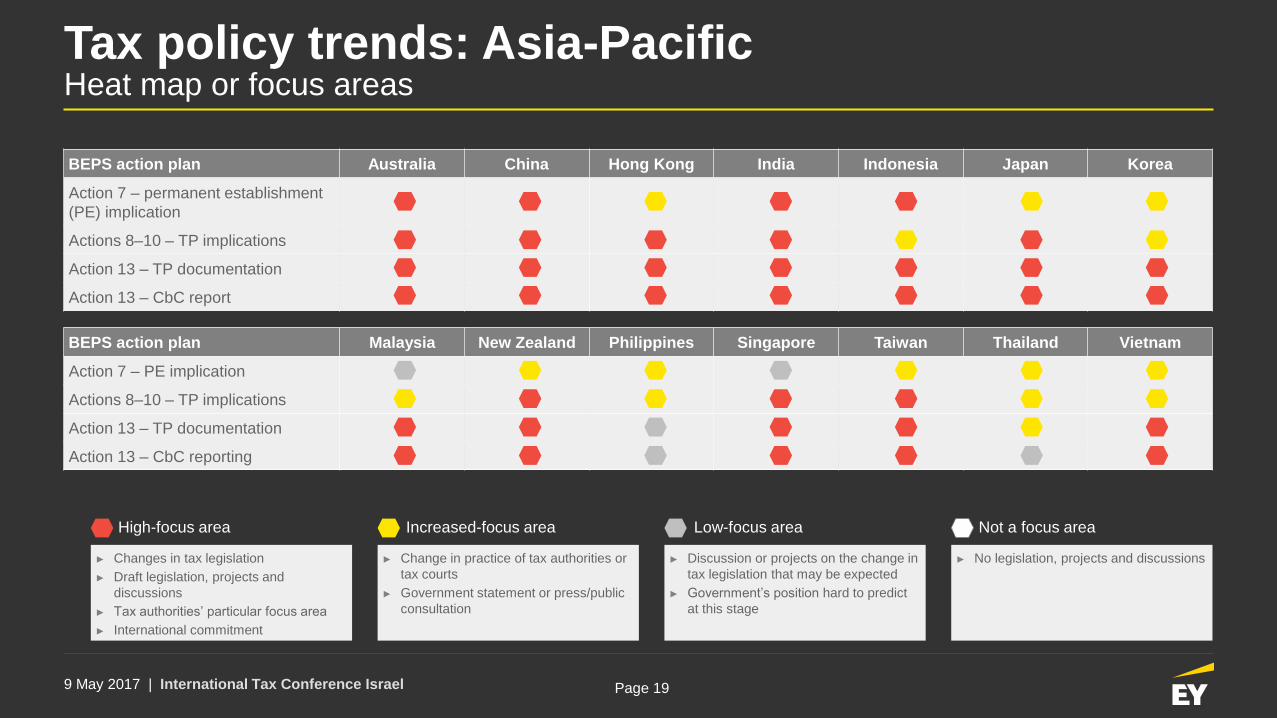

Tax policy trends: Asia-Pacific Heat map or focus areas

BEPS action plan Australia China Hong Kong India Indonesia Japan Korea

Action 7 – permanent establishment

(PE) implication

Actions 8–10 – TP implications

Action 13 – TP documentation

Action 13 – CbC report

BEPS action plan Malaysia New Zealand Philippines Singapore Taiwan Thailand Vietnam

Action 7 – PE implication

Actions 8–10 – TP implications

Action 13 – TP documentation

Action 13 – CbC reporting

► Changes in tax legislation

► Draft legislation, projects and

discussions

► Tax authorities’ particular focus area

► International commitment

► Change in practice of tax authorities or

tax courts

► Government statement or press/public

consultation

► Discussion or projects on the change in

tax legislation that may be expected

► Government’s position hard to predict

at this stage

► No legislation, projects and discussions

High-focus area Increased-focus area Low-focus area Not a focus area

9 May 2017 | International Tax Conference Israel Page 20

Tax policy trends: Latin America Heat map or focus areas

Not a focus areaHigh focus area Increased focus area Low focus area

BEPS action item Argentina Brazil Chile Colombia Mexico Peru Panama

Action 1– Digital economy

Action 2 – Hybrid mismatches

Action 3 – Strengthen CFC rules

Action 4 – Interest deduction (% of EBITDA)

Action 5 – Harmful tax practice

Action 6 – Tax treaty abuse

Action 7 – Prevent artificial avoidance of PE

Action 8. 9 and 10 - Transfer pricing

Action 12 – Disclosure of aggressive tax planning

Action 13 - Transfer pricing documentation

9 May 2017 | International Tax Conference Israel Page 21

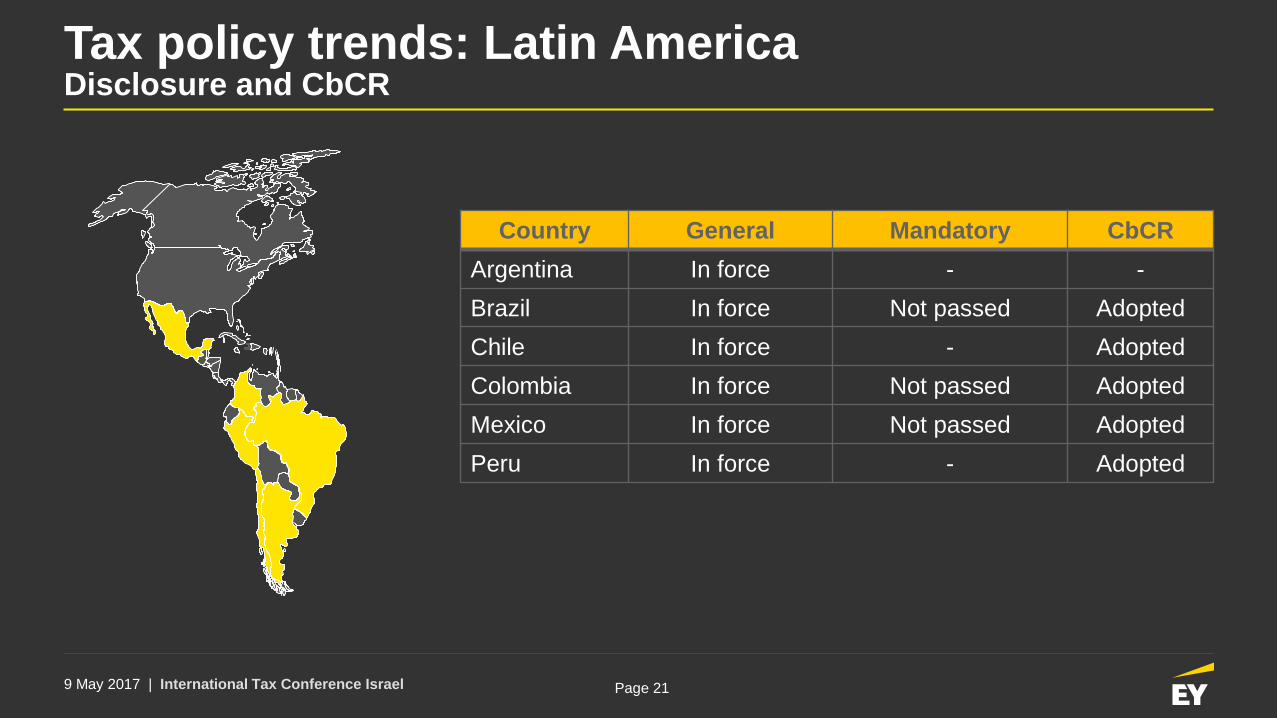

Tax policy trends: Latin AmericaDisclosure and CbCR

Country General Mandatory CbCR

Argentina In force - -

Brazil In force Not passed Adopted

Chile In force - Adopted

Colombia In force Not passed Adopted

Mexico In force Not passed Adopted

Peru In force - Adopted

9 May 2017 | International Tax Conference Israel Page 22

Tax policy trends: European Union

► Two separate legislative initiatives currently active, namely:

i. a two-stage proposal towards a Common Consolidated

Corporate Tax Base (CCCTB);

ii. a Directive on Double Taxation Dispute Resolution

Mechanisms in the European Union (EU); and

9 May 2017 | International Tax Conference Israel Page 23

Tax policy trends: European UnionATAD I

► The ATAD I provides for a broad scope of minimum standards against tax avoidance with respect

to five areas:

1) Interest deductibility limitation (BEPS action 4).

2) General Anti-Abuse Rules (GAAR).

3) Controlled Foreign Company (CFC) rules (BEPS action 3).

4) Hybrid mismatches – limited to hybrid instruments and hybrid entity mismatches between EU

Member States (now replaced with ATAD II) (BEPS action 2)

5) Exit taxation.

► EU Member States are obliged to implement the ATAD I by December 31, 2018 and the rules

should apply as of January 1, 2019. Member States that have national targeted rules preventing

BEPS risks that are equally effective to the interest deduction limitation rule, need to implement

the interest limitation rules not later than 1 January 2024. The exit taxation rule needs to be

transposed in Member States’ national laws not later than 31 December 2019.

9 May 2017 | International Tax Conference Israel Page 24

Tax policy trends: European UnionATAD II

► The ATAD II expands the territorial scope of the minimum standards for

hybrid mismatches to third countries. In addition, the scope is expanded

to:

Hybrid permanent establishment (“PE”) mismatches;

Hybrid transfers;

Imported mismatches;

Reverse hybrid mismatches; and

Dual resident mismatches.

EU Member States are obliged to implement the ATAD II by December 31,

2019 and the rules should apply as of January 1, 2020, except for the rules

on reverse hybrid mismatches that should be implemented by December

31, 2021 and apply as of January 1, 2022.

9 May 2017 | International Tax Conference Israel Page 25

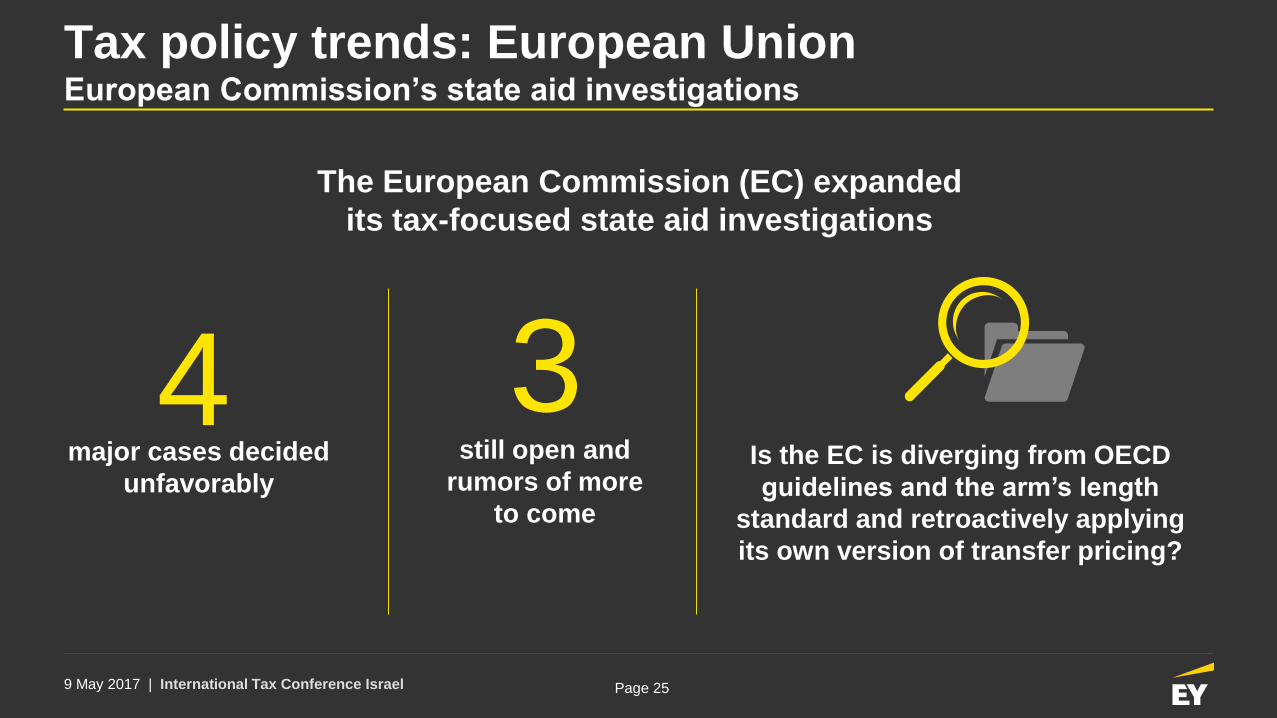

Tax policy trends: European UnionEuropean Commission’s state aid investigations

Is the EC is diverging from OECD

guidelines and the arm’s length

standard and retroactively applying

its own version of transfer pricing?

The European Commission (EC) expanded

its tax-focused state aid investigations

major cases decided

unfavorably

4still open and

rumors of more

to come

3

9 May 2017 | International Tax Conference Israel Page 26

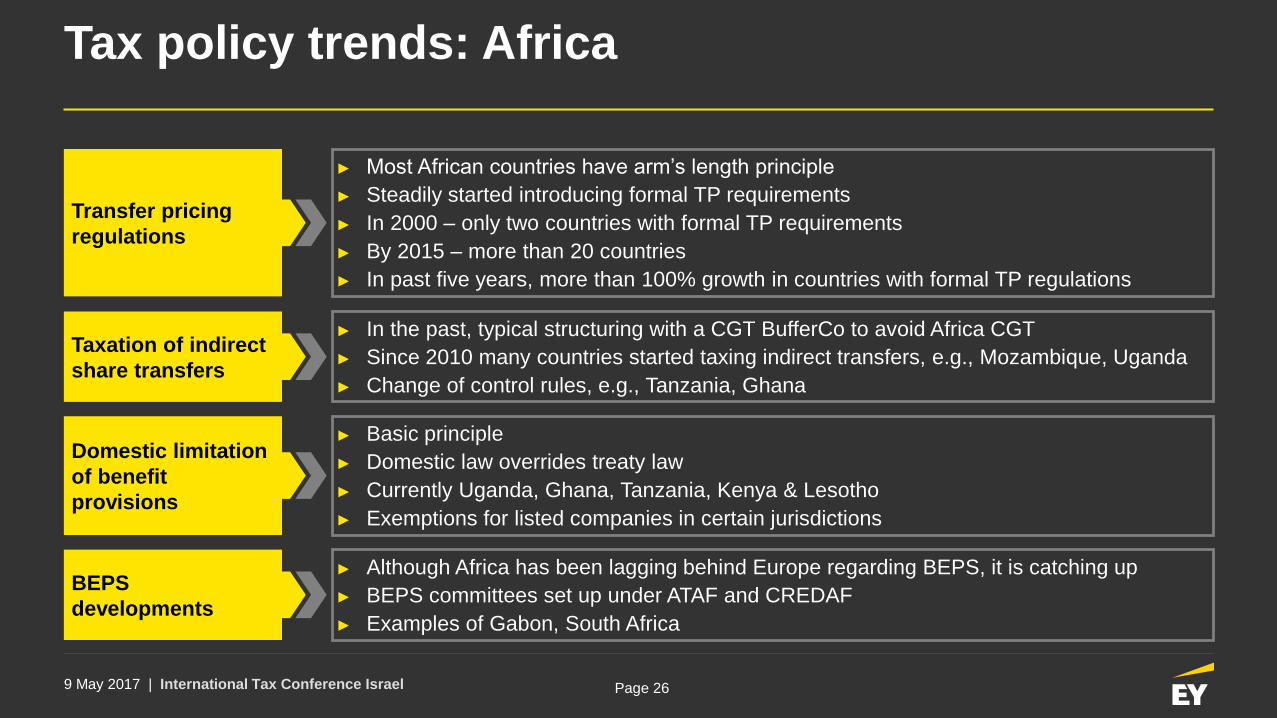

Tax policy trends: Africa

► Although Africa has been lagging behind Europe regarding BEPS, it is catching up

► BEPS committees set up under ATAF and CREDAF

► Examples of Gabon, South Africa

► Basic principle

► Domestic law overrides treaty law

► Currently Uganda, Ghana, Tanzania, Kenya & Lesotho

► Exemptions for listed companies in certain jurisdictions

► In the past, typical structuring with a CGT BufferCo to avoid Africa CGT

► Since 2010 many countries started taxing indirect transfers, e.g., Mozambique, Uganda

► Change of control rules, e.g., Tanzania, Ghana

► Most African countries have arm’s length principle

► Steadily started introducing formal TP requirements

► In 2000 – only two countries with formal TP requirements

► By 2015 – more than 20 countries

► In past five years, more than 100% growth in countries with formal TP regulations

Transfer pricing

regulations

Taxation of indirect

share transfers

Domestic limitation

of benefit

provisions

BEPS

developments

Tax Treaty Developments

9 May 2017 | International Tax Conference Israel Page 28

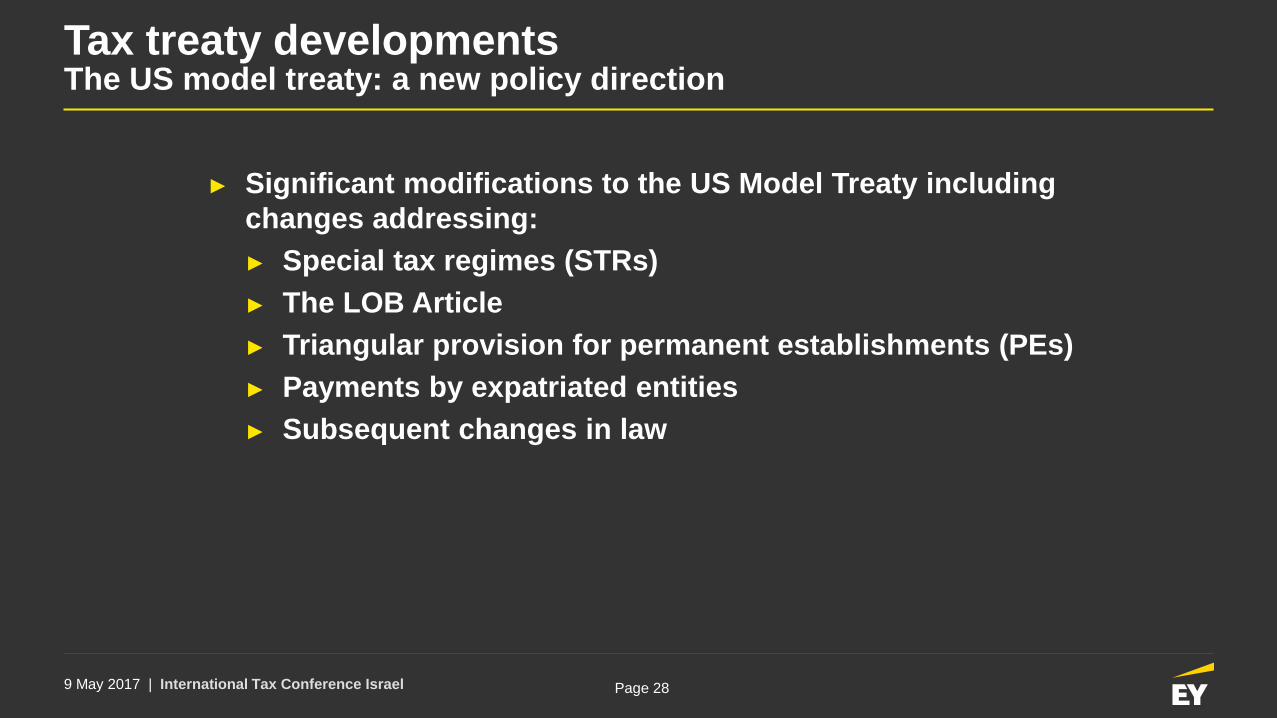

Tax treaty developmentsThe US model treaty: a new policy direction

► Significant modifications to the US Model Treaty including

changes addressing:

► Special tax regimes (STRs)

► The LOB Article

► Triangular provision for permanent establishments (PEs)

► Payments by expatriated entities

► Subsequent changes in law

9 May 2017 | International Tax Conference Israel Page 29

Tax treaty developmentsBEPS Multilateral instrument

• Revision of Art. 1 to address fiscally

transparent entities;

• Measures to address issues with the

application of the exemption method.

• Minimum standard on treaty abuse: PPT,

PPT + simplified LOB or detailed LOB +

supplemented conduit rules

• A “saving clause”;

• Specific Anti-Abuse Rules:• certain dividend transfer transactions;

• transactions involving immovable

property holding companies;

• situations of dual-resident entities; and

• treaty shopping using third-country PEs.

Acti

on

7A

cti

on

6A

cti

on

14

Andorra, Argentina, Australia, Austria, Azerbaijan, Bangladesh, Barbados, Belgium, Benin, Bhutan,

Brazil, Bulgaria, Burkina Faso, Cameroon, Canada, Chile, China, Colombia, Costa Rica, Cote

d'Ivoire, Croatia, Cyprus, Czech Republic, Denmark, Dominican Republic, Egypt, Estonia, Fiji,

Finland, France, Gabon, Georgia, Germany, Greece, Guatemala, Guernsey, Haiti, Hong Kong,

Hungary, Iceland, India, Indonesia, Ireland, Isle of Man, Israel, Italy, Jamaica, Japan, Jersey, Jordan,

Kazakhstan, Kenya, Latvia, Lebanon, Liberia, Liechtenstein, Lithuania, Luxembourg, Malaysia,

Malta, Marshall Islands, Mauritania, Mauritius, Mexico, Mongolia, Morocco, Netherlands, New

Zealand, Nigeria, Norway, Pakistan, Philippines, Poland, Portugal, Qatar, Republic of Moldova,

Romania, Russia, San Marino, Saudi Arabia, Senegal, Serbia, Singapore, Slovakia, Slovenia, South

Africa, South Korea, Spain, Sri Lanka, Swaziland, Sweden, Switzerland, Tanzania, Thailand,

Tunisia, Turkey, Ukraine, United Kingdom, United States, Uruguay, Vietnam, Zambia and Zimbabwe.

Acti

on

2

• Measures to address commissionnaire

arrangements and similar strategies;

• Modifications to the specific activity

exemptions under Article 5(4); and

• measures to address the splitting-up of

contracts to abuse the exception in Article

5(3)

• Measures included in the minimum

standards and best practices, including: • Changes to paragraphs 1 through 3 of

Article 25

• inclusion of paragraph 2 of Article 9 of

the OECD Model.

• Option for mandatory binding MAP

arbitration.

Countries member of the ad hoc group on the MLI

The MLI is open for signature since 31 December 2016. A first high-level signing ceremony will take place in the week beginning on 5 June 2017.

9 May 2017 | International Tax Conference Israel Page 30

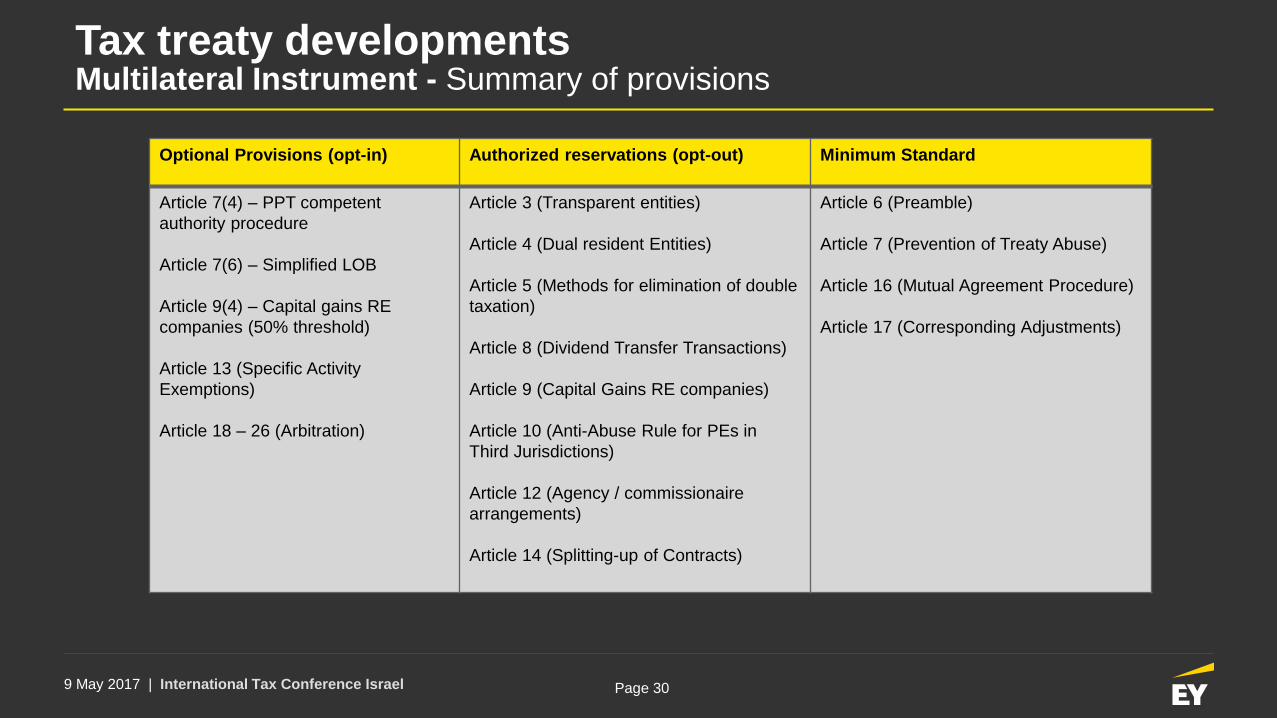

Tax treaty developmentsMultilateral Instrument - Summary of provisions

Optional Provisions (opt-in) Authorized reservations (opt-out) Minimum Standard

Article 7(4) – PPT competent

authority procedure

Article 7(6) – Simplified LOB

Article 9(4) – Capital gains RE

companies (50% threshold)

Article 13 (Specific Activity

Exemptions)

Article 18 – 26 (Arbitration)

Article 3 (Transparent entities)

Article 4 (Dual resident Entities)

Article 5 (Methods for elimination of double

taxation)

Article 8 (Dividend Transfer Transactions)

Article 9 (Capital Gains RE companies)

Article 10 (Anti-Abuse Rule for PEs in

Third Jurisdictions)

Article 12 (Agency / commissionaire

arrangements)

Article 14 (Splitting-up of Contracts)

Article 6 (Preamble)

Article 7 (Prevention of Treaty Abuse)

Article 16 (Mutual Agreement Procedure)

Article 17 (Corresponding Adjustments)

9 May 2017 | International Tax Conference Israel Page 31

Tax treaty developmentsTimeline

► Currently in excess of 3000 treaties in force and OECD expects

amendments to at least 2000

► Envisaged timeline below:

► Open for signatories since 31 December 2016

► Formal signing ceremony week commencing 5 June 2017

► Ratification under domestic law procedures

► Earliest impact January 1, 2019

At the moment of signature countries are required to provide a list of notifications so that Signatories will have the opportunity to discuss.

24 November 2016 1 January 2017 Week 5 June 2017 Uncertain: for early adapters at the earliest 1 January 2019

MLI was agreed MLI open for signature High-level signing ceremony Entry intro effect

The MLI will enter into force after five countries have ratified it. It will only apply for a specific tax treaty after all parties to that treaty have ratified the MLI and a certain period has passed.

Emerging trend: the new digital tax reality

IP alignment and the nexus approach in Israel

9 May 2017 | International Tax Conference Israel Page 34

The impact of BEPS on IP structures

Low

High

Tax risk

Low HighPost-BEPS profit attribution

Offshore IP Co with

limited functions

Onshore IP Co with

limited functions

Onshore IP Co with

commercial risk

management functions

Offshore

“cashbox” IP Co

► Funding of IP

► Decisions made remotely from

IP Co

Plus

► Regular, substantive board of directors meetings

► Potential IP or risk management committee or branch

operations

Plus

► Tax-resident IP owner (e.g., entitled to

amortization)

► Local management of certain functions, such as

supply chain operations or regional sales

Plus

Management of all relevant commercial

risks, including DEMPE functions (see next

slide)

Offshore IP Co refers to an entity that is located in a tax haven or otherwise not a tax resident.

9 May 2017 | International Tax Conference Israel Page 35

DEMPE and strategic, tactical and operational functions pyramid to align with allocation of profits

Strategic

Tactical

Operational

Develop

Enhance

Maintain

Protect

Exploit

Strategic and tactical (centralized) versus operational (local) DEMPE functions

9 May 2017 | International Tax Conference Israel Page 36

Thank you | תֹוָדה

9 May 2017 | International Tax Conference Israel Page 37

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services.

The insights and quality services we deliver help build trust and

confidence in the capital markets and in economies the world over. We

develop outstanding leaders who team to deliver on our promises to all of

our stakeholders. In so doing, we play a critical role in building a better

working world for our people, for our clients and for our communities.

EY refers to the global organization and may refer to one or more of the

member firms of Ernst & Young Global Limited, each of which is a

separate legal entity. Ernst & Young Global Limited, a UK company

limited by guarantee, does not provide services to clients. For more

information about our organization, please visit ey.com.

© 2017 EYGM Limited.

All Rights Reserved.

BSC no. 1701-2158674

ED None

Information in this publication is intended to provide only a general outline

of the subjects covered. It should neither be regarded as comprehensive

nor sufficient for making decisions, nor should it be used in place of

professional advice. Ernst & Young LLP accepts no responsibility for any

loss arising from any action taken or not taken by anyone using this

material.

ey.com