training workshop for iufr reporting - macpmacp.gov.in/sites/default/files/user_doc/ppt on...

TRANSCRIPT

Training Workshop for IUFR reporting

Disclaimer:

This training material is not a

substitute for materials/ circulars

issued by PIU / PCU.

The Views mentioned in this

presentation are personal views of

Paper Presenter.

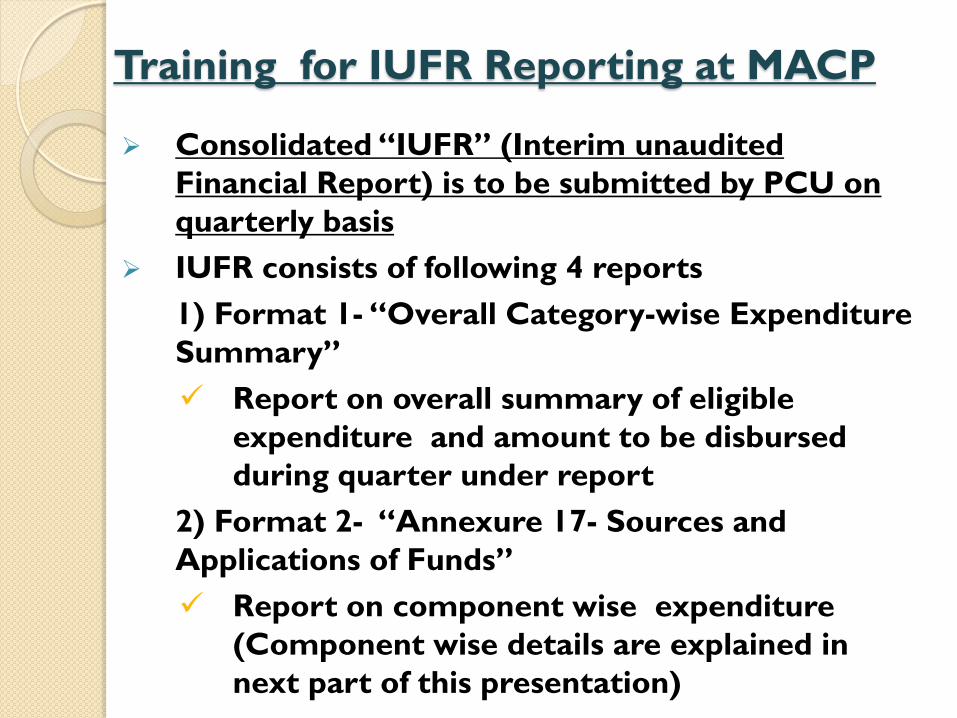

Training for IUFR Reporting at MACP

Consolidated “IUFR” (Interim unaudited

Financial Report) is to be submitted by PCU on

quarterly basis

IUFR consists of following 4 reports

1) Format 1- “Overall Category-wise Expenditure

Summary”

Report on overall summary of eligible

expenditure and amount to be disbursed

during quarter under report

2) Format 2- “Annexure 17- Sources and

Applications of Funds”

Report on component wise expenditure

(Component wise details are explained in

next part of this presentation)

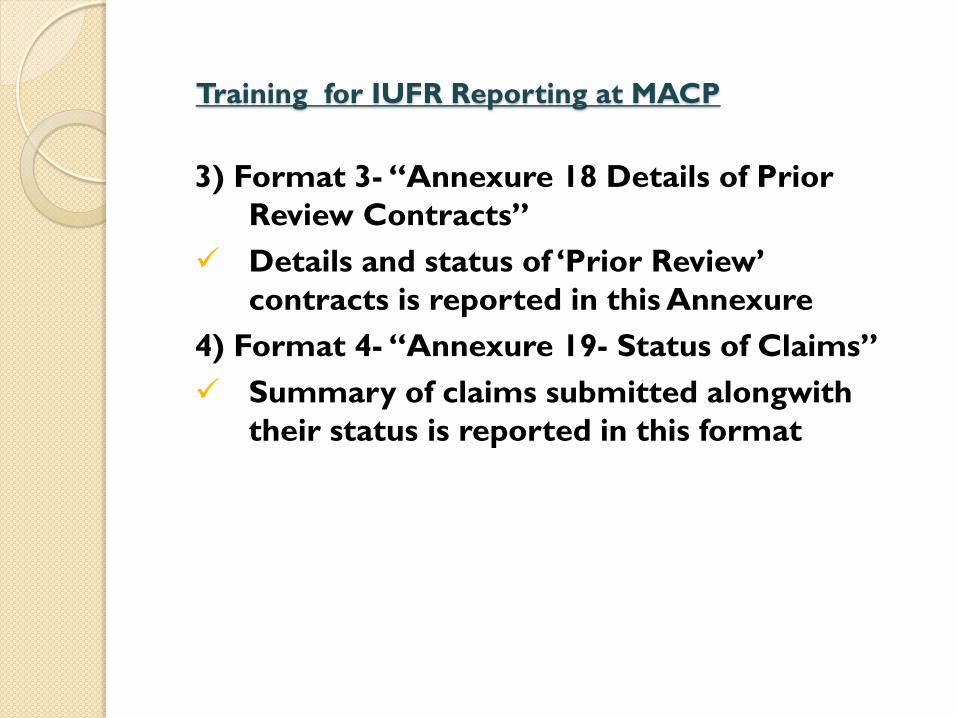

Training for IUFR Reporting at MACP

3) Format 3- “Annexure 18 Details of Prior

Review Contracts”

Details and status of ‘Prior Review’

contracts is reported in this Annexure

4) Format 4- “Annexure 19- Status of Claims”

Summary of claims submitted alongwith

their status is reported in this format

Overview on Components in IUFR Format 2

Component A- Intensification and diversification of

Market Led Production

A1(i)-Institutional strengthening for Market led Technology Transfer

In this component expenditure on following activities to be reported

1. Strengthening of Agriculture Technology Management Agencies (ATMA- located at district places) in terms of

- Manpower,

- Physical facilities (required computers, printer, furniture, etc.)

2. Strengthening of Farm Information and Advisory Centers (FIACs- located at Taluka places reporting to ATMA)

3. Strengthening of Inter-departmental Working Group and inter-departmental Coordination

PIU Agri & ATMA only to report expenses in this component

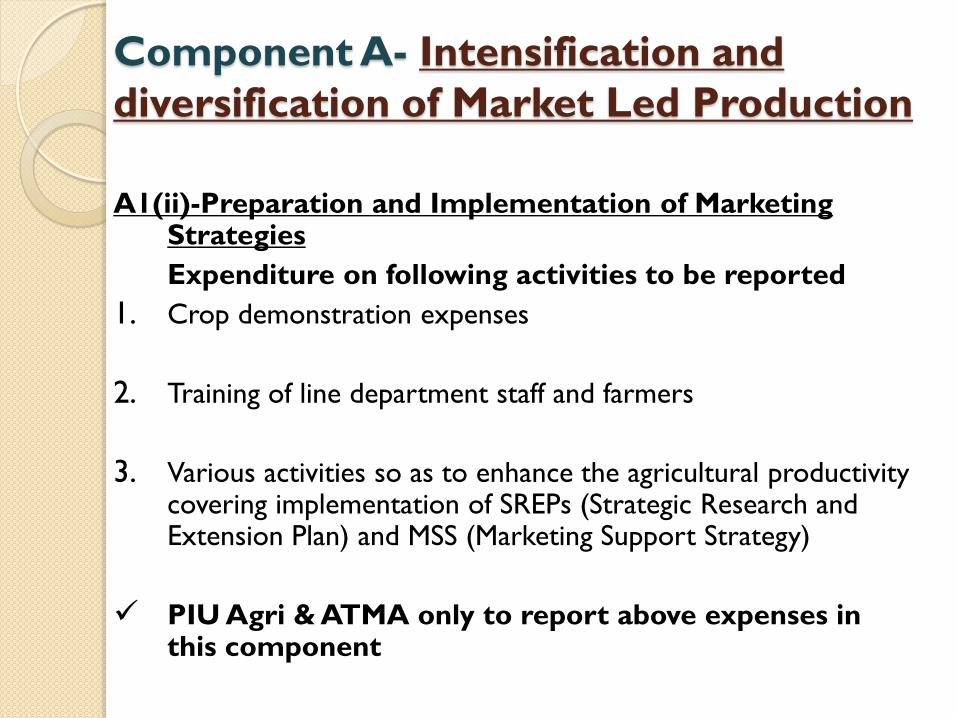

Component A- Intensification and

diversification of Market Led Production

A1(ii)-Preparation and Implementation of Marketing Strategies

Expenditure on following activities to be reported

1. Crop demonstration expenses

2. Training of line department staff and farmers

3. Various activities so as to enhance the agricultural productivity covering implementation of SREPs (Strategic Research and Extension Plan) and MSS (Marketing Support Strategy)

PIU Agri & ATMA only to report above expenses in this component

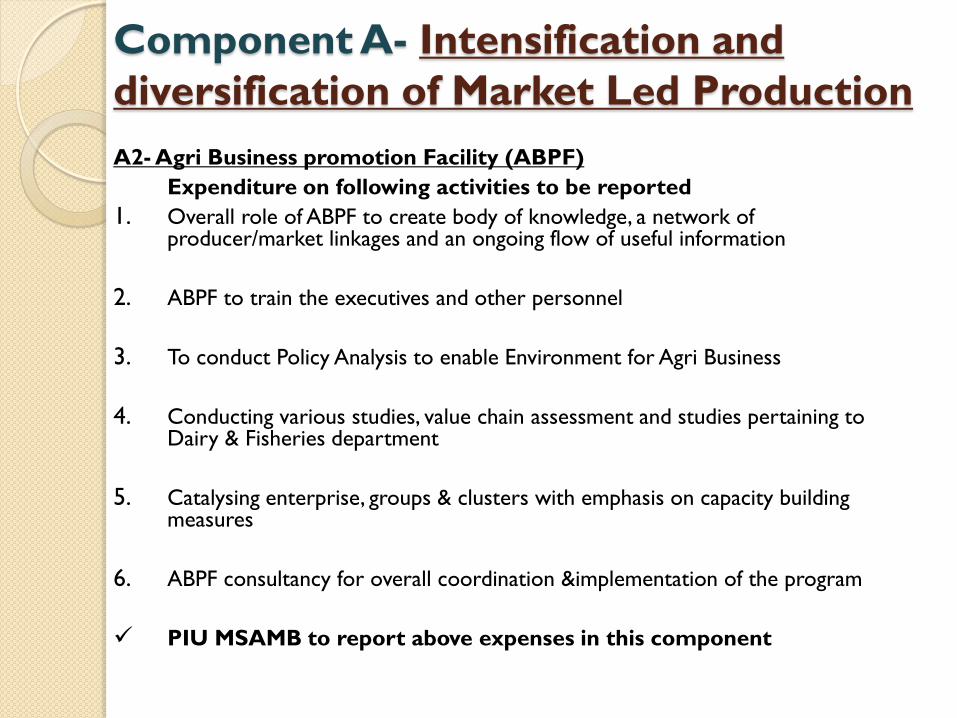

Component A- Intensification and

diversification of Market Led Production

A2- Agri Business promotion Facility (ABPF)

Expenditure on following activities to be reported

1. Overall role of ABPF to create body of knowledge, a network of producer/market linkages and an ongoing flow of useful information

2. ABPF to train the executives and other personnel

3. To conduct Policy Analysis to enable Environment for Agri Business

4. Conducting various studies, value chain assessment and studies pertaining to Dairy & Fisheries department

5. Catalysing enterprise, groups & clusters with emphasis on capacity building measures

6. ABPF consultancy for overall coordination &implementation of the program

PIU MSAMB to report above expenses in this component

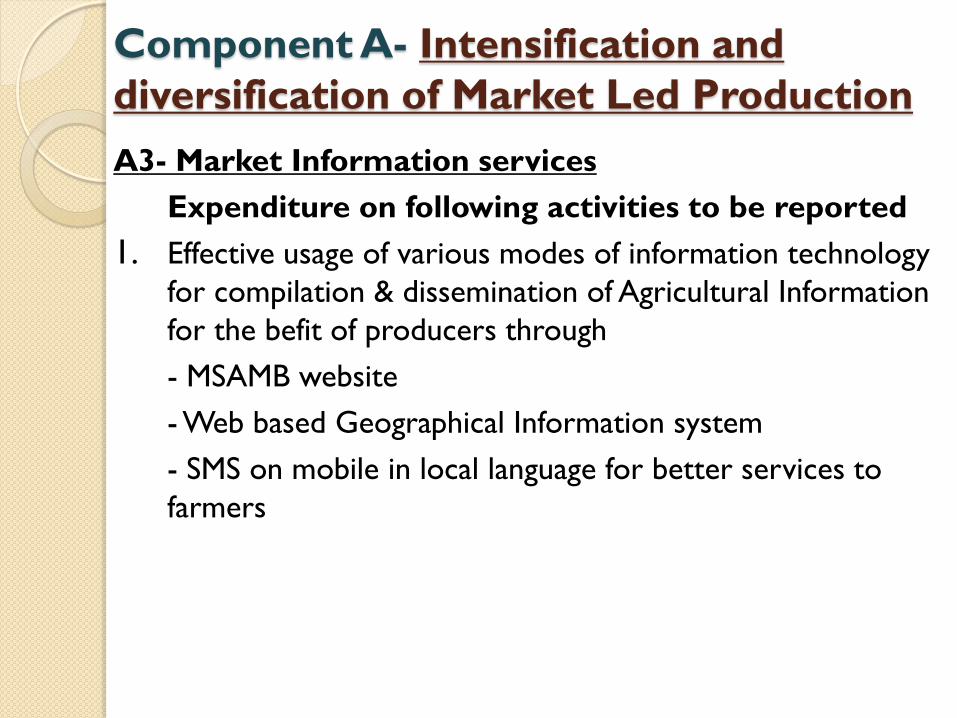

Component A- Intensification and

diversification of Market Led Production

A3- Market Information services

Expenditure on following activities to be reported

1. Effective usage of various modes of information technology

for compilation & dissemination of Agricultural Information

for the befit of producers through

- MSAMB website

- Web based Geographical Information system

- SMS on mobile in local language for better services to

farmers

Component A- Intensification and

diversification of Market Led Production

2. To improve agricultural marketing system by providing web

based e-trading platform through virtual markets in the

state

PIU MSAMB to report above expenses in this

component

Component A- Intensification and

diversification of Market Led Production

A4- Livestock Support Services

Expenditure on following activities to be reported

1. Support to be provided to small farmers for formation of

federation for conducting first aid, health care, high yielding

fodder crops and organised marketing of live animals for

breeding/ meat purposes

2. Demonstration, Cum Production unit, where farmers will be

encouraged to promote goat as high value enterprise

PIU AHD and district level offices of AHD only to

report above mentioned expenses in this

component

Component B- Improving Farmer

Access to Markets

B1- Promoting Alternative markets

B1.1 Product Aggregation through farmer Groups/

Farmer Service Centres

Expenditure on following activities to be reported

1. Basic infrastructure (Stage I) like improvement of temporary

storage & drying, common pack house, plastic crades, tables

etc. to be provided at producers associations for FCSC

Component B- Improving Farmer

Access to Markets

2. Stage II infrastructure investment for Agrimart includes

computer with internet connectivity, display board with

Accessories

PIU MSAMB through DDRC works on this

component and above expenses to be reported in

this component

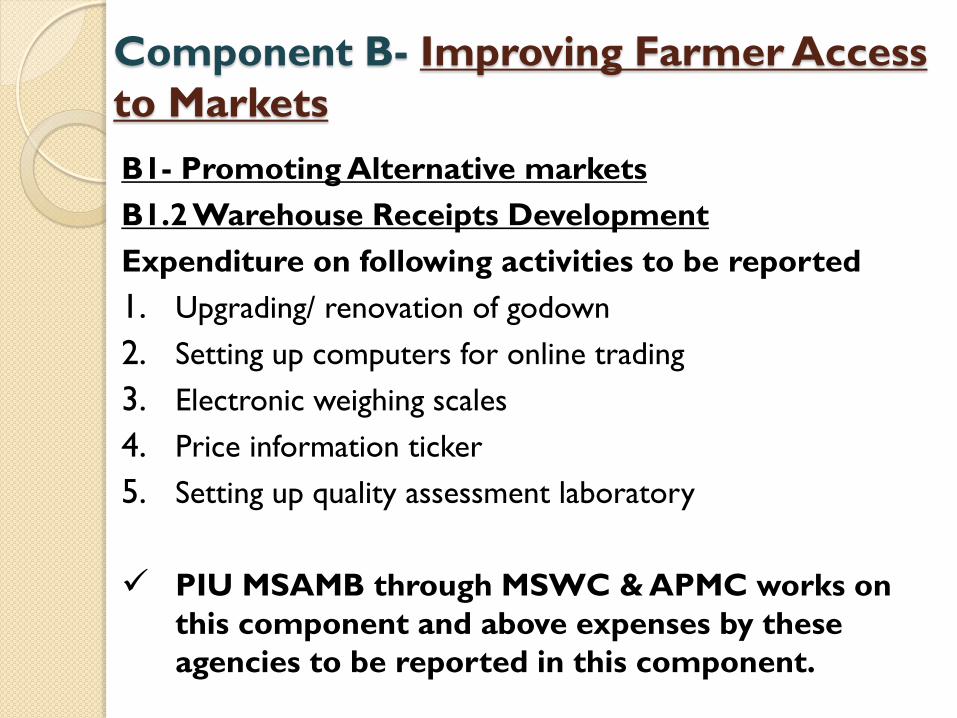

Component B- Improving Farmer Access

to Markets

B1- Promoting Alternative markets

B1.2 Warehouse Receipts Development

Expenditure on following activities to be reported

1. Upgrading/ renovation of godown

2. Setting up computers for online trading

3. Electronic weighing scales

4. Price information ticker

5. Setting up quality assessment laboratory

PIU MSAMB through MSWC & APMC works on

this component and above expenses by these

agencies to be reported in this component.

Component B- Improving Farmer Access

to Markets

B1- Promoting Alternative markets

B1.3 Rural Haat Markets

Expenditure on following activities to be reported

1. Basic infrastructure facility for 300 rural haats i.e. Platforms

with sheds for producers, pathways for buyers, electricity,

drinking water etc.

2. Productive infrastructure like Godown, small cold storage,

grading & packing unit etc. will be provided

PIU MSAMB through DDRC for Rural Haat works

on this component and above expenses by these

agencies to be reported in this component.

Component B- Improving Farmer Access

to Markets

B1- Promoting Alternative markets

B1.4 Introducing E-Marketing Platforms

Expenditure on following activities to be reported

1. 294 e-trading platforms are proposed to be made available

to the sellers (farmers) as well as the buyers (traders,

processors, exporters)

PIU MSAMB works on this component and above

expenses to be reported in this component.

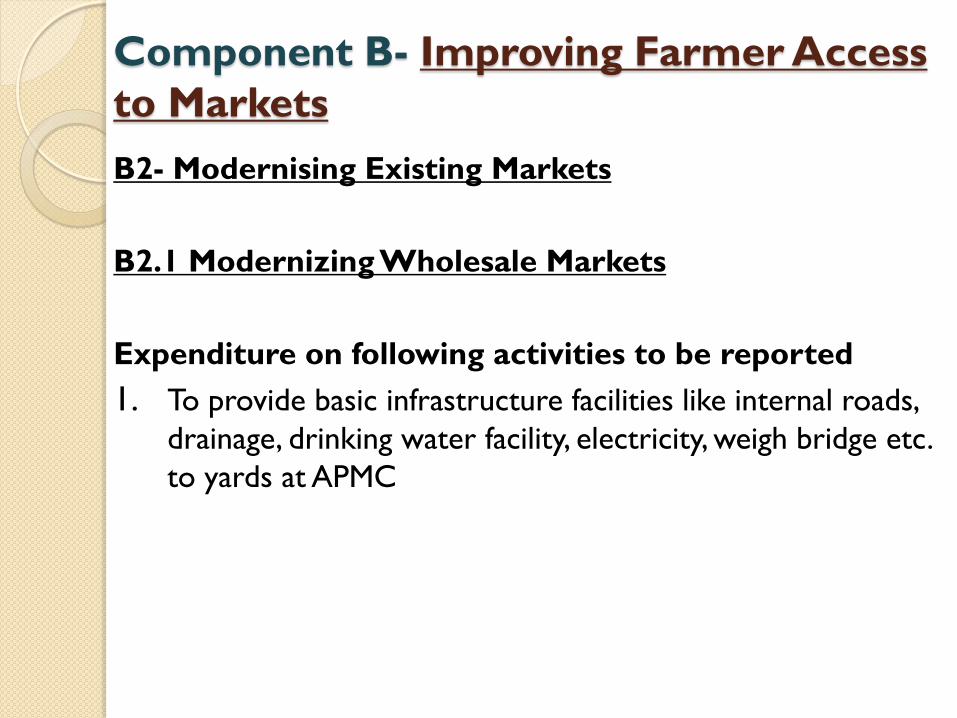

Component B- Improving Farmer Access

to Markets

B2- Modernising Existing Markets

B2.1 Modernizing Wholesale Markets

Expenditure on following activities to be reported

1. To provide basic infrastructure facilities like internal roads,

drainage, drinking water facility, electricity, weigh bridge etc.

to yards at APMC

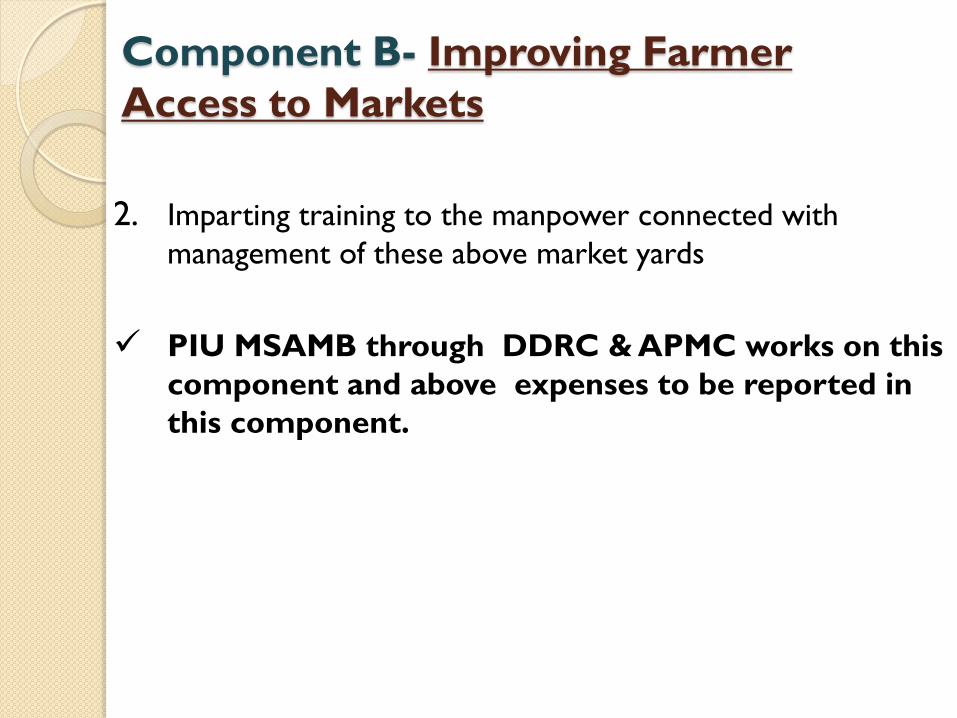

Component B- Improving Farmer Access

to Markets

2. Imparting training to the manpower connected with

management of these APMCs

3. To provide productive infrastructure like electronic auction

halls, food grain packing machine etc.

PIU MSAMB through APMC works on this

component and above expenses to be reported in

this component.

Component B- Improving Farmer

Access to Markets

B2- Modernising Existing Markets

B2.2 Upgrading Livestock yards

Expenditure on following activities to be reported

1. To provide basic infrastructure facilities like sheds for

animals, weighing machines, milking machines, waste disposal

arrangements, etc. for Live Stock Market (LSM) Yards and

Small Ruminant Market yards under local authorities

Component B- Improving Farmer

Access to Markets

2. Imparting training to the manpower connected with

management of these above market yards

PIU MSAMB through DDRC & APMC works on this

component and above expenses to be reported in

this component.

Component C- Project Management

C(i)1- Project Co-ordination Unit and Project

Implementation Units (PIUs)

Expenditure on following activities to be reported

1. Expenditure incurred by PCU and respective PIUs

2. Assisting the line departments for their annual plans and

budgets

Expenses of PCU, PIU-AM (MSAMB), PIU-Agri ,

PIU-AHD reports their expenses under this

component.

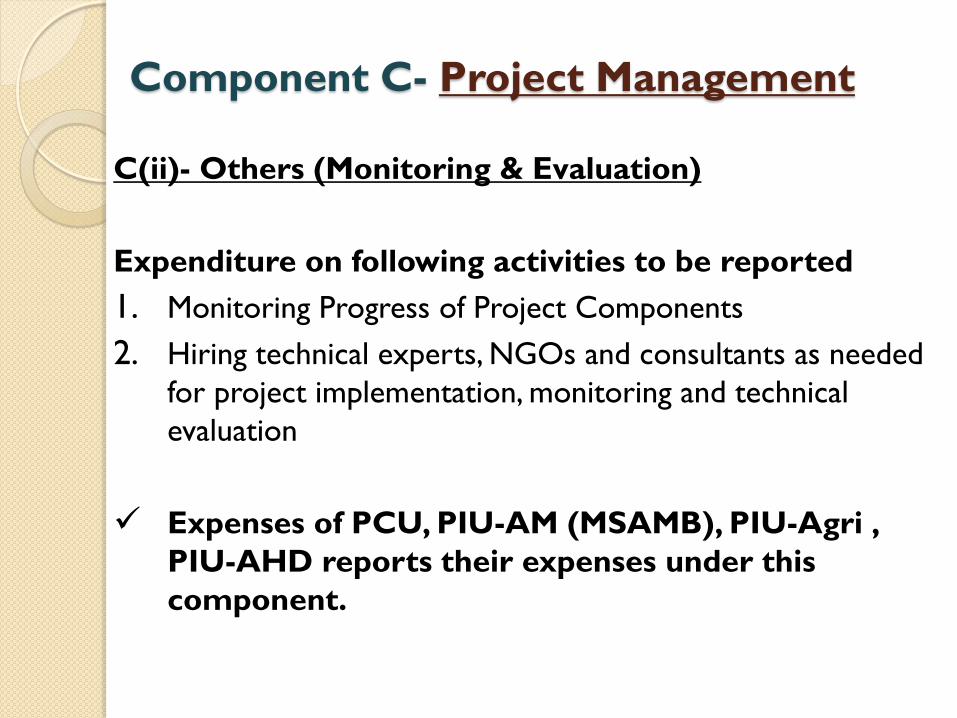

Component C- Project Management

C(ii)- Others (Monitoring & Evaluation)

Expenditure on following activities to be reported

1. Monitoring Progress of Project Components

2. Hiring technical experts, NGOs and consultants as needed

for project implementation, monitoring and technical

evaluation

Expenses of PCU, PIU-AM (MSAMB), PIU-Agri ,

PIU-AHD reports their expenses under this

component.

Important points to be noted during

IUFR preparation

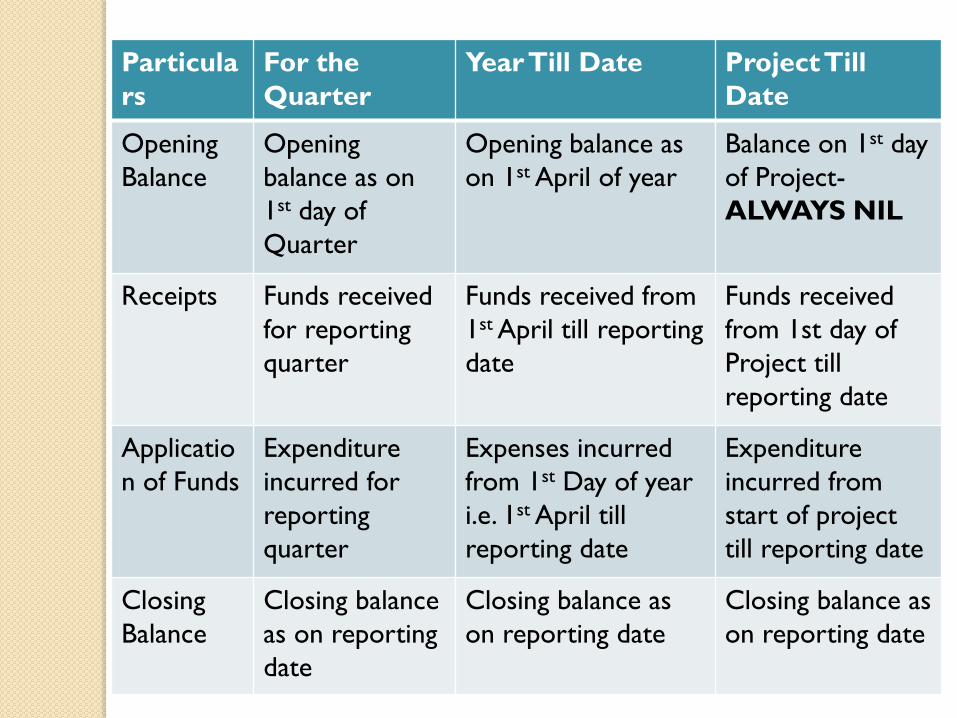

Amount to be reported in IUFR should be Rs in Lakhs

In IUFR format 2 – amounts to reported in columns “For

the Quarter”, “Year Till Date” & “Project Till Date” should

be as follows:

Particula

rs

For the

Quarter

Year Till Date Project Till

Date

Opening

Balance

Opening

balance as on

1st day of

Quarter

Opening balance as

on 1st April of year

Balance on 1st day

of Project-

ALWAYS NIL

Receipts Funds received

for reporting

quarter

Funds received from

1st April till reporting

date

Funds received

from 1st day of

Project till

reporting date

Applicatio

n of Funds

Expenditure

incurred for

reporting

quarter

Expenses incurred

from 1st Day of year

i.e. 1st April till

reporting date

Expenditure

incurred from

start of project

till reporting date

Closing

Balance

Closing balance

as on reporting

date

Closing balance as

on reporting date

Closing balance as

on reporting date

Due Date of the Reports to be

submitted by Accounting

Centers to respective PIU’s

Name of the Report

Due Date of submission

MES

7th of the following month

IUFR

15 days after the end of Quarter

PFS

15 days after the end of year

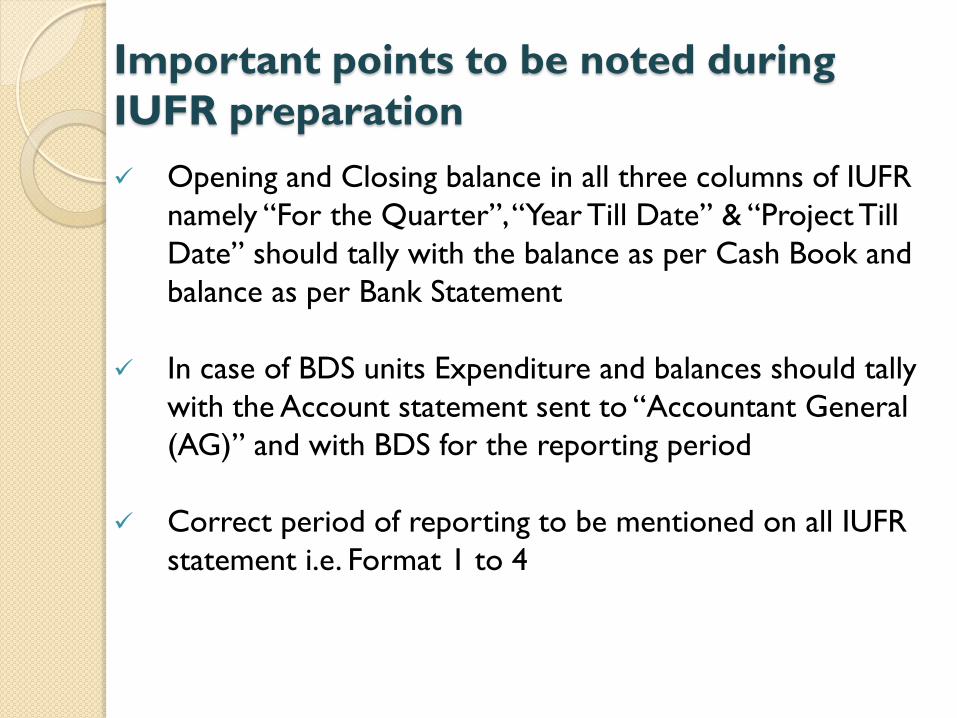

Important points to be noted during

IUFR preparation

Opening and Closing balance in all three columns of IUFR

namely “For the Quarter”, “Year Till Date” & “Project Till

Date” should tally with the balance as per Cash Book and

balance as per Bank Statement

In case of BDS units Expenditure and balances should tally

with the Account statement sent to “Accountant General

(AG)” and with BDS for the reporting period

Correct period of reporting to be mentioned on all IUFR

statement i.e. Format 1 to 4

Important points to be noted during

IUFR preparation

Total amount of expenditure for reporting period as per

“Format 1” should tally with “Format 2”

Cash System of Accounting is to be followed

Total amount of expenditure for reporting period should be

converted in “Rs lakhs” instead of conversion of

transaction wise individual amounts so as to avoid rounding

off differences in IUFR

Important points to be noted during

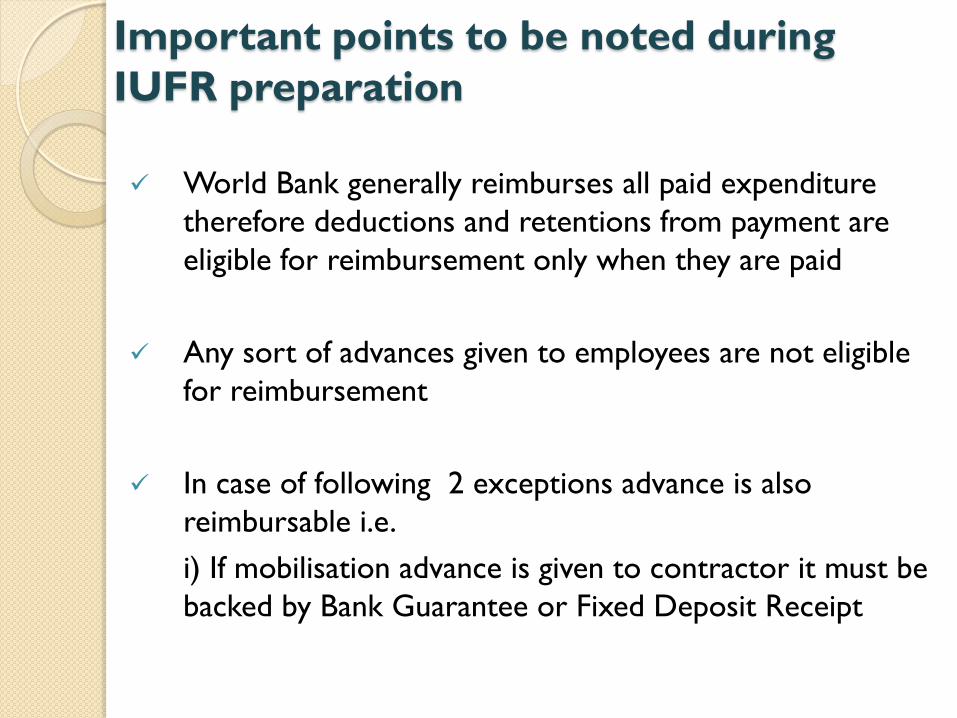

IUFR preparation

World Bank generally reimburses all paid expenditure

therefore deductions and retentions from payment are

eligible for reimbursement only when they are paid

Any sort of advances given to employees are not eligible

for reimbursement

In case of following 2 exceptions advance is also

reimbursable i.e.

i) If mobilisation advance is given to contractor it must be

backed by Bank Guarantee or Fixed Deposit Receipt

Important points to be noted during

IUFR preparation

ii) In case of Community Procurement at FCSC/ Rural Haat

level, advance given by the DDRCs to the beneficiary

organisations would be considered as expenditure

in above 2 exceptions advance could be considered as

eligible for claim

Classification of transaction wise expenses under correct

component of IUFR

Timely preparation and submission of IUFR

Important points to be noted during

IUFR preparation

Expenditure out of Beneficiary contribution (BC) and

Project grants is reported under appropriate component

in IUFR

Withdrawals from Bank account maintained for Beneficiary

Contribution not to be reported as expenditure, only

payments for MACP project expenses are to be

considered as expenditures out of BC

Important points to be noted

during IUFR preparation

Tranche released by DDRCs to Rural Haats &

FCSC to be reported as expenditure in IUFR

Bank interest received in Bank Account to be

reported as other receipts in IUFR. In case of

Bank interest by Rural Haats the same should not

be reported.

Important points to be noted

during IUFR preparation

In case of DDRcs:

It has been observed during the course of audit that in some case bifurcation between Basic and Productive Infrastructure was not properly done.

It is suggested that summarised receipt and payment account should be prepared and the same should be tallied with the cash book. It will also help to cross check whether the balances reported in IUFR are correct or not.

Important points to be noted

during IUFR preparation

In case of recording expenses in the

books of accounts when advance was

given, Utilisation Certificate along with

the supporting should be kept on record.

It was observed that IUFR was not

prepared by AHD it is suggested that they

should also prepare and submit the same.

Thank You !