transfer duty guide - south african revenue service

TRANSCRIPT

Transfer Duty Guide

Issu

e 5

Transfer Duty

Transfer Duty Guide Preface

i

Preface

This document contains a discussion of the application of the Transfer Duty Act 40 of 1949, in respect of transactions involving immovable property such as land, buildings and other real rights in connection with immovable property situated in South Africa. Although fairly comprehensive, the guide does not deal with an analysis of all the legal detail which is sometimes necessary when dealing with immovable property transactions. However, it has been necessary to include a certain amount of technical and legal terminology to explain certain concepts which underpin the transfer duty legislation.

All references to the “Transfer Duty Act” are to the Transfer Duty Act 40 of 1949, and references to “sections” are to sections in the Transfer Duty Act, unless indicated otherwise. The Tax Administration Act 28 of 2011, the Income Tax Act 58 of 1962 and the Value-Added Tax Act 89 of 1991 are referred to as the “TA Act”, the “Income Tax Act” and the “VAT Act” respectively. The terms “Commissioner” and “Minister” refer to the Commissioner for SARS and the Minister of Finance respectively, unless indicated otherwise.

For the purposes of this guide, the following terms and definitions are regarded as having essentially the same meaning, unless the context indicates otherwise:

• The terms “Republic”, “South Africa” or the abbreviation “RSA” which refer to the sovereign territory of the Republic of South Africa, as set out in the definition of “Republic” in section 1(1) of the Transfer Duty and VAT Acts or section 1 of the TA Act (as the case may be).

• The terms “immovable property”, “land” as defined in section 1 of the Alienation of Land Act 68 of 1981, “property” as defined in section 1(1) of the Transfer Duty Act and “fixed property” as defined in section 1(1) of the VAT Act.

• The terms “fair value” as defined in section 1(1) of the Transfer Duty Act, “open market value” as defined in section 1(1) of the VAT Act and ‘‘fair market value’’ as defined in section 1 of the TA Act. These terms refer to the price which could be obtained upon a sale of an asset between a willing buyer and a willing seller dealing at arm’s length in an open market. It also includes reference to other factors which the Commissioner may consider, or be required to consider, in establishing a fair and reasonable value of property which is subject to VAT or transfer duty.

• The terms “Registrar”, “Deeds Registry”, “Registrar of Deeds” and the “Mineral and Petroleum Titles Registration Office” (also referred to as the MPTRO).

A number of specific terms used throughout the guide are defined in the Transfer Duty Act, the VAT Act or the TA Act. These terms and others are listed in the Glossary in a simplified form to make the guide more user-friendly. Chapter 2 also discusses certain definitions in detail which are fundamental to the understanding of the Transfer Duty Act in the context of the law of property and the law of contract.

Transfer Duty Guide Preface

ii

Some of the main topics discussed in this document include –

• the meaning of various definitions;

• the imposition of transfer duty on acquisitions of property;

• different kinds of transactions which are subject to either VAT or transfer duty;

• calculation of transfer duty;

• exemptions; and

• issues relating to the payment of transfer duty, the submission of returns and supporting documentation and other matters generally related to the administration of the Transfer Duty Act.

The information in this guide is issued for guidance only and is not intended to be used as a legal reference. Any statement made in this guide does not have a binding effect and may not be construed as a ruling of any sort contemplated in Chapter 7 of the TA Act or section 41B of the VAT Act.

The information in this guide is based on the transfer duty legislation (as amended) as at the time of publishing of this guide and includes the amendments contained in the Taxation Laws Amendment Act 23 of 2020, the Tax Administration Laws Amendment Act 24 of 2020 and the Rates and Monetary Amounts and Amendment of Revenue Laws Act 22 of 2020. These Acts were all promulgated on 20 January 2021 as per Government Gazettes 44083, 44080 and 44082 respectively.

The previous edition of this guide has been withdrawn with effect from 30 March 2021.

For more information on the VAT treatment of fixed property transactions, see the Legal Counsel Publications webpage on the SARS website where you will find various guides to assist you.

For more details regarding the general operational aspects relating to the electronic submission of the relevant transfer duty forms and the payment of duty, see the Transfer Duty webpage on the SARS website where you will find various resources to assist you.

All guides, interpretation notes, binding general rulings, forms, returns and tables referred to in this guide are available on the SARS website and are as at the date of this publication.

Operational information contained in this guide is up to date as at the date of publishing. However, always refer to the SARS website and any external guides specifically issued on such operational matters, which may be updated from time-to-time.

Should there be aspects which are not clear or not dealt with in this guide, or should you require further information or a specific ruling on a legal issue, you may –

• visit the SARS website at www.sars.gov.za;

• contact your own tax advisor or conveyancer;

• contact your local SARS branch;

• contact the SARS National Call Centre –

if calling locally, on 0800 00 7277; or

if calling from abroad, on +27 11 602 2093 (only between 8am and 4pm South African time);

Transfer Duty Guide Preface

iii

• submit legal interpretative queries on the TA Act by e-mail to [email protected]; or

• submit a ruling application to SARS headed “Application for VAT Class Ruling” or “Application for a VAT Ruling” by email to [email protected] or by facsimile on +27 86 540 9390.

Comments on this guide may be emailed to [email protected].

Prepared by

Leveraged Legal Products SOUTH AFRICAN REVENUE SERVICE Date of 1st issue : March 2007 Date of 2nd issue : 13 March 2013 Date of 3rd issue : 28 September 2016 Date of 4th issue : 12 December 2017 Date of 5th issue : 30 March 2021

Special acknowledgements: Prof. RCD Franzsen, as Advisory Editor; and SARS acknowledges the permission granted by the University of South Africa for the use and reproduction of materials contained in Tutorial Letter 102/2004 for the LLM paper Estate Duty, Donations Tax and Transfer Duty (MESDLW-G) in Chapters 1 to 3 and Annexure A.

Transfer Duty Guide Contents

4

Contents

Preface ............................................................................................................................ i

Chapter 1 Introduction ................................................................................................. 7 1.1 Brief historical perspective ............................................................................................... 7 1.2 Scope and application ..................................................................................................... 7 1.3 Approach of the guide ...................................................................................................... 8 1.4 Tax administration ........................................................................................................... 9

Chapter 2 Definitions and concepts ......................................................................... 11 2.1 Introduction .................................................................................................................... 11 2.2 “Acquisition” ................................................................................................................... 11 2.3 “Date of acquisition” ....................................................................................................... 12 2.3.1 General rule ................................................................................................................... 12 2.3.2 Conversion from share block to sectional title ............................................................... 13 2.3.3 Transactions on behalf of companies and conditional transactions .............................. 13 2.3.4 Pre-emptive rights .......................................................................................................... 14 2.4 “Fair value” ..................................................................................................................... 14 2.4.1 General rules – land and fixtures to the land ................................................................. 15 2.4.2 Limited real rights in property ........................................................................................ 16 2.4.3 Pre-emptive rights .......................................................................................................... 18 2.4.4 Plot and plan contracts .................................................................................................. 18 2.4.5 Tenant improvements .................................................................................................... 20 2.4.6 Shares, members’ interests and contingent rights relating to residential property........ 20 2.4.7 Shares in a share block company ................................................................................. 21 2.4.8 Special rules .................................................................................................................. 22 2.5 “Property” ....................................................................................................................... 22 2.5.1 Introduction .................................................................................................................... 23 2.5.2 Land and fixtures – General .......................................................................................... 23 2.5.3 Real rights in land .......................................................................................................... 24 2.5.4 Attachment by way of planting and sowing ................................................................... 25 2.5.5 Limited real rights .......................................................................................................... 25 2.5.6 Leases ........................................................................................................................... 26 2.5.7 Licences, goodwill and production quotas ..................................................................... 26 2.5.8 Minerals ......................................................................................................................... 27 2.5.9 Rights under a mortgage bond ...................................................................................... 28 2.5.10 Shares, members’ interests and contingent rights relating to residential property........ 28 2.5.11 Shares in a share block company ................................................................................. 29 2.5.12 Fractional ownership and timeshare schemes .............................................................. 29 2.6 “Residential property” .................................................................................................... 31 2.7 “Residential property company” ..................................................................................... 32 2.8 “Transaction” .................................................................................................................. 33

Chapter 3 Tax base .................................................................................................... 36 3.1 General .......................................................................................................................... 36 3.2 Acquisition ..................................................................................................................... 36 3.2.1 General .......................................................................................................................... 36 3.2.2 “Property” must be acquired .......................................................................................... 37 3.2.3 Acquisition by way of a transaction ............................................................................... 37 3.2.4 Acquisition other than by way of a transaction .............................................................. 39 3.2.5 Property acquired on behalf of others ........................................................................... 40 3.2.6 Suspensive and resolutive conditions ........................................................................... 43 3.3 Cancellations ................................................................................................................. 44

Chapter 4 Date of liability .......................................................................................... 45 4.1 Introduction .................................................................................................................... 45 4.2 Acquisition by way of transaction .................................................................................. 46 4.3 Acquisition other than by way of a transaction .............................................................. 46

Transfer Duty Guide Contents

5

4.3.1 Prescription .................................................................................................................... 46 4.3.2 Divorce ........................................................................................................................... 47 4.3.3 Antenuptial contract ....................................................................................................... 47 4.3.4 Inheritance ..................................................................................................................... 48

Chapter 5 Person liable to pay duty.......................................................................... 49 5.1 General rules ................................................................................................................. 49 5.2 Liability of persons other than the transferee ................................................................ 49

Chapter 6 Dutiable value ........................................................................................... 51 6.1 Introduction .................................................................................................................... 51 6.2 Determination of fair value ............................................................................................. 51 6.2.1 General .......................................................................................................................... 51 6.2.2 Declared value and valuation factors ............................................................................ 53 6.2.3 Municipal valuations ...................................................................................................... 55 6.2.4 Sworn valuers or appraisers .......................................................................................... 55 6.2.5 Mineral lease valuations ................................................................................................ 55 6.3 Consideration ................................................................................................................. 56 6.3.1 Consideration ascertainable in money .......................................................................... 56 6.3.2 Consideration other than in money ................................................................................ 58 6.3.3 Exchanges ..................................................................................................................... 58 6.4 Cancelled or dissolved transactions .............................................................................. 60 6.5 Liquor-licensed premises ............................................................................................... 61 6.6 Costs of valuation .......................................................................................................... 61 6.7 Other factors .................................................................................................................. 61 6.7.1 Accession ...................................................................................................................... 61 6.7.2 Separate properties acquired for a single price ............................................................. 61 6.7.3 Object of sale consists of more than “property” ............................................................. 62 6.7.4 Land Bank values .......................................................................................................... 62 6.7.5 Quitrents ........................................................................................................................ 62

Chapter 7 Tax rates and calculations ....................................................................... 64 7.1 Introduction .................................................................................................................... 64 7.2 Rates of duty .................................................................................................................. 64 7.3 Application of the graduated rates of duty ..................................................................... 65 7.3.1 General rule ................................................................................................................... 65 7.3.2 Undivided shares in property ......................................................................................... 69 7.3.3 Limited real rights in property ........................................................................................ 72 7.4 Date of application of amended rates of duty ................................................................ 75

Chapter 8 Exemptions ............................................................................................... 76 8.1 Introduction .................................................................................................................... 76 8.2 Current exemptions ....................................................................................................... 77 8.2.1 Government [section 9(1)(a)] ......................................................................................... 77 8.2.2 Municipalities and water service providers [sections 9(1)(b) and 9(1)(bB)] .................. 77 8.2.3 Public benefit organisations and other statutory bodies [sections 9(1)(c), 9(1)(d) and

9(1A)] ............................................................................................................................. 77 8.2.4 Inheritance by heirs or legatees [section 9(1)(e)] .......................................................... 78 8.2.5 Partition between joint owners [section 9(1)(g)] ............................................................ 79 8.2.6 Acquisition by joint owner [section 9(1)(h)] .................................................................... 79 8.2.7 Surviving or divorced spouse [section 9(1)(i)] ............................................................... 80 8.2.8 Acquisition from a spouse by virtue of marriage in community of property [section 9(1)(k)]

....................................................................................................................................... 82 8.2.9 Amalgamation transactions [section 9(1)(l)] .................................................................. 83 8.2.10 Superannuation funds of former TBVC self-governing territories [section 9(1)(m)] ...... 83 8.2.11 Land reform and land restitution transactions [sections 9(1)(n) and (o)] ....................... 83 8.2.12 Rectification of registration errors [section 9(2)(i)] ......................................................... 84 8.2.13 Transfer from a partnership into the individual partner’s names [section 9(3)] ............. 84 8.2.14 Transfers to trustees, administrators, beneficiaries and insolvent persons

Transfer Duty Guide Contents

6

[section 9(4)] .................................................................................................................. 85 8.2.15 Transfer to surety [section 9(6)] ..................................................................................... 85 8.2.16 Transactions declared void by a competent court [section 9(7)(a)] .............................. 85 8.2.17 Transactions becoming void by insolvency [sections 9(7)(b) and 9(7)(c)] .................... 85 8.2.18 Exchange of adjoining portions of mining properties [section 9(7)(d)] .......................... 85 8.2.19 Acquisition of property by a subsidiary company [section 9(8)] .................................... 86 8.2.20 Expropriation [section 9(9)] ............................................................................................ 86 8.2.21 Taxable supply of goods to the person acquiring property [section 9(15)] .................... 86 8.2.22 Asset-for-share transactions under section 42 of the Income Tax Act [section 9(15A)] 88 8.2.23 VAT registered rental pool schemes [section 9(15B)] ................................................... 88 8.2.24 Mineral and prospecting rights [section 9(18)]............................................................... 89 8.2.25 Conversion from share block to sectional title [section 9(19)] ....................................... 89 8.2.26 Transfer of a residence from a company or trust [section 9(20)]................................... 89 8.3 Repealed exemptions .................................................................................................... 90

Chapter 9 Payment and recovery of transfer duty ................................................... 91 9.1 Liability and period for payment ..................................................................................... 91 9.2 Deposit on account of duty ............................................................................................ 91 9.3 Payment of duty and issuing of receipts ........................................................................ 92 9.4 Interest on late payment ................................................................................................ 92 9.5 Registration of acquisition.............................................................................................. 93 9.6 Recovery of underpaid duty and understatement penalty ............................................. 93

Chapter 10 Administrative provisions ...................................................................... 95 10.1 The Tax Administration Act and the administration of the Transfer Duty Act ................ 95 10.2 Returns .......................................................................................................................... 96 10.3 Compliance .................................................................................................................... 97 10.3.1 Outstanding taxes and tax returns ................................................................................. 97 10.3.2 Value-Added Tax ........................................................................................................... 97 10.4 Refunds.......................................................................................................................... 98 10.5 Dispute resolution .......................................................................................................... 99 10.5.1 General .......................................................................................................................... 99 10.5.2 The “pay now, argue later” principle ............................................................................ 100 Annexure A – Court cases ........................................................................................................... 101 Annexure B – Life expectancy tables ........................................................................................... 107

Glossary .................................................................................................................... 111

Contact details .......................................................................................................... 117

Transfer Duty Guide Chapter 1

7

Chapter 1 Introduction

1.1 Brief historical perspective The Transfer Duty Act was promulgated in Gazette Extraordinary 4193 on 28 July 1949. It came into effect on 1 January 1950 and applies to all acquisitions of property on or after that date. Any acquisitions before 1 January 1950 remain liable to duty under the relevant laws operative at the date of the transaction.1 Particulars as to any liability and/or rates of duty or exemptions relevant to any such acquisitions may be obtained by referring the matter to the office of the Commissioner.

Transfer duty is a tax levied by the national sphere of government and is paid into the National Revenue Fund.2

1.2 Scope and application As mentioned in the Preface, this document includes a discussion on the meaning of various definitions, how the imposition of transfer duty works, whether a transaction is subject to VAT or transfer duty, how to calculate the transfer duty which is payable, and how to establish if an exemption applies.

Although this guide is written as far as possible in plain English, its purpose is to provide technical guidance on the application of the Transfer Duty Act on property transactions in the context of the law of property, the law of contract and various other legislative acts with which it is integrally linked. It has therefore been necessary, to a certain extent, to include a discussion on how these other acts and areas of law affect the application of the Transfer Duty Act. This guide does not, however, purport to provide anything more than mere guidance on the application of those other acts and areas of law in so far as they relate to transfer duty matters.

Some areas of the transfer duty law have been explained in more detail than others because of the degree of complexity of the particular topic concerned. It has also been necessary to deal with other taxes such as VAT, Capital Gains Tax (CGT) and income tax to a certain extent, particularly when it concerns the transfer duty exemptions. These other taxes are only dealt with in so far as it is necessary to obtain a basic understanding of their link with transfer duty. The reader will therefore find numerous references to other legislation, case law and guides issued by SARS for more details relating to the tax type concerned.

The main purpose of this guide is therefore to assist the reader to –

• determine if “property” has been acquired, or if a transaction or event is otherwise subject to transfer duty in principle, or if an exemption from duty applies;

• determine if a transaction is subject to VAT or transfer duty;

• identify the factors which the Commissioner must (or may) take into account when determining the “fair value” of property as well as which amounts must be included or excluded from the consideration which is subject to duty;

1 1st proviso to section 21. 2 See section 2(1) of the Transfer Duty Act and section 213 of the Constitution of the Republic of

South Africa, Act 108 of 1996.

Transfer Duty Guide Chapter 1

8

• calculate the amount of duty (including any interest thereon) for different types of property transactions and determine the period within which transfer duty is payable;

• understand the administrative requirements relating to the submission of transactions to SARS for processing on eFiling; and

• generally understand the application of the Transfer Duty Act with regard to property transactions.

Some aspects with regard to policies and procedures on the processing of transactions are mentioned in this guide, but this is not the focus of the publication. More details regarding the submission of returns and the processing of documents and payments can be found in the Transfer Duty eFiling Guide.

1.3 Approach of the guide The approach of this guide in dealing with the topics mentioned in 1.3 is set out below.

Chapter 1 – Provides a brief historical perspective and some background information relating to transfer duty. It also describes the scope of topics that will be covered in the guide and the approach adopted.

Chapter 2 – This chapter explores some of the main definitions and concepts which underpin the application of the Transfer Duty Act in the context of the law of property, the law of contract and various other legislative acts which govern property transactions in South Africa. The most fundamental definition is that of “property” which has a particular meaning in the legal context as well as a specific defined meaning in section 1(1). The definition also has a link with the definition of the term “fixed property” as defined in section 1(1) of the VAT Act which is explained in some detail in the guide.

Chapter 3 – Describes the transactions and events which make up the tax base of transfer duty, being acquisitions of “property” either by way of a transaction or in any other manner, as well as renunciations of interests in “property” which has the effect of enhancing the value of property. As most of the important definitions and concepts would have already been explained in Chapter 2, this chapter provides a summary of the meaning of those terms and puts them into context within the meaning of the term “acquisition”. Also dealt with in this chapter is the cancellation of transactions and transactions which are concluded through representatives or agents who act on behalf of, or for the benefit of others.

Chapter 4 – Briefly sets out aspects which relate to the date of liability for transfer duty and the period in which the duty must be paid. This chapter focuses on the practical aspects relating to the definition of the terms “date of acquisition” and “acquisition” which are explained in Chapters 2 and 3.

Chapter 5 – Deals with determining who is liable to pay transfer duty in any particular situation. The general rule is that the transferee is liable, but the Transfer Duty Act also contains provisions which make other persons liable for the duty in certain types of transactions.

Transfer Duty Guide Chapter 1

9

Chapter 6 – Focuses on the determination of the dutiable value of the property acquired or the value by which property is enhanced by the renunciation of an interest therein. The applicable valuation rules as set out in the definition of the term “fair value” are discussed in the context of the different transactions and events. The chapter includes a discussion of different valuation factors that the Commissioner may consider (or which must be considered) when an inadequate consideration is paid or where the declared value is less than the fair value of the property acquired or renounced. This chapter also sets out what is to be included and excluded from the consideration paid (or payable) which will be subject to duty.

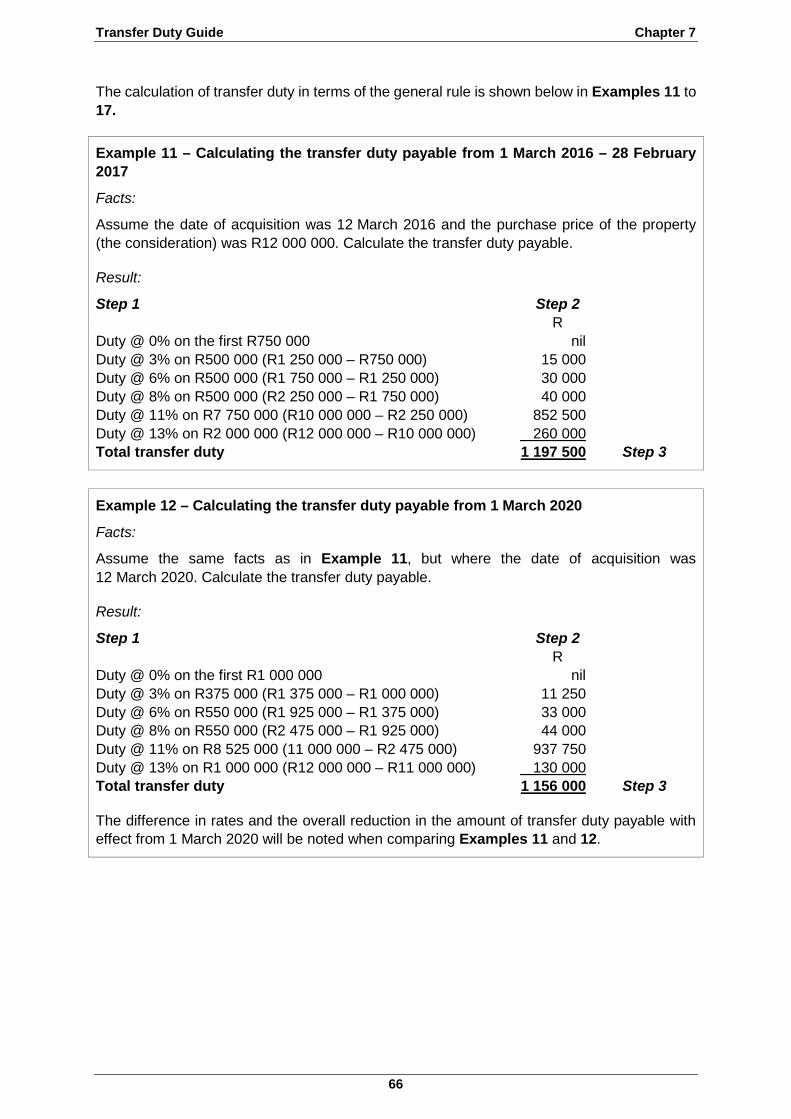

Chapter 7 – Sets out the rules for calculating transfer duty and the rates of duty that have applied over the years. Included are a number of different examples of how to calculate duty for past and current transactions as well as the application of the formula in section 2(5) for calculating the duty on an acquisition of an undivided share in property. The examples also demonstrate how to establish whether transfer duty or VAT is payable on a transaction.

Chapter 8 – Deals with exemptions from duty. One of the most important of these is section 9(15) which provides for an exemption from transfer duty when a property transaction constitutes a taxable supply of “fixed property” as defined in section 1(1) of the VAT Act. This exemption, amongst others, are explained in more detail, mainly as a result of other legislation or legal principles which apply in certain transactions, or as a result of the complexity of the wording of the exemption itself.

Chapter 9 – Deals with matters associated with the payment and recovery of duty. It covers the period for payment, the issuing of receipts and penalties or interest payable on late payments.

Chapter 10 – Deals with compliance matters concerning the administration of the Transfer Duty Act generally in the context of the TA Act. It includes a discussion on how these aspects impact on the interpretation of definitions, the submission of returns and payments, recovery of unpaid duty, objections, appeals and dispute resolution.

1.4 Tax administration The TA Act was promulgated on 4 July 2012 and came into effect on 1 October 2012. However, certain provisions relating to interest stipulated in the Schedule to Proclamation 51 dated 14 September 2012 (as per Government Gazette 35687) and Schedule 1 to the TA Act will only become effective from a future date to be determined by the President.

The TA Act only deals with tax administration, and incorporates into one piece of legislation certain administrative provisions that are generic to all tax Acts. It also seeks to align the various administrative provisions which were previously duplicated in the different tax Acts, and to simplify and harmonise the provisions as far as possible. This guide must therefore be read in the context of the TA Act and any public notices or proclamations issued in connection with any general tax administration matter.

See Chapter 10 for more information in this regard.

Transfer Duty Guide Chapter 1

10

Further information regarding the TA Act can be obtained from the Tax Administration webpage, which includes the –

• Short Guide to theTax Administration Act, 2011;

• Electronic Form of Record-Keeping under Section 30(1)(b) in Government Gazette 35733 Notice 787; and

• Interpretation Note 68 “Provisions of the Tax Administration Act that did not commence on 1 October 2012 under Proclamation 51 in Government Gazette 35687”.

Transfer Duty Guide Chapter 2

11

Chapter 2 Definitions and concepts

2.1 Introduction The Transfer Duty Act imposes a transfer duty on the value of any property acquired by any person by way of a transaction, or in any other manner, or on the value by which any property is enhanced by the renunciation of an interest in or restriction upon the use or disposal of that property. It is therefore necessary to have a look at the underlying concept of acquisition and important definitions in section 1(1) in order to establish whether there is a liability for transfer duty.The following key definitions will be discussed: “acquisition”, “date of acquisition”, “fair value”, “property”, “residential property”, “residential property company” and “transaction”. Also see Chapter 10 for the general interpretation rules which apply in the context of the TA Act when interpreting definitions contained in the Transfer Duty Act.

2.2 “Acquisition” The concepts of “acquire” and “acquisition” are not defined in the Transfer Duty Act. However, the courts have repeatedly interpreted the meaning of the term “acquisition” in the context of section 2(1), which is the main charging provision in the Transfer Duty Act. In CIR v Freddies Consolidated Mines Ltd,3 Centlivres CJ states the following (at 311C):

“The word ‘acquired’ in the charging section (section 2) must therefore be construed as meaning the acquisition of a right to acquire the ownership of property. It has been said to be a misnomer to call the duty a transfer duty: it is in fact a duty imposed, inter alia, on the consideration given by a purchaser of property for the right conferred on him to acquire the ownership of property.”

In SIR v Hartzenberg,4 Botha JA confirms this view by stating (at 409A-B):

“Although the ordinary legal meaning of the word ‘acquire’ implies the acquisition of dominium, it is clear that in section 2 of the Act the word is used in its wider meaning and includes the acquisition of a jus in personam ad rem acquirendam... Transfer duty therefore becomes payable under section 2 upon the acquisition by a person of a personal right to obtain dominium in immovable property.”

This interpretation is confirmed in several other cases5 and is supported by the definition of the term “date of acquisition” in section 1(1) as well as the wording of sections 5(2)(a), 12(1) and 13. In other words, the “acquisition of property” refers to the acquisition of a personal right that entitles the person who acquires the property to claim transfer. The close association of the Deeds Office and conveyancers with regard to the collection of transfer duty may create the impression that the liability arises at the time when a property transfer is entered in the Deeds Registry.

This is not the case, as the liability arises at the date of acquisition or at the date that the renunciation of an interest in property takes place. The liability therefore exists at the time that the transaction is completed regardless of whether or not the actual transfer of the property or the renunciation of the right has been recorded in the Deeds Registry. Transfer duty can therefore not be avoided by the failure to register the transfer of the property.

3 1957 (1) SA 306 (A). 4 1966 (1) SA 405 (A) 5 Refer, for example, to SIR v Wispeco Housing (Pty) Ltd 1973 (1) SA 783 (A) 791C-D, SIR v Estate

Roadknight 1974 (1) SA 253 (A) 258B-C; CIR v Collins 1992 (3) SA 698 (A) 707I-J.

Transfer Duty Guide Chapter 2

12

See Chapter 3 for further discussion on the concept of “acquisition”.

2.3 “Date of acquisition”

“date of acquisition” means—

(a) in the case of the acquisition of property (other than the acquisition of property contemplated in paragraph (b) by way of a transaction, the date on which the transaction was entered into, irrespective of whether the transaction was conditional or not or was entered into on behalf of a company already registered or still to be registered and, in the case of the acquisition of property otherwise than by way of a transaction, the date upon which the person who so acquired the property became entitled thereto: Provided that where property has been acquired by the exercise of an option to purchase or a right of pre-emption, the date of acquisition shall be the date upon which the option or right of pre-emption was exercised;

(b) in the case of the acquisition of property under item 8 of Schedule 1 to the Share Blocks Control Act, 1980 (Act No. 59 of 1980), and if section 9A of this Act does not apply to that acquisition, the date of the written request referred to in sub-item (1)(b) of the said item 8;

(c) ...

2.3.1 General rule

Most cases involve the acquisition of rights to receive transfer of immovable property by way of a transaction in terms of an agreement of purchase and sale. In these cases, the date of acquisition will be the date on which the transaction was entered into, being the date that the last contracting party has signed the agreement.

This rule applies even if the contract –

• stipulates a different effective date;

• is subject to any resolutive or suspensive conditions;6

• was entered into on behalf of a company (whether registered or still to be registered); or

• takes a form other than a normal sale, for example, a donation, an expropriation or a renunciation of rights.

The date of acquisition of property by a person otherwise than by way of a transaction, is the date upon which the person acquiring the property became entitled thereto. In some of these cases the date of acquisition (being the date of entitlement) may have to be determined by a court. For example, in the case of an acquisition by way of prescription, the view is that the date of entitlement is the date of the court order and not the exact date upon which prescriptive title would have vested after the 30 year period of free and undisturbed possession.7 Typically ownership will not be registered in the new owner’s name without the sanction of a court.

6 A common example is when a sale agreement for the purchase of a property is concluded, but

subject to the purchaser obtaining finance. The date of acquisition is the date that the last person signed the contract and not the later date when the finance is granted to the purchaser.

7 Prescription Act 68 of 1969, section 2(1).

Transfer Duty Guide Chapter 2

13

It should be noted that when any announcement is made by the Minister to reduce the rate of transfer duty before the effective date of the change, the parties to an agreement may not merely cancel an existing agreement and enter into a new agreement in respect of the same property to take advantage of the lower transfer duty rates. Should this occur, SARS will not regard the transaction as a true cancellation, but rather, a transaction entered into for the purpose of avoiding or evading transfer duty.

Similarly, the conclusion of an addendum setting out further negotiated terms or amendments to the original agreement will not alter the date of acquisition for transfer duty purposes, as an addendum cannot be read or applied independently of the original agreement. Transfer duty will therefore be calculated in such cases using the original date of acquisition as if the original agreement had not been cancelled.8

2.3.2 Conversion from share block to sectional title

The date of acquisition of property by virtue of a conversion of share block rights to sectional title9 is the date that the written request for conversion10 has been lodged with the share block company by the person who has the right of use under the use agreement.

2.3.3 Transactions on behalf of companies and conditional transactions

In the case of conditional transactions, or transactions on behalf of companies, the date of acquisition is also reckoned from the date on which the transaction was entered into as discussed in 2.3.1, and not –

• the date that the condition is fulfilled (that is the date that the contract becomes operational); or

• the date that the company ratifies the acquisition.

This applies whether the company is already registered or still to be registered. Although the definition of the term “date of acquisition” refers to a “company”, the definition of a “company” in section 1(1) includes a close corporation. The principle explained in this paragraph will also apply in the case of a trust which exists at the time of the transaction. However, in the case of trusts (unlike companies), no transaction may be entered into on behalf of the trust before it has been formed. In other words, the condition must be ignored for purposes of determining the date of acquisition for transfer duty purposes. (Suspensive and resolutive conditions are discussed in 3.2.6.)

Any transaction on behalf of a company which is still to be formed (pre-incorporation contract) is governed by section 21 of the Companies Act 71 of 2008 (the Companies Act). Under this provision, a person (the promoter) may enter into a written agreement or purport to act in the name of an entity that does not exist at the time, if it is to be incorporated as a company under the Companies Act. Within three months after incorporation, the board may completely, partially or conditionally ratify or reject the pre-incorporation contract. Alternatively, if during that period the company does not ratify or reject the transaction, it is deemed to have been ratified and accepted.

8 Secretary for Inland Revenue v Hartzenberg 1966(1) SA 405 (AD). 9 As contemplated in Item 8 of Schedule 1 to the Share Blocks Control Act 59 of 1980. 10 This is required under sub-item (1)(b) of Item 8 of Schedule 1 to the Share Blocks Control Act 59 of

1980.

Transfer Duty Guide Chapter 2

14

To the extent that a pre-incorporation contract has been ratified, the agreement is enforceable against the company as if the company had been a party to the agreement when it was made and any liability of the promoter is accordingly discharged to that extent. Whether the company (once formed) or the promoter turns out to be liable for the transaction, the date of transaction remains the date on which the original contract was concluded, and not the subsequent date of ratification (or deemed ratification) by the company, or the date of registration of the entity as a company.

Section 21 of the Companies Act does not apply in the case of transactions concluded in the name of shelf companies. This is because the shelf company already exists at the time of signing the sale agreement and cannot qualify as a pre-incorporation contract. It must therefore be ascertained whether that person had the legal capacity to act on behalf of that shelf company at that time, so as to constitute a valid transaction. Further, that if that person had the required capacity, it must be established whether or not the shelf company had been identified as the principal (the actual purchaser) on the date of the transaction as required under section 16 of the Transfer Duty Act.

In this regard the question of legal capacity applies not only in respect of shelf companies, but also as a generally applicable principle. For example, if a person acts in a representative capacity in purchasing immovable property, section 16 prescribes that not only must the name and certain other details of the principal be disclosed at the time of the transaction, but also that the documents authorising that person to act on behalf of the principal in the matter must be provided to the seller (for example a special power of attorney). If the intended representative of a shelf company signed such an agreement before purchasing the shelf company, then that individual is regarded as the purchaser, since he or she could not have been acting in a representative capacity at the time of the transaction.

2.3.4 Pre-emptive rights

The proviso to the definition of the term “date of acquisition” deals with a situation where a person acquires property by exercising a pre-emptive right. In such a case, the date of acquisition is the date that the right is exercised and not the date that the right was acquired. This is because the acquisition of the right itself does not constitute “property” as defined in section 1(1) and is not a registrable right unless it is intended to bind successors in title. Only when the right is exercised, does a right to acquire property arise.

2.4 “Fair value”

“fair value”—

(a) in relation to property as defined in paragraphs (a) and (c) of the definition of “property”, means the fair market value of that property as at the date of acquisition thereof;

(b) in relation to a share or member’s interest in a company as contemplated in paragraph (d) or (e) of the definition of “property”, means so much of the fair market value as at the date of acquisition of that share or member’s interest, of any property held by that company which constitutes—

(i) residential property;

(ii) a share or member’s interest in any company as contemplated in paragraph (d) or (e) of the definition of “property”; or

(iii) a contingent right in property of a trust as contemplated in paragraph (f) of the definition of “property”,

Transfer Duty Guide Chapter 2

15

(without taking into account any lease agreement or any liability in respect of any loan or any right to or an interest in the use of immovable property conferred on the owner of a share in a share block company as contemplated in section 1 of the Share Blocks Control Act, 1980 (Act No. 59 of 1980), in relation to that residential property or any residential property of any company or trust contemplated in subparagraph (ii) or (iii)), as is attributable to that share or member’s interest; or

(c) in relation to any contingent right to any property, which constitutes—

(i) residential property;

(ii) a share or member’s interest contemplated in paragraph (d) or (e) of the definition of “property”; or

(iii) a contingent right in property of a trust as contemplated in paragraph (f) of the definition of “property”, held by a discretionary trust, means the fair market value of that property (without taking into account any lease agreement or any liability in respect of any loan in relation to that residential property or any residential property of any company or trust contemplated in subparagraph (ii) or (iii)), as at the date of acquisition of that contingent right:

(d) in relation to a share in a company as contemplated in paragraph (g) of the definition of “property”, means so much of the fair market value, as at the date of acquisition of that share, of any property held by that company which constitutes property as contemplated in paragraphs (a) and (c) of that definition (without taking into account any lease agreement or any liability in respect of any loan in relation to that residential property) as is attributable to that share:

Provided that—

(a) the fair market value of any property of a company or a trust which constitutes a contingent right in property of a trust, as contemplated in paragraphs (b)(iii) and (c)(iii), shall be equal to the fair value of that contingent right as determined in terms of paragraph (c) of this definition; and

(b) where property, has been acquired by the exercise of an option to purchase or a right of pre-emption, the fair value in relation to that property shall be the fair market value thereof as at the date upon which the option or right of pre-emption was acquired by the person who exercised the option or right of pre-emption;

2.4.1 General rules – land and fixtures to the land

The definition of the term “fair value” must be read and interpreted within the context of the definition of“property” as well as section 5 which provides for the determination of the value of property on which transfer duty is payable. Paragraph (a) of the definition of the term “fair value” is the general rule which applies to land and any fixtures thereon, which specifically includes reference to the acquisitions mentioned in paragraphs (a) and (c) of the definition of the term “property”, namely –

• real rights in land (but excluding rights under mortgage bonds or leases other than those described below);

• rights to minerals or rights to mine for minerals; and

• leases or sub-leases of rights to minerals or to mine for minerals.

Transfer Duty Guide Chapter 2

16

In these cases, “fair value” means the fair market value of that property as at the date of acquisition. In an arm’s length transaction between two unrelated parties, the consideration payable by the purchaser will generally be representative of the fair market value on which transfer duty is paid. In the case of related parties and transactions where no consideration is payable, transfer duty will be paid on the declared value of the property, provided that the Commissioner may determine the fair value if the consideration payable or the declared value is less than the fair value of the property concerned. In such cases, the duty payable on the acquisition of that property will be based on the greater of –

• the consideration paid or payable for the property; or

• the fair value of the property as determined by the Commissioner.

This will apply, for example, in a case where the property is sold for less than the fair market value because the contracting parties are related, or when it otherwise appears to the Commissioner that the transaction is not concluded at arm’s length. In cases where the Commissioner determines the fair value of the property, that determination may be revised not later than two years from the date on which duty was originally paid.

In determining the fair value of a property, the Commissioner must have regard to –

• the nature of the real right in land and the period for which it has been acquired (or the period for which the property is likely to be enjoyed in cases where the property is acquired for an indefinite period, or for the natural life of any person);

• the municipal valuation;

• any sworn valuation which has been furnished by, or on behalf of the person liable to pay the duty; and

• any valuation made by the Director-General: Mineral Resources or by any other competent and disinterested person appointed by the Commissioner.11

Although the definition of the term “fair value” does not refer specifically to renunciations, it is submitted that the amount (fair value) on which transfer duty is payable is the difference between the value of the property burdened with the interest or restriction, and the value of the property not so burdened. This must be determined objectively according to the fair market values of the property in each circumstance respectively (that is burdened vs not burdened).12

2.4.2 Limited real rights in property

For the purposes of this guide, the term “limited real rights in property” includes praedial servitudes13 and personal rights par excellence such as a usufruct, usus, habitatio and fideicommissum. These are rights that are either capable of being registered, or required to be registered in a Deeds Registry. The fair value for transfer duty purposes in such cases is the fair market value of the rights as at the date of acquisition. Although it is possible for limited real rights to be the subject of a purchase and sale agreement, it is more common for the rights to be acquired by way of a donation, or as a result of an inheritance, or by way of a legal requirement.

11 See sections 5(6) and 5(7). 12 Handbook on Transfer Duty (1950), Meyerowitz and Jacobson. Also see 2.4. 13 A praedial servitude is a registered servitude which one property (the dominant property) has over

another (the servient property).

Transfer Duty Guide Chapter 2

17

The fair value of limited real rights in property is usually determined through the use of the tables which were promulgated under section 29 of the Estate Duty Act 45 of 1955. In particular, when no consideration is paid for the acquisition of these rights (which is the usual position) the Commissioner must be satisfied that the declared value is a true reflection of the fair value of the property in the circumstances. This is based on the principle that in contemplating the fair value, the Commissioner must consider the factors mentioned in section 5(7) which includes (amongst other factors) –

• the nature of the real right in the property and the period for which that property has been acquired; and

• the period for which the property is likely to be enjoyed when the property has been acquired for an indefinite period or for the natural life of any person.

In a case where the usufructuary renounces his or her rights and interests in the property, this will result in a dutiable transaction and the applicable tables will be applied to determine the value by which the property has been enhanced for transfer duty purposes. This amount will then be compared to any consideration paid to the person renouncing the rights and interests, and transfer duty will be payable on the higher value. In a situation where the owner’s property is restored to its full content by virtue of the lapsing of the encumbrance, for example, when a usufruct comes to an end as a result of the death of the usufructuary, this is not regarded as a renunciation. Consequently, there is no “acquisition” of property by the bare dominium owner which can be subject to duty.

The tables (see Annexure B) apply in the following manner:

• In the case where a person has acquired a real right in property for the rest of that person’s life, Table A “The Expectation of Life and the Present Value of R1 per Annum for Life Capitalised at 12 per cent over the Expectation of Life of Males and Females of Various Ages” is used to calculate the value. Table A is commonly referred to as the “life expectancy tables”;

• Where a person acquires a real right for a fixed period, Table B titled “Present Value of R1 per Annum Capitalised at 12 per cent over Fixed Periods” is used to calculate the value. Table B is commonly referred to as the “fixed period tables”; and

• The life expectancies apply to natural persons who hold limited rights in respect of donations and estates on or after 1 April 1977. In the case of a non-natural person, the expectancy is fixed at 50 years.

The tables are used to determine the discounting factors over the various life expectancies or fixed periods involved (as the case may be) which is multiplied by the annual yield in order to arrive at the applicable values (that is by discounting R1 by an annual factor of 12%). The values as determined by these tables are used to calculate valuations of limited rights for purposes of estate duty, donations tax and transfer duty, although in certain cases (not within the scope of this guide), there may be some differences between them. (Also see 7.3.3 for some examples, as well as 2.4.2 and section 5(7) for more information regarding valuation issues in this regard.)

Transfer Duty Guide Chapter 2

18

2.4.3 Pre-emptive rights

The value of property acquired by exercising a pre-emptive right14 is taken as at the date when the right was acquired by the person exercising it. This rule applies regardless of whether that right was obtained directly from the owner of the property, or from some intermediate holder of the right. The value of any improvements effected by a prior option holder will normally be reflected in the amount of the consideration paid by the person acquiring the option from the prior holder.

The intention is that a person acquiring property through the exercising of an option to purchase should not be chargeable with duty on any increase in value due to improvements made, or the exploring and proving of mining prospects, or fluctuations in value during the period that the right was held by that person.

The acquisition of a pre-emptive right is not, in itself, a transaction which is subject to transfer duty, unless it is intended to bind successors in title and is to be registered in the Deeds Registry as an encumbrance over the property. Any amount paid or payable for that right must be added to the consideration payable for the acquisition of the property if that consideration forms part of, or is applied as credit against, the purchase consideration for the property when the holder exercises the right. (See section 6(1)(b).)

2.4.4 Plot and plan contracts

Sometimes a developer or building contractor may sell a piece of land together with an undertaking to erect a building on the land, or to complete a partially completed building thereon. There are various ways in which this can be done. For example, the land and the building contract may be contained in a single contract or in separate contracts with the same supplier, or there could be separate contracts with the different suppliers.

The transfer duty receipt for plot and plan transactions should reflect the value of the property as at the date of registration in the Deeds Office if the building will be completed by the date of registration. If the building will not be completed by the date of registration, only the value of the land should be reflected on the receipt.

In a case where the seller is not a VAT vendor and the full consideration for both the plot and the building contract is paid to the seller, the full consideration will be subject to transfer duty. However, in most of these cases, the supplier should be registered as a VAT vendor and VAT must be charged at the standard rate on both the property and the building which is to be supplied. Therefore, it is usually only in the case where there are separate transactions involved in acquiring the land and buildings that transfer duty may be payable on the land acquired. For example, if vacant land is acquired from one person (non-vendor) and the building work is carried out by another person (vendor), transfer duty will be payable on the land and VAT will be payable on the construction work for the building.

Developers and builders who attempt to avoid VAT registration or avoid paying VAT on certain transactions could face prosecution and could be liable for administrative non-compliance penalties, as well as interest on the amounts not paid, as well as understatement penalties of up to 200% of the tax payable.

14 Also see 2.3.4.

Transfer Duty Guide Chapter 2

19

Examples of this include –

• the intentional structuring of transactions in such a manner that it appears that the supply of the land and the supply of the buildings are unconnected or are made by separate (unconnected) persons, when this is in fact not the case; or

• documents submitted to SARS which are intended to be deliberately misleading, or are omitted for the purposes of obtaining a transfer duty exemption or zero-rating, or in an attempt to pay duty on a lower amount, or to pay transfer duty instead of VAT.

Example 1 – Plot and plan: VAT anti-avoidance provisions

Facts:

Mrs M is a property developer and trades as a sole proprietor under the name ABC Properties (ABC). She is also the sole member of XYZ Construction CC (XYZ). ABC sells vacant stands in residential developments to customers and in terms of that contract, the client is required to conclude a separate contract with XYZ to build the residences on the land sold to them by ABC. ABC is not registered for VAT as its supplies of vacant stands is below the R1 million threshold for compulsory VAT registration. XYZ is registered for VAT. Mrs M deliberately split her activities to avoid having to register ABC for VAT purposes.

What are the VAT and transfer duty implications of this situation?

Result:

Section 50A of the VAT Act, is an anti-avoidance provision. It provides that where it appears to the Commissioner that the person is attempting to avoid VAT registration by artificially splitting the activities of a single enterprise between various persons, the Commissioner can deem the separate persons to be one and the same for VAT purposes.

Since Mrs M appears to be continuously or regularly supplying stands and/or plot and plan projects and has deliberately split her activities, the Commissioner may regard Mrs M and XYZ Construction cc as one and the same person. The effect of this anti-avoidance provision is that the Commissioner will aggregate the consideration paid or payable for the land and buildings to determine if the R1 million threshold for compulsory VAT registration under section 23 of the VAT Act has been exceeded. It follows that VAT will be payable on the full consideration received for the land and any improvements to be effected on that land at the standard rate under section 7(1)(a) of the VAT Act.

Alternatively, if section 50A of the VAT Act does not apply in this situation, the buyer would pay transfer duty on the unimproved land acquired from ABC and VAT on the construction services acquired from XYZ. The VAT and transfer duty treatment of the transactions will, therefore, ultimately depend on the structure of the agreement(s) and whether or not the suppliers are connected persons for VAT purposes. It is also important to note the anti-avoidance provisions contained in section 50A of the VAT Act when considering the exemption under section 9(15) (see 8.2.21).

Transfer Duty Guide Chapter 2

20

2.4.5 Tenant improvements

Transfer duty on property that is sold to a tenant who effected improvements to the property whilst being the bona fide possessor of the land, is calculated on the fair value of the property less the value of any improvements effected by that tenant.

In Kommissaris van Binnelandse Inkomste v Anglo American (OFS) Housing Company Ltd,15 the tenant who was also the bona fide possessor of land but not the owner thereof, erected houses costing more than £900 000 on the leased property. The tenant later bought the property for £129 555 and the Commissioner claimed that transfer duty should be paid on an amount in excess of £1 million, being the fair market value of the property (including the houses). The Court found that this approach was incorrect as the possessor’s right of retention diminished the dominium of the owner who was not able to sell more than such diminished dominium.

2.4.6 Shares, members’ interests and contingent rights relating to residential property

Paragraphs (b) and (c) of the definition of the term “fair value” refer to the situations in paragraphs (d), (e) and (f) of the definition of the term “property”.16 This deals with the trading of shares in companies, interests in close corporations and contingent rights in trusts which are associated with the use or ownership of “residential property” through the holding of those shares, interests or rights.17 These rules were introduced as anti-avoidance measures to deal with transactions which had the effect that the use or enjoyment of “residential property”18 could be obtained either –

• directly, by purchasing shares in a “residential property company”19 which owns the residential property; or

• indirectly, by acquiring shares in a holding company which would, together with its subsidiaries, have been regarded as a “residential property company” had they not been separate entities; or

• by substituting a beneficiary or trustee of a discretionary trust which owns residential property through its ownership of shares or interests in a “residential property company”.

The effect of these provisions is that the person acquiring rights to “residential property” in this manner can no longer avoid the payment of transfer duty on the basis that no “property” had been acquired. In these cases the “fair value” is the proportional share of the fair market value of any property held by the company which is attributable to the shares, interests or rights to which they relate. In other words, the value of the company’s residential property is attributed to the various share block owners in proportion to their overall shareholding in the company.

15 1960 (3) SA 642 (A). 16 This rule applied before 1 September 2009 if the shareblock transaction constituted the supply of

“residential property”. 17 A Real Estate Investment Trust (REIT) does not fall within the definition of “residential property

company”. The transfer of shares in a REIT will, as a result, not be subject to transfer duty. See 2.7. 18 As defined in section 1(1). 19 Residential property companies are companies (including close corporations) that own “residential

property”, whether directly or indirectly or by way of contingent rights to trust property, as their primary assets.

Transfer Duty Guide Chapter 2

21

In determining the fair value of shares or similar interests in property, no account must be taken of any lease on the property or liability in respect of any loan or debt related to the property. The fair value of the property or contingent right held must, however, comprise more than 50% of the aggregate fair value of all the company’s assets. (Also see 2.5.10.)

The taxable value is the greater of the value of the consideration for the “residential property” or the fair value thereof (excluding any loan obligation).

Example 2 – Determining the fair value of “residential property” involving the purchase of shares, member’s interests etc

Facts:

M purchases the full extent of the member’s interest in a close corporation which has as its sole asset, a beach-front holiday apartment with a fair value of R700 000. The close corporation is not conducting an enterprise for VAT purposes and the apartment is used exclusively for the enjoyment of the member. The apartment originally cost R300 000, which was funded by a member’s contribution of R100 and a member’s loan of R299 900.

What is the fair value of the residential property owned by the close corporation?

Result:

M pays R400 100 for the transfer of the member’s interest and R299 900 for the member’s loan. The transfer duty payable is based on the fair value ignoring any loan liabilities. The fair value of the member’s interest is R700 000, being the fair value of the residential property owned by the close corporation.

2.4.7 Shares in a share block company

Share block transactions are subject to transfer duty unless they are subject to VAT (see 2.4.6, 2.5.10 and 2.5.11). The taxable value is the greater of the value of the consideration for the share block or the fair value thereof (excluding any loan obligation).

The same rules apply for determining the taxable value in cases where the shares constitute “residential property” as discussed in 2.4.1, 2.4.6 and 2.6.

In practice the application of this rule includes an analysis of market conditions, historical sales as well as the type and characteristics of the underlying property in much the same manner as one would expect for other types of property. In essence, the fair market value in an arm’s length transaction will usually be the sum of the price for the shares together with any outstanding loan obligation.20

20 In the case of “residential property” the fair value applies only to the extent that the shares relate to

the residential property itself and not to assets such as boats, aircraft or other movables which are not intended to fall within the scope of transfer duty.

Transfer Duty Guide Chapter 2

22

2.4.8 Special rules

Besides the definition of the term “fair value”, the Transfer Duty Act also contains a number of other provisions which relate to the determination of the value of the property acquired which will be subject to transfer duty. For example, sections 5 to 8 prescribe further rules as to –

• how the dutiable amount or fair value is determined in certain circumstances; and

• whether certain payments are to be included or excluded from the consideration which is regarded as being payable in respect of the acquisition of the property concerned.

For example, contractual rights granting permission to take clay or soil for the making of bricks also constitute registrable rights which may be subject to transfer duty (unless the transaction is subject to VAT). In such cases where the consideration is not paid in cash, but rather by way of rent, royalty, share of profits or by some periodical payment, section 8 prescribes what factors the Commissioner must consider in determining the dutiable amount or fair value in the circumstances.

2.5 “Property”

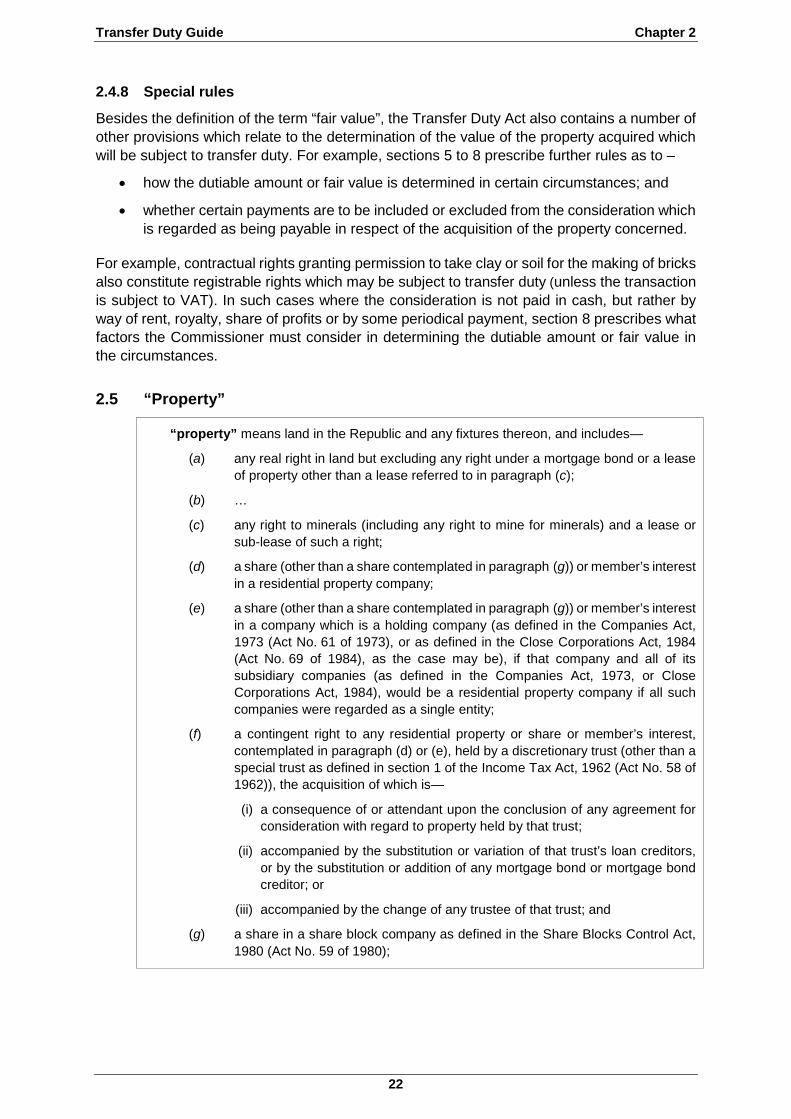

“property” means land in the Republic and any fixtures thereon, and includes—

(a) any real right in land but excluding any right under a mortgage bond or a lease of property other than a lease referred to in paragraph (c);

(b) …

(c) any right to minerals (including any right to mine for minerals) and a lease or sub-lease of such a right;

(d) a share (other than a share contemplated in paragraph (g)) or member’s interest in a residential property company;

(e) a share (other than a share contemplated in paragraph (g)) or member’s interest in a company which is a holding company (as defined in the Companies Act, 1973 (Act No. 61 of 1973), or as defined in the Close Corporations Act, 1984 (Act No. 69 of 1984), as the case may be), if that company and all of its subsidiary companies (as defined in the Companies Act, 1973, or Close Corporations Act, 1984), would be a residential property company if all such companies were regarded as a single entity;

(f) a contingent right to any residential property or share or member’s interest, contemplated in paragraph (d) or (e), held by a discretionary trust (other than a special trust as defined in section 1 of the Income Tax Act, 1962 (Act No. 58 of 1962)), the acquisition of which is—

(i) a consequence of or attendant upon the conclusion of any agreement for consideration with regard to property held by that trust;

(ii) accompanied by the substitution or variation of that trust’s loan creditors, or by the substitution or addition of any mortgage bond or mortgage bond creditor; or

(iii) accompanied by the change of any trustee of that trust; and

(g) a share in a share block company as defined in the Share Blocks Control Act, 1980 (Act No. 59 of 1980);

Transfer Duty Guide Chapter 2

23

2.5.1 Introduction

The acquisition of property is one of the two principal tax events that give rise to the liability to pay transfer duty. The other one is the renunciation of an interest in, or restriction upon, the use or disposal of property. “Property” is defined as including “land in the Republic and any fixtures thereon”. The definition further includes certain items and excludes others from the category of land and fixtures.

The most common forms of property and real rights in property are mentioned in paragraphs (a) and (c) of the definition which includes –

• land and any fixtures thereon;

• real rights in land but excluding rights under mortgage bonds or leases (other than the leases mentioned below); and

• rights to minerals or rights to mine for minerals (including any sub-lease of such a right).

These transactions are explained in more detail in 2.5.2 to 2.5.9. As they involve real rights, such transactions are required to be recorded in a Deeds Registry.

Paragraphs (d) to (g) of the definition of the term “property” are explained in 2.5.10 and 2.5.11. These transactions involve shares, rights and other interests in entities that own immovable property. Although these transactions are not recorded in a Deeds Registry, they are nevertheless transactions which will be subject to either VAT or transfer duty.

Fractional ownership and timeshare schemes which, depending on the type of scheme, could fall within paragraph (a), (d), (e), (f) or (g) of the definition of the term “property” are discussed in 2.5.12.

2.5.2 Land and fixtures – General

Land consists primarily of the soil, its geological components such as minerals and everything attached to the soil. The reference to land and fixtures is based on the well-established principle that anything which is permanently attached to the land forms part of the land and therefore acquires the status of immovable property. However, the acquisition of a fixture which must be removed from the land to which it is attached is not a dutiable event for transfer duty purposes, nor is there a dutiable event when a tenant permanently affixes assets to the property which become the owner’s property by operation of law (accession). This aspect is important when determining the fair value and the transfer duty payable on a transaction involving the sale of the land on which the fixture is located, as the value of the land increases due to the value added to the property by the addition of the fixture. Whether or not a fixture forms part of the land will depend on the facts and circumstances of each case.

A sectional title unit also qualifies as “land”,21 but rights attached to shares in a company that operates a share block scheme are rights to the use of immovable property or interests in immovable property22 and would not have qualified as “property” for transfer duty purposes had it not been specifically included.23

21 Sectional Titles Act 95 of 1986, section 2. 22 Share Blocks Control Act 59 of 1980, section 10. 23 See 2.5.10 and 2.5.11.

Transfer Duty Guide Chapter 2

24

2.5.3 Real rights in land

The question as to what constitutes a real right in land is a very complex one, but in practice a large measure of consensus exists between conveyancers and the Registrar of Deeds as regards registrable rights in land,24 without too much application of the underlying legal theory. The definition of the term “property” includes any real right in land, but a right under a mortgage bond is expressly excluded. A lease of property is also excluded, but this is subject to certain exceptions (see 2.5.6 and 2.5.8).

A real right in land is a right which is exercisable by the right holder against the owner of the land to which the right relates or anyone else who unlawfully infringes upon the holder’s ability to exercise that right. The owner of the land would, in turn, be obliged to tolerate the exploitation of the land or access to the land which is permitted by the right. This is why the registration of rights in land is important. It provides, as a matter of public record, information to prospective purchasers of land about the rights that others may have in that land.

The granting of a real right in land has been described as a “subtraction” from the ownership of land because an element of the ownership does not vest in the owner of the land until the right held over that land by the other person has been extinguished.

In a property transaction, the owner transfers the ownership of the land in its limited form to a person who acquires the land, as no person may transfer more rights than that person has vested in the land. Transfer of ownership of land and limited real rights in land are effected by way of registration in a Deeds Registry, however, this does not mean that the acquisition of a real right in land is not dutiable under the Transfer Duty Act unless it is registered.25

Some common examples of real rights in land include leases for mineral rights, mortgages,26 praedial servitudes, freehold ownership of property and rights of sectional title owners in exclusive use areas that are registerable as such.

Although the Deeds Registries Act does not provide absolute certainty as to the nature of a real right, for the purposes of this guide and paragraphs (a) and (c) of the definition of the term “property”, the term “real right” is considered to include –

• the rights referred to in section 3(1) of the Deeds Registries Act which must be registered by the Registrar; and

• those rights referred to in section 63(1) of that Act which have been registered as a result of the Registrar exercising a discretion, or making a determination in that regard.