transfer pricing - financial transactions fs... · transfer pricing - financial transactions...

TRANSCRIPT

Transfer Pricing - Financial Transactions

Bhavesh Dedhia29th April 2016

Agenda

Overview

Equity Capital

Loans

Accounts Receivables

Guarantees

Letter of Comforts

Key Takeaways

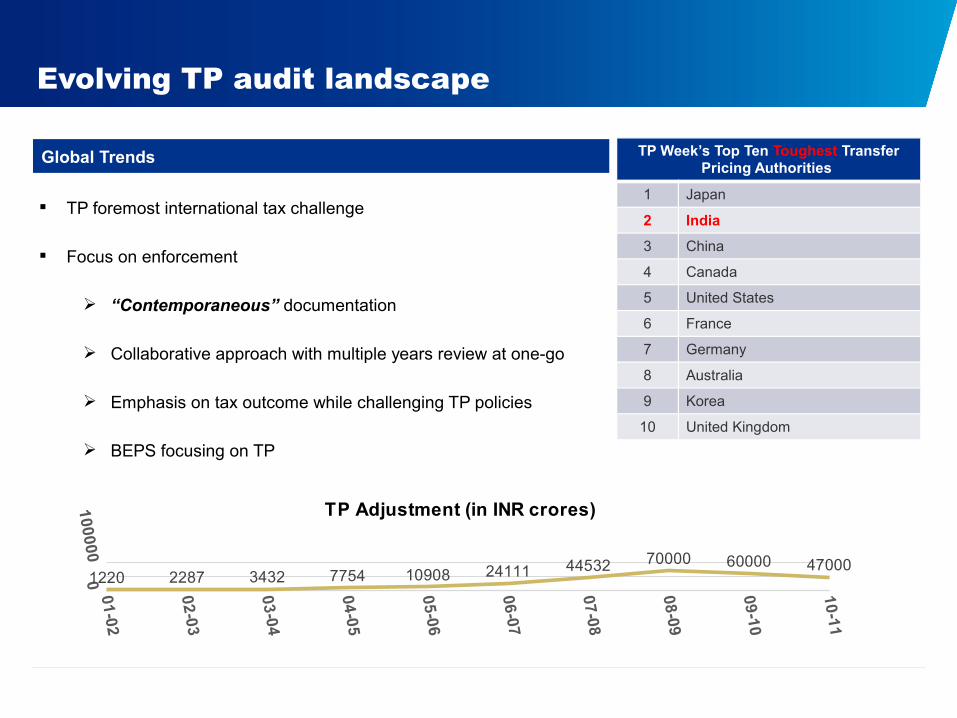

Evolving TP audit landscape

TP Week’s Top Ten Toughest Transfer Pricing Authorities

1 Japan

2 India

3 China

4 Canada

5 United States

6 France

7 Germany

8 Australia

9 Korea

10 United Kingdom

TP foremost international tax challenge

Focus on enforcement

“Contemporaneous” documentation

Collaborative approach with multiple years review at one-go

Emphasis on tax outcome while challenging TP policies

BEPS focusing on TP

Global Trends

1220 2287 3432 7754 10908 24111 44532 70000 60000 47000

TP Adjustment (in INR crores)

Focus on Financial transactionsKey Challenges

Financial international transactions comprising of equity infusion, loans, debts, guarantees, letter of comforts, etc. are common across the Industry and are often soft targets of the TPOs

Regulatory considerations – SEBI, RBI regulations etc.,

No specific guidance from Indian Transfer Pricing Regulations or OECD TP Guidelines

Limited judicial precedence - Lack of certainty in determining arm’s length price

Commercial expediency not being accepted

Stringent penalties

Retrospective amendments / explanations adds to uncertainty

Huge back-log of cases – Many cases are being remanded back to officers for fresh adjudication

Litigation is the basic legal right which guarantees every corporation its decade in court- David Porter, US Navy, (1813-1891)

5

Issues relating to Interest Free Loans

Granting of interest free loans has historically led to tax controversies with the Revenue authorities.

Issues:• Real Income

• Quasi Equity

• Purpose and Terms of Loan – Investment or for Working Capital purposes

• Ability of the AE to raise funds independently?

• Whether compulsorily convertible into debt?

• Rates to be adopted for benchmarking – Standard Bank rates, LIBOR, EURIBOR, PLR

• Limited information available on similar ECBs for application of CUP

Financial Transactions – Loans

Equity Financing

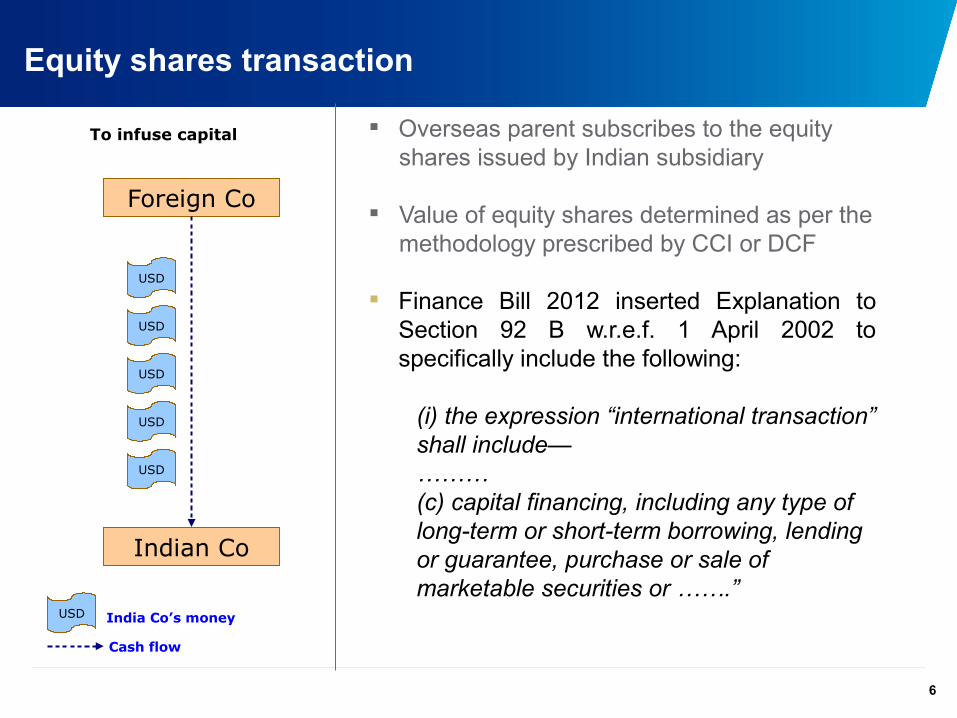

Equity shares transaction

Foreign Co

Indian Co

To infuse capital

USD

USD

USD

USD

USD

Cash flow

USD India Co’s money

6

Overseas parent subscribes to the equity shares issued by Indian subsidiary

Value of equity shares determined as per the methodology prescribed by CCI or DCF

Finance Bill 2012 inserted Explanation to Section 92 B w.r.e.f. 1 April 2002 to specifically include the following:

(i) the expression “international transaction” shall include—………(c) capital financing, including any type of long-term or short-term borrowing, lending or guarantee, purchase or sale of marketable securities or …….”

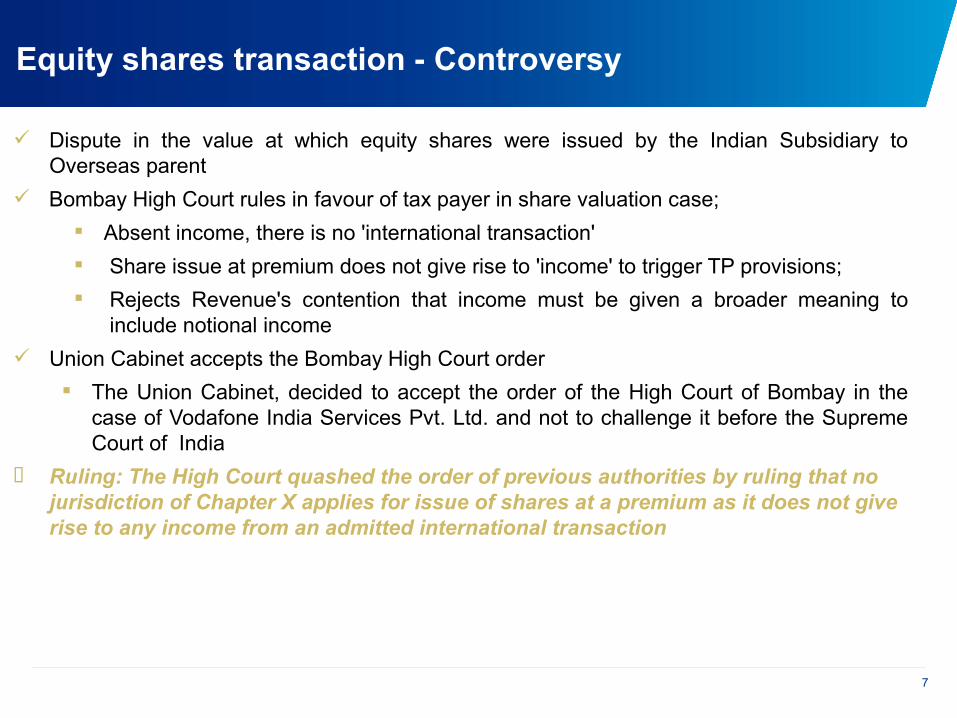

Equity shares transaction - Controversy

Dispute in the value at which equity shares were issued by the Indian Subsidiary to Overseas parent

Bombay High Court rules in favour of tax payer in share valuation case;

Absent income, there is no 'international transaction'

Share issue at premium does not give rise to 'income' to trigger TP provisions;

Rejects Revenue's contention that income must be given a broader meaning to include notional income

Union Cabinet accepts the Bombay High Court order

The Union Cabinet, decided to accept the order of the High Court of Bombay in the case of Vodafone India Services Pvt. Ltd. and not to challenge it before the Supreme Court of India

• Ruling: The High Court quashed the order of previous authorities by ruling that no jurisdiction of Chapter X applies for issue of shares at a premium as it does not give rise to any income from an admitted international transaction

7

8

Issues relating to Interest Free Loans

Granting of interest free loans has historically led to tax controversies with the Revenue authorities.

Issues:• Real Income

• Quasi Equity

• Purpose and Terms of Loan – Investment or for Working Capital purposes

• Ability of the AE to raise funds independently?

• Whether compulsorily convertible into debt?

• Rates to be adopted for benchmarking – Standard Bank rates, LIBOR, EURIBOR, PLR

• Limited information available on similar ECBs for application of CUP

Financial Transactions – Loans

Loans

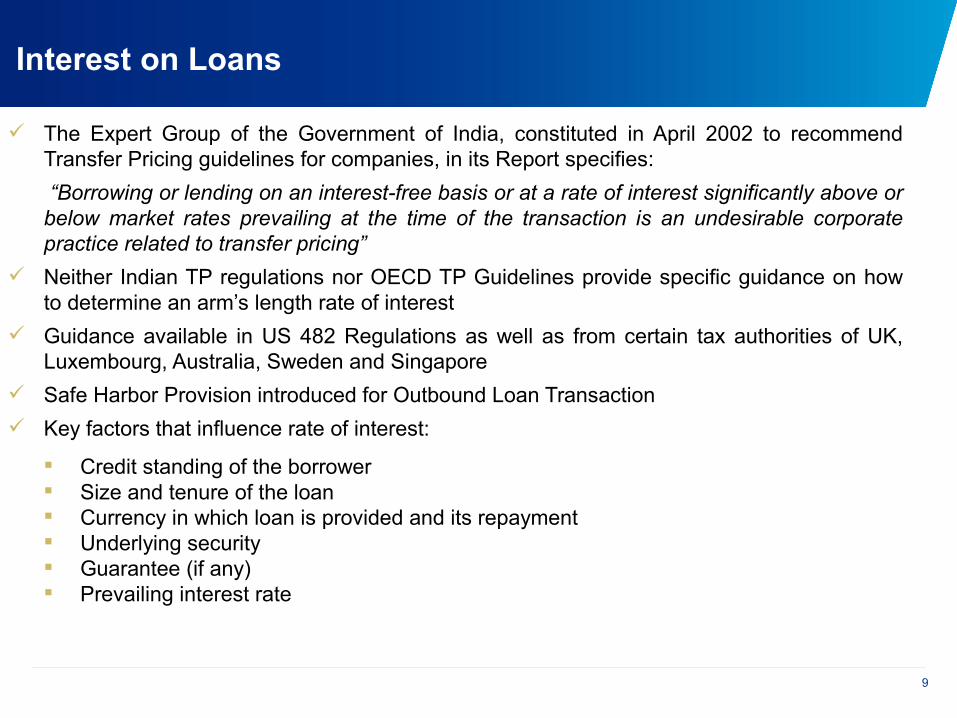

Interest on Loans

The Expert Group of the Government of India, constituted in April 2002 to recommend Transfer Pricing guidelines for companies, in its Report specifies:

“Borrowing or lending on an interest-free basis or at a rate of interest significantly above or below market rates prevailing at the time of the transaction is an undesirable corporate practice related to transfer pricing”

Neither Indian TP regulations nor OECD TP Guidelines provide specific guidance on how to determine an arm’s length rate of interest

Guidance available in US 482 Regulations as well as from certain tax authorities of UK, Luxembourg, Australia, Sweden and Singapore

Safe Harbor Provision introduced for Outbound Loan Transaction

Key factors that influence rate of interest:

Credit standing of the borrower Size and tenure of the loan Currency in which loan is provided and its repayment Underlying security Guarantee (if any) Prevailing interest rate

9

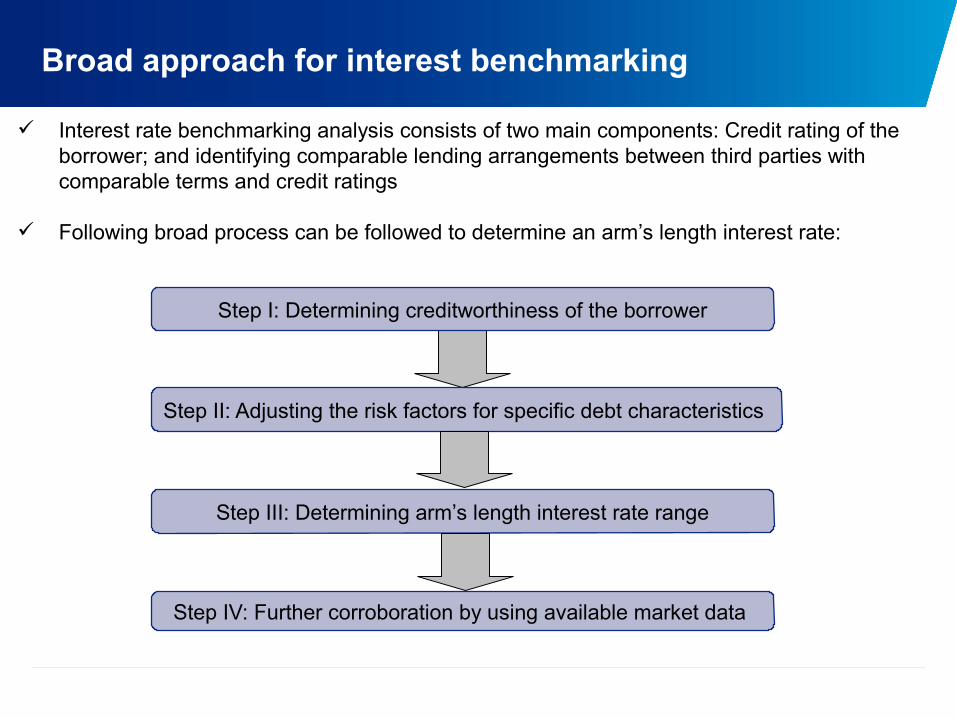

Broad approach for interest benchmarking

Step II: Adjusting the risk factors for specific debt characteristics

Step III: Determining arm’s length interest rate range

Step I: Determining creditworthiness of the borrower

Step IV: Further corroboration by using available market data

Interest rate benchmarking analysis consists of two main components: Credit rating of the borrower; and identifying comparable lending arrangements between third parties with comparable terms and credit ratings

Following broad process can be followed to determine an arm’s length interest rate:

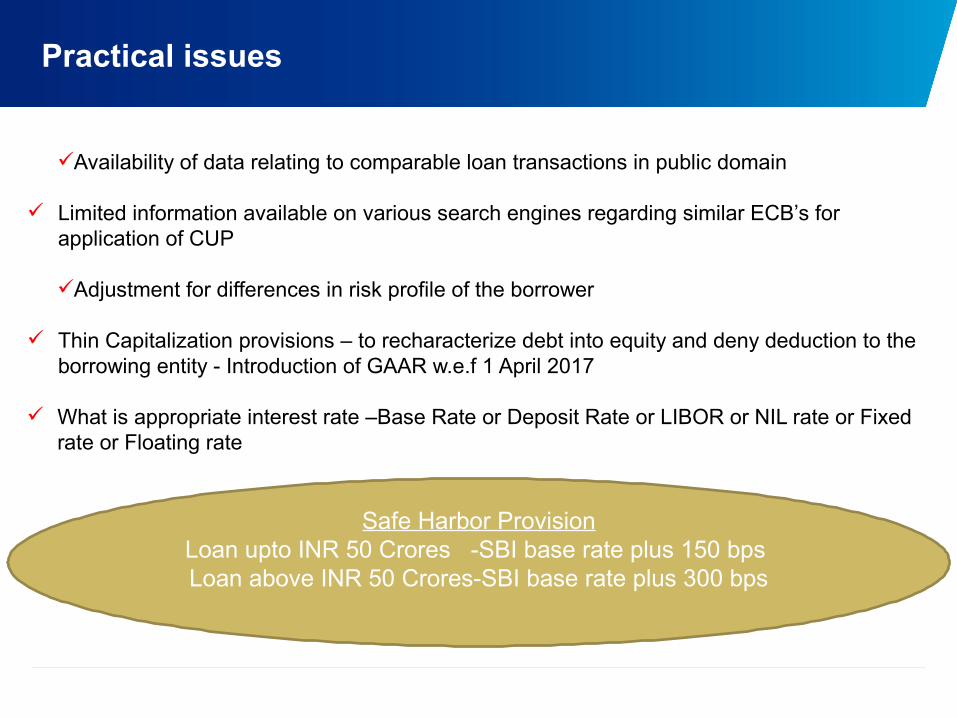

Availability of data relating to comparable loan transactions in public domain

Limited information available on various search engines regarding similar ECB’s for application of CUP

Adjustment for differences in risk profile of the borrower

Thin Capitalization provisions – to recharacterize debt into equity and deny deduction to the borrowing entity - Introduction of GAAR w.e.f 1 April 2017

What is appropriate interest rate –Base Rate or Deposit Rate or LIBOR or NIL rate or Fixed rate or Floating rate

Practical issues

Safe Harbor ProvisionLoan upto INR 50 Crores -SBI base rate plus 150 bps Loan above INR 50 Crores-SBI base rate plus 300 bps

Thinly capitalized entity = Excessive debt leading to excessive interest deductions

Different countries have adopted different mechanism to deal with the issues arising out of thin capitalization (UK, US, Australia, Netherlands, Germany)

Fixed Ratio Approach - quantum of interest on debt in excess of a pre-fixed ratio of equity is disallowed

Subjective Approach – Terms and nature of instrument considered to decide the real nature of the instrument – debt / equity

Earnings threshold approach - Maximum amount of allowable interest is defined as a percentage of EBITDA

Concept of thin capitalization has been introduced in India in form GAAR provisions by allowing re-characterization of debt as equity and vice-versa, in case of impermissible avoidance arrangements

Concept of Thin Capitalization

Not only interest rate but also the debt equity mix of the borrower would need to meet the arm’s length standard

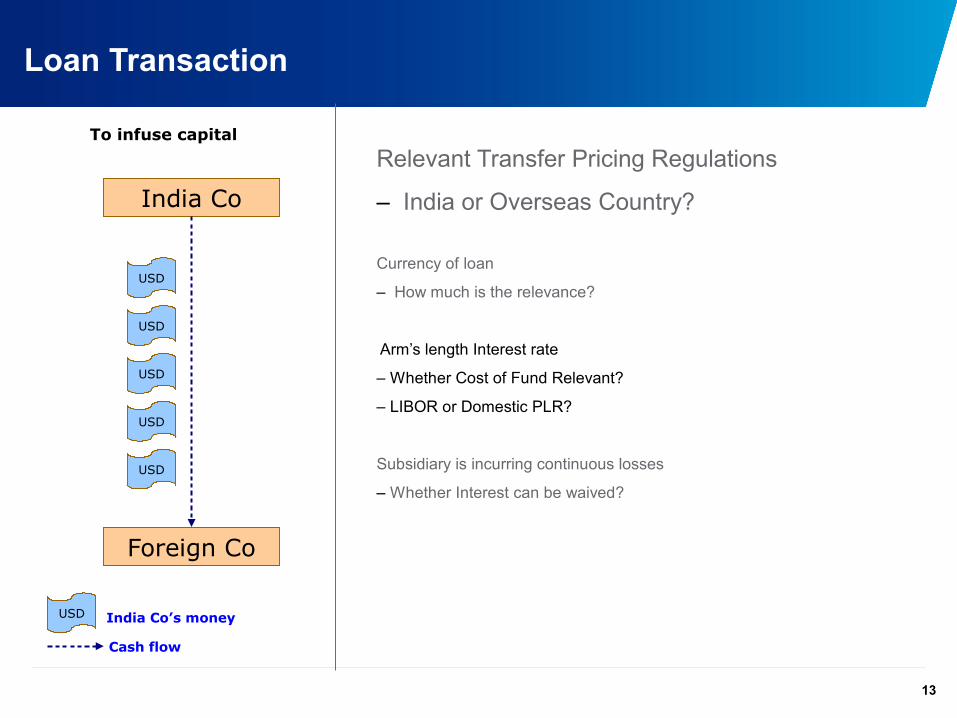

Loan Transaction

India Co

Foreign Co

To infuse capital

USD

USD

USD

USD

USD

Cash flow

USD India Co’s money

13

Relevant Transfer Pricing Regulations

– India or Overseas Country?

Currency of loan

– How much is the relevance?

Arm’s length Interest rate

– Whether Cost of Fund Relevant?

– LIBOR or Domestic PLR?

Subsidiary is incurring continuous losses

– Whether Interest can be waived?

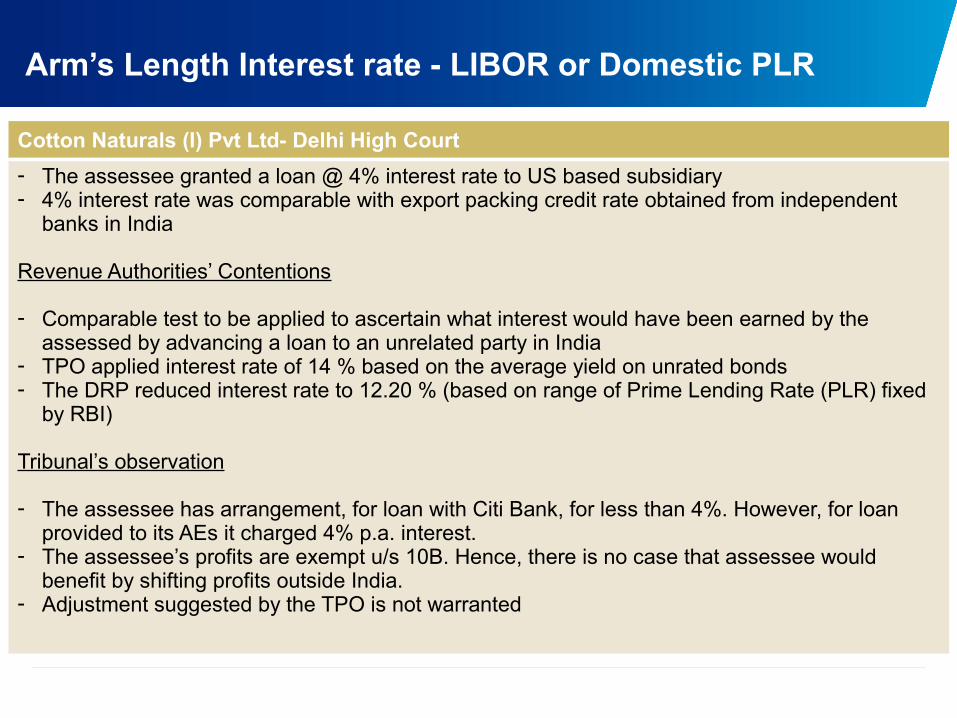

Arm’s Length Interest rate - LIBOR or Domestic PLR

Cotton Naturals (I) Pvt Ltd- Delhi High Court

- The assessee granted a loan @ 4% interest rate to US based subsidiary- 4% interest rate was comparable with export packing credit rate obtained from independent

banks in India

Revenue Authorities’ Contentions

- Comparable test to be applied to ascertain what interest would have been earned by the assessed by advancing a loan to an unrelated party in India

- TPO applied interest rate of 14 % based on the average yield on unrated bonds - The DRP reduced interest rate to 12.20 % (based on range of Prime Lending Rate (PLR) fixed

by RBI)

Tribunal’s observation

- The assessee has arrangement, for loan with Citi Bank, for less than 4%. However, for loan provided to its AEs it charged 4% p.a. interest.

- The assessee’s profits are exempt u/s 10B. Hence, there is no case that assessee would benefit by shifting profits outside India.

- Adjustment suggested by the TPO is not warranted

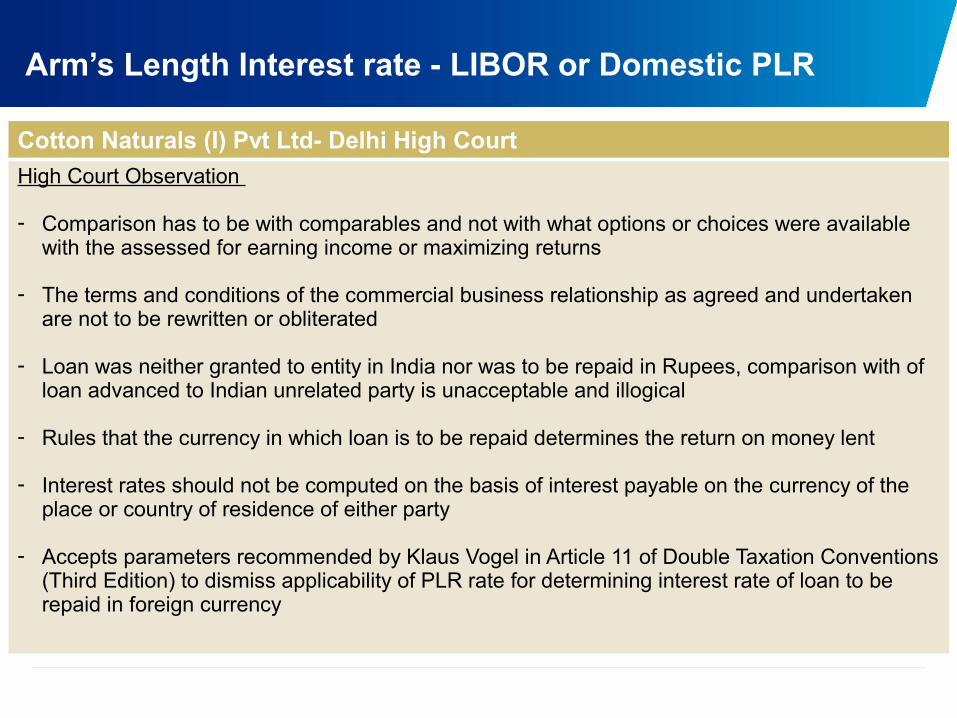

Arm’s Length Interest rate - LIBOR or Domestic PLR

Cotton Naturals (I) Pvt Ltd- Delhi High Court

High Court Observation

- Comparison has to be with comparables and not with what options or choices were available with the assessed for earning income or maximizing returns

- The terms and conditions of the commercial business relationship as agreed and undertaken are not to be rewritten or obliterated

- Loan was neither granted to entity in India nor was to be repaid in Rupees, comparison with of loan advanced to Indian unrelated party is unacceptable and illogical

- Rules that the currency in which loan is to be repaid determines the return on money lent

- Interest rates should not be computed on the basis of interest payable on the currency of the place or country of residence of either party

- Accepts parameters recommended by Klaus Vogel in Article 11 of Double Taxation Conventions (Third Edition) to dismiss applicability of PLR rate for determining interest rate of loan to be repaid in foreign currency

Arm’s Length Interest rate - LIBOR or Domestic PLR

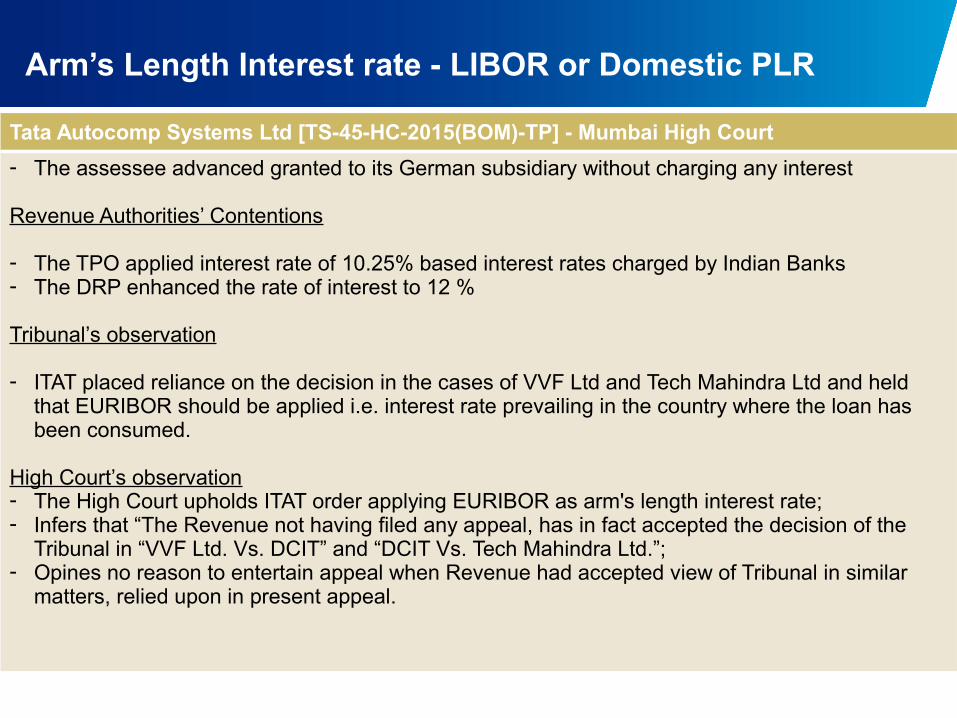

Tata Autocomp Systems Ltd [TS-45-HC-2015(BOM)-TP] - Mumbai High Court

- The assessee advanced granted to its German subsidiary without charging any interest

Revenue Authorities’ Contentions

- The TPO applied interest rate of 10.25% based interest rates charged by Indian Banks- The DRP enhanced the rate of interest to 12 %

Tribunal’s observation

- ITAT placed reliance on the decision in the cases of VVF Ltd and Tech Mahindra Ltd and held that EURIBOR should be applied i.e. interest rate prevailing in the country where the loan has been consumed.

High Court’s observation- The High Court upholds ITAT order applying EURIBOR as arm's length interest rate;- Infers that “The Revenue not having filed any appeal, has in fact accepted the decision of the

Tribunal in “VVF Ltd. Vs. DCIT” and “DCIT Vs. Tech Mahindra Ltd.”;- Opines no reason to entertain appeal when Revenue had accepted view of Tribunal in similar

matters, relied upon in present appeal.

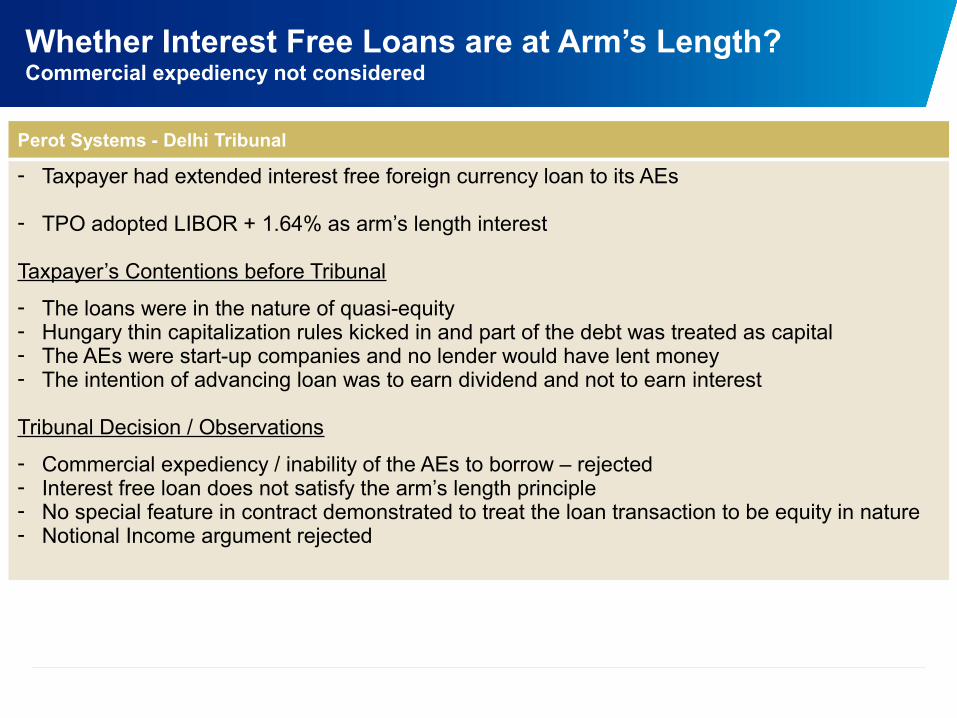

Whether Interest Free Loans are at Arm’s Length?Commercial expediency not considered

Perot Systems - Delhi Tribunal

- Taxpayer had extended interest free foreign currency loan to its AEs

- TPO adopted LIBOR + 1.64% as arm’s length interest

Taxpayer’s Contentions before Tribunal

- The loans were in the nature of quasi-equity- Hungary thin capitalization rules kicked in and part of the debt was treated as capital- The AEs were start-up companies and no lender would have lent money- The intention of advancing loan was to earn dividend and not to earn interest

Tribunal Decision / Observations

- Commercial expediency / inability of the AEs to borrow – rejected- Interest free loan does not satisfy the arm’s length principle- No special feature in contract demonstrated to treat the loan transaction to be equity in nature- Notional Income argument rejected

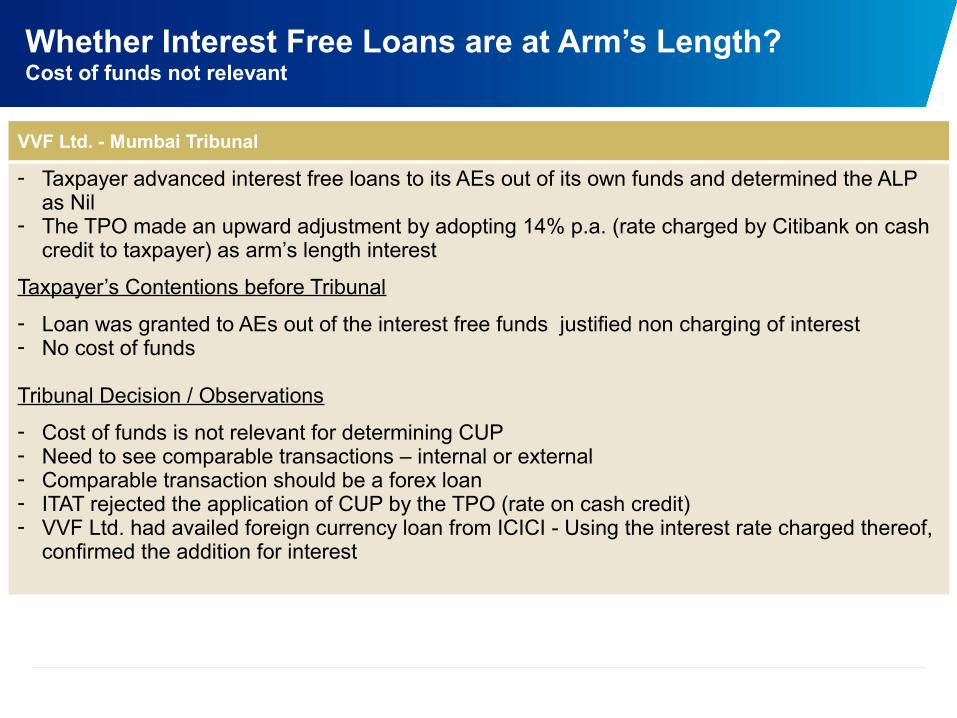

VVF Ltd. - Mumbai Tribunal

- Taxpayer advanced interest free loans to its AEs out of its own funds and determined the ALP as Nil

- The TPO made an upward adjustment by adopting 14% p.a. (rate charged by Citibank on cash credit to taxpayer) as arm’s length interest

Taxpayer’s Contentions before Tribunal

- Loan was granted to AEs out of the interest free funds justified non charging of interest- No cost of funds

Tribunal Decision / Observations

- Cost of funds is not relevant for determining CUP- Need to see comparable transactions – internal or external- Comparable transaction should be a forex loan- ITAT rejected the application of CUP by the TPO (rate on cash credit)- VVF Ltd. had availed foreign currency loan from ICICI - Using the interest rate charged thereof,

confirmed the addition for interest

Whether Interest Free Loans are at Arm’s Length?Cost of funds not relevant

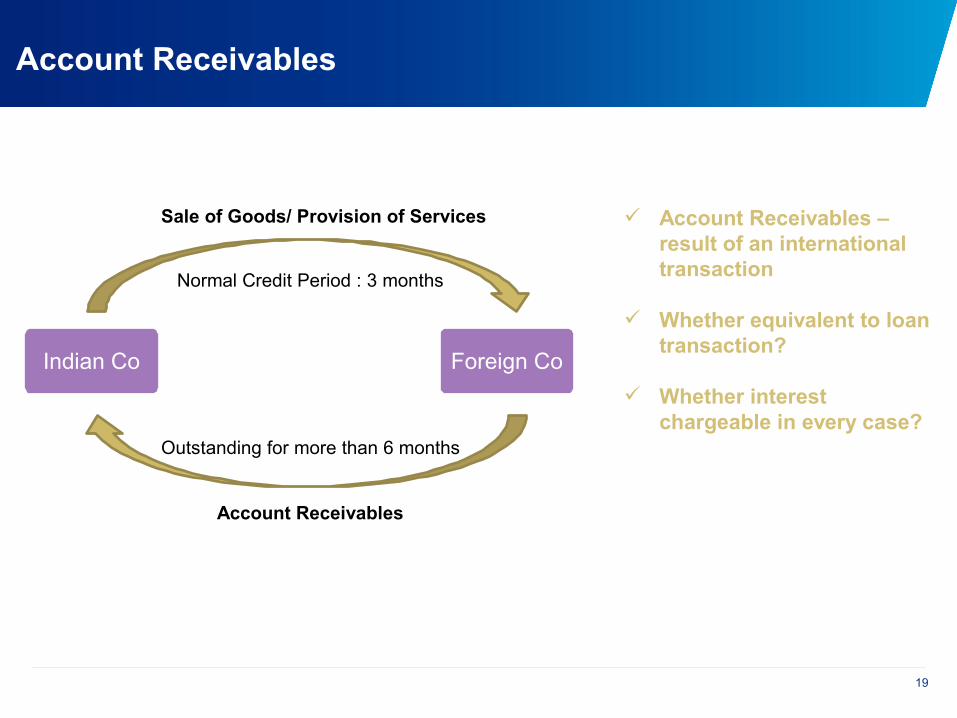

Account Receivables

19

Account Receivables – result of an international transaction

Whether equivalent to loan transaction?

Whether interest chargeable in every case?

Normal Credit Period : 3 months

Indian Co Foreign Co

Outstanding for more than 6 months

Sale of Goods/ Provision of Services

Account Receivables

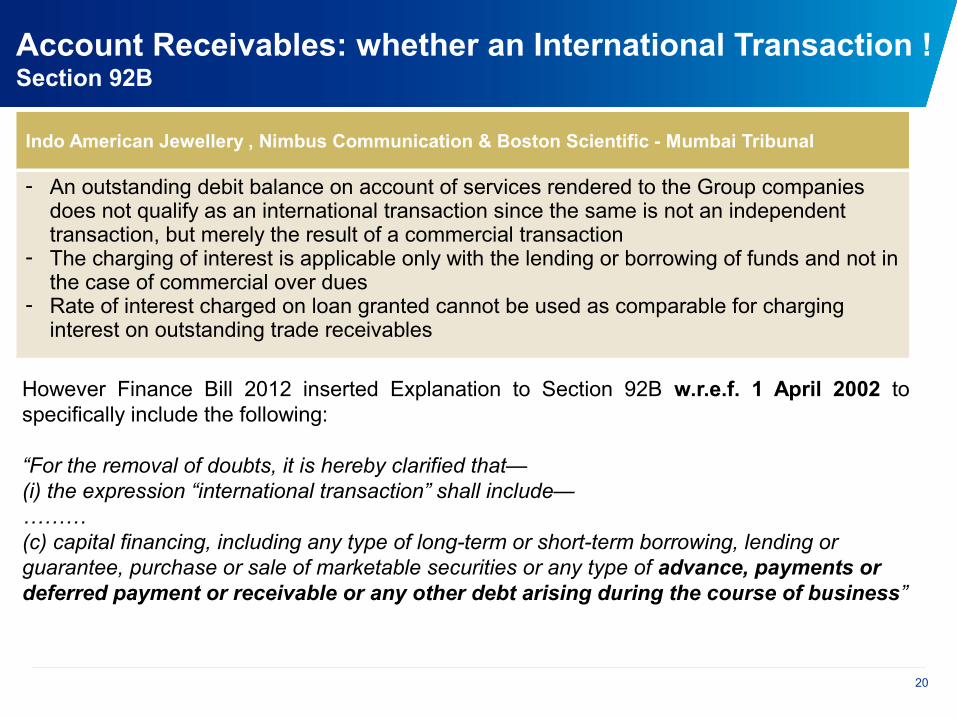

Account Receivables: whether an International Transaction !Section 92B

However Finance Bill 2012 inserted Explanation to Section 92B w.r.e.f. 1 April 2002 to specifically include the following:

“For the removal of doubts, it is hereby clarified that—(i) the expression “international transaction” shall include—………(c) capital financing, including any type of long-term or short-term borrowing, lending or guarantee, purchase or sale of marketable securities or any type of advance, payments or deferred payment or receivable or any other debt arising during the course of business”

20

Indo American Jewellery , Nimbus Communication & Boston Scientific - Mumbai Tribunal

- An outstanding debit balance on account of services rendered to the Group companies does not qualify as an international transaction since the same is not an independent transaction, but merely the result of a commercial transaction

- The charging of interest is applicable only with the lending or borrowing of funds and not in the case of commercial over dues

- Rate of interest charged on loan granted cannot be used as comparable for charging interest on outstanding trade receivables

21

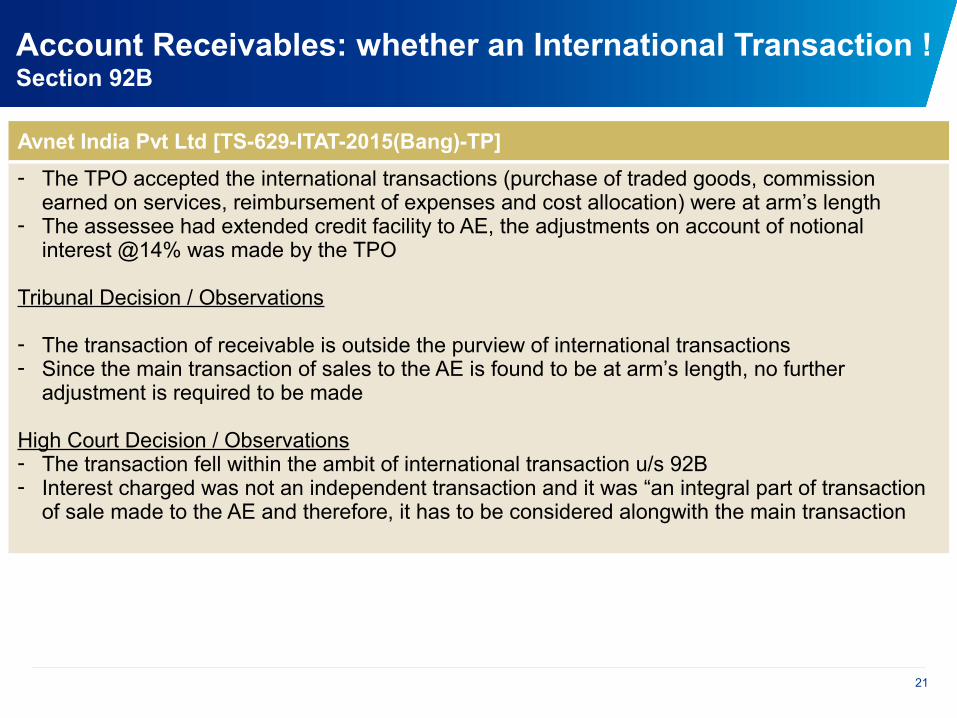

Avnet India Pvt Ltd [TS-629-ITAT-2015(Bang)-TP]

- The TPO accepted the international transactions (purchase of traded goods, commission earned on services, reimbursement of expenses and cost allocation) were at arm’s length

- The assessee had extended credit facility to AE, the adjustments on account of notional interest @14% was made by the TPO

Tribunal Decision / Observations

- The transaction of receivable is outside the purview of international transactions- Since the main transaction of sales to the AE is found to be at arm’s length, no further

adjustment is required to be made

High Court Decision / Observations- The transaction fell within the ambit of international transaction u/s 92B- Interest charged was not an independent transaction and it was “an integral part of transaction

of sale made to the AE and therefore, it has to be considered alongwith the main transaction

Account Receivables: whether an International Transaction !Section 92B

22

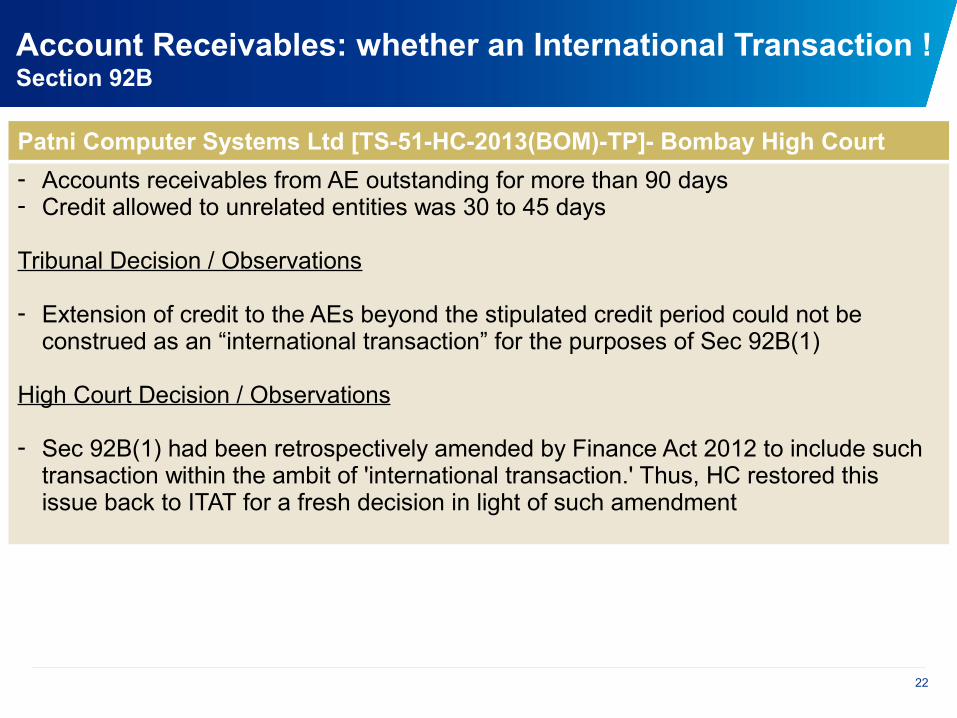

Patni Computer Systems Ltd [TS-51-HC-2013(BOM)-TP]- Bombay High Court

- Accounts receivables from AE outstanding for more than 90 days- Credit allowed to unrelated entities was 30 to 45 days

Tribunal Decision / Observations

- Extension of credit to the AEs beyond the stipulated credit period could not be construed as an “international transaction” for the purposes of Sec 92B(1)

High Court Decision / Observations

- Sec 92B(1) had been retrospectively amended by Finance Act 2012 to include such transaction within the ambit of 'international transaction.' Thus, HC restored this issue back to ITAT for a fresh decision in light of such amendment

Account Receivables: whether an International Transaction !Section 92B

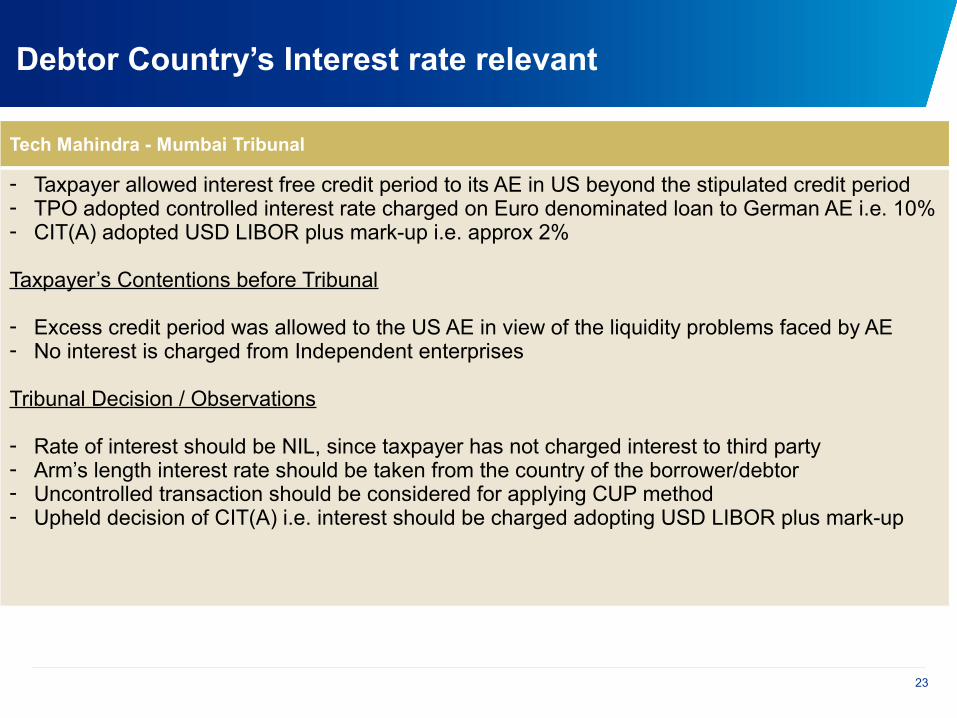

Debtor Country’s Interest rate relevant

23

Tech Mahindra - Mumbai Tribunal

- Taxpayer allowed interest free credit period to its AE in US beyond the stipulated credit period- TPO adopted controlled interest rate charged on Euro denominated loan to German AE i.e. 10%- CIT(A) adopted USD LIBOR plus mark-up i.e. approx 2%

Taxpayer’s Contentions before Tribunal

- Excess credit period was allowed to the US AE in view of the liquidity problems faced by AE- No interest is charged from Independent enterprises

Tribunal Decision / Observations

- Rate of interest should be NIL, since taxpayer has not charged interest to third party- Arm’s length interest rate should be taken from the country of the borrower/debtor- Uncontrolled transaction should be considered for applying CUP method - Upheld decision of CIT(A) i.e. interest should be charged adopting USD LIBOR plus mark-up

Guarantees and Letter of Comforts

Understanding of Guarantees

Guarantee is a legally binding agreement under which, the guarantor agrees to pay the amount due on a loan instrument in the event of default by the borrower

From an economic point of view, the returns on guarantee are linked more with risk than the cost of providing such facility

Why are guarantees given?

Provided solely because of ownership interest i.e. in its capacity as shareholder

To support downstream subsidiaries, so that the Assessee’s business can grow

Without guarantee, subsidiaries would not get any loan from banks

Quasi – Equity in nature

25

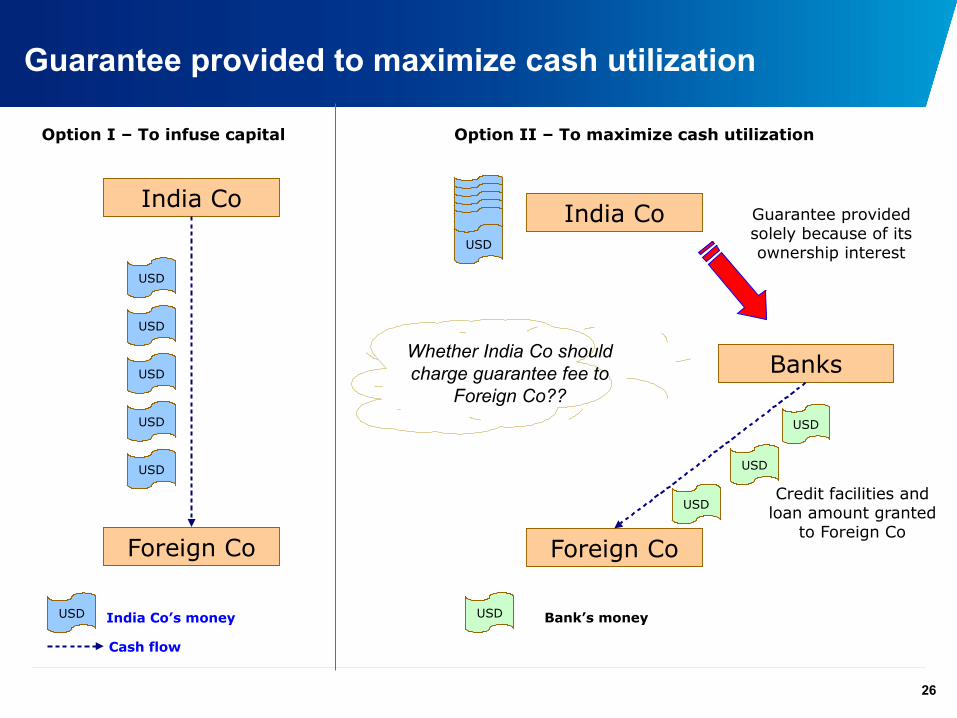

Guarantee provided to maximize cash utilization

India Co

Foreign Co

Option I – To infuse capital Option II – To maximize cash utilization

India Co

Foreign Co

Banks

USD

USD

USD

USD

USD

USD

Cash flow

USD

USD

USD

USD India Co’s money USD Bank’s money

Guarantee provided solely because of its ownership interest

26

Whether India Co should charge guarantee fee to

Foreign Co??

Credit facilities and loan amount granted

to Foreign Co

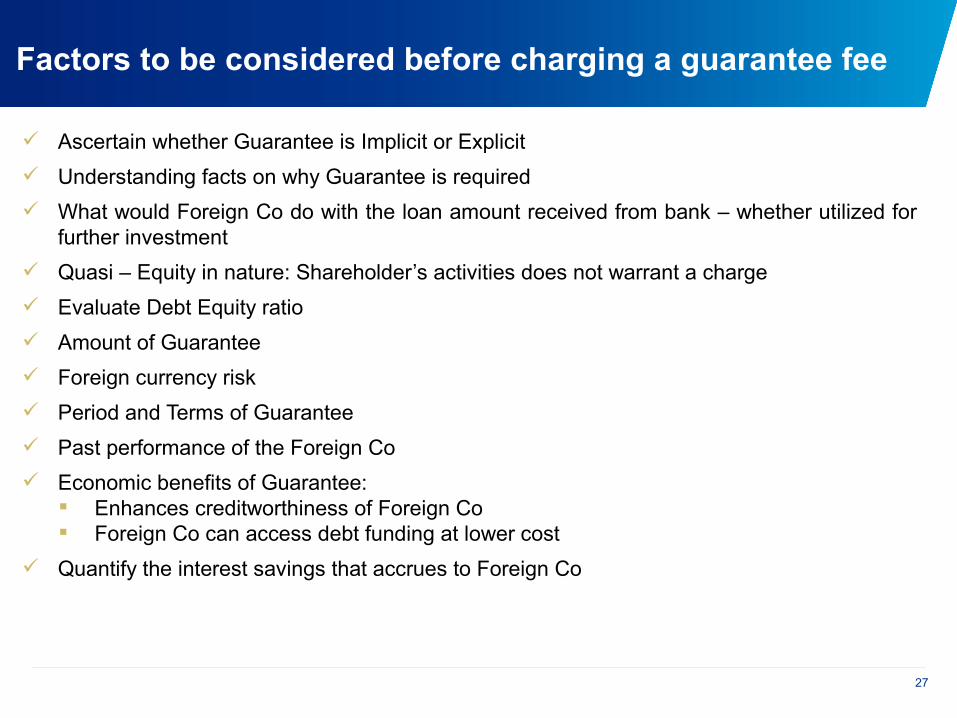

Factors to be considered before charging a guarantee fee

Ascertain whether Guarantee is Implicit or Explicit

Understanding facts on why Guarantee is required

What would Foreign Co do with the loan amount received from bank – whether utilized for further investment

Quasi – Equity in nature: Shareholder’s activities does not warrant a charge

Evaluate Debt Equity ratio

Amount of Guarantee

Foreign currency risk

Period and Terms of Guarantee

Past performance of the Foreign Co

Economic benefits of Guarantee: Enhances creditworthiness of Foreign Co Foreign Co can access debt funding at lower cost

Quantify the interest savings that accrues to Foreign Co

27

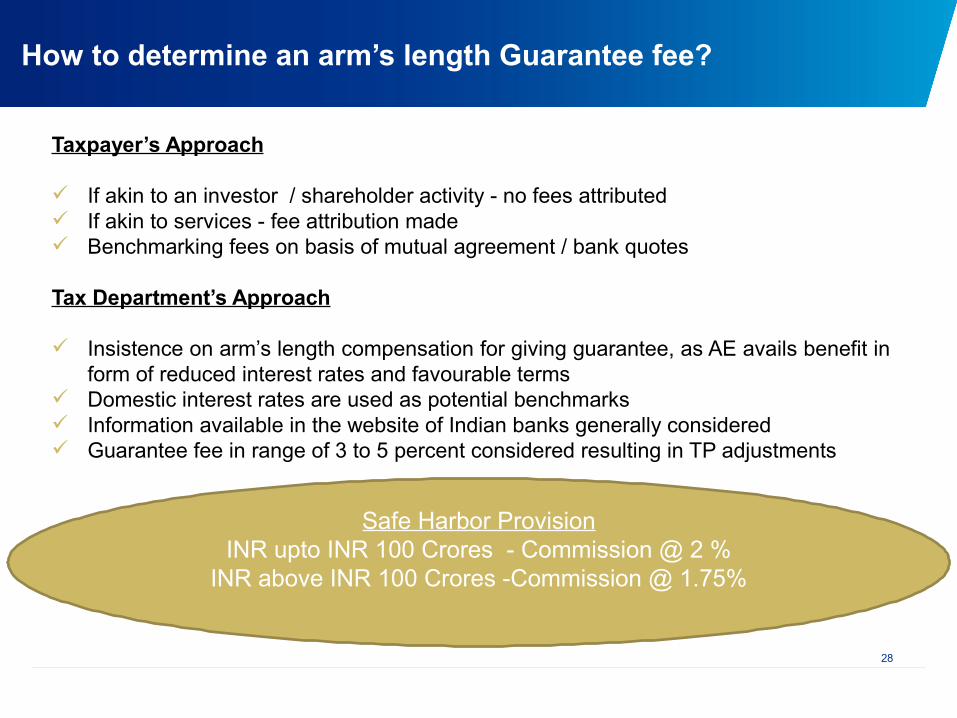

How to determine an arm’s length Guarantee fee?

Taxpayer’s Approach

If akin to an investor / shareholder activity - no fees attributed If akin to services - fee attribution made Benchmarking fees on basis of mutual agreement / bank quotes

Tax Department’s Approach

Insistence on arm’s length compensation for giving guarantee, as AE avails benefit in form of reduced interest rates and favourable terms

Domestic interest rates are used as potential benchmarks Information available in the website of Indian banks generally considered Guarantee fee in range of 3 to 5 percent considered resulting in TP adjustments

28

Safe Harbor ProvisionINR upto INR 100 Crores - Commission @ 2 %

INR above INR 100 Crores -Commission @ 1.75%

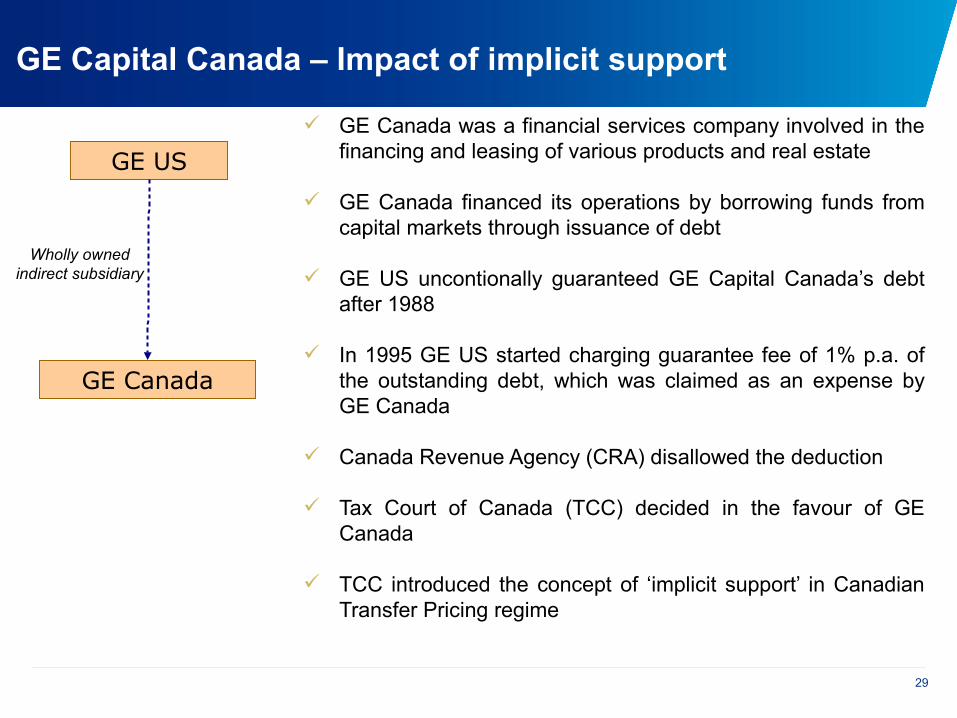

GE Capital Canada – Impact of implicit support

29

GE US

GE Canada

Wholly owned indirect subsidiary

GE Canada was a financial services company involved in the financing and leasing of various products and real estate

GE Canada financed its operations by borrowing funds from capital markets through issuance of debt

GE US uncontionally guaranteed GE Capital Canada’s debt after 1988

In 1995 GE US started charging guarantee fee of 1% p.a. of the outstanding debt, which was claimed as an expense by GE Canada

Canada Revenue Agency (CRA) disallowed the deduction

Tax Court of Canada (TCC) decided in the favour of GE Canada

TCC introduced the concept of ‘implicit support’ in Canadian Transfer Pricing regime

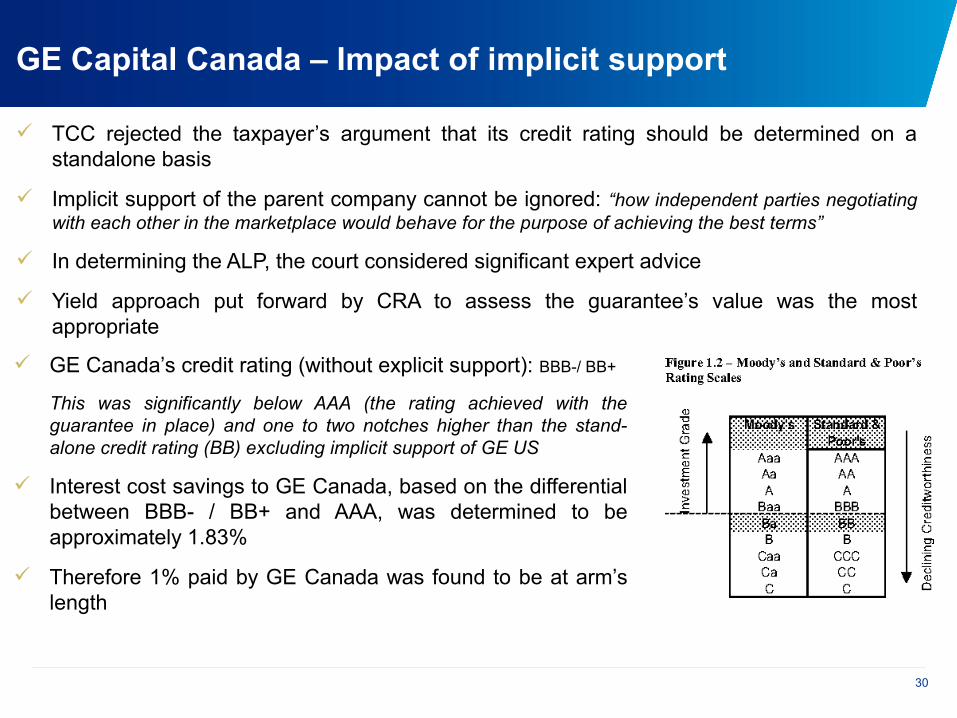

GE Capital Canada – Impact of implicit support

30

GE Canada’s credit rating (without explicit support): BBB-/ BB+

This was significantly below AAA (the rating achieved with the guarantee in place) and one to two notches higher than the stand-alone credit rating (BB) excluding implicit support of GE US

Interest cost savings to GE Canada, based on the differential between BBB- / BB+ and AAA, was determined to be approximately 1.83%

Therefore 1% paid by GE Canada was found to be at arm’s length

TCC rejected the taxpayer’s argument that its credit rating should be determined on a standalone basis

Implicit support of the parent company cannot be ignored: “how independent parties negotiating with each other in the marketplace would behave for the purpose of achieving the best terms”

In determining the ALP, the court considered significant expert advice

Yield approach put forward by CRA to assess the guarantee’s value was the most appropriate

Guarantee whether an International Transaction !!Section 92B

However Finance Bill 2012 inserted Explanation to Section 92B w.r.e.f. 1 April 2002 to specifically include the following:

“For the removal of doubts, it is hereby clarified that—(i) the expression “international transaction” shall include—………(c) capital financing, including any type of long-term or short-term borrowing, lending orguarantee, purchase or sale of marketable securities or any type of advance, payments ordeferred payment or receivable or any other debt arising during the course of business”

31

Four Soft - Hyderabad Tribunal

- Taxpayer provided corporate guarantee on behalf of its AEs

- TPO applied 3.75% as commission rate on corporate guarantee

- Tribunal ruled that the corporate guarantee given by the taxpayer does not fall within the scope of international transaction under Section 92B. TP legislation does not provide any guidelines in respect of guarantee transactions. Accordingly no TP adjustment is required

Intention to cover even implicit guarantee – shareholder activity argument could be questioned

Intra-group upto INR 50 Crores-SBI base rate plus 150 bps

32

Everest Kanto Cylinders Ltd [TS-200-HC-2015(BOM)-TP]

- The assessee’s subsidiary in Dubai had taken loan from ICICI Bank, in respect of which, the assessee provided a corporate guarantee

- The assessee had charged guarantee commission @ 0.5% from its AE- The TPO determined ALP for the guarantee commission at the rate of 3%

Revenue Authorities Contention- Without corporate guarantee, Dubai entity could not have obtained loan from Bank- Revenue Authorities appealed against the deletion made by the ITAT

High Court Decision / Observations- HC held that, “The considerations which applied for issuance of a Corporate guarantee are

distinct and separate from that of bank guarantee and accordingly we are of the view that commission charged cannot be called in question, in the manner TPO has done”.

- HC dismisses Revenue’s appeal.

Account Receivables: whether an International Transaction !Section 92B

33

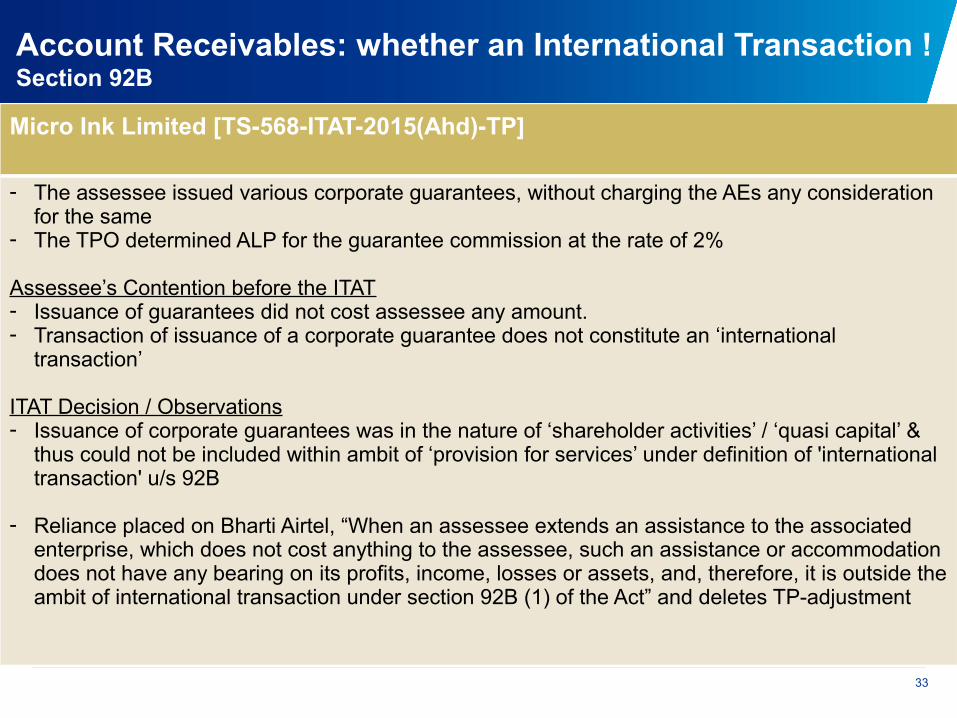

Micro Ink Limited [TS-568-ITAT-2015(Ahd)-TP]

- The assessee issued various corporate guarantees, without charging the AEs any consideration for the same

- The TPO determined ALP for the guarantee commission at the rate of 2%

Assessee’s Contention before the ITAT- Issuance of guarantees did not cost assessee any amount.- Transaction of issuance of a corporate guarantee does not constitute an ‘international

transaction’

ITAT Decision / Observations- Issuance of corporate guarantees was in the nature of ‘shareholder activities’ / ‘quasi capital’ &

thus could not be included within ambit of ‘provision for services’ under definition of 'international transaction' u/s 92B

- Reliance placed on Bharti Airtel, “When an assessee extends an assistance to the associated enterprise, which does not cost anything to the assessee, such an assistance or accommodation does not have any bearing on its profits, income, losses or assets, and, therefore, it is outside the ambit of international transaction under section 92B (1) of the Act” and deletes TP-adjustment

Account Receivables: whether an International Transaction !Section 92B

Whether guarantee fee quote availed in website valid !!

34

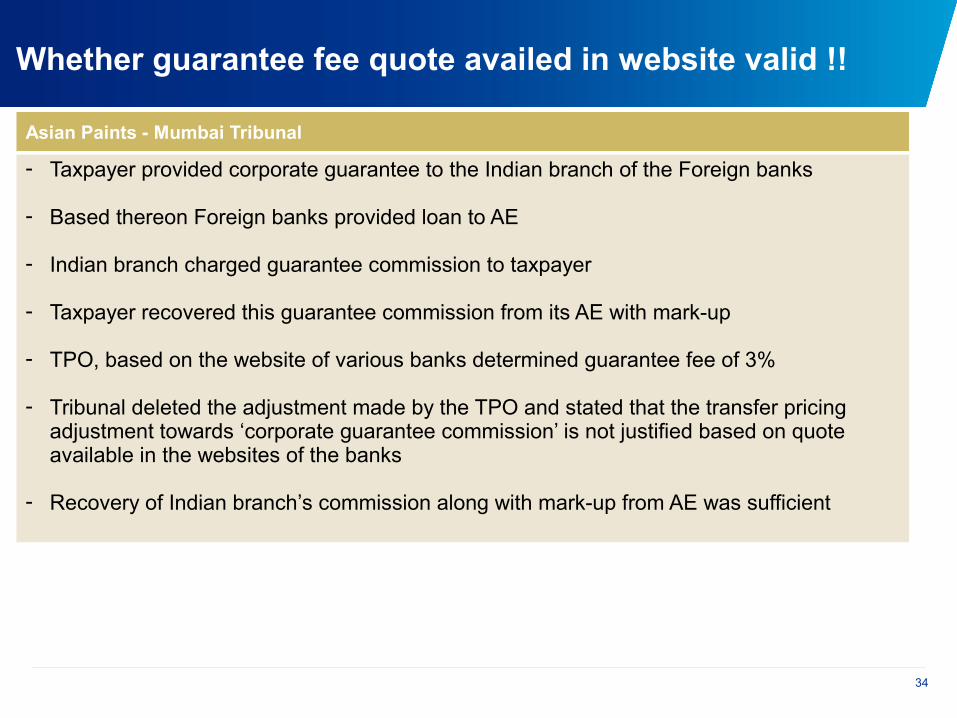

Asian Paints - Mumbai Tribunal

- Taxpayer provided corporate guarantee to the Indian branch of the Foreign banks

- Based thereon Foreign banks provided loan to AE

- Indian branch charged guarantee commission to taxpayer

- Taxpayer recovered this guarantee commission from its AE with mark-up

- TPO, based on the website of various banks determined guarantee fee of 3%

- Tribunal deleted the adjustment made by the TPO and stated that the transfer pricing adjustment towards ‘corporate guarantee commission’ is not justified based on quote available in the websites of the banks

- Recovery of Indian branch’s commission along with mark-up from AE was sufficient

35

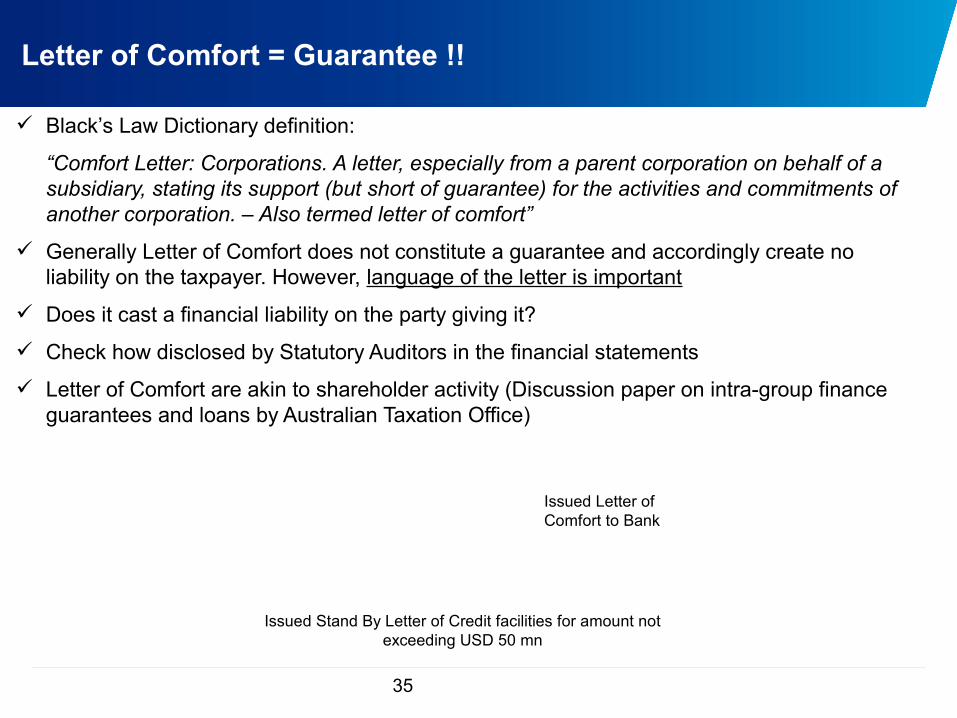

Letter of Comfort = Guarantee !!

Black’s Law Dictionary definition:

“Comfort Letter: Corporations. A letter, especially from a parent corporation on behalf of a subsidiary, stating its support (but short of guarantee) for the activities and commitments of another corporation. – Also termed letter of comfort”

Generally Letter of Comfort does not constitute a guarantee and accordingly create no liability on the taxpayer. However, language of the letter is important

Does it cast a financial liability on the party giving it?

Check how disclosed by Statutory Auditors in the financial statements

Letter of Comfort are akin to shareholder activity (Discussion paper on intra-group finance guarantees and loans by Australian Taxation Office)

Issued Letter of Comfort to Bank

Issued Stand By Letter of Credit facilities for amount not exceeding USD 50 mn

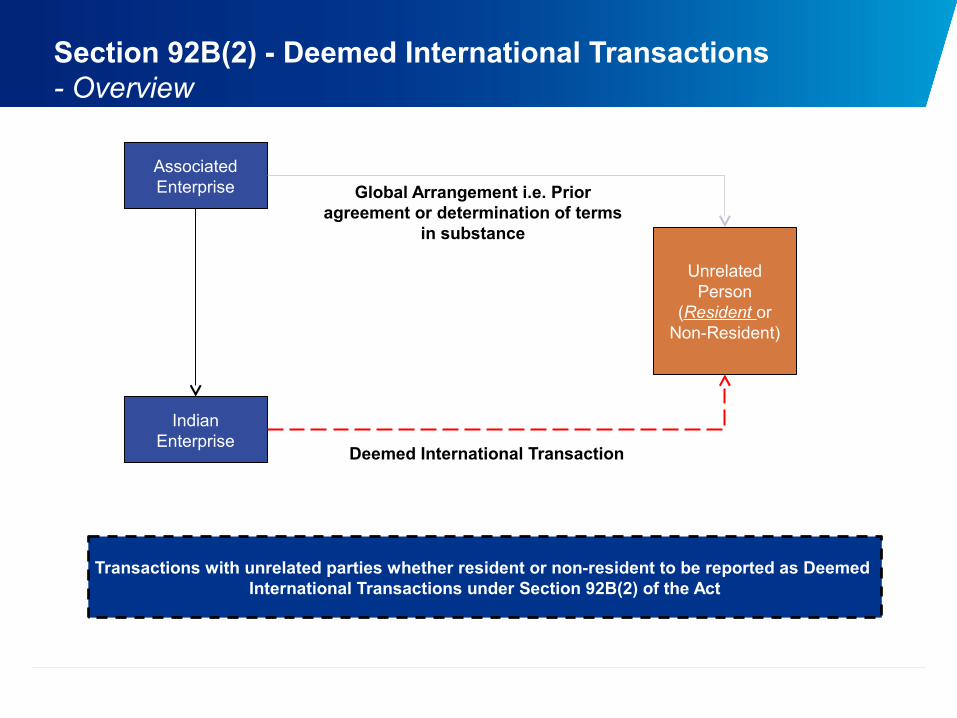

Section 92B(2) - Deemed International Transactions- Overview

Associated Enterprise

Indian Enterprise

Unrelated Person

(Resident or Non-Resident)

Global Arrangement i.e. Prior agreement or determination of terms

in substance

Deemed International Transaction

Transactions with unrelated parties whether resident or non-resident to be reported as Deemed International Transactions under Section 92B(2) of the Act

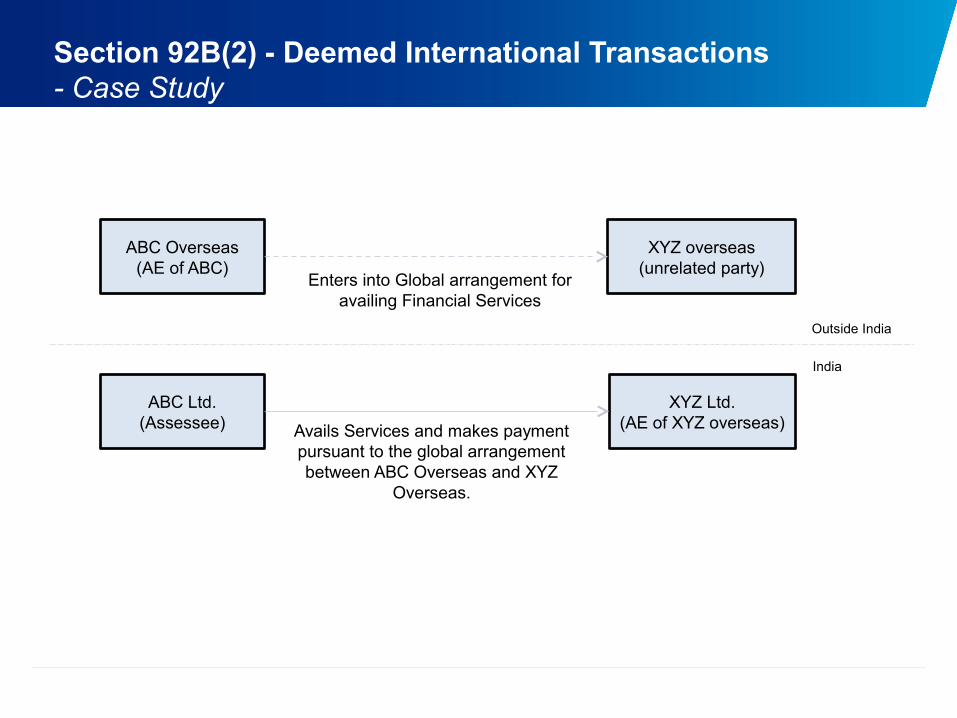

Section 92B(2) - Deemed International Transactions- Case Study

ABC Ltd.(Assessee)

XYZ overseas(unrelated party)

ABC Overseas(AE of ABC)

XYZ Ltd.(AE of XYZ overseas)

Enters into Global arrangement for availing Financial Services

Avails Services and makes payment pursuant to the global arrangement between ABC Overseas and XYZ

Overseas.

India

Outside India

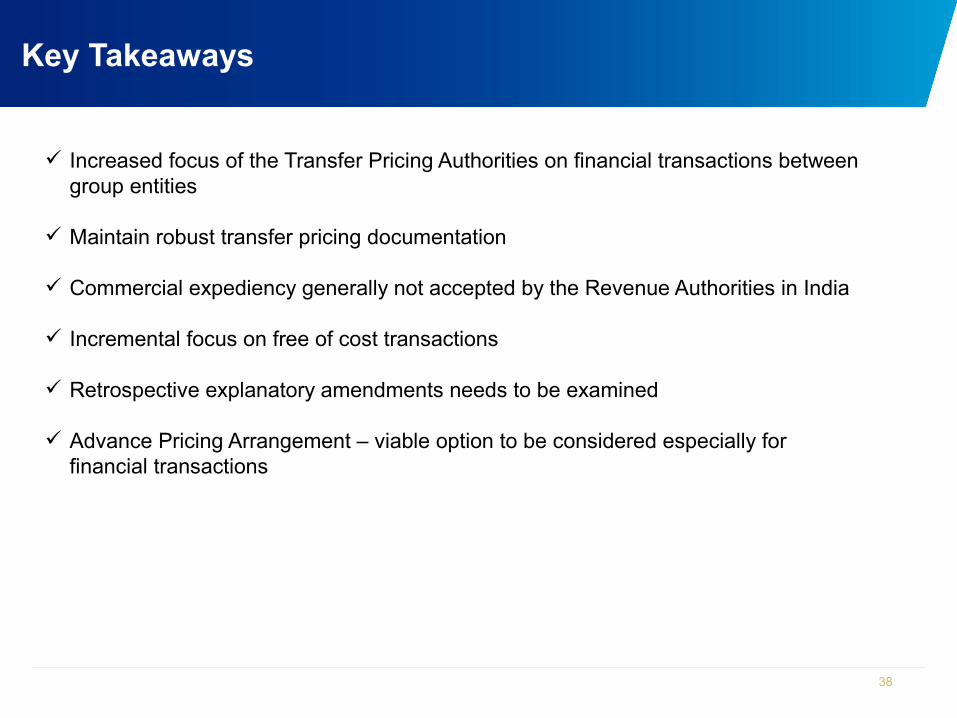

Key Takeaways

38

Increased focus of the Transfer Pricing Authorities on financial transactions between group entities

Maintain robust transfer pricing documentation

Commercial expediency generally not accepted by the Revenue Authorities in India

Incremental focus on free of cost transactions

Retrospective explanatory amendments needs to be examined

Advance Pricing Arrangement – viable option to be considered especially for financial transactions

Questions & Answers

Questions

&

Answers

39