transportpackaging transport packaging · pdf filenot stretch or shrink wrapñis a...

TRANSCRIPT

Prepared by Headley Prax Consulting in association with J. Leslie Bell for

`e Minnesota O2ce of Environmental Assistanceand the American Plastics Council

August 1998

T r a n s p o r t P a c k a g i n g

TransportPackagingCost-Efective Strategies for Reducing, Reusing,

and Recycling in the Grocery Industry

Acknowledgements

The Minnesota Office of Environmental Assistance, theAmerican Plastics Council, and Headley Pratt Consultingwould like to thank the following people for theirassistance on this project. Without their time and effort,the project would not have been possible.

Alan AndersonDale AndersonLyle BigwoodPaul BuhrmannTom Clasen

This report is printed on recycled paper made from 100 percent post-consumer waste.

Design: Jeff Fillion Design [email protected]

Transport PackagingCost-Efective Strategies for Reducing, Reusing,

and Recycling in the Grocery Industry

For more information on this project, contact:

Ken BrownMinnesota Office of Environmental Assistance520 Lafayette Road North, 2nd FloorSt. Paul, MN 51555651-215-0241

Barbara HalpinAmerican Plastics Council1801 K Street, N.W.–Suite 701LWashington, D.C. 20006202-974-5400

Linda HeadleyHeadley Pratt Consulting2709 Norwich Rd.Lansing, MI 48911517-394-7350

Notice and Disclaimer of WarrantiesAPC makes no warranty, express or implied, respecting the accuracy or completeness of the information provided herein including, but not limitedto, implied warranties of merchantability or fitness for a particular use or purpose. APC shall not be responsible for any direct, indirect, incidental orconsequential damages, damages from loss or use or profits, or cost of procurement substitute goods or services in contract, tort or otherwise,arising out of or in connection with the information contained herein. Use of this information is voluntary and reliance on it should only beundertaken after an independent review of its accuracy and completeness.

W. R. (Bob) KingJudy LambDan MohsJohn VectorBob Walfoort

The project partners would like to extend a special thankyou to Bruce Trippet, Operations Manager withSUPERVALU, who spent a great deal of time gatheringdata and working with the project team to quantify theeconomic advantages and disadvantages of plastic pallets.His willingness to answer questions, review data, anddiscuss methodologies was extremely helpful and madethis a more valuable report.

Executive Summary——v

The Project 1

Lessons on Old Corrugated Containers——5

Lessons on Plastic Film——11

Lessons on Pallets——19

Store 1: A Pro0le——26

Store 2: A Pro0le——37

Store 3: A Pro0le——45

Appendix A: Markets for OCC, Wood Pallets, and Plastic Pallets——56

Appendix B: Markets for Plastic Film——58

Appendix C: Publication Resource List——61

Appendix D: SUPERVALU Pallet Payback Analysis——64

Con

tent

s

Exec

utiv

e Su

mm

ary

Transport packaging—which the Minnesota Office of Environmen-tal Assistance (OEA) defines as old corrugated containers (OCC),plastic film, and wooden pallets—comprises about one-fifth ofMinnesota’s total municipal solid waste stream. Therefore, whenthe state set a goal to reduce its packaging discards by 25 percent, ittargeted transport packaging as the most logical place to look foropportunities to reduce, reuse, and recycle.

In addition, the state identified the grocery industry as one of thelargest generators (and, hence, disposers) of transport packaging.Thus, working with stores, distributors, wholesalers, farmers,growers, processors, and product manufacturers to better managetheir transport packaging waste was established as a high priority.

The state realized early on that a cooperative effort was key toachieving its waste reduction goals. Therefore, in a first step, ameeting was held with the OEA, the Minnesota Grocers Associa-tion, and senior managers from several grocery corporations todiscuss possible options. At that meeting, the grocery industryindicated that before it could make changes it needed more infor-mation about cost-effective strategies (or “best practices”) formanaging transport packaging waste. The group also decided that ahands-on examination of waste management practices at stores andwith wholesaler/distributors would be beneficial.

In a second step, the American Plastics Council (APC) joinedforces with the OEA to help gather the information that the groceryindustry needed. The APC was a logical partner because of itsprevious experience working with the grocery industry to implementstretch wrap recycling programs, and because of the growing use ofplastics in transport packaging applications.

Together, the OEA and APC launched a project to

determine how much transport packaging waste was generated bygrocery stores;

Executive Summary

Tranport packagng—

which the Minnesota

O2ce of Environmental

Assistance de0nes as old

corrugated containers,

plastic 0lm, and wooden

pallets—comprises about

one-0th of Minnesota’s

total municual solid

waste stream.

TRANSPORT PACKAGING

v

learn how that waste was being managed;

develop “real world” data showing thepotential economic advantages (anddisadvantages) of making certain wastemanagement decisions;

identify viable reduction, reuse, andrecycling options that grocers couldrealistically implement (given that wastemanagement is not part of their corebusiness); and

compile the information into a reportthat grocers in Minnesota and across thecountry could use to make informeddecisions about the economic and envi-ronmental benefits of reducing, reusing,and recycling transport packaging.

Three grocery stores—and, to a lesser extent,three wholesaler/distributors—also joinedthe effort. These facilities agreed to opentheir doors to the project team and provideit with a wealth of information on wastemanagement costs and practices. By workingcooperatively, the project team learned anumber of valuable lessons about the poten-tial for reducing, reusing, and recyclingOCC, plastic film, and wooden pallets inthe grocery industry.

Following are some of the key lessonslearned.

OLD CORRUGATED CONTAINERSThere is a strong economic incentive forstores to recycle OCC. Using data fromthe three participating stores, it is esti-mated that a typical grocery store willgenerate about 396 tons of OCC per

year and pay an average of $89.88 perton to dispose of it. If, however, it wereto recycle that OCC, it could realizemore than $35,000 in avoided disposalcosts. (See the sidebar entitled “Defin-ing a Typical Store.”)

There is an even greater economicincentive for recycling OCC if oneincludes the revenue generated fromrecovering it. Using a point-in-timeaverage of prices received by the threestores participating in this project, thetypical store could expect to generatemore than $24,000 per year in revenuefrom recycling OCC.

The typical store could realize an averageof $4,800 per year in avoided disposalcosts and $3,500 in additional recyclingrevenue by recovering recyclable OCCthat currently is thrown away due toconfusion with wax-coated OCC. Inaddition, the typical store could accruemore than $700 per year in avoideddisposal costs by eliminating wax-coatedOCC altogether, bringing the totaleconomic benefit to about $9,000.

All three stores participating in theproject have mature OCC recyclingprograms. (They estimate their OCCrecovery rate at about 95 percent.)Therefore, aside from changes with wax-coated OCC, the programs probablycannot grow significantly in terms ofgreater recovery. If OCC recyclingprograms in other stores are equallymature, then source reduction and reuseoptions should be emphasized withgrocers to achieve greater diversion.

EXECUTIVE SUMMARY

vi

While several options are available forreducing the amount of OCC gener-ated, the most significant effort in thegrocery industry relates to the growinguse of tray/shrink packaging. (A tray/shrink package is composed of a corru-gated tray and shrink wrap, which is usedto secure goods to the tray.) Whencomparing full corrugated cases (whichcompletely enclose products in corru-gated) with tray/shrink packages, theproject team found that the latter pack-aging strategy cuts the weight of a trans-port package in half. Industry sourcesmaintain that this reduction in weighttranslates into better shipping efficien-cies, improved processing capabilities,and lower material costs.

PLASTIC FILMThere is not a strong economic incentivefor grocery stores to recycle plastic film.Using data from the three participatingstores, it is estimated that the typicalgrocery store will generate more than10,000 pounds of stretch and shrinkwrap per year, and realize only $500 peryear in avoided disposal costs by recy-cling it. (Stretch wrap typically is used tosecure goods to pallets, and shrink wrapis used to secure smaller quantities oflike goods either together or to a corru-gated tray.)

There is, however, a greater economicincentive for wholesaler/distributors to re-cycle their own film as well as that gener-ated by the stores they serve. Using datafrom one of the participating whole-saler/distributors, the project teamcalculated that it could expect net rev-

enue of more than $45,000 per year byrecycling its own and it stores’ stretchand shrink wrap (given estimated vol-umes and its current market price). Evenat a per-pound price that is 2-centslower, the wholesaler/distributor wouldstill realize net revenue of more than$7,500 per year. (At a price below$.025 per pound, however, the eco-nomics of film recycling for this whole-saler/distributor becomes questionable.)

A typical grocery store today generatesmore shrink wrap than it does stretchwrap. Unfortunately, many recycling

Defining A Typical Store

Clearly, there is no such thing as a “typical” grocerystore. They come in all shapes, sizes, and locations.But for this report, the data assigned to a typicalstore are simply an average of the data provided bythe three stores participating in the project.

What should you know about these stores? All threewere located in suburban areas, they had an aver-age of 62,000 square feet, and their annual sales av-eraged $33 million. This information is importantbecause other stores that want to use the data willneed to adjust it accordingly. For example, a largerstore with higher annual sales will probably gener-ate more transport packaging waste than the “typi-cal” store, whereas a smaller store with lower an-nual sales will generate less.

Keep in mind that the purpose of collecting this datawas not only to inform grocers about how muchtransport packaging waste they generate, but, moreimportant, to demonstrate the “real world” eco-nomic advantages and disadvantages of differentreuse, reduction, and recycling options.

TRANSPORT PACKAGING

vii

programs in the grocery sector focusonly on stretch wrap, which means thatthe most significant portion of a store’sfilm waste is not being recovered. Thisdoes not appear to be a market-drivendecision, since 18 of the 22 film recy-cling companies interviewed for thisproject accept both stretch and shrinkwrap. Given that many stores currentlydo not recycle any of their film, and thatmany others recycle only stretch wrap, itappears that there is significant room forgrowth in recycling plastic film in thegrocery sector, particularly throughwholesaler/retailer partnerships.

Contamination—that is, anything that isnot stretch or shrink wrap—is a concernin film recycling programs. Two of thethree stores participating in this projecthad contamination levels above what isnormally accepted by markets. Thiscould be remedied, however, with fairlysimple education programs designed toinform employees about what is and isnot acceptable.

While film itself has many source reduc-tion benefits, there are products on themarket that may enable the groceryindustry to use less film. For example,one product that was discovered duringthe research phase of the project isScotch™ Brand Stretchable Tape, whichits manufacturer claims can reduce theamount of material needed to stabilizepallet loads by 77 percent. Using datafrom one participating wholesaler/distributor, it was found that the facilitywould generate 7.7 fewer tons of filmwaste per year by switching from stretch

wrap to Scotch™ Brand StretchableTape. (The manufacturer also maintainsthat Stretchable Tape is compatible withstretch wrap in recycling and, therefore,will not contaminate remaining filmstreams.)

PALLETSIndividual grocery stores do not com-monly purchase or dispose of pallets;therefore, there is little incentive forthem to explore opportunities for re-duction, reuse, or recycling. Stores do,however, benefit economically from thecurrent pallet management system.Because all pallets—whether they arewood or plastic, intact or damaged—arereturned to grocery suppliers (or givenaway to employees or consumers), storesdo not have to pay for their disposal.Because of that return and reuse system,the typical grocery store can expect torealize about $31,000 in annual avoideddisposal costs.

The most significant reuse effort under-way in the grocery industry involvesreplacing wood pallets with plastic palletsin order to extend a pallet’s useful life(thereby reducing costs and minimizingpallet waste). Any economic benefits ofsuch a switch will be minimal at thegrocery store level, but it appears thatthey may be substantial at the wholesaler/distributor level. Data provided by oneof the wholesaler/distributors participat-ing in this project showed that the facil-ity realized a savings of 63 cents per tripby using plastic pallets instead of wood.In addition, it had the potential toreduce its workers’ compensation, labor,

EXECUTIVE SUMMARY

viii

and shipping costs by about $556,000per year (or $3.70 per plastic pallet).Furthermore, the wholesaler/distributorachieved payback for its initial up-frontinvestment shortly after the second yearof use.

Although they do not realize directeconomic benefits, the grocery storesparticipating in this project said theyprefer working with plastic pallets be-cause they are lightweight, nestable, takeup less space, have four-way entry, andappear to work with all types of products,including frozen and perishable goods.The most significant drawback, accord-ing to the stores, is that plastic palletscannot be stored on existing store andwarehouse racks. (The racks are designedto hold pallets with flat boards extendingthe full length and width of the palletplatform. Plastic pallets, however, havenine small, protruding legs which arenot compatible with current rackingsystems.) In addition, the stores indi-cated that plastic pallets are more likelyto slide—particularly on truck beds infreezing weather—than their woodencounterparts which have rougher surfaces.

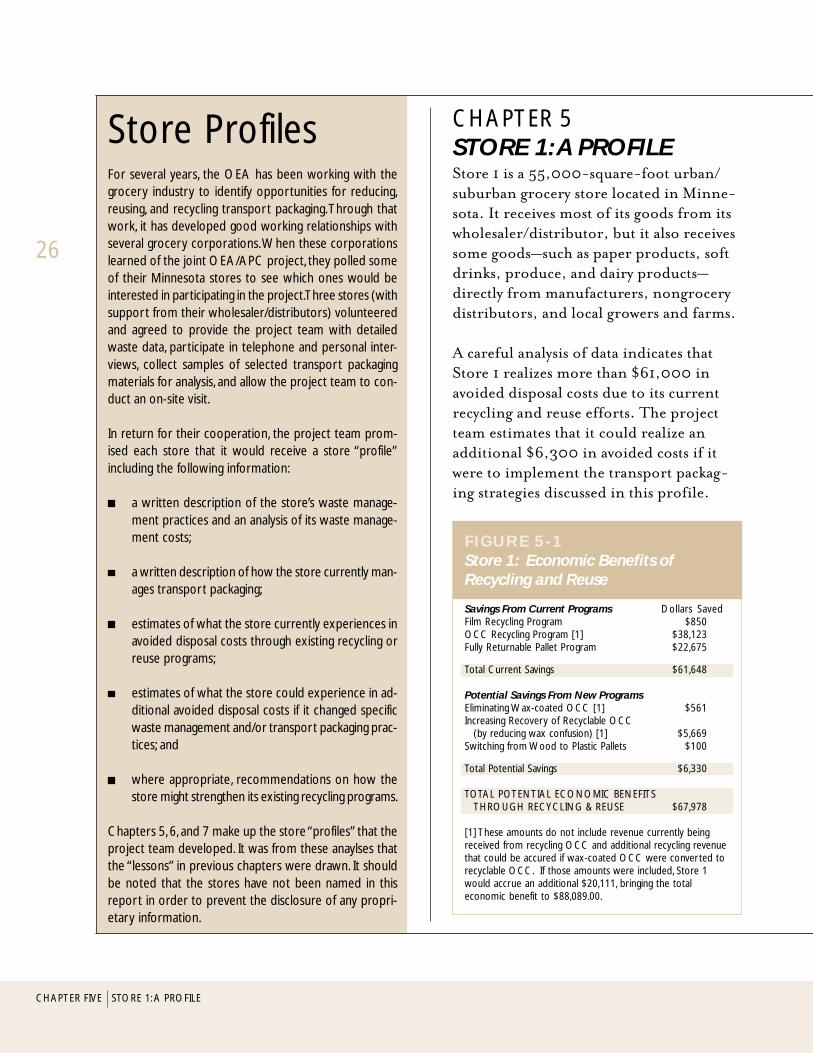

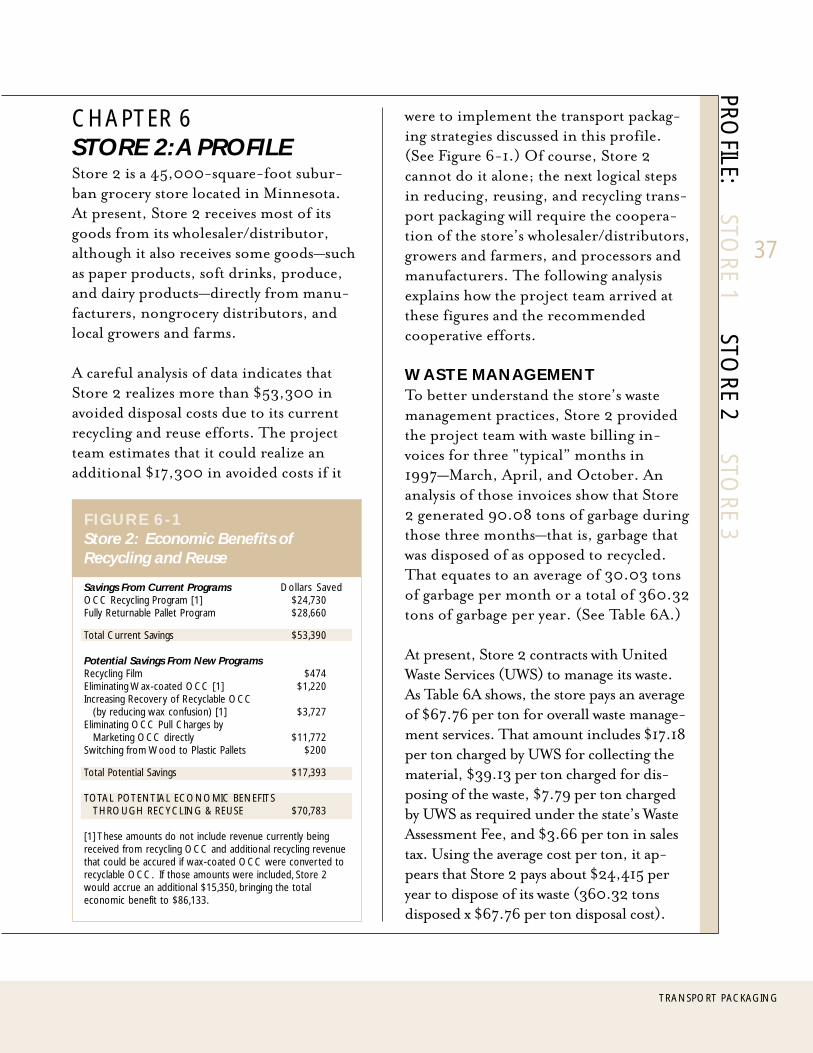

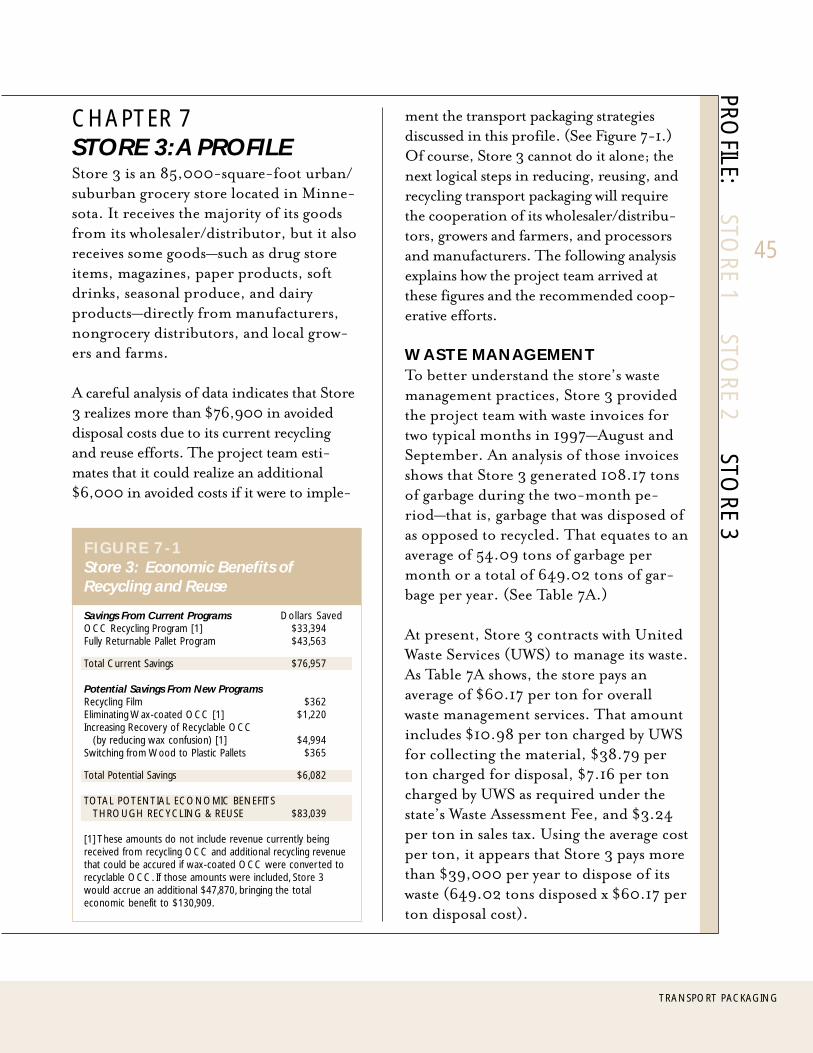

GROCERY STORESA careful analysis of data shows thatparticipating stores realize significantsavings in the form of avoided disposalcosts because of their current transportpackaging recycling and reuse efforts.Store 1 realizes about $61,000 per yearin avoided disposal costs, Store 2 realizes$53,300, and Store 3 realizes $76,900.

The stores could realize even greatersavings by implementing the additionaltransport packaging strategies discussedin the full report. The project teamestimates that Store 1 could save anadditional $6,300 in avoided disposalcosts, Store 2 could save $17,300, andStore 3 could save $6,000.

From an environmental perspective, thethree stores together are diverting morethan 2,500 tons of transport packagingwaste per year from the state’s landfillsthrough their current recycling andreuse efforts. Store 1 is diverting ap-proximately 435 tons, Store 2 is divert-ing 788 tons, and Store 3 is diverting1,279 tons.

If the three stores were to implement theadditional transport packaging strategiesdiscussed in this report, they coulddivert an additional 216 tons of trans-port packaging waste per year from thestate’s landfills. Store 1 could divertalmost 44 tons, Store 2 could divert 80tons, and Store 3 could divert 92 tons.

The following study (1) discusses how these“lessons” were learned, (2) explains how thefigures were derived, and (3) provides morein-depth information about how storesmight implement the reduction, reuse, andrecycling opportunities that are currentlyavailable for use by the grocery industry.

TRANSPORT PACKAGING

ix

Cha

pter

One

TRANSPORT PACKAGING

The Project

INTRODUCTIONIn 1992, the Minnesota Legislature set a goal for the state to reduceits packaging discards by 25 percent within three years and autho-rized that any combination of reduction, reuse, and recycling couldbe used to meet that goal. After the law was passed, the MinnesotaOffice of Environmental Assistance (OEA) embarked on severalsubsequent projects to determine (1) which components of thepackaging waste stream offered the greatest opportunities for reduc-tion, reuse, and recycling, and (2) which sectors generated thosecomponents in large quantities.

The follow-up studies all indicated that transport packaging—whichthe OEA defines as old corrugated containers (OCC), plastic film,and wooden pallets—offered more significant opportunities forreduction, reuse, and recycling than any other packaging type. Thestudies also found that the grocery industry was one of the largestgenerators of transport packaging waste and, therefore, a goodcandidate for reduction, reuse, and recycling programs.

As a result of these findings (and a 1996 study which found that thestate had not reached its 25 percent goal), the OEA formed a part-nership with the Minnesota Grocers Association and individualgrocery corporations to examine ways to address issues related totransport packaging waste. Later, the American Plastics Council(APC) joined the effort and worked cooperatively with the OEA tolearn more about how grocers manage their transport packagingwaste and what options are available to reduce, reuse, and/or recycleit. Since the APC has worked with the grocery industry on previousprojects, and since plastics are being used in greater quantities in trans-port packaging, the APC seemed a logical partner.

The OEA and the APC agreed that, to be effective, the projectshould focus primarily on individual grocery stores (since very littleinformation is available from that point in the distribution system),and on the economics of reducing, reusing, and recycling at thestore level (since economics are the primary driving factor behindall business decisions). The following report is what the two organi-zations learned over the course of the study.

1

In 1992, the Minnesota

Legslature set a goal for

the state to reduce its

packagng discards by 25

percent wihin thre years

and authorized that any

combination of

reducion, reuse, and

recycling could be used to

met that goal.

THE PURPOSEThe purpose of conducting the study wasfourfold. First, there is a great deal oftheoretical discussion about what happenswith transport packaging in the groceryindustry. Unfortunately, there is very littleconcrete information about what happensin practice, particularly at the grocery storelevel. By sponsoring this project, the OEAand the APC hoped to obtain “real world”information about how grocery storesmanage their waste.

Second, the project team wanted to putnumbers to different waste managementoptions to show grocers how implementingreduction, reuse, and recycling programscould affect their bottom lines. Because thegrocery industry is highly competitive andoperates on extremely low margins, it isunlikely that stores will implement programsunless they have some positive economiceffect. Thus, the team wanted to use “realworld” data to determine the potentialeconomic impact of making certain wastemanagement decisions.

Third, the project team wanted to identifyrealistic alternative waste managementoptions that stores could use. There are avariety of reduction, reuse, and recyclingoptions available, but it is unclear which ofthose options make the most sense forgrocery stores.

Finally, the OEA and the APC wanted totake the data gathered in this project and putit into an easy-to-read report so that othergrocery stores could benefit from the re-search. By seeing what was being done (and

could be done) at three participating gro-cery facilities, the project partners hopedthat other grocers may be more motivated tomake reduction, reuse, and/or recycling apart of their day-to-day operations.

The project team realizes that this study hassome shortcomings—it did not includeactual waste sorts which would have providedvaluable information; the data, in someinstances, are limited; and the economicanalyses focus primarily on avoided wastedisposal costs because other types of eco-nomic information either were not availableor were unreliable. Furthermore, time andbudget constraints (inherent in all projects)did not allow for a full investigation of everyreduction and reuse option—only those thatpartipating grocers deemed most significantand/or most viable. The study is, however,an excellent place to start looking at severalcost-effective opportunities to reduce,reuse, and/or recycle transport packaging inthe grocery industry.

THE REPORTWhile studying and working with the threestores and, to a lesser extent, the threewholesaler/distributors that agreed to par-ticipate in this effort, the project teamlearned a number of valuable lessons aboutthe potential for reducing, reusing, andrecycling transport packaging at the grocerystore level. These lessons, or “best prac-tices,” have been summarized in Chapters 2,3, and 4 of the report, and should helpothers in the grocery industry decidewhether or not similar efforts could orshould be undertaken in their own facilities.

2

CHAPTER ONE THE PROJECT

3

TRANSPORT PACKAGING

The project team also wanted to includedetailed information on each of the partici-pating stores. Therefore, Chapters 5, 6, and7 include the analyses that were prepared foreach store showing how they currentlymanage transport packaging waste, the costsassociated with those waste managementpractices, and proposed options for furtherreducing, reusing, and/or recycling thematerial. These analyses have been includedfor readers who want more detailed infor-mation on where the numbers in previouschapters came from, and for those who maywant to compare themselves to a particularstore.

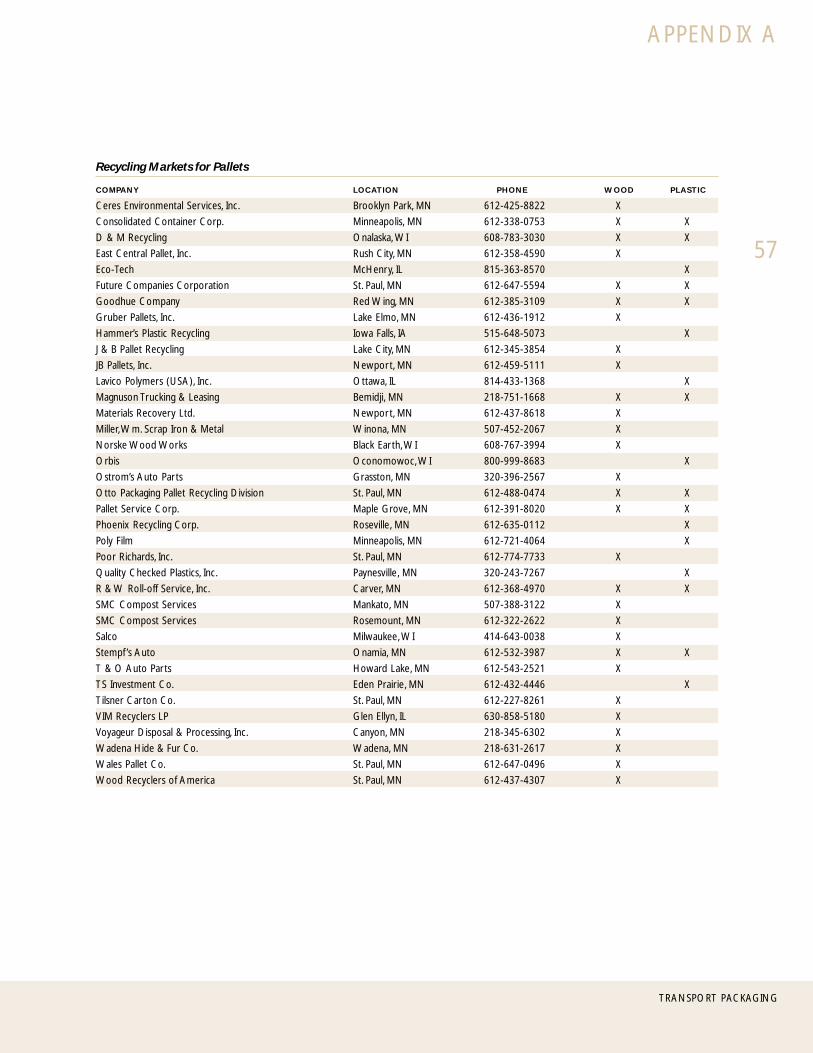

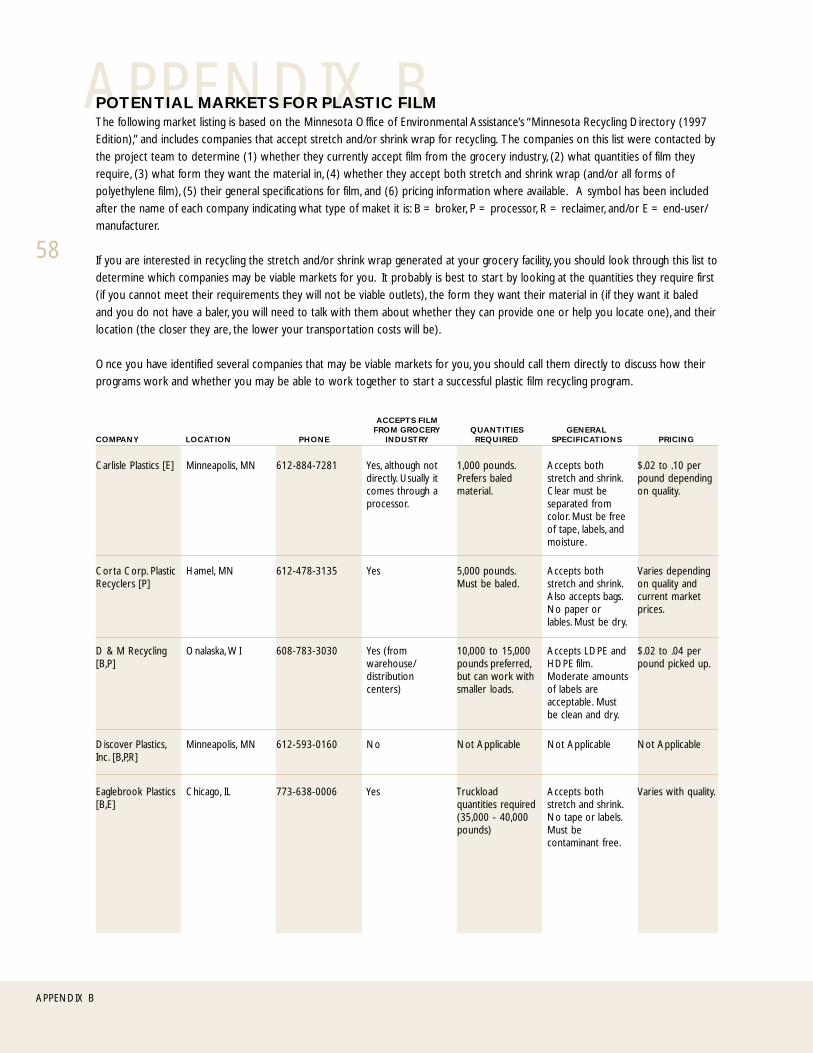

Finally, included in this report are threeother educational pieces. The first piece is alist of companies that currently acceptOCC, wood pallets, and plastic pallets forrecycling. The project team found that alack of knowledge about available markets isone of the barriers preventing grocers frommaximizing their recycling efforts. This listshould provide the assistance that grocersneed to make better program choices. (SeeAppendix A.)

The second piece is similar, but it focuseson markets that accept plastic film forrecycling. This list is more detailed than the

first: In addition to basic contact informa-tion, it includes details on the quantity offilm the markets require, the form they wantthe material in, their quality specifications,current pricing information, and an indica-tion of whether they currently accept filmfrom the grocery sector. This more compre-hensive list was prepared because the projectteam learned that grocers (as well as whole-saler/distributors) were not aware of thequestions they should ask when trying tomarket plastic film. (See Appendix B.)

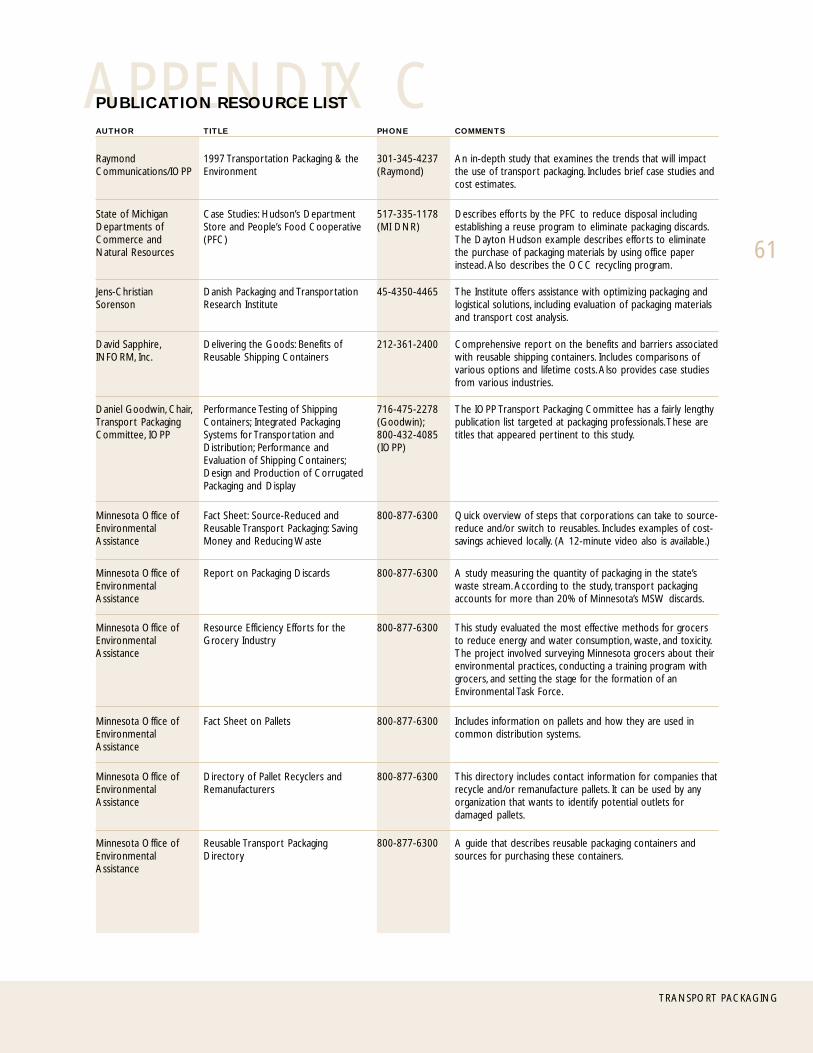

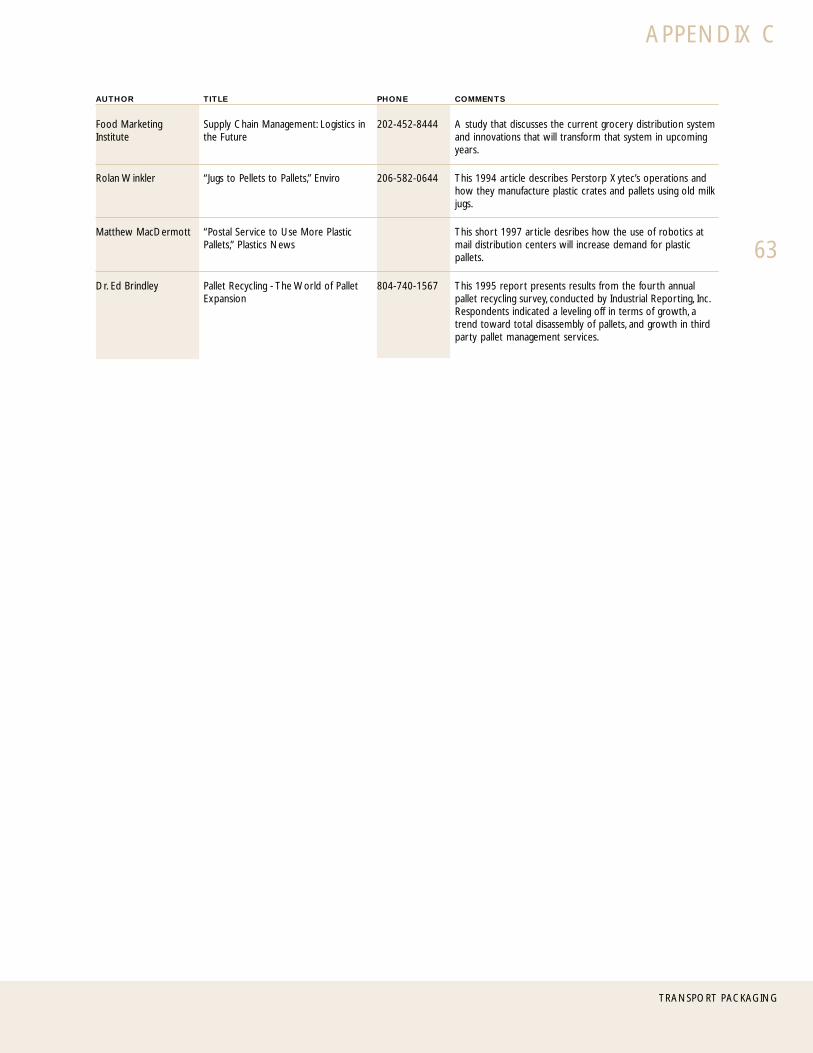

The final educational piece is a list of publi-cations that the project team read whilepreparing this report. These reports can beused by grocers that want to further exploretheir own reduction, reuse, and recyclingoptions. A brief synopsis of what waslearned from the reports has been includedto help grocers determine which ones will beof most use. (See Appendix C.)

As mentioned earlier, the project partnershope that grocers—in Minnesota and acrossthe country— will use this report to makemore informed decisions about the eco-nomic and environmental benefits of re-ducing, reusing, and recycling transportpackaging waste.

While studying and working with the thre stores and, to a lesser

extent, the thre wholesaler/distributors that agreed to

particuate in this efort, the projec team learned a number of

valuable lessons about the potential for reducing, reusing, and

recycling tranport packagng at the grocery store level.

4

Cha

pter

Tw

o

5

TRANSPORT PACKAGING

Lessons on Old Corrugated Containers

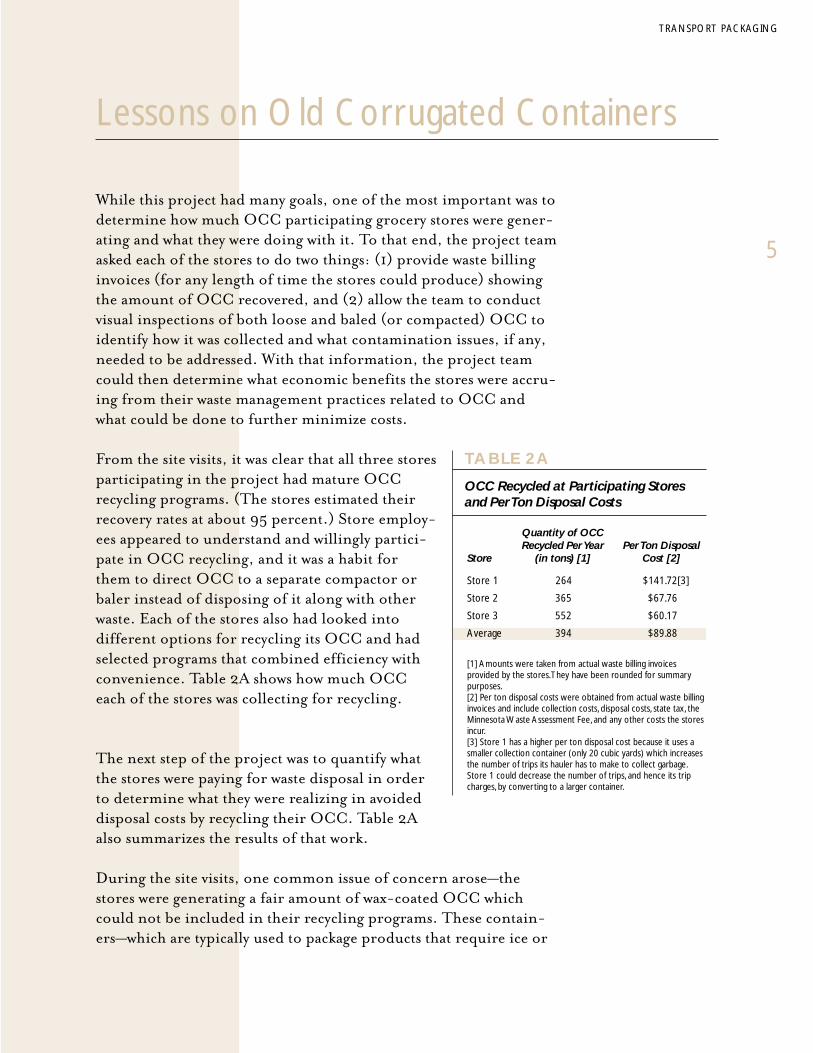

While this project had many goals, one of the most important was todetermine how much OCC participating grocery stores were gener-ating and what they were doing with it. To that end, the project teamasked each of the stores to do two things: (1) provide waste billinginvoices (for any length of time the stores could produce) showingthe amount of OCC recovered, and (2) allow the team to conductvisual inspections of both loose and baled (or compacted) OCC toidentify how it was collected and what contamination issues, if any,needed to be addressed. With that information, the project teamcould then determine what economic benefits the stores were accru-ing from their waste management practices related to OCC andwhat could be done to further minimize costs.

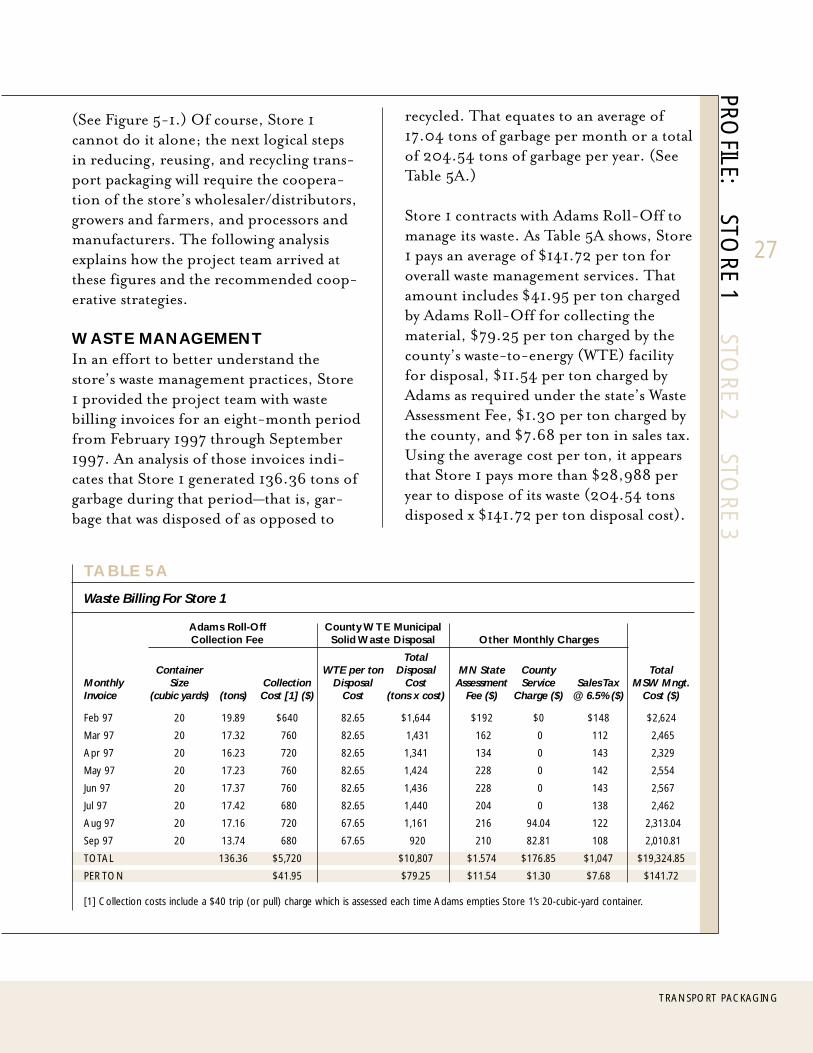

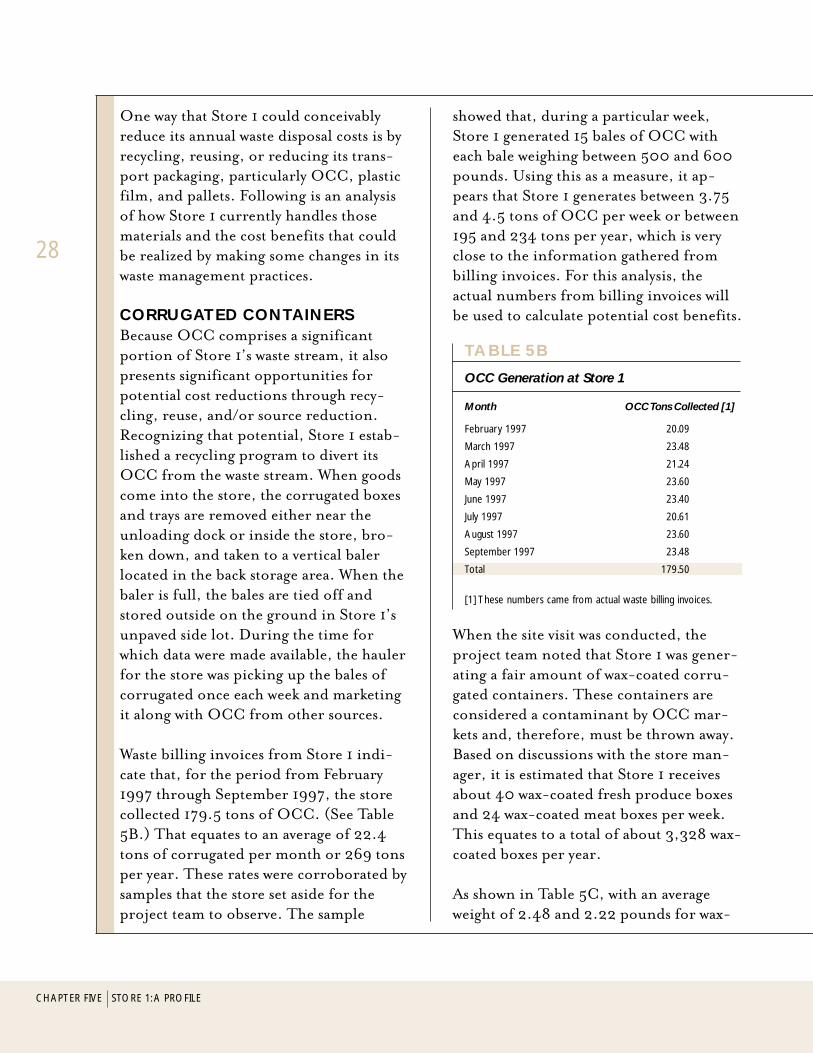

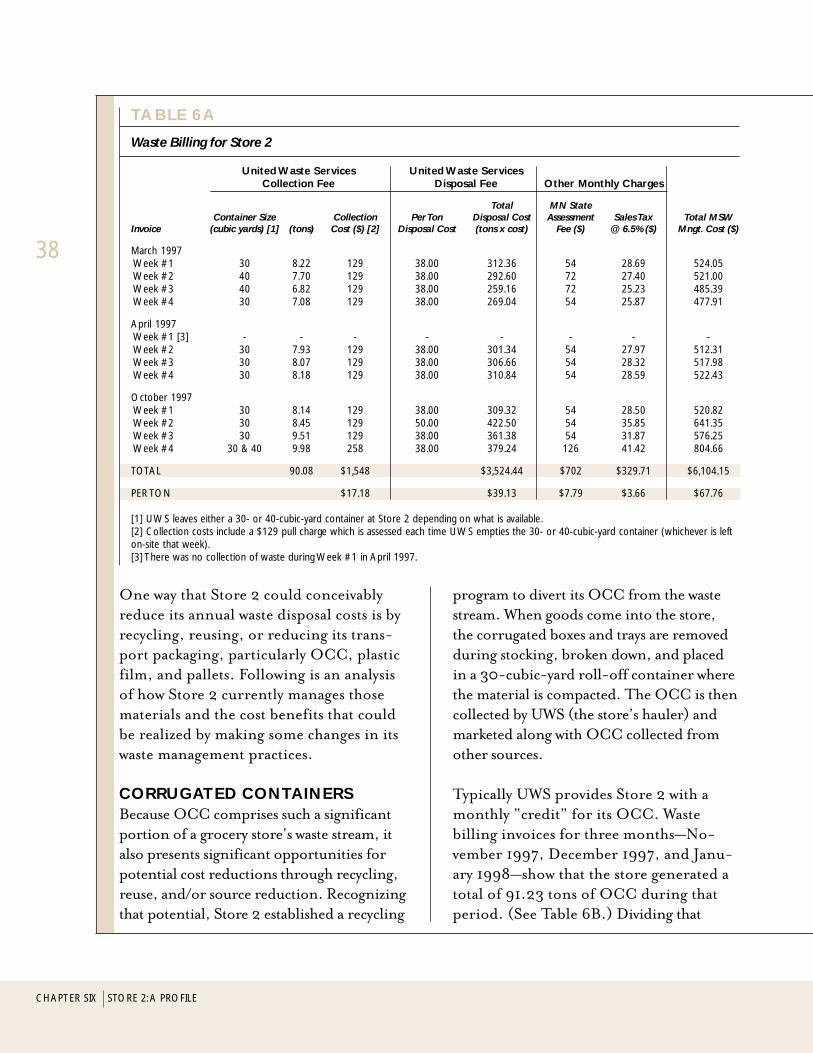

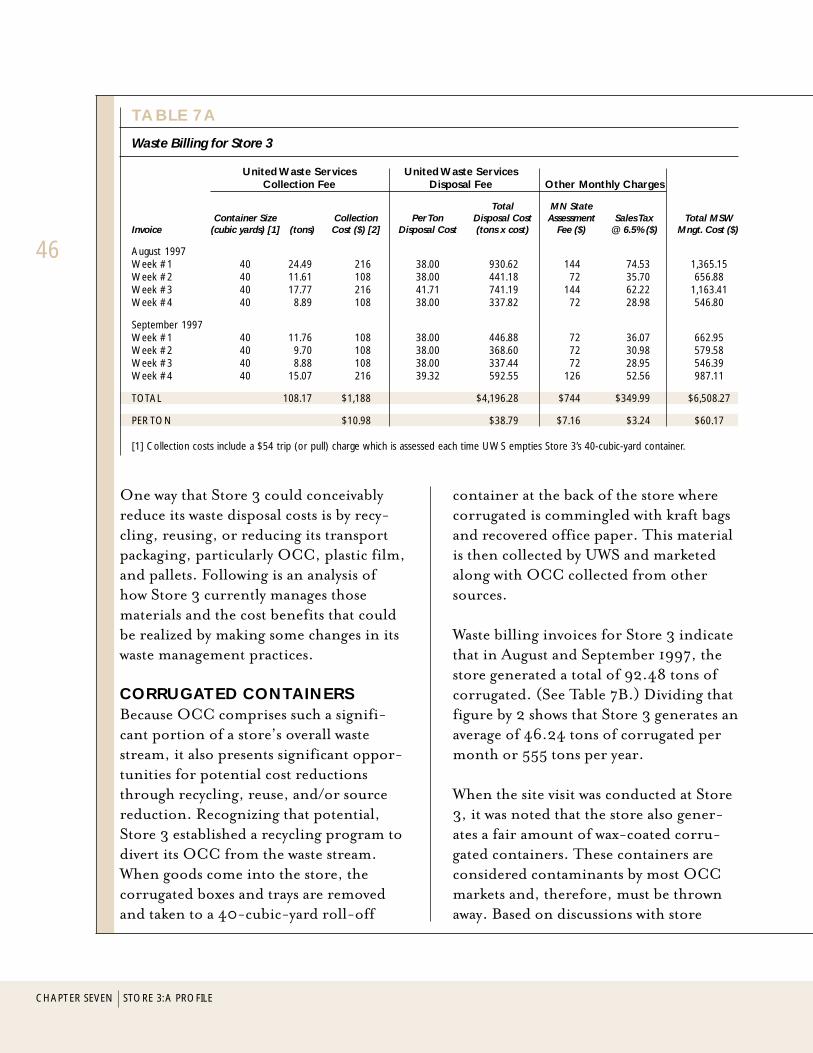

From the site visits, it was clear that all three storesparticipating in the project had mature OCCrecycling programs. (The stores estimated theirrecovery rates at about 95 percent.) Store employ-ees appeared to understand and willingly partici-pate in OCC recycling, and it was a habit forthem to direct OCC to a separate compactor orbaler instead of disposing of it along with otherwaste. Each of the stores also had looked intodifferent options for recycling its OCC and hadselected programs that combined efficiency withconvenience. Table 2A shows how much OCCeach of the stores was collecting for recycling.

The next step of the project was to quantify whatthe stores were paying for waste disposal in orderto determine what they were realizing in avoideddisposal costs by recycling their OCC. Table 2Aalso summarizes the results of that work.

During the site visits, one common issue of concern arose—thestores were generating a fair amount of wax-coated OCC whichcould not be included in their recycling programs. These contain-ers—which are typically used to package products that require ice or

TABLE 2A

OCC Recycled at Participating Storesand Per Ton Disposal Costs

Quantity of OCCRecycled Per Year Per Ton Disposal

Store (in tons) [1] Cost [2]

Store 1 264 $141.72[3]

Store 2 365 $67.76

Store 3 552 $60.17

Average 394 $89.88

[1] Amounts were taken from actual waste billing invoicesprovided by the stores. They have been rounded for summarypurposes.[2] Per ton disposal costs were obtained from actual waste billinginvoices and include collection costs, disposal costs, state tax, theMinnesota Waste Assessment Fee, and any other costs the storesincur.[3] Store 1 has a higher per ton disposal cost because it uses asmaller collection container (only 20 cubic yards) which increasesthe number of trips its hauler has to make to collect garbage.Store 1 could decrease the number of trips, and hence its tripcharges, by converting to a larger container.

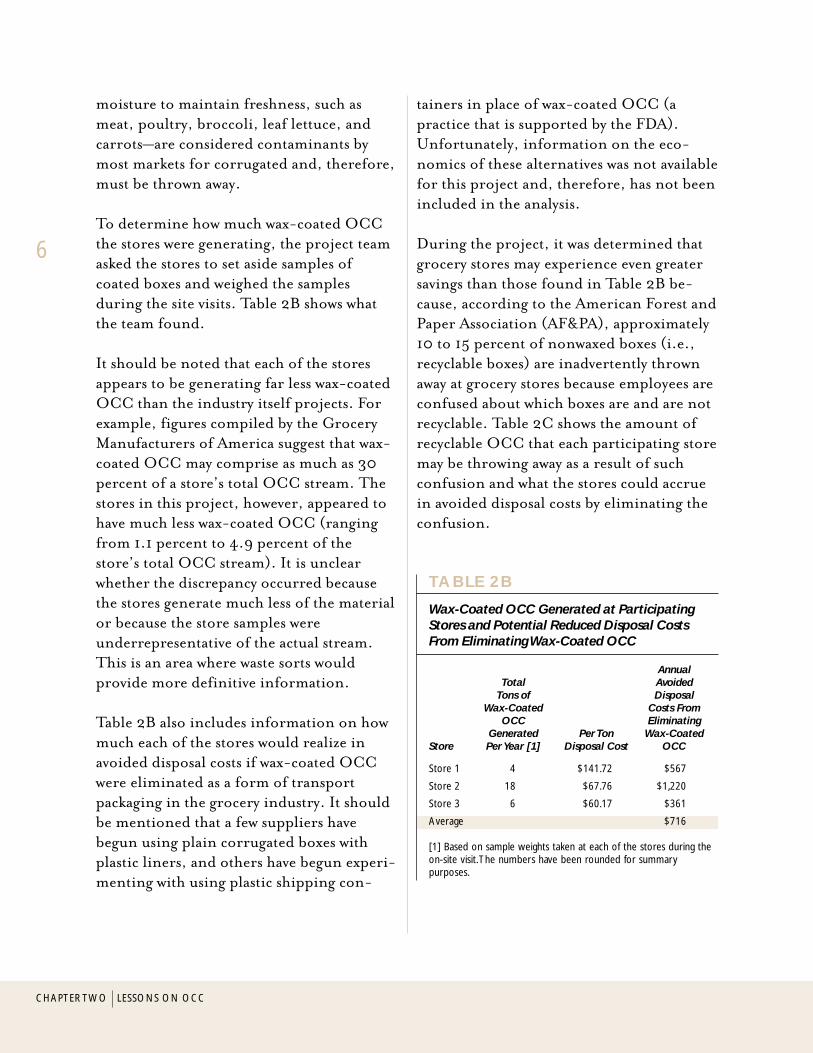

moisture to maintain freshness, such asmeat, poultry, broccoli, leaf lettuce, andcarrots—are considered contaminants bymost markets for corrugated and, therefore,must be thrown away.

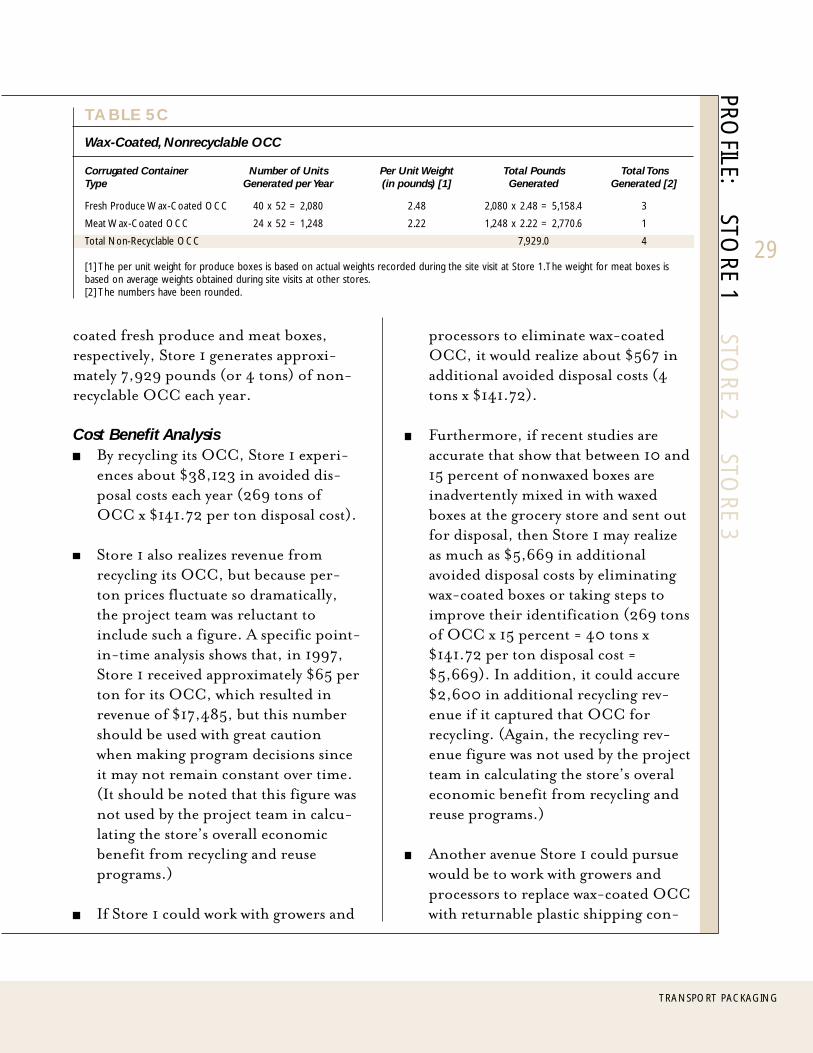

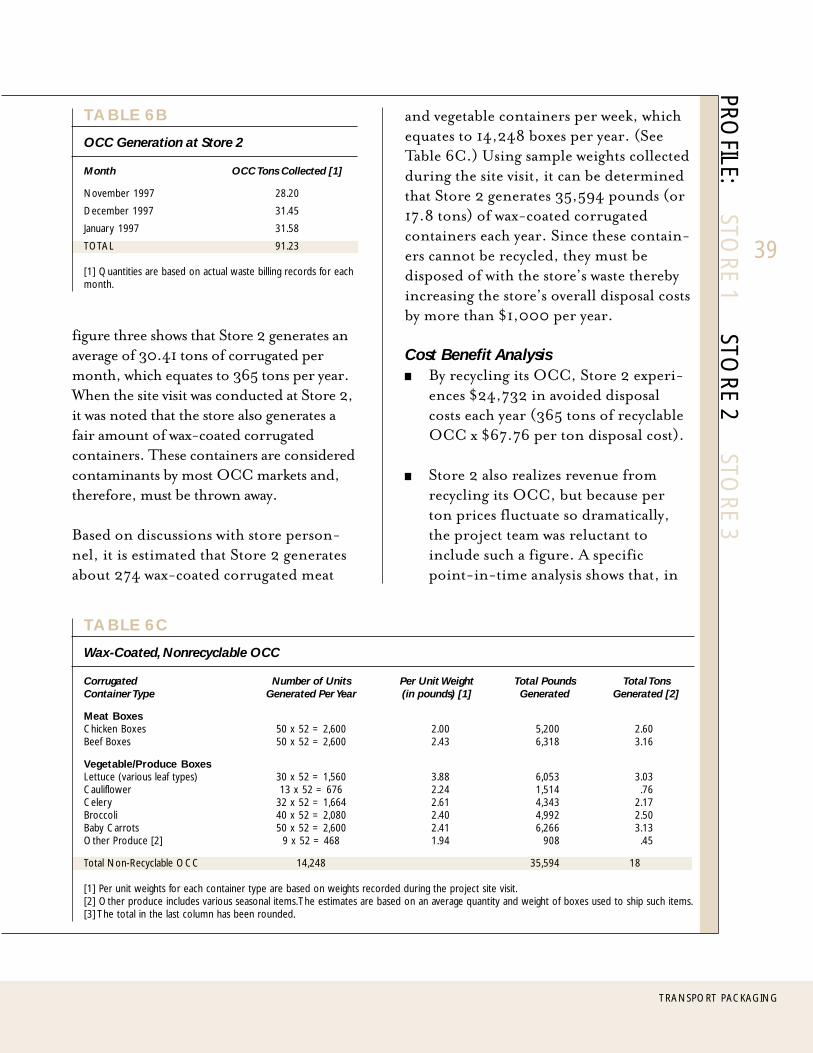

To determine how much wax-coated OCCthe stores were generating, the project teamasked the stores to set aside samples ofcoated boxes and weighed the samplesduring the site visits. Table 2B shows whatthe team found.

It should be noted that each of the storesappears to be generating far less wax-coatedOCC than the industry itself projects. Forexample, figures compiled by the GroceryManufacturers of America suggest that wax-coated OCC may comprise as much as 30percent of a store’s total OCC stream. Thestores in this project, however, appeared tohave much less wax-coated OCC (rangingfrom 1.1 percent to 4.9 percent of thestore’s total OCC stream). It is unclearwhether the discrepancy occurred becausethe stores generate much less of the materialor because the store samples wereunderrepresentative of the actual stream.This is an area where waste sorts wouldprovide more definitive information.

Table 2B also includes information on howmuch each of the stores would realize inavoided disposal costs if wax-coated OCCwere eliminated as a form of transportpackaging in the grocery industry. It shouldbe mentioned that a few suppliers havebegun using plain corrugated boxes withplastic liners, and others have begun experi-menting with using plastic shipping con-

tainers in place of wax-coated OCC (apractice that is supported by the FDA).Unfortunately, information on the eco-nomics of these alternatives was not availablefor this project and, therefore, has not beenincluded in the analysis.

During the project, it was determined thatgrocery stores may experience even greatersavings than those found in Table 2B be-cause, according to the American Forest andPaper Association (AF&PA), approximately10 to 15 percent of nonwaxed boxes (i.e.,recyclable boxes) are inadvertently thrownaway at grocery stores because employees areconfused about which boxes are and are notrecyclable. Table 2C shows the amount ofrecyclable OCC that each participating storemay be throwing away as a result of suchconfusion and what the stores could accruein avoided disposal costs by eliminating theconfusion.

6

CHAPTER TWO LESSONS ON OCC

TABLE 2B

Wax-Coated OCC Generated at ParticipatingStores and Potential Reduced Disposal CostsFrom Eliminating Wax-Coated OCC

AnnualTotal Avoided

Tons of DisposalWax-Coated Costs From

OCC EliminatingGenerated Per Ton Wax-Coated

Store Per Year [1] Disposal Cost OCC

Store 1 4 $141.72 $567

Store 2 18 $67.76 $1,220

Store 3 6 $60.17 $361

Average $716

[1] Based on sample weights taken at each of the stores during theon-site visit. The numbers have been rounded for summarypurposes.

Another thing the project team discovered isthat all of the participating grocery storeswere generating a significant portion ofheavily inked OCC, which is found prima-rily in the vegetable and fruit sections of thestores. In speaking with market representa-tives, however, the presence of this materialdoes not appear to have negatively affectedthe revenue that stores receive for theirOCC. In fact, sources indicated that the vastmajority of OCC recovery programs suc-cessfully comply with the Paper StockIndustry’s specifications for Grade 11 re-quirements. (Those specifications are forcorrugated containers having liners ofeither test liner, jute, or kraft, and contain-ing no more than 1 percent prohibitivematerials and no more than 5 percent totaloutthrows.)

The project team learned a number ofvaluable lessons while working with thestores to analyze their OCC streams andwaste management practices.

Lesson 1: Avoided Disposal CostsClearly, there is a strong economic incen-tive for grocery stores to recycle their OCC,particularly since it is generated in suchlarge quantities (making up the greatestproportion of transport packaging waste in astore’s waste stream). Using data gatheredfrom the three participating stores, a typicalstore could expect to generate an average of396 tons of OCC per year and pay anaverage of $89.88 per ton to dispose of it.If, however, it were to recycle that OCC, itcould realize more than $35,000 in avoideddisposal costs. (See sidebar entitled “Defin-ing a Typical Store.”)

Lesson 2: Recycling RevenueThere is an even greater economic incentivefor recycling OCC if one includes therevenue generated from recycling the mate-rial. Using a point-in-time average of pricesreceived by the three stores participating inthis project, the typical store could expect togenerate more than $24,000 per year inrevenue from recycling OCC. This figureshould be used with caution when makingprogrammatic decisions, however, sinceOCC prices fluctuate over time and varygreatly among stores. For example, wastebilling invoices show that Store 1 received$65 per ton for its baled OCC, Store 2received $36.55 per ton for its loose OCC,and Store 3 received $75 per ton for itsloose OCC (combined with office paperand kraft bags). None of the stores receivedthe national average per ton price for baledOCC, which industry trade publications putat $76.50 for 1997. These wide variationsindicate that any decisions that includerecycling revenue as a factor must be basedon local market prices and conditions.

7

TRANSPORT PACKAGING

TABLE 2C

Quantities of Recyclable OCC Thrown AwayDue to Confusion with Wax-Coated OCC andPotential Avoided Disposal Costs fromEliminating Confusion

Amount of Potential forRecyclable Reducing

OCC that May AnnualBe Thrown DisposalAway Due Costs by

to Confusion Per Ton EliminatingStore (in tons) Disposal Cost Confusion

Store 1 269 x 15% = 40 $141.72 $5,669

Store 2 365 x 15% = 55 $67.76 $3,727

Store 3 555 x 15% = 83 $60.17 $4,994

Average $4,797

Lesson 3: Eliminating Confusion Related toWax-Coated OCCMaking changes related to wax-coated OCCrepresents the single biggest area wherestores could accrue additional economicbenefits. Using data from the three partici-pating stores, it was found that the typicalstore could realize an average of $4,800 peryear in avoided disposal costs and $3,500 inadditional recycling revenue by recoveringrecyclable OCC that currently may bethrown away due to confusion with wax-coated OCC. (Recycling revenue is based onthe average price received by the threeparticipating stores during a specific pointin time.) In addition, the typical store couldaccrue more than $700 per year in avoideddisposal costs by eliminating wax-coatedOCC altogether. That brings the totaleconomic benefit of making changes relatedto wax-coated OCC to about $9,000 perstore per year.

Lesson 4: Alternatives to Wax-Coated OCCSome people in the grocery industry believethat wax-coated OCC cannot be replaced.This does not, however, appear to be thecase. According to the stores participating inthe project, some suppliers of meat, poul-try, vegetables, and fruit have already begunshipping their goods in alternative contain-ers, such as plastic bags that are then con-tained inside recyclable corrugated boxes.An example of such a box was found at Store2 for hydrocooled carrots distributed byGolden Valley Produce. A similar box wasused by Golden Plump Poultry to shipchicken parts. (A competitor’s chicken partswere sent in a plastic bag inside a wax-coatedbox.) In fact, Store 3 states that it no longerreceives any meat or poultry in wax-coatedcontainers.

The stores also point out that sometimesidentical products from the same manufac-turer come in both wax-coated andnonwaxed boxes. At Store 2, an employeeshowed the team a waxed box of bananas anda nonwaxed box of bananas shipped by thesame company. This, perhaps, indicates thatthe type of transport package used may notalways be driven solely by performanceissues but also by the preference of thesupplier and/or the availability of a certaintype of package. Regardless of the reasons,apparently some manufacturers/growershave already begun to reduce their relianceon wax-coated containers.

Lesson 5: Reusable Shipping ContainersWhile researching alternatives to wax-coatedOCC, the project team learned that somegrocery systems have begun replacing bothrecyclable and wax-coated OCC with re-turnable plastic shipping containers. Forexample, in a study entitled “TransportationPackaging and the Environment (1997),” itwas reported that Shaw’s Supermarkets—achain of 46 stores in Massachusetts—starteda waste reduction program in 1993 in whichreusable plastic shipping containers weresubstituted for corrugated containers,plastic bags, and polystyrene boxes whenshipping perishable goods. As a result of theswitch, the 46 stores realized a 70 percentdecrease in the amount of waste they gener-ated. While it is impossible to draw anyconclusions about what the stores partici-pating in this project might expect in theway of source reduction if they were toswitch to returnable plastic shipping con-tainers, it is worth mentioning that thispractice has been supported by the FDA forperishable goods and appears to be workingin practice within other grocery systems.

8

CHAPTER TWO LESSONS ON OCC

A precedent has been set at each of theparticipating stores for using returnableplastic shipping containers. For years theirdistributors have been shipping such thingsas health and beauty products, magazines,and general merchandise in plastic totes. Inaddition, bakeries commonly use returnableplastic trays to deliver baked goods. Obvi-ously the issues of using returnable plasticcontainers in vegetable, produce, meat, andpoultry applications are much more com-plex—such as the variety of products avail-able, the number of growers and farmersinvolved, the need to pre-cool some prod-ucts, and the shipping of wet goods—butthese programs do demonstrate that return-able systems can be developed and workeffectively in the grocery sector.

Lesson 6: Maturity of OCC RecyclingProgramsThe OCC recycling programs in the threeparticipating grocery stores appear to befairly mature. (The stores estimate theirrecovery rates at 95 percent.) Therefore,aside from changes with wax-coated con-tainers, the programs probably cannot growsignificantly in terms of greater recovery. IfOCC recycling programs in other stores areequally mature, then source reduction andreuse options should be pursued with gro-cers to achieve greater diversion. The suc-cess of store OCC recycling programsindicates that stores can effectively recyclematerials if (1) there is an economic incen-tive to do so, (2) there is support from storemanagement, and (3) the programs are easyand accessible.

Lesson 7: ContaminationThe project team did not notice any signifi-cant contamination issues associated withOCC. Two of the stores put their OCC in adesignated compactor for storage anddensification, and the project team foundfew contaminants except for an occasionalpiece of writing paper. One store—Store 1—bales its OCC, and the project team notedthat it stores the bales outside on an un-paved lot without pallets. The store’s mar-ket, however, did not have a problem withits storage practices or the fact that palletswere not used.

Lesson 8: Tray/Shrink PackagingWhile several source reduction options existfor OCC—such as replacing full corrugatedcontainers with kraft bags and source-reducing the flaps of corrugated boxes—themost significant source reduction trend inthe grocery industry is the shift from fullcorrugated containers to tray/shrink packag-ing (where goods are placed on corrugatedtrays and sealed with shrink wrap). Thesidebar entitled “Source Reduction Benefitsand Other Issues Related to Tray/ShrinkPackaging” shows that this packaging shiftcuts the weight of a transport package inhalf. This reduction translates into lowershipping costs, lower material costs, and areduction in processing costs, all of whichhelp improve the efficiency of the grocerydistribution system and reduce the amountof transport packaging waste that must behandled. (See the sidebar for more detailedinformation about the source reduction andcost benefits of tray/shrink packaging as wellas grocers’ perceptions of the package.)

9

TRANSPORT PACKAGING

10

Cha

pter

Thr

ee

11

TRANSPORT PACKAGING

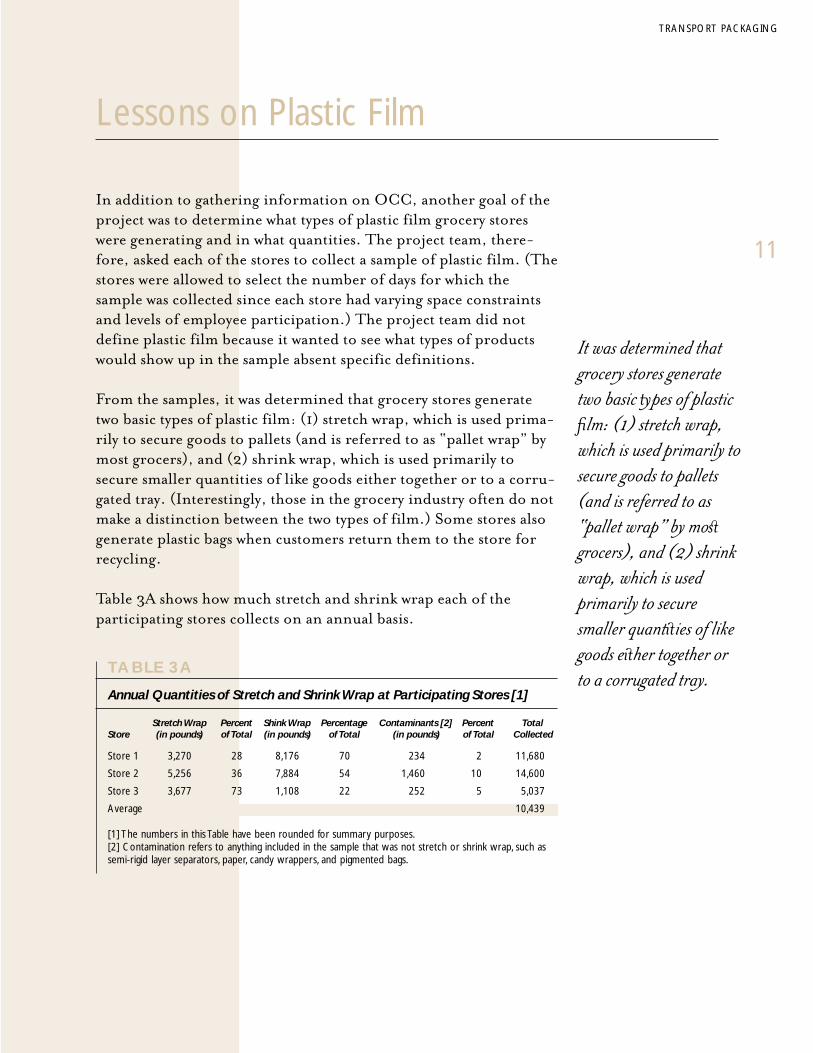

Lessons on Plastic Film

In addition to gathering information on OCC, another goal of theproject was to determine what types of plastic film grocery storeswere generating and in what quantities. The project team, there-fore, asked each of the stores to collect a sample of plastic film. (Thestores were allowed to select the number of days for which thesample was collected since each store had varying space constraintsand levels of employee participation.) The project team did notdefine plastic film because it wanted to see what types of productswould show up in the sample absent specific definitions.

From the samples, it was determined that grocery stores generatetwo basic types of plastic film: (1) stretch wrap, which is used prima-rily to secure goods to pallets (and is referred to as “pallet wrap” bymost grocers), and (2) shrink wrap, which is used primarily tosecure smaller quantities of like goods either together or to a corru-gated tray. (Interestingly, those in the grocery industry often do notmake a distinction between the two types of film.) Some stores alsogenerate plastic bags when customers return them to the store forrecycling.

Table 3A shows how much stretch and shrink wrap each of theparticipating stores collects on an annual basis.

It was determined that

grocery stores generate

two basic ypes of plastic

0lm: (1) stretch wrap,

which is used primarily to

secure goods to pallets

(and is referred to as

“pallet wrap” by mos

grocers), and (2) shrink

wrap, which is used

primarily to secure

smaller quantiies of like

goods eiher together or

to a corrugated tray.TABLE 3A

Annual Quantities of Stretch and Shrink Wrap at Participating Stores [1]

Stretch Wrap Percent Shink Wrap Percentage Contaminants [2] Percent TotalStore (in pounds) of Total (in pounds) of Total (in pounds) of Total Collected

Store 1 3,270 28 8,176 70 234 2 11,680

Store 2 5,256 36 7,884 54 1,460 10 14,600

Store 3 3,677 73 1,108 22 252 5 5,037

Average 10,439

[1] The numbers in this Table have been rounded for summary purposes.[2] Contamination refers to anything included in the sample that was not stretch or shrink wrap, such assemi-rigid layer separators, paper, candy wrappers, and pigmented bags.

12

CHAPTER THREE LESSONS ON PLASTIC FILM

The next step in the project was to quantifywhat each of the participating stores was payingfor waste disposal and what they could expect torealize in avoided disposal costs if they were torecycle their stretch and shrink wrap instead ofthrowing it away. Table 3B summarizes theresults of that work.

Of the three stores that participated in theproject, only Store 1 was actively recyclingplastic film. The store collects both stretchand shrink wrap, as well as plastic bags, andships the material through a backhaul ar-rangement to its wholesaler/distributor.The wholesaler/distributor puts the filmfrom Store 1 (along with that collected fromother stores) into a holding area where it iscombined with the stretch wrap generated bythe distribution center. The wholesaler/distributor bales the material, and it ispicked up on a regular basis by Bunzl Recy-

cling, a local market. No revenue is receivedfor the film by the store or the wholesaler/distributor; therefore, the only economicbenefit is in the form of avoided disposalcosts.

As Table 3A indicates, Store 1 does a fairlygood job of keeping contaminants out of itsfilm stream. The other two stores, however,had fairly high contamination rates in theirsamples. The contaminants included suchthings as green and blue semi-rigid layerseparators (used with produce), red andbeige potato bags, bag liners from produceboxes, strapping, plastic bottles, candywrappers, and fresh flower wraps. Most ofthese contaminants could be avoided if afairly simple, straightforward educationprogram were developed. (Keep in mindthat no education was done prior to samplecollection.)

Two of the three stores participating in theproject—Store 1 and Store 3—also collectplastic bags from customers for recycling.Samples from the stores indicate that theformer collects approximately 1,144 poundsof plastic bags per year and the latter collectsabout 1,059 pounds per year. In bothprograms, the bags are sent back to thestores’ wholesaler/distributors, where theyare consolidated for Bunzl Recycling. AtStore 1, the bags are marketed along withstretch and shrink wrap, whereas at Store 3they are marketed alone. (Store 3’s whole-saler/distributor collects its own stretch wrapfor recycling but sells it to a different market.)

The project team learned a number ofvaluable lessons while working with thestores to collect stretch and shrink wrap.

TABLE 3B

Potential Annual Avoided Disposal Costs atParticipating Stores From Recycling Stretch andShrink Wrap

PotentialQuantity of Annual Avoided

Film Collected Per Ton Disposal Costs(in tons) [1] Disposal Through

Store Per Year Cost [2] Recycling

Store 1 6 $141.72 850

Store 2 7 $67.76 474

Store 3 3 [3] $60.17 181

Average 502

[1] Quantities are based on samples collected and weighed duringthe site visits. The numbers have been rounded for summarypurposes.[2] Per ton disposal costs were obtained from actual waste billinginvoices and include collection costs, disposal costs, state tax, theMinnesota Waste Assessment Fee, and any other costs the storesincur.[3] It should be noted that Store 3’s sample was much smaller thanthat of other stores and probably represents about half of what itcould actually collect.

13

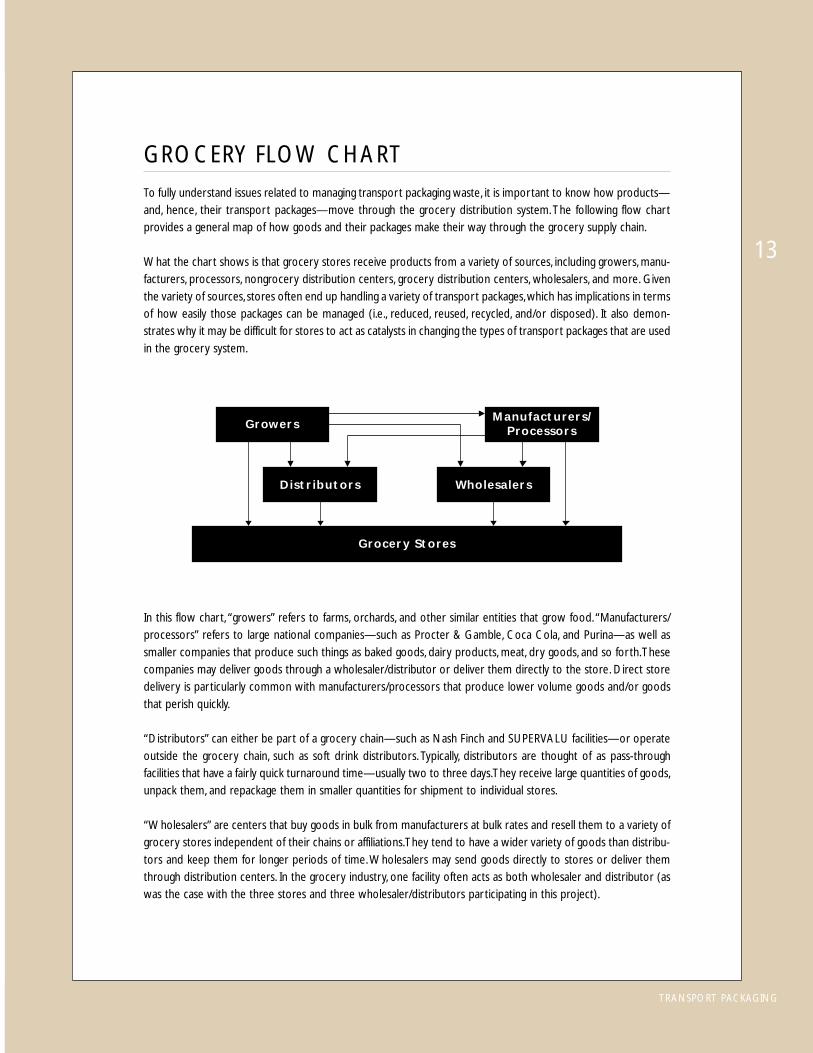

To fully understand issues related to managing transport packaging waste, it is important to know how products—

and, hence, their transport packages—move through the grocery distribution system. The following flow chart

provides a general map of how goods and their packages make their way through the grocery supply chain.

What the chart shows is that grocery stores receive products from a variety of sources, including growers, manu-

facturers, processors, nongrocery distribution centers, grocery distribution centers, wholesalers, and more. Given

the variety of sources, stores often end up handling a variety of transport packages, which has implications in terms

of how easily those packages can be managed (i.e., reduced, reused, recycled, and/or disposed). It also demon-

strates why it may be difficult for stores to act as catalysts in changing the types of transport packages that are used

in the grocery system.

In this flow chart, “growers” refers to farms, orchards, and other similar entities that grow food. “Manufacturers/

processors” refers to large national companies—such as Procter & Gamble, Coca Cola, and Purina—as well as

smaller companies that produce such things as baked goods, dairy products, meat, dry goods, and so forth. These

companies may deliver goods through a wholesaler/distributor or deliver them directly to the store. Direct store

delivery is particularly common with manufacturers/processors that produce lower volume goods and/or goods

that perish quickly.

“Distributors” can either be part of a grocery chain—such as Nash Finch and SUPERVALU facilities—or operate

outside the grocery chain, such as soft drink distributors. Typically, distributors are thought of as pass-through

facilities that have a fairly quick turnaround time—usually two to three days. They receive large quantities of goods,

unpack them, and repackage them in smaller quantities for shipment to individual stores.

“Wholesalers” are centers that buy goods in bulk from manufacturers at bulk rates and resell them to a variety of

grocery stores independent of their chains or affiliations. They tend to have a wider variety of goods than distribu-

tors and keep them for longer periods of time. Wholesalers may send goods directly to stores or deliver them

through distribution centers. In the grocery industry, one facility often acts as both wholesaler and distributor (as

was the case with the three stores and three wholesaler/distributors participating in this project).

GROCERY FLOW CHART

Grocery Stores

Distributors Wholesalers

GrowersManufacturers/

Processors

TRANSPORT PACKAGING

Lesson 1: Quantities of Plastic FilmUsing an average of the data gathered atthree participating stores, a typical grocerystore could expect to collect more than10,000 pounds of stretch and shrink wrapper year for recycling. (This is without anyconcerted collection efforts and withoutemployee education.) While this amountmay seem like a lot from a grocery store’sperspective, it is not a lot from a market’sperspective. Of the 22 markets contacted forthis project, only 9 have no minimumquantity requirements. One market acceptsminimum loads of 1,000 pounds, anotherfour markets accept minimum loads of5,000 pounds, and two markets have10,000-pound requirements. The remain-ing six markets require more material than agrocery store is likely to generate in a year.Thus, it may be difficult (although notimpossible) for stores to market stretch andshrink wrap on their own. Instead, as dem-onstrated by Store 1, it may be easier forgrocery stores to recycle their film through abackhaul arrangement with their wholesaler/distributor.

Lesson 2: Avoided Disposal CostsFrom a grocery store’s perspective, there isnot much economic incentive to recyclefilm. As Table 3B shows, the typical grocerystore can expect to save an average of only$500 per year in avoided disposal costs byrecycling stretch and shrink wrap. It isimportant to remember, however, thatdecreased costs of any amount may bevaluable in the highly competitive, low-margin grocery industry. And if film con-tinues to replace OCC in transport packag-ing, then the amount of film available forrecycling will grow and the economic ben-efits of recycling it will improve.

Lesson 3: Economic Benefits forWholesaler/DistributorsWhile there may not be an economic incen-tive for stores to recycle film, there may bean economic incentive for wholesaler/distributors to do so. For example, oneparticipating wholesaler/distributor serves180 stores in Minnesota. If each of thosestores sent an average of 10,000 pounds ofstretch and shrink wrap back to the whole-saler/distributor for recycling, that wouldequate to 1,854,000 pounds (or 927 tons)of film per year. Add to that the 34,600pounds (or 17.3 tons) of stretch wrap thatthe wholesaler/distributor generates itself,and the total annual quantity of film avail-able for recycling would be 1,888,600pounds (or 946 tons). The wholesaler/distributor reported that it currently re-ceives 5 cents per pound for its material,which means the total revenue from recy-cling film would be $94,430 per year.

The wholesaler/distributor will also incursome costs. An APC study entitled “StretchWrap Recycling: A How-To Guide” esti-mates that stretch wrap recycling programscost about $.026 per pound, includingexpenses related to employee training,special containers, baling labor, bale wire/strapping, and labor related to collectingand upgrading the material. Using thisestimate, the wholesaler/distributor couldexpect to incur costs of about $49,104.After program costs, therefore, the whole-saler/distributor could expect net revenue of$45,326 per year by recycling stretch andshrink wrap. (In addition, it would keepnearly 950 tons of waste out of the landfill.)

14

CHAPTER THREE LESSONS ON PLASTIC FILM

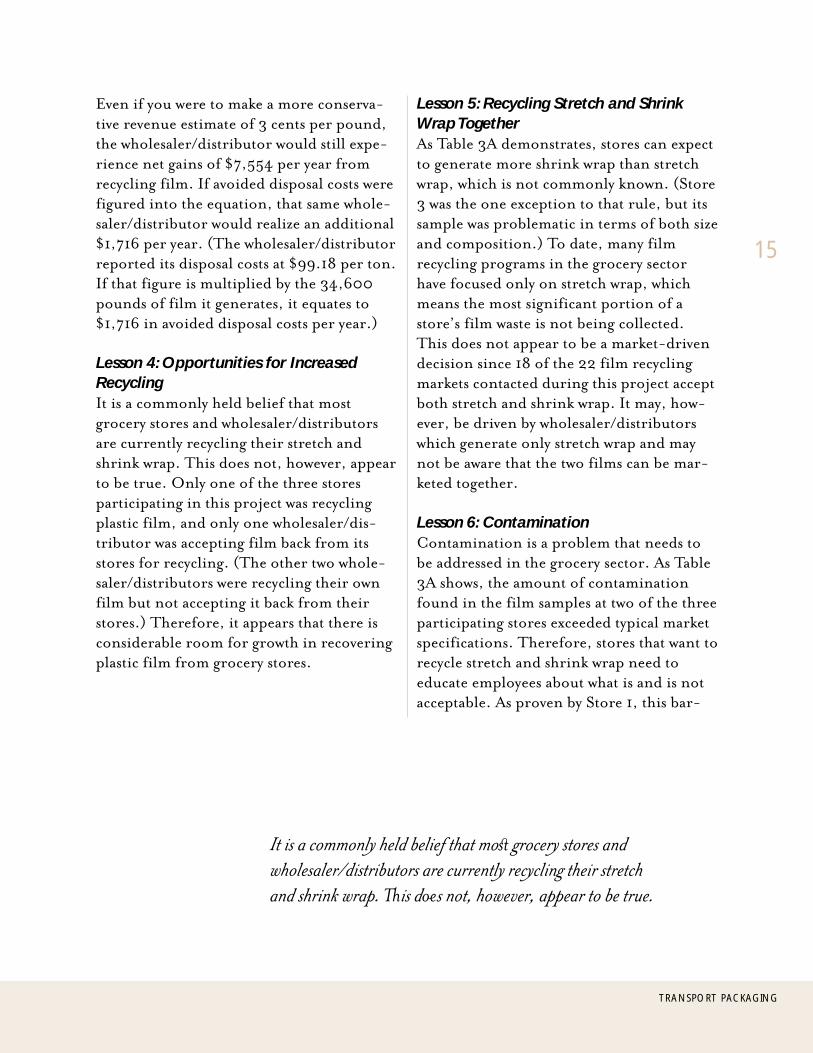

Even if you were to make a more conserva-tive revenue estimate of 3 cents per pound,the wholesaler/distributor would still expe-rience net gains of $7,554 per year fromrecycling film. If avoided disposal costs werefigured into the equation, that same whole-saler/distributor would realize an additional$1,716 per year. (The wholesaler/distributorreported its disposal costs at $99.18 per ton.If that figure is multiplied by the 34,600pounds of film it generates, it equates to$1,716 in avoided disposal costs per year.)

Lesson 4: Opportunities for IncreasedRecyclingIt is a commonly held belief that mostgrocery stores and wholesaler/distributorsare currently recycling their stretch andshrink wrap. This does not, however, appearto be true. Only one of the three storesparticipating in this project was recyclingplastic film, and only one wholesaler/dis-tributor was accepting film back from itsstores for recycling. (The other two whole-saler/distributors were recycling their ownfilm but not accepting it back from theirstores.) Therefore, it appears that there isconsiderable room for growth in recoveringplastic film from grocery stores.

Lesson 5: Recycling Stretch and ShrinkWrap TogetherAs Table 3A demonstrates, stores can expectto generate more shrink wrap than stretchwrap, which is not commonly known. (Store3 was the one exception to that rule, but itssample was problematic in terms of both sizeand composition.) To date, many filmrecycling programs in the grocery sectorhave focused only on stretch wrap, whichmeans the most significant portion of astore’s film waste is not being collected.This does not appear to be a market-drivendecision since 18 of the 22 film recyclingmarkets contacted during this project acceptboth stretch and shrink wrap. It may, how-ever, be driven by wholesaler/distributorswhich generate only stretch wrap and maynot be aware that the two films can be mar-keted together.

Lesson 6: ContaminationContamination is a problem that needs tobe addressed in the grocery sector. As Table3A shows, the amount of contaminationfound in the film samples at two of the threeparticipating stores exceeded typical marketspecifications. Therefore, stores that want torecycle stretch and shrink wrap need toeducate employees about what is and is notacceptable. As proven by Store 1, this bar-

15

TRANSPORT PACKAGING

It is a commonly held belief that mos grocery stores and

wholesaler/distributors are currently recycling their stretch

and shrink wrap. `is dos not, however, appear to be true.

rier is not insurmountable. A simple train-ing session in which employees learn whatstretch wrap and shrink wrap is and where itis generated will go a long way toward im-proving quality. Samples of acceptablematerials should be posted near collectioncontainers so that employees can check thematerial prior to putting it in the collectionbox or bag. During the training session,employees should also be shown commoncontaminants—such as those mentionedearlier—so they know what not to include.

Lesson 7: Management SupportEnthusiasm for recycling film varies widelyamong stores. One of the stores participat-ing in this project wanted very much torecycle film and was aggressive in obtainingits sample. Another store had its filmsample thrown away twice prior to the sitevisit, and the third store was less than en-thusiastic about obtaining a sample eventhough it had willingly agreed to participatein the project. The varying levels of enthusi-asm are a reminder that recycling is not partof a grocery store’s core business, and unlessmanagement is excited about recycling andcommitted to making its programs work,then stores cannot succeed.

Lesson 8: Storage SpaceWhile all of the participating stores men-tioned concerns about space constraints,none of them appeared to have problems inpractice. They simply put the film in what-ever type of container was available—rangingfrom gaylord boxes and carts to bags andmetal cages—and stored it in any availablespace. Stores working with wholesaler/distributors on backhaul programs for filmwill have trucks coming and going on a daily

basis, which should allow them to movestretch and shrink as often as necessary tokeep it from taking up floor space.

Lesson 9: Marketing FilmThe project team learned that one of thebiggest barriers to recycling film at thegrocery store and wholesaler/distributorlevel is the fact that people are not aware ofthe markets that are available for film, norare they aware of what they must do to meetmarket specifications. For that reason, theproject team developed a market listing(found in Appendix B) of companies inMinnesota and select companies fromaround the country that accept film fromthe grocery sector for recycling. For eachcompany, the project team has listed thecompany name, location, and telephonenumber, as well as the quantity of film itrequires, the form it wants its material in,its quality requirements, and pricing infor-mation where available. This listing can beused by grocers and wholesaler/distributorsthat want to start new film recycling programsor look for alternatives to current markets.

Lesson 10: Source ReductionWhen working with one grocery store, theproject team learned about a product beingmanufactured by 3M called Scotch™ BrandStretchable Tape (ST). 3M maintains thatthe product—which is made with linear lowdensity polyethylene (as is most stretch andshrink wrap), is 4 or 6 mils thick, and has asolventless adhesive—offers significantsource reduction opportunities over tradi-tional stretch film. In its product literature,the company indicates that 2.1 ounces (or60 grams) of ST can replace 9.1 ounces (or260 grams) of stretch wrap on a typical load,resulting in a 77 percent material savings.

16

CHAPTER THREE LESSONS ON PLASTIC FILM

17

TRANSPORT PACKAGING

Using ST probably would not result in anysignificant benefits at the grocery store level(except for modest avoided disposal costs ifthe store were not recycling its stretch wrap),but it may provide a more significant op-portunity for source reduction at the whole-saler/distributor level. For example, one ofthe wholesaler/distributors participating inthis project reported that it purchases ap-proximately 20,000 pounds (or 10 tons) ofstretch wrap per year to secure goods topallets and, in most instances, the stretchwrap is discarded by its stores. If the whole-saler/distributor were to use ST instead ofstretch film, it would generate only 4,600pounds (or 2.3 tons) of transport packagingwaste, which is preferable from an economicperspective because eliminating waste at thesource is more cost-effective than recyclingit at the back end.

ST may also appeal to others in the grocerydistribution system. For example, 3Mreports that a meat packing house was pack-ing 48-50 pounds of ham into 10-inch-high boxes. The boxes were then stacked inseven layers on a 48" x 40" pallet, securedwith stretch film and cornerboards, andtransported to an off-site blast freezer. At

the freezer, the cornerboards and stretchfilm were removed to improve cold air flowto the hams and reduce freezing time. Afterthat process, the hams were rewrapped andsent to a distributor.

When exploring ways to reduce its costs, themeat packing house found that ST was agood alternative to stretch wrap because (1)it allowed air to flow through the pallet loadand, therefore, did not have to be removedduring freezing, and (2) it required less rawmaterial. The meat packer was using 15.7ounces of stretch wrap each time the palletwas wrapped, which meant that a total of31.4 ounces of material was being used forshipment. The same pallet configurationrequired a total of only 3.3 ounces of ST,resulting in 28.1 fewer ounces of transportpackaging waste per pallet load. In addition,the meat packing house saved 42.5 percentin material costs.

It should be noted that the project team didnot conduct any of its own research on theperformance or cost of ST. The example isincluded only to apprise those in the grocerydistribution system of a potential sourcereduction option they may want to investigate.

Cha

pter

Fou

r

TRANSPORT PACKAGING

Lessons on Pallets

19

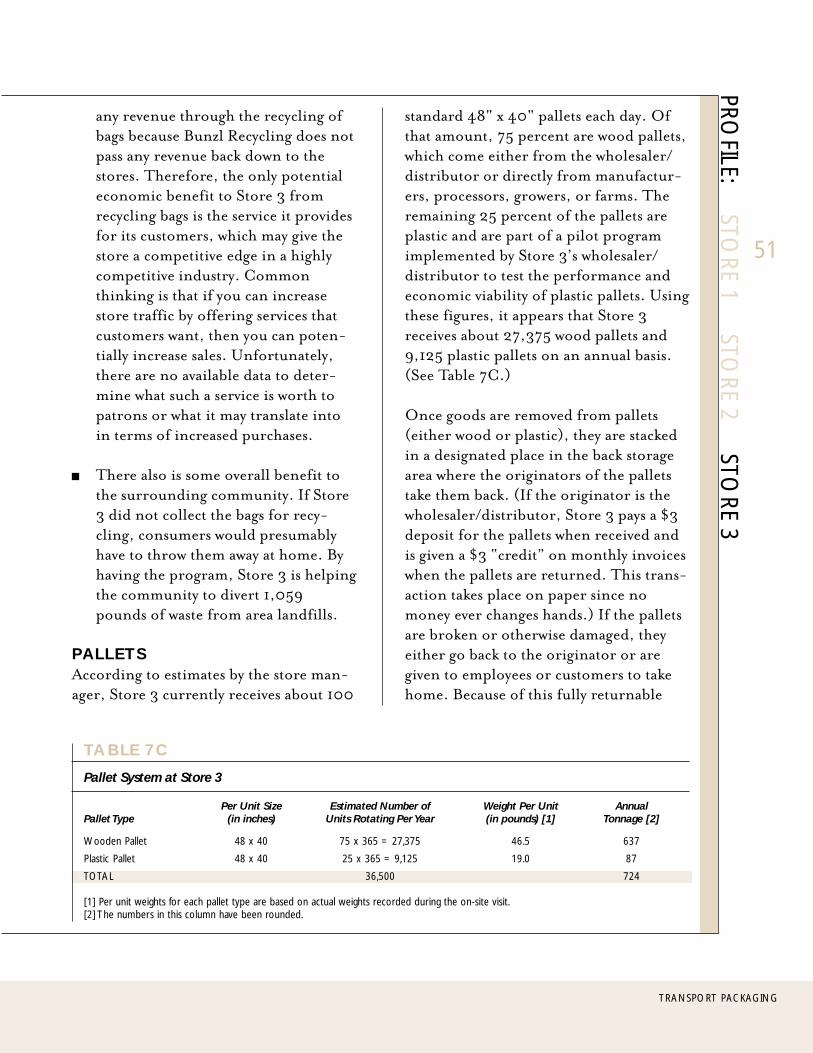

As with OCC and plastic film, one of the project goals was to deter-mine how many pallets stores receive; what they do with them afteruse; what reduction, reuse, and recycling options are available; andwhat the economic impact of those options would be on individualgrocery stores. To that end, the project team worked with the storesto estimate how many pallets they receive on a regular basis. Table4A shows the results of that work.

TABLE 4A

Tons of Pallets (48"x 40") Rotating in Stock Per Year

Number of Total Weight Number of Total WeightWood Units of Wood Plastic Pallets of Plastic

Rotating Pallets Rotating Pallets Total AnnualStore in Stock (in tons) in Stock (in tons) Tonnage [1]

Store 1 10,400 159.5 0 0 160

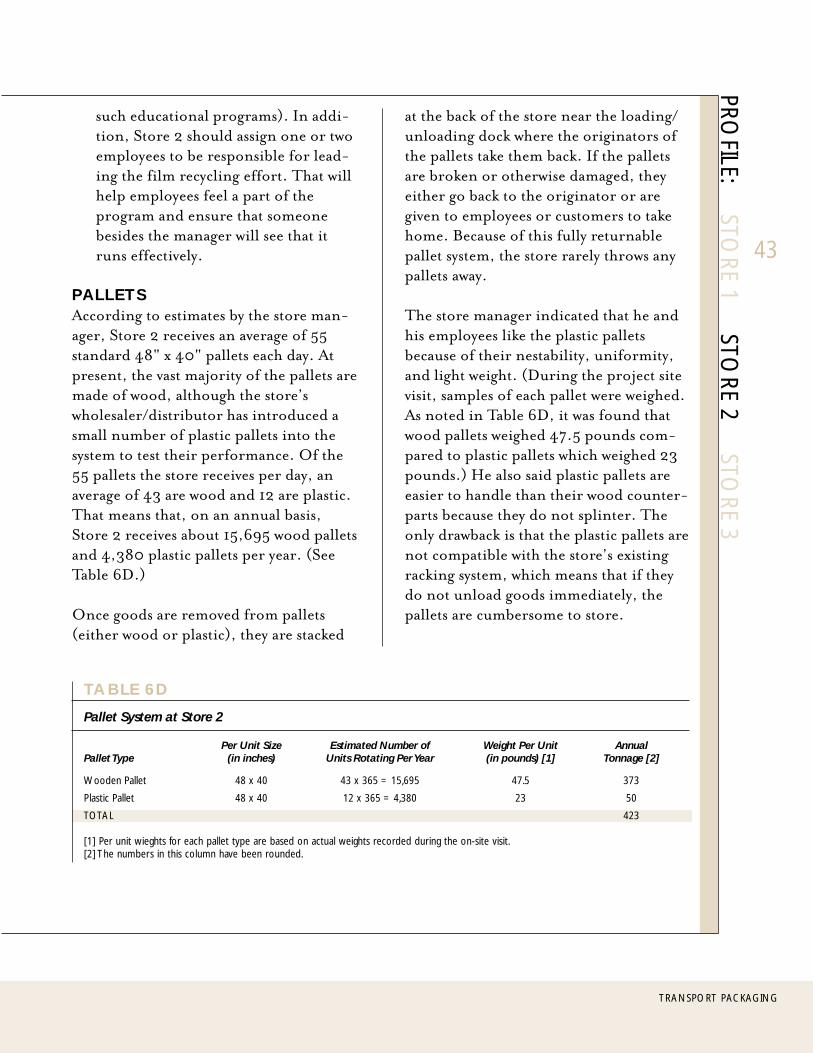

Store 2 15,695 372.8 4,380 50.37 423

Store 3 27,375 636.5 9,125 86.7 724

[1] The numbers have been rounded for summary purposes.

The stores participating in the project do not dispose of pallets attheir facilities. Instead, when goods are unloaded, the pallets arestacked near the loading/unloading area and returned to the sup-plier, whether that be the store’s wholesaler/distributor, a grower/farmer, or a processor/manufacturer. Even when pallets are dam-aged, they are returned to suppliers for repair or recycling, or givento customers and employees for their own use. This fully “return-able” pallet system, which has been in operation for many years,benefits stores economically in the form of avoided disposal costs.Table 4B shows the avoided costs that each store experiences becauseit does not have to dispose of pallets.

TABLE 4B

Avoided Disposal Costs that Result from Returnable Pallet Programs

Annual Tons of Per Ton Annual AvoidedStore Pallets Generated Disposal Cost Disposal Costs

Store 1 160 $141.72 $22,675

Store 2 423 $67.76 $28,662

Store 3 724 $60.17 $43,563

Average $31,633

During the project, it was noted that two ofthe three participating stores are currentlyreceiving goods on plastic pallets (or ship-ping platforms). In both instances, thepallets are part of a pilot project being runby the store’s wholesaler/distributor to testthe feasibility of using reusable plasticpallets in the grocery distribution system.Both stores report that they like plasticpallets because they are lightweight,nestable, uniform in size, and easier andsafer to handle than their wood counter-parts. The only drawback is that plasticpallets do not work with the stores’ existingracking systems, which means that if goodsare not immediately unloaded, the palletsmust be stored on the ground (thus, takingup valuable floor space). This did not,however, appear to be a significant problemat either facility.

Since grocery stores do not purchase ordispose of pallets, there is little incentive forthem to explore opportunities for reducing,reusing, or recycling. For that reason, theproject team refocused its efforts on palletissues that arise at the wholesaler/distributorlevel.1 At present, one of the most pressingissues related to pallets (and the issue thatwas ultimately chosen for research in thisproject) is whether plastic is an economicallyviable alternative to wood.

To answer that question, the project teamturned to SUPERVALU—the nation’s largestgrocery wholesaler/distributor headquar-tered in Eden Prairie, Minnesota—which

volunteered to provide “real world” data onthe economics of using returnable plasticpallets. Using SUPERVALU’s data, theproject team found that

SUPERVALU saved 63 cents per tripover the course of three years by usingplastic pallets instead of wood;

it could potentially reduce its “indirect”or “soft” costs by approximately$556,000 per year (or $3.70 per pal-let); and

it achieved payback on its initial invest-ment shortly after the second year ofuse.

Following is an explanation of howSUPERVALU and the project team arrivedat those figures. It should be noted that,while the numbers were derived from actualdata provided by SUPERVALU, they arebased on a series of assumptions made byboth SUPERVALU and the project team—assumptions that must be taken into consid-eration when trying to interpret the eco-nomic value of using plastic pallets. It alsoshould be noted that neither SUPERVALUnor the project team purport that plasticpallets are a panacea; instead, they are oneoption that the grocery industry can explorein its efforts to implment economicallyviable reduction, reuse, and recycling pro-grams.

COST ANALYSIS: DIRECTECONOMIC BENEFITSAt present, SUPERVALU uses approxi-mately 20 million pallets, which can bebroken down into three basic categories: (1)

20

CHAPTER FOUR LESSONS ON PALLETS

1 Slip sheets are another option that could have been explored, but thestores participating in this project believed that reusable plastic palletswere more prevalent and a better option to study given limited time andresources.

about 3.5 million are wood CHEP pallets,which are leased through a third-partysystem, (2) about 16.35 million are standardwhite wood pallets that SUPERVALU some-times purchases and manages, and (3)150,000 are standard plastic shippingplatforms that it purchases and manages.(The latter pallets are used for transportinggoods to stores only and are not rackable.)

If the grocery industry were to make astraight cost comparison based only on theinitial purchase price of a pallet, plasticpallets would not fare well. SUPERVALUreports that plastic pallets cost an average of$21, whereas white wood pallets cost only$7. SUPERVALU is quick to point out,however, that while the initial purchaseprice of a plastic pallet is three times that ofa wood pallet, plastic pallets have a signifi-cantly longer life. For example,SUPERVALU reports that its plastic palletsmake an average of 100 trips per year, andfor the past three years have required mini-mal repair and replacement, putting theirlifetime trippage to date at about 300cycles. Comparatively, its wood palletstypically make only 10 cycles before needingreplacement.

Put in financial terms, the average plasticpallet costs SUPERVALU 7 cents per trip($21.00 divided by 300 trips), compared tothe average wood pallet which costs 70 centsper trip ($7.00 pallet cost divided by 10trips). Therefore, SUPERVALU is saving 63cents per trip by using plastic pallets. (Inpractice, the savings are probably evengreater since this analysis does not includeexpenses related to repairing wooden pal-lets—expenses that are usually incurred twice

during the life of a wood pallet. In addition,the savings are based on three years of use,but SUPERVALU believes that plastic palletswill be used for a much longer period.)

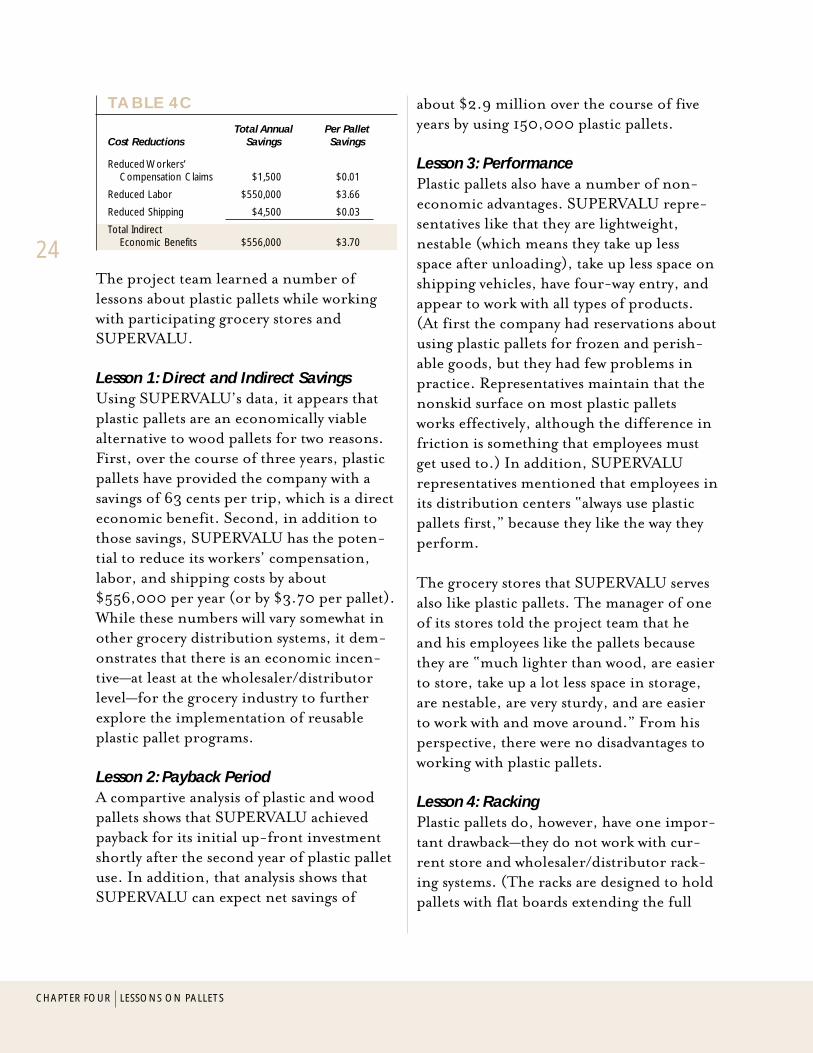

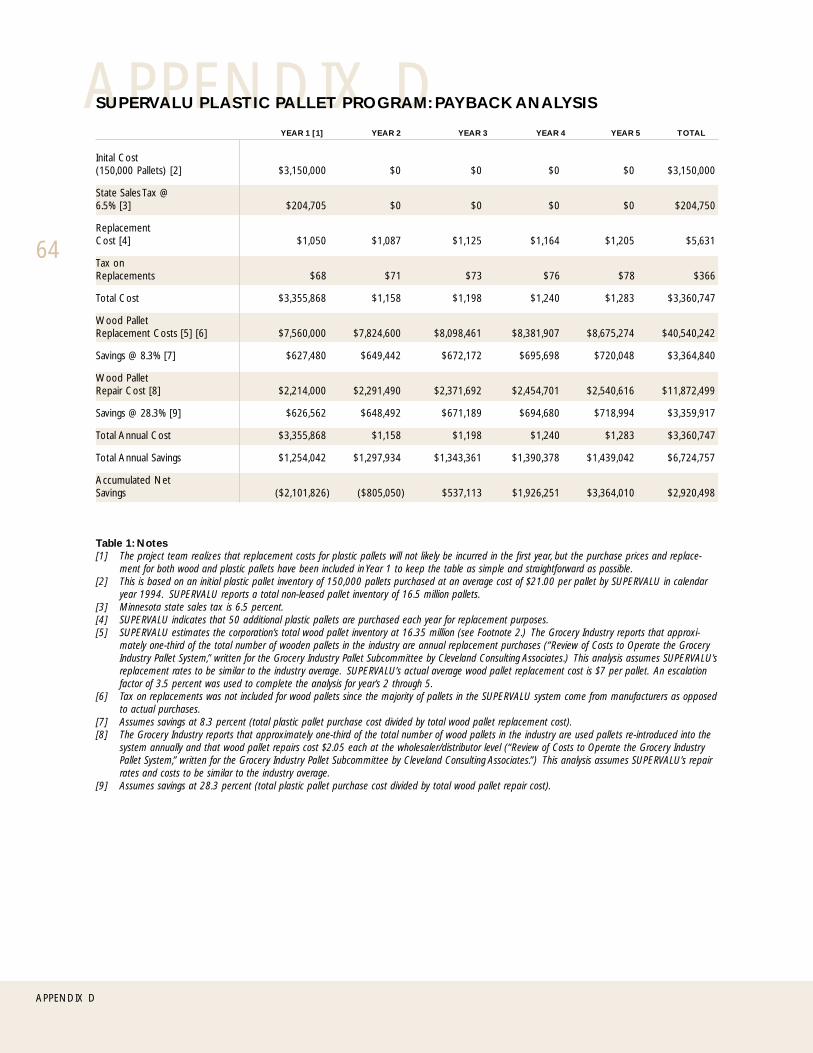

A common question from grocery industryrepresentatives regarding plastic pallets is:“How soon can we expect to achieve pay-back?” In other words, if they make a sub-stantial upfront investment in plastic pal-lets, when will the savings start outweighingthe expense? While there are several waysthat one can make that calculation, theproject team used a formula that took intoaccount (1) the initial purchase price ofboth wood and plastic pallets, (2) repaircosts for wood pallets, and (3) replacementcosts for wood and plastic pallets. The teamthen projected these costs over a five-yearperiod and found that SUPERVALUachieved payback sometime after the secondyear of using plastic pallets. The results alsoindicate that SUPERVALU can expect netsavings of about $2.9 million over thecourse of five years by using 150,000 plasticpallets. (See Appendix D for more informa-tion on how these numbers were calculated.)

Another question that grocers ask is whetherreplacing wood pallets with plastic palletswill result in avoided disposal costs (anotherpotential economic benefit). ForSUPERVALU, the answer is no because itsdistribution centers do not dispose of woodpallets. Instead, wood pallets come into thedistribution centers filled with goods frommanufacturers. The goods are then removedfrom the pallets, broken down into smallerlots, reloaded on wood pallets, shipped tothe stores that SUPERVALU serves, andshipped back to one of SUPERVALU’s

21

TRANSPORT PACKAGING

distribution centers. The distributioncenters then contract with local third-partypallet recyclers and remanufacturers to takethe pallets, repair the damaged ones, recyclethe ones beyond repair, and return theintact ones. While some SUPERVALUdistribution centers pay for this service,others receive revenue (over and above thecost) from the wood stream they generate.When looking across the entire corporation,SUPERVALU believes that the total cost ofhandling wood pallet waste is offset by therevenues generated by recycling. Therefore,if wood shipping platforms were replacedwith plastic shipping platforms, there wouldnot be an economic benefit in the form ofavoided disposal costs. (Similarly, mostplastic pallet vendors will pay a small fee forreturned damaged plastic pallets, butSUPERVALU believes these revenues wouldbe offset by transportation costs.)

COST ANALYSIS: INDIRECTECONOMIC BENEFITSWhile several studies have been conductedon the potential direct economic benefits ofusing plastic pallets, very little informationexists on potential “indirect” or “soft”benefits, such as savings that may resultfrom reduced workers’ compensationclaims, reduced labor, or reduced shippingcosts. In an effort to try to generate suchdata, SUPERVALU helped the project teamdevelop a system for measuring indirectbenefits. Following are the results of theproject team’s analysis using SUPERVALU’sdata and proposed methodology.

Reduced Workers’ Compensation ClaimsIn 1997, SUPERVALU had a total of 186pallet-related injuries, which generated

$900,000 in workers compensation claims.Although the company does not distinguishbetween claims related to wood or plasticpallets, it does track general types of pallet-related injuries, including (1) stress injuries(that result from lifting, pushing, or pullingpallets); (2) slivers and cuts; (3) crushedextremities; and (4) injuries from steppingon pallets (such as falls, twisted ankles, andso forth).

In 1997, the greatest percentage of palletinjuries at SUPERVALU were stress-related.Of the 186 injuries, between 30 and 35 per-cent were stress-related (56-65 injuries), andthose injuries accounted for 60 percent ofSUPERVALU’s pallet-related workers’ com-pensation costs (or $540,000). SUPERVALUfeels that stress-related claims probably aremore likely to occur with wood pallets thanwith plastic pallets since the latter weighconsiderably less. (The project teamweighed SUPERVALU pallets at one of itsstores and found that plastic pallets weighedonly 19 pounds whereas its wood counter-parts weighed 46.5 pounds.) Therefore, ifSUPERVALU were to use all plastic pallets,it could reduce stress-related workers’ com-pensation claims by as much as one-third or$178,200 per year. If those cost savings areapplied on a per-pallet basis, SUPERVALUcould save as much as $.009 per pallet inworkers’ compensation claims by switchingentirely from wood to plastic ($178,200/20million pallets in circulation = $.009 perpallet).

In addition, SUPERVALU reports that 5percent of all injuries in 1997 were relatedto slivers and cuts, which are most likely tooccur when using wood pallets. Considering

22

CHAPTER FOUR LESSONS ON PALLETS

that those injuries accounted for about 2percent of SUPERVALU’s total workers’compensation costs that year (or $18,000),it could save an additional $ .001 per palletby switching from wood to plastic ($18,000/20 million pallets).

Adding the $.009 per pallet in reducedclaims related to stress injuries to the $.001in reduced claims related to cuts and sliversindicates that SUPERVALU could reduce itstotal workers’ compensation claims by asmuch as $.01 per pallet by switching fromwood to plastic. Since SUPERVALU cur-rently has 150,000 plastic pallets in circula-tion, it probably has reduced its actual costsby about $1,500 per year.

Reduced Labor CostsThe way that SUPERVALU calculates re-duced labor costs relates to the way in whichpallets are moved within the system. Withplastic pallets, SUPERVALU engineers havecalculated that they can save 6 seconds perpallet in movement time each time a plasticpallet makes a trip. Therefore, sinceSUPERVALU has 150,000 plastic palletsthat each make 100 trips per year, it has atotal potential time savings of 90 millionseconds, or 1.5 million minutes, or 25,000hours.

To translate that into dollars, SUPERVALUcalculates warehouse employee salaries at$22 per hour ($15 per hour in wages plus $8per hour in benefits). Using that figure andthe 25,000 hours saved by using plasticpallets instead of wood, SUPERVALU couldrealize an annual savings of $550,000 peryear, or approximately $3.66 per pallet.

Reduced Shipping CostsBecause plastic pallets have “four-way en-try,” SUPERVALU maintains that you can“spin” them when loading the truck. Thatspinning capability translates into spacesavings on the vehicle which, in turn, allowsSUPERVALU to load more goods onto onetruck. SUPERVALU estimates that by spin-ning pallets, it can get four extra palletsonto a vehicle, thereby increasing truckcapacity by 10 percent.

It follows that if SUPERVALU can increase theamount of product it can load onto everyvehicle, then there can be fewer deliveries,which should result in fewer total miles trav-eled. In 1997, SUPERVALU trucks traveled atotal of 95 million miles at a conservative costestimate of $1.25 per mile; therefore, its travelcosts that year were $118,750,000. IfSUPERVALU used all plastic pallets, it couldreduce that cost by 10 percent or $1,187,500.Since it does not always send full loads to itsparticipating stores, SUPERVALU recom-mends that that number be cut in half, mean-ing that it would really save about $593,750 inshipping costs by switching entirely from woodto plastic pallets. Dividing $593,750 by 20million equates to a per-pallet savings of 3cents (or $.030). Of course, at present,SUPERVALU has only 150,000 plastic palletsin circulation, which puts its actual annualsavings at about $4,500.

Total Indirect Economic BenefitsAs Table 4C shows, if you add up all of thepreceding numbers, SUPERVALU couldpotentially reduce its “indirect” or “soft”costs by approximately $556,000 per year(or $3.70 per pallet) by using 150,000plastic pallets.

23

TRANSPORT PACKAGING

TABLE 4C

Total Annual Per PalletCost Reductions Savings Savings

Reduced Workers’Compensation Claims $1,500 $0.01

Reduced Labor $550,000 $3.66

Reduced Shipping $4,500 $0.03

Total IndirectEconomic Benefits $556,000 $3.70

The project team learned a number oflessons about plastic pallets while workingwith participating grocery stores andSUPERVALU.

Lesson 1: Direct and Indirect SavingsUsing SUPERVALU’s data, it appears thatplastic pallets are an economically viablealternative to wood pallets for two reasons.First, over the course of three years, plasticpallets have provided the company with asavings of 63 cents per trip, which is a directeconomic benefit. Second, in addition tothose savings, SUPERVALU has the poten-tial to reduce its workers’ compensation,labor, and shipping costs by about$556,000 per year (or by $3.70 per pallet).While these numbers will vary somewhat inother grocery distribution systems, it dem-onstrates that there is an economic incen-tive—at least at the wholesaler/distributorlevel—for the grocery industry to furtherexplore the implementation of reusableplastic pallet programs.

Lesson 2: Payback PeriodA compartive analysis of plastic and woodpallets shows that SUPERVALU achievedpayback for its initial up-front investmentshortly after the second year of plastic palletuse. In addition, that analysis shows thatSUPERVALU can expect net savings of

about $2.9 million over the course of fiveyears by using 150,000 plastic pallets.

Lesson 3: PerformancePlastic pallets also have a number of non-economic advantages. SUPERVALU repre-sentatives like that they are lightweight,nestable (which means they take up lessspace after unloading), take up less space onshipping vehicles, have four-way entry, andappear to work with all types of products.(At first the company had reservations aboutusing plastic pallets for frozen and perish-able goods, but they had few problems inpractice. Representatives maintain that thenonskid surface on most plastic palletsworks effectively, although the difference infriction is something that employees mustget used to.) In addition, SUPERVALUrepresentatives mentioned that employees inits distribution centers “always use plasticpallets first,” because they like the way theyperform.

The grocery stores that SUPERVALU servesalso like plastic pallets. The manager of oneof its stores told the project team that heand his employees like the pallets becausethey are “much lighter than wood, are easierto store, take up a lot less space in storage,are nestable, are very sturdy, and are easierto work with and move around.” From hisperspective, there were no disadvantages toworking with plastic pallets.

Lesson 4: RackingPlastic pallets do, however, have one impor-tant drawback—they do not work with cur-rent store and wholesaler/distributor rack-ing systems. (The racks are designed to holdpallets with flat boards extending the full

24

CHAPTER FOUR LESSONS ON PALLETS

length and width of the platform. Plasticpallets, however, have nine small, protrud-ing legs which do not work with currentracks.) SUPERVALU said that if the plasticpallet industry were to make a lightweightrackable plastic pallet, it would be interestedin using them. (Right now, rackable plasticpallets do not weigh much less than wood,which limits their advantages.) Anothergrocery industry representative mentionedthat a different option would be for thepallet industry to make a new racking systemthat is compatible with plastic shippingplatforms or to retrofit existing systems.

SUPERVALU representatives also indicatedthat plastic pallets are probably best used ina closed-loop system where return policies(such as small deposits) can be imple-mented. At an initial purchase price of $21per pallet, companies cannot afford to haveplastic pallets disappear, particularly sincetheir value to the company increases over time.

Lesson 5: Wholesalers as AdvocatesSince grocery stores do not purchase, dis-pose of, or manage pallets, it is unlikely thatthey will be drivers of change in convertingfrom wood to plastic pallets. Wholesaler/distributors such as SUPERVALU, however,can strongly advocate for their use withmanufacturers and third-party leasingcompanies (such as CHEP) because they candemonstrate the economic advantages thatcan be gained through the use of plasticpallets.

Lesson 6: Indirect Benefits for StoresWhile individual grocery stores will notexperience direct economic benefits if thesystem switches from wood to plastic pallets,