turkish aviation sector - garanti yatırım · please see the last page of this report for...

TRANSCRIPT

RESEARCH

Please see the last page of this report for important disclosures.

TURKISH AVIATION SECTOR

Secular growth rather than cyclical

February 2014

Analyst: Baris Ince

+90 (212) 384 1141

Sales Contact:

+90 (212) 384 1155

Please see the last page of this report for important disclosures.

2

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Table of Contents

EXECUTIVE SUMMARY 3

Recommendations & Valuations 4

A closer look at the aviation sector 8

A study on LCC vs. FSC 13

Turkey in Global Rankings 14

Global Sector Outlook 17

Turkish Aviation Sector at a glance 19

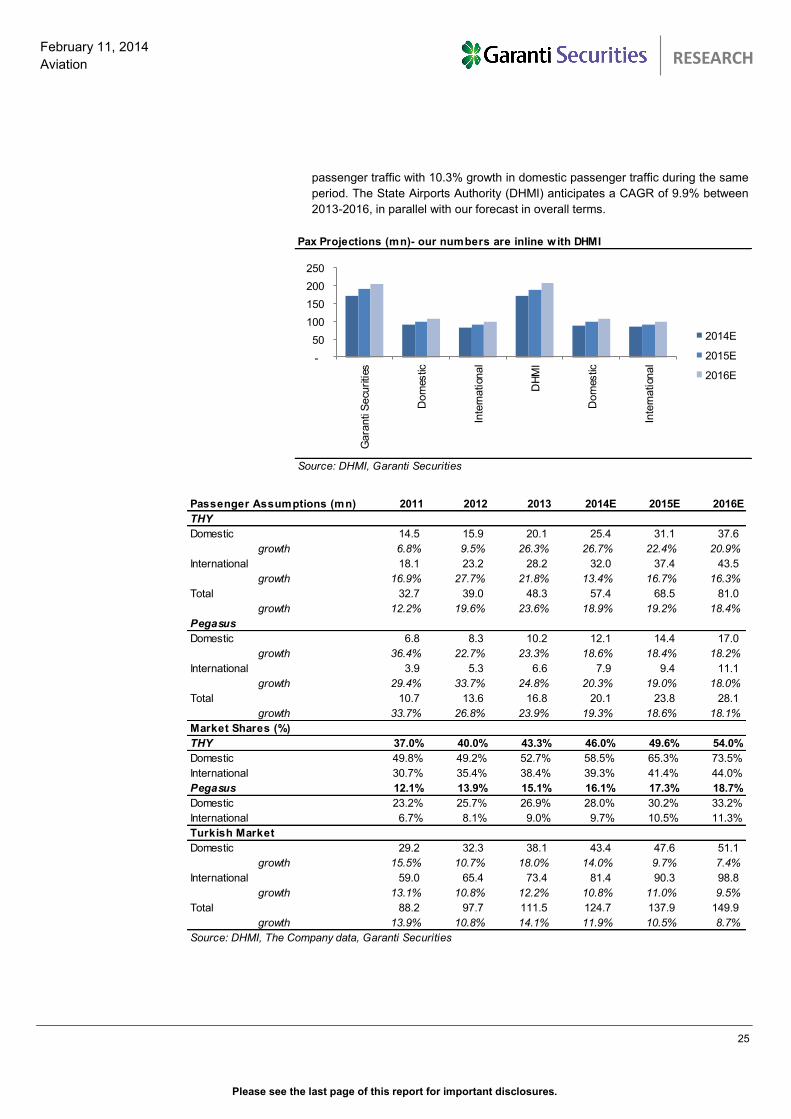

Our Passenger Forecasts 24

Airports in Turkey 26

Capacity Enhancement Studies 26

The Third Airport 29

Recent Developments in Turkish Aviation Sector 30

Airline Terminology 31

THY 32

Investment Positives 34

Investment Negatives 36

Valuation 38

Peer Comparison 38

Model Assumptions 40

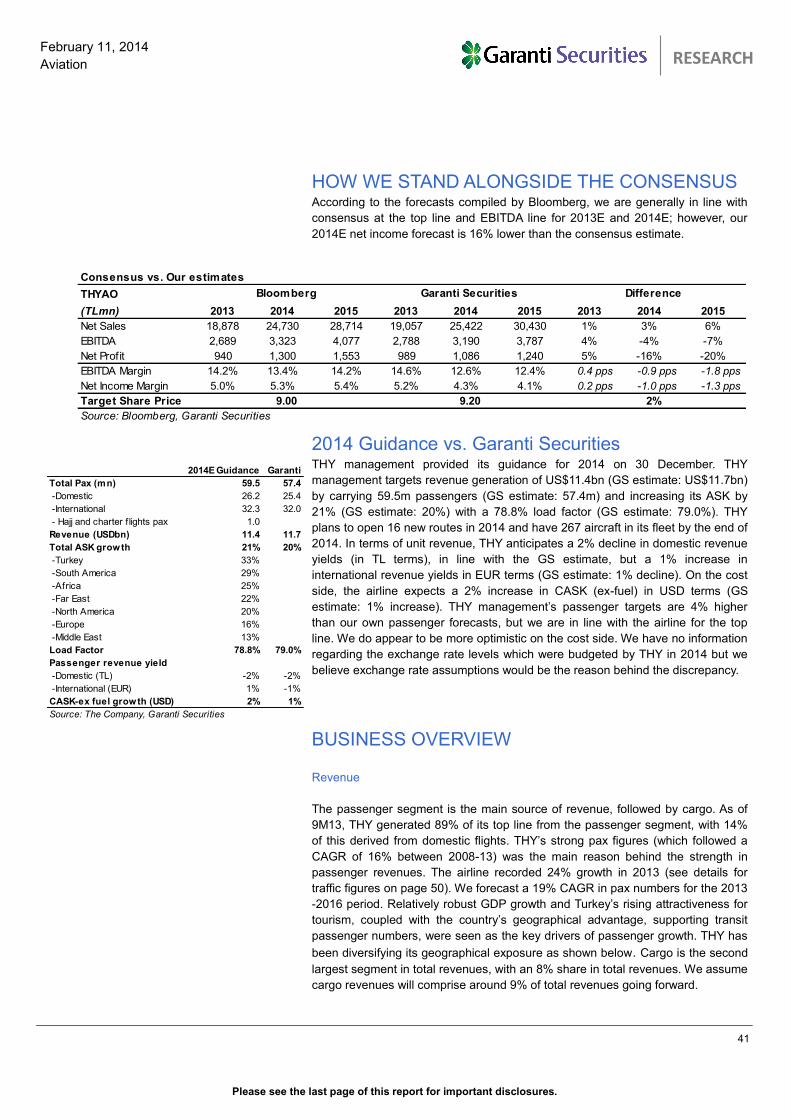

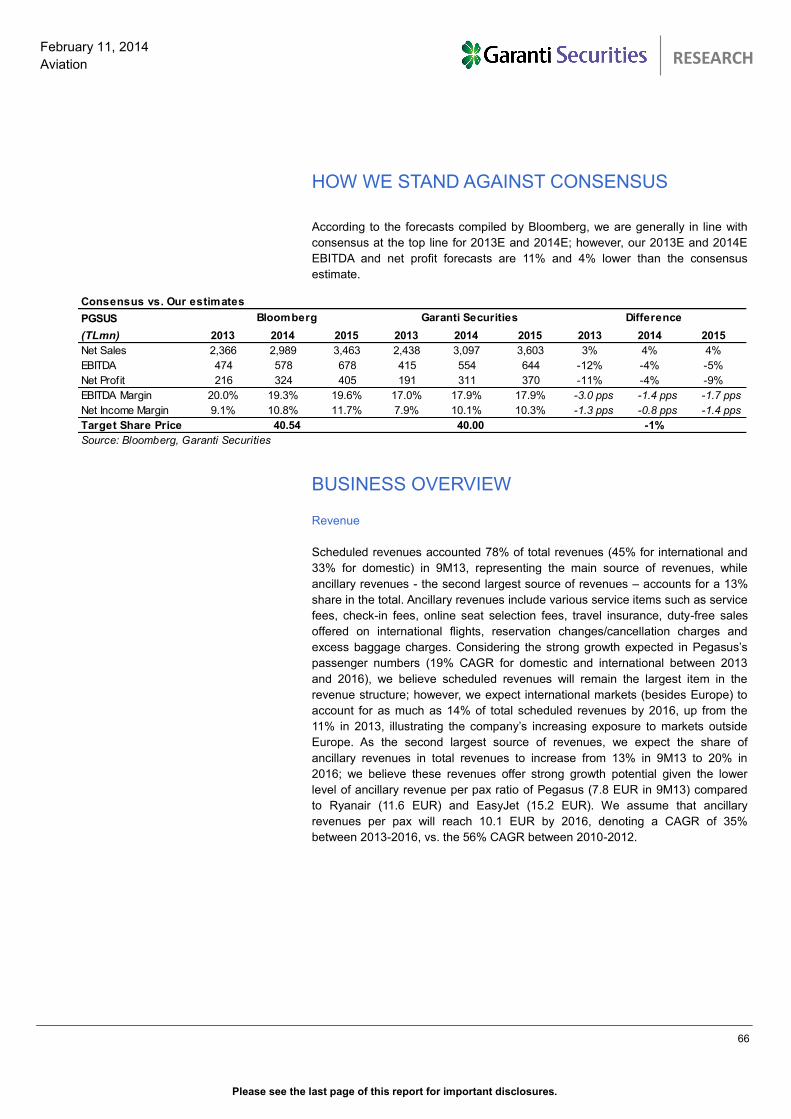

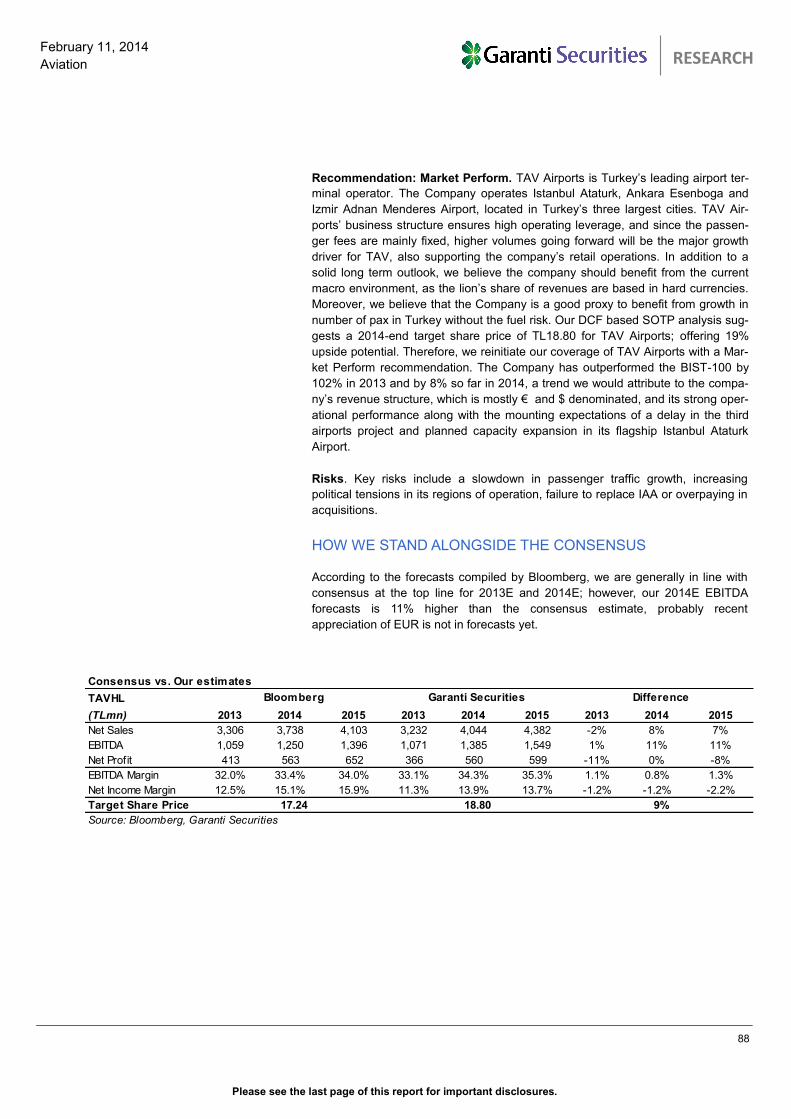

How we stand alongside the consensus 41

2014 Guidance vs. Garanti Securities 41

Bussiness Overview 41

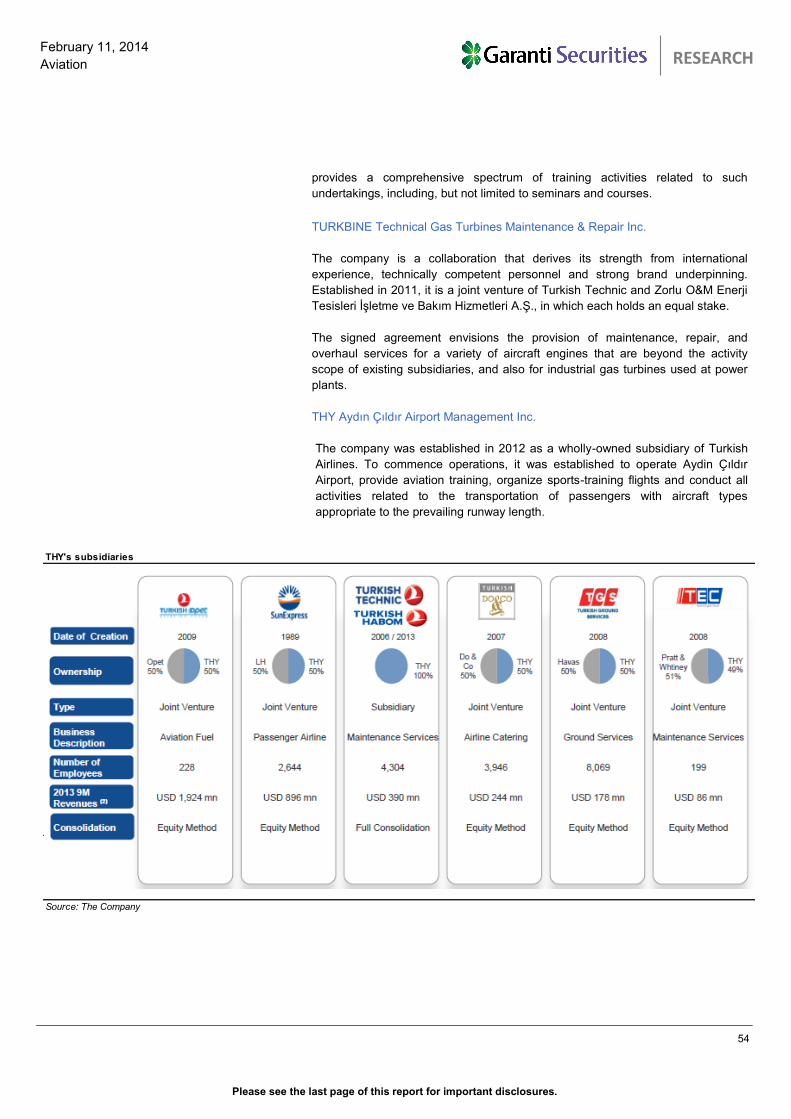

Recent Developments 49

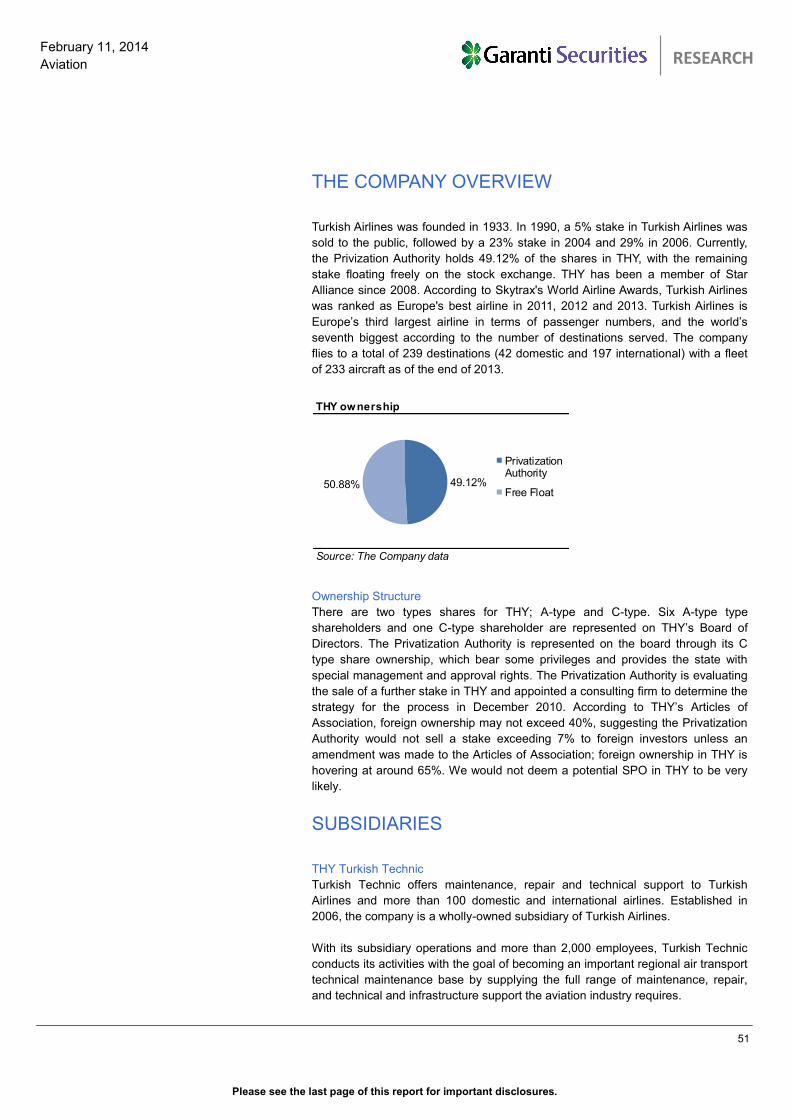

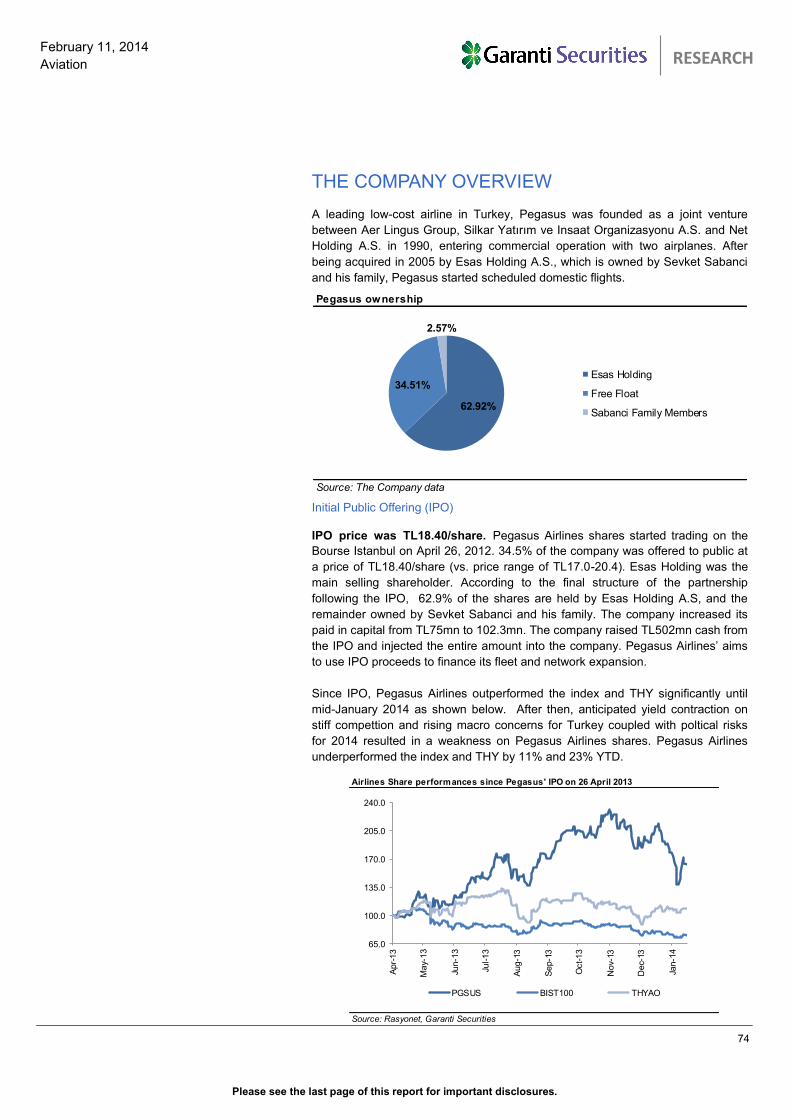

The Company Overview 51

The Company Profile 55

PE and EV/EBITDAR graphs 57

Pegasus 58

Investment Positives 60

Investment Negatives 61

Valuation 63

Peer Comparison 63

Model Assumptions 65

How we stand alongside the consensus 66

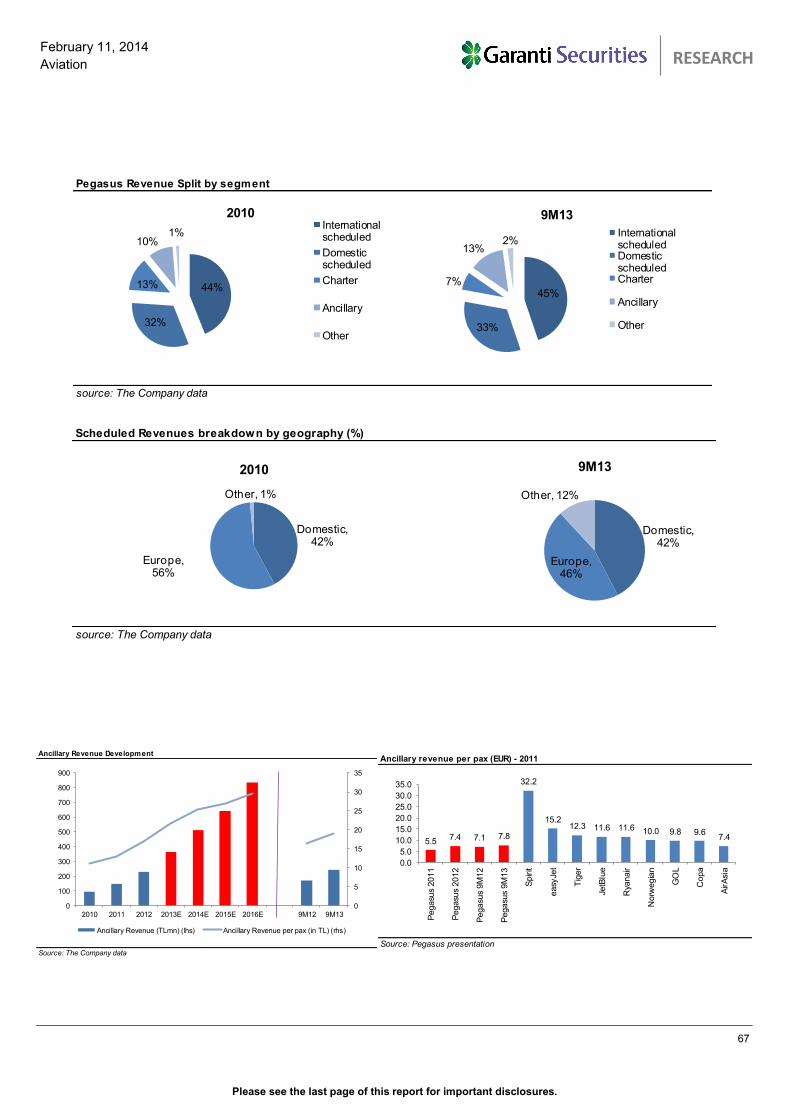

Bussiness Overview 66

The Company Overview 74

PE and EV/EBITDAR graphs 77

THY vs. Pegasus 80

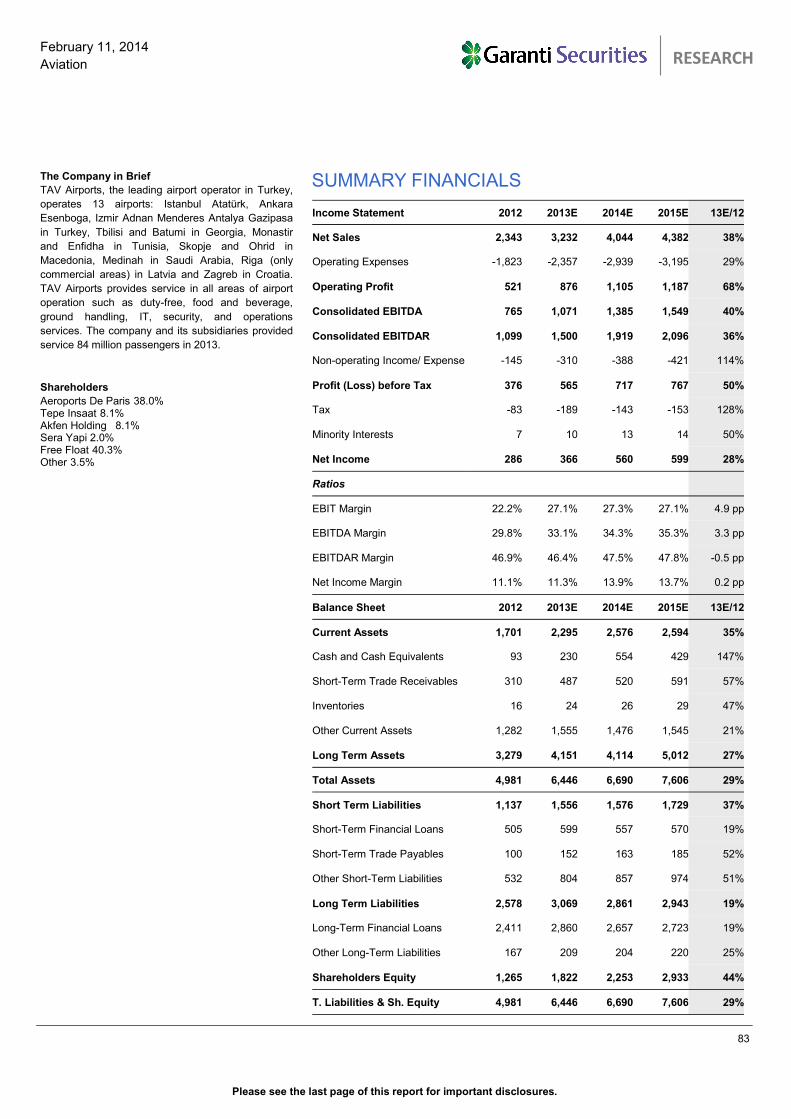

TAV 82

Investment Positives 84

Investment Negatives 85

Valuation 86

Peer Comparison 87

How we stand alongside the consensus 88

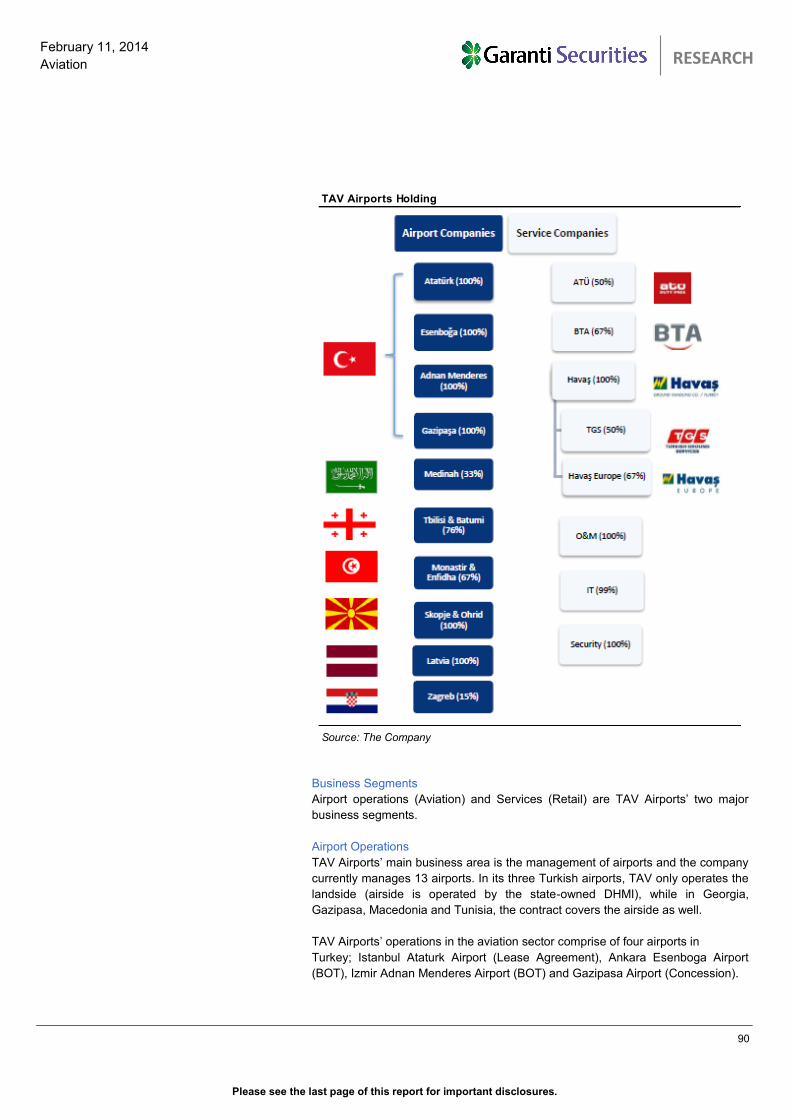

The Company Overview 89

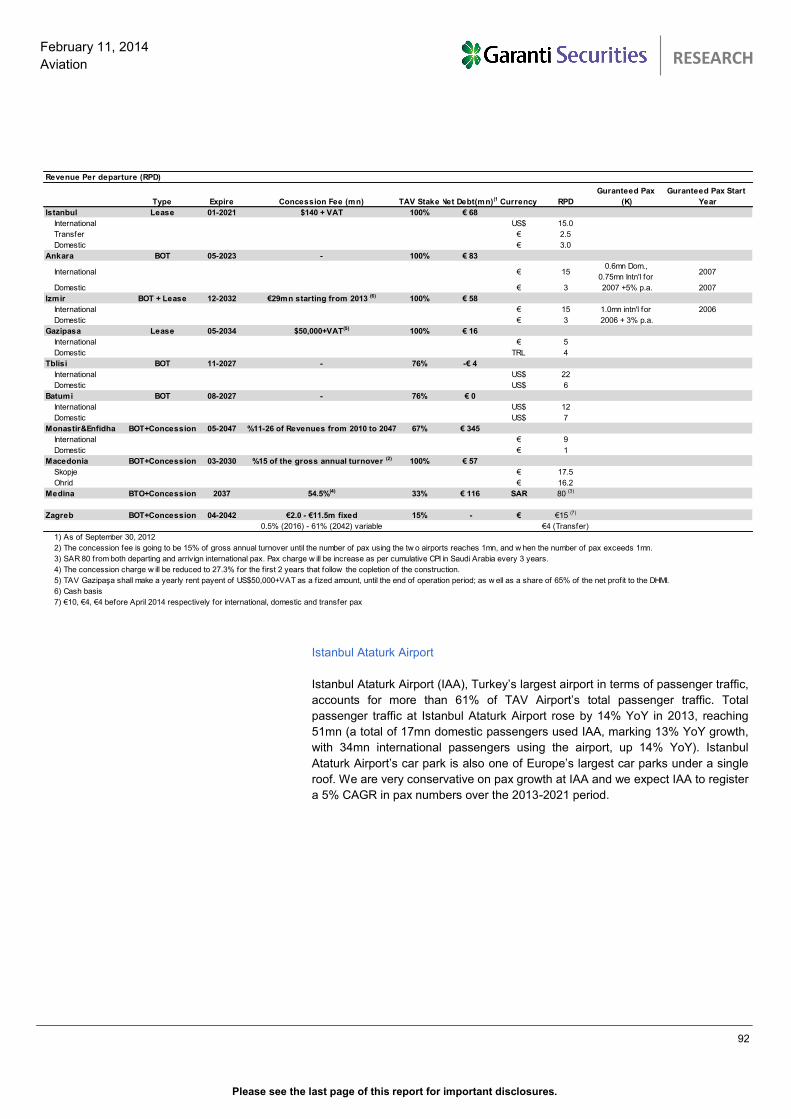

Key DCF Assumptions & Forecasts 91

The Company Profile 101

Disclaimer 105

Please see the last page of this report for important disclosures.

RESEARCH

Executive Summary

Strong traffic momentum since sector deregulation

Passenger numbers have risen at a CAGR of 16% in Turkey between 2003 and 2013, 3x the real GDP growth in the same period.

Even in 2009, when real GDP contracted by 5%, passenger numbers in Turkey expanded by 6%. We believe that Turkey’s

underpenetrated aviation market, its geographically advantageous position, the lack of alternative transportation infrastructure, its

increasing attractiveness as a tourism destination and the government’s supportive approach to the sector will help sustain this above

average growth. Only 1.2 flights are taken per capita in Turkey - half of the EU15 average. The ambitious fleet expansion plans of

Turkey’s two largest carriers’ to double their fleets in the next decade signal the anticipation of strong demand in the sector as well.

We project an 10% CAGR in Turkish air passenger traffic between 2013-2016.

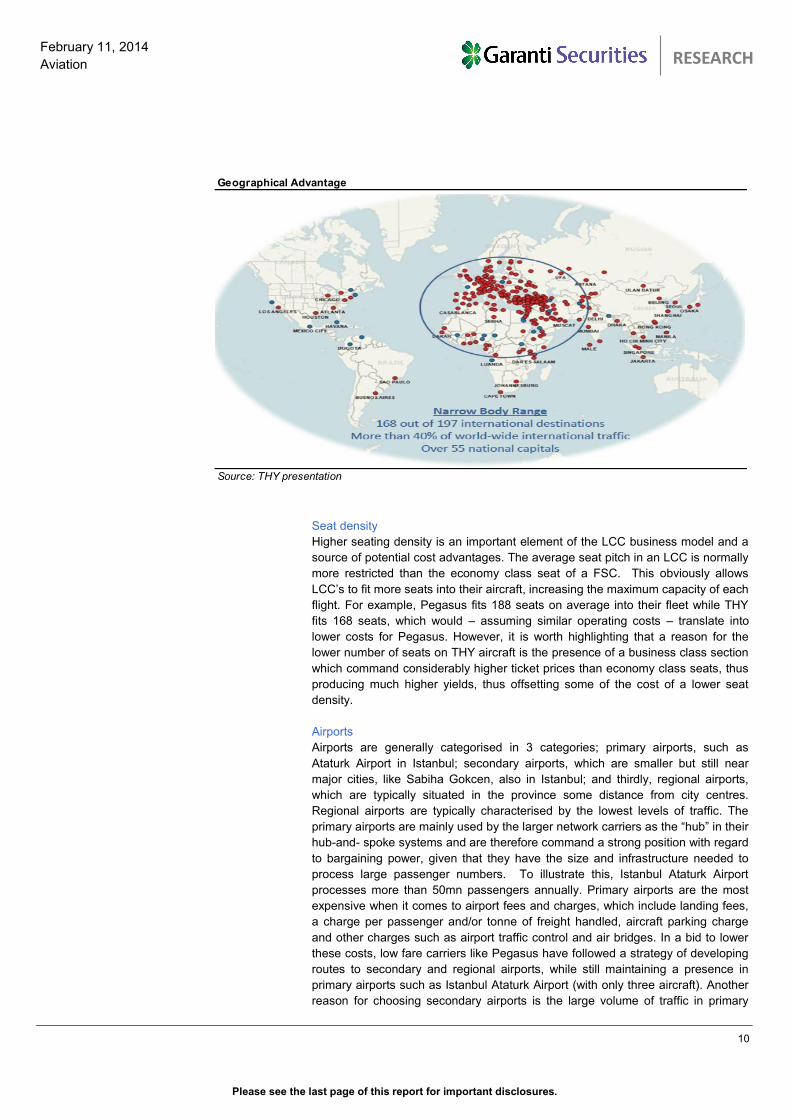

Turkey’s priceless geographical advantage

Although Gulf countries and Turkey are both well positioned to attract and distribute European passengers through Africa, Southern

Asia and the South Pacific thanks to their geographic advantage, Turkey’s position is within reach Europe, Africa and India with short-

haul flights from its Istanbul hub; however, the UAE and Qatar need wide-body aircraft to collect passengers from Europe to distribute

them to India, Southeast Asia and the Southern Pacific. However, more than 40% of world-wide international traffic from Turkey is

within the range of narrow body aircraft. Although the recently-placed massive aircraft orders by Gulf Carriers is likely to spell an

increase in competition in the region, we do not see the Gulf carriers as a major threat to Turkish Carriers. To illustrate this, THY’s

total pax numbers have grown at a CAGR of 16% over the past five years, compared to the 13% CAGR notched up by Emirates. The

deviation was more pronounced in 2013, when THY achieved 24% YoY growth vs. the 16% growth at Emirates.

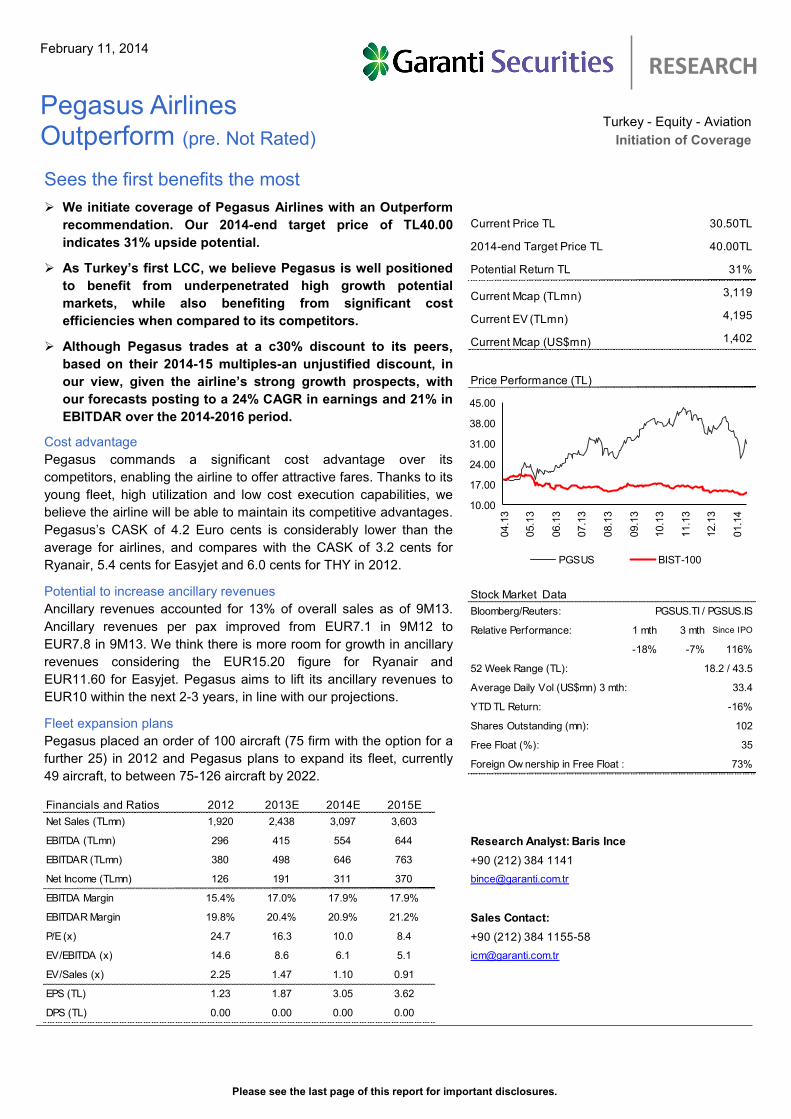

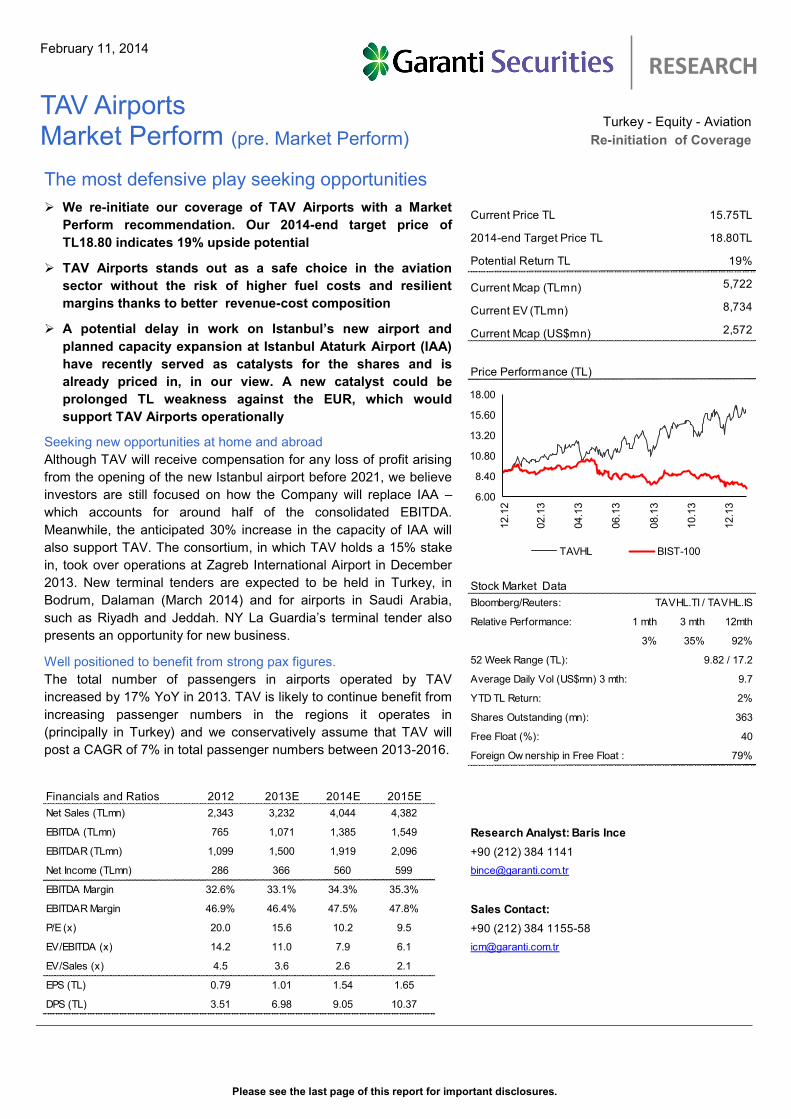

THY Outperform, Pegasus Outperform, TAV Market Perform

We reinitiate our coverage of the Turkish Aviation Sector with this report with Outperform ratings for Turkish Airlines (THYAO) and

Pegasus Airlines (PGSUS); Market Perform rating for TAV Airports (TAVHL). Our valuations for the airlines is based on 2014E target

EV/EBITDAR levels (6.3x for THY and 8.0x for Pegasus) while we value TAV through a sum-of-the parts (SOTP) valuation. On

multiple comparison side, THY and Pegasus trade at 8% and 30% discounts on the basis of their 2014 P/E multiples. THY appears

expensive on the basis of its 2014E EV/EBITDA, but it offers stronger revenue growth compared to peers. We do not rely on

comparisons for TAV, as we believe there is no perfect peer for the company given that the concession agreements differ.

Our preferred play is THY

We prefer THY over Pegasus on the back of i) having the lowest exposure to Turkey, given rising macro concerns for the time being

(domestic passengers constitute 41% of the total vs. 61% for Pegasus), ii) increasing competition from THY at Pegasus’s main hub

(Sabiha Gokcen Airport) and iii) Pegasus’s limited visibility on international expansion. We believe that capacity expansion at Ataturk

Airport and a potential delay in Istanbul’s new airport have recently served as catalysts for TAV shares and is now priced in . Aside

from ongoing political events, which could have a negative impact on growth, the current theme on Turkish Equities is exchange rate

volatility, and aviation stocks are no exception. We believe TAV is the least exposed to domestic macro concerns and the main

beneficiary of TL weakness, with Pegasus being relatively the most vulnerable. Bear in mind that TAV and Pegasus’s functional

currencies are EUR while that of THY is USD although all three report in TL.

Risks

A slowdown in passenger growth momentum, weaker than expected unit revenues or a deteriorating cost base are key risks for

airlines. In addition, failure to win new airport tenders or increasing political tension in the region where TAV operates in, as well as a

heavy dependence on Istanbul Ataturk Airport are considered as key risks for TAV. Specifically, a potential sale of the Privatization

Administration’s stake (49.12%) or a verdict in favour of Pegasus regarding its appeal to the Competition Board would lead to share

price weakness for THY.

February 11, 2014

TURKISH AVIATION SECTOR

Company Ticker Recomm. Mcap

3M Avg

Volume

Target

Price Upside

Revenue

CAGR

EBITDAR

CAGR

Net

Income

CAGR

EBITDAR

margin

(TLmn) (TLmn) (TL) 2014-2016E 2014-2016E 2014-2016E 2014E 2015E 2014E 2015E 2014E 3M YTD

Pegasus Airlines PGSUS Outperform 3,119 72 40.00 31% 18% 21% 24% 6.3 5.4 10.0 8.4 20.9% -7% -11%

Turkish Airlines THYAO Outperform 9,715 205 9.20 31% 20% 19% 17% 7.0 6.8 8.9 7.8 17.3% 9% 16%

TAV Airports TAVHL Market Perform 5,722 21 18.80 19% 10% 12% 11% 4.3 4.1 9.7 9.4 47.5% 35% 8%

Source: Garanti Securities

EV/EBITDAR P/E

BIST-100

Relative

Performances

Please see the last page of this report for important disclosures.

4

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

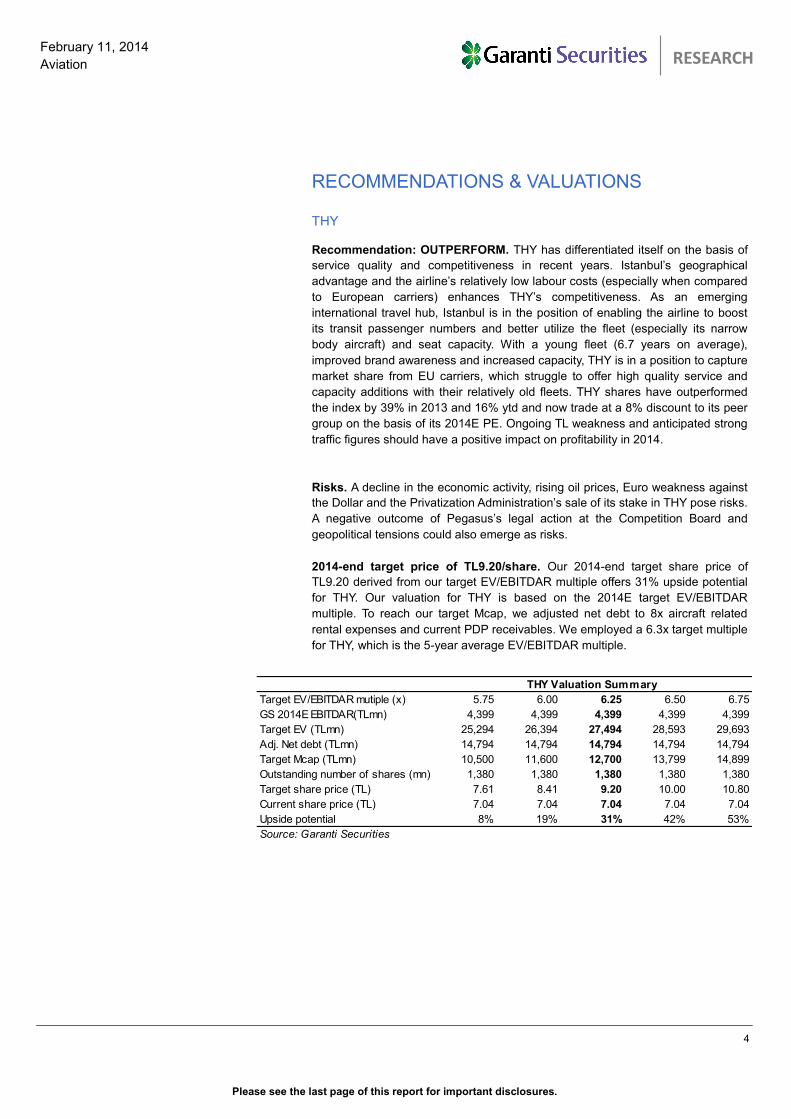

RECOMMENDATIONS & VALUATIONS THY

Recommendation: OUTPERFORM. THY has differentiated itself on the basis of

service quality and competitiveness in recent years. Istanbul’s geographical

advantage and the airline’s relatively low labour costs (especially when compared

to European carriers) enhances THY’s competitiveness. As an emerging

international travel hub, Istanbul is in the position of enabling the airline to boost

its transit passenger numbers and better utilize the fleet (especially its narrow

body aircraft) and seat capacity. With a young fleet (6.7 years on average),

improved brand awareness and increased capacity, THY is in a position to capture

market share from EU carriers, which struggle to offer high quality service and

capacity additions with their relatively old fleets. THY shares have outperformed

the index by 39% in 2013 and 16% ytd and now trade at a 8% discount to its peer

group on the basis of its 2014E PE. Ongoing TL weakness and anticipated strong

traffic figures should have a positive impact on profitability in 2014.

Risks. A decline in the economic activity, rising oil prices, Euro weakness against

the Dollar and the Privatization Administration’s sale of its stake in THY pose risks.

A negative outcome of Pegasus’s legal action at the Competition Board and

geopolitical tensions could also emerge as risks.

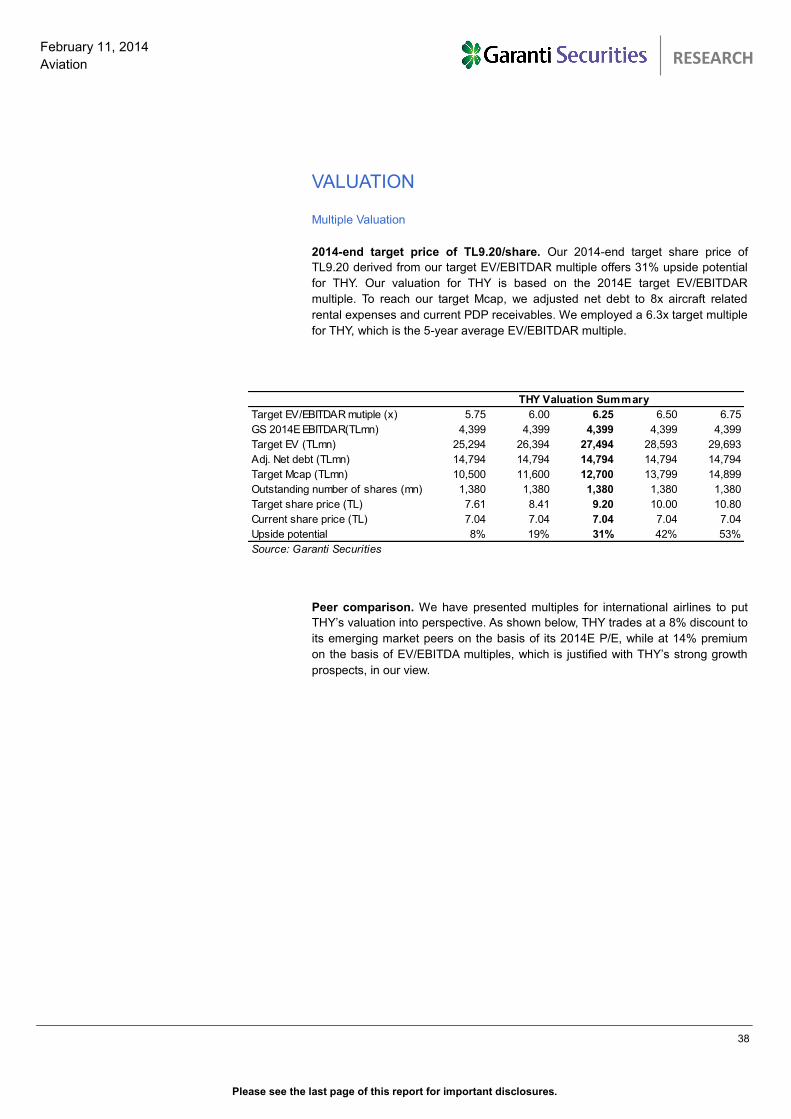

2014-end target price of TL9.20/share. Our 2014-end target share price of

TL9.20 derived from our target EV/EBITDAR multiple offers 31% upside potential

for THY. Our valuation for THY is based on the 2014E target EV/EBITDAR

multiple. To reach our target Mcap, we adjusted net debt to 8x aircraft related

rental expenses and current PDP receivables. We employed a 6.3x target multiple

for THY, which is the 5-year average EV/EBITDAR multiple.

Target EV/EBITDAR mutiple (x) 5.75 6.00 6.25 6.50 6.75

GS 2014E EBITDAR(TLmn) 4,399 4,399 4,399 4,399 4,399

Target EV (TLmn) 25,294 26,394 27,494 28,593 29,693

Adj. Net debt (TLmn) 14,794 14,794 14,794 14,794 14,794

Target Mcap (TLmn) 10,500 11,600 12,700 13,799 14,899

Outstanding number of shares (mn) 1,380 1,380 1,380 1,380 1,380

Target share price (TL) 7.61 8.41 9.20 10.00 10.80

Current share price (TL) 7.04 7.04 7.04 7.04 7.04

Upside potential 8% 19% 31% 42% 53%

Source: Garanti Securities

THY Valuation Summary

Please see the last page of this report for important disclosures.

5

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

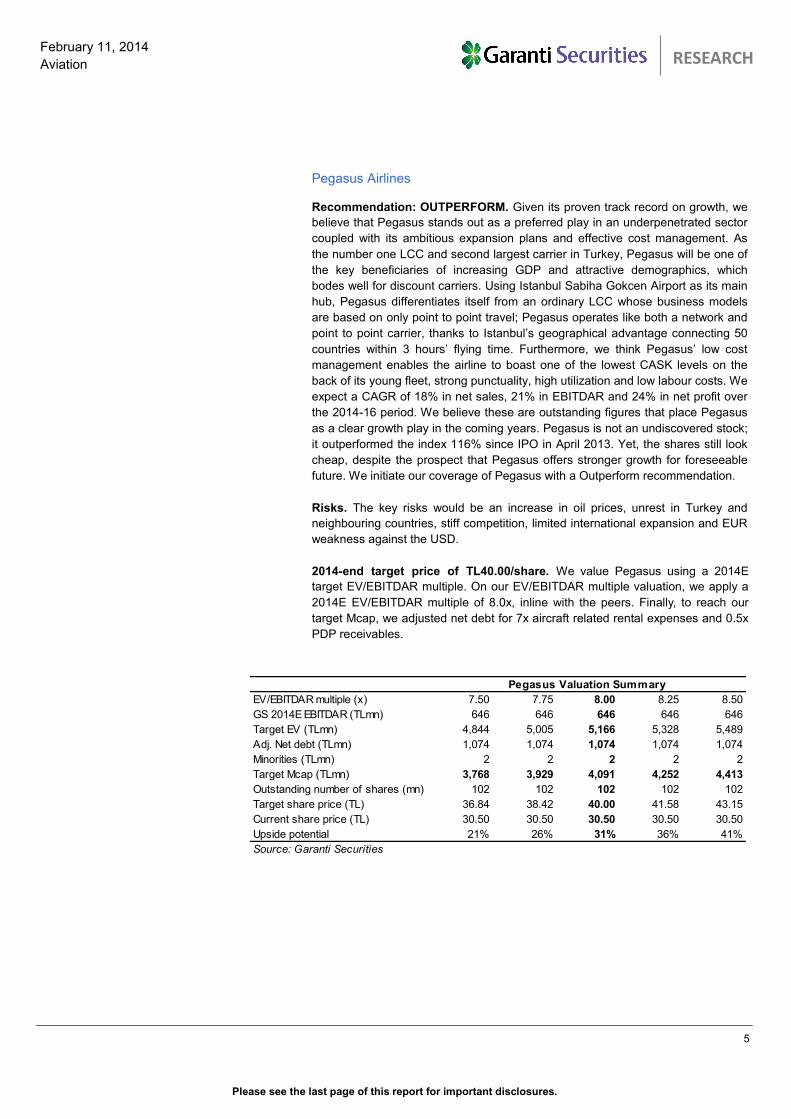

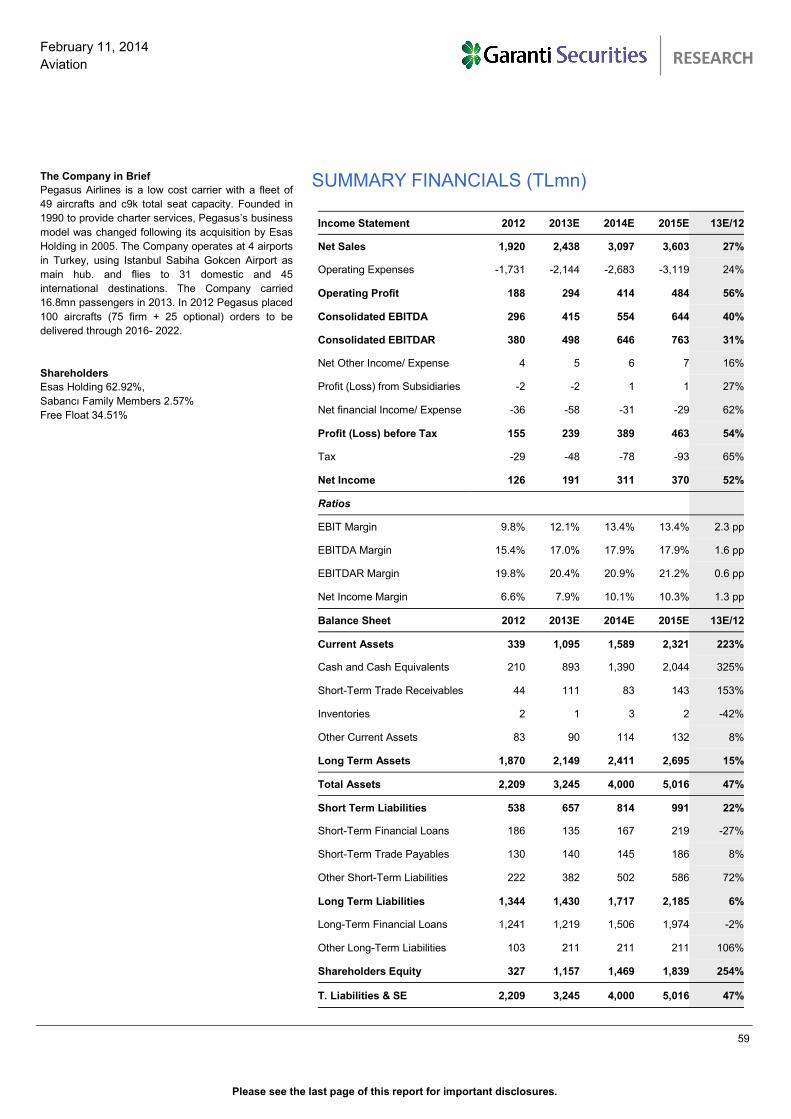

Pegasus Airlines

Recommendation: OUTPERFORM. Given its proven track record on growth, we

believe that Pegasus stands out as a preferred play in an underpenetrated sector

coupled with its ambitious expansion plans and effective cost management. As

the number one LCC and second largest carrier in Turkey, Pegasus will be one of

the key beneficiaries of increasing GDP and attractive demographics, which

bodes well for discount carriers. Using Istanbul Sabiha Gokcen Airport as its main

hub, Pegasus differentiates itself from an ordinary LCC whose business models

are based on only point to point travel; Pegasus operates like both a network and

point to point carrier, thanks to Istanbul’s geographical advantage connecting 50

countries within 3 hours’ flying time. Furthermore, we think Pegasus’ low cost

management enables the airline to boast one of the lowest CASK levels on the

back of its young fleet, strong punctuality, high utilization and low labour costs. We

expect a CAGR of 18% in net sales, 21% in EBITDAR and 24% in net profit over

the 2014-16 period. We believe these are outstanding figures that place Pegasus

as a clear growth play in the coming years. Pegasus is not an undiscovered stock;

it outperformed the index 116% since IPO in April 2013. Yet, the shares still look

cheap, despite the prospect that Pegasus offers stronger growth for foreseeable

future. We initiate our coverage of Pegasus with a Outperform recommendation.

Risks. The key risks would be an increase in oil prices, unrest in Turkey and

neighbouring countries, stiff competition, limited international expansion and EUR

weakness against the USD.

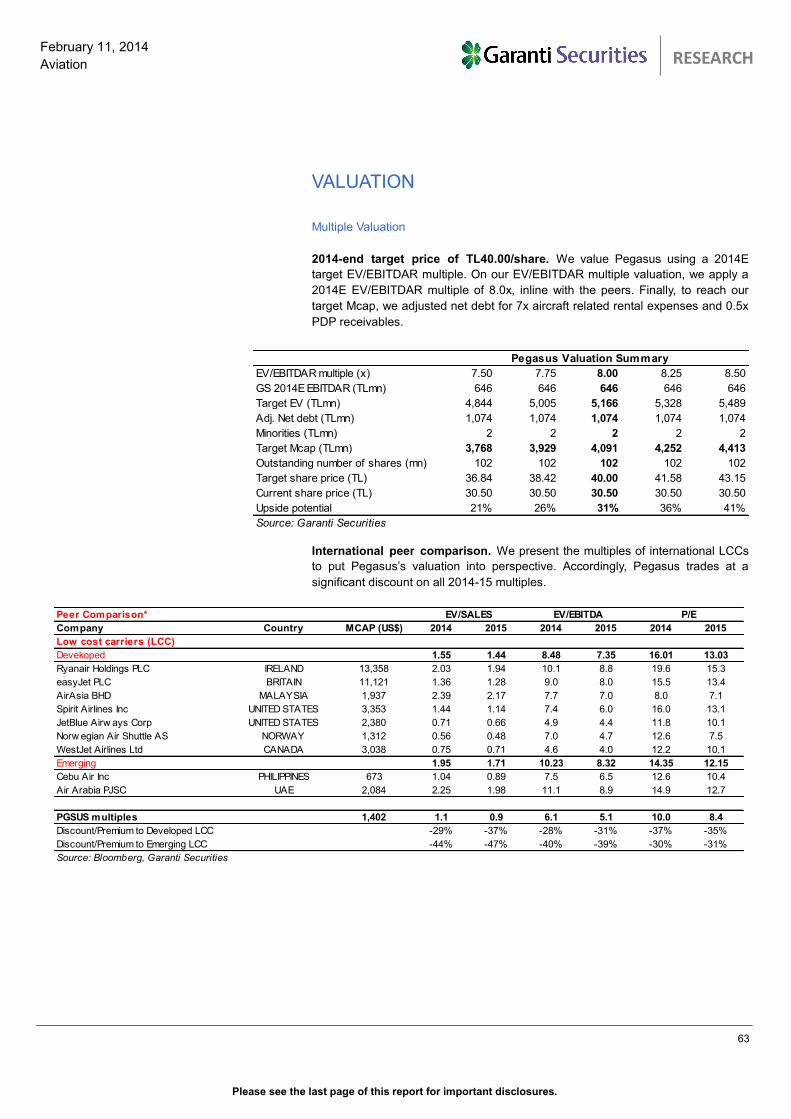

2014-end target price of TL40.00/share. We value Pegasus using a 2014E

target EV/EBITDAR multiple. On our EV/EBITDAR multiple valuation, we apply a

2014E EV/EBITDAR multiple of 8.0x, inline with the peers. Finally, to reach our

target Mcap, we adjusted net debt for 7x aircraft related rental expenses and 0.5x

PDP receivables.

EV/EBITDAR multiple (x) 7.50 7.75 8.00 8.25 8.50

GS 2014E EBITDAR (TLmn) 646 646 646 646 646

Target EV (TLmn) 4,844 5,005 5,166 5,328 5,489

Adj. Net debt (TLmn) 1,074 1,074 1,074 1,074 1,074

Minorities (TLmn) 2 2 2 2 2

Target Mcap (TLmn) 3,768 3,929 4,091 4,252 4,413

Outstanding number of shares (mn) 102 102 102 102 102

Target share price (TL) 36.84 38.42 40.00 41.58 43.15

Current share price (TL) 30.50 30.50 30.50 30.50 30.50

Upside potential 21% 26% 31% 36% 41%

Source: Garanti Securities

Pegasus Valuation Summary

Please see the last page of this report for important disclosures.

6

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

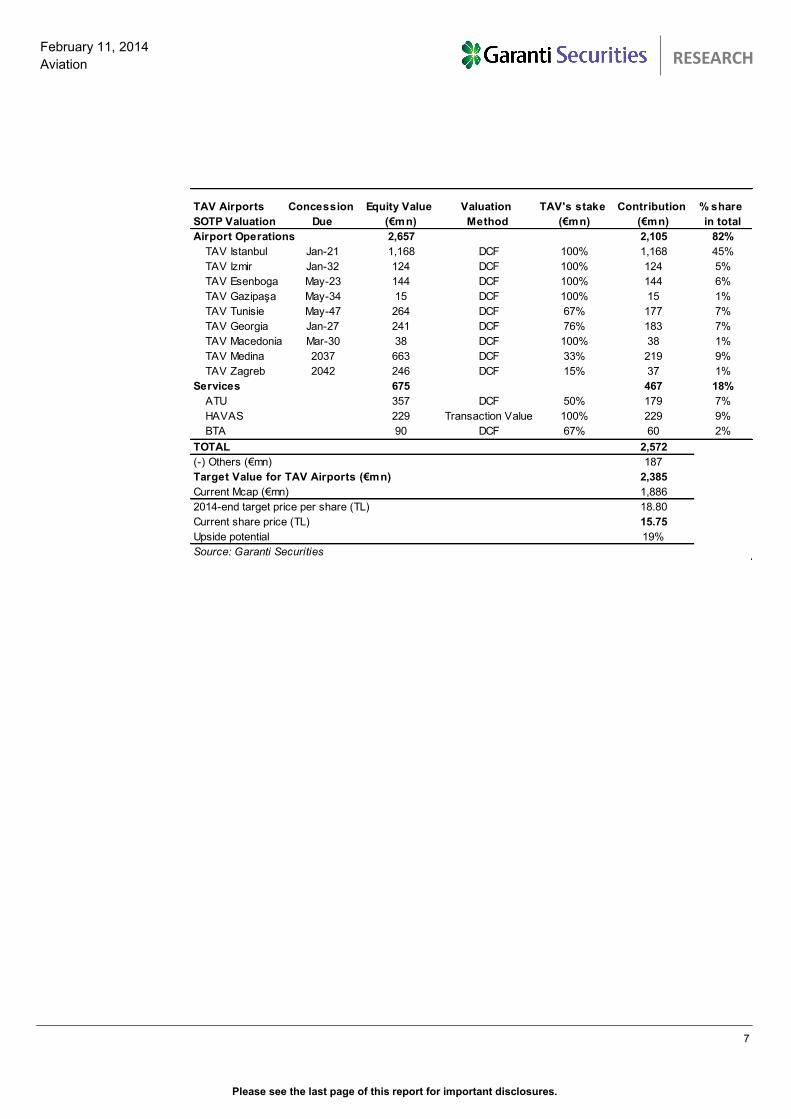

TAV Airports

Recommendation: Market Perform. TAV Airports is Turkey’s leading airport

terminal operator. The Company operates Istanbul Ataturk, Ankara Esenboga and

Izmir Adnan Menderes Airport, located in Turkey’s three largest cities. TAV

Airports’ business structure ensures high operating leverage, and since the

passenger fees are mainly fixed, higher volumes going forward will be the major

growth driver for TAV, also supporting the company’s retail operations. In addition

to a solid long term outlook, we believe the company should benefit from the

current macro environment, as the lion’s share of revenues are based in hard

currencies. Moreover, we believe that the Company is a good proxy to benefit

from growth in number of pax in Turkey without the fuel risk. The Company has

outperformed the BIST-100 by 102% in 2013 and by 8% so far in 2014, a trend we

would attribute to the company’s revenue structure, which is mostly € and $

denominated, and its strong operational performance along with the mounting

expectations of a delay in the third airports project and planned capacity

expansion in its flagship Istanbul Ataturk Airport.

Risks. Key risks include a slowdown in passenger traffic growth, increasing

political tensions in its regions of operation, failure to replace IAA or overpaying in

acquisitions.

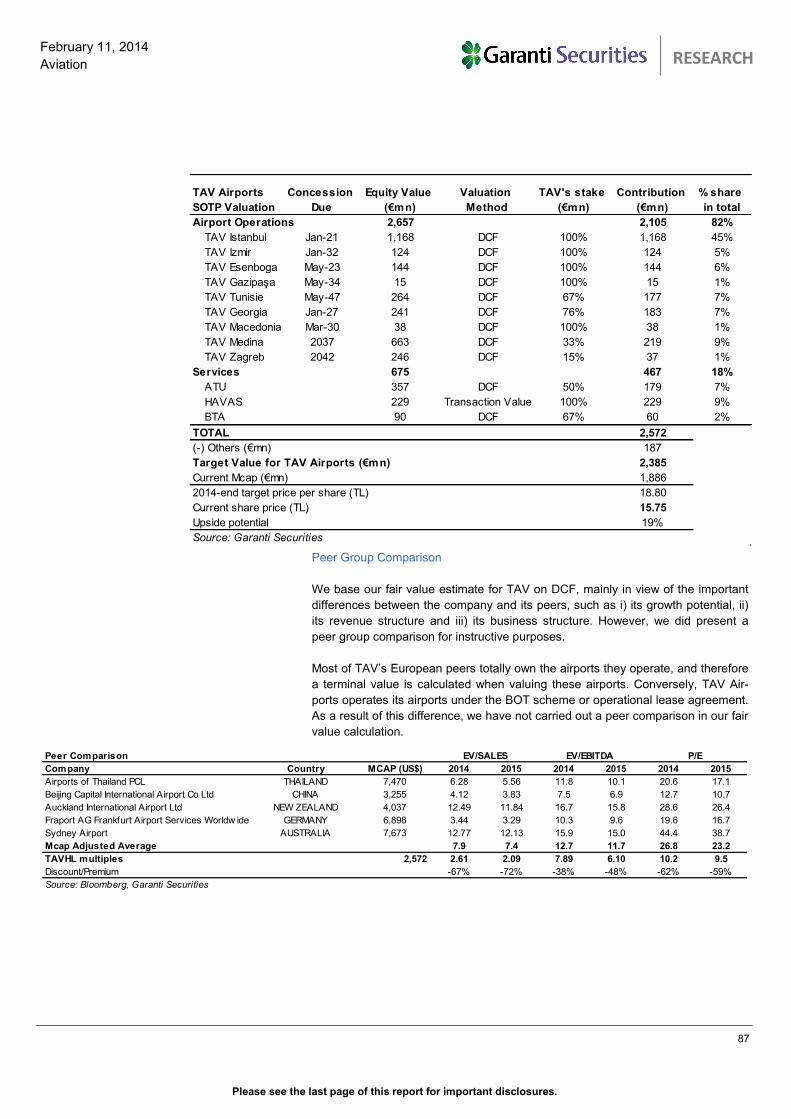

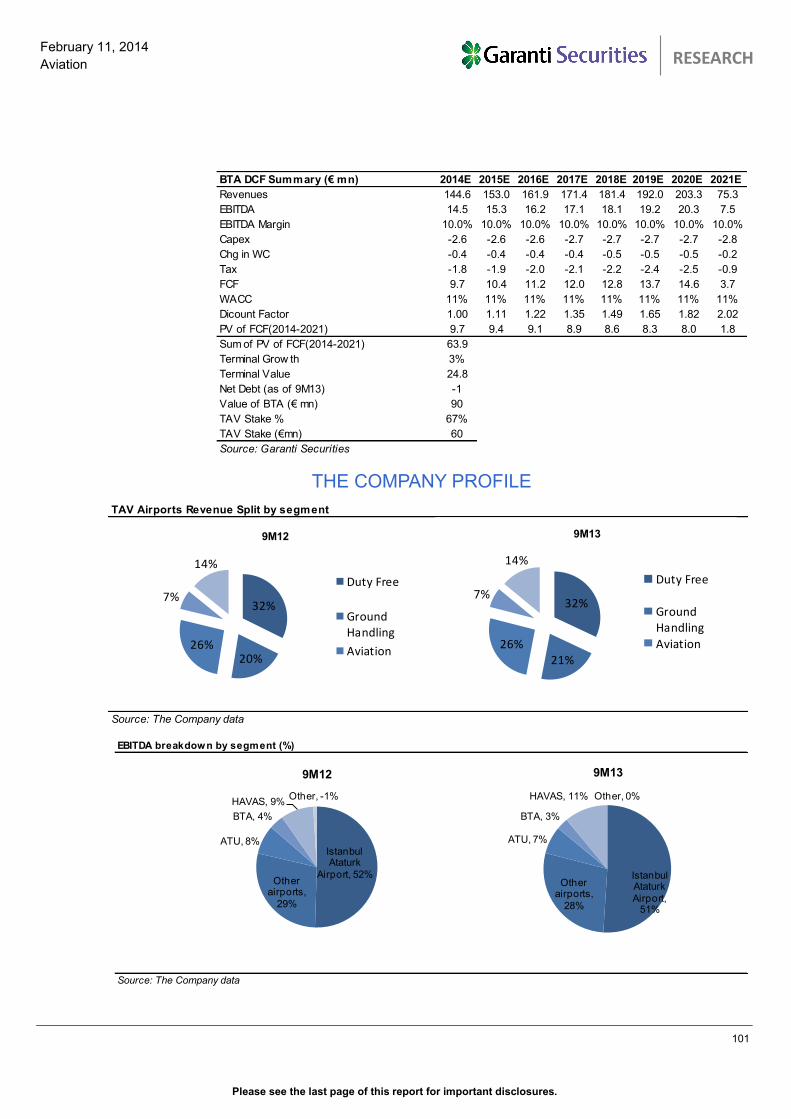

2014-end target price of TL18.80/share. We value TAV Airports using sum-of

the parts (SOTP) analysis based on target Net Asset Value (NAV). We employed

DCF analysis to value each of the Company’s operations separately. Our

valuation is solely based on DCF, as we believe DCF analysis is the most

appropriate means of reflecting TAV Airports’ long-term growth potential as well as

TAV Airports’ well designed structure. We only valued TAV Airports’ existing

airport operations, not taking into account any terminal value and assuming that

the Company would neither win any new tenders, nor would it be awarded another

term upon expiry of its current concession agreements. On the other hand, as the

services companies’ operations will not end with the expiry of operating rights at

the airports, we did include a terminal value in calculating the value of the services

companies. We put HAVAS to our valuation on its transaction value in late 2012.

TAV had paid EUR80mn for 35% of HAVAS at that time.

Please see the last page of this report for important disclosures.

7

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

TAV Airports

SOTP Valuation

Concession

Due

Equity Value

(€mn)

Valuation

Method

TAV's stake

(€mn)

Contribution

(€mn)

% share

in total

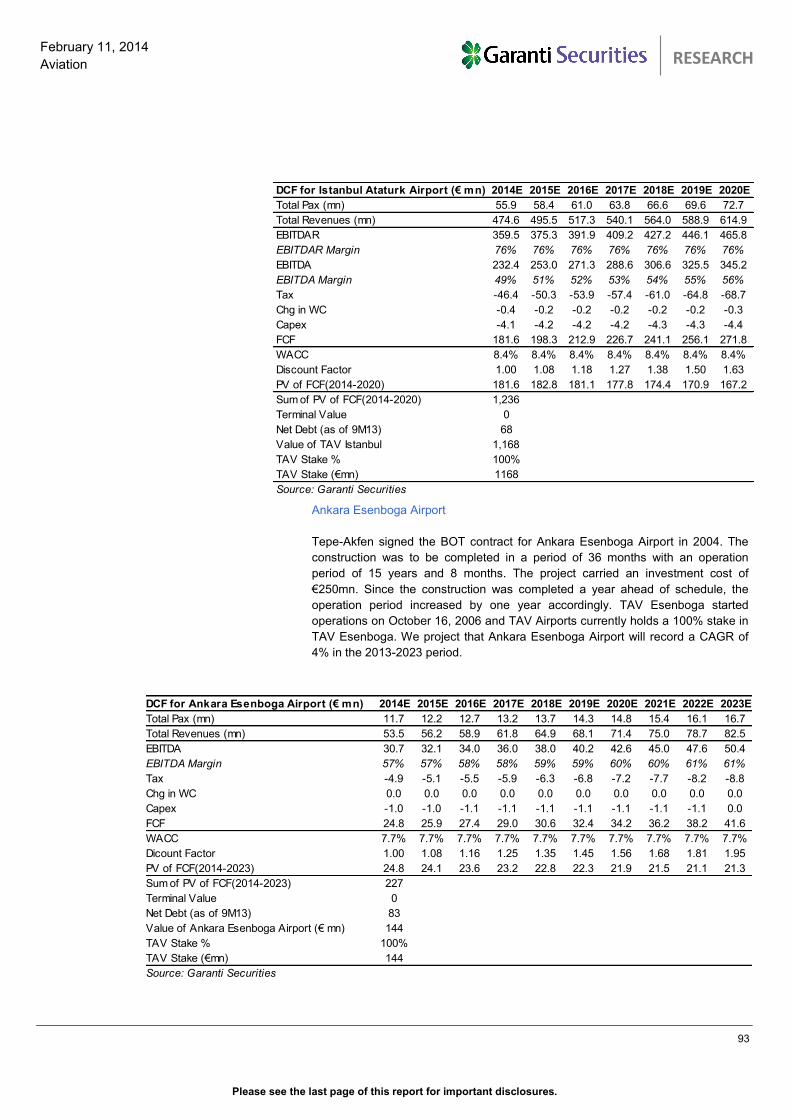

Airport Operations 2,657 2,105 82%

TAV Istanbul Jan-21 1,168 DCF 100% 1,168 45%

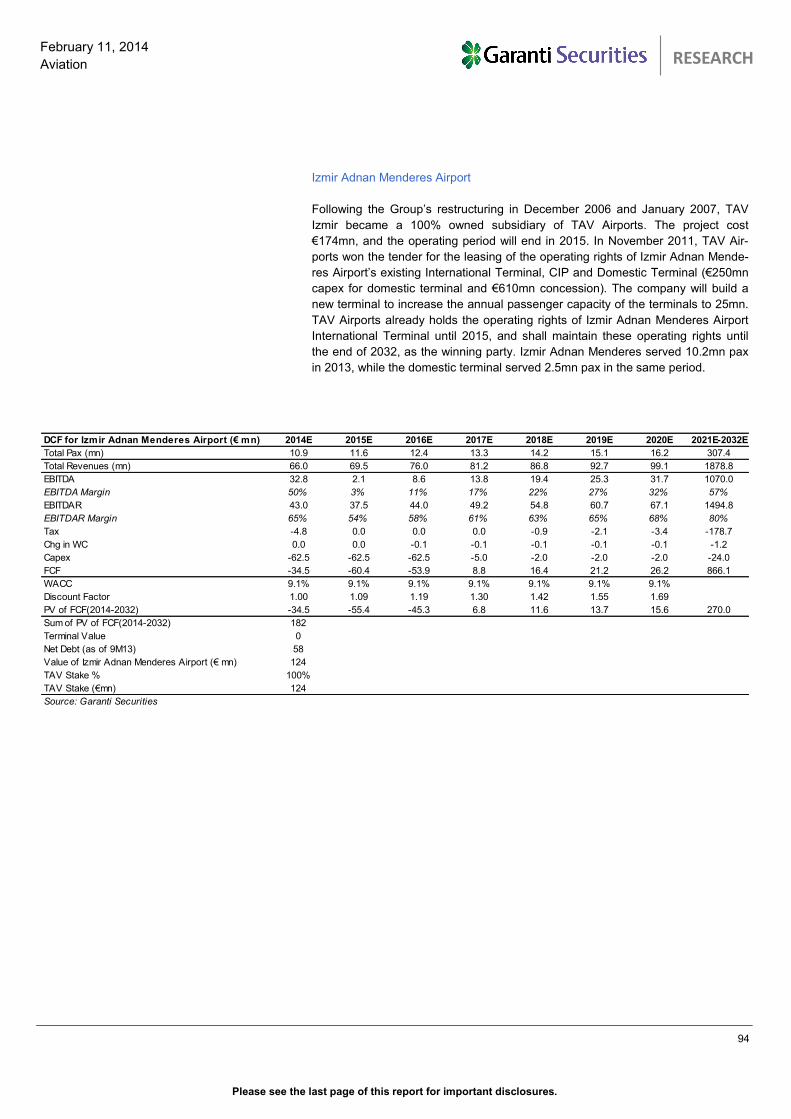

TAV Izmir Jan-32 124 DCF 100% 124 5%

TAV Esenboga May-23 144 DCF 100% 144 6%

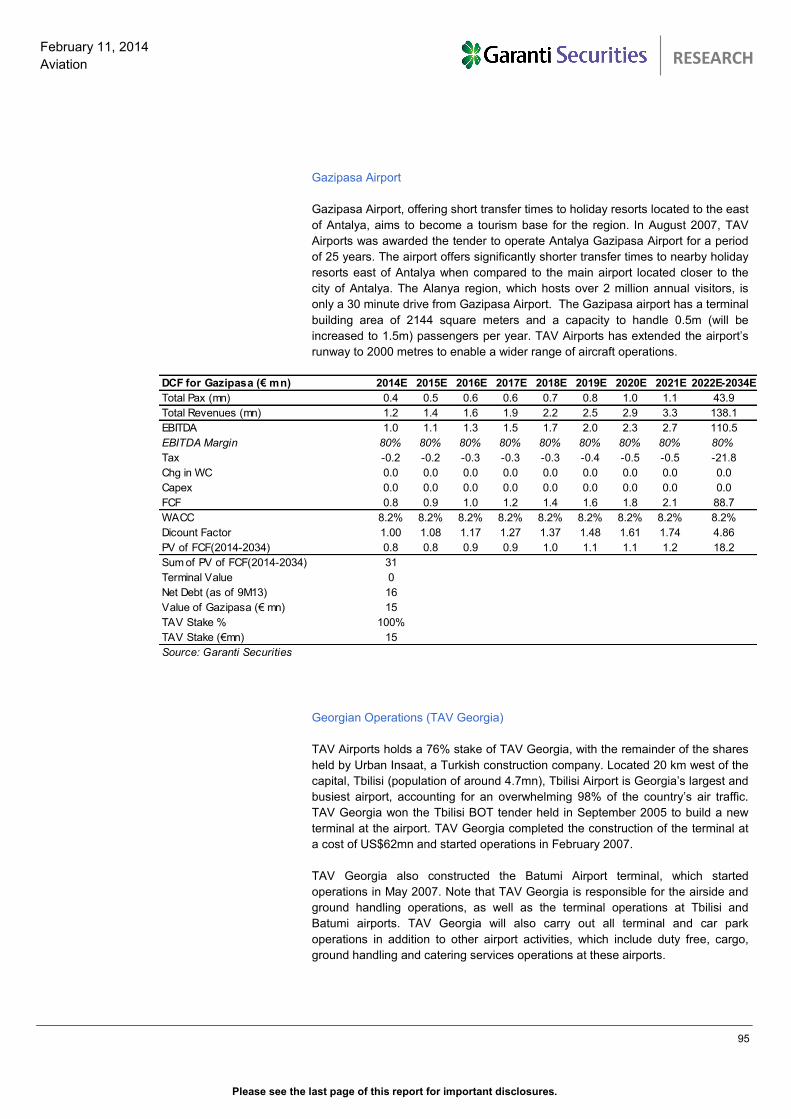

TAV Gazipaşa May-34 15 DCF 100% 15 1%

TAV Tunisie May-47 264 DCF 67% 177 7%

TAV Georgia Jan-27 241 DCF 76% 183 7%

TAV Macedonia Mar-30 38 DCF 100% 38 1%

TAV Medina 2037 663 DCF 33% 219 9%

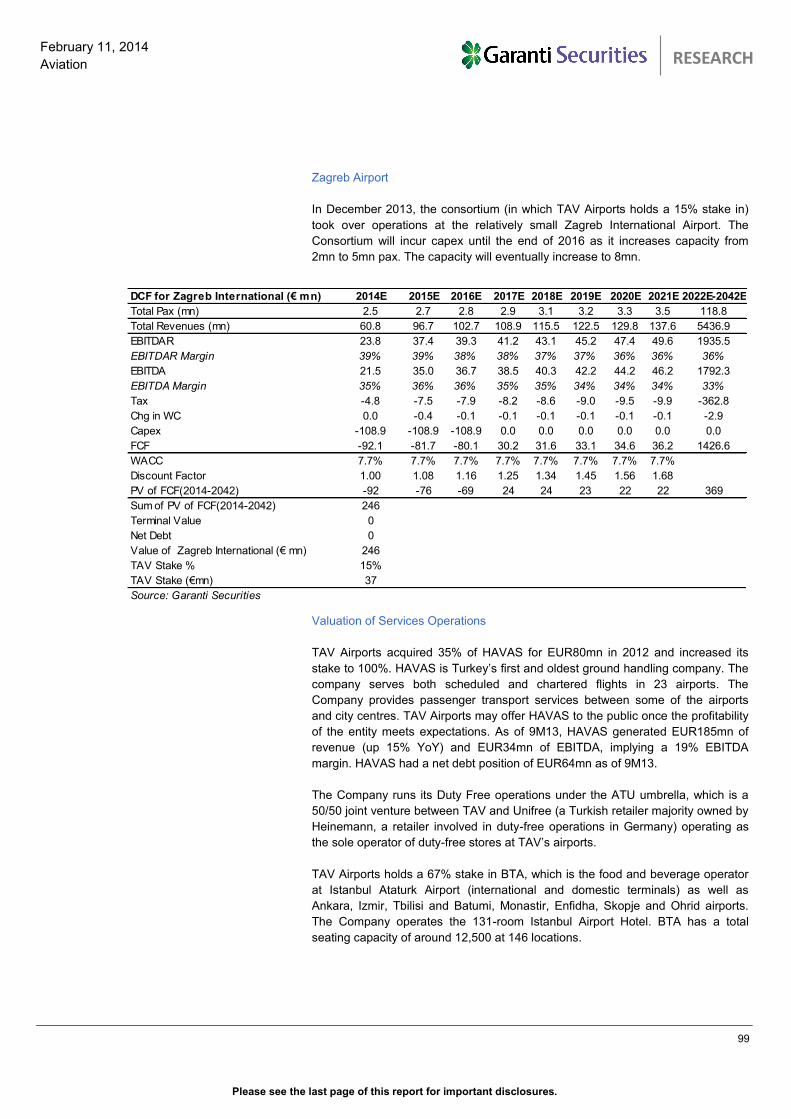

TAV Zagreb 2042 246 DCF 15% 37 1%

Services 675 467 18%

ATU 357 DCF 50% 179 7%

HAVAS 229 Transaction Value 100% 229 9%

BTA 90 DCF 67% 60 2%

TOTAL 2,572

(-) Others (€mn) 187

Target Value for TAV Airports (€mn) 2,385

Current Mcap (€mn) 1,886

2014-end target price per share (TL) 18.80

Current share price (TL) 15.75

Upside potential 19%

Source: Garanti Securities

Please see the last page of this report for important disclosures.

8

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

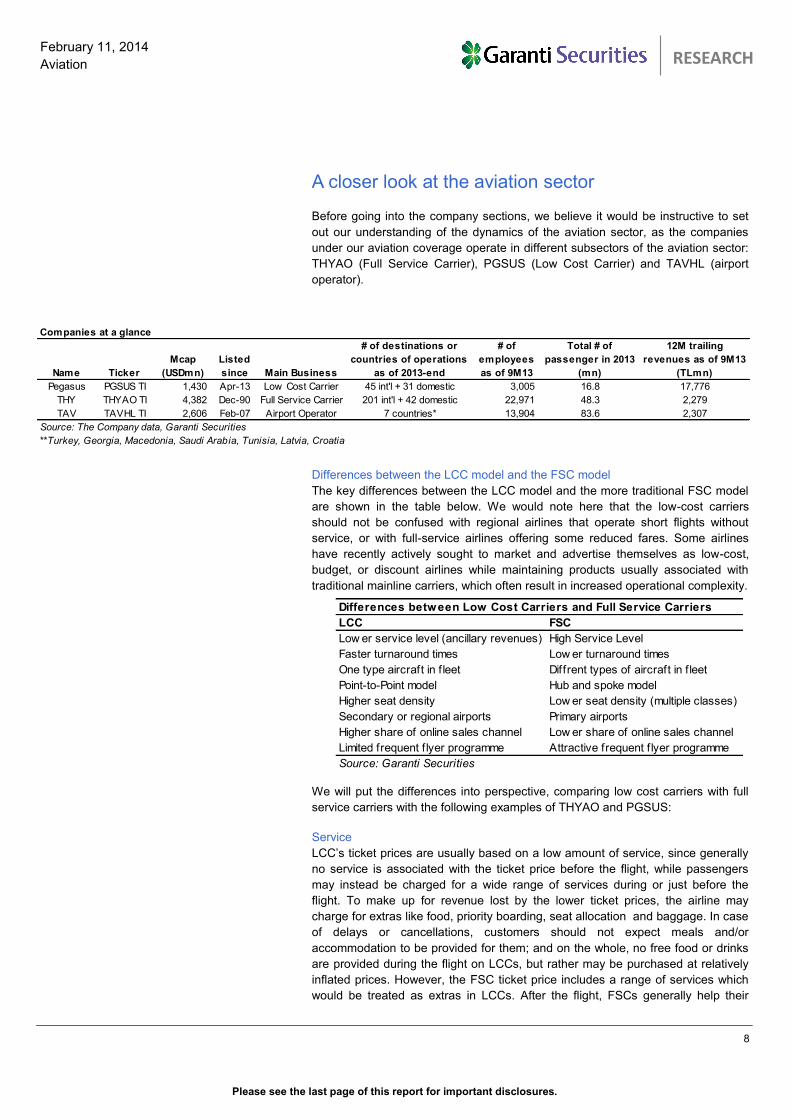

A closer look at the aviation sector

Before going into the company sections, we believe it would be instructive to set

out our understanding of the dynamics of the aviation sector, as the companies

under our aviation coverage operate in different subsectors of the aviation sector:

THYAO (Full Service Carrier), PGSUS (Low Cost Carrier) and TAVHL (airport

operator).

Differences between the LCC model and the FSC model

The key differences between the LCC model and the more traditional FSC model

are shown in the table below. We would note here that the low-cost carriers

should not be confused with regional airlines that operate short flights without

service, or with full-service airlines offering some reduced fares. Some airlines

have recently actively sought to market and advertise themselves as low-cost,

budget, or discount airlines while maintaining products usually associated with

traditional mainline carriers, which often result in increased operational complexity.

We will put the differences into perspective, comparing low cost carriers with full

service carriers with the following examples of THYAO and PGSUS:

Service

LCC’s ticket prices are usually based on a low amount of service, since generally

no service is associated with the ticket price before the flight, while passengers

may instead be charged for a wide range of services during or just before the

flight. To make up for revenue lost by the lower ticket prices, the airline may

charge for extras like food, priority boarding, seat allocation and baggage. In case

of delays or cancellations, customers should not expect meals and/or

accommodation to be provided for them; and on the whole, no free food or drinks

are provided during the flight on LCCs, but rather may be purchased at relatively

inflated prices. However, the FSC ticket price includes a range of services which

would be treated as extras in LCCs. After the flight, FSCs generally help their

Differences between Low Cost Carriers and Full Service Carriers

LCC FSC

Low er service level (ancillary revenues) High Service Level

Faster turnaround times Low er turnaround times

One type aircraft in f leet Diffrent types of aircraft in f leet

Point-to-Point model Hub and spoke model

Higher seat density Low er seat density (multiple classes)

Secondary or regional airports Primary airports

Higher share of online sales channel Low er share of online sales channel

Limited frequent f lyer programme Attractive frequent f lyer programme

Source: Garanti Securities

Companies at a glance

Name Ticker

Mcap

(USDmn)

Listed

since Main Business

# of destinations or

countries of operations

as of 2013-end

# of

employees

as of 9M13

Total # of

passenger in 2013

(mn)

12M trailing

revenues as of 9M13

(TLmn)

Pegasus PGSUS TI 1,430 Apr-13 Low Cost Carrier 45 int'l + 31 domestic 3,005 16.8 17,776

THY THYAO TI 4,382 Dec-90 Full Service Carrier 201 int'l + 42 domestic 22,971 48.3 2,279

TAV TAVHL TI 2,606 Feb-07 Airport Operator 7 countries* 13,904 83.6 2,307

Source: The Company data, Garanti Securities

**Turkey, Georgia, Macedonia, Saudi Arabia, Tunisia, Latvia, Croatia

Please see the last page of this report for important disclosures.

9

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

customers with connecting flights, transport to the city center or hotels, baggage

and in other areas, while LCCs generally would not.

Turnaround

LCC’s generally aim for low turnaround times; typically the flight schedules only

allow for less than an hour for the turnaround. This leaves only a short period of

time for passengers to disembark, baggage to be offloaded and boarding to be

complete with a new load of passengers and baggage to be completely loaded.

The fact that LCCs do not use air bridges also helps speed up this process as

passengers walk straight out of the aircraft as the stairs pull up beside the aircraft

and passengers can use both the front and back exits. As these airlines do not

serve free food and drink on-board, this also speeds up the turnaround between

flights as the cabin crew is only required to perform a quick cleaning during stops;

a thorough clean is only carried out at night. This cannot be done on full service

airlines. The low turnaround time also means that LCC’s are able to increase their

daily aircraft utilisation, in what can be considered as one of the main cost

advantages over full service airlines, as LCC’s are then obviously able to carry out

more round trips between a given city pair than an airline with longer turnaround

times. As of 2013, Pegasus’ turns per day stood at 7.4 vs. THY’s 4.5 according to

our calculations.

Fleet

LCC’s are generally pursuing a strategy of a homogenous fleet with only one type

of aircraft, enabling important cost savings with respect to pilot training and

maintenance. FSC’s are of course forced to use a mixed fleet, operating both

short-haul and long-haul flights, in contrast with LCC’s. PGSUS’s fleet is currently

composed entirely of Boeing 737-800s but the airline will shift to Airbus from 2016,

when the airline will start to receive deliveries from its 100 Airbus orders in 2H16.

On the other hand, THYAO has a range of aircraft in its fleet (45% being Boeing

49% Airbus at the end of 2013).

Point-to-point or hub-and-spoke

Point-to-point and hub-and-spoke terms stand out as one of the main differences

between LCC’s and FSC’s. Point-to-point travel basically means that the airline is

only responsible for carrying you between two points, and is usually applied by

LCC’s as it minimizes connections and travel time. In addition, given the lack of

interdependency of flights and hubs, a delayed flight or a closed airport will not

significantly affect other flight schedules. On the other hand, FSC’s tend to

operate a hub and spoke model, consisting of a hub (usually the primary airport)

and spokes, which are secondary airports that feed the hub with passengers in

order to fill the aircraft. Another reason FSC’s prefer the hub and spoke model is

that they can schedule more frequent flights along each route and make full use of

the capacity of each plane, while centralizing operations at the hub also give rise

to economies of scale. However, in contrast with most LCCs, Pegasus

differentiates itself by operating like a network carrier rather than a point to point

carrier, thanks to Istanbul’s / Turkey’s natural geographical hub. That was

emphasized by the Chairman of Pegasus Airlines, Ali Sabancı; “We aim to

combine the network benefits of full-service carriers, and the price benefits of

LCCs, to provide low cost travel, on-time performance and new planes.”.

Please see the last page of this report for important disclosures.

10

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Seat density

Higher seating density is an important element of the LCC business model and a

source of potential cost advantages. The average seat pitch in an LCC is normally

more restricted than the economy class seat of a FSC. This obviously allows

LCC’s to fit more seats into their aircraft, increasing the maximum capacity of each

flight. For example, Pegasus fits 188 seats on average into their fleet while THY

fits 168 seats, which would – assuming similar operating costs – translate into

lower costs for Pegasus. However, it is worth highlighting that a reason for the

lower number of seats on THY aircraft is the presence of a business class section

which command considerably higher ticket prices than economy class seats, thus

producing much higher yields, thus offsetting some of the cost of a lower seat

density.

Airports

Airports are generally categorised in 3 categories; primary airports, such as

Ataturk Airport in Istanbul; secondary airports, which are smaller but still near

major cities, like Sabiha Gokcen, also in Istanbul; and thirdly, regional airports,

which are typically situated in the province some distance from city centres.

Regional airports are typically characterised by the lowest levels of traffic. The

primary airports are mainly used by the larger network carriers as the “hub” in their

hub-and- spoke systems and are therefore command a strong position with regard

to bargaining power, given that they have the size and infrastructure needed to

process large passenger numbers. To illustrate this, Istanbul Ataturk Airport

processes more than 50mn passengers annually. Primary airports are the most

expensive when it comes to airport fees and charges, which include landing fees,

a charge per passenger and/or tonne of freight handled, aircraft parking charge

and other charges such as airport traffic control and air bridges. In a bid to lower

these costs, low fare carriers like Pegasus have followed a strategy of developing

routes to secondary and regional airports, while still maintaining a presence in

primary airports such as Istanbul Ataturk Airport (with only three aircraft). Another

reason for choosing secondary airports is the large volume of traffic in primary

Geographical Advantage

Source: THY presentation

Please see the last page of this report for important disclosures.

11

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

airports, which can often become congested – hardly optimal for LCC’s aiming for

low turnaround times, which would often be compromised by delays caused by

congestion in primary airports. Using less utilized secondary and regional airports

resolves this problem. The downside for passengers is, of course, that regional

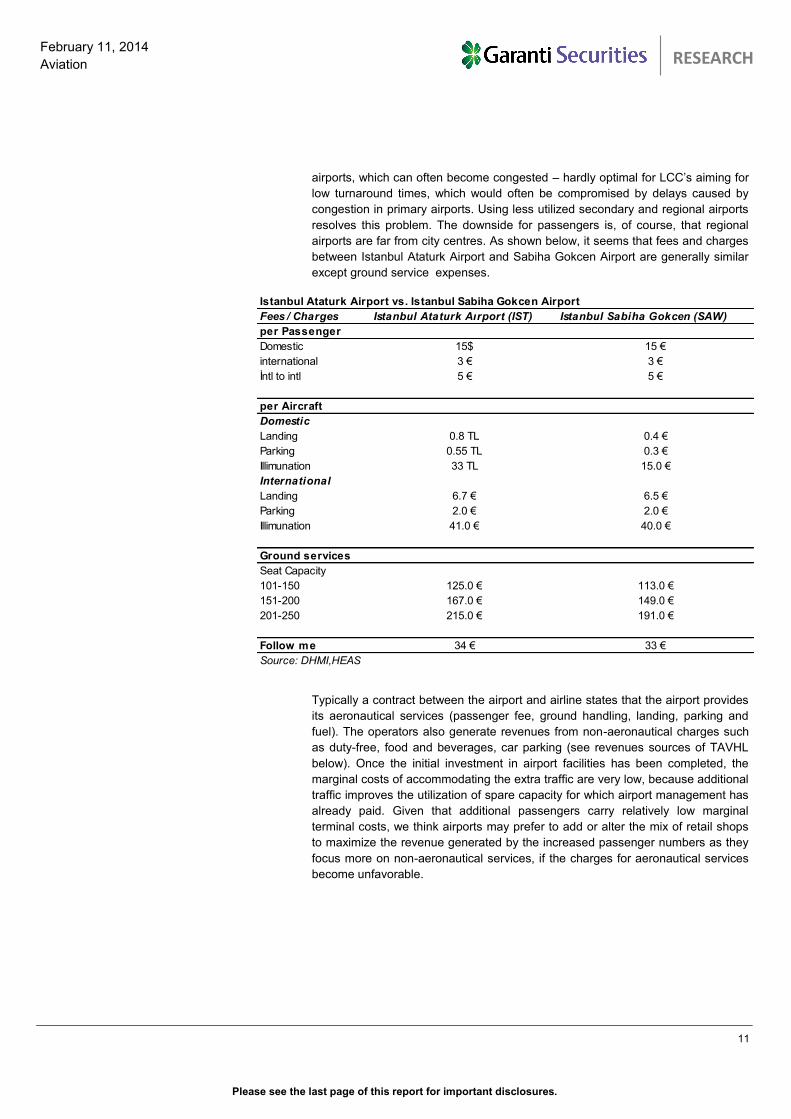

airports are far from city centres. As shown below, it seems that fees and charges

between Istanbul Ataturk Airport and Sabiha Gokcen Airport are generally similar

except ground service expenses.

Typically a contract between the airport and airline states that the airport provides

its aeronautical services (passenger fee, ground handling, landing, parking and

fuel). The operators also generate revenues from non-aeronautical charges such

as duty-free, food and beverages, car parking (see revenues sources of TAVHL

below). Once the initial investment in airport facilities has been completed, the

marginal costs of accommodating the extra traffic are very low, because additional

traffic improves the utilization of spare capacity for which airport management has

already paid. Given that additional passengers carry relatively low marginal

terminal costs, we think airports may prefer to add or alter the mix of retail shops

to maximize the revenue generated by the increased passenger numbers as they

focus more on non-aeronautical services, if the charges for aeronautical services

become unfavorable.

Istanbul Ataturk Airport vs. Istanbul Sabiha Gokcen Airport

Fees / Charges Istanbul Ataturk Aırport (IST) Istanbul Sabiha Gokcen (SAW)

per Passenger

Domestic 15$ 15 €

international 3 € 3 €

İntl to intl 5 € 5 €

per Aircraft

Domestic

Landing 0.8 TL 0.4 €

Parking 0.55 TL 0.3 €

Illimunation 33 TL 15.0 €

International

Landing 6.7 € 6.5 €

Parking 2.0 € 2.0 €

Illimunation 41.0 € 40.0 €

Ground services

Seat Capacity

101-150 125.0 € 113.0 €

151-200 167.0 € 149.0 €

201-250 215.0 € 191.0 €

Follow me 34 € 33 €

Source: DHMI,HEAS

Please see the last page of this report for important disclosures.

12

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Sales channels

The majority of LCC´s ticket sales are realised through the online channel. Both

LCC’s and FSC’s prefer the internet as a means to distribute tickets rather than

travel agents or call centres, in a bid to cut costs. No paper tickets are issued, and

the issue of a booking code, which may be presented upon check-in, reduces

distribution costs.

Unions

In countries with strong unions, it is very difficult for airlines to reduce their labour

costs by cutting wages or reducing the size of the workforce when they are hit by

downturns in the sector. The employees of many LCC’s are not unionized, helping

these airlines keep labour costs under control. Pegasus has no unionized staff,

while THY has experienced some troubles with its labour union in the past.

THY's Revenue by point of sale Pegasus' sales breakdown by channel

Source: The Company data

Europe29%

Turkey23%

Asia/Far East11%

Middle East9%

America8%

Africa5%

Internet/Call Center

14%

Other1%

Internet46%

Agent44%

Call Center2%

Other8%

Country Passenger fee Ground Handling Landing Parking Fuel Duty-free Food and Beverage Car park

Istanbul x x x x x

Ankara x x x x x

Izmir x x x x x

Gazipasa x x x x x x x x

Enfidha x x x x x x x x

Monastır x x x x x x x x

Tbilisi x x x x x x x x

Batumi x x x x x x x x

Skopje x x x x x x x x

Ohrid x x x x x x x xx

Latvia Riga x x

Saudi Arabia Medina x x x x x x x x

Source: The Company

Macedonia

Aeronautical charges Non-aeronautical charges

Turkey

Tunisia

Georgia

Please see the last page of this report for important disclosures.

13

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Frequent flyer programs/alliances

Frequent-flyer programs are marketing schemes by airlines which offer their

passengers a gift, usually free travel, when they have completed a certain amount

of travel with the airline. These programs have resulted in many passengers,

especially business travelers, preferring a certain airline or airline alliance as they

would receive bonus flights, free hotel accommodation or other free gifts provided

through the scheme, although at the same time these passengers may be able to

buy cheaper flights with another airline. The reason has often been that the flights

are paid by their companies, but the individual employee receives the air miles or

associated awards. Such programs/alliances are not generally provided by LCC’s,

while FSC’s generally do offer them. Pegasus has no intention to join any alliance

while THYAO is a part of the Star Alliance and has various frequent flyer

programs.

A Study on LCC vs. FSC

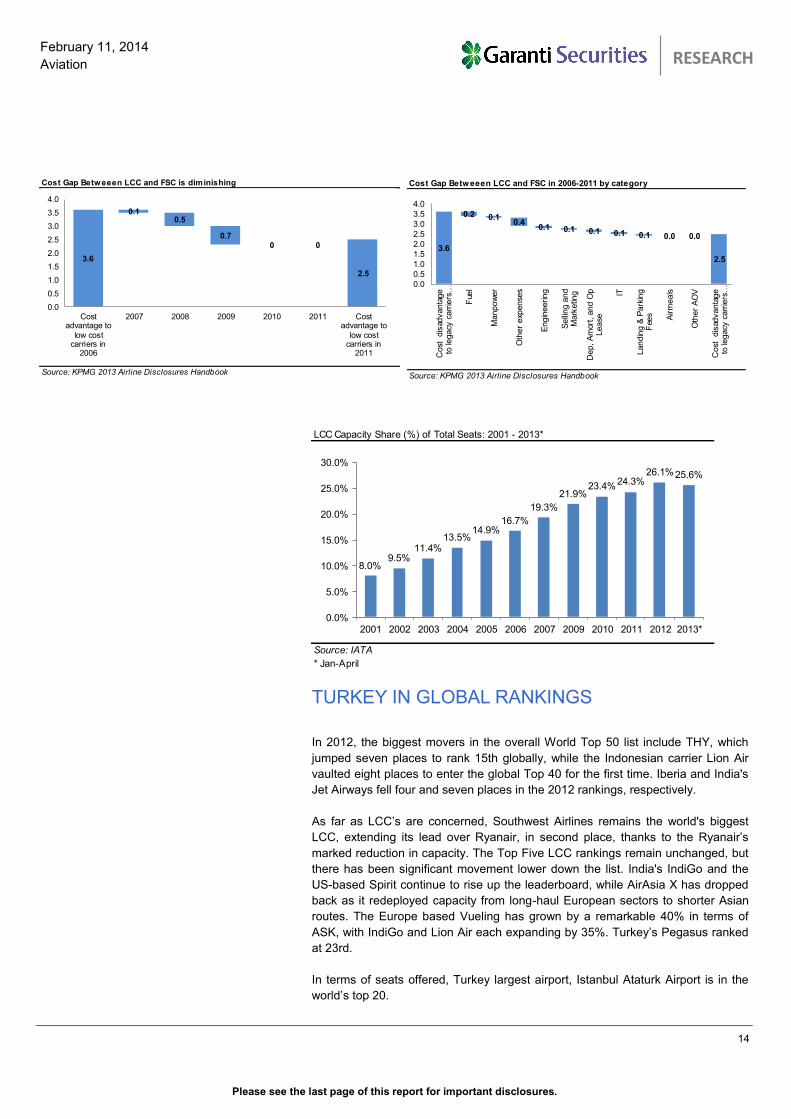

Cost gap between low cost and full service carriers is diminishing

According to a KPMG survey on airline unit costs, the cost gap between legacy

and low cost carriers has narrowed to 2.5 US cents per ASK from 3.6 between

2006-2011. The global crisis in 2009 resulted in more focus on the cost side.

Although many of the easily applicable cost minimization targets have been

achieved and both LCC’s and FSC’s continue their focus on cutting costs, it is

thought that the cost gap will never be fully closed for the following reasons; i)

FSC’s will be unable to eliminate their historical staff costs and practices, ii) Only

LCCs would viably be able to maintain further efficiencies creating by single fleet

types and iii) LCC’s have an inherent ability to operate at lower cost airports and

routes stemming from the lack of network limitations. However, LCC’s will

continue to capture market share from FSC’s by targeting their higher value

customers. This will pave the way for the launch of new products and services

such as free luggage, priority boarding and pre-assigned seating. In this respect,

the key challenge will be to maintain cost control to remain competitive in the face

of increasingly streamlined competitors. On the other hand, FSC’s will need to

evolve their business models through partnerships, joint ventures and mergers

and acquisitions to overcome the cost challenges and compete with the newer

and large hub carriers.

Turkey capacity seats share by alliance system (8-14 April, 2013)

Source: IATA

58.7%

1.5%

2.9%

36.8%

Star

oneworld

SkyTeam

Unalligned

Please see the last page of this report for important disclosures.

14

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

TURKEY IN GLOBAL RANKINGS

In 2012, the biggest movers in the overall World Top 50 list include THY, which

jumped seven places to rank 15th globally, while the Indonesian carrier Lion Air

vaulted eight places to enter the global Top 40 for the first time. Iberia and India's

Jet Airways fell four and seven places in the 2012 rankings, respectively.

As far as LCC’s are concerned, Southwest Airlines remains the world's biggest

LCC, extending its lead over Ryanair, in second place, thanks to the Ryanair’s

marked reduction in capacity. The Top Five LCC rankings remain unchanged, but

there has been significant movement lower down the list. India's IndiGo and the

US-based Spirit continue to rise up the leaderboard, while AirAsia X has dropped

back as it redeployed capacity from long-haul European sectors to shorter Asian

routes. The Europe based Vueling has grown by a remarkable 40% in terms of

ASK, with IndiGo and Lion Air each expanding by 35%. Turkey’s Pegasus ranked

at 23rd.

In terms of seats offered, Turkey largest airport, Istanbul Ataturk Airport is in the

world’s top 20.

LCC Capacity Share (%) of Total Seats: 2001 - 2013*

Source: IATA

* Jan-April

8.0%9.5%

11.4%13.5%

14.9%16.7%

19.3%

21.9%23.4%

24.3%26.1%25.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2001 2002 2003 2004 2005 2006 2007 2009 2010 2011 2012 2013*

Cost Gap Betweeen LCC and FSC is diminishing

Source: KPMG 2013 Airline Disclosures Handbook

3.6

0.10.5

0.70 0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Costadvantage to

low costcarriers in

2006

2007 2008 2009 2010 2011 Costadvantage to

low costcarriers in

2011

Cost Gap Betweeen LCC and FSC in 2006-2011 by category

Source: KPMG 2013 Airline Disclosures Handbook

3.6

0.2 0.10.4

0.1 0.1 0.1 0.1 0.1 0.0 0.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Cost

dis

advanta

ge

to le

gacy

carr

iers

…

Fue

l

Manpow

er

Oth

er

exp

ense

s

Engin

eering

Selli

ng a

nd

Mark

etin

g

Dep, A

mor

t, a

nd O

pLease

IT

Landin

g &

Park

ing

Fee

s Airm

eals

Oth

er

AO

V

Cost

dis

advanta

ge

to le

gacy

carr

iers

…

Please see the last page of this report for important disclosures.

15

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

The World's Top 20 Airports by Capacity Offered (starting week 31 March 2013)

Rank Airport Total Seats

1 ATL Atlanta Hartsfield-Jackson International Airport 2,183,726

2 PEK Beijing Capital International Airport 2,068,130

3 HND Tokyo Haneda Airport 1,887,497

4 LHR London Heathrow Airport 1,774,606

5 DXB Dubai International Airport 1,639,176

6 ORD Chicago O'Hare International Airport 1,534,449

7 LAX Los Angeles International Airport 1,491,895

8 DFW Dallas/Fort Worth International Airport 1,445,441

9 HKG Hong Kong International Airport 1,440,997

10 CDG Paris Charles De Gaulle Airport 1,421,231

11 CGK Jakarta Soekarno-Hatta International Airport 1,400,299

12 FRA Frankfurt Airport 1,394,143

13 SIN Singapore Changi Airport 1,371,158

14 BKK Bangkok Suvarnabhumi International 1,237,778

15 CAN Guangzhou Baiyun Airport 1,225,526

16 DEN Denver International Airport 1,176,220

17 JFK New York John F Kennedy International Airport 1,172,450

18 PVG Shanghai Pudong Airport 1,154,933

19 KUL Kuala Lumpur International Airport 1,134,217

20 IST Istanbul Ataturk Airport 1,125,132

Source: Innovata

Please see the last page of this report for important disclosures.

16

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

World's top 50 airlines by capacity (ASKs per week): Dec-2012 vs Dec-2011**

Ranking

Dec-11 Dec-12 Variance

United Airlines* 3,676,173,972 6,149,398,758 67.30% 4 1 3

Delta Air Lines 5,659,984,201 5,643,676,049 -0.30% 1 2 -1

Emirates 4,217,428,241 4,992,911,535 18.40% 3 3 -

American Airlines 4,740,187,417 4,800,884,481 1.30% 2 4 -2

Southw est Airlines 3,052,855,291 3,276,525,770 7.30% 6 5 1

Lufthansa 3,232,470,602 3,158,824,795 -2.30% 5 6 -1

British Airw ays 2,969,790,657 3,049,528,888 2.70% 7 7 -

Air France 2,947,863,927 2,825,526,843 -4.20% 8 8 -

China Southern 2,338,943,535 2,596,677,741 11.00% 10 9 1

Singapore Airlines 2,284,561,770 2,375,715,435 4.00% 11 10 1

Cathay Pacif ic 2,518,689,815 2,311,927,122 -8.20% 9 11 -2

Air China 1,975,786,807 2,193,529,512 11.00% 13 12 1

US Airw ays 2,148,315,118 2,016,797,120 -6.10% 12 13 -1

China Eastern 1,802,997,303 1,987,445,996 10.20% 15 14 1

Turkish Airlines 1,546,786,987 1,918,119,411 24.00% 22 15 7

Qantas Airw ays 1,967,029,665 1,863,468,681 -5.30% 14 16 -2

Qatar Airw ays 1,653,642,624 1,798,311,481 8.70% 19 17 2

KLM 1,743,421,204 1,785,622,278 2.40% 16 18 -2

Korean Air Lines 1,699,049,358 1,734,522,605 2.10% 17 19 -2

Thai Airw ays 1,601,385,091 1,702,802,250 6.30% 20 20 -

Air Canada 1,698,644,091 1,671,164,061 -1.60% 18 21 -3

All Nippon Airw ays 1,246,645,650 1,549,773,945 24.30% 25 22 3

TAM 1,484,265,530 1,494,027,291 0.70% 23 23 -

Ryanair 1,590,511,473 1,476,213,184 -7.20% 21 24 -3

Japan Airlines 1,392,363,846 1,375,619,611 -1.20% 24 25 -1

JetBlue Airw ays 1,189,448,769 1,214,788,293 2.10% 27 26 1

Aeroflot 1,032,936,073 1,197,672,318 15.90% 29 27 2

Etihad Airw ays 989,471,343 1,135,831,421 14.80% 32 28 4

easyJet 1,056,070,278 1,124,069,015 6.40% 28 29 -1

Iberia 1,197,798,613 1,046,122,223 -12.70% 26 30 -4

Malaysia Airlines 1,020,187,141 1,039,171,244 1.90% 30 31 -1

Virgin Atlantic 974,968,392 1,005,248,585 3.10% 33 32 1

Gol 1,007,352,569 913,465,718 -9.30% 31 33 -2

Asiana Airlines 801,526,420 876,324,179 9.30% 36 34 2

Air India 897,084,182 869,253,552 -3.10% 34 35 -1

Alaska Airlines 807,036,820 866,811,809 7.40% 35 36 -1

Saudi Arabian 797,784,368 859,673,901 7.80% 37 37 -

China Airlines 797,010,713 824,521,813 3.50% 38 38 -

Lion Airlines 602,332,879 810,548,478 34.60% 47 39 8

Hainan Airlines 756,248,033 789,659,041 4.40% 40 40 -

SWISS 735,342,198 768,204,291 4.50% 41 41 -

Jetstar Airw ays 627,376,629 732,129,754 16.70% 46 42 4

Air New Zealand 727,101,490 710,174,817 -2.30% 42 43 -1

Westjet 677,374,415 703,526,653 3.90% 45 44 1

Alitalia 713,564,199 702,771,404 -1.50% 43 45 -2

Jet Airw ays 766,255,713 682,168,104 -11.00% 39 46 -7

Transaero Airlines 590,637,778 681,909,360 15.50% - 47 n/a

Air Berlin 704,680,454 678,119,686 -3.80% 44 48 -4

Virgin Australia 563,988,380 667,351,376 18.30% - 49 n/a

EVA Air 600,022,403 661,811,048 10.30% - 50 n/a

GRAND TOTAL 81,823,394,427 87,310,342,925 6.70%

Source: Innovata

*United and Continental has been combined for 2012 but not 2011 **Representative sample w eek in December of each year

Note: US major airlines include the regional services operated by other carriers but marketed by the majors only.

Airline Dec-11 Dec-12 % changeGlobal rank

Please see the last page of this report for important disclosures.

17

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

GLOBAL SECTOR OUTLOOK

Airlines expecting a 31% increase in passenger demand by 2017

The International Air Transport Association (IATA) released the IATA Airline

Industry Forecast for 2013-2017, finding that airlines expect to see a 31%

increase in passenger numbers between 2012 and 2017. Total passenger

numbers are expected to reach 3.91bn by 2017, up from the 2.98bn carried in

2012.

The IATA Airline Industry Forecast 2013-2017 is a consensus outlook for system-

wide passenger growth. Demand is expected to expand at an average CAGR of

5.4% between 2013 and 2017. This would compare to the CAGR of 4.3% in global

Top 25 LCCs worldwide by capacity (ASKs per week): Dec-2012 vs Dec-2011

Ranking

Dec-11 Dec-12 Variance

Southw est Airlines 3,052,855,291 3,276,525,770 7.30% 1 1 -

Ryanair 1,590,511,473 1,476,213,184 -7.20% 2 2 -

JetBlue Airw ays 1,189,448,769 1,214,788,293 2.10% 3 3 -

easyJet 1,056,070,278 1,124,069,015 6.40% 4 4 -

Gol 1,007,352,569 913,465,718 -9.30% 5 5 -

Lion Airlines 602,332,879 810,548,478 34.60% 9 6 3

Jetstar Airw ays 627,376,629 732,129,754 16.70% 8 7 1

Westjet 677,374,415 703,526,653 3.90% 7 8 -1

AirTran Airw ays 704,027,357 593,301,841 -15.70% 6 9 -3

AirAsia Berhad 514,497,106 592,750,621 15.20% 10 10 -

Indigo 363,580,357 489,547,961 34.60% 14 11 3

Norw egian 376,017,532 460,529,531 22.50% 12 12 -

Condor 408,981,174 400,293,763 -2.10% 11 13 -2

Virgin America 350,169,261 387,519,726 10.70% 16 14 2

Spirit Airlines 297,900,830 373,126,368 25.30% 19 15 4

Volaris 305,039,639 348,697,350 14.30% 18 16 2

Frontier Airlines 363,405,399 330,101,798 -9.20% 15 17 -2

Wizz Air 314,854,410 330,075,746 4.80% 17 18 -1

SpiceJet 270,033,409 313,233,746 16.00% 20 19 1

AirAsia X Sdn. Bhd. 367,668,226 306,214,544 -16.70% 13 20 -7

Cebu Pacif ic Air 262,579,589 285,040,540 8.60% 21 21 -

Air Arabia 247,294,792 275,508,189 11.40% 23 22 1

Pegasus 247,563,308 268,113,218 8.30% 22 23 -1

Vueling Airlines 175,838,664 246,848,248 40.40% 24 24 -

Allegiant Air 173,834,741 217,749,960 25.30% 25 25 -

GRAND TOTAL 15,546,608,096 16,469,920,012 5.90%

Source: Innovata

Representative sample week in December of each year

Airline Dec-11 Dec-12 % ChangeGlobal rank

Please see the last page of this report for important disclosures.

18

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

passenger numbers between 2008 and 2012, largely reflecting the negative

impact of the 2008 global financial crisis and the recession that followed. Of the

new passengers, approximately 292mn will be carried on international routes and

638mn domestically.

The emerging economies of the Middle East and Asia-Pacific will see the

strongest international passenger growth with a projected CAGR of 6.3% and

5.7%, followed by Africa and Latin America with CAGR rates of 5.3% and 4.5%.

Routes to or within China will be the single largest driver of growth, accounting for

30% of new passengers during the forecast period. Of the anticipated 227.4mn

additional passengers, 195mn will be domestic and 32.4mn will be international.

The Asia-Pacific region (including China) is expected to add around 300mn

additional passengers by the end of the current forecast horizon. Of these, around

225mn or 75% are expected to be domestic passengers.

With 677.8mn domestic passengers in 2017, the United States will remain the

largest single market for domestic passengers, although it is only forecasted to

add 70mn passengers over the forecast period (marking a 2.2% CAGR). This

reflects the market’s maturity. China is firmly established in second place

(487.9mn passengers by 2017, with a 10.2% CAGR.). The US also will reclaim the

top spot from Germany for international passengers by the end of the forecast

period. Germany will add 27.2mn passengers to the 149.4mn in 2012 (3.4%

CAGR), while the US will add 28.2mn international passengers, the number

increasing at a CAGR of 3.5% from 149.3mn in 2012 to 177.5mn in 2017.

Forecast Highlights

International Passenger Development

International passenger numbers are expected to rise by 25% from 1.2 bn in 2012

to 1.5bn in 2017, bringing 292mn additional passengers (4.6% CAGR).

Uzbekistan (10.3% CAGR) has displaced Kazakhstan (9.0% CAGR) as the fastest

growing market for international passenger traffic. The next eight fastest growing

markets are Russia (7.7% CAGR), Turkey (7.6% CAGR), Oman (7.5% CAGR),

China (7.1% CAGR), Vietnam (6.9%CAGR), Saudi Arabia (6.9%), Azerbaijan

(6.8% CAGR), and Pakistan (6.7% CAGR). No Latin American or African countries

are among the fastest growing markets.

The United Arab Emirates will see air passenger numbers increase by 29.2 mn (a

6.6% CAGR) over the forecast period, nearly as many additions as in China. For

international traffic, routes between the Middle East and Asia-Pacific will see the

most rapid growth.

Domestic Passenger Development

Domestic passenger numbers are expected to rise from 1.82 billion in 2012 to

2.46bn in 2017, an increase of 639mn reflecting a CAGR of 6.2% over the period.

Brazil will firmly establish itself as the third largest domestic market after the US

and China, with 122.4mn passengers in 2017, an increase of 32 million

Please see the last page of this report for important disclosures.

19

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

passengers from the 90mn 2012 (a 6.3% CAGR).

Turkey will enter the top 10 largest markets with 26.3mn passengers carried with

an addition of 17.2mn more (10.6% CAGR) over the forecast period. It is also the

second fastest growing domestic market.

The lower five of the top ten fastest growing markets on the basis of domestic

passenger numbers, the bottom five are all in Latin America: Brazil, Peru,

Colombia, Mexico and Ecuador.

Regional Outlook over the 2013-2017 forecast period

Asia-Pacific passenger traffic is forecast to grow at a CAGR of 5.7%. Traffic within

the Asia-Pacific region will represent 31.7% of global passengers in 2017, up from

28.2% in 2012. North America and Europe will continue to see their share decline,

from 26% to 24% for North America, and from 24% to 23% for Europe.

The Middle East is set to follow the strongest international passenger growth, with

a CAGR of 6.3%.

Europe is on course to see international passenger demand grow at a CAGR of

3.9%.

North America is projected to see the slowest international passenger demand

growth with a CAGR of 3.6%.

Latin America is forecasted to see international passenger demand grow at a

CAGR of 4.5%.

TURKISH AVIATION SECTOR AT A GLANCE

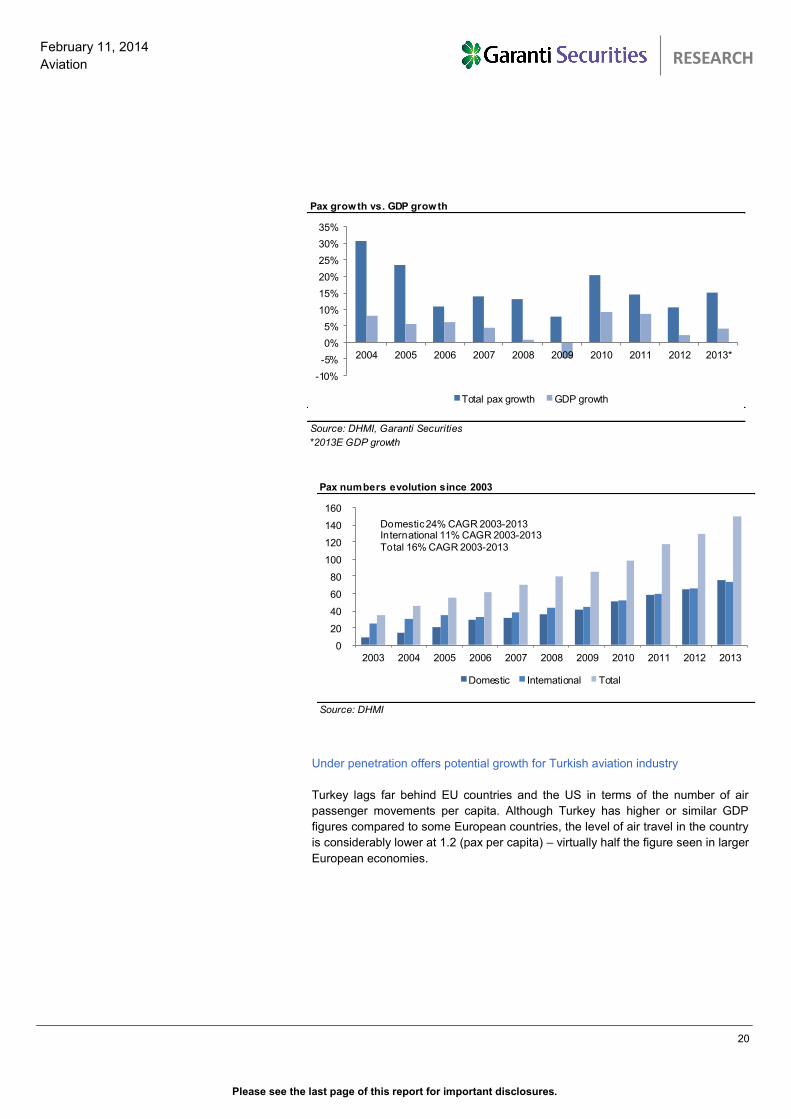

Turkish air passenger traffic posted a 16% CAGR in 2003-2013

Passenger traffic in Turkey has witnessed strong momentum since the

deregulation of the sector in 2003. Passenger numbers have grown at a CAGR of

16% in Turkey between 2003-13, at a multiple of 3x real GDP growth. Even in

2009, when real GDP contracted by 5%, passenger numbers in Turkey grew by

6%. The Turkish aviation industry continued to register high rates of growth, even

at the time of the global financial crisis (in 2008-09), the SARS outbreak (in 2004)

and natural phenomena such as the volcanic eruption in Iceland (in 2011).

Domestic passenger numbers have also surged on the back of affordable fares

with a CAGR of 24% between 2003-2013, surpassing the CAGR of 11% in

international passenger numbers. We think that Turkey’s geographical position, its

increased tourism potential, its still under-penetrated nature and a generally

supportive approach to the sector by the government will help sustain this above-

average growth. Turkey’s two biggest carriers THY and Pegasus plan to double

their fleet size by 2021, indicating their anticipation of strong demand. We project

air passenger traffic to reach 150mn by 2016, marking a CAGR of 9.3% CAGR for

2014-2016E vs. State Airports’ Authority’s projection if a 9.9% CAGR (see page

25 for details).

Please see the last page of this report for important disclosures.

20

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Under penetration offers potential growth for Turkish aviation industry

Turkey lags far behind EU countries and the US in terms of the number of air

passenger movements per capita. Although Turkey has higher or similar GDP

figures compared to some European countries, the level of air travel in the country

is considerably lower at 1.2 (pax per capita) – virtually half the figure seen in larger

European economies.

Pax growth vs. GDP growth

Source: DHMI, Garanti Securities

*2013E GDP growth

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Total pax growth GDP growth

Pax numbers evolution since 2003

Source: DHMI

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Domestic International Total

Domestic 24% CAGR 2003-2013International 11% CAGR 2003-2013

Total 16% CAGR 2003-2013

Please see the last page of this report for important disclosures.

21

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Natural geographical hub

With almost 50 countries within a 3-hour flight of Turkey, the country is placed as a

natural geographical hub. Turkey’s geographical advantage is one of the main

triggers of the Turkish aviation industry, as it helps the country to capture more

transit passengers and there are plans in Turkey to establish Istanbul as an

international hub. For this end, the government plans to build one of the world’s

largest airports in Istanbul with an initial capacity of 70mn by 2018 and a final

capacity of 150mn by 2027. (see page 29 for details).

Pax per capita (2011)

Source: Pegasus presentation

0.4 0.5 0.4 0.3

2.0

0.4 0.3 0.80.81.4 1.6

1.9

0.5

2.2

2.9 2.8

1.2

1.9 2.0 2.22.5 2.6

3.23.6

0

0.5

1

1.5

2

2.5

3

3.5

4

Turkey Italy France Germany US EU-15 UK Spain

Domestic International Total

Low penetration levels and geographical advantage

Source: Pegasus Presentation

Please see the last page of this report for important disclosures.

22

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Ambitious growth plans of THY and Pegasus

Turkish airlines and Pegasus recently placed massive aircraft orders to expand

their operations, both internationally and domestically. According to their plans,

THY’s fleet will expand from 232 aircraft in 2013 to 436 by 2021, nearly doubling

the airline’s total seating capacity from 42,200 to 83,500. Meanwhile, Pegasus

ordered 100 new aircraft (75 firm orders plus 25 optional) in December 2012. After

the deliveries, Pegasus’ fleet size is estimated to be between 75-126. We believe

the orders will bode well for growth in the industry.

Turkey’s attraction for tourism

We believe Turkey’s tourism industry offers tremendous growth potential, given

that 50 countries are all within a 3 hour flight of Turkey, Turkey’s long coastal

regions and its relatively warm climate compared to Europe. As with Spain and

Greece, Turkey could continue to benefit from an increased number of tourists

going forward, as observed in the recent years. As seen below, Turkey has

recorded an 8% CAGR in tourist arrivals over the last decade. Note that Antalya,

located on Turkey’s South coast of Turkey, has Turkey’s second largest airport in

terms of passenger numbers, after Istanbul’s Ataturk Airport. The overwhelming

majority of tourists come to Turkey by air. Gazipasa Airport (operated by TAV),

another airport serving the area near Antalya, has recently entered operation –

another clear sign of Turkey’s increasing tourism potential.

Fleet profiles of Turkish carriers

Source: Pegasus presentation

233

45 32 32 14

206

79

60

25

0

100

200

300

400

500

600

THY Pegasus Onurair SunExpress Atlasjet

Existing On order Options

Tourist figures

Source: TUIK

*Jan-Nov 2013

0

5

10

15

20

25

30

35

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Tourist numbers (mn)

8% CAGR 2004-2012

Please see the last page of this report for important disclosures.

23

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Supportive demographics

Turkey is the second largest country in Europe in terms of population, after

Germany, with a demographically young population; half of the population is under

the age of 30, meaning more people tend to fly as they reach working age. In

Turkey, it is believed that passport ownership ratio is yet at low teens and we

believe the majority of passport holders are Turkish citizens living in other

countries. We believe the high passport fees are one of the reasons for the low

passport ownership in Turkey. There has been increasing controversy on that

issue with campaigns to ensure passport ownership is more affordable or easy.

Growth in air travel supported by lack of alternative transport system and

mountainous terrain

As a generally mountainous country, Turkey currently lacks a developed network

of railways, high speed trains and infrastructure. Despite high special duties on

motor vehicle purchases (on top of VAT) and petrol, Turkish people still prefer

road travel, which accounts for 90% of total transport in Turkey. We believe that

with mounting competition, increasing seat capacity and attractive fares, the

growth in air travel will outpace road travel. Along with the increasing GDP,

disposable income rises, resulting in an increase in awareness of time value of air

travel compared to car or bus transportation. Although the government is about to

finalize a high speed rail link between Turkey’s biggest two cities of Istanbul and

Ankara, we do not expect this to significantly compromise growth in the domestic

aviation sector, as Turkey needs a much more comprehensive network of high

speed trains. According to government plans, high speed railways are going to

connect many Turkish cities. They could negatively affect the growth in domestic

air travel by the 2020s. Yet, at this stage, we do not find those plans are

worrisome.

Special Consumption Tax on autos (%)

Engine size 2002 2014

below 1,600 cc 27% 45%

1601-2000 cc 46% 90%

above 2,000 cc 50% 145%

Source: ADA

Transportation of domestic passengers in Turkey

Current 2023 Target

Road 90% 72%

Rail 2% 10%

Air 8% 14%

Sea 0% 4%

Source: Transportation Ministry

Number aircraft and seat capacity in Turkey

Source: Civil Aviation Authority

-

50

100

150

200

250

300

350

400

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Seat capacity (lhs) Number of aircrafts (rhs)

Please see the last page of this report for important disclosures.

24

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Competition

Turkish Airlines (THY): Turkish Airlines was founded in 1993 under the

supervision of the Ministry of National Defence. THY initiated its operations with a

fleet of just 5 aircraft and initiated cargo transportation operations in 1995. It is

now the 3rd biggest airline in terms of pax carried, the 4th largest in terms of ASK

and 5th largest according to RPK among AEA (Association of European Airlines).

At the end of 2013, it was operating with a fleet of 232 aircraft and served 48.3

million passengers (vs. 22.6 million in 2008). The airline generated USD8.3bn of

revenue in 2012 (vs. USD4.7bn in 2008). The airline uses Istanbul Ataturk Airport

as its hub and was flying to 42 domestic and 201 international destinations as of

2013. THY was ranked as Europe’s best airline by Skytrax three years in a row

(2011, 2012 and 2013).

Pegasus: Established in 1990, and acquired by Esas Holding in 2005, Pegasus

was Turkey’s first low cost carrier and is the second largest carrier after the

national flag carrier, THY. Based at Istanbul Sabiha Gokcen Airport, Pegasus was

flying to 76 destinations as of 2013, 31 of which were domestic and the remaining

45 international. As an LCC, ancillary revenues comprised of excess luggage,

cancellations, seat selection and meals represented 13% of total revenues in

9M13. Pegasus is named as the fastest growing LCC in Europe in 2010 and 2011

in terms of seat capacity, according to OAG.

SunExpress: SunExpress was founded in 1989 as a subsidiary of THY and

Lufthansa. SunExpress is one of the leading airlines in terms of passenger

numbers between Germany and Turkey. The home base of SunExpress is in

Antalya on the Turkish Riviera The second most important base is the hub Izmir

on the Aegean coast. As of 9M13, it flies to/from 22 airports in Germany, 21 in

Turkey and 44 in other countries and operates with 21 B737-800 aircraft with total

seat capacity of 3.969. it carried 4.3mn passengers as of 9M13, by achieving load

factor of 84.4%

AnadoluJet: Founded in 2008, as THY’s low cost carrier brand, Anadolujet uses

Ankara Esenboga Airport as its hub and is focused on domestic operations. It has

27 aircraft in its fleet, according to its website.

OnurAir: Founded in 1992, Onur Air has a fleet of 23 aircraft. It mainly operates for

charter flights both internationally and domestically. It flies to 80 destinations

internationally and serves 15 domestic airports.

Atlasjet: Founded in 2001, Atlasjet operates 17 aircraft. It also provides cargo

transportation in domestic and international routes through scheduled and non-

scheduled flights, in addition to passenger services.

OUR PASSENGER FORECASTS

Turkish air passenger traffic grew by 15% in 2013 (vs.11% in 2012), with

international passenger numbers reaching 73mn on the back of 12% annual

growth while domestic passenger traffic increased by 18% to 76mn in 2013.

We project that total passenger traffic will reach 150mn by 2016E, following a

10.3% CAGR between 2013-2016. We forecast 10.4% growth in international

Please see the last page of this report for important disclosures.

25

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

passenger traffic with 10.3% growth in domestic passenger traffic during the same

period. The State Airports Authority (DHMI) anticipates a CAGR of 9.9% between

2013-2016, in parallel with our forecast in overall terms.

Pax Projections (mn)- our numbers are inline w ith DHMI

Source: DHMI, Garanti Securities

-

50

100

150

200

250

Gara

nti

Secu

rities

Dom

estic

Inte

rnation

al

DH

MI

Dom

estic

Inte

rnation

al

2014E

2015E

2016E

Passenger Assumptions (mn) 2011 2012 2013 2014E 2015E 2016E

THY

Domestic 14.5 15.9 20.1 25.4 31.1 37.6

growth 6.8% 9.5% 26.3% 26.7% 22.4% 20.9%

International 18.1 23.2 28.2 32.0 37.4 43.5

growth 16.9% 27.7% 21.8% 13.4% 16.7% 16.3%

Total 32.7 39.0 48.3 57.4 68.5 81.0

growth 12.2% 19.6% 23.6% 18.9% 19.2% 18.4%

Pegasus

Domestic 6.8 8.3 10.2 12.1 14.4 17.0

growth 36.4% 22.7% 23.3% 18.6% 18.4% 18.2%

International 3.9 5.3 6.6 7.9 9.4 11.1

growth 29.4% 33.7% 24.8% 20.3% 19.0% 18.0%

Total 10.7 13.6 16.8 20.1 23.8 28.1

growth 33.7% 26.8% 23.9% 19.3% 18.6% 18.1%

Market Shares (%)

THY 37.0% 40.0% 43.3% 46.0% 49.6% 54.0%

Domestic 49.8% 49.2% 52.7% 58.5% 65.3% 73.5%

International 30.7% 35.4% 38.4% 39.3% 41.4% 44.0%

Pegasus 12.1% 13.9% 15.1% 16.1% 17.3% 18.7%

Domestic 23.2% 25.7% 26.9% 28.0% 30.2% 33.2%

International 6.7% 8.1% 9.0% 9.7% 10.5% 11.3%

Turkish Market

Domestic 29.2 32.3 38.1 43.4 47.6 51.1

growth 15.5% 10.7% 18.0% 14.0% 9.7% 7.4%

International 59.0 65.4 73.4 81.4 90.3 98.8

growth 13.1% 10.8% 12.2% 10.8% 11.0% 9.5%

Total 88.2 97.7 111.5 124.7 137.9 149.9

growth 13.9% 10.8% 14.1% 11.9% 10.5% 8.7%

Source: DHMI, The Company data, Garanti Securities

Please see the last page of this report for important disclosures.

26

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

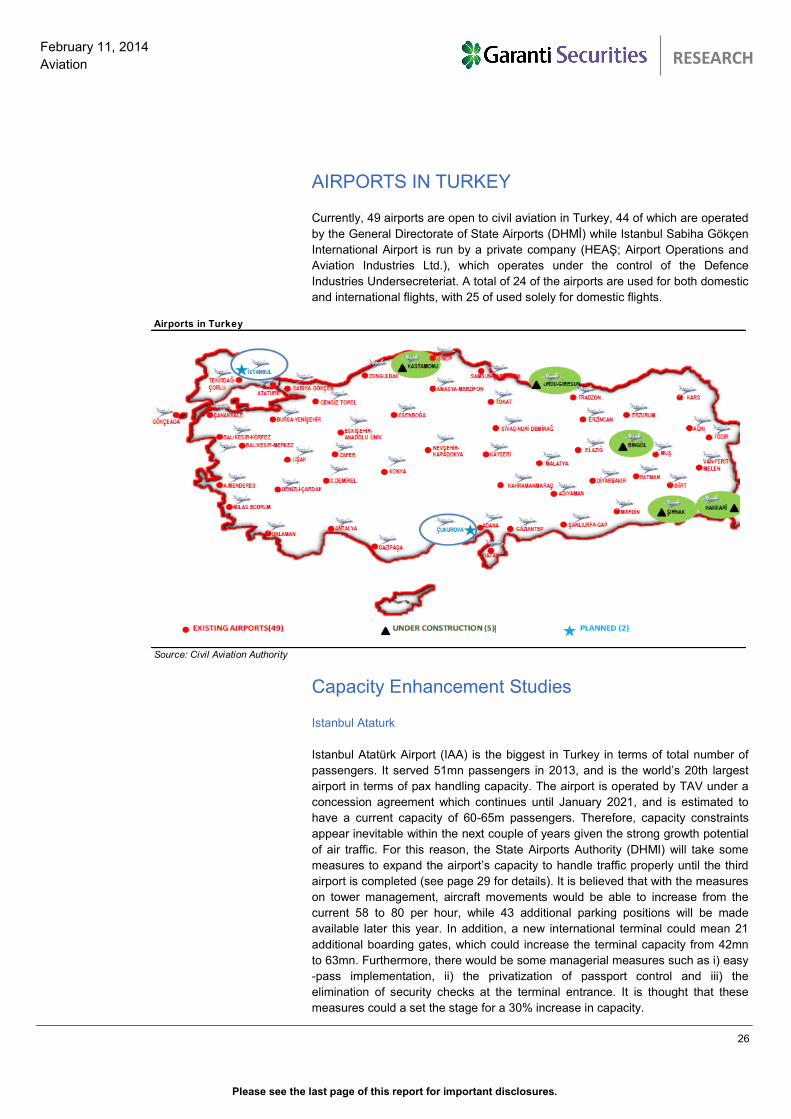

AIRPORTS IN TURKEY

Currently, 49 airports are open to civil aviation in Turkey, 44 of which are operated

by the General Directorate of State Airports (DHMİ) while Istanbul Sabiha Gökçen

International Airport is run by a private company (HEAŞ; Airport Operations and

Aviation Industries Ltd.), which operates under the control of the Defence

Industries Undersecreteriat. A total of 24 of the airports are used for both domestic

and international flights, with 25 of used solely for domestic flights.

Capacity Enhancement Studies

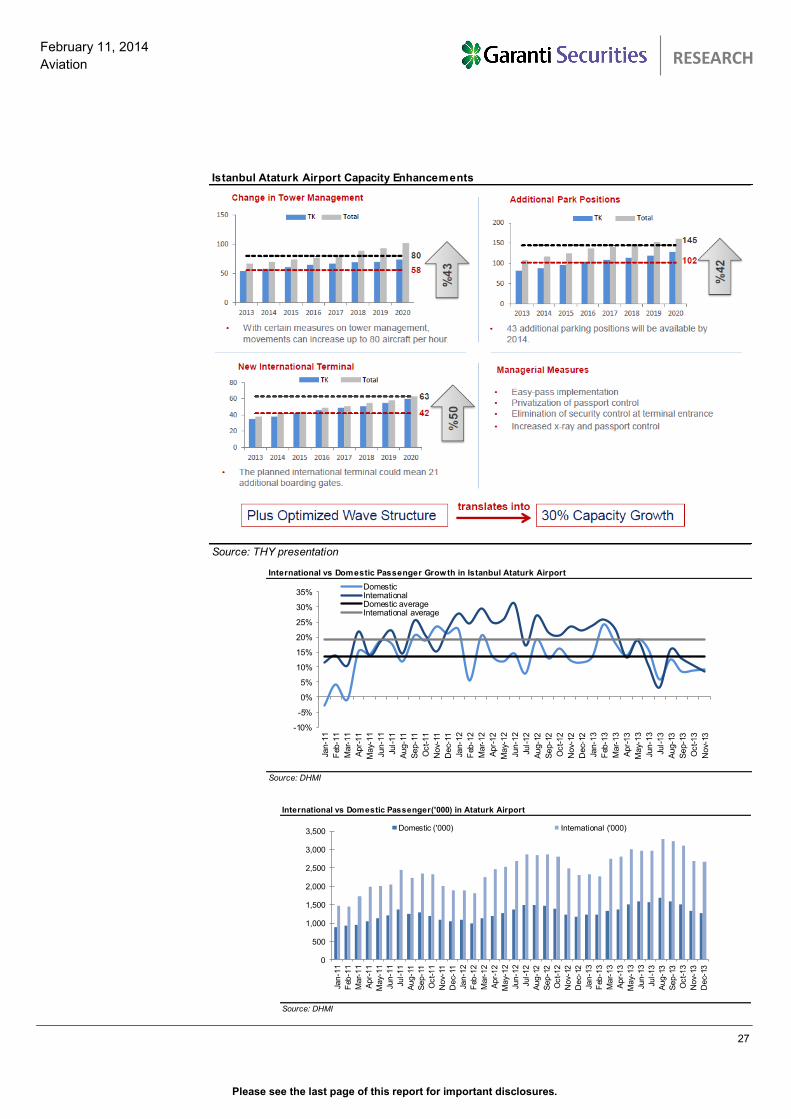

Istanbul Ataturk

Istanbul Atatürk Airport (IAA) is the biggest in Turkey in terms of total number of

passengers. It served 51mn passengers in 2013, and is the world’s 20th largest

airport in terms of pax handling capacity. The airport is operated by TAV under a

concession agreement which continues until January 2021, and is estimated to

have a current capacity of 60-65m passengers. Therefore, capacity constraints

appear inevitable within the next couple of years given the strong growth potential

of air traffic. For this reason, the State Airports Authority (DHMI) will take some

measures to expand the airport’s capacity to handle traffic properly until the third

airport is completed (see page 29 for details). It is believed that with the measures

on tower management, aircraft movements would be able to increase from the

current 58 to 80 per hour, while 43 additional parking positions will be made

available later this year. In addition, a new international terminal could mean 21

additional boarding gates, which could increase the terminal capacity from 42mn

to 63mn. Furthermore, there would be some managerial measures such as i) easy

-pass implementation, ii) the privatization of passport control and iii) the

elimination of security checks at the terminal entrance. It is thought that these

measures could a set the stage for a 30% increase in capacity.

Airports in Turkey

Source: Civil Aviation Authority

Please see the last page of this report for important disclosures.

27

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Source: DHMI

International vs Domestic Passenger Growth in Istanbul Ataturk Airport

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Jan-1

1

Feb

-11

Mar-

11

Apr-

11

May-

11

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-11

Nov-

11

Dec-

11

Jan-1

2

Feb

-12

Mar-

12

Apr-

12

May-

12

Jun-1

2

Jul-12

Aug-1

2

Sep-1

2

Oct-12

Nov-

12

Dec-

12

Jan-1

3

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun-1

3

Jul-13

Aug-1

3

Sep-1

3

Oct-13

Nov-

13

DomesticInternationalDomestic averageInternational average

Source: DHMI

International vs Domestic Passenger('000) in Ataturk Airport

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan-1

1

Feb

-11

Mar-

11

Apr-

11

May-

11

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-11

Nov-

11

Dec-

11

Jan-1

2

Feb

-12

Mar-

12

Apr-

12

May-

12

Jun-1

2

Jul-12

Aug-1

2

Sep-1

2

Oct-12

Nov-

12

Dec-

12

Jan-1

3

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun-1

3

Jul-13

Aug-1

3

Sep-1

3

Oct-13

Nov-

13

Dec-

13

Domestic ('000) International ('000)

Istanbul Ataturk Airport Capacity Enhancements

Source: THY presentation

Please see the last page of this report for important disclosures.

28

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

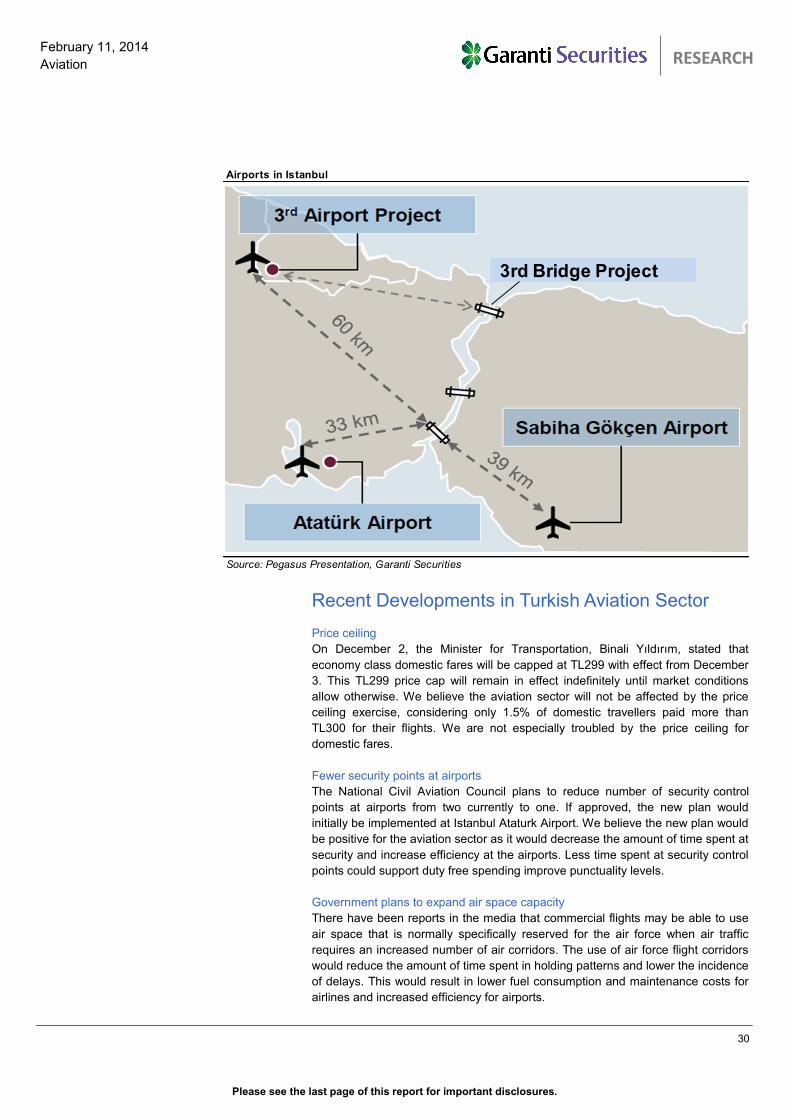

Sabiha Gokcen Airport

Sabiha Gokcen Airport (SAW) is Istanbul’s second airport and the main hub for

Pegasus Airlines. The airport was privatized in 2008 and air traffic has increased

considerably since then, as shown below. The total number of passengers using

the airport has increased at a CAGR of 34% between 2008 and 2013 and reached

to 18.6mn. Although the airport operates with a relatively low capacity (75%), the

DHMI plans to double its capacity to 50mn within the next two years following the

completion of a second runway. Since the planned third airport in Istanbul will be

located further (60km) from the city centre than Sabiha Gokcen Airport (35km), we

believe the attraction of Sabiha Gokcen for air travel will increase going forward.

Furthermore, Sabiha Gokcen is located on the Anatolian side of Istanbul, a more

rapidly developing region of the city compared to the European side.

Source: DHMI

International vs Domestic Passenger('000) in Istanbul Sabiha Gokcen Airport

0

200

400

600

800

1,000

1,200

1,400

Jan-1

1

Feb

-11

Mar-

11

Apr-

11

May-

11

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-11

Nov-

11

Dec-

11

Jan-1

2

Feb

-12

Mar-

12

Apr-

12

May-

12

Jun-1

2

Jul-12

Aug-1

2

Sep-1

2

Oct-12

Nov-

12

Dec-

12

Jan-1

3

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun-1

3

Jul-13

Aug-1

3

Sep-1

3

Oct-13

Nov-

13

Dec-

13

Domestic ('000) International ('000)

Source: DHMI

International vs Domestic Passenger Growth in Istanbul Sabiha Gokcen Airport

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Jan-1

1

Feb

-11

Mar-

11

Apr-

11

May-

11

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-11

Nov-

11

Dec-

11

Jan-1

2

Feb

-12

Mar-

12

Apr-

12

May-

12

Jun-1

2

Jul-12

Aug-1

2

Sep-1

2

Oct-12

Nov-

12

Dec-

12

Jan-1

3

Feb

-13

Mar-

13

Apr-

13

May-

13

Jun-1

3

Jul-13

Aug-1

3

Sep-1

3

Oct-13

Nov-

13

Dec-

13

Domestic International

Domestic average International average

Please see the last page of this report for important disclosures.

29

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

The third airport

In line with the government’s target of Istanbul being an international hub for air

travel, a tender for a 3rd airport in Istanbul was held in May 2013, where the

Cengiz-Kolin-Limak-Mapa-Kalyon consortium submitted the winning bid, offering a

total of EUR22,152mn in rent (EUR26,139mn including 18% VAT) over a period of

25 years (EUR1,046mn per annum). The new airport will be completed in four

phases. Once complete, the airport will have a pax capacity of 150mn. The first

phase, which will have a pax capacity of 70mn, is expected to be completed within

42 months. The Minister of Transportation, Binali Yildirim, recently said that the

construction of the 3rd airport would begin in 1Q14 at the latest. Nihat Ozdemir,

from the winning consortium, stated that the 3rd airport would enter operations by

the beginning of 2019. However, given the current global liquidity conditions and

mounting political turmoil in Turkey, we believe delays in the construction of the

3rd airport project are likely.

Istanbul’s 3rd Airport at a glance…

There will be a pax revenue guarantee for the first 12 years of the concession, as

indicated in the table below. Pax fees are consist of €20 per international outgoing

passenger, €5 per transfer passenger and €3 for each domestic outgoing

passenger transferring to an international flight.

Istanbul's Third Airport 1st phase 2nd phase 3rd phase 4th phase Total

New terminal capacity/passenger per annum 70,000,000 20,000,000 30,000,00 30,000,000 150,000,000

# of terminals 2 1 1 4

Runways 3 1 1 1 6

Taxiways 8 3 2 3 16

Aircraft parking capacity 500

*Phase 4 to be completed by 2027

(mn €) 1 2 3 4 5 6 7 8 9 10 11 12 Total

Rev. guarantee 316 334 351 367 541 563 585 607 628 649 670 690 6,300

Please see the last page of this report for important disclosures.

30

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Recent Developments in Turkish Aviation Sector

Price ceiling

On December 2, the Minister for Transportation, Binali Yıldırım, stated that

economy class domestic fares will be capped at TL299 with effect from December

3. This TL299 price cap will remain in effect indefinitely until market conditions

allow otherwise. We believe the aviation sector will not be affected by the price

ceiling exercise, considering only 1.5% of domestic travellers paid more than

TL300 for their flights. We are not especially troubled by the price ceiling for

domestic fares.

Fewer security points at airports

The National Civil Aviation Council plans to reduce number of security control

points at airports from two currently to one. If approved, the new plan would

initially be implemented at Istanbul Ataturk Airport. We believe the new plan would

be positive for the aviation sector as it would decrease the amount of time spent at

security and increase efficiency at the airports. Less time spent at security control

points could support duty free spending improve punctuality levels.

Government plans to expand air space capacity

There have been reports in the media that commercial flights may be able to use

air space that is normally specifically reserved for the air force when air traffic

requires an increased number of air corridors. The use of air force flight corridors

would reduce the amount of time spent in holding patterns and lower the incidence

of delays. This would result in lower fuel consumption and maintenance costs for

airlines and increased efficiency for airports.

Airports in Istanbul

Source: Pegasus Presentation, Garanti Securities

3rd Bridge Project

Please see the last page of this report for important disclosures.

31

February 11, 2014

Aviation

TURKISH AVIATION SECTOR

RESEARCH

Airline Terminology

Revenue passengers: Revenue passengers represents the total number of paying

passengers flown on all flight segments.

Revenue passenger kilometers (RPK): Revenue passenger kilometers (RPK)

represents the numbers of kilometers flown by revenue passengers

Available seat kilometers (ASK): Available seat kilometers (ASK) represents the

aircraft seating capacity multiplied by the number of kilometers the seats are

flown.

Load factor: Load factor represents the percentage of aircraft seating capacity that

is actually utilized (calculated by dividing RPK by ASK).

Breakeven load factor: Breakeven load factor is the passenger load factor that will

result in passenger revenues being equal to operating expenses.

Aircraft utilization: Aircraft utilization represents the average number of block hours

operated per day per aircraft for the total aircraft fleet.

Block hours: Block hours refers to the elapsed time between an aircraft leaving an

airport gate and arriving at an airport gate.

Yield per passenger kilometer: Yield per passenger kilometer represents the

average amount one passenger pays to fly one kilometer.

Passenger revenue per available seat kilometer: Passenger revenue per available

seat kilometer represents passenger revenue divided by available seat kilometers.

Operating revenue per available seat kilometer (RASK): Operating revenue per

available seat kilometer (RASK) represents operating revenues divided by

available seat kilometers.

Average stage length: Average stage length represents the average number of

kilometers flown per flight.

Operating expense per available seat kilometer (CASK): Operating expense per

available seat kilometer (CASK) represents operating expenses divided by

available seat kilometers.

Wet Lease Arrangement: A wet lease is a leasing arrangement whereby one

airline (lessor) provides an aircraft, complete crew, maintenance, and insurance,

to another airline (lessee), who pays by hours operated. The lessee provides fuel,

covers airport fees, and any other duties, taxes, etc. The flight uses the flight

number of the lessee. A wet lease generally lasts one month to two years,

anything less would be considered an ad-hoc charter. A wet lease is typically

utilized during peak traffic seasons or annual heavy maintenance checks, or to

initiate new routes. Ground handling is usually done by the lessor although this

can vary from country to country. In some cases the lessee provides these

services (or one of its partners).

Please see the last page of this report for important disclosures.

RESEARCH

February 11, 2014

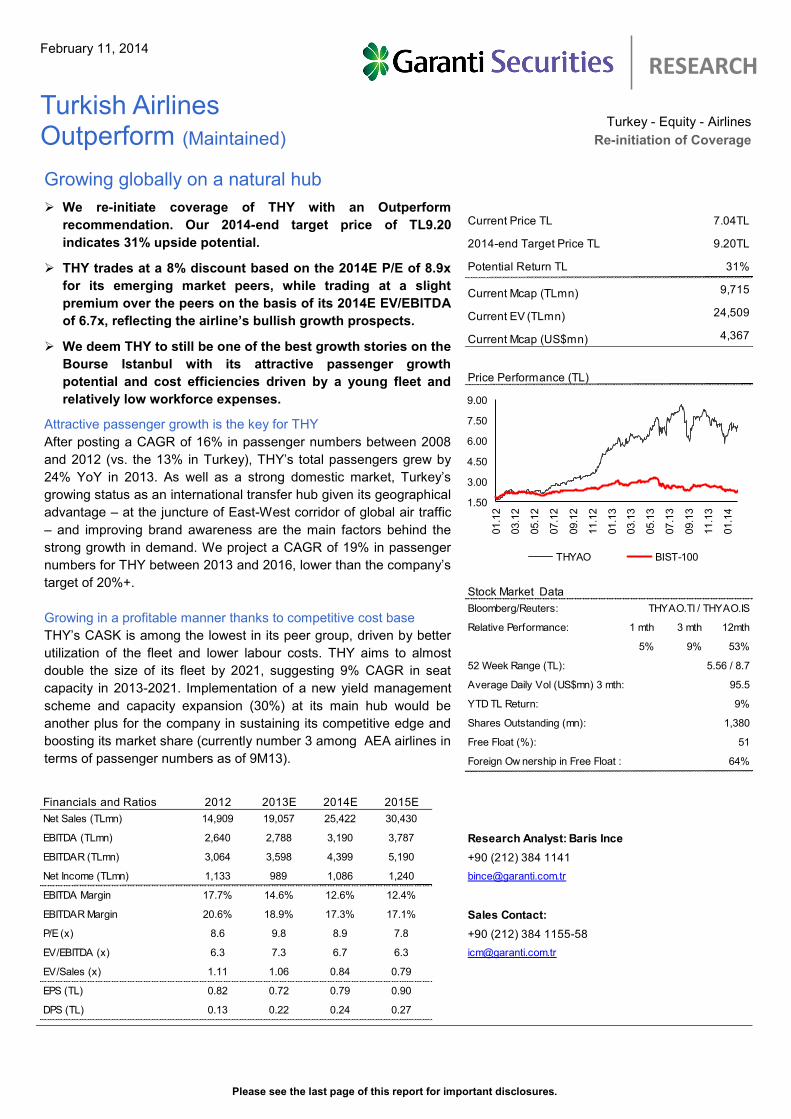

Turkish Airlines Outperform (Maintained)

Current Price TL 7.04TL

2014-end Target Price TL 9.20TL

Potential Return TL 31%

Current Mcap (TLmn) 9,715

Current EV (TLmn) 24,509

4,367

Bloomberg/Reuters:

1 mth 3 mth 12mth

5% 9% 53%

95.5

YTD TL Return: 9%

1,380

Free Float (%): 51

64%

Financials and Ratios 2012 2013E 2014E 2015E

Net Sales (TLmn) 14,909 19,057 25,422 30,430

EBITDA (TLmn) 2,640 2,788 3,190 3,787 Research Analyst: Baris Ince