two words from author -...

TRANSCRIPT

1 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Accounting Standard is the foundation of accounts. We can’t learn

accounts without the use of accounting standards. Accounts without AS is like

breathing without oxygen!

I know many of the students avoid learning accounting standards with the

reason that these are very difficult. What I feel is that the Accounting standards

seems to be difficult not because they are but because they are given in somewhat

difficult language & exactly here the role of the teacher starts.

It is the responsibility of the teacher to make the Accounting standards

easy & create the interest of the students in it. Thus these notes are divided in 2

parts:

1. Conceptual questions to understand the basic concepts in particular

AS & their use,

2. Practical questions to apply these concepts & to get the mastery on

it.

So lets start the journey of knowledge in accounting standards and I am sure

everyone will not only realize the importance of Accounting Standards but also will

start enjoying them and applying them in their studies as well as practical life also.

Remember “The journey of miles starts with the first step only”

Good luck.

CA Yogesh Panchakshari

98820 26393, 2571545

TWO WORDS FROM AUTHOR

2 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

INDEX:

AS No. Accounting Standard Page No.

4 Contingencies & Events Occurring after balance sheet date 3 5 Net Profit Or Loss For The Period, Prior Period Items And Changes In

Accounting Policies 9

11 Effects of changes in foreign exchange rates 14 12 Accounting for government grants 24 16 Borrowing Cost 27 19 Accounting for Leases 39 20 Earnings Per Share 47 26 Intangible Assets 57 29 Provisions, Contingent Liabilities And Contingent Asset 67

3 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

AS-4: CONTINGENCIES AND EVENTS OCCURING AFTER THE BALACNE SHEET DATE

Objective – It gives guidelines of accounting treatment for accounting, contingent assets, and event s occurring after Balance Sheet date.

Conceptual Questions: Q.1 – Mr. Aditya Birla purchased one lottery ticket for Rs. 5 lakhs. He wishes to show the amount as

income receivable in asset side. Comment. Ans – As per AS 4, when outcome of event depends on another uncertain event then it is called as

contingent event. In this case lottery income will be the contingent event. Thus, it can be recorded in the books [Conservatism Concept]

Q. 2 – There is case against ‘A Ltd.’ and accountant is confused whether to record this or not.

Comment. Ans – As per AS4, Contingent Liabilities are divided into three parts

1) Remote liability – Ignore 2) Probable liability – Disclose below Balance Sheet 3) Possible – Create Provision.

An accountant will have to analyze the current provision of liability on the above basis and then he should decide the accounting treatment.

Q.3 – Book of accounts of ‘P Ltd.’ were closed on 31-3-2011 and fire occurred on 7-7-2011. books

accounts sanctioned by board of directors on 1-9-2011. An accountant wish to show fire loss in books of accounts of last year. Comment.

Ans – As per AS4, such event is called as Events occurring after Balance Sheet date. In this case the accounting treatment is suggested as follows-

i) If event was known on the Balance Sheet date but confirmed after Balance Sheet date, then adjust it in last year’s book.

ii) If the event was unknown on Balance Sheet date but confirmed afterwards, then, it can be adjusted in the books but it must be shown as a disclosure.

In the above case, fire breakout after Balance Sheet date and it was unknown on Balance Sheet date. Thus we can give the disclosure below Balance Sheet.

Q4 – The accounting year for Q Ltd. ended on 31-3-2011 but dividend declared on 7-7-2011. can it be

adjusted in the books? Ans – As per AS 4, the dividend cannot be recorded because it was unknown on Balance Sheet but it is

declared as an exception to AS 4 in AS4 itself. Application – In the above case, dividend must be adjusted in books of accounts i.e. at the debit side of P & L Appropriation A/c and provision in the liability side.

4 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Practical Questions:

1. XYZ Ltd. Had written off Rs. 11.50 lakhs of debts of PQ Ltd. Treating the same as bad and doubtful during the year ending on March 3,2005, as the amount was not recovered for last five years. Company is in the process of finalizing the Balance Sheet, XYZ Ltd. Is able to recover the entire amount from PQ Ltd. What treatment should been given to this information in preparation if Balance sheet as on 31.03.2005.

2. During the year 2004, it has been found that there was a loss of goods by theft during the year 2003, valued at Rs. 2,70,000. How would you deal with the above in financial statements for the year 2003 and 2004?

3. ABC Ltd. Prepared its financial statements as on 31.3.04. The following events took place in April, 2004: a. A fire broke out in the premises damaging goods costing Rs. 12,00,000 (salvage value Rs.

3,50,000). b. Dividend proposed by the Board, Rs. 7 per share.

4. Las Ltd. Has received a demand notice on 15.6.03 for Rs. 78,00,000 from the Excise Department in respect of duty payable for several years. The financial statements for the year 2002-03 have been approved in August,2003. In July, 2003, the company has appealed against the demand of Rs. 62,00,000 and the balance has been deposited by it. The company has expected that the demand of Rs.62,00,000 should be reduced to Rs. 27,00,000 only. Show the above in the financial statements for the year 2002-03.

5. In one of the plant of XYZ Ltd., there was a fire on 10.5.04 in which the entire plant was damaged and the loss of Rs. 40,00,000 is estimated. The claim with the insurance company has been filed and a recovery of Rs. 27,00,000 is expected. The financial statement for the year ending 31.3.04 were presented on 30.08.04. Show how should it be shown? What would be the presentation if the financial year ended on 30.6.04?

6. While preparing its final accounts for the year ended 31st March, 2003 a company made a provision for bad debts @ 5% of its total debtors. In the last week of February, 2003 a debtor for Rs. 2 lakhs had suffered heavy loss due to an earthquake; the loss was not covered by any insurance policy. In April, 2003 the debtor became a bankrupt. Can the company provide for the full loss arising out of insolvency of the debtor in the final accounts for the year ended 31st March, 2003?

7. A major fire has damaged the assets in a factory of AS Limited on 2nd April, two days after the year-end closure of account. The loss is estimated at Rs. 20 Crores out of which Rs. 12 crores will be recoverable from the insurers. Explain briefly how the loss should be treated in the final accounts for the previous year.

8. AS Ltd invested Rs. 100 lakhs in April, in the acquisition of another Company doing similar business, the negotiations for which had started during the Financial Year just ended on 31st March. How will this be treated in the final accounts for the year just ended.

9. The company has not made provision for proposed Divided in its accounts but has carried forward the balance on the Profit & Loss Account and proposes to charge the dividend to the Profit & Loss Account when payment is made. Comment.

10. AS Ltd had taken a large-sized civil construction contract, for a public sector undertaking, valued at Rs. 2 crores. In the course of execution of the work on 29th May, the company found while raising the work that it had met a rocky surface and cost of contract would go up by an extra Rs. 50 lakhs, which

5 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

would not be recoverable from the Contractee. The Company’s accounting year had ended on 31st March and the accounts were considered and approved by the Board of Directors on 15th May. How will you treat the above in the accounts for the year ended 31st March.

11. AS Ltd entered into an agreement to sell its immovable property included in the Balance Sheet at Rs. 5 lakhs to another Company for Rs. 20 lakhs. The agreement to sell was concluded on 31st January but the Sale Deed was registered only on 30th April. The Company’s accounting year ended on 31st March and the accounts for that period were considered and approved by the Board of Directors on 15th May. How will you treat the above in the accounts for the year ended 31st March?

12. A Company deals in petroleum products. The sale price of petrol is fixed by the Government. After the Balance Sheet date, but before the finalization of the Company’s accounts, the Government unexpectedly increased the price retrospectively. Can the Company account for additional revenue at the close of the year? Discuss.

13. You are the Auditor of a Manufacturing Company, whose year ends on 31st March. An event occurred after the year ended, but before you complete the audit. The Audit Report issued by you is dated 20th July. The Sales Ledger balance at 31st March was Rs. 95,000. By 20th July Rs. 65,000 only had been received against this amount as full and final payment. How will you deal with the above?

14. These was a Government Notification in June 20x1 increasing the limit for gratuity payment with effect from 24th September 20x0. The accounts were approved by the Board of Directors in July 20x1. The Board of opines that since the change took place after the Balance Sheet Date, no effect should be given to it in the Financial Statements for the year ended 31st March 20x1. Is the view correct?

15. AS Ltd wants to adjust the bank balance on the Balance Sheet Date by reversing the entry for a cheque issued in the normal course of business and cancelled after the year-end but before the finalization of accounts. The cheque was returned on the ground that the signature differs. Give your views on the above.

16. A Limited Company closes its accounts on 31st March every year. It issued a cheque in favour of one of its customers towards the refund of advance in January. In July, the customer returned the cheque to the Company without presentation to the Bank while accounts of the Company for that year were being finalized. Since the cheque was cancelled, the reversal entry was passed in the books of accounts as on 31st March with a view to disclose the correct balance as on that date, instead of showing the Bank Balance lower by treating the cheque as “issued but not encashed as on 31st March.” Whether the reversal entry passed in the books of accounts of the Company as on 31st March was proper since the cheque was cancelled before closing of the accounts for the year?

17. You are an accountant preparing accounts of AS Ltd. As at 31st March. After the end of the year, the following events took place in April. • A fire broke out in the premises damaging, uninsured stock worth Rs. 10 lakhs (Salvage Value

Rs. 2 lakhs) • A suit against the Company’s advertisement was filed by a party claiming damage of Rs. 20

lakhs. • Dividend proposed at 20% on Share Capital of Rs. 100 lakhs.

Describe, how the above will be dealt with in the accounts for the year ended 31st March.

18. The Financial statement of Construction Limited for the year ended 31st March, 2008 were considered and approved by the board of directors on 20th May, 2008.

6 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

The company was engaged in construction work involving Rs. 10 core. In the course of execution of work, a portion of factory shed under construction came crashing down on 30th May, 2008. Fortunately, there was no loss of life, but the company will have to rebuild the structure at an additional at an additional cost of Rs. 2 crores which cannot be recovered from the contractee. How should this event be reported?

Q. No. Answer Hints

1

2

3

4

5

6

7

7 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

8

9

10

11

12

13

14

15

16

8 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

17

18

9 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

AS-5: NET PROFIT OR LOSS FOR THE PERIOD, PRIOR PERIOD ITEMS

AND CHANGES IN ACCOUNTING POLICIES

Conceptual Questions:

Objective – To give guidelines for – i) Finding up appropriate profit of current year ii) Dealing with

prior period items and iii) Dealing with changes in items.

Q. 1 – Mr. Ajay is finalizing his books of accounts and he found that there was loss by theft of Rs.

500. considering small amount, he added it in miscellaneous expenses, comment.

Ans – As per AS5, Net Profit of every fanatical year must be calculated by showing ordinary and extra

ordinary items separately.

Analysis – In the above case, even if amount is small, loss by theft is an extra ordinary item and must

be shown separately thus above accounting treatment is incorrect.

Q. 2 – Your client Mr. Ambani showed Bad Debts of Rs. 30 lakhs in 2009-10. but amount is recovered

in 2011—12. he has credited this amount in general income of 2009-10. Comment.

Ans – As per AS 5, if any adjustment is done in current year due to adjustment of earlier year’s mistake,

then it is called as prior period items and it should be record in current year separately.

Analysis – In above case Mr. Ambani should credit P & L A/c of year 2011-12 and not the year 2009-

10. It should be shown separately as prior period item.

Q. 3 – In year 2011-12, Mr. Ratan Tata made provision for doubtful debts @ 10%. But after year end it

is needed at 12% p.a. Comment.

Ans – As per AS 5, such provision is called as estimate and such change is called as changes in estimates.

It should be adjusted in Financial Year.

Analysis – In above case even if Mr. Tata realized change estimate after year end, still he must

adjust it in Financial Year 2011-12.

10 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Practical Questions:

1. Show the presentation of following items in the financial statements : a. Last year, stock was overvalued by Rs. 5,30,000. b. Insurance claim lodged last year but received in current year, Rs. 1,20,000. c. Change of method of valuation of raw material inventory from FIFO to weighted average method.

2. Show the presentation of following items in the financial statements : a. Payment of expense of Rs. 1,10,000 for previous year. It was not recorded last year due to

oversight. b. A debtor was considered bad and full provision for doubtful debt was created. In the current year,

however, a part of the total amount has been recovered. c. An employee retired last year from the firm. He lodged a claim in the court of law for Rs. 7,20,000

in the current year. Court’s verdict may come in current year or may be declared in future years.

3. X Ltd. Is a regular buyer of goods from Y Ltd. Under an agreement, 50% of the order amount is payable in advance and balance 50% is payable at the time of delivery. In case, the delivery is not taken within 15 days of intimation, the buyer has to pay Rs. 1,000 per day as storage charges to the seller, In the past, whenever such charges were paid, were included in the valuation of inventory. However, in the current year, X Ltd. Has decided not to include this expense as a part of inventory value, but as a general expense. Comment.

4. RST Ltd. Has a policy of providing 10% provision for doubtful debts on the gross value of debtors. In the current year also, it has applied the same policy. However, it has created an additional provision of Rs. 60,000 (over and above 10%) in respect of a debtor which is outstanding for more than one year and it is expected that he may be declared insolvent. It is a change in accounting policy? Comment.

5. Whether disclosure of advances / receivable written back / written off is necessary even if the amount involved does not exceed 1% of the revenue?

6. The company found in 2002-2003 that stock sheet as on 31.03.2002 had included twice an item of Rs. 1,97,221/-. How will this be dealt with, in the books?

7. ABC Ltd. Was making provision for non-moving stocks based on no issues for the last 12 months upto 31.3.2002. The company wants to provide during the year ending 31.3.2003 based on technical evaluation: Total value of stock Rs. 100 lakhs Provision required based on 12 months issue Rs. 3.5 lakhs Provision required based on technical evaluation Rs. 2.5 lakhs Does this amount to change in accounting policy? Can the company change the method of provision?

8. State, how you will deal with the following matters in the accounts of U Ltd. For the year ended 31st March, 2003 with reference to Accounting Standard: a. The company finds that the stock sheets of 31.3.2002 did not include two pages containing

details of inventory worth Rs. 14.5 lakhs.

9. State briefly the duty of an auditor with a regard to each of the following: a. A sum of Rs. 10,00,000 is received from an insurance company in respect of a claim for loss a

goods in transit costing Rs. 8,00,000. The amount is credited to the Purchases Account. b. A loss of Rs. 2,00,000 on account of embezzlement of cash was suffered by the company and it

was debited to Salary Account.

11 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

10. As a Company Auditor how would you react to the following situations?

a. Sale value of scrap items adjusted miscellaneous expenditure. b. Insurance claim of Rs. 2 lakhs received stands included under miscellaneous income.

11. Sagar Limited belongs to the engineering industry. The Chief Accountant has prepared the draft accounts for the year ended 31.03.2006. You are required to advise the company on the following items from the viewpoint of finalization of accounts, taking not of the mandatory accounting standards. An audit stock verification during the year revealed that the opening stock of the year was understated by Rs. 3 lakhs due to wrong counting.

12. In preparing the financial statements of R Ltd. For the year ended 31st March, 1998 you come across the following information. State with reasons, how you would deal with them in the financial statements- There was a major theft of stores valued at Rs. 10 lakhs in the preceding year, which was detected only during the current financial year (1997-98).

13. As an auditor state your views on the following situations : Y Ltd. Provided Rs. 25 lakhs for inventory obsolescence in 1998-99. In the subsequent year, it was determined that 50% of such stock was usable. The company wants to adjust the same through prior period adjustment account as the provision was made in the earlier year.

14. In the context of relevant Accounting Standards, give your comments on the following matters for the financial year ending on 31.3.2002. While preparing its final accounts for the year ended 31st March, 200 Rainbow Limited created a provision for Bad and Doubtful debts at 2% on trade debtors. A few weeks later the company found that payments from some of the major debtors were not forthcoming. Consequently the company decided to increase the provision by 10% on the debtors on 31st March, 2002 as the accounts were still open awaiting approval of the Board of Directors. Is this to be considered as an extraordinary items or prior period item?

15. What will be the treatment of the following in the final statement of account for the year ended 31st March, 1995 of a limited company? Revision in the salary, effective 1st April, 1994, would cost the company an additional liability of Rs. 3,00,000 per annum.

16. M/s. Dinesh & Company signed an agreement with workers for increase in wages with retrospective effect. The out-flow on account of arrears was for 2005-06 – Rs. 10.00 lakhs, for 2006-07 – Rs. 12.00 lakhs and for 2007-08 – Rs. 12.00 lakhs. This amount is September, 2008. The accountant wants to charge Rs. 22.00 lakhs as prior period charges in financial statement for 2008-09. Discuss.

Q. No. Answer Hints

1

12 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

2

3

4

5

6

7

8

9

10

13 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

11

12

13

14

15

16

14 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

AS-11: EFFECTS OF CHANGES IN FOREIGN EXCHANGE RATES

Objective – To give guidelines for accounting of effect of change in foreign exchange rates

Conceptual Questions: Q. 1 – What are three types of Forex Dealings? Ans – Provision of AS11: All the business transactions in for-ex terms are divided in three parts as follows –

Sr. No.

Type Explanation Difference transferred

to 1. Forex Transaction These are day to day transactions in for – ex. E.g.

sales/purchases in for-ex P&L A/c

2. Forex operation i) Integral - These are dependant branches in abroad. P&L A/c ii) Non-Integral Independent branches in abroad. For-ex

Reserve A/c

3. Forward Contract. These are the contracts which are entered in today’s date but to be completed on future date at the rates decided today.

P&L A/c

Q. 2 – Mr. Ajay purchased goods for $1000 on 1/1/2011. When rate was Rs. 40 per $ amount to be

transferred after 4 months i.e. 30/4/2011. Year ending 31/3/2011. He made forward contract to purchase dollar at Rs. 44/$ it means he will pay extra Rs. 4/$ for 1000 dollars. What is accounting treatment?

Ans – Provision of AS11: Such extra payment of Rs. 4000 is called as differed discount. It is for 4 months of which, 3 months are in current year and remaining in next month. Application of AS11: Ajay should record Rs. 4000 in asset side as differed discount ¾th is transferred to current year and remaining Rs. 1000 in next year.

Practical Questions:

1. A company had imported raw materials worth US dollars 250,000 on 25th January, 2005 when the

exchange rate was Rs. 46 per US dollar. The company had recorded the transaction at that rate. The payment for the imports was made only on 15th April,2005 when the exchange rate was Rs.49 per US dollar. However on 31st March 2005, the rate of exchange was Rs. 50 per UD dollar. The company passed an entry on 31st March,2005 adjusting the cost of raw materials consumed for the difference between Rs. 49 and Rs.46 per US dollar.

2. ABC Ltd. of India has taken a loan few years back. An amount of $ 1,00,000 is due for payment after 3 months. It enter into a forward cover for the period of 3 moths @ Rs.47.90, whereas the spot rate on the date of contract was Rs. 47.10. How should it be recorded by ABC Ltd.

15 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

3. The company has adopted and followed the following accounting policy:”In respect of foreign currency transactions, current assets and current liabilities are revalued at year end rates. However, if there is net loss due to exchange difference, the same is charged off to the profit and loss account but if there is net gain the same is ignored in view of the prudent accounting principle of not recording unrealised gains due to exchange rate fluctuations”. Comment on the appropriateness of above.

4. Exchange Rate Goods purchased on 24-2-2005 of US $ 10,000 Rs. 46.60 Exchange Rate on 31-3-2005 Rs. 47.00 Date of actual payment 5-6-2005 Rs. 47.50 Calculate the loss/gain for the financial years 2004-2005 and 2005-2006.

5. A.S. Ltd. (Delhi) has a branch in Sydney, Australia. At the end of 31st March,2005 the following ledger balances have been extracted from the books of the Sydney office.

Sydney (Australia dollars thousand) Debit Credit Plant & Machinery(Cost) 200 -- Depreciation on Plant & Machinery(Accumulated) -- 130 Debtors / Creditors 60 30 Stock (1-4-2004) 20 -- Cash / Bank balance 10 -- Purchases / Sales 20 123 Goods sent to branch 5 -- Wages and Salaries 45 -- Rent 12 -- Office Expenses 18 -- Commission Receipts -- 100 Branch / H.O. Current A/c -- 07 ------------------------------------- 390 390

------------------------------------- The following information is also available: Goods sent by H.O. Rs.100 thousand. Branch A/c. In H.O. Rs. 120 thousand. Stock at 31-3-2005, Sydney Branch Australia $ 3,125, you are required to convert the Branch Trial Balance into Rupees: (use the following rate of exchange: Opening rate A $=Rs. 20 Closing rate A $=Rs. 24 Average rate A $=Rs. 22 which approximate the actual exchange rate. For fixed assets A $=Rs. 18) Required: Translate the branch trail balance if it is classified as- a: Integral foreign operation. b: Non-integral foreign operation.

6. Comment: The account of a foreign branch is incorporated in the head office books at a standard rate and a resultant notional profit is credited to the head office profit and loss account.

7. A.S. Ltd. imported a machine on 04.01.1999 for Euros 12,000 on deferred payment basis;

16 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Payment in six equal annual installments at the end of every financial year, commencing from 31.03.1999 onwards. Use Revised AS 11 provisions irrespective of financial year / date and determine the exchange differences and carrying amount of the liability at the end of each financial year, if the following exchange rates are given. One Euro equals Indian Rupees on

04.01.1999 31.03.1999 31.03.2000 31.03.2001 31.03.2002 31.03.2003 31.03.2004

Rs. 50,4872 Rs. 45.5208 Rs. 41.8463 Rs. 41.0175 Rs. 41.6400 Rs. 51.4400 Rs. 53.1000

8. Distinguish between Integral Foreign operation(IFO) and Non-Integral Foreign Operation (NOF).

9. An exporter has $50,000 due in 6 months. Rate on the date of sale 1st January, Is Rs.47. The

forward rate offered is Rs.47.50. Year ends on 31st March when the exchange rate was 47.20. On settlement date i.e. 30th June was 47.60. Show the accounting including for forward contract. (it is a forward contract to sell the foreign currency).

10. A party enters forward contract for trading or speculation. Contract is to sell $1,00,000 due on 30.6 @ Rs.47.50. Today (1st January) spot rate is Rs.47. On 31st March (i.e. at year end) the forward contract for 3 months (i.e. remaining maturity period up to 30.6) to sell $ is available at Rs. 47.55 rate on 30.6 is Rs. 47.60. Account for the transactions.

11. A.S. Ltd. has a branch in the US. The company has so far recorded goods sent to the branch and amount received there from. At the end of the year the branch has sent a detailed statement which should be incorporated in the accounts of the company.

Trial Balance as on 31.03.2005 Rs. in ‘000 Head Office Trial Balance Dr. Cr.

Share Capital General Reserve Profit & Loss A/c Foreign Currency Loan ($ 10 million) Sales Transfer to Branch Branch Account( Sales minus Cash Received $ 2 million=117.5) Purchases Opening Stock Tangible Fixed Assets Accumulated Depreciation Debtors Cash and Bank Balances Closing Stock

82.25 1000.00 20.00 500.00 300.00 22.75

100.00 500.00 10.00 470.00 600.00 200.00 45.00

1925.00 1925.00 25.00

Rs. ‘000 US $

17 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Branch Trial Balance Dr. Cr.

Transfer From HO Expenses Tangible Fixed Assets Accumulated Depreciation HO Account Bank Balance Sales Closing Stock-Cost Closing Stock-net realizable value

4.26 3.00 2.00 0.50

0.50 2.26 7.00

9.76 9.76

1.00 1.02

Other Information: Exchange Rates- A: When foreign currency loan was taken by the company US $ 1=47. B: When tangible fixed assets were acquired US $ 1=45. C: When closing stock was acquired US $ 1=47.47. D: Closing Stock exchange rate US $ 1=47.50. E: Details of Sales and expenses: (Translation is carried actual rates) F: Current year depreciation for Branch in Rs. ‘000.25. Prepare Translated Branch Trial Balance, P & L A/c. And Balance Sheet of company on a whole as at 31.03.2005.

12. Frequently Asked Questions on AS 11 notification- Companies (Accounting Standards) Amendment Rules, 2009 (G.S.R.225(E)dt.31.3.09)issued by Ministry of Corporate Affairs

Sales In ‘000 US $ Exchange Rate In ‘000 US $

1 2 3 4 5 Expenses 1 2 3 4 5

2 1 1 2 1

47.50 47.40 47.20 47.10 47.05 47.40 47.30 47.25 47.18 47.10

95.00 47.40 47.20 94.20 47.05

7 330.85 0.50 0.90 0.60 0.50 0.50

23.70 42.57 28.35 23.59 23.55

3.00 141.76

18 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

ASB Guidance in the form of FAQs on AS 11 notification- Companies (Accounting Standards) Amendment Rules,2009(G.S.R.225(E)dt.31.3.09)issued by Ministry of Corporate Affairs does not form part of the Standard. The purpose of this Guidance is to illustrate and to assist in clarifying the application on the notification. 1:The notification uses the term ‘depreciable capital asset’. What is meant by the term ‘depreciable capital asset’ as none of the accounting standards use this terminology?

13. Would the notification cover exchange difference including those arising in terms at paragraph 36 of the Standard which deals with the forward exchange contracts?

14. Which other category of long term monetary assets would be covered apart from the depreciable capital asset? For example will this cover Fixed Deposits with a foreign bank held for more than 12 months as well as the amount payable for a period exceeding 12 months?

15. Will the assets acquired in India by payment in foreign currency also be covered by the notification? If this presumption is correct will it contradict the requirements of Schedule VI to the Companies Act 1956?

16. The exemption provided by the notification is in respect of those items which are covered in paragraph 15 which deals with monetary items that in substance from part of the net investment in a non-integral foreign operation of the enterprise. Whether the monetary items in case of integral foreign operation will be covered by the notification?

17. How the transaction account under head ‘Foreign Currency Monetary Item

Translation Difference Account’ is to be amortised?

18. Will exercising the option under the Companies (Accounting Standards) Amendment Rules, 2009 be a change in the accounting policy?

19. Is the option once exercised irreversible? If an enterprise does not want to adopt the treatment as per the new paragraph, can it do so? Can it exercise the option?

20. What will be the status of the ICAL announcement regarding derivatives? Will derivatives also be valued on the basis of this notification or the announcement of ICAI would continue to be applicable?

21. Will the recognised of income and expense in accordance with the notification be treated as an item of unusual nature referred to in paragraph 12 and 13 of AS 5?

22. Will assets acquired from foreign currency monetary item that are not depreciated but amortised be included?

23. In case the foreign currency monetary item is not fully utilised for acquisition of fixed assets, then will proportionate adjustment be permissible in the fixed asset cost and balance of exchange fluctuation will be adjusted to Foreign Currency Monetary Items Transaction Difference Account?

24. If the long term foreign currency monetary item is received in installment whether the installment received within a period of 12 months should be treated as short term in nature?

25. How ‘Foreign Currency Monetary Item Translation Difference Account’ should be presented in the Balance Sheet?

19 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

26. Does this notification apply to exchange difference arising on forward exchange contracts entered into to hedge the foreign currency risks of future transaction in respect of which firm commitments are made or which are highly probable forecast transactions or only to forward contracts foreign currency items included in Para 36 of AS 11?

27. Whether the notification applies to non-corporate entities which are not covered by Companies Act?

28. Does the notification also apply to those exchange differences which are regarded as an adjustment to interest costs in term of paragraph 4(e) of Accounting Standard (AS) 16, Borrowing Costs?

29. Should we capitalize exchange differences arising on settlement of long term foreign currency monetary items?

30. The notification refers to the acquisition of depreciable capital assets. Will it include the self constructed assets and acquired by other means?

31. Suppose a company has got two separate long term foreign currency monetary Items; one for use in connection with acquisition of a depreciable asset and second for use in working capital. Should the treatment suggested in the notification be followed only for acquisition of depreciable assets?

32. If capitalisation of exchange difference results in carrying value greater than recoverable amount. Is it permissible?

33. If the company exercises the option, what are the implication on current tax and deferred tax?

34. What are the disclosures to be furnished in the financial statements if the option Is exercised?

Q. No. Answer Hints

1

2

3

4

20 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

5

6

7

8

9

10

11

12

13

21 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

14

15

16

17

18

19

20

21

22

22 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

23

24

25

26

27

28

29

30

31

23 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

32

33

34

24 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

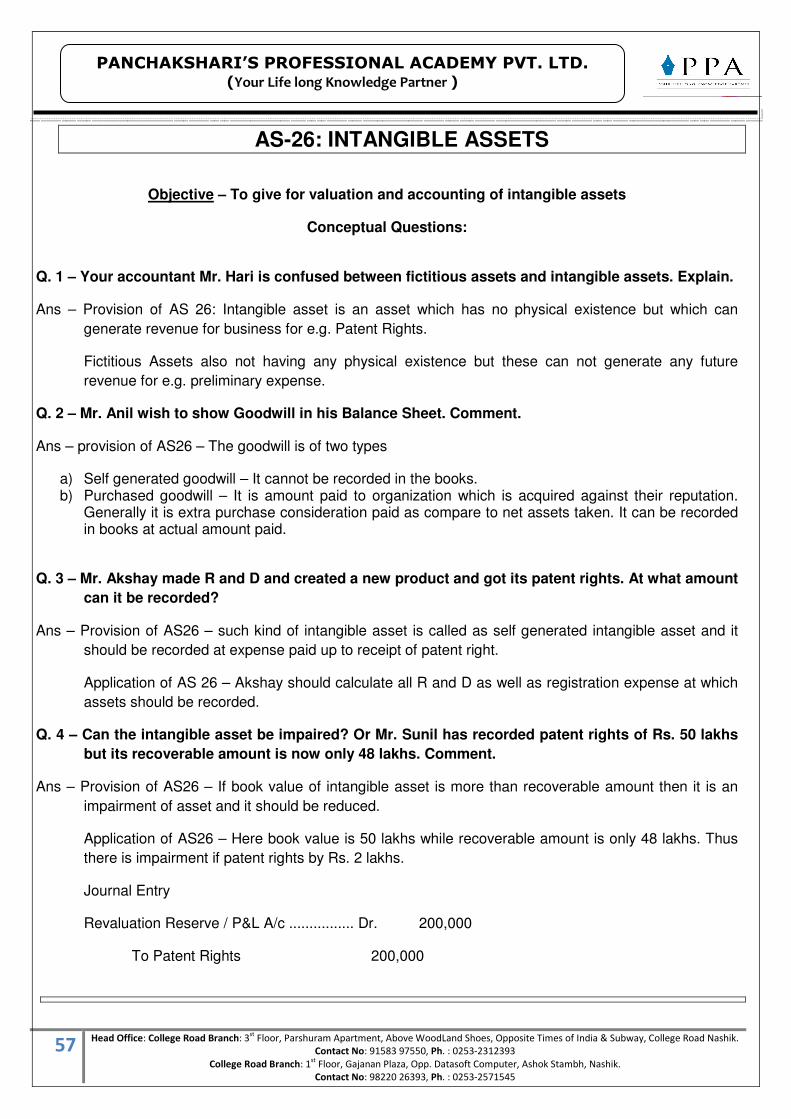

AS-12: ACCOUNTING FOR GOVERNMENT GRANTS Objective – To give guidelines for grants received for government in cash or kind.

Conceptual Questions: Q. 1 – A Ltd. received Rs. 20 lakhs from government grant for machine costing Rs. 50 lakhs.

Depreciation @ 10% p.a. straight line. Show accounting treatment Ans - Machinery A/c ................ Dr. 50 To Bank A/c 30 To Government Grant 20

Every year depreciation will be 10% of 50 lakhs i.e. 5 lakhs debited to Profits and losses A/c and 10% of Government Grant i.e. 2 lakhs per annum will be transferred to P&L credit side.

Q. 2 – B Ltd. received 5 lakhs as government grant for building and 20 lakhs for regular operation.

Where the grant will be recorded? Ans – Provision of AS 12 – Government grant received for building is capital receipt.

Application of AS12 – 1st Grant will be received in Liability side while second grant in income side. Q. 3 – Government sanctioned grant for 20 lakhs to C Ltd. but signature of minister is due. Can it be

recorded in the books? Ans – Provision of AS9 and AS12 – As per AS9 any income cannot be recorded unless its amount legal

claim is confirmed. Thus as per AS12, government grant can’t be recorded unless all formalities are completed. Application of AS12 – C Ltd. should not record government grant in above situation

Q. 4 – B Ltd. in Q. 2 failed to complete formalities thus received letter from government to repay

entire government grant. Show accounting effect Ans – Provision of AS12 – If government grant is to be refunded then all effects must be cancelled.

Application of AS 12 – In above case b Ltd. will have to i) Repay 100% government grant ii) Cancel balance of government form liability side. iii) Reversed depreciation on granted portion of asset. iv) Reversed portion of government grant which was credited to P&L A/c earlier.

Q. 5 – D Ltd. received one asset worth Rs. 50,000 free of cost from government. Life = 5 years. Give

accounting treatment. Ans - Asset A/c ................ Dr. 50,000 To Government Grant 50,000

Every year depreciation of Rs. 10,000 will be debited to profit and loss A/c and government grant Rs. 5,000 will be transferred to revenue i.e. P&L A/c credit side i.e. Depreciation Tax shield will be unavailable.

Practical Questions:

1. Mukund Mehta Nath and Co. Ltd., purchased a fixed asset of worth Rs.64 lakhs. Expected useful life is 10 years and expected residual value is Rs.10 lakhs. The purchase of the asset was supported by Government Grant to the extent of Rs.25 lakhs. The company follows Income Approach, in accounting for government grants. Required:

25 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

A: The amount of Government Grant brought over to P & L for each of the first five years. Assume that the asset was purchased on the first day of the accounting Period and grant was also received on that date. B: The Company changes the method of depreciation from WDV to SLM in 6th year (i.e. after completion of full five years). Advise how the change in the method of Depreciation will be given effect to in the books, and also explain the treatment For grant, when this change in depreciation method takes place.

2. Explain the treatment of the following: A: A firm acquired a fixed asset for Rs.250 lacs on which the government grant Received was 40%. B: Capital subsidy received from the central government for setting up a plant in The notified backward region. Cost of the plant Rs.300 lacs, subsidy received Rs.100 lacs. C: Rs.50 lacs received from the state government for the setting up of water treatment plant. D: Rs.25 lacs received from the local authority for providing medical facilities to The employees.

3. RST Ltd. set up a plant at a cost of Rs.360 lacs with an expected life of 9 years. The company

received a grant from the state government, of Rs. 80 lacs which was to be utilized after fulfilling certain conditions. The company treated this grant as a deferred income. The company could not fulfill the condition and the grant was to be refunded. At the time of refund, balance in the deferred income was Rs.72 lacs, and the balance of the Plant A/c was Rs.280 lacs. What should be the treatment of refund of Grant? In case, the grant was deducted from the cost of plant and a residual value of Rs.10 lacs was expected after a life of 9 years, what would be the treatment of refund of grand?

4. A limited company has set up its business in a designated backward area which entitles it to receive, as

per a public scheme announced by the GOI, a subsidy of 15% of the cost of investment. Having fulfilled all the condition laid down under the scheme, the company on its investment of Rs.100 lakhs in capital assets during its accounting year ending on 31st March,1995 received a subsidy of Rs.15 lakhs in January 1995 from GOI. The account of the company would like to record the receipt as an item of revenue and to reduce the losses on P & L for the year ended 31st March, 1995, is his action justified?

5. Top & Top Limited has set up its business in a designated backward area which entitles the company to receive from the Governments of India a subsidy of 20% of the cost of investment. Having fulfilled all the conditions under the scheme, the company on its investment of Rs.50 core in capital assets, received Rs.10 core from the Government in January, 2005 (accounting period being 2004-05), The company wants to treat this receipt as an item of revenue and thereby reduce the losses on profit and loss account for the year ended 31st March, 2005. Discuss.

Q. No. Answer Hints

1

26 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

2

3

4

5

27 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

AS-16: BORROWING COSTS

Objective – To give guidelines for accounting treatment of cost paid against borrowings e.g. interest

on loan.

Conceptual Questions:

Q. 1 – A Ltd. took a loan of Rs. 10 lakhs on 1/4/2001 for construction of office building @ 10% p.a.

Building was ready to use on 1/10/2003 but actual use started form 1/4/2004. What is

accounting treatment of interest up to 31/3/2007.

Ans – Provision of AS16 – In case of borrowing cost against qualifying asset

a) Interest up to asset being ready to use must be capitalized. b) Thereafter interest must e treated as revenue expense

Application of AS16 – Points are given below

a) For 1st 25 years (between 1/4/01 and 1/10/03) was under construction thus interest of Rs. 2.5 lakhs must be capitalized (10L X 10% X 2.5 yrs.)

b) Fore remaining 3.5 years interest of Rs. 3.5 lakhs must be treated as revenue expense i.e. debited to P&L A/c.

Q. 2 – Mr. Ajay paid Rs. 30 lakhs to acquire patent rights for which he took loan when product was

under-construction. Can apply AS16.

Ans – Provision of AS 16 – AS is applicable to qualifying assets which means an asset which takes

considerable time span for its completion thus it is applicable to tangible as well as intangible assets.

Application of AS 16 – Ajay can apply AS 16 for patent right also.

Q. 3 – Anil took a loan of Rs. 20 lakhs @ 10% p.a. for construction of two office buildings.

On1/4/2007, first building completed on 31.3.2009, second on 31/3/2010. What is treatment of

interest up to 31/3/11?

Ans – Provision of AS16 – If loan is taken for variety of assets, then its capitalization should stop when the

building was completed proportionately.

Application of AS16:

Year Building under

construction

Building

complete

Interest

capitalized

Revenue

interest

07-08 2 0 2 lakhs -

08-09 2 0 2 lakhs -

09-10 1 1 1 lakhs 1 lakhs

10-11 0 2 0 2 lakhs

28 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Q. 4 – Mr. X took loan on 1/7/11 but construction of building was stopped for 7 months and started

back and still continued. Can be capitalizing interest of all 12 months as on 31/3/2012.

Ans – Provision of AS 16 – If construction is stopped due to normal reason, there capitalization should be

continued. But if it is due abnormal reason like strike, court case etc. then interest of that period

should be treated as revenue expense.

Q. 5 – Airtel Ltd. got licence for Mumbai on 1/4/2001 it took the loan on some date and started

digging of roads, and installing towers which was completed on 31/3/2002. Service actually

started form 1/9/2001 up to which period capitalization should be done.

Ans – The Company started installing tower and digging roads form 1/4/2001. It means use of its license

was already been started form 1/4/2001. Thus interest can not be capitalized and whole interest

must be treated as revenue expense.

Practical Questions:

1. Comment on the following Notes on Accounts:

I. Interest on loans from financial institution and a debenture issue made for the purpose of a particular plant, amounting to Rs. 200 lacs has been capitalized.

II. Interest on bridge loan from banks taken for a particular plant, amounting to Rs. 150 lacs has been capitalized and added to the cost for the project. This amount of interest includes interest of Rs. 25 lacs appropriated for the funds used for other purpose.

III. Interest cost on loans taken for construction of a captive power plant has been IV. The company has taken a loan for meeting the requirement of liquor business. It takes a period of few

years for brewing the liquor. Its included all costs of brewing and interests on loans in the valuation of inventory of liquor.

2. A.S. Ltd. has taken loan Rs. 500 lacs for up-gradation of its plant. Out of the said loan, Rs. 350 lacs has been spent on the plant during the year and balance Rs. 150 lacs have been used for the general working capital requirement of the company. The total interest cost fort he period amounted to Rs. 70 lacs. Advise the company in respect of capitalization of interest.

3. A.S. Ltd. has taken a loan of Rs. 20 lacs which has been used to buy trees. The average remaining period for the maturity of tree, to be sold as timer, is three years. The company wants to include the interest cost for the period of three years in the inventory cost of timber. Comment.

4. A.S. Ltd. is establishing an integrated steel plant consisting of four phases. It is expected that the full plant will be established over several years, but pending that, Phase l and Phase ll would be started as soon as they are completed. Following is the detail of the work done on the different phases of the plan during the current year.

Phase l Phase ll Phase lll Phase lV Cash expenditure Rs.20,00,000 Rs.35,00,000 Rs.25,00,000 Rs.40,00,000 Plants Purchased 28,00,000 40,00,000 30,00,000 48,00,000 Total expenditure 48,00,000 75,00,000 55,00,000 88,00,000 Total expenditure 2,66,00,000 Loan taken @ 16% 2,40,00,000 During current year, Phase l and ll have become operational. Find out the amount to be capitalized and to be expensed during the year.

5. Following information is available from the records of A.S. Ltd. in

respect of a project on which the work started on 1-1-03 Capital expenditure incurred for the project till 31-12-03 Rs. 8,00,000

Borrowings from bank @ 15% (with effect from 1-1-03) 3,00,000

29 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

Assets transferred to project during the year, 2004 2,00,000 Expenses incurred during the year, 2004 1,25,000 Payments received during the year from the client 8,20,000

Additional borrowing for the project @ 16% (on 1-1-04) 2,00,000 Find out the borrowing costs to be capitalized during the years, 2003 and 2004.

6. A.S. Ltd. is working on a new project for which a construction period of 2 years has been planned. The work started on 1-1-04. The company has availed bank loan from time to time in general. It has taken loan for this new project also. Following details are available regarding the loan, for the year 2004.

Date Loan Purpose 1-1-04 16% Rs. 10,00,000 General Requirement 1-7-04 15% Rs. 8,00,000 Plant for the new project 1-10-04 14% Rs. 6,00,000 General Requirement The company has incurred expenses of Rs. 50,000 for general purpose and Rs. 1,20,000 in respect of the new project. Both these expenses qualify as borrowing costs to be capitalized. The qualifying assets at the end of year 2004 are: New projects Rs. 11,00,000 Other assets 3,00,000 Buildings 4,00,000 Find out the amount of borrowing costs to be capitalized for different assets for the year 2004.

7. A.S. Ltd. took a loan of USD 20,000 at 6% p.a. on 1st April, for a specific capital expansion project. The interest was payable annually. The exchange rate at the date of the loan was 1 USD = Rs. 45.00. However, the Company could have taken a corresponding Rupee Loan from Banks at 12% p.a. on that date. At the end of the year, the exchange rate was 1 USD = Rs. 48.00. How will you treat the Borrowing Costs and exchange differences in the above case?

Analyse the impact of the following changes independently. What would be the accounting treatment if the Rupee Loan were to carry interest at 14%p.a.? What will be the treatment if the exchange rate at the end of the year were 1 USD =Rs. 46.00?

8. A Co. Has generally borrowed funds and used the funds to acquire assets also. How should the amount of borrowing cost eligible for capitalisation be determined?

9. Paras Ltd. had the following borrowings during a year in respect of capital expansion. Plant Cost of Asset Remarks Rs. Plant P 100 lakhs No specific borrowings Plant Q 125 lakhs Bank loan of Rs. 65 lakhs at 10 % Plant R 175 lakhs 9% Debentures of Rs. 125 lakhs were issued. In addition to the specific borrowings stated above, the company had obtained term loans from two banks (1) Rs. 100 lakhs at 10% from Corporation Bank and (2) Rs. 110 lakhs at 11.50% from State Bank of India, to meet its capital expansion requirements. Determine the amounts of borrowing costs to be capitalized in each of the above Plants, as per AS-16.

10. Unique Ltd. had purchased during the year, a ship on deferred payment basis, payable over next 10 years. The Company has computed the interest payable over these 10 years and debited Interest Suspense A/c. Every year, 1/10th of the same is written off to P&L Account, treating the same as Deferred Revenue Expenditure. Comment.

11. A.S. Ltd. has obtained Institutional term loan of Rs. 580 Lakhs for modernisation and renovation of its Plant & Machinery. Plant and Machinery acquired under the modernisation scheme and installation completed on 31st March amounted to Rs. 406 lakhs, Rs. 58 lakhs has been advanced to suppliers

30 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

for additional assets and the balance loan of Rs. 116 lakhs has been utilised for Working Capital purpose. The Accountant is in a dilemma as to how to account for the total interest of Rs. 52.20 lakhs incurred during the year, on the entire Institutional Term Loan of Rs. 580 lakhs. Give your views.

12. The Notes to Accounts of Gopal Ltd for the year ended 31st March includes the following – “Interest on Bridge Loan from Banks and Financial Institutions and on Debentures specifically obtained for the Company’s Fertilizer Project amounting to Rs. 1,80,80,000 has been capitalised during the year, which includes approximately Rs. 1,70,33,465 capitalised in respect of the utilisation of loan and debenture money for the said purpose”. Is the treatment correct? Briefly comment.

13. A.S. Ltd. borrowed Rs. 12 Crores for its capital expansion which for 18 months. The relevant borrowing rate was 12.5%. During this period, the Company invested the temporary surplus funds at 4.5% on short-term basis and earned interest of Rs. 25 lakhs, which was offered as Miscellaneous Income in the P & L A/c. The Company has capitalised the entire interest cost and added to its Plant and Machinery. Is this correct?

14. Cost of an inventory items is Rs. 90,000. Borrowing Cost capitalised as per AS – 16 is Rs. 12,000. What will be accounting treatment if the NRV of this item is (a) Rs. 1,15,000 and (b) Rs. 87,000? What will be the consequence if the NRV increases to Rs. 96,000 in the subsequent year in situation (b) above?

15. ABC Ltd commenced construction of a flyover in Mumbai in January 2006 under BOLT schemes. The same was completed in February 2007. Due to heavy seasonal rains in July 2006 in the area, the work on the flyover had to be suspended for a month. The Company accordingly suspended capitalization of Borrowing Costs of Rs. 12.50 lakhs for that month. Comment.

16. A.S. Ltd has undertaken a project for expansion as per the following details : Month Plan Actual

April Rs. 2,00,000 Rs. 2,00,000 May Rs. 2,00,000 Rs. 3,00,000 June Rs. 10,00,000 – July Rs. 1,00,000 – August Rs. 2,00,000 Rs. 1,00,000 September Rs. 5,00,000 Rs. 7,00,000 The Company pays to its Bankers at the rate of 12% p.a. interest being debited on a monthly basis. During the half year, the Company had Rs. 10 lakhs Overdraft up to 31st July, surplus cash in August and again Overdraft of over Rs. 10 lakhs from 1st September. The Company had a strike during June and hence, could not continue the work during June . Work again commenced on 1st July and all the works were completed on 30th September . Assume that expenditure were incurred on 1st day of each month. Calculate the interest to be capitalized, giving reasons wherever necessary. You may assume that- Calculate the interest to be capitalised, giving reasons wherever necessary. You may assume that- a. Overdraft will be less, if there is no capital expenditure. b. The Board of Directors considering facts and circumstances, has decided that any capital

expenditure taking more than 3 months will be substantial period of time.

17. In February, a Company took a Bank Loan to be used specifically for the construction of a new Factory Building. The construction was completed in September and the building was put to its use immediately thereafter. Interest on the actual amount used for construction of the building till its completion was Rs.18 lakhs, whereas the total interest payable to the bank on the loan for the period till 31st December(end of accounting year) amounted to Rs. 25 lakhs. Can Rs. 25 lakhs be treated as part of the cost of Factory Building and thus be capitalized on the plea that the loan was specifically taken for the construction of factory building?

31 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

18. A.S Ltd borrowed Rs.1500 lakhs at 12% interest for creation integrated additional plant facilities. The

expenditure was incurred in the phase manner, each resulting in specifically identifiable capital asset as under-

Particulars Phase I Phase II Phase III

Asset Created Machinery Purchased Cost of Buildings Other Utilities

Plant L Rs. 500 lakhs Rs. 150 lakhs Rs. 50 lakhs

Plant M Rs. 400 lakhs Rs. 100 lakhs Rs. 50 lakhs

Plant N Rs. 600 lakhs Rs. 150 lakhs Rs. 100 lakhs

Total Costs Rs. 700 lakhs Rs. 550 lakhs Rs. 850 lakhs

Note: A: Each of the above Plants is a continuous process whereby output of L is transferred to M for further processing and thereafter to N, before sale to customers. B: Plant N includes machinery on which a Capital Grant of Rs. 100 lakhs is received from the Government. Determine the amount to be capitalised in respect of each of the above Plants. You need not allocate the same between machinery, buildings and other utilities.

19. A.S. Ltd. purchased machinery from Kusuma Ltd. on 30-9-2006. The price was rs. 370.44 lakhs after

charging 8% Sales Tax and giving a trade discount of 2% on the quoted price. Transport charges were 0.25% on the quoted price and installation charges 1% on the quoted price.

A loan of Rs. 300 lakhs was taken on the trial from the bank on which interest at 15% per annum was to be paid. Expenditure incurred on the trial run was Materials Rs. 35,000, wages Rs. 25,000 and Overheads Rs. 15,000. The Machinery was ready for use on 1.12.2006, but it was actually put to use only on 1.5.2007. Find out the cost of the machine and suggest the accounting treatments for the expenses incurred in the interval between the dates 1.12.2006 to 1.5.2007. The entire loan amount remained unpaid on 1.5.2007.

20. Rainbow Limited borrowed an amount of Rs. 150 crores on 1.4.2008 for construction of boiler plant @ 11% p.a. The plant is expected to be completed in 4 years. Since the weighted average cost of capital is 13% p.a., the accountant of Rainbow Ltd. capitalized Rs.19.50 crores for the accounting period ending on 31.3.2009. Due to surplus fund, out of Rs. 150 crores, an income of Rs. 3.50 crores was earned and credited to profit and loss account. Comment on the above treatment of account with reference to relevant accounting standard.

21. An amount of Rs.20,00,000 was incurred for construction of a building and it was ready occupation on 31.12.2007. The construction expenditure was incurred out of working capital facilities availed from the Bank. Interest payable to it @ 15%p.a. The average working capital loan has never fallen below Rs. 25 lakhs during the construction period.

The details of expenditure incurred are as follows:

July, 2007 3,00,000

August, 2007 4,50,000

September, 2007 2,00,000

October, 2007 5,00,000

32 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

November, 2007 3,00,000

December, 2007 2,50,000

20,00,000

Calculate the value of the qualifying asset.

22. A Firm produces its finished products in a peak season of five to six months in a year. No production takes place during the rest of the year. However sales takes place throughout the year and therefore large inventories need to be carried resulting in interest burden. Can this interest be included in the valuation of Finished Goods?

23. A.S. Ltd. dealing in timber finds it advantageous to store selected grades of timber for a prolonged period in order to improve their quality. It desires to include an actual interest cost of holding the timber as part of the value of unsold timber in inventory, and consults you in order to determine whether, in your opinion, such a method of valuation would be fair and reasonable and in accordance with generally accepted accounting principles. You are required to indicate your opinion with reasons. Would your answer be different if the Company did not actually incur any interest charges for holding the timber but desired to include notional interest charges which could be imputed to the Company’s own paid-Up Capital and Reserves which are invested in holding the timber for maturity?

24. X Ltd. began construction of a new building on 1st January, 2007. It obtained Rs.1 lakh special loan to finance the construction of the building on 1st January,2007 at an interest rate of 10% .The company’s other outstanding two non-specific loans were:

Amount Rate of Interest Rs. 5,00,000 11% Rs. 9,00,000 13% The expenditure that were made on the building project were as follows: Rs. January 2007 2,00,000 April 2007 2,50,000 July 2007 4,50,000 December 2007 1,20,000 Building was completed by 31st December, 2007. Following the principles prescribed in AS-16 ‘Borrowing Cost’, calculate the amount of interest to be capitalized and pass one Journal entry for capitalizing the cost and borrowing cost in respect of the building.

25. In May, 2004 Speed Ltd. took a bank loan to be used specifically for the construction of a new factory building. The construction was completed in January, 2005 and the building was put to its use immediately thereafter. Interest on the actual amount used for construction of the building till its completion was Rs. 18 lakhs, whereas the total interest payable to the bank on the loan for the period till 31st March, 2005 amounted to Rs. 25 lakhs

Can Rs. 25 lakhs be treated as part of the cost of factory building and thus be capitalized on the plea that the loan was specifically taken for the construction of factory building?

26. The borrowings profile of Santra Pharmaceuticals Ltd. set up for the manufacture of antibiotics at Navi Mumbai is as under:-

Date Nature of Borrowings Amount. Purpose of Incidental

borrowed Rs. Borrowings Expenses

33 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

1st January, 2008 15% demand loan 60 lakhs Acquisition of fixed 8.33% 1st July, 2008 14.5% Term loan 40 lakhs Acquisition of plant & Machin. 5% 1st October, 2008 14% bonds 50 lakhs Acquisition of fixed assets 8% The incidental expenses consist of commission and service charges for arranging the loans and are paid after rounding off to the nearest lakh. Fixed assets considered as qualifying assets are as under Rs. Sterile Manufacturing shed 10,00,000 Plant and machinery (total) 90,00,000

Other fixed assets 10, 00,000 The project is completed on 1st January, 2009 and is ready for commercial production. Show the capitalization of the borrowings costs.

27. Sweet & co. Is a sugar company. Due to the regulation by Central Government, the Company cannot

decide, the quality to be sold in the markets. It is regulated on the basis of release orders issued by the Central Government and quantity to be sold is also notified by the Central Government on monthly basis. Because of the seasonal nature of production, the company has to carry large inventories throughout the year. The average holding period of the sugar stock is generally 12-15 months. In the years when there is surplus stock of sugar, the Government creates a buffer stock and reimburses the carrying charges to the sugar factories for the inventory to be carried by the sugar mill, which includes interest. Sweet & Co. Incurs high interest costs since borrowings are required to meet the large demand for the working capital and payment to sugarcane producers, Interest costs is the second largest item in the profit and loss account of the Company, next to raw materials consumed. Can interest be capitalised under AS 16 or AS 2 as cost of inventory?

28. The company pays delayed cotton clearing charges, over the negotiated price, for taking delivery from supplier’s godown. The charge is in the nature of interest and is determined at 7% per annum. The company wants to include such charge in valuation of inventory since it is incurred in bringing the inventory to its present location and condition.

29. How would you, as a statutory auditor, deal with the following situation? The company deals in purchase and sale of timber and has included notional interest charges (calculated on. The paid-up share capital and free reserves) in the value of stock of timber as at the Balance Sheet date as part of cost of holding the timber.

30. R Ltd. has borrowed Rs 25 crores from financial institution during the financial year 2001-02 These borrowings are used to invest in shares ofPPA Ltd.. a subsidiary company, which is implementing a new project estimated to cost 50 crores. As on 31st March, 2002 since the said project was not yet complete, the Directors of R Ltd. resolved to capitalise the interest on the borrowing amounting to Rs.3 crores and add it to the cost of investment. As a statutory auditor, please comment.

31. A company has been consistently valuing its short-term inventory of finished goods by considering interest as an element of cost. The opening stock includes interest costs. It argues that on the principles of consistency it should be allowed to include interest cost in inventory valuation. It also argues that because interest cost is included in opening and closing inventory, the net impact is not significant. As an auditor how would you deal with this situation?

32. A company imports heavy machinery, which took significant amount of time in the voyage and was held up at the customs due to certain legal formalities. Can under these circumstances borrowing cost incurred in the intervening period be eligible for capitalization?

33. Capitalisation of borrowing cost on part ceases on completion of the parts (e.g. each building is distinct from other buildings in a business park). The question could arise if an entire building itself is

34 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

not complete, yet individual floors are complete and ready for use (for example, a high-rise office building). In that circumstance, when should capitalization of borrowing costs cease?

34. On 20.4.2003 JLC Ltd. obtained a loan the bank for Rs. 50 lakhs to be utilized as under. Rs. Lakhs Construction of a shed 20 Purchase of machinery 15 Working capital 10 Advance for purchase of truck 5 In March, 2004 construction of shed was completed and machinery installed. Delivery of truck was not received. Total interest charged by the bank for the year ending 31.3.2004 was Rs.9 lakhs. Show the treatment of interest under AS 16.

35. A company obtained term loan during the year ended 31st March, 2002 to the extent of Rs.650 lakhs for modernisation and development of its factory. Building worth Rs. 120 lakh were completed and Plant and Machinery worth Rs.350 lakhs were installed by 31st March, 2002. A sum of Rs.70 lakhs has been advanced for assets, the installation of which is expected in the following year. RS.110 lakhs has been utilised for Working Capital requirements. Interest paid on the loan of Rs. 650 lakhs during the year 2001-2002 amounted to Rs.58.50 lakhs. How should the interest amount be treated in the Accounts of the Company? Q. No. Answer Hints

1

2

3

4

5

35 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

6

7

8

9

10

11

12

13

14

36 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

15

16

17

18

19

20

21

22

23

37 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

24

25

26

27

28

29

30

31

32

38 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393

College Road Branch: 1st Floor, Gajanan Plaza, Opp. Datasoft Computer, Ashok Stambh, Nashik.

Contact No: 98220 26393, Ph. : 0253-2571545

PANCHAKSHARI’S PROFESSIONAL ACADEMY PVT. LTD. (Your Life long Knowledge Partner )

33

34

35

39 Head Office: College Road Branch: 3

st Floor, Parshuram Apartment, Above WoodLand Shoes, Opposite Times of India & Subway, College Road Nashik.

Contact No: 91583 97550, Ph. : 0253-2312393