uk remuneration review 2015 - proxy insight report 2015.pdf · uk remuneration review 2015 2...

TRANSCRIPT

UK Remuneration Review 2015

In associat ion with

2

ContentsUK Remuneration Review 2015

2 Preface

4 Unclear messages

7 What the shareholders say

10 The policies

Preface

Since the so called shareholder spring

of 2012, executive pay has rarely been

out of the headlines. Companies must

now walk the tightrope of attracting

and retaining their top executives in an

increasingly global market place while

avoiding allegations of fat cats.

UK Companies have had to report on

their Directors’ Remuneration since

2002 allowing shareholders a say, albeiit

on an advisory basis. However In 2013

the UK government went much further

and introduced new rules regarding the

reporting of executive remuneration:

The Remuneration Report

The Remuneration Report will continue

to include information on an annual

basis explaining how much directors

have been paid in the reporting year, and

how the pay policy will be implemented

in the current financial year.

Now companies must also disclose the

amount each director has been paid and

to express this as a single figure taking

account of all aspects of remuneration.

The company must also explain on

what basis the level of variable pay

has been set therefore linking actual

performance to remuneration.

As before voting on the remuneration

report is on an advisory basis only.

The Remuneration Policy

The Remuneration Policy is a new

requirement detailing how each

element of a directors’ remuneration

package “supports the short and

long term strategy of the company, its

potential value, and any performance

measures relating to it”. It must also set

out a policy for paying newly recruited

directors and a policy for loss of office

payments.

The Policy must be submitted to a

binding shareholder vote at least every

3 years.

2014 saw the vast majority of the

FTSE350 put their Remuneration

Report and Remuneration Policy to a

shareholder vote. For the first time it is

possible to see how shareholders voted

on remuneration on a binding basis and

also their views on the future direction

of executive pay.

This report looks at:

- Voting across the FTSE350 enabling

individual companies to compare their

voting results with their peers.

- Which investors most commonly

voted against Remuneration Reports

and Policies and why.

- A look ahead to 2015 with

Remuneration policy changes from key

asset managers.

13 Appendix Part 1

FTSE 100 Companies

16 Appendix Part 2

FTSE 250 Companies

www.proxyinsight.com

Don’t leave it to

chance

Proxy Insight has all the intelligence you need for a successful shareholder vote. Understanding who votes, how and why puts you in control—so don’t leave it to chance.

A lot has been written about the conflicting messages

investors sent to issuers in 2014 through their voting

patterns on executive pay. Indeed, Ecclesiastical’s

Neville White told Proxy Insight earlier this year that the different

outcomes for binding Remuneration Policy and advisory

Remuneration Reports were at times “schizophrenic”.

Overall, however, the average rate of support across the FTSE100

was very close with 93.7% for Policy and 92.8% for Reports.

Across the FTSE250, the results were exactly the same at 95.2%.

Analysis on the next two pages reviews the companies in

the FTSE100 and FTSE250 with the lowest support for both

resolution types.

Unclear messagesWhy rates of support for Remuneration Reports and Policies have become detatched, and how issuers can understand what shareholders want.

4

FTSE100

While Burberry was the only FTSE100

company to lose a remuneration vote,

a number failed to garner reasonable

support on either or both categories.

The companies with the lowest support

in each category are listed below while

the full list may be found in the appendix

to this report. Interestingly, while 85

companies secured support for their

Remuneration Policy of 90% or more,

only 78 managed to reach this level in

votes on their Remuneration Report.

While Carnival and – to an extent,

Burberry, HSBC, Reckitt Benkiser

and Astra Zeneca fared poorly in both

votes – others had issues in just one

of the categories. Despite receiving a

very low level of support for their Policy,

Standard Chartered’s Report actually

received a higher than average level of

support. Likewise, Pearson’s Policy had

a highly respectable level of support but

performed poorly for the Report vote.

These results matter, and are likely to

prove confusing for issuers. Support

for Policies may indicate a company is

heading in the right direction but this is

unlikely to make life easier for investor

relations teams trying to get their

Reports approved.

Having approved the principles for

executive pay, shareholders may still

object to the actual compensation

planned once details are announced in

proxy filings each year. Industries where

returns can be highly volatile, such as

banks, may be particularly affected.

5

The divergent outcomes for Remuneration Report and Remuneration

Policy votes have been described as schizophrenic”

“Remuneration Policy Remuneration Report

Rank Company % For Vs Avg % For Vs avg

1 Standard Chartered PLC 59.2 63 94.6 102

2 Carnival PLC 61.9 66 58.6 63

3 WM Morison Supermarkets PLC 73.5 78 89.1 96

4 HSBC Holdings PLC 79.4 85 84.0 90

5 Reckitt Benckiser Group PLC 80.2 86 68.5 74

FTSE 100-Lowest support for remuneration policy

FTSE 100-Lowest support for remuneration report

Remuneration Report Remuneration Policy

Rank Company % For Vs Avg % For Vs avg

1 Burberry Group PLC 47.3 51 83.9 90

2 Carnival PLC 58.6 63 61.9 66

3 AstraZeneca PLC 61.5 66 85.0 91

4 Pearson PLC 65.8 71 95.8 102

5 BG Group PLC 67.2 72 93.7 100

Source: Proxy Insight

Source: Proxy Insight

Remuneration Policy Remuneration Report

Rank Company % For Vs Avg % For Vs avg

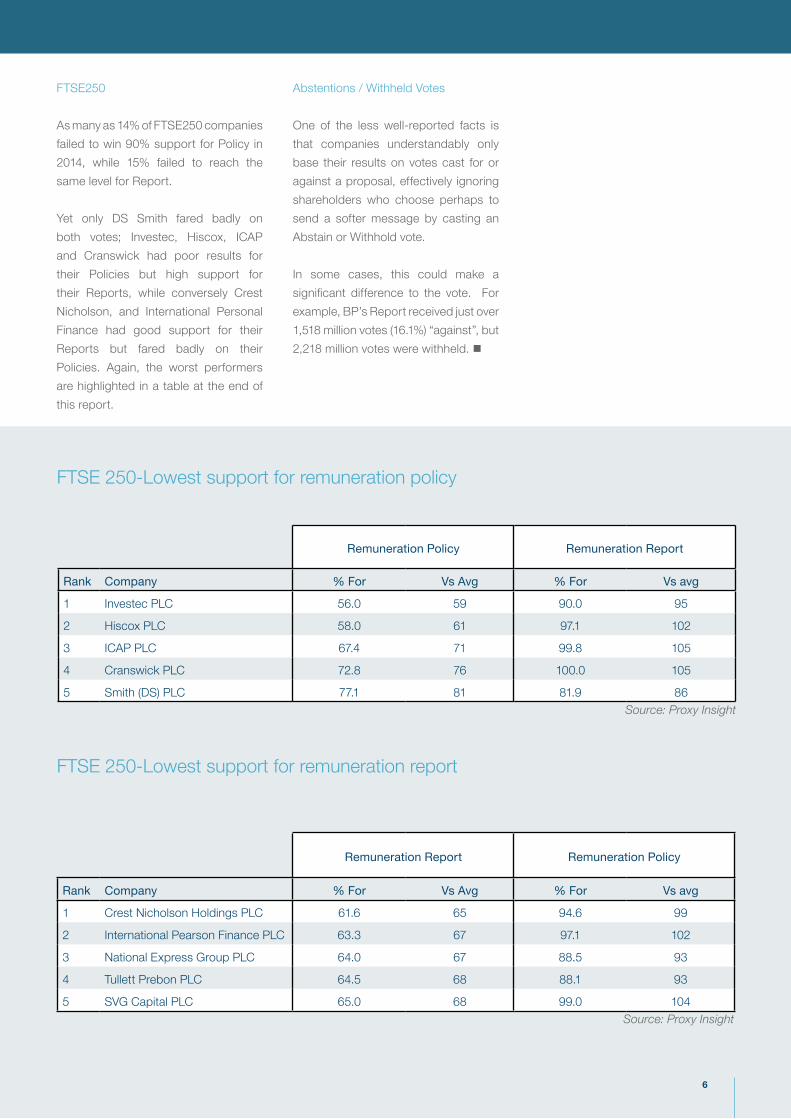

1 Investec PLC 56.0 59 90.0 95

2 Hiscox PLC 58.0 61 97.1 102

3 ICAP PLC 67.4 71 99.8 105

4 Cranswick PLC 72.8 76 100.0 105

5 Smith (DS) PLC 77.1 81 81.9 86

Remuneration Report Remuneration Policy

Rank Company % For Vs Avg % For Vs avg

1 Crest Nicholson Holdings PLC 61.6 65 94.6 99

2 International Pearson Finance PLC 63.3 67 97.1 102

3 National Express Group PLC 64.0 67 88.5 93

4 Tullett Prebon PLC 64.5 68 88.1 93

5 SVG Capital PLC 65.0 68 99.0 104

FTSE250

As many as 14% of FTSE250 companies

failed to win 90% support for Policy in

2014, while 15% failed to reach the

same level for Report.

Yet only DS Smith fared badly on

both votes; Investec, Hiscox, ICAP

and Cranswick had poor results for

their Policies but high support for

their Reports, while conversely Crest

Nicholson, and International Personal

Finance had good support for their

Reports but fared badly on their

Policies. Again, the worst performers

are highlighted in a table at the end of

this report.

Abstentions / Withheld Votes

One of the less well-reported facts is

that companies understandably only

base their results on votes cast for or

against a proposal, effectively ignoring

shareholders who choose perhaps to

send a softer message by casting an

Abstain or Withhold vote.

In some cases, this could make a

significant difference to the vote. For

example, BP’s Report received just over

1,518 million votes (16.1%) “against”, but

2,218 million votes were withheld.

FTSE 250-Lowest support for remuneration policy

FTSE 250-Lowest support for remuneration report

6

Source: Proxy Insight

Source: Proxy Insight

A COMPUTERSHARE COMPANY

Would you make the right moves?

When protecting against activism, your preparation is crucial:

• Profilingtheactivist

• Assessingthevotingriskoftheinstitutionsandproxyadvisors’influence

• Weighinguptheinfluenceoftheretailholders

• Craftinganddeliveringthemessagetoactivatetherightinvestorsanddrivevotes

Let us prepare your activist strategy:CasSydorowitz

[email protected]+44(0)8707030302www.georgeson.com

Remuneration Reports

Investors represented on Proxy

Insight’s database supported

management in votes on Remuneration

Reports an average of 83.5% of the

time, across the FTSE350 in 2014. Only

5 investors – Quantitative Management

Associates, Ignis Asset Management,

Aerion Fund Management, Putnam

and Parametic Portfolio Associates

(voting over 50 times) supported every

such resolution.

The Remuneration Report therefore

continues to be a contentious issue,

with many shareholders unconvinced

that current rewards are suitably linked

to the performance of the companies

themselves. The investors with the

highest level of opposition are shown

in Figure 1.

Aviva is the most aggressive investor,

supporting less than half of all

Remuneration Reports it voted for.

Helpfully, Aviva disclose the rationale

for their voting and so it is possible

to categorise the reasons for their

opposition, as seen in Figure 2 (see

overleaf.)

Nearly half of all Aviva’s opposition to

Remuneration Reports was due, at

least in part, to a lack of disclosure. In

some cases, this means a general lack

of detail is included in the Reports, while

a more specific recurring theme is a lack

of information regarding retrospective

bonus awards. Either way, Aviva clearly

believes pay awards are being made

without adequate rationalisation on the

part of remuneration committees.

The lack or limits of appropriate

linkages between compensation

and performance is a common

theme in discussions with Corporate

Governance teams and unsurprisingly

features highly in Aviva’s rationale.

Recent press coverage on WPP and

Standard Chartered, both of whom

have seen big increases in executive

pay, is of interest here. While many

WPP shareholders—although not

including Aviva—are relaxed about the

package Sir Martin Sorrell recieves due

to the company’s recent performance,

the same cannot be said of Peter

Sands at Standard Chartered after a

series of profit warnings at the bank.

However, it is worth noting that a further

critical factor in Aviva’s considerations

is whether pay levels are simply

excessive. If the pure quantum of

the package is too high for them to

approve, they are not averse to making

their views felt. For Aviva, Burberry falls

in to this camp, as does WPP.

Dutch Pension fund PGGM voted

against 45% of all their Remuneration

Report votes, the highest of our survey.

PGGM also provide detailed rationale

for their voting decisions and while

there are many company specific

issues raised a number of issues

commonly occur:

• Insufficient Disclosures—82% (of

votes against)

• Not Sufficiently Stretching—13%

• Not linked to performance—9%

• Corresponding poor performance of

business—9%

• Pay is high relative to peers—7%

Commenting on our results, Marcel

Jeucken, Managing Director

What the shareholders sayA look at the key determinants of voting decisions, with the corporate governance teams of the most stringent institutional investors.

Aviva Investors

PGGM Investments

RPMI

Ecclesiastical Investment

APG (Stichting PF ABP)

Threadneedle Investments

F&C Asset Management

Florida State Board

Goldman Sachs AM

Dimensional Fund Advisors

48 35

70

17

141670

72568

2063

14554

17

73

1317

23 4

75 25

79 12 9

79 12 9

% For % Against % Abstain

Top 10 Investors opposing Remuneration Reports 2014

Source: Proxy InsightFigure 1

Responsible Investment at PGGM

Investment said:

“Voting against proposals is not

something PGGM takes lightly. PGGM

is however very pleased that in the

UK shareholders can vote on both

remuneration policies and reports

as this significantly strengthens the

system of proper checks and balances.

The UK is a pioneer on this issue and

we believe it can (and will) improve

remuneration practices over time.”

RPMI has been a leading driver in

promoting longer term remuneration

targets around remuneration. It is

therefore of little surprise to see it at

third place in our rankings.

Ecclesiastical Investment

Management has also been a vocal

player on the subject of executive

pay. Commenting on our study, the

investor’s Head of SRI, Neville White,

stated:

“We are gratified by these results

as they suggest our rigorous policy

against supporting excessive awards

disconnected from long-term, superior

outperformance is firmly integrated

into our voting outcomes. Among

the top UK companies (FTSE30) we

find it increasingly difficult to support

executive remuneration packages,

and these results show that in around

half of FTSE350 cases we have been

unable to support management”.

The top US public pension

fund, Florida State Board of

Administration (SBA) provided Proxy

Insight with some of the key criteria it

applies when voting on remuneration.

Mike McCauley, its Senior Officer for

Investment Programs & Governance,

highlighted these points:

• SBA voting on FTSE companies is

similar to other developed markets and

generally in line with its overall global

voting statistic of approximately 20% to

25% votes against.

• Poor disclosure surrounding

performance objectives, award

thresholds, and key structural features

of any existing/proposed equity plans.

• Sufficient transparency is necessary

to fully understand how short/long term

incentive plans have been designed

and have worked.

• SBA prefers to see a strong

performance orientation embedded

within compensation framework, with

high correlation between financial

performance, total compensation,

and total stock returns (and votes

accordingly).

• It also examines compensation on

a relative basis, adjusting for industry

and size, and utilises several external

compensation models (e.g., ISS, Glass

Lewis, and Farient Advisors).

Remuneration Policy

For all investors in the Proxy Insight

database in 2014, the average support

for Remuneration Policy across the

FTSE350 was 88.5%, five percentage

points higher than the average support

for the Remuneration Report. Eight

investors supported every resolution

they voted on, including TIAA-CREF

and Ignis Asset Management.

As a binding resolution, the level

of opposition is lower than for

Remuneration Report. However, there

is still significant opposition from key

investors, as seen in Figure 3 (see

overleaf.)

Fidelity Worldwide took a much

tougher stance on Remuneration for

the 2014 proxy season, citing concerns

around the lack of long-term structure

in executive pay. Trelawny Williams,

Global Head of Corporate Finance at

Fidelity, commented on our analysis as

follows:

“Our votes against management were

a consequence of our campaign to

extend LTIP retention periods to five

years. We are not proud of having had

to vote against so many companies but

on the plus side it has led to significant

and continuing change on the ground

Voting against proposals is not something PGGM takes lightly”“

49%43%

37%31%

16%15%

14%10%

7%6%

5%

Lack of Disclosure

Lack/Low Performance link

Excessive Actual/Potential Pay Level

Lack of Retrospective Disclosure on Bonus Awards

Inappropriate Discretionary Payments

Generous Pension

Undue Ratcheting up of pay

No Limits Under Incentive Schemes

Lack of Claw-back Policy

Inappropriate Service Contracts

Lack of Independence on Committee

Key issues causing Aviva to oppose Remuneration Reports

Source: Proxy Insight

9

Figure 2

with over 50 FTSE companies now

having an LTIP share retention period

of over three years, up from only 13

two years ago.”

Of additional interest is that Fidelity is

the only investor to actually vote against

either of the remuneration categories

as opposed to a combination of against

and abstain votes.

Aviva applies much the same concerns

for its votes against Remuneration

Policy as for its votes against Reports

(Figure 4.) However, in a reversal of its

priorities, excessive potential pay is its

highest concern when deciding how

to vote on policies. The lack of bonus

deferral shows Aviva’s concerns that

companies are not being long-term

enough in their planning of variable

pay. In addition, Aviva also believes

certain boards are seeking too much

discretion to determine remuneration,

rather than seeking shareholder

approval. Linked to this point is the lack

of suitable clawback should a reward

prove to be inappropriate as a result of

future losses.

The final issue raised by Aviva is the lack

or limit of a shareholding requirement.

The investor remains a supporter

of requiring executives to think more

long-term and increase their linkage to

the wider shareholder base by owning

stock in the company they manage.

Report versus Policy

The different approaches investors

take to Remuneration Reports and

Policies continues to surprise and

enliven the debate around executive

compensation. But why should this be

so? True, one is historic, while the other

is forward looking. One is advisory

and the other binding. But should

there really be any difference between

investors’ voting on the two?

This report suggests investors take

a slightly more aggressive stance

on Reports than they do on Policies,

although in reality there seems little

difference at an aggregate level. Most

variations appear to be peculiar to

each company; for example, Standard

Chartered had very poor support for

its forward looking Policy, though

its Report received a slightly above

average level of support compared

to the wider FTSE100. Conversely,

Burberry’s Report failed, while its

Policy received reasonable, albeit

below average, support.

In terms of actual voting, three Dutch

pension funds—PGGM Investments,

Tandtechniek Stichting Pernsioenonds

and BPL Pensioen—opposed over 20%

more Remuneration Reports than they

did for Remuneration Policies. Conversely

while Fidellity Worldwide opposed 57% of

Policies this fell to only 13 % for Reports.

Likewise Ecclesiastical’s opposition was

47% and 32% for Policies and Reports

respectively.

43 54 3

53 32 15

56 26 18

59 22 19

76 21 3

77 22 1

79 12 9

80 10 10

80 20

84 11 5

Fidelity Worldwide

Ecclesiastical Investment

Aviva Investors

RPMI

F&C Asset Management

PGGM Investments

APG (Stichting PF ABP)

Threadneedle Investments

Florida State Baord

Dreyfus Corp.

% For % Against % Abstain

Top 10 Investors opposing Remuneration Policies 2014

Excessive Actual/Potential Pay Level

Lack Bonus Deferral

Too Much Discretion

Low/No Shareholding Requirement

Lack of Disclosure

Lack of Claw-Back Policy

Lack/Low Performance Link

Inappropriate Service Contracts

Uncapped Bonus

Too Short Term

30%29%

26%16%16%16%

13%11%11%

7%

Key issues causing Aviva to oppose Remuneration Reports

Source: Proxy Insight

Source: Proxy Insight

Figure 3

Figure 4

Aviva: A new policy includes requests

for annual disclosure of the remuneration

policy table within the remuneration

report. It also includes requests

for identifiable limits to executive

compensation, as Aviva is unlikely to

support compensation without limits.

Furthermore, the new policy indicates

support for companies that are

accredited as paying the living wage,

and expands and clarifies the investor’s

ideal clawback provision to include

performance adjustment or post-vesting

clawback.

BlackRock: Its new policy has a more

detailed explanation of BlackRock’s

say on pay analysis—where its old

policy says say on pay votes are

likely to correspond with votes on

the directors who are compensation

committee members, the new policy

explains the following preferences in

compensation: disclosure; long-term;

not solely formulaic; explanation of

unusual structure; avoid benchmarking;

good peer selection; no arbitrary limits;

no preference for specific plan; and

responsive to shareholders. The policy

also explains BlackRock’s engagement

process when it has concerns about

executive compensation.

BNP Paribas: Its new approach

expands requirements for a company’s

remuneration policy to include: an

explanation of the philosophy of the

remuneration policy; the link with

strategy and HR policy; the split between

the different remuneration mechanisms

chosen; long-term plan with extra-

financial performance metrics. New

negative aspects of the remuneration

policy include remuneration that is

disproportionate relative to the evolution

of its employees’ median remuneration.

For approving short-term remuneration,

BNP’s new policy adds requirements for

the disclosure of rules for formulating

short-term remuneration and

performance criteria of short-term

remuneration. The new policy adds

clawback and performance disclosure

requirements for long term remuneration.

SBA will vote for proposals to ratify or renew management/

profit sharing contact with other companies“CalSTRS: The pension fund’s old

policy says that additional forms of

compensation such as retirement

benefits are not warranted for director

compensation. The new policy explains

that this is because this kind of benefit

could create perverse incentives. An

old policy says the Audit Committee

should receive greater compensation

than other Board Committees, while

the new policy doesn’t mention this.

Charles Schwab: Used to simply

follow Glass Lewis, but now has its

own policy, which is used in addition

to the Glass Lewis policy and

includes: advisory vote on executive

compensation; equity awards plans;

employee stock purchase plans; and

the repricing of options.

CPPIB: A new policy cautions against

the use of external peer benchmarking

as it could lead to an escalation in

executive pay, unsupported by company

performance. The new policy also

expands the investor’s clawback policy

to include other performance metrics, as

well as misstated financial results.

F&C: Its new policy expands on

performance metrics and talks about

reputational and regulatory risks for

companies and industries where pay

levels were seen by regulators, investors

and the general public as excessive and

insufficiently aligned with performance.

Florida SBA: The new policy says the

SBA will vote for proposals to ratify

or renew management/profit-sharing

contracts with other companies (in

which the company retains or gains

management control over the other). It

also expands and clarifies the investor’s

views on golden parachutes.

Glass Lewis: The proxy adviser’s new

policy has a section on risk-taking in

its opening paragraph. It also includes

implementation and effectiveness as

criteria for its “say on pay” review. The

new policy includes a section on one-off

awards and expands on the following

points: clawback; compensation

consultants; golden parachutes; and

employee stock purchase plans.

ISS: A new scorecard is used to evaluate

equity plans. Rather than listing pass

and fail requirements, the scorecard is

designed to give a more balanced review

of equity plans.

The policiesHere, we review how voting policies are changing for a number of significant investors

11

Janus: The old policy says Janus will

generally vote against plans where the

proposed cost of an equity-based-plan

is above the allowable cap determined

by the proxy adviser. The new policy

adds that the investor will also vote

“against” if plan’s features and grant

practices are misaligned with the

maximising of shareholder value.

OTPP: The investor’s new policy

expands “say on pay” guidelines, and

aligns pay with performance. It also lists

certain trigger points that could result

in an “against” vote on say on pay.

The new policy changes the wording

of disclosure requirements from hurdle

rate to vesting conditions.

Royal London: A new policy says the

investor will vote against a remuneration

policy if it has concerns with how

remuneration is structured or if the policy

allows for excessive remuneration. The

new policy adds that Royal London

will vote against the remuneration

policy when pension payments are

excessive and out of line with pension

benefits awarded to employees, and

expands the approach to performance

periods from a hard requirement for “a

minimum of three years” to “preferably

for five years”. It also adds a section on

additional post-vesting holding periods

and adds a minimum credit quality

performance requirement.

SWIB: The old policy says SWIB will

evaluate the link between pay and

performance by reviewing proxy

materials. The new policy details

performance evaluation criteria that

SWIB considers positive and negative

and its position on non-performance

based compensation. The old policy

says plans that are not clear or lack

specific information on which to

determine pay and performance links

are typically not supported. The new

policy details exactly what must be

disclosed (e.g. Performance targets;

Financial Metrics; Compensation drivers

etc.). The acceptable level of dilution for

compensation plans has been revised

from 20% to 15%. The new policy

also gives more detail and specifics

on retirement plans and severance

payments.

T. Rowe Price: An old policy says

votes against bank bonuses are likely,

while the new policy has no mention of

them. An old policy says the investor

will generally vote for Section 162(m)

proposals. Their new policy adds unless

evergreen provisions are present.

Union Investment: The new policy

includes a request for key ‘non-financial’

performance indicators and requests

quantifiable limits and disclosure for

remuneration. It takes a critical view of

retrospective improvements to existing

share-option schemes or performance

measures that make it easier to achieve

specified targets.

Companies that successfully passed

both remuneration votes, even by small

margins, may be tempted to think that

this year’s focus on compensation will

not have long-term consequences and

continue broadly as they are. However,

the following risks illustrate why this may

be a poor decision:

Bad PR – Burberry, Standard

Chartered, Barclays and others all

received negative press coverage

over pay practices. More than merely

embarrassing these companies, the

negative coverage will no doubt cause

issues with staff, customers and

suppliers, as well as with shareholders.

Increasing Investor scrutiny – The

voting behaviour of investors is under

greater scrutiny than ever before and the

need to be shown to be good stewards

is of paramount importance. In addition,

many shareholders are introducing

more stringent rules on what forms of

remuneration are acceptable.

Competition for Capital – In a global

equity market, issuers must compete

with numerous other sources of capital.

Removing any obstacles to shareholder

support is surely a no-brainer for

Investor Relations teams.

Activism – Low levels of shareholder

support is a key screening tool used by

Activist investors when selecting new

targets. Indeed, it is no coincidence

that Marathon Partners chose to

nominate three directors to the board of

US issuer Shutterfly, after the company

received just 50.01% support for its

Remuneration Report last year.

So what?

12

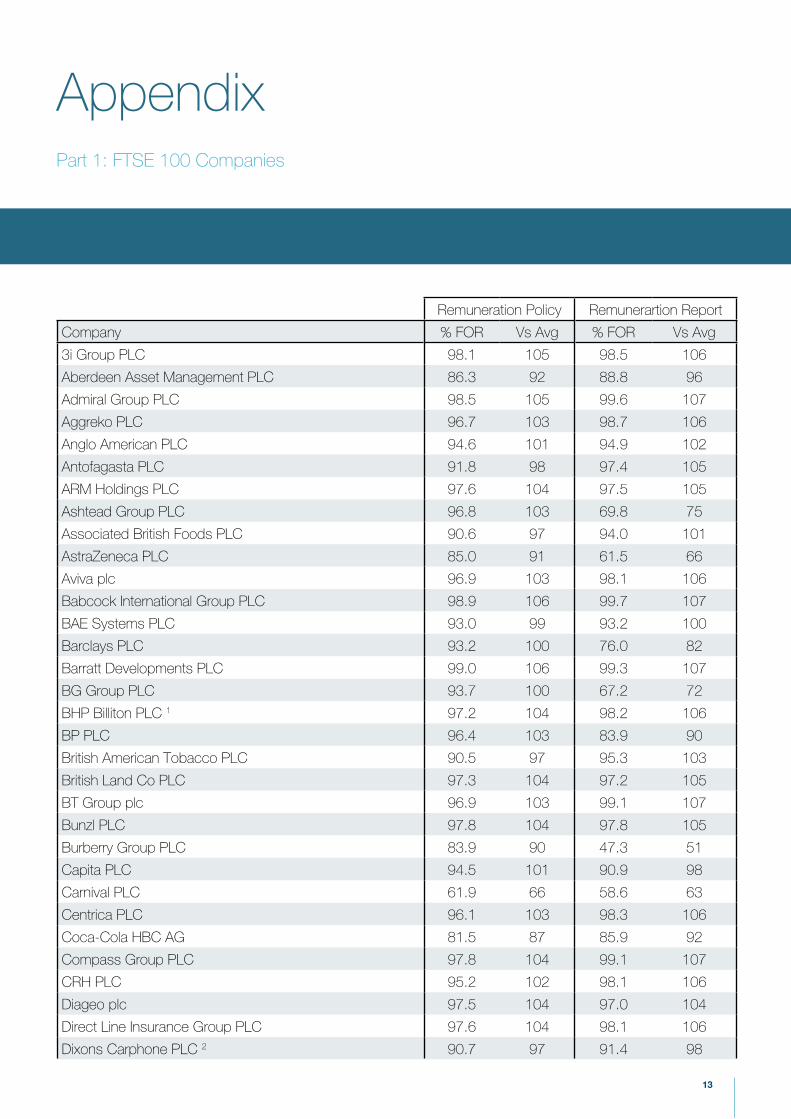

AppendixPart 1: FTSE 100 Companies

Remuneration Policy Remunerartion Report

Company % FOR Vs Avg % FOR Vs Avg

3i Group PLC 98.1 105 98.5 106

Aberdeen Asset Management PLC 86.3 92 88.8 96

Admiral Group PLC 98.5 105 99.6 107

Aggreko PLC 96.7 103 98.7 106

Anglo American PLC 94.6 101 94.9 102

Antofagasta PLC 91.8 98 97.4 105

ARM Holdings PLC 97.6 104 97.5 105

Ashtead Group PLC 96.8 103 69.8 75

Associated British Foods PLC 90.6 97 94.0 101

AstraZeneca PLC 85.0 91 61.5 66

Aviva plc 96.9 103 98.1 106

Babcock International Group PLC 98.9 106 99.7 107

BAE Systems PLC 93.0 99 93.2 100

Barclays PLC 93.2 100 76.0 82

Barratt Developments PLC 99.0 106 99.3 107

BG Group PLC 93.7 100 67.2 72

BHP Billiton PLC 1 97.2 104 98.2 106

BP PLC 96.4 103 83.9 90

British American Tobacco PLC 90.5 97 95.3 103

British Land Co PLC 97.3 104 97.2 105

BT Group plc 96.9 103 99.1 107

Bunzl PLC 97.8 104 97.8 105

Burberry Group PLC 83.9 90 47.3 51

Capita PLC 94.5 101 90.9 98

Carnival PLC 61.9 66 58.6 63

Centrica PLC 96.1 103 98.3 106

Coca-Cola HBC AG 81.5 87 85.9 92

Compass Group PLC 97.8 104 99.1 107

CRH PLC 95.2 102 98.1 106

Diageo plc 97.5 104 97.0 104

Direct Line Insurance Group PLC 97.6 104 98.1 106

Dixons Carphone PLC 2 90.7 97 91.4 98

13

easyJet PLC 55.0 59 55.5 60

Experian PLC 87.4 93 85.9 93

Fresnillo PLC 99.7 106 100.0 108

Friends Life Group Ltd 96.9 103 98.1 106

G4S PLC 98.4 105 98.3 106

GKN PLC 97.8 104 99.3 107

GlaxoSmithKline PLC 97.4 104 98.5 106

Glencore Plc 97.9 105 99.1 107

Hammerson PLC 97.1 104 97.8 105

Hargreaves Lansdown PLC 98.4 105 93.0 100

HSBC Holdings plc 79.4 85 84.0 90

Imperial Tobacco Group PLC 88.0 94 92.6 100

InterContinental Hotels Group PLC 90.9 97 94.0 101

International Consolidated Airlines Group SA 0 86.0 93

Intertek Group PLC 98.4 105 97.1 105

Intu Properties PLC 99.8 107 99.7 107

ITV PLC 96.0 103 77.5 83

Johnson Matthey PLC 97.6 104 99.1 107

Kingfisher PLC 98.9 106 99.7 107

Land Securities Group PLC 99.1 106 99.7 107

Legal & General Group PLC 97.6 104 98.7 106

Lloyds Banking Group Plc 98.0 105 87.3 94

London Stock Exchange Group PLC 94.9 101 96.9 104

Marks & Spencer Group PLC 98.3 105 99.2 107

Meggitt PLC 99.0 106 99.8 107

Mondi PLC 98.1 105 99.0 107

National Grid PLC 96.3 103 99.0 107

Next PLC 97.9 105 99.6 107

Old Mutual PLC 97.2 104 97.0 105

Pearson Plc 95.8 102 65.8 71

Persimmon PLC 90.8 97 93.2 100

Prudential PLC 91.9 98 94.5 102

Randgold Resources Ltd 97.9 105 89.9 97

Reckitt Benckiser Group PLC 80.2 86 68.5 74

Reed Elsevier PLC 93.8 100 89.1 96

Rio Tinto PLC 1 94.8 101 97.2 105

Rolls-Royce Holdings plc 96.3 103 94.2 101

Royal Bank Scotland plc (The) 99.7 106 99.8 108

Royal Dutch Shell PLC (A) 92.9 99 93.3 101

Royal Mail PLC 96.5 103 99.7 107

RSA Insurance Group PLC 96.9 103 99.7 107

SABMiller PLC 92.3 99 95.4 103

Sage Group (The) PLC 95.0 101 96.2 104

Sainsbury (J) PLC 99.2 106 99.5 107

14

Schroders PLC 92.2 98 94.2 102

Severn Trent PLC 97.7 104 99.4 107

Shire PLC 94.7 101 97.0 104

Sky PLC 93.0 99 86.2 93

Smith & Nephew PLC 93.5 100 98.0 106

Smiths Group PLC 95.0 101 93.6 101

Sports Direct International PLC 87.5 93 97.9 105

SSE PLC 99.1 106 97.6 105

St. James’s Place PLC 99.9 107 100.0 108

Standard Chartered PLC 59.2 63 94.6 102

Standard Life PLC 95.8 102 97.7 105

Taylor Wimpey PLC 98.2 105 99.4 107

Tesco PLC 97.5 104 98.6 106

Travis Perkins PLC 93.3 100 96.6 104

TUI Travel PLC 97.6 104 99.4 107

Tullow Oil PLC 90.8 97 92.1 99

Unilever PLC 97.5 104 99.1 107

United Utilities Group PLC 98.5 105 99.4 107

Vodafone Group Plc 96.0 102 97.3 105

Weir Group PLC 99.6 106 99.8 108

Whitbread PLC 99.4 106 99.1 107

Wm Morrison Supermarkets PLC 73.5 78 89.1 96

Wolseley PLC 93.6 100 98.4 106

WPP PLC 81.9 87 81.8 88

Average 93.7 92.8

Notes:1 As dual listed companies Rio Tinto PLC and BHP Billiton PLC had Remuneration Report votes for both UK and Austalian law. The UK law vote was used for this analysis2 Data shown was for Carphone Warehouse PLC

15

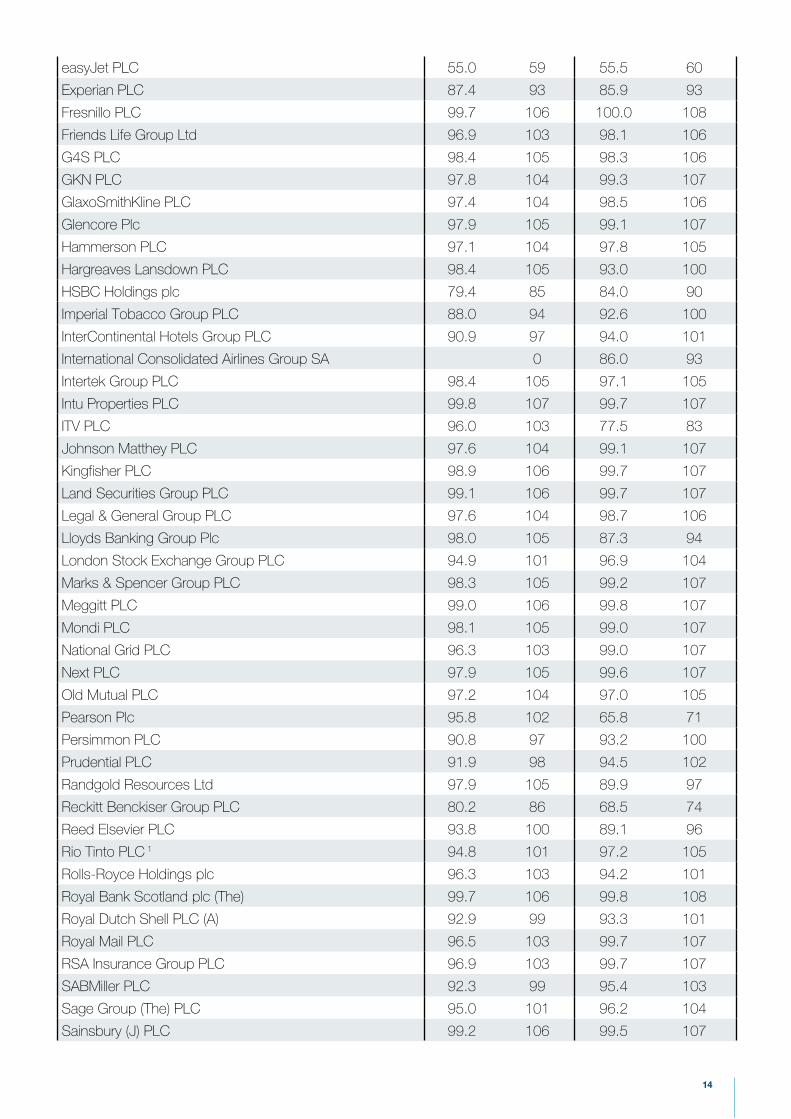

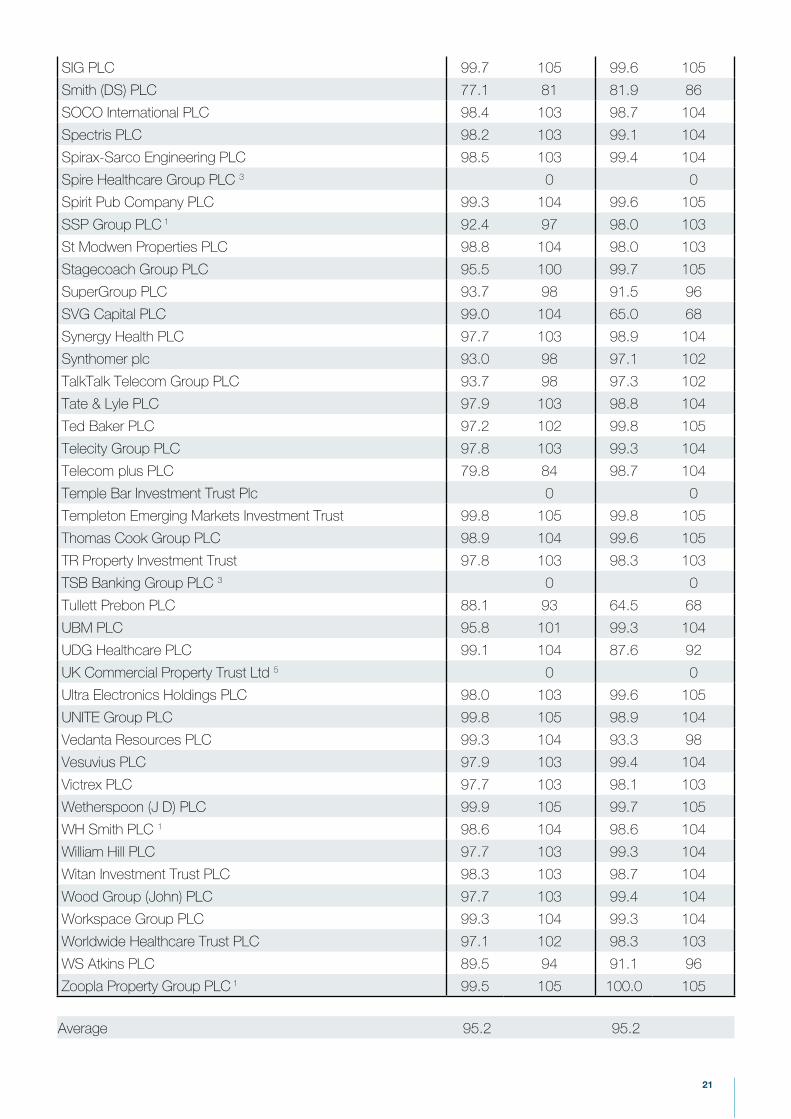

AppendixPart 2: FTSE 250 Companies

16

Remuneration Policy Remuneration Report

Company % FOR Vs Avg % FOR Vs Avg

3i Infrastructure PLC 2 99.9 105

Aberforth Smaller Companies Trust Plc 100.0 105 100.0 105

Acacia Mining PLC 98.4 103 85.4 90

Afren PLC 91.6 96 91.8 96

Al Noor Hospitals Group PLC 98.2 103 100.0 105

Alent PLC 96.8 102 99.4 104

Alliance Trust PLC 89.2 94 93.8 99

Allied Minds PLC 3 0 0

AMEC Foster Wheeler PLC 81.3 85 88.4 93

Amlin PLC 97.6 103 98.9 104

AO World plc 99.6 105 99.4 104

Ashmore Group PLC 82.2 86 99.0 104

AVEVA Group PLC 97.3 102 96.6 101

Balfour Beatty PLC 97.2 102 92.2 97

Bank of Georgia Holdings plc 91.9 97 93.6 98

Bankers Investment Trust PLC 96.3 101 96.3 101

Barr (A G) PLC 96.8 102 99.5 105

BBA Aviation PLC 95.1 100 99.4 104

Beazley PLC 98.2 103 83.3 88

Bellway PLC 97.7 103 98.5 103

Berendsen PLC 99.3 104 99.3 104

Berkeley Group Holdings (The) PLC 95.9 101 91.6 96

Betfair Group PLC 99.8 105 68.1 72

BH Macro Ltd 2 0 99.9 105

Big Yellow Group PLC 99.7 105 99.5 104

BlackRock World Mining Trust plc 99.7 105 99.8 105

BlueCrest AllBlue Fund Ltd 4 0 0

Bodycote PLC 96.1 101 98.5 104

Booker Group PLC 98.4 103 99.1 104

Bovis Homes Group PLC 96.6 102 95.5 100

Brewin Dolphin Holdings plc 96.5 101 96.6 101

BRIT PLC 3 0 0

17

British Empire Securities and General Trust 2 0 99.5 104

Britvic PLC 1 97.9 103 99.1 104

Brown (N) Group PLC 95.9 101 81.5 86

BTG PLC 95.1 100 99.3 104

Bwin.party digital entertainment plc 83.2 87 86.5 91

Cable & Wireless Communications PLC 97.3 102 89.9 94

Cairn Energy PLC 98.1 103 99.3 104

Caledonia Investments PLC 99.8 105 99.8 105

Capital & Counties Properties PLC 80.3 84 78.7 83

Card Factory PLC 3 0 0

Carillion PLC 96.1 101 95.7 101

Catlin Group Ltd 98.4 103 89.6 94

Centamin PLC 2 0 74.0 78

Cineworld Group PLC 86.5 91 71.1 75

City of London Investment Trust PLC 98.7 104 98.6 104

Close Brothers Group PLC 92.5 97 89.0 93

CLS Holdings PLC 82.4 87 91.1 96

Cobham PLC 98.4 103 97.1 102

Colt Group SA 94.9 100 98.1 103

Computacenter PLC 99.7 105 99.6 105

Countrywide plc 95.2 100 99.5 105

Cranswick PLC 72.8 76 100.0 105

Crest Nicholson Holdings plc 94.6 99 61.6 65

Croda International PLC 98.2 103 98.3 103

CSR PLC 93.7 98 94.8 100

Daejan Holdings PLC 97.9 103 99.5 105

Dairy Crest Group PLC 96.0 101 93.5 98

DCC PLC 98.9 104 99.2 104

De La Rue PLC 98.8 104 99.8 105

Debenhams PLC 98.7 104 99.8 105

Dechra Pharmaceuticals PLC 98.3 103 99.8 105

Derwent London PLC 99.5 105 98.1 103

Dignity PLC 98.2 103 99.0 104

Diploma PLC 93.8 98 99.6 105

Domino Printing Sciences PLC 97.8 103 96.4 101

Domino’s Pizza Group PLC 98.4 103 99.5 104

Drax Group PLC 94.1 99 82.7 87

Dunelm Group PLC 98.7 104 99.2 104

Edinburgh Investment Trust Plc 98.9 104 99.1 104

Electra Private Equity PLC 99.7 105 99.7 105

Electrocomponents PLC 99.3 104 99.3 104

Elementis PLC 97.5 102 97.0 102

Enterprise Inns PLC 99.8 105 99.3 104

Entertainment One Ltd 90.4 95 99.7 105

18

Essentra PLC 96.7 102 97.9 103

Esure Group plc 99.0 104 99.9 105

Euromoney Institutional Investor PLC 88.6 93 92.2 97

Evraz plc 99.3 104 99.4 104

F&C Commercial Property Trust Ltd 99.9 105 99.9 105

Fidelity China Special Situations PLC 99.3 104 99.4 104

Fidelity European Values PLC 99.1 104 99.3 104

Fidessa Group PLC 99.6 105 99.9 105

FirstGroup PLC 89.0 93 74.5 78

Fisher (James) & Sons PLC 98.2 103 99.3 104

Foreign & Colonial Investment Trust 92.7 97 93.0 98

Galliford Try PLC 98.1 103 99.5 104

Game Digital Plc 1 100.0 105 100.0 105

Genesis Emerging Markets Fund PLC 5 0 0

Genus PLC 99.4 104 99.0 104

Go-Ahead Group (The) PLC 97.1 102 97.9 103

Grafton Group PLC 98.2 103 99.9 105

Grainger PLC 88.7 93 92.5 97

Great Portland Estates PLC 96.7 102 98.1 103

Greencore Group PLC 1 98.8 104 99.1 104

Greene King PLC 95.8 101 99.5 105

Greggs PLC 98.0 103 99.9 105

Halfords Group PLC 97.0 102 99.3 104

Halma PLC 99.0 104 99.7 105

Hansteen Holdings plc 92.9 98 98.1 103

Hays PLC 92.6 97 98.6 104

Hellermanntyton Group PLC 95.4 100 98.2 103

Henderson Group PLC 89.7 94 72.2 76

HICL Infrastructure Company 2 0 98.2 103

Hikma Pharmaceuticals PLC 92.5 97 98.7 104

Hiscox Ltd 58.0 61 97.1 102

Home Retail Group PLC 94.9 100 98.8 104

Homeserve PLC 90.5 95 93.9 99

Howden Joinery Group PLC 98.4 103 98.8 104

Hunting PLC 91.5 96 98.4 103

ICAP PLC 67.4 71 99.8 105

IG Group Holdings PLC 96.1 101 99.5 104

IMI PLC 95.9 101 98.9 104

Inchcape PLC 96.5 101 97.3 102

Indivior PLC 3 0 0

Infinis Energy Plc 97.8 103 98.9 104

Informa PLC 93.9 99 98.6 104

Inmarsat PLC 96.7 102 98.4 103

Intermediate Capital Group PLC 79.9 84 77.3 81

19

International Personal Finance PLC 97.1 102 63.3 67

International Public Partnerships Limited 5 0 0

Interserve PLC 98.2 103 99.0 104

Investec PLC 56.0 59 90.0 95

IP Group PLC 99.9 105 99.9 105

Jardine Lloyd Thompson Group PLC 97.1 102 97.7 103

JD Sports Fashion PLC 95.5 100 86.4 91

Jimmy Choo PLC 3 0 0

John Laing Infrastructure Fund 5 0 0

JPMorgan American Investment Trust 99.7 105 99.7 105

JPMorgan Emerging Markets Inv Trust 99.7 105 99.8 105

Jupiter Fund Management PLC 96.9 102 99.8 105

Just Eat PLC 3 0 0

Just Retirement Group PLC 97.4 102 90.1 95

Kaz Minerals PLC (was Kazakhmys PLC) 99.3 104 86.9 91

Keller Group PLC 97.9 103 99.5 105

Kennedy Wilson Europe Real Estate plc 5 0 0

Kier Group PLC 98.9 104 88.5 93

Ladbrokes PLC 98.0 103 99.5 105

Laird PLC 94.7 100 98.0 103

Lancashire Holdings Ltd 90.1 95 69.9 73

Law Debenture Corporation 99.8 105 99.7 105

LondonMetric Property PLC 98.8 104 94.8 100

Lonmin PLC 82.8 87 89.4 94

Man Group PLC 96.5 101 96.5 101

Marston’s PLC 97.3 102 99.8 105

Melrose Industries PLC 77.4 81 95.8 101

Mercantile Investment Trust 99.7 105 99.7 105

Merlin Entertainments plc 99.4 104 99.8 105

Michael Page International PLC 98.7 104 98.2 103

Micro Focus International PLC 90.6 95 73.4 77

Millennium & Copthorne Hotels PLC 99.1 104 99.9 105

Mitchells & Butlers PLC 1 99.3 104 99.9 105

MITIE Group PLC 98.8 104 71.9 75

Moneysupermarket.com Group PLC 95.0 100 95.1 100

Monks Investment Trust 99.7 105 99.8 105

Morgan Advanced Materials PLC 97.8 103 99.6 105

Murray International Trust PLC 99.1 104 99.3 104

National Express Group PLC 88.5 93 64.0 67

NB Global Floating Rate Income Fund 2 0 99.7 105

NMC Health PLC 97.5 102 100.0 105

Northgate PLC 95.2 100 94.4 99

Nostrum Oil & Gas PLC 3 0 0

Ocado Group PLC 87.2 92 80.0 84

20

Ophir Energy PLC 98.9 104 74.2 78

Oxford Instruments PLC 98.8 104 99.6 105

Pace PLC 91.2 96 87.3 92

Paragon Group of Companies (The) PLC 91.4 96 93.7 98

PayPoint PLC 97.7 103 99.8 105

Pennon Group PLC 97.1 102 95.8 101

Perpetual Income and Growth Investment Trust Plc 99.7 105 99.7 105

Personal Assets Trust 97.9 103 97.7 103

Petra Diamonds Ltd 95.3 100 100.0 105

Petrofac Ltd 77.5 81 98.4 103

Pets at Home Group Plc 99.2 104 100.0 105

Phoenix Group Holdings 84.7 89 81.0 85

Playtech PLC 96.4 101 99.4 104

Polar Capital Technology Trust 99.4 104 99.3 104

Polymetal International plc 99.8 105 99.8 105

Poundland Group Plc 91.8 96 99.9 105

Premier Farnell PLC 95.4 100 98.0 103

Premier Oil PLC 86.1 90 98.6 104

Provident Financial PLC 96.0 101 96.0 101

PZ Cussons PLC 87.4 92 99.5 104

QinetiQ Group PLC 84.7 89 99.4 104

Rank Group (The) PLC 92.1 97 90.0 95

Rathbone Brothers plc 95.7 101 84.2 88

Redefine International plc 1 99.7 105 99.8 105

Redrow PLC 95.3 100 90.5 95

Regus PLC 99.6 105 98.3 103

Renishaw PLC 86.4 91 97.1 102

Rentokil Initial PLC 96.1 101 99.5 104

Restaurant Group (The) PLC 99.2 104 99.5 105

REXAM PLC 97.1 102 98.4 103

Rightmove PLC 98.6 104 99.8 105

RIT Capital Partners PLC 99.2 104 99.7 105

Riverstone Energy 5 0 0

Rotork PLC 96.6 102 98.6 104

RPC Group PLC 97.8 103 99.5 105

RPS Group PLC 89.7 94 94.6 99

Saga PLC 3 0 0

Savills PLC 99.7 105 99.6 105

Scottish Investment Trust 96.6 101 96.7 102

Scottish Mortgage Investment Trust plc 99.5 105 99.5 105

Segro PLC 98.6 104 95.6 100

Senior PLC 97.6 103 96.5 101

Serco Group PLC 98.1 103 99.6 105

Shaftesbury PLC 98.7 104 98.9 104

21

SIG PLC 99.7 105 99.6 105

Smith (DS) PLC 77.1 81 81.9 86

SOCO International PLC 98.4 103 98.7 104

Spectris PLC 98.2 103 99.1 104

Spirax-Sarco Engineering PLC 98.5 103 99.4 104

Spire Healthcare Group PLC 3 0 0

Spirit Pub Company PLC 99.3 104 99.6 105

SSP Group PLC 1 92.4 97 98.0 103

St Modwen Properties PLC 98.8 104 98.0 103

Stagecoach Group PLC 95.5 100 99.7 105

SuperGroup PLC 93.7 98 91.5 96

SVG Capital PLC 99.0 104 65.0 68

Synergy Health PLC 97.7 103 98.9 104

Synthomer plc 93.0 98 97.1 102

TalkTalk Telecom Group PLC 93.7 98 97.3 102

Tate & Lyle PLC 97.9 103 98.8 104

Ted Baker PLC 97.2 102 99.8 105

Telecity Group PLC 97.8 103 99.3 104

Telecom plus PLC 79.8 84 98.7 104

Temple Bar Investment Trust Plc 0 0

Templeton Emerging Markets Investment Trust 99.8 105 99.8 105

Thomas Cook Group PLC 98.9 104 99.6 105

TR Property Investment Trust 97.8 103 98.3 103

TSB Banking Group PLC 3 0 0

Tullett Prebon PLC 88.1 93 64.5 68

UBM PLC 95.8 101 99.3 104

UDG Healthcare PLC 99.1 104 87.6 92

UK Commercial Property Trust Ltd 5 0 0

Ultra Electronics Holdings PLC 98.0 103 99.6 105

UNITE Group PLC 99.8 105 98.9 104

Vedanta Resources PLC 99.3 104 93.3 98

Vesuvius PLC 97.9 103 99.4 104

Victrex PLC 97.7 103 98.1 103

Wetherspoon (J D) PLC 99.9 105 99.7 105

WH Smith PLC 1 98.6 104 98.6 104

William Hill PLC 97.7 103 99.3 104

Witan Investment Trust PLC 98.3 103 98.7 104

Wood Group (John) PLC 97.7 103 99.4 104

Workspace Group PLC 99.3 104 99.3 104

Worldwide Healthcare Trust PLC 97.1 102 98.3 103

WS Atkins PLC 89.5 94 91.1 96

Zoopla Property Group PLC 1 99.5 105 100.0 105

Average 95.2 95.2

22

Notes:1 2015 data used as Rem Policy included2 No Rem Policy in 2014 and meeting not yet occurred in 20153 New Issue - no AGM yet4 No Rem Policy or Rem Report vote in 20145 Vote Breakdown Not Disclosed

Are youprepared?

www.activistinsight.com

Activist Insight Online brings you the most extensive coverage of activist investors worldwide to ensure you know what to expect from their engagement. Stand out from the crowd with market leading knowledge of activist situations across the globe, whilst saving valuable time in your research efforts.