understanding the wildfish harvesting business...

TRANSCRIPT

Understanding the wildfish

harvesting business

Webjørn Barstad CEO HAVFISK ASA

• The Global Picture – Supply side – Markets – From science to individual vessel quotas

• Norwegian fisheries and HAVFISK

• Outlook

Agenda HAVFISK ASA

The Global Picture Supply side

World capture production stable at «maximum potential»

The most important white fish species from the fisheries

3.543

1.050

1.216

345

280494

260

White fish catch -‐ 2015 E

Alaska Pollock

Hakes

Atlantic Cod

Haddock

Saithe

Pacific Cod

HokiSource: Kontali AnalyseSource: Kontali Analyse

(1000 tonnes)

Catch by nations and species (mt)

Alaska Pollock

Atlantic cod Hake Saithe Haddock SBW

Pacific cod Hoki TOTAL

Chile - - 40 000 - - 14 000 - 40 000 94 000 88 000

Argentine - - 270 000 - - 9 000 - 45 000 324 000 328 000

USA 1 405 000 - 250 000 8 000 3 000 - 330 000 - 1 996 000 1 984 000

Canada 10 000 18 000 50 000 5 000 8 000 - 5 000 - 96 000 88 000

Russia 1 670 000 448 000 2 000 1 000 77 000 - 80 000 - 2 278 000 2 212 000

Norway - 475 000 2 000 156 000 94 000 - - - 727 000 659 000

Iceland - 239 000 - 53 000 36 000 - - - 328 000 329 000

Faroe Islands - 17 000 - 17 000 3 000 - - - 37 000 51 000

EU - 160 000 68 000 54 000 50 000 - - - 332 000 318 000

Namibia - - 140 000 - - - - - 140 000 140 000

South Africa - - 150 000 - - - - - 150 000 145 000

Japan/S-Korea 280 000 - - - - 3 000 65 000 - 348 000 343 000

New Zealand - - - - - 35 000 - 150 000 185 000 195 000

Others - 10 000 96 000 14 000 1 000 2 000 2 000 4 000 129 000 118 000

Total 3 365 000 1 367 000 1 068 000 308 000 272 000 63 000 482 000 239 000 7 164 000 6 998 000

Source; National statistics/KA-Est.

NationCatch by nation and species 2014

E 2015

The Global Picture Markets

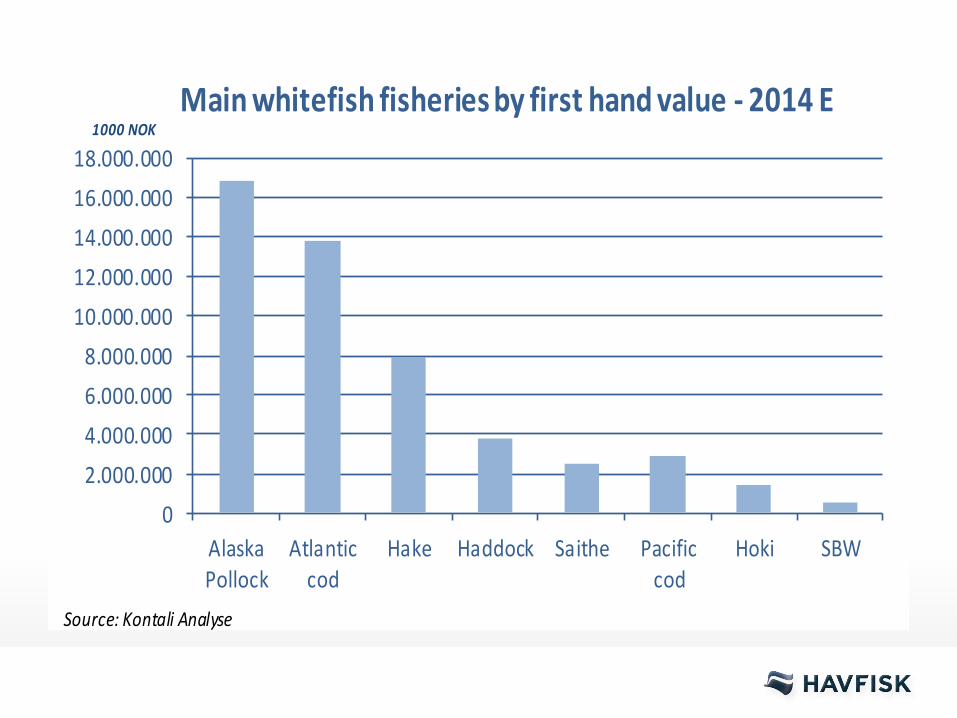

02.000.0004.000.0006.000.0008.000.000

10.000.00012.000.00014.000.00016.000.00018.000.000

AlaskaPollock

Atlanticcod

Hake Haddock Saithe Pacificcod

Hoki SBW

1000 NOKMain whitefish fisheries by first hand value -‐ 2014 E

Source: Kontali Analyse

The world market of whitefish

47 %

14 %12 %

9 %8 % 7 %

2 %

5 %

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

40 %

45 %

50 %

EU North America Asia Russia South America Japan Africa Others

Source: Kontali Analyse

The global volume of groundfish -‐ Where is it consumed? (2014 E)

White Fish Cod Alaska Pollock Haddock Saithe Hakes HokiTotal

Germany 547 70 411 3 23 36 4UK 474 250 101 86 15 20 2Spain 473 190 32 0 6 245 0France 359 60 183 13 26 55 22Scandinavia (SE, DK, FI) 245 134 26 23 40 10 12Poland 243 97 109 7 6 13 11Be/Ne/Lux 237 89 71 17 32 26 2Portugal 162 98 5 0 0 59 0Italy 158 44 30 0 0 84 0Others 115 45 57 3 5 3 2

3013 1077 1025 152 153 551 55

Top 3 Markets1 Germany UK Germany UK Scandinavia Spain France2 UK Spain France Scandinavia Be/Ne/Lux Italy Scandinavia3 Spain Scandinavia Poland Be/Ne/Lux France Portugal Poland

Source: Kontali Analyse

1000 tonnes R.W.

EU country split -‐ whitefish consumption 2014

Vessel quotas

From science to individual vessel quotas

• Annual quota advice from the relevant scientific institution – Interna<onal Council for the Explora<on of the Sea – Species by species scien<fic advice

• Problem: Fish don’t care about borders in the sea… • Solution: Agreement on total allowable catches (TAC)

and quota sharing between nations through annual bi- or multilateral negotiations – Based on scien<fic advice – End result: na<onal TACs for various species

How is the vessels quota decided?

• Bi-lateral fisheries agreements involving Norway: – Russia / Norway – EU / Norway – Greenland / Norway – Faroe Islands / Norway – Iceland / Norway

• Multi-lateral fisheries agreements where Norway is part (and participate in fisheries): – NEAFC – NAFO – CCAMLR

How is the vessels quota decided?

National TAC from agreements - Allocations for science, political purposes etc = TAC available to commercial fishing fleet Divided between variety of vessel groups according to long term quotasharing agreement within the Norwegian Fishermens Association

-‐ Different agreed shares from species to species

How is the vessels quota decided?

How is the vessels quota decided?

• Trawler groups quota share (eg. Cod 33%) allocated with an equal quota size per individual vessel quota

• Total of ~88 individual vessel quotas in trawl group (Cod)

• One vessel can hold up to 4 quotas

Norwegian fisheries and HAVFISK

Ocean area > 6 x land area

• World fishing nation no. 10 by volume (largest in Europe)

• World fishing nation no. 2 by export value

• The worlds largest Cod stock

• EU 31 mt pr fisherman • Norway 255 mt pr

fisherman

Positioned for profitability

Modern, efficient, well managed, sustainable Norway as a fishing nation

20

40

60

80

100

120

140

1980 1985 1990 1995 2000 2005 2010 2014

Vessels

Number of cod trawl vessels Norway 1980-‐2014

Source: Fiskeridirektoratet

• Norway’s largest harvesting company and quota holder – 11% of the Norwegian whitefish quota (cod, saithe, haddock)

– 7 Barents Sea shrimp licenses + 1 Greenland

• 10 operational trawlers – Three new vessels delivered in 2013 and 2014

Key facts Company overview

Norwegian fishing companies The 35 largest fishing companies in 2014 (gross catch value in mill. NOK)

MNOK

• 390 employees • Ownership to fish

industry facilities in northern Norway

• Facilities are operated by sister company Norway Seafoods

• Listed on Oslo Stock Exchange

• Aker ASA 73,25 %

Key facts Company overview

Year 2014 • Operating Revenues:

1 049 MNOK • EBITDA: 299 MNOK

(28 %) • EBITDA per kilo: 5,0 NOK • Equity ratio: 35 % • Volume 2014: 59 295 mt (~83 000 mt live weight)

Q2- 2015 Operating Revenues: 257 MNOK EBITDA: 84 MNOK (34 %) EBITDA per kilo: 6,1 NOK Equity ratio: 36,2 % Q3 figures – 6 November

Results 2014 & Q2 2015 Financials

Key value drivers HFISK

• Strong supply growth and financial downturn in key markets have negative impact on cod prices.

• Cod-prices appears to have bottomed out in Q1/2013

Export prices for frozen cod h/g in NOK. Source: Norwegian Seafood Council

Historic price trend - Cod Value drivers

Cost breakdown (based on 2014 figures) Value drivers

28

100

150

200

250

50

Dri

vers

Cost per day in operation Fixed cost : yearly maintenance in ship yards

Cost

615732

159101

316

Personnel

10% 31%

Freight/ packaging

Maintenance

6% 3%

Fuel

6%

Fishing gear

16%

Administration

Cost (MNOK) % of revenue

Percentage of catch value Cost per kilo

Cost per day in operation Average consumption for a freezing trawlers = 10 000 litres/day

Cost per day in operation Average of NOK/day 10 000

Fixed cost Overhead cost, administration, insurance

Low fixed sum per day Main personnel cost is in % of catch value

• Significant increase in catch efficiency – Change in fleet – Availability of fish

• New vessels: – improvement in catch efficiency

– flexibility to par<cipate in alterna<ve fisheries

Catch efficiency Value drivers

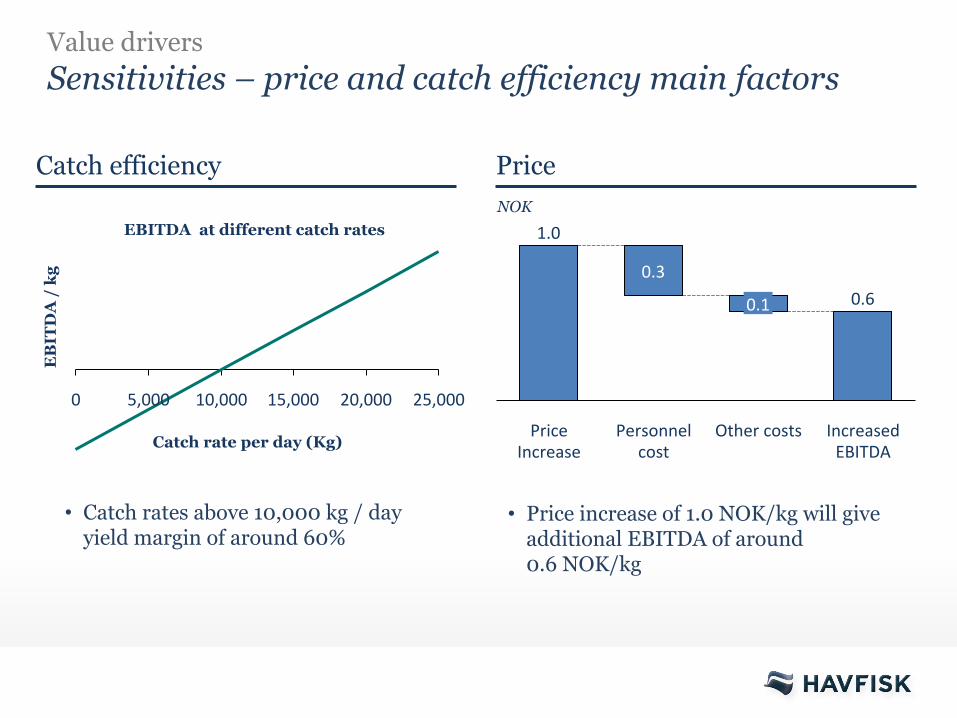

Sensitivities – price and catch efficiency main factors Value drivers

5,000 10,000 15,000 20,000 25,000 0

Catch efficiency Price

Catch rate per day (Kg)

• Catch rates above 10,000 kg / day yield margin of around 60%

Personnel cost

Price Increase

Other costs

1.0

0.3

0.1

Increased EBITDA

0.6

• Price increase of 1.0 NOK/kg will give additional EBITDA of around 0.6 NOK/kg

EB

ITD

A /

kg

NOK EBITDA at different catch rates

«Virtual tour» at Gadus Neptun http://invisual.no/havfisk/

Outlook HFISK

§ Quotas 2016 § Cod -‐ same level as in 2015 § Haddock + 9 % § Saithe + 7 %

§ Q3 presenta<on – 6 November 2015 9 am § Hotel Con<nental – Oslo

§ Industry Handbook § www.havfisk.no/investor rela<ons/reports and presenta<ons

Outlook HAVFISK

• Health, convenience, environment and ethics – Fish is an important source of

protein, vitamins and minerals – The Norwegian fishing for cod,

haddock and saithe is certified by MSC standard for sustainable fisheries

– Fish is an environmentally friendly source of protein

• Growing focus on fish in retail – customer demands drives convenience

Long term mega trends Outlook

Aker Seafoods invests in the future!

Source: Prof Ray Hilborn, University of Washington

• The Food Gap Challenge towards 2050

Long term mega trends Outlook

69% increase in food

production will be necessary

The world needs more

seafood - less than 10 percent of food consumption is

sea-based

HAVFISK – ca 200 mill meals per year

Disclaimer

This Presenta<on includes and is based, inter alia, on forward-‐looking informa<on and statements that are subject to risks and uncertain<es that could cause actual results to differ. These statements and this Presenta<on are based on current expecta<ons, es<mates and projec<ons about global economic condi<ons, the economic condi<ons of the regions and industries that are major markets for HAVFISK ASA including subsidiaries and affiliates. These expecta<ons, es<mates and projec<ons are generally iden<fiable by statements containing words such as ”expects”, ”believes”, ”es<mates” or similar expressions. Important factors that could cause actual results to differ materially from those expecta<ons include, among others, economic and market condi<ons in the geographic areas and industries that are or will be major markets for HAVFISK`s businesses, fish prices, market acceptance of new products and services, changes in governmental regula<ons, interest rates, fluctua<ons in currency exchange rates and such other factors as may be discussed from <me to <me in the Presenta<on. Although HAVFISK ASA believes that its expecta<ons and the Presenta<on are based upon reasonable assump<ons, it can give no assurance that those expecta<ons will be achieved or that the actual results will be as set out in the Presenta<on. HAVFISK ASA is making no representa<on or warranty, expressed or implied, as to the accuracy, reliability or completeness of the Presenta<on, and neither HAVFISK ASA nor any of its directors, officers or employees will have any liability to you or any other persons resul<ng from your use.