unit 1: sap business one standard financial processes contents: standard financial processes sales...

TRANSCRIPT

Unit 1: SAP Business One Standard Financial Processes

Contents: Standard financial processes Sales and purchasing processes and their consequences on book keeping

SAP Business One Standard Financial Processes: Unit Objectives

After completing this unit, you will be able to: Discuss some general accounting conventions Describe the steps in the standard financial processes in SAP Business One Give examples of the automatic journal entries created during the sales, purchasing

and inventory processes Discuss the financial consequences of the processes on the general ledger

SAP Business One Standard Financial Processes: Course Overview Diagram

SAP Business One Standard Financial Processes

Topic 1: Standard Financial Processes

Topic 2: Sales and Purchasing Processes

You are implementing SAP Business One at a new customer, OEC Computers: Your main contact in the customer site is Maria the accountant. Maria asks about the way SAP Business One handles the financial

accounting processes. She wants to make sure she understands the big picture so she can report

to the company owners the business results periodically.

SAP Business One Standard Financial Processes:Business Example

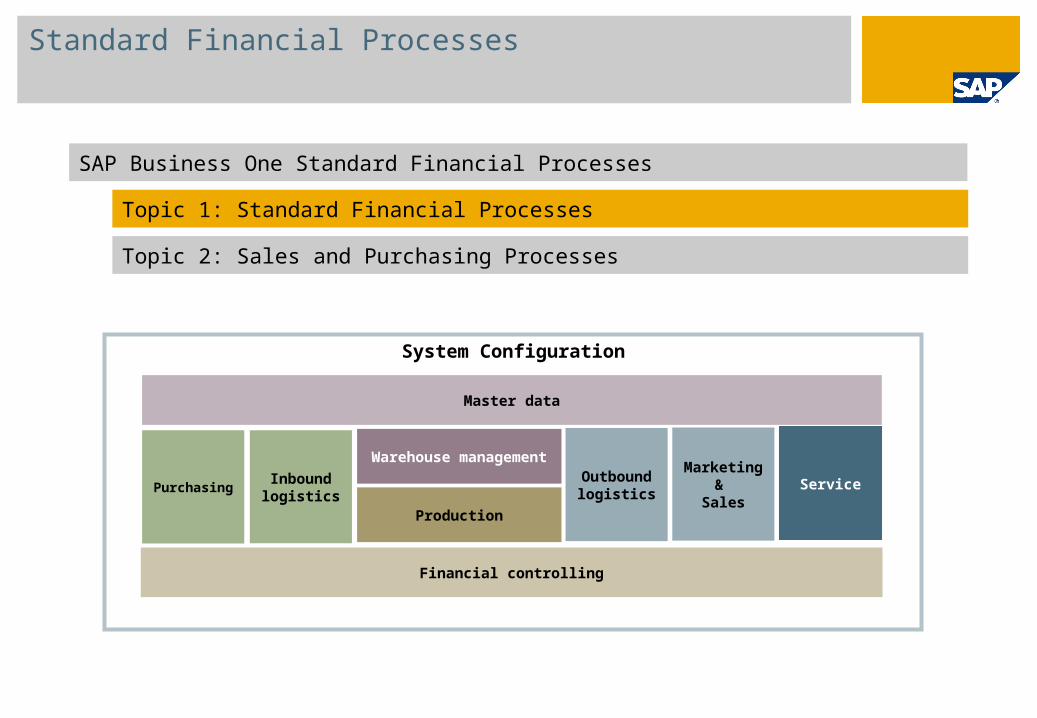

Standard Financial Processes

SAP Business One Standard Financial Processes

Topic 1: Standard Financial Processes

Topic 2: Sales and Purchasing Processes

System Configuration

Purchasing

Warehouse management

Production

Inbound logistics

Outbound logistics

Marketing &

SalesService

Financial controlling

Master data

After completing this topic, you will be able to:

Discuss some general accounting conventions

Standard Financial Processes: Topic Purpose

Finance Basics

Every business transaction is recorded in the company's books. This allows you: To manage your company effectively with the option of producing financial

reports To report the business transactions to the authorities.

Every business transaction results with a value exchange: A certain account increases value and another decreases value, resulting in the

recording of balancing debit side and credit side postings.

Value Exchange: Question

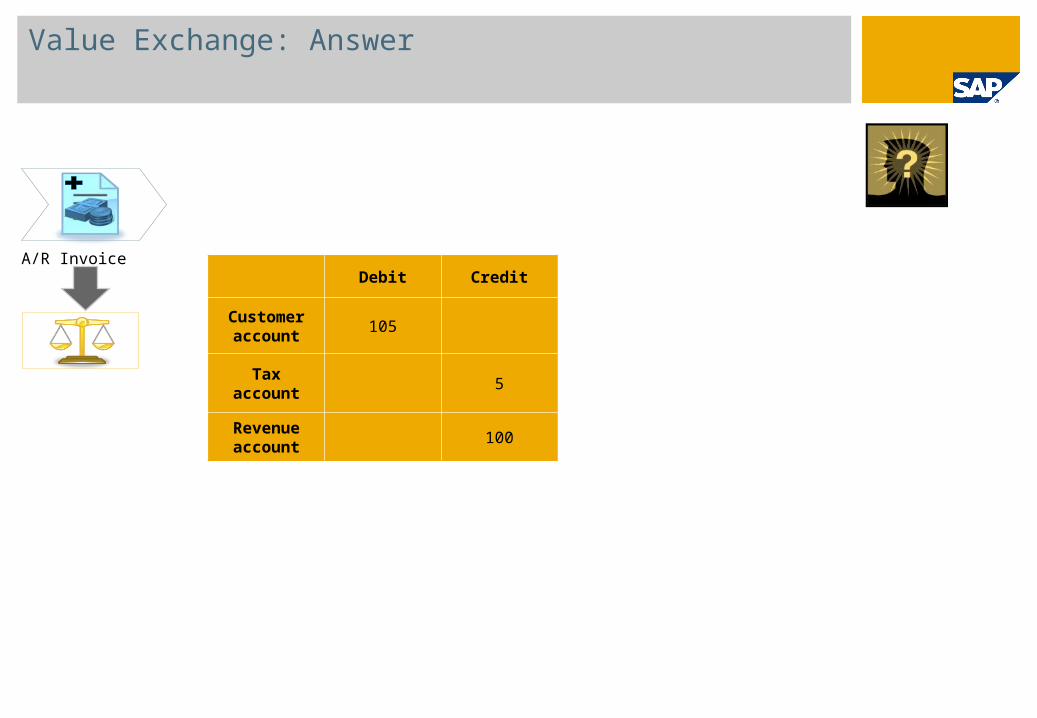

A/R Invoice

In a current sales process what happens to the accounts involved in the A/R Invoice? (Let us assume that this is a non-perpetual inventory system)

Value Exchange: Answer

A/R InvoiceDebit Credit

Customeraccount

105

Tax account 5

Revenue account

100

Some General Accounting Conventions (1)

Debit Credit

Cash clearing account

105

Bank account 105

Deposit no. 500070

Each journal entry represents one posted business transaction. Each line in the journal entry represents one posting to an account (which could represent a

customer, vendor or a regular general ledger account). Each line in the journal entry represents a posting of either a debit or a credit amount (but never

both together).

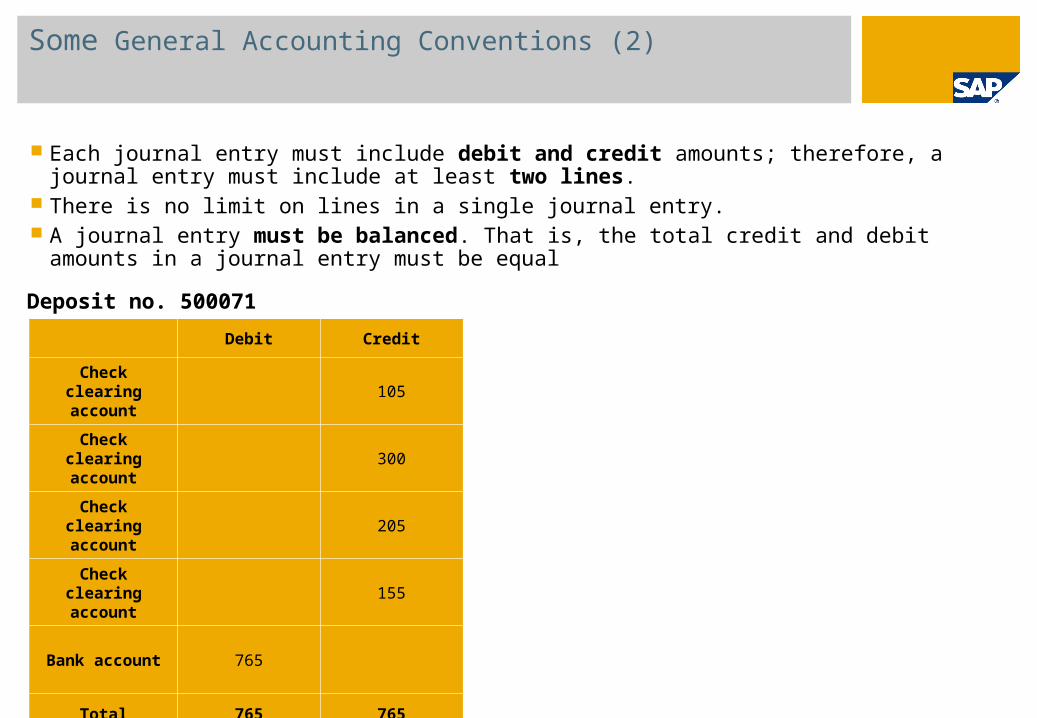

Some General Accounting Conventions (2)

Debit Credit

Check clearing account

105

Check clearing account

300

Check clearing account

205

Check clearing account

155

Bank account 765

Total 765 765

Deposit no. 500071

Each journal entry must include debit and credit amounts; therefore, a journal entry must include at least two lines.

There is no limit on lines in a single journal entry. A journal entry must be balanced. That is, the total credit and debit amounts in a journal entry must

be equal

The Account Balance (1)

Customer XXXX7

Debit Credit Origin

105 Debit A/R Invoice

600 Debit A/R Invoice

400 Debit A/R Invoice

705 Credit Incoming Payment

200 Debit A/R Invoice

100 Debit A/R Invoice

Account Balance

700 Debit

The account balance represents the difference between the total debit transactions and the total credit transactions recorded for that account.

The transaction summary or the balance of a certain G/L account or business partner is the initial information the accounting system can provide about the business.

The Account Balance (2)

Previously, we mentioned that in each journal entry a certain account increases value and another decreases value, resulting in the recording of balancing debit side and credit side postings.

The effect on the account balance: Assets, Expenses, and Drawings accounts are generally in debit. Liability, Revenue, and Capital (Equity) accounts are generally in credit.

The Account Balance and the Account Type

Bal

ance

Sh

eet

Acc

ou

nts

Pro

fit

and

Lo

ss

Acc

ou

nts

Value Exchange and the Account Balance

Debit Credit

Customeraccount

440

Revenue account

440

A/R Invoice

The two accounts increase their values: ▲

(Let us assume that the customer is tax exempt and that this is a non-perpetual inventory system)

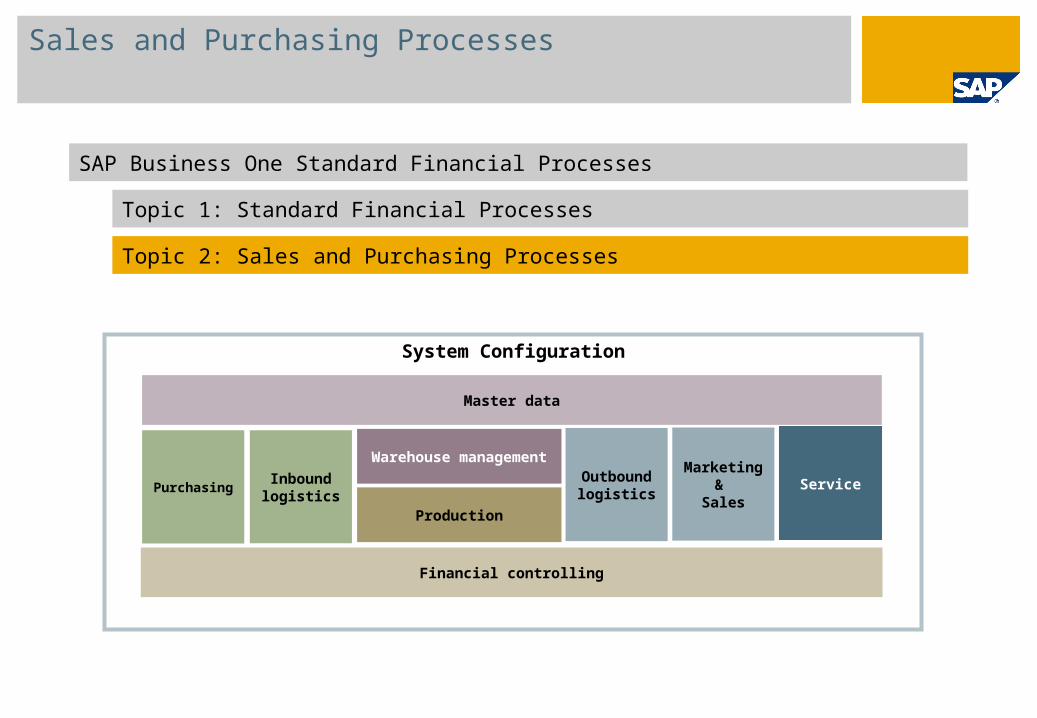

Sales and Purchasing Processes

SAP Business One Standard Financial Processes

Topic 1: Standard Financial Processes

Topic 2: Sales and Purchasing Processes

System Configuration

Purchasing

Warehouse management

Production

Inbound logistics

Outbound logistics

Marketing &

SalesService

Financial controlling

Master data

After completing this topic, you will be able to: Describe the steps in the standard financial processes in SAP Business

One. Describe the automatic journal entries created during the sales and

purchasing processes. Discuss the financial consequences of the processes on the general ledger.

Sales and Purchasing Processes:Topic Purpose

Automatic Journal Entries:Reflection Question

Standard

Sales Quotation Sales Order Delivery A/R Invoice Incoming Payment Deposit

In a standard sales process which documents affect the accountingsystem?

Automatic Journal Entries:Answer

Standard

Sales Quotation Sales Order Delivery A/R Invoice Incoming Payment Deposit

When managing perpetual Inventory

In a standard sales process which documents affect the accountingsystem?

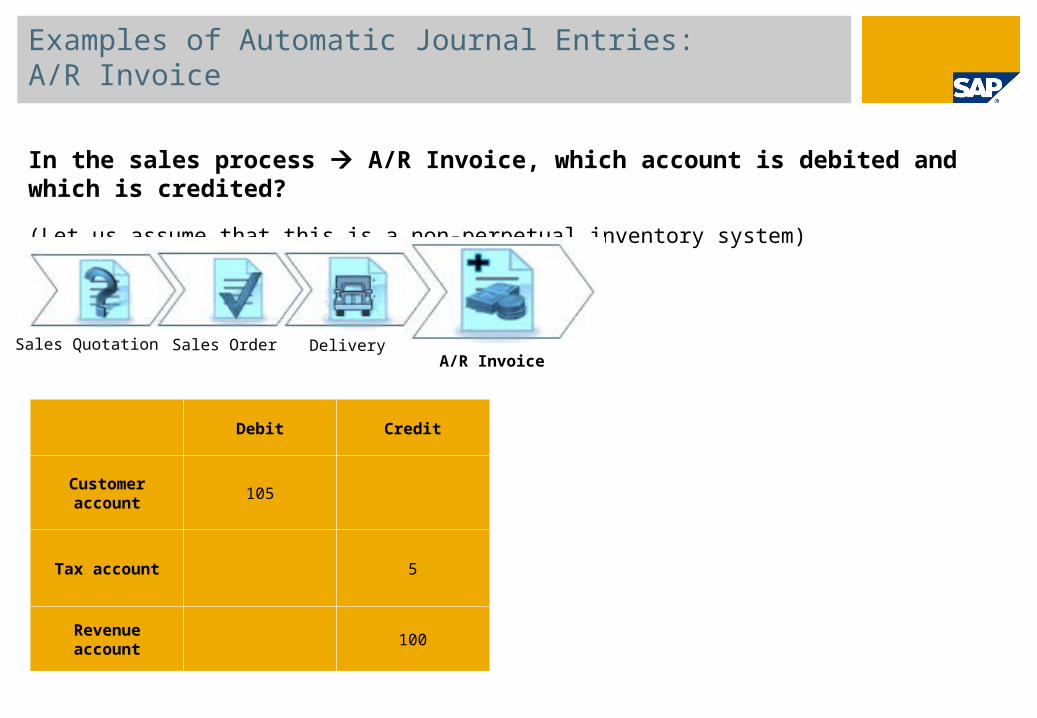

Examples of Automatic Journal Entries: A/R Invoice

Debit Credit

Customer account

105

Tax account 5

Revenue account 100

In the sales process A/R Invoice, which account is debited and which is credited?

(Let us assume that this is a non-perpetual inventory system)

Sales Quotation Sales Order DeliveryA/R Invoice

Examples of Automatic Journal Entries – Incoming Payment

Debit Credit

Cash clearing account

105

Customer 105

Possible Payment Means

Check Credit card Cash Bank transfer *BOE

*BOE - Bill of Exchange. This option is relevant for Italy, Portugal, Spain and France and activated by default.

In the sales process Incoming Payment, which account is debited and which is credited?

Sales Quotation Sales Order Delivery A/R Invoice Incoming Payment

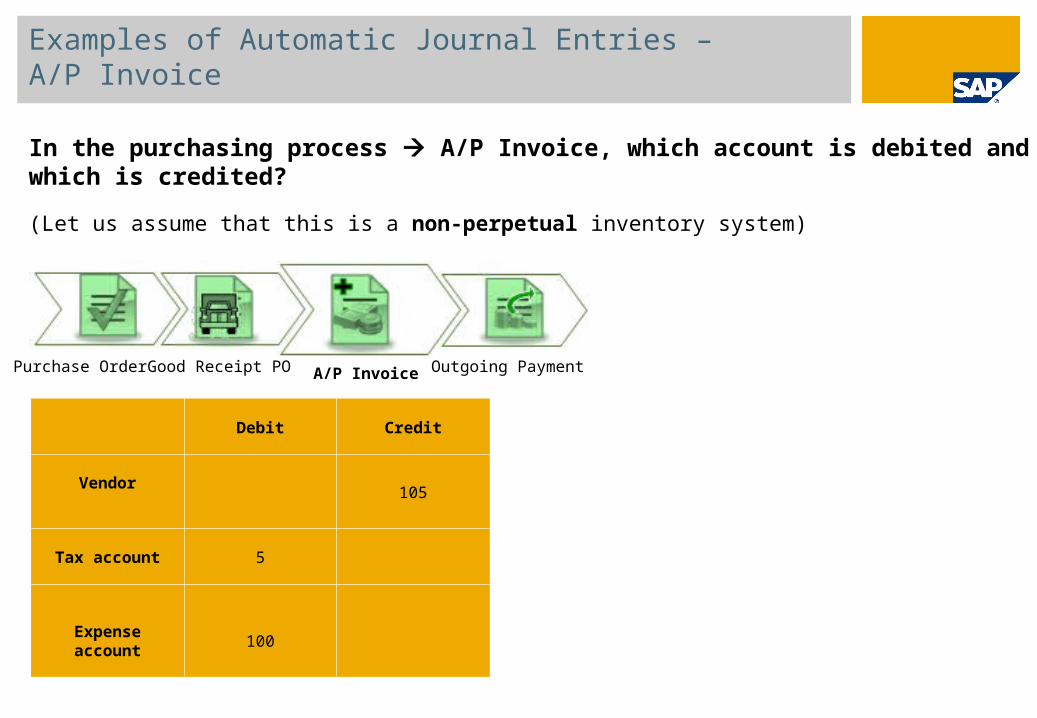

Examples of Automatic Journal Entries – A/P Invoice

Debit Credit

Vendor105

Tax account 5

Expense account 100

In the purchasing process A/P Invoice, which account is debited and which is credited?

(Let us assume that this is a non-perpetual inventory system)

)

Purchase Order Good Receipt PO A/P Invoice Outgoing Payment

Financial Settings: Reflection Question

G/L Account Determination Control Accounts

How does the system “know” which accounts to use automatically?

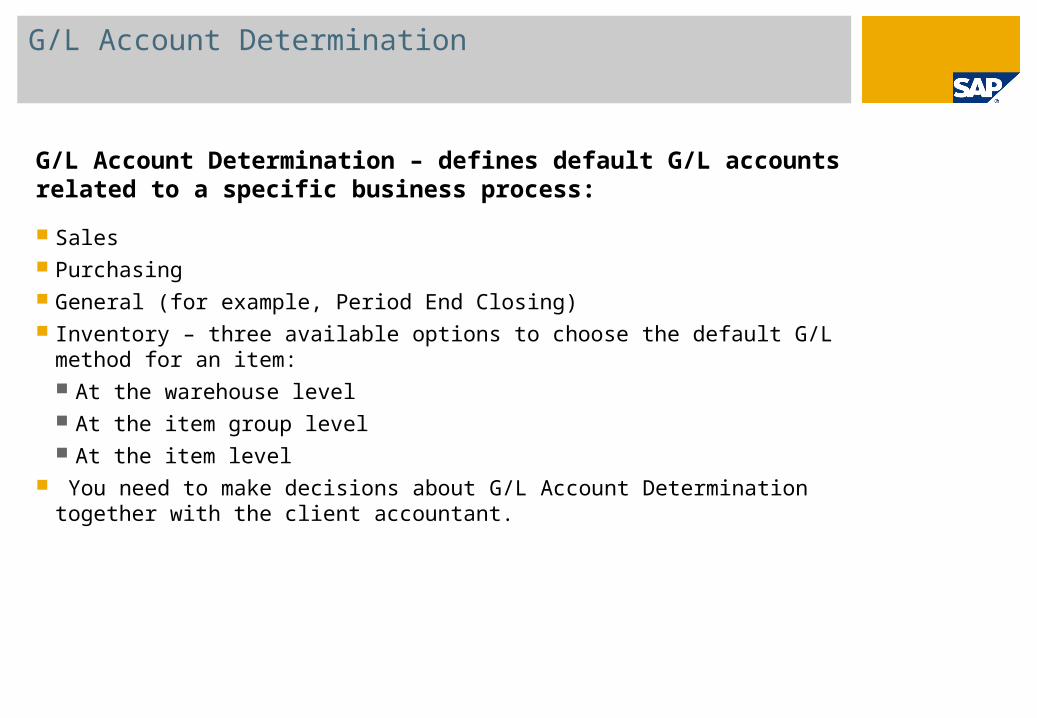

G/L Account Determination

G/L Account Determination – defines default G/L accounts related to a specific business process:

Sales Purchasing General (for example, Period End Closing) Inventory – three available options to choose the default G/L method for an item:

At the warehouse level At the item group level At the item level

You need to make decisions about G/L Account Determination together with the client accountant.

G/L Account Determination - Example

Debit Credit

Customeraccount

105

Tax account 5

Revenue account

100

A/R Invoice

The Revenue default G/L account is defined in the G/L Account Determination window, under the Sales tab.

Revenue account

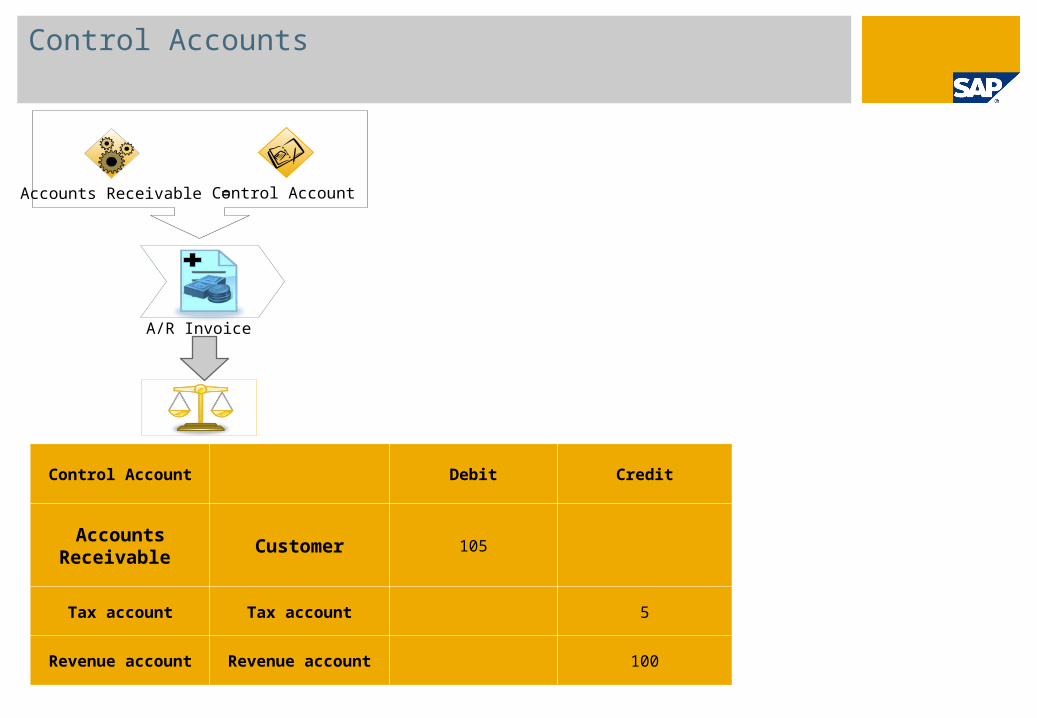

Control Accounts

Control Account Debit Credit

Accounts Receivable

Customer 105

Tax account Tax account 5

Revenue account Revenue account 100

Control AccountAccounts Receivable =

A/R Invoice

Exercise - Control Accounts

The Automatic Journal Entry Value

Debit Credit

Customeraccount

440

Revenue account

440

How does the system “know” the value to be credited and debited in an automatic journal entry created by an A/R Invoice?

(Let us assume that the customer is tax exempt).

A/R Invoice

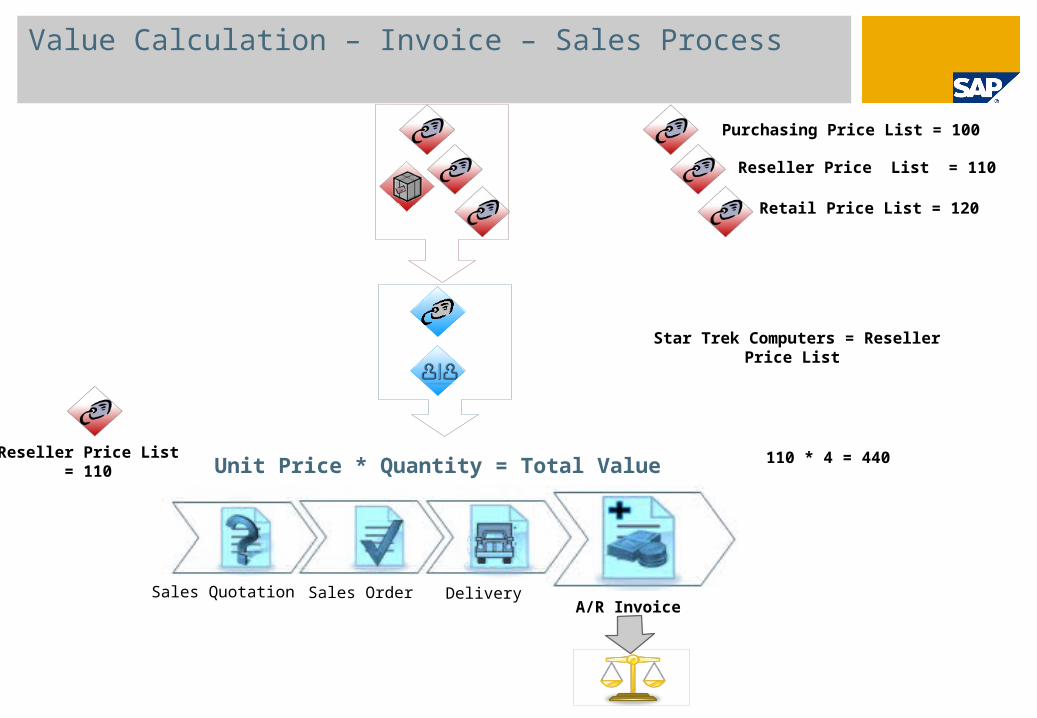

Value Calculation – Invoice – Sales Process

Unit Price * Quantity = Total Value

Purchasing Price List = 100

Reseller Price List = 110

Retail Price List = 120

Star Trek Computers = Reseller Price List

110 * 4 = 440Reseller Price List = 110

Sales Quotation Sales Order DeliveryA/R Invoice

Value Calculation – A/P Invoice – Purchasing Process

Unit Price * Quantity = Total Value

Coconut Devices = Purchasing Price List

100* 10 = 1000

Debit Credit

Vendor 1000

Clearing acc. 1000

Purchasing Price List =

100

Purchase Order Good Receipt PO A/P Invoice

Purchasing Price List = 100

Reseller Price List = 110

Retail Price List = 120

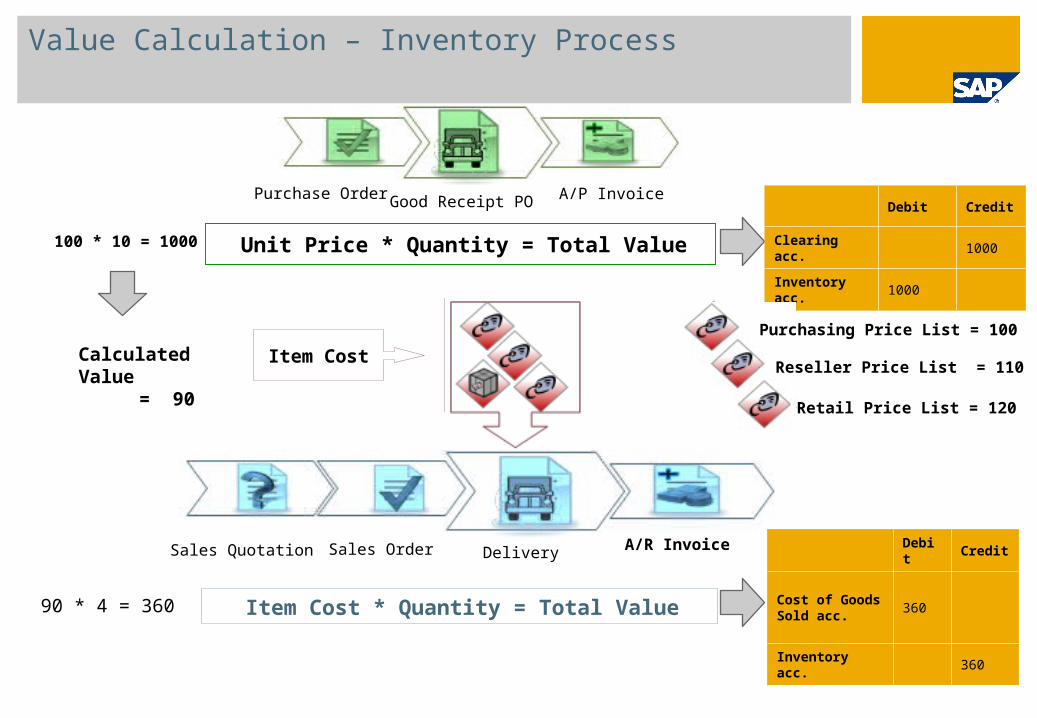

Value Calculation – Inventory Process

100 * 10 = 1000

Item CostCalculated Value = 90

Unit Price * Quantity = Total Value

Item Cost * Quantity = Total Value90 * 4 = 360

Debit Credit

Clearing acc. 1000

Inventory acc. 1000

Purchasing Price List = 100

Reseller Price List = 110

Retail Price List = 120

Debit Credit

Cost of Goods Sold acc.

360

Inventory acc. 360

Sales Quotation Sales Order Delivery A/R Invoice

Purchase Order Good Receipt PO A/P Invoice

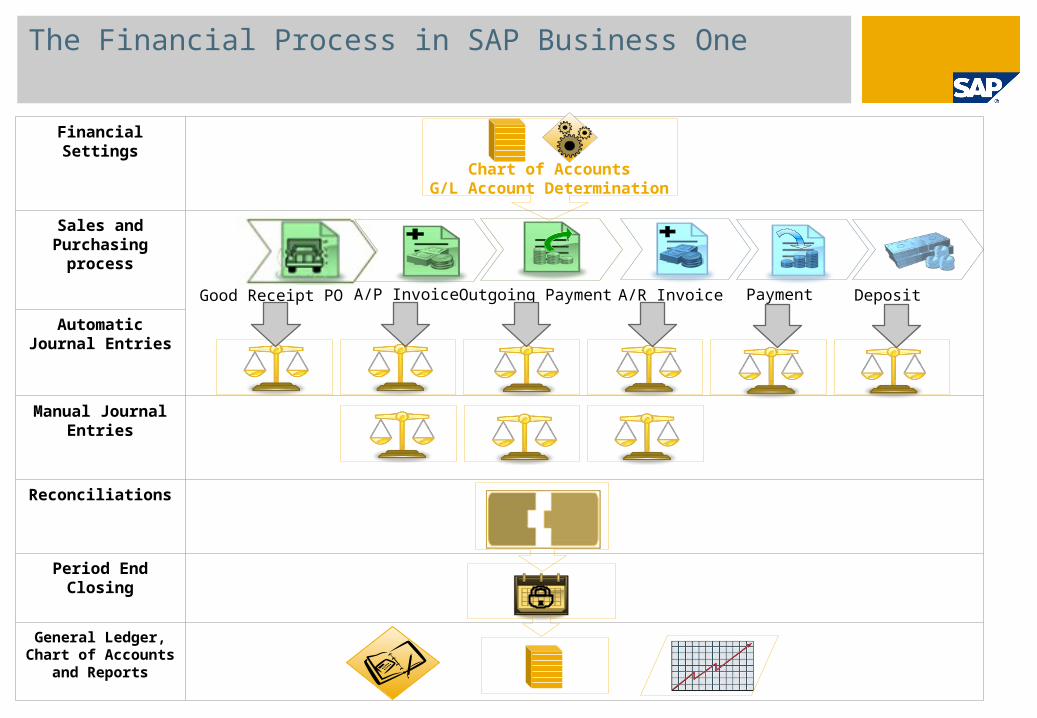

The Financial Process in SAP Business One

Financial Settings

Sales and Purchasing

process

Automatic Journal Entries

Manual Journal Entries

Reconciliations

Period End Closing

General Ledger, Chart of Accounts

and Reports

A/R Invoice Payment DepositA/P Invoice Outgoing PaymentGood Receipt PO

Chart of AccountsG/L Account Determination