unlocking constraints for better private sector …

TRANSCRIPT

PARTNERSHIPS FOR A HEALTHIER INDONESIA

UNLOCKING CONSTRAINTS FOR BETTER PRIVATE SECTOR PARTICIPATION

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

PARTNERSHIPS FOR A HEALTHIER INDONESIA

UNLOCKING CONSTRAINTS FOR BETTER PRIVATE SECTOR PARTICIPATION

ACKNOWLEDGMENTS

This document has been prepared by Vikram Rajan (Senior Health Specialist, World Bank) and Massimiliano Calì (Senior Economist, World Bank), in collaboration with Dev Terway (Health Care Consultant, World Bank Group), and with the assistance of Pui Shen Yoong (Economist, World Bank). It is a joint product of the Health, Nutrition and Population (HNP) and the Macroeconomics, Trade and Investment (MTI) Global Practices of the World Bank Group. The team would like to thank Tomio Komatsu (Senior Investment Officer, International Finance Corporation [IFC]), Jeffrey Delmon (Senior Public-Private Partnership [PPP] Specialist, World Bank), Dhawal Jhamb (Investment Officer, PPP Advisory Services, IFC), Natasha Beschorner (Senior Digital Development Specialist, World Bank), Pandu Harimurti (Senior Health Specialist, World Bank), Reem Hafez (Senior Economist, Health, World Bank), Eko Pambudi (Health Specialist, World Bank), and the Health Policy Plus private sector team for useful comments, as well as Nabil Rizky Ryandiansyah (Consultant, World Bank) for excellent research assistance. The layout design was done by Indra Irnawan.

We would also like to thank all the stakeholders in the health sector (the government, private sector providers, investor groups, consulting firms, and other development partners) who shared their valuable insights with us. The team would also like to thank Rodrigo A. Chaves (Country Director, Indonesia) and Enis Baris (Practice Manager, East Asia and Pacific, HNP) for their overall guidance. The opinions and conclusions shared in this document are the sole responsibility of the authors

CONTENTS

EXECUTIVE SUMMARY 1

section oneIntroduction 5

section twoDemand for and supply of health services and the role of the private sector 9

Growing demand for health services 10

Supply of health services has increased, but the quality is uneven 12

Private sector can help close the gaps between demand and supply 14

Private sector involvement also poses risks that call for proper oversight 15

section threeThe markets for health care providers 17

Primary health care 18

Secondary/specialist health care providers 24

Diagnostics providers 29

section fourAddressing constraints to private sector participation in health 31

The government should articulate a clear private sector engagement strategy for health 33

Revenue and expenditure reforms should address BPJS-K financial deficits 34

BPJS-K should strengthen its strategic purchasing function to improve quality of services and fill supply-side-gaps 36

Reforms in health education and in recognition of qualifications are needed to expand the quantity and quality of HRH 39

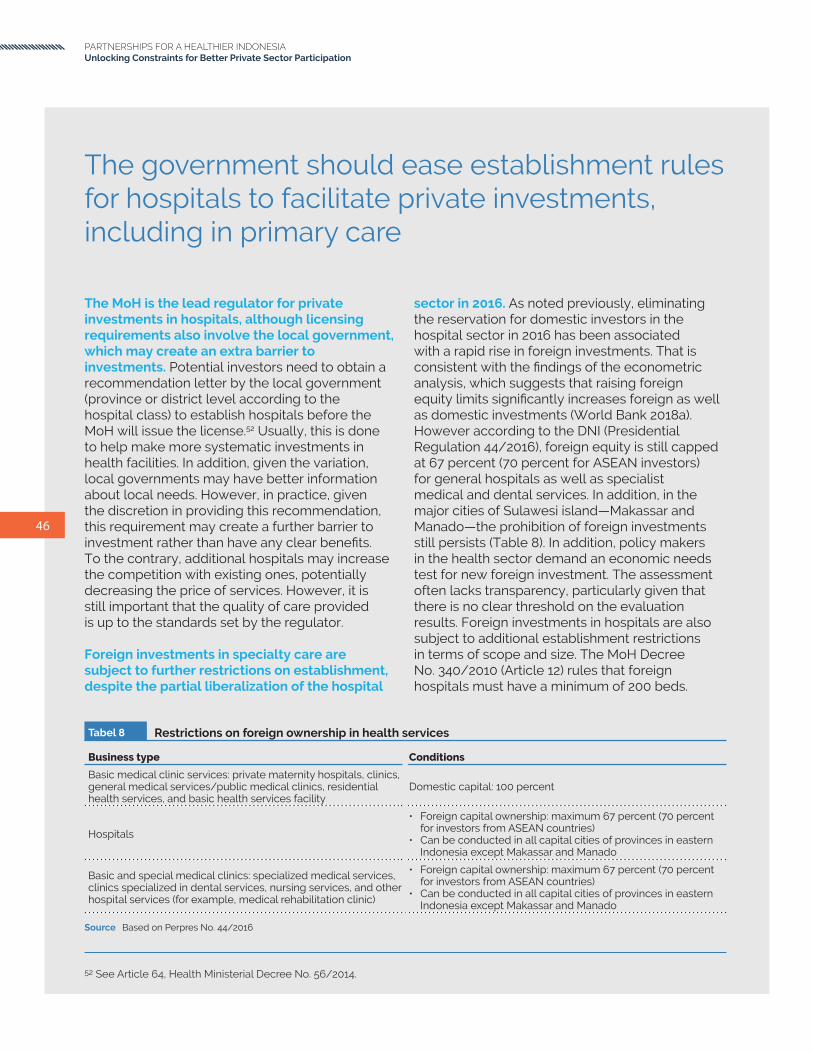

The government should ease establishment rules for hospitals to facilitate private investments, including in primary care 46

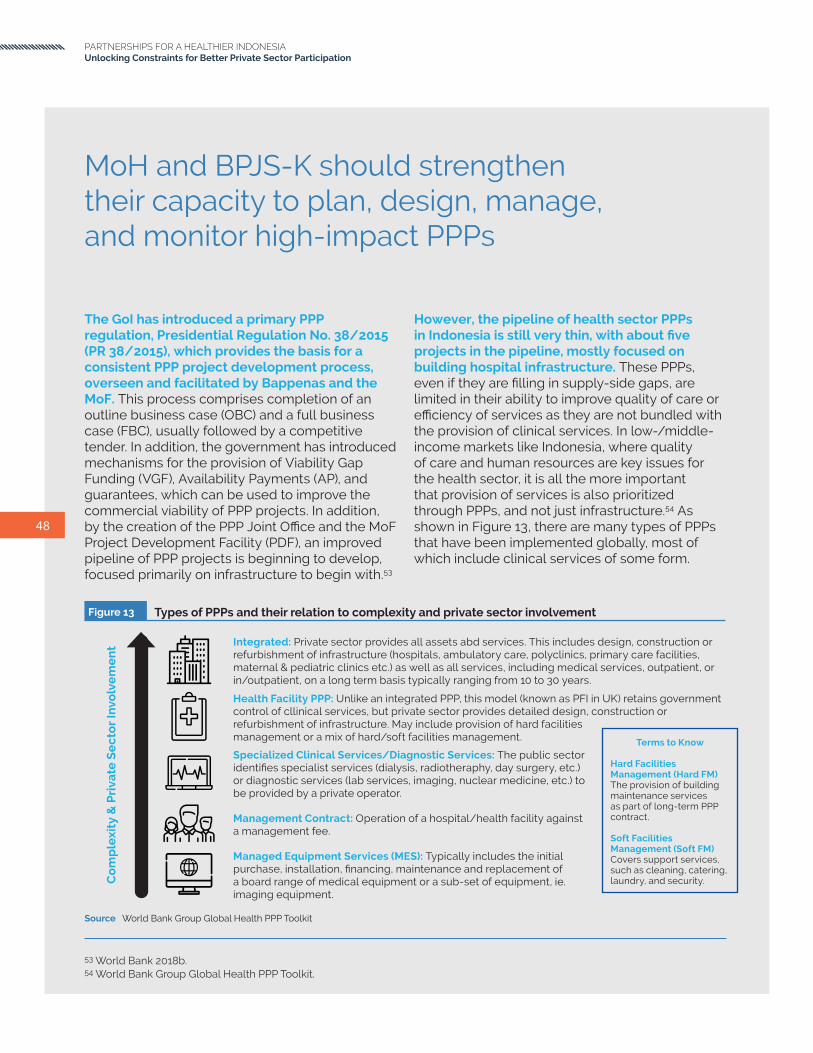

MoH and BPJS-K should strengthen their capacity to plan, design, manage, and monitor high-impact PPPs 48

The government should strengthen hospital and primary accreditation capacity to facilitate empanelment by BPJS-K 54

MoH should clarify and ease e-health regulations to foster digital health innovations 56

APPENDIXES 63

Abbreviations & Acronyms

AI Artificial Intelligence

AP Availability Payments

AR Accounts Receivable

ASEAN Association of Southeast Asian Nations

ASSRI Asociasi Rumah Sakit Swasta Indonesia or Indonesian Private Hospitals Association

BKPM Badan Koordinasi Penanaman Modal or Investment Coordinating Board

BMC Bhubaneswar Municipal Corporation

BPJS Badan Penyelenggara Jaminan Sosial (BPJS) or National Social Insurance Agency

BPJS-K Badan Penyelenggara Jaminan Sosial - Kesehatan or National Social Insurance Agency - Health

Bappenas Badan Perencanaan dan Pembangunan Nasional or Ministry for National Development Planning

BUMD Badan Usaha Milik Daerah or Provincial/Municipal-Owned Enterprises

BUMN Badan Usaha Milik Negara or State-Owned Enterprises

COB Coordination of Benefits

CSR/KTJS Social Responsibility Partnership

CT Scan Computerized Tomography Scan

DAK Dana Alokasi Khusus or Special Allocation Fund

DinKes Dinas Kesahatan or District Health Office

DJSN Dewan Jaminan Sosial Nasional or National Social Security Council

DNI Daftar Negatif Investasi or Negative Investment List

DRG Diagnosis-related Group

EMR Electronic Medical Record

FBC Full Business Case

FHP Foreign Health Professional

GDP Gross Domestic Product

GNI Gross National Income

GoI Government of Indonesia

GP General Practitioner

HHG Hermina Hospital Group

HIS Hospital Information Systems

HNP Health, Nutrition and Population

HPV Human Papillomavirus Virus

HRH Human Resources for Health

ICT Information and Communication Technology

IDI Ikatan Dokter Indonesia or Indonesian Doctors Association

IDHS Indonesia Demographic and Health Survey

IFC International Finance Corporation

IFLS Indonesia Family Life Survey

IIGF Indonesia Infrastructure Guarantee Fund

INA-CBG Indonesia Case-mix Based Groups

ISQua International Society for Quality in Health Care

IT Information Technology

JKN Jaminan Kesehatan Nasional or National Health Insurance Scheme

KAFKTP Komisi Akreditasi Fasilitas Kesehatan Tingkat Primer or Primary Care Accreditation Commission

KARS Komisi Akreditasi Rumah Sakit or Hospital Accreditation Commission

KBK Kapitasi Berbasis Komitmen or Commitment-based Capitation

KKI Konsil Kedokteran Indonesia or Indonesian Doctors’ Council

KPBU Kerjasama Pemerintah Dengan Badan Usaha or Government Cooperation with Business Entities

KSO Kerjasama Operasi or Operational Cooperation Contract

LPDP Lembaga Pengelola Dana Pendidikan or Indonesia Endowment Fund for Education

MCU Medical Checkups

MMR Maternal Mortality Rate

MoF Ministry of Finance

MoH Departemen Kesehatan or Ministry of Health

MRA Mutual Recognition Arrangements

MRI Magnetic Resonance Imaging

MTI Macroeconomics, Trade and Investment

MTKI Majelis Tenaga Kesehatan Indonesia or Indonesian Health Practitioners Assembly

NCD Noncommunicable Disease

NTT Nusa Tenggara Timur or East Nusa Tenggara

NUS National University of Singapore

OBC Outline Business Case

OECD Organisation for Economic Co-operation and Development

OOP Out-of-pocket

OTC Over-the-counter

PBI Penerima Bantuan Iuran or Public Subsidy for Insuring the Poor

PDF Project Development Facility

PERSI Perhimpunan Rumah Sakit Seluruh Indonesia or Association of All Indonesian Hospitals

PERKENI Perkumpulan Endokrinologi Indonesia or Indonesian Society of Endocrinologists

PHC Primary Health Care

PMK Peraturan Menteri Kesehatan or Minister of Health Regulation

PPP Public-Private Partnership

R&D Research and Development

RPTKA Rencana Penempatan Tenaga Kerja Asing or Foreign Worker Utilization Plan

RSCM Rumah Sakit Cipto Mangkukusumo or the Jakarta National Hospital

SIP Surat Ijin Praktek or Practice License

SUPAS Survey Penduduk Antar Sensus

TB Tuberculosis

UHC Universal Health Coverage

UI University of Indonesia

VGF Viability Gap Funding

WHO World Health Organization

vi

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

EXECUTIVE SUMMARY

1

EXECUTIVE SUMMARY

2

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

The supply of health care services in Indonesia has grown along with the demand for health services but public sector health services expansion remains strained. The demand for health services in Indonesia collects low fiscal revenues and allocates relatively little of its budgets to health services. As a result private providers have started to step up their investments and out-of-pocket (OOP) expenditures in health remain high. According to the Investment Coordinating Board (Badan Koordinasi Penanaman Modal or BKPM), private investment in the health and human services subsector reached US$148.7 million in 2018, growing some 130 percent per year, on average, since 2014. However, Indonesia’s annual inpatient admission rates, bed-to-population ratio, and doctor-to-population ratio remain among the lowest in the region and well below World Health Organization (WHO) recommendedstandards. The quality of health services offered in Indonesia also remains low, even for wealthier Indonesians who can afford better quality care.

The private sector involvement represents an opportunity to improve the availability and quality of health services by introducing better health products and medical technologies. Increased private investments that can bring better quality of services, improve access, and introduce efficient models of service delivery are key to ensure that supply meets demand. Besides providing needed scarce capital, greater private investment could promote local innovation, technology transfer, and low-cost solutions for health services and products such as medical devices and drugs.

However, increased private sector involvement is not a panacea and also poses challenges. Regulating private sector providers can be difficult to implement without effective regulatory levers and incentives. An expansion of the private sector could even worsen or create inequities in the distribution and quality of health services. Evidence does not necessarily support the assumption that private sector delivery by itself provides better quality care more efficiently. Similarly, for public-private partnerships (PPPs), results can be mixed and effectiveness depends on government commitment and capacity to

a large extent. Nonetheless, increasing private sector involvement in the health sector potentially offers more benefits than costs. The challenge is to manage trade-offs between equity and efficiency, growth and access to health, and private and public sector participation.

The private sector is already active at varying levels across all main health service sectors in Indonesia—primary, specialty, and diagnostics. Data on utilization rates suggest that it provides close to half of outpatient health services and 30–40 percent of inpatient services in Indonesia. The private sector’s presence in the primary care market is highly fragmented and is dominated by small providers with single doctor or multiple doctor clinics. The dominant form of private providers is general practitioner (GP) clinics, which are generally small and often consist of a single person business. Through providing online access to consultations, medications, and information, the emergence of digital health providers (such as HaloDoc, YesDoc, and Alodokter) can help address the limited access to primary health services particularly to underserved populations due to geographical location or socioeconomic status.

Private investment in the secondary/specialist health care subsector has grown rapidly, given the recent opening of the sector to foreign investments and the rapid development of the National Health Insurance Scheme (Jaminan Kesehatan Nasional, JKN). Unlike primary care, private investments in this segment are dominated by hospital groups (including Siloam, Hermina, Mitra Keluarga, and Awal Bros), which own many of the specialty hospitals. In spite of recent growth, they remain relatively small by international standards confirming the growth opportunities of the sector. The diagnostics sector has a similar structure, with a few specialized groups (including Prodia, BioMedika, and Paramita) dominating the private landscape and ample room existing for increased investments in light of rapidly rising demand.

The further development of private sector participation in the sector would require addressing a number of key regulatory/policy and nonregulatory constraints. The major constraints include (a) lack of a clearly articulated

EXECUTIVE SUMMARY

3

strategy for private sector engagement by the Government of Indonesia (GoI); (b) sustained and increasing financial deficit of the social health insurance agency or Badan Penyelenggara Jaminan Sosial - Kesehatan (BPJS-K)—the largest source of demand for many private providers—which constrain the ability of private providers to plan; (c) underutilization of the BPJS-K strategic purchasing function to drive improvements in service provision and quality; (d) inadequate availability of skilled health professionals; (e) restrictive establishment rules for private sector players—foreign in particular; and (f) lack of an enabling government environment to design, manage, and monitor PPPs. The other constraints are (g) poor capacity of the hospital and primary care accreditation systems; and (h) unclear and at times overly restrictive e-health regulations.

Possible options to address each of these constraints are described below

The government should articulate a clear private sector engagement strategy for health: (a) The Ministry of Health (Departemen Kesehatan, MoH), with BPJS-K, to prepare a database of private (and public) providers using multiple information sources and (b) the MoH, with BPJS-K, and the Ministry of National Development Planning (Badan Perencanaan dan Pembangunan Nasional, Bappenas to prepare a private sector engagement strategy, with differential strategies for various subsectors, to fulfill supply-side gaps by improving access, quality, and efficiency.

Revenue and expenditure reforms should address BPJS-K financial deficits: (a) Simplify the overall tobacco tax structure and increase tobacco excise taxes at the national level, with potential earmarking to BPJS-K; (b) update JKN premiums based on actuarial analysis; (c) subsidize premiums for the informal sector to address adverse selection by attracting and retaining a larger pool of healthy members; (d) address open-ended hospital payments where most spending occurs by introducing a budget and/or volume ceiling; and (e) introduce an explicit benefit package commensurate with available resources.

BPJS-K should strengthen its strategic purchasing function to improve quality of services and fill supply-side-gaps: (a) clarify roles of the MoH and BPJS-K to strengthen the purchasing role of BPJS-K; (b) BPJS-K, with the MoH, to strengthen performance-based capitation and hospital payments to incentivize broader health sector results; (c) the MoH, with BPJS-K, to target underserved areas and populations by introducing incentives; (d) the MoH, with BPJS-K, to develop an effective referral process regulation and modify/develop the necessary information systems to make this more patient centric, transparent, and supply evidence driven; (e) BPJS-K, with the MoH, to strengthen guidelines on quality of care by introducing clinical pathways, instituting clinical audits, strengthening monitoring of quality of care, and embedding quality-based criteria for reimbursement of providers.

Reforms in health education and in recognition of qualifications are needed to expand the quantity and quality of HRH: (a) Increase the domestic production of quality health professionals by expanding the capacity of the tertiary education sector; (b) relax restrictions to the hiring of foreign health professionals (FHPs), thus enabling the system to expand the stock of qualified human resources for health (HRH); and (c) reduce requirements to convert medical qualifications of Indonesian physicians who studied abroad.

The government should ease establishment rules for hospitals to facilitate private investments, including in primary care: (a) The MoH could remove the need for a recommendation letter from the local governments for the establishment of hospitals and have a transparent set of criteria for investment, endorsed by local governments, to replace it; (b) the MoH could remove the restriction on the scope of services for foreign hospitals; and (c) the President (through the decree on Negative Investment List [Daftar Negatif Investasi, DNI] could expand foreign equity limits to 100 percent across all health services sectors.

MoH and BPJS-K should strengthen their capacity to plan, design, manage, and monitor high-impact PPPs: (a) The Ministry of Finance

4

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

(MoF) and Bappenas, with MoH and BPJS-K, to establish a cross-government coordination mechanisms (also involving Indonesia Infrastructure Guarantee Fund [IIGF] and local governments) as well as public-private platforms to identify a pipeline of ‘high-impact PPPs’ that have private sector interest; (b) the MoH, with BPJS-K, to identify clear gaps which could be fulfilled by the private sector, including PPPs, based on demand patterns (population, disease burden, and utilization of services) as well as using available data on public and private sector provision; (c) the MoH and BPJS-K, with the MoF and Bappenas, to develop capacity as well as identify clear roles and responsibilities to design and manage the PPP transaction process, manage and monitor PPPs, and evaluate PPP results.

The government should strengthen hospital and primary accreditation capacity to facilitate empanelment by BPJS-K: The MoH and the Primary Care Accreditation Commission (Komisi Akreditasi Fasilitas Kesehatan Tingkat Primer, KAFKTP), to expand capacity (for facilitation and accreditation) and the latter to become fully independent of the MoH (both financially and institutionally) and (b) the Hospital Accreditation Commission (Komisi Akreditasi Rumah Sakit, KARS), to expand its capacity to cover the increased demand for hospital accreditation services.

MoH should clarify and ease e-health regulations to foster digital health innovations: (a) The MoH and BPJS-K should develop data privacy standards as well as pass the necessary legislation in consultation with stakeholders; (b) the MoH and BPJS-K should develop protocols for sharing data with privacy protections and consider using digital health providers for data analytics and service delivery; (c) the MoH, with BPJS-K, could develop legislation that focuses on e-prescriptions to improve access to prescribed medications, while maintaining necessary safeguards; (d) the MoH could lift restrictions on foreign telemedicine providers, specifically in pathology and radiology; and (e) the GoI to focus on the upgrading of mobile infrastructure in remote regions to improve access to 3G and the use of smartphones.

5section 1 .

Introduction

6

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

Indonesians have become healthier in recent decades as confirmed by the progress on key health indicators. Over 1960–2016, average life expectancy increased from 45 to 69 years.1 Under-five mortality declined nearly tenfold to 25 per 1,000 live births, while infant mortality declined sixfold to 21 per 1,000 live births over the same period. The share of pregnant women receiving four or more antenatal care visits has also increased, from 55 percent in 1991 to 77 percent in 2017.2 Importantly, Indonesia has charted remarkable progress on its path towards universal health coverage (UHC). With the introduction of National Health Insurance Scheme (Jaminan Kesehatan Nasional, JKN) in 2014, health insurance coverage rates have increased significantly from 27 percent in 2004 to around 80 percent in 2018.3

Despite these advancements, significant challenges remain in improving maternal health and nutrition and in tackling persistent communicable diseases. Indonesia’s maternal mortality ratio remains high relative to its income level at 126 per 100,000 live births in 2015 (from 446 in 1990).4 This means that one Indonesian mother dies in childbirth every 1.4 hours on average. In addition, a third of children under five years or 9 million children suffer from stunting in 2018,5 the fifth highest prevalence in the world. Finally, Indonesia is now the second largest contributor to the global tuberculosis (TB) burden, with over 1 million cases reported in 2017 (WHO and MoH Indonesia 2018). New challenges such as multidrug-resistant TB have also emerged.

As the Indonesian population grows older, new challenges are emerging. Noncommunicable diseases (NCDs) already account for the largest share of the disease burden (66 percent),6 nearly doubling since 1990. NCDs are likely to rise further as the share of the population ages 65 years and above doubles to 10 percent between 2015 and 2030. Moreover, unhealthy lifestyle choices contribute to the prevalence of NCDs. Indonesia has one of the highest rates of cigarette consumption in the world: about half the adult population (about 85 million people) smoke, including 68 percent of adult males. Tobacco is an important risk factor in the top five leading causes of death in Indonesia, which are stroke, ischemic heart disease, diabetes, TB, and cirrhosis.7

Regional and income-related inequalities in health outcomes persist. National averages obscure wide disparities in health outcomes between urban and rural areas, the rich and poor, and East and West Indonesia. In 2012, the under-five mortality in the Eastern Indonesian provinces of East Nusa Tenggara (Nusa Tenggara Timur, NTT) and Maluku was close to 60 per 1,000 live births, much higher than the (then) national average of 40 per 1,000.8 In addition to large regional disparities, income-related inequalities9 remain across the country. Although the gap in health outcomes between the richest and poorest households has decreased over the last two decades, under-five and infant mortality rates are still more than double among poorer households.10

1 World Bank World Development Indicators; latest data available on April 1, 2019.2 Refers to the share of women ages 15–49 years who attended antenatal care visits once each in the first and second trimesters

and twice in the third trimester. Source: Indonesia Demographic and Health Survey (IDHS) 2017.3 Susenas household survey, various years, and estimation from online Badan Penyelenggara Jaminan Sosial - Kesehatan (BPJS-K)

database (health facilities).4 Based on World Health Organization (WHO)-United Nations Children’s Fund-World Bank estimates 2017. Census data indicate

that the maternal mortality rate (MMR) may be even higher; the official MMR used by the Government of Indonesia (GoI) is 305 per 100,000 live births, Survey Penduduk Antar Sensus (SUPAS) 2015.

5 MoH Riset Kesehatan Dasar (Riskesdas) survey, 2018.6 Institute of Health Metrics and Evaluation 2017.7 Ibid.8 IDHS 2012 is used to compare between regional and national estimates as this is not yet available for IDHS 2017. 9 The consumption Gini Index, a measure of income inequality, grew from 30 (2003) to 40 (2016).10 World Bank staff calculations from IDHS 2017.

7

The private sector can play an important role in driving better health outcomes for all Indonesians. In many developing countries where public resources are limited, the private sector could help ensure that the supply of health care services meets the demand. Indonesia is no exception, particularly at a time when growing incomes and demographic and epidemiological transitions increase the demand for health services and public sector providers are already strained. The private sector could also introduce efficiency and innovations through technology. Examples include digital health, telemedicine, low-margin high-volume specialty care, and innovations in diagnostics and radiology.

There has been increased utilization of outpatient and inpatient private sector health services by all Indonesians, including the poor (bottom 40 percent of the population in terms of wealth, Table 1). Also, with the introduction of JKN in 2014, utilization rates have almost doubled on average for inpatient care and for the poor, including in private sector facilities. While outpatient utilization rates have increased only marginally, even post JKN, private sector utilization constitutes between one-half and almost two-thirds of total outpatient utilization.

8

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

Tabel 1 Inpatient and outpatient utilization rates for private and all facilities

Function 2011 2012 2013 2014 2015 2016 2017 2018

Outpatient utilization (all)

National 13.4 12.9 13.5 14.4 17.0 16.1 13.3 15.1

Bottom (40%) 12.2 11.8 12.3 13.2 16.0 15.1 12.2 14.3

Outpatient utilization (private)

National 8.4 8.5 9.1 9.8 10.8 10.1 8.5 9.1

Bottom (40%) 6.7 6.8 7.4 8.1 8.9 8.3 6.8 7.5

Inpatient utilization (all)

National 2.1 1.9 2.3 2.5 3.6 3.7 4.2 4.7

Bottom (40%) 1.4 1.3 1.6 1.7 2.6 2.7 3.1 3.6

Inpatient utilization (private)

National 1.0 0.8 1.1 1.2 1.7 1.7 2.0 2.2

Bottom (40%) 0.5 0.4 0.6 0.6 0.9 0.9 1.1 1.3

Source Susenas

Of course, increased private sector involvement is not a panacea. An expansion of the private sector could even worsen or create inequities in the distribution and quality of health services (Chanda 2002) by creaming off the top consumers and human resources in the system. In addition, a rapid expansion of the private sector in the health sector may generate the challenges of ensuring quality of care in a system with limited oversight capacity. The challenge is to manage trade-offs between equity and efficiency, growth and access to health, and private and public sector participation.

Considering these trade-offs, this report investigates the opportunities and constraints to more and better private sector participation in the Indonesian health services sector. It focuses on three key segments of the health care market—primary care (including digital health), secondary/specialist health, and diagnostics,11 drawing from interviews with existing private providers as well as recent secondary evidence to illustrate challenges faced on the ground. This report also benefits from discussions with policy makers from various government agencies on issues related to the report but not necessarily done only for the report. The report identifies some of these constraints and proposes possible recommendations to address them. While the list of factors and corresponding recommendations are not necessarily exhaustive, it does highlight key priority areas to be considered. The report concludes with some options for reforms that could help unleash the potential of the private sector to contribute towards a healthier, happier, and more productive Indonesia.

11 Given the large scope of private sector health delivery, the report focuses on three subsectors that were most service delivery oriented. Hence, this excludes other important subsectors such as pharmaceuticals and medical technology, which could be covered as part of additional analytical work.

9section 2 .

Demand for and supply of health services and the role of the private sector

10

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

Out-of-pocket (OOP) expenditures on health are high in Indonesia compared to developed countries. In 2016, public health spending made up nearly half (45 percent) of total health spending in Indonesia but this was followed by private or OOP expenditures, which accounted for about 35 percent.12 Social health insurance accounted for about 17 percent and development aid accounted for the rest. The share of OOP spending has decreased in recent years and is on par with other lower-middle-income countries, but it remains nearly triple the average level in developed countries.13 The high OOP share is in part due to low public health expenditures and the fact that public facilities lack trained staff, diagnostic capacity, and medicines, driving patients to pay out of pocket for better quality services.

The demand for privately funded health services in Indonesia is likely to rise further as several trends persist.

Continued expansion of the middle class, especially in urban areas. The growth of the Indonesian economy, along with the increase in the share of the population living in urban areas, has facilitated the emergence of a large middle class14 that requires more and better health services. The middle class expanded at 10 percent per year between 2002 and 2016 and now represents a fifth of the population (World Bank, 2019). Growing affluence, along with limitations in public service delivery, is increasing the demand for private health services, especially in urban areas. In 2018, half of the households classified as middle class and 62 percent of the upper class used private hospitals for inpatient treatment,

compared with about one-fifth of Indonesians who are poor or vulnerable to poverty (Figure 1). Similarly, the middle and upper classes are more likely to go to a hospital for childbirth instead of the local health center or clinic and they are more likely to be attended by a doctor rather than a midwife or nurse. As economic growth and urbanization continue to boost the expansion of the middle class, demand for better quality health services—at least as perceived by the patient15 —will continue to grow.

Growing demand for health services

12 MoH National Health Accounts, 2016.13 According to WHO/World development Indicators data, OOP makes up only 13 percent of total current health expenditures in

high-income countries. The average for lower-middle-income countries excluding Indonesia is 40 percent. 14 Defined as those who have less than a 10 percent chance of being poor or vulnerable in the future, given their current consumption15 Patients may be able to perceive better services using proxies on how good the services are, but they may not be able to make a

judgment on whether they received the appropriate treatment or not.

Figure 1 Middle- and upper-class Indonesians are more likely to use private health services

(Choice of health care by consumption class, percent of households)

Source World Bank staff calculations using Susenas 2018..

Public hospital Puskesmas Private hospital Others

Vulnerable

24

Aspiringmiddle class

34

Middleclass

53

Upperclass

62

Poor

19

11

Demographic and epidemiological shifts. Demographic, epidemiological, and financing transitions will further increase the demand for health services. The rising burden of NCDs, in addition to existing communicable diseases and perinatal conditions, will increase the demand for health services, especially as the needs move toward continuous, chronic care rather than just acute, episodic care. Demand could also increase due to more frequent visits to facilities, longer treatment periods, and more specialized care at the primary and referral levels, as well as due to complications that arise from the lack of early diagnosis and effective treatment.

Expansion of health insurance. In 2014, Indonesia introduced JKN and committed to achieving UHC by 2019. As of April 1, 2019, nearly 220 million Indonesians or about 82 percent of the total population were covered by the scheme,16 making it the largest single payer social health insurance scheme in world. JKN provides a generous benefit package covering all medically necessary treatment with no caps or co-payments. It is separated into two categories: BPJS-K (for nonemployees, self-employed, or informal workers) and BPJS Ketenagakerjaan (for employees of public and

private companies, who are required to make contributions to BPJS-K). While the premium for the poor is completely covered through a public subsidy, Public Subsidy for Insuring the Poor (Penerima Bantuan Iuran, PBI), the remaining population pays for the premium through payroll or voluntary contributions (for informal sector nonpoor).

With the introduction of JKN, Indonesia’s private hospitals have seen a significant increase in the total number of patients seeking treatment. While most rural Indonesians only have access to a puskesmas (public primary health centers) as a means of primary care, populations in urban or semi-urban areas can also access several private sector providers for primary care, and if required, can be referred to specialist treatment by either public or private providers that are empaneled by BPJS-K. As a result, inpatient and to some extent outpatient utilization rates have increased since 2014, especially among the bottom 40 percent (Figure 2). Major hospital groups such as Siloam, Mitra Keluarga, and Hermina have long-term expansion plans for hospitals in second-tier cities, where increasing incomes and enrolment in private insurance have increased the demand for private providers.

16 Source: BPJS-K online dashboard. Accessed April 12, 2019. https://faskes.BPJS-K-kesehatan.go.id/aplicares/#/app/peta

Figure 2 Inpatient and outpatient utilization rates have increased after JKN introduction (2014)

Source World Bank staff calculations from Susenas.

0%

2%

4%

6%

8%

16%

National

Outpatient utilization (all)

2011 2013 2018

14%

12%

10%

Bottom (40%) National

Inpatient utilization (all)

Bottom (40%)

12

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

17 Indonesia spends US$49 per capita on health, well below the recommended US$110 per capita needed to deliver an essential package of UHC (according to the Disease Control Priorities initiative, DCP3). In share of GDP terms, total current health spending in Indonesia is among the lowest in the world at 3.3 percent of GDP.

As the demand for health services has risen, so has the overall supply of health care services, but public services are underfunded. Total per capita spending on health care has steadily increased in Indonesia, growing by 14 percent per year between 2000 and 2015.17 Nonetheless, public expenditure on health only amounts to 1.4 percent of gross domestic product (GDP)—almost half of what other lower-middle-income countries spend. This is in part due to the fact that Indonesia

Supply of health services has increased, but the quality is uneven

does not collect sufficient revenues for a country of its size and income level, constraining the overall envelope available for public spending (at 14.7 percent of GDP in 2017, Indonesia has one of the lowest revenue-to-GDP ratios in the world). However, this is also due to a relatively low allocation of public expenditures to health. Even the Dominican Republic, with a similar revenue-to-GDP ratio and GDP per capita, spent twice the amount on health as a share of GDP (Figure 3).

Figure 3 Indonesia spends less on health compared to countries with similar per capita income

(Y-axis: General Government health expenditures as a share of GDP, X-axis: log GDP per capita in 2011 purchasing power parity terms)

Source World Bank staff calculations from World Development Indicators.Note Data on GDP per capita for 2017; data on general government health expenditure from 2015.

Dominican Republic

Indonesia

Malaysia

Thailand

Vietnam

-2

0

2

4

6

8

10

6 7 8 9 10 11 12

13

As the expansion in public services is unable to meet the demand for health care, private providers have started to step up their investments. According to the Investment Coordinating Board (BKPM), private investment in the health and human services subsector reached US$148.7 million in 2018, growing some 130 percent per year on average since 2014 (Figure 4). Most of the increase is due to growth in domestic investment, which still accounts for the bulk of private investment in the health sector, but foreign investment has also charted remarkable growth, increasing by 73 percent per year over the same period to US$43 million in 2018. There is clearly still scope for increased private sector participation, as domestic and foreign investments in health accounted for only 0.45 and 0.15 percent, respectively, of total investments.

Notwithstanding the increase in the public and private supply of health care services, pockets of the Indonesian population remain underserved. Indonesia’s annual inpatient admission rate remains one of the lowest in the region and despite recent increases the bed-to-population ratio remains low at 1.16 per 1,000 people—more than half the WHO-recommended standard of 2.5 beds per 1,000 people. Furthermore, the national average

masks the maldistribution of beds across the country, as the ratio ranges from 0.68 in West Nusa Tenggara to 2.24 in Jakarta.18 Many Indonesians, especially in eastern provinces, still face significant physical and time barriers in accessing health care (World Bank 2016), resulting in high morbidity and mortality rates and the inefficient use of potentially productive time by patients as well as of accompanying family members and friends (Schoeps et al. 2011).

The perceived quality of health services offered in Indonesia also leaves much to be desired, especially for wealthier Indonesians who can afford better quality care. In 2015, it was estimated that 600,000 Indonesians sought medical tests and treatment abroad, spending US$1.4 billion,19 mostly in Malaysia, followed by Singapore and Thailand. When indirect spending is included, it is estimated that Indonesia is losing some US$4 billion a year due to outbound medical tourism (Lim et al. 2018). However, while Indonesian patients with the financial means can seek medical treatment abroad, the domestic market—particularly for those that fall just below the affordability line of foreign medical treatment—remains the prime targets for the top domestic hospitals.

Figure 4 Investment in health has increased significantly, especially since reducing some restrictions in 2016

Source BKPM, World Bank staff calculations.

18 MoH Profil Kesehatan 2017.19 https://www.liputan6.com/bisnis/read/2455394/berobat-ke-luar-negeri-orang-ri-habiskan-rp-182-triliun

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2012 2013 2014 2015 2016 2017 2018

Domestic investment in health in USD mn Foreign investment in health, USD mn

14

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

The unmet demand for health services in Indonesia represents an opportunity for the private sector. Globally, the private sector plays an important role in health financing and health service delivery. This is especially the case in lower-middle-income countries such as Indonesia where limited fiscal space and competing development priorities constrain the amount of public resources that can be channeled toward addressing public health needs. Private providers can also help improve access to health care services by lower-income populations, especially if they are linked to social health insurance schemes. Indeed, analysis by World Bank (2010) shows that the rise in private physicians in Indonesia has been associated with greater utilization of health services by the poor, through a reduction in the congestion in clinics.

Private sector can help close the gaps between demand and supply

The private sector also plays a critical role in improving the availability and quality of health products and the development of medical technologies. The private sector plays a critical role in research and development (R&D) and manufacturing of medicines, commodities, and medical devices, spending over US$135 billion a year on pharmaceutical R&D. In emerging markets such as Indonesia, greater private investment could promote local innovation, technology transfer, and low-cost solutions to improve the availability of medical devices and drugs. Again, the private sector also has a role to play in diminishing inequities: in Tanzania, for example, AirTel Tanzania sends free text messages about infant care to mothers and pregnant women, helping reduce infant mortality by 64 percent and maternal mortality by 55 percent (West 2015). Advancements in telemedicine can also help develop the quality of human resources for health (HRH), for example, through remote diagnosis and training.

15

This is not to say that greater involvement of the private sector automatically improves the overall quality of care or efficiency. Evidence does not necessarily support the assumption that private sector delivery by itself provides better quality care more efficiently. While the private sector performs better on drug supply, timeliness, and patient hospitality, some reviews point to poor quality of care and worse patient outcomes and efficiency than in the public sector—partly because of the perverse incentives for unnecessary testing and treatment that are provided by fee-for-service systems (Basu et al. 2012; Berendes et al. 2011; Herrera et al. 2014; Patouillard et al. 2007). This may also be reflective of the enormous heterogeneity of providers in the private sector.

In Indonesia, a study on primary health care (PHC) supply-side readiness indicated that publicly funded puskesmas were in fact more prepared to provide both general and specific PHC services compared to private general practitioner (GP) clinics. The general service readiness—an index20 of tracer indicators that measures supply-side readiness as a key prerequisite for improved quality of care21 —for public primary health facilities was 78 percent while private health facilities was 61 percent (Rajan et al. 2018). Put differently, to assess the facilities’ readiness for provision of general health care services, this report analyzed the availability of about 34 components—including basic amenities, equipment, diagnostics, and essential medicines.

Private sector involvement also poses risks that call for proper oversight

On average, the puskesmas had 26 components available compared to private GP clinics that had only 20 components. There are significant gaps in the readiness of private sector clinics to serve patients: for example, only 35 percent of all private primary health facilities had facilities for basic diagnostics compared to 66 percent of puskesmas.22 Among private sector facilities, those empaneled for BPJS-K tend to be more supply-side ready than those that were not. For all the specific clinical and outreach services, such as for child health, immunization, and communicable diseases, the puskesmas were better prepared than the private clinics to offer services.

Without the necessary regulation, private sector health care expansion may lead to distortions in service provision, including the distribution, quality, and price of health services. These distortions arise from the failures usually associated with health care markets due to the underlying information and power asymmetry between providers and patients associated with many health care interventions (Doherty and McIntyre 2013). Hence, normal market mechanisms that provide incentives for profit making can threaten broader health policy objectives such as the achievement of equitable, efficient, and sustainable health systems (Afifi, Busse, and Harding 2003). In the context of an expanding private health sector, it is important that regulatory frameworks are established to ensure that these potential market failures are

20 Service readiness is measured by a set of tracer indicators across five domains: basic amenities, basic equipment, standard precautions for infection prevention, diagnostic capacity, and essential medicines.

21 The results of this study should not, therefore, be interpreted as a study on quality of care outcomes at the public and private sector PHC facilities in Indonesia but as a measure of supply-side readiness as a necessary, but not sufficient, prerequisite to improve quality of care.

22 Part of the reason for the low level of capital equipment of private primary care clinics is their low profitability which typically does not suffice for capital investments beyond the basic level.

16

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

mitigated and private health markets contribute to achievement of health policy goals. Regulatory frameworks clarify policy objectives, establish instruments for regulation (such as legislation or voluntary incentives), set up regulatory structures, ensure dialogue between the members of regulatory networks, and monitor the effectiveness of regulation (Afifi, Busse, and Harding 2003).

Regulating private sector providers can be more difficult and expensive than public sector providers (Wadge et al. 2017). It is important to note that the impact of private sector participation in health can also differ by subsector, depending on the barriers to entry. There is a strong case for private sector involvement in outpatient services, for instance, because it is easier to establish criteria for licensing and regulating service provision, making them more contractible and open to

competition. Pharmacies and laboratory services are also easy to regulate, so they also see high levels of private provision. On the other hand, it is more difficult to monitor services provided by informal health providers or unauthorized drug retailers operating in more remote areas. It is estimated that in many low-income and lower-middle-income countries about 28.5 percent of medicines can be counterfeit or substandard (Almuzaini, Choonara, and Sammons 2013).

The private sector does offer some advantages over the public sector and can be a policy option, if the distortions arising due to the health market failures are mitigated (Doherty and McIntyre 2013). Hence, increasing private sector involvement in the health sector needs carefully designed and well-implemented policies and regulations to ensure that the potential benefits outweigh the costs.

Tabel 2 Potential benefits and costs of increased private sector participation in the health sector

POTENTIAL BENEFITS POTENTIAL COSTS

Reduce the patients’ burden of public sector structures Reduce the quality of and accessibility to health services for the poor

Expand the range and quality of health services Internal brain drain (poaching of the private sector from the public sector)

Help retaining health professionals Reduce support for quality public health services

Facilitate positive spillovers to public sector (for example, via exchanges of ideas, knowledge, imitation effects)

Deteriorate quality of training due to private sector-led expansion

Use of private sector to reach public sector objectives (for example, public-private partnership [PPP])

Upgrade and expand the health services infrastructures

Expand health training facilities

Facilitate expansion of health insurance

Source Cali and Stern 2009

17section 3 .

The Markets for Health Care Providers

18

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

The primary care market is highly fragmented in Indonesia, consisting mostly of puskesmas or publicly funded community health care centers and private GP clinics. There are roughly 9,909 puskesmas across the archipelago.23 Although there are no reliable statistics on the number of private primary care providers, there are at least an estimated 10,000 private GP clinics that have been approved by BPJS-K. Since the introduction of BPJS-K, the number of GPs has seen a significant increase in their patient numbers, and they have been instrumental in relieving some of the demand from puskesmas and public hospitals.

Each puskesmas covers a large catchment area, and their growth has not kept pace with demand growth, thus opening further opportunities for private sector participation. Each puskesmas meets the needs of close to 30,000 people, mostly catering for outpatient services although about a third of them also provides inpatient care. The supply of public PHC facilities grew at 0.4 percent per year from 2013 to 2017, suggesting that the government’s focus has been to expand secondary and tertiary care facilities rather than primary care facilities. This creates further investment opportunities for the private sector whose growth presents challenges as well.

While health care groups have developed some chains of primary clinics, the private sector remains dominated by single-practice GP clinics. Some hospital groups have invested in primary care clinic chains, such as Mayapada Clinics, Siloam Clinics, and Brawijaya Clinics. These clinics are located mostly in Jakarta and Bali and serve as outpatient service providers or

Primary Health Care

as referral centers to their hospitals for patients covered by private insurance and OOP payers. However, the absence of clear economies of scale and the importance of patients’ relation with the GP—as opposed to the brand of the clinic—have largely kept the private sector highly dispersed. GP clinics represent the highest number of private primary care facilities across the country, with many being individual or group GP clinics that provide outpatient services.

While there are no specific data on the cost structures of these private primary care clinics, the fact that supply-side readiness in these clinics is lower than that of puskesmas may indicate that this is a lower-margin business that may need specific investments and incentives from the public sector to improve quality and performance. In terms of broader health system efficiency, this would be beneficial as early diagnosis and treatment at the primary care level (primary and secondary prevention) would be much less expensive than treating complications of undiagnosed and untreated diseases at the hospital level,24 justifying public financing. In addition, most OOP expenditures to purchase services at the private clinics are inefficient by themselves.

The Ministry of Health (Departemen Kesehatan, MoH) and the Indonesian Doctors Association (Ikatan Doktor Indonesia, IDI) allow for the issuance of three practice licenses (Surat Ijin Praktek, SIPs) to both GPs and specialist doctors. The implementation of this is strict for GPs where they can utilize their SIPs at a private or public hospital, a clinic, and a private practice. GPs are

23 As of end-2017. Source: MoH, Profil Kesehatan 2017.24 Diagnosis and treatment of hypertension to control blood pressure versus treatment of complications like cardiovascular disease

or stroke.

19not required to utilize all three licenses. However, many doctors work at one hospital in the morning hours, one in the afternoon/evening hours, and at a private practice (usually at their home). The regulations require that a doctor obtain an SIP from the local district Department of Health (Dinas Kesehatan, DinKes) where they practice.

The market is dominated by domestic investors, as foreign investors are essentially not allowed to invest in the PHC sector under current regulations. The latest Negative Investment List (Daftar Negatif Investasi, DNI) (Presidential Regulation No. 44/2016) reserves virtually all of the PHC services to domestic investors.25 Foreign investors are instead allowed to invest in outpatient polyclinics but are required to provide specialist doctor outpatient services (such as dental clinics and rehabilitation services). However, specialist doctors in Indonesia typically prefer to work at hospitals where they can provide higher-value inpatient services, or at their own private practice for outpatient services; hence, foreign specialized outpatient polyclinics are rare.

The role of JKN in (re-)shaping PHC

The JKN scheme is increasingly responsible for the growing demand for PHC, with BPJS-K now covering all public clinics and around half of the private ones. BPJS-K patients can receive treatment under BPJS-K coverage across the country in all of the 9,909 puskesmas and in approximately half of the 10,000 private clinics and pratama clinics (primary care outpatient clinics). There are also an estimated 2,100 private hospitals, 1,200 dentists, and 1,050 opticians that cater to BPJS-K patients.26 On the other hand, private hospitals and clinics are not authorized to receive BPJS-K patients for GPs, so a majority of patients that receive primary care at hospitals come from private insurance, employee benefits, and OOP payers. GPs that are certified to receive BPJS-K patients at their private practice now benefit from increased patient flow, particularly in areas that are underserved by hospitals and clinics.

25 These restrictions apply to Indonesia Standard Industrial Classification or Klasifikasi Baku Lapangan Usaha Indonesia (KBLI) 86103, 86104, and 86109.

26 https://www.thejakartapost.com/academia/2018/04/06/qa-BPJS-K-kesehatan-health-for-all-indonesians.html.

20

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

BPJS-K pays PHC clinics through a capitation scheme based on registered patients, which should incentivize prevention. The base rates were calculated using the capitation structure applicable under the Jaminan Kesehatan Masyarakat (Jamkesmas)—the social health insurance scheme for the poor and near-poor that was wrapped into JKN in 2014 (Britton, Koseki, and Dutta 2018). The capitation rates for private facilities were then adjusted to account for higher cost structures in the private sector. The maximum capitation amount for private sector facilities is IDR 10,000 per member per month versus IDR 6,000 per member per month for a puskesmas. Primary clinics are paid a set amount per month per member assigned to their clinics, regardless of whether they have provided any service to that member. Thus, in theory, this payment arrangement should incentivize providers to focus on preventive care. Some disease-specific services such as family planning are reimbursed separately (non-kapitasi).

The JKN has helped consolidate the role of primary care clinics as the first point of call for all nonemergency illnesses thus enhancing the use of their services. Unless they are in emergencies or labor and delivery, BPJS-K patients are required to access primary clinics which become the gatekeepers of the health system. While puskesmas typically have basic diagnostic equipment (blood glucose, cholesterol, and uric acid tests), that is not always the case in private facilities. The latter often cannot afford the capital costs associated with such equipment and cannot ensure the volumes needed to make these investments profitable. If specialist care is necessary, the primary care clinic must refer the patient to either Class C or D hospitals. These hospitals then become the gatekeepers for further specialized care, where the providers from these hospitals must refer the patient up to Class A or B hospitals should the patient want or need care at that highly specialized level.

BPJS-K empanelment appears to greatly enhance the patients’ flow to private health care centers in areas interviewed. Interviews conducted for this study in Bali suggest that a number of GPs have opened BPJS-K-empaneled certified clinics and have seen a significant increase in the number of patients they treat (up to 50 percent) since they were BPJS-K empaneled. However, this varies across the country and a majority of the population is still enrolled by puskesmas to receive capitation compared to the population enrolled by private sector clinics. This increased demand for basic health services is also encouraging GPs to establish home-based clinics to treat additional patients outside of working hours, an option that requires the use of multiple SIPs (up to three) that doctors can avail in Indonesia. At the same time, private insurance and OOP expenditures are still an important source of demand for many private GP clinics, particularly in more affluent urban areas, where the need to empanel with BPJS-K is less stringent among private facilities.

The availability of health centers is disparate across regions reflecting different population densities and relative market size. In particular, primary health centers are concentrated in areas with higher population and incomes, including Java-Bali. However, given the high populations in these areas, the number of centers per 1,000 is lower than in more sparsely populated regions in eastern Indonesia (Figure 5). At the same time, the sparse population implies that there are many villages in more remote regions without any health centers (Figure 6).

27 According to the WHO, ‘digital health’ or e-Health is defined as the cost-effective and secure use of information and communication technologies (ICTs) for health- and health-related fields. It also includes mobile health (m-Health), which involves the provision of health services and information through mobile technologies.

Figure 5 Number of health centers per 1,000 people

Source Podes Survey 2018.

Figure 6 Share of villages without health centers

Source Podes Survey 2018.

< 0,1

0,1 - 0,18

0,18 - 0,27

0,27 - 0,41

> 0,41

< 20%

20 - 40%

40 - 60%

60 - 80%

> 80%

21

22

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

Digital health providers

The scarce availability of primary health infrastructure makes it difficult for individuals to access the health systems, particularly in the less-affluent parts of the country; the emergence of digital health providers may eventually help relieve that constraint.27 A number of companies are starting to provide digital health services in Indonesia acting as a first point of contact with health professionals. For example, HaloDoc provides online consultations, helps set up doctors’ appointment, and provides last-mile delivery of over-the-counter (OTC) medicines from pharmacies or hospitals to the patient. The latter service could also help alleviate logistical difficulties that pharmaceutical companies and retail pharmacies face with inventory management, expiration of medications, and distribution costs of medicines to remote regions. Similarly, AloDokter is an online platform which provides medical-related content in Indonesia encouraging preventive care and helping people gauge the need for a medical checkup (MCU).

Besides the promise for the people with limited physical access, the digital health sector is currently growing on the back of technology-savvy urban populations in Indonesia. The great penetration and use of mobile broadband devices in Indonesia—even relative to countries at similar level of income (Figure 7)—has helped create a large base of customers for digital services, including health services. This base is particularly concentrated in urban areas where a more tech-savvy population is reducing transaction costs by exploiting the benefits of digital connectivity.28 Most of the emerging digital health services are provided through mobile platforms, which make them particularly suitable to Indonesia’s pattern of online usage, although the relatively slow download speed in the country can make it challenging to use video-based services (for

example, video call with health professionals and educational videos).

HaloDoc and AloDokter are the two key domestic players in the Indonesian digital health market, providing online access to consultations, medicine, and information. HaloDoc was incorporated in 2016 with the aim to ease the end-to-end experience for patients, by providing online appointments, consultations, diagnostic referrals, and medicine delivery through the ride hailing app GoJek, delivering medicine as quickly as within one hour from the order. HaloDoc has also partnered with private insurance groups to provide services to those covered by employee benefits.29 AloDokter is Indonesia’s leading health content portal (similar to WebMD in the United States) providing good-quality, relevant health information for patients in Bahasa Indonesia. The platform has eventually started to also provide direct chat facilities with doctors, as well as artificial intelligence (AI) bot-assisted question and answer sessions where patients can inquire about specific conditions and treatment options. According to AloDokter, they have over 20 million unique monthly users and 1 million patients using the chat platform to interact with doctors on the platform.

While the uptake of appointments, medicine delivery, and online content consultation has seen growth, mobile consultations with doctors have remained slow, as this requires patient behavioral change. Younger patients typically call a doctor through a platform for a general illness but will opt to see a specialist in person. This pattern is consistent with that on many global digital health platforms. An exception has been pediatric consultations, which have experienced significant growth through the HaloDoc platform, as many first-time parents prefer the peace of mind of speaking to a doctor when their child is ill. Dermatologists also have seen an increase in mobile consultations, as many of the diagnoses can be made over the phone and often require only OTC medicines.

27 According to the WHO, ‘digital health’ or e-Health is defined as the cost-effective and secure use of information and communication technologies (ICTs) for health- and health-related fields. It also includes mobile health (m-Health), which involves the provision of health services and information through mobile technologies.

28 Data collected by the leading digital health providers in Indonesia suggest that users under 30 years of age are increasingly using their mobile phones to find health information online.

29 The potential prospects of this business model in Indonesia have been confirmed by two significant rounds of funding, which have secured HaloDoc a total of US$76 million in 2017–2019.

23Other digital providers are also emerging providing appointment and telemedicine services. YesDok is a digital health service launched in 2017 that focuses on providing mobile consultations 24 hours a day. Other providers such as DokterSehat and KlikDokter are health content providers that also have chat and appointment services for physicians and diagnostics. Foreign providers such as Practo (India) and RingMD (Singapore) are seeking to provide telemedicine services direct to Indonesian patients with doctors abroad. Lifetrack Medical Systems provides tele-radiology for hospitals and diagnostic chains. The shortage of radiologists in Indonesia means that hospital groups or diagnostic providers could potentially utilize excess radiology capacity in markets such as India and the Philippines to increase the efficiency of operations in the Indonesian market.

While, to date, the ability of a patient to receive digital health services is limited to written or verbal interactions, the rapid technological advances may enable the sector to vastly expand its services. In particular, the increase

in wearables and other mobile medical devices could eventually improve a doctor’s ability to remotely monitor patients’ overall health and to provide tailored guidance for both medication and overall wellness. In addition, the progress in AI may enable digital companies to provide tailored advice to individuals on the basis of information such as symptoms and patients’ history. Besides health care provision, opportunities exist for digital health providers to create technology solutions for accessibility, coordination of benefits, and integration of hospital information systems (HISs) to mobile devices.

Digital platforms could also be utilized by BPJS-K to provide preventive health information. A key focus for future cost savings of BPJS-K is on preventive health and providing access to health care information to the public. Given the development of a wide range of health-related content, digital platforms are well positioned to provide the infrastructure for BPJS-K to provide targeted information campaigns to both health care workers and the general public.

Figure 7 Indonesia has a relatively high penetration of mobile broadband

Source ITU 2017 and World Development Indicators

Indonesia

Low Income

High IncomeMiddle Income

50

100

150

200

6 7 8 9 10 11 12

Log GNI per capita (current US$)

World

OECD

ASEAN

Indonesia

24

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

Market landscape

Private investment in the secondary/specialist health care subsector has grown rapidly. The number of private hospitals has grown by 9.2 percent per year over 2014–2017—a much faster rate compared to the growth in the number of public hospitals, which increased by 1.3 percent per year over the same period.30 As of end-2017, about 60 percent of all 2,198 hospitals in the country were privately owned.31 By contrast, the number of hospitals owned by the MoH and state-owned enterprises (Badan Usaha Milik Negara, BUMN) has decreased substantially over the past two decades.

Secondary/specialist Health Care Providers

About a fifth of Indonesia’s hospitals are specialist hospitals. The specialist hospital market in Indonesia mostly consists of stand-alone hospitals that are either family-owned or have a few small investors that make up the ownership structure. The larger, conglomerate-owned hospital groups such as Siloam Hospitals (Lippo Group) or Mitra Keluarga (Kalbe Farma) maintain majority ownership, with foreign or domestic investors in the minority. Hermina Hospital Group (HHG) is the largest mid-market private chain that provides practicing doctors with ‘sweat equity’32 in the hospital where they operate, allowing for rapid expansion in second- and third-tier cities. These three hospital groups—Siloam, Hermina and Mitra Keluarga—are the

30 World Bank staff calculations using data from the MoH (Profil Kesehatan 2017). Latest data available as of April 12, 2019.31 MoH, Profil Kesehatan 2017.32 Sweat equity shares means equity shares that are issued by a company to its directors or employees at a discount or for

consideration, other than cash, for providing their know-how or services. The consensus among practicing doctors is that the equity model can be attractive in recruiting high-profile specialists in second- and third-tier cities.

2000 2017

Subnationalgovernment

357

Private550

Army/police111

State-owned enterprise/other department

68

Ministry of Health59

Ministry of Health14

Subnationalgovernment

672

Army/police164

State-owned enterprise/other department

14

Private1334

Figure 8 Total number of hospitals by ownership

Source MoH, World Bank staff calculations.

25Figure 9 Breakdown of Indonesian private hospitals, by class (2011–2017)

Source Britton, Koseki, and Dutta (2018).

major players in the industry, with Siloam leading in terms of number of hospitals and revenues (around US$50 million), but the other two groups are in close proximity.

Many private hospitals have been built (or have been planned) following the implementation of JKN, with the intent to capture the increased demand for specialist services.33 Two of Indonesia’s leading private hospital groups—Siloam and Hermina—have opened 20 branded hospitals since 2016, with another 20 hospitals in the pipeline by the end of 2020.34 Most of Siloam’s hospitals have been acquisitions or management buy-outs of existing hospitals, whereas Hermina has mostly built greenfield hospitals, focusing on Type ‘C’ hospitals to receive BPJS-K referrals. Indeed, most general hospitals in Indonesia are of Type C or D, which only offer basic services.35 Foreign operators from Malaysia, India, and Singapore have also invested in private hospital

groups. Malaysia’s Creador, for example, has a minority stake in Hermina.

The number of lower-level hospitals, which are gatekeepers to higher-level specialist care, has grown faster than the higher-level ones, a possible result of the BPJS-K referral system. As mentioned previously, BPJS-K requires patients to access services first through the primary care level and be referred up to Class C and D hospitals should the need arise. If further specialist care is required, these hospitals will further refer up to Class A and B hospitals. Stakeholders note that since Class C hospitals are at a higher level than Class D and get higher reimbursement rates, but can still accept referrals directly from primary care, more facilities are upgrading to Class C hospitals. As such, the proportion of Class C and Class D hospitals has grown quite rapidly in the last years (Figure 9).

33 Britton, Koseki, and Dutta 2018.34 This is based on information collected through interviews with the companies.35 MoH Regulation No. 340/2010 classifies all general hospitals according to the services provided, with A being the most

advanced and D being the most basic. Type A provides, at a minimum, four basic specialist services, five medical support specialist services, twelve other specialist services, and thirteen subspecialist services. Type B provides, at a minimum, four basic specialist services, four medical support specialist services, eight other specialist services, and two subspecialist services. Type C provides, at a minimum, four basic specialist services and four medical support specialist services. Type D provides, at a minimum, two basic specialist services.

44%46% 46% 47% 51% 52% 53%

0

20

40

60

80

100

81%67%

2011 2012 2013 2014 2015 2016 2017

A B C D

26

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

Key players

Since many large (200-bed plus) private hospital groups are owned by conglomerates, the need for foreign capital has remained limited to minority foreign equity stakes (as detailed below). A majority of foreign investment has flowed into hospitals, specialized health care groups, or start-up health care technology ventures. The large domestic players such as Lippo Group (Siloam Hospitals) and Kalbe Farma (Mitra Keluarga) have been rapidly expanding their hospitals as complementary businesses to their dominant real estate and pharmaceutical business, respectively. HHG and Awal Bros Hospitals are involved only in health care services and have taken on foreign and domestic private equity funding, respectively.

Siloam Hospitals is majority owned by the Lippo Group, with a 15 percent minority stake held by CVC Capital Partners. Siloam maintains the

largest hospital and clinic network in Indonesia, with 34 hospitals and approximately 6,000 beds.36 Eleven of its hospitals are located in the Greater Jakarta area, with the remainder across Java-Bali, Sumatra, Kalimantan, Sulawesi, and Nusa Tenggara. Siloam’s current focus is on acquiring existing hospitals in smaller cities and bringing them under Siloam management. It plans to have up to 40 hospitals and 30 outpatient clinics by 2020, primarily focused on the middle- and upper-middle-class segment. Siloam accepts BPJS-K patients at 24 out of its 34 hospitals. Moreover, hospitals in smaller cities accept BPJS-K referrals from provincial public hospitals.

HHG has traditionally focused on the middle-income segment and has an operating model where doctors are shareholders in their operating hospital. Hermina currently operates 30 hospitals with approximately 3,000 beds and has the largest coverage of hospitals across Indonesia of any private group. This doctor-owner model has allowed Hermina to rapidly expand in second-tier

36 Siloam Prospectus, 2019.

Tabel 3 Major hospital groups in Indonesia, 2018

Company Hospital name Number of hospitals

Number of hospitals serving BPJS-K

New hospitals planned in 2019

Siloam International Hospitals Siloam 34 24 7

HHG Hermina 30 30 4

Mitra Keluarga Karyasehat Mitra Keluarga 20 12 2

Awal Bros Awal Bros 12 n.a. n.a.

Source Company websites and press clippings. Information valid as at end-2018.

Tabel 4 Financial performance of market-listed hospital groups, end-2018

Assets Liabilities Equity Sales P/E ratio D/E ratio ROA ROE NPM

Mitra Keluarga 4,976 718 4,258 2,033 35.31 0.17 13.89 16.23 34.01

Hermina 3,950 1,566 2,384 2,288 51.78 0.66 5.47 9.06 9.44

Siloam 7,701 1,390 6,312 4,396 1,463.03 0.22 0.17 0.2 0.29

Source Indonesia Stock Exchange, Statistics 2018.Note P/E = Price to earnings; D/E = Debt to equity; ROA = Return on assets; ROE = Return on equity; NPM = Net profit margin.

27

cities with specialist practitioners as shareholders. All Hermina hospitals accept BPJS-K patients, with some of the hospitals having up to 50 percent of patients coming through BPJS-K referrals. Hermina plans to open 40 hospitals by 2020 and has started entering into hospital management agreements as it has done in Provita Jayapura Hospital (Papua). Hermina’s focus is to expand Class C hospitals through greenfield or managed service agreements. As a pure health care operator, Hermina is in a good position to develop PPPs in the form of joint ventures, particularly for the diagnostics sector and Centers of Excellence due to its doctor shareholder model, which allows for greater incentives to specialist doctors.

Mitra Keluarga has 13 hospitals mostly in the Greater Jakarta area, with approximately 2,200 beds. Its greatest advantage is the fact that it is part of Kalbe Farma (the parent company) and

its distribution and logistics platform, which allows for efficient distribution of pharmacies and consumables throughout Mitra Keluarga’s hospital chain. This has allowed the group to become the hospital of choice for private middle-income customers in the Greater Jakarta area. Kalbe Farma’s vast doctor network has also become a convenient recruiting ground for doctors across Indonesia. The group is now planning an acquisition and greenfield expansion of hospitals in second- and third-tier cities focused on BPJS-K customers. Backed by Kalbe Farma, Mitra Keluarga has the capital and human resources to develop PPPs, particularly in the area of diagnostics and specialty centers. As one of the largest pharmaceutical producers (both branded and generic), Kalbe Farma has a strong relationship with the government as a major pharmaceutical provider to BPJS-K.

28

PARTNERSHIPS FOR A HEALTHIER INDONESIAUnlocking Constraints for Better Private Sector Participation

The role of JKN and private hospitals

The initial uptake of BPJS-K patients by private hospitals was limited upon its rollout in 2014, as many providers initially feared that basic services would be overrun by BPJS-K patients. Private hospital groups were reluctant to take on a government body such as BPJS-K as a client. Those that did take on clients did view this cooperation between BPJS-K and private hospitals as a PPP. One medical director said there was a moral obligation on part of private health care providers to offset the sudden increase in demand of medical services that was overburdening the public health care system. In addition, the national socialization program for the public was not well coordinated, and there was a lack of understanding on the types of services covered by BPJS-K.

However, the uptake of BPJS-K services increased significantly in 2015–2016, particularly with lower-income patients, once the BPJS-K outreach program informed the public that their health care costs were now covered if patients go through the referral system. With incremental growth in private health insurance coverage, as well as an increase in health insurance provided through employee benefits, many of the hospitals serving the middle-income segment are seeing an overall increase in the number of patients utilizing BPJS-K where possible, and then topping

off with their employee benefits where required. Siloam and Hermina indicated that it was in their interest to accommodate BPJS-K patients and provide patients with the same level of service to their privately insured or OOP patients, as they would be paying customers in the future. One leading hospital group indicated that for four of its hospitals in the Greater Jakarta area, some 40–50 percent of the patients were using BPJS-K.

Today, private hospitals are required to have BPJS-K patients referred for specialist services at their facilities either through puskesmas or government hospitals. The determination of which hospital receives which patient for specialized care is determined by BPJS-K based on geography and the availability of the specialized services at the respective private hospitals. Private hospital groups that have a broader geographic footprint are in a better position to take advantage of BPJS-K patients, many of whom access health care in second- or third-tier cities. Since the coordination of health insurance benefits of BPJS-K and private insurance remains complicated at the hospital level (and reimbursement for the patient), many patients have opted to pay OOP once they reach the threshold of their BPJS-K coverage.

29

Market landscape