us pe middle market report - mcfllc.com · data software for vc, pe and m&a. contact...

TRANSCRIPT

2017 1Q Sponsored by

US PE Middle Market

ReportIn partnership with

Built solid.Communicate. Commit. Deliver.®

Since 2001, our record speaks for itself...

billion of net commitments new transactions private equity sponsors

of transactions closed as Administrative Agent, Sole Lender or Co-Agent since 2012

MANUFACTURING | DISTRIBUTION | SERVICES | CONSUMER PRODUCTS | HEALTHCARE | INSURANCE/FINANCIAL SERVICES | AEROSPACE & DEFENSE | TECHNOLOGY SERVICES

Madison Capital Funding LLC is a subsidiary of New York Life Insurance Company. MCF-1732377© 2017 New York Life Investment Management LLC. All rights reserved.

* As of March 31, 2017

170-year commitment

exceptional success for ourselves and our partners.

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

Content

DYLAN E. COX Analyst

BRYAN HANSON Data Analyst

NIZAR TARHUNI Analysis Manager

GARRETT JAMES BLACK Publisher

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2017 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Methodology 4

Introduction 5

Overview 6-7

Deals by Middle-Market Segment 8

Company Inventory 9

Exits 10

Fundraising 11

League Tables 12

CONTENTS

The PitchBook PlatformThe data in this report comes from the PitchBook Platform–our

data software for VC, PE and M&A. Contact [email protected]

to request a free trial.

IN PARTNERSHIP WITH

CO-SPONSOR3 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

METHODOLOGY

Madison Capital, founded in 2001, and headquartered in Chicago, Illinois, is a premier finance company focused exclusively on the corporate financing needs of middle market private equity firms. Madison Capital has closed transactions with over 255 different private equity firms and provides enterprise-value

leveraged financing for leveraged buyouts, management buyouts, add-on acquisitions and recapitalizations. Madison Capital Funding LLC is a subsidiary of New York Life Insurance Company. Additional information may be found at: www.mcfllc.com

IN PARTNERSHIP WITH

CO-SPONSOR4 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

MIDDLE MARKET DEFINITIONFor this report, the middle market (MM) is defined as US-based companies acquired through buyout transactions between $25 million and $1 billion. Note that minority deals are not included. The middle market is further broken down into the lower middle market (LMM; $25 million to $100 million), the core middle market (CMM; $100 million to $500 million) and the upper middle market (UMM; $500 million to $1 billion). The lower bound of each range is inclusive of deals that are that exact amount, e.g. a transaction that is $100 million in size will be bucketed into the CMM rather than the LMM. This report covers only US-based middle-market companies that have received some type of private equity investment.

TOTAL CAPITAL INVESTED/DEAL VALUETotal amount of equity and debt used in the private equity investment

Ex. $10 million of equity and $20 million of debt = $30 million of total capital investment

PitchBook’s total capital invested figures include deal amounts that were not collected by PitchBook but have been estimated using a multidimensional estimation matrix, which takes into account year of investment, deal type, platform v. add-on, industry and sector. Some datasets will include these extrapolated numbers while others will be compiled using only data collected directly by PitchBook; this explains any potential discrepancies that may be noticed.

EXITSThe report includes both full and partial exits of middle-market companies via corporate acquisition, secondary private equity buyout and initial public offering (IPO). PitchBook has utilized its multidimensional substitution and estimation matrix to estimate transaction sizes where the deal amount is unknown. For the MM company inventory, we included companies that are expected to exit between $25 million and $1 billion.

FUNDRAISINGPitchBook defines middle-market funds as PE investment vehicles with between $100 million and $5 billion in capital commitments. The report only includes PE funds that have held their final close. Funds-of-funds and LP secondary funds are not included.

LEAGUE TABLESAll league tables are compiled using deal counts for middle-market leveraged buyouts only to better reflect the other datasets within the report, with only the Lenders table also including all PitchBook debt round types in order to capture all debt provided to facilitate buyouts. For example, the Most Active Advisors league table shows the number of US-based middle-market buyouts that a firm advised on during the fourth quarter of 2016. Deals on which a firm advised multiple parties will only be counted once for that firm.

INTRODUCTION

Look up a company.

And its cap table.

And its investors.

And its EBITDA

multiples.

And its board

members.

In seconds.

The PitchBook Platform

has the data you need

to close your next deal.

Learn more at

pitchbook.com

Key takeaways

» Concerns surrounding trade policy and poor earnings performance

hampered middle-market private equity deal flow in the B2C sector last

quarter.

» IT companies comprised one-fifth of all middle-market PE deals. IT is now

the second most common industry behind B2B.

» PE firms recorded a second consecutive quarter of strong fundraising

performance, totaling $34.95 billion across 40 vehicles.

» Exit activity was at its lowest level in nearly four years, though the IPO

avenue returned to prominence.

In 2016, PE firms flocked toward the lower middle market to find suitable add-

ons and buyouts at relatively lower valuations. However, the first quarter of this

year was marked by larger middle-market deals as firms sought to deploy newly

raised capital in larger chunks. Though multiples remain high and quality targets

sparse, discerning investors are finding ways to complete deals and limited

partners are nothing but exuberant when it comes to fundraising.

We hope this report is useful in your practice. As always, feel free to send any

questions or comments to [email protected].

DYLAN E. COX

Analyst

IN PARTNERSHIP WITH

CO-SPONSOR

5 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

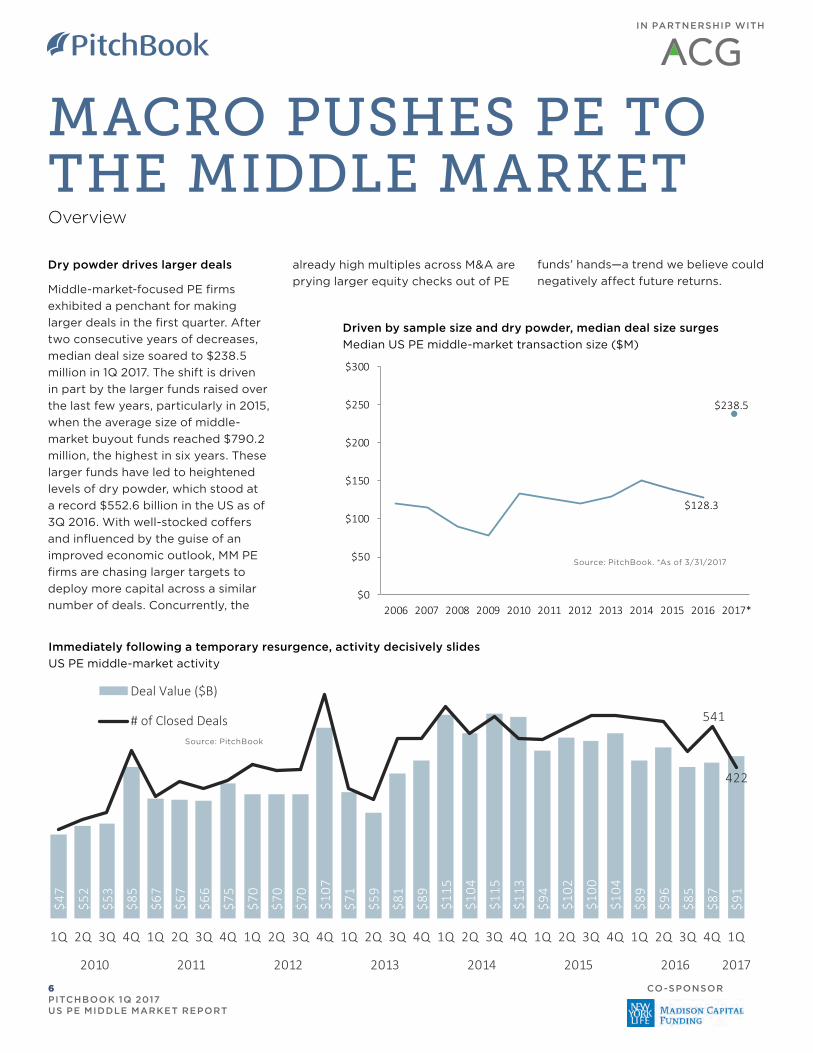

MACRO PUSHES PE TO THE MIDDLE MARKETOverview

Dry powder drives larger deals

Middle-market-focused PE firms

exhibited a penchant for making

larger deals in the first quarter. After

two consecutive years of decreases,

median deal size soared to $238.5

million in 1Q 2017. The shift is driven

in part by the larger funds raised over

the last few years, particularly in 2015,

when the average size of middle-

market buyout funds reached $790.2

million, the highest in six years. These

larger funds have led to heightened

levels of dry powder, which stood at

a record $552.6 billion in the US as of

3Q 2016. With well-stocked coffers

and influenced by the guise of an

improved economic outlook, MM PE

firms are chasing larger targets to

deploy more capital across a similar

number of deals. Concurrently, the

Immediately following a temporary resurgence, activity decisively slides

US PE middle-market activity

Source: PitchBook

$47

$52

$53

$85

$67

$67

$66

$75

$70

$70

$70

$107

$71

$59

$81

$89

$115

$104

$115

$113

$94

$102

$100

$104

$89

$96

$85

$87

$91

541

422

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2010 2011 2012 2013 2014 2015 2016 2017

Deal Value ($B)

# of Closed Deals

Driven by sample size and dry powder, median deal size surges

Median US PE middle-market transaction size ($M)

$128.3

$238.5

$0

$50

$100

$150

$200

$250

$300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*2017*

Source: PitchBook. *As of 3/31/2017

already high multiples across M&A are

prying larger equity checks out of PE

funds’ hands—a trend we believe could

negatively affect future returns.

IN PARTNERSHIP WITH

CO-SPONSOR6 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

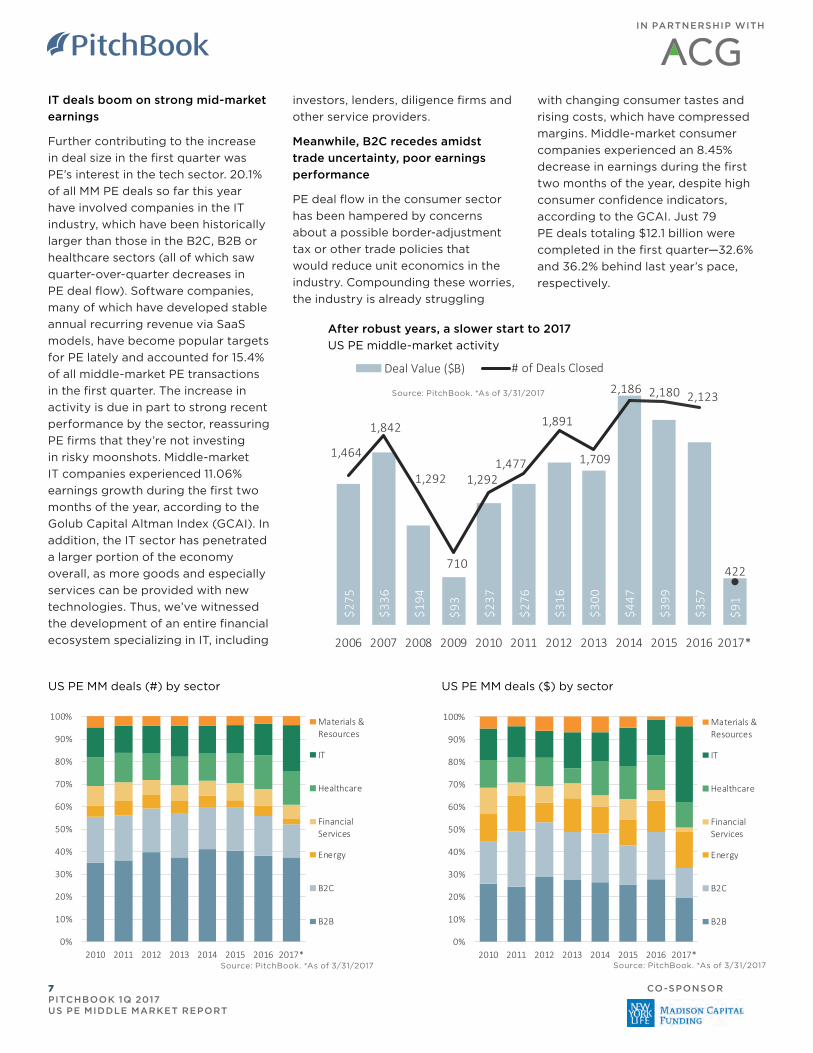

IT deals boom on strong mid-market

earnings

Further contributing to the increase

in deal size in the first quarter was

PE’s interest in the tech sector. 20.1%

of all MM PE deals so far this year

have involved companies in the IT

industry, which have been historically

larger than those in the B2C, B2B or

healthcare sectors (all of which saw

quarter-over-quarter decreases in

PE deal flow). Software companies,

many of which have developed stable

annual recurring revenue via SaaS

models, have become popular targets

for PE lately and accounted for 15.4%

of all middle-market PE transactions

in the first quarter. The increase in

activity is due in part to strong recent

performance by the sector, reassuring

PE firms that they’re not investing

in risky moonshots. Middle-market

IT companies experienced 11.06%

earnings growth during the first two

months of the year, according to the

Golub Capital Altman Index (GCAI). In

addition, the IT sector has penetrated

a larger portion of the economy

overall, as more goods and especially

services can be provided with new

technologies. Thus, we’ve witnessed

the development of an entire financial

ecosystem specializing in IT, including

investors, lenders, diligence firms and

other service providers.

Meanwhile, B2C recedes amidst

trade uncertainty, poor earnings

performance

PE deal flow in the consumer sector

has been hampered by concerns

about a possible border-adjustment

tax or other trade policies that

would reduce unit economics in the

industry. Compounding these worries,

the industry is already struggling

with changing consumer tastes and

rising costs, which have compressed

margins. Middle-market consumer

companies experienced an 8.45%

decrease in earnings during the first

two months of the year, despite high

consumer confidence indicators,

according to the GCAI. Just 79

PE deals totaling $12.1 billion were

completed in the first quarter—32.6%

and 36.2% behind last year’s pace,

respectively.

After robust years, a slower start to 2017

US PE middle-market activity

Source: PitchBook. *As of 3/31/2017

$275

$336

$194

$93

$237

$276

$316

$300

$447

$399

$357

$91

1,464

1,842

1,292

710

1,292 1,477

1,891

1,709

2,186 2,180 2,123

422

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Deal Value ($B) # of Deals Closed

US PE MM deals (#) by sector US PE MM deals ($) by sector

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017*

Materials &Resources

IT

Healthcare

FinancialServices

Energy

B2C

B2B

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017*

Materials &Resources

IT

Healthcare

FinancialServices

Energy

B2C

B2B

Source: PitchBook. *As of 3/31/2017

Source: PitchBook. *As of 3/31/2017

IN PARTNERSHIP WITH

CO-SPONSOR7 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

Plenty of accessible capital and competition push up prices

US PE UMM deal flow

Source: PitchBook. Transactions sized between $25 million and

$100 million comprise the lower middle market.

AN UPPER END SURGEDeals by middle-market segment

UMM investment rises, spurred by pricing pressures and cyclicality.

Select US UMM PE deals in 1Q 2017

Company Investor(s)Deal Size ($M)

SunGard Public Sector

Vista Equity Partners

$850

SM Energy (Non-operated Eagle Ford Assets)

EnCap Investments, KKR, Riverstone Holdings

$800

DeVilbiss Healthcare

Clayton, Dubilier & Rice

$800

Surgical Specialties

Vivo Capital, ZQ Capital

$505

Blue NileBain Capital, Bow Street, Adama Partners

$500

Source: PitchBook

A contested middle ground subject to volatility

US PE CMM activity

A decline partially due to pricing pressures

US PE LMM activity

$10.

5

$7.1

$6.2

$7.2

$8.2

$9.5

$6.3

$5.9

$13.

5

$8.1

$9.1

$5.2

$5.3

220

177 174 162 174

235

186 165

272

206 186

177

147

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2014 2015 2016 2017

Deal Value ($B) # of Deals Closed

$59

$52

$46

$63

$54

$37

$45

$37

$44

$44

$41

$38

$34

306

268

274 282 277

197

282 275

227

262

218

266

165

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2014 2015 2016 2017

Deal Value ($B) # of Deals Closed

Source: PitchBook. Transactions sized between $100 million and

$500 million comprise the lower middle market.

$37

$19

$32

$32

$45

$44

$63

$43

$31

$55

$48

$60

$31

$43

$35

$44

$51

69

31

57 6169 74

118

63

51

106

103

131

60

85

64

98110

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2013 2014 2015 2016 2017

Deal Value ($B)

# of Deals Closed

Source: PitchBook. Transactions sized between $500 million

and $1 billion comprise the upper middle market.

IN PARTNERSHIP WITH

CO-SPONSOR8 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

INVENTORY UNREADY TO TURN OVERUS PE middle-market company inventory

US PE middle-market company inventory by count and year

Despite slowing exit activity, PE firms have succeeded in turning over some of their older holdings—though a fair portion of aged assets still remain to be sold—and concentrating portfolios on the younger side.

1,1411,271

1,4431,686

1,9512,264

2,6623,101

3,4673,611

3,8194,052

4,3194,521

4,7815,061

5,271 5,297

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

2011-2017*

2006-2010

2000-2005

Pre-2000

Year of Investment

Source: PitchBook. *As of 3/31/2017

US PE middle-market company inventory over time

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 2017*Pre-2000 2000-2005 2006-2010 2011-2017*

Source: PitchBook. *As of 3/31/2017

IN PARTNERSHIP WITH

CO-SPONSOR9 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

A COMING DROUGHT?US PE-backed middle-market exits

Early stages of a drought, IPOs bounce

back

In the first quarter of the year, middle-

market PE experienced its slowest

quarter of exits in nearly four years.

Most investments made prior to 2008

have already been exited and the bulk

of inventory purchased between 2014

and 2016 is not yet ready for a sale.

Thus, the PE exit environment has

hit the early stages of a drought. The

median hold time for a MM company

in 2016 was 5.2 years, which means

the faucet will likely be restricted to

its current trickle for the next one to

two years. This lack of PE-backed

companies coming to market could

pose problems for MM firms who

have recently raised a fund and tend

to source their deals via secondary

buyout.

SBOs continue to predominate by count

US PE-backed MM exits (#) by type

2014 and 2015 were boom years, 2016 slowed, is 2017 set for a drought?

US PE-backed middle-market exits

PE buyers reap value from all avenues

US PE-backed MM exits ($B) by type

$73

$88

$45

$28

$77

$81

$92

$75

$122

$111

$87

$15

616

748

495

296

670752

906

830

1,089 1,075

927

180

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Exit Value ($B)

# of Exits

Source: PitchBook. *As of 3/31/2017

$0

$50

$100

$150

$200

$250

$300

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

2014 2015 2016

Corporate Acquisi�on IPO Secondary Buyout

0

50

100

150

200

250

300

350

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2014 2015 2016 17*

Corporate Acquisi�on IPO Secondary Buyout

Source: PitchBook. *As of 3/31/2017

$0

$5

$10

$15

$20

$25

$30

$35

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2014 2015 2016 17*

Corporate Acquisi�on IPO Secondary Buyout

Source: PitchBook. *As of 3/31/2017

Though the market overall may be

dry, PE investors rode a wave of IPO

activity through the first quarter.

Fueled by a backlog of companies that

had postponed their initial offerings in

a rocky first half of 2016, 12 PE-backed

IPOs of middle-market businesses were

completed in 1Q, the highest since 2Q

2015.

IN PARTNERSHIP WITH

CO-SPONSOR10 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

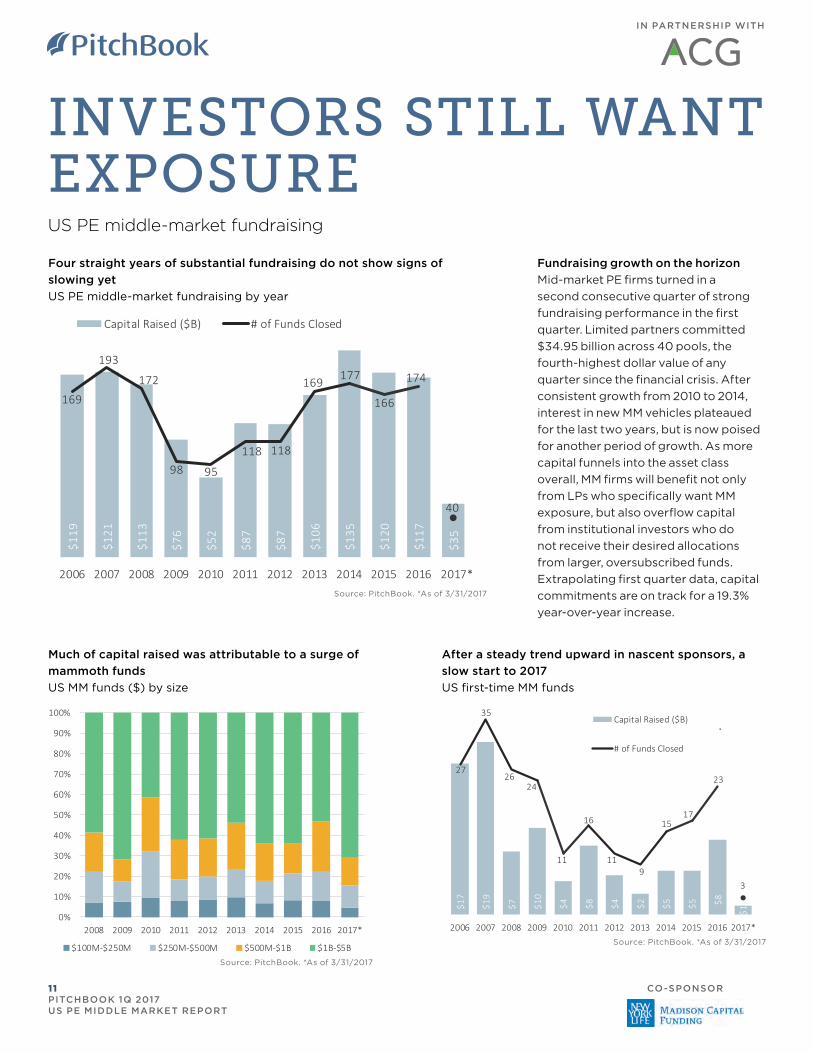

Four straight years of substantial fundraising do not show signs of

slowing yet

US PE middle-market fundraising by year

Much of capital raised was attributable to a surge of

mammoth funds

US MM funds ($) by size

After a steady trend upward in nascent sponsors, a

slow start to 2017

US first-time MM funds

Fundraising growth on the horizon

Mid-market PE firms turned in a

second consecutive quarter of strong

fundraising performance in the first

quarter. Limited partners committed

$34.95 billion across 40 pools, the

fourth-highest dollar value of any

quarter since the financial crisis. After

consistent growth from 2010 to 2014,

interest in new MM vehicles plateaued

for the last two years, but is now poised

for another period of growth. As more

capital funnels into the asset class

overall, MM firms will benefit not only

from LPs who specifically want MM

exposure, but also overflow capital

from institutional investors who do

not receive their desired allocations

from larger, oversubscribed funds.

Extrapolating first quarter data, capital

commitments are on track for a 19.3%

year-over-year increase.

$119

$121

$113

$76

$52

$87

$87

$106

$135

$120

$117

$35

169

193

172

98 95

118 118

169 177

166

174

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Capital Raised ($B) # of Funds Closed

$17

$19

$7 $10

$4 $8 $4 $2 $5 $5 $8

$1

27

35

2624

11

16

119

1517

23

3

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

Capital Raised ($B)

# of Funds Closed

Source: PitchBook. *As of 3/31/2017

Source: PitchBook. *As of 3/31/2017

Source: PitchBook. *As of 3/31/2017

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

$100M-$250M $250M-$500M $500M-$1B $1B-$5B

INVESTORS STILL WANT EXPOSUREUS PE middle-market fundraising

IN PARTNERSHIP WITH

CO-SPONSOR11 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

MIDDLE MARKET

LEAGUE TABLES1Q 2017

HarbourVest Partners 12

Audax Group 11

ABRY Partners 10

CI Capital Partners 9

Genstar Capital 7

Maranon Capital 7

TA Associates Management 7

The Carlyle Group 7

American Securities 6

GTCR 6

Hellman & Friedman 6

Providence Equity Partners 6

AlpInvest Partners 5

Altamir 5

Apax Partners 5

Bain Capital 5

Blue Point Capital Partners 5

H.I.G. Capital 5

InTandem Capital Partners 5

Kohlberg Kravis Roberts 5

Littlejohn & Company 5

Most active investors by deal count

Source: PitchBook

Antares Capital 18

Madison Capital Funding 10

Golub Capital 7

Twin Brook Capital Partners 7

Monroe Capital 5

NXT Capital 5

Bank of America 4

Franklin Synergy Bank 4

Citizens Bank 3

Crescent Capital 3

Fifth Street 3

J.P. Morgan 3

Most active lenders by deal count

Source: PitchBook

Madison Dearborn Partners 5

Shore Capital Partners 5

The Blackstone Group 5

The Riverside Company 5

The Sterling Group 5

Warburg Pincus 5

Webster Capital 5

Most active investors, ctd.

Find out more

at pitchbook.com

This report sums up the big trends.

Dig into the details on the PitchBook Platform.

IN PARTNERSHIP WITH

CO-SPONSOR

12 PITCHBOOK 1Q 2017 US PE MIDDLE MARKET REPORT

See how the PitchBook Platform can

help your private equity firm close your

next deal.

We do EBITDA multiples,private comps,valuations,market trends,growth metrics.

You build a better portfolio.