us pe & vc ipo trends - pitchbookfiles.pitchbook.com/pdf/pitchbook_2016_us_pe_vc_ipo...pe ipo...

TRANSCRIPT

PE IPO activity Analysis of trends in IPO count

and capital raised over recent

years. Page 7

2016 REPORT

In partnership with

US PE & VCIPO TRENDS

VC prior to IPO Breakdowns of VC activity before

public debuts. Page 10

IPO pipeline Tables of upcoming

PE & VC-backed IPOs. Page 16

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

Content

NIZAR TARHUNI Senior Analyst

KYLE STANFORD Analyst

DYLAN COX Analyst

ELIZABETH ARMON Analyst

BRYAN HANSON Data Analyst

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2016 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Contents

Introduction 4

Overview 5-6

PE IPOs: Activity 7

PE IPOs: Metrics 8

PE IPOs: Sector 9

VC Prior to IPO 10

VC IPOs: Activity 11

VC IPOs: Metrics 12

VC IPOs: Sector 13

IPO pricing & window 14-15

IPO pipeline 16

Methodology 17

3 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

2016 IPOs on pace to record lowest level since 2009Introduction

Donnelley Financial Solutions (NYSE: DFIN) provides software and services that enable clients to communicate with confidence in a complex regulatory environment. With 3,500 employees in 61 locations across 18 countries, we provide thousands of clients globally with innovative tools for content creation, management and distribution, as well as data analytics and multi-lingual localization services.

Leveraging advanced technology, deep-domain expertise and 24/7 support, we deliver cost-effective solutions to meet the evolving needs of our clients. For more information about Donnelley Financial Solutions, visit dfsco.com.

Our Venue® secure online workspace provides a powerful set of features and an intuitive design that allows you to easily organize, manage, share and track all of your sensitive information. Venue® data rooms provide complete control, allowing you to manage who has access to your data room, which documents they see, and how they can interact with those documents.

Venue® gives you access to hands-on, start-to-finish service that’s unique in the industry and that earns us a satisfaction rating of more than 97% from our demanding users. Get full Venue® room service or manage your room yourself, with our experienced in-house team ready 24/7/365. As part of Donnelley Financial Solutions, the global leader in managing time-sensitive, highly confidential documents, Venue provides the control you need with the security you demand.

Donnelley Financial Solutions is the sponsor of the Venue Venture Capital Update. All information contained in this publication is for informational purposes only and should not be construed as legal, accounting, tax, or other professional advice of any kind, on any subject matter. Donnelley Financial Solutions expressly disclaims all liability in respect to actions taken or not taken based on any or all the content herein.

NIZAR TARHUNI

Senior Analyst

Thus far into 2016, the IPO market has continued

to suffer considerably from a basket of headwinds

stemming from both domestic and political strains,

diverging global market outlooks, and a significant

amount of capital sitting in the funds of private

financiers able to prolong the private lifetimes of

many companies that traditionally would be on the

cusp of IPOing. In fact, the first month of the year

saw no IPOs come to market, and for private equity,

no portfolio companies completed a public offering

throughout the entire first quarter of the year! At the

current pace, 2016 is set to see both capital raised

and completed IPO counts come in at their lowest

levels since 2009.

For PE, many managers continue to take advantage of

strategic acquirers hungry to purchase growth rather

than build organically. However, the sponsor-backed

listings that we’ve seen have tended to be rather large

compared to the rest of the market, a trend indicative

of mangers holding certain assets that might simply

be too large to try and push to a strategic or to

another PE firm.

For VC, we continue to see the most highly valued

companies remain private. Just two VC-backed

companies valued at over $1 billion came to market

and although both were able to list in a relatively

smooth manner, we haven’t seen them set the tone for

other heavily-funded venture portfolio companies.

If you have any questions or comments on the analysis

and datasets within this report, feel free to reach out

to us at [email protected].

4 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

Overview

Despite a recent wave of IPO pricings

giving rise to speculation regarding the

IPO window opening, 2016 collectively

paints a very different picture. Three

quarters through the year, just $7.2

billion was raised across 49 PE and

VC-backed public offerings, reflecting

declines of roughly 49% and 48%,

respectively, relative to the same

period last year. At the current pace,

2016 is set to see both total IPO capital

raised and volume come in at their

lowest levels since 2009, which saw

just over $9 billion raised via 36 public

listings.

With an abundance of capital available

from both PE and venture investors,

the incentives to move forward with

a costly public listing simply aren’t

there, especially when you couple the

rich dry powder environment with an

uncertain global economic, business,

political and exit landscape. Public

flotations tend to perform better

during times where the public markets

are stable and moving consistently

higher, and while equities in the US are

Source: PitchBook

$2 $5 $2 $4 $11

$5 $2 $5 $5 $20

$3 $4 $4 $8 $5 $17

$9 $13

$4 $9 $2 $8 $5 $5 $4 $3

19

26

17

29

22

26

1822

40

23

24

19

22

43

41

49

55 54

36

54

21

46

28

22

6

20 23

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2010 2011 2012 2013 2014 2015 2016

Capital Raised ($B) IPO Count

$20

$24

$4 $9 $13

$24

$31

$34

$35

$19

$7

130

144

2836

91

88106

155

199

117

49

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Capital Raised ($B) IPO Count

up YTD, we continue to remain a bit

confused around the main drivers of

equities in this environment. Earnings

and revenue growth have remained

less than optimal, and economists

continue to forecast slow GDP growth,

but the markets have fought off just

about all signs of adversity, whether

those be concerns around monetary

policy, the UK referendum or even the

surprising results of the US presidential

election. On a relative basis, US

equities have certainly outperformed

the bulk of European and Asian stock

markets in 2016, so while at first glance

US public markets may look well

US IPO activity by year

US PE and VC-backed IPO activity by quarter

Source: PitchBook

*As of 9/30/2016

5 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

The average offering size has fallen for the 4th consecutive year

Median and average offering size of US IPOs

Source: PitchBook

*As of 9/30/2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

*

High

In Range

Low

Over 60% of filings are being priced within their expected range

% of US IPOs pricing above, within and below expected price range

Median ($M)

Average ($M)

$100

$88

$90

$187$163

$148

$0

$50

$100

$150

$200

$250

$300

$350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

suited to handle new listings, we think

a notable driver of US stocks today

stems from an investor base that has

looked to avoid the turbulence we’ve

seen in foreign equities. With that in

mind, companies looking to list will

need to prove to institutional investors

that despite the sluggish macro

environment we highlighted above,

they have the stewardship, capital

expenditure discipline and ultimately

the business model to continue driving

growth and profitability in a slower-

moving market.

One trend we’ve noted when looking

at private financings, especially on

the PE side, has been the split in

the quality of companies PE firms

have chased. The result of this can

be seen in the heightened multiples

PE continues to pay to close deals,

however there continues to remain

a group of second-tier companies

that simply can’t garner the multiples

we’ve seen in recent years. We think

we’ve noticed a similar occurrence

in the IPO markets today. Through

the third quarter of 2016, just under

12% of companies priced at the high

end of their respective IPO range, yet

we saw a rather impressive 60% of

companies hit their target range, the

highest figure we’ve seen since 2008,

which saw nearly 67% of companies

do that. Further, 28% of companies to

list this year priced at the low end of

their range, slightly less than the 30%

and 35% figures we saw in 2015 and

2014, respectively. While total IPO

activity has remained subdued, the

quality of companies willing to move

forward with a public flotation appears

to be improving and such companies

have had success completing offerings

efficiently.

The rest of 2016 might be marked by

continued uncertainty, yet as investors

continue to adjust to a changing

dynamic that involves a new president

in place, along with a potential new

wave of venture-backed companies

prepping to test the markets in 2017,

we’ll begin to gain a better picture of

where institutional investor appetite

lies for new offerings. Performance

on the secondary markets will also be

important to monitor, and that also

applies to listings that see significant

pops in their newly traded stock. While

Twilio was able to come to market and

hold a successful IPO, the fact that

their stock traded up close to 300%

within one month of listing should be

looked at from a couple of different

angles. Primarily, we should credit

the company for standing out and

attracting significant interest, yet we

also think that stock could have been

underpriced by its advisors. With little

IPO activity for bankers to benchmark

against at the moment, the task of

marketing and pitching companies to

institutional investors understandably

may come with significant uncertainty.

To say the least, syndicate desks

will have their hands full finding the

adequate equilibrium in terms of

offering price for future listings next

year.

Source: PitchBook

*As of 9/30/2016

6 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

$16

$16

$4 $8 $10

$18

$10

$25

$25

$11

$5

71 59

1826

49

42 45

67

78

41

18

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Capital Raised ($B) IPO Count

PE IPOs: Activity

Through the first three quarters of

2016, PE-backed companies accounted

for 37% of IPOs, which is about the

same as 2015, but well below the

portion we saw for most of the last

decade. For comparison, PE-backed

companies made up 72% of US IPOs

in 2009, a number which has declined

fairly consistently since.

18 PE-backed IPOs have been

completed this year, raising a total of

$5 billion, on track for the slowest year

we’ve seen since 2008 in terms of both

the number of IPOs and the funds that

they raise. About half of the capital

raised this year ($2.4 billion) has been

concentrated in the offerings of just

three companies: commercial kitchen

supplier US Foods, pharmaceutical

developer Patheon, and hotel and

casino operator Red Rock Resorts.

Two of these three, US Foods and Red

Rock Resorts either have completed

or are in talks to complete a debt

refinancing post-IPO, a move not

uncommon with companies who have

recently gone public and subsequently

Source: PitchBook

*As of 9/30/2016

$2 $4 $1 $3 $10

$3 $2 $2 $3 $3 $2 $2 $3 $6 $3 $13

$6 $11

$3 $6 $5 $2 $3 $3 $2

9

14

9

17

11 1110 10

18

10

11

6

12

18

12

25

15

27

12

24

6

16

12

7

0

9 9

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2010 2011 2012 2013 2014 2015 2016

Capital Raised ($B) IPO Count

US PE-sponsored IPO activity by year

have easier access to the full range of

capital markets.

On a quarterly basis, PE-backed IPOs

have fared better in recent months

than the annual data would suggest.

After a grand total of zero IPOs in the

first quarter, both 2Q and 3Q of this

year produced nine IPOs each—still

far from the record numbers put up

in 2013-2014, but more of a reversion

to the mean rather than a complete

vanishing act.

US PE-sponsored IPO activity by quarter

Source: PitchBook

7 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

PE IPOs: Metrics

The median offering size for PE-

backed IPOs has come in at $183

million, slightly down from the $186

million number we saw in 2015, yet

relatively high on a historical basis.

Compared to the entire IPO market,

PE-backed offerings raised more than

double the $90 million median we saw

when taking a look at the offering size

from both VC and PE-backed raises.

Larger raises are to be expected

from PE-backed businesses due to

the nature of where these companies

typically lie in their lifecycles. Where

venture capitalists back earlier-stage

companies, PE sponsors can many

times be operating companies that

are multiple decades old. The mature

nature of these businesses culminates

in a group of companies that have

been able to grow their revenues and

respective businesses over a much

longer period. Thus, while PE has

potentially been able to help such

companies boost margins and drive

cash flows, the sheer size of these

companies results in larger capital

raising requirements.

At $863 million, the median

postvaluation of PE-backed companies

completing public listings this year

came in at the highest level we’ve

seen since at least 2005. Although

many sponsors have had success

selling smaller portfolio companies

to other PE counterparts, as well as

to strategics looking to put money to

work acquiring PE-backed companies,

the bulk of that activity occurs along

the core middle market. Moving

forward, sponsor-backed IPOs won’t

likely increase dramatically, yet the

ones that come forward will typically

lay at the upper end of the size

spectrum and thus, offering sizes and

postvaluations should stay high.

PE-sponsored offering sizes show little change over 2015

Median and average offering size of PE-sponsored IPOs

Source: PitchBook

*As of 9/30/2016

PE IPO postvaluations fall for third consecutive year

Median and average IPO postvaluation

Source: PitchBook

*As of 9/30/2016

Median ($M)

Average ($M)

$199

$186

$183

$360

$270 $277

$0

$100

$200

$300

$400

$500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Median ($M)

Average ($M)

$762

$643

$896

$1,689

$1,361$1,295

$0

$500

$1,000

$1,500

$2,000

$2,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

8 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

PE IPOs: Sector

Source: PitchBook

*As of 9/30/2016

B2B has accounted for 25% of all PE-sponsored offerings

% of PE-sponsored IPO activity by sector

Source: PitchBook

*As of 9/30/2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

*

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials &Resources

More than 20% of capital raised in IPOs has gone into healthcare

% of IPO capital raised by sector

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

*

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials &Resources

In a year with very few initial public

offerings in the US, the normal

distribution of capital raised by

industry has landed far from the

norm. In the first three quarters

of the year, there were no IPOs

in the IT, energy or materials &

resources sectors. The void of

offerings was expected in the

energy and materials segments,

due to the sustained depression

in commodities prices and lack

of investor confidence that those

prices will recover anytime soon.

In these two sectors, we have seen

more bankruptcies and divestitures

instead of IPOs. The dearth of

offerings by IT companies, however,

is not so easily explained. After the

IPOs of PE-backed companies like

GoDaddy and First Data in 2015,

as well as the heightened interest

in the IT sector shown by PE firms

this year, we expected to see

more tech IPOs in recent quarters.

That being said, the October IPOs

by fintech developer BlackLine

Systems and exploration company

Extraction Oil and Gas show some

renewed interest in these sectors.

Due to the weakness of the overall

market, 41% of capital raised via

PE-backed IPOs this year has been

by B2B companies. The $2.0 billion

raised by B2B PE-backed offerings

so far this year has already

exceeded the $1.9 billion in 2015,

and the sector is on pace to match

the eight IPOs it produced in 2015.

Both years however, are a far cry

from the more than $6 billion

raised across 13 IPOs in 2013.

9 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

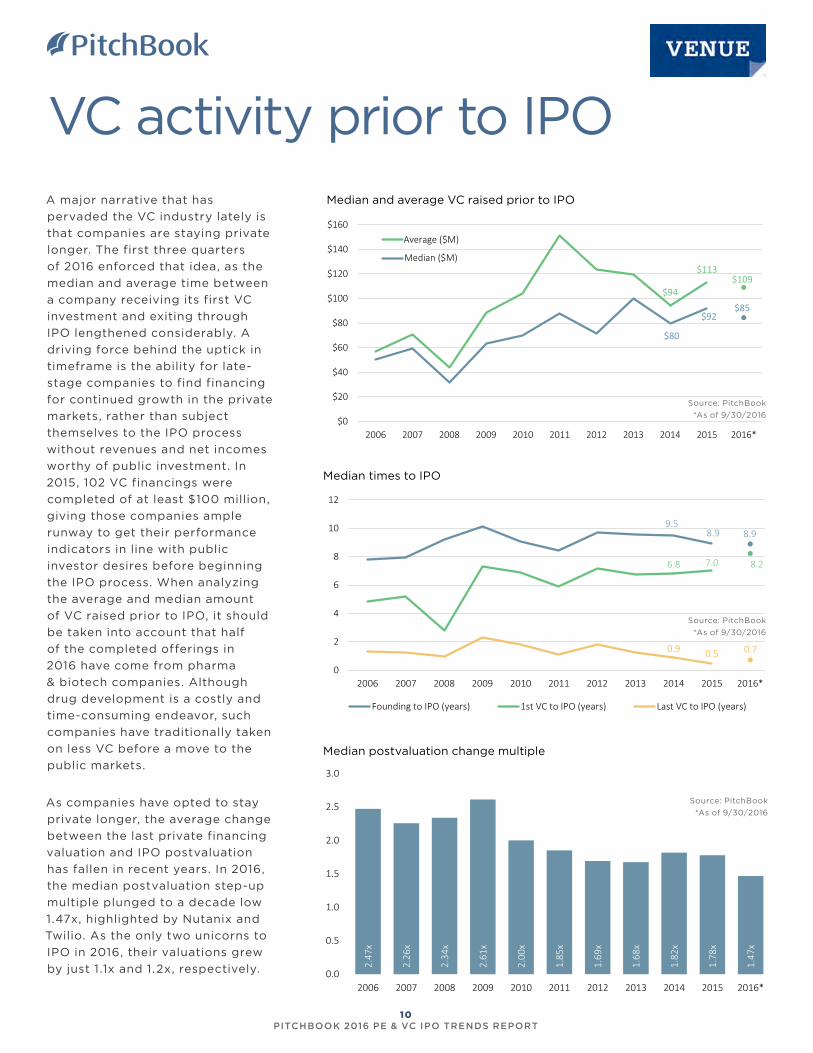

9.58.9 8.9

6.8 7.0 8.2

0.9 0.5 0.7

0

2

4

6

8

10

12

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Founding to IPO (years) 1st VC to IPO (years) Last VC to IPO (years)

VC activity prior to IPO

Median ($M)

Average ($M)

$80

$92$85

$94

$113$109

$0

$20

$40

$60

$80

$100

$120

$140

$160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Source: PitchBook

*As of 9/30/2016

Source: PitchBook

*As of 9/30/2016

Median and average VC raised prior to IPO

Median times to IPO

Median postvaluation change multiple

2.47

x

2.26

x

2.34

x

2.61

x

2.00

x

1.85

x

1.69

x

1.68

x

1.82

x

1.78

x

1.47

x

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Source: PitchBook

*As of 9/30/2016

A major narrative that has

pervaded the VC industry lately is

that companies are staying private

longer. The first three quarters

of 2016 enforced that idea, as the

median and average time between

a company receiving its first VC

investment and exiting through

IPO lengthened considerably. A

driving force behind the uptick in

timeframe is the ability for late-

stage companies to find financing

for continued growth in the private

markets, rather than subject

themselves to the IPO process

without revenues and net incomes

worthy of public investment. In

2015, 102 VC financings were

completed of at least $100 million,

giving those companies ample

runway to get their performance

indicators in line with public

investor desires before beginning

the IPO process. When analyzing

the average and median amount

of VC raised prior to IPO, it should

be taken into account that half

of the completed offerings in

2016 have come from pharma

& biotech companies. Although

drug development is a costly and

time-consuming endeavor, such

companies have traditionally taken

on less VC before a move to the

public markets.

As companies have opted to stay

private longer, the average change

between the last private financing

valuation and IPO postvaluation

has fallen in recent years. In 2016,

the median postvaluation step-up

multiple plunged to a decade low

1.47x, highlighted by Nutanix and

Twilio. As the only two unicorns to

IPO in 2016, their valuations grew

by just 1.1x and 1.2x, respectively.

10 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

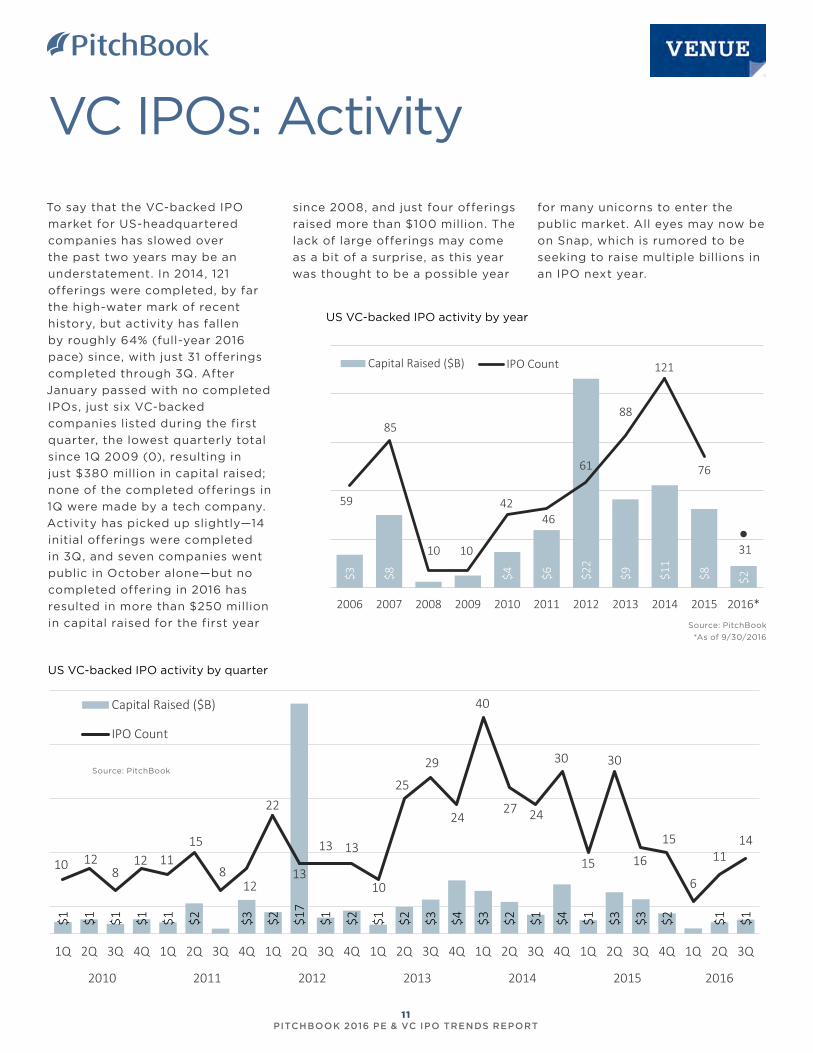

$1 $1 $1 $1 $1 $2 $3 $2 $17

$1 $2 $1 $2 $3 $4 $3 $2 $1 $4 $1 $3 $3 $2 $1 $1

10 128

12 1115

812

22

13

13 13

10

25

29

24

40

27 24

30

15

30

16

15

6

1114

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2010 2011 2012 2013 2014 2015 2016

Capital Raised ($B)

IPO Count

VC IPOs: Activity

Source: PitchBook

$3 $8 $4 $6 $22

$9 $11

$8 $2

59

85

10 10

4246

61

88

121

76

31

0

20

40

60

80

100

120

140

$0

$5

$10

$15

$20

$25

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Capital Raised ($B) IPO Count

US VC-backed IPO activity by year

US VC-backed IPO activity by quarter

To say that the VC-backed IPO

market for US-headquartered

companies has slowed over

the past two years may be an

understatement. In 2014, 121

offerings were completed, by far

the high-water mark of recent

history, but activity has fallen

by roughly 64% (full-year 2016

pace) since, with just 31 offerings

completed through 3Q. After

January passed with no completed

IPOs, just six VC-backed

companies listed during the first

quarter, the lowest quarterly total

since 1Q 2009 (0), resulting in

just $380 million in capital raised;

none of the completed offerings in

1Q were made by a tech company.

Activity has picked up slightly—14

initial offerings were completed

in 3Q, and seven companies went

public in October alone—but no

completed offering in 2016 has

resulted in more than $250 million

in capital raised for the first year

since 2008, and just four offerings

raised more than $100 million. The

lack of large offerings may come

as a bit of a surprise, as this year

was thought to be a possible year

for many unicorns to enter the

public market. All eyes may now be

on Snap, which is rumored to be

seeking to raise multiple billions in

an IPO next year.

Source: PitchBook

*As of 9/30/2016

11 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

VC IPOs: Metrics

$66$76

$67

$88 $107 $72

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Median Offering Size ($M)

Average Offering Size ($M)

$249 $285 $249

$438$519

$424

$0

$500

$1,000

$1,500

$2,000

$2,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Median Postval ($M)

Average Postval ($M)

Source: PitchBook

*As of 9/30/2016

Source: PitchBook

*As of 9/30/2016

Median and average IPO offering size

Median and average IPO postvaluation

Falling well below $100 million, the

average offering size dropped 32%

from last year to $72 million, the

lowest level since 2008. The steep

decline in comparison to recent

years has been accentuated by

the lack of outsized offerings that

previously pushed up the averages.

Four VC-backed companies raised

over $400 million in IPOs in 2015,

along with two companies in

2014—Facebook’s $16 billion IPO

in 2012 is what’s driving the spike

seen in the chart to the right. This

year, however, the largest offering

through 3Q has come in at just

$237 million (Nutanix), while 87%

of completed IPOs have fallen

below the $100 million mark.

While in theory public offerings

still offer a more probable path to

liquidity than acquisitions for the

most heavily funded and valued

companies, they do come along

with the investor scrutiny that

private markets are able to shield

against. Even with $1 billion-plus

valuations, many unicorns continue

to operate in a state of massive

growth that brings along high burn

rates and negative bottom lines.

Rather than face likely criticism

with an IPO, the unicorns that

the industry hoped would make

a public offering this year have

instead opted to tap into easily

accessible late-stage capital from

the private markets once more,

or still have enough runway from

a large financing raised last year.

Those unicorns that did complete

an IPO priced their offerings fairly

conservatively and realized only

moderate valuation climbs. That

said, both names did see their

stocks soar in secondary trading.

12 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

VC IPOs: Sectors

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

*

Pharma & Biotech

HC Services & Systems

HC Devices & Supplies

Commercial Services

Consumer Goods &RecreationEnergy

IT Hardware

Media

Software

Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

*

Pharma & Biotech

HC Services & Systems

HC Devices & Supplies

Commercial Services

Consumer Goods &RecreationEnergy

IT Hardware

Media

Software

Other

Source: PitchBook

*As of 9/30/2016

Source: PitchBook

*As of 9/30/2016

Following the market selloff at

the turn of the year, the investor

demand for tech IPOs that

founders had come to expect in

2014 and 2015 lagged considerably.

After a quiet first quarter with

zero tech offerings, the software

and IT hardware sectors have

picked up their pace a bit,

debuting a combined nine VC-

backed companies on US markets.

Twilio’s $150 million raise in 2Q,

and subsequent move to a high

of nearly $71 per share (~400%

growth), was hoped by many to

spur an “open window” for the IPO

market, but just one other tech

company privately valued at $1

billion or more has completed an

offering.

Continuing to represent the

largest share of IPO volume,

pharma & biotech has accounted

for 52% of all offerings this year,

a considerable uptick when

compared with its 17% share

in 2011. The extended drug

development cycle creates a need

for such companies to access

consistent funding that the

traditional VC model might not

be able to support. Establishing a

capital markets presence can be a

major benefit for pharma & biotech

companies as it allows them to

conduct follow-on offerings and

access more immediate capital at

a much quicker pace than what

might be available in the private

realm.

Pharma & biotech has accounted for more than 50% of VC IPOs in 2016

VC-backed IPOs by sector (#)

Despite lack of offerings, software has raised 30% of capital raised in IPOs

VC-backed IPO capital raised by sector ($)

13 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

IPO pricing & window

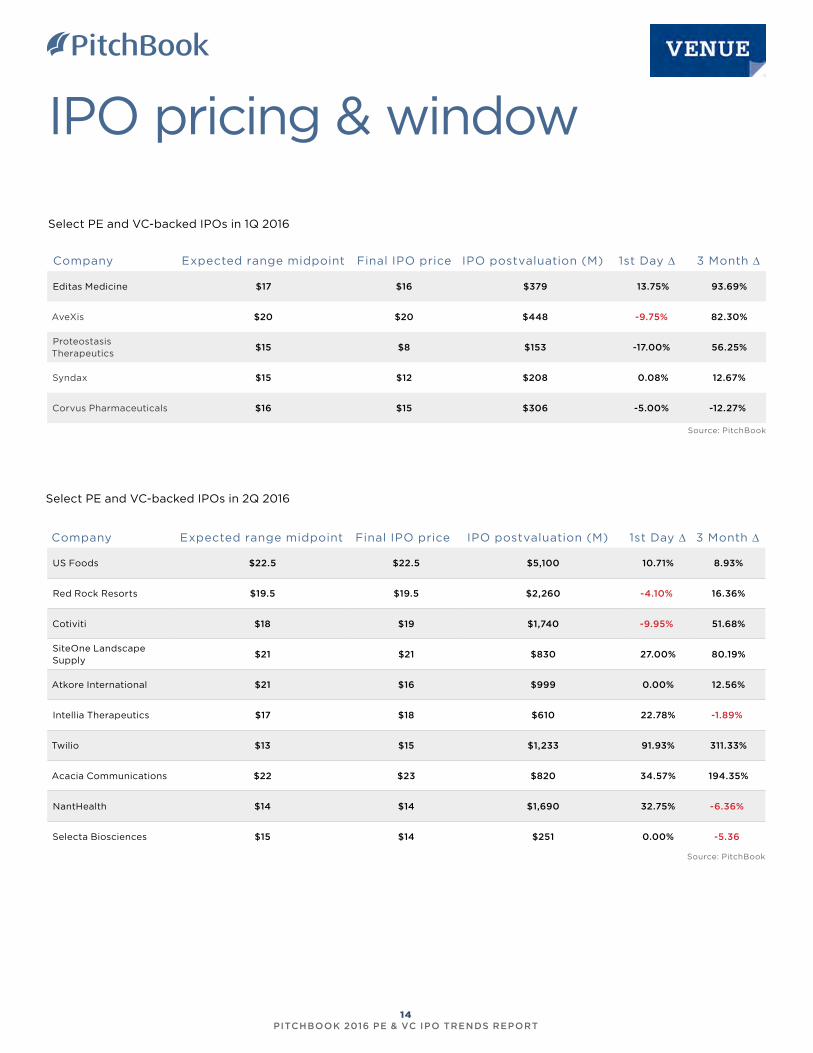

Editas Medicine $17 $16 $379 13.75% 93.69%

AveXis $20 $20 $448 -9.75% 82.30%

Proteostasis Therapeutics

$15 $8 $153 -17.00% 56.25%

Syndax $15 $12 $208 0.08% 12.67%

Corvus Pharmaceuticals $16 $15 $306 -5.00% -12.27%

Company Expected range midpoint Final IPO price IPO postvaluation (M) 1st Day ∆ 3 Month ∆

US Foods $22.5 $22.5 $5,100 10.71% 8.93%

Red Rock Resorts $19.5 $19.5 $2,260 -4.10% 16.36%

Cotiviti $18 $19 $1,740 -9.95% 51.68%

SiteOne Landscape Supply

$21 $21 $830 27.00% 80.19%

Atkore International $21 $16 $999 0.00% 12.56%

Intellia Therapeutics $17 $18 $610 22.78% -1.89%

Twilio $13 $15 $1,233 91.93% 311.33%

Acacia Communications $22 $23 $820 34.57% 194.35%

NantHealth $14 $14 $1,690 32.75% -6.36%

Selecta Biosciences $15 $14 $251 0.00% -5.36

Source: PitchBook

Source: PitchBook

Select PE and VC-backed IPOs in 1Q 2016

Select PE and VC-backed IPOs in 2Q 2016

Company Expected range midpoint Final IPO price IPO postvaluation (M) 1st Day ∆ 3 Month ∆

14 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

IPO pricing & window

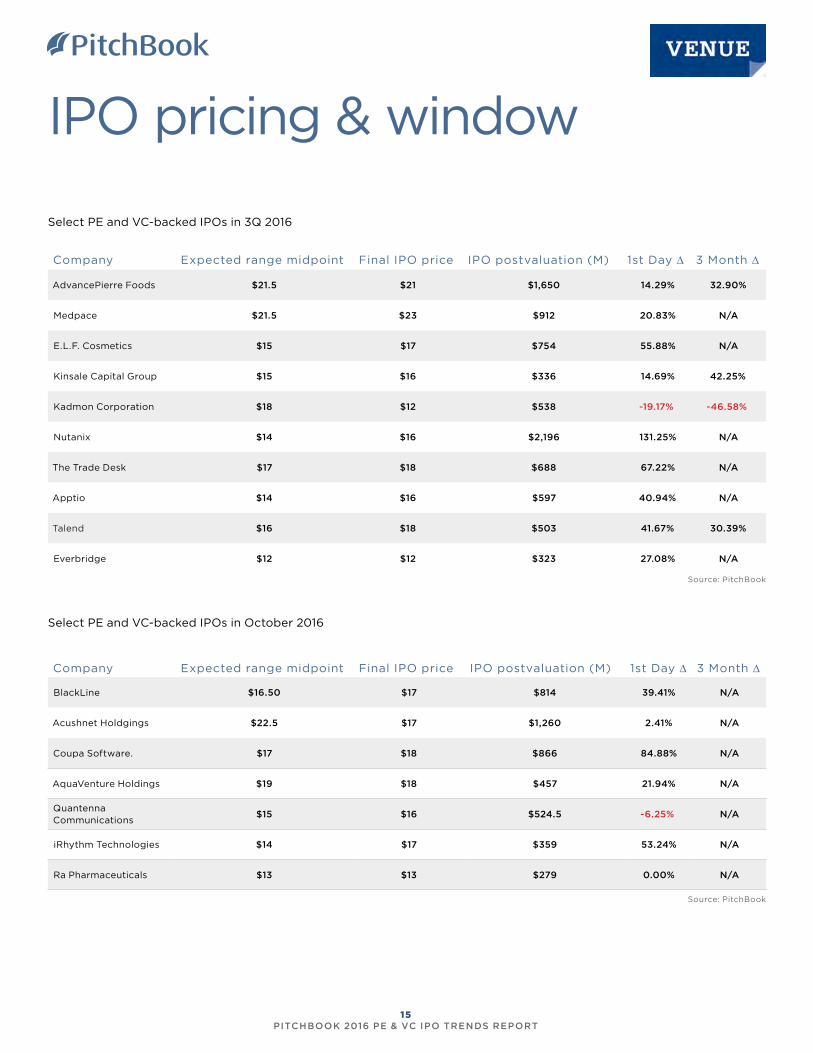

AdvancePierre Foods $21.5 $21 $1,650 14.29% 32.90%

Medpace $21.5 $23 $912 20.83% N/A

E.L.F. Cosmetics $15 $17 $754 55.88% N/A

Kinsale Capital Group $15 $16 $336 14.69% 42.25%

Kadmon Corporation $18 $12 $538 -19.17% -46.58%

Nutanix $14 $16 $2,196 131.25% N/A

The Trade Desk $17 $18 $688 67.22% N/A

Apptio $14 $16 $597 40.94% N/A

Talend $16 $18 $503 41.67% 30.39%

Everbridge $12 $12 $323 27.08% N/A

Select PE and VC-backed IPOs in 3Q 2016

BlackLine $16.50 $17 $814 39.41% N/A

Acushnet Holdgings $22.5 $17 $1,260 2.41% N/A

Coupa Software. $17 $18 $866 84.88% N/A

AquaVenture Holdings $19 $18 $457 21.94% N/A

Quantenna Communications

$15 $16 $524.5 -6.25% N/A

iRhythm Technologies $14 $17 $359 53.24% N/A

Ra Pharmaceuticals $13 $13 $279 0.00% N/A

Select PE and VC-backed IPOs in October 2016

Source: PitchBook

Source: PitchBook

Company Expected range midpoint Final IPO price IPO postvaluation (M) 1st Day ∆ 3 Month ∆

Company Expected range midpoint Final IPO price IPO postvaluation (M) 1st Day ∆ 3 Month ∆

15 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

IPO pipeline

Company Select investors Sector 2015 revenue ($M) Last buyout date Last buyout size (M)

Company Select Investors Sector

VC raised

to date (M)

2015 Revenue

(M)

Most recent private

postval (M)

Select upcoming PE-sponsored offerings

Select upcoming VC-backed offerings

Albertsons Cerberus Capital Management B2C $5.873 N/A N/A

PSAVGoldman Sachs Alternative Investments, Olympus Partners

B2C $1,487 1/27/2014 $1,020

YETICortec Group, Fifth Street Asset Management

B2C $468.9 6/15/2012 $67

Soul CycleGoldman Sachs, Leonard Green & Partners

B2C $117.7* 5/31/2011 $719

McGraw-Hill Education

Apollo Global Management B2C $1,834 3/22/2013 $2,400

Laureate Education

Sterling Partners, KKR, Point27 Asset Management, StepStone Group

B2C $4,292 7/20/2007 $3,800

Jeld-Wen Onex B2B $3,381 10/3/2011 $1,502

VisterraFlagship Ventures, Polaris Partners, Bill & Melinda Gates Foundation

Pharma & biotech

$69.8 — $111.25

Thar Pharmaceuticals Innovation WorksPharma & biotech

$6.6 — $19.5

Elevate Credit**Sequoia Capital, TCV, Startup Capital Ventures

Financial Services

— $237.7 —

**denotes spinout

Source: PitchBook

Source: PitchBook

*denotes figure for the nine months ended September 30, 2015

16 PITCHBOOK 2016 PE & VC IPO TRENDS REPORT

All datasets in this report cover US-based companies debuting on US exchanges, and unless otherwise noted, they are as of September 30, 2016.

DEFINITIONSPostvaluation: For this report, PitchBook calculated

postvaluation as the total number of outstanding

common shares multiplied by the final IPO price.

Offering size: PitchBook calculates offering size as

the total number of common stock shares offered

multiplied by the final offering price. If the stock has

not achieved a final price, the midpoint of the pricing

range is used. If the pricing range has not been filed,

the proposed maximum aggregate offering price is

used.

Upcoming IPOs: The companies were selected among

the total number of PE and VC-backed companies

that are currently in registration to go public.

Investors were also sampled from the total number of

backers.

PE or VC sponsorship: PitchBook bases PE or VC

sponsorship on whether or not a PE or VC investor

owns an interest in a company that has filed for an

upcoming IPO.

American Depository Shares: When applicable,

PitchBook calculates American Depository Shares

as a representation of ordinary (common) shares,

taking into account whatever representation is

outlined in the company’s SEC filing.

1-day and 3-month performance: In this report, the

first-day performance is calculated by comparing

the offering price to the price at the end of first

trading day; the 90-day performance is calculated

comparing the offering price to the price at the end

of the first three months of trading.

MAKE WAY FOR

SMARTER, ON-THE-FLY MEETING PREP

US +1 206.623.1986

UK +44 (0)207.190.9809

pitchbook.com

Introducing PitchBook Mobile. The same excellent data, technology

and service from the PitchBook Platform, now available on a mobile

device.

Search:

“PitchBook”Available for

Methodology