ut510 iowa motor vehicle taxes - zillionforms.com

TRANSCRIPT

A 5% motor vehicle use tax is imposed on thepurchase price of a vehicle subject to registration.This tax is payable to the appropriate Iowa county treasureror Iowa Department of Transportation.

A 5% motor vehicle lease tax is imposed on thelease of a qualified vehicle and is based on the“lease price” of the vehicle. To qualify, a vehicle mustbe available to be leased for 12 months or longer andhave a gross registered weight rating of less than 16,000 pounds.This tax is paid to the appropriate county treasurer, IowaDepartment of Transportation, or directly to the Iowa Departmentof Revenue.

UT510Iowa Motor Vehicle Taxes

Use Tax Manual forVehicles Subject to Registration

78-614 (3/04)

DEFINITIONS...................................................... 1

EXPLANATIONS................................................. 3CASUAL SALES .................................................... 3TRADE-INS AND TRADES ................................... 3Trade-ins to Dealers ...................................... 3Trades between persons ................................ 4

REFUNDS -CORRECTIONS OF ERRORS .............................. 5REGISTRATION BY MANUFACTURERS ............ 5REBATES ............................................................... 5RETURNED VEHICLES ....................................... 6RETURNED VEHICLES UNDER THE IOWALEMON LAW — IOWA CODE CHAPTER 322G . 6REPOSSESSIONS ................................................. 6INSURANCE SETTLEMENTS .............................. 6PREVIOUSLY-OWNED VEHICLES ..................... 7SALVAGE TITLES ................................................. 7FEDERAL EXCISE TAX........................................ 7IMPLEMENTS OF HUSBANDRY ........................ 7SALES TO NATIVEAMERICAN INDIANS ........................................... 7SPECIAL MOBILE EQUIPMENT ........................ 7DISABLED VETERAN .......................................... 8SALE OF CHASSIS WITH ADDEDEQUIPMENT OR ACCESSORIES ........................ 8SALE OF A BOAT OR ATVWITH A TRAILER ................................................. 8OPTIONAL SERVICE AGREEMENTS ................. 9UT510 AFFIDAVIT TRANSACTIONCERTIFICATE AFFIDAVIT FORMS.................... 9PENALTY FOR FALSE STATEMENT ................... 9

UT510 EXEMPTION OPTIONS

EXEMPTION #1 ................................................ 10GIFT, PRIZE, OR TRANSFER WITHOUTCONSIDERATION

RAFFLE PRIZE ................................................... 10PROMOTION ...................................................... 10TRANSFERSRESULTING FROM MERGERS ......................... 10GIFT TRANSFERS ............................................... 11TRANSFERS FROM A CORPORATIONTO AN EMPLOYEE.............................................. 11TRANSFERSTO A RETIRING EMPLOYEE ............................. 11TRANSFERS INVOLVING FAMILY ..................... 11TRANSFERS INVOLVING TRUSTS ................... 12

EXEMPTION #2 ................................................ 13CERTAIN NONPROFIT ORGANIZATIONS

EXEMPTION #2 continued .............................. 14PRIVATE NONPROFIT EDUCATIONALINSTITUTIONS

EXEMPTION #2 continued .............................. 15GOVERNMENT UNIT ORQUALIFYING GOVERNMENTALCORPORATION

EXEMPTION #3 ................................................ 16BUSINESS TRANSFERS

TRANSFERS TO NEW CORPORATIONSFROM PARTNERSHIPS ...................................... 17TRANSFERS TO NEW CORPORATIONSFROM INDIVIDUALS ........................................ 17TRANSFERS FROM A SOLEPROPRIETORSHIP TO A CORPORATION ....... 17TRANSFERS TO A NEW CORPORATIONWHEN OWNERSHIP DOES NOT REMAINTHE SAME .......................................................... 17TRANSFERS UPON DISSOLUTION WITHCONTINUATION OF THE BUSINESS .............. 18TRANSFERS FROM CORPORATIONTO STOCKHOLDER ........................................... 18TRANSFERS FROMCORPORATION TO CORPORATION................ 18

Contents

EXEMPTION #4 ................................................ 19DEALERS

PROMOTIONS AND RAFFLES ......................... 19EXEMPT DEALER USE...................................... 20

EXEMPTION #5 ................................................ 21VEHICLES PURCHASED FORRENTAL OR LEASE

PURCHASED FOR RENTAL .............................. 21PURCHASED FOR LEASE ................................ 21

EXEMPTION #6 ................................................ 22INTERSTATE COMMERCE,LEASED VEHICLE

EXEMPTION #7 ................................................ 23VEHICLES USED IN INTERSTATECOMMERCE

EXEMPTION #8 ................................................ 24MANUFACTURED HOUSINGAND MOBILE HOMES

MOBILE HOME TRADE-INS ............................. 24MANUFACTURED HOUSING ........................... 25

EXEMPTION #8 ................................................ 26INHERITANCE WITH AND WITHOUTA COURT ORDER / TRANSFER OF TITLE

TRANSFERS RESULTINGFROM COURT ORDERS .................................... 26TRANSFERS WITHOUT COURT ORDERS(BY WILL AND INTESTATE) .............................. 26

EXEMPTION #8 ................................................ 27PURCHASED WITH NO INTENTTO USE VEHICLE IN IOWA

PURCHASED IN FOREIGN COUNTRY ............ 27NONRESIDENT IN-TRANSIT ............................. 27NONRESIDENT MOVE-IN ................................. 27DETERMINING USE .......................................... 28

EXEMPTION #8 ................................................ 29OTHER

EXEMPTION #8 ................................................ 30HOMEMADE VEHICLES

EXEMPTION #8 ................................................ 31TAX PAID TO ANOTHER STATE

MOTOR VEHICLE LEASE TAX (MVLT) .... 33Qualifying vehicles ..................................... 33MVLT imposed on lessor ............................ 33MVLT imposed on lease, not vehicle ......... 33Refunds ....................................................... 33How to complete the MVLT worksheet ...... 33

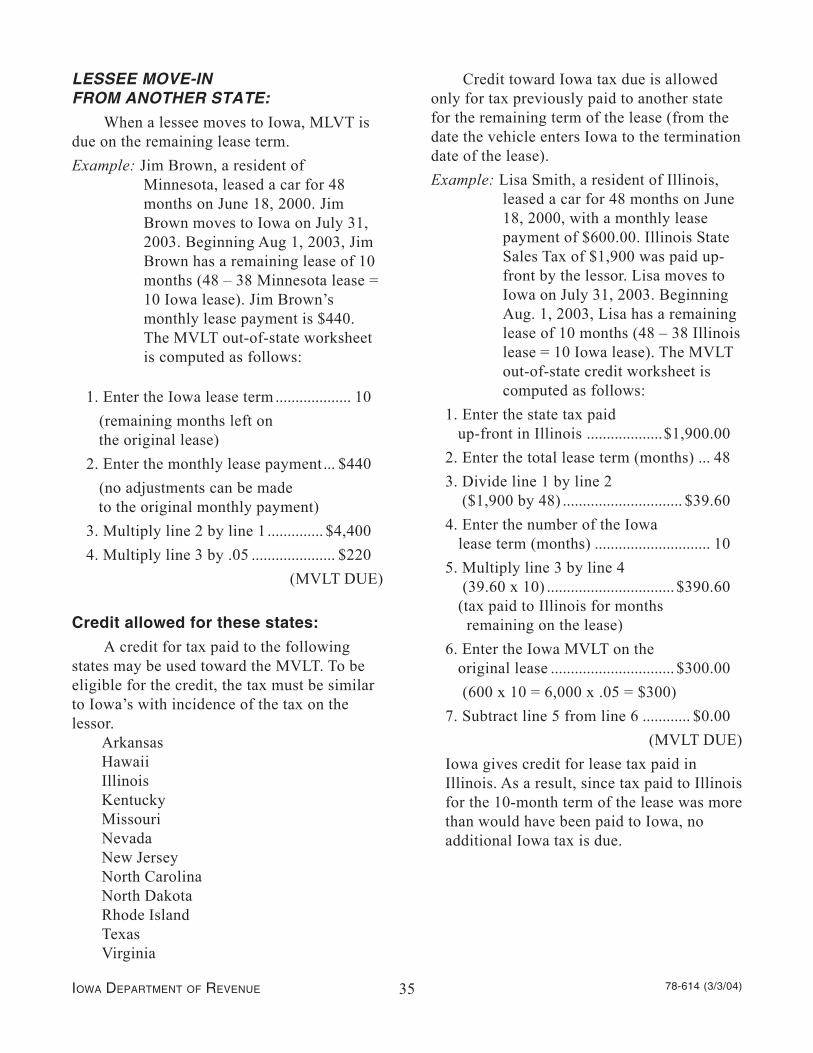

LESSEE MOVE-INFROM ANOTHER STATE: .................................. 35Credit allowed for these states: ................... 35Lessee terminates lease to purchase ............ 36

Questions? or For More Information............... 38TO TALK TO A TAX SPECIALIST ...................... 38TO OBTAIN PUBLICATIONS AND FORMS ...... 38TDD FOR HEARING IMPAIRED ....................... 38MAILING ADDRESS ........................................... 38

1IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

DEFINITIONS

“Consideration” — Not only a gain toone contracting party, but also a detriment,forebearance, inconvenience or liabilityassumed by the other. See Homesteader’s LifeAssociation v Solinger, 235 N.W. 485, (Iowa1931).

“Gift” — A voluntary transfer ofpersonal property without consideration. Agift takes effect at once and is not dependentupon any agreement or contingency occurring.See Black’s Law Dictionary, page 817.

“Manufactured housing” — Housingwhich is factory built to specificationsrequired by 42 U.S.C. section 5403, anddisplays a seal from the United StatesDepartment of Housing and UrbanDevelopment.

“Mobile home” — Any vehicle withoutmotive power used or manufactured orconstructed to use as conveyance on thepublic streets and highways and designed,constructed, or reconstructed to permit thevehicle to be used as a place for humanhabitation by one or more persons. See IowaCode section 321.1(39)(a).

“Motor vehicle” — A vehicle which isself-propelled, but not including vehiclesknown as trackless trolleys which arepropelled by electric power obtained fromoverhead trolley wires and are not operatedupon rails. See Iowa Code section321.1(42)(a),

“Person” — Any individual, firm,partnership, joint adventure, association,corporation, municipal corporation, estate,trust, business trust, receiver, or any othergroup or combination acting as a unit in theplural as well as the singular number. SeeIowa Code sections 422.42(8) and 423.4(14).

“Purchase” — Any transfer, exchange,conditional or otherwise, in any manner or byany means whatsoever, for a consideration.See Iowa Code section 423.1(5).

“Purchase price” — The total amountfor which tangible personal property is sold,valued in money, whether paid in money orotherwise:

a. Cash discounts on sales are notincluded. A cash rebate provided by amotor vehicle manufacturer is notincluded if the rebate is applied to thepurchase price of the vehicle.

b. If tangible personal property is tradedtoward the purchase price of a vehicle,the purchase price is the portionpayable in money to the retailer if:1. The tangible personal property

traded to the dealer is the type ofproperty normally sold in regularcourse of the dealer’s business, or

2. The tangible personal propertytraded to the dealer is intended bythe dealer to be ultimately sold atretail or is intended to be used bythe dealer in the re-manufacturingof a like item.

c. In transactions between persons,neither of which is a dealer of vehiclessubject to registration, in which avehicle subject to registration is tradedtoward the purchase price of anothervehicle subject to registration:The purchase price is the differencebetween the total purchase price andthe amount of the traded vehicle. SeeIowa Code section 423.1(6).

d. The purchase price includes allaccessories, additional equipment,enumerated services, freight andmanufacturer’s taxes.

e. The taxable purchase price does notinclude the charge commonly knownas document fees. Document fees arecharges that most dealers impose forthe non-taxable service of processingthe paper work involved in thepurchase of a vehicle.

2IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

“Taxable use” — The exercise of anyright of ownership over tangible personalproperty in Iowa by any person owning orusing the property. Vehicles are tangiblepersonal property.

“Taxpayer” — Any person who issubject to a tax imposed by Iowa Codechapters 422 and 423, whether acting on theperson’s own behalf or as a fiduciary. SeeIowa Code sections 422.42(19) and 423.1(14).

“Use” — The exercise by any person ofany right or power over tangible personalproperty incident to the ownership of thatproperty. It does not include processing or thesale of that property in the regular course ofbusiness. See Iowa Code section 423.1(12).

For the purpose of proper administrationand to prevent evasion of the tax, evidencethat tangible personal property was sold byany person for delivery in this state is primafacie evidence that such tangible personalproperty was sold for use in this state. SeeIowa Code section 423.5.

“Vehicles subject to registration” — Avehicle subject to registration pursuant toIowa Code sections 321.18 and 423.1(13).

3IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXPLANATIONS

CASUAL SALESThe casual sale exemption does not apply

to vehicles subject to registration.

TRADE-INS AND TRADESA trade is a type of sales transaction in

which only the owner(s) with legal title to avehicle can transfer that vehicle. The owner(s)is the person(s) named on the vehicle title.

When a trade-in occurs, the name(s) onthe title and registration of the vehicle beingpurchased must be the same name(s) on thetitle and registration of the vehicle being usedfor trade-in.

There is one exception. If multiplenames are on the title and registration and arelisted with “or” separating the names, any oneof the individuals may use the vehicle fortrade. The reason is that “or’” means eachperson on the title and registration owns100% of the vehicle. In this instance, thetrade-in allowance is allowed. NOTE: Theexception only applies to “trade-ins” and not“consideration.”

Trade-ins to DealersWhen a person trades with a dealer, the

purchase price is the portion paid in money ifthe following conditions are met:

a. The tangible personal property beingtraded is the type normally sold in theregular course of the dealer’s business,and

b. The property traded is intended to besold at retail or is intended to be usedin the re-manufacturing of a like item.

“Regular course of business” means aretailer makes sales of the same type of itemon a recurring basis.Example: John trades a boat toward the

purchase of a new car. The car’spurchase price is $10,000, and the

dealer allows a trade-in allowanceof $5,000 for the boat. The dealeris not regularly engaged in thebusiness of selling boats. Thetrade-in amount of $5,000 for theboat does not reduce the amountsubject to use tax. Use tax is dueon $10,000.

Example: Mike is purchasing a new car for$40,000 and trades in a combine.The dealer is regularly engaged inthe business of selling cars andfarm equipment. The dealer allowsa trade-in of $30,000 for Mike’scombine. Therefore, the price ofthe car is $40,000 minus the$30,000 trade allowance. Mikepays the dealer the difference of$10,000. Since the dealer isregularly engaged in the businessof selling farm equipment, the$30,000 trade-in allowance is notsubject to use tax. Use tax is dueon $10,000.

Example: Joe leases a vehicle from FordMotor Credit Co. for nine months.Joe agrees to transfer the car hecurrently owns to a Ford dealer.The Ford dealer will be selling thecar that Joe is leasing to FordMotor Credit Co. The car sold toFord Motor Credit Co. has a retailprice of $30,000, and the dealerallows a $5,000 trade allowance.Thus, Ford Motor Credit Co. paysthe Ford dealer $25,000. Since thename on the vehicle beingpurchased (Ford Motor Credit Co.)is not the same name on the vehicletraded (Joe), the trade-in allowanceof $500 cannot be used for use taxpurposes. Use tax is due on the$30,000.

4IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

Example: On June 24, Cathy purchases a newtruck and uses a truck she owns asa trade. Cathy goes to Truck Autoto purchase the new truck. Thetruck Cathy wants has to beordered from the manufacturer andwill take six months for delivery.Truck Auto prepares a purchaseorder showing the retail price of$50,000 and a trade-in allowancefor Cathy’s truck of $20,000. Sincethe truck being ordered will not bedelivered for six months, TruckAuto allows Cathy to drive hertruck until the new truck arrives.Truck Auto still allows Cathy the$20,000 trade-in allowanceregardless of the additional milesCathy may put on her traded truck.Since the purchase order for thenew truck shows a $20,000 tradeallowance, use tax is imposed onthe $30,000.

Example: George owns a car dealershipcorporation and a farm tractorcorporation. Cecil wishes topurchase a car worth $40,000 fromthe car dealership. Cecil uses atractor as trade, and the cardealership allows a trade-inallowance of $40,000. Cecilfurnishes no money. Since Cecil’stractor was traded to the cardealership and not the tractordealership, the trade-in allowancecannot be used for use taxpurposes. Use tax is imposed on$40,000.

Example: Sarah owns two cars and wants totrade both cars toward the purchaseof a new car. Honest Abe’sdealership allows a trade-inallowance of $5,000 for the firstcar and $7,000 for the second car,for a total trade-in allowance of$12,000. The new car purchaseprice is $14,000. Since HonestAbe’s is in the business of resellingused cars, both cars can be used asa trade-in allowance Use tax isimposed on $2,000.

Trades between personsWhen vehicles subject to registration are

traded between persons, neither of which is adealer, the purchase price is the differencebetween the prices of the vehicles.Example: John Doe has an automobile with a

value of $2,000. His neighbor, BillJones, has an automobile valued at$3,500. They decide to tradeautomobiles. John pays Bill $1,500cash difference. John will pay usetax on $1,500. Bill’s purchase isexempt from use tax.

Example: Jane has an automobile with a valueof $5,000. Her friend Jim also hasan automobile valued at $5,000.They decide to trade automobiles.Jane and Jim make an even trade,automobile for automobile with nomoney changing hands. No tax isdue on either automobile becausethere is no exchange of money.

5IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

REFUNDS -CORRECTIONS OF ERRORS

If tax is mistakenly paid, it may berefunded. The owner of the vehicle must file aClaim for Refund (form IA 843) directly withthe Iowa Department of Revenue within threeyears after the tax payment became due or oneyear after the payment was made, whichevertime is the later.

REGISTRATION BY MANUFACTURERSManufacturers who title and register

vehicles in Iowa from an MSO are allowed topay use tax based on a purchase price of 50percent of the fabricated costs of the vehicle.The 50 percent tax base was the result of anagreement between vehicle manufacturers andthe department.

Note: Registrations made by subsidiariesof manufacturers are taxed on 100 percent ofthe purchase price.

REBATESManufacturers’ rebates can be used to

reduce the taxable purchase price of a vehicle.To qualify, all of the following must bepresent:

1. A rebate must be a return of an amountpaid (or required to have been paid) bythe purchaser;

2. The rebate must be in the form of cash;3. The rebate must be offered by a

manufacturer, which is any person orentity that fabricates, assembles orcombines materials and parts to createa vehicle subject to registration inIowa;

4. The rebate must be applied to thepurchase price of the vehicle. Therebate cannot be used to reduce thegross receipts of the purchase.

5. The rebate is strictly a transactionbetween a manufacturer and apurchaser:a. The rebate must be from an entity

acting as a manufacturer of thevehicles when offering the rebate. Itcannot be from a vehiclemanufacturer engaging in otheractivities, such as a manufactureracting in the capacity of a creditcard issuer or a financing program;and

b. The purchaser must be in theprocess of purchasing the vehiclewhen the rebate is given. The rebatecannot be given to a customer in asituation similar to the credit cardrebate program, in which thecustomer earns the right to therebate over a period of time.

Credit cards issued by Ford Motor andGeneral Motors that are used as a rebatetoward the price of a Ford or GM vehicle arenot a manufacturer’s rebate. These types ofrebates cannot be used toward reducing thetaxable purchase price of a vehicle.

6IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

Example:Price of Ford vehicle $30,000Less trade-in $10,000Less credit card “rebate” $ 1,000Purchase price $19,000Use tax is due on $20,000 value.

RETURNED VEHICLESWhen a vehicle subject to registration is

sold and later returned to the seller and the“entire purchase price” is refunded by theseller, the purchaser is entitled to a refund ofthe use tax paid. The “entire purchase price”means 100 percent not including tax, title andregistration fees. To obtain a refund, thepurchaser must be able to show that the entirepurchase price was returned and provide proofthat the use tax had been paid. The purchasermust send proof with a completed form IA843 to the Iowa Department of Revenue.

RETURNED VEHICLES UNDER THEIOWA LEMON LAW —IOWA CODE CHAPTER 322G

If a vehicle manufacturer reimburses apurchaser for tax paid on a returned defectivevehicle, the manufacturer may obtain a refundfrom the Iowa Department of Revenue. Proofthat the tax was paid and the purchaserreimbursed in accordance with the provisionsof Iowa Code chapter 322G must be sent tothe department with a completed form IA 843.

REPOSSESSIONSRepossessions can be made by dealers,

financial institutions, or by individuals.Whether or not tax is due on a repossessiondepends on the manner in which therepossession is conducted. There must be alien on the title, and the repossession must beregulated under the Uniform Commerce Code(Iowa Code, Chapter 554) for a repossessionto be considered valid. If a valid repossessionhas occurred, taxability of the sale of therepossessed vehicle depends on the type of

entity performing the repossession and thedocumentation of the transaction as shown inthe following examples:Example: If a licensed dealer repossesses a

vehicle and will be reselling thevehicle, the dealer can use thedealer resale exemption to avoiduse tax. There must be a lien on thetitle, and the repossession must beregulated under the Iowa UniformCommerce Code.

Example: If a financial institution repossessesa vehicle and does not have adealer’s license, tax is based on oneof the following:

a) If the financial institution uses theforeclosure affidavit to take title tothe vehicle and register the vehicle,tax is due based on the outstandingloan amount. The affidavit offoreclosure can only be used forrepossessions.

b) If the financial institution uses theforeclosure affidavit merely toretain possession of the vehicleuntil a buyer is found, no tax is due.In this instance, the personperforming the repossession doesnot take title to the vehicle.

Repossessions of mobile homes are to behandled in the same manner as vehicles.

INSURANCE SETTLEMENTSWhen an insurance company takes title to

a vehicle after paying an insured client fordamage to the client’s vehicle, tax is due onthe amount of money paid by the insurancecompany to the policy holder, unless theinsurance company has a used dealer’slicense.

7IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

PREVIOUSLY-OWNED VEHICLESA common misconception is that if a

person sells a vehicle he/she owns and thenbuys the same vehicle back, the transaction isexempt from use tax. These are two separatetransactions and both are taxable.

Note: This is not the same as a returnedvehicle. In a returned vehicle situation, thepurchaser makes the decision to return thevehicle, and the seller agrees to accept thereturned vehicle and to void the saleagreement.

SALVAGE TITLESIf a salvage vehicle is repaired and

subsequently registered for highway use, usetax is due on the parts, supplies andequipment, unless sales or use tax has beenpreviously paid by the person who owns thesalvaged vehicle. Upon registration, proof ofsales or use tax paid on the parts, supplies andequipment must be provided. If proof of taxpaid cannot be furnished, use tax is imposedon the fair market value of the vehicle.

FEDERAL EXCISE TAXFederal excise tax imposed on the act of

manufacturing rather than at the time of salemay not be deducted from the taxable price ofvehicle. To be excluded from Iowa use tax,the Federal excise tax must (1) be due at thetime of the retail sale and (2) must be billed orcharged as a separate item. Proof that the tworequirements have been met must be providedto the county treasurer or Iowa Department ofRevenue.

Federal Luxury Excise Tax (FLET) iscollected by the retailer and remitted directlyto the IRS. This tax is based on a retail saleand cannot be subtracted from the purchaseprice before calculating Iowa use tax.Example:

Retail sale $45,000Less FLET threshold $32,000Vehicle subject to FLET $13,000Vehicle subject to use tax $45,000

IMPLEMENTS OF HUSBANDRYLivestock trailers registered as

implements of husbandry and drawn by avehicle subject to registration are exemptfrom use tax. However, if the livestock traileris titled and registered, use tax is due.

SALES TO NATIVEAMERICAN INDIANS

If a dealer delivers a vehicle to a residentNative American Indian on the reservationand at a later time the resident NativeAmerican Indian registers the vehicle at thecounty treasurer’s office, no tax is due sincethe delivery took place on the reservation.

If the vehicle is delivered off thereservation, use tax is due even if the sole useof the vehicle is on the reservation.

If delivery takes place on the reservationbut the owner is not a member of anyrecognized tribe, use tax is due.

All three tribes with land in Iowa – Sacand Fox, Winnebago, and Omaha – havegoverning bodies duly recognized by theSecretary of the Interior. These governingbodies resemble municipal, county and stategovernments. Therefore, purchases by thegoverning bodies of the above NativeAmerican Indian tribes on or off thereservation are exempt from tax. This isbecause governing tribal entities areconsidered to be quasi-governmental entitiesentitled to the same tax-exempt status grantedto other governmental entities. (See PolicyStatement dated 9-19-94.)

SPECIAL MOBILE EQUIPMENTIf special mobile equipment is titled and

registered, use tax is due.

8IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

DISABLED VETERANIf a governmental entity takes title or

ownership of a vehicle subject to registration,the exemption granted to governmentalentities can be claimed. However, if thegovernmental agency does not take title, thegovernmental exemption does not apply.

Example: Joe Beck is a disabled veteranand needs a van. Joe Beck contacts theVeterans Administration to see if they wouldprovide the funds to purchase a van. TheVeterans Administration agrees to provide thefunds. Joe Beck purchases a van from BigMike Ford for $14,000. The VeteransAdministration writes a check for $14,000payable to Big Mike Ford. The title is issuedin the name of Joe Beck. Since the VeteransAdministration did not take title of the van,Joe Beck’s purchase of the van withgovernment funds is subject to use tax. Usetax is due on $14,000.

SALE OF CHASSIS WITH ADDEDEQUIPMENT OR ACCESSORIES

If a dealer sells a chassis and thepurchaser has the dealer install anyequipment, use tax is due on the full purchaseprice, including the chassis and theequipment. This is a completed vehicle whendriven off the dealer’s lot.Example: Joe’s Tree Trimming Service

purchases a chassis from Ford Autofor $20,000. Joe’s Tree TrimmingService wants a lift added to thechassis. Ford Auto agrees to selland install the lift for $15,000.Ford Auto takes the chassis toGeorge’s Lift Sales for purchaseand installation of the lift. After theinstallation, Joe’s Tree TrimmingService returns to Ford Auto totake delivery of the completedvehicle. Joe’s Tree Trimming

Service requests Ford Auto toitemize the chassis price of$20,000 and the lift price of$15,000. Joe’s Tree TrimmingService pays Ford Auto $35,000 forthe complete vehicle. The chassisand lift are a vehicle subject toregistration and use tax is due on$35,000.

Example: Joe’s Tree Trimming Servicepurchases a chassis from Ford Autofor $20,000. Joe’s Tree TrimmingService wants a lift added to thechassis. However, Joe’s TreeTrimming Service will purchase thelift from a third party and not fromFord Auto. Joe’s Tree TrimmingService pays Ford Auto $20,000 forthe chassis. Joe’s Tree TrimmingService drives the chassis toGeorge’s Lift Sales to purchase andinstall a lift for $12,000. Thepurchase of the chassis from FordAuto is subject to Iowa use tax.The purchase and installation of thelift from George’s Lift Sales aresubject to Iowa sales tax and anyapplicable local option tax.

SALE OF A BOAT OR ATVWITH A TRAILER

It is not uncommon for a boat dealer tosell a boat with a trailer as a packaged deal.The dealer must put a separate price on theboat, boat accessories, and trailer, so thecorrect amount of use tax may be imposed onthe trailer. If the boat dealer does not, it isassumed the package deal is for the purchaseof a trailer and not for the boat andaccessories. It is not the responsibility ofeither the county treasurer or the countyrecorder to determine the purchase price ofthe property within the package deal.

9IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

OPTIONAL SERVICE AGREEMENTSA dealer is required to collect sales tax

on the sale of an optional service agreement.If the dealer includes the optional serviceagreement in the taxable price of the vehicle,the county treasurer is required to return alldocuments to the dealer with instructions toremit the sales tax on the sale of the optionalservice agreement directly to the IowaDepartment of Revenue. The dealer thensubmits the use tax to the county treasurerbased on the sales price of the vehicle less thecost of the optional service agreement.

UT510 AFFIDAVITTRANSACTION CERTIFICATEAFFIDAVIT FORMS

UT 510 affidavit exemption certificatesare used to confirm a purchase price orestablish exemption from use tax.

The affidavit is used to report a purchaseof a vehicle subject to registration and showsthe total delivered purchase price of a vehiclesubject to registration.

The exemption form separately lists theexemptions from use tax in eight majorcategories. If the affidavit is used to exempt apurchase from use tax and the owner isclaiming exemption number 1 or number 3;the completion of the transaction action formis required. For exemptions 2,4, 5, 6, 7, and 8,the treasurer, with the approval of thedepartment, determines if the affidavit isnecessary for a particular transaction.

Note: The burden of proof regardingwhether an exemption applies is upon theperson claiming the exemption. If theexemption appears questionable, the countytreasurer should allow the exemption, “flag”the affidavit for review, and advise the personthat the Iowa Department of Revenue willreview the exemption. If the departmentdisallows the exemption, the person claimingthe exemption is liable for any applicable tax,penalty and interest.

Affidavits of exemption that are notcorrect in both substance and form will not beaccepted by the county treasurer, the motorvehicle division or the Department ofRevenue. When in doubt, the county treasureror motor vehicle division will collect the tax.If the owner believes tax has been erroneouslycollected, a Claim for Refund form IA 843may be filed with the Iowa Department ofRevenue.

The Iowa Department of Revenuerequires signatures on all affidavits. If a fleet(five or more vehicles) of vehicles is beingregistered, affidavits for each vehicle withinthe fleet need to be completed and signed. Thedepartment does allow the use of signaturestamps to complete the signature portion ofthe affidavit form.

PENALTY FOR FALSE STATEMENTA person who willfully makes a false

statement in regard to the purchase price of avehicle subject to taxation under Iowa Codesection 423.7 is guilty of a fraudulentpractice. See Iowa Code sections 423.26 and423.18(2).

10IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #1GIFT, PRIZE, OR TRANSFER WITHOUT CONSIDERATIONRAFFLE PRIZE

When an organization purchases avehicle from a dealer to subsequently award itas a raffle prize under Iowa Code chapter99B, neither the recipient of the prize nor theprize sponsor is liable for use tax (O.A.G. 4-16-91).Example: A children’s hospital purchases a

vehicle from a local dealer to beused as a prize in a raffle. Raffletickets are sold to raise funds for anew children’s wing to the hospital.The purchase of the vehicle by thehospital as a prize for the raffle isnot subject to Iowa use tax. Inaddition, when the raffle winnerregisters the vehicle, use tax is notdue on the vehicle.

Example: Kings Dealership donates (gives) acar to a non-profit organization,which will use the car as a prize ina licensed raffle. Since the car is aprize in a licensed raffle anddonated to a nonprofit organizationunder Iowa Code section422.45(3), the dealer’s purchase ofthe car is exempt from use tax.

PROMOTIONWhen a vehicle is given away by a dealer

as a promotion, use tax is imposed on thedealer’s purchase price. Because the vehiclewas not resold, the dealer exemption does notapply. In some promotional giveaways, thedealer may require the winner to pay the usetax. Iowa law does not prohibit contest rulesthat require a prize recipient from paying thetax on behalf of the dealer. Even if therecipient is required to pay the use tax basedon contest rules, the responsibility of payingthe tax remains on the dealer.

Example: Bob’s Chevrolet has a drawing forthe purpose of promoting hisdealership. Bob’s Chevroletdisplays a new car as the prize.Bob’s Chevrolet purchased the carfor $7,000. One of the rules of thepromotion is that the winner mustpay any and all taxes imposed onBob’s Chevrolet. Jill is the winnerand agrees to the drawing rules.The car used is subject to use tax.Tax is due on the $7,000.

TRANSFERSRESULTING FROM MERGERS

If title to a vehicle is transferred fromone corporation to another, the transfer is notsubject to Iowa use tax if all of the followingfive criteria exist:

1) The merger is pursuant to statute (IowaCode Section 490.1106);

2) By the terms of the statute, the title ofthe vehicle is transferred from amerging corporation to a survivingcorporation;

3) The transfer is not based onconsideration such as required incontract law;

4) The merging corporation isextinguished and dissolved themoment of the merger; and

5) The merging corporation does notreceive any benefit of the merger as aresult of the dissolution.

Example: ABC Corporation and LuckyCorporation enter into a voluntarymerger agreement governed byIowa Code section 490.1106. ABCand Lucky corporations voluntarilynegotiate an arms-length mergeragreement which results in thetransfer of ABC’s assets, including

11IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

all vehicles, to Lucky Corp for thedissolution of ABC Corp. In return,ABC Corp stockholders receivestock in Lucky Corp. ABC Corp’stransfer of the vehicles to thesurviving company Lucky Corp is astatutory merger; no use tax is due.

GIFT TRANSFERSA gift of a vehicle from one person to

another is exempt from use tax because noconsideration has occurred.

Note: Transfers among family involvingconsideration are not exempt from use tax.

TRANSFERS FROM A CORPORATIONTO AN EMPLOYEE

Most transfers of vehicles by acorporation to an individual are subject toIowa use tax. However, there are twoexceptions to this general rule. A corporationmay make gifts of corporate vehicles withoutuse tax being paid by the corporation or therecipient if (1) the gift is a charitablecontribution or (2) if the transfer is a gift to aretiring employee.Example: George is a shareholder and

employee in MAC Corporation. Inthe months of April throughNovember, George worked asubstantial amount of overtime. InDecember, the corporation allowedGeorge to choose whether to bepaid for the overtime by receivingadditional wages or by taking titleto a corporate vehicle. Georgechooses to take the vehicle, andMAC Corporation transfers thetitle of the corporate vehicle toGeorge.

The transfer of the vehicle toGeorge was “in-kind”compensation paid by thecorporation to George for theovertime hours worked. Thiscompensation constitutes sufficientconsideration. Use tax is due on theamount of the overtime pay.

TRANSFERSTO A RETIRING EMPLOYEEExample: Easy-Tow Corporation executive

Joe Rich has use of a company carwhile employed. Joe Rich retiresand receives the car as a retirementgift. The car is fully depreciated onthe corporation books.A transfer of a vehicle uponretirement indicates that it isintended as a gift.Note: If Easy-Tow Corporationprovides George with a W-2 or1099, Easy-Tow Corp intends thetransfer of the vehicle to be incometo George and not a gift. Use tax isdue on the amount reported on theW-2 or 1099 as wages. (PolicyStatement 02-21-94)

TRANSFERS INVOLVING FAMILYTransfers among family members are

subject to use tax if consideration is given:Example: John and Mary Smith paid cash for

a new car. The car is titled andregistered as joint tenancy with fullrights of survivorship by indicating“or” between the names on thetitle. John decides to remove hisname from the title.The removing of John’s name doesnot create consideration. Underjoint tenancy, both John and MarySmith own 100% of the new car.As a result, the transaction is notsubject to Iowa use tax. (PolicyStatement 07-27-89)

12IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

Example: Mike Smith owns Big Mike Auto, asole proprietorship. Mike’s son,Craig, needs a car, and Mike gives(gifts) a car to Craig worth $5,000.Craig does not provide anyconsideration. Craig does not oweuse tax on the transfer. However,Big Mike Auto owes use tax on thepurchase price. The vehicle waspurchased for resale; however, itwas not sold by Big Mike Auto. Asa result, Big Mike Auto loses itsdealer exemption for resale, andtax is due on the fair market value.

Example: Susan purchases a vehicle and titlesit in her name. The outstandingloan on the vehicle and is co-signed by Susan’s mother. At alater date, for insurance purposes,the vehicle is transferred fromSusan to Susan’s mother. A lienremains on the vehicle followingtransfer of title. Susan’s motherreceived the vehicle; however,Susan received nothing of value inreturn. There has been no newconsideration in support of thetransfer. No use tax is due.

Example: A vehicle is titled in the father’sname with a loan in the father’sname. The father transfers the titleto his child Jim, who assumes theunpaid balance of the loan. A newlien is filed. Use tax is due on theoutstanding loan balance.

Example: A vehicle is titled in the mother’sname with an outstanding loanbalance of $10,000. The mothertransfers the title to her son Alan.Alan takes out a $15,000 loan topay off his mother’s outstandingloan of $10,000 and have $5,000for repairs to his house. Use tax isdue only on the mother’soutstanding loan balance of$10,000.

TRANSFERS INVOLVING TRUSTSExample: Sam Spade, grantor, establishes a

living trust for the benefit ofhimself and his wife. Sam Spadetransfers all his property in thetrust, including his two vehicles.Since Sam Spade only transferredhis property into a living trust, noconsideration has occurred and nouse tax is due.

Example: Paul Brown, grantor, establishes atrust for his daughter. Pauldesignates his brother, Sam Brown,as trustee. Paul transfers a vehicleto the trust. Sam, as trustee, usesthe vehicle as a trade-in on a newervehicle for the trust. The trust payscash totaling $15,000 for the newvehicle. This scenario involves twotransactions. The first, from PaulBrown to the trust, is not subject touse tax because there was noconsideration to support thetransfer. The second transactionwas between the dealer and thetrust for the new vehicle. In thistransaction, $15,000 was given asconsideration for the new vehicleand use tax is due on the amount.

13IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #2CERTAIN NONPROFIT ORGANIZATIONS

f. Community mental health centersaccredited by the Iowa Department ofHuman Services under Iowa Codechapter 225c.

g. Nonprofit legal aid organizationsh. Nonprofit private museums if used for

educational, scientific, historicpreservation, or aesthetic purpose

i. Nonprofit hospitals licensed under IowaCode chapter 135B in which theproperty will be used in the operationof such hospital.

j. Free-standing nonprofit hospiceoperating under 42C.F.R., Ch. 16,§418.3 and the purchases are used inthe operation of the hospice program.

k. Statewide nonprofit organ procurementorganization as defined in Iowa Code§142C.2.

Exemption Authority:Iowa Code section 422.45(22)Iowa Code section 422.45(37)Iowa Code section 422.45(43)

Just because an organization is nonprofitdoes not mean it is automatically exempt frompaying use tax when purchasing a vehicle.

The purchase of vehicles by thefollowing types of nonprofit corporations areexempt if (1) the vehicle is purchased for useby the nonprofit organization and (2) it takestitle to the vehicle.

a. Community health centers as defined in42 USCA §254c.

b. Migrant health centers as defined in 42USCA §254b.

c. Residential care facilities andintermediate care facilities for thementally retarded and residential carefacilities for the mentally ill licensedby the Iowa Department of Healthunder Chapter 135C.

d. Residential facilities for mentallyretarded children licensed by the IowaDepartment of Human Services underIowa Code chapter 237.All residential facilities for child fostercare licensed by the Iowa Departmentof Human Services under Iowa Codechapter 237, other than thosemaintained by “individuals” as definedin Iowa Code subsection 237.1(7), areeligible for the exemption.

e. Rehabilitation facilities that provideaccredited rehabilitation services topersons with disabilities which areaccredited by the Iowa Commission onAccreditation of RehabilitationFacilities or the Accreditation Councilfor Services for Mentally Retarded andother developmentally disabledpersons and adult day care servicesapproved for reimbursement by theIowa Department of Human Services.

14IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #2 continuedPRIVATE NONPROFIT EDUCATIONAL INSTITUTIONSExemption from use tax on vehicles

subject to registration is provided to privatenonprofit educational institutions. Iowa Codesection 422.45(8) provides as follows:

“The gross receipts of all sales ofgoods, wares or merchandise, orservices used for educational purposesto any private nonprofit educationalinstitution in this state. The exemptionprovided by this subsection shall alsoapply to all sales of goods, wares ormerchandise, or services subject to usetax under the provisions of Iowa Codechapter 423.”

A private nonprofit educationalinstitution consists of a school, college, oruniversity with students, faculty, and anestablished curriculum, a group of qualifyingorganizations acting in concert, or libraries.Example: The purchase of a vehicle by a

church is subject to tax if registeredin the church’s name. However, if aparochial school operated by thechurch purchases a vehicle andregisters it in the name of theschool, the vehicle is exempt fromthe tax.

Exemption Authority:Iowa Code section 422.45(8)Iowa Code section 423.4.Department rule 701 IAC 32.2

15IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #2 continuedGOVERNMENT UNIT OR

QUALIFYING GOVERNMENTAL CORPORATIONWhen the purchaser of a vehicle subject

to registration is a governmental unit orcertain federal corporation, the vehicle isexempt from use tax.

Department rule 701 IAC 34.5(4)provides as follows:

“When vehicles are purchased by anyfederal or state governmental agency ortax certifying or tax levying body ofIowa or governmental subdivisionthereof. The exemption shall not applyto vehicles purchased or used inconnection with the operation of or by amunicipally-owned public utilityengaged in selling gas, electricity orheat to the general public and,therefore, shall be subject to use tax.”

Department rule 701 IAC 17.5 providesas follows:

“Receipts from the sale of tangiblepersonal property or from rendering,furnishing or providing taxable servicesto the American Red Cross, CoastGuard Auxiliary, Navy-Marine CorpsRelief Society, and USO shall be exemptfrom sales tax. Purchases made by theRed Cross, Coast Guard Auxiliary,Navy-Marine Corps Relief Society andUSO outside of Iowa for use in Iowashall be exempt from use tax.”

To claim the exemption, thegovernmental unit or qualifying governmentalcorporation must (1) pay for the vehicle and(2) take title to the vehicle.

Department rule 701 IAC 17.7enumerates some of the federal corporationsimmune from the imposition of sales and usetax in connection with their purchases:

1. Central Bank for Cooperatives andBanks for Cooperatives

2. Commodity Credit Corporation3. Farm Credit Banks4. Farmers Home Administration5. Federal Credit Unions6. Federal Crop Insurance

Corporation7. Federal Deposit Insurance

Corporation8. Federal Financing Bank9. Federal Home Loan Banks

10. Federal Intermediate Credit Banks11. Federal Land Banks and Federal

Land Bank Association12. Federal National Mortgage

Association13. Federal Reserve Bank14. Federal Savings and Loan

Insurance Corporation15. Production Credit Association16. Student Loan Marketing

Association17. Tennessee Valley Authority

The federal statutes creating the abovecorporations contain provisions substantiallyidentical with the “Federal Farm Loan Act,”section 26, which has been construed asbarring the imposition of state and local salestaxes.

Exemption Authority:Iowa Code section 423.4(4)Iowa Code section 422.45(5)Department rule 701 IAC 17.5Department rule 701 IAC 17.7Department rule 701 IAC 34.5(4)

16IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #3BUSINESS TRANSFERS

Department rule 701 IAC 34.5(9) andIowa Code section 423.4(9) provide anexemption from use tax for vehiclestransferred between certain businesses:

• A transfer from one corporation toanother corporation is a transfer fromone entity to another entity and is ataxable transaction, unless the transferis pursuant to a statutory merger.

• Vehicles transferred from a soleproprietorship or partnership to acorporation for the purpose ofcontinuing the business are exemptfrom tax.

Note: The exemption applies only if allof the stock of the corporation is owned bythe sole proprietor and spouse or by all thepartners if the business was a partnership.

This exemption is also applicable ifvehicles are transferred from a corporation oran LLC to a sole proprietorship or partnershipformed for the purpose of continuing thebusiness when carried on by the same personor persons who were stockholders of thecorporation.

This exemption contains the followingprovisions:

1. If the business transferring the vehicleis a sole proprietorship or partnership,the vehicle must be transferred to anew corporation or LLC. To constitutethe transfer of a vehicle to a newcorporation or LLC, the transfer mustoccur within 12 months from the dateof incorporation to be exempt.

2. The new corporation or LLC must havebeen formed for the purpose ofcontinuing the business of the soleproprietorship or partnership. Theactivities of the new corporation orLLC must be the same as the soleproprietorship or the partnership.

3. The new corporation or LLC must beowned 100 percent by the soleproprietor, the sole proprietor’s spouseor all the partners, in case of apartnership.

The vehicle subject to registration mustbe transferred from a business or individualconducting business in Iowa. Therefore, thevehicle must already be registered in Iowa.

The following are some examples of usetax applicability in various situationsinvolving the transfer of vehicles betweenbusinesses:

17IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

TRANSFERS TO NEW CORPORATIONSFROM PARTNERSHIPSExample: Greg, Janice and Gary are partners

in a retail business. All threepartners agree that the businessshould continue as a corporation.On January 2, 2000, the Articles ofIncorporation are filed with theSecretary of State. Over the courseof the next 12 months, vehiclespreviously used in the partnershipare transferred to the corporation.During this same 12-month period,Greg, Janice and Gary continue tobe the sole shareholders in thenewly-created corporation. No usetax is due.

TRANSFERS TO NEW CORPORATIONSFROM INDIVIDUALSExample: Shirley decides to open a floral

business. Shirley found a locationfor a shop and leased the premises,and purchased equipment andinventory. Prior to the scheduledopening of the shop, Shirleypurchased a van for use as adelivery van in the business. At thetime of purchase, use tax was paidon the van and it was titled in theShirley’s name. After purchasingthe van but prior to opening theshop, Shirley consulted an attorney,who advised her to form acorporation for the purpose ofconducting the floral businessrather than operating the businessas a sole proprietorship. Within afew weeks after the purchase of thevan, the Articles of Incorporationwere filed with the Secretary ofState. Upon incorporation, Shirleytransferred the van to thecorporation. There is no use taxdue.

TRANSFERS FROM A SOLEPROPRIETORSHIP TO ACORPORATIONExample: Bill forms a corporation in 1990. In

1994, he transfers an automobilethat is titled and registered in Bill’sname as a sole proprietor. Transfersmust take place within 12 monthsof incorporation to constitute atransfer to a “new” corporation tobe exempt. Therefore, use tax isimposed on the corporate bookvalue.

TRANSFERS TO A NEWCORPORATION WHEN OWNERSHIPDOES NOT REMAIN THE SAMEExample: Hank, Cecil and Marie are partners

in a partnership. The partnershipdecides to incorporate. At the timeof incorporation, Suzie joins thecorporation as a shareholder,thereby making all the shares in thecorporation owned by Hank, Cecil,Marie and Suzie. A motor vehicleowned by the old partnership hasan outstanding liability of $5,000.The outstanding loan balance istransferred to the new corporationwithin 12 months from the date ofincorporation. The corporation alsoassumes the outstanding liabilityon the vehicle. Since Suzie was notone of the original partners, use taxis imposed on the $5,000outstanding loan balance.

18IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

TRANSFERS UPON DISSOLUTIONWITH CONTINUATION OF THEBUSINESSExample: Sam is the sole stockholder in SAM

Corporation, which engages in thebusiness of plumbing repair. Samdecides to operate the business as asole proprietor. The SAMCorporation files a Statement ofIntent to Dissolve with the IowaSecretary of State. Upondissolution, the SAM Corporationtransfers title of a motor vehiclewith all other corporate assets tothe individual (Sam). Sam uses thisvehicle in the plumbing repairbusiness that he continues tooperate as a sole proprietor. Thereis no use tax liability. Since thetransfer from SAM Corporation toa sole proprietorship is for thepurpose of continuing the businessof the corporation and all thecorporate shareholders are the sameat the time of dissolution, no usetax is due.

TRANSFERS FROMCORPORATION TO STOCKHOLDERExample: John Doe owns 100% of John Doe

Inc. One of John Doe Inc. assets isa Rolls Royce and is carried on thecorporate books with a book valueof $75,000. John Doe Inc. transfersthe Rolls Royce to John Doe, 100%stockholder. Although John Doeowns 100% of John Doe Inc., JohnDoe only owns the corporation.John Doe Inc. owns the assets. Usetax is imposed on the $75,000.

TRANSFERS FROMCORPORATION TO CORPORATIONExample: GO Corporation owns three

vehicles: a truck, a car, and a newvan. The truck is fully depreciated;the car has a book value of $8,000,and the van a book value of$25,000 with an outstanding loanof $30,000. GO Corporation wantsto get rid of the three vehicles andtransfers the three vehicles to PICKCorporation. MAXI Corporationowns both the GO Corporation andPICK Corporation. No money isexchanged. Since the truck wasfully depreciated, use tax is due onthe fair market value. Use tax isdue on the car’s $8,000 book value.The van’s book value is $25,000;however, use tax is imposed on the$30,000 outstanding loan balance.

Exemption Authority:Iowa Code, Section 423.4(9)Department Rule 701 IAC 34.5(9)

19IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #4DEALERS

Persons licensed as dealers who purchasevehicles for resale are allowed an exemptionfrom use tax if licensed to sell that make ofvehicle.Example: Henry Ford is licensed as a

franchised Ford dealership. Anynew Ford make or model may bepurchased tax exempt if HenryFord has the vehicle in their resaleinventory.

Example: Henry Ford is a franchised Forddealership. A relative of the ownerof Henry Ford dealership wants topurchase a new Buick. The ownerof Henry Ford purchases a newBuick for his relative. Since HenryFord is not franchised to sellBuicks, his purchase is subject touse tax. The sale of the Buick to hisrelative is also subject to use tax.

Example: A Chevrolet dealer not licensed tosell new Fords registers a newFord. The dealer’s resaleexemption is not applicablebecause the dealer is not licensedto sell new Fords. Since the sale ofthat vehicle is not in the regularcourse of business, the dealer hasexercised “use” of the Ford andowes use tax at the time it isregistered.

Example: A Ford dealer purchases a Fordchassis with a manufacturer’s MSOstating it is a Ford. The chassis isthen used and is converted to aWinnebago. After completion ofthe conversion, the MSO isconverted to Winnebago. Uponcompleting the conversion, theFord dealer claims exemption fromtax at the time he registers thevehicle by claiming it is a Ford

product, which the dealer islicensed to sell. In this scenario,use tax is due on the vehicle at thetime the vehicle is registered andtitled by the dealer. A chassis is nota complete vehicle. At the time thevehicle is completed and the dealerseeks to title it, the vehicle is aWinnebago and the dealer is notauthorized to sell that type ofvehicle. Consequently, the dealer’sexemption based on his licensedoes not apply

PROMOTIONS AND RAFFLES(SEE EXEMPTION 1)

When a dealer provides a vehicle to begiven away as part of a promotion, the dealeris subject to tax on the vehicle based on thedealer’s cost of the vehicle, to be paid as partof the dealer’s periodic return. The dealer’sexemption does not apply because the vehiclewas purchased for resale and a sale of thevehicle did not occur. The recipient of thevehicle is not liable for tax.

If a dealer donates a vehicle to a charityfor a fund-raising raffle, the dealer does notpay use tax on the vehicle. Tangible personalproperty (including a vehicle) given as a prizein a licensed raffle is exempt. Neither thecharity, the raffle winner, nor the dealer isrequired to pay tax on the vehicle.

20IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPT DEALER USEA dealer that holds a proper dealer’s

license may register a vehicle free from usetax if the vehicle is held for resale at all times.To qualify a vehicle as “being held for resaleat all times,” all of the following criteria mustbe met:

1. The dealer must be licensed in Iowapursuant to Iowa Code chapter 322;

2. The “use” of the vehicle by the dealermust not constitute a taxable “sale”under Iowa Code section 423.1(5);

3. The dealer must keep the vehicle in itsinventory for sale at all times;

4. The person using the vehicle must beaware of and accept that the vehiclemay be sold at any time, resulting inthe vehicle being removed from thatperson’s possession at any given time;

5. The dealer permits the vehicle to beused without charge; and

6. The dealer does not title the vehicle inits name and only registers the vehiclewith “dealer plates.”

Note: It is the department’s position thattax is due on a dealer’s registration of avehicle. If the dealer states the vehicle is forresale at all times, the dealer may file a Claimfor Refund (IA 843) with the IowaDepartment of Revenue.

Persons having restricted licenses forselling repossessed vehicles and licensedwholesalers can purchase for resale under thedealer’s exemption.

Recyclers, if licensed, may purchaseparts and salvage title vehicles for resale.

If a dealership license expires and is notrenewed or the dealer license has beenrevoked, the dealer must title and register allthe vehicles in the dealership inventory. Usetax is due on the purchase price of eachvehicle by the dealer at the time of titling andregistration. However, if a dealer license issuspended, a dealer is not required to title orregister the vehicles in the dealer’s inventorysince a suspension is merely a temporaryinterruption in the dealership business. Thedealer’s exemption remains intact during theperiod of suspension.

Exemption Authority:Iowa Code Section 423.1(1)Department Rule 701 IAC 34.7

21IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #5VEHICLES PURCHASED FOR RENTAL OR LEASE

PURCHASED FOR RENTALIf a vehicle subject to registration is

purchased for rental, the vehicle is exemptfrom tax if both of the following conditionsexist:

1. The person must be regularly engagedin the business of renting vehicles andlicensed under Iowa Code chapter 322;and

2. The vehicle must be held for rental fora period of 120 days or more andactually rented for periods of 60 daysor less.

All rentals are subject to taxation underIowa Code chapter 422C.

PURCHASED FOR LEASEThe purchase of a vehicle that will be

subject to Iowa lease tax is exempt from usetax if all of the following criteria exist:

1. The vehicle is subject to registrationunder Iowa Code chapter 321; and

2. The vehicle has a gross vehicle weightrating of less than sixteen thousandpounds (16,000). (This excludesmotorcycles and motorized bicycles.);and

3. The vehicle is purchased for lease andtitled by a lessor licensed pursuant toIowa Code chapter 321F; and

4. The vehicle is leased for a period of 12months or longer; and

5. The lease of the vehicle is subject tomotor vehicle lease tax under IowaCode section 423.7A.

Exemption Authority:Iowa Code chapter 422CIowa Code section 423.4(14)Department Rule 701 IAC 34.10Department Rule 701 IAC 32.11

22IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #6INTERSTATE COMMERCE, LEASED VEHICLE

Motor trucks, truck tractors, roadtractors, trailers, or semi-trailers defined inIowa Code section 321.1, purchased for thepurpose of leasing, and then actually leasedfor use solely outside of Iowa (interstatecommerce) are exempt.

Note: Vehicles designed primarily forcarrying persons are not exempt. See 701 IAC32.9 and 34.5(8) and Iowa Code section423.4(7).

The Iowa Department of Revenue makesa distinction between a true lease and acontract to haul. While an agreement may be alease for I.C.C. purposes, this does not meanit is a lease for Iowa use tax purposes. A truelease exists when the owner (lessor) gives thelessee exclusive possession of the lessor’sproperty for a specified period. A contract tohaul exists when an owner contracts to do apiece of work while retaining control of thevehicle and methods of operation. A contractto haul is not a lease; therefore, the vehicle isnot exempt. Ballstadt v. Iowa Department ofRevenue, 368 N.W.2d 147 (Iowa 1985).

Example: ABC Leasing purchased a Fordcargo van for the purpose ofleasing it to Pop’s Trucking. Thelease agreement is for 36 months.Pop’s Trucking will pick upproperty from Iowa businesses tobe delivered out of state. Nodelivery in Iowa ever occurs. SincePop’s Trucking never uses the vanfor deliveries in Iowa, the van issolely used (100%) outside of Iowaand may be purchased exempt fromuse tax.

Example: ABC Leasing purchases a GMflatbed truck for the purpose ofleasing it to Get-Up-N-GoTrucking. The lease is for fivemonths. Get-Up-N-Go Truckingwill use the truck for deliveries outof state and in Iowa. Since somedeliveries occur in Iowa, the soleuse out-of-state requirement(100%) will not be met. ABCLeasing’s (lessor) purchase of theGM flatbed is subject to use tax.Note: Although a contract to haulmay not qualify for this exemption,they may qualify under Exemption#7.

Exemption Authority:Iowa Code, Section 423.4(7)Department Rule 701 IAC 32.9Department Rule 701 IAC 34.5(8)

23IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #7VEHICLES USED IN INTERSTATE COMMERCE

Vehicles (power units), trailers, andsemi-trailers that are registered or operatedunder Iowa Code chapter 326 are exempt fromuse tax if (1) they accrue at least 25% of theirmileage outside of Iowa; and (2) they areregistered for a gross weight of 13 tons(26,000 pounds) or more. Both conditionsmust be met to claim the exemption.

Periods for substantiating mileage by theIowa Department of Revenue are fiscal yearJuly 1-June 30, with the exception if theinitial registration period is a short year (lessthan 12 months). Mileage during that periodwill be totaled with the first full year forsubstantiation purposes (Department Rule 701IAC 32.4).

If a vehicle, trailer, or semi-trailer wasoriginally prorated, then fully registered withtraditional county plates, the exemptionapplies if the 25% mileage factor andregistered weight requirement are met.

The 25% out-of-state mileage factor mustbe maintained for the first four years ofoperation. If the mileage factor is not met foreach year of the 4-year period, tax is due andis imposed on book value or market value,whichever is less.Example: ABC Trucking purchased two semi-

tractors two years ago in August;mileage was prorated for that year.Twenty-five percent of the mileagefor each was out-of-state mileage.Two years later, ABC Truckingdecides to register with traditionalcounty plates one of the semi-tractors; it will be used only inIowa. ABC Trucking’s book valueis $60,000, and the market value is$75,000. The book value is lessthan the market value; use tax isimposed on the $60,000 bookvalue.

Example: Two years ago, ABC Truckingpurchased a power unit and a semi-trailer. Both the power unit andsemi-trailer were used in excess ofthe 25% mileage requirement andregistered prorate (more than26,000 pounds). This year, ABCTrucking decided to register withtraditional county plates the semi-trailer, instead of renewing theprorate registration. Although thesemi-trailer will be county plated,ABC Trucking will still use thesemi-trailer 25% outside of Iowa.The gross registered weight did notchange. Since both the 25%mileage factor and the 26,000pound registered weight factor aremet, no tax is due.

Example: Two years ago, ABC Truckingpurchased a power unit and a semi-trailer. Both the power unit andsemi-trailer were used in excess ofthe 25% mileage requirement andregistered prorate (more than26,000 pounds). This year, ABCTrucking decided to register withtraditional county plates the semi-trailer, instead of renewing theprorate registration. The semi-trailer will not be used 25% outsideof Iowa. The gross registeredweight did not change. Since bothfactors are not met and the 25%mileage factor was maintained forthe first four years, tax is due basedupon book value or market value,whichever is less.

Exemption Authority:Iowa Code, Section 423.4(10)Department Rule 701 IAC 32.4Department Rule 701 IAC 32.10Department Rule 701 IAC 33.6

24IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #8MANUFACTURED HOUSING AND MOBILE HOMES

Mobile homes are exempt from motorvehicle use tax if Iowa use tax has beenpreviously paid. (Department rule 701 IAC32.3). Mobile homes are taxed at 60% of thepurchase price. Tax on the mobile home is dueat the time it is registered. However, when amobile home becomes real property and thetitle to the mobile home is surrendered, norefund is allowed for the tax previously paid.Example: A new mobile home is purchased by

the State Conservation Commissionfor use at a state park. No tax ispaid at the time of initialregistration. This mobile home islater sold to Bill Smith, a residentof Iowa. Bill Smith titles themobile home in Iowa. Since Iowause tax was not paid by the StateConversation Commission, BillSmith owes use tax on 60% of hispurchase price.

Example: Hank Jones, resident of Nebraska,titles a mobile home in Nebraska.Hank Jones later moves to Iowaand titles the mobile home in Iowa.No use tax is due since Hank Jonesdid not purchase it for use in Iowa.(Use the move-in exemption.)Hank Jones later sells it to RichardSmith, a resident of Iowa. SinceIowa use tax has not beenpreviously paid, Richard Smithowes use tax on 60% of hispurchase price.

When tax is paid on a mobile home, theamount of tax paid should be entered on thetitle.

New mobile homes are taxed only on theportion of the cost of the mobile homeattributable to materials used in building themobile home. For purposes of this exemption,40% of the mobile home cost is attributable tolabor, so that mobile homes are to be taxed at60% of the purchase price. This exemptiondoes not apply to RVs and travel trailers,which are taxed at full value.

MOBILE HOME TRADE-INSIn order for a trade-in allowance to apply,

it must:a. be the type of property normally sold in

the regular course of the retailer’sbusiness and

b. be intended to be ultimately sold atretail or used to manufacture a likeitem.

When the traded mobile home isultimately sold, it will not be subject to usetax if the Iowa use tax has been previouslypaid.Example: A mobile home dealer receives from

the factory a new mobile home thathas a sales price of $40,000. Thedealer sells the mobile home toLarry and Lola Smith. Larry andLola Smith trade in their oldmobile home for $5,000. The usedmobile home has been previouslytitled in Iowa and use tax was paid.The dealer lists the trade-in forsale. Iowa use tax is computed asfollows:

Sales price ................... $40,000Less trade-in ................ $ 5,000Buyer’s price ............... $35,000Amount subject to tax . $21,000($35,000 X 60%)Use tax at 5% ................ $1,050($21,000 X 5%)

25IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

The trade-in allowance applies since thetraded-in mobile home will be ultimately soldat retail.Example: ABC Inc. is a dealer of mobile

homes. ABC Inc. sells a mobilehome to Larry and Lola Smith for$40,000 less the $5000 trade-in oftheir old mobile home. The usedmobile home has been previouslytitled in Iowa and use tax was paid.The mobile home will be retainedby the dealer as an office. The Iowause tax is computed as follows:

Sales price ................... $40,000Less trade-in ................ $ 5,000Buyer’s price ............... $35,000Amount subject to tax . $21,000($35,000 X 60%)Use tax at 5% ................ $1,050($21,000 X 5%)

The trade-in allowance does not applysince the traded-in mobile home will not besold at retail or used to manufacture a likeitem.

MANUFACTURED HOUSINGManufactured housing is subject to Iowa

use tax only on 60% of the purchase pricewhich is to be paid by the owner of the hometo the county treasurer. “Manufacturedhousing” is defined as housing which isfactory built to specifications required by 42U.S.C. section 5403, and must display a sealfrom the United States Department ofHousing and Urban Development. Typically, amanufactured home has the following threecharacteristics:

1. It is a structure built on a permanentchassis; and

2. It is transportable in one or moresections; and

3. It is designed to be used as a dwellingwith or without a permanentfoundation.

The tax is based on the installed purchaseprice. The incidence of the tax is on the ownerof the manufactured home and not the dealerwho sells the manufactured home.Example: Woods Home Sales sells a

manufactured housing to Kelvinand Renee Jones for $120,000,which includes placing themanufactured housing on afoundation. Kelvin and Renee takethe title to their county treasurer toconvert the title to real estate.Tax is figured as follows: 60% x$120,000 = $72,000 x 5% =$3,600.

Exemption Authority:Iowa Code section 423.4(11)Iowa Code section 234.4(12)Department rule 701 IAC 32.3Department rule 701 IAC 33.10

26IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #8INHERITANCE WITH AND WITHOUT A COURT ORDER

TRANSFER OF TITLETRANSFERS RESULTINGFROM COURT ORDERS

Court-ordered transfers of vehicles, suchas those arising as a result of probateadministration, divorce proceedings and othertypes of court orders, are exempt from tax.The vehicle must be transferred by court orderand not by mutual agreement of the parties.Example: John and Mary own a Ford Explorer

valued at $32,000 and a Chevroletvan valued $22,000. John and Maryget a divorce. In the divorcedegree, John receives the Chevroletvan and Mary receives the FordExplorer. No use tax is due.

Example: Mary and her husband John aredivorcing. Mary Jones owns a newCorvette. John Jones has aRockwell painting. Each areappraised at $80,000. Before thedivorce, Mary transfers title of theCorvette to John in exchange forthe Rockwell painting. Since thistransfer was not court ordered,Mary received consideration(Rockwell painting). John owes taxon the $80,000 Corvette.

Example: Pete Baker owns a motor homeworth $100,000. Pete passes awayand is survived by his two children.Pete Baker’s estate is worth$200,000. A court orders that it isto be divided equally between hisson and daughter. The son takes themotor home, and the daughter takesall other property. Since the sonreceived the motor home from hisdad’s estate, no use tax is due.

Note: The results would be thesame if Pete Baker did not have awill as long as there is a courtorder.

Example: Pete Baker owns a motor homeworth $100,000. Pete Baker passesaway and is survived by his twochildren. The only other property inPete’s estate is a $20,000 checkingaccount. His will gives his childrenall his property equally. A courtorder states that each child’s shareof the estate should be $60,000.The son wants the motor home andagrees to pay his sister $40,000 incash. His agreeing to pay her$40,000 constitutes consideration,and use tax is due on the $40,000.

TRANSFERS WITHOUT COURT ORDER(BY WILL AND INTESTATE)

Vehicles being titled as a result ofinheritance without a court order or a will areexempt from tax.

Department rule 701 IAC 34.5(6) readsas follows:

“When a vehicle subject to registrationis inherited, the county treasurer shallrequire the registrant to set forth thefacts before such exemption isgranted.”

Supporting documentation such as a copyof the will, death certificate, or a copy of theinheritance tax return may be requested at thediscretion of the county treasurer to supportthe exemption.

Exemption Authority:Department Rule 34.5(6)

27IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #8PURCHASED WITH NO INTENT

TO USE VEHICLE IN IOWAThe most common types of exemptions:

Nonresident move-inNonresident in transitTemporary use by a nonresident inIowaVehicles purchased in foreigncountries

PURCHASED IN FOREIGN COUNTRYIf a vehicle at the time of purchase was

not intended to be in used Iowa, but later theowner moves to Iowa, an exemption appliesand no use tax is due on the vehicle.Department Rule 34.5(7).

Department rule 701 IAC 34.5(7) statesan exemption shall apply:

“When an applicant for an Iowaregistration has moved from anotherstate with intent of changing residencyto Iowa and if the vehicle subject toregistration was purchased for use inthe state from which the applicantmoved and was not, at or near the timeof such purchase, purchased for use inIowa.”

Example: A soldier stationed in Germanypurchases, titles, and registers avehicle in Germany for traveling inGermany. At the time of purchase,the soldier has one year left on herservice assignment in Germany.After the one year, the soldier isreassigned to Iowa. The soldiertitles and registers the same vehiclein Iowa. Since the soldierpurchased the vehicle to travelGermany with no intent for use inIowa at the time of purchase, thenno use tax is due.

NONRESIDENT IN-TRANSITWhen a nonresident of Iowa purchases a

vehicle subject to registration and acquires anonresident in-transit registration, anexemption applies under department rule 701IAC 34.5(3).

This rule, 701 IAC 34.5(3) reads asfollows:

“When a nonresident of Iowa appliesfor a ‘nonresident-in-transit’registration for a motor vehiclepurchased in Iowa but which theperson intends to permanently registerin a state other than Iowa, theapplicant shall execute and file anaffidavit, in duplicate, with the officeissuing the registration establishingthis fact.”

NONRESIDENT MOVE-INIf a nonresident is registering a vehicle

purchased outside of Iowa, and thenonresident is bringing the vehicle into Iowafor personal use while in Iowa, the exemptionprovided in Iowa Code section 423.4(2)applies.

Iowa Code section 423.4(2) providesexemption for:

“All articles of tangible personalproperty brought into the state of Iowaby a nonresident individual thereof forthe individual’s use or enjoyment whilewithin the state.”

Example: Jim Strong, a resident of Illinois,purchases a new Lexus while livingin Illinois and employed withSpace Rocket Corporation. SpaceRocket Corp. transfers Jim Stormto the Space Rocket Corp. office inIowa. Jim Strong brings the Lexushe just purchased in Illinois to be

28IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

titled and registered in Iowa. SinceJim Strong was not aware of thepending transfer, the purchase ofthe Lexus was for use in Illinoisand no Iowa use tax is due on thevehicle.

DETERMINING USEThe determination of whether a vehicle

was purchased for use in a foreign country orpurchased for use in Iowa is a factualdetermination. In most instances, this appliesto military service personnel. In thesecircumstances, the following factors should beconsidered:

1. Length of time the person owned thevehicle prior to returning to Iowa. Ifthe vehicle was purchased early in theperson’s tour of service, it mightindicate the intent was to use thevehicle in the foreign country ratherthan Iowa. Conversely, if the vehiclewas purchased near the end of theperson’s tour of service, it mightindicate an intent to use in Iowa.

2. Registration in the foreign country.Registration of the vehicle for use inthe foreign country might indicate thatthe vehicle was purchased for use inthe foreign country rather than Iowa. Ifthe person did not register the vehiclein the foreign country, this lack ofregistration indicates that the vehiclewas purchased for use in Iowa.

3. Mileage documentation. If the personcan show thorough mileagedocumentation that substantial mileswere driven in the foreign country, itmight indicate an intent to use thevehicle in the foreign country ratherthan Iowa. Evidence of this intent iswhen the mileage incurred on thevehicle in the foreign country is morethan the mileage incurred on thevehicle in Iowa.

Example: A soldier purchases a vehicle whilestationed in Germany. The soldierwill ship the vehicle to his nextduty station. The soldier receiveshis orders; his next duty stationwill be Iowa. The vehicle isshipped to Iowa. When the soldierpurchased the vehicle, the soldierhad no intent to use the vehicle inGermany. Iowa use tax is imposedon the soldier’s purchase price(U.S. dollar and not the Germandollar).

Exemption Authority:Department rule 701 IAC 34.5(3)Department rule 701 IAC 34.5(7)Iowa Code section 423.4(2)

29IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #8OTHER

This category is for any exemptions notcovered by exemptions 1-7. If this “other”category is used, a full and detailedexplanation must be attached.

Note: Proper use of the “other” categoryincludes correction of title, qualifying sales toNative American Indians, salvage titles,returned vehicles, registration bymanufacturers, vehicles directly and primarilyused in recycling, or any miscellaneousexempt transaction.

“Directly and primarily used inrecycling” means that the vehicle is used morethan 50% of the time in the process ofobtaining waste to be remanufactured intoanother product.Example: Stan Perkins purchases a garbage

truck to be used primarily to collectbottles and transport them to abottle recycling plant. No tax isdue. However, if the garbage truckis primarily used to pick up bottlesto be taken to the landfill and notto be recycled, then the purchase ofthe truck is subject to Iowa tax.

30IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #8HOMEMADE VEHICLES

Homemade vehicles subject toregistration are exempt from use tax upon thefirst registration if sales or use tax was paidon the parts purchased at retail used to buildthe vehicle. If proof of the tax having beenpaid is not provided, the taxable price is fairmarket value.

Department rule 701 IAC 34.5(2) readsas follows:

“When the consumer applies forregistration of a ‘homemade vehiclesubject to registration’ built from partspurchased at retail, upon which theconsumer paid a tax to the seller, andnever before registered, the applicantshall execute and file an affidavit induplicate, establishing these facts withthe office issuing the registration. Theoriginal shall be forwarded to thedepartment along with the monthly

report; and the copy shall be retainedby the issuing office. The term‘homemade vehicle subject toregistration’ shall include such thingsas homemade automobiles, trucks,trailers, motorcycles and motorbikes,but shall not include those vehiclessubject to registration which are madeby a manufacturer engaged in thebusiness for the purpose of sales orrental.”

This rule is not applicable when ahomemade vehicle is being registered otherthan for the first registration.

A UT510 form must be filled out for allhomemade vehicle exemptions.

Exemption Authority:Department Rule 701 IAC 34.5(2)

31IOWA DEPARTMENT OF REVENUE 78-614 (3/3/04)

EXEMPTION #8TAX PAID TO ANOTHER STATE

When a vehicle is purchased in anotherstate for use in Iowa, credit can be allowed forstate tax paid to the other state. For the creditto apply, the person must show proof theywere legally required to pay a state sales tax, astate use/sales tax or a state occupational taxto the other state. Evidence of the paymentmay include purchase records, cancelledchecks, invoices or some form ofdocumentation by the other state. This wouldbe sufficient proof the tax was paid to theother state.

Iowa Code section 423.25 reads asfollows:

“If any person who causes tangiblepersonal property to be brought intothis state has already paid a tax inanother state in respect to the sale oruse of such property, or an occupationtax in respect thereto, in an amountless than the tax imposed by this title,the provisions of this title shall apply,but at a rate measured by thedifference only between the rate hereinfixed and the rate by which theprevious tax on the sale or use, or theoccupation tax, was computed. If suchtax imposed and paid in such otherstate is equal to or more than the taximposed by this title, then no tax shallbe due in this state on such personalproperty.”

Department rule 701 IAC 34.5(1) readsas follows:

“When the applicant for an Iowaregistration for a vehicle subject toregistration has paid to another state asales, use or occupational tax on thatunit, credit shall be allowed againstthe Iowa tax due in the amount paid.Credit shall not be allowed when suchtax is paid upon equipment rentalreceipts. If tax paid is equal to orgreater than the Iowa tax due, nofurther tax shall be collected. If taxpaid is less than the Iowa tax due, thedifference shall be collected by Iowa.”

Example: John and Angel Banks are Iowaresidents. While they were inNevada, they purchased a newcamper for $20,000. Nevada didnot required the Banks to pay astate sales, use, or occupationaltax. John and Angel Banks bringthe camper back to Iowa. Thecamper requires an Iowa title andregistration. Since no state sales,use, or occupational tax was paid tothe State of Nevada, Iowa use tax isdue on the purchase price of$20,000.

Example: John Henry is an Iowa resident andspends the winter months inFlorida. John decides to purchase anew Buick in Florida for $35,000from Florida Auto Sales. John isrequired to pay 5% Florida state