vaasaett world energy retail market rankings 2010

DESCRIPTION

The world's leading report on international switching rates, trends and analysis in competitive liberalised electricity and gas markets. Part of the VaasaETT Utility Customer Switching Research Project series. Main writer Dr Philip E Lewis of VaasaETT.TRANSCRIPT

www.utility-customer-switching.com

Editor and lead writer: Dr Philip E. Lewis

2010 VaasaETT World Energy Retail Market Rankings Report 2010 2

2009 was a year where global electricity customer switching activity reached new

boundaries. While New York and Texas eased off a little, Europe and Australia were

more active than ever before, continuing their growth in switching momentum.

Of the 33 markets followed by the VaasaETT Utility Customer Switching Research

project in 2009/2010, nine substantially increased their switching rates.

The global average switching rate for 2009 was 6.12%, around one percentage

point higher than two years ago.

Australia, and in particular Victoria, once again led the world in electricity

customer switching, increasing to record levels and establishing itself as the

example for others to follow.

For the first time since the start of global electricity market liberalization, Great

Britain (still a hot market) was knocked off the top spot in Europe, surprisingly by

Ireland, a former laggard in terms of customer switching.

In 2009, nearly 21% of all electricity customers in the Republic of Ireland switched

supplier, 2% more than in Great Britain. Between February 2009 and February

2010, Bord Gáis Energy won nearly 21% of the residential electricity market in

Ireland, by far the world’s most successful marketing campaign ever for an

electricity retailer, measured in terms of the percentage of residential customers

in the market who were won over a 12 month period.

For the first time social media marketing was shown to be a major trigger and

channel for utility customer switching.

Switching also increased in other medium activity markets, such as Finland and

Sweden as well as lower activity markets such as Italy, the Czech Republic,

France, Greece, Portugal and Slovenia.

in Austria, Germany, Belgium (Flanders, Wallonia and Brussels), Norway and the

Netherlands, switching trends were at similar or lower levels to 2008, limited in

part by reduced price volatility and a generally uneventful market.

Other markets remained dormant, for now, but the evidence shows a general

increase in the momentum of switching activity globally. The trend is typically

upward.

Active utility customer switching can no longer be considered an Anglo Saxon or

Nordic only phenomenon.

2009 Highlights - A Record Year for Customer Switching

2010 VaasaETT World Energy Retail Market Rankings Report 2010 3

Introducing the 2010 World Energy

Retail Market Rankings Report

The Fifth Edition of the VaasaETT World Energy Retail Market Rankings Report remains to this

day the only truly comparative global view of utility customer switching activity.

Drawn from the VaasaETT Utility Customer Switching Research Project (UCSRP), the most

comprehensive and uniform source of comparable switching statistics (past and present) in the

electricity and gas markets worldwide, this report is merely an overview of selected analysis that

has been collected by the UCSRP in 2010, combined with some additional analysis collected

during the past 14 years. If you would like to enquire about information from the UCSRP please

visit www.utility-customer-switching.com or contact us through any of our direct phone numbers

or email addresses listed at www.vaasaett.com/contact.

IMPORTANT NOTE: Please note that in this report we generally refer to energy Suppliers as

Retailers. Unless otherwise stated, statistics refer to electricity and to Aggregated (weighted

residential and I&C) data.

We encourage you to use tables, charts and other figures from this report in your own reports

and presentations providing they are unchanged and accompanied by full reference to the

VaasaETT World Energy Retail Market Rankings Report, or alternatively to www.VaasaETT.COM .

If you would like further usage rights, please contact [email protected]

CONTENTS

1. About the VaasaETT Global Energy Think-Tank 4-5

2. The Utility Customer Switching Research Project 6-10

3. 2009-2010 Switching Trends 10-13

4. Market Switching Reports 14-37

5. Little Bits

a. Switching Myths 26-27

b. The Importance of Timing 38

6. Authors and Sources 39-41

2010 VaasaETT World Energy Retail Market Rankings Report 2010 4

The VaasaETT Global Energy

Think-Tank

The VaasaETT Global Energy Think-Tank is a unique and

independent collaborative concept based on the

philosophy of mutuality. Through its network of thousands

of senior executives, officials, researchers and other

experts who are for the most part known and trusted

personally, the Think-Tank provides value-to-all by

combining an interactive Community and Collaborative

Projects. The Think-Tank focuses broadly on practical strategic business and market issues, as

well as envisioning state of the art innovations and developments. The VaasaETT Global Energy

Think Tank brings together utilities, authorities, universities, NGOs and other players in the

energy industry. More Information at www.vaasaett.com

The VaasaETT Global Energy Think-Tank offers knowledge sharing through its extensive online

knowledge centre, unique data sharing through various projects such as the Household Energy

Price Index for Europe and the Utility Customer Switching Research Project, networking

integration through its intimate high level events, the VaasaETT Community and world leading

round-tables and coalitions such as the Smart Energy Demand Coalition based in Brussels.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 5

The VaasaETT Global Energy Think-Tank also publishes an array of free reports, on its own or in

partnership with other organizations such as Capgemini, and its collaborative projects, such as

the renowned Respond 2010 smart metering and demand response project, incorporate the best

partner organizations and experts that the world has to offer.

This knowledge sharing, best practice identification and collaboration ultimately leads to

outstandingly innovative strategies, solutions, methodologies, tools and visions, such as the

Utility Churn Radar, the most advanced loyalty/disloyalty prediction tool available in the energy

utilities market, developed through 14 years of research and collaboration in over 35 liberalised

energy markets around the globe.

“VassaETT provided a concise and infomative report using primary and

secondary information to survey international energy markets. The depth of

content and speed of which the report was assimilated was remarkable and of

great value to us”

Pádraig Fleming, Head of Regulation, Bordgais, Ireland

2010 VaasaETT World Energy Retail Market Rankings Report 2010 6

The Utility Customer Switching research project (UCSRP),

founded jointly in 2004 by Dr Philip E. Lewis and Paul

Grey, monitors switch rates and trends in all fully liberalised

energy retail markets worldwide.

It was the first and remains to this day the only global view of

utility customer switching activity, as well as being the most

comprehensive and uniform source of comparable switching

statistics in the electricity and gas markets worldwide. For all

observed markets we have switch trend data since the time

those markets were fully liberalised until the present.

It also provides ever-increasing analysis of observed trends

and explanations for utility customer switching behavior.

Some of this information is provided free or through

subscription services to our network members, additional

insight is provided through client offerings.

More Information at:

www.utility-customer-switching.com

The Utility Customer

Switching Research Project

The Utility Customer Switching

Research Project is used

extensively around the global

utilities industry and in leading

reports such as the Capgemini

European Energy Market

Observatory

Project Scope Research, measure and compare customer switch rates

Historical customer switching trends and projections

Identify factors promoting and hindering competitive retail activity

Insights into successful customer acquisition and retention strategies

Customer switch rates as a benchmark for market success

Retail market share analysis

The UCSRP currently follows 37 liberalised electricity markets, many of which also have liberalised

gas markets. Both residential and I&C switch rates are covered separately, although publicly, only

aggregated switch rates are published. This year however, while Alberta was followed and

recorded, it was not included in the rankings due to data comparability issues.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 7

Why Measure Customer Switch Rates?

Customer switch rates are an important dimension of energy market competitiveness and have

the advantage of being objective, measurable and comparable between markets. Many energy

market commentators tend to focus on the wholesale aspects of the utility value chain as a

measure of restructured market success, such as generation sources, transmission

interconnections and wholesale market trading. The UCSRP contends that both retail and

wholesale markets must be successful for consumers to receive the full benefits of competition.

A Definition of Customer Switching

In January 2006 Dr Philip E. Lewis, in a report for the European Regulators Group for

Electricity and Gas (ERGEG) proposed a comprehensive definition of utility customer

switching which has been adopted by the CEER (Council of European Energy Regulators),

ERGEG and therefore the effectively the European Union:

Switching supplier is defined as “the action through which a customer changes supplier”.

More specifically: A switch is essentially seen as the free (by choice) movement of a

customer (defined in terms of an overall relationship or the supply points and quantity of

electricity or gas associated with the relationship) from one supplier to another. Switching

activity is defined as the number of switches in a given period of time.

A switch additionally includes: a) A re-switch: when a customer switches for the second or

subsequent time, even within the same measured period of time b) A switch -back: when a

customer switches back to his/her former or previous supplier. When a customer m oves, a

switch should only be recorded if a customer switches to a supplier other than the supplier

which is incumbent in the area where he/she is moving to. Theoretically, a switch should

NOT be recorded if the customer remains with the same supplier as before the move, but

for practicality this specification has been removed from the definition for this project and

from those of CEER and ERGEG. A change of tariff with the same retailer is not equivalent

to a switch (this exclusion extends to: changing to a new tariff; changing from a regulated

to a non-regulated tariff with the same supplier or a subsidiary of the same supplier).

Sources of Data

The Utility Customer Switching Research Project draws on more than 60 of the best sources for

data collection. These sources typically include national or regional regulators, system operators,

energy associations, meter registration organizations and statistical authorities.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 8

Levels of Activity

Taking account of the rapid growth in the number of competitive markets, and increasing

diversity of switching activity and market maturity, levels of switching are now divided into

six categories:

Super Hot Markets: A new category for the 2009 rankings. These are markets where

activity is (in the current year) over 20% and has been consistentl y at or above 20% for at

least three years. These are markets where high levels of switching and competition are an

inevitable reality of the market, where at least half of all customers have switched supplier.

These are the truly competitive markets where customers come first (or on a level par with

other key business objectives) and complacency leads to major losses of customers. Prices

may not be lower than in less active markets, nor may retailer image be higher, but a high

emphasis is placed on the development of long-term lifestyle and added value services.

Energy efficiency, smart home, demand response and other offerings are expected to

flourish in such markets, depending on regulatory and other market structure conditions.

Hot Markets: Annual switching is approximately 15% or higher. Typically, switching activity

is so intensive that competitive positioning becomes one of the utility’s most strategic

issues. Switching momentum is usually high, constant, needs little encouragement and

easily flares up.

Warm Active Markets: Annual switching is between 8.5% and 14%. Typically, switching

activity is sufficient that utilities risk losing significant numbers of customers if they do not

actively compete, or if they make loyalty-related errors. Switching momentum is significant

but less permanent and mainly related to occasional stimulants in the market, such as price

rises or profit announcements. While many utilities are far more customer focused,

traditional corporate attitudes and over-complacency often remain despite the looming

major threat facing revenues and customer profitability.

Active Markets: ek. Entry into this level of activity often acts as a wake-up call for utilities,

although for many it will not take place until at least the next level of switching activity.

Cool Active Markets: Annual switching is between 1% and 3.0%. Typically, switching is

noticeable and measurable, but insufficient to affect substantial change in the attitudes or

behaviour of utilities. Competition is barely visible and customer awareness poor. The

seeds of future activity may nevertheless already be sown.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 9

Dormant Markets: Annual switching is less than 1%. Typically, switching and competition

exist only in theory. The markets may be officially open to competition, and customers are

able to choose their supplier, but in practice only larger consumers are motivated or able

to do so, competitors may not be able to compete with the prices of incumbent utilities

(due to scale, access to energy or low-set regulated incumbent price issues) and in general

the market is likely to be inhibited by insufficient conditions for real competition. This is

not necessarily to say that competition cannot emerge, however, but regulators may need

to take action in order to break the deadlock.

Comparative Data

It should be noted that not all countries/markets collect or document data in a way that

corresponds to this definition. Through cooperation with our data sources and careful re-

calibration (where necessary) we are able to largely overcome these limitations, but some

markets are nevertheless unavoidably non-comparable (and therefore left out of the rankings),

and a margin of error is factored into all ranking comparisons.

Defining Fully Liberalised Markets

Full liberalisation (otherwise known as full retail competition or FRC) is when residential and I&C

(Industrial and Commercial) customers are all eligible to choose their energy (electricity and or

gas) retailer (otherwise known as supplier). In the Utility Customer Switching Research Project

Full Liberalization additionally refers to electricity or gas markets where end customers can

choose their retailer freely, where they have at least one alternative retailer realistically available

to them, and where switching supplier does not incur additional financial costs, reprisals from the

former utility/retailer, technical changes (such as the need for an additional meter), or other

unreasonable or excessive effort on the part of the customer. The dates when markets became

fully liberalised are given in the following timeline.

Switch Rate Metric

The UCSRP customer switching rate metric is calculated by dividing the number of customers

who switched suppliers in a given period by the total number of customers in the market, and the

result is then converted to an annual rate. For example, if one percent of customers switch

suppliers in a given month, that month would have a 12 percent annualised customer switch

rate. Similarly, where switching trend data is reported on a quarterly basis, the quarterly switch

percentage has been multiplied by four to derive the `annualised quarterly' switching rate.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 10

2009-2010 Switching Trends

Levels of Activity

2009 saw a steady increase in the number of active and highly active markets. All in all the

VaasaETT Utility Customer Switching Research Project recorded 23 active markets, compared to

13 dormant markets. Of the active markets five reached only Cool Active levels but a further 5

reached the Hot level of activity, a record number of markets.

For the first time, one market, namely Victoria, was so active that it reached a ‘Super Hot’ level

of activity, reflecting not only extreme levels of switching, but also an average switching level of

above 25% over the past three year period. This level of switching was well above that of any

other market.

It is also important to note that in 2009, the myth that switching is a Nordic or Anglo Saxon

phenomenon was exposed, with three non-Nordic or Anglo Saxon markets reaching annual levels

of switching above 10%, in addition to four other such markets in the Active category.

The Dormant markets were a mixed bunch, but apart from Spain, Portugal and Iceland, all

represented Eastern or South Eastern Europe.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 11

Dormant Markets

Lithuania

Slovakia

Bulgaria

Croatia

Hungary

Latvia

Romania

Luxembourg

Poland

Spain

Greece

Portugal

Iceland

Cool Active

Markets

New York

Austria

Czech Republic

Italy

France

Active Markets

Germany

Slovenia

Flanders

Brussels

Finland

Denmark

Warm Active

Markets

Norway

Wallonia

Sweden

New South Wales*

Netherlands

South Australia*

Hot Markets

New Zealand

Queensland*

Great Britain

Ireland

Texas

Super Hot Markets

Victoria*

Levels of Switching Activity 2009

The true extent of the variation in switching levels in only apparent when more switching

percentages are compared. The VaasaETT Utility Customer Switching Research Project precisely

and in great detail analyses these percentages, a simple summary of which is provided below. For

more detailed analysis please contact VaasaETT.

In the following chart it can be seen that despite the enormous variation in switching levels, there

is something of an evenness to the range of the spread, from markets with 20-26% annual

switching right down to those with 0%.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 12

The percentage of customers in these markets who have switched at least one likewise ranges

massively, from nearly 0% right up to over 60%. The higher the level of switching however, the

higher the amount of re-churn (customers who have switched more than once). In fact in the

most active markets, most customers who switch have switched from once to several times

before. Utility companies’ costs-to-serve are therefore increased, pushing profitability down.

Copyright 2010 VaasaETT

2010 VaasaETT World Energy Retail Market Rankings Report 2010 13

By looking at historical switching patterns (the VaasaETT Utility Customer Switching Research

Project has collected historical switching trends for all tracked markets since the onset of

competition in those markets) it can furthermore be seen that despite obvious differences

between market switch patterns, there are some statistically observable commonalities. For

instance, put simply all markets tend to follow common rules and dynamics relating to seasonal,

cyclical and other market variables. In general, markets furthermore tend to follow an upward

long-term trend.

Consequently switching trends can be predicted and leading markets explained.

Copyright 2010 VaasaETT

2010 VaasaETT World Energy Retail Market Rankings Report 2010 14

For electricity Victoria had by far the highest level of switching throughout 2009, but unlike the

other jurisdictions, saw a slight decline in the last two quarters of the year. According to the

2009/2010 VaasaETT ranking definition, only Victoria is a ‘Super Hot’ market in terms of

activity. The other Australian jurisdictions are ‘Hot’ or ‘Warm Active’.

Australia

Australia remains the most active country in the world

in terms of electricity and gas customer switching, but rates

differ greatly between jurisdictions.

For electricity a clear activity divide exists between the two most

active markets (Victoria and Queensland) and the less active

markets (South Australia and New South Wales), with Victoria

the clear leader overall. For gas, Victoria is out on its own. In fact in 2009 Victoria achieved the

highest levels of calendar year residential and aggregated* customer switching ever recorded

for an electricity or gas market, anywhere in the world**.

*Important Note: The following trends illustrate aggregated (residential plus commercial)

switch rates. All quarterly values have been annualized.

**In 2007 slightly higher rates were recorded in Victoria, but that was based on NEMMCO data,

which is believed to overstate switching levels by approximately 2-3% compared to Switchstats

Australia data (due to methodological and definitional differences). When this is taken into

account the 2009 Victoria switching levels are higher than the 2007 levels.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 15

In the Gas market, Victoria saw

switching rates consistently

between 25- 30% throughout

2009, around 15-20% higher

than the other jurisdictions.

While all jurisdictions are

therefore ‘Warm Active’ or

‘Hot’ according to VaasaETT

ranking definitions, only

Victoria is ‘Super Hot’.

“The (VaasaETT Switchstats Australia) figures show that Victorian energy consumers are

embracing retail choice, setting a global benchmark for competition among electricity and gas

companies,…Since electricity retail price competition was introduced in Victoria in 2002, over 60

per cent of the state's residential and small business energy customers have chosen to change

retailers…The switch has saved them between 5 to 10 per cent on their energy bills, Our

Government removed energy retail price caps for small businesses customers in 2008, and for

residential customers in 2009, and the decision has allowed Victorian energy consumers to choose

from an even wider range of energy price and service options. The figures released today show

the success of this competition, with Victorian households and businesses able to choose from

about a dozen electricity and gas retailers.”

Peter Batchelor , Energy and Resources Minister, Victorian Government,

Australia, May 2010

Commentary

2010 VaasaETT World Energy Retail Market Rankings Report 2010 16

Australia State-by-State

Victoria

Victoria’s “Super Hot” ranking continues the pattern of it being Australia’s most active state

market. The record customer switching in 2009 owes much to the decision of the State

Government to phase out retail price regulation from 1 January that year. Regulation was

replaced by a regime of price monitoring by the Essential Services Commission of Victoria (ESCV),

which involves all retailers actively selling to small customers, of which there are fourteen, having

default tariffs listed and compared on the regulator’s web-site.

With other Australian states yet to follow the Victorians in removing price regulation retailers

upped their marketing efforts in the state and the pursuit of customers became even more

intense than in previous years. Use of door to door strategies was extensive and with marketing

occurring against the backdrop of a possible domestic emissions trading scheme, consumers were

perhaps more engaged on energy matters than usual.

It is likely that high levels of activity will continue in the current year as there are limited

prospects for price deregulation in other states, and the failure to pass the proposed emissions

trading scheme means that wholesale energy prices should remain fairly stable.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 17

South Australia

What had traditionally been Australia’s second “hot” market came off the boil in 2009. While

activity is still apparent new entrant retailers are shunning the market in the belief that its high

summer “peaks” and lack of wholesale market liquidity are significant barriers to entry. There is

also a view that the current regulated tariffs in the state provide limited “headroom”. Switching

that did occur in 2009 was largely between the retailers with an established presence in South

Australia, most of whom have generation cover in the state.

The independent review and rule setting body, the Australian Energy Markets Commission

(AEMC), had found in 2008 that the South Australian market was “effectively competitive” and

that price regulation should be removed. The incumbent state government chose to reject that

recommendation in the lead up to a state election in 2010. Unless that decision is revisited and

prices are deregulated it seems unlikely the South Australian market will return to its “hot” status

in the near term.

Queensland

Since being opened up to full contestability on 1 July, 2007 the Queensland market has been on

somewhat of a rollercoaster ride. When one looks at Queensland, it really should be considered

as two markets, the largely urbanised south-east corner of the state and the extensive regional

and rural areas north of the Sunshine Coast.

With its price regulation policy the State Government maintains a “maximum uniform tariff” for

all consumers regardless of where they live. To do so in regional areas requires a government

Community Service Obligation (CSO) payment, which is payable only to consumers serviced by

the incumbent government owned retailer for those areas. Customers who move away from the

incumbent retailer lose the CSO and therefore competing providers are unable to offer a more

attractive product, making switching almost non-existent outside the south-east corner.

In the south-east customer switching was particularly high in the year after full contestability

began, which also coincided with the privatisation of the government owned retailers in that part

of the state. New entrant retailers were therefore competing against new incumbents without

brand loyalty so activity was high and “headroom” was allowed for in the initial regulated tariff

decision. After a consumer backlash about price increases and some service issues, the state

government began interfering in pricing decisions from mid 2008 and the squeezing of margin

and regulatory risk led to a downscaling of activity. The pick-up in switching to ‘Hot’ in the second

half of 2009 indicates “headroom” is returning to the market although new entrants remain wary

of the regulated price setting process.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 18

New South Wales

New South Wales continued to exhibit moderate levels of customer switching in 2009, although

largely between the incumbent government owned electricity retailers and existing gas retailer.

The level of “headroom” in the regulated tariff and the high level of public ownership of the

energy industry continued to keep private new entrant retailers out of the market. Ongoing

uncertainty about a drawn out privatisation policy of the state government, which will shape the

market structure in both retailing and generation, has also

impacted on the willingness of new players to enter New

South Wales.

Until the ownership and market structure issues are

resolved, it is unlikely NSW will see a significant pick-up in

customer switching. On the positive side a controversial

2010 three year price determination may have improved the

outlook for “headroom” and could make consumers more

active in seeking out market contracts.

Some keys to success in the Australian market

have included clear, simple, hassle free

marketing and sign-up processes, lifestyle

focused incentives and products by multiple

competing newcomers, as well as excellent

price comparison and switching web sites

including SwitchWise and others.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 19

“The success of Australian Power & Gas has been around understanding

that within the Australian market customer acquisition has been primarily

a marketing channel strategy plan rather than a product play. What that means is that in our

market most customers are not self seeking a

better energy offer but will respond to one when it

is put to them directly. Therefore most energy

sales at a residential level are made directly by a

cold call either through door to door or

telemarketing.

The core strength of APG has been to build its outsourced relationships in particular with the

Cobra Group who are one of the world’s biggest

direct sales companies to sell for APG. Cobra

were incentivised to come with a smaller retailer

initially as they were able to earn equity into APG

as their success grew. Cobra now has about a

20% ownership of the company and is very

aligned as our success grows so does their wealth

as shareholders.

Secondly we then diversified away from a singular channel to where we now have 2 direct sales

companies, we tele-market are part of a home movers channel where people get their utilities

moved for them when they

move house and we are

using internet switching

which is continuing to grow.

As with the UK we believe

this channel will continue to

increase as energy prices rise

in Australia.”

James Myatt, CEO,

Australian Power &

Gas

CASE STUDY

Australian Power & Gas has been named

the fastest growing company in Australia

by Business Review Weekly Magazine with

1,300% growth in the last 3 years.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 20

SwitchStats Australia

The Switchstats Australia Scheme is a collaboration between

the VaasaETT Global Energy Think-Tank and 10 Australian

energy retailers representing over 80% of electricity customers

and 90% of gas customers in Victoria, New South Wales,

Queensland and South Australia. The collaboration is conducted

in partnership with the Energy Retailers Association of Australia

(ERAA)

VaasaETT collects switch data directly from the retailers,

according to a strict and consistent methodology and definition,

in compliance with the same definition used with the Utility

Customer Switching Research Project. This is based on the same

definition (by Dr Philip E. Lewis) used by the European Union

regulators, and therefore allows direct

comparison against switching data from all

European markets as well as fully liberalized

markets in the USA and Canada.

For more information on members,,

methodologies and definitions, please contact

Dr Philip E. Lewis at

Members of

SwitchStats Australia

Australia Power & Gas

Momentum Energy

Energy Australia

Simply Energy

Victoria Electricity

Country Energy

Integral Energy

Origin

AGL

TRU

Note: Victoria Electricity

Includes Victoria Electricity,

South Australia Electricity,

Queensland Electricity, New

South Wales Electricity.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 21

Republic of Ireland

The Republic of Ireland (referred to here as Ireland) electricity market has been open

to competition for larger businesses since February 2000 and has been fully open to

competition in all market segments since 2005, but it was only in 2009, with the arrival of

two key new entrants in February 2009, Bord Gáis Energy (the Incumbent Irish Gas Provider) and

Airtricity, that the residential market became active, resulting in the electricity incumbent ESB

losing large numbers of retail customers.

After the initial wave of switching activity among larger energy users following market opening in

2000, there was a slow but steady level of switching only within business markets with the ESB

losing approximately 4% of business consumption per annum during the period 2002-2008. Both

Bord Gáis Energy and Airtricity had both been active in this business market for a number of

years but had only built up relatively small (yet nevertheless significant customer bases), mainly

in the SME markets.

The entry of Bord Gáis Energy and Airtricity into the domestic market in 2009 howevver,

transformed the competitive landscape not only in the domestic market, but also in the business

market where it has had a major knock-on effect on business awareness of supplier switching

options.

Record Irish Switching in 2009-2010

Between February 2009 and 2010, Bord Gáis Energy won

nearly 21% of the occupied residential electricity market in

the Republic of Ireland. This Bord Gáis Energy campaign

has in fact been by far the world’s most successful

marketing campaign ever for an electricity retailer, if

measured in terms of the percentage of residential

customers in the market who were won over a 12 month

period.

Only five national markets have ever managed a (calendar)

yearly level of switching above 20% (the Australian markets

of Victoria, Queensland and South Australia, plus Great

Britain and New Zealand). Prior to 2009, the highest

national switch rate ever recorded for a 12 month period

was 28.33% in Victoria, Australia, between the 4th Quarter

2006 and 3rd Quarter 2007, and that switch level was

shared between competitors in the market.

The Irish Experience is

additional proof that there is

no such thing as a safe

customer for incumbent

energy companies. Markets

that are uncompetitive now,

can become active very

quickly if the conditions are

right. In the coming few

years it is predicted that

similar the experiences will

happen in other markets

around Europe and

elsewhere, especially since

evidence indicates that once

truly active, such markets

tend to remain active.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 22

Bord Gáis Energy are though not the only energy company in Ireland that has won customers

from the incumbent. Airtricity has also won significant numbers of residential customers, and

additional new entrants into the market are now a possibility since the market has shifted from

near inactivity just over a year ago, to being one of the most active electricity markets in the

world.

It remains to be seen if there is yet enough long-term momentum in the market to sustain this

level of activity, but the high rate of switching has continued from 2009 into 2010 with over

30,000 switches every month in the domestic market, approximately 1.5% of the total domestic

market.

Why the change in fortunes ?

The main reason for this extraordinary level of customer switching has arguably been price

margins at a time of economic downturn in Ireland. Price margins were achieved through a

combination of regulatory price controls placed on the incumbent ESB (ESB was not allowed by

the regulator CER to lower its regulated standard prices in the face of lowered price offerings

from the new entrants) and happenings in the wholesale market. More specifically, the lower

new entrant prices were facilitated by the softening of the wholesale market in 2008 and 2009 in

the context of former extensive high cost forward hedging by the incumbent at a time of very

high fuel prices.

The ’clever’ or ’fortunate’ purchasing strategies of Bord Gáis Energy in particular and Airtricity,

combined with the ’price-to-beat’ price regulations of CER therefore enabled the new entrants to

offer significant discounts ranging from a minimum of 5% on the incumbent’s regulated tariffs up

to 14% depending on payment options and dual fuel discounts.

One should not underplay the significance of marketing on Irish switching levels however. Energy

companies typically fail to achieve sufficiently simple, clear and appealing campaigns. Energy may

seem like a simple product to sell but few companies have ever managed to win many customers

in this market. Ireland’s outstanding marketing has made the difference. Nicky Doran, Head of

Marketing at Bord Gáis Energy states that the success of the campaign was down to a number of

factors, “the right price point, the simplicity of the message and great creativeness were all major

factors in the success of the campaign” according to Doran. Furthermore Doran states that “The

web has proved to play a huge part in the success of the campaign with as many as 30% of

customers switching on our micro site thebigswitch.ie”. The advertising campaigns of the new

entrants have been very effective in communicating the message that significant savings were to

be made through engaging in a simple, pain-free switching process, and that the reliability of the

service offered would not be affected by switching. Most significant though was the extensive

role of social media, the first time this has been proven to have won large numbers of customers

within competitive electricity markets.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 23

Most significantly Bord Gais Energy launched, ‘The Big Switch’ campaign which has had a high-

profile media presence across all major forms of advertising in 2009 and 2010. Airtricity has

followed suit and this has undoubtedly raised awareness of switching and created a momentum

which has continued unabated to date. The simplicity of the industry switching process has also

been key to this success.

The Significance of Regulation

Nowhere else has switching been influenced more by regulation than in Ireland, but in response

to these changing competitive conditions, the CER published its consultation on a ‘Roadmap’ to

deregulation in December 2009. This document set out the competitive milestones that would

signal the end to regulated prices in the Irish retail market. The CER reviewed the relevant

markets; domestic, small and medium businesses and large industrial & commercial customers

and concluded that all three business markets are sufficiently competitive to allow for the

complete removal of regulated prices. Unregulated competitors currently account for more than

half of business market consumption and therefore ESB Customer Supply was freed to compete

in business segments from 1st October 2010. They will be free to compete in the domestic market

as soon as it has lowered its domestic market share to no more than 60%.

Regulatory support for competition will not end there, however. As part of the broader retail

market workstream, The CER plans to continue to take measures to sustain and potentially

improve upon the high rate of customer switching in the Irish market, focusing especially upon

improving general customer awareness and price transparency as well as encouraging active

market participation across all market sectors.

Social media marketing

has been a key to the

Irish Switching

Phenomenon

2010 VaasaETT World Energy Retail Market Rankings Report 2010 24

Great Britain Great Britain was Europe’s second most active market in 2009, supported once

again by for example, aggressive and effective marketing, significant retail margins,

high levels of customer awareness, powerful online switching and comparison

services, active media and retail price volatility. The element of recession also appears to

have played a supportive role.

The continued activity of the Great Britain market, having remained highly active for over 11

years, is testament to the switching momentum that can develop in competitive electricity

markets. Although 2009 saw a general easing off of electricity tariffs switching remained the 3rd

highest in the world. Some of this activity was however a delayed response to large gas and

electricity price increases in 2008 as well as increasing public annoyance at what is seen as unfair

growing price margins of retailers, especially for gas where wholesale prices have fallen far more

sharply than retail prices.

In a market where the majority of switching for the past 13 years appears to have been directly

or indirectly the result of perceptions of price increases, margins and profits, it is both ironic and

paradoxical that one of the world’s highest levels of switching still exists in parallel with some of

Europe’s highest gross retail margins and costs-to-serve. It is not illogical though, that high levels

of competition appear to have left relatively large margins intact, since retail margins facilitate

price savings, encourage customer focus/acquisition/retention and give retailers a reason to stay

in the market.

Source: Household Energy Price Index for Europe 2010 (HEPI), E-

Control and VaasaETT, 2010 http://www.vaasaett.com/projects/hepi/

2010 VaasaETT World Energy Retail Market Rankings Report 2010 25

At the same time the high levels

of switching heavily increase

cost-to-serve through costs

associated with winning,

switching and retaining

customers. Churn is an expensive

business and who wants to be in

a business with low margins?

What is perhaps surprising

however, is that after nearly 13

years of such high levels of

competition, and apparently

strong handed regulation,

utilities in Great Britain

appeared in 2009 to generally still

be publicly heavily criticsised,

average gross margins rose

temporarily to extreme levels and

utility profit increases followed. Under such circumstances, it is perhaps easy to see why skeptic

onlookers may view the energy industry in Great Britain as non-competitive, even anti-

competitive or monopolistic, despite its high levels of switching and relatively high levels of

customer focus.

It is interesting therefore to note that, finally, after 13 years of full liberalization, in 2010 British

utilities have begun to move away from the tradition of competing over price and ‘service’,

towards a new paradigm of competition through partnership with the customers. The imminence

of mandated smart meter rollout throughout Great Britain has been preceded by attempts by

utilities to build closer relationships with customers.

A number of the leading retailers in particular for instance are now offering customers in-home

feedback displays to assist them to save energy and therefore money. These offerings are

accompanied by energy savings advice, associated tariffs and even (in at least one case) the

ability to remotely turn off devices to save money. Not only do such offerings help customers to

save money in other ways than switching supplier (potentially avoiding the need to change

supplier to ensure a good deal), but they also build a more mutual relationship with the

customer, to some extent may tie in the customers, and may go some way to reversing the

negative images associated with the utilities and the energy industry. In the longer-term they

may also enable more advanced revenue generating or cost-reducing offerings to the mass

market.

Source: Office for National Statistics/Bloomberg

2010, Chart produced and published by BBC:

www.bbc.co.uk.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 26

Switching Myths

Research over the years has revealed a myriad of myths associated with utility

customer switching: That customers need large savings to switch retailers, that

satisfaction and loyalty are closely correlated, that energy is necessarily boring,

that energy needs to be interesting for customers to switch retailer. The list goes

on and on. In this edition of the world energy retail market rankings we bring

your attention to just two myths: that switching process speed and the number of contracts a

customer has to sign correlate with national switching levels.

Regarding the relationship between the time taken to switch suppliers and the level of switching,

the following graph indicates that not only is such a relationship at best weak, but that there is

probably no significant relationship at all. While retailers may find less profitability in a market

where switching is more complex and thus more expensive, customers generally have no idea

how long it will take to switch when they decide to do so, and for the most part they do not care.

What appears to matter most to customers is that from their point of view the switching process

is smooth, simple and predictable. As long as they know it will take a month, then that is rarely a

problem for them, as long as they know it is happening. They are not excitedly waiting for

something to happen.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 27

Regarding the relationship between the number of contracts a customer has to sign

if they switch retailers, the following chart concerning electricity, supported also by

survey data, clearly reveals that in Europe at least, as elsewhere, there is no sign of

any impact of the number of contracts.

For sure customers would prefer to have just one contract, and thus one bill relating

to the supply of electricity or gas. At present for instance in Sweden, Norway and

typically also Finland, customers who switch retailers will end up with two regular

bills for electricity instead of one, one bill for distribution and one for the electricity commodity.

The distribution bill will be sent by the distribution company and the electricity commodity bill

will be sent by the retailer.

Interestingly Great Britain and France both have one bill, yet Great Britain is highly active and

France is not. Sweden has two bills and is a Warm Active market, yet Austria and Greece which

have one bill are not very active. This would indicate at least that having one bill is not a pre-

requisite for an active market, even though it is desirable from the customer’s perspective. Nor

are two bills a major deterrent to switching even though customers who find out about having

two bills once they have already switched are sometimes disappointed.

A single biller regime can therefore be seen as a preferred market characteristic, but not one of

the more important determinants of an active electricity market.

Source: VaasaETT

& Capgemini

2010 VaasaETT World Energy Retail Market Rankings Report 2010 28

The Netherlands The Netherlands was a Warm Active market in 2009, standing 8th in the rankings,

with stabilization in its switching trend at around 11% per annum. The outlook

for switching was however downgraded in Autumn 2009 following the

introduction of a 'do not call me - register' and an apparent consumer tiring of direct marketing

coinciding with reduced (survey) stated intentions to switch. The consequence of the ‘don’t call

me register’ is thought that once a customer has registered himself, retailers are forbidden to

call them. For retailers, canvassing via telephone was formerly by far the most significant

channel of customer acquisition.

Typical of more active and mature liberalised electricity markets, this is a year-on-year slight

decrease in the number of customers switching away from their incumbents to one of the

newcomers in the market. This is not a sign of slowing competition, but a reflection of the

maturity of the market (the lower hanging fruit have already dropped) and the fact that more

and more customers are now switching between retailers for the second or successive time. To

date, almost one third of the residential customers in the Netherlands have switched at least

once and (once again in line with other active markets) customers who have switched at least

once have a higher than average intention to switch in the future.

The level of activity in the Netherlands is though somewhat masked by the significant number

of customers renegotiating their contract with their own retailer. These customers do not

actually switch retailers, but do switch contracts.

Copyright 2010 VaasaETT

2010 VaasaETT World Energy Retail Market Rankings Report 2010 29

Sweden Sweden was 10th in the 2009 rankings,

and a Warm Active Market, where as of

January 2010 approximately 75% of

customers had either switched retailers or at least

switched contracts with their incumbent, around

9% higher than the previous year. A total of almost

1.8 million domestic customers (40% of the total

number of such customers in the Swedish

electricity market) either switched suppliers or

changed contracts with their existing one.

The increased activity is considered to be a reflection of Customers moving away from standard

price contracts to the preferred variable contracts. In December 2009, for the first time ever,

variable-price contracts were the most common type of supply contract among Swedish

households with 30% of customers on variable-price contracts as opposed to 22% in December

2008. Activity is also supported by the Energy Markets Inspectorate’s independent, web-based

price comparison site Elpriskollen, which brings together prices and terms and conditions for all

Swedish electricity supply companies in order to facilitate the choice by consumers of the

supplier that best suits them.

It should be noted however, that the ability for Swedish electricity customers to request and

receive personal improved contract offers from their existing retailers, may be seen as a barrier

to more intensive competition rather than an illustration of it. As in other parts of the Nordic

region, retailers can offer lower prices to their customers who request offers, than to those who

do not (termed price-matching). This cherry picking means that incumbent retailers can subsidise

their competitiveness to active and valuable (preferred) customers using margins from their less

active incumbent customers. This extends their already significant home advantage against

newcomers and neutralises much customer switching that would have occurred if price-matching

was not allowed (price matching for instance does not occur in Australia or Great Britain for

instance).

Of course it can be argued that does this matter, well it does matter because it prevents greater

switching momentum in the market (essential for more newcomer competition), and since prices

do not have to be as low to keep customers as to win them, the customer may end up with a

worse price than if they had switched retailers. Incumbent retailers therefore retain most of their

customers and most of their original market power, and true competition is killed off before it

can even truly begin.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 30

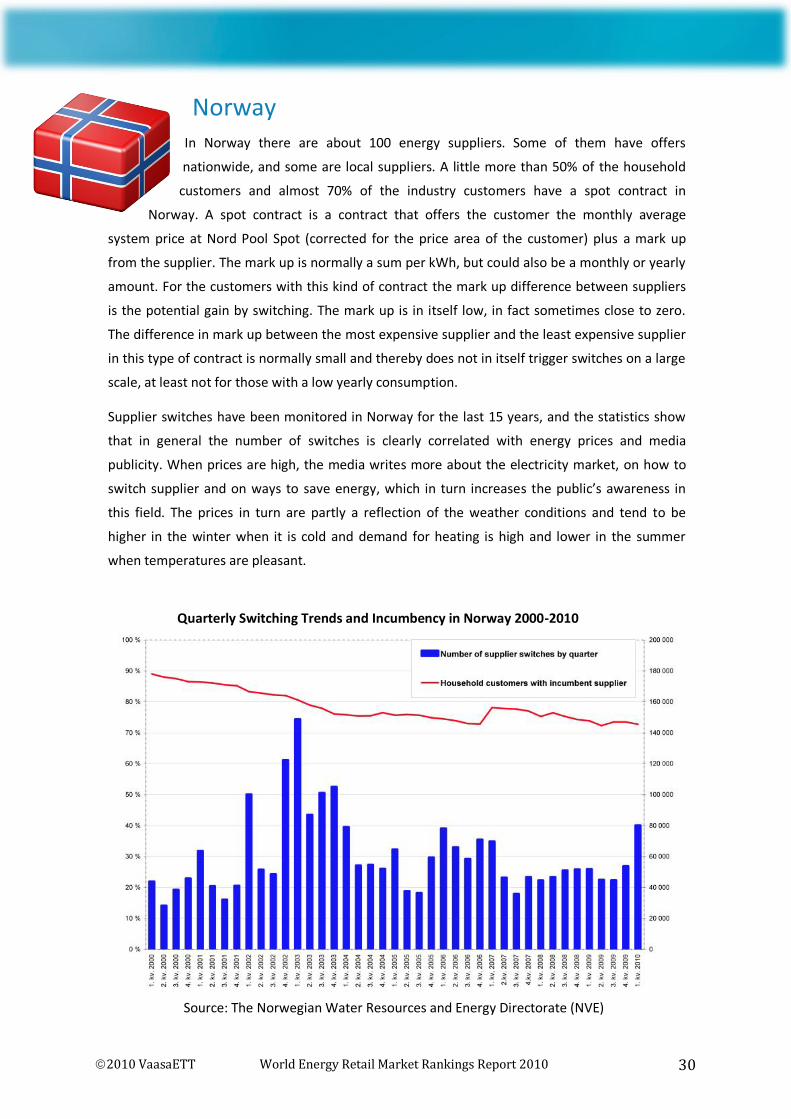

Norway In Norway there are about 100 energy suppliers. Some of them have offers

nationwide, and some are local suppliers. A little more than 50% of the household

customers and almost 70% of the industry customers have a spot contract in

Norway. A spot contract is a contract that offers the customer the monthly average

system price at Nord Pool Spot (corrected for the price area of the customer) plus a mark up

from the supplier. The mark up is normally a sum per kWh, but could also be a monthly or yearly

amount. For the customers with this kind of contract the mark up difference between suppliers

is the potential gain by switching. The mark up is in itself low, in fact sometimes close to zero.

The difference in mark up between the most expensive supplier and the least expensive supplier

in this type of contract is normally small and thereby does not in itself trigger switches on a large

scale, at least not for those with a low yearly consumption.

Supplier switches have been monitored in Norway for the last 15 years, and the statistics show

that in general the number of switches is clearly correlated with energy prices and media

publicity. When prices are high, the media writes more about the electricity market, on how to

switch supplier and on ways to save energy, which in turn increases the public’s awareness in

this field. The prices in turn are partly a reflection of the weather conditions and tend to be

higher in the winter when it is cold and demand for heating is high and lower in the summer

when temperatures are pleasant.

Source: The Norwegian Water Resources and Energy Directorate (NVE)

Quarterly Switching Trends and Incumbency in Norway 2000-2010

2010 VaasaETT World Energy Retail Market Rankings Report 2010 31

Supplier switching trends behaved typically in 2009, with the highest levels in the first and last

quarter of the year (incidentally similar to most other European energy markets). Switching levels

were also similar to previous years with 195 250 household market switches and about 24 700

I&C switches, representing 8.1% and 7.9% of the market respectively. These numbers were

unremarkable in part because there were no sustained periods of extreme prices, but also

because the Norwegian electricity market appears to have somewhat matured and stabilised

within the Warm Active switching level category. Only in periods of relatively very high energy

prices do switching rates substantially increase beyond typical levels.

This stabilisation could be partly explained by the fact that the margins of energy retailers are low

and so the differences in prices between the retailers are not big enough to motivate the

customer to switch. Some customers also have other preferences than prices when choosing a

retailer, for instance supporting local initiatives or retaining familiarity or peace of mind.

Because of many factors including relative price volatility, fast and simple switching procedures

with no economic costs for the customer, and relatively high levels of customer awareness,

Norway has for over a decade been one of Europe’s most active energy markets in terms of

customer switching. Nevertheless the majority of customers in Norway tend to stay with or

return to their local supplier, even if that supplier is not the cheapest one. In fact around 70% of

household customers and 65% of I&C customers still have a contract with the retailer connected

with the local DSO.

Norway could therefore be described as a relatively mature, moderately active, low margin

market with volatile tendancies, where incumbents remain dominant and most customers

remain loyal , but those who switch tend to be habitual switchers.

Denmark Denmark was an emerging market in 2009. Although still only 6.3% of electricity

customers switched retailers, this was approximately twice the previous highest ever

recorded level of activity (recorded in 2008), and it brings Denmark very near the border

with the Warm Active markets category. The main reasons for this activity was the increased

marketing activity of new entrants combined with increased customer elasticity resulting from

the effects of the recession. Switching has not been very evenly spread around the market

however, with some of the more local players experiencing much lower levels of switching.

Switching levels appear however to be even higher in 2010 than in 2009.

As in other Nordic markets, many customers (2.5% in the case of Denmark) instead negotiated or

received better contracts from their existing retailer, thus reducing the potential for genuine

switching activity, but competition has apparently led to an emerging interest in additional

competitive offerings such as home smart meter based energy feedback and the development of

forthcoming home energy management and smart home services.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 32

Nordic Switching Determinants

Research conducted by VaasaETT in collaboration with he Central Research Institute of the

Electric Power industry of Japan (CRIEPI) in 2009, indicates that switching in the Nordic markets

is primarily influenced by a number of key drivers. In the following table, the degree to which

each market conforms to each criteria is defined by the numbers in the columns, ranging from

1 to 4 (where 4 indicates the highest and 1 the lowest degree of confirmation). By averaging the

numbers for each market it is possible to then consider the overall switching propensity of each

market. Analysis found that the relative propensities of the four markets closely reflected the

relative observed switching levels in each market, indicating the importance of the selected

switching variables.

The Churn Radar

Through extensive analysis such as this and much more, covering 13 years and markets around

the world, VaasaETT has now developed a loyalty / disloyalty engine, known as the Churn Radar

which enables utilities to predict, in real-time the switching propensity and likely switch levels

in their market . The Churn Radar integrates more than 100 variables and is totally

customizable to almost any liberalised market. This tool is now available to all utilities.

Source: VaasaETT & CRIEPI

2010 VaasaETT World Energy Retail Market Rankings Report 2010 33

Belgium In general, switching levels in Belgium, where three separate regional liberalised

markets co-exist, are mid-table ranging from modestly Active to Warm Active.

Switching is stimulated and restricted by the same flawed competitive environment.

Limited switching has been restricted by a mixture of factors including for instance

excessive market concentration (two utilities control over 80% of generation), insufficient savings

opportunities and switching process and rule inefficiencies. Factors including for instance

dissatisfaction with incumbents, prices and the industry in general have on the other hand

stimulated switching despite the restrictions.

Wallonia is the most active of the Belgian markets, with an annual switch rate of around 10% and

incumbent retailers losing in the region of between 1-3% of their customer base each year

(meaning that the majority of switching is taking place between former incumbents). Switching

would now appear to be sustained by a reasonably stabilised level of momentum, but further

activity is arguably restricted by unclear game rules between retailers.

Since full liberalisation was achieved on July 1st 2003, Flanders has seen a consistent increase in

the level of switching. The trend has however been (at least temporarily) been leveling off (even

slightly decreasing for gas) during the past two years and in 2009 was just under 6% in the Active

switching level category. This downturn is considered to be at least in part in part a response to

reduced price differentials in the market and an overall downward trend in energy prices during

2009 (in comparison to a peak at the end of 2008). Not only could many customers benefit less

from switching, but there was less impetus from news media as a result of the absence of price

shocks (customers are even more likely to switch because of price increases than in response to

increases in price differentials).

Switching in Brussels has nearly doubled since 2008 making it an Active market, and while not

exactly a volatile or prolific market (switching rates for each quarter in 2009 did not vary much),

it would appear to be a market with some potential. Nonetheless, the Brussels trend is showing

that it will be a more active market in the coming years.

Slovenia

In Slovenia, switching levels in 2009 were approximately 150% higher than 2008,

making it the most active market in the Eastern and South Eastern European region.

Activity was enhanced by increased marketing activity from one marketing focused new entrant

player GEN-I. GEN-I increased its market portion in the total retail market by approximately 6%

whereas most other retailers approximately retained their 2008 positions, except one

distribution company / retailer which increased its market share by approximately 2%.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 34

France

In France in 2009, an increase in marketing activity for electricity, and a relatively

favorable wholesale market for gas, meant that non-incumbent (new entrant) retailers

temporarily showed signs of prospering, especially in the residential segment, arguably for the

first time since French electricity and gas markets were fully liberalised on 1 July 2007 (although

end-user regulated prices still exist in all market segments).

Electricity

The number of monthly switchers remained remarkably stable between July 2008 and August

2009, promoting France into the Cool Active switching level category for the first time since the

market was fully liberalised. New entrant marketing activity however subsequently slowed down

again in early 2010, due to the squeeze effect between wholesale sourcing costs and the retail

price cap established by the government based on the (relatively low) cost of nuclear base owned

by the national incumbent EDF. Additionally, an important change has taken place since

September 2009, as competitors have been focusing on improving the quality of their portfolio

rather than indiscriminately gaining new customers.

On the positive side, ten country wide suppliers compete with EDF in the residential market

compared to six in 2008. New entrant retailers also doubled their customer base in 2009. On the

negative side, by mid 2010, three years after market opening their market share was still only 5%

of the market (in terms of numbers of customers), even though approximately 10% choose a new

entrant when moving home. In the non-residential segment the situation was rather different.

The market has been inactive throughout 2009-2010, despite the existence of 18 country wide

competitors to EDF, resulting in new entrant market share decreasing to around 8% by mid 2010.

Changes in store for 2011

The French government has drafted a bill which is currently under discussion in the Parliament to

achieve two objectives: to impose a right of access for alternative suppliers to EDF nuclear

facilities at a wholesale price based on cost; and to remove retail price regulation on the non

residential market.

Gas

In 2009 and the first half of 2010, wholesale market prices have been lower than long term

contract prices indexed on oil. As a consequence retailers have had the opportunity to compete

fully with end user regulated prices based on long term contracts.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 35

Nevertheless, only six country wide retailers compete with the incumbent GDF Suez on the

residential market (although this compares to three in 2008) and new entrant retailers’ customer

base represents only 6% of the market three years after market opening. This market continues

to suffer from the lack of customer awareness and the complex legislation that impeded

customers having switched to a non regulated offer to switch back to it.

In contrast to the residential market, the non-residential market has 21 retailers covering the

whole country and competitors to GDF Suez have reached 17+ % market share (25% in volume).

An optimistic outlook

The possibility to switch back to a regulated offer has been introduced in the legislation since the

beginning of 2010 for residential customers.

Marketing Characteristics for Gas and Electricity

All new entrants have now chosen a dual fuel strategy. It would seem that today, gas is

the main driver for the electricity market: competitors try to target those customers with

the highest gas bill.

The smaller competitors mostly rely on door-to-door sales, in spite of high acquisition

costs associated to this channel.

Competitors have re-internalized their sales forces after several years of outsourcing, in

part because they intend to place a lot more emphasis on customer segmentation.

Increased targeting and segmentation: Until now, the lack of proper customer targeting

has resulted in important portfolio adjustments: both Poweo and Direct Energy had to

terminate a large number of contracts due to bad debt problems. Another issue for new

entrants related to segmentation is the fact that they had difficulty to recruit

homeowners. With a majority of leaseholders among their portfolio, they suffer from

important churn rates when those customers move. Poweo for example has seen its

churn rate peak at 6% per month by mid 2009 (according to a press release). It appears

new entrants are now trying to improve their targeting, in order to reduce churn and

debt. New massive recruitment campaigns are not expected to start again until the

details of the NOME law are known.

Czech Republic

An increase in marketing and new supplier activity characterised the 2009 switching

environment in the Czech republic, along with the collapse of a major electricity trader (Moravia

Energo, a.s.) and the subsequent application (for the first time) of the concept of supplier of last

resort.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 36

2009 was the first year when competition was visibly active in the household segment, rather

than just larger consumer groups. Nearly four times as many residential customers switched their

retailer in 2009 compared to 2008, and nine retailers were competing for residential customers.

Alberta, Canada

Alberta is considered an Active market, but due to switching data comparability issues,

it is not included in the VaasaETT World Energy Retail Market Rankings List for 2009.

Fully open to competition already in January 2001, between January 2002 to December 2009 the

percentage of customers (metering sites) that switched to a competitive retailer increased from

approximately 3% to 30%, representing all customer classes. In the same time period 82% of

large commercial and industrial customers and 47% of small commercial and industrial customers

switched to a competitive retailer. Commercial and industrial customers are (relative to other

customer groups) generally more knowledgeable of the electricity markets and therefore more

comfortable in choosing an electricity retailer.

In the Alberta retail market customers who use less than 250,000kWh annually can choose

between a regulated rate option (RRO) or a competitive contract. The rate under the RRO

consists of a blend of monthly forward contacts and long-term hedges that RRO providers

purchase on behalf of their customers. Customers have, since 2006, gradually been transitioning

to a rate where the RRO will be entirely based on monthly forward hedges. In July 2010 the RRO

will be based 100% on monthly forward hedges. There are currently four residential retailers and

ten commercial and industrial retailers. Most competitive contracts available to residential

customers are either for one to five year terms or for a flow-through of the monthly average

wholesale price. The Alberta retail electricity market has shown a continuous increase in the

number of customers switching from the RRO to competitive market products.

Portugal

In 2009 Portuguese competition activity benefited from the Spanish new entrant

utilities (facilitated by low interconnection constraints with Spain), with the context of

savings potentials driven by wholesale opportunities. Nevertheless, Portugal remains a Dormant

market according to the VaasaETT UCSRP definition. Following the voluntary return of most non-

residential customers to the regulated tariff in 2008, switching from the regulated tariff has

however once again returned due to favorable conditions for the transition of customers from

the regulated market to liberalized market, (taking advantage of the gap that existed between

the last resort tariffs and the prices in the liberalized market).

2010 VaasaETT World Energy Retail Market Rankings Report 2010 37

In 2009, the existence of a small but significant price spread between Portugal and Spain and

reduced interconnect congestion, meant that trading risk for Spanish retailers (which do not have

generation in Portugal) reduced, encouraging more competitiveness and competition from those

retailers, enabling the new entrants to gain slightly larger numbers of customers. The level of

aggregated switching remained under 1% per annum, as it did in 2008, but there are signs of

sprouts in the Portuguese market. The future of competition in Portugal is nevertheless

considered bleak unless regulated tariffs are removed.

Greece

Greece’s still Dormant switching level increased ever so slightly in 2009, largely due to

high retail prices for smaller consumption segments combined with wholesale opportunities for

new entrants, and increased activity from new entrants (known as non PPC suppliers). The trend

furthermore appeared to continue into 2010, with nearly 25000 customers (mainly industrial and

commercial) switching retailer (to a non-incumbent retailer) in the first quarter of 2010.

According to ERSE, the Portuguese energy regulatory authority, there are two main reasons for

the increase in switching:

a. The tariffs of the integrated company PPC suffer from distortions and cross subsidies that

benefit residential customers at the expense of I&C customers. This provides opportunities for

retailers that focus on the needs of I&C customers.

b. During 2009 high hydro generation meant wholesale prices were quite low, offering a

considerable margin to suppliers to enter the retail market. Nevertheless, during 2010 it is

expected that the tariffs of PPC will be rebalanced and all cross subsidies and distortions will be

removed, result the containment of switching to new suppliers.

Greece is expected to remain a dormant market, especially for residential customers, in the

foreseeable future, and until major regulatory and structural reform takes place.

2010 VaasaETT World Energy Retail Market Rankings Report 2010 38

From a marketing perspective, there is no

more important determinant of switching

than effective timing. Timing manifests

itself in the dynamics of switching through

a multitude of ways.

Whether competing to win or keep customers, utilities must consider

factors such as seasonality, cyclicality, taking advantage of competitors’

price rises and publicity mishaps and

playing to customer emotions and

levels of critical awareness, to name but a few.

Furthermore, we are not just talking about approximate

timing, sometimes windows of opportunity extend no more

than a matter of days.

No switching determinant dominates however. VaasaETT has

identified and analysed over 100 variables that are all

significant within the context of switching rates. It is the

state, interplay and dynamics of all these variables that

determines switching levels and trends.

The Importance of Timing

On average, across all markets

(excluding AUS and NZ), over 69% of

switching takes place in Q1 & Q2

2010 VaasaETT World Energy Retail Market Rankings Report 2010 39

Meet the Authors

Dr Philip E Lewis

Dr Lewis is a leading international specialist in utility customer behaviour and

psychology and related market and marketing issues including especially

Customer Loyalty, Demand Response/Eco-Home/Smart Grid and Market

Competitiveness.

During 14 years in the liberalized utilities industry Dr Lewis has conducted customer

switching related research in over 50 countries and four continents for over 330

organizations including for instance Shell, E.ON, EDF, Panasonic, BP, Nokia and British Gas.

Dr Lewis has also worked extensively at an industry and market-wide

level, having written major benchmarking and advisory reports for

e.g. the European Regulator’s Group for Electricity and Gas (ERGEG)

and government ministries, as well as providing opinion and advice

for e.g. the EU, the Finnish Parliament and various other

governmental organizations around the world.

Dr Lewis is a globally renowned expert in the field of customer

switching and loyalty. His World Energy Retail Market Rankings report

is the leading authority on customer switching trends around the

world, and his definition of customer switching has been effectively

adopted as the European norm within Europe and Australia (by the

European Union / European Regulators) as the Energy Retailers of

Australia Association). Dr Lewis also has an extensively array of both

Industry and Academic publications to his name and was founding

chief editor of the book 'The Energyforum Global Report’, as well as a

co-writer of the renowned Capgemini European Energy Markets Observatory. He has also

chaired and co-organized dozens of high level conferences globally.

Dr Lewis was formerly head of Marketing Research and Analysis for a UK based retailing

subsidiary of Amoco and (now) EDF, during the onset of competition in the British retail

energy market. Following this Dr Lewis was founder and chief of the University of Vaasa

Energy Markets Group (VaasaEMG) as well as an Assistant Professor of Marketing. Dr Lewis

holds a PhD in Marketing (customer psychology and behaviour) from the University of Edinburgh,

Scotland and developed his graduate marketing expertise in the banking sector with American

Express Bank in Frankfurt and National Westminster Bank in London. More information at:

www.vaasaett.com/contact

2010 VaasaETT World Energy Retail Market Rankings Report 2010 40

Sean Brennan

Sean is a research analyst at VaasaETT, and has been investigating

global utility customer switching trends for the past two years under the

guidance of Dr Philip E. Lewis.

Sean, collaborating with contacts within the Utility Customer Switching Research Project’s

extensive global network of sources, is VaasaETT’s lead connection to the latest and best

switching data from around the world. Born and educated in the USA, Sean is now based in

Finland and is additionally trained in IT related market issues as well as network

development.

Contributors The authors gratefully acknowledge and appreciate all the many

people who generously donated time, knowledge and or data to