value fund - series 1 - mutual funds india · pdf file2 contents 1 why equities now? 2 value...

TRANSCRIPT

GOOD BUYSGOOD BUYSGREAT PRICESGREAT PRICES

at

OUR VALUE INVESTMENT PHILOSOPHY

Value Fund - Series 1Value Fund - Series 1A Close-Ended Equity Scheme

NFO Period: October 18, 2013 to October 28, 2013

2

Contents

Why Equities Now?1

Value Investing2

Identifying Value in the market3

Value Investing - Globally4

ICICI Prudential Value Fund Series 15

Key Take Aways6

Why Equities now?

3

Why Equities now? –Valuations lagging Fundamentals

4

• India's market cap to GDP indicates valuations are at historical low.

• The gap between nominal GDP and market cap of BSE has widened post 2010

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Nominal GDP Mcap (BSE)

INR

bn

Source: Bloomberg

5Red mark represents elections in that year

In the past, elections have been a good trigger point for market direction.

Why Equities now? – 2014 General Elections

S&P BSE Sensex

0

5000

10000

15000

20000

25000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

1991 Elections - Previous Govt was dissolved just 16 months after formation

1996 Elections - Hung parliament

1998 – Re-elections as the Govt collapsed

2004 Elections –The Indian national Congress gained majority with the help of its allies.

2009 Elections - The United Progressive Alliance (UPA) led by the Indian National Congress formed the government.

1999 Elections - first time a united front of parties attained a majority

Source: www.bseindia.com and Election Commission of India 6

Why Equities now? –S&P BSE Sensex & Elections

Above chart explains how S&P BSE Sensex has performed post elections.

Provided only for reference and understanding of market movement post elections. Nothing in the slide must be construed as future performance of S&P BSE Sensex.

Elections Absolute Appreciation

Election Year Date Sensex20%

Appreciation50%

Appreciation 70%

Appreciation

1991 21-Jun-91 1361.7 Within 1 year Within 1 year Within 1 year

1996 9-May-96 3694.3 Within 2 years The bull phase that started in 1991ended in 1997.

1998 3-Mar-98 3646.0 Within 2 years Within 2 years

1999 7-Oct-99 4963.1 Within 1 year

2004 13-May-04 5399.5 Within 1 year Within 2 years Within 2 years

2009 16-May-09 12173.4 Within 1 year Within 2 years Within 2 years

7Source:www.bseindia.com

Why Equities now? –Broad Market Valuations

Current valuations below 10 year average, despite some stocks trading at very high valuations

Sensex P/E Ratio

8

11

14

17

20

23

26

29

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0

1

2

3

4

5

6

7

8

Sensex P/B Ratio

Avg PBAvg PE

8Source: UBS Securities

Why Equities now? –Polarisation of Valuation

Cyclical – Consumer Discretionary, Energy, Financials, Industrials, IT, MaterialsDefensives – Consumer Staples, Healthcare, Telecom, Utilities

• In the past, valuation gap between cyclical and defensives have converged

• Since 2010, the gap has widened and defensives are trading at high valuations

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

P/E

2005

2006

2007

2008

2009

2010

2011

2012

2013

Cyclicals

Defensives

Defensives vs Cyclicals

Source:www.bseindia.com 9

Why Equities now? – Market Segmented

Since the last peak in Nov 2010 the Small and Mid cap stocks are trading at a discount to their Large cap counterparts

Discount is calculated taking Nov’10 index values as base.

50%

60%

70%

80%

90%

100%

Nov-10 Mar-11 Jul-11 Nov-11 Mar-12 Jul-12 Nov-12 Mar-13 Jul-13

S&P BSE Mid Cap S&P BSE Small Cap

Small cap discount toSensex

Mid cap discountto Sensex

Mid & Small Cap discount to Sensex

Value Investing

10

• Investing in stocks that trade at a discount to their true value.

• Investing at a price lower than what justifies the company’s long term fundamentals.

• Value investing is a long-term strategy - it does not provide instant gratification.

Value Investing

11

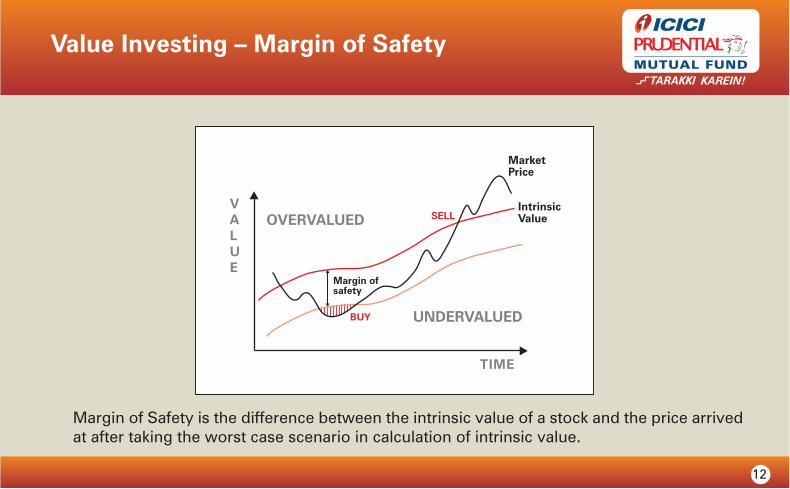

Value Investing – Margin of Safety

12

Margin of Safety is the difference between the intrinsic value of a stock and the price arrived at after taking the worst case scenario in calculation of intrinsic value.

13Source: Bloomberg

Understanding Value Investing

• During the period 2011-2013, BSE Sensex remained range bound.• However, during the same period stocks shown above have grown multi fold times.This is a high level oversimplified illustration to explain the concept of Value Investing. Actual results may vary significantly from the ones mentioned here and may not always be beneficial or profitable. The stocks given above should not in any manner be construed as recommendation and ICICI Prudential Mutual Fund/AMC may or may not have any future position in these stocks. There may be other value stocks in the market which may have significantly underperformed large cap stocks. No inference must be drawn that value stocks generate long term performance as there may be cases where such value stocks may actually be value trap.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Dec-10Mar-11

Jun-11Sep-11

Dec-11Mar-12

Jun-12Sep-12

Dec-12Mar-13

Jun-13Sep-13

S&P BSE Sensex Natco Pharma Ltd Amara Raja Tech Mahindra Ltd

Rs 20,193

Rs 34,405

Rs 19,892

Rs 10,386

Values rebased to 10,000

IDENTIFYING VALUE IN THE MARKET

14

Identifying Value in the Market

• Between 2001 and 2003, the stocks in the consumer basket represented a value buying opportunity.

• Market cap of these stocks did not mirror the consistently growing profits.

• In the ensuing period the market realized the true value of these stocks and market cap soared.

• Consumption basket is currently, trading near historical high valuations

15Source: Morgan Stanley Research

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0

20

40

60

80

100

120

140

160

180

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Trailing Net Profit Market Cap (RS)

in INR Bn

MS Coverage Consumer Basket - Earnings vs Market Cap

Earnings Market Cap

16

Identifying Value in the Market

• It is believed that currently mid cap IT stocks are trading at attractive valuations compared to large cap IT stocks.

• Revenue growth led to re-rating of mid cap IT companies in 2006.

Source: MSCI, RIMES, Top 4 - TCS, Infosys, Wipro, HCL Tech Midcap – Mindtree, Hexaware & Infotec Ent.

This is a high level oversimplified illustration to explain the concept of identifying value. Actual results may vary significantly from the ones mentioned here and may not always be beneficial or profitable. The stocks given above should not in any manner be construed as recommendation and ICICI Prudential Mutual Fund/AMC may or may not have any future position in these stocks. The performance of stocks would ultimately depend on various factors such as prevailing market conditions, global political scenario, exchange rate etc. It may have adverse bearing on their performance.

0

5

10

15

20

25

30

35

40

2005 2006 2007 2008 2009 2010 2011 2012 2013

TOP 4 Mid Caps

Large cap IT vs Midcap IT

17Source:www.bseindia.com

Identifying Value in the Market

• Midcap valuations are currently at 2009 lows. The midcap index rallied from 3300 levels to 8000 levels between 2009-2011.

• The increase in book value of the stocks in the midcap index has not been accompanied by increase in valuations.

P/B S&P BSE Midcap Index

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

0

1

2

3

4

5

6

7

8

9

2006 2007 2008 2009 2010 2011 2012 2013BSE Midcap P/B BSE Midcap

Current valuations close to 2009 lows

Source: Bloomberg, Jefferies estimates

• The top 20 stocks have trebled, now making up 30% of the BSE100 market cap versus barely 10% in Dec-07

• These stocks continue to outperform, providing gloss to the headline indices like Sensex and Nifty

Identifying Value in the Market

18

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013

Top 20 performers Bottom 80 performers BSE100

Top 20 performers vs Rest of the market

Values rebased to 100

VALUE INVESTING - GLOBALLY

19

Value Investing – Globally, is working

20Source: Bloomberg

0

100

200

300

400

500

600

20002001

20022003

20042005

20062007

20082009

20102011

2012

MSCI China Index MSCI China Value Index

0

200

400

600

800

1000

1200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

MSCI Russia Index MSCI Russia Value Index

CHINA INDICES RUSSIA INDICES

0

500

1000

1500

2000

2500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US INDICES

S&P 500 Value Index Russell 2000 Value Index S&P 500 Growth index

Values rebased to 100

Values rebased to 1000

Values rebased to 100

21

• Long term wealth creation solution• A close-ended diversified equity fund that aims to provide capital appreciation by investing in a well

diversified portfolio of stocks through fundamental analysis.* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

HIGH RISK(BROWN)

This product is suitable for investors who are seeking*:

(BLUE) investors understand that their principal will be at low risk

(YELLOW) investors understand that their principal will be at medium risk

(BROWN) investors understand that their principal will be at high risk

Note: Risk may be represented as:

Value Fund - Series 1Value Fund - Series 1(A Close-ended Equity Scheme)

The Product

About the fund

22

• A 3 year close ended scheme of focused 25-30 high conviction stocks.#

• Aims to:

• Find commendable companies at reasonable price rather than generic companies at bargain price.

• Capture profits by selling equities or using derivatives.

• Declare commensurate dividends.*

• Invest in multi-cap stocks.

*Dividends will be declared subject to availability of distributable surplus and approval from Trustees#The number of stocks provided is to explain the investment philosophy and the actual number may go up or down depending on then prevailing market conditions at the time of investment

Why Focused Approach?

23

• Due to large fund size and liquidity condition of the above stocks, size of holding is small.

• Any favourable movement in the stock prices may have a nominal effect on the overall portfolio returns.

Some value picks in existing funds

Company/IssuerFund 1

% to NAVFund 2

% to NAV

Value Stock 1 0.21% 0.60%

Value Stock 2 0.25% 1.38%

Value Stock 3 0.56% 0.30%

Value Stock 4 0.57% 1.33%

For illustration purpose only

24

Why close ended?

Lock-in brings in the necessary discipline

Restrict in/outflow to

capture limited market

opportunity

Aiming to identify

potential much ahead of the market

Exposure toless traded

stocks

25

Investment Approach

Absolute andrelative basis

Cyclical stocks

Contra play

Growth stocks atreasonable valuations

• Low P/E, P/B• Good Dividend Yield• Valuation attractive relative to peers / market

• Demerger / Spin-offs by companies• Mergers & Acquisitions• Value unlocking from subsidiaries, sale of assets

• Aim to identify sectors in a downturn• Aiming to buy good companies to play for revival of the sector

• Companies going through bad news-flows• Increased competitive environment, etc.

• High Return on equity and capital employed• Low Debt

Others

Stock Selection Process

26

High Conviction Portfolio (25 - 30 stocks)*

Data Integrity Screens

Investable Universe

Company CharacteristicsFinancial Strength • Business Durability • Management Behavior

Valuation & Fundamental verification

Value ParametersLow PE/PB • Good Dividend Yields • Attractive ROE/ROCE

Rec

urrin

g pr

oces

s

Daily Risk control

5000+ stocks

300

100

*The number of stocks provided is to explain the investment philosophy and the actual number may go up or down depending on then prevailing market conditions at the time of investment

Key Take Aways

• Institutional participation lopsided towards the top 15-20 stocks; valuations attractive in other pockets.

• The fund aims to hold limited number of stocks; allowing the scheme to benefit from potential positive price movements.

• Post 2008, the fund house has gained experience in managing close ended funds.

• Existing track record of managing value oriented funds.

• Past experience has shown that investors have earned returns when investments are made in bear phases.

27

Scheme Features

Type of scheme A Close ended equity scheme

Investment Objective The investment objective of the Scheme is to provide capital appreciation by investing in a well diversified portfolio of stocks through fundamental analysis. However, there can be no assurance that the investment objectives of the scheme will be realized.

Options Direct Plan – Dividend Option; Regular Plan – Dividend Option Only Dividend payout facility available

Minimum Application Amount Rs 5,000 (plus in multiple of Rs.10)

Entry Load Not Applicable

Exit Load Not Applicable

Benchmark Index S&P BSE 500 Index

Fund Manager Mr. Sankaran Naren & Mr. Mittul Kalawadia

28

29

Disclaimer: In the preparation of the material contained in this document, the AMC has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the AMC and/or its affiliates and which may have been made available to the AMC and/or to its affiliates. Information gathered and material used in this document is believed to be from reliable sources. The AMC however does not warrant the accuracy, reasonableness and / or completeness of any information. We have included statements / opinions / recommendations in this document, which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions, that are “forward looking statements”. Actual results may differ materially from those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and / or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc.

The AMC (including its affiliates), the Mutual Fund, the trust and any of its officers, directors, personnel and employees, shall not liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipient alone shall be fully responsible/are liable for any decision taken on this material.

The sector(s)/stock(s) mentioned in this presentation do not constitute any recommendation of the same and ICICI Prudential Mutual Fund may or may not have any future position in these sector(s)/stock(s). Past performance may or may not be sustained in the future. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information document of the scheme. Please refer to the SID for investment pattern, strategy and risk factors.

Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the units of ICICI Prudential Mutual Fund.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Disclaimers

30

Note

31

Note