view legal webinar - everything you need to know to deliver exceptional value (22 march 2017)

TRANSCRIPT

Patrick Ellwood, Director

Tara Lucke, Director of Adviser Solutions

22 March 2017

ADVISER FACILITATED ESTATE PLANNING –EVERYTHING YOU NEED TO KNOW TO DELIVER EXCEPTIONAL VALUE

Overview

Estate planning toolkit1

Adding value as a facilitator2

Interactive case study examples3

Tips for young players 4

How Are We Different?

Relationship driven

Wholesale – not retail1

Compliance focus2

Technology3

Quality4

Upfront service guaranteed pricing5

6

View Legal Adviser Solution Platforms

IT’S NOT MEANT TO BE HARD

Start with WHY1

Use estate planning to position wealth advice2

Increased revenue from risk and other advice3

Intergenerational advice opportunities4

Solutions focused, not product focused5

Why are we so Passionate?

TIPS FOR FACILITATING

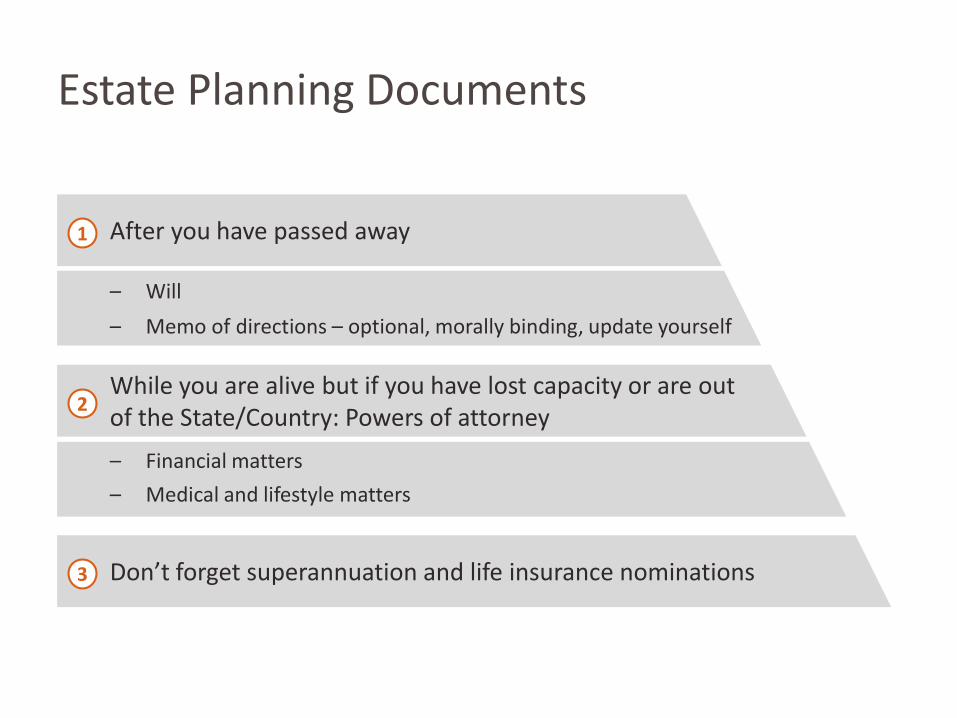

Estate Planning Documents

After you have passed away1

While you are alive but if you have lost capacity or are outof the State/Country: Powers of attorney

2

Don’t forget superannuation and life insurance nominations3

– Will

– Memo of directions – optional, morally binding, update yourself

– Financial matters

– Medical and lifestyle matters

I Love You Approach

Debts

Assets

Beneficiaries

Estate

No Testamentary Trust

Bankruptcy

Estate Challenge

Spendthrift

Divorce

Tax on income

Simplicity

Cost

✓✗

Testamentary Trust Approach

Assets

Estate

Trustee

TT

Beneficiaries

Testamentary Trust

Estate Challenge Bankruptcy

Spendthrift

Divorce

Tax on income

✓✗

A TT will be appropriate where:

Children1

Asset protection important2

Tax flexibility important 3

Assets in estate sufficient to justify extra administration toaccess tax and asset protection advantages (don’t forget lifeinsurance and super!)

4

No children but contemplating children in future5

When in doubt, use a TT!

How many Testamentary Trusts?

Single TT Multiple TTs

Some or all the children are minors All the children are adults or close to being adults

Asset protection is criticalAsset protection is important but autonomy for each child is more important

Children are intended to be the custodians of wealth for next generation

Children should have autonomy over their inheritance

Assets are difficult to divide between multiple trusts Assets can easily be divided between multiple trusts

The relationship between children is good, and it is practical for them to jointly manage the trust

Poor relationhip between some or all children means it would be difficult to manage a single trust

Children in same life cycle with their own familiesChildren are in different life cycles with their own families

Same control mechanism is appropriate for all children

Different children should have different control mechanisms over their inheritance

Children are in the same country and can easily manage the trust together

Children are living in different countries

Risk profiles of children are similar Children have vastly different risk profiles

If a couple, when should TT start?

Option Use if:

Only after both clients have died

• Older couple with grown up children• Majority of assets are held as joint tenants, superannuation or in a

trust• No grandchildren• Spouse is not in a high-risk occupation• No need for surviving spouse’s control over assets to be limited • Establishing multiple TTs after both passed

On death of the first spouse

• If a young couple with minor children• If an older couple with adult children, TT should come into operation

in first instance if:– Significant assets can pass into the TT on death of first spouse– Asset protection is important to surviving spouse– There are grandchildren where it would be useful to stream

income to them from the TT– Surviving spouse is in a high-risk occupation– Don’t want assets to pass under surviving spouse’s will

EstateTrustee

TT

Beneficiaries

Assets

Receives assets personally e.g.

• Assets held as joint tenants

• Superannuation

• Joint bank accounts

Receives assets as trustee for TT e.g.

• Life insurance

• Assets owned 100% by will maker

Assets

Estate

TT

Beneficiaries

Trustee

Surviving spouse receives all assets personally

All assets held via TT after both spouses have passed

EstateTrustee

TT #1

Beneficiaries

Assets

Receives assets personally e.g.

• Assets held as joint tenants

• Superannuation

• Joint bank accounts

Estate

TT #2

Beneficiaries

Estate

TT #3

Beneficiaries

TrusteeTrustee

Assets

Estate

Surviving spouse receives all assets personally

EstateTrustee

TT #1

Beneficiaries

Estate

TT #2

Beneficiaries

Estate

TT #3

Beneficiaries

TrusteeTrustee

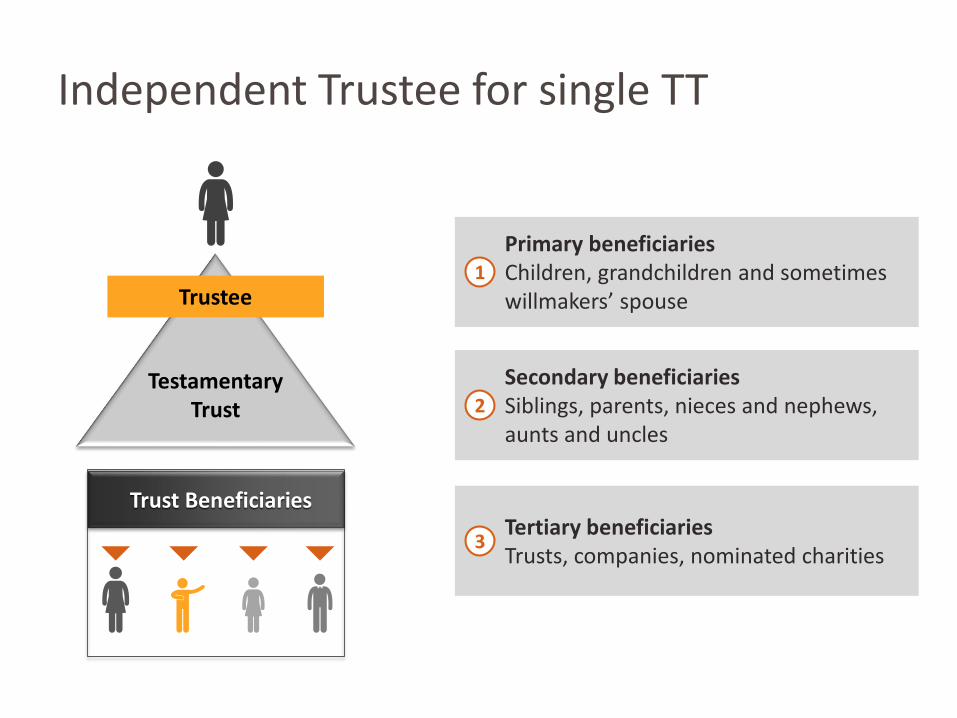

Independent Trustee for single TT

Trust Beneficiaries

TestamentaryTrust

Trustee

Primary beneficiariesChildren, grandchildren and sometimes willmakers’ spouse

1

Secondary beneficiariesSiblings, parents, nieces and nephews, aunts and uncles

2

Tertiary beneficiariesTrusts, companies, nominated charities

3

Independent back up Trustee

Where:

– Back up trustee is also a secondary beneficiary and manages TT for benefitof primary beneficiaries

– If several children are trustees and beneficiaries of the TT, and one childdies, leaving children of their own

Tara and Jayne are trustees of the Lucke TT. If Jayne dies, Tara should manage the TT equally for herself and Jayne’s children. However, there is nothing preventing Tara from distributing the TT assets to herself solely,

excluding her nieces and nephews if Tara is the sole trustee.

Mirror image for couples

Couples with children should have the same financial controllers and guardians for minors

Executors, trustees and financial attorneys should be the same so there is consistent management of finances for children regardless of how assets are held

1

2$

Be careful when nominating couples –what happens if they divorce or one dies?

3

Robust Succession for Executors and Trustees

For couples with children, consider having at least twofinancial controllers

1

Shares responsibility2

Keeps trustees accountable3

Back up plan if someone is acting out of character or has unexpectedlife event

4

Each side of the family has a seat at the table 5

Consider second level successors to fill vacancy and maintain twocontrollers at all times

6

How do children obtain control of TT?

Memo of directions versus hardwire into the will1

Balance flexibility versus certainty2

Memo of directions:3

– Morally binding only

– Give guidance on value based decisions

– Empower people will maker trusts to assess appropriatecircumstances at the relevant time

– Will maker can amend themselves over time

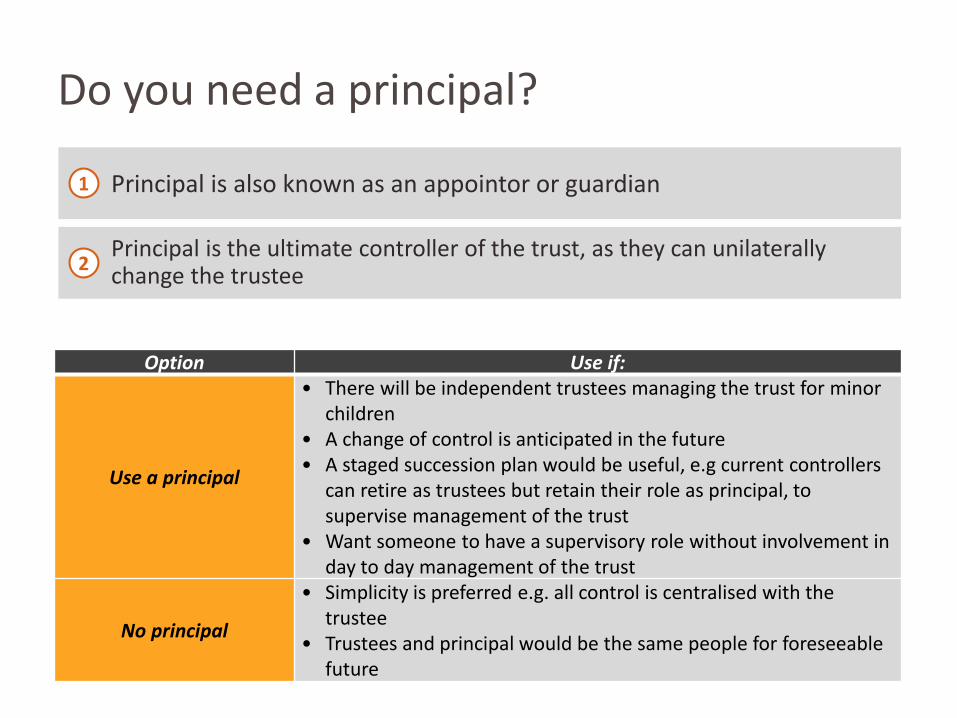

Do you need a principal?

Principal is also known as an appointor or guardian1

Principal is the ultimate controller of the trust, as they can unilaterally change the trustee

2

Option Use if:

Use a principal

• There will be independent trustees managing the trust for minor children

• A change of control is anticipated in the future• A staged succession plan would be useful, e.g current controllers

can retire as trustees but retain their role as principal, to supervise management of the trust

• Want someone to have a supervisory role without involvement in day to day management of the trust

No principal

• Simplicity is preferred e.g. all control is centralised with the trustee

• Trustees and principal would be the same people for foreseeable future

Use full names and complete addresses

Don’t forget back ups

Triple check spelling

Don’t use CAPS

Include AKA names

Some common issues

1

2

3

4

5

Calls to action

Have the conversations now1

Audit even if they appear 2017 compliant2

Level of specialisation unique in the market3

Truly leverage being the trusted adviser4

War stories5

Immediate opportunities even if an estate plan is 2017 compliantand health excellent

6

THANK YOUPatrick EllwoodDirector

Mobile: 0400 503 111

Email: [email protected]

Website: http://www.viewlegal.com.au/

Blog: http://www.blog.viewlegal.com.au/

Linked in: https://au.linkedin.com/pub/patrick-ellwood/96/625/348

The material contained in this presentation is based either on information derived from our proprietary business diagnostics (including research) or fromother sources within the market, which we believe to be reliable and accurate. It is general in nature and does not constitute specific advice. BusinessHealth makes no representation or warranty as to the validity, relevance or accuracy of this information as it pertains to any specific practice or business.

Proprietary & Confidential

THANK YOUTara LuckeDirector of Adviser Solutions

Mobile: 0417 578 150Email: [email protected]: http://www.viewlegal.com.au/Blog: http://www.blog.viewlegal.com.au/Twitter: https://twitter.com/tlucke1Linked in: https://au.linkedin.com/pub/tara-lucke/60/1bb/532

The material contained in this presentation is based either on information derived from our proprietary business diagnostics (including research) or fromother sources within the market, which we believe to be reliable and accurate. It is general in nature and does not constitute specific advice. BusinessHealth makes no representation or warranty as to the validity, relevance or accuracy of this information as it pertains to any specific practice or business.

Proprietary & Confidential