visa stock analysis report

TRANSCRIPT

Stock Analysis Report Birkey Investment Group By: John Conner, Trè Cotton, and Jon Blumberg

2

Table of Contents

I. Executive Summary 3

II. Industry Analysis 3

A. The Payment Card Industry 3

B. Industry Macro-Environment 10

C. Five Forces Analysis 11

D. Driving Forces 16

III. Financial Analysis 17

A. Price Trends 17

B. Revenue Trends 18

C. Earnings Trends 19

D. Return on Assets 20

E. Return on Equity 21

IV. Visa Europe 23

V. Recent News 23

VI. Recommendation 24

VII. References 27

VIII. Appendix: Visa’s Financial Statements - 2012-2014 29

3

I. Executive Summary

Visa operates in the payment card industry. Visa is the largest with a market cap of

$190B. The other three major players are MasterCard, Discover, and American

Express. The payment card industry continues to grow as consumers look to replace

cash and check transactions. The ease of debit and credit card use as well as reward

programs has led to growing consumer use. There is very little threat to new entrants

due to the scale of the corporations. Visa’s $23.4 billion acquisition of their European

counterpart Visa Europe will help grow the company in the European market. Visa

Europe controls 52% of the payment transactions in Europe. Europe is second to the

United States in credit/debit transactions. Visa is listed in the Top 10 relating to brand

equity on Forbes.com, with an estimated value of $90 billion.

Visa’s strong financial (See Appendix) position the company well in the payment

card industry and help support reasons for purchasing the stock. Strong trends in

revenue, earnings, profit margin help distinguish Visa from competitors. Visa has

advantageous buyback programs and continued dividend payouts that make it attractive

to investors. Visa’s earnings are projected to increase more than 10% in the next two

years, supporting the need for growth in a stock to make it a solid investment.

II. Industry Analysis

a. The Payment Card Industry

The Payment Card Industry (PCI) consists of all organizations that store, process

and transmits cardholder data, and is mostly known for debit cards and credit cards

(Payment Card Industry (PCI), n.d.). The PCI is guided by the Payment Card Industry

Security Standards Council (PCI SSC) which is a trade association that was created by

4

companies in the industry including; American Express, Discover Financial Services,

JCB International, MasterCard, and Visa Inc. All five payment brands share equally in

the Council’s governance, have equal input into the PCI Security Standards Council,

and share responsibility for carrying out the work of the organization (PCI Security

Standards Council, n.d.).

The credit card industry is a big business with many components. Business

Insider estimates that the credit card industry processed $4 trillion in the U.S. in 2014.

Seven of the largest card issuers – American Express, JP Morgan, Capital One, Bank of

America, Citigroup, Discover and U.S. Bancorp – reported more than $490 billion in

total credit card payments made in the fourth quarter of 2014 alone (Holmes, n.d.). The

percent of cards in circulation held by Visa, Inc. and each of its competitors in the

United States at the end of 2014 are as follows (Papadimitriou, n.d.):

● Visa: 48.9% with 304 million cards in circulation

● MasterCard: 30.7% with 191 million cards in circulation.

● American Express: 10.1% with 63 million cards in circulation

● Discover Financial: 10.1% with 64 million cards in circulation

5

However, based on the number of purchase transactions made with commercial and

consumer credit, debit, and prepaid cards worldwide in 2014, Visa owned more than

half of the market with 58% and $112.9 billion in transactions. Percentage of

transactions and the value of these transactions for Visa’s main competitors can be

seen in Figure1.

Essentially, Visa is the largest payment brand. Starting with a value of $16.36 billion

U.S. dollars in 2009, Visa reached the value of $91.96 billion in 2015 (See Figure 2). In

2014, Visa’s U.S. credit purchase volume was $1.2 trillion, up from $1.1 trillion in 2013.

Figure 1: Purchase Transactions Worldwide

6

There were 304 million Visa credit cards in circulation in the U.S. and 545 million Visa

credit cards in circulation outside of the United States in September 2014 (Holmes,

n.d.). Compared to 2013, there were 285 million Visa credit cards in circulation in the

United States and 526 million cards in the rest of the world.

Visa, Inc. and MasterCard run on an “Open-Loop Payment” System (see Figure 3

and 4). The open-loop payment system usually involves two banks and a payment

brand, apart from the merchant. A typical open-loop payment transaction works as

follows:

Figure 2: Visa's global brand value from 2009 to 2015 (in billion U.S. dollars)

7

● A cardholder uses the payment card at a merchant establishment or place of

business.

● The merchant sends the card details to an acquiring bank that the merchant has

signed up with.

● The acquiring bank requests authorization through a payment brand (Like Visa or

MasterCard) to an issuing bank which is the bank that has issued the

cardholder's payment card.

● The payment brand sends the information to an issuing bank who authorizes or

denies the transaction.

● Then the issuing bank sends the information back through the payment brand to

complete the processing cycle.

Figure 3: "Open-look Payment System"

8

Payment brands like Visa and MasterCard make money by facilitating transactions

made with their products. Due to so many transactions between payment brands,

financial institutions, and merchants, the following fees are generated (see figure 5 for

example):

Merchant discount fee: This is the fee charged to merchants by the acquiring

bank which is the bank that processes the card sales and credits the funds to the

merchant’s account and is generally 1 percent to 3 percent. The discount fee is

divided among the parties involved in the processing of the transaction. The

biggest division is the interchange fee, or the money collected by the issuer for its

part in the transaction. Essentially, the rates are set by Visa and MasterCard.

Processor and acquirer fee: This a flat transaction fee that is charged on all

authorized transactions which kept by the payment brand.

Credit card network fees: This when the card networks charge certain non-

negotiable fees that are passed through to the merchant.

Figure 4: Visa Payment Network

9

Interchange Reimbursement Fees and Assessments: These are the fees that

card-issuing banks and the payment brand charge for each transaction which is

the largest expense merchants pay per sale and per month.

o Interchange fees consist of a percentage of each transaction

accompanied by a flat fee per transaction.

o Assessment fees are based on a percentage of the total transaction

volume for the month.

Figure 5: Example of fees in the Payment Card Industry

10

In addition to Visa’s, high volume of purchase transactions, It is has recently

acquired its counterpart Visa Europe. Visa and Visa Europe’s boards are in agreement

on the terms of the deal which is expected to close in the second quarter of 2016.

Essentially, the merger will bring all of Visa’s global operations under one company. The

merger will give Visa a base of more than 14,000 financial institutions and 2.2 billion

accounts worldwide.

b. Industry Macro-Environment

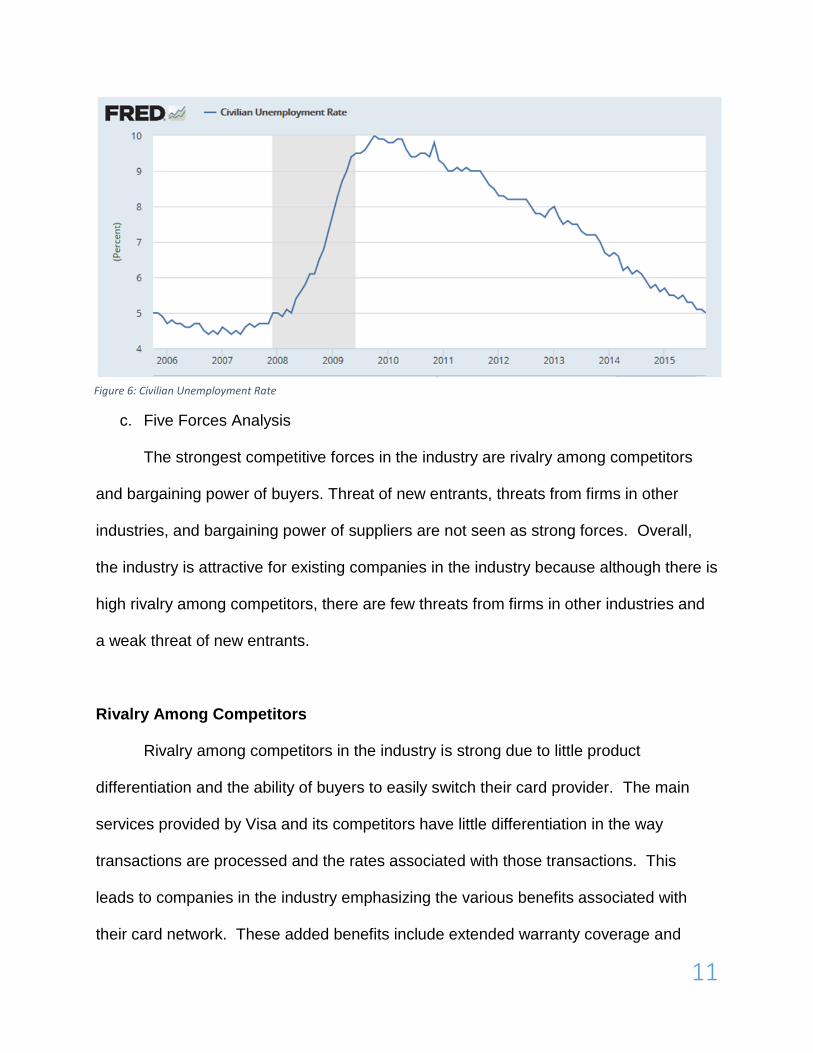

An aspect of the macroeconomic environment that affects the payment card

industry is unemployment. Companies in the industry generate a majority of their

revenue through the fees they receive each time a card is swiped. As unemployment

decreases, there are more people with an income who are willing to spend that money

in the economy. With an increased number of consumers’ spending money, there are

more transactions to be processed in the industry. This increase in transactions leads to

increased profits for companies in the industry. According to projections by the Federal

Reserve, the unemployment rate is expected to decrease below 5 percent through

2018, which means more people with disposable income to spend on goods beyond

their basic necessities.

11

c. Five Forces Analysis

The strongest competitive forces in the industry are rivalry among competitors

and bargaining power of buyers. Threat of new entrants, threats from firms in other

industries, and bargaining power of suppliers are not seen as strong forces. Overall,

the industry is attractive for existing companies in the industry because although there is

high rivalry among competitors, there are few threats from firms in other industries and

a weak threat of new entrants.

Rivalry Among Competitors

Rivalry among competitors in the industry is strong due to little product

differentiation and the ability of buyers to easily switch their card provider. The main

services provided by Visa and its competitors have little differentiation in the way

transactions are processed and the rates associated with those transactions. This

leads to companies in the industry emphasizing the various benefits associated with

their card network. These added benefits include extended warranty coverage and

Figure 6: Civilian Unemployment Rate

12

price protection. Marketing plays a big role in the competitive nature of the credit

services industry.

Companies have to appeal to three different customer bases: financial

institutions, merchants, and consumers. By targeting cardholders, companies in the

industry are able to establish their brand in a way that consumers develop a superior

image of one company over others in the industry. If consumers have a consensus

favorite among the companies in the industry, then financial institutions and merchants

will be inclined to offer cards from the preferred company in order to improve their own

customer base. In an industry with four members, branding is likely an important part of

why some companies are more successful than others.

Bargaining Power of Buyers

Three groups of buyers can be identified in the industry. (See Figure

7) Companies in the industry market their products to financial institutions, merchants

and consumers.

Buyers in the Payment Industry

Financial Institutions Merchants Consumers

Banks agree to long-term agreements with Visa or MasterCard to issue credit and debit cards to their customers.

Many merchants choose to offer a credit card with their brand on it to benefit from interest payments and attempt to increase consumers’ overall spending by offering discounts and rewards when consumers use their card.

Consumers can choose to apply for a credit card from any of the companies in the industry. Their decisions are often based on rewards offered by the card or interest rates.

Figure 7: Buyers in the Payment Industry

13

Financial institutions have moderate bargaining power in the industry. They are

the buyers that have the most power over companies in the industry because the

agreements they make with credit processing companies result in the most lucrative

transactions for the companies. In order to compete for deals with financial institutions,

companies in the industry must be aware of what financial institutions are looking for,

and attempt to meet their expectations to gain their business and increased revenue.

Once the agreements expire, there are limited factors preventing companies to switch

between credit card providers. This ability and willingness of financial institutions to

switch credit providers has been exhibited recently by institutions switching between

companies in the industry. USAA made the switch from MasterCard to Visa, citing the

ability to provide end-users with more benefits and eliminating foreign transaction fees

as the main reasons for making the switch.

Merchants, such as Target, have weak to moderate bargaining power in the

industry because credit card companies compete to be the company merchants choose

to issue their cards through. These agreements normally are not as large in volume of

transactions as the agreements with banks to issue cards but still provide credit card

companies with an additional revenue stream. An example of a merchant that issues its

own credit card is Costco, which in the past has not only issued American Express

credit cards, but it only accepted American Express, until it recently made an agreement

to switch to Visa.

Consumers have weak bargaining power in the industry because the decisions of

one consumer have no effect on how companies in the industry operate. Companies

market toward consumers by highlighting the rewards offered by certain cards or

14

favorable interest rates. The reasoning for consumers to choose one card over another

varies based on the consumer’s use of the card. If consumers pay their bills off as soon

as they accrue any charges, it is likely they will base their decision on the rewards and

benefits they receive from using a particular card. Consumers who usually have a

balance on their card and make monthly payments may look for a card that offers the

lowest interest rates.

Threats of Substitute Products

There is a weak threat of substitute products in the payment card industry. With

e-commerce sales growing by almost 48% since 2013, there are multiple electronic

payment methods that have been introduced to the marketplace. Some of these forms

of payment, such as PayPal, have become familiar to many consumers while other

forms, such as Bitcoin, are still foreign to many people and therefore not as easily

understood.

PayPal, introduced in 2002, is integrated into most e-commerce shopping carts

and allows customers to make purchases without having to type in a card number. It

does this by connecting consumers’ bank accounts with online shopping carts. PayPal

is a substitute to both the debit and credit aspects of companies within the industry by

acting as both an online wallet linked to a bank account and by directly issuing credit to

consumers. PayPal also offers a credit card through MasterCard, which offers rewards

and extends the scope of PayPal’s involvement of overall transactions.

Bitcoin, introduced in 2008, is a newer method of payment that acts as a whole

new type of currency. The Bitcoin process involves consumers using electronic wallets

15

that enable the transfer of funds between consumers. Bitcoin is not as easy for

consumers to understand as concepts like PayPal, along with its recent decline in

popularity makes Bitcoin a less imposing threat to the credit services

industry. However, as transactions move from the traditional market place to more

online transactions there will likely be more electronic solutions introduced that could

hurt conventional credit providers in the future.

Even though there is potential for companies like PayPal to have an impact on

the payment card industry, e commerce transactions currently make up only about 6.5%

of all retail transactions worldwide. E-commerce is projected to make up about 8.8% by

2018, so even though e-commerce transactions are likely to make up a greater share of

all retail sales they are not increasing at a rate that poses a threat to the industry in the

near future.

Threat of New Entrants

The threat of new entrants has a weak effect on competition in the industry

because of the barriers to entry. These barriers include the size of the companies in the

industry, the extensive networks they have in place, and high start-up costs. Companies

in the industry have established strong brand recognition among consumers, making it

hard for a new company to come in and steal their market share. In order for a

company to come in and have an impact on the industry, it would need to overcome the

high startup costs, and execute a marketing plan that leads to buyers wanting its

product over the industry leaders.

16

Bargaining Power of Suppliers

The bargaining power of suppliers is another factor that has a weak effect on

competition in the industry. Companies in the payment card industry rely very little on

other companies to supply them with products or services needed to be

successful. The most significant supplier companies may have is one that sets up and

maintains their servers, but these companies have little power over the credit

companies.

d. Driving Forces

The revenue of the industry is driven by not only processing fees, but swipe fees

as well. Using any major credit, or debit card has become a part of many people’s lives

and businesses which can affect profitability and be seen as a driving force. The

Payment Card Industry is a growing industry due to the technological components

which is why increasing globalization and technology is another factor. Having

Consistent innovation and new technological processes to make things easier for

consumers to make payments and purchases around the world is essential. Most

importantly, changes in regulations can be a driving force. The current litigation that

some of the major card services are involved in can could possibly lead to a different

business model or redefine processing fees. All of these driving forces have a major

effect on the industry and can easily change the way things are done in the future.

17

III. Financial Analysis

a. Price Trends

Displayed in Figure 8 is the growth in price from November of 2010 until

November 23, 2015. Visa and MasterCard have experienced similar growth in market

price over the past five years with Visa being the outright leader. Visa’s stock price

growth is 313 percent to MasterCard’s stock price growth of 299 percent. Visa’s growth

has been steady over the five year period including a 65 percent growth since the

beginning of the current year. Discover’s stock kept pace until early 2015, has

experienced 203 percent growth. American Express’ stock price has increased 61%

since 2011, much slower than the other three companies but still more than Dow Jones’

Industrial Average 57% growth during the same time period. Visa and MasterCard have

continued to outperform the overall market recently.

Figure 8: Growth in Price from November 2010 – November 2015

18

b. Revenue Trends

Figures 9 and 10 show that Visa has had consistent revenue growth over the

past five years. Visa has experienced the highest percentage growth of its competitors

at a 47% increase since 2011. The potential addition of Visa Europe, which is

dominating the European market, and constant development of Visa aims to continue

this revenue growth in future years. Europe is the second only to the United States in

credit/debit transactions worldwide.

V MA DFS AXP

2011 9,188 6,714 7,066 29,962

2012 10,421 7,391 7,653 31,582

2013 11,778 8,346 8,224 32,974

2014 12,702 9,473 8,477 34,292

TTM 13,538 9,553 8,573 33,722

Figure 9: Annual Revenue 2011 - 2014 (in millions)

Figure 10: Revenue Trends since 2011

19

c. Earnings Trends

Figure 11 and 12 show the earnings trends since 2011. Visa’s earnings

increased each of the past two years, totaling a 61% increase in earnings over the past

five years. In 2012 Visa had a 41% decrease in earnings due to a $2.59 billion net

litigation settlement of an antitrust suit pertaining to excessive swipe-fees charged to

merchants.

Although MasterCard’s earnings increased 97% over the same time period, Visa

recorded $2 billion more in earnings than MasterCard during the latest 12-month period.

Visa’s profit margin is 43%, compared to MasterCard’s 39%, Discover’s 25%, and

American Express’s 18% in the past 12 months. According to Zacks Investment

Research, Visa’s forecasted earnings growth is 10.20% and 16.42% for fiscal years

ending in September of 2016 and 2017, respectively. Earnings growth is a key financial

statistic used by investors to determine the financial state of a company.

V MA DFS AXP

2011 3,650 1,906 2,202 4,935

2012 2,144 2,759 2,340 4,482

2013 4,980 3,116 2,414 5,359

2014 5,438 3,617 2,270 5,885

TTM 5,889 3,757 2,181 5,904

Figure 11: Earnings Trends since 2011

20

Figure 12: Earnings Trends since 2011

d. Return on Assets

Visa had the second highest return on assets of its main competitors with a

15.28% return (See Figure 13). Only MasterCard had a higher return at 25.34% while

Discover and American Express were below 4%. Return on Assets gives an idea as to

how efficient management is at using its assets to generate earnings. Visa has

increased ROA 43% since 2011 while MasterCard has increased ROA 30% during that

time. Visa is improving an already strong ROA faster than its competitors.

21

V MA DFS AXP

2011 10.71 19.52 3.40 3.29

2012 5.73 23.83 3.22 2.92

2013 13.11 23.34 3.04 3.50

2014 14.59 24.46 2.79 3.77

TTM 15.28 25.34 2.66 3.81

Figure 13

e. Return on Equity

Visa is third (TTM) regarding ROE when compared with competitors. Shown in

Figure 14 is the ROE for all companies since 2011. Visa had the second highest

increase in ROE during the five-year time period. Discover’s ROE has been decreasing

since 2011 while American Express has stayed relatively even during that span. Visa

has been improving ROE steadily, generating profits from the investments of its

shareholders at a faster rate than Discover and American Express.

V MA DFS AXP

2011 14.19 34.43 29.96 28.18

2012 7.93 43.16 26.55 23.79

2013 18.28 43.27 23.55 27.92

2014 20.04 50.68 21.80 29.30

TTM 21.06 59.31 20.27 28.05

Figure 14

22

Analysis

Visa’s (V) financials are favorable when compared with other industry leaders

MasterCard (MA), Discover Financial (DFS), and American Express (AXP). Data is

shown below (See Figure 15). Visa is the leader or close second in multiple financial

categories shown in figure15 below. Visa is the only company with a Beta below 1,

meaning that volatility in the overall market is not going to affect Visa’s price as

significantly compared to the other three competitors. Visa’s P/E and PEG ratios are

higher than the industry averages of 14.29 and .98, respectively. The high P/E ratio is

primarily due to sustained success resulting in Visa reporting income in 19 consecutive

quarters. According to yahoo finance the forward P/E ratio estimate is 27.19, which

means investors will be paying less for each dollar of earnings in the future than the

current P/E ratio of 32.36.

V MA DFS AXP

Market Cap (Billions) 190.20 112.79 24.40 73.08

P/E 32.36 30.56 11.72 13.39

PEG 1.69 1.82 1.27 1.77

Beta 0.93 1.26 1.29 1.08

ROA (%) 14.25 21.51 2.65 3.71

ROE (%) 21.07 58.93 19.47 27.71

Long-term D/E 0.00 23.23 210.56 247.62

Trailing Dividend $0.60 $0.60 $1.80 $1.50

Figure 15

23

IV. Visa Europe

Visa has agreed to a merger with Visa Europe worth $23.4 billion that would

likely steepen the growth trajectory for Visa. Visa Europe was spun off of Visa prior to

Visa’s initial public offering. Visa Europe currently controls 52% of the European market,

while MasterCard currently controls around 26%. The deal will expand Visa into Europe

and making it a single global company that will add more than 3,000 financial

institutions to Visa’s partner list and 500 million European cards to its clientele which is

responsible for about 18 billion transactions that is worth more than 1.5 trillion

euros. Visa Europe already utilizes some of the technologies that Visa is developing to

help deal with digital theft and credit card fraud, including the use of chips in their cards.

Visa is placing a lot of emphasis on developing new technologies that make

transactions more secure for consumers that use their product, and security is one of

the biggest issues in today’s market. By leading the industry in security developments,

Visa looks to secure its position as the world’s largest money card processor, and a

merger with Visa Europe will only make the company that much stronger.

V. Recent News

According to the balance sheet there is an increase in “Restricted cash—litigation

escrow” which is due to a class action lawsuit that was initiated by over 8,000

merchants like Wal-Mart, Target, and Amazon. The ligation has been pending since

2005 and the lawsuits accused Visa and MasterCard of fixing the fees that merchants

are charged each time that a consumer uses their credit or debit cards. The current

value of the settlement is approximately $5.7 billion. In order to be prepared for the

future of the settlement, which will be divided between Visa and MasterCard, Visa has

24

set aside a portion of its monetary assets to cover the costs and expenses of the

settlement.

Additionally, there is a decrease in “accounts payable” and increase in “client

incentives” which show that Visa is paying more of its accounts off and investing more

money into client incentives. Investing into client incentives helps sustain current long-

term contracts with financial institution clients and other business partners for various

programs designed to build payments volume, increase Visa-branded card and product

acceptance and win merchant routing transactions.

VI. Recommendation

We believe Visa to be a wise investment for the Birkey Investment Fund based of

the following reasons:

Visa’s value can been seen in its powerful network. Visa is poised to

answer questions as to why consumers should pay with Visa cards over

competitors and why merchants should choose Visa cards over

alternatives. As of December 2014, Visa cards are accepted in 36 million

merchant locations and had 2.9 billion issued cards. The large card base

along with great number of merchants who accept such cards is vital in

the payment card industry; Visa is well positioned in these areas.

Visa’s largest competitor, MasterCard, holds a strong position in

acceptance points, being accepted in 36 million merchant locations.

However, the advantage for Visa is its card count, which is 38% greater

than MasterCard resulted in Visa cards being used for 45% greater total

volume. Total volume is the dollar value of payments and cash accessed.

25

American Express falls significantly behind Visa in both aspects with 112

million issued cards and only 16 million merchant locations.

The acquisition of Visa Europe estimates to add 500 million cards to

Visa’s network which are members of 3000 financial institutions. Europe

is the second to the United States in the number of payment card

transactions.

Visa is the leading market share in the industry, being responsible for

51% or purchase transactions worldwide. Visa is the largest company in

the payment card industry and with the addition of Visa Europe this trend

will likely hold for years to come.

According to Zacks Investment Research forecasted earnings growth is

10.20% and 16.42% for fiscal years ending in September of 2016 and

2017, respectively.

Visa has zero Long-term debt meaning as a company they are extremely

liquid. Visa is able to pay their obligations as they come due immediately.

Visa has a leading profit margin at 43%, meaning that Visa is the most

efficient in terms of the money they make from their revenues than their

competitors.

The Visa global brand is valued at $91 billion. MasterCard’s global brand

is valued at $40 billion. Brand equity is the positive and negative affects a

company's brand has on consumers and business partners. Brand equity

can be defined as a brand’s power derived from the goodwill and name

recognition that it has earned over time, which translates into higher sales

26

volume and higher profit margins against competing brands.

Visa stock has a high price to earnings ratio of 30.88 at close on Monday,

November 23, 2015. This may raise some concerns about purchasing the

stock. We feel strongly that Visa’s high price to earnings ratio does not

signify that Visa is a poor investment going forward based upon past

stock price growth. Following this ratio back to July 2012 identifies a price

to earnings ratio hovering around 65. The price to earnings ratio has not

dropped below 23 since prior to July 2012. Visa’s stock on July 1, 2012,

closed at a price of $31.32. On November 10, 2015, Visa closed at

$79.48. This is a roughly 250% price increase over that time period. A

high price to earnings ratio generally signifies investors believe a

company has strong future growth potential and are willing to pay a larger

amount per dollar of earnings. A value investor is typically searching for a

price to earnings ratio that is improperly valued. Visa investors over the

past three years noticing a high price to earnings ratio have continually

invested.

27

VII. References

A simple explanation of fees in the payment card industry. (2014, August 9). Retrieved November 24, 2015, from http://gendal.me/2014/08/09/a-simple-explanation-of-fees-in-the-payment-card-industry/

Allison, I. (2015, June 25). Visa, MasterCard and Amex: Payments dinosaurs face off Bitcoin

technology threat. Retrieved from International Business Times: http://www.ibtimes.co.uk/visa-mastercard-amex-payments-dinosaurs-face-off-bitcoin-technology-threat-1507973

Alpha, Seeking. (2015, May 18). Visa: Market Power, Stable Growth And High Profitability

Doesn't Come Cheap. Retrieved from Nasdaq: http://www.nasdaq.com/article/visa-market-power-stable-growth-and-high-profitability-doesnt-come-cheap-cm478051

Charts & Graphs Archive. (2015). Retrieved from Nilslon Report:

http://www.nilsonreport.com/publication_chart_and_graphs_archive.php Citi, Visa Win Costco Credit Card Business. (2015, March 2). Retrieved from Forbes:

http://www.forbes.com/sites/laurengensler/2015/03/02/citi-visa-win-costco-credit-card-business/

Holmes, T. E. (n.d.). Credit card market share statistics. Retrieved from Credit Cards:

http://www.creditcards.com/credit-card-news/credit-card-market-share-statistics-1264.php

How does Bitcoin work? (n.d.). Retrieved from bitcoin: https://bitcoin.org/en/how-it-works How Visa, MasterCard Earn Cash (and Why You Should Care). (n.d.). Retrieved November 24,

2015, from http://www.dailyfinance.com/2014/07/29/how-visa-mastercard-make-money/ Investor's Business Daily. (2015, September 29). Visa Aims For A 'Token' Of Customers' Appreciation. Retrieved from Nasdaq: http://www.nasdaq.com/article/visa-aims-for-a-token-of-customers-appreciation-cm525489 Isidore, C. (2015, March 3). Costco teams with Citi and Visa. Retrieved from CNN Money:

http://money.cnn.com/2015/03/02/news/companies/costco-citi-visa/ Millward Brown. (n.d.). Visa's global brand value from 2009 to 2015 (in billion U.S. dollars).

InStatista - The Statistics Portal. Retrieved November 24, 2015, from http://www.statista.com/statistics/326068/visa-global-brand-value/

Papadimitriou, Odysseas;. (n.d.). Market Share by Credit Card Network. Retrieved 2015, from

CardHub: http://www.cardhub.com/edu/market-share-by-credit-card-network/ PayPal Extras MasterCard. (n.d.). Retrieved November 24, 2015, from

https://www.paypal.com/webapps/mpp/credit-card Payment Card Industry (PCI). (n.d.). Retrieved from Techopedia:

https://www.techopedia.com/definition/1557/payment-card-industry-pci

28

PCI Security Standards Council. (n.d.). About Us. Retrieved from PCI Security Standards

Council: https://www.pcisecuritystandards.org/organization_info/index.php Sidel, R. (2015, October 25). USAA Switching Credit, Debit Cards to Visa From Longtime

Partner MasterCard. Retrieved from The Wall Street Journal: http://www.wsj.com/articles/usaa-switching-credit-debit-cards-to-visa-from-mastercard-1445723841

The Complete Guide to Credit Card Processing Fees & Rates. (2013, January 9). Retrieved

November 24, 2015, from http://www.merchantmaverick.com/the-complete-guide-to-credit-card-processing-rates-and-fees/

US court hears challenge to US$5.7 billion Visa, MasterCard settlement. (2015, September 29). Retrieved from Channel NewsAsia: http://www.channelnewsasia.com/news/business/us-court-hears-challenge/2157070.html Visa Acquirer Processing Fee (APF). (n.d.). Retrieved November 24, 2015, from http://www.cardfellow.com/acquirer-processing-fee/

29

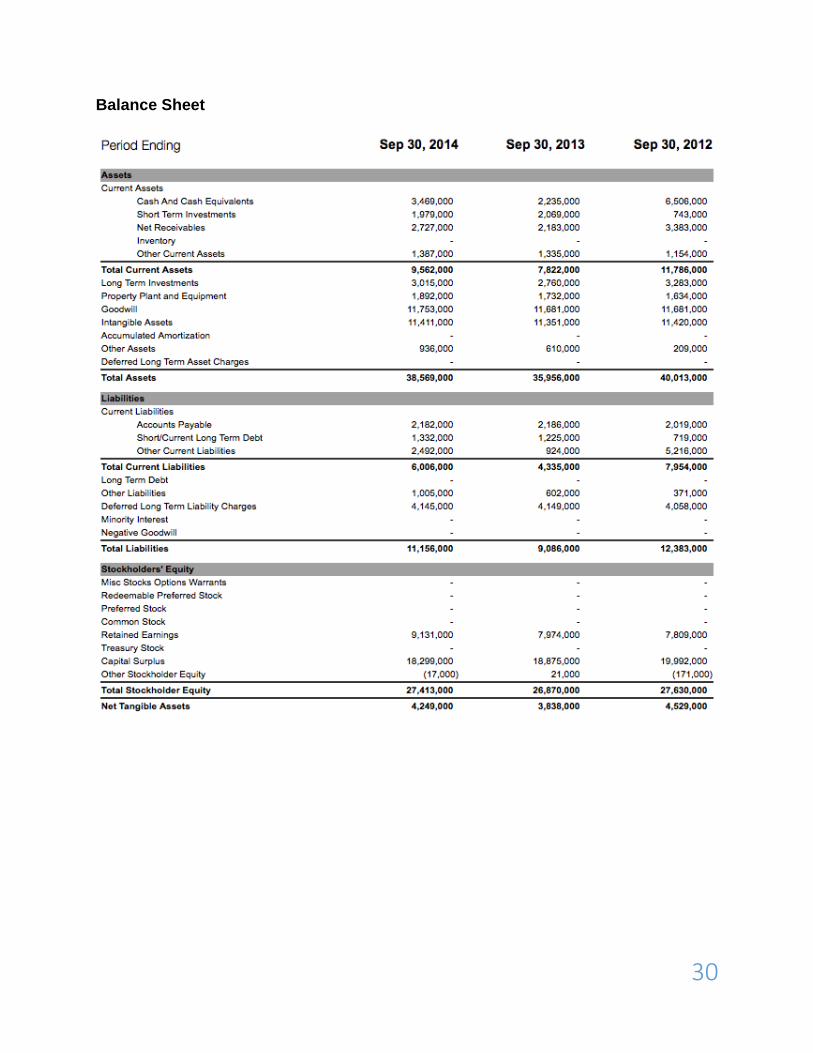

VIII. Appendix

Income Statement

30

Balance Sheet

31

Cash Flow