volume 75 j number 5 j october 2010 american sociological ... · the electronic files should be...

TRANSCRIPT

volume 75 j number 5 j october 2010

j A Journal of the American Sociological Association j

AmericanSociological

ReviewQ

Racial and Ethnic inEquality

Racial Segregation and the American Foreclosure Crisis Jacob S. Rugh and Douglas S. Massey

Stratification by Skin Color in Contemporary Mexico Andrés Villarreal

WoRkplacE dynamics

Personal Characteristics, Sexual Behaviors, and Male Sex Work Trevon D. Logan

The Motherhood Penalty across White Women’s Earnings DistributionMichelle J. Budig and Melissa J. Hodges

cRoss-national invEstigations

Postwar Labor’s Share of National Income in Capitalist DemocraciesTali Kristal

The Rise of the Nation-State across the World, 1816 to 2001Andreas Wimmer and Yuval Feinstein

suRvEy mEthods

Requests, Blocking Moves, and Rational (Inter)action in Survey IntroductionsDouglas W. Maynard, Jeremy Freese, and Nora Cate Schaeffer

ASR_v75n1_Mar2010_cover revised.indd 1 01/10/2010 7:44:45 PM

ASA Members of the Council

Editors

Deputy Editors

Tony N. Brown

Vanderbilt University

Katharine M. Donato

Vanderbilt University

Larry W. Isaac

Vanderbilt University

Holly J. McCammon

Vanderbilt University

Nicola BeiselNorthwestern

Claudia BuchmannOhio State

Karen CookStanford

Daniel Cornfield Vanderbilt

Guang GuoUNC, Chapel Hill

Gary JensenVanderbilt

Editorial Board

Patricia A. AdlerColorado

Sigal AlonTel-Aviv U.

Edwin AmentaUC, Irvine

Kenneth T. AndrewsUNC, Chapel Hill

Sandra L. BarnesVanderbilt

Paul E. BellairOhio State

Lawrence D. BoboHarvard

Kenneth A. BollenUNC, Chapel Hill

John Sibley ButlerUT, Austin

William C. CockerhamAlabama-Birmingham

Mark CooneyGeorgia

William F. DanaherCollege of Charleston

Timothy J. DowdEmory

Jaap DronkersMaasticht U.

Mitchell DuneierPrinceton & CUNY

Jennifer EarlUC, Santa Barbara

Rachel L. EinwohnerPurdue

Wendy Nelson Espeland

Northwestern

Ron F. EyermanYale

Joseph GalaskiewiczArizona

Adam GamoranWisconsin

Peggy C. GiordanoBowling Green

Karen HeimerIowa

Rubén Hernández-León

UCLA

Alexander HicksEmory

Dennis P. HoganBrown

Gregory HooksWashington State

Matt L. HuffmanUC, Irvine

Guillermina JassoNYU

Gloria Jones-JohnsonIowa State

Prema KurienSyracuse

Erin LeaheyArizona

Matthew R. LeeLouisiana State

Nan LinDuke

J. Scott LongIndiana

Wendy D. ManningBowling Green

Karin A. MartinMichigan

Cecilia MenjivarArizona State

Joya MisraMassachusetts,

Amherst

Phyllis MoenMinnesota

John F. MylesToronto

Orlando PattersonHarvard

Trond PetersenUC, Berkeley

Townsand Price-Spratlen

Ohio State

Charles C. RaginArizona

Raka RayUC, Berkeley

Jen’nan ReadDuke

Linda RenzulliGeorgia

Barbara Jane RismanUI, Chicago

William G. RoyUCLA

Deirdre RoysterNYU

Rogelio SaenzTexas A&M

Vicki SmithUC, Davis

David T. TakeuchiWashington

Maxine S. ThompsonNC State

Andrés VillarrealUT, Austin

Henry A. WalkerArizona

Mark WarrUT, Austin

Bruce WesternHarvard

Mark WesternQueensland

Jonathan ZeitlinWisconsin

American Sociological Review

Managing EditorMara Nelson Grynaviski

Editorial CoordinatorLaura White Dossett

Senior Editorial AssociateHeather Hensman Kettrey

Editorial AssociateMary Laske

Editorial Assistants

Kate Pride BrownBecky Conway

Carly Rush Samuel C. Shaw

Jarrett Thibodeaux

Randall Collins, President, PennsylvaniaDavid Snow, Vice President,

California-IrvineCatherine White Berheide, Secretary,

Skidmore College

Erik Olin Wright, President-Elect, Wisconsin-Madison

Edward Telles, Vice President-Elect, PrincetonEvelyn Nakano Glenn, Past President,

California-Berkeley

John Logan, Past Vice President, Brown Donald Tomaskovic-Devey,

Past Secretary, Massachusetts-AmherstSally T. Hillsman, Executive Officer

Elected-at-Large

Sarah Fenstermaker, California-Santa Barbara

Rosanna Hertz, Wellesley College

Pierrette Hondagneu-Sotelo, Southern California

Jennifer Lee, California-Irvine

Omar M. McRoberts, Chicago

Cecilia Menjivar, Arizona State College

Debra Minkoff, Barnard

Joya Misra, Massachusetts-Amherst

Mario Luis Small, Chicago

Sandra Smith, California-Berkeley

Sarah Soule, Stanford

Robin Wagner-Pacifici, Swarthmore College

ASR_v75n1_Mar2010_cover revised.indd 2 01/10/2010 7:44:45 PM

Contents

Articles

Racial Segregation and the American Foreclosure Crisis Jacob S. Rugh and Douglas S. Massey 629

Stratification by Skin Color in Contemporary Mexico Andrés Villarreal 652

Personal Characteristics, Sexual Behaviors, and Male Sex Work: A Quantitative Approach Trevon D. Logan 679

Differences in Disadvantage: Variation in the Motherhood Penalty across White Women’s Earnings Distribution Michelle J. Budig and Melissa J. Hodges 705

Good Times, Bad Times: Postwar Labor’s Share of National Income in Capitalist Democracies Tali Kristal 729

The Rise of the Nation-State across the World, 1816 to 2001 Andreas Wimmer and Yuval Feinstein 764

Calling for Participation: Requests, Blocking Moves, and Rational (Inter)action in Survey Introductions Douglas W. Maynard, Jeremy Freese, and Nora Cate Schaeffer 791

Erratum 815

Volume 75 Number 5 October 2010

American Sociological Review

The American Sociological Review (ISSN 0003-1224) is published bimonthly in February, April, June, August, October, and December on behalf of the American Sociological Association by Sage Publications, 2455 Teller Road, Thousand Oaks, CA 91320. Copyright ©2010 by American Sociological Association. All rights reserved. No portion of the contents may be reproduced in any form without written permission from the publisher. Periodicals postage paid at Thousand Oaks, California, and at additional mailing offices. POSTMASTER: Send address changes to American Sociological Review, c/o SAGE Publications, Inc., 2455 Teller Road, Thousand Oaks, CA 91320.

Scope and Mission: The American Sociological Review (ASR) publishes original (not previously published) works of interest to the discipline in general, new theoretical developments, results of qualitative or quantitative research that advance our understanding of fundamental social processes, and important methodological innovations. All areas of sociology are welcome. Emphasis is on exceptional quality and general interest.

Ethics: Submission of a manuscript to another professional journal while it is under review by the ASR is regarded by the ASA as unethical. Significant findings or contributions that have already appeared (or will appear) elsewhere must be clearly identified. All persons who publish in ASA journals are required to abide by ASA guidelines and ethics codes regarding plagiarism and other ethical issues. This requirement includes adhering to ASA’s stated policy on data-sharing: “Sociologists make their data available after completion of the project or its major publications, except where proprietary agreements with employers, contractors, or clients preclude such accessibility or when it is impossible to share data and protect the confidentiality of the data or the anonymity of research participants (e.g., raw field notes or detailed information from ethnographic interviews)” (ASA Code of Ethics, 1997).

Manuscript Submission Format: Manuscripts should meet the format guidelines specified in the Notice to Contributors published in the February and August issues of each volume. The electronic files should be composed in MS Word, WordPerfect, or Excel. All text must be printed double-spaced on 8-1/2 by 11 inch white paper. Use Times New Roman, 12-point size font. Margins must be at least 1 inch on all four sides. On the title page, note the manuscript’s total word count (include all text, references, and footnotes; do not include word counts for tables or figures). You may cite your own work, but do not use wording that identifies you as the author.

Submission Requirements: Submit two (2) print copies of your manuscript and an abstract of 150 to 200 words. Include all electronic files on a CD. Enclose a $25.00 manuscript processing fee in the form of a check or money order payable to the American Sociological Association. Provide an e-mail address and ASR will acknowledge the receipt of your manuscript. In your cover letter, you may recom-mend specific reviewers (or identify individuals ASR should not use). Do not recommend colleagues, collaborators, or friends. ASR may choose to disregard your recommendation. Manuscripts are not returned after review.

Address for Manuscript Submission: American Sociological Review, PMB 351803, 2301 Vanderbilt Place, Nashville, TN 37235; phone: 615-343-0426 (e-mail: [email protected]).

Editorial Decisions: Median time between submission and decision is approximately 12 weeks. Please see the ASR journal website for more information (http://www2.asanet.org/journals/asr/).

Non-Member Subscription Information: All non-member subscription inquiries, orders, back issues, claims, and renewals should be addressed to SAGE Publications, 2455 Teller Road, Thousand Oaks, CA 91320; telephone: (800) 818-SAGE (7243) and (805) 499-0721; fax: (805) 375-1700; e-mail: [email protected]; http://www.sagepublications.com. Subscription Price: Institutions: $311 (online/print), $280 (online only). Individual subscribers are required to hold ASA membership. For all customers outside the Americas, please visit http://www.sagepub.co.uk/customerCare.nav for information. Claims: Claims for undelivered copies must be made no later than six months following month of publication. The publisher will supply replacement issues when losses have been sustained in transit and when the reserve stock will permit.

Member Subscription Information: American Sociological Association member inquiries, change of address, back issues, claims, and membership renewal requests should be addressed to the Executive Office, American Sociological Association, 1430 K Street NW, Suite 600, Washington, DC 20005; website: http://www.asanet.org; e-mail: [email protected]. Requests for replacement issues should be made within six months of the missing or damaged issue. Beyond six months and at the request of the American Sociological Association the publisher will supply replacement issues when losses have been sustained in transit and when the reserve stock permits.

Abstracting and Indexing: Please visit http://asr.sagepub.com and, under the “More about this journal” menu on the right-hand side, click on the Abstracting/Indexing link on the left-hand side to view a full list of databases in which this journal is indexed.

Copyright Permission: Permission requests to photocopy or otherwise reproduce material published in this journal should be submitted by accessing the article online on the journal’s website at http://asr.sagepub.com and selecting the “Request Permission” link. Permission may also be requested by contacting the Copyright Clearance Center via their website at http://www.copyright.com, or via e-mail at [email protected].

Advertising and Reprints: Current advertising rates and specifications may be obtained by contacting the advertising coordinator in the Thousand Oaks office at (805) 410-7772 or by sending an e-mail to [email protected]. To order reprints, please e-mail [email protected]. Acceptance of advertising in this journal in no way implies endorsement of the advertised product or service by SAGE or the American Sociological Association. No endorsement is intended or implied. SAGE reserves the right to reject any advertising it deems as inappropriate for this journal.

Change of Address for Non-Members: Six weeks’ advance notice must be given when notifying of change of address. Please send the old address label along with the new address to the SAGE office address above to ensure proper identification. Please specify name of journal.

The American Sociological Association acknowledges with appreciation the facilities and assistance provided by Vanderbilt University.

Printed on acid-free paper

Racial Segregation and theAmerican Foreclosure Crisis

Jacob S. Rugha and Douglas S. Masseya

Abstract

The rise in subprime lending and the ensuing wave of foreclosures was partly a result of mar-ket forces that have been well-identified in the literature, but it was also a highly racializedprocess. We argue that residential segregation created a unique niche of minority clients whowere differentially marketed risky subprime loans that were in great demand for use inmortgage-backed securities that could be sold on secondary markets. We test this argumentby regressing foreclosure actions in the top 100 U.S. metropolitan areas on measures of black,Hispanic, and Asian segregation while controlling for a variety of housing market conditions,including average creditworthiness, the extent of coverage under the Community Reinvest-ment Act, the degree of zoning regulation, and the overall rate of subprime lending. Wefind that black residential dissimilarity and spatial isolation are powerful predictors of fore-closures across U.S. metropolitan areas. To isolate subprime lending as the causal mecha-nism through which segregation influences foreclosures, we estimate a two-stage leastsquares model that confirms the causal effect of black segregation on the number and rateof foreclosures across metropolitan areas. We thus conclude that segregation was an impor-tant contributing cause of the foreclosure crisis, along with overbuilding, risky lending prac-tices, lax regulation, and the bursting of the housing price bubble.

Keywords

segregation, foreclosures, race, discrimination

Four decades after passage of the Fair Hous-

ing Act, residential segregation remains

a key feature of America’s urban landscape.

Levels of black segregation have moderated

since the civil rights era, but declines are

concentrated in metropolitan areas with small

black populations (Charles 2003). In areas

with large African American communities—

places such as New York, Chicago, Detroit,

Atlanta, Houston, and Washington—declines

have been minimal or nonexistent (Iceland,

Weinberg, and Steinmetz 2002). As a result,

in 2000 a majority of black urban dwellers

continued to live under conditions of hyper-

segregation (Massey 2004). At the same

time, levels of Hispanic segregation have

been rising; during the 1990s, Latinos in

New York and Los Angeles joined African

Americans among the ranks of the hyper-

segregated (Wilkes and Iceland 2004).

Although much of the increase in Hispanic

segregation stems from rapid popula-

tion growth during a period of mass immigra-

tion, levels of anti-Latino prejudice and

aPrinceton University, Office of Population

Research

Corresponding Author:Douglas S. Massey, Princeton University, Office

of Population Research, Wallace Hall, Princeton,

NJ 08544

E-mail: [email protected]

American Sociological Review75(5) 629–651� American SociologicalAssociation 2010DOI: 10.1177/0003122410380868http://asr.sagepub.com

discrimination have also risen in recent years

(Charles 2003; Massey 2009; Ross and

Turner 2005). In addition, much research

shows that dark-skinned Latinos experience

higher levels of segregation than do their

light-skinned counterparts (Denton and Mas-

sey 1989; Massey and Bitterman 1985; Mas-

sey and Denton 1992).

During the 1990s, rates of subprime mort-

gage lending, home equity borrowing, and

home ownership increased among minorities;

in the context of high segregation, many

new borrowers were necessarily located in

minority neighborhoods (Been, Ellen, and

Madar 2009; Squires, Hyra, and Renner

2009). Williams and colleagues (2005) esti-

mate, for example, that subprime lending ac-

counted for 43 percent of the increase in

black home ownership during the 1990s and

33 percent of the growth in ownership within

minority neighborhoods. As a result, when the

housing bubble burst in 2007 and deflated in

2008 and 2009, the economic fallout was

unevenly spread over the urban landscape

(Immergluck 2008). Given that segregation

concentrates the effects of any economic

downturn spatially (Massey and Denton

1993), the rise in foreclosures hit black and

Hispanic neighborhoods with particular force

(Bromley et al. 2008; Hernandez 2009; Im-

mergluck 2008; Schuetz, Been, and Ellen

2008).

Economic studies generally conclude that

leveraged refinancing, overbuilding, the col-

lapse of home prices, and a poorly regulated

mortgage market were primarily responsible

for the rise in foreclosures across metropolitan

areas (Doms, Furlong, and Krainer 2007; Ger-

ardi, Shapiro, and Willen 2009; Glaeser,

Gyourko, and Saiz 2008; Haughwout, Peach,

and Tracy 2008; Khandani, Lo, and Merton

2009). We argue that the foreclosure crisis

also had significant racial dimensions.

Although prior research has considered race

as a factor, it was mainly to attribute inter-

group disparities in defaults and foreclosures

to minority group members’ weaker econo-

mic position. A careful reading of recent

scholarship on segregation and mortgage

lending reveals, however, that racial discrimi-

nation occurred at each step in the complex

chain of events leading from loan origination

to foreclosure (Bond and Williams 2007;

Immergluck 2009; Stuart 2003; Williams,

Nesiba, and McConnell 2005; Wyly et al.

2006). Specifically, ongoing residential segre-

gation and a historical dearth of access to

mortgage credit in U.S. urban areas combined

to create ideal conditions for predatory lending

to poor minority group members in poor

minority neighborhoods (Been et al. 2009;

Squires et al. 2009). This racialized the ensu-

ing foreclosure crisis and focused its negative

consequences disproportionately on black bor-

rowers and home owners (Hernandez 2009;

Oliver and Shapiro 2006; Shapiro, Meschede,

and Sullivan 2010; Wyly et al. 2006, 2009).

SEGREGATION AND THEFORECLOSURE CRISIS

High levels of segregation create a natural

market for subprime lending and cause

riskier mortgages, and thus foreclosures, to

accumulate disproportionately in racially

segregated cities’ minority neighborhoods.

By definition, segregation creates minority-

dominant neighborhoods, which, given the

legacy of redlining and institutional discrim-

ination, continue to be underserved by main-

stream financial institutions (Renuart 2004;

Ross and Yinger 2002). Moreover, the finan-

cial institutions that do exist in minority

areas are likely to be predatory—for exam-

ple, pawn shops, payday lenders, and check

cashing services that charge high fees and

usurious rates of interest—so that minority

group members are accustomed to exploita-

tion and frequently unaware that better serv-

ices are available elsewhere (Immergluck

and Wiles 1999). Segregation also spatially

concentrates the disadvantages associated

with minority status, such as poverty and job-

lessness (Massey and Fischer 2000). When

the economy stagnated, families in minority

630 American Sociological Review 75(5)

neighborhoods were more likely than others

to turn to home equity loans as a means of

maintaining consumption, thereby creating

a ready demand for unscrupulous brokers to

exploit (Sullivan, Warren, and Westbrook

2000).

Under conditions of high residential segre-

gation, individual disadvantages associated

with minority status are compounded in space

and amplified in markets that are necessarily

organized geographically (Dymski and Veitch

1992; Immergluck 2008). By concentrating

underserved, financially unsophisticated, and

needy minority group members who are

accustomed to exploitation in certain well-

defined neighborhoods, segregation made it

easy for brokers to target them when market-

ing subprime loans (Stuart 2003). Avery, Bre-

voort, and Canner (2008) found that among

mortgage lenders who went bankrupt in

2007, black borrowers who received loans in

2006 were three times more likely to receive

a subprime than a prime loan (74 versus 26

percent) and Hispanics were twice as likely

to receive a subprime than a prime loan (63

versus 37 percent). By contrast, whites were

slightly more likely to get a prime than a sub-

prime loan from the same lenders (46 versus

54 percent). Among institutions that did not

go bankrupt in 2007, blacks who borrowed in

2006 were just as likely to receive prime as

subprime loans (51 versus 49 percent), under-

scoring the discriminatory nature of predatory

lending practices in the United States.

Securitization and Rewards to

Risky Lending

Residential segregation has always created

dense concentrations of potentially exploitable

clients in need of capital, but in the 1990s,

these borrowers’ attractiveness to mortgage

lenders changed. Before the 1980s, lenders

avoided inner-city minority neighborhoods

through a combination of fear, prejudice,

and institutional discrimination (Squires

1994). The invention of securitized mortgages,

however, changed the calculus of mortgage

lending and made minority households very

desirable as clients. Indeed, the spread of

mortgage-backed securities during the 1980s

transformed home lending throughout the

United States by splitting apart the origination,

servicing, and selling of mortgages into dis-

crete transactions that made it possible for

banks to earn more money quickly by originat-

ing and selling loans than by lending money

and collecting interest payments over time

(Raynes and Rutledge 2003; Sowell 2009).

The advent of securitized mortgages

transformed what had been a bank-based

intermediary credit system into a securities-

based market system (Dymski 2002). In so

doing, the new financial instruments vastly

expanded the pool of money available for

lending. Under traditional systems of lend-

ing, the number of mortgages was limited

by the amount of deposits a bank had on

hand to lend. Under the new system, the vol-

ume of mortgages was no longer limited by

deposits, but by the number of potential bor-

rowers and investors’ willingness to pur-

chase mortgage-backed securities. The new

arrangements thus created a demand on the

part of banks to expand the pool of

borrowers.

Securitized mortgages are not sold whole

but are pooled together and divided into dif-

ferent shares, or tranches, on the basis of

risk (Raynes and Rutledge 2003). High inter-

est mortgages pay more to investors, of

course, but they also carry more risk; to man-

age the risk, financial engineers combined dif-

ferent risk tranches into diversified bonds that

could be sold on secondary markets. By mix-

ing different tranches together, financiers

could create a salable security with almost

any risk rating and interest rate they wished.

In theory, the risk of default by borrowers in

high-risk tranches was offset by the surety

of payments within low-risk tranches, thereby

yielding a relatively safe investment that rat-

ing services beholden to the financiers were

happy to affirm for a generous fee (Raynes

and Rutledge 2003).

Rugh and Massey 631

Because virtually any mortgage, however

shaky, could be sold and repackaged as part

of a collateralized debt obligation, risky bor-

rowers who were formerly shunned by lenders

suddenly became quite attractive. The resul-

tant wave of predatory lending was spear-

headed by independent mortgage brokers

who did not bear the risk of their reckless

lending practices. They simply generated

mortgages and immediately sold them to

banks and other financial institutions, which

in turn capitalized the shaky subprime instru-

ments as securities and sold them to third-

party investors who ended up assuming the

risk, typically in ways they neither appreciated

nor understood (Engel and McCoy 2007;

Lewis 2010; Peterson 2007). These lucrative

subprime lending and securitization practices

did not suddenly appear ‘‘at the fringes of

finance,’’ but were produced and legitimated

by the financial industry using new, high-

tech tools such as credit scoring, risk-based

pricing, securitization, credit default swaps,

and variable rate mortgages that were billed

as rational, scientific, and safe (Langley

2008, 2009; Stuart 2003).

How Segregation Shaped Unequal

Lending

With the move to securitized lending, dis-

crimination in real estate lending shifted

from the outright denial of home loans to

the systematic marketing of predatory loans

to poor black and Hispanic households,

which were easily found within segregated

neighborhoods (Engel and McCoy 2008;

Massey 2005a). Before the subprime boom,

black borrowers were more likely to be

denied loans overall, especially in white

areas, whereas whites were often denied

loans in minority neighborhoods (Holloway

1998). During the boom, minority borrowers’

underserved status made them prime targets

for subprime lenders who systematically tar-

geted their communities for aggressive

marketing campaigns (Dymski and Veitch

1992; Holloway 1998; Stuart 2003). Discrim-

inatory real estate practices (e.g., steering)

prevented black and Latino homebuyers

from accessing better housing and sounder

loan products in affluent suburbs (Friedman

and Squires 2005; Hanlon 2010) and chan-

neled them into depressed inner-ring suburbs

that were undergoing sustained disinvest-

ment (Hackworth 2007).

In a very real way, as Williams and col-

leagues (2005) show, the old inequality in

home lending made the new inequality possi-

ble by creating geographic concentrations of

underserved, unsophisticated consumers that

unscrupulous mortgage brokers could easily

target and efficiently exploit (see also Hernan-

dez 2009; Lee 1999). A study of subprime

borrowers in Los Angeles, Oakland, Sacra-

mento, and San Diego found that African

Americans were significantly more likely

than whites (40 versus 24 percent) to report

lender marketing efforts as the impetus for

taking out a home equity loan (California

Reinvestment Committee 2001). In the end,

subprime lending not only saddled borrowers

with onerous terms and unforeseen risks, but

it also reinforced existing patterns of racial

segregation and deepened the black-white

wealth gap (Bond and Williams 2007; Fried-

man and Squires 2005; Williams et al. 2005).

In the new regime of racial inequality,

African American and Latino homeowners

bore a disproportionate share of costs stem-

ming from the bursting of the housing bubble.

Compared with whites with similar credit pro-

files, down payment ratios, personal charac-

teristics, and residential locations, African

Americans were much more likely to receive

subprime loans (Avery, Brevoort, and Canner

2007; Avery, Canner, and Cook 2005; Bocian,

Ernst, and Li 2006; Pennington-Cross, Yezer,

and Nichols 2000). Moreover, after control-

ling for background factors, black and His-

panic homeowners were significantly more

likely than whites to receive loans with unfa-

vorable terms such as prepayment penalties

(Bocian et al. 2006; Farris and Richardson

2004; Quercia, Stegman, and Davis 2007;

632 American Sociological Review 75(5)

Squires 2004), higher cost ratios (Elliehausen,

Staten, and Steinbuks 2008; LaCour-Little and

Holmes 2008), and higher rate spreads (Bo-

cian et al. 2006). The racial gap in subprime

lending holds across all income levels (Brom-

ley et al. 2008; Immergluck and Wiles 1999;

Williams et al. 2005), with perhaps an

increase at higher income levels (Institute on

Race and Poverty 2009; Williams et al. 2005).

During the 1990s, the United States was

increasingly characterized by a dual, racially

segmented mortgage market, one that was

structured by the race of borrowers and the

racial composition of neighborhoods (Apgar

and Calder 2005; Stuart 2003; U.S. Depart-

ment of Housing and Urban Development

2000). Controlling for neighborhood charac-

teristics, the incidence of subprime lending

was significantly greater among black and

Hispanic borrowers (Calem, Hershaff, and

Wachter 2004) and among people who had

not gone to college (Manti, Raca, and Zorn

2004). As a result, from 1993 to 2000, the

share of subprime mortgages going to house-

holds in minority neighborhoods rose from 2

to 18 percent (Williams et al. 2005).

The rise of racially targeted subprime lend-

ing destabilized minority neighborhoods by

increasing turnover (Gerardi and Willen

2008), and the destabilizing effects on home-

ownership did not remain confined to minor-

ity neighborhoods, but spilled over into

adjacent white and mixed neighborhoods

(Schuetz et al. 2008). National evidence

from a longitudinal study of homeowners

from 1999 to 2005 shows that the racial gap

in homeownership exit rates widened in

a way that cannot be explained by social, eco-

nomic, or financial factors that historically ac-

counted for black-white differentials (Turner

and Smith 2009). The coincidence of the

peak in subprime lending with the inexplica-

ble decline in the stability of black home own-

ership and exit rates offers compelling

evidence that segregation and the new face

of unequal lending combined to undermine

black residential stability and erode any accu-

mulated wealth (Shapiro et al. 2010).

Race and the Housing Bust

From a lender’s perspective, the new system

worked well as long as real estate and lend-

ing markets remained liquid and housing pri-

ces continued to rise. For a while, minority

ownership rates rose and everyone involved

in securitized lending made good money—

the broker who originated the loan, the lender

who put up the money, the firm that pack-

aged and underwrote the mortgage-backed

security, the rating agency that affirmed its

creditworthiness, and the company that

insured the investments through novel instru-

ments known as credit default swaps. To

keep the system in operation and profits roll-

ing in, however, more borrowers had to be

constantly found and housing prices had to

continue rising. As the number of buyers

increased and housing prices inflated, a spec-

ulative fever took hold (Andrews 2009; Shil-

ler 2008). People began to finance home

purchases on the assumption that home

prices would rise indefinitely (Khandani et

al. 2009), buying properties with interest-

only loans, waiting for real estate prices to

rise, and then ‘‘flipping’’ the properties to

realize the capital gain. Research shows

that minority-owned properties were more

likely than others to be involved in loan flip-

ping and equity stripping schemes (Immer-

gluck and Wiles 1999).

After 2004, as the market peaked, specula-

tors, dubious lenders, negligent securities

dealers, and compromised ratings firms

increasingly focused on a select few booming

regional markets, such as Las Vegas, Phoenix,

and South Florida. These markets appear to

have played a large role in the final run-up

in risky lending. At the height of the bubble,

fraud may have been the rule rather than the

exception. When Pendley, Costello, and

Kelsch (2007:4) analyzed a sample of delin-

quent subprime loans made in 2006, for exam-

ple, they found widespread ‘‘appearance of

fraud or misrepresentation’’; two-thirds of

stated owner-occupied dwellings were never

actually occupied, and nearly half of all

Rugh and Massey 633

claims to first-time ownerships did not appear

to be valid. These findings suggest that the in-

flated housing bubble motivated sophisticated

lenders, brokers, and buyers to engage in an

unparalleled level of deceit.

As the market became fully saturated in

2006, housing prices ultimately stalled, fore-

closures rose, and faith in mortgage-backed

securities evaporated, bringing down the

entire system of collateralized debt obliga-

tions and taking much of the U.S. economy

with it (Khandani et al. 2009; Shiller 2008).

Ultimately, brokers, lenders, securitizers, and

most of all, ratings agencies, failed to foresee

the perils of ‘‘default correlation,’’ or the

interrelated risks bound up in interconnected

portfolios of troubled loans (Langley 2009).

The utter collapse of subprime lending

exposed the extremes of a pricing regime

that assessed risks individually but not collec-

tively, not accounting for the aggregate risk of

ever-increasing subprime lending and securiti-

zation. Less than 1 percent of mortgage loans

were in foreclosure at the end of 2005; this

rate more than quadrupled to over 4.6 percent

by the end of 2009. At the same time, the fore-

closure rate on riskier subprime loans went

from 3.3 percent in 2005 to 15.6 percent in

2009 (Mortgage Bankers Association 2006,

2010).

The resulting tidal wave of foreclosures

was concentrated in areas that only a few

years earlier had been primary targets for the

marketing of subprime loans (Bond and Wil-

liams 2007; Edmiston 2009), and minority

neighborhoods often bore the brunt of the

foreclosures (Bromley et al. 2008; Edmiston

2009; Hernandez 2009; Immergluck 2008;

Institute on Race and Poverty 2009; Mallach

2009; Marquez 2008). In the end, the housing

boom and the immense profits it generated

frequently came at the expense of poor minor-

ities living in central cities and inner suburbs

who were targeted by specialized mortgage

brokers and affiliates of national banks and

subjected to discriminatory lending practices

(Been et al. 2009; Engel and McCoy 2008;

Peterson 2007; Powell 2010; Squires et al.

2009).

Two additional lines of research also sug-

gest that predatory lending and subsequent

asset stripping were structured on the basis

of race as well as class. First, contrary to con-

ventional wisdom, the housing crisis was not

caused primarily by a decline in underwriting

standards (Haughwout 2009; see also Khan-

dani et al. 2009). Bhardwaj and Sengupta

(2009) show, for example, that average credit

scores within the subprime loan sector actu-

ally increased in years prior to the housing

bust and that most of the loans fell into the

near-prime, low- or no-documentation ‘‘Alt-

A’’ category, rather than in more speculative

B and C categories. Second, the crisis cannot

be attributed to riskier lending engendered by

the Community Reinvestment Act (CRA).

Using a regression discontinuity design,

Bhutta (2008) examined lending rates just

below and above the CRA neighborhood

income cutoff and found that while CRA

oversight did increase lending in targeted

areas, unregulated lending activity also

increased substantially in the same places.

Only 6 percent of subprime loans were

made to low-income borrowers or individuals

in neighborhoods subject to CRA oversight,

and less than 2 percent of loans that originated

with unregulated independent mortgage

brokers were CRA credit-eligible (Bhutta

and Canner 2009).

Although lending standards often left much

to be desired, it appears that ongoing racial

segregation, discriminatory lending, and an

overheated housing market combined to leave

minority group members uniquely vulnerable

to the housing bust. As Immergluck (2009)

wryly notes, financial literacy and creditwor-

thiness did not suddenly plummet on the eve

of the crisis—home prices did. At the same

time, although CRA regulations stimulated

lending to minority households in low-income

neighborhoods, the increase was not nearly

enough to bring about the housing crisis

(Bhutta and Canner 2009; Park 2008).

634 American Sociological Review 75(5)

DATA SOURCES

From the above research, we conclude that

residential segregation was significant in

structuring how the rise of predatory lending

and the consequent wave of foreclosures

played out in U.S. housing markets (Bond

and Williams 2007; Engel and McCoy

2008; Hernandez 2009; Stuart 2003; Wil-

liams et al. 2005; Wyly et al. 2006, 2009).

We hypothesize, first, that segregation facil-

itated racially targeted subprime mortgage

lending during the boom and, second, that

it magnified the consequences of the housing

crisis for blacks and Latinos by concentrating

foreclosures in poor minority neighborhoods

during the bust. To test these assertions, we

draw on two principal sources of data. We

define our dependent variables based on

data obtained from RealtyTrac, the nation’s

largest provider of foreclosure listings. We

compute the number of properties with

at least one foreclosure action in 2006,

2007, and 2008 in the nation’s 100 largest

metropolitan statistical areas and divisions

(MSAs), as defined in 2003. We then divide

this figure by the number of housing units in

2006 to derive a foreclosure rate.1 Over 77

percent of all foreclosure properties during

the period under consideration were located

in this set of MSAs. This sample is especially

useful for making inferences about minorities

in the United States because these 100 MSAs

were home to over 75 percent of African

Americans, nearly 80 percent of Hispanics,

and 90 percent of Asians in the country in

2000.

Our principal explanatory variables are

measures of residential unevenness and spatial

isolation for Hispanics, African Americans,

and Asians computed across census tracts in

the top 100 metropolitan areas (see Iceland

et al. 2002). We measured unevenness with

the well-known index of dissimilarity and iso-

lation using the P* within-group isolation

index. The former gives the relative propor-

tion of minority group members who would

have to exchange tracts with majority group

members to achieve an even residential distri-

bution; the latter gives the proportion of own-

group members in a tract inhabited by the

average minority group member. Of the five

dimensions of segregation identified by Mas-

sey and Denton (1988), evenness and isolation

are the most important and empirically

account for most of the common variation

(Massey, White, and Phua 1996).

Our analytic strategy is to regress the num-

ber and rate of foreclosures in MSAs on these

two measures of segregation while holding

constant the effect of metropolitan-level fac-

tors shown to influence the odds of foreclo-

sure. Our controls include standard census-

based variables, such as 2008 MSA popula-

tion and racial and ethnic composition from

2000, as well as socioeconomic characteristics

obtained from the 2005 to 2007 American

Community Surveys, such as percent of per-

sons holding a college degree, median house-

hold income, and percent of homeowners with

a second mortgage (all defined as of 2006).

We also include the median age of MSA

housing stock from the 2000 housing census.

The 2006 unemployment rate and the 2000

to 2006 change in rate of annual unemploy-

ment come from the Bureau of Labor Statis-

tics; the share of the workforce that was

unionized comes from Hirsch and MacPher-

son (2007). In initial specifications of the

model we also tested for effects of the poverty

rate, share of female-headed households, and

per capita income, but these variables add

nothing to the explanatory power of the mod-

els and were dropped from further consider-

ation. The final models also include dummy

variables to control for region, coastal loca-

tion, and location along the Texas border

with Mexico (the Rio Grande River).

In addition to these standard indicators, we

include three specialized measures of condi-

tions in metropolitan real estate markets that

prior research finds to be important in explain-

ing the foreclosure crisis. First, we construct

a measure of overbuilding by computing the

ratio of 2000 to 2006 MSA housing starts to

housing units in 2000, a procedure closely

Rugh and Massey 635

following that of Glaeser and colleagues

(2008). Second, we include the Wharton Res-

idential Land Use Regulation Index as a mea-

sure of local land use planning regulation.

Gyourko, Summers, and Saiz (2008) devel-

oped this index for different municipalities;

following Rothwell and Massey (2009), we

take the weighted average of the index for

municipalities within each MSA that responds

to Gyourko’s survey. We then center the dis-

tribution on the mean for the top 100 areas to

yield a measure that controls for housing price

premiums stemming from regulatory con-

straints on housing supply (Fischel 1990;

Glaeser 2009; Glaeser and Gyourko 2003,

2008; Glaeser et al. 2008). Finally, we include

a measure of the housing price boom in each

MSA by using the Federal Housing Finance

Agency’s quarterly metropolitan area House

Price Index (HPI), which is a weighted,

repeat-sales index based on transactions

involving single-family homes. We bench-

mark the housing price boom for each MSA

by dividing annualized change in HPI from

2000 to 2006 by the annualized change in

the two decades prior to 2000.

We also include MSA-level controls for

the degree of subprime lending, the extent of

CRA regulatory oversight, and borrowers’

average creditworthiness. To assess the preva-

lence of subprime lending, we compute the

aggregate share of all loans originated in

2004, 2005, and 2006 that were subprime,

drawing on data from the Federal Financial

Institutions Examination Council (http://

www.ffiec.gov/hmda). The FFIEC tabulates

information that lending institutions must pro-

vide to the federal government under the

Home Mortgage Disclosure Act (HMDA).

These data cover more than 28 million loans

originated during the peak years of the hous-

ing boom. More than 6.9 million loans, or

nearly one in four, were subprime, meaning

that the interest rate at origination exceeded

that for a comparable U.S. Treasury security

(e.g., a 30-year bond) by 3 percent or more.

This is the cutoff for reporting a loan in the

data files (rates of lower priced loans are

intentionally left blank in fields) and is the

definition of subprime lending used in other

research (e.g., Been et al. 2009; Bocian

et al. 2006; Squires et al. 2009).2

To measure the degree of regulatory over-

sight, we draw on 2004 to 2006 HMDA data

and compute the weighted share (by dollar

amount) of all 2004 to 2006 loans in each

MSA that were originated by CRA-covered

lending banking institutions (following Fried-

man and Squires 2005). In doing so, we use

HMDA data on conventional loans (i.e., those

not guaranteed by government) for the pur-

chase of single-family properties (1 to 4 units)

and take a 20 percent extract of the nearly 28

million mortgage loans originated in the top

100 metropolitan areas and compute the share

of subprime loans going to borrowers. On

average, less than two-thirds of total lending

per MSA fell under the ambit of federal

CRA regulation, but this share is noticeably

lower, about half or less, in MSAs with ele-

vated foreclosures (e.g., Detroit, Michigan;

Las Vegas, Nevada; and Bakersfield, Califor-

nia). This suggests that greater CRA lending

oversight reduces foreclosures even as it

makes more loans available to minority group

members (Bond and Williams 2007; Friedman

and Squires 2005).

Finally, to control for borrowers’ credit-

worthiness, we compute the average consumer

credit score at the MSA level using informa-

tion obtained from the Experian National

Score Index. The index ranges from 672 to

720 for the top 100 MSAs and constitutes

the mean FICO (Fair Isaac Corporation) credit

score for all consumers living in all counties

of each MSA whose credit behavior is re-

ported to Experian, one of the nation’s three

major credit reporting bureaus. We expect

that higher overall MSA credit scores will

be associated with lower foreclosure rates

because of the higher aggregate creditworthi-

ness of borrowers, and by extension, mortgage

holders. To mitigate omitted variables bias,

we include this variable as a proxy for differ-

ences in credit history and access that co-vary

with racial composition and segregation.

636 American Sociological Review 75(5)

Table 1 presents means and standard devi-

ations of the foregoing variables. In terms of

our leading explanatory variable, levels of

segregation are highest for African Ameri-

cans, lowest for Asians, and Hispanics are

in-between. The index of dissimilarity, for

example, averages .59 for blacks with a range

of plus or minus two standard deviations that

goes from .34 to .83. By convention, dissimi-

larities below .3 are considered low, those

from .3 to .6 are considered moderate, and

those above .6 are regarded as high, with any-

thing above .75 considered extremely high.

Under these criteria, black segregation runs

from moderate to extremely high. By contrast,

the comparable range for Asians is .25 to .52

with a mean of .39, and Hispanics have a range

of .24 to .67 with a mean of .46. Asians range

from low to moderate, and Hispanics range

from low to high.

Similar patterns prevail with respect to the

isolation index. The black isolation index

averages .45 and ranges from .07 to .84, going

from minus to plus two standard deviations;

the Hispanic index averages .32 and ranges

from zero to .75; and the Asian mean stands

at a very low .14 and ranges from zero to

.40. If segregation creates a natural niche for

subprime lending, then the more extreme

maxima and greater variability of black segre-

gation measures hold by far the greatest

potential to predict foreclosures, followed by

Hispanic segregation measures. The generally

low averages and restricted variation of isola-

tion and dissimilarity among Asians suggest

a more limited potential to influence inter-

metropolitan variation in foreclosures.

Segregation’s effect in creating fertile ter-

rain for subprime lending also depends on

a group’s socioeconomic status. This general-

ization holds because segregation not only

concentrates minority group members spa-

tially within particular neighborhoods, but it

also concentrates any characteristic associated

with minority group status (Massey and Den-

ton 1993; Massey and Fischer 1999). For

underprivileged minorities, segregation spa-

tially concentrates poverty and its correlates

to create areas of concentrated disadvantage

that constitute prime targets for subprime

lending. For privileged minorities, segregation

has the opposite effect—it concentrates

advantage and its correlates to produce areas

that are unlikely targets for subprime lending.

As of 2008, the poverty rate for Asians stood

at 12 percent, compared with 25 percent

among African Americans and 23 percent

among Hispanics (DeNavas-Walt, Proctor,

and Smith 2009). Likewise, the median per

capita income for Asians was $30,000 in

2008, compared with just $18,000 for Afri-

can Americans and $16,000 for Hispanics.

The Asian median income even exceeded

that for non-Hispanic whites ($28,500). To

the extent that segregation has an effect

on the economic geography of Asians, it

would be to concentrate advantage and

thus diminish the frequency of subprime

lending and foreclosures.3

SEGREGATION’S EFFECT ONFORECLOSURES

Despite the persistence of residential segre-

gation and its prevalence in areas with large

minority populations, racial segregation is

no longer as universal across U.S. urban

areas as it once was. As indicated by the

wide variance just described, there is now

considerable variation across metropolitan

areas in the degree of black and Hispanic

segregation (Charles 2003; Iceland et al.

2002; Massey, Rothwell, and Domina

2009). In addition to a small minority popu-

lation, other characteristics that predict lower

levels of residential segregation are a small

urban population, newer housing stock, pres-

ence of a college or a university, proximity to

a military base, higher socioeconomic status,

and location in the West or the Southwest

(Farley and Frey 1994). Inter-urban differen-

tials in Hispanic and black segregation thus

carry the potential to contribute significantly

to variation in foreclosure rates across U.S.

metropolitan areas.

Rugh and Massey 637

To assess the effect of segregation on fore-

closures, we estimate a simple OLS multiple

regression model defined by the equation:

F ¼ aþ b1S þ b2Z þ e ð1Þ

where F represents either the log of the total

number of foreclosure filings or the log of

foreclosures per housing unit, a is the inter-

cept, S is a vector of segregation measures

with associated coefficients b1 , Z is a vector

of control variables with associated coeffi-

cients b2, and e is the error term.4 Table 2

presents estimates of equations that use dis-

similarity and isolation indices to predict the

log of total foreclosures by MSA; Table 3

shows estimates that predict the log of fore-

closure rates by MSA.

In both tables the models fit the data

extremely well, with the predictor variables

explaining, on average, 77 percent of the var-

iance in the log of the foreclosure rate and 90

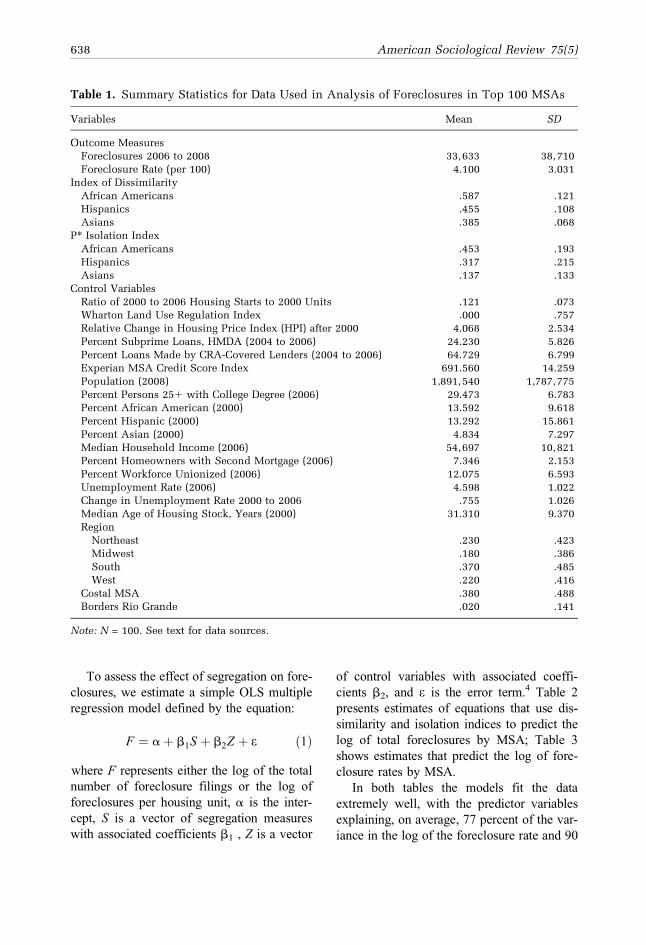

Table 1. Summary Statistics for Data Used in Analysis of Foreclosures in Top 100 MSAs

Variables Mean SD

Outcome Measures

Foreclosures 2006 to 2008 33,633 38,710

Foreclosure Rate (per 100) 4.100 3.031

Index of Dissimilarity

African Americans .587 .121

Hispanics .455 .108

Asians .385 .068

P* Isolation Index

African Americans .453 .193

Hispanics .317 .215

Asians .137 .133

Control Variables

Ratio of 2000 to 2006 Housing Starts to 2000 Units .121 .073

Wharton Land Use Regulation Index .000 .757

Relative Change in Housing Price Index (HPI) after 2000 4.068 2.534

Percent Subprime Loans, HMDA (2004 to 2006) 24.230 5.826

Percent Loans Made by CRA-Covered Lenders (2004 to 2006) 64.729 6.799

Experian MSA Credit Score Index 691.560 14.259

Population (2008) 1,891,540 1,787,775

Percent Persons 251 with College Degree (2006) 29.473 6.783

Percent African American (2000) 13.592 9.618

Percent Hispanic (2000) 13.292 15.861

Percent Asian (2000) 4.834 7.297

Median Household Income (2006) 54,697 10,821

Percent Homeowners with Second Mortgage (2006) 7.346 2.153

Percent Workforce Unionized (2006) 12.075 6.593

Unemployment Rate (2006) 4.598 1.022

Change in Unemployment Rate 2000 to 2006 .755 1.026

Median Age of Housing Stock, Years (2000) 31.310 9.370

Region

Northeast .230 .423

Midwest .180 .386

South .370 .485

West .220 .416

Costal MSA .380 .488

Borders Rio Grande .020 .141

Note: N = 100. See text for data sources.

638 American Sociological Review 75(5)

percent of the variance in the logged absolute

number of foreclosures. Moreover, coeffi-

cients for the segregation indices closely

follow theoretical expectations. Whether mea-

sured in terms of residential dissimilarity or

spatial isolation, segregation of African Amer-

icans is a powerful and highly significant pre-

dictor of the number and rate of foreclosures

across U.S. metropolitan areas. For instance,

a .1 unit increase in black dissimilarity is asso-

ciated with 37 percent more foreclosure ac-

tions and a 34 percent increase in the

foreclosure rate. Inter-metropolitan variation

in the segregation of Hispanics, however,

does not consistently affect the rate and abso-

lute number of foreclosures. As we discuss in

the next section, the effect of Hispanic segre-

gation may be overwhelmed by the effect of

black segregation. These statistical estimates

are consistent with the findings of Been and

colleagues (2009) and Squires and colleagues

(2009).

By contrast, Asian-white residential dis-

similarity significantly reduces the number

and rate of foreclosures across metropolitan

areas, and spatial isolation also has a negative,

Table 2. OLS Estimates of Effect of Selected Measures of Residential Segregation on Log ofTotal Foreclosures

Dissimilarity Index Isolation Index

Variables B SE B SE

Index of Segregation

African Americans 3.718** .725 2.122** .619

Hispanics 2.773 .596 .080 .656

Asians 22.080* .920 22.161 1.636

Control Variables

Housing Starts Ratio 2.980** .960 3.067** 1.077

Wharton Land Use Index .250** .082 .272** .096

Change in Housing Price Index .082** .024 .092** .029

CRA-Covered Lending Share 21.295 .912 2.810 1.061

Subprime Loan Share 3.022* 1.353 4.310** 1.581

MSA Credit Score Index 2.015* .007 2.016* .007

Log of Population 1.008** .089 1.013** .093

Percent with College Degree 21.341 1.315 2.997 1.459

Log Median Household Income .253 .509 .340 .515

Percent with Second Mortgage .751 3.687 .225 4.350

Percent Workforce Unionized 2.025** .011 2.022* .011

Unemployment Rate 2.010 .064 .012 .071

Change in Unemployment Rate .245** .052 .213** .063

Age of Housing Stock .004 .012 .014 .013

Region

Midwest .434* .200 .631** .200

South .042 .257 .081 .296

West .463 .384 .679 .436

Coastal MSA 2.053 .123 .070 .133

Borders Rio Grande 21.030** .370 21.054** .380

Constant 1.960 7.557 .979 8.150

R2 .91 .90

Joint F-Test for Region 3.35* 7.97**

Joint F-Test for Segregation 10.48** 6.28**

Note: N = 99. Robust standard errors. Model also includes percent black, percent Hispanic, and percentAsian.*p \ .05; **p \ .01 (two-tailed tests).

Rugh and Massey 639

although insignificant, effect. Residential seg-

regation concentrates group characteristics,

whatever they are, in space. In the case of

blacks, the prevailing characteristics are pov-

erty and socioeconomic deprivation; given

that Asian incomes exceed those of whites,

on average, their prevailing characteristics

are affluence and socioeconomic privilege.

By concentrating affluence, the segregation

of Asians creates communities that are inher-

ently resistant to the entreaties of subprime

lenders—hence the negative relationship

between Asian segregation and foreclosures.

The various control variables generally

function as hypothesized, lending face validity

to the equation estimates. As expected, fore-

closures are positively predicted by greater

housing start shares, higher rates of subprime

lending, increasing unemployment, rising

home prices, lower credit scores, more second

mortgages, higher median incomes, greater

levels of land use regulation, and location in

the Midwest or the West.5 If we assume that

the housing start ratio measures overbuilding

and that rising relative home prices capture

the housing bubble, then our results are

Table 3. OLS Estimates of Effect of Selected Measures of Residential Segregation on the Logof the Foreclosure Rate

Dissimilarity Index Isolation Index

Variables B SE B SE

Index of Segregation

African Americans 3.412** .725 1.990** .604

Hispanics 2.686 .580 .074 .642

Asians 21.7611 .906 21.572 1.562

Control Variables

Housing Starts Ratio 2.868** .946 2.973** 1.032

Wharton Land Use Index .236** .081 .259** .092

Change in Housing Price Index .072** .023 .080** .027

CRA-Covered Lending Share 21.331 .901 2.847 1.026

Subprime Loan Share 3.269* 1.358 4.560** 1.547

MSA Credit Score Index 2.0141 .007 2.015* .007

Log of Population .012 .087 .010 .089

Percent with College Degree 21.746 1.291 21.420 1.410

Log Median Household Income .750 .489 .8581 .500

Percent with Second Mortgage 1.468 3.643 .703 4.190

Percent Workforce Unionized 2.027* .010 2.024* .011

Unemployment Rate .016 .063 .031 .068

Change in Unemployment Rate .224** .051 .200** .060

Age of Housing Stock .003 .012 .012 .013

Region

Midwest .409* .194 .583** .192

South .032 .251 .072 .286

West .448 .372 .663 .422

Coastal MSA 2.077 .124 .030 .129

Borders Rio Grande 21.040* .392 21.042* .395

Constant 1.121 7.443 .098 8.005

R2 .78 .76

Joint F-Test for Region 3.17* 7.44**

Joint F-Test for Segregation 8.71** 5.62**

Note: N = 99. Robust standard errors. Model also includes percent black, percent Hispanic, and percentAsian.1p \ .10; *p \ .05; **p \ .01 (two-tailed tests).

640 American Sociological Review 75(5)

consistent with prior work on the economic

causes of the U.S. foreclosure crisis (e.g.,

Glaeser et al. 2008; Haughwout et al. 2008;

Immergluck 2009; Kochhar, Gonzalez-Bar-

rera, and Dockterman 2009; Mayer, Pence,

and Sherlund 2009; National Association of

Realtors 2004).

In the attempt to understand the foreclo-

sure crisis, our study adds the important

and independent role played by racial segre-

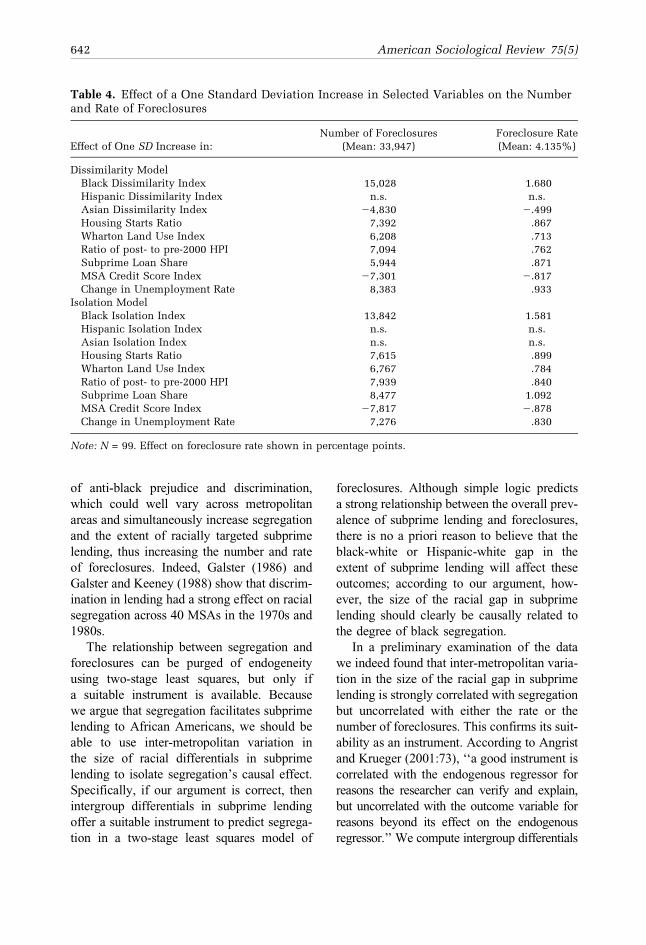

gation in structuring the housing bust. Table

4 shows segregation’s relative predictive

power compared with other significant fac-

tors by reporting the standardized effect

sizes evaluated at the sample mean of the

foreclosure total and rate (in terms of num-

ber of foreclosures and percentage points,

respectively). In the model using dissimilar-

ity indexes, a standard deviation increase in

the segregation of African Americans in-

creases the number of foreclosures by

15,028 actions and the rate of foreclosures

by 1.68 percentage points. This effect ex-

ceeds the effect of MSA home building,

house price booms, and all other important

explanatory variables. Changes in the proxy

measures of economic conditions, land use

restrictions, and overbuilding exert a consid-

erably smaller impact on foreclosures, with

absolute standard effect sizes just 40 to 56

percent of that for black segregation.

In the isolation model, one standard devia-

tion in black segregation leads to a large

change in foreclosures (13,842) and the fore-

closure rate (1.58 percentage points). Stan-

dardized changes in the subprime lending

share lead to an increase of nearly 8,500 fore-

closures and an even greater effect on foreclo-

sure rates, at 1.1 percentage points. Relative

changes in house prices and housing starts,

average credit scores, and changes in unem-

ployment rates show an increase of 7,000 to

8,000 foreclosures and .8 to .9 percentage

points in the foreclosure rate. While the effect

size of Hispanic segregation in the dissimilar-

ity model is not statistically distinguishable

from zero, Hispanic isolation has a standard-

ized effect of more than 3,800 foreclosures

and a .66 percentage point increase in the

foreclosure rate.

FORECLOSURES AND THESEGREGATION-SUBPRIMELINK

Taking into account the distribution of effect

sizes estimated in Table 4, we conclude that

the influence of black residential segregation

clearly exceeds that of other factors linked by

earlier studies to inter-metropolitan variation

in foreclosures. Furthermore, racial segrega-

tion is an important and hitherto unappreci-

ated contributing cause of the current

foreclosure crisis. This conclusion rests, of

course, on a cross-sectional ecological

regression and thus may be subject to certain

methodological criticisms. Because we are

not seeking to infer individual behavior

from aggregate data, ecological bias itself is

not an issue—our argument is structural

and specified at the metropolitan, not the

individual, level.

As with any cross-sectional analysis, how-

ever, endogeneity or reverse causality is

a potential problem. In this case, it does not

seem likely that foreclosures could reasonably

cause segregation. Patterns of racial segrega-

tion are the cumulative product of decades

of actions in the public and private spheres,

and high levels of black segregation were

well institutionalized in U.S. urban areas by

the mid-twentieth century (Massey and Den-

ton 1993). In addition, we measure segrega-

tion in 2000 and foreclosures in 2006 to

2008, so the independent variable is tempo-

rally prior to the dependent variable.

A more serious threat to causal inference is

endogeneity. Perhaps there is a third, unmea-

sured variable that influences both segregation

and foreclosures to bring about the observed

association between them. Although we

endeavored to apply a rather exhaustive set

of controls, it is simply not possible to control

for all potential confounding variables. One

possible confounding variable is the degree

Rugh and Massey 641

of anti-black prejudice and discrimination,

which could well vary across metropolitan

areas and simultaneously increase segregation

and the extent of racially targeted subprime

lending, thus increasing the number and rate

of foreclosures. Indeed, Galster (1986) and

Galster and Keeney (1988) show that discrim-

ination in lending had a strong effect on racial

segregation across 40 MSAs in the 1970s and

1980s.

The relationship between segregation and

foreclosures can be purged of endogeneity

using two-stage least squares, but only if

a suitable instrument is available. Because

we argue that segregation facilitates subprime

lending to African Americans, we should be

able to use inter-metropolitan variation in

the size of racial differentials in subprime

lending to isolate segregation’s causal effect.

Specifically, if our argument is correct, then

intergroup differentials in subprime lending

offer a suitable instrument to predict segrega-

tion in a two-stage least squares model of

foreclosures. Although simple logic predicts

a strong relationship between the overall prev-

alence of subprime lending and foreclosures,

there is no a priori reason to believe that the

black-white or Hispanic-white gap in the

extent of subprime lending will affect these

outcomes; according to our argument, how-

ever, the size of the racial gap in subprime

lending should clearly be causally related to

the degree of black segregation.

In a preliminary examination of the data

we indeed found that inter-metropolitan varia-

tion in the size of the racial gap in subprime

lending is strongly correlated with segregation

but uncorrelated with either the rate or the

number of foreclosures. This confirms its suit-

ability as an instrument. According to Angrist

and Krueger (2001:73), ‘‘a good instrument is

correlated with the endogenous regressor for

reasons the researcher can verify and explain,

but uncorrelated with the outcome variable for

reasons beyond its effect on the endogenous

regressor.’’ We compute intergroup differentials

Table 4. Effect of a One Standard Deviation Increase in Selected Variables on the Numberand Rate of Foreclosures

Effect of One SD Increase in:

Number of Foreclosures

(Mean: 33,947)

Foreclosure Rate

(Mean: 4.135%)

Dissimilarity Model

Black Dissimilarity Index 15,028 1.680

Hispanic Dissimilarity Index n.s. n.s.

Asian Dissimilarity Index 24,830 2.499

Housing Starts Ratio 7,392 .867

Wharton Land Use Index 6,208 .713

Ratio of post- to pre-2000 HPI 7,094 .762

Subprime Loan Share 5,944 .871

MSA Credit Score Index 27,301 2.817

Change in Unemployment Rate 8,383 .933

Isolation Model

Black Isolation Index 13,842 1.581

Hispanic Isolation Index n.s. n.s.

Asian Isolation Index n.s. n.s.

Housing Starts Ratio 7,615 .899

Wharton Land Use Index 6,767 .784

Ratio of post- to pre-2000 HPI 7,939 .840

Subprime Loan Share 8,477 1.092

MSA Credit Score Index 27,817 2.878

Change in Unemployment Rate 7,276 .830

Note: N = 99. Effect on foreclosure rate shown in percentage points.

642 American Sociological Review 75(5)

in subprime lending by metropolitan area

using the combined HMDA data from

2004, 2005, and 2006 (described in the

Data Sources section). If lending discrimi-

nation is greater in more segregated MSAs,

then racial-ethnic differentials in subprime

lending permit us to identify the causal

effect of residential segregation on MSA

foreclosure rates, enabling us to specify

the following two-stage model:

S ¼ hþ dRACEDIFF þWlþ n ð2Þ

F ¼ aþ ðhþ RACEDIFFd

þWlþ nÞb1 þ Zb2 þ e:ð3Þ

In this system, Equation 2 expresses the

first-stage relationship between segregation,

S, and RACEDIFF, the black-white or

Hispanic-white gap in the likelihood of ob-

taining a subprime loan in 2006. In this equa-

tion, d is the coefficient associated with this

variable; W is a vector of controls including

percent black, percent Hispanic, and percent

Asian; l is a vector of coefficients associated

with these variables; and n is the error term.

Equation 3 simply substitutes the value of seg-

regation predicted from this first-stage equa-

tion into Equation 1 to yield a second-stage

equation that expresses foreclosures as a func-

tion of the segregation instrument plus the

variables in Z. b1 and b2 are then re-estimated

in the second-stage equation, along with e.

To generate a more refined measure of

lending discrimination to use as our instru-

ment, we estimate black-white and Hispanic-

white differentials in the likelihood of receiv-

ing a subprime loan after adjusting for bor-

rower and neighborhood characteristics

reported in the HMDA data. That is, using

an extract of 5,360,007 HMDA loan-level

records with non-missing data, we predict

RACEDIFF for each MSA using a probit

model where the dependent variable is

a dichotomous indicator equal to one if the

loan is flagged as subprime in the data by

a non-missing interest rate greater than or

equal to 3 percent. The probit model expresses

the likelihood of receiving a subprime loan as

a function of the type (i.e., home purchase,

refinance, or improvement) and amount of

the loan, borrower income, first or second

lien status, occupancy (i.e., investor or

owner), type of loan purchaser (i.e., govern-

ment agency, private, bank, finance company,

lender affiliate, or other independent entity),

median tract income and tract-to-MSA ratio,

ratio of total tract single-family units to popu-

lation, and tract minority percentage.

We also merge the following extended

control variables to the foregoing data com-

puted from the HMDA data: tract population

density in persons per square mile, median

age of tract housing stock, and the MSA-level

average credit score index, described earlier.

The probit estimation clusters errors at the

MSA level. Avery and colleagues (2005)

show that HMDA data file variables explain

nearly half (48 percent) of the black-white

gap in subprime lending, whereas credit fac-

tors such as FICO scores, loan-to-value ratios,

and interest rate type account for only an addi-

tional one-sixth (17 percent) of the observed

gap. Although we recognize the limitations

of ecological data at the tract- and MSA-

levels, we believe our proxies for credit fac-

tors in the probit equation adequately reduce

potential bias in our estimates.

For each MSA, we average the group like-

lihood of receiving a subprime loan in 2004 to

2006 by summing the predicted probability by

race and ethnicity across all loans and then

dividing by the total number of loans to

each borrower race/ethnic group (i.e., non-

Hispanic white, non-Hispanic black, and His-

panic). We then calculate the black-minus-

white and Hispanic-minus-white differences

in regression-adjusted predicted subprime

lending probabilities for each of the 100

MSAs. The black-white differential has

a mean of 11.8 percent (sd 4.3 percent) and

ranges from 2.3 to 24.0 percent; the

Hispanic-white differential is also always pos-

itive, with a mean of 8.1 percent (sd 3.8 per-

cent) and a range of 1.4 to 17.5 percent. We

Rugh and Massey 643

merge these two differential variables to the

main data file.

We use the regression-adjusted black-

white and Hispanic-white differentials in

subprime lending by MSA to predict the

segregation instrument inserted into the sec-

ond-stage equation. Table 5 reports OLS

and 2SLS estimates of the effect of black

and Hispanic segregation on the rate of fore-

closures for the top 100 MSAs, excluding

Honolulu, Hawaii, as in our main analysis.

The model includes the same covariates as

in Table 1 except log of population, level

of unemployment, the Rio Grande border

dummy, and age of housing stock.6

The estimated OLS coefficient for black

segregation (see the first column in Table 5)

is highly significant, and at 3.84 it is compara-

ble to that in our initial model (see Table 2).

This suggests that a .10-point rise in black

segregation is associated with a 38 percent

increase in the foreclosure rate. By contrast,

the instrumental variable estimate of the coef-

ficient is 4.64. This coefficient is estimated

quite precisely and attains significance at the

.001 level. Its higher point estimate implies

that a .10-point increase in black segregation

is associated with a 46 percent increase in

the foreclosure rate. While this effect is not

statistically different from the OLS effect

due to overlapping confidence intervals, its

higher value offers more evidence that segre-

gation indeed has a causal effect on the MSA

foreclosure rate by producing racial differen-

tials in subprime lending.

Test statistics for endogeneity indicate that

the racial differential instrument is indeed

exogenous, a conclusion corroborated by the

fact that it is uncorrelated with the residuals

of the reduced form model in Equation 3.

The percent of the MSA population that is

black has no impact whatsoever on our segre-

gation estimates and a much smaller offsetting

impact on the rate of foreclosures. This auxil-

iary finding underscores our hypothesis that

racial concentration in space, and not race

alone, is a significant structural cause of the

current foreclosure crisis.

Likewise, the coefficient for Hispanic seg-

regation is initially insignificant with a coeffi-

cient of .81 when estimated using OLS, but

using the instrumental variable estimator the

value rises to 1.12, which is nearly statistically

significant ( p = .15 using a two-tailed test and

p = .08 under a one-tailed test). A .10-point

increase in Hispanic dissimilarity is estimated

to result in an 11 percent increase under IV

estimation, indicating that unexplained His-

panic-white differences in subprime loan

usage augment our understanding of the effect

of Latino segregation on metropolitan-level

foreclosures.7 Note that the OLS and IV mod-

els yield similar coefficient estimates for the

effect of economic trends, housing market

conditions, land use regulation, region, and

other controls. This suggests that segregation

contributes to explaining variation in the fore-

closure rate above and beyond the standard in-

dicators heretofore employed in analytic

models.

CONCLUSIONS

The analyses provide strong empirical sup-

port for the hypothesis that residential segre-

gation constitutes an important contributing

cause of the current foreclosure crisis, that

segregation’s effect is independent of other

economic causes of the crisis, and that segre-

gation’s explanatory power exceeds that of

other factors hitherto identified as key causes

(e.g., overbuilding, excessive subprime lend-

ing, housing price inflation, and lenders’

failure to adequately evaluate borrowers’

creditworthiness). Simply put, the greater

the degree of Hispanic and especially black

segregation a metropolitan area exhibits, the

higher the number and rate of foreclosures

it experiences. Neither the number nor the

rate of foreclosures is in any way related to

expanded lending to minority home owners

as a result of the Community Reinvestment

Act.

The confluence of low interest rates, un-

paralleled levels of equity extraction via

644 American Sociological Review 75(5)

refinancing, and the bust of the housing bub-

ble may have combined with overbuilding

and lax regulation to make the foreclosure cri-

sis possible (Glaeser 2009; Khandani et al.

2009). However, we add a crucial addition

to the understanding of the causes and

consequences of the foreclosure crisis by

demonstrating the key role of residential seg-

regation in shaping how the crisis played out.

By concentrating foreclosures in metropolitan

areas with large racial differentials in sub-

prime lending, segregation structured the

causes of the crisis, as well as the geo-

graphic and social distribution of its costs,

on the basis of race. Segregation therefore

racialized and intensified the consequences

of the American housing bubble. Hispanic

and black home owners, not to mention

entire Hispanic and black neighborhoods,

bore the brunt of the foreclosure crisis.

This outcome was not simply a result of

neutral market forces but was structured on

the basis of race and ethnicity through the