watc h in 2011 and beyond - navigant research€¦ · watc h in 2011 and pete senio clint w beyo r...

TRANSCRIPT

CleaTen Publis

an Enn Tren

shed 2Q 2

nergynds to

2011

: o Watc

ch in

2011 and

PeteSenio

Clint W

Beyo

er Asmusor Analyst

WheelockPresident

ond

t

k t

© 2011 Pike ReAll Rights Reseexpress written

1.1

1.1.1

search LLC. rved. This publicationpermission of Pike Re

Ten Tr

This whthe cleasolar, wtechnoloqualify fCongresResearcWe havglobal renuclear

A few otowardsbeing rewith powin the 1When itmicro-dimake Ththe increa sign, n

Global

Investgenerare tw

Econoincreamodula med

Movinhydroksolar P

The rBig-nacurrenhigh-vpionee

may be used only asesearch LLC.

ends to Wa

hite paper prean energy deswind, geothermogies as natufor the proposss. In most cch syndicatedve arranged enewable enindustry.

overarching t business st

evived. Evidewer generatio970s, with th

t comes to teistribution andhomas Edisoeasing diversno doubt, of th

Deploymen

tor-owned uation: Solar o noteworthy

omies of scasing in size (ar nuclear reaium-sized city

ng power plakinetic wave, PV onto floatin

revival of diame advocatent (AC) to diroltage DC tr

ering efforts a

s expressly permitted

SeEXECUT

atch in Clea

esents ten kesignation is tymal, biomassural gas-fired sed “Clean Encases, the tred reports andthem into thergy insights

themes run tructures andence of this con deploymenhe most radicechnology, thd high voltagen proud. Theity of scale anhe growing m

nt Trends

utilities returphotovoltaicsexamples.

ale: Power ge(e.g., wind tuactors that coy).

nts from tradand tidal gen

ng structures

irect currentes are jumpinrect current. ransmission at developing

by license from Pike

1

ection 1TIVE SUM

an Energy

y trends shaypically synons and hydrokmicroturbine

nergy Standaends identified

insights colleree broad ca; and 3) Chin

through this technologiescan be seen nts, which runcal shift in uthe growing pe transmissioe second overnd resources

maturity of this

rning to ows (PV) in Cali

enerators currbines as lar

ould power a

ditional terrenerators are at reservoirs

t (DC) transng on board tExamples incin the North DC-based mi

Cleto Wa

Research LLC and m

1 MARY

ping future mnymous with kinetic – Pikees and nucleard” currently ud in this whitected from reategories: 1) na’s cleantec

top trends as that were owith utilities

ns counter totility roles oc

popularity of don levels of serarching thembeing deploy

s market segm

wnership/devifornia and of

rrently being rge as 10 MWshopping cen

estrial sites tprime examp

s, ponds, and

smission anto support aclude SiemeSea to sup

icrogrids.

ean Energatch in 201

may not otherwise be

markets for clrenewable so

e Research aar power, sincunder considte paper buil

ecent custom Global depl

ch growth and

analysis. Firsonce abandobecoming mo

o deregulationccurring withindirect currentervice is unex

me evident in yed within thement.

elopment offfshore wind

deployed in gW) and shrinknter, small bu

to marine sitples; firms arother water-b

nd distributiproposed shns’ and ABB

pport offshore

y: Ten Tre11 and Bey

accessed or used, w

ean energy.ources of enealso includesce these mayeration by thed on existingresearch prooyment trendd the future o

st, is a shift oned, but nowore involved

n trends originn the solar st (DC) at botxpected and wthese top tre

e renewable s

f new renewprojects in E

global markeking in scaleusiness comp

tes: Offshore re looking to based sites.

on technoloift from altern

B’s major plae wind and

ends yond

without the

While ergy – such y also e U.S. g Pike ojects. ds; 2) of the

back w are again nating sector. th the would nds is

sector,

wable urope

ts are (e.g.,

plex or

wind, install

ogies: nating ys on Intel’s

© 2011 Pike ReAll Rights Reseexpress written

1.1.2

1.1.3

search LLC. rved. This publicationpermission of Pike Re

Global

Greatethe mathis soelectricnow th(comp(CSP)well asAdditiomatch

Greateproducfor exalarge-ssized investo

The bStatesnew dpopulaof was

Geothstandacapacigrow athan fisame j

China’

Are Csigns China transminto thregionChinessector

Did ncorresincreagovernverge

may be used only asesearch LLC.

Renewable

er diversificaain focus for olar PV segmcity. Howeverhe largest maared to an av, also known s northern Afonally, interesthose of CSP

er diversificact diversity, boample, are incscale bulk powturbines (100ors, particular

business of ws: Hindered domestic waation and wasste-to-energy

hermal poweards (RPS) ity, the appeaas renewablerming up varijob without in

s Cleantech

hina’s wind that the Chinrepresented

mission, a large market. Ad are frustratese wind and s consolidate

nuclear powponding worssing regulatnment suppoof a major co

s expressly permitted

e Technolo

ation in the investors for ent on panel r, the overall

anufacturer ofverage of 6%as solar ther

frica and elsest is growing P.

ation in the woth in terms ocreasingly bewer utility app0 kW to 1 Mrly in the Unit

waste-to-eneby the availaste-to-energy

ste generationtransformatio

er generatioin the weste

al of renewabs such as winiable renewab

ncreasing carb

h Growth a

and solar pnese clean ed the top wige percentagedditionally, maed by Chinasolar produc

e.

wer just mist nuclear diory scrutiny rt may indee

omeback in th

by license from Pike

2

gy Trends

solar sectordecades. Toefficiency, co

sector has bef thin film sola for other thinrmal electric,ewhere, boasfor concentra

wind power sof design and eing producedplications for W) are vyinged States.

ergy power bility of cheapy power plann are catapulton.

n growth laern U.S. Desle baseload pnd and solar cbles with fossbon emissions

nd the Futu

power growthnergy markend market i

e of the countany of the gloa’s high domcts are also f

ss the boasaster in wo

and changd spell the de world’s lead

Cleto Wa

Research LLC and m

r: Traditional oday, SunPoonverting 20%ecome much ar PV panels n film PV panis seeking a

sting efficiencated solar PV

sector: The w scale. Vertic

d for on-site doffshore mar

g for attentio

plants in Chp landfills, thent in roughlting it to the to

argely due tspite remarkapower from gcontinue dousil fuels, new s.

ure of Nucle

h rates sustet is experienn the worldtry’s installed obal corporat

mestic contentfacing increa

at? The earld history, wging politicaldeath of a tecding nuclear m

ean Energatch in 201

may not otherwise be

polysilicon sower is the m% of the sun’smore diversedue to its 11

nels). Concena revival in thecy levels that V (CPV), whos

wind industrycal axis and twdistributed genrkets. And for on from both

hina, Europee United Staty a decadeop of the glob

to state renably low groweothermal soble-digit annugeothermal c

ear Power

tainable? Thncing growing. However, turbines nev

tions that havt requiremen

ased scrutiny

arthquake in was just the l winds thachnology thamarket: the U

y: Ten Tre11 and Bey

accessed or used, w

solar PV has arket leader s solar energ

e, and First So% efficiency

ntrated solar pe United Statmay exceed

se efficiency

y is offering gwo-bladed deneration as wthe first timepolicymakers

e, and the Utes has not s. China’s subal market in

newable porwth in recen

ources continuual growth. Rcapacity can d

ere are increg pains. Last due to a laer sold their o

ve moved in tnts. The qua

as manufac

Japan, andtip of the ice

at favor shrt appeared o

United States.

ends yond

without the

been within

gy into olar is rating power tes as 30%.

levels

reater signs,

well as e, mid-s and

United een a urging terms

rtfolio t new ues to Rather do the

easing year,

ack of output to this lity of

cturing

d the eberg; inking

on the

© 2011 Pike ReAll Rights Reseexpress written

2.1

2.1.1

search LLC. rved. This publicationpermission of Pike Re

Utilitie

A shift tof new punderwa(PURPArecessioassociaton utilitie

Utility-

The solafourth inthese princreasi

Solar Pterrestriathe estascale coStates. (compoulast sevefor utility

CalifornIt is oneCalifornfor imple

SoutheauctionIPPs, b

Pacificwith anMW) wutility r

San Dwith aMW) wutility r

Despite concentResearcboth utilthe Nort

may be used only asesearch LLC.

GLO

s Back Into

oward reliancpower plants ay since theA) in 1976. on hampered ted with largees to help und

Owned, Uti

ar PV market nternationally,rojects are beng share of la

PV has tradital markets w

ablishment of ommercial syAfter a brie

unded by a reral years. Wy-scale solar P

ia currently ae of the few stia Public Utiliementation ov

ern Californians that beganbut will sell in

c Gas & Elecnnual solicitatwill be develorate base.

Diego Gas & Ennual auctionwill be develorate base.

the fact thattrated in one ch forecasts slity-scale solatheast and So

s expressly permitted

SeOBAL DEP

o Key Renew

ce on indepen– particularly U.S. CongrHowever, ththe rising tre

e-scale commderwrite new

ility-Scale S

is booming, w, the country eing developarger systems

ionally been were off-grid,

a federal proystems begaef rise in craw materials

When the fedePV finally too

ccounts for 1tates to authoties Commissver the next fi

a Edison: 500 n in April 201

nto wholesale

ctric: 500 MWtions that begoped by IPPs

Electric: 100 ns pending fioped by IPPs

t the utility-scstate (Califor

significant groar PV and UOoutheast also

by license from Pike

3

ection 2PLOYMEN

wable Ener

ndent power renewable e

ress passed he recent Waend toward f

mitments to offcapital intens

Solar PV in

with 441 MW is at the foreed by IPPs, s that feed dir

viewed as remote commoduction tax n to domina

costs when silicon short

eral solar tax ck root.

,717 MW (63orize utility-owsion has authive years:

MW; 1-2 MW0. Half of themarkets and

W; 1-20 MW gan in the firsts, but will sel

MW; 1-5 MWnal CPUC ap

s, but will sel

cale solar PVrnia) and repowth over theOG projects arepresent via

Cleto Wa

Research LLC and m

2 T TREND

rgy Markets

producers (IPenergy and co

the Public all Street mefinancing renefshore wind asive projects i

California

W added in 201efront of utilitybut investor-orectly into util

a distributedmunities; rescredit of 30%te overall cademand sub

tage), costs hcredits were

3%) of the totawned generathorized a tota

W projects – pese systems be part of the

projects – pt quarter of 20l into wholes

W projects – ppproval. The l into wholes

V market (inclpresents a rece next five yeaare Coloradoable markets.

ean Energatch in 201

may not otherwise be

DS

s

PPs) as the pogeneration faUtilities Regeltdown and ewable techn

also promptedin Europe.

10. While the y-scale projecowned utilitieity wholesale

d generation idential roofto

% in 2008, theapacity additibsequently ohave droppedextended to u

al utility-scaletion (UOG) syl of 1,100 MW

primarily on ro(250 MW) wie utility rate b

rimarily grou011. Half of thale markets

primarily groumajority of t

ale markets

luding UOG scent market pars. The best o, Nevada, an

y: Ten Tre11 and Bey

accessed or used, w

primary develacilities – hasulatory Policlingering fin

nologies. Thed a greater re

U.S. market cts. The majoes are financi grids.

technology. ops followed.e market for ons in the U

outstripped sd by 40% oveutilities, the m

e solar PV pipystems. In facW of UOG sys

ooftops with all be develop

base.

nd-mount syshese systemsand be part o

nd-mount systhese systemand be part o

solar PV) is phenomenonnear-term be

nd Arizona, th

ends yond

without the

lopers s been cy Act ancial

e risks liance

ranks ority of ng an

Initial . With large-

United supply er the

market

peline. ct, the stems

annual ped by

stems s (250 of the

stems ms (74

of the

highly , Pike ets for hough

© 2011 Pike ReAll Rights Reseexpress written

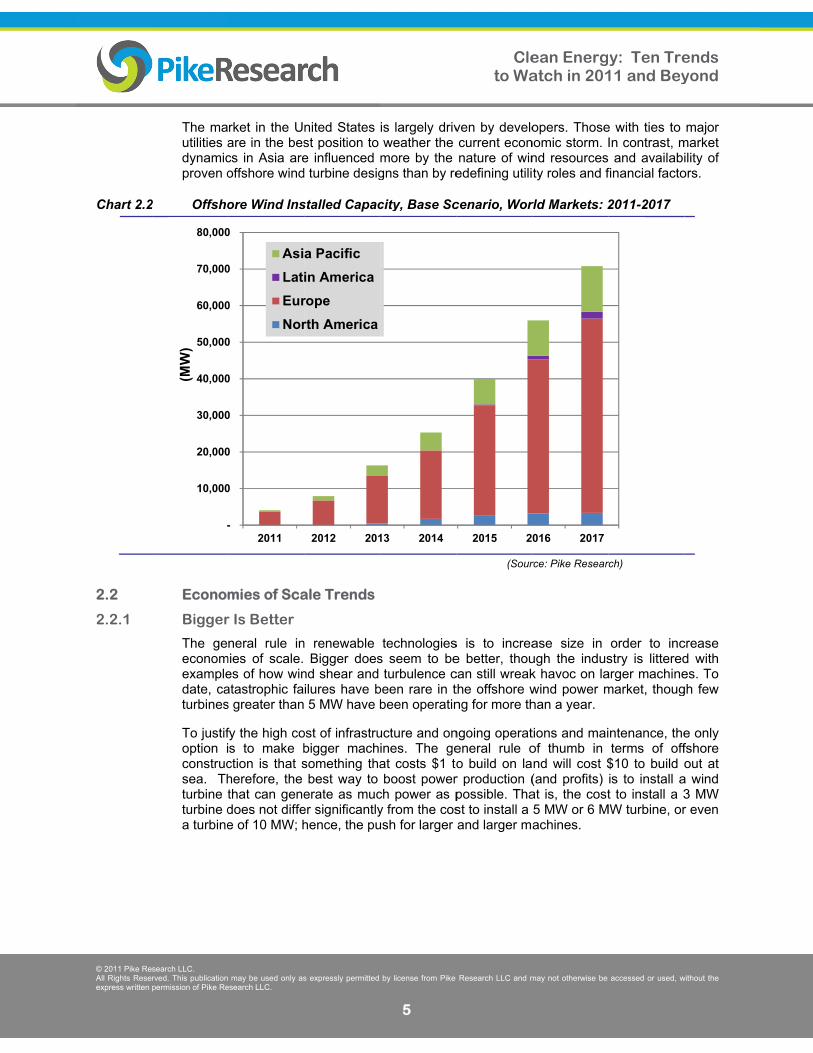

Chart 2.1

2.1.2

(MW

)

search LLC. rved. This publicationpermission of Pike Re

1 Utility

Offsho

In Europlargely bmove inutilities functionbecome

The moutility baoperatioGermancompanstake inapproximKent, inworld. Land opeoffshore Today, vumbrellainstitutiofinancinthe boom

-

2,000

4,000

6,000

8,000

10,000

12,000

2010

(MW

)

may be used only asesearch LLC.

y-Scale Cumu

re Wind Po

pe, pilot offshby major Euronto the mainhave other os, the offsho

e sustainable.

st significant ased in Swedons span weny, Poland, tny announcedn the first commately $1 bill the United K

Long-term plaerator in nore wind capacit

virtually everya of companon as well as g are neededming U.K. ma

2011

s expressly permitted

ulative Solar

ower in Euro

ore wind projopean utilitiesstream, othe

obligations in re wind indus

utility playerden with rootll beyond Swthe United Kd a strategic mmercial offshion into the 3

Kingdom – cuans call for Vrthern Europety by 3000%

y offshore winnies, which aunregulated

d and utilities arket.

2012

by license from Pike

4

r PV Capacity

ope

ects developes with strong er sources of

terms of mestry needs to

r in the offshots in wind poweden’s bordKingdom, the

move into rehore wind far

300 MW Thanurrently the laVattenfall to be. The compby 2030.

nd project undalmost alwayarms of largein southern

2013

Cleto Wa

Research LLC and m

y, United Sta

(Sour

ed over the pbalance shee

f capital will eeting the deo find new so

ore wind secower technoloders, with cue Netherlandsenewable enerm in Denmanet offshore wargest operatbecome the lapany has set

der developmys includes e utilities, sucEurope are lo

2014

ean Energatch in 201

may not otherwise be

ates: 2010-20

rce: Pike Resear

past decade hets. Howeverbe necessar

emands of thources of inve

ctor is Vattenfogy that dateustomers in Ds, and Belgiergy and pur

ark. In 2008, wind farm proing offshore wargest offshot a goal of i

ment in Europea governmen

ch as Vattenfaooking for su

2015

y: Ten Tre11 and Bey

accessed or used, w

016

rch)

have been finar, as these prry. Given tha

heir regulatedestment in ord

fall, a state-oe back to 198Denmark, Finium. In 2005rchased a maVattenfall inv

oject near Mawind project

ore wind devencreasing its

e is financed nt-owned finall. New sourcch opportunit

2016

ends yond

without the

anced ojects at the d T&D der to

owned 80. Its nland, 5, the ajority

vested rgate, in the eloper s total

by an ancial ces of ties in

© 2011 Pike ReAll Rights Reseexpress written

Chart 2.2

2.2

2.2.1

search LLC. rved. This publicationpermission of Pike Re

The mautilities adynamicproven o

2 Offsho

Econom

Bigger

The geeconomexampledate, caturbines

To justifoption iconstrucsea. Thturbine tturbine da turbine

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

(MW

)

may be used only asesearch LLC.

rket in the Uare in the bescs in Asia areoffshore wind

ore Wind Ins

mies of Sca

r Is Better

neral rule inmies of scale. es of how winatastrophic fas greater than

fy the high cos to make bction is that sherefore, the that can genedoes not diffee of 10 MW; h

-

0

0

0

0

0

0

0

0

2011

Asi

Lat

Eur

Nor

s expressly permitted

nited States st position to e influenced d turbine desig

stalled Capac

ale Trends

n renewable Bigger does

nd shear and ilures have b 5 MW have b

ost of infrastrubigger machsomething thabest way to

erate as mucer significantlyhence, the pu

2012 201

a Pacific

in America

rope

rth America

by license from Pike

5

is largely drivweather the more by the gns than by re

city, Base Sc

technologiess seem to beturbulence c

been rare in tbeen operatin

ucture and onines. The geat costs $1 toboost power

ch power as py from the cosush for larger

13 2014

Cleto Wa

Research LLC and m

ven by develocurrent econnature of winedefining utili

cenario, Wor

(Sour

s is to increae better, thoucan still wreakthe offshore wng for more th

ngoing operateneral rule oo build on lar production (possible. Thast to install a and larger m

2015 2

ean Energatch in 201

may not otherwise be

opers. Thosenomic storm. Ind resourcesty roles and f

rld Markets: 2

rce: Pike Resear

ase size in ugh the indusk havoc on lawind power mhan a year.

tions and maiof thumb in nd will cost $(and profits) at is, the cost5 MW or 6 Machines.

016 2017

y: Ten Tre11 and Bey

accessed or used, w

e with ties to In contrast, m and availabifinancial facto

2011-2017

rch)

order to incstry is litteredarger machinemarket, thoug

ntenance, theterms of off

$10 to build ois to install at to install a 3

MW turbine, or

ends yond

without the

major market ility of

ors.

crease d with es. To gh few

e only fshore out at

a wind 3 MW r even

© 2011 Pike ReAll Rights Reseexpress written

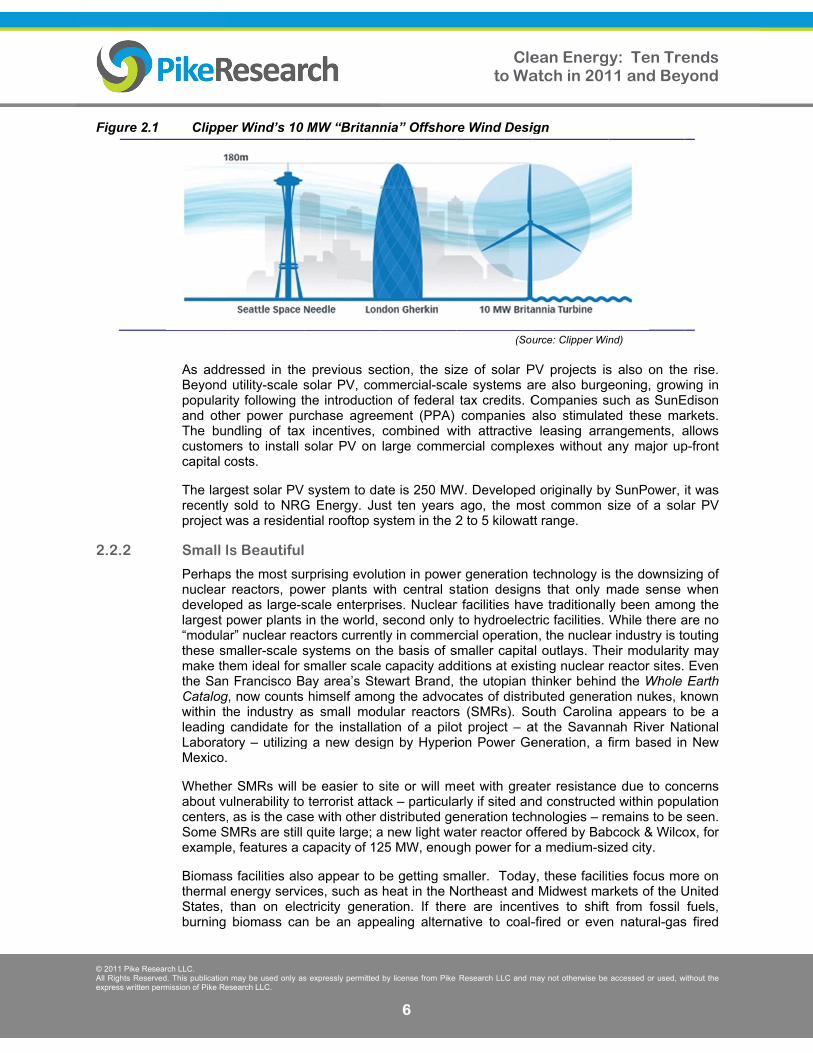

Figure 2.

2.2.2

search LLC. rved. This publicationpermission of Pike Re

1 Clippe

As addrBeyond populariand othThe buncustomecapital c

The largrecentlyproject w

Small I

Perhapsnuclear developlargest p“modulathese smmake ththe SanCatalogwithin thleading LaboratoMexico.

Whetheabout vucenters,Some Sexample

Biomassthermal States, burning

may be used only asesearch LLC.

er Wind’s 10

ressed in theutility-scale s

ity following ter power pundling of taxers to install costs.

gest solar PV y sold to NRGwas a residen

s Beautiful

s the most sureactors, poed as large-spower plants ar” nuclear reamaller-scale s

hem ideal for s Francisco B, now counts he industry acandidate foory – utilizing

r SMRs will bulnerability to as is the cas

SMRs are still e, features a c

s facilities alsenergy servicthan on elecbiomass can

s expressly permitted

MW “Britann

e previous sesolar PV, comthe introductiorchase agree

x incentives, solar PV on

system to daG Energy. Juntial rooftop sy

rprising evoluwer plants wscale enterpriin the world,

actors currentsystems on thsmaller scale

Bay area’s Stehimself amo

as small modor the installag a new desig

be easier to s terrorist attac

se with other dquite large; a

capacity of 12

so appear to bces, such as ctricity genern be an appe

by license from Pike

6

nia” Offshor

ection, the sizmmercial-scaon of federal ement (PPA) combined wlarge comme

ate is 250 MWust ten years ystem in the 2

ution in powewith central stises. Nuclearsecond only tly in commerhe basis of s

e capacity addewart Brand,ng the advoc

dular reactorstion of a pilogn by Hyperi

site or will meck – particuladistributed gea new light wa25 MW, enou

be getting smheat in the N

ration. If therealing alterna

Cleto Wa

Research LLC and m

re Wind Desi

(Sou

ze of solar Pale systems a

tax credits. Ccompanies a

with attractive ercial comple

W. Developedago, the mo

2 to 5 kilowat

r generation tation designr facilities havto hydroelect

rcial operationsmaller capitaditions at existhe utopian t

cates of distribs (SMRs). Soot project – aion Power Ge

eet with greaarly if sited aneneration techater reactor ogh power for

maller. TodayNortheast andre are incentative to coal-

ean Energatch in 201

may not otherwise be

ign

urce: Clipper Win

PV projects isare also burgeCompanies salso stimulat leasing arra

exes without a

d originally byost common stt range.

technology isns that only mve traditionalltric facilities. n, the nuclear

al outlays. Thsting nuclear thinker behinbuted generaouth Carolina

at the Savanneneration, a f

ater resistancnd constructedhnologies – re

offered by Baba medium-siz

y, these facilitd Midwest matives to shift-fired or even

y: Ten Tre11 and Bey

accessed or used, w

nd)

s also on theeoning, grow

such as SunEed these maangements, aany major up

y SunPower, size of a sola

s the downsizmade sense y been amonWhile there ar industry is toeir modularityreactor sites.d the Whole

ation nukes, ka appears to nah River Nafirm based in

ce due to cond within popuemains to be bcock & Wilcozed city.

ties focus moarkets of the Ut from fossil n natural-gas

ends yond

without the

e rise. wing in Edison arkets. allows p-front

it was ar PV

zing of when

ng the are no outing y may Even Earth

known be a

ational n New

ncerns ulation seen.

ox, for

ore on United fuels,

s fired

© 2011 Pike ReAll Rights Reseexpress written

2.3

2.3.1

2.3.2

search LLC. rved. This publicationpermission of Pike Re

heat. Hoactually fuel colle

Fossil fuhave befossil fueand wascomplex

Moving

Offsho

Why wowhere tThere isclose to involve concernterrestria

Due to toffshoremandategreater betweenachievin

Europe already Neverthalso comoffshoreshows tU.K. and

Hydrok

The Unmake usdevelopwind tra

While thresourceriver hydinterest KingdomJapan. Iwill becoburgeon

In termscompeti

may be used only asesearch LLC.

owever, the cwork in reve

ection and tra

uel technologeen a mainstel generator tste fuels. Duexes, creating

g from Trad

re Wind Po

ould developehe deployme

s no single anurban demanadditional co

ns, particularlyal projects, pa

the significane wind is primes to reduceemphasis is

n European ng the EU’s ca

has been opobtains moreeless, the Unming on strone wind movemhat China’s od Germany --

kinetic Tech

ited Kingdomse of wave ament of thesensmission inf

he total instaes – a categodrokinetic resin these opt

m, Ireland, theIt is expectedome commerning market fo

s of emerginng for attenti

s expressly permitted

ost of fuel corse, with smaansportation c

gies are not imtay for emergtoday is the me to low emissnew markets

ditional Terr

ower

rs, manufactuent challengenswer. Many nd centers ha

osts associatey wind powerarticularly in t

t build-outs omarily based e carbon emis being placcountries on arbon-reducti

perating offshe than 25% onited Kingdomng, despite itsment is not limoffshore wind by 2017.

hnologies

m is also in thnd tidal motioe emerging refrastructure b

alled capacityory that includsources – wastions has gene United Stat

d that within trcialized to thor carbon-free

g technologieon. Most of t

by license from Pike

7

llection from sall facilities recosts.

mmune to thegency backupmicroturbine, wsions, they cafor micro-gen

restrial Site

urers, governes for renewa

of the best laave already bed with build’s impact on the United Kin

of the past anon a lack o

issions throued on large-

transmissionon goals with

hore wind turbof its total elem is the curres limited coasmited to Euro market will b

he lead in hyon. Being an enewables byeing deployed

y of emergindes wave, tidas less than 1nerated a detes, Portugal,the next five te point that t

e and non-pol

es, hundredsthese firms a

Cleto Wa

Research LLC and m

small sourceselying on regio

ese reverse-sp and remotwhich may alan be sited innerators.

es to Marine

ments, and inable energy sand-based reeen developeing long distbirds and batngdom and U

nd population of available oughout the E-scale megan issues in

h offshore win

bines for neaectricity froment market lest on the Nortpe. In fact, Pbe even with

ydrokinetic teisland, the U

y allowing thed.

g “second gal stream, oce0 MW at the

eepening curio, South Koreato eight yearsthey can beglluting renewa

s of designs are smaller st

ean Energatch in 201

may not otherwise be

s is high, so eonal sources

scale trends. e power, butlso be able to

n urban areas

e Sites

nvestors wansources are

enewable resoed, and the retance transmts, have also

United States.

density in Euonshore sitesuropean Uni

a-projects. Grthe North Se

nd turbines.

arly a decade wind power

eader in the rth Sea. Howe

Pike Research Europe’s lar

echnologies sUnited Kingdom to piggy-ba

generation” mean current, oend of 2008

osity, particua, Australia, s, these emein competingable resource

from more thtartups. How

y: Ten Tre11 and Bey

accessed or used, w

economies of of fuel to min

Diesel genet the hottest o combust bio within comm

t to move offsso much gre

ource sites loemaining sitesission lines. delayed trad

urope, the mos. With clear on (EU), an reater coopeea will be vi

e. Denmark, , is a key pioregion. Germaever, the longh’s market forrgest players

such as thoseom may enaback on the off

marine hydrokocean therma, a recent sularly in the UNew Zealand

erging techno for a share

es.

han 100 firmwever, a few

ends yond

without the

f scale nimize

rators small

omass mercial

shore, eater? ocated s may Siting itional

ove to legal even

eration ital to

which oneer. any is g-term recast – the

e that ble the fshore

kinetic al, and rge of United d, and logies of the

ms are larger

© 2011 Pike ReAll Rights Reseexpress written

Figure 2.

2.3.3

2.4

search LLC. rved. This publicationpermission of Pike Re

players businesShell arDehlsendeploy wperhapsrenewabcommer

While Epotentiatidal.

2 Wave

Wave Energ

Floatin

Perhapsfloating Novato, Australiaproject engaged

Direct

IronicallytechnoloThomasbased bmicrogri

The ideemerginDC-base

may be used only asesearch LLC.

– Scottish Pos opportunitiere also invesn – formerly wwave and ocs the most able resource, rcial deploym

Europe is cleaal. Of all state

and Tidal En

gy Potential

ng Solar PV

s the most ssolar arrays.Calif. has ins

a has signedon a hydroeld in a trial dem

Current T&

y, today’s uogy could cars Edison was business modids, each serv

ea of switchinng entrepreneed microgrid

s expressly permitted

ower, Lockhees in the marsting in the swith Zond Sysean current dappealing of but is also thents.

arly in the leaes, Oregon lea

nergy Potent

surprising tren. Only a handstalled two su a deal with lectric reservmo with the F

&D Systems

utility grid evry power bettpromoting be

del. In fact, Eving only a sm

ng back to Deurs and giands is ZBB

by license from Pike

8

eed Martin, anrine renewablsector. And fstems, Enron devices. The

marine hydhe ocean ene

ad, North Amads in terms

tial, North Am

Tidal

nd in deploydful of firms uch projects oIndia’s larges

voir near MumFrench utility E

s May Trans

volved to anter over long defore the elec

Edison’s first mall number o

DC-based micnt IT firms. AEnergy Corp

Cleto Wa

Research LLC and m

nd Pacific Gales space. Oiformer wind Wind and CliGulf Stream

drokinetic oppergy option th

merica also hof wave pow

merica

l Energy Pote

ying renewabare active inon ponds for st private utilmbai; and SoEDF on a res

sform Clean

n AC-based distances thactric utility indpower plantsof customers

crogrids is pAmong the moporation. In

ean Energatch in 201

may not otherwise be

as & Electric –il companies entrepreneurpper Wind --

m just off the portunities, s

hat is the furth

has tremendower deployme

ential

(Source: EP

bles on waten this new tre

California wiity, Tata Powolaris Synergervoir in the s

n Energy M

grid worldwan low-voltagedustry matureds were all esswith low-volta

icking up suore advanced

2010, the

y: Ten Tre11 and Bey

accessed or used, w

– are also seChevron, BP

rs such as Jare now lookcoast of Flor

since it is ahest away fro

ous wave andnt; Maine lea

PRI)

r is the adveend: SPG Soneries; Sune

wer, to build agy of Israel issouth of Franc

arkets

wide becausee DC, a technd into a monosentially DC-bage power.

pport amongd small vendofirm signale

ends yond

without the

eeking P, and James king to rida is 24/7

om full

d tidal ads on

ent of olar of rgy of a pilot s also ce.

e this nology opoly-based

g both ors of

ed its

© 2011 Pike ReAll Rights Reseexpress written

Figure 2.3

search LLC. rved. This publicationpermission of Pike Re

commitmCenter and DCmanufacto tap inthat dieabsorbehighlightHonolulu

3 DC Sy

Cutting-the viabmore efcurrent electricit

IronicallyNikola Treputatioone to g

Today, that offepower htransmislines aninfrastru

may be used only asesearch LLC.

ment to micro(PECC), whicC power soctured by its cnto a variety

esel generatoer for the mits a proposedu, Hawaii, wh

ystems Alrea

edge researcbility of DC-bfficient, and amicrogrids). ty grid could t

y, Edison’s vTesla’s AC, don as a “mad

gain wide com

high-voltage ers superior has to be trssion cable ond sea cableucture, as dep

s expressly permitted

ogrids by offech features aources directcompetitors. of storage d

ors no longercrogrid. Thed PECC proje

here the DC m

ady Proliferat

ch is underwaased microg

are more comWhile Intel

take literally a

vision of a DCdespite an in scientist.” Of

mmercial succ

direct currenservice over

ransmitted moption. Note ts when relyi

picted in Figur

by license from Pike

9

ering a patena configurabletly to DC e This unique evices to enhr have to fole limitation iect powering

microgrid is pr

te in Today’s

ay at Intel’s rids. These

mpatible with efreely acknow

a century, it a

C-based elecntense propaf all of Tesla’s

cess.

nt (HVDC) telong distanc

ore than 50 the significanng exclusivere 2.4.

Cleto Wa

Research LLC and m

nt-pending moe architectureenergy storastorage-basehance microgllow load, ans having onan elevator s

rojected to red

s Home Envi

New Mexico microgrids lo

emerging stowledges the ppears this tr

ctric power staganda camps futuristic inv

echnology repces when co miles offsho

nt line losses ely on today’s

ean Energatch in 201

may not otherwise be

odular Powere that can coage units, ined approach grids. Havingnd storage sly one-way psystem at theduce electrici

ironments

(Source: In

Energy Systose less ene

orage devicespath back t

ransition is alr

tructure lost opaign that maventions, AC

presents a traompared to Aore, HVDC that occur w

s widespread

y: Ten Tre11 and Bey

accessed or used, w

r & Energy Connect multipncluding batenables end

g a DC-bus merves as a spower flow. e Pualani Maty costs by 40

tel)

tems Researergy, making s (the weak lito a DC-domready underw

out to his arcade fun of Twas really the

ansmission cAC systems. is the only v

with both oved AC transm

ends yond

without the

Control le AC tteries users

means shock ZBB nor in 0%.

rch on them

nk for minant way.

chrival Tesla’s e only

choice If the viable rhead ission

© 2011 Pike ReAll Rights Reseexpress written

Figure 2.4

search LLC. rved. This publicationpermission of Pike Re

4 Comp

The grow

Advanprocesso-call

Some other specifidecisio

AC tralosses

HVDCcontracontribfirewal

may be used only asesearch LLC.

parisons of L

wing level of

nces in powess plants, anled electricity

of the same consumer g

ically, computon-making wit

ansmission sys are closer to

C systems arest, AC syste

butes to rollinlls, limiting gr

s expressly permitted

ine Losses b

interest in HV

er electronicsnd mass trantransmission

kinds of powgadgets havters and softwthin nanoseco

ystems suffer o just 2%.

e 100% controems sometimng blackouts id disturbance

by license from Pike

10

between AC

VDC stems fro

s originating nsit traction n and distribut

er electronicsve occurred ware systemsonds are now

“line losses”

ollable: the pomes flow in

or brownoutses to a small

Cleto Wa

Research LLC and m

and DC Tran

om the follow

from the indsystems) hation (T&D) ind

s innovations within large

s that create aw infiltrating m

that can rang

ower will onlyunpredictabl

s. In this wageographical

ean Energatch in 201

may not otherwise be

nsmission Ca

(Source: AB

wing developm

dustrial sectoave now beedustry.

occurring witer industrial algorithms tha

modern power

ge from 10% t

y go where yole ways, a

ay, HVDC sysl area.

y: Ten Tre11 and Bey

accessed or used, w

ables

BB)

ments:

or (electric den adapted t

th PCs, iPodssystems.

at enable rear grids.

to 15%. HVD

ou want it to characteristicstems can ac

ends yond

without the

drives, to the

s, and More

al-time

C line

go. In c that ct like

© 2011 Pike ReAll Rights Reseexpress written

3.1

search LLC. rved. This publicationpermission of Pike Re

Greate

While thprimary 0.1% of

Solar phquite pofrom smand mos

The woritself froefficient First SobecomeThis is projectsconstrucSolar alas Juwi,

Beyond solar pcommerrequire generatedirect sothe reghemisphto includNevada

Today, mslated fhoweveCSP plaCSP carepresen

The thre

Parabwater focusinresultintraditio

may be used only asesearch LLC.

GLOBAL

er Diversific

he sun offers energy, the fthe world’s to

hotovoltaic (Popular with themall distributest recently, ut

rld’s largest som the majorit

than the maolar has beene vertically intexemplified b, and Turnection (EPC) sso partners w, EDF Energie

this diversifiower (CSP) rcial installatihigher concee electricity folar electricityion situated heres). This isde the United, Texas, Colo

more than 31for Californiar, the vast maants are up apacity under nting 98% of

ee primary typ

olic Troughspipes runnin

ng the sunligng solar-powonal turbine a

s expressly permitted

SeL RENEWA

cation withi

10,000 timesfull portfolio otal supply.

PV) systems e general pubd residential tility-scale wh

solar PV modty of PV manjority of prod

n a leader integrated, allowby First Solar Renewableservices aimewith investorses Nouvelles,

cation on thetechnologie

ons in southentrations of srom direct-bey production

between 15s the area witd States’ De

orado, and Ca

1 GW of CSPa, Arizona, Najority of thesand running tconstruction. operating cap

pes of CSP te

s: This technng through thght to reach wered steam nd generate e

by license from Pike

11

ection 3ABLE EN

in the Solar

s more radiatof installed s

can be instablic and invesrooftops, to olesale powe

dule producerufacturers byucts on the m moving dowwing it to botr’s acquisition

e Energy, a ed particularlys and other fin, and enXco.

e solar PV ses, which arhern Californisolar fuel thaeam radiationis basically re

5° to 35° latth the largest

esert Southwealifornia.

P is in the pipeNevada, Colse power planthroughout thBy far, parab

pacity and 70

echnologies a

nology consisheir centers. temperatures

is integrateelectricity.

Cleto Wa

Research LLC and m

3 ERGY TR

r Sector

tion energy thsolar energy t

alled virtuallytors. As notedlarge comme

er plants.

r is now Firsty developing tmarket, thin-fiwn the supplyth supply panns of OptiSoprovider of ey at reducingnance provid

side is the apre experienca deserts in

an solar PV sn, not more destricted to thtitude in bott increase in eest region, in

eline in the Uorado, New

nts will never he United Stabolic trough te

0% of those fa

are:

sts of large, These curve

s as high ased with stea

ean Energatch in 201

may not otherwise be

RENDS

han the worldtechnologies

y anywhere, ad previously,

ercial on-site

t Solar Inc., wthin-film solarilm solar PV y chain throunels and thenolar, a develoengineering,

g balance-of-sers as well a

pparent revivcing a come

the 1980s. systems becadiffused light. he “sun belt th the northenergy demancluding Arizo

United States,Mexico, Te

be built. At pates, with anoechnology is

acilities now u

U-shaped reed mirrors til 750 degree

am Rankine

y: Ten Tre11 and Bey

accessed or used, w

d actually neeprovides less

and have beapplications power gener

which differenr PV. Althougis also less c

ugh acquisition develop prooper of utility-

procurementsystem costsas companies

al of conceneback after CSP techno

ause they canAlthough effof the world,”ern and sound, and it hapona, New M

, including prexas, and Hresent, 480 M

other 1,347 Mthe market le

under constru

flectors withlt toward the

es Fahrenheitcycles to s

ends yond

without the

eds as s than

ecome range ration,

ntiates h less costly. ons to ojects. -scale t, and . First

s such

trated initial

logies n only ficient, ” (i.e., uthern ppens exico,

ojects awaii;

MW of MW of eader, ction.

oil or e sun, t. The pin a

© 2011 Pike ReAll Rights Reseexpress written

Chart 3.1

(MW

)

search LLC. rved. This publicationpermission of Pike Re

Powerheliostof a cesalt, wcan cr

Dish arrangmountthermaare thsophisHowevmeet poption

1 Conce

The abadvantalevelizedwhy grothe mosdevelopinvestman IPO f

Perhapsconceptlenses oattractio

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2

Ba

may be used only asesearch LLC.

r Towers: Atats that trackentral tower. A

which can reaeate steam to

Stirling: Instged in a circlted a short dal troughs, caheoretically msticated solarver, companiproject milest, and dish Sti

entrated Sola

ility to store age, which mad cost of ene

owing numberst promise forer BrightSouents from Chfor $250 millio

s the most ints – known asor mirrors co

on of this appr

2010 20

ase Scenario

s expressly permitted

lso called cek the sun, but Again, the so

ach temperatuo spin a turbin

tead of the e. These disistance from an run on gasmore efficientr tracking syes promotingtones. The drling varieties

ar Power Ins

solar poweray make it theergy (LCOE) rs of developr succeeding rce Energy o

hevron, BP, Gon through G

nteresting devs “concentratncentrate solroach is that i

011 2012

o Averag

by license from Pike

12

entral receivefocus the raylar energy is ures as high ne or can be s

troughs, thisshes reflect s

the center oseous fuels it than parabystem with tg this technodrop in solar s represent th

stalled Capac

r gives the e preferred Ccan be reducers are lookinin the curren

of Oakland, CGoogle, and ooldman Sach

velopment in ting solar PV”lar energy onit achieves ef

2 2013

ge Scenario

Cleto Wa

Research LLC and m

ers, this apprys onto a singconcentratedas 1,050 deg

stored for late

s technology sunlight into of the cluster.n the absencbolic troughstwo axes ratology lack finPV prices m

he most risky

city, United S

(Sour

power towerSP technologced by 20% wng in this dire

nt market for CCalif. The coothers. On Aphs, Citi, and D

solar is the” (CPV). Thento high-efficifficiencies gre

2014

Aggress

ean Energatch in 201

may not otherwise be

roach relies ogle receiver lod to heat a flugrees Fahrener use.

relies on a a single sma. These systece of adequas because thther than jus

nancing and may spell the

of CSP choic

States: 2010-

rce: Pike Resear

r CSP techngy over the lowith thermal ection. The cCSP technolo

ompany has pril 22, 2011,

Deutsche Ban

merging of Ce twist to this iency solar Peater than 40%

2015

sive Scenario

y: Ten Tre11 and Bey

accessed or used, w

on a series oocated near thuid, such as mnheit. The ho

cluster of dall collector tems, like the te solar fuel.

hey have a st one long consistently fdoom of the

ces.

-2016

rch)

ology an inhong term. Sinc

storage, it isompany that ogy is power been bolsterethe company

k.

CSP and solatechnology i

PV cells. The %. (In compa

2016

o

ends yond

without the

of flat he top molten ot fluid

dishes that is solar They more axis.

fail to e CSP

herent ce the clear holds tower ed by y filed

ar PV s that main

arison,

© 2011 Pike ReAll Rights Reseexpress written

3.2

search LLC. rved. This publicationpermission of Pike Re

the top efficientwith thepromisinsystems

At preseCPV is ttemperaThose d

Greate

Similar tdesign athe clasdesigns a comewhile vefor on-sin the fo

Here areTwo-blanoisy aintroducadvantaa remarfunds fo

Not eveEnergy applicat

It appeageneratiPhiladelinstallatidrawbacbest winveteran many alhas not for offshdominangearboxBoulogn

In termsthan 1 Mon-site pturbinesare attramicrogri

may be used only asesearch LLC.

polysilicon so.) California, a company Amng sign is ths innovator, a

ent, however,the need for matures, both odynamics can

er Diversific

to solar poweas well as scassic Danish t– which wereback. Two-bl

ertical axis deite residentia

orm of 10 MW

e some enginaded downwinand have higced a two-blaages over comkably simple

or professiona

ryone has giv6 MW mac

ions, is sched

ars that the bion for skyslphia Eagles ions to date ock for residennd resourceswind power so question tstopped Nen

hore marketsnt wind turbix. A 1/10 scane sur Mer.

s of scale, moMW for utility-power generas (which the Nacting governids and virtua

s expressly permitted

olar PV panelagain, appeamonix signinghe partnershind Concentrix

, existing CPVmore sophistiof which introd

increase unc

cation withi

er, the wind male. Considerthree-bladed e the most poladed design

esigns are bel power, they

W giants desig

neering factond rotors – wgh failure raded 1 MW up

mpeting three-turbine) to co

al operations a

ven up on twochine, the fiduled to be in

best applicatcrapers or ffootball stad

of this new clntial applicatios, which are advocates snthe practicalitnuphar of Lille. A prototypene topology, ale 35 kW pr

ost turbines s-scale wind faation of homeNational Renenment suppoal power plan

by license from Pike

13

l offered by Srs to be the te

g a 25 MW PPp between Jx, a firm now

V capacity is cated trackingduce more cocertainty and

in the Wind

market is alsr this: Virtuallyupwind desi

opular three tos are being ing offered pr are also founed for offsho

ids that showwhich dominates. To coupwind turbine-bladed desig

ommunities loand maintena

o-bladed downrst two-bladestalled in U.K

ions for vertifootball stadidium. The latlass of micro ons is the saalmost alwa

neer at thesety of vertical ae, France frome is schedule

this design rototype has

sold today ararms or thoses, ranches an

ewable Energrt in the Unitnts, are crea

Cleto Wa

Research LLC and m

SunPower Coesting groundPA with SoutJohnson Conowned by So

in the low dog and the reqomplexity andcosts if not m

Sector

so undergoingy every commgn. Howevero four decadepromoted durimarily at thend at the extrore power ge

wcase the evoated offeringsnter these de that claims gns, explicitly ooking for selfance crews.)

wnwind rotors,ed prototype

K. waters in 20

ical axis desums, as evitter example vertical axis

ame drawbacays at higher e vertical desiaxis machinem developing

ed to be unvelacks a yawbeen in ope

re those with e with 10 kW ond farms in ru

gy Lab definested States. A

ating incentive

ean Energatch in 201

may not otherwise be

orporation is ad for this vershern Californntrols, the Uoitec.

ouble-digits. Tquirement to md greater eng

managed prop

g considerablmercial wind tr, two-bladedes ago – are aue to capital e small-scalereme other eneration.

olution of wins in the pastdrawbacks, Nreliability as marketing th

f-reliance (and

however. Foe designed 012.

igns may beidenced by is one of thdesigns. His

k for this desr elevations. igns for resids for any app

g a 3.5 MW veiled later thisw system, piteration since

a generationor less in capural areas. Nos as betweenAggregation pes for comm

y: Ten Tre11 and Bey

accessed or used, w

approximatelysion of solar pia Edison. An.S.-based bu

The challengemanage highegineering expeperly.

le diversificatturbine is basd and verticaattempting to cost savings end of the mnd of the ma

nd turbine det – are notorNordic Windp

one of its pris reliability (dd those witho

or example, thfor offshore

for on-site pthe plans fo

he few high pstorically, the sign: access tThat is why

dential use. Inplication. Thatvertical axis tus year. Countch system, a

March 2010

n capacity of pacity, designow, mid-sizedn 100 kW to 1platforms, suunity and reg

ends yond

without the

y 20% power, nother uilding

e with er site ertise.

tion in sed on al axis

stage s. And market rket –

signs. riously power rimary due to out the

he B-2 wind

power or the profile prime to the most

n fact, t view urbine nter to and a

0 near

more ed for

d wind MW) ch as gional

© 2011 Pike ReAll Rights Reseexpress written

Figure 3.

3.3

search LLC. rved. This publicationpermission of Pike Re

renewabeconomcustome

A numbEnergy they arAdditionfor emeCanada

1 Mid-S

Waste-

The gigabecomemethod environmpollutionappear t Today, These pestimate

may be used only asesearch LLC.

ble systems. mics of mid-siers.

ber of recent Laboratory, be optimized

nally, “pay as erging marke and southern

ized Wind M

-to-Energy

antic amount e a major en

for managingment, includinn, odor, and ato be a noble

more than 90plants treat aed output of 1

s expressly permitted

Aggregate zed power s

developmentbode well for

for lower wyou go” finants in the den Mexico.

Market for Nor

Market: Ch

of waste haunvironmental g and treatingng: land occuaesthetics. Trsolution.

00 thermal wan estimated

30 terawatt h

by license from Pike

14

net meteringystems looki

ts, including the long-term

wind speed cncing programveloping wor

rth America,

hina, Europe

uled to dumpsissue. Landfg waste. Yet upation, greeransforming t

waste-to-energ0.2 billion to

hours (TWh) o

Cleto Wa

Research LLC and m

g is the keyng to share

R&D supportm viability of m

conditions bms will increarld – includin

Average Sc

(Sour

e, and the U

s, accumulatifilling is still this practice

nhouse gas these wastes

gy (WTE) plans of municipof electricity.

ean Energatch in 201

may not otherwise be

y policy reforesources am

t from the Namid-sized turby increasing

ase the appeang remote re

cenario: 2007

rce: Pike Resear

United Stat

ing in heaps the world's

e has detrime(GHG) emiss

s into electric

ants operate pal solid was

y: Ten Tre11 and Bey

accessed or used, w

rm optimizinmong a hand

ational Renewbines, particul the swept

al of these turegions of no

7-2015

rch)

tes

and open pitsmost widely

ental effects osions, groundity and heat w

around the gste (MSW) w

ends yond

without the

g the dful of

wable larly if area.

rbines rthern

s, has used

on the dwater would

globe. ith an

© 2011 Pike ReAll Rights Reseexpress written

Chart 3.2

search LLC. rved. This publicationpermission of Pike Re

2 Waste

As Pikeleadershgrowth oppositiadd 20 dense pworldwid

Massiv1 billiorate ofexpect

GoversustainWTE subsid

China top twto tack

Policiesstructurestrong delectricitenergy.”Denmar

$

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

($ M

illi

on

s)

may be used only asesearch LLC.

e-to-Energy R

e Research’s hip role in wain consumpton dynamics new WTE pl

population ande. Strong dri

ve urban growon people willf 8% to 10%ted to grow to

nment policienable treatmeas a renewa

dies and a cor

needs massio consumerskle energy de

, regulationse of the WTEdriver for maty and 55 TW” The electrrk, roughly 40

$-

0

0

0

0

0

0

0

0

2010

Ro

As

Ea

W

No

s expressly permitted

Revenue by R

market foreste-to-energytion (and wato these ofteants per yea

nd lack of reaivers reinforci

wth and daun live in cities per year. C

o 210 million t

es to supporent of MSW aable and alterporate tax ex

ive sources o of energy in pendency an

, and rules E market. For arket growth,

Wh of heat in 2icity supply

0% of its renew

2011 20

oW

sia Pacific

astern Europ

Western Europ

orth America

by license from Pike

15

Region, Wor

cast shows, y revenue, thaaste), as wen unpopular t

ar throughout al estate), Ching the growth

nting MSW gs in China by hina generattons by 2015.

rt the develond the producernative sourxemption for f

of energy to sthe world. W

d availability.

have had a example, thewhere close

2009. About 5was sufficiewable energy

012 2013

pe

pe

a

Cleto Wa

Research LLC and m

rld Markets:

(Sour

Asia Pacificanks to surginell as less technologies.the forecast

hina is the mh of the WTE

generation. Th2050. MSW

tes 150 millio.

opment of tection of renewrce of energfive years of o

sustain its groWaste can bec

fundamentale Landfill Diree to 400 WT50% of the ent for powe

y comes from

2014

ean Energatch in 201

may not otherwise be

2010-2016

rce: Pike Resear

c is moving ing populationproblematic . Although Japeriod and

most attractiveE market in Ch

he United Na generation h

on tons of MS

echnologies fowable energygy. Specific Woperation.

owth. The coucome a strate

l impact on ective of the ETE plants sunergy is cons

ering 8 millioWTE.

2015 201

y: Ten Tre11 and Bey

accessed or used, w

rch)

nto the worls and an attesiting and c

apan is expecbeyond (due e market for hina include:

ations expecthas increasedSW yearly. T

for the soundy. China recogWTE laws in

untry is amonegic energy s

the evolutionEU has actedpplied 30 TWsidered “renewon household

6

ends yond

without the

dwide endant citizen cted to

to its WTE

ts that d at a

This is

d and gnizes nclude

ng the source

n and d as a Wh of wable ds. In

© 2011 Pike ReAll Rights Reseexpress written

3.3.1

Table 3.1

ReAlaCaCoHawIdaLouMisNeNewOreTexUtaWy

Tot

search LLC. rved. This publicationpermission of Pike Re

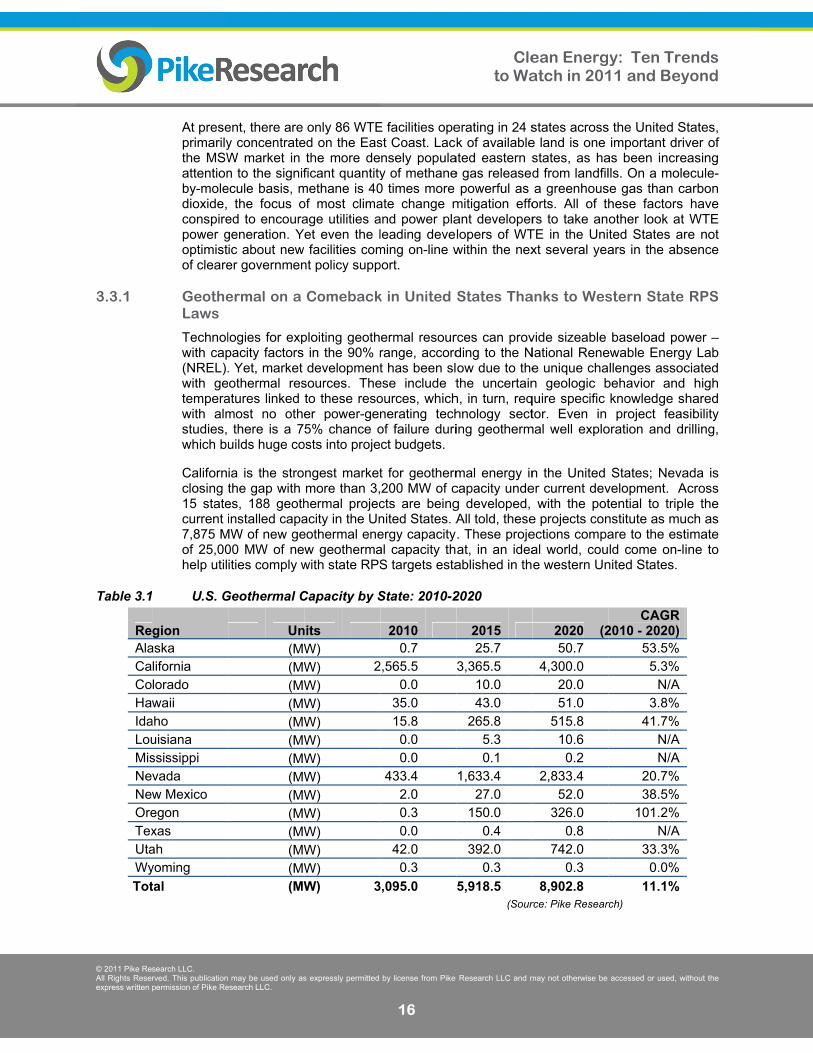

At preseprimarilythe MSWattentionby-moledioxide, conspirepower goptimistof cleare GeotheLaws

Technolwith cap(NREL).with getemperawith almstudies, which bu

Californclosing t15 statecurrent i7,875 Mof 25,00help util

1 U.S. G

gion aska lifornia lorado waii

aho uisiana ssissippi vada w Mexico egon xas ah yoming

tal

may be used only asesearch LLC.

ent, there are y concentrateW market in n to the signifecule basis, m

the focus oed to encourageneration. Yic about newer governmen

ermal on a

logies for exppacity factors . Yet, market othermal res

atures linked most no othe

there is a 7uilds huge co

ia is the strothe gap with es, 188 geothinstalled capa

MW of new ge00 MW of neities comply w

Geothermal C

Un(MW(MW(MW(MW(MW(MW(MW(MW(MW(MW(MW(MW(MW(MW

s expressly permitted

only 86 WTEed on the Easthe more deficant quantity

methane is 40of most climaage utilities aet even the l facilities com

nt policy supp

Comeback

ploiting geothin the 90% rdevelopment

sources. Theto these resoer power-gen5% chance o

osts into proje

ngest marketmore than 3,hermal projecacity in the Uneothermal enew geothermawith state RPS

Capacity by S

nits W) W) 2

W) W) W) W) W) W) W) W) W) W) W) W) 3

by license from Pike

16

E facilities opest Coast. Lacknsely populay of methane0 times more ate change mand power plaleading deveming on-line wport.

k in United

ermal resourrange, accordt has been sl

ese include tources, whichnerating techof failure durict budgets.

t for geotherm200 MW of ccts are beingnited States. Aergy capacityal capacity thS targets esta

State: 2010-2

20100.7

2,565.50.0

35.015.80.00.0

433.42.00.30.0

42.00.3

3,095.0

Cleto Wa

Research LLC and m

erating in 24 sk of available

ated eastern se gas released

powerful as mitigation effoant developerlopers of WTwithin the nex

States Tha

rces can provding to the Now due to thethe uncertain

h, in turn, reqhnology secting geotherm

mal energy incapacity undeg developed, All told, these. These projeat, in an ideaablished in th

2020

201525.7

3,365.510.043.0

265.85.30.1

1,633.427.0

150.00.4

392.00.3

5,918.5(Sour

ean Energatch in 201

may not otherwise be

states acrosse land is one states, as had from landfila greenhousorts. All of thrs to take an

TE in the Unixt several yea

anks to Wes

vide sizeable National Renee unique chan geologic b

quire specific tor. Even in

mal well explo

n the United er current dev

with the pote projects conections compaal world, coue western Un

2020 (250.7

4,300.0 20.0 51.0

515.8 10.6 0.2

2,833.4 52.0

326.0 0.8

742.0 0.3

8,902.8 rce: Pike Resear

y: Ten Tre11 and Bey

accessed or used, w

s the United Simportant dri

as been incrells. On a mole

se gas than chese factors other look at ted States arars in the abs

stern State

baseload poewable Energllenges assoc

behavior andknowledge sproject feas

oration and d

States; Nevavelopment. Atential to tripnstitute as muare to the estld come on-l

nited States.

CAGR 2010 - 2020)

53.5%5.3%

N/A3.8%

41.7%N/AN/A

20.7%38.5%

101.2%N/A

33.3%0.0%

11.1%rch)

ends yond

without the

States, ver of

easing ecule-

carbon have WTE

re not sence

RPS

ower – y Lab ciated high hared sibility rilling,

ada is Across le the

uch as timate ine to

© 2011 Pike ReAll Rights Reseexpress written

search LLC. rved. This publicationpermission of Pike Re

In a buStates w5,816 Mfor the pgovernmincrease

In the abbleak. TgeothermdescribeCounty best solthe Sunthis richdevelop

may be used only asesearch LLC.

usiness-as-uswill add 2,313

MW is forecasperiod of 201

ment subsidiee this rate.

bsence of staThese state pomal developmed as the “cis notable noar resources

nrise Powerlinh renewable red by CalEne

s expressly permitted

ual, base ca MW of geoth

st to come on10-2020. Brees and legisla

ate RPS policolicies are nowment since vicrown jewel” ot only for its , as well as s

nk transmissioresource basergy – with loa

by license from Pike

17

ase scenario,hermal capac-line, represeeakthroughs ative support

cies, the geothw driving inveirtually all geof renewabprime geothe

significant winon line is now

sin – includinad centers in

Cleto Wa

Research LLC and m

, Pike Reseacity by 2015. enting a still rin drilling tect for renewab

hermal markeestment in ne

eothermal resle resource ermal sites bnd capacity.w under con

ng four new gSan Diego.

ean Energatch in 201

may not otherwise be

arch forecastOver the nex

remarkably lochnology, as bles at the fe

et in the Uniteew transmissiosource areas

regions in Cbut also for soAfter considestruction, ultigeothermal p

y: Ten Tre11 and Bey

accessed or used, w

ts that the Uxt decade, a tow CAGR of 5well as cons

ederal level,

ed States wouon, which is vare remote.

California, Imome of the werable controvimately conne

power plants

ends yond

without the

United otal of 5.44% sistent could

uld be vital to Often

mperial world’s versy, ecting being

© 2011 Pike ReAll Rights Reseexpress written

4.1

search LLC. rved. This publicationpermission of Pike Re

Is Chin

By 2020fossil fupower mthe counproductslarger, mChinesegeneratecontent supply cthe prosreturns fand lose

In 2010previousslowing

While its lawinstallecarbon

Many compe

TraditinonethdeveloChina

One Chparticulamost soGoldwintechnoloall possability to

Unlike oGoldwinlauncheturbine delivery

may be used only asesearch LLC.

CHINAND THE

na’s Wind P

0, the Chinesel alternative

market in the ntry is now ims have suffermore establise wind power e the revenurules that re

chain. In whats and cons ofor China – aers.

0, China incres year. Howevdue to the fo

China used Gws have yet toed wind capan-free electric

of the PPAensation, redu

onally, subsiheless, subsiopers. This bwhen depend

inese wind carly in the U.Sophisticated snd Science &ogy and creatible worlds: E

o drive down t

other successnd is lookingd a joint venin Pipestone project (>106

s expressly permitted

SeNA’S CLEE FUTURE

ower Grow

se governmenes, such as wworld, but is

mposing new red from quashed firms. Fmarket, such

ues they hadequire 70% ot has now bec

of doing businand not foreig

eased its totaver, for the firllowing:

Germany’s fee be enforced.

acity has yet tcity.

As signed inucing expecte

dy payouts idies are pai

bi-annual payding on intern

ompany stanS. Goldwind trategy for gl

& Technologytive business European engtechnology co

sful Chinese w well beyondnture in the Town, Minne

6 MW) in Sha

by license from Pike

18

ection 4EANTECHE OF NUC

wth Rate Sus

nt plans to owind and solaexperiencingquality stand

ality control, Furthermore, h as the Spand anticipated.of all compocome a familness in a man internationa

al wind powerst time since

ed-in tariffs a. In fact, it is eto be connect

n China coned profits for d

in most cound out every

yout makes inational sourc

ds out becauScience & Teobal wind po

y is impressinapproach. T

gineering exposts to the low

wind turbine cd China’s boUnited State

esota and haady Oaks, Illin

Cleto Wa

Research LLC and m

4 H GROWTCLEAR PO

stainable?

obtain 15% ofar power. To

g a backlash odards to weedand is conceEuropean m

nish company This is larg

onents to be iar tale, foreig

arket that is cal corporation

er capacity te 2005, the co

nd mandatoryestimated thated to the gri

ntain grid cudevelopers.

ntries occur osix months, t particularly

ces of credit.

use its makinechnology is

ower developmng wind induhe company

perience, U.Swest possible

companies –orders for bues. The comps also signed

nois.

ean Energatch in 201

may not otherwise be

TH OWER

f the nation’soday, China ion several frod out smaller entrating manmanufacturersy Gamesa, hagely due to C

manufacturegn manufactuclearly tilted tns. There are

to 41.8 GW, ountry’s growt

y grid accessat approximatid and actuall

urtailment pro

on a monthlycreating casdifficult to f

g an impact the Chinese

ment. A stateustry veteransappears to co

S. entrepreneu levels.

such as Sinousiness oppopany has insd a contract f

y: Ten Tre11 and Bey

accessed or used, w

s total energys the largestonts. For exacompanies w

nufacturing as that entereave been unaChina’s stricted by its domurers try to batoward maxim inevitable wi

up 62% fromth in wind pow

as a model, ely 30% of Cly deliver valu

ovisions that

y basis. In Csh flow issuefinance proje

on global macompany wi

e-owned coms with its suombine the burship and C

ovel Wind Grortunities andstalled its 1.5for a larger tu

ends yond

without the

y from t wind ample, whose among ed the able to t local mestic alance mizing inners

m the wer is

so far hina’s uable,

t lack

China, es for cts in

arkets, th the

mpany, perior

best of hina’s

roup – d has 5 MW urbine

© 2011 Pike ReAll Rights Reseexpress written

4.2

search LLC. rved. This publicationpermission of Pike Re

The Chithe focudomestithe solawitnesse

In the ldistributcountry utility-sc2015 angoals, p

The booboth scaplaguingdistribut

The receHoldingssolar indworld’s 2 GW aentrywanegotiatMongoli

Chineseworld’s Chinesethe past

Did Nu

The serMarch 1United Sfrom thegreen athat the designe

Other nnotably (23%), i

Supporta Galluenvironmicon Whvirtues oanswer

may be used only asesearch LLC.

nese market us has been cally. While t

ar PV marketed with wind p

ong term, soted generatiothat currently

cale wind pownd 20 GW by articularly if s

oming Chinesale and techng wind powerted solar, a dy

ent agreemens, Ltd. signalsdustry. The mleading Eurolready in the y into what mtions to consa.

e manufacturesolar PV ca

e market instet several year

uclear Powe

ries of grave 11 earthquakStates and ae right – not ths of late due United Stated to revive a

nations acrosGermany, whs now phasin

t for nuclear pp poll showementalists suhole Earth Caof micro-nuketo global clim

s expressly permitted

for solar is, inplaced on e

this is about tt in China topower.

olar PV shoun technologyy lack a modwer projects. 2020. Close

solar PV is int

se economy anology. It cour at the transynamic that e

nt between Fs that China

move by First opean solar pipeline, Firs

may become struct a new

ers such as Spacity in 201ead of Europers.

er Just Miss

nuclear mishke and tsunaround the wohe left – may to concerns

es will plow $3nuclear indus

ss the world,hich derives ang out the tech

power hit an aed that 62%uch as Stewaatalog, tout nes, which Bec

mate change.

by license from Pike

19

n many waysexporting proto change, it a

o reach anyw

uld be a bigy and can offeern grid, its g All told, Chobservers su

tegrated into n

allows the sould be that thsmission levechoes Califor

irst Solar Inc.is looking forSolar was almarket due

st Solar sees the next sola

w thin film so

Suntech Powe10, are refoce, which has

s the Boat?

haps at multipmi is still affeorld. Within thspell doom foover global c

36 billion of festry on the ve

however, aa similar amohnology for go

all-time high inof the gene

art Brand, theuclear plants

chtel of San F

Cleto Wa

Research LLC and m

s, the inverse oducts overseappears that

where near th

hit in Chinaer carbon-fregrowth is lesina has set auggest that Cnew construc

olar industry ahe problems el open the drnia’s situatio

. and China Pr help from mlegedly due tto recessionthis partners

ar boom targeolar manufac

er Holdings, cusing their been the wo

?

ple reactors ifecting percephe United Staor the power climate changederal taxpay

erge of a surp

appear to be ount of its totaood.

n the United Seral public sue Bay Area ps. Brand now Francisco also

ean Energatch in 201

may not otherwise be

of its wind poeas rather thit will take an

he momentum

a. Since solaee power in las impacted ba goal of 5 G

China could ection in urban

a wide range with grid inte

door to a gren over the pa

Power Internamajor internatito the predicten-induced beship with Chinet. First Solacturing plant

Inc., which inmarket plans

orld’s best sol

in Japan thatptions of nucates, current source that h

ge. Presidentyer money intrising renaiss

diverging fral electricity fr

States exactlyupported nucpublisher of ttours the co

o claims to be

y: Ten Tre11 and Bey

accessed or used, w

ower market, han installing other few yeam the countr

ar PV is largarge swaths by grid issuesGW of solar Pasily exceedregions.

of opportuniterconnectionseater emphasast decade.

ational New Eonal players ed falling-off elt-tightening. na Power as r has also bein northern

nstalled 80% s on the domar PV marke

t resulted froclear power political dyn

has been drapt Obama mainto loan guarasance.

rom Obama,rom nuclear p

y a year ago, clear power. the counter-cuntry, extolline a vital part

ends yond

without the

since them

ars for ry has

gely a of the s than PV by these

ties in s now sis on

Energy in the of the With

a key een in Inner

of the mestic t over

m the in the amics ped in ntains

antees

most power

when Even

culture ng the of the

© 2011 Pike ReAll Rights Reseexpress written

search LLC. rved. This publicationpermission of Pike Re

And theso far ascountry’than “renuclear Even Cdecadesgeneratiproposenuclear applied The trutnuclear concernU.S. soioperatorloan guaBush ha While Oclaim thless comthan nuelectricitsocialistParty thworld’s t Globallyreactorsappearssupport the counleader oanswers

may be used only asesearch LLC.

e U.S. federals to redefine s states: New

enewable,” coand “clean” c

alifornia, whis, has not ion. Areva,

ed a “clean enplant, alongsto next-gener

th of the mattas a viable

ns, and the cal in two decadr in the Unitearantee prog

ad allocated.

Obama sticks ey want to tr

mpatible with uclear powerty from nucletic energy polat drives the top market hi

y, there are 4s have been us to be dead i

has evaporantry now seemon solar PV s, such as offs

s expressly permitted

l government“renewable”

wly proposedomprising a ncoal.

ch has had been immunthe giant F

nergy” park inside solar andration nuclear

ter is that eveoption in th

apital risks assdes. A few daed States tesram not be e

up for nuclearim governmethe GOP’s lo. Virtually al

ear – France,licies. Ironicaultimate stakestorically.

42 reactors uunder construn Europe. Ja

ated in light oms poised to technologies

shore wind.

by license from Pike

20

t, with encourenergy stand federal stan

new category

a de facto bne to growinFrench state- Fresno, Califd wind arraysr facilities.

en before the he United Stsociated with ays before thestified before expanded bey

ar power, whaent down? If yove of free mal of the cou, Lithuania, Ully, it may bee in the heart

up and runninuction in Ruspan, too, was

of recent revere-focus its e

s, Japan is n

Cleto Wa

Research LLC and m

ragement frodards that alrendards wouldy of technolo

ban on nucleng internation-controlled nfornia that wos, highlighting

earthquake, tates due to a technology

e earthquakeCongress, r

yond the $18

at about the Tyou think aboarkets and disuntries that dUkraine, Swede the Tea Part of the nuclea

ng, just over sia, China, Ins building moelations abouefforts on renenow looking

ean Energatch in 201

may not otherwise be

m President eady exist in focus on “cle

ogies that inc

ear power fonal interest nuclear enginould feature itg the clever g

utilities werelow natural

y that had not, the CEO of recommendin8.5 billion tha

Tea Party far rout it, there issdain for reguderive the grden – featurerty movementar industry in

100 in the Unndia, and Braore nuclear ret nuclear meewable optiontoward large

y: Ten Tre11 and Bey

accessed or used, w

Obama, has more than haean” energy ludes both “c

r more than in nuclear pneering firmts latest genegreen sheen

e shying awaygas prices,

t been deploythe largest nu

ng that the nuat former Pres

right, the folkss no power sulation and sureatest amoue central plant in the Repuwhat has bee

nited States. azil, the technactors, but poltdowns. Howns. Once the er-scale altern

ends yond

without the

gone alf the rather clean”

three power , has

eration being

y from siting

yed on uclear uclear sident

s who source ubsidy unt of nning, blican en the

While nology olitical wever,

world native

© 2011 Pike ReAll Rights Reseexpress written

Alternatin

Concentra

Concentra

Direct Cu

High-Volta

Independe

Levelized

Megawatt

Photovolta

Power Pu

Renewab

Terawatt

Utility Ow

search LLC. rved. This publicationpermission of Pike Re

g Current .....

ated Solar Ph

ated Solar Po

rrent .............

age Direct Cu

ent Power Pr

Cost of Ener

t ....................

aic ................

urchase Agree

le Portfolio St

Hours ...........

ned Generati

may be used only asesearch LLC.

ACRON

.....................

hotovoltaics ...

ower ..............

.....................

urrent ...........

oducers ......

rgy ................

.....................

.....................

ement ..........

tandards ......

.....................

on ................

s expressly permitted

SeNYM AND

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

by license from Pike

21

ection 5D ABBREV

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

......................

Cleto Wa

Research LLC and m

5 VIATION L

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

ean Energatch in 201

may not otherwise be

LIST

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

.....................

y: Ten Tre11 and Bey

accessed or used, w

................. AC

................. CP

................. CS

................. DC

................. HV

................. IPP

................. LC

................. MW

................. PV

................. PP

................. RP

................. TW

................. UO

ends yond

without the

C

PV

SP

C

VDC

P

COE

W

V

PA

PS

Wh

OG

© 2011 Pike ReAll Rights Reseexpress written

Section 1Executive

1.1 1.1.11.1.21.1.3

Section 2Global De

2.1 2.1.12.1.2

2.2 2.2.12.2.2

2.3 2.3.12.3.22.3.3

2.4 Section 3Global Re

3.1 3.2 3.3

3.3.1Section 4China’s C

4.1 4.2

Section 5AcronymSection 6Table of CSection 7Table of CSection 8AdditionaSection 9Sources Notes .....

search LLC. rved. This publicationpermission of Pike Re

1 ...................e Summary .Ten Trends t

1 Global De2 Global Re3 China’s C2 ...................eployment TUtilities Back

1 Utility-Ow2 Offshore Economies o

1 Bigger Is 2 Small Is BMoving from

1 Offshore 2 Hydrokin3 Floating SDirect Curren

3 ...................enewable EnGreater DiveGreater DiveWaste-to-En

1 Geotherm4 ...................Cleantech GrIs China’s WDid Nuclear

5 ...................m and Abbrev6 ...................Contents .....7 ...................Charts and F8 ...................al Reading ..9 ...................and Methodo.....................

may be used only asesearch LLC.

.....................

.....................to Watch in Ceployment Trenewable Tec

Cleantech Gro.....................

Trends ..........k Into Key Rewned, Utility-S

Wind Power of Scale Trend

Better ..........Beautiful .......Traditional TWind Power etic TechnoloSolar PV ......nt T&D Syste.....................

nergy Trendsersification witersification witergy Market:

mal on a Com.....................rowth and th

Wind Power GrPower Just M.....................