water supply and sanitation strategy - world...

TRANSCRIPT

Water Supplyand Sanitation StrategyBuilding on a solid foundation

Prepared by Camellia Staykova (EWDWS)Task managed by Bill Kingdom (EASUR)

As Vietnam becomes richer it faces challenges in adapting its infrastructurepolicies and institutions. While the old challenges of providing basic servicesto all remain, new challenges are emerging, such as accessing new sources offinance, refining planning processes, preparing for rapid urbanization,improving the efficiency of infrastructure service providers, developingstronger institutions to encourage private finance of infrastructure or directprivate provision of infrastructure, and developing more targeted approachesto poverty alleviation.

This report on Water Supply and Sanitation Strategy - Building on aSolid Foundation is one of six volumes dealing with Vietnam's InfrastructureChallenge. Other volumes deal with Infrastructure Cross Sectoral Issues,Urban Development, Transport, Telecommunications, and Electricity.

The work for these reports was carried out between 2004 and 2006 byWorld Bank staff and consultants. The reports have been revised to takeaccount of comments made by the Government in workshops during May15-17, 2006. The comments of numerous colleagues from the World Bank,the United Kingdom's Department for International Development Bank, theAsian Development Bank, and the Japan Bank for International Cooperationare gratefully acknowledged.

Vietnam’s infrastructure challenge

iv

v

ADB Asian Development BankBOO Build-operate-ownedBOT Build-operate-transferBSP Bank for Social PolicyCAPEX Capital expenditureCERWASS Center for Rural Water Supply and SanitationCGPRS Comprehensive Growth and Poverty Reduction StrategyDAF Development Assistance FundDARD Department for Agriculture and Rural DevelopmentDOH Department of HealthDOSTE Department of Science, Technology and EnvironmentFDI Foreign Direct InvestmentGoV Government of VietnamGSO General Statistical OfficeHCMC Ho Chi Minh CityHR Human ResourceIEC Information, Education and Communication JBIC Japanese Bank for International CooperationJICA Japan International Cooperation AgencyJV Joint ventureMARD Ministry of Agriculture and Rural DevelopmentMDGs Millennium Development GoalsMoC Ministry of Construction MoF Ministry of FinanceMONRE Ministry of Natural Resources and Environment MPI Ministry of Planning and InvestmentNEA National Environmental AgencyNRW Non-revenue waterNRWSS National Rural Water Supply and Sanitation Strategy NTP National Target ProgramO&M Operation and MaintenanceOBA Output-based aidODA Official Development AssistanceOPEX Operating expenditurePC People’s CommitteePLC Public Limited CompanyPPP Public Private PartnershipRWSS Rural Water Supply and Sanitation

Abbreviations

vi

SOCB State-owned commercial banksSOE State-owned enterprisesUDC Urban Drainage CompanyURENCO Urban and Environment CompanyVBARD Vietnam Bank for Agriculture and Rural DevelopmentVBSP Vietnam Bank for Social PoliciesVDGs Vietnam Development GoalsVLSS Vietnam Living Standards SurveyVND Vietnam Dong (Currency)VUWSDP Vietnam Urban Water Supply Development Project VWSA Vietnam Water and Sanitation AssociationWHO World Health Organization WSC Water Supply companyWSP Water and Sanitation ProgramWSS Water Supply and Sanitation

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .ixExecutive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xi

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xiCurrent Situation - By Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xiiThe Way Forward . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xvBoosting Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xx Building Capacity and Knowledge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .xxi

I. Water Supply and Sanitation Policy and Institutional Framework . . . . . . . . . . .1

A. Laws and Institutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1B. Policies and Responsibilities - Urban . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2C. Policies and Responsibilities - Small Towns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4D. Policies and Responsibilities - Rural . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

II. Sector Structure and Ownership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

A. Water Supply . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Unility Provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9Small Towns / Townslets Provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11Self-Provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12Local Private Sector in Rural Areas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12

B. Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13Urban Provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13Rural Provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

III. Water Supply and Sanitation Investment Needs and Financing . . . . . . . . . . . . .17

A. Investment Needs in Water and Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17B. Sources of Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

IV Sector Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

A. Water Supply . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Access . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Overall Performance of the Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Water Tariffs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

Affordability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30B. Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

Table of Contents

vii

Access . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32Urban Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34Small Towns Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35

Rural Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .35Public Subsidies in Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .36

V. Main Issues in Water Supply and Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39The Financing Gap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .39Maturity of Sector Institutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40Sector Performance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40Private Sector Participation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44

VII. The Way Forward in Water Supply and Sanitation . . . . . . . . . . . . . . . . . . . . . . . .47A. Bridging the Financing Gap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47B. Improved Efficiency and Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49C. Boosting Sanitation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .51D. Building Capacity and Knowledge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .52

Annex 1: Laws and Regulations in Vietnam Water and Sanitation Sector . . . . . . . . . . . . . . . . . . . .55Annex 2: BOT Projects and FDI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .58Annex 3: WSS Providers: Successful Alternative Provision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .59Annex 4: Sanitation in HCMC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .60Annex 5: Investment in WSS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .61Annex 6 Access and Affordability of Water Supply Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .62Annex 7: Urban Water Utilities Operating Cost Savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64Annex 8: New Developments in RWSS Micro-credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .65Annex 9: Realistic Framework for Water Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66

viii

This study was undertaken to assist the World Bank dialoguewith the GoV and other donors/partner organizations insupporting WSS reform; to guide World Bank lending and

technical assistance in the sector; and to provide a useful source ofinformation on existing studies and data.

The report is organized as follows: The Executive Summaryoutlining the key issues for the sector and proposing a way ahead.Chapter I sets the scene by describing the policy and institutionalframework of water supply and sanitation sector in Vietnam. ChapterII describes the sector structure and provision of services, Chapter IIIgoes into the details of sector financing and investment needs withChapter IV analyzing the sector performance. Chapters V and VIinclude the summary of the issues facing water supply and sanitationin Vietnam and recommended actions.

Preface

ix

Introduction

Since 1990 Vietnam has achieved the remarkablegrowth rate of 7.4% p.a.1 , making it the world'seighth fastest growing economy. This growthhas been particularly well converted into povertyreduction. From 1990- 2005 $1 per day povertyfell from 58% -to just 8%; a rate second only toChina2. Still, Vietnam is not a rich country andthe productivity and well-being of its populationremain below their potential. Slow progress onstate-owned enterprise reform, as well ascontinued weaknesses in the lending decisionsby state-owned commercial banks andgovernment lending institutions may lead tocapital misallocation and weaken long-termgrowth.

At the end of 2005, it is estimated that about73.2% of the population in Vietnam isconcentrated in rural areas. Vietnam is urbanizingrapidly, albeit slower than other East Asiancountries but urbanization pressures will place aparticular strain on the country, especially infinancing infrastructure. Such pressures might bereduced if there is a rapid improvement of wellbeing in rural areas (including better water andsanitation services)4.

In the water and sanitation sector the level ofaccess to services is mixed. According to the

Vietnam Household Living Standards Survey(VHLSS 2004) rural access to water supply andsanitation in 2004 is, respectively, 48% and 16%.The corresponding access rates in urban areasare 82% water and 76% for sanitation. As acountry water coverage rose from 26% to 57%over the period 1993-2004 whilst thecorresponding figures for sanitation saw anincrease from 10% to 31%. However otherstudies have indicated lower levels of access5.

Investment needs to meet the Vietnam MDGsin both rural and urban water and sanitation by2020 are tentatively estimated at $600 millionannually - which is roughly 4 times the annualinvestment in the last 10 years. This pastinvestment, particularly in the urban sector, hasbeen predominantly from ODA (nearly 85% ofthe $1 billion invested). Given that donors areunlikely to massively increase their support forthe water supply and sanitation sector inVietnam, it is clear that that the financing gap willhave to be funded from within the country -either from government, or through borrowing inthe capital markets. The latter would be fundedby surpluses generated from higher user fees, andincreasing efficiency of service providers.

The challenges faced by Vietnam to meet theVietnam MDGs in water supply and sanitationare not unlike those to be found in most

Executive Summary

1. Source: General Statistics Office (GSO) figures2. Source: WDI (April, 2005)3. Source: Vietnam Growth and Reduction of Poverty, annual progress report of 2004-2005, Hanoi November 20054. Taking stock 2003. Consultative Group Meeting, December 20035. Figures from Vietnam MDG Report, April 2004 show figures of rural water & sanitation at 40% and 11.5%

respectively, and urban water & sanitation at 76% and 68% respectively. WHO-UNICEF Joint Monitoring Program(JMP) gives rural access to water supply and sanitation in 2002 is, respectively, 68% and 26%. The correspondingaccess rates in urban areas are 93% water and 84% sanitation.

xi

developing countries. Investment needs arehuge, compared to the revenue base. Low tariffsmake it impossible to expand services usinginternally generated funds. This is oftenexacerbated by low efficiency and weak technicaland managerial capacity. Efficiency andcustomer responsiveness are further reduced bythe limited incentives for management andowners. Service provision is dominated by thepublic sector leading to overlapping roles andresponsibilities, multiple objectives and poorfocus on service delivery. Inappropriate designstandards are used leading to higher capitalcosts, and adverse impact on tariffs andaffordability. Sanitation is considered a privategood requiring support to mobilize, and thusmaximize the benefits to accrue from a newwater supply.

However, compared to other developingcountries, the Vietnamese sector is dynamic andrapidly changing and there are many positiveaspects on which to build a sound future for WSSin the country.

Commercial practices in the urban sector rivalthe best in the world. Collection rates are above95% with collection periods typically being lessthan 30 days, whilst the recent Circular 104 isputting upward pressures on tariffs. Thisprovides a sound foundation from which tomobilize investment capital for furtherexpansion, and to fund adequate maintenanceand rehabilitation. All water companies alreadycover their operating costs from user fees with anational average working ratio of a verycreditable 0.63.

In addition the last two years have seen anumber of important institutional changes. Infour water companies equitization is under wayto change the legal framework under which thecompanies operate. The sector has also seenincreasing use of the private sector, for example

in the use of operating contracts in district townsand the proposed PPP contract to improveleakage management in HCMC. In rural watersupplies, fundamental change to the role ofCERWASS is under way through a new Bankfinanced project - leading to the creation of ruralwater supply companies and refocusingCERWASS on its policy and regulatory role.

On finance a new lending window has beenestablished in DAF to provide long term, nonsubsidized, financing for WSS investments andto illustrate sector opportunities to other lenders.Whilst small in size the facility is a step in theright direction. At the same time targeted capitalsubsidies are being piloted in a planned OutputBased Aid scheme in HCMC.

Finally, the Government is formulating a newUrban Water Decree to capture the new directionand provide guidance for the way ahead. Anumber of the recommendations in this report areunderstood to be reflected in the draft Decree.

Overall, therefore the pace of change is rapidand generally positive. The WSS strategypresented in this report will further support andenhance the development of the sector.

The key findings from the study aresummarized below, in two parts. The firstpresents the current situation, by sector. Thesecond draws on the sectoral assessments toidentify a number of key themes and to presentsuggestions on how the Government of Vietnammight address them..

1. Current Situation - By Sector

A. Urban Water Supply

Water supply service in Vietnam is not sufficientto meet growing demand6. The effectiveness andquality of service is variable, with larger urbancenters having higher coverage and better

xii

6. Vietnam Urban Water Supply Development Project: Pre-feasibility study, 2004

service than smaller ones. The key challenges aresummarized as follows:● Access to sufficient capital: The level of

autonomy of the urban WSCs remainslimited and tariff levels, set by the provincialPeople Committees (PCs) do not ensure thelong term financial sustainability of theutility. Over the last decade 85% ofinvestment in the urban sector has comefrom ODA, yet investment needs over thenext period are four times as high. There ismuch work to be done to build utilities thatcan be considered creditworthy to lenders,and in parallel, there is a need to develop alocal capital market that provides long-termfinancing which is currently unavailable.Access to short-term debt from commercialbanks is already occurring on a limited basisand the recent BOT initiative in HCMCshows that a range of sources of funds can bemobilized.

● Efficient operations and use of capital:Although the WSCs operational performancecompare favorably to other developingcountries, the utilization of treatment plantcapacity, particularly in small towns is low,the level of NRW remains high at 35% andthe number of staff per connection is about60% higher than the level expected in wellrun systems in developing countries. Thusthere are many opportunities to improveoperational performance and releaseresources for more productive use. Inaddition, the pilot benchmarking assessmentof capital costs in Vietnam showed widevariations in unit costs of providing systemcapacity. Taking into account that financingof capital costs usually accounts for 60-80% ofthe full cost recovery tariff, there are clearlybenefits to be derived from improved capitalefficiency.At the same time there remains someuncertainty over ownership of assets. Water

companies, PC and even central government,can potentially claim ownership of differentassets, depending on how they were financedin the first place. Whilst not a critical issuewhen the WSC are owned by the Provinces,this will become more important asequitization takes place and an increasinglycommercial logic takes hold.

● Institutional barriers and the need forincentives: Current regulations should beupdated and consistently enforced -particularly those relating to tariffs. At thesame time, the institutional models of WSCsneed to evolve to provide better incentivesfor efficient and effective service delivery.This will include formalizing assetownership, defining required performancelevels and dividend policy as well as byincreasing the autonomy and accountabilityof WSCs. With the present micro-management of the sector, the water utilityperformance is a reflection of theperformance of both the WSC managementand the PC oversight. Thus, it is alsoimportant that the PCs themselves areincentivized to deliver improved service.

● Towns require particular attention: Onlyabout one third of approximately 600 DistrictTowns have piped water supplies. These areimportant urban centers both in terms ofeconomic development, and providingalternative destinations for rural urbanmigration. Often, however, they lack financialresources or human capacity. Providingsustainable piped water supplies to thesetowns is therefore a development priority.

B. Rural Water Supply

In many rural areas people lack even theminimum amount of water needed for domesticuse. The key challenges facing the rural watersupply sector are summarized below:

xiii

● Overlapping and conflicting roles ofinstitutions: The responsible institution underMARD, CERWASS, has a dual role asregulator/developer/fund manager, andservice provider. This results in conflicts ofinterest, which isolates the provider from thegenuine needs of the beneficiary (buildingsystems that people do not want nor are willingto pay for), and develops a focus on assetcreation rather than sustainable asset operation.

● Fragmentation of the sector: Rural serviceprovision comes from many models and atmany levels (commune, district, etc.). Thisfragmentation may be acceptable for simplesystems, but for piped systems, it can lead todeterioration in service. In addition, from thegovernment side there is also a fragmentedapproach. This has been highlighted inearlier studies and led to the creation of inter-ministerial Standing Committee on ruralwater and sanitation. However, this has notmet.

● Role of the private sector: In response to aconsumer demand not being met by publicservices, the private sector has stepped intothe rural and small towns water supplyprovision by leveraging funds from fee-paying customers and own contributions.The private sector investment continuesgrowing despite the limited GoV incentivesfor private sector participation.

● Capacity in the rural sector: The highlyfragmented approach to service delivery, andthe lack of clear institutional models, leavesthe sector without any vehicles to assist eitherthe technical operations/management of thesystems, nor of their oversight by thecommunes and others. The professionalassociation VWSA is predominantly focusedon urban water companies, and given thefragmentation of the rural sector, reachingout to such a large number of

owners/operators will require a new modelof capacity building.

● Sustainability of service provision: In the pastthe focus was on asset creation with limitedeffort put into creating the institutionalarrangements for sustainable service provision.Paying for water services and maintainingO&M funds, has been insufficient. It isunderstood that a significant proportion of thewells drilled under previous assistanceprograms are not operational.

● Asset ownership. Unlike in the urban sectorthis is a more serious issue in rural waterservices where consumers typically provide60% of the initial capital costs to build thesystems. Despite this significant investment,the institutional arrangements leave theconsumer outside the system. Yet, it is alsounclear, how they can better participate.

C. Sanitation (Urban and Rural)

Sanitation in Vietnam is predominantly a privategood with the majority of households investingin septic tanks or latrines, depending on location.There are currently few wastewater treatmentplants in the cities. As a result, the watercourses,especially in the big cities, are severely polluted.GoV is paying commendable attention toaddressing environment degradation. Hanoi,HCMC, Haiphong, Danang, Halong and severalsecondary cities will all have sewerage andsewage treatment facilities in place in the nextfew years.

Sanitation in rural areas is rudimentary. Despitethe very low sanitation coverage of 11.5%7 in therural areas, the access to latrines has had animpressive growth rate of 238% between 1998 and2002 comparing to the water access growth rate of36% for the same period. The financing source forthis impressive growth has been predominantlycommunity/user contributions.

xiv

7. Vietnam MDG Report, April 2004 show figures of rural water & sanitation at 40% and 11.5% respectively.

● Predominantly an urban challenge in theshort term: With urbanization and theincreasing degradation of urbanenvironment the focus of the governmentshould be on urban sanitation. Here, giventhe relative inexperience of sanitation in thecountry and the region, there is a need todevelop an improved understanding of thekey issues including:

i. Institutional arrangements, e.g. stand-alone wastewater companies,combined companies, separation ofroles and responsibilities;

ii. Cost recovery via tariffs;iii. Financing by utilizing ODA, mix of

grant and loans;iv. Appropriate technical approaches and

standards of service;v. Capacity building since there is a

general lack of expertise in the sector.● Huge need and limited capacity: The Urban

Environmental Companies, who areresponsible for drainage, sewerage, solidwaste management and other urbanactivities, are institutionally and financiallymuch weaker than WSCs.

● Urban tariffs: The GoV Decree 67/2003introduces a uniform environmentalprotection charge for wastewater serviceswhich must not exceed 10% of the cleanwater tariff and should be collected by theWSCs. There is some confusion about thepurpose of this charge. The Provinces believethis is the wastewater fee, whereas, in fact,MONRE's purpose was to establish this as aseparate environmental charge, in addition toany wastewater fees. In many developedcountries the wastewater tariffs exceed watertariffs - so a 10% ceiling on wastewater tariffsis not sustainable and needs to be revised.

● Urban subsidies: The use of localgovernment subsidies for operating costs is

not sustainable. Those cities that areintroducing sanitation services are alsostarting to charge for the service. However,the charges levied are low and will not coverO&M costs in the short term. The intentionis that charges will rise as consumersbecome accustomed to the benefits of thenew services. This will need carefulmonitoring to avoid major future drains onlimited local government resources. As aminimum tariffs should cover both O&Mcosts and the depreciation of short livedassets.

● Sanitation benefits leveraged with softinterventions: Provision of latrines andsanitation infrastructure brings improvedoutcomes. However, these are significantlyincreased when beneficiaries are exposed toIEC on household sanitation practices. SuchIEC also generates demand for householdsanitation facilities, which can be providedby the private sector.

D. Cross Sectoral Issues

Whether urban or rural, water or sanitation,there is a need to improve the collection andquality of data about the sector. This will providepolicy makers and other stakeholders with theinformation they need to make the best decisionsfor the sector.

In addition, as the sectors become larger andmore sophisticated, there will be a need tofurther enhance the technical and managerialcapacity of a full range of stakeholders includingservice providers, system owners, oversightagencies in government, and customers.

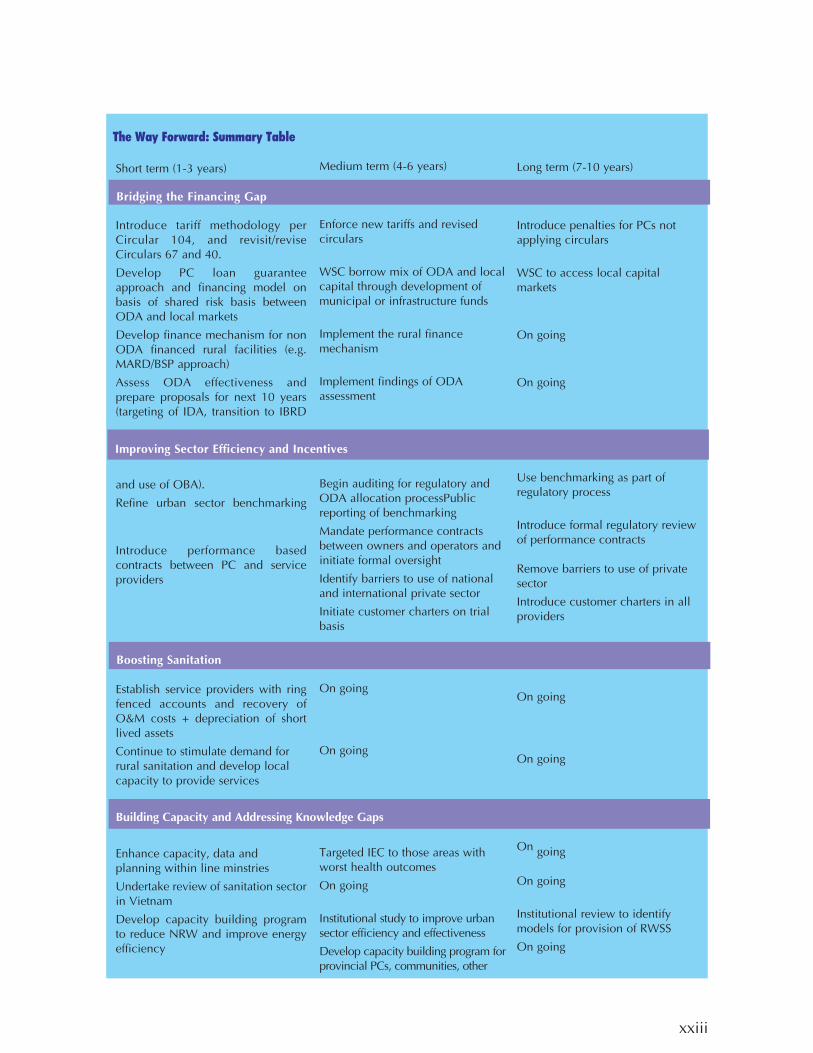

2. The Way Forward

Based on the above sectoral assessments, thefollowing themes have been identified asneeding specific attention by the Government in

xv

order to further improve sector performance.The recommendations presented under eachtheme are directed at further clarifying the GoVurban and rural WSS strategies:

a) Bridging the financing gapb) Improving the sector efficiency and

incentivesc) Boosting sanitationd) Building capacity and addressing

knowledge gaps

A. Bridging the Financing Gap

Allocation of public funds and ODA

A forward-looking detailed development planfor the sector is needed where public investmentand recurrent expenditure are linked and scarceresources efficiently and effectively allocated. TheGoV resources as well as ODA funds should bedistributed based on assessment of externalities,cost of service provision, and the wealth ofrecipients - possibly using output-based aid(OBA) as a tool to allocate grant components.Currently, the relatively wealthy urban areasreceive 84% of ODA funds whereas the ruralareas, where 75% of the population resides, enjoyonly 13%.

The effectiveness of ODA over the past 10years needs to be assessed and supplementedby proposals for changing the role and use ofODA in the future. This will be particularlyimportant given the likely graduation ofVietnam from IDA to IBRD over the coming 10year period. Gradually, ODA should moveaway from water production to waterdistribution, from water supply to sanitation,and from funding investment to leveraginglocal capital. IDA funds should be used tosupport sanitation projects where publicbenefits are high and beneficiary awarenessand willingness to pay are more limited. Thiswill require alternative sources of financing,

particularly for water investments. The GoVneeds be proactive in determining the use ofODA funds through improved policyimplementation and coordination by the lineministries MoC and MARD.

As part of the need to expand alternativesources of finance, particularly for waterinvestments, the government should revisitCircular #40 (May 2005). This determines on-lending terms for ODA in a manner that is likely toreduce, rather than expand, alternative financingsources.

Tariffs and cost recovery.

The key to the success of the sector is higher butrealistic and affordable tariffs. Introducing andenforcing a uniform tariff mechanism for thewhole country is step in the right direction.Whilst joint circular 104 (November 2004) and itspredecessor (Circular #3, June 1999) both have asound basis for tariff calculations, the issue is oneof enforcement. In the long term the governmentshould consider the possibility of automaticindexation of tariffs as one way of retaining thevalue of user fees in real terms.

On the wastewater side the governmentshould review Circular #67 (2003), which capswastewater fees at 10% of water tariffs. Giventhat wastewater operations and investmentstypically cost more than the equivalent waterservices, such constraints will further diminishthe sustainability of the wastewater sector. As aminimum the wastewater tariffs should fullyrecover operations and maintenance costs, aswell as depreciation of short lived assets.

Currently, tariff affordability and willingnessto connect do not seem to be an issue in watersupply in Vietnam.

A new financing framework for urban utilities

As the creditworthiness of the sector improves,access to longer term local financing will become

xvi

important. The existing lending and riskmitigation instruments of IFIs can support localcapital market development. For waterinvestments a staged progression could beenvisaged over the next 10 years from currentreliance on ODA, through mixed financing, to asector built on local capital markets. Sanitationinvestments are likely to rely on grant orsubsidized funds for the foreseeable future - withsubsidies being targeted to those that most needthem.

The state banks can play a more significant rolein the financing of water infrastructure byparticipating as lenders rather than servicingagents to WSCs, thus assuming the full credit riskfor a fee. However, they need to strengthen theircommercial orientation, operational practices,profitability, balance sheet quality and loanappraisal capabilities8 in order to start lending toutilities or channel funds directly to communities.

Besides providing counterpart funding forODA water investments, the provincialgovernments could participate as guarantors onloans extended to WSCs by the SOBs. This addedsecurity on loans provided by state banks not onlyreduces the ultimate cost of funds to WSCs, andconsumers, but would better structure incentivesfor cost recovery and more cost-effective service.

The issuing of bonds by WSCs wouldencourage fiscal prudence in an otherwiseunregulated sector. The WSCs could be preparedfor such opportunities through improvedfinancial accounting rules, auditing,benchmarking, and the development of a ratingsystem.

Given the continuing high level of centralgovernment involvement in local infrastructureprojects and the immature financial sector, it islikely that a financial intermediary for local

infrastructure projects will be needed in the future.The key issue is how it will be operated and howthe sub-sovereign securities market will be built.The IDA funded Urban Water SupplyDevelopment Project includes a new unit withinDAF dealing with lending to water utilities on acommercial basis, which will recover its operatingexpenditure through the interest rate spread. Giventhe small size of the facility it must be viewed as justa small step towards the long term goal.

The proposed financing frameworkdeveloped by Baietti9 is based both on full costrecovery as a key to sustainability as well as oneffective corporate governance defining theroles, responsibilities and incentive structure forevery WSS stakeholder. Its ultimate target issustainable financing of new investment andintroducing private sector participation.

Small towns and rural areas.

As evident from the discussion above, the newfinancing mechanism relies on mobilizing localcurrency borrowing by WSCs. By contrast, insmall towns and rural areas, the consumers takeon local currency debt from micro financeinstitutions to finance small scale infrastructuredirectly. Since customers pay for the servicethrough their own debt obligations, this type ofborrowing is much more interested inefficiencies and sustainability of services andshould be actively supported by the GoVincluding with possible allocation of grants.

More precisely, a coherent workable financemechanism needs to be implemented based onthe review of the existing financing models. TheMARD proposal10 for a national creditmechanism with subsidized loans forhouseholds through the BSP and subsidized

xvii

8. The WB and IMF. Vietnam Poverty Reduction Strategy Paper Progress Report & Joint Staff Assessment, 20049. Based on Aldo Baietti. Financing framework for urban water utilities in Vietnam, July 2002. Annex 910. See Annex 8.

loans to enterprises through DAF could tacklethe issue of rural WSS finance.

B. Improved efficiency and incentives

Rationalizing sector institutions

Legal framework: The consistency andenforceability of the legal framework as well asthe speed of implementation of the sectorstrategies need improvement.

For example, a new legal frameworksupporting the National RWSS Strategy isnecessary, e.g. a legislation allowing communitywater user groups to take loans and open bankaccounts. In small towns, an appropriateregulatory framework on investment in small-scale projects for both authorities andcommunities to follow is required in order todecentralize investment decision-making thusavoiding the confusion of responsibilitiesbetween investor and investment implementingagency and simplify the project preparation11.

Policy coordination: A coordination andintegration of rural and urban water supplyprograms needs to be ensured together with thenational programs on flood and environmentalprotection as well as poverty alleviationprograms. The emphasis should be on use,sustainability and impact rather thaninvestment alone. Roles and responsibilities ofsector institutions need to be mapped andclarified - with complimentary approachesbeing adopted by donors. In addition the smalltowns/townlets segment requires a customizedpolicy and specific institutional responsibilities.Any sector policy will have to be all-inclusiveand consideration should be given toestablishing a single body governing andmonitoring water and sanitation services in

urban and rural areas.Continuing reform of rural institutions: A

plan for improving inter-ministerialcoordination, e.g. by making the NationalStanding Committee functional, should bedesigned and enforced. The plan needs toinclude the appropriate incentive structure forGoV staff, and capacity building program.Perhaps the most important task is to increasethe separation of sector policy/regulatory role ofCERWASS from its service provider role - ascurrently being piloted in the IDA funded RedRiver Delta Rural Water Supply and SanitationProject.

Targeted poverty interventions: With rapidurbanization, the GoV should decide on the focusof poverty interventions. Clearly, there is a needfor a careful analysis to establish the urban andrural priorities, although the existing strongercommunity support in the rural areas wouldsuggest that interventions in peri-urban areasmay have a greater poverty impact. Output basedaid should be considered as a mechanism for theuse of grant financing for poverty interventions.

Improving WSCs accountability, autonomyand incentives

WSCs governance and performance:International experience suggests that thefollowing attributes must be met in well run WSSservice providers:● The provider is autonomous and

accountable, i.e. able to make decisions,having access to resources and being heldaccountable for non-performance

● The provider is customer oriented, i.e.proactively informing and educating itscustomers

● The provider is market oriented, i.e.

xviii

11. WSP. Global initiative for small town WSS, October 2001.

benchmarking costs and services andoutsourcing selected activities through acompetitive process, thus introducing thebenefits of competition in the otherwisemonopolistic industry

● The sector has technical and managerialcapacity both within the service provider andin the local government (as owners). A broad strategy will be required which will

build on the following three components:i. More widespread knowledge about the

top performing water companies andbenchmark capital and operating costs

ii. Capacity building among sectorprofessionals on ways to reduce capitalcosts and improve operating efficiencieswithout sacrificing quality

iii. Policies must be put in place to provideincentives to water companies to achievehigher levels of performance

The first two are discussed later. Provision ofincentives to water companies requires a strictevaluation of performance and the need formeaningful rewards and sanctions which affectboth the service provider and their owners.

As a first step performance contracts can beprepared between the PPC and the serviceprovider. A central agency could review andadvise on these contracts to help reduce thepotential for conflicts of interest at theProvincial level. Establishing clear contractualrelationships will provide both the PC and theWSC with incentives to be flexible andresponsive to the changing businessenvironment and increasing demand. Anenforceable agreement will resolve the issueswith WSC asset ownership so that the collateralelement in securing finance is cleared. MoCshould consider an appropriate framework thatprovides WSCs with the correct incentives, andpenalties, so that the sector can grow in asustainable fashion.

Further reform would include transformingthe WSC into a Public Water PLC with the

municipality as a single shareholder. This willimprove their long term viability and provideopportunities in the future for a broaderequitization process.

Regulation: Regulation in its different formsprovides opportunities for increased autonomyand accountability of WSCs. The MoF issuedDecree 104 in 2004 introducing a uniform tariffmechanism for Vietnam based on the full costrecovery principle. In late 2005 the MoC has beendeveloping a new urban water decree that mightinclude the introduction of performance contractsbetween the PCs and the WSCs. However, theenforceability, management and monitoring ofthe current and proposed decrees poses genuinequestions of conflict of interest at the Provincelevel (as both tariff setter and owner of the WSC).Thus some form of oversight agency (nascentregulator) will be needed at the national level toreview these contracts/proposed tariffs. As aminimum such an agency could provideadvice/guidance to the PC on the design of thecontract, and on relative performanceassessments of the WSCs, even if it doesn't have aformal enforcement role.

Increasing competition: Public reporting ofthe performance of WSCs could be a promisingstart to improving transparency andaccountability. At a marginal cost, thebenchmarking initiative started in 2002 with theassistance of VWSA can be improved andformalized. The data can be used by theprovincial governments, the regulator/centraloversight agency (when established), the WSCsand the potential private investors, for cross-sectoral comparison. This initiative continuesand further funding is included in the IDAUrban Water Supply Development Project.

Increasing customer orientation: Improvedcustomer service standards enshrined in acustomer charter could prove the basis for thisorientation. The annual benchmarking datacould be supplemented by publishing a range ofstandard performance indicators. This would

xix

ensure both greater customer orientation andimproved quality of information.

Focusing on the core business. Within thenext ten years WSCs should divest theirconstruction and other services from thewater business. This will provide the basis forthe development of a competitive market forconstruction services, reduce the opportunityfor hidden cross subsidies between thedifferent businesses, and allow themanagement of the water company to focuson their core business12.

Private sector development and models forservice provision

Private sector in urban areas: The successfulreform and improved performance of WSCswill indicate the readiness of the sector formarket entry of both international players andlocal private providers. The short-term priorityshould be on network management, andfocused services (e.g. pump stationmaintenance) where a combination ofcompetition and collaboration between the localWSCs and the private sector through openbidding for service contracts could beconsidered. Whilst there has been some limitedprivate investment in the sector it is expected toremain limited or modest until the regulatoryand financial strength of the sector improves.

Management models small towns andrural: In small towns and rural areas it isexpected that contracting out operations forextended periods will be the most sustainableapproach in the short term. This is theapproach planned for the recently approvedWorld Bank Urban Water Supply DevelopmentProject and Red River Delta Rural WaterSupply and Sanitation Project.

3. Boosting Sanitation

Urban sanitation

Establishing a profit & loss entity for the provisionof sanitation services, with a defined customer andrevenue base, is the immediate step in sanitationreform. This can be complemented by increasingcost efficiency by selective outsourcing to theprivate sector. Merging the wastewater activitiesinto the business of the urban WSC will takeadvantage of operating and administrativesynergies and should be considered in all but thelargest cities where a separate wastewater companymay be appropriate.

Considering the limited resources, step-by-step improvements in urban sanitation are moreappropriate than building up expensivewastewater treatment plants and extensiveseparate collection systems. Evaluating andprioritizing appropriate capital expenditures willbe important - the use of combined versusseparate systems, for example, needs to becarefully weighed in order to achieve maximumbenefit from each VND invested. Expansion ofpiped networks to less dense areas needs to becarefully considered, alongside the extent oftreatment and the capacity of wastewater plant.These technical decisions have a significantimpact on the pace at which appropriatesanitation services can be provided.

More effective sanitation projectmanagement in rural areas

Market research is essential to understand whatintervention strategies will work and besustainable. The GoV should make use of thefindings from many other countries thatsuccessful sanitation programs require lesseducational and more promotional approaches

xx

12. Ian Walker, 2002.

to find out what motivational forces work forlocal populations in bringing about behavioralchange13.

The provinces, districts and communesshould be ranked and projects prioritized basedon poverty, existing WS coverage, water-relateddiseases, population density, and existingcapacity of local government agencies to supportproject activities. The utilization of a clusteringapproach would optimize management costsand achieve high coverage within selecteddistricts rather than spreading project activitiesout over too many districts/provinces14.

At the grass roots level, developing localcapacity to supply skills and materials to meetsanitation needs will enhance sustainability. Forexample, the type of latrine offered has to becompatible with the physical, economic andsocial reality of the household. Offering a rangeof options with upgrade possibility and range offinancing arrangements may help stimulate andsustain demand and usage.

Continuing Soft Interventions

Raising public awareness and education on thelinkages between sanitation and health is neededto support any physical investments. Since watersupply itself is insufficient to dramaticallyreduce diarrhea disease, sanitation and hygienebehavior change needs much greater emphasisin all areas. A very important initiative is theactive promotion of hand washing.

The interventions need to build on theconsiderable knowledge and educationalmaterials prepared so far. Process monitoring,self-assessments, and other methods would

support learning and dissemination of bestpractices15. The measure of success should notonly be the coverage (ownership) of sanitationfacilities but also the access, use and upgrade ofthe facilities, changes in hygiene behavior andself-sustained demand for more facilities.

4. Building Capacity and Knowledge

Incentivizing the service providers and oversightagencies will only be successful provided there isadequate capacity among them. Buildingcapacity on a sound foundation also calls forimproved data about the sector.

Addressing knowledge gaps

Compilation and analysis of sector information:Government needs to be more active in compilingand analyzing sector data. This information willallow for better and more informed decisionmaking on sector policy, on allocation of scarceODA resources, and in oversight of the sector asa whole. This will be particularly relevant if acentral responsibility is allocated to reviewcontracts and tariffs at the provincial level undercurrently drafted or existing decrees.

Sanitation: A sanitation study is required toreview the sub-sector and to develop and keepupdated comprehensive and reliable data. Themapping of access, providers and institutionalresponsibilities will allow better planning and resourceallocation. The dissemination of best practices in ruraland small towns' sanitation will ensure sustainedgrowth in access and hygiene behavior.

Review of institutional options for urbanand rural water sectors: As the water sector

xxi

13. WSP 2002 Study.

14. The World Bank, Project Appraisal Document, Red River Delta Rural Water Supply and Sanitation Project,

August 15, 2005.

15. The World Bank, WSP, Danida. VRWSIHIP, draft inception report, March 2004.

develops there will be a need to study sectordevelopments including critically assessing theissues of asset ownership, increasingseparation of roles within the sector (policy,sector regulation, ownership, corporateoversight and service provision), providingand aligning incentives, and the role ofregulation. These reviews would include anassessment of the various service models in thecountry.

Building capacity

Government: The line ministries need to buildtheir oversight and policy development skillsthrough improved collection and analysis ofdata. This will facilitate the efficient allocation ofresources and the expansion of the WSS servicesto better meet the needs of the country.

Institutions: Training is required to properlyintroduce commercial relationships andeffective corporate governance and oversightbetween the owners and the service providers.The PCs, as owners, need to improve theirunderstanding of the opportunities for sectordevelopment and how they can benefit. No suchcapacity building facility exists and nationalagencies will have to take a lead to fill this gap.

Providers: The VWSA (or appropriatetechnical institutions) should play a bigger rolein building technical and managerial capacity

in service providers. As a first step acoordinated action to reduce NRW, andimprove energy efficiency, would have mostbeneficial results. Training programs on anational scale targeting small-scale providersneed to be carried out as well in order toenhance their management and financialcapability, and capacity for quality control,contract and contractor management. It alsomakes little sense to assign communitiesresponsibility for O&M if they do not have theknowledge, skills, motivation and finances todo it. Dramatic improvements in communitycapacity and capability are needed to ensuresustainability of project investments. The small-scale IEC projects of both local and internationalNGOs could address the on-site training of localmasons. Other examples include thedevelopment of a technical backstoppingfacility for rural systems and the introduction ofa certification system for operators.

Civil society: The civil society and consumerpower groups require capacity building as amajor stakeholder naturally able to exercisesubstantial pressure on the PCs and WSCs inimproving the service provided to theconsumers. A well informed civil society isimportant to building political and publicawareness and commitment to providingimproved services and giving voice toconsumers.

xxii

xxiii

The Way Forward: Summary Table

Short term (1-3 years)

Introduce tariff methodology perCircular 104, and revisit/reviseCirculars 67 and 40.Develop PC loan guaranteeapproach and financing model onbasis of shared risk basis betweenODA and local marketsDevelop finance mechanism for nonODA financed rural facilities (e.g.MARD/BSP approach)Assess ODA effectiveness andprepare proposals for next 10 years(targeting of IDA, transition to IBRD

and use of OBA). Refine urban sector benchmarking

Introduce performance basedcontracts between PC and serviceproviders

Establish service providers with ringfenced accounts and recovery ofO&M costs + depreciation of shortlived assetsContinue to stimulate demand forrural sanitation and develop localcapacity to provide services

Enhance capacity, data andplanning within line minstriesUndertake review of sanitation sectorin VietnamDevelop capacity building programto reduce NRW and improve energyefficiency

Medium term (4-6 years)

Enforce new tariffs and revisedcirculars

WSC borrow mix of ODA and localcapital through development ofmunicipal or infrastructure funds

Implement the rural financemechanism

Implement findings of ODAassessment

Begin auditing for regulatory andODA allocation processPublicreporting of benchmarkingMandate performance contractsbetween owners and operators andinitiate formal oversight Identify barriers to use of nationaland international private sectorInitiate customer charters on trialbasis

On going

On going

Targeted IEC to those areas withworst health outcomesOn going

Institutional study to improve urbansector efficiency and effectiveness Develop capacity building program forprovincial PCs, communities, other

Long term (7-10 years)

Introduce penalties for PCs notapplying circulars

WSC to access local capitalmarkets

On going

On going

Use benchmarking as part ofregulatory process

Introduce formal regulatory reviewof performance contracts

Remove barriers to use of privatesectorIntroduce customer charters in allproviders

On going

On going

On going

On going

Institutional review to identifymodels for provision of RWSS On going

Bridging the Financing Gap

Improving Sector Efficiency and Incentives

Boosting Sanitation

Building Capacity and Addressing Knowledge Gaps

A. Laws and Institutions

Vietnamese law comprises an extensive set oflegislation, decrees, circulars, decisions and otherregulations. The main laws and regulationsgoverning the water supply and sanitation sectorin Vietnam are included in Annex 1.

The separation of regulations and institutionalresponsibility between urban centers and smalltowns follows the classification of urban centers,presented in Table 1.1, and which is usedthroughout this report. The responsibilities andregulations of WSS in rural areas are separatedfrom the urban one although, as the countrydevelops, the rural/urban split in terms ofcustomer expectations and technical solutions willstart to disappear, thus calling for a more uniformapproach.

Under the Water Resource Law, which cameinto force in January 2000, the state manages waterresources and all customers and agencies (exceptfor households) are required to obtain a license

from MARD or the relevant provincial PC to usewater sources. Based on river basin management,the Law identifies the link between land wateruse, surface and underground management andwater quality and quantity.16

Water sector responsibilities are dividedbetween central and provincial governments, asshown in Table 1.2. The Strategy and Orientationfor rural and urban water supply is a matterrequiring the approval of the Prime Minister. Theline ministries have authority over sector policyand submission of major projects to the PrimeMinister for approval whereas provincial PCs areresponsible for supply services in projects ofinvestment costs below VND 200 billion in theirrespective jurisdictions. The provincial WaterSupply Company is responsible for provision ofwater supply to urban areas and operates andcontrols both the treatment plants anddistribution networks.

In addition, a number of other formal andinformal groups are active in improving the

1

I. Water Supply and Sanitation Policy and Institutional Framework

Table 1.1: Classification of Urban Centers

Class Type Population Number/CommenSpecial Cities Largest Cities 1.5 million and more Hanoi and Ho Chi Minh City

1 National Cities 0.5 to 1.5 million Three cities2 Regional Cities 250,000 to 500,000 12 cities3 Provincial Cities 100,000 to 250,000 16 cities4 District Towns 50,000 to 100,000 58 Towns5 Townlets 4,000 to 50,000 612 Townlets

16. Vietnam Urban Water Supply Development Project: Pre-feasibility study, 2004.

sector coordination and collaboration: ThematicAd-hoc Group of MARD; Donor WSSCoordination Group; the Vietnam WaterPartnership; River Basin Organizations, andINGO Working Group17.

B. Policies and Responsibilities -Urban

The major policies in urban water and sanitationare listed in Table 1.3.

2

17. "Towards the Vietnam Development Goals for Water Supply and Sanitation", April 2004

Table 1.2: Major WSS Institutions in Vietnam

The Prime Minister Approval of WSS sector strategy and orientations

Ministry of Planning Allocates state budget. All major investment projects must have theand Investment approval of MPI

Ministry of Finance Distributes state funds to sectors and projects, sets annual sector goalsand regulates accounting

Ministry of Health Controls drinking water and sanitation quality

Ministry of Natural Manages water resources, water use, pollution and hydrologyResources and Environment

Ministry of Science and Manages standardization and technology in water & sanitationTechnology

Ministry of Education Manages integration of health, water and environmental issues into and Training standard curricula and lessons plans

Ministry of Construction Line Ministry of urban water supply, sanitation & drainage

Ministry of Agriculture Line Ministry of rural water supply and sanitationRural Development

Local City Government 3-tier system: city, urban/suburban districts and wards/communes. (People’s Committees) At each level, the people’s council elected by votes elects people’s

committee. The people’s committee has departments mirroring all keyMinistries

Departments of People’s Department of Construction or Department of Transportation and Committee Public Works supervises the operations of the WSCs

Water Supply Companies 64 state-owned WSCs in 61 provinces and cities.

Adopted from the Study on Urban Drainage and Sewerage System for Ho Chi Minh City, JICA, December 1999 and Vietnam

Water Supply Development Project. Report of Deacons and Vision & Associates, July 2002.

Water Supply: The MoC is responsible forurban water policy, which is set down in the"Orientation for Urban Water SupplyDevelopment" of March 1998 - a sound documentunderpinned by the principle that water is aneconomic and social good. The implementation ofthe policy is decentralized to provincial levelgovernments with the MoC providing oversight.The objectives of the program are as follows:

i. 100% of urban population havingaccess to safe water of 120-150l/capita/day by 2020

ii. Reform the sector including thefinancial policy

iii. Modernize technology and equipmentand enhance human resourcedevelopment

iv. Mobilize contributions from

communities and all sectors of theeconomy

During the second half of 2005 the MoC waspreparing a new decree governing the urbanwater sector. At the time of writing this report theDecree has not been published. Draft textsindicate that the government is building on the1998 document and placing greater emphasis ona clearer separation of roles and responsibilities ofthe various parties, and the introduction ofperformance contracts between the serviceprovider (the PWC) and the owner (the PPC).This will likely be complemented by greaterattention to the collection and publication ofperformance benchmarking data.

WSCs are established under decisions of provincialPCs. In large cities, WSCs report to the City Transport andUrban Public Works Departments, which are equivalent tothe Department of Construction at the Provincial level18.

3

Table 1.3: Major WSS Policies in Vietnam Urban

Main WSS Policies

GoV Strategies

CGPRS

VDGs

GoV 2010Environmental Strategy

Urban

Water Supply

Orientation for Urban Water SupplyDevelopment:By 2020, 100% of urban populationhaving access to safe water of 120-150 l/capita/day.

By 2005, 80% of urban population,especially those living far from themajor transport roads, having accessto clean water with an average dailysupply of 50 l/day/capita.

By 2005, 80% of the urban populationhaving access to clean and safe water.

By 2010, 95% urban access to cleandrinking water

Sanitation

Orientation for the Development of UrbanSewerage and Drainage until 2020:By 2020, all urban areas with suitable waterdrainage systems and wastewater treatmentfacilities.

By 2010, all wastewater in towns and citiestreated.

By 2010, 40% urban wastewater treatment and60% disposal of "dangerous waste" fromindustry, hospitals, etc.

Note: There is no policy specifically targeting small towns.

18. Vietnam Urban Water Supply Development Project: Pre-feasibility study, 2004.

Water and sanitation is clearly referenced inthe CGPRS. The WSS sector is seen as acontributor to ensuring growth and povertyreduction with concrete targets set for increasedaccess to WSS services. Within the largeinfrastructure projects in water supply, drainageand sewerage, a priority is given to Hanoi andHCMC. Besides overall WSS targets, the CGPRSalso gives directions for the provision of essentialinfrastructure facilities to poor people, poorcommunities and poor communes.

The GoV is committed to achieving theMillennium Development Goals and theVietnam Development Goals (VDG). Thedetailed targets of the VDGs are listed below.

Sanitation: Parallel to policy developmentsin water supply, in March 1999 the MoC issuedthe "Orientation for the Development of UrbanSewerage and Drainage until 2020". Theobjective of the Orientation is to reducesubsidy requirements through theimplementation of an urban drainage publicservices enterprise model, which needs toreach self-sustainability over the longer termby the means of: introducing drainage andsewerage charges and incorporating them intothe water tariff; tariffs should cover operating

costs and gradually move towards covering aportion of capital costs; and combining themanagement of water supply andsanitation/drainage except in the largest cities.

The policy aims to ensure that all urban areasshould have suitable water drainage systems andwastewater treatment facilities that guaranteeenvironmental hygiene and address floodingissues. Wastewater should be treated beforeentering the sewerage system, mostly throughthe use of septic tanks. The application of thesepolicy elements is in its very early stage.

In December 2003, the GoV issued a new 2010environmental strategy, which contains relevanttargets for water and sanitation that are notcompletely aligned with those of theCPRGS/VDG (see Table 1.3). It is interesting thatthe targets of the CGPRS are not reflected in thedecisions of other government institutions. Thiscalls for a better coordination in increasing thecooperation among the institutions and theconsistency of the government policies.

The institution responsible for urbansanitation is the Ministry of Construction.However, there is lack of clarity over the exactdivision of responsibilities between city andcentral government. The Department of UrbanInfrastructure under the MoC collects data onurban sewerage. The data is reported annuallyby the provincial Departments ofConstruction.

C. Policies and Responsibilities -Small Towns

Small towns in Vietnam comprise a) small towns(population between 4-30,000), which representcategory 5 urban areas in Table 1.1, and b)townlets (3,000 country-wide of minimumpopulation of 2,000). The population residing insmall towns and townlets amounts to 15million19 (about 22% of total population).

4

19. Evolving management models for small towns water supply in a transition economy (Vietnam), 2002

Hanoi Water Business Company’s Nam Du WaterTreatment Plant

Small towns fall under the mandate orjurisdiction of MoC, as do water supply servicesin all larger urban areas. Townlets fall underMARD, in which CERWASS is the lead agency.No single organization is responsible for settingthe WSS policy and managing itsimplementation and coordination in both smalltowns and townlets as a distinct market segment.This segment does not completely fit either theurban or the rural context since small towns areconsidered either too small for institutionalmanagement or too big for effective communitymanagement. No target policy dealing with thedistinct issues of small towns has beendeveloped so far.

Water supply: The responsibility forproviding water differs with major dutiesbelonging to the District PCs. In some casesthough, the management has been assigned bythe PCs to the provincial WSC20. All investmentprojects of the small town PCs need to beapproved by the provincial PC. On the otherhand, the small town PC could be the watersupply project owner or the supervisor of theconstruction and O&M of the water system.

Sanitation: The Orientation for UrbanSewerage and Drainage Development to 2020includes small towns as part of the urbanpopulation whereas the National Strategy forRWSS to 2020 includes townlets as part of therural population. As part of the latter, the GoVundertakes to clarify official ownership rights,legal requirements, and operation andsupervision management rights, including therole of the consumer groups.

There is no clear responsibility for managingsewerage, drainage and sanitation in smalltowns and townlets. In principle, the small townPCs have the responsibility in managing waterand sanitation under the support of the DistrictIndustry, Construction and TransportationDivision, but there is lack of sufficient attention

and investment planning.

D. Policies and Responsibilities -Rural

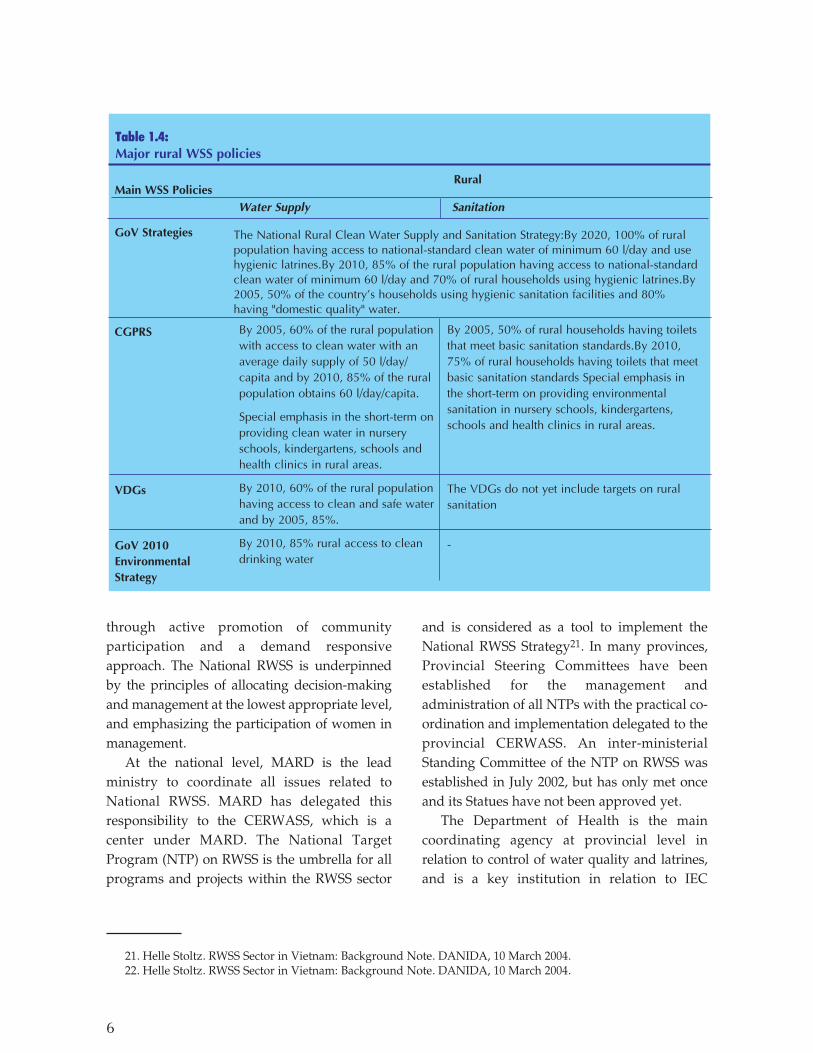

The major policies in rural water and sanitationare listed in Table 1.4.

As noted in the urban section above, waterand sanitation is clearly referenced in theCGPRS. In particular a priority is given ingovernment spending to the development ofrural infrastructure, of which WSS is a part.

Apart from the CPRGS, government policy isarticulated through the National RWSS Strategy.The underlying principle of the NRWSS strategyis sustainability rather than speed ofimplementation. IEC activities have beenrecognized as a vital element of NRWSS and giveparticular emphasis to promoting construction ofhygienic latrines and their proper use as well ason making people fully aware of the relationshipbetween sanitation facilities, water supply andhealth. The objectives call for the improvedhealth and living conditions of the ruralpopulation as well as reduced environmentalpollution from human and livestock excreta

5

20. Vietnam Urban Water Supply Development Project: Pre-feasibility study, 2004

National Rural Water Supply and Sanitation Strategybringing treated water to rural areas

through active promotion of communityparticipation and a demand responsiveapproach. The National RWSS is underpinnedby the principles of allocating decision-makingand management at the lowest appropriate level,and emphasizing the participation of women inmanagement.

At the national level, MARD is the leadministry to coordinate all issues related toNational RWSS. MARD has delegated thisresponsibility to the CERWASS, which is acenter under MARD. The National TargetProgram (NTP) on RWSS is the umbrella for allprograms and projects within the RWSS sector

and is considered as a tool to implement theNational RWSS Strategy21. In many provinces,Provincial Steering Committees have beenestablished for the management andadministration of all NTPs with the practical co-ordination and implementation delegated to theprovincial CERWASS. An inter-ministerialStanding Committee of the NTP on RWSS wasestablished in July 2002, but has only met onceand its Statues have not been approved yet.

The Department of Health is the maincoordinating agency at provincial level inrelation to control of water quality and latrines,and is a key institution in relation to IEC

6

21. Helle Stoltz. RWSS Sector in Vietnam: Background Note. DANIDA, 10 March 2004. 22. Helle Stoltz. RWSS Sector in Vietnam: Background Note. DANIDA, 10 March 2004.

Table 1.4: Major rural WSS policies

Main WSS Policies

GoV Strategies

CGPRS

VDGs

GoV 2010EnvironmentalStrategy

Rural

Water Supply Sanitation

By 2005, 60% of the rural populationwith access to clean water with anaverage daily supply of 50 l/day/capita and by 2010, 85% of the ruralpopulation obtains 60 l/day/capita.

Special emphasis in the short-term onproviding clean water in nurseryschools, kindergartens, schools andhealth clinics in rural areas.

By 2010, 60% of the rural populationhaving access to clean and safe waterand by 2005, 85%.

By 2010, 85% rural access to cleandrinking water

By 2005, 50% of rural households having toiletsthat meet basic sanitation standards.By 2010,75% of rural households having toilets that meetbasic sanitation standards Special emphasis inthe short-term on providing environmentalsanitation in nursery schools, kindergartens,schools and health clinics in rural areas.

The VDGs do not yet include targets on ruralsanitation

-

The National Rural Clean Water Supply and Sanitation Strategy:By 2020, 100% of ruralpopulation having access to national-standard clean water of minimum 60 l/day and usehygienic latrines.By 2010, 85% of the rural population having access to national-standardclean water of minimum 60 l/day and 70% of rural households using hygienic latrines.By2005, 50% of the country’s households using hygienic sanitation facilities and 80%having "domestic quality" water.

activities. The provincial Women's Union (WU),Youth Union (YU), Farmers' Association (FA)and other mass organizations play key roles inIEC activities22.

Rural households and communities areexpected to take the lead responsibility for ruralinfrastructure development to ensuresustainability. Government agencies play afacilitating role and ensure adherence to national

regulations and standards. The overall approachto be taken is underlain by the principle ofdemand responsiveness, with households andcommunities making decisions about what typeof service they want and are willing to pay forthrough a process of informed choice. As ageneral principle, users are expected to pay forall construction and operating costs of water andsanitation systems.

7

A. Water Supply

There are 4 main types of provision of watersupply services in Vietnam:

1) Utility provision by state-owned WSCs2) Small towns/townlet provision3) Self-provision - households and

communes that obtain water forthemselves

4) Local private sector in rural areas

Utility Provision

Over the past 10 years, the utility provision ofwater supply and drainage services has beendecentralized from central to provincial level ofthe government and the utilities have beenestablished as legally distinct state-ownedeconomic entities. Despite decentralization, thelevel of autonomy of the water supplycompanies remains limited. Water supply tariffsare set by the provincial PCs at levels whichcover O&M costs but are insufficient to fullyrecover the costs of capital needed by the utility.Key management and operating decisions suchas overall production levels, capital investmentand maintenance expenses, staff salary andbenefits, and senior management appointmentsstill require government approval23. WSCs donot have ownership rights over water resourcesor public land usage24. Although the province

exercises ownership on the assets of the WSC,there are no contractual relationships betweenthe two parties to govern this right. Most of thePWCs are Public Service Enterprises, operatingunder the Enterprise Law, except the watertariffs, as mentioned above, are set by therespective Provincial People's Committee.

In each province or city the relevant WSC ismainly responsible for the operation and controlof both the water treatment and distributionnetworks together with billing and collection.However, many companies carry out additionalactivities, mainly in the field of construction andequipment trading, and these can be performedin other provinces (see Figure 2.1).

There is no competition in the utility provisionof water services. However, in January 2004, theMoC was assigned the responsibility to develop aproposal on "Renovation of organizational modelsand management mechanism for WSCs" targetingWSC restructuring, water supply planning, andNRW management (reduction to 30%) as well asavoidance of monopoly abuse through issuingtechnical and economic norms for clean watersupply. The MoC proposed to allow the WSCs toprovide services outside existing service areas,make municipal authorities responsible for watersupply, and equitize the WSCs. These proposalsrequire further discussion to ensure they willmeet the needs of the sector - particularly withregard to achieving economies of scale in service

9

II. Sector Structure and Ownership

23. Ian Walker, 200224. Vietnam Water Supply Development Project. Report of Deacons and Vision & Associates. July 2002.

delivery, and having sufficient capacity on theowner side to manage such arrangements.

However, as noted earlier in this report, thesector is undergoing rapid change. The MoC isdrafting a new urban water decree which willlikely propose formal contracts between ownersand operators, as well as clarifying issues of assetownership. At the same time a number of PWCshave converted from Public Service Enterprisesto equitized companies. These includeHoChiMinh City, the largest water company inthe country, as well as smaller companies in theprovinces of Son La and Can Tho. Theseequitized companies operate under theEnterprise Law and, in theory at least, have moreflexibility than their PSE counterpart.

Private Sector and Competition: Vietnam hasnow more than 130,000 local private enterpriseswith a combined capital of US$10 billion. TheGoV plans to equitize 50% of the remaining state-owned enterprises by 200526 - although it is clearthat progress has not been as rapid as originallyanticipated. In May 2004, the MPI announced theplans for two new laws to provide a uniformlegal framework and level playing flied for all

businesses in the country, and among others, toease the foreign investors' participation ininfrastructure projects27.

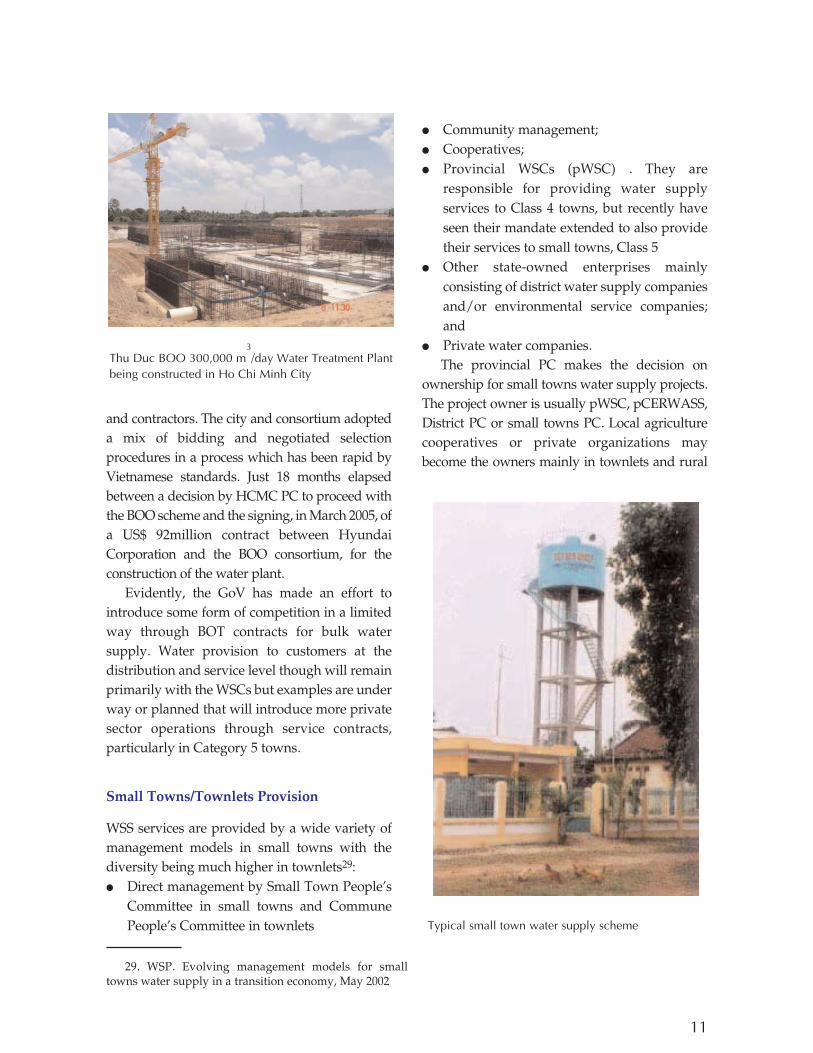

The Law on Enterprise of 1999 does notprohibit the involvement of private companies inwater supply services. However there are only afew private companies operating in the waterservice area in Vietnam28. In order to attract FDIin large infrastructure projects, the GoV issuedregulations governing BOT contracts byamending the foreign investment law in 1992.However, while foreign investments in Vietnamhave been growing rapidly, investment inwater/wastewater BOT have been slow withsome contracts cancelled (see Annex 2). The mainreason stated by the HCMC for the cancellationof two of the BOT contracts with foreigninvestors was the tariffs becoming too high as aresult of imported know-how, equipment andmaterials.

Notwithstanding, HCMC subsequentlyproceeded to procure a new water treatment plant(Thu Duc) on a BOO basis, using a localconsortium of companies as the investmentvehicle, supported by international consultants

10

25. VWSA Benchamarking Report December 2004.26. Oxford Analytica. Vietnam: Equitization raises more questions than answers. 21 June 2004.27. Dow Jones, May 200428. Vietnam Water Supply Development Project. Report of Deacons and Vision & Associates. July 2002.

and contractors. The city and consortium adopteda mix of bidding and negotiated selectionprocedures in a process which has been rapid byVietnamese standards. Just 18 months elapsedbetween a decision by HCMC PC to proceed withthe BOO scheme and the signing, in March 2005, ofa US$ 92million contract between HyundaiCorporation and the BOO consortium, for theconstruction of the water plant.

Evidently, the GoV has made an effort tointroduce some form of competition in a limitedway through BOT contracts for bulk watersupply. Water provision to customers at thedistribution and service level though will remainprimarily with the WSCs but examples are underway or planned that will introduce more privatesector operations through service contracts,particularly in Category 5 towns.

Small Towns/Townlets Provision

WSS services are provided by a wide variety ofmanagement models in small towns with thediversity being much higher in townlets29:● Direct management by Small Town People's

Committee in small towns and CommunePeople's Committee in townlets

● Community management;● Cooperatives;● Provincial WSCs (pWSC) . They are

responsible for providing water supplyservices to Class 4 towns, but recently haveseen their mandate extended to also providetheir services to small towns, Class 5

● Other state-owned enterprises mainlyconsisting of district water supply companiesand/or environmental service companies;and

● Private water companies.The provincial PC makes the decision on

ownership for small towns water supply projects.The project owner is usually pWSC, pCERWASS,District PC or small towns PC. Local agriculturecooperatives or private organizations maybecome the owners mainly in townlets and rural

11

29. WSP. Evolving management models for smalltowns water supply in a transition economy, May 2002

Thu Duc BOO 300,000 m3/day Water Treatment Plant

being constructed in Ho Chi Minh City

Typical small town water supply scheme

areas. For larger projects, project owners mustobtain a water license. Private investors haveparticipated in construction of a number oftownlet projects in areas with good economicprospects, high demand for clean water, andscarce water resources by investing sums ofbetween VND 300 million to 1 billion.

In the past pCERWASS has been the mostactive government agency in the provision ofrural water supplies. They have played the rolenot only of the owner/promoter of the ruralschemes, but also the operator. However, thismodel has not been a great success as theemphasis has been on asset creation rather thanon asset operation and maintenance. As a resultmany schemes have been built which are eithernot wanted by the community, or have falleninto disrepair due to disinterest or lack ofcapacity in pCERWASS. A new model hastherefore been adopted in the Red River DeltaRural Water Supply and Sanitation Projectapproved by the Bank in September 2005. In thisproject the pCERWASS role has been refocusedon policy and sector oversight, leaving newlyformed rural water supply companies to takethe lead in asset creation and operation. Thesenew companies are likely to be joint stockcompanies, and are expected to contract outsome or all of their operations to the localprivate sector. This new institutionalarrangement is complemented by the use ofdemand responsive approaches in systemselection and design as a means to ensurecommunity buy in to the new facilities.