watson wyatt's global powerpoint template - the caribbean

TRANSCRIPT

International Regulatory Developments

Simone Brathwaite, FSA, FCIA, CERA

Principal

Oliver Wyman

December 2, 2010

An Introduction to Solvency II

2

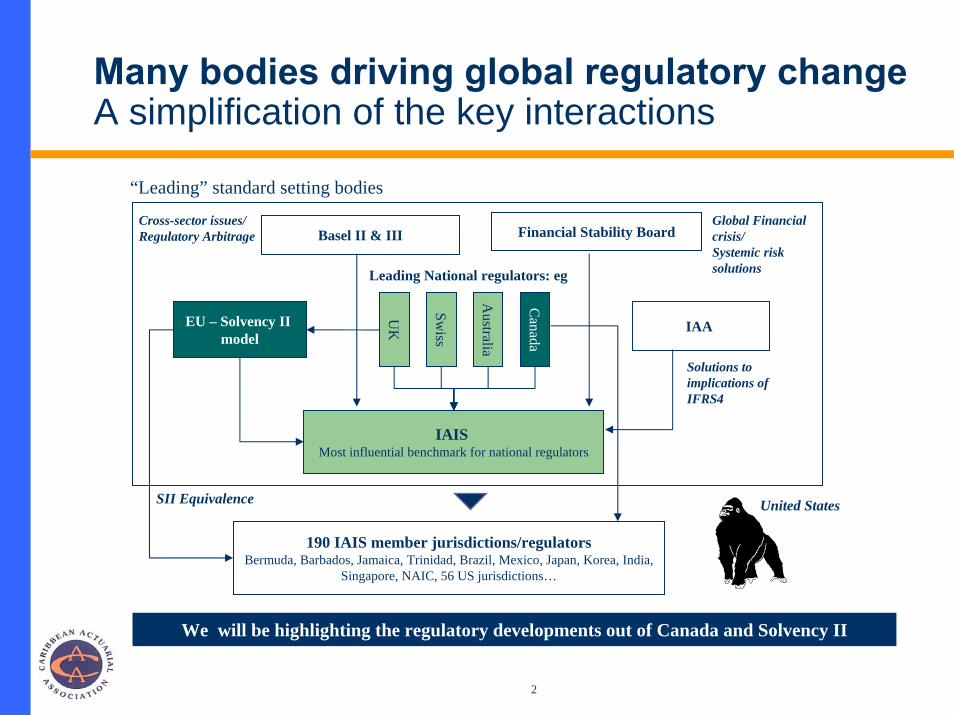

We will be highlighting the regulatory developments out of Canada and Solvency II

EU – Solvency II model

Financial Stability Board

“Leading” standard setting bodies

IAA

Global Financial crisis/Systemic risk solutions

Cross-sector issues/Regulatory Arbitrage

190 IAIS member jurisdictions/regulatorsBermuda, Barbados, Jamaica, Trinidad, Brazil, Mexico, Japan, Korea, India,

Singapore, NAIC, 56 US jurisdictions…

Leading National regulators: eg

Canada

UK

IAIS Most influential benchmark for national regulators

Australia

Swiss

Basel II & III

Solutions to implications of IFRS4

SII Equivalence United States

Many bodies driving global regulatory change A simplification of the key interactions

3

Motivation – the change was long overdue– Solvency I was inept with dealing with the inherent risks of the modern insurance industry– Some EU regulators (e.g FSA, FTK) were forced to revamp their frameworks before Solvency II Process was slow, but to be expected– The leading EU regulators were able to guide the development of SII over the last 6 years – But still needed to consider the realities of the implications on the various member countries and

their industries Proposed outcome- not perfect but still pretty advanced – “leaped-frogged’ many existing frameworksImplementation date – January 2013– All EU companies were advised to participate in QIS 5 for a final chance to help establish the final

calibration of the solvency testImpacts the global industry – Will impact IAIS’s new initiatives – Impacts countries with companies who do significant transactions with EU companies, including

- International reinsurers – in non-EU countries (third countries) – Bermuda, Barbados- EU Group companies with subsidiaries outside of EU (AXA, ING, Global reinsurers)- Non-EU Group companies with subsidiaries operating in Europe (e.g RGA)

Solvency II is unquestionably the most significant regulatory change for the insurance industry that is happening right now

4

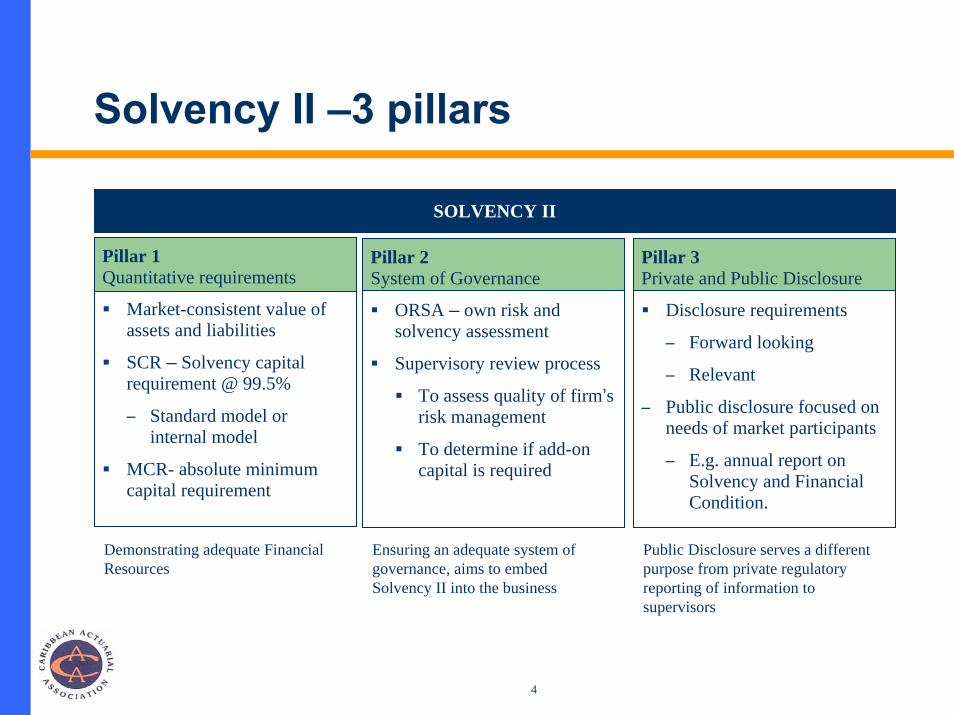

Solvency II –3 pillars

Demonstrating adequate Financial Resources

Ensuring an adequate system of governance, aims to embed Solvency II into the business

Public Disclosure serves a different purpose from private regulatory reporting of information to supervisors

Pillar 2System of Governance

ORSA – own risk and solvency assessment

Supervisory review process

To assess quality of firm’s risk management

To determine if add-on capital is required

Pillar 3Private and Public Disclosure

Disclosure requirements

– Forward looking

– Relevant

– Public disclosure focused on needs of market participants

– E.g. annual report on Solvency and Financial Condition.

Market-consistent value of assets and liabilities

SCR – Solvency capital requirement @ 99.5%

– Standard model or internal model

MCR- absolute minimum capital requirement

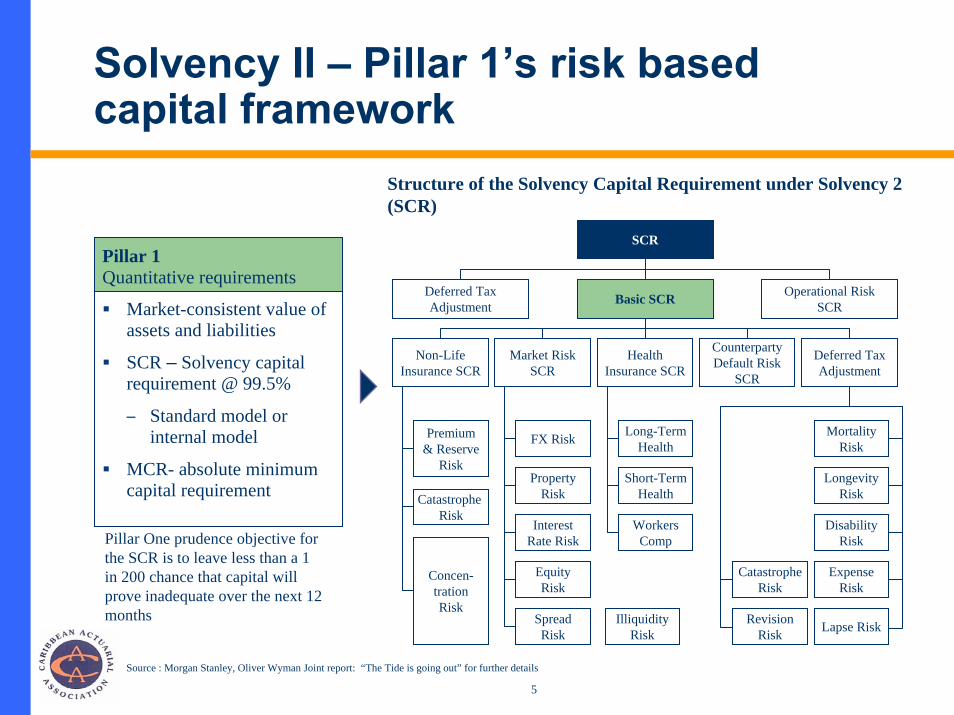

Pillar 1Quantitative requirements

SOLVENCY II

5

Non-Life Insurance SCR

Structure of the Solvency Capital Requirement under Solvency 2 (SCR)

Solvency II – Pillar 1’s risk based capital framework

Pillar One prudence objective for the SCR is to leave less than a 1 in 200 chance that capital will prove inadequate over the next 12 months

Market-consistent value of assets and liabilities

SCR – Solvency capital requirement @ 99.5%

– Standard model or internal model

MCR- absolute minimum capital requirement

Pillar 1Quantitative requirements

SCR

Deferred Tax Adjustment Basic SCR Operational Risk

SCR

Market Risk SCR

Health Insurance SCR

Counterparty Default Risk

SCR

Deferred Tax Adjustment

FX Risk

Property Risk

Interest Rate Risk

Equity Risk

Spread Risk

Illiquidity Risk

Premium & Reserve

Risk

Catastrophe Risk

Concen-trationRisk

Long-Term Health

Short-TermHealth

Workers Comp

Mortality Risk

Longevity Risk

Disability Risk

Expense Risk

Lapse Risk

CatastropheRisk

Revision Risk

Source : Morgan Stanley, Oliver Wyman Joint report: “The Tide is going out” for further details

6

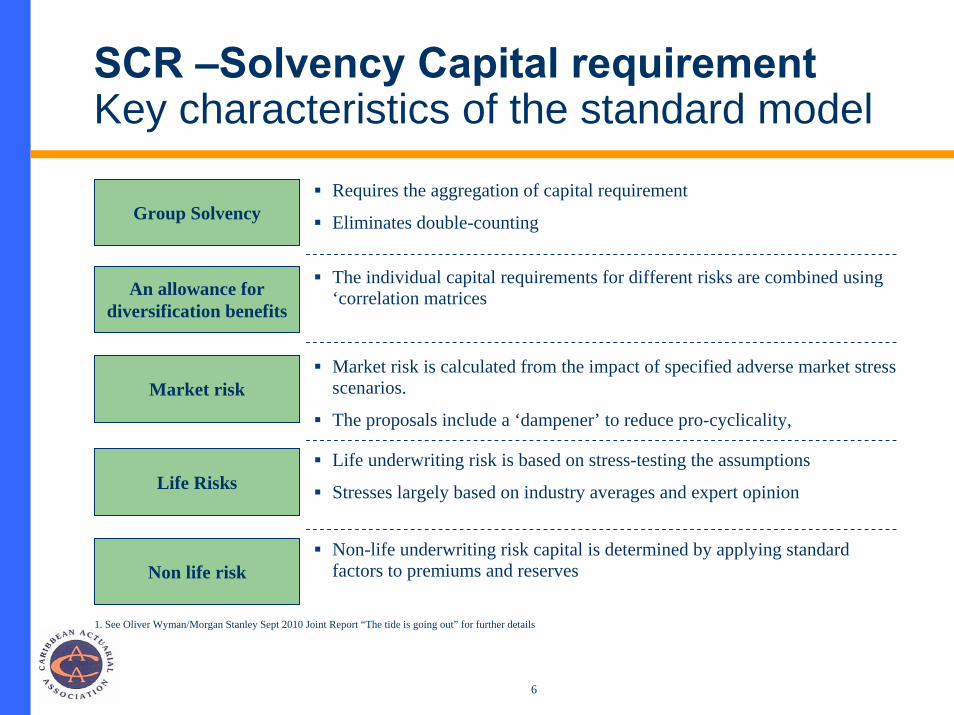

Group SolvencyRequires the aggregation of capital requirement

Eliminates double-counting

1. See Oliver Wyman/Morgan Stanley Sept 2010 Joint Report “The tide is going out” for further details

An allowance for diversification benefits

Market risk is calculated from the impact of specified adverse market stress scenarios.

The proposals include a ‘dampener’ to reduce pro-cyclicality, Market risk

Life Risks

Non life riskNon-life underwriting risk capital is determined by applying standard factors to premiums and reserves

The individual capital requirements for different risks are combined using ‘correlation matrices

Life underwriting risk is based on stress-testing the assumptions

Stresses largely based on industry averages and expert opinion

SCR –Solvency Capital requirementKey characteristics of the standard model

7

Morgan Stanley / Oliver Wyman proprietary QIS5 model estimates a decline in the solvency ratio for the listed European insurers from ~200% to 135%.

Solvency 2 will be a catalyst for a fundamental reappraisal of traditional insurance business models

The transparency brought by Solvency 2 will expose the economic volatility of balance sheets

We see reinsurers as relative winners, while small insurers including many mutuals may struggle

European insurers may become competitively challenged in markets with ‘non-Solvency 2 equivalent’ regimes

Will be a reference model for the IAIS and other jurisdictions reforming their capital frameworks to be congruent with IFRS 4

Key implications of Solvency II

International Regulatory Developments

Allan BrenderSpecial Advisor, Regulation SectorOffice of the Superintendent of Financial Institutions Canada

December 2, 2010

- A Canadian Perspective on Capital

9

Agenda

The current situation w.r.t. financial reporting and capital

Introduction of IFRS in Canada

Changing capital requirements (MCCSR)

Pillar II

Own Risk and Solvency Assessment (ORSA)

10

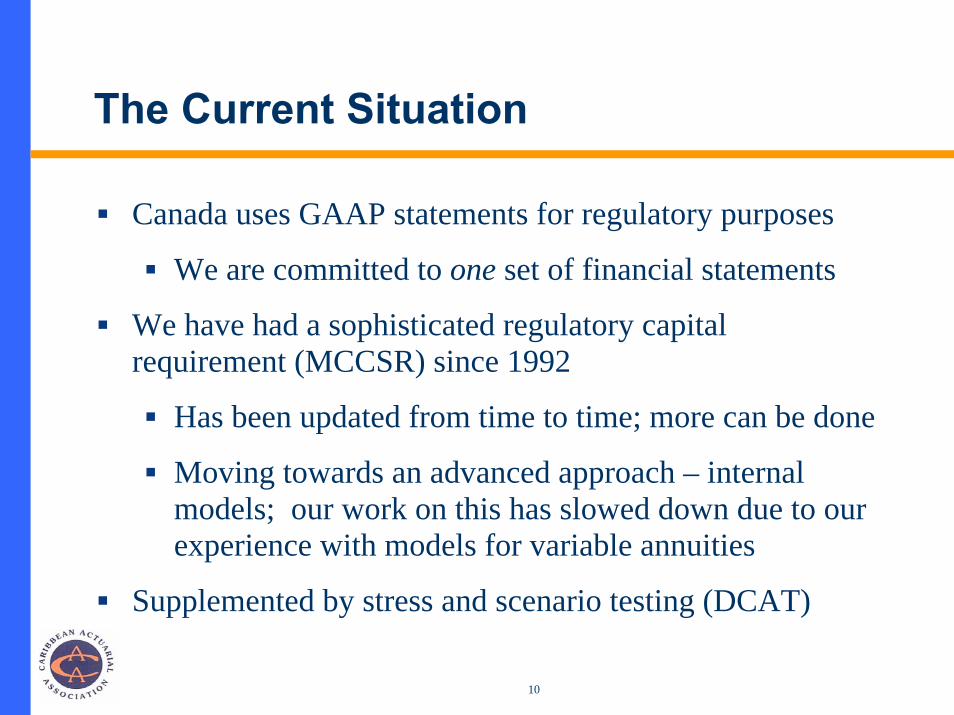

The Current Situation

Canada uses GAAP statements for regulatory purposes

We are committed to one set of financial statements

We have had a sophisticated regulatory capital requirement (MCCSR) since 1992

Has been updated from time to time; more can be done

Moving towards an advanced approach – internal models; our work on this has slowed down due to our experience with models for variable annuities

Supplemented by stress and scenario testing (DCAT)

11

Introduction of IFRS

IFRS comes into effect in Canada on 1 January 2011

All IFRSs adopted verbatim from IASB

For insurance, not many significant changes in 2011

Some small adjustments to MCCSR for 2011 because of adoption of IFRS

The major challenge and change will come with the introduction of Phase II of IFRS4 on insurance contracts

12

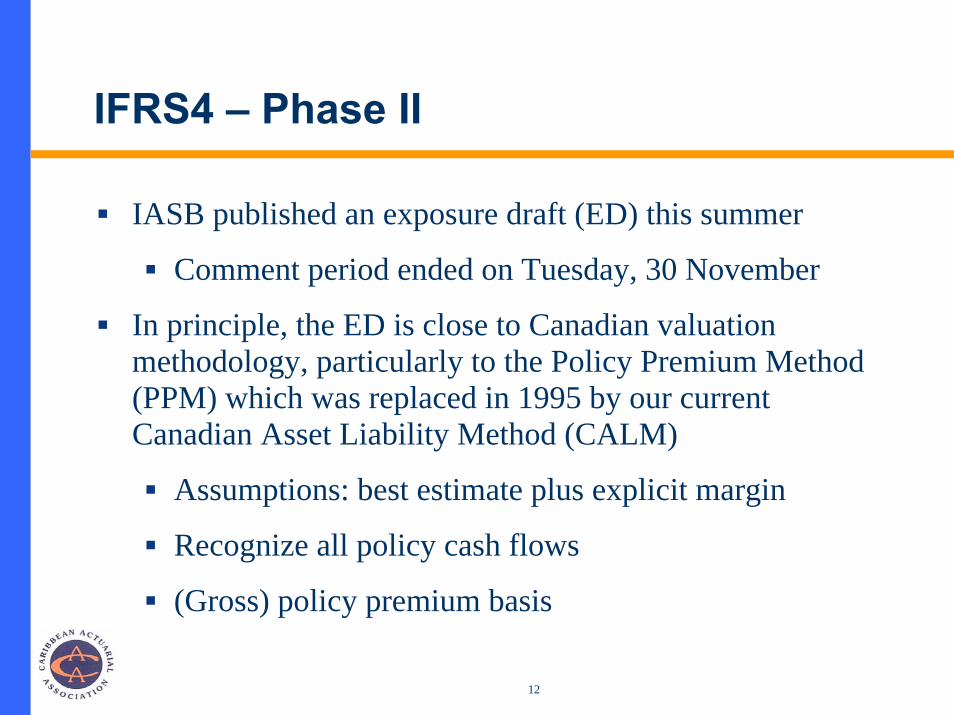

IFRS4 – Phase II

IASB published an exposure draft (ED) this summer

Comment period ended on Tuesday, 30 November

In principle, the ED is close to Canadian valuation methodology, particularly to the Policy Premium Method (PPM) which was replaced in 1995 by our current Canadian Asset Liability Method (CALM)

Assumptions: best estimate plus explicit margin

Recognize all policy cash flows

(Gross) policy premium basis

13

IFRS4 – Phase II

IASB and IFRS4 will not recognize any link between a company’s policy liabilities and the assets it uses to support those liabilities

The valuation discount rate is, for many, the main issue with the ED

Current Canadian method, CALM, recognizes

Cost of expected asset defaults

Asset / liability mismatch

Therefore, with the introduction of IFRS4 – Phase II, required capital (MCCSR) must be adjusted to make complete provision for credit and ALM risks

14

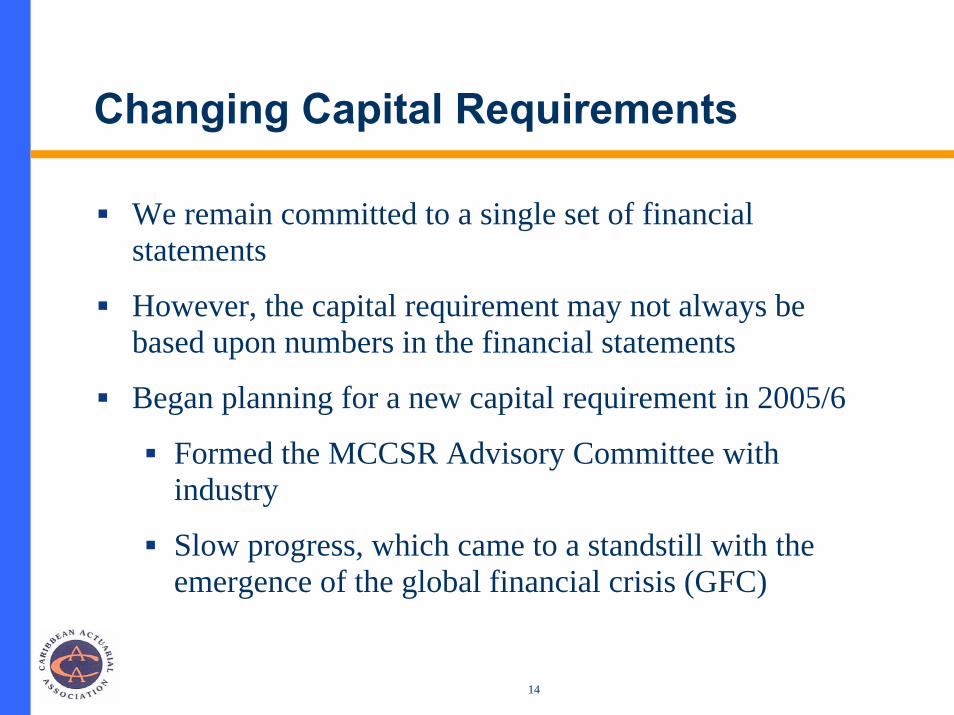

Changing Capital Requirements

We remain committed to a single set of financial statements

However, the capital requirement may not always be based upon numbers in the financial statements

Began planning for a new capital requirement in 2005/6

Formed the MCCSR Advisory Committee with industry

Slow progress, which came to a standstill with the emergence of the global financial crisis (GFC)

15

Effect of the GFC on Variable Annuities

Valuation of VAs was primarily based upon the use of internal models

Company models were required to be approved by OSFI

Since most companies did not sufficiently hedge the financial risks, when equity markets suffered a severe decline, VA liabilities experienced a huge increase, especially since we are dealing with a non-diversifiable risk

16

Effect of the GFC on Variable Annuities

This VA experience raised two significant issues:

The use of company-specific (internal) models

Calibration

Controls, use test, etc.

Recognition of (the absence of) hedging

Market consistent methodology

17

Adapting MCCSR to IFRS

Need a consistent view of liabilities and capital – i.e. the right hand side of the balance sheet

It is clear that policy liabilities under IFRS4 will not make reference to the particular assets used by an insurer to support those liabilities

Therefore, policy liabilities will take no account of credit or ALM risks

Provision for these risks must be contained wholly within required capital

Work is underway to develop these new pieces for MCCSR

18

Redesigning MCCSR

Total Asset RequirementImmunize capital structure from changes in accounting into which OSFI has virtually no inputDetermine the total assets we want an insurer to hold to support a product portfolioSubtract from this total the liabilities determined by financial reportingThe balance is required capital (SCR)Need an independent minimum capital requirement (MCR)

19

Redesigning MCCSR

20

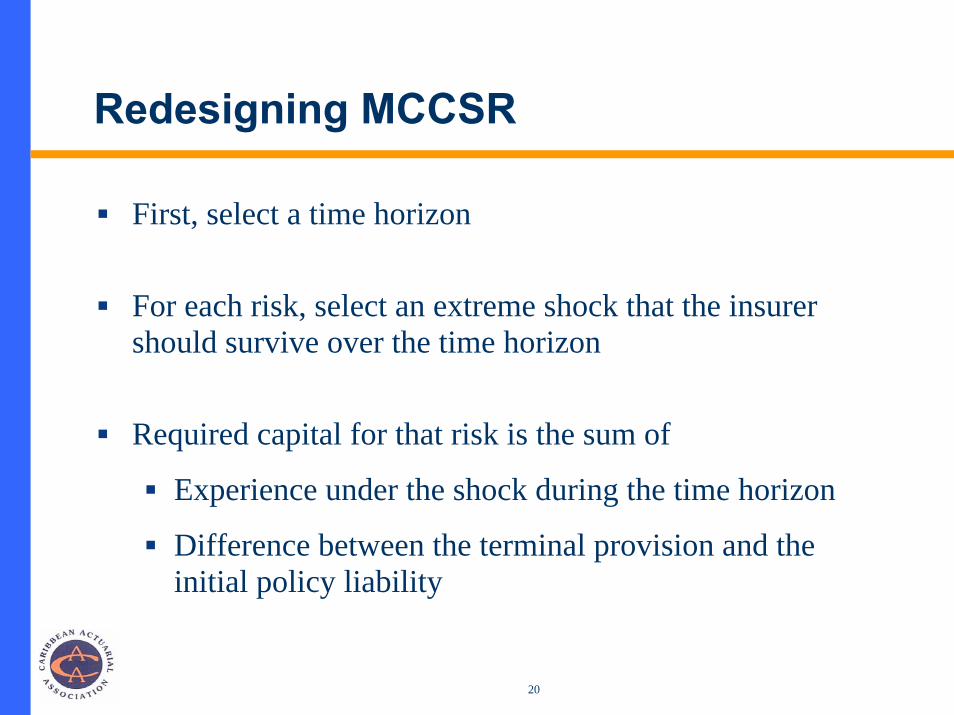

Redesigning MCCSR

First, select a time horizon

For each risk, select an extreme shock that the insurer should survive over the time horizon

Required capital for that risk is the sum of

Experience under the shock during the time horizon

Difference between the terminal provision and the initial policy liability

21

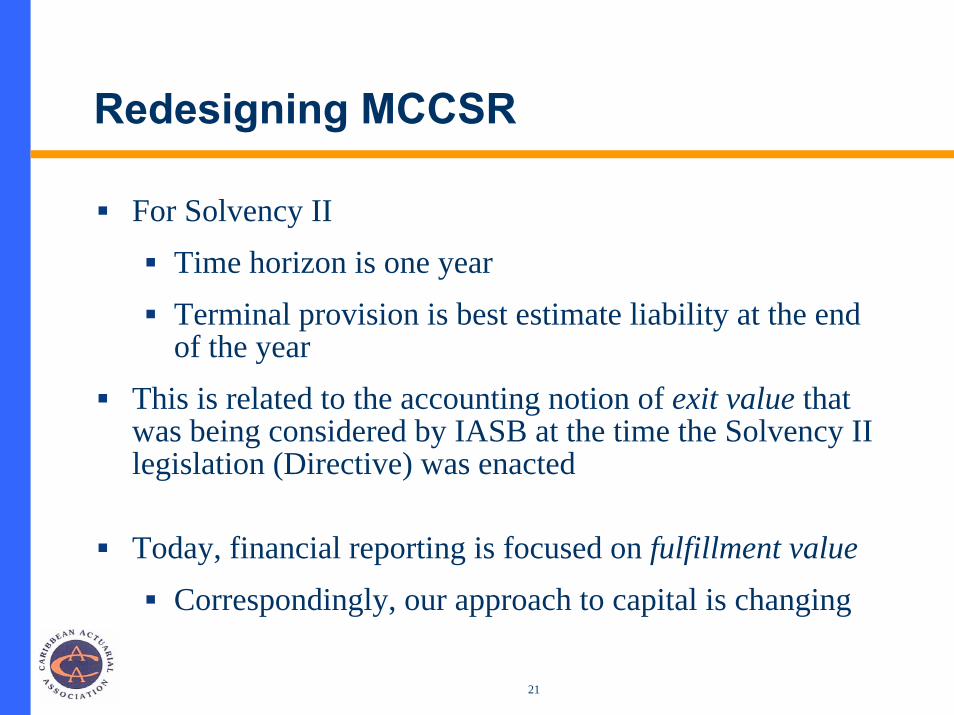

Redesigning MCCSR

For Solvency IITime horizon is one yearTerminal provision is best estimate liability at the end of the year

This is related to the accounting notion of exit value that was being considered by IASB at the time the Solvency II legislation (Directive) was enacted

Today, financial reporting is focused on fulfillment valueCorrespondingly, our approach to capital is changing

22

Redesigning MCCSR

OSFI is unlikely to introduce correlation between risks

Solvency II structure:

23

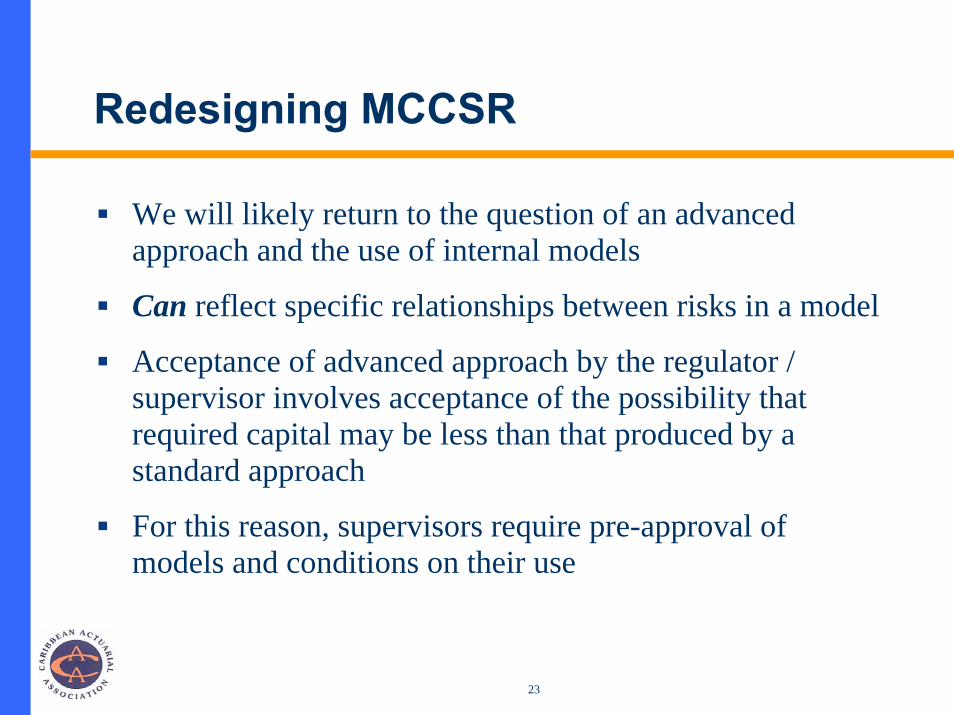

Redesigning MCCSR

We will likely return to the question of an advanced approach and the use of internal models

Can reflect specific relationships between risks in a model

Acceptance of advanced approach by the regulator / supervisor involves acceptance of the possibility that required capital may be less than that produced by a standard approach

For this reason, supervisors require pre-approval of models and conditions on their use

24

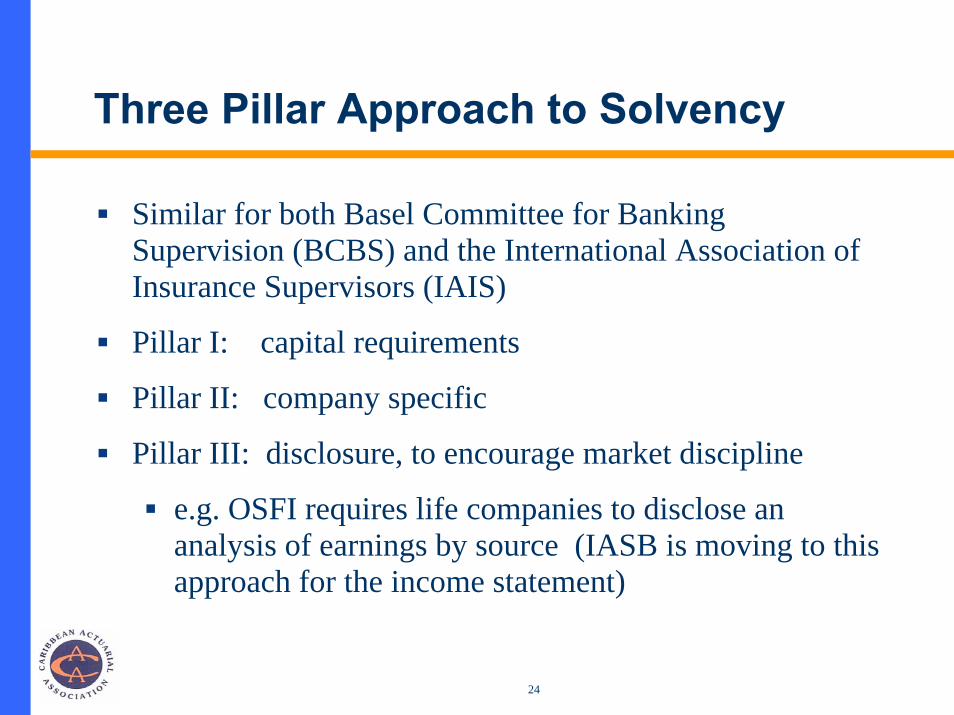

Three Pillar Approach to Solvency

Similar for both Basel Committee for Banking Supervision (BCBS) and the International Association of Insurance Supervisors (IAIS)

Pillar I: capital requirements

Pillar II: company specific

Pillar III: disclosure, to encourage market discipline

e.g. OSFI requires life companies to disclose an analysis of earnings by source (IASB is moving to this approach for the income statement)

25

Pillar II

Involves supervisory action on individual company basis

Control levels

Possible additional requirements

Involves company management action

Risk management

DCAT / stress testing is part of this

Own Risk and Solvency Assessment (ORSA)

26

ORSA

A company should analyze and know the type and degree of risks it faces

It should have a view on total capital needs

Not just those specified by the regulator /supervisor

Economic capital

Generally requires a sophisticated internal model

IFRS4 Phase II ED seems to assume all companies have such models

27

ORSA

It would be a serious error to treat ORSA as a compliance exercise

Ultimately, regulators are much more interested in companies that are safe, well run and know what they are doing than in having companies merely comply with legal requirements

28

Forthcoming IAA Publications

The IAA Solvency Subcommittee (of the Insurance Regulation Committee) is preparing two useful and practical papers designed to help actuaries (and others) in this work:

A paper on internal models

A paper on scenario and stress testing

International Regulatory Developments

Bob Diefenbacher, FSA, MAAA

SVP – Life Reinsurance

Manulife Reinsurance

December 2, 2010

Solvency II Equivalence Issues

30

Agenda

Definition of Equivalence

Equivalence and Bermuda

Equivalence and the US

Transition Countries?

31

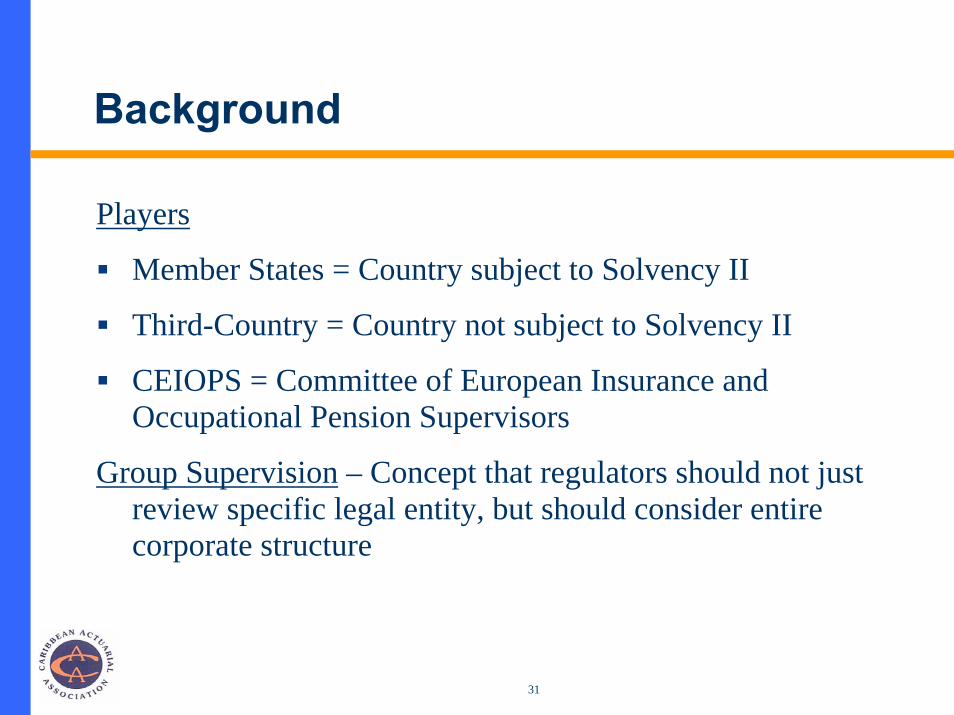

Background

Players

Member States = Country subject to Solvency II

Third-Country = Country not subject to Solvency II

CEIOPS = Committee of European Insurance and Occupational Pension Supervisors

Group Supervision – Concept that regulators should not just review specific legal entity, but should consider entire corporate structure

32

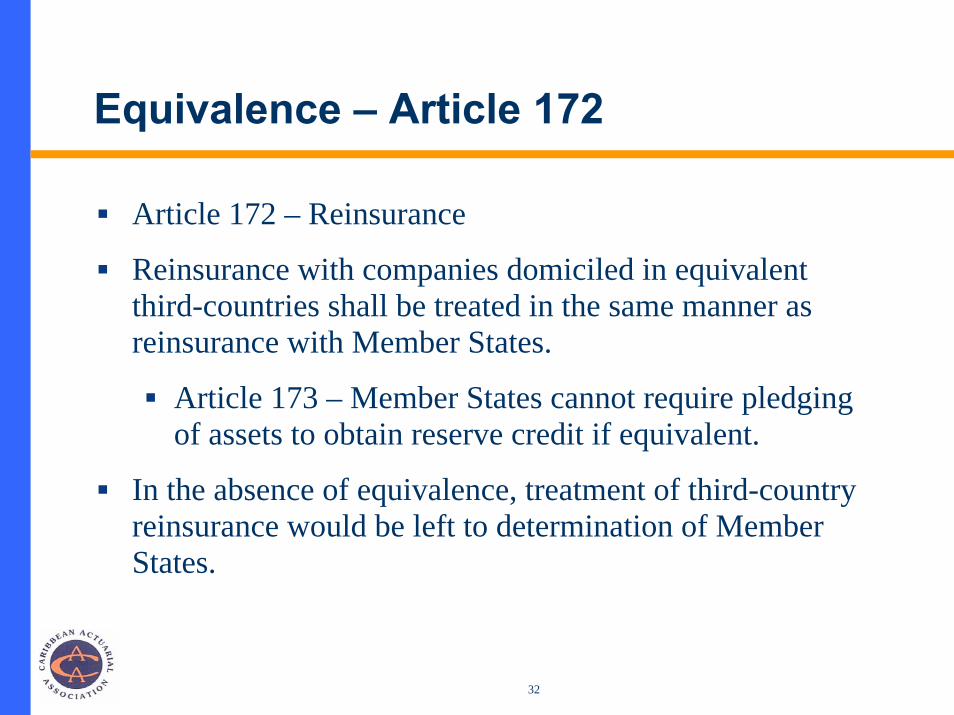

Equivalence – Article 172

Article 172 – Reinsurance

Reinsurance with companies domiciled in equivalent third-countries shall be treated in the same manner as reinsurance with Member States.

Article 173 – Member States cannot require pledging of assets to obtain reserve credit if equivalent.

In the absence of equivalence, treatment of third-country reinsurance would be left to determination of Member States.

33

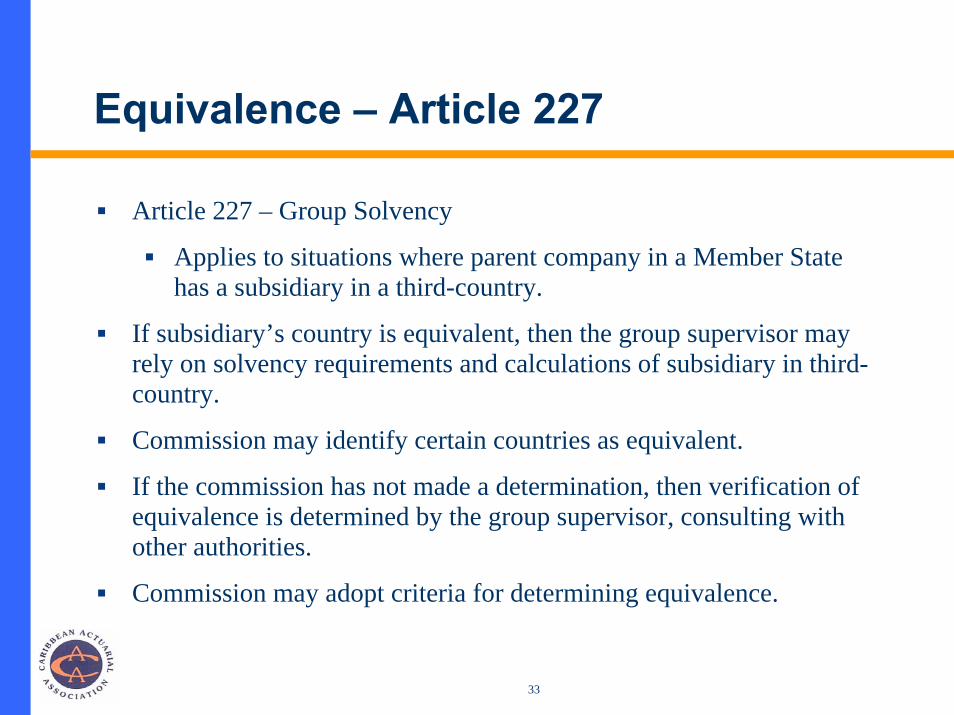

Equivalence – Article 227

Article 227 – Group Solvency

Applies to situations where parent company in a Member State has a subsidiary in a third-country.

If subsidiary’s country is equivalent, then the group supervisor may rely on solvency requirements and calculations of subsidiary in third-country.

Commission may identify certain countries as equivalent.

If the commission has not made a determination, then verification of equivalence is determined by the group supervisor, consulting with other authorities.

Commission may adopt criteria for determining equivalence.

34

Equivalence – Article 260

Article 260 – Group Supervisor

Applies to situations where a company doing business in a Member State has a parent domiciled in a third-country.

If parent’s third country is equivalent, then Member State supervisor shall rely on the group supervision of the third country.

If parent country not deemed equivalent, then Member State can make its own determination of equivalence.

Article 261 also references the need for cooperation with third-country regulators.

CEIOPS has stressed the importance of setting up cooperation agreements.

35

Pro’s and Con’s of Equivalence

Why Would A Country Want Equivalence? Insulates local companies from uncertainty associated with not having equivalence

Fair treatment for reinsurance assumed from EU. Protects local reinsurers business model. Avoids potential need for local companies to have to provide information to EU regulator in addition to local regulator.

Why Would A Country Not Want Equivalence? May require significant additional investment in resources to achieve equivalence.May require significant changes in existing solvency regime.

Local regulator may not agree with every principle of Solvency II.May impact market segments completely unrelated to Solvency II

36

Current Status of Equivalence Deliberations

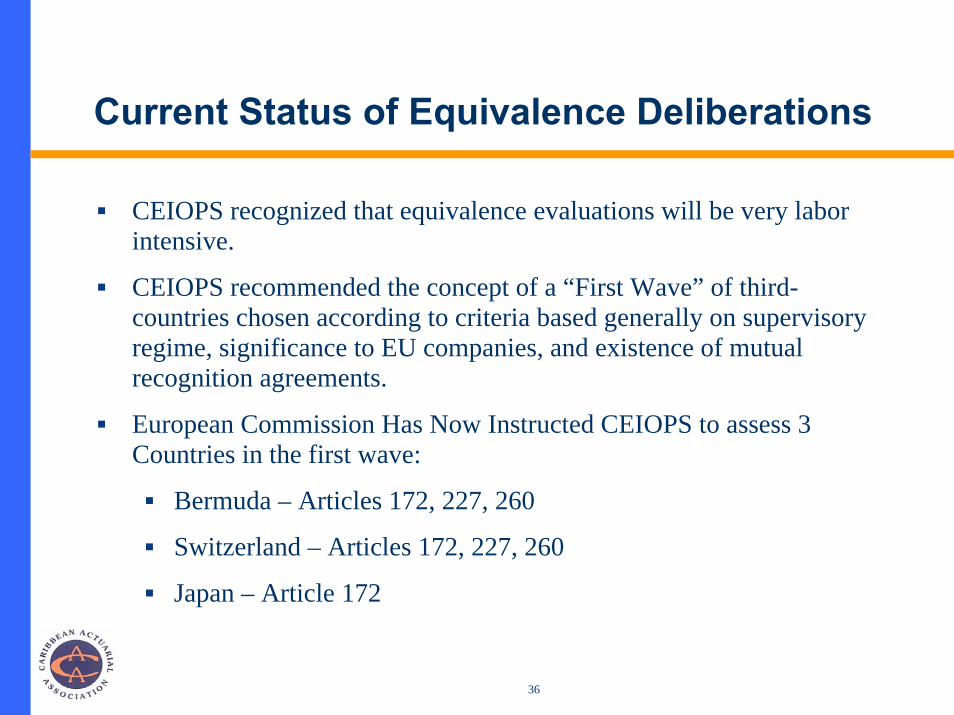

CEIOPS recognized that equivalence evaluations will be very labor intensive.

CEIOPS recommended the concept of a “First Wave” of third-countries chosen according to criteria based generally on supervisory regime, significance to EU companies, and existence of mutual recognition agreements.

European Commission Has Now Instructed CEIOPS to assess 3 Countries in the first wave:

Bermuda – Articles 172, 227, 260

Switzerland – Articles 172, 227, 260

Japan – Article 172

37

Bermuda

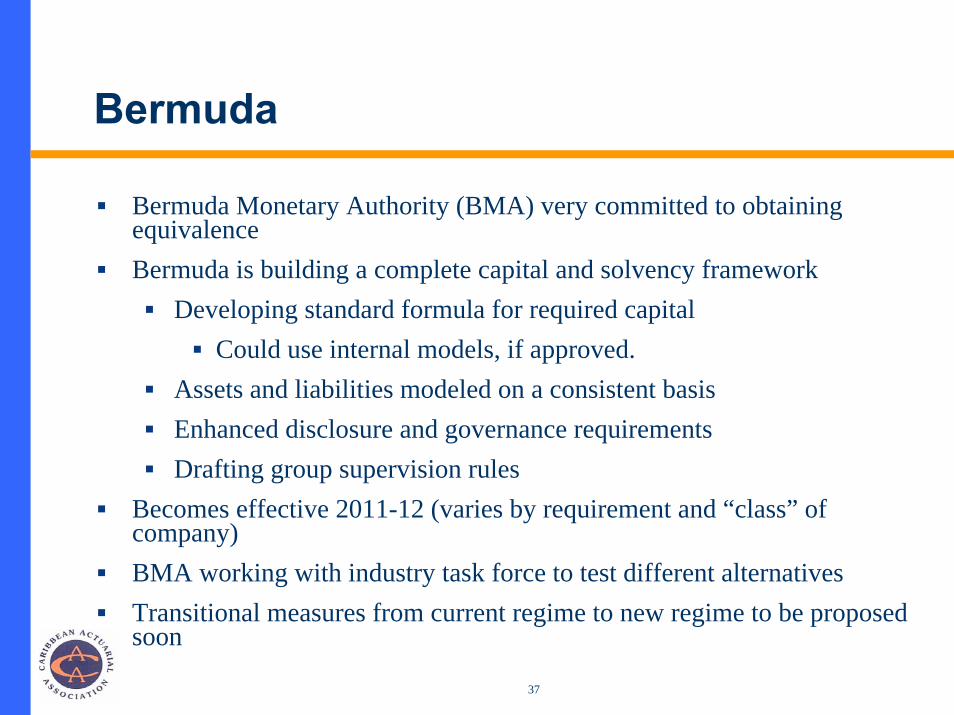

Bermuda Monetary Authority (BMA) very committed to obtaining equivalenceBermuda is building a complete capital and solvency framework

Developing standard formula for required capitalCould use internal models, if approved.

Assets and liabilities modeled on a consistent basisEnhanced disclosure and governance requirementsDrafting group supervision rules

Becomes effective 2011-12 (varies by requirement and “class” of company)BMA working with industry task force to test different alternativesTransitional measures from current regime to new regime to be proposed soon

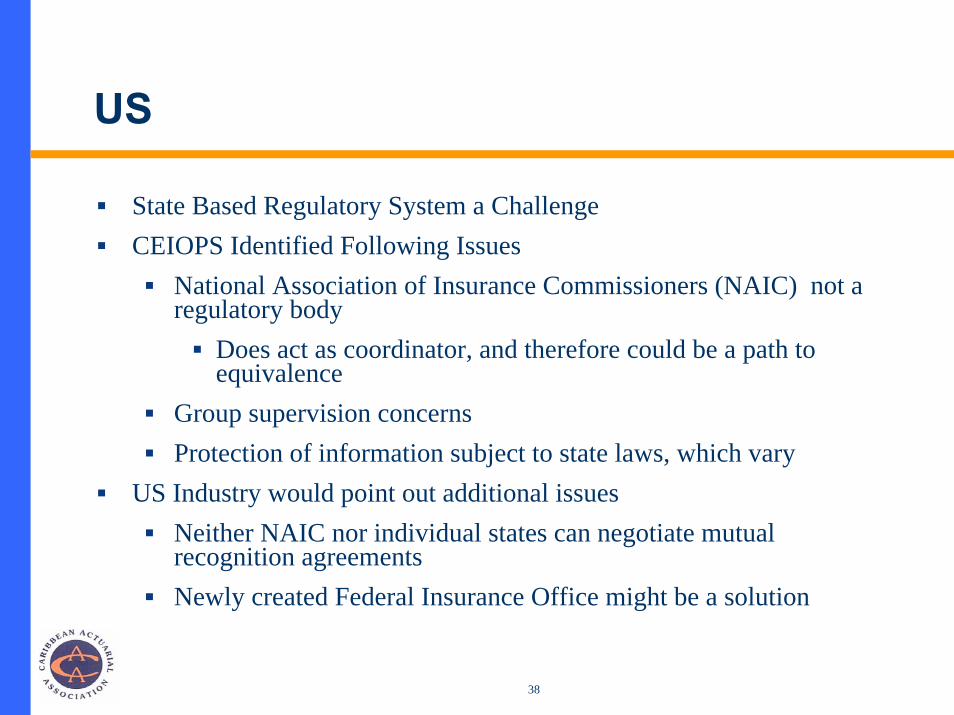

38

US

State Based Regulatory System a ChallengeCEIOPS Identified Following Issues

National Association of Insurance Commissioners (NAIC) not a regulatory body

Does act as coordinator, and therefore could be a path to equivalence

Group supervision concernsProtection of information subject to state laws, which vary

US Industry would point out additional issuesNeither NAIC nor individual states can negotiate mutual recognition agreementsNewly created Federal Insurance Office might be a solution

39

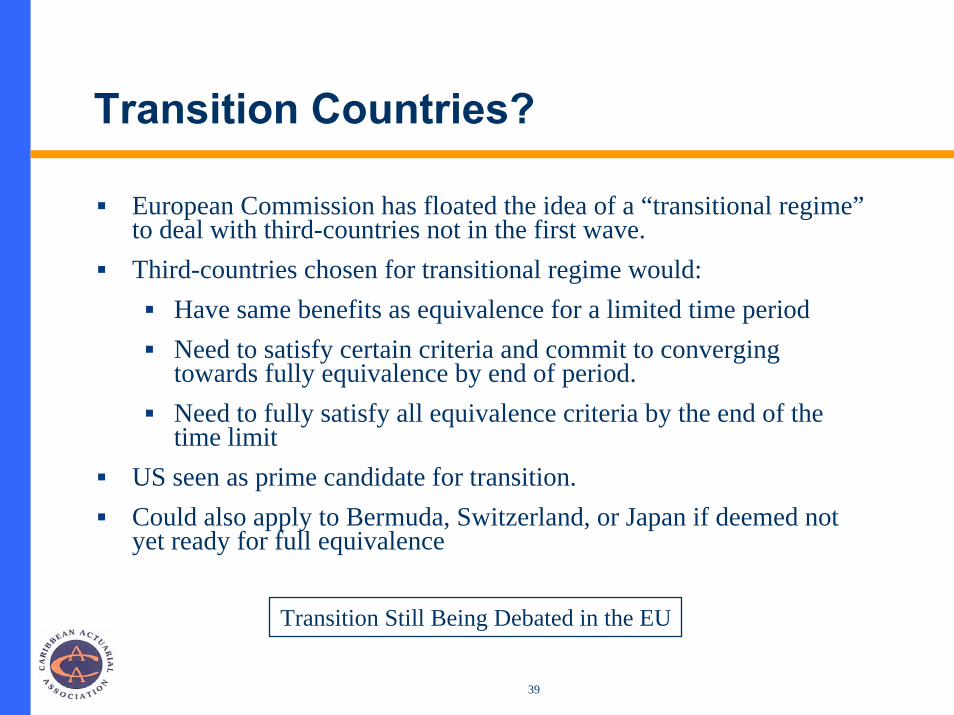

Transition Countries?

European Commission has floated the idea of a “transitional regime”to deal with third-countries not in the first wave.Third-countries chosen for transitional regime would:

Have same benefits as equivalence for a limited time periodNeed to satisfy certain criteria and commit to converging towards fully equivalence by end of period.Need to fully satisfy all equivalence criteria by the end of thetime limit

US seen as prime candidate for transition. Could also apply to Bermuda, Switzerland, or Japan if deemed notyet ready for full equivalence

Transition Still Being Debated in the EU