ways & means committee 2016 budget...

TRANSCRIPT

Onondaga County Legislature

DEBORAH L. MATURO J. RYAN McMAHON, II KATHERINE FRENCH Clerk Chairman Deputy Clerk

401 Montgomery Street Court House Room 407 Syracuse, New York 13202 Phone: 315.435.2070 Fax: 315.435.8434

www.ongov.net

WAYS & MEANS COMMITTEE – 2016 BUDGET REVIEW OF

WAYS & MEANS COMMITTEE DEPARTMENTS September 16, 2015

MEMBERS PRESENT: Mr. Jordan, Mr. Kilmartin, Mrs. Ervin, Ms. Williams, Mr. May, Mr. Holmquist ALSO PRESENT: Chairman McMahon, Mr. Liedka, Mrs. Rapp, Dr. Chase, Mr. Ryan

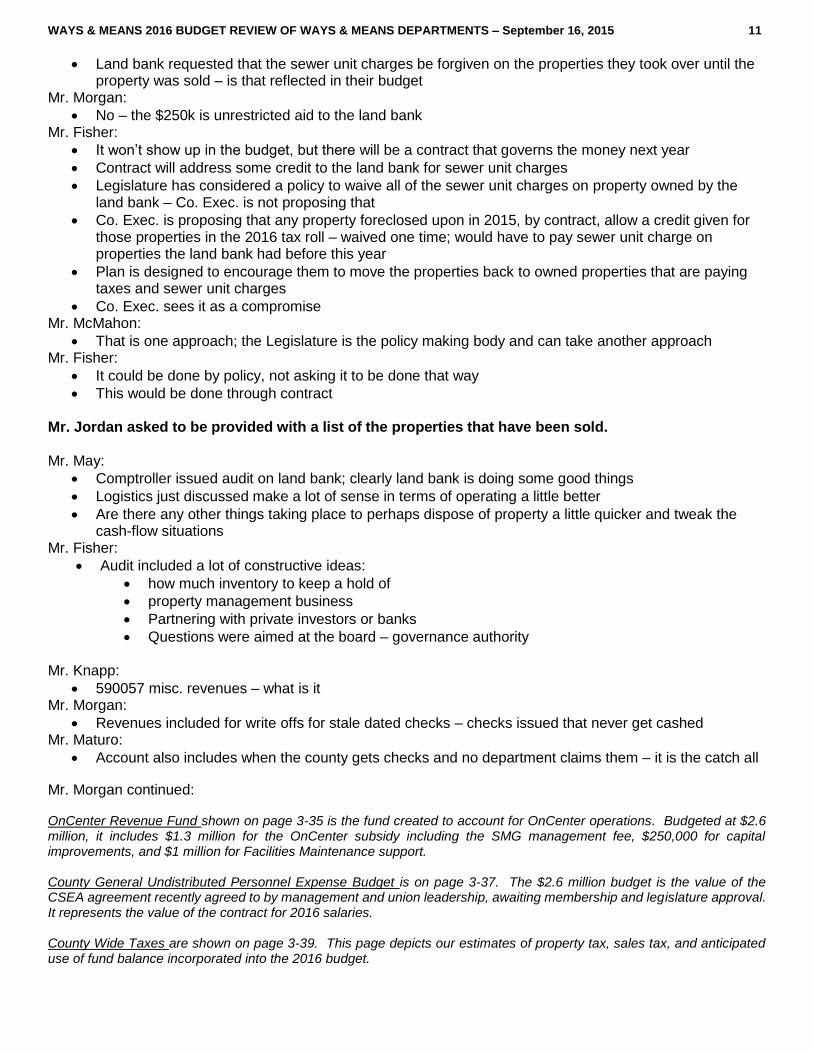

Chairman Knapp called the meeting to order at 1:12 p.m. CONVENTION CENTER – PG 3 -35 – Kelly Carr, General Manager Oncenter Mr. Carr presented the following:

Financial Statement Recap FY 2014 3

FY 2014 Highlights 4

Financial Statement Forecast FY 2015 5

FY 2016 Proposed Budget Commentary 6

FY 2016 Proposed Budget Subsidy 7

Facility Fees Update 8

Capital Reserve Update 9

Table of Contents 2

Financial Statement Recap FY 2014

Revenue $8,749,434

Expenses $10,054,439

Subsidy $1,500,000

Net Income $194,995

3

FY 2014 Highlights

Significant Events – FY 14

• Motley Crue in concert• Avenged Sevenfold in concert• Coming Back Together Conference• Trinity Motivation Convention• Five Finger Death Punch in concert

Noteworthy Achievements – FY 14

• Booked six (6) new conventions in 2014 highlighted by a 3-year agreement with the American Quilters Society for 2015-17.

• Total new estimated Room Nights booked in 2014-9,556; with an estimated economic impact of $9,815,400

• SMG provided over $32,000 in funding to Arts groups in 2014.• Assembly Hall upgrade: New carpeting, paint and Veterans mural wall

were installed prior to the start of the Crunch Season.• SMG renewed or sold $98,500 in sponsorships/advertising in 2014.

4

Financial Statement Forecast FY 2015Actual YTD Forecast 2015 Over/(Under) Last Year 31-Aug Sept To Dec 15 FYE 2015 Budget Variance Actual

Attendance 295,443 120,431 415,874 369,182 46,692 421,053

# of Events 334 115 449 300 149 594

Event Net Income

Rental Income 813,984 478,661 1,292,645 1,257,737 34,908 1,149,241

Service Revenue 956,301 503,580 1,459,881 1,603,466 (143,585) 1,394,080

Service Expense (1,476,893) (715,488) (2,192,381) (2,063,209) (129,172) (2,211,853)

Total Direct Event Net Income 293,392 266,754 560,146 797,994 (237,848) 331,468

Ancillary Income

Concession 468,827 268,684 737,511 612,402 125,109 570,947

Catering 1,030,164 541,322 1,571,486 1,407,054 164,432 1,653,850

Novelty 17,779 280 18,059 35,312 (17,253) 46,133

Event Parking 210,817 62,259 273,076 304,440 (31,364) 280,915

Total Ancillary Net Income 1,727,587 872,544 2,600,132 2,359,208 240,924 2,551,845

-

Other Event Income

Other Event Related Income 48,601 44,381 92,982 198,550 (105,568) 80,562

Ticket Rebates 157,048 - 157,048 157,048 158,687

Facility Fees -

Total Other Event Income 205,649 44,381 250,030 198,550 51,480 239,249

-

Total Event Net Income 2,226,628 1,183,679 3,410,307 3,355,752 54,555 3,122,561

Other Income 844,432 292,000 1,136,432 1,112,000 24,432 1,182,466

-

Adjusted Gross Income 3,071,060 1,475,679 4,546,739 4,467,752 78,987 4,305,028

-

Indirect Expense

Net Salaries, Benefits & Taxes 2,011,068 1,122,345 3,133,413 3,101,474 31,939 3,077,769

Contracted Services 68,046 31,647 99,692 94,940 4,752 92,252

General & Administrative 186,413 110,519 296,932 370,798 (73,866) 350,882

Operational 175,186 175,844 351,030 319,121 31,909 289,088

Repairs and Maintenance 4,145 2,667 6,812 8,000 (1,188) 10,664

Operational Supplies 11,330 3,200 14,530 9,600 4,930 18,600

Insurance 120,559 62,271 182,830 208,416 (25,586) 196,324

Utilities 447,909 232,079 679,987 789,394 (109,407) 720,006

Other 392,162 381,036 773,198 798,371 (25,173) 757,278

Total Other Direct Expenses 3,416,817 2,121,607 5,538,425 5,700,114 (161,689) 5,512,862

0 - -

Net Income Before Other Income & Expenses (345,757) (645,928) (991,685) (1,232,362) 240,677 (1,207,834)

Other Income/(Expenses)

Depreciation (50,647) (25,323) (75,970) (67,638) 8,332 (97,170)

ROTS 525,518 774,484 1,300,002 1,300,000 (2) 1,500,000

Total Other Income/(Expenses) 474,871 749,161 1,224,032 1,232,362 8,330 1,402,829

Net Income 129,114 103,233 232,347 0 232,347 194,995

5

FY 2016 Proposed Budget Commentary

The budget for FY 2016 has been created in accordance with current definitive sales and historical trends from 2013-2015.

Sales For 2016 budgeted sales are approximately $428,000 higher than 2015:

• Increased Convention activity• Increased Family Shows• Increased other income

ExpensesOperating income is budgeted at 50.7% in 2016 vs. 50.3% in 2015.

Indirect ExpensesWe are budgeting 2016 indirect expenses $331,000 higher than 2015. This is due primarily to increases in payroll/benefits, adding two positions, and increase in sales, events and type of events.

6

FY 2016 Proposed Budget Subsidy

FY 2015 Request

Subsidy $1,300,000

Capital Reserve $250,000

FY 2016 Request

Subsidy $1,300,000

Capital Reserve $250,000

7

Facility Fee Report FY13-16

2013 2014 2015 2016Begin Balance 106,541 105,312 130,515 99,961

Sources 178,835 178,711 180,042 180,000

Uses

Convention Center

Catering Equipment 43,623

Drapes 15,040

IT Equipment 20,152 10,478 2,496 10,000

Smallwares, Glassware & Bars 40,367

Projector Equipment 5,691

Operation Equipment 5,703 70,000

Lobby Upgrade 18,911

POS System/Bev. Inventory System 152,929

Reserve Upgrade 12,500

ADP GL Import 22,000

Parking Garage Office 8,500

F&B Equipment 80,000

Theaters

Carrier Theater Seating Project 52,132 6,640

Cable Ramps 6,371

War Memorial

Vets Museum 6,380

Replay System 11,000

Olympia Repairs 15,000

TV Monitors 7,784

Wireless Mic 8,953

Press Box Cleanup 17,891

Owners Box 31,082

Assembly Hall Upgrade 16,746

WAM Project 5,800

Surge Area's Improvements 30,000

Total Uses 180,064 153,509 210,596 190,000

Ending Balance 105,312 130,515 99,961 89,961

8

Capital Reserve Report FY13-16

2013 2014 2015 2016

Begin Balance 102,096 308,287 209,393 -

Sources 250,135 500,151 250,000

Uses

Catering Equipment 1,513

Micro Terminals 10,635

IT Equipment 7,839

Parking Garage Camera/EBS Project 4,420 227,557

Meeting Room Renovation 19,538 89,075 20,181

Way Finding Signs 9,819

Ballroom Lighting Project 394,432

Restroom Hand Dryer Project 50,000

Laundry Facility 17,375

Gallagher Hall & Atrium Project 125,000

Marquee's 125,000

Total Uses 43,945 98,894 709,544 250,000

Ending Balance 308,287 209,393 - -

9

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 4

Mr. Carr noted that they project to finish 2015 with $237,347 ahead of budget. Mr. Jordan:

Asked about two new positions being added, Mr. Carr:

One is on the operational side to assist with set up and the other is a sales position. Chairman McMahon:

Thanked Mr. Carr for the work he and his team has done

Subsidy two years ago was higher than it is now, which frees up revenue in the budget

Asked about potential with the Expo Center at the Fair – what does it do for the community to drive more convention business, assuming they will work with the county in a coordinated fashion

Mr. Carr:

More venues to sell for the destination is always a good thing

Will look to expand the Alliance to include the Fair with the Expo Center

Alliance has been a successful entity – able to do some good things so far Chairman McMahon:

Louisville, KY, has a fairgrounds where there is a convention business and has a downtown convention center – seems to work well there

Mr. Kilmartin:

Thanked Mr. Carr for the work that has been done

Asked how the renovation of the Hotel Syracuse will impact Oncenter’s work/business Mr. Carr:

With the hotel coming on line, it will change the model of business that they have

Will be looking to go more after convention business and conferences

Know that a lot of social business will leave the Oncenter and go to the hotel; have looked at it and budgeted for it

Idea of being able to generate more conventions with the downtown hotel, which hasn’t been in this market for at least 10 years, will be such a benefit across the board

Will allow to compete for business that once was here and left, and for new business that has never been here before

Mr. Jordan:

Projecting net profit of $232,347- asked what happened with net revenue Mr. Carr:

It goes into Oncenter revenue fund; not used for operational purposes Mr. Morgan:

It ultimately reduces the Oncenter subsidy Mr. Maturo:

If it is decided to reduce the subsidy, that fund balance can be used for the operation of the convention center

Mr. Jordan said that right now it accumulates until we decide what to do with it; Mr. Morgan agreed. Chairman Knapp

Questioned $58,380 increase in interdepartmental changes Mr. Morgan

It is charges from Facilities Management to the Oncenter Revenue Fund = $1 million is district heating and cooling; $50k is general overhead from Facilities that support the Oncenter

Basic cost increases from year to year

Oncenter revenue fund supports all charges related to operating the Oncenter, included charges from Facilities

It goes against all the revenues and expenses that occur during the year to run the Oncenter as well as the subsidy

Facility use fee does not come into this

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 5

Chairman Knapp asked to be provided with a list of programs supported with the SMG fund; Mr. Carr will provide it. Chairman Knapp:

692150 Furniture, Furnishing & Equip - has been all over the place from 2014 to 2016; now shows negative ($221,816)

Mr. Morgan:

$221k is capital expenses from prior year,

When Oncenter Corp was dissolved, there was equity left – the expenses are drawing down that equity Mrs. Ervin:

Veterans groups are wondering why they can’t have use of a bigger facility for Veterans Day instead of the small room that they have every year

Mr. Carr:

It wasn’t asked for, but they absolutely can. Mrs. Ervin said that she is asking. Mr. Morgan said that he misspoke about the $221k. The $250k allocated to Oncenter every year in capital, the county was the purchasing agent for them for almost all of it in 2015 to purchase items. It was decided that the items could be purchased by the county at a lower rate. They were expended directly out of the Oncenter revenue fund. Mr. Carr said that it was the parking garage project. Chairman Knapp said that SMG did a great job at the amphitheater for the concert. CENTERSTATE CEO/CVB, pg. 3-35/pg 3-33 - Rob Simpson, President, CenterState CEO; David Holder, President CVB Mr. Simpson, CenterState CEO:

Over 12 months there has been tremendous progress on economic development and destination marketing fronts

Tremendous amount of enthusiasm with new amphitheater, investments at State Fair, and reality that the Hotel Syracuse is coming back on line

Investments speak to a higher level of integrations between our region’s destination marketing efforts between county, private sector, and business community, and economic development efforts as a whole, than what has been seen in a really long time

David Holder and his team desire a tremendous amount of credit for what has taken place; value partnership with CVB

Upstate Revitalization Initiative - 5 days left before finishing the proposals to submit to Governor

Communty has a significant opportunity - $500,000,000 investment in CNY

Proposal has been worked on since November of last year – volume of work for entire team

Mr. Holder and Oncenter team have been critical partners in crafting the proposal

Develop a strategy for investment that creates jobs immediately and long-term sustainable employment, regions best to position Syracuse and CNY as a place where business can thrive, people can prosper and individuals can visit

Thanked the legislature for their support

Mr. Holder distributed the following:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 6

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 7

Mr. Holder, CVB

Most productive year that he recalls for Visit Syracuse Team

2015 hosted immense number of familiarization tours, site visits, ranging from travel journalists, media, meeting planners, financial analysts – best way to get familiar with what destination has to offer

Huge amount of marketing done in Canada via state grant – seen 600% increase in website visitation from Canada

Hosted enormous events – NCAA, American Quilting Society, Half Iron Man, religious groups, Training/motivation skills, and World Indoor Lacrosse Championships

Launched new brand – Syracuse Do Your Thing – consumers telling them they wanted – their input help create the brand

Implemented a Tourist Assistance Portal in collaboration with Syracuse University- S.U. paid for 11 multi-media units throughout downtown and university hill

About to launch new website – completely overhauled, most dynamic travel website that this area has ever seen

Jumped heavily into food, beer, spirits, wine – connected with Julie Taboulie, chef to underwriter her efforts

Packaging done around state fair to boost Canadian visitation to the fair

Convention sales team partnering with a new information resource, Meetings Database Institute, to grow level of prospecting

Syracuse Refreshed –mouthwash sponsored by Syracuse at meeting planner shows

Destination between NYC and Niagara Falls – pushing heavily in UK, Canada and China

Probably NYS’s leading participant by national tourism office, Brand USA

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 8

Plotting for dramatic Change

Proposed budget is $75,000 inrease in room tax spending/investment- 4% increase

Marriott Downtown Syracuse – putting huge amount of investment in convention sales, promotions and marketing, and convention services

Looking at new trade shows, booking incentive, will be doing a lot of site visits in connection with Oncenter

2016 hosting largest travel/trade show in NYS – destinations group travel show

New promotions – rolling out a lot of video around new destination product; as more product comes on board - amphitheater and equestrian facilities – will be integrated

Sports – new rowing/racing product; county parks is a great partner – CVB is a sales instrument

Developing new strategic plan, implemented in 2016 - a lot of consumer research done this year

Community pride – saw a lot when new brand was rolled out – had traction, created a new sense/vitality – want to use it to amp up what local residents feel for the area they live in

Doing programming in 2016 with how to create better ambassadors out of our own local residents

People to help sell the area for more tourism

Proactive/aggressive role in utilizing the asset of winter

Roll out a program next fall – entire banner over winter and say that no better place on earth is better suited for owning winter – will draw national and international attention for the area

Targeting 2016 for last 5 years that the subsidy is started to reduce or end with CenterState

Are the only destination/marketing organization that has a subsidy from a parent organization

Proposing to reduce that subsidy by 50% - better in line with how other destination marketing organizations operate around the country

Important piece going forward – not sustainable – need to look at model that is out there

Chairman Knapp asked about the $75,000. Mr. Holder:

It’s not just about the Hotel; Hotel gives a brand new chance to re-message the area.

Syracuse Refreshed notion has been out for awhile – can now show another dimension

It’s about marketing Syracuse in its entirety and a convention destination – Hotel, other hotels, convention center, State Fairgrounds – all products together – what do you do when not in a meeting room elements

Looking to boosting up investment in those programs – sales, promotions, site visits, services to take care of groups when they come here

Mr. Fisher:

Have heard from CVB and Oncenter management that we should prepare for a significant shift after the Hotel comes on

Currently Oncenter has a lot of weddings, local events, that don’t bring in sales tax or visitors – will have opportunity to go after business that will shift the business model

Start putting more of the CVB ‘s budget into the long lead sales – room block agreement with Marriott allows them to be aggressive in responding to RFPs

2016 will be selling business for 2019 – first year after the bowlers.

2016 - focus more of the budget on that type of marketing that is needed for 2019 to be successful Chairman Knapp:

RFPs are out for operator and promoter for amphitheater – asked what CVB’s role will be Mr. Holder:

Can utilize venue, concerts, as another resource when bringing in convention planners, tour planners, media – a great way to get them introduced to the community

Can use a concert as the hook to bring them in or showcase everything else going on – a welcome mat to draw people in

Canada is an enormous market place – an audience to draw from; amphitheater is another asset to draw visitors from Canada

Can package and push the marketplace into Canada – have tools in place through grants at least through next year

Mr. Simpson said that he doesn’t want investments like the amphitheater to be lost in how important they are to the broader economic development agenda. In going through the Upstate Revitalization Initiative process, one of the things that has become clear is the reorientation that is going on in this community. A “lake to the hills”

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 9

strategy; thinking about the new orientation of our community – from Carrier Dome looking down the hill as energy flows from it to downtown, inner harbor, and forward faction of the lake. An obstacle that they have always had is convincing those they are trying to recruit to the area that this is a vibrant, energetic, modern community. It was impossible to sit on the lawn for the concert and not feel that you were in someplace special. It becomes a marketing asset to not only tell tourism, but can be used to sell people on this community. We are now in a position to market the lake as an asset for the first time. Mr. Jordan:

Referred to the Market New York Investment, went up $5,000 -- what is it Mr. Holder:

State grant – competitive through Regional Economic Development Counsel

$370,000 for this year; $375,000 allocated for 2016 to go into Canada an push Syracuse Do Your Thing COUNTY GENERAL/ROT – pg. 3-33; 3-39 – Steven Morgan, CFO Mr. Morgan presented the following:

For the Countywide funds I will go in the same order as the budget. The County General Other Items budget is shown on page 3-33. This budget includes funding for the CVB, Erie Canal Museum, OHA, the County’s memberships and dues, and our contribution to the Village Infrastructure fund.

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 10

The Contractual Expenses account includes $6,475,000 for the following:

Village Infrastructure Fund - $4.5 million

Convention and Visitors Bureau - $1,910,000 whose budget was previously reviewed

Syracuse Nationals - $25,000 The OHA is funded at $165,452. The Erie Canal Museum is funded at $62,616. The all other expenses line, budgeted at $81,916, is for countywide memberships and dues for NYSAC, NYS County Executive’s Association, audit fees for the County’s deferred savings plans and other County wide expenses. The transfer to grants line of $250,000 includes continued support for the Land Bank at half of the amount adopted in the 2015 budget. The first revenue line, Non Real Property Tax Items, is the ROT required to fund CVB, OHA, and the Erie Canal Museum. The County Services revenue line is monies collected from 401B plan vendors to cover the cost of plan audits.

Miscellaneous revenues include write-offs for stale dated checks.

Chairman Knapp asked about the Land Bank funds being cut in half. Mr. Fisher:

When Co. Exec. first asked the legislature to support the land bank, she made it clear that it would be startup money and would not be a permanent subsidy – would be proposing less as it went forward, as they became more self-sufficient

2015 budget includes $500k; $300k is unrestricted, $200k put into zombie properties

Supports zombie properties idea, but this is not intended for that

Seen significant benefits from land bank – City can now more aggressively collect delinquent property tax, foreclose on property and bring it back on tax rolls

More than a dozen properties are back on tax rolls – would like to see that as to where the land bank looks for revenue

State statute – allows city/county to share property tax for first 5 years – a more, sustainable, long-term way to fund this

Comptroller’s audit had many suggestions about moving from a subsidy to something more sustaining – consider the ideas – it is time for legislature to consider moving in that direction

Chairman Knapp:

Contractual expenses – non government - $40k delta – asked for detail Mr. Morgan:

$40k for space rental at the Nano film hub

Relocate film commissioner to that location – amount of space to occupied will be negotiated Mr. Jordan:

Land bank - properties purchased so far, are they exclusively in City of Syr, any in outlying towns Chairman McMahon:

Majority of properties through tax delinquency are easier to get from city

In the past year they have gotten properties from our auction in Dewitt, Jordan, Elbridge, Geddes, Baldwinsville; have reached out to other towns – there were properties in Clay, but they chose not to participate

Some of the monies are earmarked for villages, specifically Jordan, Elbridge, Baldwinsville – had properties that were bundled and could fix up a whole block easily

The majority of properties to date are in City of Syracuse Mr. Jordan asked to be provided with a list of all the properties that the land bank has purchased. Mrs. Rapp:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 11

Land bank requested that the sewer unit charges be forgiven on the properties they took over until the property was sold – is that reflected in their budget

Mr. Morgan:

No – the $250k is unrestricted aid to the land bank Mr. Fisher:

It won’t show up in the budget, but there will be a contract that governs the money next year

Contract will address some credit to the land bank for sewer unit charges

Legislature has considered a policy to waive all of the sewer unit charges on property owned by the land bank – Co. Exec. is not proposing that

Co. Exec. is proposing that any property foreclosed upon in 2015, by contract, allow a credit given for those properties in the 2016 tax roll – waived one time; would have to pay sewer unit charge on properties the land bank had before this year

Plan is designed to encourage them to move the properties back to owned properties that are paying taxes and sewer unit charges

Co. Exec. sees it as a compromise Mr. McMahon:

That is one approach; the Legislature is the policy making body and can take another approach Mr. Fisher:

It could be done by policy, not asking it to be done that way

This would be done through contract Mr. Jordan asked to be provided with a list of the properties that have been sold. Mr. May:

Comptroller issued audit on land bank; clearly land bank is doing some good things

Logistics just discussed make a lot of sense in terms of operating a little better

Are there any other things taking place to perhaps dispose of property a little quicker and tweak the cash-flow situations

Mr. Fisher:

Audit included a lot of constructive ideas:

how much inventory to keep a hold of

property management business

Partnering with private investors or banks

Questions were aimed at the board – governance authority Mr. Knapp:

590057 misc. revenues – what is it Mr. Morgan:

Revenues included for write offs for stale dated checks – checks issued that never get cashed Mr. Maturo:

Account also includes when the county gets checks and no department claims them – it is the catch all

Mr. Morgan continued: OnCenter Revenue Fund shown on page 3-35 is the fund created to account for OnCenter operations. Budgeted at $2.6 million, it includes $1.3 million for the OnCenter subsidy including the SMG management fee, $250,000 for capital improvements, and $1 million for Facilities Maintenance support. County General Undistributed Personnel Expense Budget is on page 3-37. The $2.6 million budget is the value of the CSEA agreement recently agreed to by management and union leadership, awaiting membership and legislature approval. It represents the value of the contract for 2016 salaries. County Wide Taxes are shown on page 3-39. This page depicts our estimates of property tax, sales tax, and anticipated use of fund balance incorporated into the 2016 budget.

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 12

The first line item includes our proposed property tax levy, adjusted by estimates of unpaid current year taxes and payments of delinquent taxes. Our estimates for deferred and uncollectable taxes as well as prior year tax collections are based on historical data. We anticipate approximately $12 million of deferred and uncollectable taxes and $10 million of prior year tax collections in the 2015 budget. The property tax levy is $140 million, exactly the same as the 2015 levy. The second line labeled “Non real Property Tax Items” is our $262 million estimate of sales tax revenue. We estimate 2015 sales tax collections will finish 2.0% higher than 2014 actual collections and assumes growth of 1.5% above our estimate for 2015. The last line is the $4 million required in fund balance to balance the 2016 budget. Also we are using $1 million of the $5 million in committed fund balance to support Do’s budget. Interfund Transfers are on page 3-41. These are simply the transfer of general fund dollars into OCC, the Road Fund, Library and so forth. It is the local dollar portion of those budgets. You will review these items when you review the budgets for those departments. The debt service portion is the amount needed to cover debt for OCC and Oncenter complex. The services other gov’t – education revenue is college chargeback revenue used to offset OCC debt and is being budgeted at $600,000. The interdepartmental revenue line is the offset to indirect costs which is prepared by the Comptroller’s office. Debt Service costs are on page 3-43 and reflect countywide debt service including WEP, Water and the General Fund. The 2016 budget includes gross debt service payments of $62.3 million, essentially flat compared to 2015. Transfers from the General fund into the debt service fund were mitigated by using $6.9 million of RBD, allocating $600,000 from our college chargeback collections to partially offset OCC debt, and recognizing $2.8 million in surcharge revenue from our land line and wireless surcharge to help mitigate the debt service cost associated with the radio project.

In answer to Chairman McMahon, Mr. Morgan said that this is all the debt related to all of the funds/ it is $62.3 million. A breakdown of the different funds can be provided. It is rolled up into the types of debt that will be paid next year; will see it as an expense in each department. Mrs. Venditti referred to the following page:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 13

Mrs. Rapp:

Will be paying out $13 million less in debt this year Mr. Morgan:

Yes, but debt was refunded this year - $12 million was a result of that – debt refinanced at a lower interest rate

Funds are an expense to pay to an escrow agent that pays the bonds that were refunded – there is an offsetting revenues – other sources

Chairman Knapp asked about doing that again this year. Mr. Morgan:

It was done earlier this year; will work with advisors and continue to monitor the market and look at the feasibility of doing another one next year

The market has soured a bit Chairman McMahon:

How many debt issuances are there where interest rates are higher than they are right now Mr. Morgan:

A lot depends on if they are callable

Don’t want to start refunded far out in advance where potentially there is a negative arbitrage

Have contract with an advisor – they evaluate all outstanding debt, work with underwriters for potential opportunities on an annual basis

Chairman Knapp:

Reserve for bonded debt using $6.9 million; does it include the $1 million for DOT Mr. Morgan:

It does not – the $1 million is fund balance

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 14

$6.9 million is reserve for bonded debt received from either premiums when debt is issued, interest on holdings, and if they over borrow for projects and don’t spend all of those funds – which goes into a reserve and allowed for use to offset debt service cost

Roughly in line with what was used last year

Mrs. Rapp:

How close are we to our debt bonding limit; what percentage Mrs. Venditti:

15.8% Chairman Knapp

590082 other sources –the money used to refinance this year and asked about 2014 - $34 million Mr. Morgan:

It is - $12.9 million payment to agent to pay off the bonds that were refunded

Hold it and make payments as we go forward; $13.04 million represents the proceeds

2014 was an unusual year with EFC – there were EFC loans going from short term to long term

Typically don’t budget anything in this line item – all based on whether a refinancing is done or if projects that are short term go to long term

Mr. Morgan continued: Countywide Allocations on page 3-45 depicts a number of budgetary items. The “All Other Expenses” line is the estimated $2.5 million cost of college chargebacks for County residents attending a community college outside Onondaga County. As you know the amount we pay to each county is based on how much the county subsidizes its community college. We basically hold that county harmless from the local cost of one of our residents attending their college. The next expense is the expected cost of tax certiorari settlements budgeted at $200,000. This is the estimated payment back to residents who successfully challenge their assessment and are due a refund of improperly assessed County tax.

Mr. Morgan said that it was more in 2014; budgeted $200k for year not knowing potentially what it would be. A big part of that was Shoppingtown. The final expense item is the $88 million sales tax revenue we share with the City and schools. In the revenue section, the $10.3 million in “Other Real Property Tax Items” consists of two items:

PILOTS of $2.8 Million

$7.5 million of interest and penalties on delinquent taxes. The Interest and Earnings account is our investment income. Our investable balances earn an estimated .26% return in the 2016 budget.

Chairman Knapp said that the investments have to be kept conservative; Mr. Morgan said that all investments have to be approved by New York State. They have had people come in and look at how the funds are invested, and they really haven’t uncovered any new things or advantageous vehicles than what is being done now. Lori Pietruniak, Fiscal Analyst, does a really good job of analyzing balances, when bills need to be paid. They are looking at cash flow on a daily, monthly, quarterly, and annual basis so that when the interest rates start to pop back up, they have information to invest in vehicles the can earn a higher rate, and know when they need cash to pay bills. Chairman McMahon:

Sales tax to other government has gone down; is it the school districts coming off Mr. Morgan:

It is; it’s the last shift – schools going down: .71% of the 3%; .62% of the 1%

There are some small shifts toward the end of it – this is the last major decrease to schools Mr. Fisher:

It doesn’t go to zero for schools – school districts are in the 10 year agreement all the way through it

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 15

Mr. Morgan:

The current sales tax agreement goes through year 2020. Chairman McMahon:

Understands that there is a cross threshold where it can be renegotiated Mr. Fisher:

Law Department can research it Chairman Knapp:

What does 590003 – other real property tax items consist of Mr. Morgan:

PILOT payments ($2.8M) and interest and penalties on delinquent taxes ($7.5M)

Mr. Jordan:

Understands that collections on property taxes has gone down, but the amount of uncollected property taxes has gone up

Mr. Morgan:

Projecting an increase in deferred and uncollectible taxes and in prior year collection

Net last year was -$2.8M; next year projected to be -$2M

Look at trend data and actuals from current years, do the best estimation. It is booked at end of the year; try to estimate what it will be.

County General Undistributed Personnel Expenses, pg. 3-37 Mr. Morgan:

Total $2,567,062 – general fund portions

2016 value of CSEA contract not approved

Fund also put into WEP and MWB for it

Mrs. Ervin asked how much money has been spent on outside law firms to negotiate the contract. Mr. Morgan will provide it. Mrs. Ervin asked what CPI was used – how was the offer determined. Mr. Morgan said the Mr. Troiano is the chief negotiator and feels more comfortable with him answering. Chairman McMahon said that there was a mediator and it was their proposal. Mr. Morgan said there was a mediator the second time around and the proposal was what management and union leadership agreed to. Mr. Jordan referred to the 2015 adopted, $2,029,140 vs. 2015 modified $2,576,062, and asked what happens to the extra $96,000. Mr. Morgan said that the budget was modified to take funds out to fund the Human Rights Commission. If there is no agreement this year, the balance will drop to the bottom line – fund balance. If there is no agreement this year, there is potential retro that will have to be dealt with next year. FINANCE - PAGE 3-91 – Steven Morgan, CFO; Tara Venditti, Deputy Director; Dan Hammer, Budget Analyst; Don

Weber, Real Property Tax Director Mr. Morgan: Finance Administration This unit has a number of distinct responsibilities. It collects delinquent taxes and other revenues owed to the County, and then manages those funds until they are needed to pay bills. As a part of our tax collection responsibilities, we also run an installment program for the repayment of back taxes and, as the last step in the enforcement process, we auction tax delinquent property. The legislature approved $600,000 earlier this year to support a new delinquent tax collection software application. The software will provide for the standardization and modernization of property tax collection software across all taxing

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 16

jurisdictions along with the modernization of current delinquent tax collection software utilized by Onondaga County Finance Dept. for tax collection and enforcement. The implementer is in place and had started work with an estimated go live date by the end of next year.

Mr. Morgan said that he will continue to come over and give updates on it, as it will ultimately impact towns and villages in terms of coming on the same platform as the county in collected taxes Chairman Knapp asked if it will be offered to the towns to hop onto it. Mr. Weber said that the hope is to offer it to them for free, and save money on the software vendors they are currently using. In answer to Mr. Knapp, Mr. Fisher said that the current system is on the mainframe; the new system will not be. Chairman Knapp asked what the towns use now. Mr. Weber said that it is a little bit of everything:

They have either their own vendor, some have in-house things that they have done, some still use paper

The hope is that they will all be on the same system as the county.

They would go on line and long it, a Citrix type application.

County would see instantaneously when someone made a payment; how much is outstanding at towns; how much we would have to make them whole for

Wouldn’t be a week-long lag that we have now Chairman Knapp:

Would it be just for tax collectors in towns Mr. Weber:

Towns, schools, villages collect current year taxes and then it comes to the county to collect delinquent taxes

The delinquent portion is the part on the mainframe at the county – hoping to tie the two together and have one big tax collection system that everyone would use

Chairman Knapp:

Asked about the assessors Mr. Weber:

They have their own NYS database; housed at the County and they s access via Citrix Mr. Morgan continued: Finance also administers the real property tax system in Onondaga County, maintaining tax maps on behalf of the City and all of the towns, preparing assessment rolls, and tax bills, and providing expert advice and guidance to area assessors. Finance is also charged with issuing and managing debt authorized by the Legislature and managing the County’s cash and investments. With our stable finances we’ve maintained our strong credit rating—one of the best ratings of any unit in government in the United States. Division of Management and Budget As you know, the Budget Office is involved in the preparation, monitoring, and enforcement of the County’s $1.26 billion budget. Earlier this year we restructured the division to dedicate resources to launch and implement the County’s performance management initiative, OnWard. Performance measures will help us better define the benefit created by the services being provided by the County in a tangible way by quantifying outcomes. Rather than merely identifying a program’s cost to the County, we will analyze the value the programs create and how they align with the County’s overall strategic goals and priorities. This approach will provide us with the necessary information to evaluate the cost and

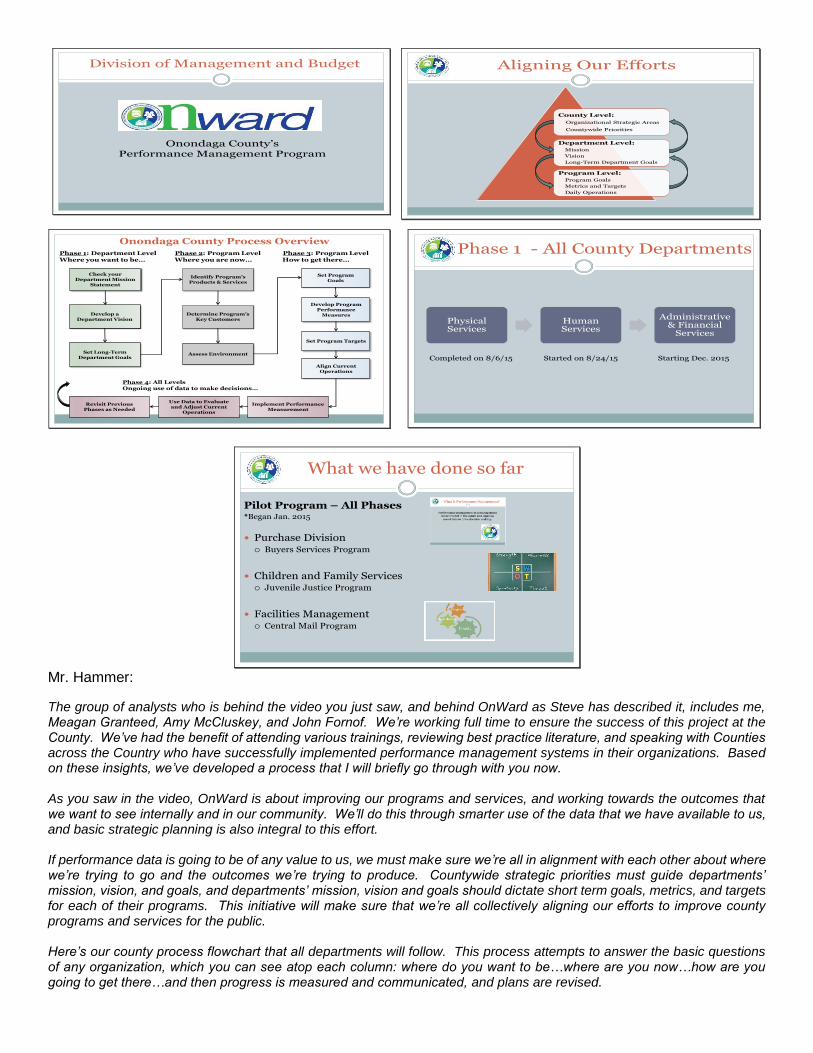

effectiveness of each program to improve them and guide investment decisions. I’d like the performance management team member to take you through a brief presentation of the initiative. Mr. Hammer presented the following PowerPoint:

Onondaga County’s Performance Management Program

Division of Management and Budget

Aligning Our Efforts

County Level:

Organizational Strategic Areas

Countywide Priorities

Department Level:

Mission

Vision

Long-Term Department Goals

Program Level:

Program Goals

Metrics and Targets

Daily Operations

Identify Program’s Products & Services

Determine Program’s Key Customers

Check your Department Mission

Statement

Develop a Department Vision

Set Long-Term Department Goals

Assess Environment

Set Program Goals

Develop Program Performance

Measures

Set Program Targets

Align Current Operations

Implement Performance Measurement

Phase 2: Program LevelWhere you are now…

Phase 1: Department LevelWhere you want to be…

Phase 3: Program LevelHow to get there…

Onondaga County Process Overview

Phase 4: All LevelsOngoing use of data to make decisions…

Use Data to Evaluate and Adjust Current

Operations

Revisit Previous Phases as Needed

Phase 1 - All County Departments

Physical Services

Human Services

Administrative & Financial

Services

Completed on 8/6/15 Started on 8/24/15 Starting Dec. 2015

What we have done so far

Pilot Program – All Phases*Began Jan. 2015

Purchase Division Buyers Services Program

Children and Family Services Juvenile Justice Program

Facilities Management Central Mail Program

Mr. Hammer:

The group of analysts who is behind the video you just saw, and behind OnWard as Steve has described it, includes me, Meagan Granteed, Amy McCluskey, and John Fornof. We’re working full time to ensure the success of this project at the County. We’ve had the benefit of attending various trainings, reviewing best practice literature, and speaking with Counties across the Country who have successfully implemented performance management systems in their organizations. Based on these insights, we’ve developed a process that I will briefly go through with you now. As you saw in the video, OnWard is about improving our programs and services, and working towards the outcomes that we want to see internally and in our community. We’ll do this through smarter use of the data that we have available to us, and basic strategic planning is also integral to this effort. If performance data is going to be of any value to us, we must make sure we’re all in alignment with each other about where we’re trying to go and the outcomes we’re trying to produce. Countywide strategic priorities must guide departments’ mission, vision, and goals, and departments’ mission, vision and goals should dictate short term goals, metrics, and targets for each of their programs. This initiative will make sure that we’re all collectively aligning our efforts to improve county programs and services for the public. Here’s our county process flowchart that all departments will follow. This process attempts to answer the basic questions of any organization, which you can see atop each column: where do you want to be…where are you now…how are you going to get there…and then progress is measured and communicated, and plans are revised.

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 18

Take a look at Phase 1, which we’re doing now with all departments. This is where we embark on some very basic strategic planning. During this phase, we ask departments: what is the fundamental purpose you are trying to achieve; describe what the ideal state looks like; and develop long-term goals that will help mark achievement of your ideal state. We’ll complete this with all departments, ensuring along the way that what they come up with is in alignment with county-wide priorities. Many departments already have mission, and sometimes a vision and goals, but we’ll help them formalize it and systematically tie it to the work happening in their programs and across the County. In Phases 2 and 3, we work with Department program managers, helping to facilitate the implementation of this management system. We’ve piloted this work with individual program managers within Child and Family Services, Purchasing, and Facilities Management. I’ll explain more on the pilot in a moment. Phase 4, focused on ensuring the continuous use of this information to drive internal decision making, will start to take shape next year as well. Internal procedures will change at some point in the near future to reflect this work and to begin to hold departments accountable to this work. So that’s the process. As I mentioned, we are piloting the full process with three programs: The Buyers Unit within Purchasing, Juvenile Justice within Child and Family Services, and Central Mail within Facilities Management. These programs represent each of the 3 county functional areas: Human services, Physical services, and Administrative services, and they vary in scope and complexity. This has allowed us to refine our tools and our approach as we attempt to create a performance system that works for all departments. The pilot work in those areas is nearly complete. Additionally, we are rolling out Phase One in every Department. Physical Services is complete and you will notice that each Physical Service department has an updated mission statement in this year’s budget book. Phase One will be completed with all county departments by early 2016

Mr. Morgan:

Legislature has heard him talk about the ability to budget and record expenses at a lower level – a program functional level – 1st step

This is the second step – if we have data or ability to create the data, and nothing is done with it, then there is no need to have an accounting

Next logical step is to put some performance around the program - are the investments being made achieving the outcomes that we expect

Has been tried in the past, and has fizzled

Committed to dedicating resources in the office to do it – if it is someone’s part-time job, it’s not going to get done

Will continue to keep legislature updated on progress, supplying different types of information in the budget as it moves forward

Mr. Morgan continued: As part of this budget cycle, we have included legislation to modify the budget calendar starting with the 2017 budget cycle. Last year, we successfully had the State amend our tax act to allow us to deliver the tax abstract to the City at a later date. We now have until December 20th. Please turn your attention to the chart on the screen. Go through revised calendar. The main goal of revising the budget cycle calendar is to have current information on the County’s major revenues and expenditures to make more informed and hopefully accurate projections. A large number of counties do not adopt their budgets until much later in the year compared to our County. For example, Monroe County adopts their budget the second Tuesday of December while Erie County adopts theirs the first Tuesday of December.

Mr. Morgan:

Rough dates - some of the dates may change

Is art of the legislation brought over for consideration

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 19

Budget Cycle Calendar

Division of Financial Operations This division was initially created to consolidate the fiscal operations of the human services departments restructured in 2014 with the longer term goal of folding in the remaining County department’s fiscal operations over the next few years. Since then we’ve added the financial operations of the Sheriff and Health Departments with the Library being phased in the end of this year. The division is headed in the right direction and is close to completing the work of restructuring the division’s staff and tasks into functional areas. Once complete, each functional area will provide its particular services to all of the departments the division supports as opposed to specific employees supporting a department’s finances in their entirety. We believe this structure will provide many benefits that will result in increased effectiveness and efficiencies. For 2016, we are proposing to add the fiscal operations of Law, IT, MWB, and Community Development. A total of 4 positions are proposed to be abolished in the respective departments and created in the Finance Department to continue our move towards a countywide financial operation. Show org chart.

Division of Financial Operations

Mr. Morgan:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 20

Long term goal is a functional basis where all the people, i.e. in procurement area, are supporting all departments fashion of that work

Right now departments that have their own finance office have specific people that perform all of the work for that department

The goal is to become more efficient and effective; cross training is very important – allows people to leave and their work doesn’t pile up

Ability to transfer knowledge through multiple people going forward Mr. Morgan continued: The proposed budget to support the Finance Department is $9 million—with $5 million in direct expenditures and $4 million in indirect appropriations.

$7.6 million, or 84% of the finance budget is for wages and benefits. Most of the rest of this budget goes for expenses tied to our tax enforcement programs—to advertise delinquent properties and the auction, pay for title searches and process serving fees, and so forth. The salary line increase is the result of the fiscal consolidations I previously mentioned. Revenues are generally in line with this year’s levels aside from interdepartmental revenue which is increasing due to charging back the new departments we’ll be supporting. I can go through these very quickly.

The “non-real property tax” item is the Finance Department’s charge to the Room Occupancy Tax for the collection and enforcement of the Room Tax. This is the same as 2015. The Co Svc Revenue account is primarily made up of fees charged to delinquent taxpayers to cover the administrative expenses of tax collection and enforcement—for the cost of legal ads, title searches, certified mailings, and staff time we spend to collect back taxes. The Svc Other Govt account is the revenue we receive from towns, villages and school districts to maintain their tax rolls and print their tax bills. We charge them $2 per parcel. The Interest & Earnings account is essentially a portfolio management charge by Finance for investing and managing the County’s funds. The money comes from interest earned on those funds, and is used to offset the cost of the Finance Department’s Treasury function. The Sales of Property Account, is the amount of money we receive from the tax auction in excess of the amount of taxes due. If, for example, we sell a property for $1,000 that has $800 of delinquent taxes on it, the $200 excess is deposited into this account. The account also includes $2,600 in tax map sales. And last, the Other Misc Rev account contains fees for administering tax installment accounts plus wire transfer fees and unclaimed accounts. It also includes a charge to the Tobacco Securitization Corporation for costs we incur to administer the on-going administrative tasks of the securitization. Our interdepartmental revenue account is our charge to WEP and the Water Board for preparing their tax bills as well as charges to the departments we support through the Financial Operations Division.

Mr. May:

For clarification – every position proposed as an addition has an abolish against it in the source department

Mr. Morgan:

There is for the consolidations; there is another funding adjustment that is not related to the centralization, but everything else is related to the centralization of those functions

Mr. May:

Is it your opinion that on a one to one basis these folks need to come in Mr. Morgan:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 21

The position for MWB, haven’t even asked for funding for it – attempting to see if it can be absorbed – want position, but not asking for money behind it

If that can’t be done, will look to other options and potentially need support for that Mr. May:

OnWard – it is hard thing to accomplish; what are we trying to get to Mr. Morgan:

County and local taxpayers expend a local dollar budget, for 2016 proposed at $412 million – trying to get to – seeing and achieving the outcomes and goals that were expected to achieve for the programs they operate

Not a concept enacted in many other governments; in New York the team has been hard-pressed to find a municipality that it doing this

Mr. May:

Almost sounds like the private sector Mr. Morgan:

Bringing in revenue from taxpayers – the county executive and county’s interest is in knowing if we are receiving the benefits that were intended to be received when investments were made

It will be a long process

Has 4 people dedicated to it; would like to have 20

Direction we need to move in and will ultimately allow legislature and county executive the ability to make informed decisions, investment decisions, and give the county manager the tools to operate their department on a daily basis

It is using the data that is going to be produced by identifying metrics; and using it to change what we are doing to improve

Mr. May:

Ultimately it is a process to enable getting to good fiscal decisions Mr. Morgan:

Fiscal and program decisions Mr. Fisher:

The last time there was a real set back in the economy, policy makers weren’t left with good decision options

There will be another recession, sales tax will drop – at that point the legislature and county executive will be stuck with some really bad options or enough information to make informed decisions about what to do about it

Dr. Chase:

Positions – added 7, but eliminated the Fiscal Officer Health Mr. Morgan:

When Health fiscal operations was consolidated into Finance Dept., the position isn’t applicable any more

Administrative Director position being created is taking the place of that position

When move into Finance, that person was in the title of Fiscal Officer Health; requesting to create a title of Administrative Director at the same grade and abolish Fiscal Officer Health

Dr. Chase:

As positions are moved into Finance, do those people still have responsibility of seeing over the department they came from

Mr. Morgan:

Yes, initially the people sit in the same place and do the same thing for a time. Then, slowly they are analyzed on what they do, who they serve, level of work.

They are moving to functional areas - i.e. if responsible for procurement, they may go into the procurement function division and support multiple departments from that perspective, or go to a different functional area

Goal is to get them unhooked from a specific department and get them into a functional area to support multiple departments

Dr. Chase:

Will departments continue to be represented Mr. Morgan:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 22

They will be represented in the structure created as department liaisons

They are higher level managers that are expected to have first-hand knowledge of the department, polices and operations, attend senior staff meetings and have first-hand knowledge of that department

Chairman Knapp:

Multiple people will be familiar with each department Mr. Morgan:

There will be a main person – a lot of them came from that department and have the institutional knowledge to be able to support that department at a higher level

Goal will be to have the higher managers establish and create the ability to support departments at the higher level. Lower level personnel responsible for the transactional work will be supporting all of the departments

Mr. Holmquist:

Surprised to see the county executive bring forth a local law changing the budget calendar

The leadership approached the membership and asked us our opinions on a variety of options

Had a very detailed, robust discussion on the various options

All options have pros and cons – no perfect proposal

The reason it was decided that we don’t want to have the budget later on in the year, despite the positives outlined, at the end of the day, this is the biggest thing that the legislature does

To have the budget process after election day is a horrible idea – it has tremendous downside on multiple fronts – most members feel that way

In a $1.2 billion budget the public is part of the budget process

The election is in early Nov.; this proposal is to vote on it in early Dec., which is the middle of a holiday – the public participation would be greatly inhibited

Any time there is an election in December, the turnout is low – referenced the fire departments holding elections in December and have about 25 people turn out (referred to Dewitt Fire Commissioners election)

Bad for democracy, bad for our budget process

Debated already – went to leadership, and believes that they went to the county executive and said that the legislature doesn’t support this

Confused as to why the county executive would bring this back for discussion Mr. Morgan:

Legislature may have debated it, but it is still a desire from the executive perspective to pursue this change

Fully support it – in front of legislature right now, and it is September and is trying to estimate sales tax and large mandates and he doesn’t have a good idea of what they will be this year let alone next year

Strictly from a financial standpoint, it makes perfect sense Mr. Holmquist:

Does not disagree – recognizes the positives – it is really hard – have to make all kinds of projections

So does the legislature; it is moving target – making estimates; the later in the year the estimates are going to be – no question about it

All the scenarios were reviewed – there are number that could happen after election day – people on the legislature who may have been unelected

Most importantly the county budget is a report card of the county legislature and county executive; it is the most important thing that we do

In the spirit of transparency and good government…making sure we are on the record with what the tax rate will be, and with what our spending priorities are, what entire budget book looks like, the entire process, and the public participation in the process -- if all that takes place after Election Day, despite the benefits of putting together the best document that we can, it is disrespectful to the public – it cuts them out entirely. There isn’t going to be public participation during the holidays – certainly not to the extent that it should be.

Currently we have a pretty good process – may be drawbacks, but it is less worse than the alternatives.

Passing the budget after election day is a huge mistake

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 23

Mr. Fisher:

Give thought to how a corporation works. I.e. -- when the board of Key Bank is evaluated, it is not on the basis of a budget – it is almost a non-event when the board adopts a budget

Measured on results – how the board did in hiring management; how did management do in taking the adopted budget and carry it out

By November, the voters should know if we did a good job by the budget adopted last year

We should be measured on results, not a plan

There is plenty of information about how you did as a legislator throughout the year. If you give the voters some credit, it should weigh far more heavily than a budget that might happen next year.

Mr. Holmquist:

Legislature has two functions: budget and policy. With respect to the budget – those are our results: tax rate, spending priorities. What kind of changes are going to happen after Election Day – there is no accountability.

If there are elections, followed by the budget, and things are done that deviate from what was said before Election Day – elected officials change their priorities and raise taxes or pass an Agenda 21 Program or some nonsensical program like it, those are our results, on the record and there is no accountability. It’s a long time to the next Election Day.

Right now the public has participation – at the public hearing and during the budget review there is all kinds of contact with interested parties in the budget in various departments, stakeholders.

During holidays, it is unfair and disrespectful.

Currently we have a good system – it’s not perfect. There are some good points, certainly on the financial side. Even with that, it is only (proposed) a few weeks later, and not enough to overcome that on Election Day people have a right to know what our properties are and what the actual vote is for next year’s budget.

Chairman Knapp:

Have talked in concept in depth; now we have an actual local law with specific dates

We need to take a look at it and talk about it like we did before. Mr. Holmquist:

Feels like we have had tangible, good outlines of the options

The outline in the local law was debated and discussed.

We can vote formally “no”. Mr. Fisher:

This would be an open, public discussion. Mr. Jordan:

Likes the idea of setting up goals and parameters in terms of what we want to accomplish in the different departments, measuring the goals to see if we are accomplishing them. If not, then taking action to correct procedures and operate county government more efficiently.

Everyone talks about having government run more like private business, but there are obviously outside influences that affect how governments operate. Unfortunately, there are influences affecting decisions being made that aren’t governed solely by business principles.

One objection was the smooshing things down to a very short period of time. If we are voting on a budget in December, what needs to be done procedurally to go from an adopted budget to actually issuing tax bills – an awful lot has to happen, and now it is a much more dense period of time

Taxpayers may not have an idea of what they will have to owe for taxes – will have a shortened period of time to get their financial house in order to actually pay their tax bills.

Mr. Morgan:

Their bills will still come the same time – it will not change Mr. Jordan:

Right now the press will say if taxes are going up, staying flat, etc., so people can have an idea of the impact that they have on their bill. Right now, if it is passed in October, they have 2 -3 months before they have to pay the bill. They will know, for example, if it will be $300 higher than it was before and can make arrangements to pay that increased bill.

If they don’t find out until the middle of Dec., and have to pay that bill the following month, they won’t have that much time to get their financial house in order. They won’t know if there will be a financial impact on their tax bill until 2 – 3 weeks before they get the bill.

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 24

Mr. Morgan:

It’s a fair point – history has shown that the tax rate does nothing but go down here

Have worked closely with the City and Don Weber to ensure that this timetable is something his office and the city administration can ensure that the tax bills go out on time.

The city had to agree, or the Tax Act wouldn’t have been amended by the state. Mr. Jordan:

Have other counties that have a similar timeframe experienced any problems with their budget cycle Mr. Morgan:

Erie County and Monroe County – one adopts their budget the 1st week of Dec., the other adopts it the 2nd week – doesn’t have any information as to whether it has created issues in the past.

Mr. Morgan said that he can find out if desired; Mr. Jordan indicated that he would. Chairman McMahon:

Most counties in the state adopt it later

To Mr. Holmquist’s point of electoral transparency – have any options been looked at that would have the budget presentation at the end of October and move the budget vote after the elections. It would meet the goal of having more accurate data.

This hasn’t been debated publicly, but it has been debated all year long; we decided not to do it this year

Concern: are electoral transparency and jamming it in at end of the year with 2 significant holidays – numerous employees take vacation time

If the budget is presented before Election Day, the budget presented by the County Executive is the framework of what typically happens. Changes are made, but they aren’t Draconian. It would be enough to hopefully take care of some of those concerns.

Understand it is cleaner to do it all before or all after, but if the main goal is about financial data and the road blocks are these types of concerns, then there might be some common ground that can be reached.

Mr. Morgan:

Mr. Holmquist pointed out that is one of the main things the legislature does; if it is not voted on before election, he doesn’t know if that is satisfactory to members.

Chairman McMahon:

In talking to colleagues, it was not the main concern from everybody; other had other issues. Some people didn’t think making this decision this year made any sense, but we are talking about next year now.

Chairman Knapp:

Asked how the agreement with Madison County is going -- sharing our Dir., Real Property Tax Svcs. Mr. Weber:

Going pretty well; their deputy county treasurer has taken on some of the real property supervisor functions – she runs things on a day to day basis.

I am used as a contractor – if they have questions or concerns

It was a heavy lift initially – as role has been defined, it has become much more manageable. The staff there has learned what their duties are on a daily basis.

Chairman Knapp:

What software does Madison County use Mr. Weber:

They are implementing Tyler Technologies Munis in their treasury department; Onondaga County did not go with the vendor.

Chairman Knapp:

OnWard – asked to be kept in the loop on that – would love to see what happens down the road – metrics for various departments

Mr. Morgan:

It is a work and progress; will provide periodic updates Chairman Knapp:

Overtime line - $0 for this year, but have had money in there in the past – asked what it was for Mr. Morgan:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 25

In 2014 it was probably out of Financial Operations; sometimes they get behind in paying vendors, so push overtime at it

If any is used for 2016, it will be a small amount of money that can be absorbed in the budget Chairman Knapp:

103 line – how many are there and what is the primary use for part time employees Mr. Morgan:

A few seasonals

Real Property Tax Services has a handful of temporary staff – they are permanent, part time Chairman Knapp:

Asked about the supplies and materials increase Mr. Morgan:

Assuming additional expenses with the moves into financial operations – when staff is moved, some additional support will be needed for them

Chairman Knapp:

Is it going down in the other departments to reflect it Mr. Morgan:

It is not a one for one – not decreasing dollar for dollar in other areas Mr. Weber:

New paper was needed for the tax bills – has a pressure seal – more expensive Chairman Knapp:

Asked about the significant increase in 408 – professional services Mr. Weber:

Vendor contract that provides the tax information/search on the website Mrs. Ervin:

Regarding the budget calendar, it hasn’t been talked about in total – is not sure we all agree on anything at this point. Looks forward to the discussion.

Chairman Knapp recessed the meeting for 10 minutes. The meeting was reconvened at 3:40 p.m. INSURANCE – PG. 3-105 – Peter Troiano, Commissioner, Personnel Department Mr. Troiano presented the following:

INSURANCE FUNDJOANNE M. MAHONEY, COUNTY EXECUTIVE

STEVE MORGAN, CHIEF FISCAL OFFICER

PETER TROIANO, COMMISSIONER OF PERSONNEL

2016 ANNUAL BUDGETWays & Means Committee Report

TA

BLE

OF

CO

NTEN

TS

2

Table of Contents

Slide 3: Insurance Fund Budget SummarySlide 4: Benefits BreakdownSlide 5: Health BreakdownSlide 6: UnemploymentSlide 7: Long Term DisabilitySlide 8: Insurance PoliciesSlide 9: Professional ServicesSlide 10: Workers’ CompensationSlide 11: Judgments & ClaimsSlide 12: Questions

BU

DG

ETS

UM

MA

RY

AN

ALYSIS

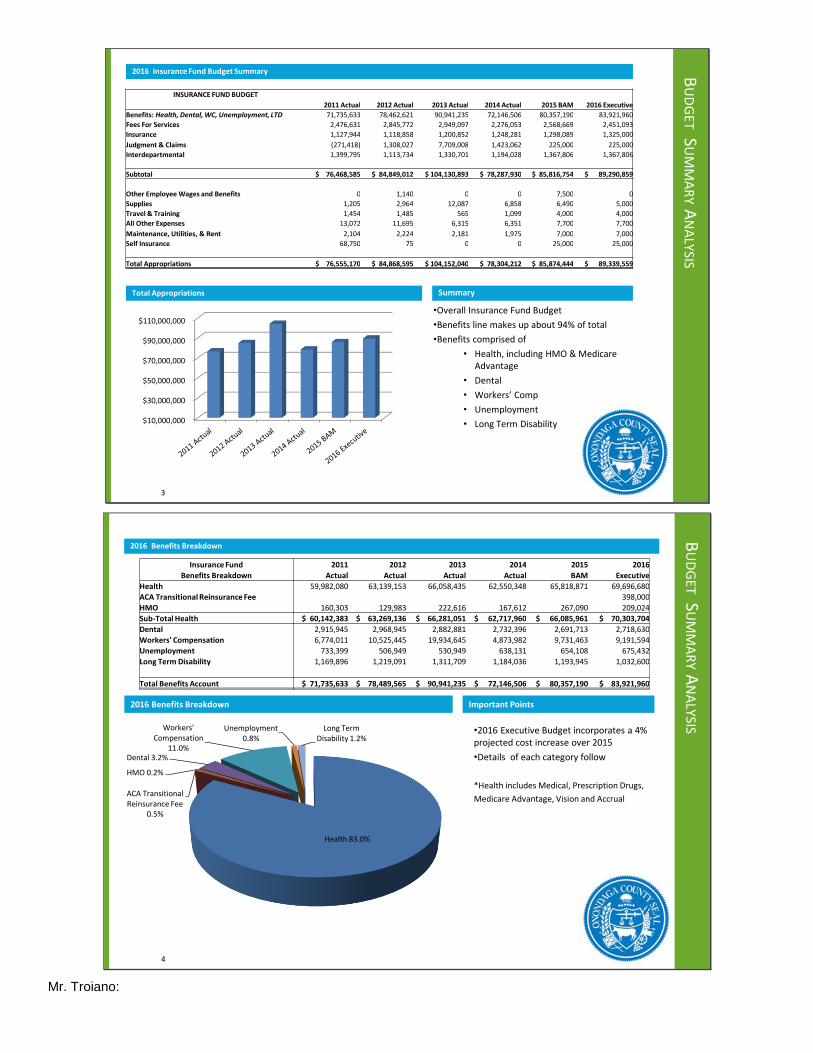

2016 Insurance Fund Budget Summary

Total Appropriations Summary

•Overall Insurance Fund Budget

•Benefits line makes up about 94% of total

•Benefits comprised of

• Health, including HMO & Medicare Advantage

• Dental

• Workers’ Comp

• Unemployment

• Long Term Disability

3

INSURANCE FUND BUDGET

2011 Actual 2012 Actual 2013 Actual 2014 Actual 2015 BAM 2016 Executive

Benefits: Health, Dental, WC, Unemployment, LTD 71,735,633 78,462,621 90,941,235 72,146,506 80,357,190 83,921,960

Fees For Services 2,476,631 2,845,772 2,949,097 2,276,053 2,568,669 2,451,093

Insurance 1,127,944 1,118,858 1,200,852 1,248,281 1,298,089 1,325,000

Judgment & Claims (271,418) 1,308,027 7,709,008 1,423,062 225,000 225,000

Interdepartmental 1,399,795 1,113,734 1,330,701 1,194,028 1,367,806 1,367,806

Subtotal $ 76,468,585 $ 84,849,012 $ 104,130,893 $ 78,287,930 $ 85,816,754 $ 89,290,859

Other Employee Wages and Benefits 0 1,140 0 0 7,500 0

Supplies 1,205 2,964 12,087 6,858 6,490 5,000

Travel & Training 1,454 1,485 565 1,099 4,000 4,000

All Other Expenses 13,072 11,695 6,315 6,351 7,700 7,700

Maintenance, Utilities, & Rent 2,104 2,224 2,181 1,975 7,000 7,000

Self Insurance 68,750 75 0 0 25,000 25,000

Total Appropriations $ 76,555,170 $ 84,868,595 $ 104,152,040 $ 78,304,212 $ 85,874,444 $ 89,339,559

$10,000,000

$30,000,000

$50,000,000

$70,000,000

$90,000,000

$110,000,000

BU

DG

ETS

UM

MA

RY

AN

ALYSIS

2016 Benefits Breakdown

2016 Benefits Breakdown Important Points

•2016 Executive Budget incorporates a 4% projected cost increase over 2015

•Details of each category follow

*Health includes Medical, Prescription Drugs,

Medicare Advantage, Vision and Accrual

4

Health 83.0%

ACA Transitional Reinsurance Fee

0.5%

HMO 0.2%

Dental 3.2%

Workers' Compensation

11.0%

Unemployment 0.8%

Long Term Disability 1.2%

Insurance Fund 2011 2012 2013 2014 2015 2016

Benefits Breakdown Actual Actual Actual Actual BAM Executive

Health 59,982,080 63,139,153 66,058,435 62,550,348 65,818,871 69,696,680

ACA Transitional Reinsurance Fee 398,000

HMO 160,303 129,983 222,616 167,612 267,090 209,024

Sub-Total Health $ 60,142,383 $ 63,269,136 $ 66,281,051 $ 62,717,960 $ 66,085,961 $ 70,303,704

Dental 2,915,945 2,968,945 2,882,881 2,732,396 2,691,713 2,718,630

Workers' Compensation 6,774,011 10,525,445 19,934,645 4,873,982 9,731,463 9,191,594

Unemployment 733,399 506,949 530,949 638,131 654,108 675,432

Long Term Disability 1,169,896 1,219,091 1,311,709 1,184,036 1,193,945 1,032,600

Total Benefits Account $ 71,735,633 $ 78,489,565 $ 90,941,235 $ 72,146,506 $ 80,357,190 $ 83,921,960

Mr. Troiano:

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 27

History with being self-insured trends below regional and national levels; continues in 2016 budget

ACA Transitional Reinsurance Fee – now charged for as part of the Affordable Care Act

Dental (Self-insured 3 years ago), Unemployment, Disability Insurance – continue to trend relatively flat

BU

DG

ET

SU

MM

AR

YA

NA

LYSIS

2016 Overview of County Health, HMO and Dental Expenses

Health Breakdown Major Drivers

Expenditures

•2016 budgeted increase is 4% over 2015 projections, and is based on 3-year trend analysis of our claims blended with national trend.

•Medicare Advantage budget formulated using two full years of actual data.

5

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000 Dental

HMO (MVP)

ACA TransitionalReinsurance Fee

Net Accrual

Vision (Davis)

Prescription Drugs(ProAct)

Medicare Advantage

Medical(Onpoint/Indemnity)

INSURANCE FUND 2011 Actual 2012 Actual 2013 Actual 2014 Actual 2015 BAM 2016 Executive

HEALTH BENEFITS BREAKDOWN

Medical (Onpoint/Indemnity) 41,439,669 40,245,757 45,378,760 41,613,354 43,711,214 43,723,212

ERRP Subsidy (199,026)

Medicare Advantage 2,072,810 7,478,113 6,500,000 9,000,000 Prescription Drugs (ProAct) 18,330,009 19,403,625 17,172,809 13,021,251 14,190,861 15,500,000

Vision (Davis) 719,693 713,934 699,402 509,352 647,024 672,905

Net Accrual (308,265) 2,775,836 734,654 (71,722) 769,772 800,563

Sub-Total Health Plan $ 59,982,080 $ 63,139,153 $ 66,058,435 $ 62,550,348 $ 65,818,871 $ 69,696,680

ACA Transitional Reinsurance Fee 398,000

HMO (MVP) 160,303 129,983 222,616 167,612 267,090 209,024

Sub-Total HMO and Health $ 60,142,383 $ 63,269,136 $ 66,281,051 $ 62,717,960 $ 66,085,961 $ 70,303,704

Dental 2,915,945 2,968,945 2,882,881 2,732,396 2,691,713 2,718,630

TOTAL $ 63,058,328 $ 66,238,081 $ 69,163,932 $ 65,450,357 $ 68,777,674 $ 73,022,334

Medicare Advantage – have 2 years of cost experience – have better figures/expectations for 2016; currently in the RFP process for different vendor

Prescription Drugs – across the country seeing an increase in number of specialty drugs and increased utilization of specialty drugs

Specialty drugs – very expensive drugs brought on the market by pharmaceutical companies – used to treat extreme forms of illness, i.e. cancer, lupus; expansion of specialty drugs for other disease treatment

BU

DG

ETSU

MM

ARYA

NALYSIS

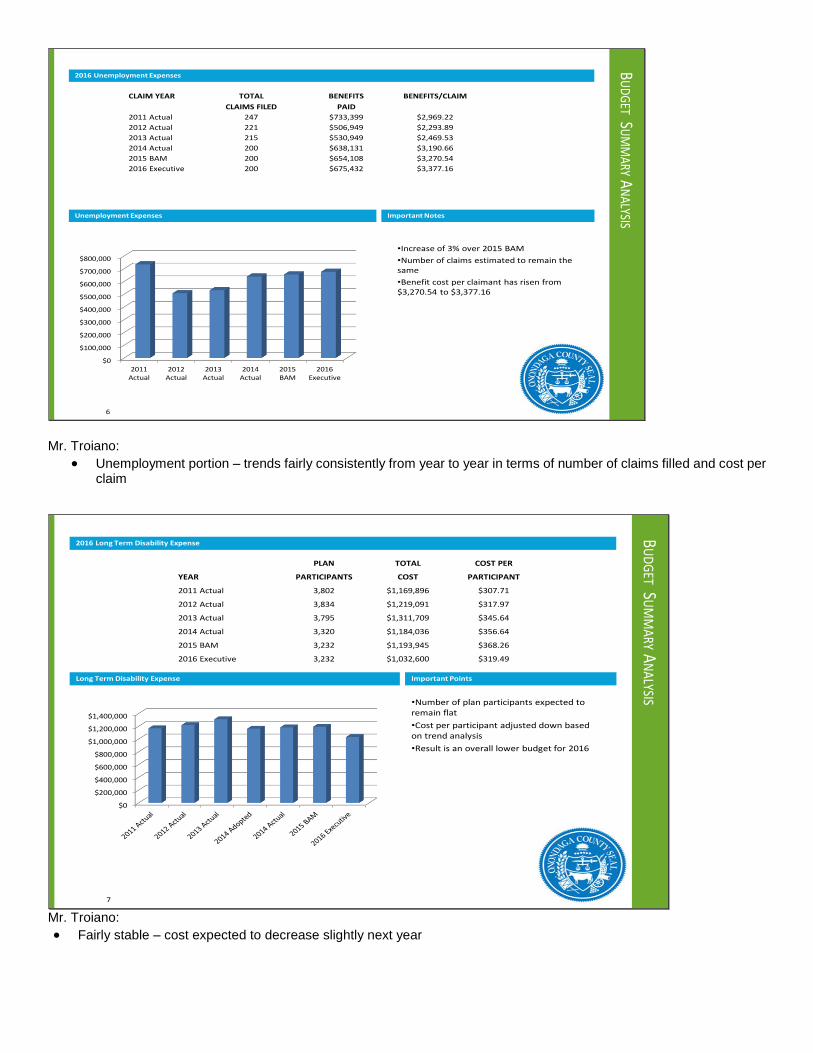

2016 Unemployment Expenses

Unemployment Expenses Important Notes

•Increase of 3% over 2015 BAM

•Number of claims estimated to remain the same

•Benefit cost per claimant has risen from $3,270.54 to $3,377.16

6

CLAIM YEAR TOTAL BENEFITS BENEFITS/CLAIM

CLAIMS FILED PAID

2011 Actual 247 $733,399 $2,969.22

2012 Actual 221 $506,949 $2,293.89

2013 Actual 215 $530,949 $2,469.53

2014 Actual 200 $638,131 $3,190.66

2015 BAM 200 $654,108 $3,270.54

2016 Executive 200 $675,432 $3,377.16

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

2011Actual

2012Actual

2013Actual

2014Actual

2015BAM

2016Executive

Mr. Troiano:

Unemployment portion – trends fairly consistently from year to year in terms of number of claims filled and cost per claim

BU

DG

ETSU

MM

ARYA

NALYSIS

2016 Long Term Disability Expense

Long Term Disability Expense Important Points

•Number of plan participants expected to remain flat

•Cost per participant adjusted down based on trend analysis

•Result is an overall lower budget for 2016

7

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

PLAN TOTAL COST PER

YEAR PARTICIPANTS COST PARTICIPANT

2011 Actual 3,802 $1,169,896 $307.71

2012 Actual 3,834 $1,219,091 $317.97

2013 Actual 3,795 $1,311,709 $345.64

2014 Actual 3,320 $1,184,036 $356.64

2015 BAM 3,232 $1,193,945 $368.26

2016 Executive 3,232 $1,032,600 $319.49

Mr. Troiano:

Fairly stable – cost expected to decrease slightly next year

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 29

BU

DG

ETS

UM

MA

RY

AN

ALYSIS

2016 County Insurance Policies

County Insurance Policy Costs Important Points

• 2.03% increase in premiums

8

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

FOSTER CARE

CRIME

INLAND MARINE

CHIEF FISCAL OFFICER

AVIATION LIABILITY

OTHERS

PROPERTY

EXCESS LIABILITY

LIABILITY INSURANCE POLICIES 2011 Actual 2012 Actual 2013 Actual 2014 Actual 2015 BAM 2016 Executive

PROPERTY 540,345 568,814 527,355 641,924 662,498 638,800

INLAND MARINE 2,550 2,563 2,691 2,691 3,000

AVIATION LIABILITY 53,387 -1,426 54,636 49,343 60,000 60,000

EXCESS LIABILITY 519,809 519,719 605,822 536,901 558,377 570,000

OTHERS 1,250 18,513 39,000

INSURANCES SUBTOTAL $ 1,117,341 $ 1,108,183 $ 1,190,504 $ 1,228,168 $ 1,283,566 $ 1,310,800

CHIEF FISCAL OFFICER 1,250 1,250 565 2,000 2,000

CRIME 9,353 9,425 9,783 11,957 12,523 12,200

BONDS SUBTOTAL $ 10,603 $ 10,675 $ 10,348 $ 11,957 $ 14,523 $ 14,200

SUBTOTAL $ 1,127,944 $ 1,118,858 $ 1,200,852 $ 1,240,125 $ 1,298,089 $ 1,325,000

FAMILY DAY CARE 8,711

FOSTER CARE 49,503 50,566 12,487 8,156

GRAND TOTAL $ 1,186,158 $ 1,169,424 $ 1,213,339 $ 1,248,281 $ 1,298,089 $ 1,325,000

Mr. Morgan:

Counties insurance policies – mainly excess liability and property

Projecting 2% increase

WAYS & MEANS 2016 BUDGET REVIEW OF WAYS & MEANS DEPARTMENTS – September 16, 2015 30

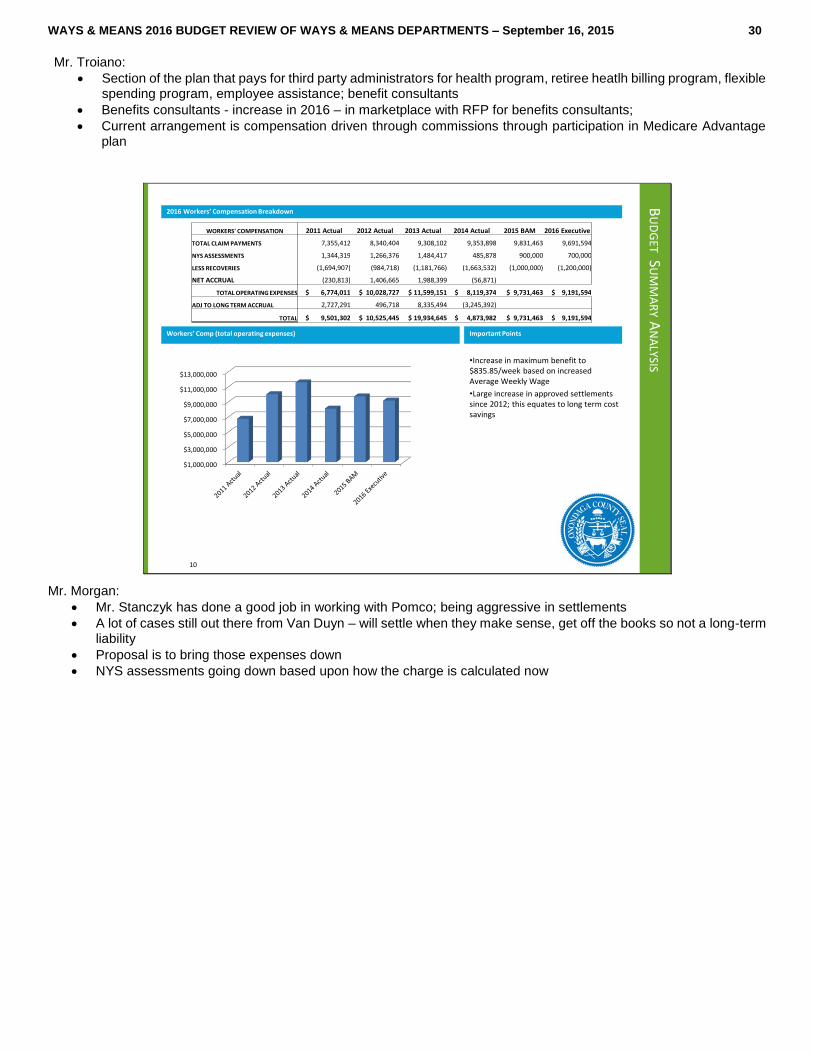

Mr. Troiano:

Section of the plan that pays for third party administrators for health program, retiree heatlh billing program, flexible spending program, employee assistance; benefit consultants

Benefits consultants - increase in 2016 – in marketplace with RFP for benefits consultants;

Current arrangement is compensation driven through commissions through participation in Medicare Advantage plan

BU

DG

ETS

UM

MA

RY

AN

ALYSIS

2016 Workers’ Compensation Breakdown

Workers’ Comp (total operating expenses) Important Points

•Increase in maximum benefit to $835.85/week based on increased Average Weekly Wage

•Large increase in approved settlements since 2012; this equates to long term cost savings

10

$1,000,000

$3,000,000

$5,000,000

$7,000,000

$9,000,000

$11,000,000

$13,000,000

WORKERS' COMPENSATION 2011 Actual 2012 Actual 2013 Actual 2014 Actual 2015 BAM 2016 Executive

TOTAL CLAIM PAYMENTS 7,355,412 8,340,404 9,308,102 9,353,898 9,831,463 9,691,594

NYS ASSESSMENTS 1,344,319 1,266,376 1,484,417 485,878 900,000 700,000