webinar slides: revenue recognition update for the technology industry

TRANSCRIPT

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

Revenue Recognition Update for the Technology Industry James Comito and Mark Winiarski Oct. 13 or Dec. 10, 2015

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

#cbizmhmwebinar 6

Presenters

The Director of MHM’s Professional Standards Group, James has

expertise in all aspects of revenue recognition, business combinations,

impairment of goodwill and other intangible assets, accounting for

stock-based compensation, accounting for equity and debt instruments

and other accounting issues.

James also has significant experience with a variety of other regulatory

and corporate governance issues pertaining to publicly traded

companies, including all aspects of internal control.

In addition, James frequently speaks on accounting and auditing matters

at various events for MHM.

858.795.2029 • [email protected]

JAMES COMITO, CPA MHM’s National Director of

Professional Standards

#cbizmhmwebinar 7

Presenters

Located in our Kansas City office, Mark is a member of our Professional

Standards Group (PSG). Mark's role includes instructing in our national

training program, presenting as a subject matter expert at webinars and

conferences, and preparing MHM publications on accounting and

auditing issues.

As a PSG member, Mark consults with clients and engagement teams

across the country in many areas of accounting and auditing. Mark has

served clients as an auditor, consultant and advisor in numerous

industries including manufacturing, distribution, mining, retail sales,

services and software.

913.234.1656 • [email protected] • @KCWini

MARK WINIARSKI, CPA MHM Shareholder

#cbizmhmwebinar 8

Agenda

Topic 606 Refresh

02

01

03

04

Changing Recognition Methods

Selected Revenue Recognition Issues

Revenue Recognition Update

#cbizmhmwebinar 9

TOPIC 606 REFRESH

Overview of the New Revenue Recognition Guidance

#cbizmhmwebinar 10

An entity should recognize revenue to depict the transfer of promised goods, or services, to

customers in an amount that reflects the consideration to which the entity expects to be

entitled, in exchange for those goods or services.

Core Principle

#cbizmhmwebinar 11

Five steps to apply the core principle:

Five-Step Process

1 • Identify the contract(s) with a customer.

2 • Identify the performance obligations in the contract.

3 • Determine the transaction price.

4 • Allocate the transaction price to the performance obligations

in the contract.

5 • Recognize revenue when (or as) the entity satisfied a

performance obligation.

#cbizmhmwebinar 12

• The objective of the disclosure requirements (Topic 606) is for an entity to disclose sufficient information to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. • The disclosure requirements are significantly in excess of

what is currently required under U.S. GAAP. • Non-public entities get excluded from many (but not all)

detailed disclosure requirements.

Disclosures

#cbizmhmwebinar 13

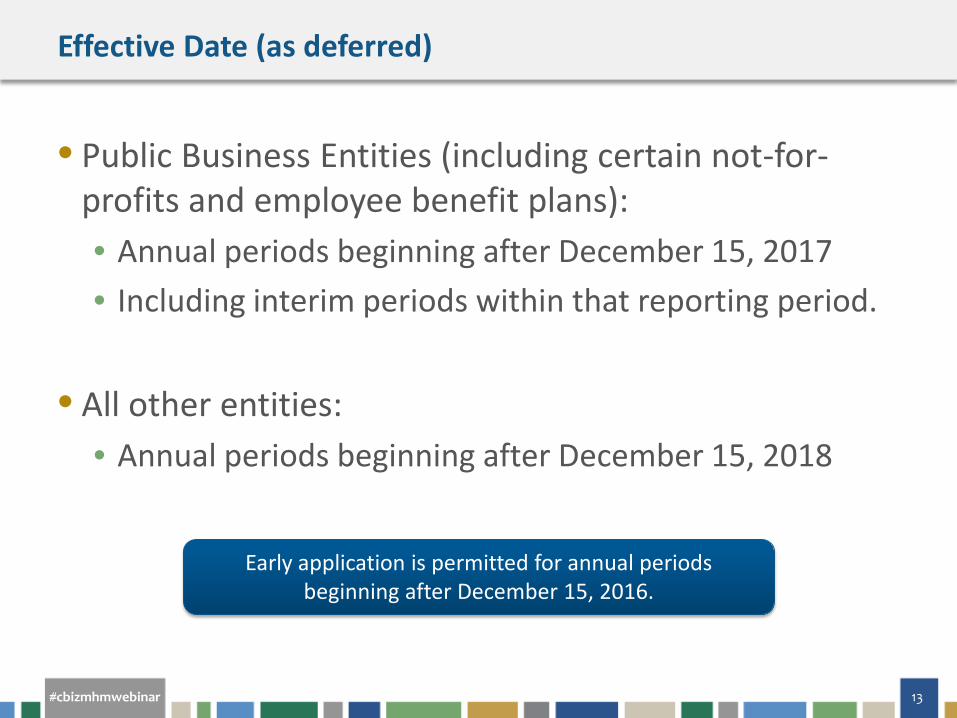

Effective Date (as deferred)

• Public Business Entities (including certain not-for-profits and employee benefit plans): • Annual periods beginning after December 15, 2017 • Including interim periods within that reporting period.

• All other entities:

• Annual periods beginning after December 15, 2018

Early application is permitted for annual periods beginning after December 15, 2016.

#cbizmhmwebinar 14

Transition Method

• Retrospectively to each prior reporting period presented • Practical expedients provided

• Modified retrospectively

• Cumulative effect of initially applying the guidance recognized at the date of initial adoption

• Disclosure showing revenue recognition under Topic 605 in the year of adoption

• An explanation of the reasons for significant changes

#cbizmhmwebinar 15

CHANGING RECOGNITION METHODS

Revenue recognition could be different.

#cbizmhmwebinar 16

Transfer of Control

Revenue is recognized when control transfers to the customer

• Over-time recognition occurs when: • Customer receives and consumes the benefits as

performance occurs • Performance creates or enhances an asset the

customer controls • Performance creates an asset without an alternative

use to the entity and the entity has a right to payment for performance completed to date

• Revenue not recognized over-time is recognized at a point in time

#cbizmhmwebinar 17

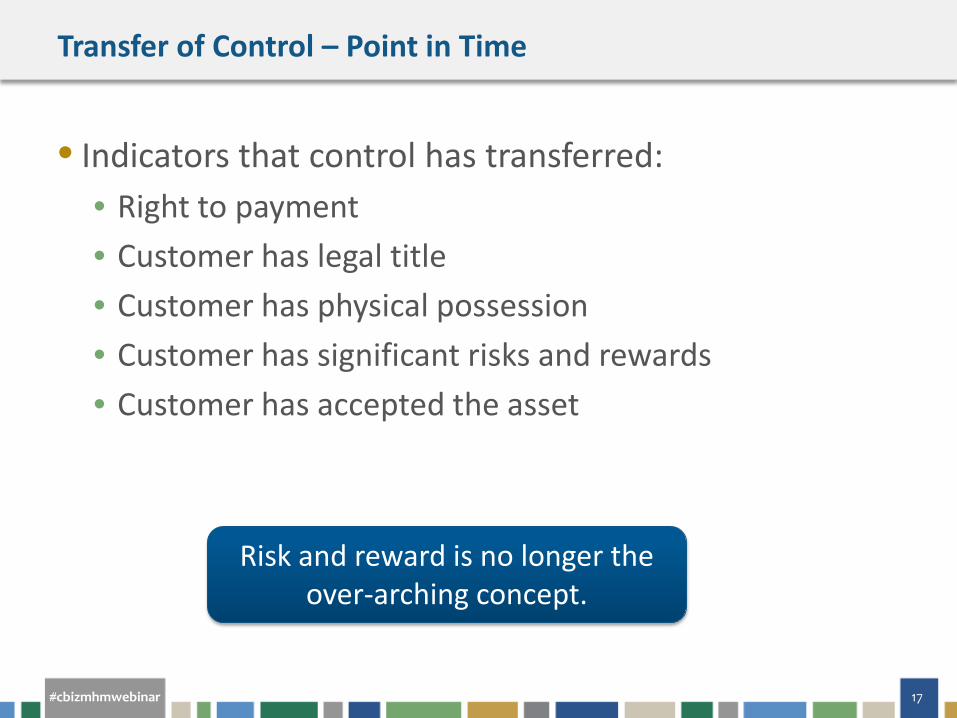

Transfer of Control – Point in Time

• Indicators that control has transferred: • Right to payment • Customer has legal title • Customer has physical possession • Customer has significant risks and rewards • Customer has accepted the asset

Risk and reward is no longer the over-arching concept.

#cbizmhmwebinar 18

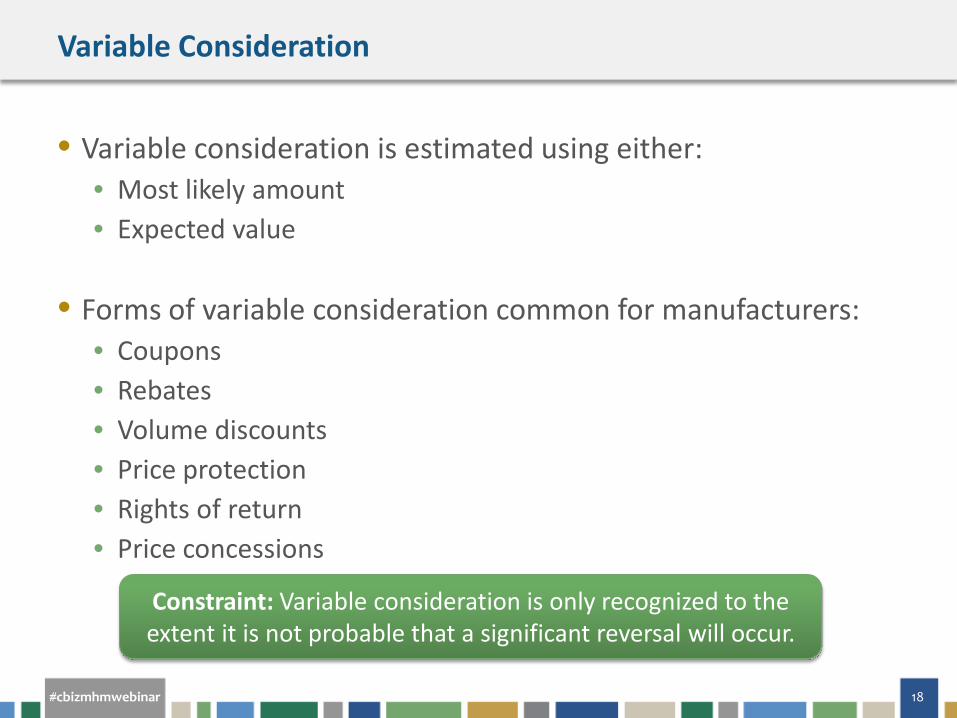

Variable Consideration

• Variable consideration is estimated using either: • Most likely amount • Expected value

• Forms of variable consideration common for manufacturers:

• Coupons • Rebates • Volume discounts • Price protection • Rights of return • Price concessions

Constraint: Variable consideration is only recognized to the extent it is not probable that a significant reversal will occur.

#cbizmhmwebinar 19

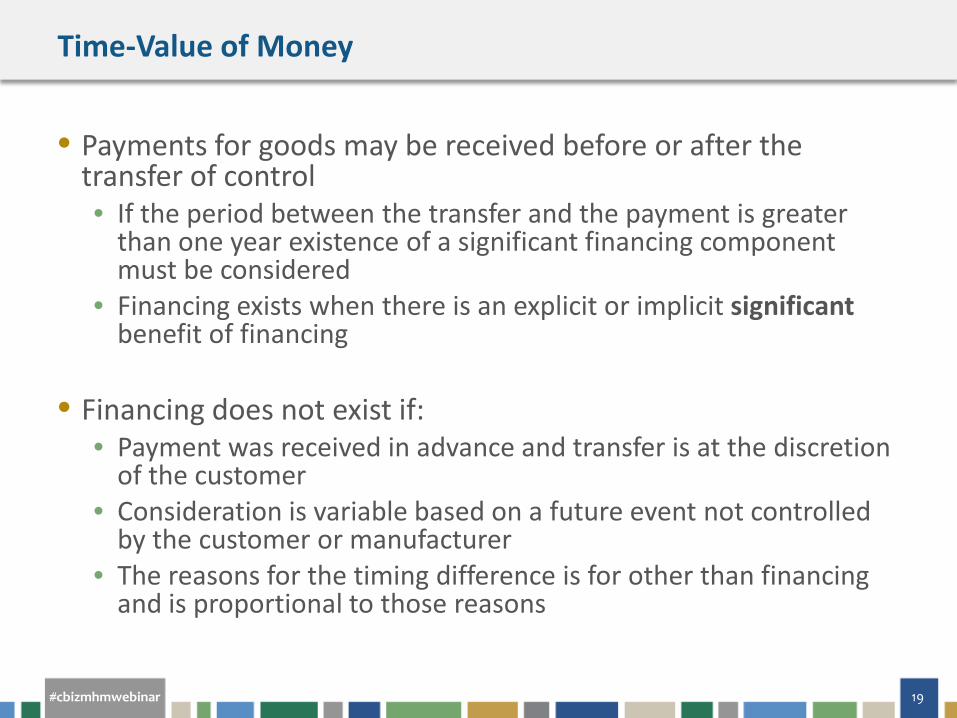

Time-Value of Money

• Payments for goods may be received before or after the transfer of control • If the period between the transfer and the payment is greater

than one year existence of a significant financing component must be considered

• Financing exists when there is an explicit or implicit significant benefit of financing

• Financing does not exist if:

• Payment was received in advance and transfer is at the discretion of the customer

• Consideration is variable based on a future event not controlled by the customer or manufacturer

• The reasons for the timing difference is for other than financing and is proportional to those reasons

#cbizmhmwebinar 20

SELECTED REVENUE RECOGNITION ISSUES

Changes for Technology Companies

#cbizmhmwebinar 21

Multiple Element Arrangements

• It is common practice for technology companies to provide multiple products and services to their customers under a single contract or arrangement. • Hardware • Software/technology license • Professional services • Extended maintenance agreements

#cbizmhmwebinar 22

Multiple Element Arrangements

• Under existing U.S. Generally Accepted Accounting Principles, the allocation of arrangement consideration among the “elements” is often complex and as a result different industry guidance has been developed for software and non software arrangements.

• Topic 606 replaces all previous multiple element guidance with a single revenue recognition model, regardless of industry

#cbizmhmwebinar 23

Multiple Element Arrangements

• Under Topic 606; management must identify the separate performance obligations based on the contractual terms and its own customary business practices. • A performance obligation is a promise in a contract to

transfer either: • a good or service (or bundle of goods or services) that is

distinct; or • a series of distinct goods or services that are substantially

the same and that have the same pattern of transfer to the customer.

#cbizmhmwebinar 24

Multiple Element Arrangements

• Under Topic 606, the transaction price is allocated to the separate performance obligations identified in the contract. • The allocation is based on the relative stand alone

selling price or the good and/or service. • In the event a good or service is not separately sold;

management would need to estimate the stand alone selling price.

#cbizmhmwebinar 25

Software Transactions

• Impact on software transactions • Existing guidance for software transactions requires

vender specific objective evidence (VSOE) for separating multiple elements. VSOE as currently defined and practiced is a very high hurdle to overcome.

• The elimination of the requirement for VSOE may accelerate the timing of revenue recognition in those situations where VSOE was previously not considered available and revenue recognition deferred.

• While no longer required, some believe that VSOE will continue to provide a proxy for standalone value.

#cbizmhmwebinar 26

Software Transactions

• Post contract customer support (PCS) • PCS will typically be identified as a performance

obligation. However, the PCS contract may contain additional services (e.g., 24/7 telephone support; “if and when” available upgrade rights and other enhancements or services. • Management will need to evaluate these services

to determine whether they represent separate performance obligations.

#cbizmhmwebinar 27

Software Transactions

• Extended payment terms • Current software guidance contains a rebuttable

presumption that fees due more than 12 months after delivery are not fixed and determinable. Payments are then typically recognized when they come due.

• Topic 606 does not carryforward the same rebuttable presumption related to extended payment terms. However, management will need to determine whether extended payment terms are representative of a significant financing component. If so, the impact of this will be presented separate from revenue as interest expense/income.

#cbizmhmwebinar 28

Sell-Through Method

Existing Guidance • If price is not fixed or

determinable when a sale occurs to a distributor a manufacturer recognizes revenue when product is sold to the end user.

Topic 606 • A manufacturer must

estimate the amount of consideration if it has transferred control of a good or service to the distributor.

#cbizmhmwebinar 29

“Percentage of Completion”

Existing Guidance • Difficult for a

manufacturer to recognize revenue over-time

• Generally a cost-to-cost method is not permissible if the manufacturing process is standardized

Topic 606 • Over-time recognition

is more likely to be acceptable if: • The good does not

have an alternate use for the manufacturer, and

• The manufacturer has a right to payment

#cbizmhmwebinar 30

REVENUE RECOGNITION UPDATE

Upcoming changes to Topic 606

#cbizmhmwebinar 31

Transition Resource Group (TRG)

• FASB has been addressing implementation issues leading to multiple projects: • Deferral of revenue recognition issued in August • Identifying Performance Obligations and Licenses • Narrow-Scope Improvements and Practical Expedients • Principal versus Agent (reporting gross versus net)

#cbizmhmwebinar 32

Identifying Performance Obligations and Licenses

• The FASB recently voted to finalize amendments to the guidance pertaining to licenses of intellectual property (IP) and identifying performance obligations. • Determining the nature of an entity’s promise in granting a

license of IP • The amendments require entities to classify IP in one of

two categories: Functional – IP in this category has standalone

functionality (e.g., many types of software, films, TV, music). Revenue for “functional” licenses is recognized at the point in time when the IP is made available for the customers use and benefit.

#cbizmhmwebinar 33

Identifying Performance Obligations and Licenses • The FASB recently voted to finalize amendments to the

guidance pertaining to licenses of intellectual property (IP) and identifying performance obligations. • Determining the nature of an entity’s promise in granting a

license of IP • The amendments require entities to classify IP in one of

two categories: Symbolic - IP in this category does not have

significant standalone functionality (e.g., brands, team and trade names, character images). Revenue for “symbolic” licenses is recognized over time as the performance obligation is satisfied (e.g., over the license period).

#cbizmhmwebinar 34

Identifying Performance Obligations and Licenses

• Identifying performance obligations • Identifying promised goods and services.

• The amendments provide management with the ability to disregard promises that are deemed to be immaterial in the context of the contract. Additionally, such promises are not required to be aggregated and evaluated against materiality at the entity level.

• Distinct within the context of the contract • The amendments provide clarification related to when a

promised good or service is “separately identifiable” from other promises in the contract (i.e., considered distinct within the context of the contract).

#cbizmhmwebinar 35

Shipping and Handling

• Shipping and handling • Entities will now be allowed an election to account for

the cost of shipping and handling (after transfer of control of the good) as a fulfillment cost (expense).

• Without the election, management would need to evaluate FOB shipping point arrangements to determine whether shipping represents a performance obligation.

#cbizmhmwebinar 36

Significant Proposed Changes

• Sales tax practical expedient • Permit all sales taxes to be presented net

• Transition practical expedients • Simplify transitioning long term contracts

#cbizmhmwebinar 37

? QUESTIONS

#cbizmhmwebinar 38

If You Enjoyed This Webinar…

Upcoming Courses: • 10/28 & 11/10: Maximizing Tax Savings for Closely Held Companies with the IC-DISC Federal

Export Tax Incentive

• 10/29, 11/3 & 11/4: Eye on Washington: Quarterly Business Tax Update, Q3 2015

• 11/5 & 12/2: Individual Year-End Tax Planning Tips for 2015 and Beyond

• 11/11: Revenue Recognition Updates for Manufacturers

• 12/1 & 12/15: Recent Tax Developments Impacting the Construction Industry

Related Thought Leadership: • MHM’s Revenue Recognition Resources Page

• Narrow Scope Improvements Proposed to Revenue Recognition Guidance

• Top Revenue Recognition Considerations for the Construction Industry

• Principal Versus Agent Changes Proposed to Revenue Recognition Standard

#cbizmhmwebinar 39

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ