week 1 - introduction and balance sheet.pdf

DESCRIPTION

The first week lecture notes of the "Introduction to financial accounting" course offered on Coursera by Wharton School of Business, university of Pennsylvania.TRANSCRIPT

KNOWLEDGE FOR ACTION

Definition of Accounting

• Accounting is a system for recording information about business transactions to provide summary statements of a company's financial position and performance to users who require such information.

• Three sets of books– Financial accounting

• Standardized reports for external stakeholders– Tax accounting

• IRS rules for computing taxes payable– Managerial accounting

• Custom reports for internal decision making

KNOWLEDGE FOR ACTION

What are the financial reporting requirements?

• The Securities and Exchange Commission (SEC) requires periodic financial statement filings:– 10 – K: Annual report – 10 – Q: Quarterly report– 8 – K: Current report (material events)– Must be prepared in accordance with Generally Accepted Accounting Principles

(GAAP)• Periodic filing requirements create much of the “tension” in financial

accounting– Ship goods to a customer in one quarter, collect cash in the next

• When did the sale occur?– Buy equipment in one quarter, use it for the next 23 quarters

• When does the expense occur?

KNOWLEDGE FOR ACTION

Who makes the rules?

• Generally Accepted Accounting Principles (GAAP) established by:– U.S. Congress, but they delegate to:– The SEC, but they delegate to:– Financial Accounting Standards Board (FASB)

• Emerging Issues Task Force (EITF)• American Institute of CPA’s (AICPA)

• International Financial Reporting Standards (IFRS) are established by the IASB and are required in over 70 countries, including the EU– US GAAP is still required for US firms– For intro accounting topics, there is a high degree of overlap in the two standards

• Standard setting is a political process

KNOWLEDGE FOR ACTION

Who is responsible for financial reporting?

• Management is responsible for preparing financial statements– The Audit Committee of the Board of Directors provides oversight of

management’s process– Auditors are hired by the Board to “express an opinion” about whether the

statements are prepared in conformity with GAAP• The SEC and other regulators take action against the firm if any

violations of GAAP or other rules are found• Information intermediaries (stock analysts, institutional investors, the

media) may expose or flee firms with questionable accounting

KNOWLEDGE FOR ACTION

What are the required financial statements?

• Balance Sheet– Financial position (listing of resources and obligations) on a specific date

• Income Statement– Results of operations over a period of time using accrual accounting (i.e.,

recognition tied to business activities)• Statement of Cash Flows

– Sources and uses of cash over a period of time• Statement of Stockholders’ Equity

– Changes in stockholders’ equity over a period of time

KNOWLEDGE FOR ACTION

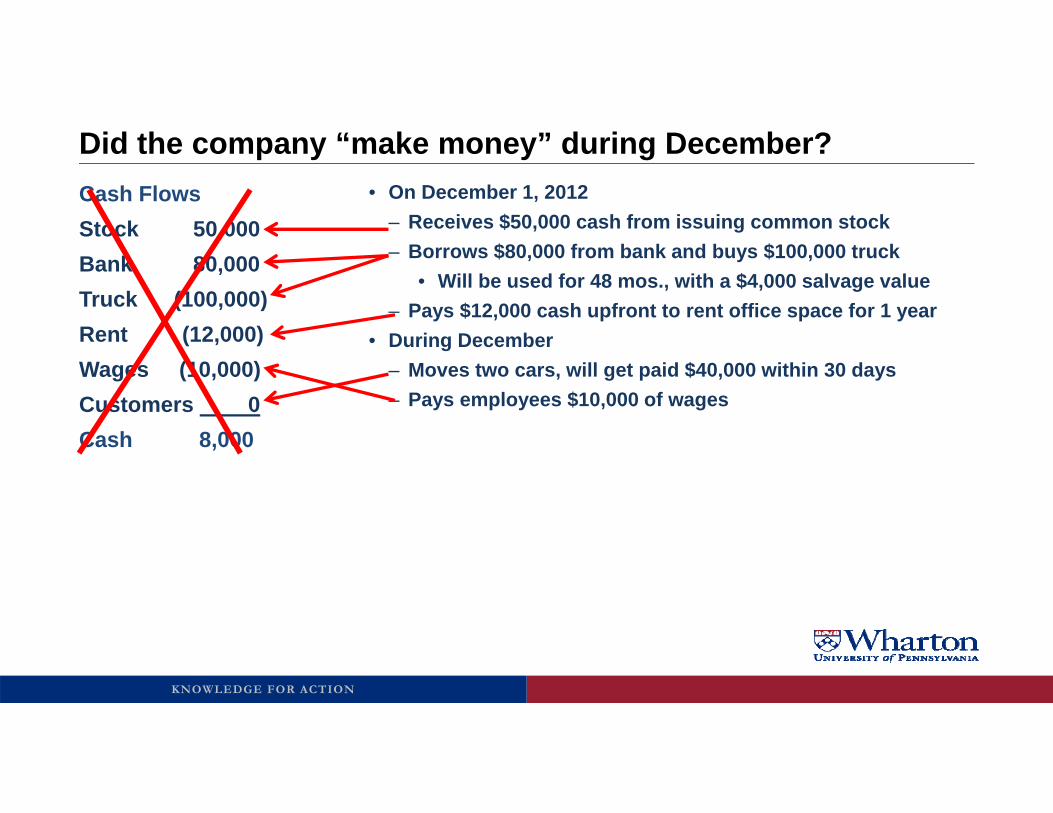

Example: Dave’s Car Transport Service

• Dave starts a business to transport expensive cars• On December 1, 2012

– Receives $50,000 cash from issuing common stock– Borrows $80,000 from bank and buys $100,000 truck

• Will be used for 48 mos., with a $4,000 salvage value – Pays $12,000 cash upfront to rent office space for 1 year

• During December– Moves two cars, will get paid $40,000 within 30 days– Pays employees $10,000 of wages

• December 31: Bank wants to see financial statements

KNOWLEDGE FOR ACTION

Did the company “make money” during December?Cash FlowsStock 50,000Bank 80,000Truck (100,000)Rent (12,000)Wages (10,000)Customers 0Cash 8,000

• On December 1, 2012– Receives $50,000 cash from issuing common stock– Borrows $80,000 from bank and buys $100,000 truck

• Will be used for 48 mos., with a $4,000 salvage value – Pays $12,000 cash upfront to rent office space for 1 year

• During December– Moves two cars, will get paid $40,000 within 30 days– Pays employees $10,000 of wages

KNOWLEDGE FOR ACTION

Did the company “make money” during December?Cash FlowsOperatingRent (12,000)Wages (10,000)Customers 0CFO (22,000)InvestingTruck (100,000)CFI (100,000)FinancingStock 50,000Bank 80,000CFF 130,000Cash 8,000

• On December 1, 2012– Receives $50,000 cash from issuing common stock– Borrows $80,000 from bank and buys $100,000 truck

• Will be used for 48 mos., with a $4,000 salvage value – Pays $12,000 cash upfront to rent office space for 1 year

• During December– Moves two cars, will get paid $40,000 within 30 days– Pays employees $10,000 of wages

KNOWLEDGE FOR ACTION

Statement of Cash FlowsDec 2012 Cash FlowsOperatingRent (12,000)Wages (10,000)Customers 0CFO (22,000)InvestingTruck (100,000)CFI (100,000)FinancingStock 50,000Bank 80,000CFF 130,000Cash 8,000

• Reports cash transactions over a period of time

• Operating Activities– Transactions related to the provision of goods or

services and other normal business activities

• Investing Activities– Transactions related to the acquisition or disposal of

long-lived productive assets

• Financing Activities– Transactions related to owners or creditors

KNOWLEDGE FOR ACTION

Did the company “make money” during December?Accounting IncomeRevenue 40,000Truck Expense (2,000)Rent Expense (1,000)Wages Expense (10,000)Net Income 27,000

Notes: Truck expense (“depreciation”) = (100,000-4,000)/48

Rent expense is one month at $1000/mo.

• On December 1, 2012– Receives $50,000 cash from issuing common stock– Borrows $80,000 from bank and buys $100,000 truck

• Will be used for 48 mos., with a $4,000 salvage value – Pays $12,000 cash upfront to rent office space for 1 year

• During December– Moves two cars, will get paid $40,000 within 30 days– Pays employees $10,000 of wages

KNOWLEDGE FOR ACTION

Income StatementDec 2012 Accounting IncomeRevenue 40,000Truck Expense (2,000)Rent Expense (1,000)Wages Expense (10,000)Net Income 27,000

Notes: Truck expense (“depreciation”) = (100,000-4,000)/48

Rent expense is one month at $1000/mo.

• Reports results of operations over a period of time using accrual accounting– Recognition tied to business activities

• Revenues– Increases in “owners’ equity” from providing goods or

services

• Expenses– Decreases in “owners’ equity” incurred in the process

of generating revenues

• Net Income (or Earnings or Net Profit)= Revenues – Expenses

=> DOES NOT EQUAL CHANGE IN CASH!!!

KNOWLEDGE FOR ACTION

Did the company “make money” during December?Dec 2012 Accounting IncomeRevenue 40,000Truck Expense (2,000)Rent Expense (1,000)Wages Expense (10,000)Net Income 27,000

Notes: Truck expense (“depreciation”) = (100,000-4,000)/48

Rent expense is one month at $1000/mo.

Dec 2012 Cash FlowsOperatingRent (12,000)Wages (10,000)Customers 0CFO (22,000)InvestingTruck (100,000)CFI (100,000)FinancingStock 50,000Bank 80,000CFF 130,000Cash 8,000

KNOWLEDGE FOR ACTION

What is financial position at end of the month?Balance SheetAssetsCash 8,000 (Cash in the bank on 12/31/2012)Accounts Receivable 40,000 (Cash owed by customers on 12/31/2012)Prepaid Rent 11,000 (Prepaid for 11 months of future space on 12/31/2012)Truck 98,000 (100,000 original cost – 2,000 “depreciation”)

Total 157,000Liabilities & Stockholder’s EquityBank Debt 80,000 (Cash owed to the bank on 12/31/2012)Common Stock 50,000 (Stockholder investment as of 12/31/2012)Retained Earnings 27,000 (Accounting Net income – Dividends as of 12/31/2012)Total 157,000

KNOWLEDGE FOR ACTION

Balance SheetDec 12, 2012 Balance SheetAssetsCash 8,000 Accounts Receivable 40,000 Prepaid Rent 11,000Truck 98,000

Total 157,000Liabilities & Stockholder’s EquityBank Debt 80,000 Common Stock 50,000 Retained Earnings 27,000Total 157,000

• Reports financial position (resources and obligations) on a specific date

• Assets– Resources owned by a business that are

expected to provide future economic benefits

• Liabilities– Claims on assets by “creditors” (non-owners)

that represent an obligation to make future payment of cash, goods, or services

• Stockholders’ Equity (Owners’ Equity)– Claims on assets by owners of business

• Contributed Capital (arises from sale of shares)• Retained Earnings (arises from operations)

KNOWLEDGE FOR ACTION

Statement of Stockholders’ Equity

• We’ll get to this later…

KNOWLEDGE FOR ACTION

Review: Required financial statements

• Balance Sheet– Financial position (listing of resources and obligations) on a specific date

• Income Statement– Results of operations over a period of time using accrual accounting (i.e.,

recognition tied to business activities)• Statement of Cash Flows

– Sources and uses of cash over a period of time• Statement of Stockholders’ Equity

– Changes in stockholders’ equity over a period of time

KNOWLEDGE FOR ACTION

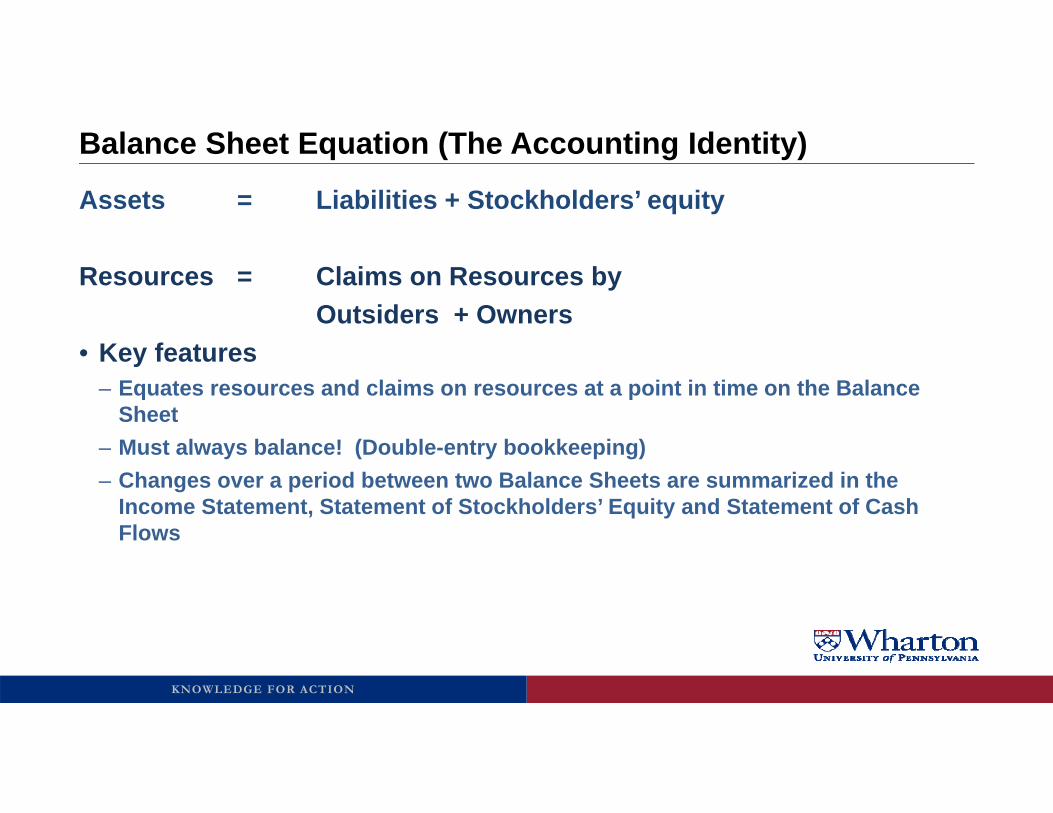

Balance Sheet Equation (The Accounting Identity)

Assets = Liabilities + Stockholders’ equity

Resources = Claims on Resources byOutsiders + Owners

• Key features– Equates resources and claims on resources at a point in time on the Balance

Sheet– Must always balance! (Double-entry bookkeeping)– Changes over a period between two Balance Sheets are summarized in the

Income Statement, Statement of Stockholders’ Equity and Statement of Cash Flows

KNOWLEDGE FOR ACTION

Financial Statements

Balance Sheet at 12/31/11Assets = Liabilities + Stockholders’ equityCash + Noncash assets = Liabilities + Contributed Capital + Retained Earnings

Cash + Noncash assets = Liabilities + Contributed Capital + Retained Earnings

Assets = Liabilities + Stockholders’ equityBalance Sheet at 12/31/12

Statement of Cash Flowsfor year ended 12/31/12

Income Statementfor year ended 12/31/12

Statement of SEfor year ended 12/31/12

KNOWLEDGE FOR ACTION

Complete Balance Sheet Equation

Assets = Liabilities + Stockholders’ equity

Stockholders’ Equity = Contributed Capital + Retained Earnings

Retained Earnings = Prior Retained Earnings + Net Income – Dividends

Net Income = Revenues – Expenses

Assets = Liabilities + Contributed Capital + Prior Retained Earnings + Revenues – Expenses – Dividends

KNOWLEDGE FOR ACTION

Using the Balance Sheet equation

• Assets = 100, Liabilities = 50. What is Stockholders’ Equity?

• Liabilities increase by 100 and Stockholders’ Equity is unchanged. What is the change in Assets?

• All noncash assets = 70, Total Liabilities = 60, Total Stockholders’ Equity = 30. What is Cash?

• Cash decreases by 10 and noncash Assets increase by 15. What is the change in Liabilities?

KNOWLEDGE FOR ACTION

Using the Balance Sheet equation

• Retained Earnings increase by 100, Dividends = 50. What is Net Income?

• Revenue increases by 100 and all other categories are unchanged, except Assets. What is the change in Assets?

• Expenses increase by 60 and all other categories are unchanged, except Cash. What is the change in Cash?

KNOWLEDGE FOR ACTION

Assets

• An asset is a resource that is expected to provide future economic benefits (i.e. generate future cash inflows or reduce future cash outflows)

• An asset is recognized when:– It is acquired in a past transaction or exchange– The value of its future benefits can be measured with a reasonable degree of

precision

KNOWLEDGE FOR ACTION

Which of the Following are Assets?

• BOC sells $100,000 of merchandise to a customer that promises to pay cash within 60 days

• BOC signs a contract to deliver $100,000 of natural gas to DEF each month for the next year

• BOC buys $100,000 of chemicals to be used as raw materials, with payment made in time to secure a 2% discount on the purchase price.

• BOC pays $12 million for the annual rent on its office building. It has already occupied it for one month.

• BOC buys a piece of land for $100,000. Its broker says this was a “steal” because the land is probably worth $150,000.

• BOC is advised by a marketing firm that its brand name is worth $63 million

KNOWLEDGE FOR ACTION

Liabilities

• A liability is a claim on assets by “creditors” (non-owners) that represents an obligation to make future payment of cash, goods, or services

• A liability is recognized when:– The obligation is based on benefits or services received currently or in the past– The amount and timing of payment is reasonably certain

KNOWLEDGE FOR ACTION

Which of the Following are Liabilities?

• BOC receives $300,000 of raw materials from its supplier and promises to pay within 60 days

• Based on this quarter’s operations, BOC estimates that it owes the IRS $3 million in taxes

• BOC signs a three-year, $120 million contract to hire Al Dokes as its new CEO, starting next month

• BOC has not yet paid employees who earned salaries of $1,000,000 during the most recent pay period

• BOC borrows $500,000 from a bank on a one-year note with a 10% interest rate

• BOC is sued by a group of customers who claim their products were defective. The suit claims damages of $6 million.

KNOWLEDGE FOR ACTION

Stockholders’ Equity

• Stockholders’ equity is the residual claim on assets after settling claims of creditors (= assets – liabilities)– Also called “net worth”, “net assets”, “net book value”

• Sources of Stockholders’ equity:– Contributed capital (arises from sale of shares)

• Common stock (par value)• Add’l paid-in-capital (excess over par value)• Treasury Stock (stock repurchased by company)

– Retained earnings (arises from operations)• Accumulation of net income (revenues minus expenses), less dividends, since start of

business• Retained EarningsEND =

Retained EarningsBEG + Net Income – Dividends

KNOWLEDGE FOR ACTION

Stockholders’ Equity Issues

• Dividends– Distributions of retained earnings to shareholders

• Not an expense• Recorded as a reduction of retained earnings on the declaration date (creates a liability

until payment date)

• Statement of Stockholders’ Equity– Required financial statement– Reports changes in stockholders’ equity over a period of time

KNOWLEDGE FOR ACTION

Three Fundamental Bookkeeping Equations

Assets = Liabilities + Stockholders’ Equity

Sum of Debits = Sum of Credits

Beginning account balance + Increases - Decreases = Ending account balance

• These equations must be in balance at all times!• The balance sheet equation can be preserved through the use of

“debits” and “credits”• Definitions of Debit and Credit:

– Debit (Dr.) = Left-side Entry– Credit (Cr.) = Right-side Entry

KNOWLEDGE FOR ACTION

Debit/Credit Bookkeeping

Assets = Liabilities + Shareholders’ EquityAssets = Liabilities + Contrib. Capital + Retained Earnings + Revenues – Expenses Assets + Expenses = Liabilities + Contrib. Capital + Retained Earnings + Revenues

Debits = Credits

• Rules of Debits and Credits:– Every transaction must have at least one debit and at least one credit– Debits must equal credits for all transactions– No negative numbers are allowed

KNOWLEDGE FOR ACTION

Accounts and Account Balances

• Normal Balance – The type of balance (debit or credit) the account carries under normal

circumstances• T Account

– A record of all changes in an accounting quantity– Debits are listed on the left side of the T – Credits are listed on the right side of the T

• Account Balance– Difference between sum of debits and sum of credits for the account

• Change in Account Balance Equation:– Beginning Balance + Increases - Decreases = Ending Balance

KNOWLEDGE FOR ACTION

Normal Balances and T-accounts

• Assets, Expenses– Normal Balance is Debit (Left side of T) – Increases through Debits (Left entries)– Decreases through Credits (Right entries)– Beginning (Debit) Balance + Debits - Credits = Ending (Debit) Balance

Accounts Receivable (A)

Beg. Balance 1,000

New Sales (Increase) 100 80 Cash Collections (Decrease)

End. Balance 1,020

KNOWLEDGE FOR ACTION

Normal Balances and T-accounts

• Liabilities, Stockholders' Equity, Revenues– Normal Balance is Credit (Right side of T) – Decreases through Debits (Left entries)– Increases through Credits (Right entries)– Beginning (Credit) Balance + Credits - Debits = Ending (Credit) Balance

Accounts Payable (L)

1,000 Beg. Balance

Cash Payments (Decrease) 80 100 New Purchases (Increase)

1,020 End. Balance

KNOWLEDGE FOR ACTION

Super T-account

Assets LiabilitiesContributed

Capital

Assets Liabilities & Stockholders’ Equity

RevenuesExpenses

Retained Earnings

Dr.+

Cr.-

Dr.-

Cr.+

Dr.-

Cr.+

Cr.+

Dr.-

Cr.+

Dr.-

Cr.-

Dr.+

KNOWLEDGE FOR ACTION

Analyzing Transactions & Journal Entries

• Three questions in analyzing transactions– Which specific asset, liability, stockholders' equity, revenue or expense accounts

does the transaction affect?– Does the transaction increase or decrease the affected accounts?– Should the accounts be debited or credited?

• Journal entry formatDr. <Name of Account Debited> $XXX

Cr. <Name of Account Credited> $XXX• Always list Debits first and always indent Credits

KNOWLEDGE FOR ACTION

Bookkeeping Examples - I

• Increase an asset and increase a liability or equity– Receive $100 cash from a bank loan

• Balance Sheet EquationAssets = Liabilities + Equity100 = 100 + 0

• Journal EntryDr. Cash (+A) 100

Cr. Notes Payable (+L) 100• T - accounts

Cash (A)100 100

Notes Payable (L)

Bal. 100 100 Bal.

KNOWLEDGE FOR ACTION

Bookkeeping Examples - II

• Decrease an asset and decrease a liability or equity– Repay $20 of a bank loan

• Balance Sheet EquationAssets = Liabilities + Equity(20) = (20) + 0

• Journal EntryDr. Notes Payable (-L) 20

Cr. Cash (-A) 20• T - accounts

Cash (A)20

Notes Payable (L)20100 100

Bal. 80 80 Bal.

KNOWLEDGE FOR ACTION

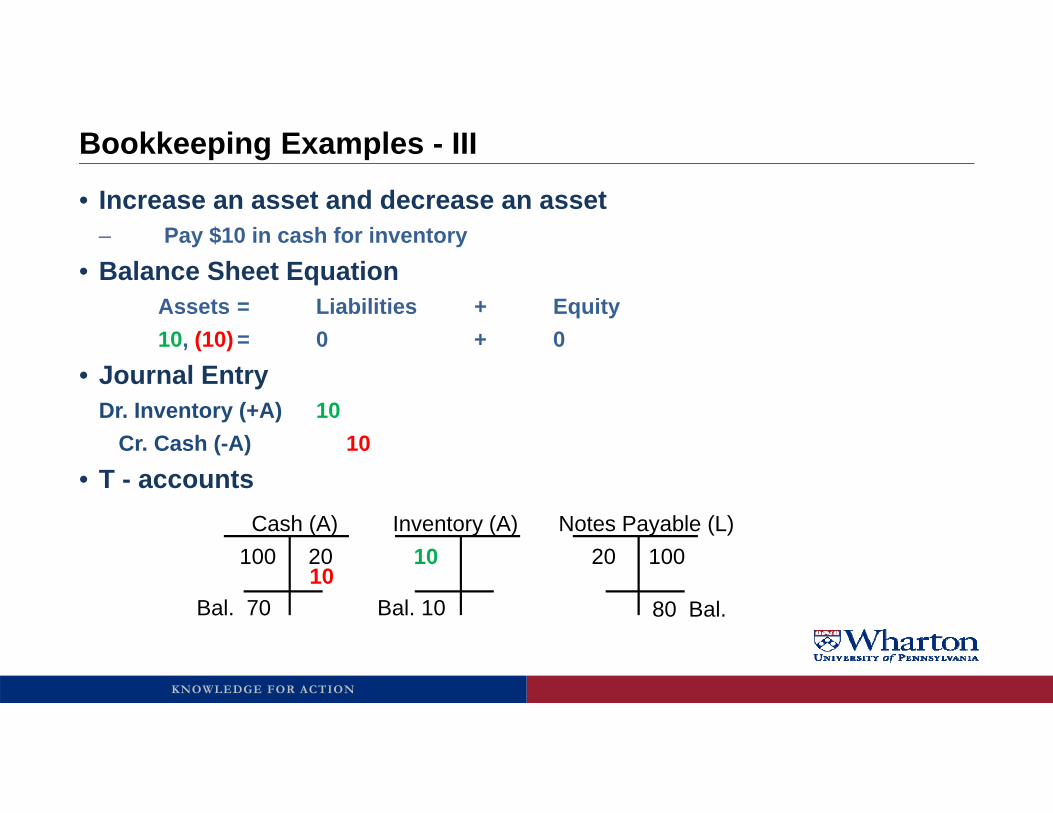

Bookkeeping Examples - III

• Increase an asset and decrease an asset– Pay $10 in cash for inventory

• Balance Sheet EquationAssets = Liabilities + Equity10, (10) = 0 + 0

• Journal EntryDr. Inventory (+A) 10

Cr. Cash (-A) 10• T - accounts

10

Inventory (A)10

Cash (A)20100

Bal. 70 Bal. 10

Notes Payable (L)20 100

80 Bal.

KNOWLEDGE FOR ACTION

Bookkeeping Examples - IV

• Increase a liability or equity and decrease another liability or equity– Issue $80 in Common Stock to pay off the bank loan

• Balance Sheet EquationAssets = Liabilities + Equity0 = (80) + 80

• Journal EntryDr. Notes Payable (-L) 80

Cr. Common Stock (+SE) 80• T - accounts

80

Common Stock (SE)80

Notes Payable (L)20 100

0 Bal. 80 Bal.10

Inventory (A)10

Cash (A)20100

Bal. 70 Bal. 10

KNOWLEDGE FOR ACTION

What is the Journal Entry?

1. BOC issues 10,000 shares of $5 par value stock for $15 cash per share

2. BOC acquires a building costing $500,000. It pays $80,000 cash and assumes a long-term mortgage for the balance of the purchase price

3. BOC obtains a 3-year fire insurance policy and pays the $3,000 premium in advance

KNOWLEDGE FOR ACTION

What is the Journal Entry?

4. BOC acquires on account office supplies costing $20,000 and merchandise inventory costing $35,000

5. BOC pays $22,000 to the suppliers above

6. BOC exchanges a building valued on the books at $200,000 for a piece of undeveloped land

KNOWLEDGE FOR ACTION

What is the Journal Entry?

7. BOC retires $1,000,000 of debt by issuing 100,000 shares of $5 par value stock

8. BOC receives an order for $6,000 of merchandise to be shipped next month. The customer pays $600 at the time of placing the order.

9. BOC declares and pays $8,000 of cash dividends

KNOWLEDGE FOR ACTION

Quick Review

• Journal entries and T-accounts are used to track the effects of transactions• Sum of Debits = Sum of Credits=> Assets = Liabilities + Stockholders’ Equity

• Debit = left-side entry; Credit = right-side entry– Assets and Expenses have Debit balances

• Debits increase assets and expenses• Credits decrease these accounts

– Liabilities, Shareholders’ Equity and Revenues have Credit balances• Credits increase liabilities, shareholders’ equity, and revenues • Debits decrease these accounts

KNOWLEDGE FOR ACTION

Quick Review: Super T-account

Assets LiabilitiesContributed

Capital

Assets Liabilities & Shareholders’ Equity

Revenues

Retained Earnings

Dr.+

Cr.-

Dr.-

Cr.+

Dr.-

Cr.+

Cr.+

Dr.-

Cr.+

Dr.-

Cr.-

Dr.+

Expenses

KNOWLEDGE FOR ACTION

The Accounting Cycle

AnalyzeTransactions

Journalizeand Post

AdjustingEntries

FinancialStatements

ClosingEntries

During PeriodStart new period

UnadjustedTrial Balance

AdjustedTrial Balance

End of Period

KNOWLEDGE FOR ACTION

The Accounting Cycle

AnalyzeTransactions

Journalizeand Post

During Period

1. Journalize: recording each transaction as a journal entry in the general journal

2. Post: journal entries are transferred to the T-accounts or general ledger.

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case

• In March 2012, Rebecca Park identified an excellent business opportunity while she was a first-year MBA student at Wharton.

• She read a story about an MBA student who tripped while jogging in Fairmount Park and found an ancient gold coin in the underbrush. It was an old Viking coin that was appraised at $77,500.

• She realized that she could set up a profitable business that rented out portable Metal Detectors to people that wanted to search Fairmount Park for more Viking relics.

• Also, Park had the idea of stocking her store with “sundries,” such as water bottles and energy bars, that she could sell at a huge mark-up to renters before their expedition into the park.

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case

• Park prepared a business plan and approached a fellow student, Jay Girard, who had a sizable trust fund and who she believed would invest in this new venture.

• Due to his myriad of other investments, and his heavy course load, Girard agreed to invest as a silent partner and allow Park to run the business, which she named Relic Spotter Inc.

• We will now record journal entries and post to t-accounts for all of the transactions of this start-up company.

• After each transaction is read, you should pause the video and try to do the journal entry. Think about (1) what accounts are involved? (2) did they increase or decrease? (3) do we debit or credit?

• Then, resume the video to see the answer and the explanation.

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 1

• (1) On April 1, 2012, Girard decided to invest $200,000 and Park put up $50,000 to purchase a total of 25,000 shares in the new company. The par value of the shares was $1.00.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 2

• (2) Lacking the funds for her initial investment, Park borrowed the $50,000 from the Imperial Bank of Philadelphia on April 1, using her parent’s house as collateral.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 3

• (3) On April 2, Park hired a lawyer to have the business incorporated. Because this was a fairly simple organization, the legal fees were only $5,100.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 4

• (4) To house the business, Park bought an abandoned pizza parlor near Fairmount Park for $155,000 on April 7. The building was old and needed renovation work. The purchase documents allocated $103,000 to the land and $52,000 to the building. Park paid for the building with $31,000 cash and a $124,000 mortgage from the Imperial Bank.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 5

• (5) Park felt that some renovation work would extend the life of the building to 25 years (with an expected salvage value of $10,000). She ordered the renovation work, costing $33,000, to begin immediately. The work was completed on May 25, at which time she paid in cash the amount owed for the renovations.

• Journal Entry

KNOWLEDGE FOR ACTION

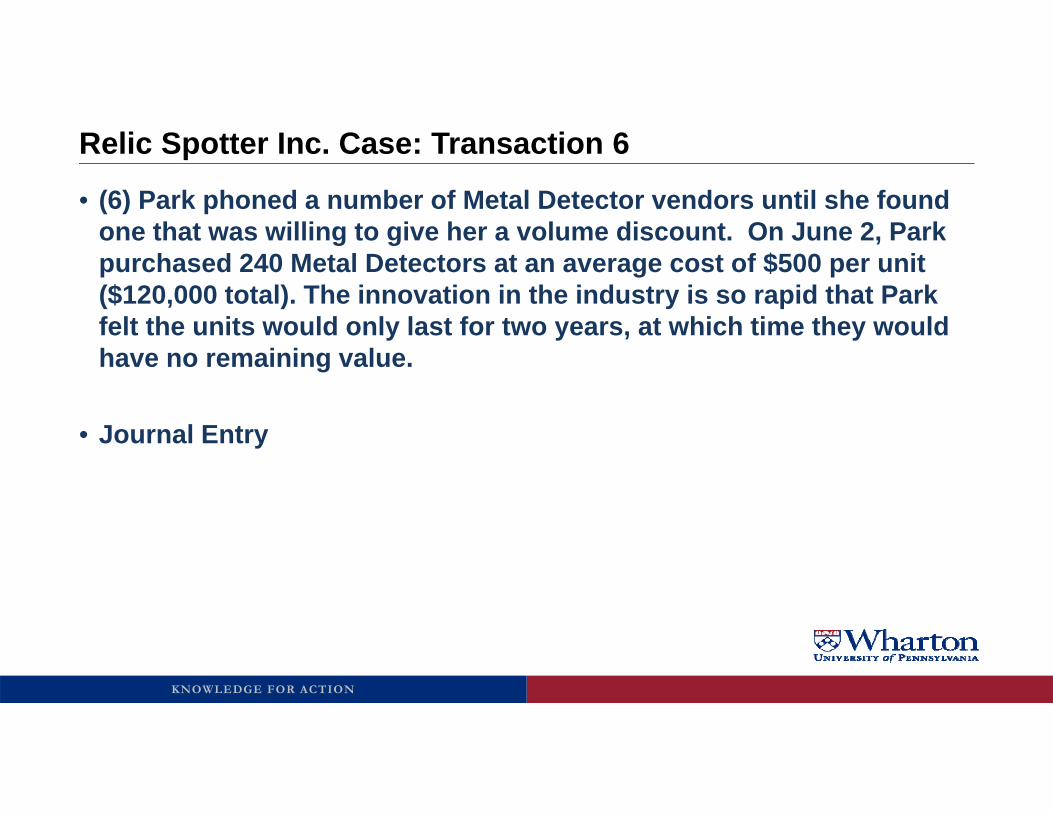

Relic Spotter Inc. Case: Transaction 6

• (6) Park phoned a number of Metal Detector vendors until she found one that was willing to give her a volume discount. On June 2, Park purchased 240 Metal Detectors at an average cost of $500 per unit ($120,000 total). The innovation in the industry is so rapid that Park felt the units would only last for two years, at which time they would have no remaining value.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 7

• (7) On June 15, Park ordered $2,000 of sundries inventory (e.g., water bottles, energy bars, etc.) to be delivered on June 30. Park was able to purchase the inventory “on account”, which meant she had up to 30 days after delivery to pay the supplier.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 8

• (8) On June 30, Park paid $700 for a site license to use geo-contour mapping software in the Metal Detectors. The license was good for three-years with $700 due to be paid annually (i.e., the total cost over three-years will be $2,100).

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 9

• (9) On June 30, Park signed a contract with a local advertising agency to provide various forms of advertising for a period of one year. She paid $8,000 upfront for advertising through June 30, 2013.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 10

• (10) On June 30, Park needed cash to make a payment on the Imperial Bank loan that funded her purchase of Relic Spotter stock. She borrowed $5,000 from Relic Spotter at 10% interest, with the principal and interest due in a lump sum on June 30, 2013.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 11

• (11) On June 30, Park also hired two employees, Linda Carlyle and Charlotte Cafferly, to run the shop. They signed employment contracts promising each salaries of $32,000 per year.

• Journal Entry

KNOWLEDGE FOR ACTION

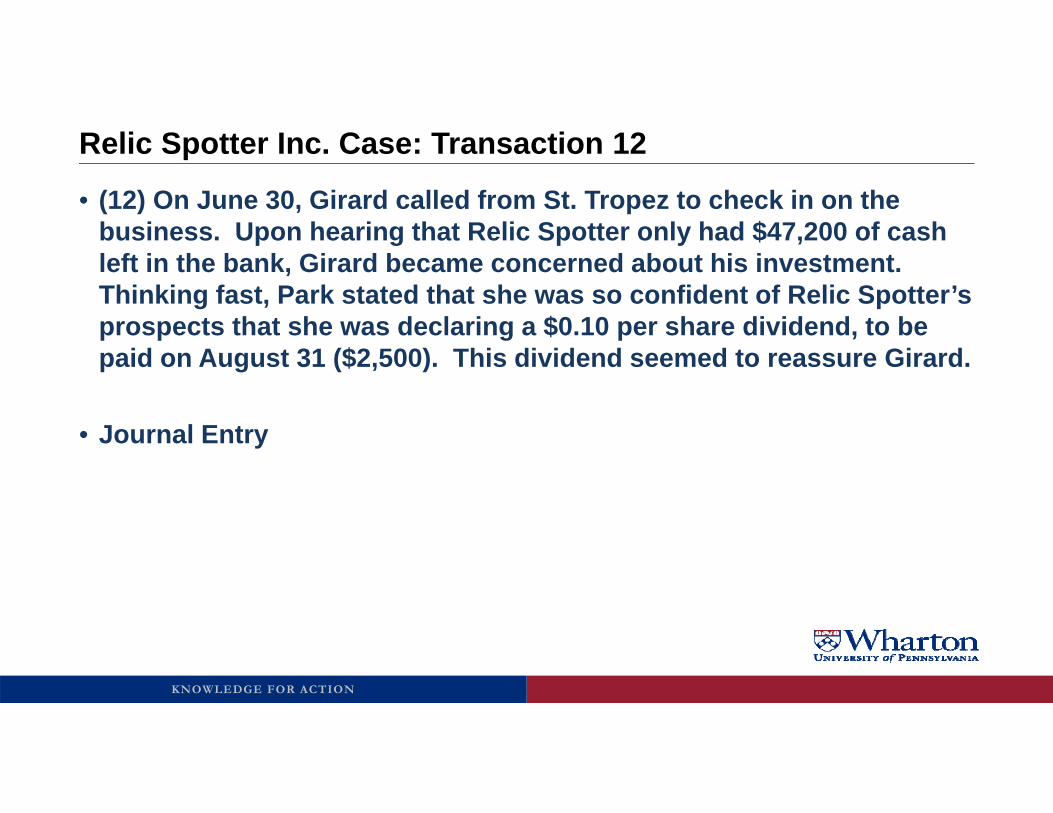

Relic Spotter Inc. Case: Transaction 12

• (12) On June 30, Girard called from St. Tropez to check in on the business. Upon hearing that Relic Spotter only had $47,200 of cash left in the bank, Girard became concerned about his investment. Thinking fast, Park stated that she was so confident of Relic Spotter’s prospects that she was declaring a $0.10 per share dividend, to be paid on August 31 ($2,500). This dividend seemed to reassure Girard.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 13

• (13) Relic Spotter opened for business on July 1, 2012, just in time for the big Independence Day weekend. On July 31, Park paid the supplier the $2,000 it was owed.

• Journal Entry

KNOWLEDGE FOR ACTION

Relic Spotter Inc. Case: Transaction 14

• (14) On August 31, Park paid the $2,500 dividend that had been declared in June.

• Journal Entry

An Introduction to Financial Accounting

Summary of Common Transactions and Accounts

Examples of Common Transactions

• The following slides review the most commonly-used accounts and shows the transactions that generally affect these accounts

• Note that you will learn additional transactions for many of these accounts later on—these are just the basic transactions

• Also, there are additional accounts that we will learn later on—this is the basic set to get you started.

Typical Current Assets

CashMarketable Securities (short-term, liquid investments)Accounts Receivable (amounts owed by customers on sales)Notes Receivable (amounts owed by noncustomers on loans)Interest Receivable (accrued revenue not yet received in cash)Inventory (costs of goods available for sale)Prepaid Expenses (rent, insurance, etc.—deferred expenses)

Accounts Receivable

• Sell products to customersDr. Accounts Receivable (+A) 100

Cr. Sales (+R, +SE) 100• Collect cash from customers

Dr. Cash (+A) 80Cr. Accounts Receivable (-A) 80

Accounts Receivable

Beg. Balance 1,000

Sales (Revenue) 100 80 Collections (Cash)

End. Balance 1,020

Notes Receivable

• Lend moneyDr. Notes Receivable (+A) 100

Cr. Cash (-A) 100• Collect cash principal on loan

Dr. Cash (+A) 100Cr. Notes Receivable (-A) 100

Notes Receivable

Beg. Balance 1,000

Cash payment 100 100 Collect Cash Principal

End. Balance 1,000

Interest Receivable (Accrued Revenue)

• Recognize accrued interest receivable on a loanDr. Interest Receivable (+A) 100

Cr. Interest Revenue (+R , +SE) 100• Collect cash for interest

Dr. Cash (+A) 80Cr. Interest Receivable (-A) 80

Interest Receivable

Beg. Balance 1,000

Accrued Revenue 100 80 Collection in Cash

End. Balance 1,020

Inventory

• Purchase inventoryDr. Inventory (+A) 100

Cr. Accounts Payable (+L) or Cash (-A) 100• Sell inventory

Dr. Cost of Goods Sold (+E , -SE) 80Cr. Inventory (-A) 80

Inventory

Beg. Balance 1,000

Purchases (Cash or AP) 100 80 Sales (COGS Expense)

End. Balance 1,020

Prepaid Expenses

• Pay for rent (or other expense) in advance of useDr. Prepaid Rent (+A) 100

Cr. Cash (-A) 100• Occupy space and recognize expense

Dr. Rent Expense (+E , -SE) 80Cr. Prepaid Rent (-A) 80

Prepaid Rent

Beg. Balance 1,000

Prepayment (Cash) 100 80 Recognize Expense

End. Balance 1,020

Typical Long-Term Assets

Land (tangible asset, not depreciated)Buildings, Equipment (tangible assets that are depreciated)Accumulated Depreciation (contra asset—sum of past

depreciation)Investments (long-term investments)Notes Receivable (could also be noncurrent)Intangible assets (patents, goodwill, etc.)

Land

• Purchase LandDr. Land (+A) 100

Cr. Cash (-A) or Notes payable (+L) 100• Sell Land (assumes no gain or loss on sale)

Dr. Cash (+A) 100Cr. Land (-A) 100

(note: no depreciation on Land)Land

Beg. Balance 1,000

Purchase (Cash or NP) 100 100 Cash Sales (Not Revenue!)

End. Balance 1,000

Buildings & Equipment

• Purchase Buildings & EquipmentDr. Buildings & Equipment (+A) 100

Cr. Cash (-A) or Notes payable (+L) 100• Sell Bldgs & Equip (assumes no gain/loss on sale)

Dr. Cash (+A) 20Dr. Accumulated Depreciation (-XA, +A) 80

Cr. Buildings & Equipment (-A) 100Buildings and Equipment

Beg. Balance 1,000

Purchase (Cash) 100 100 Cash Sales (Not Revenue!)

End. Balance 1,000

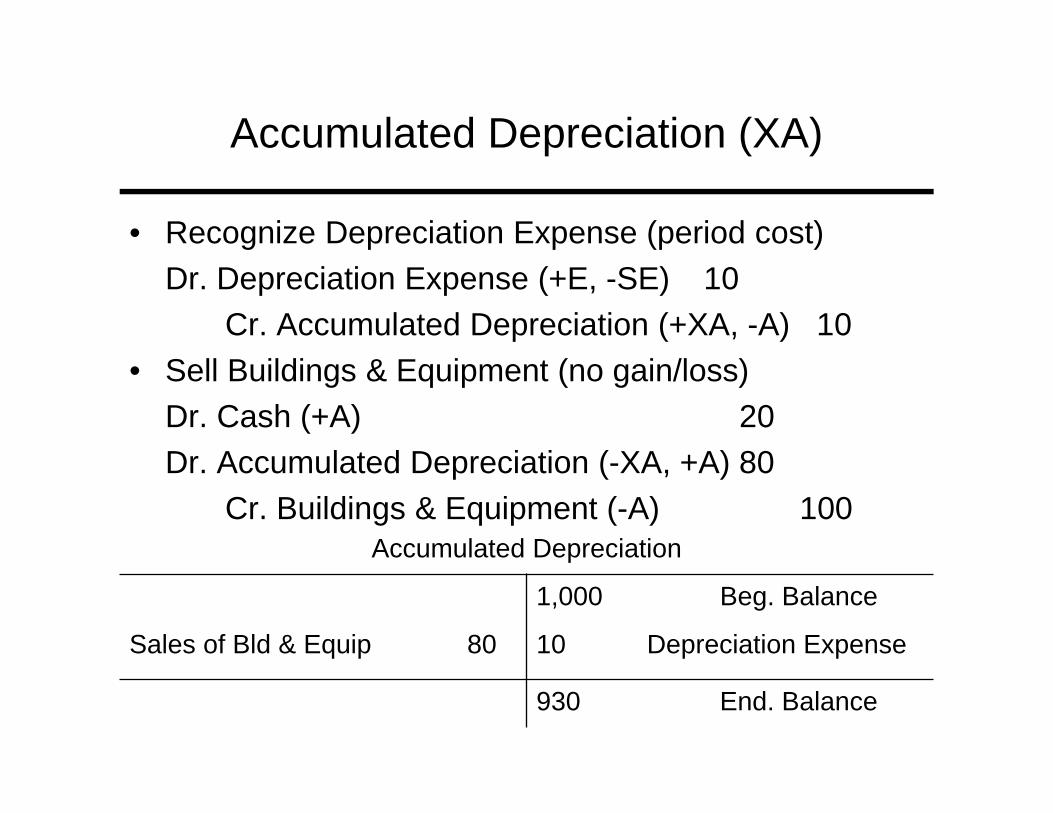

Accumulated Depreciation (XA)

• Recognize Depreciation Expense (period cost)Dr. Depreciation Expense (+E, -SE) 10

Cr. Accumulated Depreciation (+XA, -A) 10• Sell Buildings & Equipment (no gain/loss)

Dr. Cash (+A) 20Dr. Accumulated Depreciation (-XA, +A) 80

Cr. Buildings & Equipment (-A) 100Accumulated Depreciation

1,000 Beg. Balance

Sales of Bld & Equip 80 10 Depreciation Expense

930 End. Balance

Intangible Assets

• Purchase PatentDr. Patent (+A) 100

Cr. Cash (-A) 100• Recognize Amortization Expense (period cost)

Dr. Amortization Expense (+E, -SE) 10Cr. Patent (-A) 10

Patents

Beg. Balance 0

Purchase (Cash) 100 10 Amortization

End. Balance 90

Typical Liabilities

Accounts Payable (amounts owed to suppliers on purchases)Notes Payable (or mortgage payable—amounts owed to

creditors [banks] on loans—could be current or noncurrent)

Accrued Payables (or Accrued Expenses) (wages, salaries, interest, dividends, taxes, warranties, etc.—accrued expenses not yet paid in cash)

Unearned Revenue (also advances from customers—deferred revenues)

Accounts Payable

• Purchase inventory (or another asset) on accountDr. Inventory (+A) 100

Cr. Accounts Payable (+L) 100• Pay cash to supplier

Dr. Accounts Payable (-L) 80Cr. Cash (-A) 80

Accounts Payable

1,000 Beg. Balance

Payments (Cash) 80 100 Purchases (Receive Asset)

1,020 End. Balance

Notes Payable

• Borrow money on a loan from a bank/creditorDr. Cash (+A) 100

Cr. Notes Payable (+L) 100• Pay cash principal to creditor

Dr. Notes Payable (-L) 80Cr. Cash (-A) 80

Notes Payable

1,000 Beg. Balance

Repayments (Cash) 80 100 Receive Cash

1,020 End. Balance

Accrued Payables – Settled in Cash

• Recognized expense for unpaid wages (or other Exp.)Dr. Wages Expense (+E, -SE) 100

Cr. Wages Payable (+L) 100• Pay cash to satisfy liability

Dr. Wages Payable (-L) 80Cr. Cash (-A) 80

Wages Payable

1,000 Beg. Balance

Payments (Cash) 80 100 Recognize Expense

1,020 End. Balance

Accrued Payables – Settled with Goods

• Recognized expense for warranties at time of saleDr. Warranties Expense (+E, -SE) 100

Cr. Warranties Payable (+L) 100• Delivery new inventory to satisfy liability

Dr. Warranties Payable (-L) 80Cr. Inventory (-A) 80

Wages Payable

1,000 Beg. Balance

Deliver inventory 80 100 Recognize Expense

1,020 End. Balance

Unearned Revenues

• Receive cash in advance of delivering goods/servicesDr. Cash (+A) 100

Cr. Unearned Revenue (+L) 100• Recognized revenue upon delivery

Dr. Unearned Revenue (-L) 80Cr. Revenue (+R, +SE) 80

Unearned Revenue

1,000 Beg. Balance

Delivery (Revenue) 80 100 Receive cash

1,020 End. Balance

Typical Stockholders Equity

Common Stock (at Par) (Shares issued times par value)Additional Paid-in-Capital (Shares issued times [market price

– par value])Retained Earnings (Equals prior retained earnings plus

revenues minus expenses minus dividends)

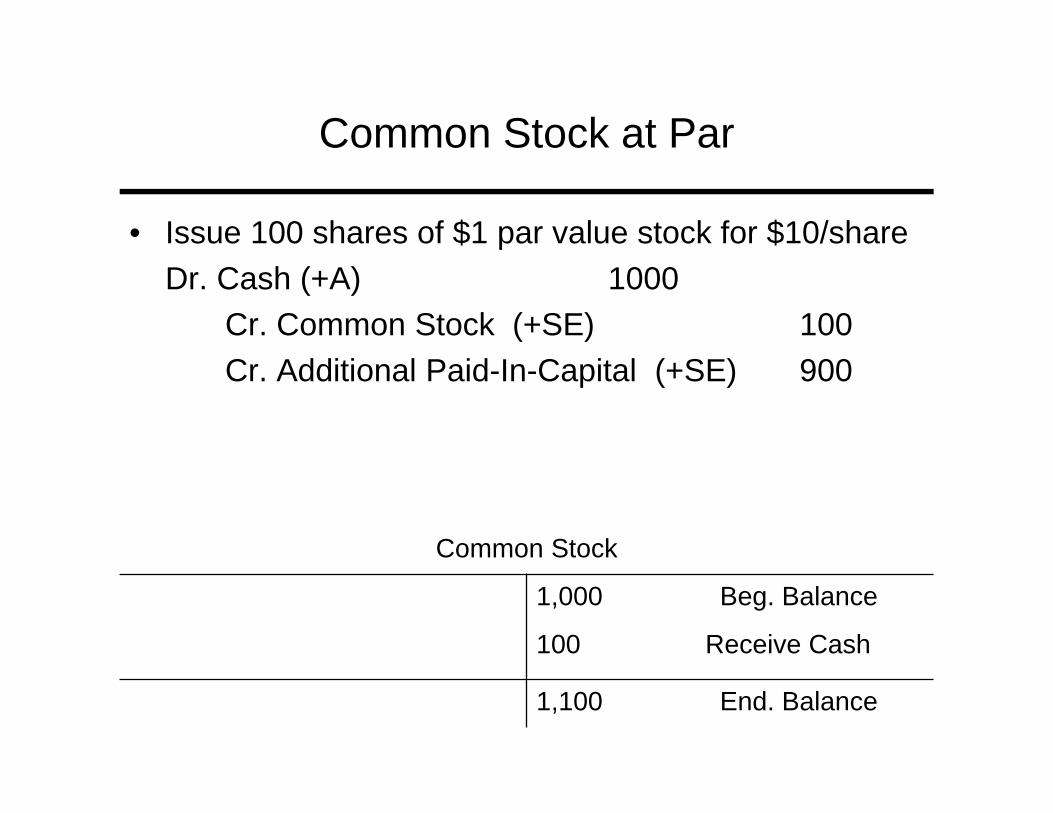

Common Stock at Par

• Issue 100 shares of $1 par value stock for $10/shareDr. Cash (+A) 1000

Cr. Common Stock (+SE) 100Cr. Additional Paid-In-Capital (+SE) 900

Common Stock

1,000 Beg. Balance

100 Receive Cash

1,100 End. Balance

Additional Paid-in-Capital

• Issue 100 shares of $1 par value stock for $10/shareDr. Cash (+A) 1000

Cr. Common Stock (+SE) 100Cr. Additional Paid-In-Capital (+SE) 900

Additional Paid-in-Capital

1,000 Beg. Balance

900 Receive Cash

1,900 End. Balance

Retained Earnings

• Declare dividendsDr. Retained Earnings (-SE) 10

Cr. Cash (-A) or Dividends Payable (+L) 10• Close Revenue accounts

Dr. Revenue Accounts (-R, -SE) 100Cr. Retained Earnings (+SE) 100

• Close Expense accountsDr. Retained Earnings (-SE) 80

Cr. Expense Accounts (-E, +SE) 80

Retained Earnings

Declare dividends 10 1,000 Beg. Balance

Close Expenses 80 100 Close Revenues

1,010 End. Balance