welcome illini bank - ucb: united community bank atm county market 1099 jason pl. gillespie united...

TRANSCRIPT

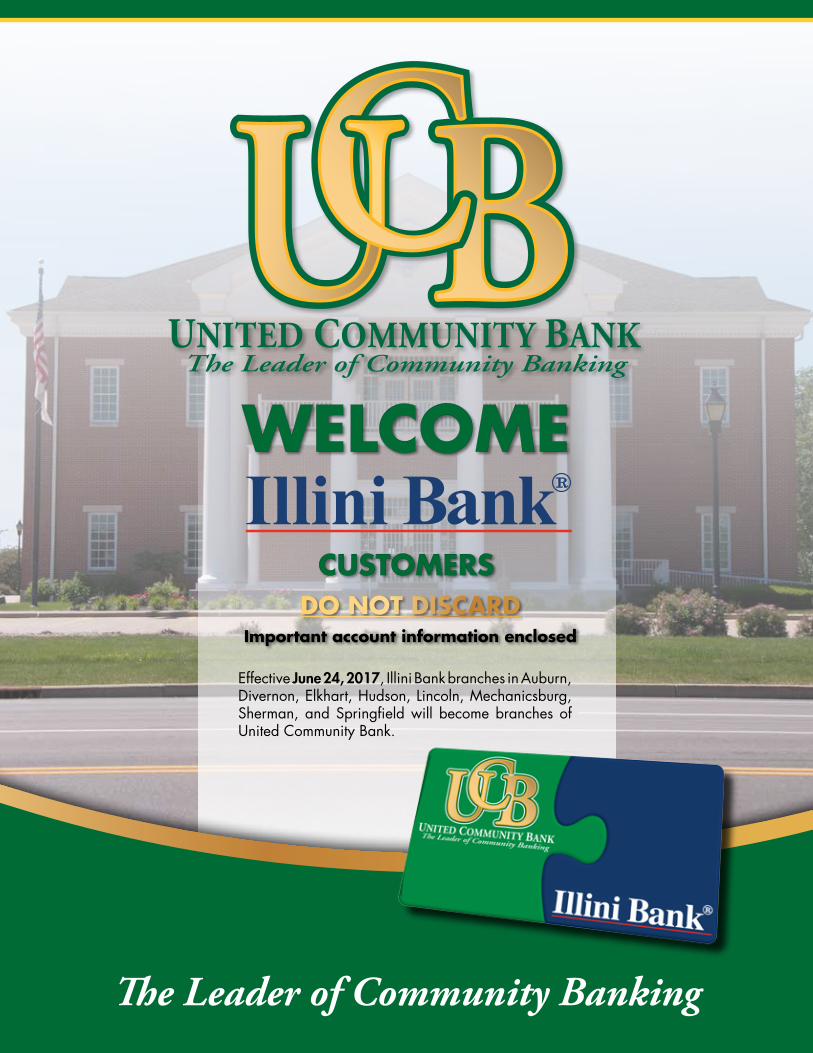

WELCOME

CUSTOMERS

Effective June 24, 2017, Illini Bank branches in Auburn, Divernon, Elkhart, Hudson, Lincoln, Mechanicsburg, Sherman, and Springfield will become branches of United Community Bank.

DO NOT DISCARD

Important account information enclosed

The Leader of Community Banking

Illini BankR

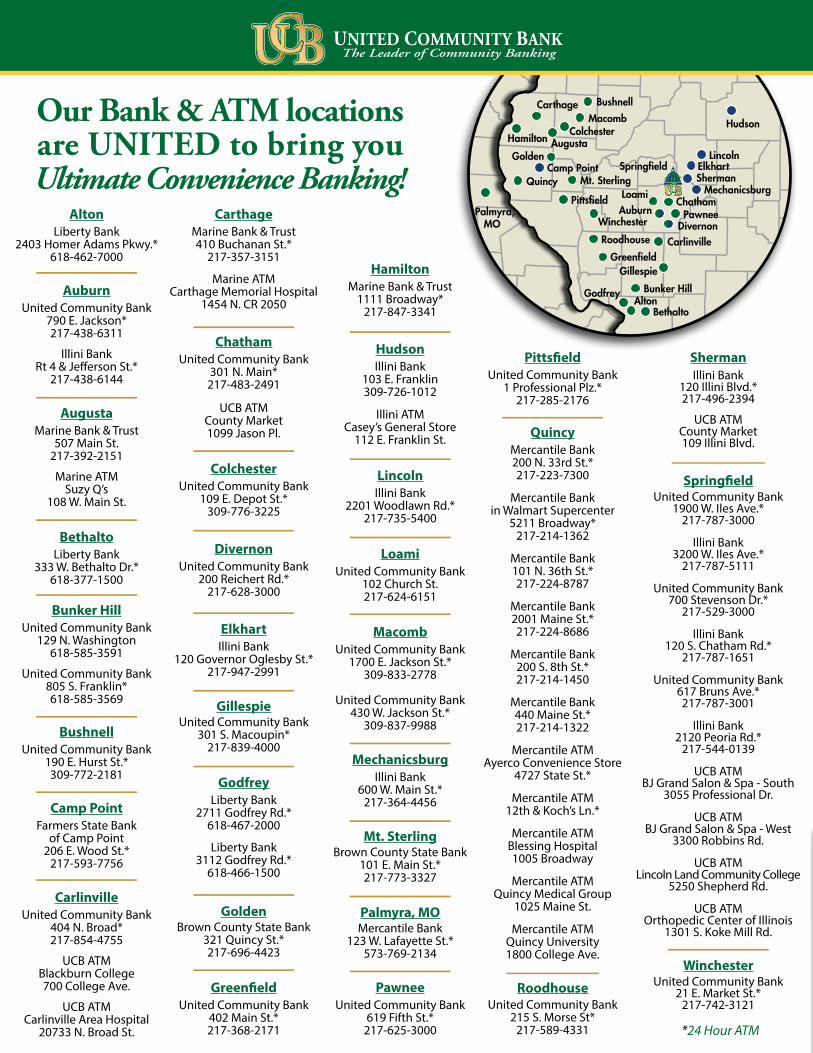

Springfield

Palmyra, MO

HamiltonColchester

Winchester

Carthage

Golden

Quincy

Macomb

Bushnell

Mt. SterlingCamp Point

Augusta

Bunker Hill

Gillespie

CarlinvilleGreenfield

Roodhouse

PittsfieldAuburn

ChathamMechanicsburg

LincolnElkhartSherman

Hudson

Pawnee

Loami

Divernon

AltonBethalto

GodfreyAuburnUnited Community Bank

790 E. Jackson*217-438-6311

Illini BankRt 4 & Jefferson St.*

217-438-6144

Bunker HillUnited Community Bank

129 N. Washington618-585-3591

United Community Bank805 S. Franklin*618-585-3569

ChathamUnited Community Bank

301 N. Main*217-483-2491

UCB ATMCounty Market1099 Jason Pl.

GillespieUnited Community Bank

301 S. Macoupin*217-839-4000

GreenfieldUnited Community Bank

402 Main St.*217-368-2171

LoamiUnited Community Bank

102 Church St.217-624-6151

PawneeUnited Community Bank

619 Fifth St.*217-625-3000

Our Bank & ATM locationsare UNITED to bring youUltimate Convenience Banking!

AugustaMarine Bank & Trust

507 Main St.217-392-2151

Marine ATMSuzy Q’s

108 W. Main St.

BushnellUnited Community Bank

190 E. Hurst St.*309-772-2181

Camp PointFarmers State Bank

of Camp Point206 E. Wood St.*

217-593-7756

CarthageMarine Bank & Trust410 Buchanan St.*

217-357-3151

Marine ATMCarthage Memorial Hospital

1454 N. CR 2050

ColchesterUnited Community Bank

109 E. Depot St.*309-776-3225

DivernonUnited Community Bank

200 Reichert Rd.*217-628-3000

ElkhartIllini Bank

120 Governor Oglesby St.*217-947-2991

CarlinvilleUnited Community Bank

404 N. Broad*217-854-4755

UCB ATMBlackburn College700 College Ave.

UCB ATMCarlinville Area Hospital

20733 N. Broad St.

GoldenBrown County State Bank

321 Quincy St.*217-696-4423

HamiltonMarine Bank & Trust

1111 Broadway*217-847-3341

HudsonIllini Bank

103 E. Franklin309-726-1012

Illini ATMCasey’s General Store

112 E. Franklin St.

LincolnIllini Bank

2201 Woodlawn Rd.*217-735-5400

MacombUnited Community Bank

1700 E. Jackson St.*309-833-2778

United Community Bank430 W. Jackson St.*

309-837-9988

MechanicsburgIllini Bank

600 W. Main St.*217-364-4456

Mt. SterlingBrown County State Bank

101 E. Main St.*217-773-3327

Palmyra, MOMercantile Bank

123 W. Lafayette St.*573-769-2134

PittsfieldUnited Community Bank

1 Professional Plz.*217-285-2176

QuincyMercantile Bank200 N. 33rd St.*217-223-7300

Mercantile Bankin Walmart Supercenter

5211 Broadway*217-214-1362

Mercantile Bank101 N. 36th St.*217-224-8787

Mercantile Bank2001 Maine St.*217-224-8686

Mercantile Bank200 S. 8th St.*217-214-1450

Mercantile Bank440 Maine St.*217-214-1322

Mercantile ATMAyerco Convenience Store

4727 State St.*

Mercantile ATM12th & Koch’s Ln.*

Mercantile ATMBlessing Hospital1005 Broadway

Mercantile ATMQuincy Medical Group

1025 Maine St.

Mercantile ATMQuincy University1800 College Ave.

*24 Hour ATM

RoodhouseUnited Community Bank

215 S. Morse St*217-589-4331

ShermanIllini Bank

120 Illini Blvd.*217-496-2394

UCB ATMCounty Market109 Illini Blvd.

SpringfieldUnited Community Bank

1900 W. Iles Ave.*217-787-3000

Illini Bank3200 W. Iles Ave.*

217-787-5111

United Community Bank700 Stevenson Dr.*

217-529-3000

Illini Bank120 S. Chatham Rd.*

217-787-1651

United Community Bank617 Bruns Ave.*217-787-3001

Illini Bank2120 Peoria Rd.*

217-544-0139

UCB ATMBJ Grand Salon & Spa - South

3055 Professional Dr.

UCB ATMBJ Grand Salon & Spa - West

3300 Robbins Rd.

UCB ATMLincoln Land Community College

5250 Shepherd Rd.

UCB ATMOrthopedic Center of Illinois

1301 S. Koke Mill Rd.

WinchesterUnited Community Bank

21 E. Market St.*217-742-3121

GodfreyLiberty Bank

2711 Godfrey Rd.*618-467-2000

Liberty Bank3112 Godfrey Rd.*

618-466-1500

BethaltoLiberty Bank

333 W. Bethalto Dr.*618-377-1500

AltonLiberty Bank

2403 Homer Adams Pkwy.*618-462-7000

Todd W. WisePresident & CEO

Robert A. NarmontChairman of the Board

Todd W. WisePresident & CEO

Welcome to the UCB family! United Community Bank offers many innovative products, outstanding customer service and the latest in online and mobile banking technology to accommodate all of your banking needs. We have always believed in local decision making, delegated authority and giving back to the communities that we serve. We have maintained this hometown community banking philosophy since 1973.

UCB is 100% employee-owned. We answer to no outside group, allowing us to make smart decisions that provide the best possible services and products to our customers.

UCB’s staff will work hard to make this transition as smooth and seamless as possible. We hope this book will be a valuable resource to help guide you through this process by providing information regarding changes to your current accounts, as well as outlining the features and benefits of additional products and services.

Inside this book you will find important information regarding:• Changes to your checking and savings accounts• Mailing of your new debit card and additional debit card options• Set-up for Online Banking, Online BillPay and more

We appreciate your business and are pleased to have the opportunity to serve you. We invite you to stop by any of our locations and meet us. Please do not hesitate to contact any of our staff if you have any questions or need assistance.

Welcome to our family!

Sincerely,

Matt SemanSenior Vice President

Robert A. NarmontChairman of the Board

Matt SemanSenior Vice President

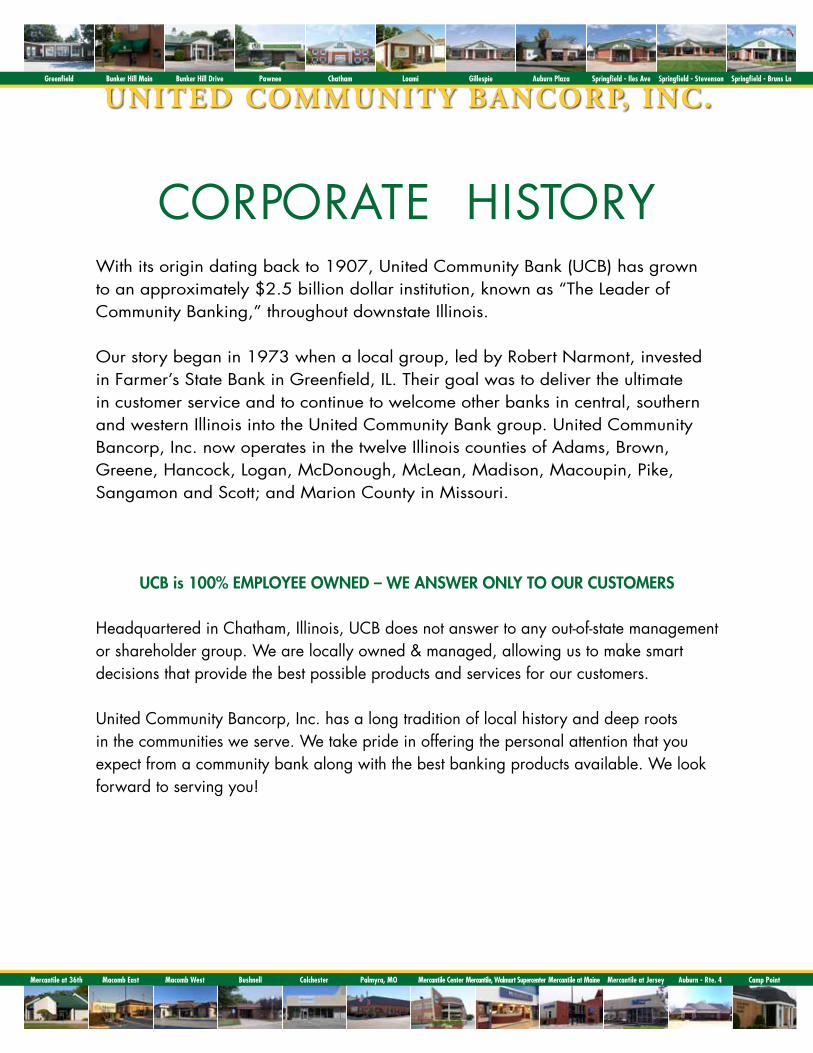

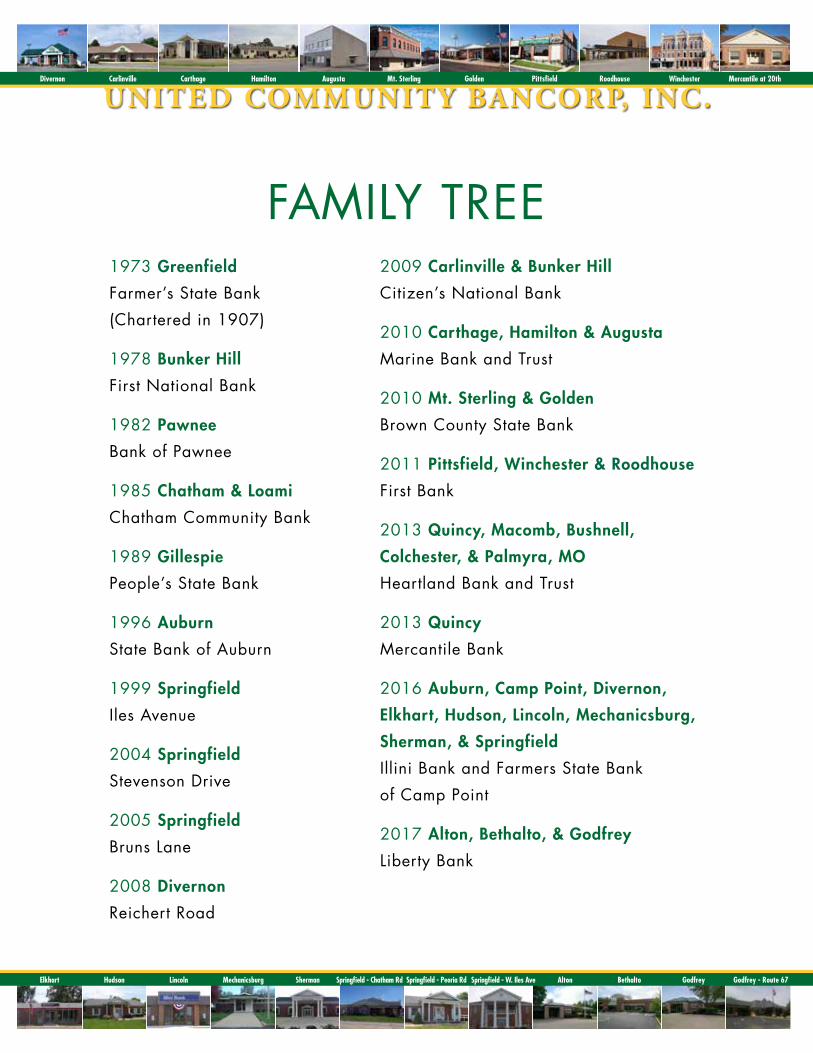

UNITED COMMUNITY BANCORP, INC.

CORPORATE HISTORYWith its origin dating back to 1907, United Community Bank (UCB) has grown to an approximately $2.5 billion dollar institution, known as “The Leader of Community Banking,” throughout downstate Illinois.

Our story began in 1973 when a local group, led by Robert Narmont, invested in Farmer’s State Bank in Greenfield, IL. Their goal was to deliver the ultimate in customer service and to continue to welcome other banks in central, southern and western Illinois into the United Community Bank group. United Community Bancorp, Inc. now operates in the twelve Illinois counties of Adams, Brown, Greene, Hancock, Logan, McDonough, McLean, Madison, Macoupin, Pike, Sangamon and Scott; and Marion County in Missouri.

UCB is 100% EMPLOYEE OWNED – WE ANSWER ONLY TO OUR CUSTOMERS

Headquartered in Chatham, Illinois, UCB does not answer to any out-of-state management or shareholder group. We are locally owned & managed, allowing us to make smart decisions that provide the best possible products and services for our customers.

United Community Bancorp, Inc. has a long tradition of local history and deep roots in the communities we serve. We take pride in offering the personal attention that you expect from a community bank along with the best banking products available. We look forward to serving you!

Pawnee ChathamBunker Hill Main LoamiBunker Hill Drive Gillespie Auburn Plaza Springfield - Iles Ave Springfield - Stevenson Springfield - Bruns LnGreenfield

Bushnell ColchesterMacomb East Palmyra, MOMacomb West Mercantile Center Mercantile, Walmart Supercenter Mercantile at Maine Mercantile at Jersey Auburn - Rte. 4Mercantile at 36th Camp Point

Mechanicsburg ShermanHudson Springfield - Chatham RdLincoln Springfield - Peoria Rd Springfield - W. Iles Ave Alton Bethalto GodfreyElkhart Godfrey - Route 67

UNITED COMMUNITY BANCORP, INC.

FAMILY TREE2009 Carlinville & Bunker Hill

Citizen’s National Bank

2010 Carthage, Hamilton & Augusta

Marine Bank and Trust

2010 Mt. Sterling & Golden

Brown County State Bank

2011 Pittsfield, Winchester & Roodhouse

First Bank

2013 Quincy, Macomb, Bushnell,

Colchester, & Palmyra, MO

Heartland Bank and Trust

2013 Quincy

Mercantile Bank

2016 Auburn, Camp Point, Divernon,

Elkhart, Hudson, Lincoln, Mechanicsburg,

Sherman, & Springfield

Illini Bank and Farmers State Bank

of Camp Point

2017 Alton, Bethalto, & Godfrey

Liberty Bank

1973 Greenfield

Farmer’s State Bank

(Chartered in 1907)

1978 Bunker Hill

First National Bank

1982 Pawnee

Bank of Pawnee

1985 Chatham & Loami

Chatham Community Bank

1989 Gillespie

People’s State Bank

1996 Auburn

State Bank of Auburn

1999 Springfield

Iles Avenue

2004 Springfield

Stevenson Drive

2005 Springfield

Bruns Lane

2008 Divernon

Reichert Road

Hamilton AugustaCarlinville Mt. SterlingCarthage Golden Pittsfield Roodhouse Winchester Mercantile at 20thDivernon

FREQUENTLY ASKED QUESTIONS

4

Will my account change?Unless you have been personally contacted, your account number will remain the same. Your account type, however, will change to the UCB account that most closely matches the features and benefits of your current Illini account. Please turn to page 6 for more information about your new account types, as well as the terms and conditions beginning on page 18.

Can I still use my checks? If you have not already been personally contacted, you may continue to use your current Illini Bank checks until they are gone. When you do need to reorder checks, we will automatically update your checks to reflect your new UCB routing number (071108407). If you are low or out of Illini Bank checks, you may order new UCB checks at any time to be used on or after June 26, 2017.

Will my Debit card change? IMPORTANT! You may continue to use your current Illini Bank Debit card(s) until 2:00 a.m. on Monday, June 26, 2017. You will receive your new UCB Debit card(s) and your new PIN (personal identification number), mailed separately, the week of June 12th.

Once you receive your new UCB card and PIN, activate your card by calling us, toll-free, at (866) 392-9952 prior to June 26 to ensure your card is active and ready for use beginning on June 26.

Please remember:

1. Activate upon receipt, but PLEASE DO NOT USE YOUR NEW UCB CARDS PRIOR TO 2:00 a.m. JUNE 26.

2. Contact any service providers or creditors who use your old debit card number for recurring or automatic payment arrangements. Provide them with your new UCB card number and expiration date for payments due on or after June 26, 2017.

3. Please destroy and safely discard your Illini Bank debit card on or after June 26, 2017.

Please Note: If you currently have an Illini Photo Debit Card, your photo will not automatically transfer to your new card. Once you receive your new UCB debit card, visit ucbbank.com/cardshop to create and order a new photo card. There is no fee for photo cards at UCB; you can order up to one free photo card per year!

Will there be any changes to my current Direct Deposit or ACH Transactions?We will make every effort to update existing direct deposit instructions or ACH agreements you currently have in place; however, some companies may require your signature. For any NEW direct deposits or ACH transaction agreements, please use your new UCB Routing Number (071108407). Please note: this does not apply to any automatic payments that use your debit card. Please see Debit card questions above for more information.

Will my accounts continue to be FDIC insured? YES. Deposits in both banks are currently insured for up to $250,000.00 or more, depending on the account’s ownership structure. If you have a savings or checking account with both UCB and Illini Bank, each account, in each bank, will remain fully insured for a 6-month grace period following the merger. Time Deposits (Certificates of Deposit) will be fully insured until the first maturity date after the 6-month grace period. If maturity occurs within the 6-month grace period, the certificate will continue to be covered until the next maturity date if renewed for the same dollar amount and the same terms as the original deposit. For more information, please contact a Banker or call the FDIC toll-free at 1-877-ASK-FDIC (1-877-275-3342), or visit www.fdic.gov/deposit.

Will I still have overdraft protection? YES. Depending on the type of overdraft coverage you had with Illini Bank, your UCB account will be set up with similar overdraft coverage. Your current election with Illini Bank for overdraft coverage on your ATM and debit card transactions will be honored by UCB. You may change your election at any time by contacting your nearest UCB branch. Please refer to the Overdraft Programs Disclosure on page 24.

What are the daily cut-off times for receiving same-day credit on my deposits or payments? UCB’s cut-off time is 5:00 p.m., Monday – Friday (excluding holidays), for all deposits made in person. The daily cut-off time for ATM deposits and transfers is 1:00 p.m. & Mobile Deposits is 2:00 p.m., Monday – Friday (excluding holidays). Transactions conducted after the daily cut-off times will be credited on the next business day.

70-840/711

MP

PAY TO THEORDER OF

DATE

DOLLARS

$

MEMO

www.UCBbank.com

Ann Johnson301 North Main

Chatham, IL 62629

John Smith7/9/13

20.00

Twenty and ⁄00 100

Bank Routing No. Account No. Check No.

a071108407a 02497673c 1973

FREQUENTLY ASKED QUESTIONS

5

Can I access my accounts Online and use Online Bill Pay? IMPORTANT!YES. You will be able to access your accounts online at ucbbank.com beginning on Monday, June 26, 2017. However, please read the following section regarding important times and dates when online account access and activities will be temporarily unavailable.

Online Banking

• Online banking access will be temporarily suspended beginning at 11:00 a.m. on Friday, June 23, 2017 to begin conversion through Sunday, June 25, 2017.

• When you login for the first time at UCBbank.com on or after Monday, June 26, 2017, your username will remain the same, but in all lowercase, and you will use a temporary password. Your temporary password will be the last 6 digits of your Social Security or Tax ID No.

• Any Account Alerts that you may have set-up will not transfer. You will need to customize these again under Alerts.

Online Bill Pay

• If you are a current Online Bill Pay user, your biller information and any pending/scheduled payments (made prior to Thursday, June 22, 2017 at 4:30pm) will transfer over with no changes, however your Bill Payment history will not transfer.

• Beginning at 4:30 p.m. on Thursday, June 22, 2017, Bill Pay will be temporarily limited to a View-Only mode. In this mode, you will not be able to make, schedule, or change any online Bill Payments. Please make or schedule any Bill Payments due prior to or on June 26, 2017 before June 22nd at 4:30 p.m.

• E-Bills and person-to-person payments will not convert. You will need to re-initiate any E-Bills you currently receive.

• Recurring Bill Payments that fall on weekend dates or federal holidays will process on the previous business day.

Mobile Banking

• To use mobile banking for the first time, you will need to first login to your Online Banking account at UCBbank.com. Once you have done this (see Online Banking login information above), you will be able to setup and use Mobile Banking.

• Download UCB’s mobile app. Search for “UCB Bank” in the iTunes App or Google Play Stores.

Updates & Information: The above information and any additional instructions are available online at www.ucbbank.com/welcome. Please be sure to refer to this web page for updates and important contact information or call our nearest branch.

Can I access my accounts by telephone? YES. UCB’s Telephone Banking number is toll-free 888-226-5822. In order to use UCB’s Telephone Banking service, simply call this number and use the last 4 digits of your Social Security Number as your phone link pin. Should you need assistance using this service, please contact your nearest UCB location and our bankers will be happy to assist you.

Will there be changes on my statement? YES. All customers with either a checking or savings account will receive a cut-off statement through Sunday, June 25, 2017. Interest-bearing accounts (other than Certificates of Deposit and IRAs) will be paid interest through that date. There will be no monthly service or maintenance fees assessed on this statement. After June 25, 2017, interest-bearing accounts will receive the balance of their June interest on their new UCB statement. Savings statements are printed quarterly unless required more frequently, based on transaction activity, or if the account is combined with a monthly checking statement. UCB also offers E-statements (electronic or “paperless” statements) free of charge to all customers. Please contact a banker to have your checking and/or savings statements combined, or to sign up for E-statements.

Will I receive two different year-end tax reporting forms? NO. You will receive all year-end tax reporting forms (for amounts over $10) from UCB.

Will my loans remain the same? YES. This transition does not affect the financing terms of your loan. Your loan number will remain the same and you will now have the added convenience of additional locations. For specific loan account questions, you may contact our UCB Loan Servicing Center toll-free at 1-888-822-4087. The mailing address is PO Box 148, Gillespie, IL 62033. You will receive a letter in the mail outlining the complete details of the changes to your loan service provider.

What happens to my IRA? UCB will become the new custodian of all IRA plans as of June 24, 2017. These plans include Traditional, Roth and Simplified Employee Pension accounts.

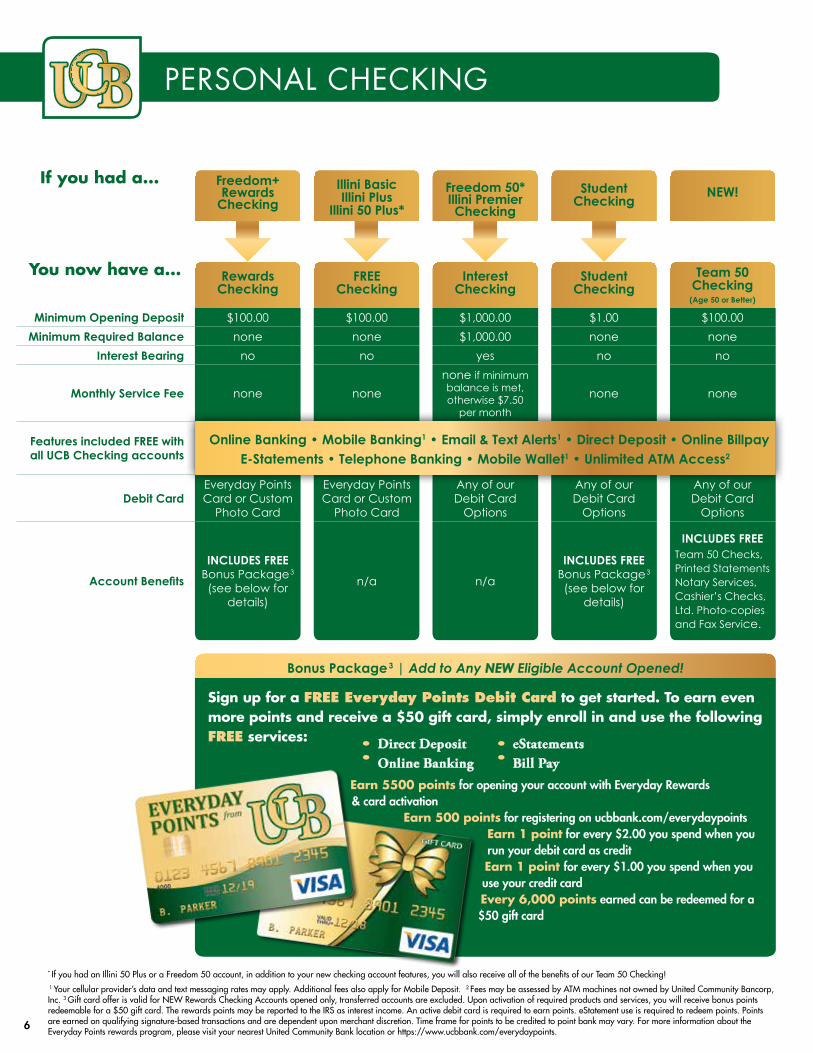

PERSONAL CHECKING

6

* If you had an Illini 50 Plus or a Freedom 50 account, in addition to your new checking account features, you will also receive all of the benefits of our Team 50 Checking! 1 Your cellular provider’s data and text messaging rates may apply. Additional fees also apply for Mobile Deposit. 2 Fees may be assessed by ATM machines not owned by United Community Bancorp, Inc. 3 Gift card offer is valid for NEW Rewards Checking Accounts opened only, transferred accounts are excluded. Upon activation of required products and services, you will receive bonus points redeemable for a $50 gift card. The rewards points may be reported to the IRS as interest income. An active debit card is required to earn points. eStatement use is required to redeem points. Points are earned on qualifying signature-based transactions and are dependent upon merchant discretion. Time frame for points to be credited to point bank may vary. For more information about the Everyday Points rewards program, please visit your nearest United Community Bank location or https://www.ucbbank.com/everydaypoints.

If you had a...

You now have a... RewardsChecking

FREEChecking

InterestChecking

StudentChecking

Team 50Checking

(Age 50 or Better)

Minimum Opening Deposit $100.00 $100.00 $1,000.00 $1.00 $100.00Minimum Required Balance none none $1,000.00 none none

Interest Bearing no no yes no no

Monthly Service Fee none nonenone if minimum balance is met, otherwise $7.50

per month

none none

Features included FREE with all UCB Checking accounts

Online Banking • Mobile Banking1 • Email & Text Alerts1 • Direct Deposit • Online Billpay E-Statements • Telephone Banking • Mobile Wallet1 • Unlimited ATM Access2

Debit CardEveryday Points Card or Custom

Photo Card

Everyday Points Card or Custom

Photo Card

Any of our Debit Card

Options

Any of our Debit Card

Options

Any of our Debit Card

Options

Account Benefits

INCLUDES FREEBonus Package3

(see below for details)

n/a n/a

INCLUDES FREEBonus Package3

(see below for details)

INCLUDES FREETeam 50 Checks,Printed Statements Notary Services, Cashier’s Checks, Ltd. Photo-copies and Fax Service.

Bonus Package3 | Add to Any NEW Eligible Account Opened!

Sign up for a FREE Everyday Points Debit Card to get started. To earn even more points and receive a $50 gift card, simply enroll in and use the following FREE services: Direct Deposit

Online BankingeStatementsBill Pay

Earn 5500 points for opening your account with Everyday Rewards & card activation

Earn 500 points for registering on ucbbank.com/everydaypointsEarn 1 point for every $2.00 you spend when you run your debit card as credit Earn 1 point for every $1.00 you spend when you use your credit cardEvery 6,000 points earned can be redeemed for a $50 gift card

Freedom+ Rewards

CheckingIllini BasicIllini Plus

Illini 50 Plus*Freedom 50*Illini PremierChecking

StudentChecking NEW!

If you had a...

You now have a...

PERSONAL SAVINGS

1 Your cellular provider’s data and text messaging rates may apply. Additional fees also apply for Mobile Deposit. 2 Fees may be assessed by ATM machines not owned by United Community Bancorp, Inc.. 3 A $2.00 fee will apply for each transaction in excess of six per month. 4 A $7.50 fee will apply for each transaction in excess of six per month. Specific transaction limits may apply. See a banker for details.

UCB SavingsAccount

Money MarketSavings Account

MinorSavings Account

Christmas ClubSavings Account

Minimum Opening Deposit $100.00 $2,500.00 $50.00 noneMinimum Required Balance $100.00 $2,500.00 none none

Interest Bearing yesYes

(Tiered interest structure based on

balance)

yes yes

Monthly Service Fee$1.00 if minimum

balance of $100.00 is not maintained

$7.50 if minimum balance of $2,500.00

is not maintainednone none

Features included FREE with all UCB Savings accounts

Online Banking • Mobile Banking1 • Email & Text Alerts1 • Direct Deposit E-Statements • Telephone Banking • Unlimited ATM Access2

ATM Card with Unlimited ATM access yes2 yes2 no no

Transaction LimitsUp to 6

transactions allowed per month3

Up to 6 transactions

allowed per month4

Up to 6 transactions

allowed per month3

Interest is forfeited if a withdrawal is made prior to November disbursement

7

Other Savings Options

CDs - CERTIFICATES OF DEPOSITCDs are a great choice when you want a greater return on your investment and don’t need immediate access to your money. Invest as little as $1,000 and receive competitive rates guaranteed for the term you select. We can help you build a CD portfolio to save time and put your money to work.

IRAs - INDIVIDUAL RETIREMENT ACCOUNTSIRAs aren’t just for retirement anymore - save for your first home or maybe a college degree and even realize tax advantages. Learn more about the type of IRA that offers you the options, benefits, and flexibility you need.

HEALTH SAVINGS ACCOUNTSHealth Savings Accounts are designed to help individuals save for qualified medical and retirement health expenses as well as for businesses to be able to provide affordable health insurance plans with income tax benefits.

For more detailed information, call or visit your banker today.

Basic SavingsPersonal OD-ProtNon-Personal OD

High Yield OD

High Yield MMDAIllini Premier MMDA

Illini 50 PlusBank at School NEW!

BUSINESS CHECKING ACCOUNTS

8

FREE Small Business

Checking

Simplified Small Business

Checking

Business Checking1

Business Interest

Checking2

Business Money Market

Checking

Qualifying Parties

CorporationsLLCs

PartnershipsSole ProprietorshipsNot-for-Profits

CorporationsLLCs

PartnershipsSole ProprietorshipsNot-for-Profits

CorporationsLLCs

PartnershipsSole ProprietorshipsNot-for-Profits

Sole ProprietorshipsNot-for-Profits

CorporationsLLCs

PartnershipsSole ProprietorshipsNot-for-Profits

Interest Bearing No No No Yes Yes

Monthly Service Fees FREE

$25.00 (only if $15,000

average daily col-lected balance is not maintained)

$5.00 $3.00

$5.00(only if $10,000

average daily col-lected balance is not maintained)

Fee Per DebitA combination of debits and

items deposited up to 200 per

statement cycle are free. A $.25

fee will apply for each item over

200.

A combination of debits and

items deposited up to 400 per

statement cycle are free. A $.25

fee will apply for each item over

400.

$.10 Per Debit (checks paid, ACH

debit, or ATM/Debit Cards)

$.10 Per Debit (checks paid, ACH

debit, or ATM/Debit Cards)

No Per Debit Fee (No fee for checks

paid or ACH debits)3

Fee Per Credit$.10 Per Item

Deposited(check or

ACH credit)

$.07 Per Item Deposited(check or

ACH credit)

$.05 Per Item Deposited

(only if $10,000 average daily col-lected balance is not maintained)

Transaction Limits None None None NoneConduct up to

6 free debits per month3

Minimum Opening Deposit $100 $100 $100 $100 $100

If you had a...

You now have a...

Basic BusinessSmall Business & Non-Profit

Checking

NEW!Illini

CommercialChecking

Illini Premier Business

Checking

Basic Business & High Yield

SavingsIllini Bus. Premier Money Market

1 The fees in the Business Checking account can be offset totally or in part by the Earnings Credit determined by the bank. 2 Only if $5,000 average daily collected balance is not maintained. 3 A $7.50 fee will apply for each debit transaction in excess of six per month.

At UCB, your

is our

At UCB, yourBOTTOM LINEis our TOP PRIORITY

BUSINESS SERVICES

REMOTE DEPOSIT CAPTURE*With Remote Deposit Capture, you can make your deposits without leaving the office. Your banking just got easier!

• No more driving to the bank to make a deposit • Ongoing on-site training provided • Checks are scanned on-site • Deposits are sent electronically to the bank • Combine with other UCB Online Services and conduct all of your daily banking without leaving your desk • Data is instantly accessible via your computer • Deposits can be collected from other offices • Friendly, fast and simple to use

CASH MANAGEMENT*Good cash management is vital to running a successful business. UCB offers a variety of cash management services to help improve your financial operations, and our bankers will work with you to determine the most effective tools to meet your business goals. Our Cash Management Services include:• Online account access:

• Review account activity and balances• Transfer funds between accounts• Pay loans and taxes• Stop payment on checks• Reconcile accounts

• CD-Rom with check images and account information• Account reconciliation services• Account analysis• Positive pay• Wire transfer services• Direct deposit services• ACH services, including payroll, corporate payments and consumer credits/debits

* Fees may apply for select services. See your banker for complete details.

ADDITIONAL BUSINESS AND COMMERCIAL SERVICES AND FINANCINGWe also offer a wide variety of business financing options, including term loans, lines of credit, letters of credit, commercial mortgage refinancing, construction loans, agricultural loans, physician and professional service loans and SBA loans. For additional information, please see one of our UCB lenders.

l First-time Home Buyers Program l Fixed and Adjustable Ratesl VA Loans

l Lot Loans l Construction Loansl Home Equity Loans

9

NMLS #571141

ELECTRONIC “E-SERVICES”

United Community Bank offers a variety of electronic services designed to be environmentally friendly and provide the ultimate in convenience for our customers. Now you can conduct your banking from anywhere via computer, tablet or smart phone!

E-STATEMENTSUCB offers electronic statements (E-Statements) for your personal and business deposit and loan statement accounts. E-Statements are available in the Online Banking portal by logging into your account, clicking on a specific account, then clicking the “Documents” tab. You may “opt in” to receive your statement by email instead of receiving a paper copy in the mail. E-Statements are FREE, and include all the same information that you receive with a paper statement including your check images and any notices or important information from UCB.

E-Statements are: • FREE: There is no cost to enroll for E-Statement service• SECURE: E-Statements are located within our secure Online Banking Portal • CONVENIENT: You can view, print or download your E-Statements at any time• EASY: Just click the Profile link within Online Banking to enroll • FAST: Your E-Statement will be available one or two days earlier than you would normally receive your paper statement

ONLINE BANKINGUnited Community Bank’s Online Banking gives you 24/7 real-time access to do the following: • View account balances, including checking, savings, loans and lines of credit• View & print statements online• Transfer funds between deposit accounts and make payments to loans• View account transaction history• Download transactions into financial management software• Get your account balance delivered via email or wireless device, with free Account Alerts • View, search for, print or save copies of posted checks

Online Banking is:• FREE: There is no charge to use Online Banking• FAST: There is no software to download or learn – just register online at UCBbank.com to set up your account• SECURE: Bank online at UCBbank.com with confidence – our security features are designed to guard your personal information

DEBIT CARD OPTIONSEVERYDAY POINTS CARDThe “Everyday Points” debit card allows you to earn Rewards Points for purchases you make every day. You can earn points toward travel, merchandise or gift cards.

LOYALTY CARD — SUPPORT YOUR LOCAL SCHOOL!“Loyalty” debit cards are available for a variety of schools in the communities we serve. Loyalty cards allow you to show your school spirit by earning money for your school.

10

ELECTRONIC “E-SERVICES”

ONLINE BILLPAYPay bills online for free and without any fees! When you use our Online BillPay, you no longer need to write checks or mail payments, and going digital allows you to minimize paperwork. It’s true convenience, including the ability to:• Pay unlimited bills to anyone in the U.S.• Schedule payments in advance – both one-time and recurring payments – handy for vacations and business travel • Pay multiple bills quickly, from the same screen • Set up automatic bill payments while maintaining control – make changes with a click of your mouse anytime, anywhere

In order to sign up for Online BillPay, log into your account at UCBbank.com and click “Bill Payment” to get started.

UCB MOBILE BANKING (Online Banking via smart phone)

Mobile Banking is a FREE* Internet-based service that delivers the convenience of Online Banking to your mobile device. Mobile Banking allows you to perform transactions from your smart phone with 24/7 access.

With UCB Mobile Banking, you can: • View account balances • View transaction history • View pending transactions• Pay bills • Transfer funds • Make mobile deposits**• Make loan payments or advances • Receive “E-Alerts” on banking transactions • Locate your nearest branch or ATM

In order to use Mobile Banking, you must first be enrolled in Online Banking with UCB. Then, just navigate to the iTunes or Google Play app store on your smart phone and search for “UCBbank” to download the Mobile Banking app.

*Your carrier’s standard messaging and data rates may apply. **Mobile Deposit fees of $0.50 per deposit also apply. Ask your banker for complete Mobile Deposit terms and conditions.

Please contact our Electronic Services department at 217-438-4101 or 1-855-822-5880 with your Electronic Services questions.

DEBIT CARD OPTIONSREGULAR DEBIT CARDThe “Regular” debit card is our standard debit card which can be used for purchases or ATM access. There are no fancy features on this card – it’s your basic debit card.

CUSTOM CARDThe UCB “Custom” debit card allows you to upload your favorite photo or choose from one of our galleries to make your debit card uniquely yours. Visit UCBcardshop.com to design your card today!

11

13855-822-5880 | UCBbank.com

Take advantage of UCB’s

MOBILE BANKINGfeaturing MOBILE DEPOSIT

Make deposits directly into your UCB Checking Account – search

for the “UCBbank” app oniTunes or Google Play!

*Must be a UCB Online Banking user in order to use Mobile Banking. Standard text and data rates apply.

The Leader ofCommunity Banking

l View account balances l View transaction history l View pending transactions l Transfer funds

l Make loan payments or advances l Receive “E-Alerts” on banking transactions

13

UCB is proud to be Downstate’s Leading Mortgage Lender. We offer a variety of mortgage options at competitive interest rates. Whether you are interested in buying a home, refinancing your current home loan, building a new house or taking advantage of your home’s equity, UCB’s lenders will help you find the product that best fits your needs. We service 100% of our loans locally, so you always make your payments directly to UCB. Our dedicated loan servicing team watches over your accounts and manages all of your tax and insurance payments for you if you choose to have escrow on your loan. Our outstanding mortgage options include the following products.

FIRST-TIME HOME BUYERS PROGRAMSUCB offers mortgage loans to first-time home buyers through Guaranteed Rural Housing or FHA. We also participate in the Down Payment Plus program. Please consult a UCB lender for more information on programs available to you as a first-time home buyer.

FIXED-RATE MORTGAGE LOANWould you like the security of knowing that your monthly principal and interest payments will not change? Consider the option of a fixed-rate mortgage to finance your home purchase or refinance your current mortgage. Terms of 10, 15, 20 and 30 years are available for fixed-rate mortgage loans.

ADJUSTABLE RATE MORTGAGES (ARM) ARMs offer borrowers a lower interest rate for an initial term of 3 - 7 years. This initial fixed-rate is followed by a period when your rate will be adjusted at regular intervals. All ARMs have rate caps in place to limit interest rate increases over the life of the loan.

VETERAN AFFAIRS LOANS (VA)Backed by the Department of Veterans Affairs (VA), VA loans help eligible service members and veterans buy or refinance a home with little or no down payment, lower monthly payments, and a simplified approval process.

LOT LOANS Begin building equity before you start construction of your new home by taking advantage of a UCB Lot Loan. Terms between 6 months to 60 months are available, or you may arrange a longer amortization in order to keep your payments low.

CONSTRUCTION & BRIDGE LOANSFinance your home Construction Loan for a term of 6 - 9 months with UCB. Or take advantage of a Bridge Loan, to ease your transition during the construction process.

HOME EQUITY LOANSA Home Equity Loan is a term loan that allows you to borrow against the equity in your current home. Interest rates are determined by the length of the term and your loan-to-value ratio. Home Equity Loans offer the opportunity to use the equity in your home for such things as home improvements, debt consolidation, school tuition or traveling.

HOME EQUITY LINES OF CREDIT A Home Equity Line of Credit is a revolving line of credit secured by the equity you have in your home. Once your application is approved and your credit limit determined, you can conveniently access your loan account by check or transfer request as you need it. The interest rates on Home Equity Lines of Credit are usually variable and are based on the prime lending rate, with both floor and ceiling rate limits.

Visit UCBbank.com for details or see a lender for more information on mortgage products from UCB.

MORTGAGE SERVICES

FACTS WHAT DOES UNITED COMMUNITY BANCORP, INC. DO WITHYOUR PERSONAL INFORMATION?

Why? Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do.

What? The types of personal information we collect and share depend on the product or service you have with us. This information can include:

How? All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information, the reasons United Community Bancorp, Inc. chooses to share; and whether you can limit this sharing.

• Social Security number• Account balances• Payment history

• Account transactions• Mortgage rates and payments• Checking account information

Reasons we can share your personal information

Does United Community Bancorp, Inc. share? Can you limit this sharing?

For our everyday business purposes - Such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus.

Yes No

For our marketing purposes -To offer our products and services to you. Yes No

For joint marketing with other financial companies. Yes No

For our affiliates’ everyday business purposes - Information about your transactions and experiences.

Yes No

For our affiliates’ everyday business purposes - Information about your creditworthiness.

Yes Yes

For non-affiliates to market to you No We don’t share

To limit our sharing

• Call Toll-free 800-328-2822• Visit us online: www.ucbbank.com/privacy

Please note:If you are a new customer, we can begin sharing your information 30 days from the date we sent thisnotice. When you are no longer our customer, we continue to share your information as described inthis notice.However, you can contact us at any time to limit our sharing.

Questions? Call toll-free 800-328-2822

REV. 3/2017

PRIVACY POLICY

14

15

PRIVACY POLICY

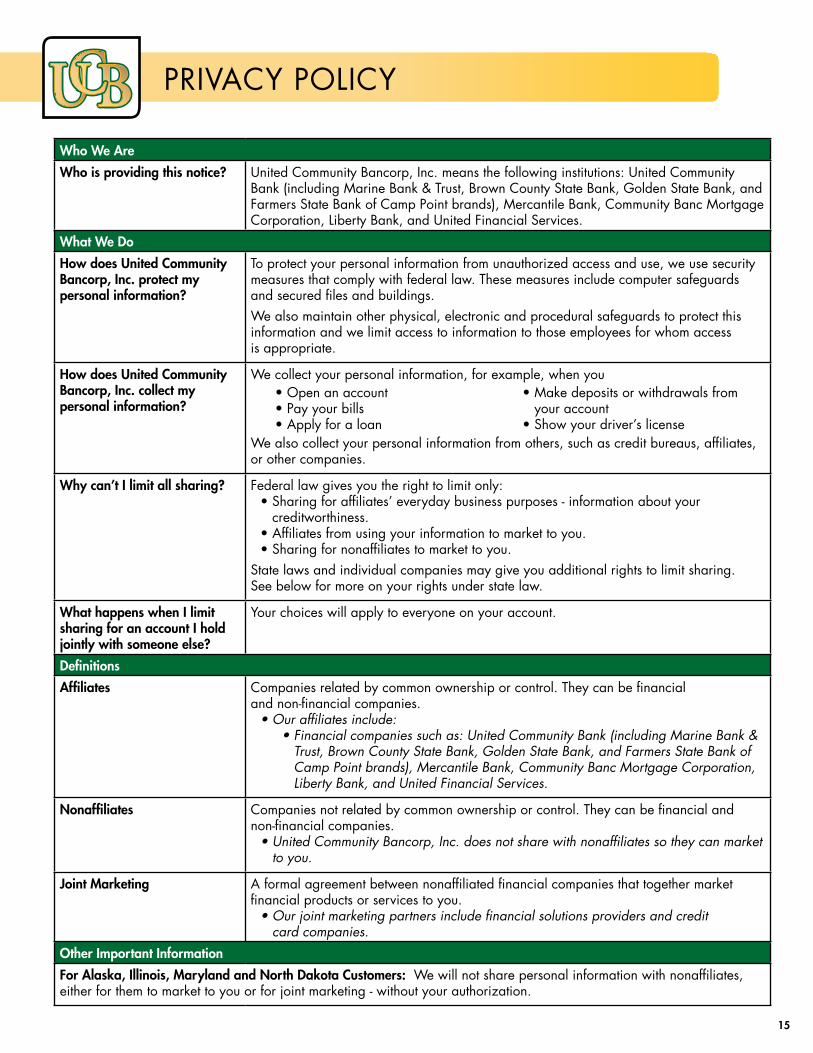

Who We Are

Who is providing this notice? United Community Bancorp, Inc. means the following institutions: United Community Bank (including Marine Bank & Trust, Brown County State Bank, Golden State Bank, and Farmers State Bank of Camp Point brands), Mercantile Bank, Community Banc Mortgage Corporation, Liberty Bank, and United Financial Services.

What We Do

How does United Community Bancorp, Inc. protect my personal information?

To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings.

We also maintain other physical, electronic and procedural safeguards to protect this information and we limit access to information to those employees for whom access is appropriate.

How does United Community Bancorp, Inc. collect my personal information?

We collect your personal information, for example, when you

We also collect your personal information from others, such as credit bureaus, affiliates, or other companies.

Why can’t I limit all sharing? Federal law gives you the right to limit only:• Sharing for affiliates’ everyday business purposes - information about your

creditworthiness.• Affiliates from using your information to market to you.• Sharing for nonaffiliates to market to you.

State laws and individual companies may give you additional rights to limit sharing.See below for more on your rights under state law.

What happens when I limit sharing for an account I hold jointly with someone else?

Your choices will apply to everyone on your account.

Definitions

Affiliates Companies related by common ownership or control. They can be financialand non-financial companies.

• Our affiliates include:• Financial companies such as: United Community Bank (including Marine Bank &

Trust, Brown County State Bank, Golden State Bank, and Farmers State Bank of Camp Point brands), Mercantile Bank, Community Banc Mortgage Corporation, Liberty Bank, and United Financial Services.

Nonaffiliates Companies not related by common ownership or control. They can be financial and non-financial companies.

• United Community Bancorp, Inc. does not share with nonaffiliates so they can market to you.

Joint Marketing A formal agreement between nonaffiliated financial companies that together market financial products or services to you.

• Our joint marketing partners include financial solutions providers and credit card companies.

Other Important Information

For Alaska, Illinois, Maryland and North Dakota Customers: We will not share personal information with nonaffiliates, either for them to market to you or for joint marketing - without your authorization.

• Open an account• Pay your bills • Apply for a loan

• Make deposits or withdrawals from your account

• Show your driver’s license

BEST BANK

UCB has won more than 30 “Best” awards since 2009, including:

• Best Bank• Best Mortgage Lender• Best Customer Service• Best Rewards Program• Best Family-Owned Business

• Best Locally-Owned Business

UCBbank.com

UCBcoupons.com

FREE Exclusive Discounts from your Favorite Local Businesses for valued UCB Checking Customers!

Download the FREE My Bank Coupons App or ask for details

18

TERMS AND CONDITIONS OF YOUR ACCOUNTIMPORTANT INFORMATION ABOUT PROCEDURES FOR OPENING A NEW ACCOUNT

To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an account.

What this means for you: When you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your driver’s license or other identifying documents.

AGREEMENT - This document, along with any other documents we give you pertaining to your account(s), is a contract that establishes rules which control your account(s) with us. Please read this carefully and retain it for future reference. If you sign the signature card or open or continue to use the account, you agree to these rules. You will receive a separate schedule of rates, qualifying balances, and fees if they are not included in this document. If you have any questions, please call us.

This agreement is subject to applicable federal laws, the laws of the state of Illinois and other applicable rules such as the operating letters of the Federal Reserve Banks and payment processing system rules (except to the extent that this agreement can and does vary such rules or laws). The body of state and federal law that governs our relationship with you, however, is too large and complex to be reproduced here. The purpose of this document is to:

1. summarize some laws that apply to common transactions;2. establish rules to cover transactions or events which the law does not regulate;3. establish rules for certain transactions or events which the law regulates but permits variation by

agreement; and4. give you disclosures of some of our policies to which you may be entitled or in which you may

be interested.

If any provision of this document is found to be unenforceable according to its terms, all remaining provisions will continue in full force and effect. We may permit some variations from our standard agreement, but we must agree to any variation in writing either on the signature card for your account or in some other document.

As used in this document the words “we,” “our,” and “us” mean the financial institution and the words “you” and “your” mean the account holder(s) and anyone else with the authority to deposit, withdraw, or exercise control over the funds in the account. However, this agreement does not intend, and the terms “you” and “your” should not be interpreted, to expand an individual’ s responsibility for an organization’ s liability. If this account is owned by a corporation, partnership or other organization, individual liability is determined by the laws generally applicable to that type of organization. The headings in this document are for convenience or reference only and will not govern the interpretation of the provisions. Unless it would be inconsistent to do so, words and phrases used in this document should be construed so the singular includes the plural and the plural includes the singular.

LIABILITY - You agree, for yourself (and the person or entity you represent if you sign as a representative of another) to the terms of this account and the schedule of charges. You authorize us to deduct these charges, without notice to you, directly from the account balance as accrued. You will pay any additional reasonable charges for services you request which are not covered by this agreement.

Each of you also agrees to be jointly and severally (individually) liable for any account shortage resulting from charges or overdrafts, whether caused by you or another with access to this account. This liability is due immediately, and can be deducted directly from the account balance whenever sufficient funds are available. You have no right to defer payment of this liability, and you are liable regardless of whether you signed the item or benefited from the charge or overdraft.

You will be liable for our costs as well as for our reasonable attorneys’ fees, to the extent permitted by law, whether incurred as a result of collection or in any other dispute involving your account. This includes, but is not limited to, disputes between you and another joint owner; you and an authorized signer or similar party; or a third party claiming an interest in your account. This also includes any action that you or a third party takes regarding the account that causes us, in good faith, to seek the advice of an attorney, whether or not we become involved in the dispute. All costs and attorneys’ fees can be deducted from your account when they are incurred, without notice to you.

DEPOSITS - We will give only provisional credit until collection is final for any items, other than cash, we accept for deposit (including items drawn “ on us” ). Before settlement of any item becomes final, we act only as your agent, regardless of the form of indorsement or lack of indorsement on the item and even though we provide you provisional credit for the item. We may reverse any provisional credit for items that are lost, stolen, or returned. Actual credit for deposits of, or payable in, foreign currency will be at the exchange rate in effect on final collection in U.S. dollars. We are not responsible for transactions by mail or outside depository until we actually record them. We will treat and record all transactions received after our “ daily cutoff time” on a business day we are open, or received on a day we are not open for business, as if initiated on the next business day that we are open. At our option, we may take an item for collection rather than for deposit. If we accept a third-party check for deposit, we may require any third-party indorsers to verify or guarantee their indorsements, or indorse in our presence.

WITHDRAWALSGenerally - Unless clearly indicated otherwise on the account records, any of you, acting alone, who signs to open the account or has authority to make withdrawals may withdraw or transfer all or any part of the account balance at any time. Each of you (until we receive written notice to the contrary) authorizes each other person who signs or has authority to make withdrawals to indorse any item payable to you or your order for deposit to this account or any other transaction with us.

Postdated checks - A postdated check is one which bears a date later than the date on which the check is written. We may properly pay and charge your account for a postdated check even though payment was made before the date of the check, unless we have received written notice of the postdating in time to have a reasonable opportunity to act. Because we process checks mechanically, your notice will not be effective and we will not be liable for failing to honor your notice unless it precisely identifies the number, date, amount and payee of the item.

Checks and withdrawal rules - If you do not purchase your check blanks from us, you must be certain that we approve the check blanks you purchase. We may refuse any withdrawal or transfer request which you attempt on forms not approved by us or by any method we do not specifically permit. We may refuse any withdrawal or transfer request which is greater in number than the frequency permitted, or which is for an amount greater or less than any withdrawal limitations. We will use the date the transaction is completed by us (as opposed to the date you initiate it) to apply the frequency limitations. In addition, we may place limitations on the account until your identity is verified. Even if we honor a nonconforming request, we are not required to do so later. If you violate the stated transaction limitations (if any), in our discretion we may close your account or reclassify it as a transaction account. If we reclassify your account, your account will be subject to the fees and earnings rules of the new account classification.

If we are presented with an item drawn against your account that would be a “substitute check,” as defined by law, but for an error or defect in the item introduced in the substitute check creation process, you agree that we may pay such item.

See the funds availability policy disclosure for information about when you can withdraw funds you deposit. For those accounts to which our funds availability policy disclosure does not apply, you can ask us when you make a deposit when those funds will be available for withdrawal. We may determine the amount of available funds in your account for the purpose of deciding whether to return an item for insufficient funds at any time between the time we receive the item and when we return the item or send a notice in lieu of return. We need only make one determination, but if we choose to make a subsequent determination, the account balance at the subsequent time will determine whether there are insufficient available funds.

A temporary debit authorization hold affects your account balance - On debit card purchases, merchants may request a temporary hold on your account for a specified sum of money, which may be more than the actual amount of your purchase. When this happens, our processing system cannot determine that the amount of the hold exceeds the actual amount of your purchase. This temporary hold, and the amount charged to your account, will eventually be adjusted to the actual amount of your purchase, but it may be up to three days before the adjustment is made. Until the adjustment is made, the amount of funds in your account available for other transactions will be reduced by the amount of the temporary hold. If another transaction is presented for payment in an amount greater than the funds left after the deduction of the temporary hold amount, that transaction will be a nonsufficient funds (NSF) transaction if we do not pay it or an overdraft transaction if we do pay it. You will be charged an NSF or overdraft fee according to our NSF or overdraft fee policy. You will be charged the fee even if you would have had sufficient funds in your account if the amount of the hold had been equal to the amount of your purchase.

Here is an example of how this can occur - assume for this example the following: (1) you have opted-in to our overdraft services for the payment of overdrafts on ATM and everyday debit card transactions, (2) we pay the overdraft, and (3) we do not charge the overdraft fee if the transaction overdraws the account by less than $10.

You have $120 in your account. You swipe your card at the card reader on a gasoline pump. Since it is unclear what the final bill will be, the gas station’ s processing system immediately requests a hold on your account in a specified amount, for example, $80. Our processing system authorizes a temporary hold on your account in the amount of $80, and the gas station’ s processing system authorizes you to begin pumping gas. You fill your tank and the amount of gasoline you purchased is only $50. Our processing system shows that you have $40 in your account available for other transactions ($120 - $80 = $40) even though you would have $70 in your account available for other transactions if the amount of the temporary hold was equal to the amount of your purchase ($120 - $50 = $70). Later, another transaction you have authorized is presented for payment from your account in the amount of $60 (this could be a check you have written, another debit card transaction, an ACH debit or any other kind of payment request). This other transaction is presented before the amount of the temporary hold is adjusted to the amount of your purchase (remember, it may take up to three days for the adjustment to be made). Because the amount of this other transaction is greater than the amount our processing system shows is available in your account, our payment of this transaction will result in an overdraft transaction. Because the transaction overdraws your account by $20, your account will be assessed the overdraft fee according to our overdraft fee policy. You will be charged this fee according to our policy even though you would have had enough money in your account to cover the $60 transaction if your account had only been debited the amount of your purchase rather than the amount of the temporary hold or if the temporary hold had already been adjusted to the actual amount of your purchase.

Overdrafts - You understand that we may, at our discretion, honor withdrawal requests that overdraw your account. However, the fact that we may honor withdrawal requests that overdraw the account balance does not obligate us to do so later. So you can NOT rely on us to pay overdrafts on your account regardless of how frequently or under what circumstances we have paid overdrafts on your account in the past. We can change our practice of paying overdrafts on your account without notice to you. You can ask us if we have other account services that might be available to you where we commit to paying overdrafts under certain circumstances, such as an overdraft protection line-of-credit or a plan to sweep funds from another account you have with us. You agree that we may charge fees for overdrafts. For consumer accounts, we will not charge fees for overdrafts caused by ATM withdrawals or one-time debit card transactions if you have not opted-in to that service. We may use subsequent deposits, including direct deposits of social security or other government benefits, to cover such overdrafts and overdraft fees.

Multiple signatures, electronic check conversion, and similar transactions - An electronic check conversion transaction is a transaction where a check or similar item is converted into an electronic fund transfer as defined in the Electronic Fund Transfers regulation. In these types of transactions the check or similar item is either removed from circulation (truncated) or given back to you. As a result, we have no opportunity to review the check to examine the signatures on the item. You agree that, as to these or any items as to which we have no opportunity to examine the signatures, you waive any requirement of multiple signatures.

Notice of withdrawal - We reserve the right to require not less than 7 days’ notice in writing before each withdrawal from an interest-bearing account other than a time deposit, or from any other savings account as defined by Regulation D. (The law requires us to reserve this right, but it is not our general policy to use it.) Withdrawals from a time account prior to maturity or prior to any notice period may be restricted and may be subject to penalty. See your notice of penalty for early withdrawal.

OWNERSHIP OF ACCOUNT AND BENEFICIARY DESIGNATIONThese rules apply to this account depending on the form of ownership and beneficiary designation, if any, specified on the account records. We make no representations as to the appropriateness or effect of the ownership and beneficiary designations, except as they determine to whom we pay the account funds.

Individual Account - is an account in the name of one person.

Joint Account - With Survivorship (And Not As Tenants In Common) - is an account in the name of two or more persons. Each of you intend that when you die the balance in the account (subject to any previous pledge to which we have agreed) will belong to the survivor(s). If two or more of you survive, you will own the balance in the account as joint tenants with survivorship and not as tenants in common.

Joint Account - No Survivorship (As Tenants In Common) - is owned by two or more persons, but none of you intend (merely by opening this account) to create any right of survivorship in any other person. We encourage you to agree and tell us in writing of the percentage of the deposit contributed by each of you. This information will not, however, affect the “ number of signatures” necessary for withdrawal.

Revocable Trust or Pay-On-Death Account - If two or more of you create this type of account, you own the account jointly with survivorship. Beneficiaries of either of these account types cannot withdraw unless: (1) all persons creating the account die, and (2) the beneficiary is then living. If two or more beneficiaries are named and survive the death of the owner(s) of the account, such beneficiaries will own this account in equal shares, without right of survivorship. The person(s) creating either a Pay-On-Death or Revocable Trust account reserves the right to: (1) change beneficiaries, (2) change account types, and (3) withdraw all or part of the account funds at any time.

BUSINESS, ORGANIZATION AND ASSOCIATION ACCOUNTSEarnings in the form of interest, dividends, or credits will be paid only on collected funds, unless otherwise provided by law or our policy. You represent that you have the authority to open and

19

conduct business on this account on behalf of the entity. We may require the governing body of the entity opening the account to give us a separate authorization telling us who is authorized to act on its behalf. We will honor the authorization until we actually receive written notice of a change from the governing body of the entity.

STOP PAYMENTS - Unless otherwise provided, the rules in this section cover stopping payment of items such as checks and drafts. Rules for stopping payment of other types of transfers of funds, such as consumer electronic fund transfers, may be established by law or our policy. If we have not disclosed these rules to you elsewhere, you may ask us about those rules.

We may accept an order to stop payment on any item from any one of you. You must make any stop-payment order in the manner required by law and we must receive it in time to give us a reasonable opportunity to act on it before our stop-payment cutoff time. Because stop-payment orders are handled by computers, to be effective, your stop-payment order must precisely identify the number, date, and amount of the item, and the payee. You may stop payment on any non-debit card item drawn on your account whether you sign the item or not. Generally, if your stop-payment order is given to us in writing it is effective for six months. Your order will lapse after that time if you do not renew the order in writing before the end of the six-month period. If the original stop-payment order was verbal your stop-payment order will lapse after 14 calendar days if you do not confirm your order in writing within that time period. We are not obligated to notify you when a stop-payment order expires. A release of the stop-payment request may be made only by the person who initiated the stop-payment order.

If you stop payment on an item and we incur any damages or expenses because of the stop payment, you agree to indemnify us for those damages or expenses, including attorneys’ fees. You assign to us all rights against the payee or any other holder of the item. You agree to cooperate with us in any legal actions that we may take against such persons. You should be aware that anyone holding the item may be entitled to enforce payment against you despite the stop-payment order.

Our stop-payment cutoff time is one hour after the opening of the next banking day after the banking day on which we receive the item. Additional limitations on our obligation to stop payment are provided by law (e.g., we paid the item in cash or we certified the item).

TELEPHONE TRANSFERS - A telephone transfer of funds from this account to another account with us, if otherwise arranged for or permitted, may be made by the same persons and under the same conditions generally applicable to withdrawals made in writing. Unless a different limitation is disclosed in writing, we restrict the number of transfers from a savings account to another account or to third parties, to a maximum of six per month (less the number of “ preauthorized transfers” during the month). Other account transfer restrictions may be described elsewhere.

AMENDMENTS AND TERMINATION - We may change any term of this agreement. Rules governing changes in interest rates are provided separately in the Truth-in-Savings disclosure or in another document. For other changes, we will give you reasonable notice in writing or by any other method permitted by law. We may also close this account at any time upon reasonable notice to you and tender of the account balance personally or by mail. Items presented for payment after the account is closed may be dishonored. When you close your account, you are responsible for leaving enough money in the account to cover any outstanding items to be paid from the account. Reasonable notice depends on the circumstances, and in some cases such as when we cannot verify your identity or we suspect fraud, it might be reasonable for us to give you notice after the change or account closure becomes effective. For instance, if we suspect fraudulent activity with respect to your account, we might immediately freeze or close your account and then give you notice. You agree to keep us informed of your current address at all times. Notice from us to any one of you is notice to all of you. If we have notified you of a change in any term of your account and you continue to have your account after the effective date of the change, you have agreed to the new term(s).

STATEMENTS - Your duty to report unauthorized signatures, alterations and forgeries - You must examine your statement of account with “ reasonable promptness.” If you discover (or reasonably should have discovered) any unauthorized signatures or alterations, you must promptly notify us of the relevant facts. As between you and us, if you fail to do either of these duties, you will have to either share the loss with us, or bear the loss entirely yourself (depending on whether we used ordinary care and, if not, whether we substantially contributed to the loss). The loss could be not only with respect to items on the statement but other items with unauthorized signatures or alterations by the same wrongdoer.

You agree that the time you have to examine your statement and report to us will depend on the circumstances, but will not, in any circumstance, exceed a total of 30 days from when the statement is first sent or made available to you.

You further agree that if you fail to report any unauthorized signatures, alterations or forgeries in your account within 60 days of when we first send or make the statement available, you cannot assert a claim against us on any items in that statement, and as between you and us the loss will be entirely yours. This 60-day limitation is without regard to whether we used ordinary care. The limitation in this paragraph is in addition to that contained in the first paragraph of this section.

Your duty to report other errors - In addition to your duty to review your statements for unauthorized signatures, alterations and forgeries, you agree to examine your statement with reasonable promptness for any other error - such as an encoding error. You agree that the time you have to examine your statement and report to us will depend on the circumstances. However, such time period shall not exceed 60 days. Failure to examine your statement and report any such errors to us within 60 days of when we first send or make the statement available precludes you from asserting a claim against us for any such errors on items identified in that statement and as between you and us the loss will be entirely yours.

Errors relating to electronic fund transfers or substitute checks - For information on errors relating to electronic fund transfers (e.g., computer, debit card or ATM transactions) refer to your Electronic Fund Transfers disclosure and the sections on consumer liability and error resolution. For information on errors relating to a substitute check you received, refer to your disclosure entitled Substitute Checks and Your Rights.

ACCOUNT TRANSFER - This account may not be transferred or assigned without our prior written consent.

DIRECT DEPOSITS - If we are required for any reason to reimburse the federal government for all or any portion of a benefit payment that was directly deposited into your account, you authorize us to deduct the amount of our liability to the federal government from the account or from any other account you have with us, without prior notice and at any time, except as prohibited by law. We may also use any other legal remedy to recover the amount of our liability.

TEMPORARY ACCOUNT AGREEMENT - If this option is selected, this is a temporary account agreement. Each person who signs to open the account or has authority to make withdrawals (except as indicated to the contrary) may transact business on this account. However, we may at some time in the future restrict or prohibit further use of this account if you fail to comply with the requirements we have imposed within a reasonable time.

SETOFF - We may (without prior notice and when permitted by law) set off the funds in this account against any due and payable debt you owe us now or in the future, by any of you having the right of withdrawal, to the extent of such persons’ or legal entity’ s right to withdraw. If the debt arises from

a note, “ any due and payable debt” includes the total amount of which we are entitled to demand payment under the terms of the note at the time we set off, including any balance the due date for which we properly accelerate under the note.

This right of setoff does not apply to this account if prohibited by law. For example, the right of setoff does not apply to this account if: (a) it is an Individual Retirement Account or similar tax-deferred account, or (b) the debt is created by a consumer credit transaction under a credit card plan (but this does not affect our rights under any consensual security interest), or (c) the debtor’ s right of withdrawal only arises in a representative capacity. We will not be liable for the dishonor of any check when the dishonor occurs because we set off a debt against this account. You agree to hold us harmless from any claim arising as a result of our exercise of our right of setoff.

CONVENIENCE DEPOSITOR (Individual Accounts only) - A single individual is the owner. The convenience depositor is merely designated to conduct transactions on the owner’ s behalf. The owner does not give up any rights to act on the account, and the convenience depositor may not in any manner affect the rights of the owner or beneficiaries, if any, other than by withdrawing funds from the account. The owner is responsible for any transactions of the convenience depositor. We undertake no obligation to monitor transactions to determine that they are on the owner’ s behalf.

The owner may terminate the authorization at any time, and the authorization is automatically terminated by the death of the owner. However, we may continue to honor the transactions of the convenience depositor until: (a) we have received written notice or have actual knowledge of the termination of authority, and (b) we have a reasonable opportunity to act on that notice or knowledge. We may refuse to accept the designation of a convenience depositor.

RESTRICTIVE LEGENDS - The automated processing of the large volume of checks we receive prevents us from inspecting or looking for special instructions or “ restrictive legends” on every check. Examples of restrictive legends placed on checks are “ must be presented within 90 days” or “ not valid for more than $1,000.00.” For this reason, we are not required to honor any restrictive legend placed on checks you write unless we have agreed in writing to the restriction. We are not responsible for any losses, claims, damages, or expenses that result from your placement of these or other special instructions on your checks.

PAYMENT ORDER OF ITEMS - The order in which items are paid is important if there is not enough money in your account to pay all of the items that are presented. The payment order can affect the number of items overdrawn or returned unpaid and the amount of the fees you may have to pay. To assist you in managing your account, we are providing you with the following information regarding how we process those items.

We process all credits (deposits) before processing debits (withdrawals). Debits are processed in the following order: Scheduled transfers (this includes internet banking and preauthorized transfers), Misc. Debit Tickets, Wire Debits, POS, ATM, ACH & Telephone/Internet Banking express transfers, checks and similar items. Transactions are posted by category in lowest to highest dollar amount for the day on which they are processed, with the exception of checks, which are posted in numerical order for the day on which they are processed (items without check numbers post first).

If a check, item or transaction (other than an ATM or one-time debit card transaction) is presented without sufficient funds in your account to pay it, we may, at our discretion, pay the item (creating an overdraft) or return the item for insufficient funds (NSF). The amounts of the overdraft and NSF fees are disclosed elsewhere, as are your rights to opt in to overdraft services for ATM and one-time debit card transactions, if applicable. We encourage you to make careful records and practice good account management. This will help you to avoid creating items without sufficient funds and potentially incurring the resulting fees.

FACSIMILE SIGNATURES - Unless you make advance arrangements with us, we have no obligation to honor facsimile signatures on your checks or other orders. If we do agree to honor items containing facsimile signatures, you authorize us, at any time, to charge you for all checks, drafts, or other orders, for the payment of money, that are drawn on us. You give us this authority regardless of by whom or by what means the facsimile signature(s) may have been affixed so long as they resemble the facsimile signature specimen filed with us, and contain the required number of signatures for this purpose. You must notify us at once if you suspect that your facsimile signature is being or has been misused.

CHECK PROCESSING - We process items mechanically by relying solely on the information encoded in magnetic ink along the bottom of the items. This means that we do not individually examine all of your items to determine if the item is properly completed, signed and indorsed or to determine if it contains any information other than what is encoded in magnetic ink. You agree that we have not failed to exercise ordinary care solely because we use our automated system to process items and do not inspect all items processed in such a manner. Using an automated process helps us keep costs down for you and all account holders.

CHECK CASHING - We may charge a fee for anyone that does not have an account with us who is cashing a check, draft or other instrument written on your account. We may also require reasonable identification to cash such a check, draft or other instrument. We can decide what identification is reasonable under the circumstances and such identification may be documentary or physical and may include collecting a thumbprint or fingerprint.

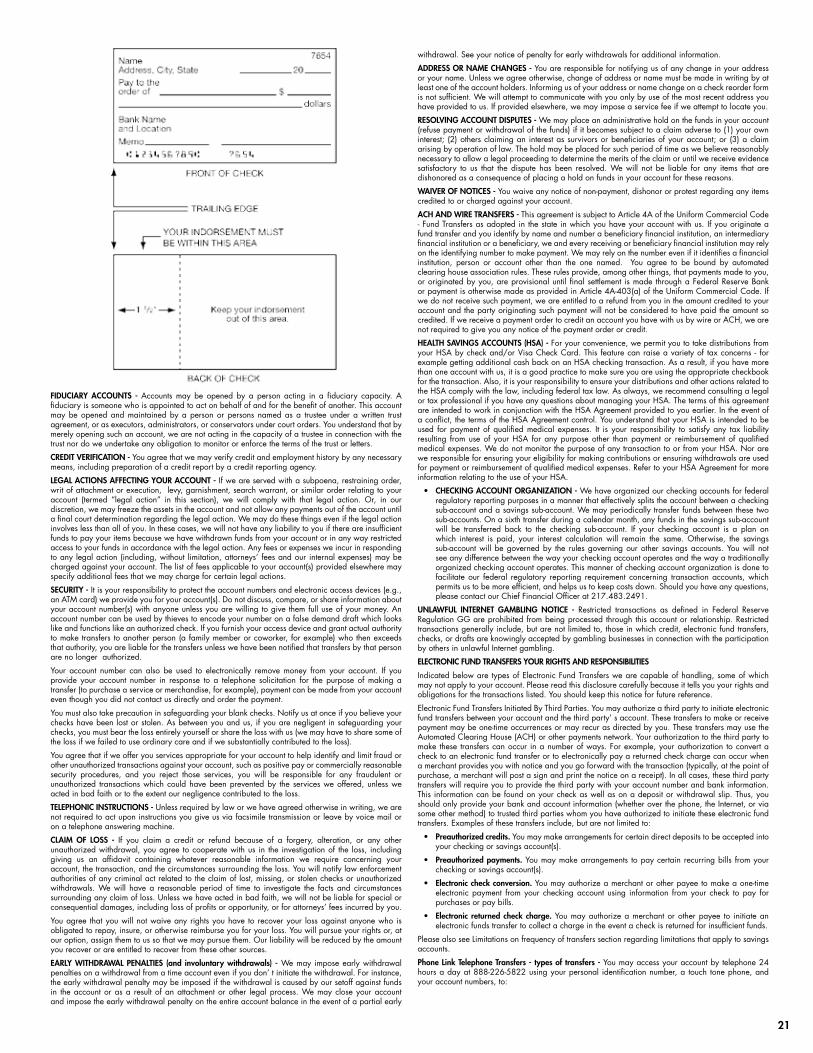

INDORSEMENTS - We may accept for deposit any item payable to you or your order, even if they are not indorsed by you. We may give cash back to any one of you. We may supply any missing indorsement(s) for any item we accept for deposit or collection, and you warrant that all indorsements are genuine.

To ensure that your check or share draft is processed without delay, you must indorse it (sign it on the back) in a specific area. Your entire indorsement (whether a signature or a stamp) along with any other indorsement information (e.g. additional indorsements, ID information, driver’ s license number, etc.)must fall within 1 1/2” of the “ trailing edge” of a check. Indorsements must be made in blue or black ink, so that they are readable by automated check processing equipment.

As you look at the front of a check, the “trailing edge” is the left edge. When you flip the check over, be sure to keep all indorsement information within 1 1/2” of that edge.

It is important that you confine the indorsement information to this area since the remaining blank space will be used by others in the processing of the check to place additional needed indorsements and information. You agree that you will indemnify, defend, and hold us harmless for any loss, liability, damage or expense that occurs because your indorsement, another indorsement or information you have printed on the back of the check obscures our indorsement.

These indorsement guidelines apply to both personal and business checks.

DEATH OR INCOMPETENCE - You agree to notify us promptly if any person with a right to withdraw funds from your account(s) dies or becomes legally incompetent. We may continue to honor your checks, items, and instructions until: (a) we know of your death or incompetence, and (b) we have had a reasonable opportunity to act on that knowledge. You agree that we may pay or certify checks drawn on or before the date of death or legal incompetence for up to ten (10) days after your death or legal incompetence unless ordered to stop payment by someone claiming an interest in the account.

855-822-5880 | UCBbank.com

Maximize your Everyday Points by combining points earned on your

credit card and debit card with UCB

The Leader ofCommunity Banking

What will you do with YOUR

EVERYDAY POINTS?

REWARD YOURSELF with UCB Debit & Credit Cards

*For more info on how to earn and redeem Everyday Points, please contact your local branch or visit

UCBbank.com/everydaypoints.

FIDUCIARY ACCOUNTS - Accounts may be opened by a person acting in a fiduciary capacity. A fiduciary is someone who is appointed to act on behalf of and for the benefit of another. This account may be opened and maintained by a person or persons named as a trustee under a written trust agreement, or as executors, administrators, or conservators under court orders. You understand that by merely opening such an account, we are not acting in the capacity of a trustee in connection with the trust nor do we undertake any obligation to monitor or enforce the terms of the trust or letters.

CREDIT VERIFICATION - You agree that we may verify credit and employment history by any necessary means, including preparation of a credit report by a credit reporting agency.

LEGAL ACTIONS AFFECTING YOUR ACCOUNT - If we are served with a subpoena, restraining order, writ of attachment or execution, levy, garnishment, search warrant, or similar order relating to your account (termed “legal action” in this section), we will comply with that legal action. Or, in our discretion, we may freeze the assets in the account and not allow any payments out of the account until a final court determination regarding the legal action. We may do these things even if the legal action involves less than all of you. In these cases, we will not have any liability to you if there are insufficient funds to pay your items because we have withdrawn funds from your account or in any way restricted access to your funds in accordance with the legal action. Any fees or expenses we incur in responding to any legal action (including, without limitation, attorneys’ fees and our internal expenses) may be charged against your account. The list of fees applicable to your account(s) provided elsewhere may specify additional fees that we may charge for certain legal actions.