what’s inside? - ibm www page · pdf filethe popularity of shared services delivery...

TRANSCRIPT

WHAT’S INSIDE?

Implementing Shared Services in the Public and Private Sector

Activity-Based Costing in the Public Sector

Using Activity-Based Costing to Optimize Production Capacity Utilization

Created for Chief Financial Officers, Controllers and other senior Finance professionals

Financial Management

Edition 3, Spring 2007

WHAT’S INSIDE?

Implementing Shared Services in the Public and Private Sector

Activity-Based Costing in the Public Sector

Using Activity-Based Costing to Optimize Production Capacity Utilization

IBMInsights

To receive this complimentary newsletter, to request previous editions, or to read other IBM thought leadership, please visit our Web site: www.ibm.com/services/ca/bcs

On the subscription form, you will have the option to request the newsletter in hard copy or as a PDF by e-mail.

2 IBM Financial Management Insights

Page 4Implementing Shared Services in the Public and Private SectorThe popularity of shared services delivery model has grown significantly over the years from traditional finance, HR and IT functions to supply chain, back office and expertise areas (e.g. tax, credit risk management).While the benefits of shared services have been established, its success depends on a sound implementationapproach. In this article, we look at some of the common concerns and recommend how we can address them.

Page 12Activity-Based Costing in the Public Sector ABC can assist managers in understanding the linkages between products and services and how they consumeresources (people, assets, dollars). Using IBM’s proven ABC methodology, our project team is working with a ministry of transportation to implement ABC in the division that is responsible for all driver and vehicle products.One of our key objectives – beyond the typical ABC benefits – is to assist the ministry in complying with the “Eurig” decision. Managers within the ministry now have access to a host of new information and metrics abouttheir operation that will ultimately lead to more informed decisions.

Highlights in this issue:

Page 16Using Activity-Based Costing to Manage SKU ProliferationRecently, a leading manufacturer of soft drinks and other beverage products faced a major capacity shortfall at one ofits facilities and needed to assess its capability to take on added business. Management’s challenge was to ‘find’ thisextra capacity without physically adding to facilities or using third party manufacturers. Our activity-based costinganalysis demonstrated that it was indeed able to take on the additional volumes, in part by instilling a disciplinedapproach to managing individual SKUs.

IBM Financial Management ServicesIBM Global Business Services is a leading business and technologyadvisor in Canada. Our Financial Management practice has a provenand successful history in helping CFOs and finance organizationsdesign and implement the financial processes and underlyingtechnologies required to overcome today's most complex businesschallenges. Whether a finance organization needs guidance in planningits business strategy, acquiring the tools to measure performance moreaccurately or leveraging shared services to streamline its operations,IBM can help.

We are focused on helping clients better integrate process, technologyand information to:� Drive enterprise-wide profit improvement and shareholder value;� Create a "finance on demand" organization that is responsive,

variable, focused and resilient; � Reduce the cost of finance through efficient transaction processing; � Provide decision-makers at all levels with the right information,

when and where they need it; and � Effectively manage risk and opportunity.

For further information, please contact:

TOM WHELANPartner Canadian Leader, Financial ManagementIBM Global Business ServicesTel: [email protected]

3IBM Financial Management Insights

Welcome to the 2007 issue of IBM Financial Management Insights, a newsletter for senior finance

professionals in business and government organizations. This newsletter is written by Canadian subject matter

experts for CFOs, VPs of Finance and Controllers who have a keen interest in current financial management issues

and are seeking creative ways to meet the increasing demands facing financial professionals. We understand your

need to become more effective in supporting core needs across the enterprise while maintaining regulatory

compliance. The good news is that you are not alone.

The articles in this issue focus on how private and public sector organizations can:

� Discover a successful approach to implementing shared services;

� Improve cost-effectiveness by using activity-based costing to understand linkages between products,

services and resource consumption; and

� Optimize production capacity utilization using activity-based costing for SKU analysis.

IBM Financial Management Insights

4 IBM Financial Management Insights

Implementing Shared Services in the Public and Private Sector:What it really means and strategies to successfullymanage the change in your organization

Written by LISA KNIGHT Senior Managing Consultant

5IBM Financial Management Insights

Introduction The concept of “shared services” is certainly well known, and it’s due

to the fact that it is not a new concept; shared services centres were first

implemented in the 1990s and numerous organizations around the world

have since implemented a shared services model.

The early adopters of shared services were in the consumer products

goods industry. However, shared services today is much more widely

used and currently there is a strong focus on shared services as a

delivery model within the banking sector and by governments globally.

While the impetus to move to shared services continues to vary, the

benefits are evident. Our IBM 2005 Global CFO Study indicated that

organizations that have successfully migrated to a shared services model

have been the most effective at implementing process and technology

improvements enterprise-wide. In other words, these organizations

have succeeded in implementing best practices through standardizing,

simplifying, and more cost-effectively delivering services.

Based on our IBM 2005 Global CFO Study*,organizations that have successfully moved to a shared services model have been the mosteffective at implementing the following process and technology improvements enterprise-wide:

Process• A standard chart of accounts• Standard policies and business rules• Use of functional best practices• Process simplification

Technology• Rationalized finance budgeting/forecasting tools• Reduced the number of common finance platforms• Reduced the number of ERP instances• Rationalized the number of data warehouses

* IBM Global Business Services, in collaboration with theEconomist Intelligence Unit, conducted the IBM 2005 GlobalCFO Study of 889 CFOs (over 350 CFOs/Deputy CFOs) andsenior Finance professionals to gain perspective on currenttrends, key challenges and the future direction of Finance.

6 IBM Financial Management Insights

A Wider ScopeWhat has changed since shared services models were first implemented

approximately 15 years ago is that the scope of functions involved in

shared services continues to expand. Traditionally, Human Resources,

Information Technology and heavily transaction-based Finance areas

(Accounts Payable, General Accounting and Reporting) were considered

for shared services. Today, the scope includes:

• More areas within the traditional HR, IT and Finance functions

(i.e., for Finance, fixed assets, accounts receivable, etc.);

• Supply Chain areas (e.g., procurement, catalog management,

warranty administration, etc.);

• Back office functions other than Finance (i.e., other operational

processing); and/or

• Expertise areas (e.g., tax, credit risk management, treasury, real

estate management).

For example, in the private sector area of banking, shared services

delivery models are being established for securities, loans, claims

processing and foreign exchange.

In addition to the broadening scope of shared services, more

organizations are adopting “enabling technology” such as scanning,

document workflow and storage tools to more effectively manage high

volumes of transactions. This helps them achieve greater control over

the transaction, both in terms of understanding the status of transactions

in a given process and in managing approvals of the transactions

(e.g., invoices in accounts payable).

What Hasn’t Changed: The People AspectOne thing that has remained constant is that once an organization

has made the decision to embark on shared services, the organizational

challenges in gaining acceptance are familiar. Implementing shared

services is a significant change to the organization. In addition, both

private and public sector organizations face many of the same challenges

even though the approach to addressing these challenges may differ.

The reality is that even if the changes are successfully made to implement

shared services (by addressing the potential improvements that can

be made in terms of processes, technology and organization), if the

‘people aspect’ is not paramount throughout the project, the shared

services centre will not be successful.

Change management is a critical component of success. This refers

to more than just communications and training (which are very

important). Change management is about helping all individuals

understand the change and its impact on them, then assisting them

through the change so they are successful in the new environment.

Unfortunately, based on IBM experience, change management

continues to be the most underestimated aspect of implementing

shared services. This is particularly the case in the public sector

where past failures of large projects often point to the lack of attention

focused on the change management aspects.

Addressing the change management aspects, or “people” aspect, is

by no means easy, so there is a low comfort level in addressing these

The most common concerns raised in implementing shared services are as follows:

• “Isn’t shared services just centralization…why all this effort to centralize our operations?”

• “How can there be any savings when we (the department) still need to approve everything and be accountable for the information;won’t establishing a shared service centre only fragment the process?”

• “Why does it take so much time and effort to transition to shared services; why can’t we just implement best practices in ourcurrent organization structure?”

• The perception that:o Their department is “unique”; their processes are substantially different than the other departments

(or business units) being considered for inclusion in the shared services centre.

o Departments being supported by the shared services centre will receive less service at a higher cost.

o It is necessary to retain a significant number of roles within the department or business unit rather than transition these roles to the shared services centre.

o There may be the possibility of a department or business unit to “opt out” of the shared services centre in the future.

o Their department/business unit will not be able to effectively manage their operations if they are required to move to a common ERP system instance.

7IBM Financial Management Insights

aspects amongst executives and senior staff. This is partially because

senior stakeholders understand the shared services concept at a high

level, while a true understanding of what it means to move to shared

services is not clear to them until implementation is underway. This

lack of clarity is often driven by the timeframe taken to assess the

feasibility of shared services, combined with the fact that centralization

and shared services are discussed interchangeably – even though

they are different service delivery models.

When embarking on shared services, similar concerns tend to surface

amongst both the private and public sectors. Individuals are trying to

grasp how the change affects them and their organization. It is

daunting to realize that the change is coming and it’s real. Hence,

a proactive focus on the people side of the implementation is required.

The challenge many organizations face is the difficulty of investing

money in this aspect of the implementation when there is often a focus

on minimizing project costs to realize the benefits. However, factored

into such a decision must be the implementation risks. The potential

risks range from losing key staff during implementation to an

unsuccessful implementation in spite of the dollars invested.

To assist customers in implementing shared services in their own

organizations and managing the change to shared services, a look

at the most common concerns that surface are highlighted below.

However, what is key are the strategies needed to successfully address

these concerns. We have provided a recommended approach based

on our experience with both private and public sector organizations.

1The question of: “Isn’t shared servicesjust centralization? Why all this effortto centralize our operations?”

Frequently, there is confusion amongst those impacted as to what

shared services means, because it is viewed as synonymous with

centralization. Therefore, it is important to take a step back to ensure

all employees truly understand what shared services is, what it really

means, and why this is a significantly different service delivery model

than their current organizational structure.

Recommended Approach

(public and private sector companies):

To address this problem, you should first discuss the similarity and

differences between shared services and centralized and decentralized

models so it is clear what shared services really is.

Second, you should explain that another key advantage of shared

services is a more disciplined approach to service delivery. This delivers

visibility to the costs for the services delivered, as well as the level

of service delivered, and ensures that clear accountability and

performance targets are defined (through a service level agreement).

People & Culture

Processes & Controls

OrganizationTechnology

• Lean, Flat, Organization

• Business Unit Maintains Control of Decisions

• Responsive to Clients Needs

• Common Systems & Support

• Consistent Standards & Controls

• Economics of Scale

• Independent of Business

• Synergies

• Dissemination of Best Practices

• Variable Standards

• Different Control Environment

• Higher Costs

• Duplication of Effort

• Remote from Business

• Unresponsive

• No Business Unit Control of Central Overhead

• Inflexible to Business Unit Needs

DecentralizedShared

Centralized

Shared services combines the benefits of both centralized and decentralized operationsto deliver value to business partners; it is the result of bundling business support

processes and non-strategic activities across an organization.

All levers of change must be addressed (particularly people and culture) when implementing shared services.

2 The question of: “How can there beany savings when we (the department)still need to approve everything and be accountable for the information? Won’t the establishment of a sharedservices centre only fragment theprocess?”

When the current process is working, it can be challenging to visualize

how it can be more effective, particularly from an individual department

perspective. The other factor that drives this concern is the lack of

control over the entire process in the future. Since traditionally

transactional-based activities move to a shared services centre, the

departments will retain some process aspects but fewer than before,

while the shared services centre manager will be responsible for

the other process aspects. What remains unchanged is that the

accountability remains with the departments; hence, this can create

a high level of discomfort.

Recommended Approach:

There is a fundamental transformation in shifting from a centralized

or decentralized model to shared services – which initially may not

be obvious. Rather than focusing on work from functional or individual

tasks, an end-to-end process perspective is taken. For example, rather

than having separate procurement and accounts payable functions,

it would make sense to have a Procure-to-Pay structure where the

two organizations physically and organizationally work together.

As we examine the processes themselves, the ‘future state’ incorporates

both process and technology best practices. So, in the case of accounts

payable, an optimal model could be to have all non-purchase order

invoices received centrally in one location, scanned into the system

and then, if the key information is acceptable in the ERP system,

the invoice is routed via workflow for approval. This represents a

substantial change in the process. With shared services, the processing

of invoices for multiple departments will be managed centrally.

3The question of: “Why does it take so much time and effort to transitionto shared services? Why can’t we just implement best practices in ourcurrent organizational structure?”

Even though many organizations seem to have embarked on some

degree of process improvement in recent years, improvements have

typically occurred in a particular department rather than across an

organization. Often, the degree of change in terms of what was actually

implemented compared to what was planned has been significantly

less as well. Conceptually, simplification, standardization and

reengineering of processes could be examined without moving

to a shared services model.

Procure to Pay Cycle

Purchasing - Dept #1

Purchasing - Dept #n

A/P - Dept #1

A/P - Dept #n

8 IBM Financial Management Insights

Central Services Unite.g. Accounting

Allocation of Costs

Departments or Business Areas/Units

Shared Services Centre

Cost and Value of Service

Departments or Business Areas/Units

Centralized Services Shared Services

Cost Unknown Cost Explicit

Shared services enables service delivery costs to be visible todepartments/business units and customers then associate actual costs with the

service provided. This is a key strength of shared services over a centralizedmodel. Service level agreements are established so that costs are explicit ad

service levels are known and agreed upon prior to any services being provided.This allows for greater accountability within the Shared Service Centre and

provides clear expectations for service delivery to customers.

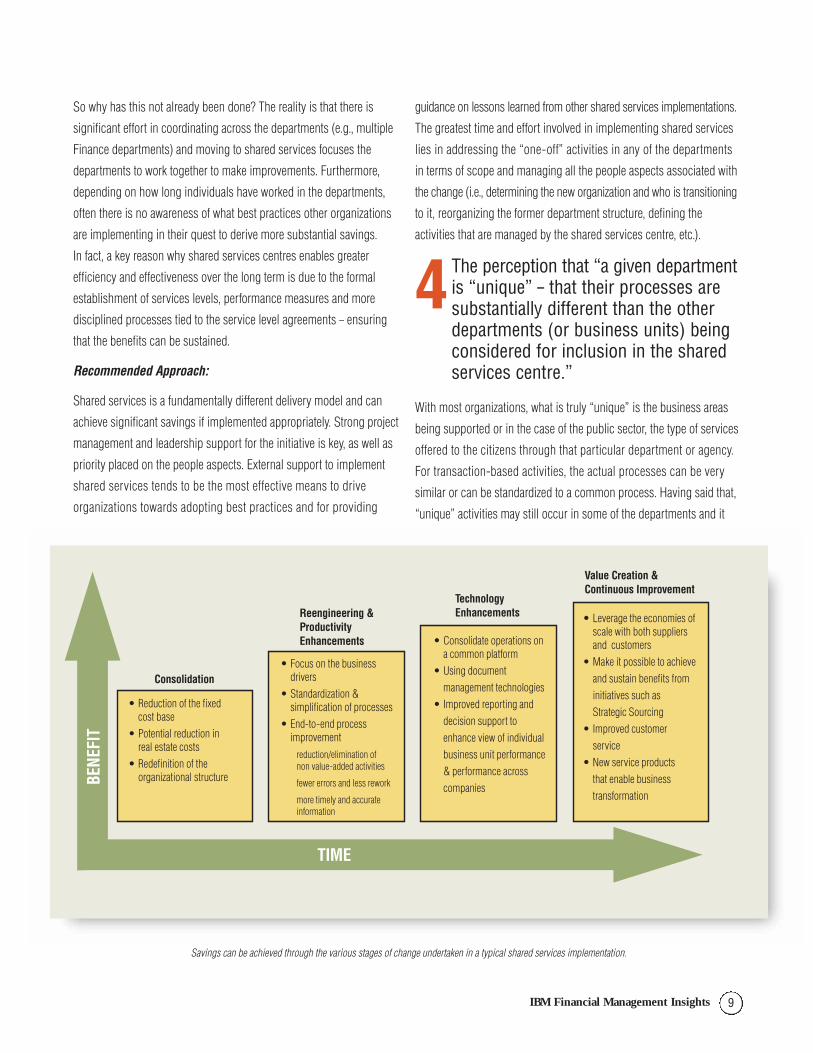

So why has this not already been done? The reality is that there is

significant effort in coordinating across the departments (e.g., multiple

Finance departments) and moving to shared services focuses the

departments to work together to make improvements. Furthermore,

depending on how long individuals have worked in the departments,

often there is no awareness of what best practices other organizations

are implementing in their quest to derive more substantial savings.

In fact, a key reason why shared services centres enables greater

efficiency and effectiveness over the long term is due to the formal

establishment of services levels, performance measures and more

disciplined processes tied to the service level agreements – ensuring

that the benefits can be sustained.

Recommended Approach:

Shared services is a fundamentally different delivery model and can

achieve significant savings if implemented appropriately. Strong project

management and leadership support for the initiative is key, as well as

priority placed on the people aspects. External support to implement

shared services tends to be the most effective means to drive

organizations towards adopting best practices and for providing

guidance on lessons learned from other shared services implementations.

The greatest time and effort involved in implementing shared services

lies in addressing the “one-off” activities in any of the departments

in terms of scope and managing all the people aspects associated with

the change (i.e., determining the new organization and who is transitioning

to it, reorganizing the former department structure, defining the

activities that are managed by the shared services centre, etc.).

4 The perception that “a given departmentis “unique” – that their processes aresubstantially different than the otherdepartments (or business units) beingconsidered for inclusion in the sharedservices centre.”

With most organizations, what is truly “unique” is the business areas

being supported or in the case of the public sector, the type of services

offered to the citizens through that particular department or agency.

For transaction-based activities, the actual processes can be very

similar or can be standardized to a common process. Having said that,

“unique” activities may still occur in some of the departments and it

• Reduction of the fixed cost base

• Potential reduction in real estate costs

• Redefinition of the organizational structure

• Leverage the economies of scale with both suppliers and customers

• Make it possible to achieve

and sustain benefits from

initiatives such as

Strategic Sourcing

• Improved customer

service

• New service products

that enable business

transformation

• Consolidate operations on a common platform

• Using document

management technologies

• Improved reporting and

decision support to

enhance view of individual

business unit performance

& performance across

companies

• Focus on the business drivers

• Standardization & simplification of processes

• End-to-end process improvement

reduction/elimination of non value-added activities

fewer errors and less rework

more timely and accurate information

Consolidation

TIME

BEN

EFIT

Reengineering &Productivity Enhancements

TechnologyEnhancements

Value Creation &Continuous Improvement

Savings can be achieved through the various stages of change undertaken in a typical shared services implementation.

9IBM Financial Management Insights

will need to be determined how those activities will be managed in the

future. However, this is often a small number; the majority of activities

can follow a common process. The perception often ties to service

levels as well, with the main concern being the need to provide

“flexibility to customers.”

Recommended Approach:

Without a doubt, subject matter experts from each of the departments

need to be involved in defining what responsibilities will move to the

shared services centre and what will remain in the business. This is

important, not only because of their expertise but to also gain acceptance

of the changes being made. A clear definition of the criteria for inclusion

in the shared services centre needs to be developed upfront and utilized

in defining responsibilities. In addition, strong leadership is required

to ensure that what the shared services centre is managing is not

significantly reduced. In the consensus decision-making environment

of the public sector, this can be particularly challenging. However, the

consensus approach can only be used to a point; ultimately, the project

leadership may be required to make some tough decisions that may

not be popular with all the departments involved.

5 The perception that “departmentsbeing supported by the shared servicescentre will receive less service at ahigher cost.”

The greatest concern of department managers is that any of the work

that is transferred to the shared services centre will be of lower quality

or less customer focused than their department would deliver and that

they will have to pay a higher amount for the services received. This

fear is most substantial with departments that are smaller and will have

fewer people moving in the shared services centre. However, once a

decision is made to implement shared services, this concern can

become widespread as department managers realize that they will

be losing control of some of their department’s activities.

Recommended Approach:

The key to successfully managing this concern is ensuring that current

performance levels of the various departments are gathered. These

performance levels indicate the volume of transactions processed in

each of the departments in addition to the service levels currently

being provided. Without this baseline, there is the risk of departments

viewing their individual performance levels prior to shared services

as being superior to the shared services centre. Furthermore, this

baselining is necessary in terms of defining what service levels will

be provided to the departments in the future and what the costs for

the services will be.

6 The perception that “it’s necessary to retain a significant number of roleswithin the department or business unitrather than transition these roles to theshared services centre.”

Once again, as the “rubber hits the road” and implementation becomes

a reality, there is an increased concern over the loss of control over

activities and the level of support that will be received by the

departments in the future. Suddenly, there is a desire to revisit FTEs

that are being considered for the shared services centre and a multitude

of reasons surface as to why some of these resources must remain

in the group. There is a fine line distinguishing between the support

required for the “unique” activities that will remain in the department

and the activities that will be transferred to the shared services centre.

This is an important distinction and strong leadership is once again

required for these decisions. Otherwise, the shared services model

will be sub-optimized if much of the staff and work remain in the

departments.

Recommended Approach:

The first step is to clearly define what is going to be transferred to the

shared services centre. Depending on the desired culture for the shared

services centre, the physical location and a number of other factors,

the actual staff being considered for the positions may vary. However,

a number of things are necessary: a net reduction in the departments

the shared services centre will support; a reorganization of responsibilities

retained by the departments; defining the number of FTE; and roles

and responsibilities within the shared services centre. In a unionized

environment, this will be driven by the union agreements and therefore

is more complex to address both in terms of responsibilities being

transferred into the centre and the unionized individuals affected.

Having said that, shared services centres have been established

successfully in unionized environments. However, union involvement

and agreement at the outset is a critical success factor.

10 IBM Financial Management Insights

7The concern that there may be thepossibility of a department or businessunit “opting out” of the shared servicescentre in the future.

This concern arises most prevalently when shared services is

implemented by departments, business units, regions, or countries

in different “waves” or phases. Departments in the first phase are

very concerned that they will be required to be part of this significant

change but departments in later phases may not be mandated to do so.

This comes back to the executive leadership supporting the project. If

the desire is to truly implement a shared services model, an “opt out”

option will only be to the detriment of the planned benefits in the

business case.

Recommended Approach:

Typically, those departments viewed as being at higher risk for

implementation problems (note that criteria needs to be established

for this decision) will be addressed in later phases, as it is essential to

have initial success with the shared services centres, and then address

the more complex departments. The service level agreements should

stipulate whether “opting out” is ever an option; however, this is not

recommended.

8 The perception that their department/business unit “will not be able toeffectively manage their operationsif they are required to move to a“common” Enterprise ResourcePlanning (ERP) system instance(which is typically a common, non-customized configuration).”

This is of great concern, particularly in organizations where multiple

ERPs/multiple instances of an ERP are currently used and when

flexibility was given in the past to customize some aspects of the

system. Again, the objection is that “things are fine now but we won’t

support moving to shared services unless the new system has the

same customization.” The reality is that the benefits that are derived

from technology in the shared services business case are a combination

of moving to a common ERP/common instance and lower maintenance

costs and upgrade costs going forward. The only way to ensure this

happens is to minimize or eliminate the system customizations, even

though this is not a popular option.

Recommended Approach:

Many of the ERP systems (particularly Finance modules) are very

advanced, with new features being provided in each release. Hence,

there is a significant amount of inherent flexibility. Often the departments

in scope are not aware of this, so early education during the project is

required to answer the question, “Will the system work the way the

current processes are designed?” The answer is, “Not necessarily,

particularly if the common ERP system selected is different than what

is currently used in a given department.” That’s why there is a need to

re-examine the way things are done today and incorporate best practices

into the new processes which align with the systems. This change,

combined with enabling technology, should address many concerns.

The “one-off” customizations that aren’t covered by the “out-of-box”

ERP system can be looked at, but typically a hard line is taken (e.g.,

if there is even consideration of a system customization particularly

department specific, consideration will be given to having that department

incur a greater portion of maintenance and upgrade costs).

ConclusionAddressing organizational challenges early, understanding what

concerns typically arise, and having strategies to overcome them are

key. Placing priority on change management aspects helps to mitigate

risks associated with the loss of key personnel during implementation.

Process, technology and organizational aspects are necessary to

achieving business case benefits – but ultimately, what matters most

in successfully implementing shared services is properly addressing

the “people aspects.”

11IBM Financial Management Insights

ABC: THE KEYDIFFERENCE BETWEENPRIVATE AND PUBLICSECTOR CLIENTSAs an ABC practitioner with a focus on the public sector, one of

the questions I frequently encounter is, “What is the key difference

between private sector and public sector clients?” The most significant

difference is the legal implications of “total cost” for publicly mandated

products and services. In simple terms, governments cannot make a

profit on mandated services. An example of this would be regular

license plates. Since all vehicles require them, the cost attributed to

the plate should equal the price being charged; however, for custom

or “vanity” license plates, governments are free to set the price without

consideration of the cost incurred to create and deliver the product,

since it is the consumer’s choice to buy this type of specialty plate.

In all jurisdictions in Canada, this distinction stems from a Supreme

Court of Canada ruling from October 1998, Eurig vs. The Registrar

of the Ontario Court (General Division) and The Attorney General for

Ontario. In this case, Marie Eurig – as executor for her late husband’s

estate – refused to pay the applicable probate fee, contending instead

that the fee was, in fact, a tax.

IS IT A TAX, OR A FEE-FOR-SERVICE?The primary distinction between a tax and fee-for-service is that taxes

raise government revenues and fees defray the cost of providing the

service or the cost of regulation. The government must be able to

demonstrate what it costs to provide a service or to perform a regulatory

function by supplying analysis and documentation of how government

resources are consumed in the process.

13IBM Financial Management Insights

ACTIVITY-BASED COSTINGIN THE PUBLIC SECTORWritten by CHRIS REDMONDSenior Managing Consultant

USING ABC METHODSIn selecting ABC as their preferred costing methodology, clients

can expect that it will:

• Inform managers about the full cost of current processes,

and the drivers of those costs;

• Reveal opportunities for business process improvements

and re-engineering;

• Provide benchmarking internally and in relation to other

organizations/jurisdictions;

• Reveal the costs of complexity and uniqueness;

• Promote a cross-functional look at how products and

services are delivered;

• Set target costs;

• Determine performance measurement

(quality, efficiency and cost) criteria; and

• Provide feedback on “Eurig” tests

(see more in “The Key Difference,” below).

In one of our engagements, most line managers were able to

quote the price they charged for providing certain transactions

but had no idea of what it cost to process that transaction. In

addition, there was no linkage to activities being consumed

by the Cost Objects (in this case, products and services).

In our experience, models range from transaction-oriented

processing to areas that provide advice and consulting services

to other parts of the government. In this respect, governments

are similar to the private sector since they have both internal

and external customers.

Upon examination of the fees in question in the Eurig case, the Court

concluded that they were, in fact, taxes since there was no consideration

of the activities and costs associated with the service of granting the

probate; the larger the estate the greater the fee (tax).

Since the statute did not expressly authorize the imposition of taxes,

the taxes were inconsistent with Section 53 of the Constitution Act

1867, and therefore, unconstitutional.

As a result of the Eurig case, all governments in Canada must now

understand and document all costs associated with the myriad of

products and services that are mandated for public consumption

to protect itself from similar legal actions.

HOW IBM’SMETHODOLOGY CAN HELPOne of the key objectives – beyond the typical ABC benefits – would

be to determine the effect of the Eurig decision with respect to existing

costing and pricing practices.

Working with subject matter experts, we document and understand the

required linkages between products and services offered to the public,

and the work activities and resources that they consume.

Diagram 1 illustrates the “bottom up” concept of consumption where

Cost Objects consume Activities, as defined through Activity Drivers,

and Activities consume Resources (dollars, time, assets) through

Resource Drivers.

In order to provide visibility into certain categories of cost, we segment

the resources into user-defined resource pools. This facilitates the

simplification of resource drivers in terms of logic and the number

required to show the linkage between different resources and activities.

For example, a resource pool called “Labour” can be expected to reflect

the cost of salaries, wages and benefits; however, it also contains costs

for office supplies, telephone and similar expenses. The logic behind

this grouping reflects the fact that those costs behave in the same

manner as the consumption of labour in performing the respective

activities.

Resource drivers show causal linkages that illustrate the relationship

of how activities consume the resources. This linkage is defined by the

people responsible for the work, but generally reflects the percentage

of time spent on performing specific activities by all people directly

or indirectly involved in the process.

14 IBM Financial Management Insights

Resources

ABCTrace costs based on their demand

for activities

Resource Driver

Activities

Activity Driver

Cost Objects

Diagram 1

During activity workshops, we work with a cross-section of staff to

document and understand the activities that are performed to create

their Cost Objects. Our sessions vary from leveraging process maps,

to story boarding, to just having a person tell us what they do. The

documentation of these activities would be an integral part of the

process of demonstrating fees for service as it relates to the Eurig

decision.

The next step in the process is to identify the linkage between the defined

activities and the products or services they create. This linkage helps

to distinguish a fee which relates to the cost of goods and services

provided, versus a tax where the fee is not related to the cost of goods

and services.

Activity drivers measure the frequency, complexity, and duration of

performing an activity one time, for a specific Cost Object. Let’s look

at a department that is responsible for processing public requests

relating to commercial vehicles in any provincial government. The

activity of processing an “Oversize/Overweight Permit” used by large

commercial vehicles will not always consume the same amount of effort,

depending on the different type of vehicle it is being processed for.

Where multiple types of permits exist, the activity needs to be analyzed

to see if it is performed equally for all Cost Objects. In our example,

a Single Trip Permit may require five minutes of effort to process, but

a “Wide Load” Permit may take 60 minutes to complete since there are

many additional steps in determining allowable routes based on bridge

reports for clearance and gross vehicle weight allowances. In this case,

the cost consumed for a Wide Load Permit is 12 times greater than

it is to perform the same activity for a Single Trip Permit.

Another key component of work is the documentation and linkage of

previously unrelated costs from an organizational standpoint. Amounts

that were previously viewed as another department’s costs and

considered unrelated to a product may now be linked via a deeper

analysis of the cause and effect of a product’s consumption. Typical

examples are costs associated with Information Technology, Corporate

Finance and Human Resources. Organizationally, these costs belong

to other divisions and may have been viewed as overhead. By examining

the costs of the Information Technology area, we are able to identify

and document transactional-level relationships of what is being

processed by the various automated systems being maintained. This

linkage can show that these previously defined overhead costs can

be viewed as a direct cost in the provision of specific products and

services. These systems can be integral for processing transactions

at the counter, at the kiosk or over the Internet.

SUMMARY OF BENEFITSManagers now have access to a host of new information and metrics

about their operation that will ultimately lead to more informed decisions.

The following list summarizes the benefits of ABC derived to date:

• Informs managers of absolute and relative cost

of a product or service;

• Identifies cost and unit cost of activities;

• Shows activities used to produce a product/service

(bill of activities);

• Reveals number of people doing each activity;

• Identifies gaps in the organization;

•Reveals opportunities for business process improvement

and reengineering;

• Reveals costs of complexity and uniqueness; and

• Assists with the determination of Eurig compliance.

While ABC can directly benefit managers in the private and public

sector alike, the attribution of costs for the “Eurig” analysis will

assist governments in determining the impact on their costing and

subsequent pricing of mandated products and services to the public

in the future.

15IBM Financial Management Insights

Using Activity-BasedCosting to ManageSKU Proliferation

16 IBM Financial Management Insights

Written by ROBERT TOROKExecutive Consultant

NOTE: This article is based on the author’s experience with a leading global consumer packaged goods manufacturer.All financial and operational data has been disguised to preserve confidential and competitively sensitive information.

Recently, a leading manufacturer of consumerpackaged goods faced a major capacityshortfall at one of its facilities. Its largestcustomer, extensively served through thisparticular facility, was planning for a substantialincrease in sales and approached themanufacturer to assess its capability to take on the added business.

Management’s challenge was to ‘find’ thisextra capacity without physically adding tofacilities or using third party manufacturers.

To understand the context of this challenge, it is important to note that this company’sproducts shared a number of key

characteristics with similar products in theindustry, such as:

• Low unit cost/value;

• High unit weight (relative to cost or value)since the major ingredient is water;

• Large unit size (again relative to cost orvalue);

• Transportation challenges; in otherwords, both bulk and individual packagequality can degrade when shipped longerdistances (generally accepted in theindustry as being no more than roughlyone day’s distance by truck);

• Highly seasonal sales patterns, i.e., muchhigher sales in certain seasons than atother times, and further emphasized by regional climate differences;

• Capital-intensive production that requiresdedicated equipment by package size;

• High turnover (at the retail level, often the product line with the highest turnover);and

• Very similar direct unit costs within agiven package size, i.e., costs vary moreby size than by brand or flavour (singleserve items vs. 1 litre or 2 litre bottles, etc.).

Finding Extra Capacity: Background Information

The combination of these characteristics

means that manufacturers are generally

reluctant to add physical capacity to their

plants, and thus seek to maximize existing

facilities, often relying on third-party

manufacturers (“co-packers”) – contracted for

‘spike’ volumes or to serve customers distantly

located from core manufacturing facilities.

In this particular case, plant management

viewed its manufacturing facility to be at or

very close to capacity, producing almost 17

million units/year spread across approximately

400 SKUs1 , already operating on a 24/7

basis in and around peak season.

While some production could be shifted from

peak season to shoulder or even off-season,

that option brings with it accompanying

inventory storage challenges (cost, degradation

of quality, and reliance on dubious forecasting

accuracy). That is why management needed

to find capacity without physically adding to

their facilities or using co-packers.

Hypothesis and Key DataOne hypothesis that management put forward

was that certain SKUs were likely to be

unprofitable in their own right and thus their

elimination might free up capacity. This

hypothesis is what the author was engaged

to analyze. Activity-based costing analysis

was undertaken to identify the least profitable

SKUs, based on the following definitions and

categories agreed upon by the plant, the sales

organization, and the author/consultant

(A being the highest volume items, D the

lowest):

• Single serve SKUs:

A > 52,000 cases sold per year,

D < 4,000, with B and C in between;

• Multiple Serving SKUs

(1, 2, and 3 litre bottles):

A > 36,000 cases sold per year,

D <11,000, with B and C in between.

While the above data clearly suggested both a

serious problem and an opportunity, the next

question was to determine the costs associated

with the most obvious inefficiencies of the ‘D’

SKUs, and to a lesser extent, the ‘B/C’ ones

as well. The first step in this analysis was to

identify the key activities that were performed

at different levels of the business, such as:

• SKU: Product line change-over, largely

consisting of a new supply of single

serve packaging materials which arrive

pre-labeled by brand and flavour (empty

bottles are identical for all brands and are

labeled during production), clean-out of

preparation and production equipment,

and certain new raw materials;

• Package Size: Production line change-

over, largely consisting of line change-

over from one size to another 4;

• Brand: Consists of many elements but

certainly includes all the SKU changes,

likely the package size changes, and new

labels for bottles. This also includes the

periodic redesign of labels as logos

change and/or as regulatory requirements

for label information change.

As is the case with virtually all manufacturing

processes, every time a production line

changes, some type of loss is experienced.

At a minimum, it is simply time; in this case,

in addition to time (the most valuable

commodity here), raw materials are lost

as they are flushed out during the cleaning

process.5 This is referred to as yield loss,

and what was considered relevant was not

the absolute amount (some, of course, is

inevitable) but the relative amounts across

SKU types. We defined yield loss as the

number of cases of finished product that

would have been produced with the raw

material lost during a flavor change-over,

17IBM Financial Management Insights

Single 1 Litre 2 Litre 3 Litre Serve2 Bottles Bottles Bottles

# of ‘A’ SKUs 38 19 22 4

# of ‘B/C’ SKUs 57 18 26 9

# of ‘D’ SKUs 16 37 41 12 Average Annual 217 151 174 50Sales of ‘A’ SKUs3

Average Annual 35 16 18 21Sales of ‘B/C’ SKUs3

Average Annual 4 4 2 3Sales of ‘D’ SKUs3

Average Length of 5.0 4.3 4.0 4.0Production Run3 ‘A’

Average Length of 2.3 1.2 1.0 1.9Production Run3 ‘B/C’

Average Length of 1.8 0.7 0.7 1.2Production Run3 ‘D’

expressed as a percentage of total cases

produced. For example, 7,798 cases’ worth

of ingredients was lost during change-overs

within the 1 litre package size for ‘A’ items;

this represents a loss of 0.23% of cases

produced.6 For ‘B/C’ items, the equivalent

figure was 3,312 cases, but with a significantly

greater percentage loss at 0.79%.

Next, the team calculated the efficiency-loss

ratio; namely, the number of cases lost as per

the yield analysis and divided by the total

number of cases produced in that production

run (using averages). As above, the 7,798

cases lost represented about 5.09% of the

1 litre cases produced.

Continuing the format of the above table,

here is what was found:

Two major conclusions can bedrawn from these two tables:

1. The yield loss increases very substantially

as one moves from A to B/C and especially

to D items. Essentially, the yield loss on D

items is 2.5 to 5 times greater than for A

items. Similar results are seen for the

efficiency loss ratio.

2. The average length of an A production run

is 2.5 to 6 times longer than for a D item,

leading to much higher efficiency losses for

D items relative to A items.

Based principally on this data, the team was able to determine the relative costs of A, B/C, and Dcategory SKUs:

• Single Serve: D items cost 6 to 12 cents

more per case to produce than A items,

plus an additional 1 to 2 cents in yield loss.

• 1 Litre bottles: D items cost 50 to 80 cents

more per case to produce than A items,

plus an additional 2 to 4 cents in yield loss.

• 2 Litre bottles: D items cost 22 to 36 cents

more per case to produce than A items, plus

an additional 1 to 2 cents in yield loss.

Initial ConclusionsThe operational data clearly demonstrated

that D SKUs were particularly inefficient and

relatively high cost to produce. In addition,

a number of semi-fixed and fixed costs were

being incurred to create and maintain these

SKUs. While the same costs were incurred

for all other SKUs as well8, due to the lower

volumes, the ‘amortization’ of these costs

generated a much higher per case cost for

the D items.

Therefore, the initial conclusion was that

the facility would be more profitable if it

manufactured a greater volume of A SKUs

instead of D SKUs, but this was hardly

actionable information. That’s because

eliminating SKUs that are profitable – as most

of the D SKUs were, albeit significantly less

so than A items – might reduce profitability as

well as alienate the customers of those SKUs.

Extension of AnalysisAs a result, the analysis was extended to

review specific D SKUs with the view to

determine the likely impact of their elimination.

These results were somewhat surprising,

as shown by these five examples:

1. Brand A, Flavour 1:

Sold in a 2 litre bottle as well as two different

single serve package formats, all D items.

2. Brand 2, Flavours 2, 3, 4, 5, and 6:

Each sold in a 2 and 3 litre bottle as well as

one single serve package format, all D items.

3. Brand 3, Flavour 2:

Sold in a 2 litre bottle as well as two different

single serve package formats, all D items.

4. Brand 4, Flavour 2:

Sold in a 2 litre bottle (D SKU) as well as

three different single serve package formats

(two of which were B/C and one was a D

SKU).

5. Brand 5, Flavour 6:

Sold in a 2 litre bottle and two single serve

package formats (A SKUs), a third single

serve format and 3 litre bottle (both B/C),

and a 20 ounce bottle (D).

18 IBM Financial Management Insights

Single 1 Litre 2 Litre 3 Litre Serve7 Bottles Bottles Bottles

Yield loss from ‘A’ 0.30% 0.23% 0.18% 0.16%

Yield loss from ‘B/C’ 0.56% 0.79% 0.68% 0.34%

Yield loss from ‘D’ 0.74% 1.30% 0.92% 0.53%

Efficiency loss from ‘A’ 6.7% 5.1% 4.7% 4.0%

Efficiency loss from ‘B/C’ 12.9% 18.2% 18.0% 8.5%

Efficiency loss from ‘D’ 16.4% 29.8% 25.8% 13.3%

19IBM Financial Management Insights

In other words, it was not the individual SKU

that was inherently unprofitable. Rather, while

the total volume of many brand-flavour

combinations was at the A or B volume levels,

the sheer number of packages offered made

most of the individual SKUs appear to be poor

performers.

This led the team to the next question: if

certain SKUs (i.e. brand-flavour-package

combinations) were eliminated, would those

sales be lost or would they migrate to other

package sizes within the same brand-flavour?

This of course is a sales or marketing question,

not one likely to be adequately answered by

a team of cost accountants! But it does

demonstrate the linkage and importance of

ABC to other parts of the business.

The team then reviewed what became known

as the ‘package proliferation problem’ across

every brand-flavour combination, in order to

identify situations where a substantial volume

migration/retention could be expected. The key

assumption to volume retention was that

consumers of 2 and 3 litre bottles would not

migrate to 1 litre or single serve formats and

vice versa (the former being ‘take-home’

products and the latter generally being

consumed immediately), while consumers

of single serve formats required at least one

other such package format from which to

choose. The company assumed that a

consumer of a particular single serve package

would not switch brands just because the same

flavour was now sold in a different package

configuration (but still as a single serving).

Conclusions andLessons LearnedThis analysis enabled the team to determine

that the majority of ‘lost’ sales would in fact

not be lost, but simply transferred to other

package sizes. This allowed the facility to

reap a cascading set of benefits:

1The elimination of about 60% of the D

SKUs in the facility, and the associated

yield and efficiency losses, as well as

related soft costs associated with inventory,

obsolescence, materials management, etc.

2The migration of about two-thirds of

the eliminated sales volume to other

package sizes, effectively boosting the

sales volumes of a number of remaining D

SKUs and some C SKUs. This meant that

almost 90% of the original D SKUs were

either eliminated or now produced in C

or better volumes.

3The creation of approximately 7% more

production capacity than had existed

previously (over and above the

incremental migration volumes noted above),

through the elimination of the D efficiency

losses as well as a portion of the C efficiency

losses.

4Although a ‘softer’ benefit, there was a

material simplification in the facility’s

business and an opportunity to reduce

indirect expenses or take on additional

volumes at current indirect expense levels.

Most importantly, the facility was able to

demonstrate to its key customer that it was

indeed able to take on the additional volumes,

in part by instilling a disciplined approach

to managing individual SKUs.

The application of this type of analysis can

easily be extended to virtually any industry

or product/service situation. The organization

must accept the key underlying philosophy

that complexity carries cost, not necessarily

measurable at the individual product or service

level, but very measurable in the aggregate;

furthermore, potential savings that are deemed

very small at the individual SKU level can

have dramatic business impact in total.9

The activity-based analysis allows an

organization to identify the specific work steps

pertaining to individual products/services and

groups of products/services. Then, one can

identify the costs that are expected to ‘go away’

should a SKU be eliminated. However, as this

example demonstrated, costs that do not ‘go

away’ might be better deployed by producing

more profitable products/services or even to

serve customers with greater potential.

1. An SKU is a single item at the manufacturer or retail level, in this case, a unique combination ofbrand, flavour, packaging, and unit size. For example, Flavour 1 manufactured under brand X,produced in a 1 litre bottle and sold as a single bottle is a different SKU from exactly the sameproduct sold as a 6-pack of single serve items. Each SKU is produced in volumes rangingfrom hundreds to tens of thousands of cases.

2. This manufacturer produced single serve items in a number of different formats, but theseare combined here for simplicity.

3. In thousands of cases4. Generally speaking, single serve SKUs are produced on one line and bottles on another,

with no sharing of assets between them until packages come off the line, at which timewarehouse transfer and subsequent assets are common.

5. No consumer wants to find traces of say honey mustard in a vinegar dressing (perhaps dueto health, allergy, religious, or other dietary restrictions).

6. Cases produced closely approximate cases sold but not exactly.7. This manufacturer produced single serve SKUs in a number of different formats, but these

are combined here for simplicity. 8. Examples of such costs – in order from semi-fixed to fixed - include production scheduling,

warehouse space for raw and finished goods, materials procurement and management, billof materials/formulation maintenance, and package development.

9. It was once said that “Just because peanuts are light does not mean you can carry a billion of them.” (author unknown).

Endnotes

This publication has been prepared by the IBM Global BusinessServices practice of IBM Canada Limited for general informationpurposes only and is not intended, and should not be construed, asprofessional advice or opinion. The information reflectsinterpretations and practices regarded as valid when published basedon available information at that time. Readers who are concernedabout the applicability of the information in this publication to theiractivities are advised to seek legal or professional advice based ontheir particular circumstances.

IBM and the IBM logo are trademarks or registered trademarks ofInternational Business Machines Corporation in the United States and are used under licence by IBM Canada Ltd.© Copyright IBMCorporation 2006. All rights reserved. Other company, product andservice names may be trademarks or service marks of others.

Oracle – a registered trade mark of Oracle International Corporation

EDITOR: EDMUND LEE Senior Managing Consultant IBM Global Business ServicesFinancial Management ServicesTel: [email protected]

20 IBM Financial Management Insights

OUTSOURCINGIS GOOD FOR THEBOTTOM LINE Today's business leaders are looking for innovative ways

to deliver shareholder value and bolster investor confidence.

Common strategies include implementing new management

practices, revitalizing business processes or engaging in

information technology outsourcing. Questions naturally

arise: Is there value in outsourcing information technology?

Will shareholders see the return? A study conducted by

scientists in the IBM Watson Research Center of companies

outsourced to a number of service providers says: "Yes!"

Long-term effects on companies that outsourced a major

portion of their IT infrastructure between 1998 and 2002

were investigated. Unlike previous research that relied on

the case-study approach, the IBM Research study is the first

to apply rigorous statistical analysis to measure the impact of

an outsourcing agreement on a company. The study concludes

that companies outperformed their peers on a long-term

basis in key business metrics, specifically SG&A expenses,

ROA and EBIT. Further the research indicates the larger

the outsourcing contract, the more likely the improvement

in bottom-line results. A summary of the study results

"Business Impact of Outsourcing — A Fact-Based Analysis"

and a video are available to download at www.ibm.ca