widening and diversifying sme financing through capital market

DESCRIPTION

This presentation was given at the Policy Dialogue: Financing SMEs: Sharing Ideas for Effective Policies which was held in Jakarta, Indonesia on 15-16 October 2014.Read more about the event: http://bit.ly/1VZsLcbTRANSCRIPT

Widening and Diversifying SME Financing

through Capital Market

Jae Ha PARK

Deputy Dean Asian Development Bank Institute

“Financing SMEs: Sharing Ideas for Effective Policies” Capacity Building and Training Workshop

Jointly organized by ADB Institute and Bank Indonesia

Jakarta, Indonesia, 15-16 October 2014 The views expressed in this presentation are the views of the author and do not necessarily reflect the views or policies of the Asian Development Bank

Institute (ADBI), the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms.

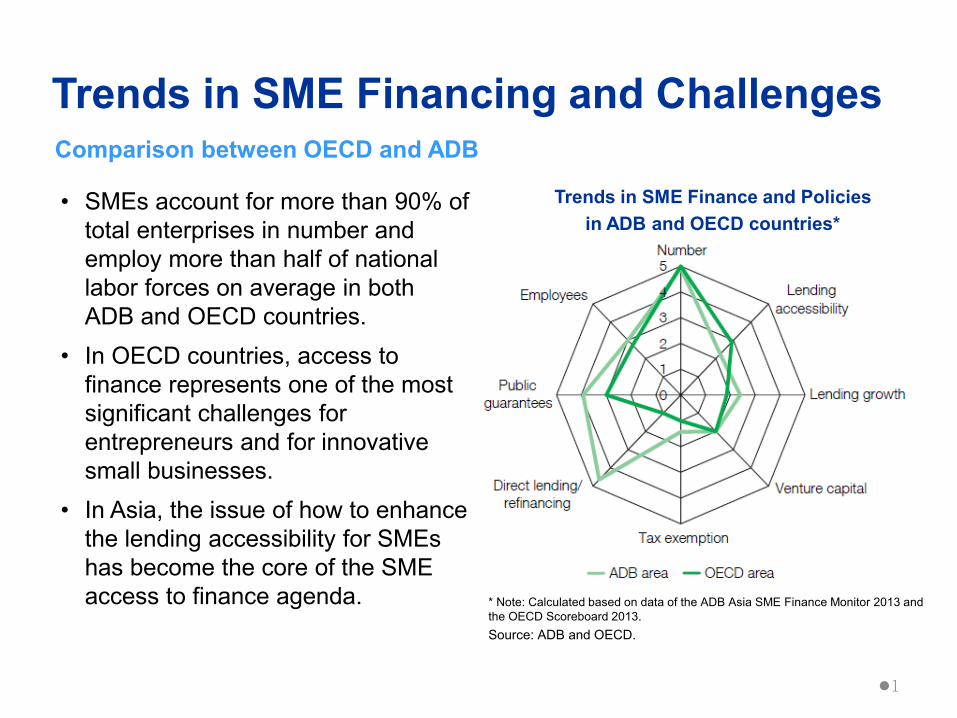

Trends in SME Financing and Challenges

• SMEs account for more than 90% of total enterprises in number and employ more than half of national labor forces on average in both ADB and OECD countries.

• In OECD countries, access to finance represents one of the most significant challenges for entrepreneurs and for innovative small businesses.

• In Asia, the issue of how to enhance the lending accessibility for SMEs has become the core of the SME access to finance agenda.

Trends in SME Finance and Policies in ADB and OECD countries*

Comparison between OECD and ADB

* Note: Calculated based on data of the ADB Asia SME Finance Monitor 2013 and the OECD Scoreboard 2013. Source: ADB and OECD.

1

• Given the largely bank-centered financial systems established in Asia, three issues have become the priority of policy agenda: 1. Enhancing the bankability for SMEs; 2. Raising more bank lending efficiency for them; and 3. Filling the supply–demand gap in SME finance.

• Accordingly, governments have developed a variety of measures to support SME access to banks. (i.e. public credit guarantee schemes)

• In addition, policy measures supplementing the promotion of bank lending to SMEs include: 1. Concessional direct lending: by policy banks/government authorities; 2. Refinancing schemes for bank: by development organizations or

government; and 3. Government interest rate subsidies.

Trends in SME Financing and Policies Government Support Measures in Asia

2

SME Financing and Financing Gap • The sources for SME financing is limited, and there is a

‘financing gap’ in SME financing − Majority of SMEs experience a ‘financing gap,’ often defined as the

difference between demand for funds by SMEs and supply of funds available to SMEs, even in developed countries.

• SME financing gap is particularly prevalent in developing countries

− As past financial crises raised Asian DMs’ consciousness against global uncertainty, growing access to SME finance to reduce the supply-demand gap has becoming a priority for sustainable and inclusive growth.

− OECD countries do not report any generalized SME financing gap. They reported financing gap primarily in equity financing, which is concentrated in certain sectors such as startups and high-tech firms.

3

SME Financing: Major Source of Funds • In most countries, commercial banks are the main source

of SME financing − In Asia, the lending scale to SME is relatively large (double-digit to GDP)

in several countries, including Korea (38.9%), Thailand (33.7%), and Malaysia (20.1%) in 2012-13. (ADB-OECD, 2014)

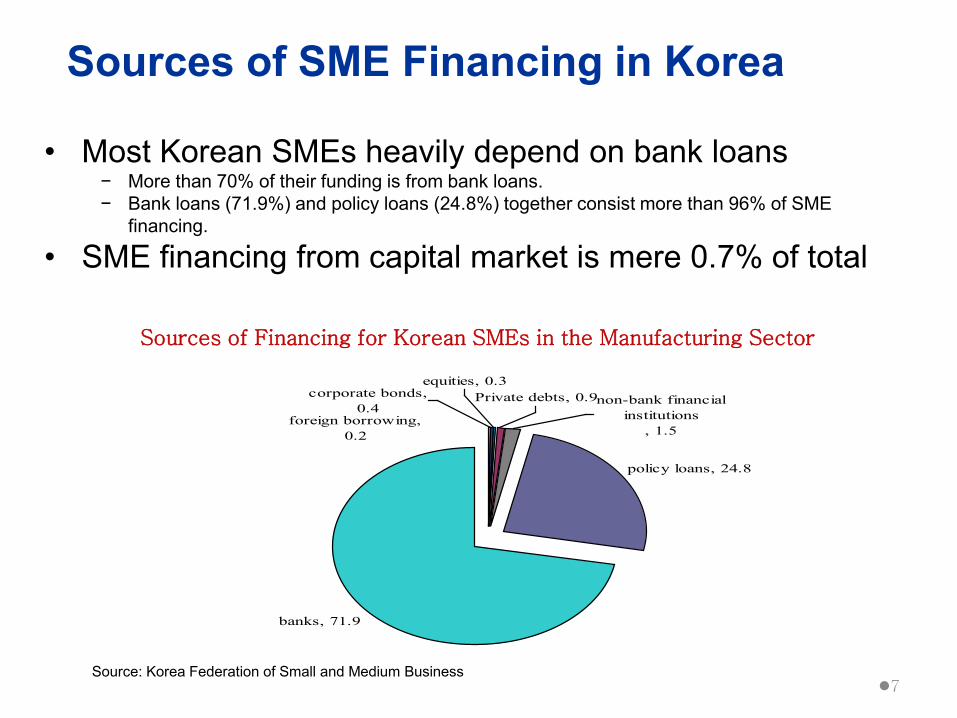

• In Korea, most SMEs heavily depend on bank loans − More than 70% of their funding is from bank loans.

− Bank loans (71.9%) and policy loans (24.8%) together consist more than 96% of SME financing.

4

SME Financing: Diversification of Sources

• SMEs’ heavy reliance on bank loans as a mean of long-term financing, however, is not desirable since there is a possibility of failure in roll-over for the maturing loans when banks face liquidity problems.

• Therefore, development of diversified financing models to help SMEs raise long-term growth capital has become a key challenge in SME finance.

• Capital markets are one of the best candidates as alternative sources of long-term funding for SMEs.

5

SME Financing through Capital Market: Challenges

• SME Financing through Capital Markets is desirable for long-term financing

• However, most countries have problems in SME financing especially through capital markets

− e.g. SMEs’ illiquid financial instruments hard to find investors

6

Sources of SME Financing in Korea

policy loans, 24.8

banks, 71.9

Private debts, 0.9equities, 0.3

corporate bonds,0.4

foreign borrowing,0.2

non-bank financialinstitutions

, 1.5

• Most Korean SMEs heavily depend on bank loans − More than 70% of their funding is from bank loans. − Bank loans (71.9%) and policy loans (24.8%) together consist more than 96% of SME

financing.

• SME financing from capital market is mere 0.7% of total

Sources of Financing for Korean SMEs in the Manufacturing Sector

Source: Korea Federation of Small and Medium Business 7

Major Obstacles for Capital Market Financing

• Hurdles to be overcome in order to facilitate SME financing in capital markets includes

− having an adequately developed capital market in terms of depth and liquidity

− There exist severe information asymmetry in this segment of enterprises.

− SMEs, in essence, have relatively high credit risk. (more vulnerable to sudden changes in economic and competitive environment)

− SME financing in capital market is inherently associated with a higher implementation cost per deal. (smaller size of funding, higher information cost)

8

Government’s Role in Capital Market Financing

• Thus, government and policy makers not only have to focus on the development and growth of capital market itself.

• But also search for a means to overcome the obstacles inherent to SMEs in order to facilitate active SME financing in capital market: that is

− To provide access to credible corporate information on SMEs

− To alleviate higher credit risk and higher transaction cost

9

SME Financing in Bond Market: P-CBO Program in Korea

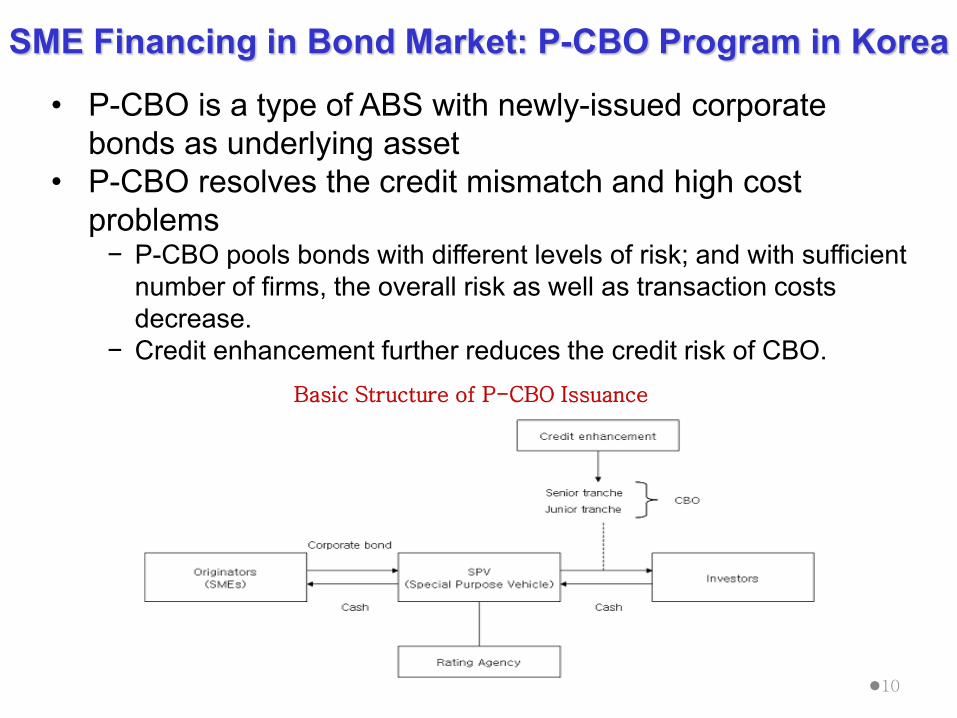

• P-CBO is a type of ABS with newly-issued corporate bonds as underlying asset

• P-CBO resolves the credit mismatch and high cost problems

− P-CBO pools bonds with different levels of risk; and with sufficient number of firms, the overall risk as well as transaction costs decrease.

− Credit enhancement further reduces the credit risk of CBO. Basic Structure of P-CBO Issuance

10

Variations of P-CBO in Korea

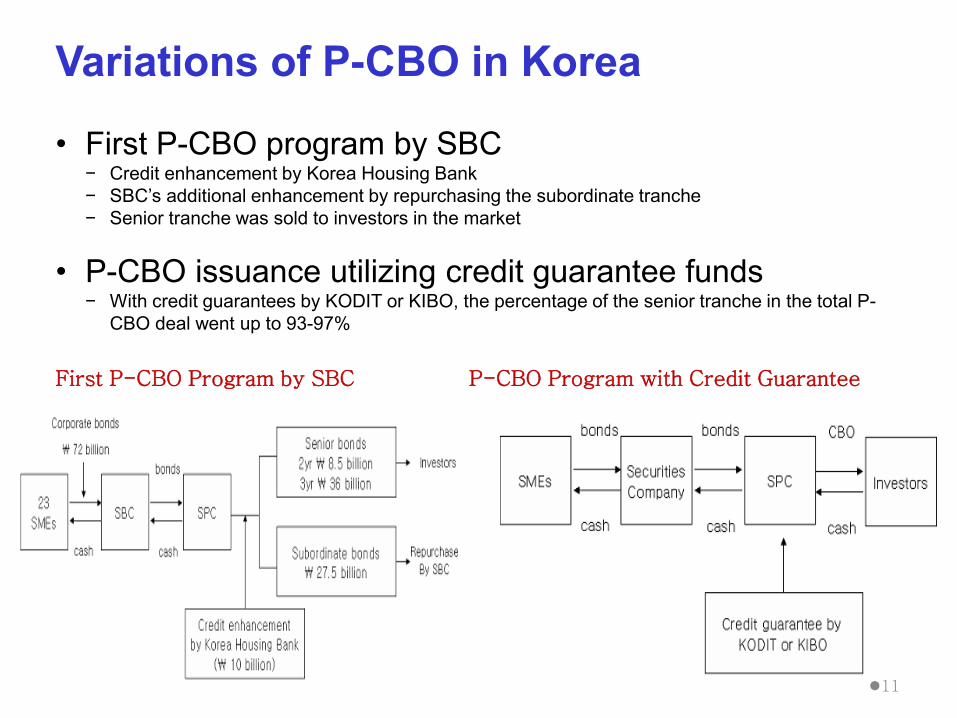

• First P-CBO program by SBC − Credit enhancement by Korea Housing Bank − SBC’s additional enhancement by repurchasing the subordinate tranche − Senior tranche was sold to investors in the market

• P-CBO issuance utilizing credit guarantee funds − With credit guarantees by KODIT or KIBO, the percentage of the senior tranche in the total P-

CBO deal went up to 93-97%

First P-CBO Program by SBC P-CBO Program with Credit Guarantee

11

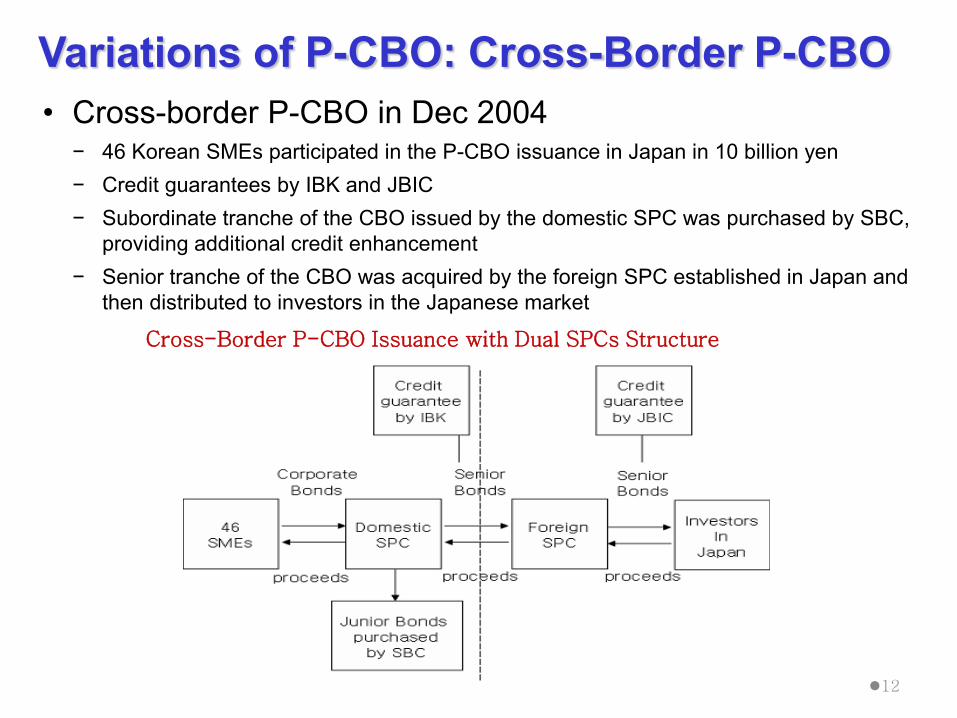

Variations of P-CBO: Cross-Border P-CBO • Cross-border P-CBO in Dec 2004

− 46 Korean SMEs participated in the P-CBO issuance in Japan in 10 billion yen − Credit guarantees by IBK and JBIC − Subordinate tranche of the CBO issued by the domestic SPC was purchased by SBC,

providing additional credit enhancement − Senior tranche of the CBO was acquired by the foreign SPC established in Japan and

then distributed to investors in the Japanese market

Cross-Border P-CBO Issuance with Dual SPCs Structure

12

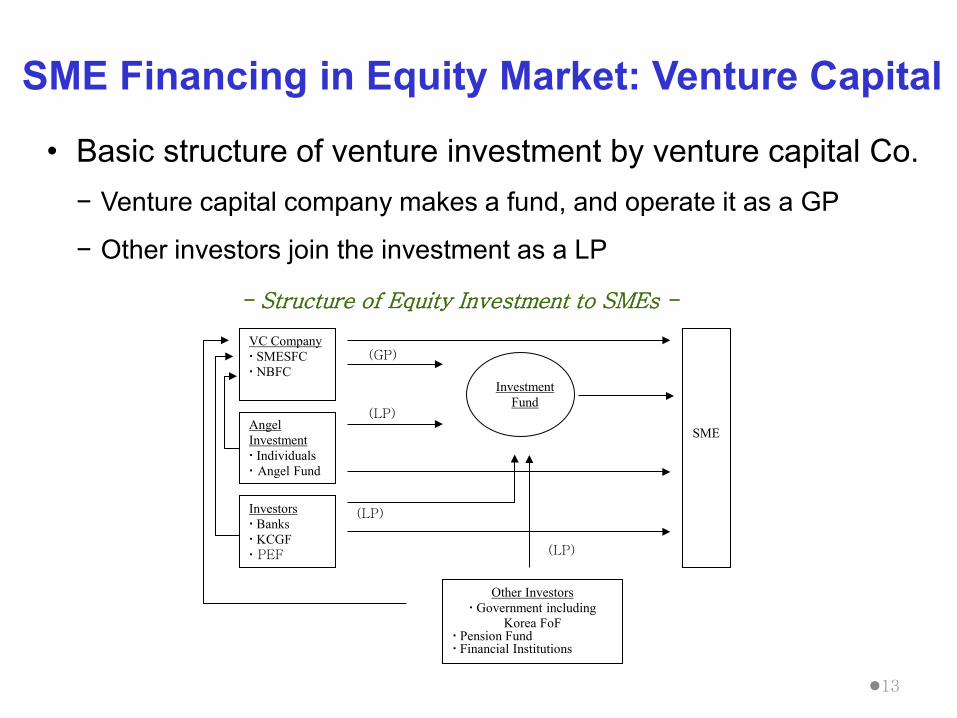

SME Financing in Equity Market: Venture Capital

• Basic structure of venture investment by venture capital Co. − Venture capital company makes a fund, and operate it as a GP

− Other investors join the investment as a LP

- Structure of Equity Investment to SMEs -

VC Company SMESFC NBFC

Angel Investment Individuals Angel Fund

SME

Investment

Fund

(GP)

(LP)

(LP)

(LP)

Other Investors Government including

Korea FoF Pension Fund Financial Institutions

Investors Banks KCGF PEF

13

Venture Capital in Korea: Fundraising Stage

• Central and local government are the largest investors to venture investment funds

• The share of institutional investors is expected to grow − Recent removal of restrictions on banks, insurance companies, mutual

savings banks

− The soundness in the venture capital market would be enhanced if institutional investors actively participate in the market with monitoring funds’ management

− VC market gains another reliable source of investment, and institutional investors have a high-risk, high-return investment instrument => mutually beneficial

14

Venture Capital in Korea: Investment Stage

• Recent rebound of venture capital market − Venture capital industry is in recovery due to the gov’t’s effort to

rehabilitate VC market since 2004

• Share of investment to early stage companies is increasing − Average size of fund is also growing.

− Investment in early stage companies is associated with higher risk and longer time to exit.

15

Venture Capital in Korea: Exit Stage

• IPO is the main exit channel − Only 10% of venture capital investment depends on M&A

• Venture firms’ IPOs with venture capital investment is increasing − The ratio of IPOs with venture capital investment to total IPOs

has increased : 50.5% (2002) →81% (2007)

− Average time-span with venture capital investment to IPO is 7.9 years, while that without venture capital investment is 11.5 years.

16

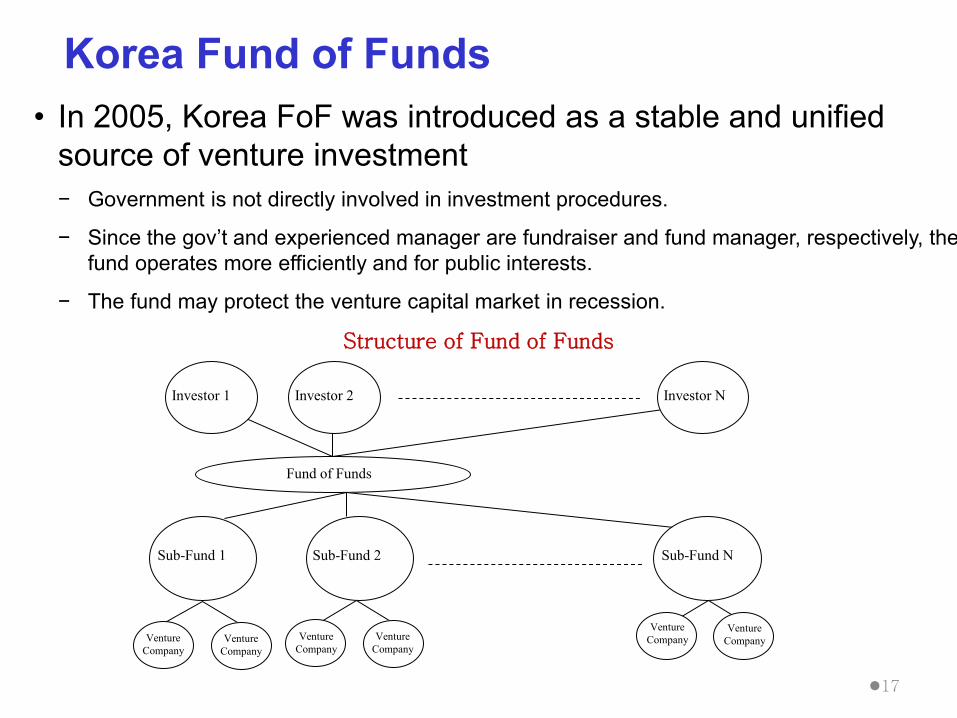

Korea Fund of Funds • In 2005, Korea FoF was introduced as a stable and unified

source of venture investment − Government is not directly involved in investment procedures.

− Since the gov’t and experienced manager are fundraiser and fund manager, respectively, the fund operates more efficiently and for public interests.

− The fund may protect the venture capital market in recession.

Structure of Fund of Funds

Fund of Funds

Investor 1 Investor 2 Investor N

Sub-Fund 2 Sub-Fund N Sub-Fund 1

Venture Company

Venture Company

Venture Company

Venture Company

Venture Company

Venture Company

17

Korea Fund of Funds (cont.) • Korea FoF makes more transparent VC market and provides

a stable investment source to venture firms − Since KFoF selects sub-funds with good track records, sub-funds have incentives to

manage their assets efficiently. − KFoF is expected to raise 1 trillion won over five years, and creates new VC ranging from

500 to 600 billion won each year. − The scheme is more efficient than when the government directly selects venture

companies and makes investment decisions.

Source: Park (2005)

Capital Market

Government

Government

SME

SME

Direct investment decision making

Lack of specialty, moral hazard, corruption…

Finance/Credit Guarantee

Effective Risk Sharing and Screening Mechanism need to be

developed

Investment decision making and management

follow up

Capital Market

Government

Government

SME

SME

Direct investment decision making

Lack of specialty, moral hazard, corruption…

Finance/Credit Guarantee

Effective Risk Sharing and Screening Mechanism need to be

developed

Investment decision making and management

follow up

Government SME Financing through Capital Market

18

Implications from the Korean Experience • Needs to set specific targets within SME sector in which

financing gap is most serious − If a government does not set a specific target sector, then government’s funds may

direct to sectors which does not need financing support. − Early-stage innovative SMEs are most likely to have a financing gap

• Innovative efforts with various financing tools is crucial − P-CBO was attractive to investors because the overall default risk decreased.

• Even in VC market, government’s role was important in rehabilitating the market and KFoF will play an significant role − Rather than direct intervention in the market, construct investor friendly, incentive

compatible and efficient infrastructure

19

Policy Recommendations

• Building a credible SME information sharing system − Removing information asymmetry is an important first step. − Policy makers should search for a way to utilize information currently scattered around

the banking sector, in credit guarantee schemes, and other existing government and commercial lending programs.

− The government must take the initiative and play a major role in the data collection process.

− The credit information on individual consumers will also play a significant role since the credit assessment of SMEs often depends on an individual, namely the owner and/or manager of the company.

• Facilitating SME financing through bond market − For corporate bond issuance, pooling a group of SMEs may provide a plausible solution to the

inherently higher credit risk and transaction costs associated with SMEs. − If a deal is structured with number of tranches, the base of potential investors will be broadened with

different levels of risk preferences. − The liquidation of bank loan assets in the market via CLO will provide another indirect way of

tapping into the debt capital market.

20

Policy Recommendations • Fostering venture capital market

− For the equity market, fostering venture capital and providing an incentive compatible environment throughout the whole activity cycle of venture capitalists are the first priority.

− Search stage: credible information sharing system and networks of technology and business assessment industries are crucial.

− Raising value of portfolio firm: venture capitalist can play an active role in raising corporate value through cooperation with the management of the company.

− Exit stage: there should be a viable number of exit strategies for the venture capitalists.

• Cooperation and coordination between public and private sectors − Government’s role is crucial in alleviating SME financing gap in the capital market.

However, government’s role is a necessary but not sufficient condition. − Without active participation from the private sector and investors, the whole endeavor

cannot be a success. − The government should focus on constructing an investor-friendly, incentive

compatible, and efficient market infrastructure in order to promote more active participation from the private sector.

21

Thank you

22