world bank documentdocuments.worldbank.org/curated/pt/107641468743674392/pdf/multi0... · document...

TRANSCRIPT

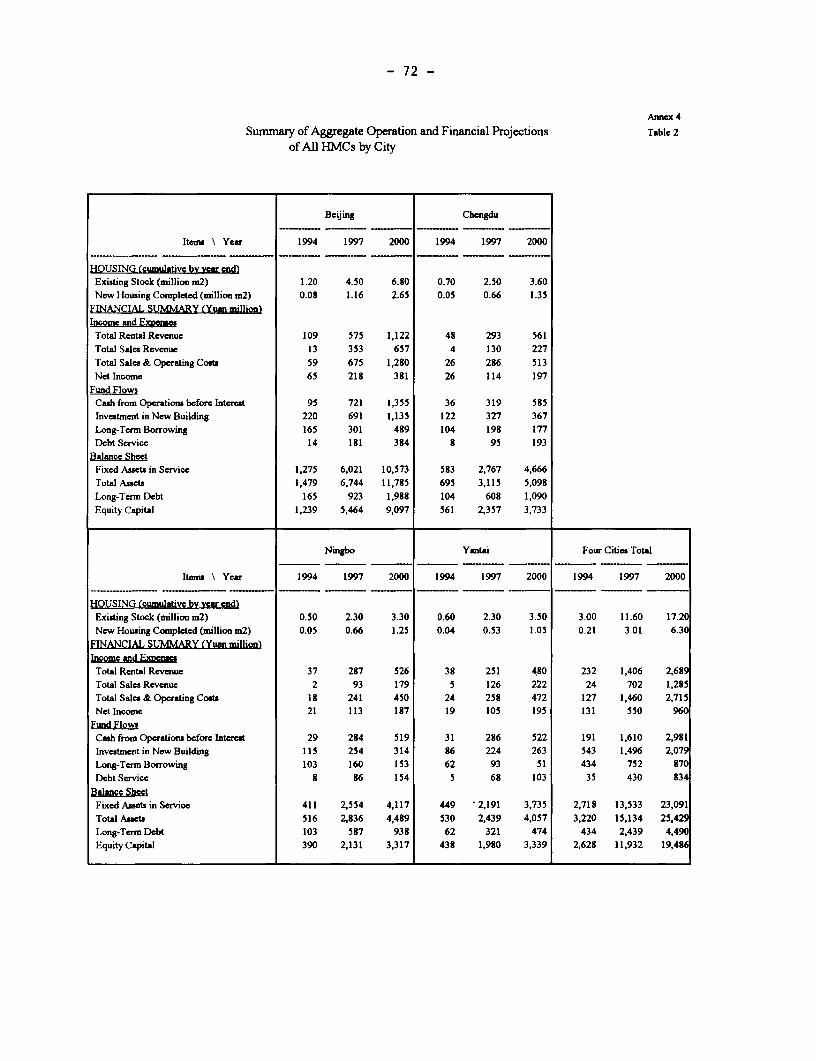

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No.12757-CHA

STAFF APPRAISAL REPORT

CHINA

ENTERPRISE HOUSING AND SOCIAL SECURITY REFORM PROJECT

JUNE 10, 1994

Environment and Urban Development Operations DivisionCountry Department II (China and Mongolia)East Asia and Pacific Region

This document has a restricted distribution and may be used by recipients only in the performnance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Currency Equivalents(as of June 1994)

Currency Name - Renminbi (RMB)Currency Unit - Yuan (Y) = 100 fen

Y1.00= $0.11$1.00 = Y8.70

Fiscal Year

January 1 - December 31

Principal Abbreviations and Acronyms

CCG Central Coordination GroupCOE Collectively Owned EnterpriseCPRP Comprehensive Pilot Reform ProgramEIA Environmental Impact AssessmentEPB Environmental Protection Bureau

HMC Housing Management Company (Joint Stock Company)HRO Housing Systems Reform OfficeICBC Industry and Commerce Bank of ChinaJGF Japan Grant Facility

MOC Ministry of ConstructionMOF Ministry of FinanceMOL Ministry of LaborMOPH Ministry of Public Health

PAYG Pay-As-You-Go fundingPBC People's Bank of China (The central bank)PCBC People's Construction Bank of ChinaPFI Participating Financial IntermediaryPMO Project Management Office

RECD Real Estate Credit DepartmentSIA Social Insurance AgencySOE State-owned EnterpriseSPC State Planning CommissionSRC Systems Reform Commission

TA Technical AssistanceUI Unemployment InsuranceYHSB Yantai Housing Savings Bank

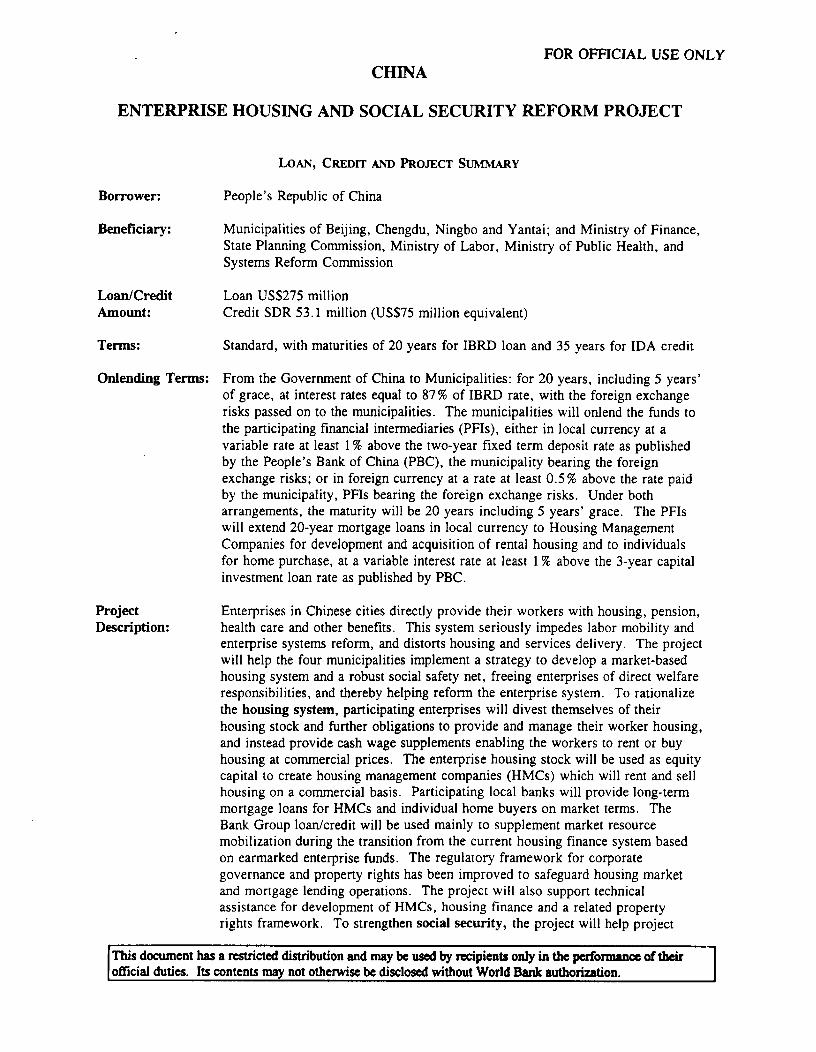

FOR OFFICIAL USE ONLYCHINA

ENTERPRISE HOUSING AND SOCIAL SECURITY REFORM PROJECT

LOAN, CREDIT AND PROJECT SUMMARY

Borrower: People's Republic of China

Beneficiary: Municipalities of Beijing, Chengdu, Ningbo and Yantai; and Ministry of Finance,State Planning Commission, Ministry of Labor, Ministry of Public Health, andSystems Reform Commission

Loan/Credit Loan US$275 millionAmount: Credit SDR 53.1 million (US$75 million equivalent)

Terms: Standard, with maturities of 20 years for IBRD loan and 35 years for IDA credit

Onlending Terms: From the Government of China to Municipalities: for 20 years, including 5 years'of grace, at interest rates equal to 87% of IBRD rate, with the foreign exchangerisks passed on to the municipalities. The municipalities will onlend the funds tothe participating financial intermediaries (PFIs), either in local currency at avariable rate at least I % above the two-year fixed term deposit rate as publishedby the People's Bank of China (PBC), the municipality bearing the foreignexchange risks; or in foreign currency at a rate at least 0.5% above the rate paidby the municipality, PFIs bearing the foreign exchange risks. Under botharrangements, the maturity will be 20 years including 5 years' grace. The PFIswill extend 20-year mortgage loans in local currency to Housing ManagementCompanies for development and acquisition of rental housing and to individualsfor home purchase, at a variable interest rate at least 1 % above the 3-year capitalinvestment loan rate as published by PBC.

Project Enterprises in Chinese cities directly provide their workers with housing, pension,Description: health care and other benefits. This system seriously impedes labor mobility and

enterprise systems reform, and distorts housing and services delivery. The projectwill help the four municipalities implement a strategy to develop a market-basedhousing system and a robust social safety net, freeing enterprises of direct welfareresponsibilities, and thereby helping reform the enterprise system. To rationalizethe housing system, participating enterprises will divest themselves of theirhousing stock and further obligations to provide and manage their worker housing,and instead provide cash wage supplements enabling the workers to rent or buyhousing at commercial prices. The enterprise housing stock will be used as equitycapital to create housing management companies (HMCs) which will rent and sellhousing on a commercial basis. Participating local banks will provide long-termmortgage loans for HMCs and individual home buyers on market terms. TheBank Group loan/credit will be used mainly to supplement market resourcemobilization during the transition from the current housing finance system basedon earmarked enterprise funds. The regulatory framework for corporategovernance and property rights has been improved to safeguard housing marketand mortgage lending operations. The project will also support technicalassistance for development of HMCs, housing finance and a related propertyrights framework. To strengthen social security, the project will help project

This document has a restricted distribution and may be used by recipients only in the performance of theirofficial duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

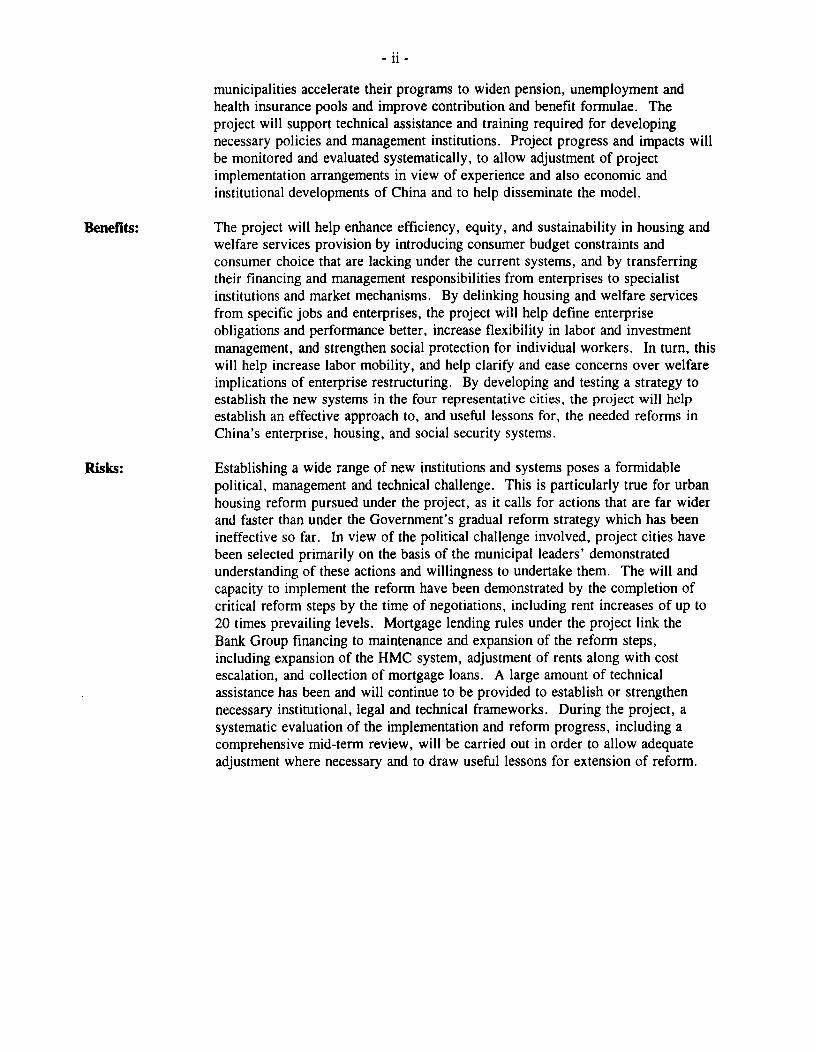

municipalities accelerate their programs to widen pension, unemployment andhealth insurance pools and improve contribution and benefit formulae. Theproject will support technical assistance and training required for developingnecessary policies and management institutions. Project progress and impacts willbe monitored and evaluated systematically, to allow adjustment of projectimplementation arrangements in view of experience and also economic andinstitutional developments of China and to help disseminate the model.

Benefits: The project will help enhance efficiency, equity, and sustainability in housing andwelfare services provision by introducing consumer budget constraints andconsumer choice that are lacking under the current systems, and by transferringtheir financing and management responsibilities from enterprises to specialistinstitutions and market mechanisms. By delinking housing and welfare servicesfrom specific jobs and enterprises, the project will help define enterpriseobligations and performance better, increase flexibility in labor and investmentmanagement, and strengthen social protection for individual workers. In turn, thiswill help increase labor mobility, and help clarify and ease concerns over welfareimplications of enterprise restructuring. By developing and testing a strategy toestablish the new systems in the four representative cities, the project will helpestablish an effective approach to, and useful lessons for, the needed reforms inChina's enterprise, housing, and social security systems.

Risks: Establishing a wide range of new institutions and systems poses a formidablepolitical, management and technical challenge. This is particularly true for urbanhousing reform pursued under the project, as it calls for actions that are far widerand faster than under the Government's gradual reform strategy which has beenineffective so far. In view of the political challenge involved, project cities havebeen selected primarily on the basis of the municipal leaders' demonstratedunderstanding of these actions and willingness to undertake them. The will andcapacity to implement the reform have been demonstrated by the completion ofcritical reform steps by the time of negotiations, including rent increases of up to20 times prevailing levels. Mortgage lending rules under the project link theBank Group financing to maintenance and expansion of the reform steps,including expansion of the HMC system, adjustment of rents along with costescalation, and collection of mortgage loans. A large amount of technicalassistance has been and will continue to be provided to establish or strengthennecessary institutional, legal and technical frameworks. During the project, asystematic evaluation of the implementation and reform progress, including acomprehensive mid-term review, will be carried out in order to allow adequateadjustment where necessary and to draw useful lessons for extension of reform.

- iii -

Project Costs/a: Local Foreign Total---------------- US$ Million-------------

Technical Assistance and TrainingSocial Security 2.8 10.7 13.5Housing and Housing Finance 1.8 4.4 6.2

Total Base Cost 4.6 15.1 19.7

Physical and Price Contingencies 1.9 3.4 5.3

Total TA in Current Prices 6.5 18.5 25.0

Total Cost of Housing Financed Partlyby the Project, in Current Prices 601.2 323.8 925.0

Total in Current Prices 607.7 342.3 950.0

Financing Plan:

Local Banks 325.0 - 325.0

Housing Management Companiesand Individual Homebuyers 274.5 - 274.5

Central and Municipal Governments 0.5 - 0.5

IBRD/IDA 7.7 342.3 350.0

Total 607.7 342.3 950.0

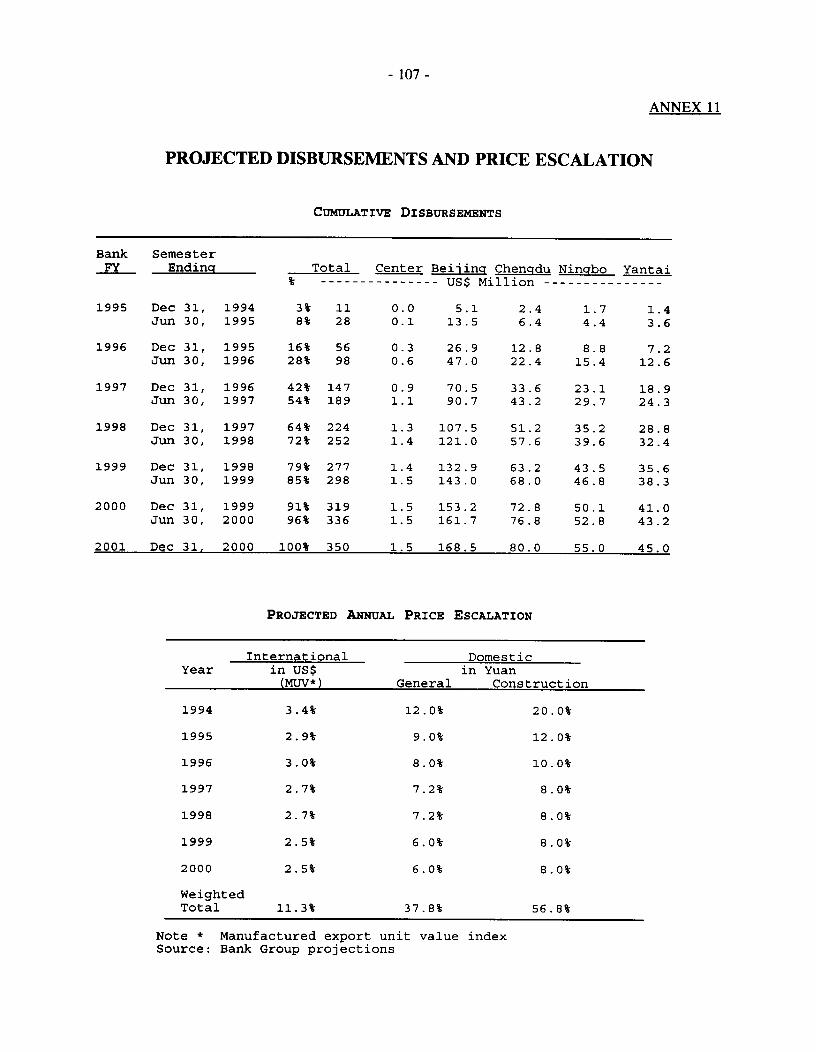

Estimated Disbursements:

IBRD/IDA Fiscal Year 1995 1996 1997 1998 1999 2000 2001------------------------ US$ Million------------------------

Annual 28.0 70.0 91.0 63.0 46.0 38.0 14.0Cumulative 28.0 98.0 189.0 252.0 298.0 336.0 350.0

Poverty Category: Not Applicable

Economic Rate of Not Estimated. The main project benefits from institutional and economicReturn: management reforms could not be quantified.

Map: IBRD No. 25747R

/a Does not include taxes, tariffs, supervision and management expenses.

I-

- v -

CONTENTS

1 Enterprise Reform, Housing and Social Security in Urban China: Current Systems andIssues

A. Issues in Enterprise Reform ..................................... 1B. Financing and Supply of Housing .................................. 2C. Social Security .............................................. 4

2 Strategies for Reform

A. Government's Economic Reform Strategies . ........................... 6B. Bank Group Strategies and Experience ................................ 6C. Strategies for Housing Reform .................................. 8D. Social Security Reform Strategy and Tasks .............................. 13

3 The Project

A. Project Background .15B. Objectives and Rationale ....................................... 16C. Systems Reform Action Plans .17D. Housing Mortgage Loans .20E. Technical Assistance and Training .21F. Project Cost and Financing .23

This Staff Appraisal Report is based on the findings of the appraisal mission that visited China inOctober-November 1994, comprising Songsu Choi (Task Manager), Nicolette DeWitt (Counsel),Yonghui Fan (Operations Officer), Andrew Hamer (Economist), Chingboon Lee (Economist), FengWang (Legal Consultant), T.J. Luckens (Consultant Housing Specialist), and Youxuan Zhu(Resettlement Specialist/Planner). Earlier missions also included Alain Bertaud (Urban Planner), IvyCheng (Financial Analyst), Zafer Ecevit (Division Chief), Kevin Ayre, Barry Friedman (ConsultantSocial Security Specialists), Nena Manley (Counsel), Joanna Siegle (Consultant Health PolicySpecialist), and Yuan Wang (Economist). Project preparation was supported by Japan Grant Fund,which financed services of consultants including: Brian Abel-Smith, John Arnott, Brian Christensen(Social Security/Health Specialists), Gilles Horenfeld, Community Association Services, Inc. (HousingSpecialists), Jianxiang Ding, Robert Josephs, Richard Lawrence, Neal Stender (Lawyers), AprilLeClair, Robert Losey, Edgar Su (Banking Specialists), Clarence Chan (Property Specialist),Gwendolyn Ball, Paul Chan, Alice Huang, Mingjiang Li, Zichao Li (Financial Analysts) andXiaoyong Wu (Information Specialist).Peer reviewers are Bertrand Renaud, Lawrence Hannah, and Adrienne Nassau. The managingDivision Chief is Katherine Sierra and Director is Nicholas C. Hope.

- vi -

4 Institutions and Finances

A. Central and Local Governments .................................... 25B. Social Security Administration .................................... 26C. Housing Management Companies and the Enterprises ...... ................ 27D. Taxes and Finances ....................................... 29E. Financial Intermediaries ...................................... 30F. Property Rights and Legal Framework . ............................... 31

5 Project Implementation

A. Project Preparation ....................................... 34B. Responsible Agencies ................... 35C. On-Lending Arrangements ................... 35D. Disbursement ................... 37E. Procurement ................... 38F. Monitoring and Supervision ................... 40

6 Benefits and Risks

A. Economic Benefits . ................................... 41B. Equity Aspects ................................... 41C. Environment and Resettlement ................................... 42D. Policy and Implementation Risks ................................... 43

7 Agreements Reached and Recommendation . .............................. 45

ANNEXES

1. Project Cities and Their Reform Programs ................................ 472. Housing Rents and Prices, and Wage Reform .. 523. TA Programs for Housing Management Companies and Housing Market Development .... 584. Housing Management Companies: Financial Projections .. 655. Summary of Criteria and Procedures for Appraising and Servicing Housing Mortgage Loans 746. Housing Finance Technical Assistance Program: Outline .. 787. Financial Projections of Participating Financial Institutions .. 818. Property Rights and Other Legal Framework .. 879. Social Security Policy Reform Framework and Schedule .. 9310. Social Security Technical Assistance Programs .. 9611. Projected Disbursements and Price Escalation Factors .. 10712. Project Costs and Loan/Credit Allocation by City .. 10813. Monitoring, Supervision, and Evaluation .. 10914. Selected Documents and Data in Project File .. 113

- vii -

TABLEs IN TEXT

3.1 Summary of Reform Action Plans of the Four Cities ......................... 183.2 Estimated Housing Construction and Financing by City ........................ 243.3 Summary of Project Cost and Financing . .................................. 245.1 Disbursement Arrangements ......................................... 375.2 Procurement Arrangements .......................................... 39

FIGURE iN TEXT

Figure 1 Housing Delivery and Finance: Current System in China and a Market-Based System . .9

MAP

IBRD 25747R (Location of Project Cities)

- 1 -

1. ENTERPRISE REFORM, HOUSING, AND SOCIAL SECURITY INURBAN CHINA: CURRENT SYSTEMS AND ISSUES

A. IssuEs iN ENTERRSE REFORM

1.1 China's impressive economic growth in recent years owes largely to the economic systemsreform that started with the agriculture sector in the late 1970s and later expanded to urban enterprisesectors. Especially fast growing are non-state sectors consisting of a nascent private sector in the citiesand a significant township and village enterprise sector operating in the rural and suburban areas.However, the bulk of manufacturing and service sector output in China is still produced by state-ownedand collectively owned enterprises (SOEs and COEs) as well as public sector non-profit entities locatedin cities.

1.2 A major thrust of urban economic reform has been decentralization of management decisions,from the government to enterprise managers and from the central to local governments. Before thereform process began, the government exercised direct control over production, investment and labormanagement of the enterprises. Enterprises remitted all their operating surpluses to the government andreceived investment and operating funds. As part of the reforms introduced over the last decade,enterprises now have considerable autonomy in production and marketing decisions. "Contractmanagement" systems introduced in the mid-1980s converted SOEs' formal objectives from gross outputto profit maximization, and provided enterprise managers with substantially enhanced autonomy over theallocation of resources and labor within individual enterprises. Instead of remitting earnings, they nowpay taxes and allocate after-tax profits for investment, worker bonus and welfare, and other expenses,subject to certain guidelines.

1.3 While increased management autonomy has helped rationalize resource allocation within eachenterprise, reforms in pricing and financing systems have increased efficiency of resource allocationamong enterprises. Final output markets have become far less subject to state control but subject toincreasing competitive pressures. Energy and key raw materials are now sold at generally realistic marketprices, except for a limited amount of supplies allocated and priced under the state plan. Financing forindustrial investment has been largely shifted from the budgetary allocation to bank lending andenterprises' own retained earnings. State-fixed prices now govern less than 15 % of transactions, and thestate controls no more than a quarter of industrial investment. These reforms have resulted in a visiblyupward trend in urban enterprise productivity.

1.4 The fundamental character of labor and welfare systems, however, has changed only modestly.Traditionally, workers were assigned jobs by the Government and provided with a whole range of in-kindbenefits along with nominal cash wages. The wages and benefits were provided by, or through, theenterprises but they differed little either among or within enterprises. In the state-controlled sector, thatsystem continues today with few major changes. Although a growing proportion of new workers are nowhired on contract basis, actual layoffs and job mobility are limited. Wage scales are strictly controlledby govermment regulations, with minimal variations across and within enterprises. For example, in early1993 monthly wages of the middle 60% of the workers in Chengdu fell within a narrow range betweenabout Yuan 320 and 350. Cash wages steadily increased with the economic growth, and all but displacedrationing of subsidized food and consumer goods. However, enterprise responsibilities for housing,health care, and pensions became stronger, as the government transferred the responsibility to financethe benefits, in addition to the management and delivery responsibility. This increase in enterprise

responsibility combined with increase in their authority over resource allocation has led to greaterdifferentiation of these benefits among and within enterprises, as the main available means ofcompensation. While this has helped introduce incentives needed for economic growth, it has reinforcedthe tie between benefits and jobs with serious negative effects both on the delivery of the servicesconcerned and on the enterprise system.

1.5 The in-kind benefits system has seriously limited efficiency and equity in housing and healthcare delivery. With little role played by consumer budget constraints and consumer choice, the standardsand levels of housing and health care services are constrained mainly by enterprise budget availability.As the fast economic growth and decentralization of the last decade eased the budget constraints onenterprises and local governments, housing and health care expenditures have grown much faster thanoverall growth of production, to levels far higher than those in countries at a comparable stage ofeconomic development (refer to Sections B and C below). However, the increased expenditures haveresulted more in rapidly escalating quantitative standards and unit costs of housing and health care, thanin increasing the range of service options and number of beneficiaries. As a result, inefficiencies in theresource use has grown as has the gap between those who enjoy improved standards of services and thosewhose employers are unable to provide them.

1.6 Another clear, negative consequence of this system is that it suppresses voluntary labormobility while severely restricting management and restructuring options on the part of enterprises. Thein-kind benefits, once extended, cannot easily be adjusted. As a result, the compensation system cannotbe used as an effective management tool. Each new worker hired requires a heavy commitment by theemployer, involving large lump-sum investments in housing and an entire obligation to provide healthbenefits and retirement pensions. This limits labor mobility, and deters employment expansion byprofitable enterprises, and entry by new ones. This particularly affects small COEs and private sectorfirms which do not have access to the welfare system catering mainly to SOEs and large COEs. Further,profitable enterprises bear a disproportionate burden of housing and welfare provision. Many employeesof unprofitable enterprises depend on the housing and health care benefits provided by family members'employers or by the government. The government also has to subsidize unprofitable enterprises to allowthem to provide welfare benefits.

1.7 Close to a third of SOEs and COEs are estimated to incur losses regularly. Their visible lossesare currently equivalent to about 5% of China's gross domestic product, and impose a large burden onthe Government budget, being twice as large as the net budget deficit. The economy suffers additional,hidden losses incurred to shield the unprofitable enterprises from hard budget constraints. The latter,indirect subsidies are incurred in the form of bank loan roll-overs, tax concessions, and cross-subsidiesprovided by profitable enterprises as described in para 1.6 above. These subsidies, necessary mainly inorder to protect workers of inefficient enterprises, have resulted in limited overall productivity growthof the SOE sector and inefficient resource allocation for the economy as a whole. Further developmentof China's economy would depend critically upon more vigorous growth of efficient enterprises andrestructuring of inefficient ones, which would be severely constrained by the tangled web of subsidiesand the lack of sustainable alternatives for housing and social security provision.

B. FINANCING AND SUPPLY OF HOUSING

1.8 Since urban economic reforms began in the early 1980s, fast economic growth and expandeddiscretion over resource allocation by enterprises and local governments fueled a housing constructionboom, sharply reversing the stagnation of the preceding decade, during which little urban housing wasadded. Each year during the last decade, approximately 150-200 million square meters of housing,equivalent to 3-4 million apartments, have been added to the urban housing stock. The stock stands todayat nearly 4 billion square meters of housing, of which more than two-thirds have been built after 1985.

- 3 -

In contrast to the old system under which the government built and allocated housing to enterprises, mostof the new stock has been financed by enterprises and many local governments also transferred much ofthe older stock to enterprises. The housing is managed either by the enterprise that owns it or bymanagement companies under municipal housing bureaus.

1.9 Most of current urban housing, about 80% of total in a typical city, is owned by businessenterprises and other types of public sector work units and rented out to their workers at nominal rent.Throughout the 1980's, while housing construction was surging, average rents stayed the same at 13 Fenper square meter of floor space per month. Even after relatively large increases since 1988, currentaverage monthly rent stands at only about 35 Fen/m2 . Thus the rent of a typical apartment unit (52 m2

renting for about Yuan 18 or US$2 a month) accounts for less than 3% of household income and fallsfar short of minimal operation and maintenance cost. As one result, maintenance is neglected and muchof the existing housing stock, including that added in the last ten years, is likely to suffer seriousstructural deterioration and require large infusions of resources to deal with deferred maintenanceproblems in the near future. Within each enterprise, housing is generally allocated on the basis of job-related criteria such as seniority and rank, as well as "needs" defined by family characteristics and actualspace used. Once allocated, however, the housing is indefinitely kept by the employees, except to moveto better accommodation or to change jobs, even after retirement and even passed on to their offspring.These workers and their household members thus gain effective control over an asset worth about 20times average annual household income. Because individuals may live in housing provided by theemployer of another member of the household, or de facto inherited from a close relative, there is noone-to-one correspondence between the owner of a unit and the employer of the household head. In fact,as noted, enterprises with little if any profits depend on other enterprises and public authorities to housetheir workers.

1.10 Because housing has come to be viewed as an entitlement as well as a wage-related benefit,the government has maintained a powerful role in the sector, though reduced and indirect compared withthe former responsibilities of direct construction and allocation of housing. Periodically, the Ministryof Construction issues guidelines specifying the minimum desirable size of housing per person, which areoften further inflated by municipalities. The high and escalating standards have limited the number ofbeneficiaries of the housing boom of the last decade, who have been allocated new housing of highstandards, to typically less than half of the total population of the city. Households occupying less thanhalf the target level are usually classified as the "housing poor". Typically the "housing poor" are notlow-wage earners but employees of loss-making enterprises or non-profit agencies. Solving their housing"needs" then becomes a public policy issue, addressed by municipal governments through municipalhousing investment plans, financed by resources of the governments or other enterprises.

1.11 Long-term financing for housing is at a nascent, experimental stage in China, and mostenterprises purchase housing in cash. They acquire and maintain their worker housing units with fundsset aside from retained earnings and, although not formally sanctioned, often also from accounts reservedfor production and investment. Various "housing fund" systems have been introduced as an element ofthe Government's recent housing reform program, but most of them function not as genuine housingfinance systems but essentially as trust arrangements for funds earmarked for housing, raised fromenterprises and individual payrolls. One of the uses of the housing funds appears to be to assistenterprises which are otherwise unable to acquire housing for their workers, and otherwise solve theproblem of the "housing poor".

1.12 In contrast to housing management and financing systems, the housing development system hasundergone a process of significant reform. In the mid-1980s, a few real estate development companieswere first established as subsidiaries of large SOEs and COEs in several cities. Now there are numeroussuch companies in most cities, aggressively competing in a manner similar to their counterparts in market

economies. These companies no longer wait for specific orders but develop a supply pipeline basedpartly on municipal housing plans and vigorously market their products to enterprises. As a result, thereis increasing variety in design, although the basic pattern still are 5- to 6-story walk-up apartmentbuildings, and more high-rises in large cities. The materials supply industry has grown in a similarfashion. The land occupied by housing complexes used to be provided by the local government, eitherby requisitioning agricultural land from peri-urban communities or relocating existing urban occupants(often temporarily) to free up land for redevelopment. The investor who buys a housing unit has fullproperty rights over the structure, but only ambiguously defined "use rights" over the associated land.This system, however, is now being replaced in many cities by a system of land leases obtained throughcompetitive bidding or negotiation and carrying property rights that can be transferred or mortgaged.Relatively few of the distortions in urban enterprise housing, identified above, are seen in the suburbanareas which, as a result, are fast becoming suppliers of private rental housing for urban workers who areable to pay market rents.

C. SOCIAL SECURI

1.13 China's labor insurance system was established in the early 1950s in the context of an economymanaged predominantly by the state. Government prescribed a wide range of benefits mandated forworkers of SOEs and certain COEs, including retirement and disability pensions, health care, and evenunemployment protection. As part of the economic decentralization during the 1980s, responsibilities forfinancing and managing these benefit programs have transferred almost completely to enterprises, andresulted in increasing divergence of benefits among enterprises and growing problems of mismatchbetween resources and obligations of individual enterprises. In response to these and various other issuesarising with the changing economic structure, the Government is introducing piecemeal modifications tothe social insurance system as reform "experiments".

1.14 The social security responsibilities place a heavy and growing burden on enterprises. Overalllabor insurance costs of SOEs and urban COEs increased from about 20% of their total wages in 1982to 35% in 1992 (3.5% and 4.5% of GDP, respectively). Furthermore, this burden often falls mostheavily on enterprises that can least afford it, such as older enterprises in declining industries which haveinherited a large number of retirees and are experiencing declining profitability. In 1992, SOEs andCOEs, many of which were established in the early 1950s and 1960s, had pension expendituresamounting to 19% of the wage bill, compared to the 4% paid out by the relatively new group of jointventure, foreign- and privately-owned enterprises. With the aging of their work force, the pensionobligations of SOEs and COEs as currently structured are projected to reach 25 % of their total wages by2010. To buttress the social safety net, the government is compelled to subsidize such enterprises. Thiscontributes not only to the growing fiscal deficit but also to ambiguous enterprise accountability, impedingenterprise reform.

1.15 As a main thrust of the social security reform program begun in the mid-1980s, Governmenthas been promoting resource pooling for retirement pensions. By now pension pools for SOE workershave been established in most localities. In many cities, pension pools for COE workers and even forjoint venture workers has been formed, but separate from the SOE pension pool and at differentcontribution rates. Even within the SOE sector, funds for permanent workers are kept separate fromthose for workers hired under the new contract system, which has been in use for new employees since1987. In most cities, a considerable and growing portion of the workers of private and joint-ventureenterprises and smaller COEs are not included in any pension pool. While the pooling has achieved amodest redistribution of the pension burden among similar types of enterprises, the separation of pensionschemes severely limits their effectiveness and stability as a social safety net. Not only does the systemexclude the fast growing non-SOE workers, but it also separate young workers who tend to be oncontracts with SOEs or joint ventures from permanent SOE workers who are retiring in steadily growing

numbers. Further, management tasks to collect contributions and deliver benefits also remain mostly withenterprises.

1.16 Another important initiative introduced as part of the reform program is unemploymentinsurance for workers of SOEs and large COEs, funded with a 1 % payroll tax. However, the funds areused less for unemployment income support than for training and other employment services and so farhave run large surpluses. This is partly due to restrictive eligibility criteria for unemploymentcompensation, but fundamentally due to Government policies which still try to limit unemployment byrequiring enterprises to redeploy and retrain redundant employees.

1.17 Government operates health insurance, financed out of the general budget, only forgovernment employees and retirees, university students and demobilized soldiers. Each SOE is requiredto finance and operate its own group insurance providing coverage for active and retired workers. Asidefrom limited coverage and uneven burdens on enterprises, the most pressing problem of the existinghealth care system is the rapid cost escalation. Medical expenditures for active SOE workers increasedat an average rate of 23% a year during 1985-90, to account for 28% of total labor insurance costs in1992, and equivalent to 14% of SOEs' total payroll -- twice the budgeted figure. The rapid costescalation are largely attributable to a perverse incentive structure and a general lack of cost containmentmeasures. The lack of co-payment requirement encourages workers to overuse health care, and the rigidreimbursement formulae induce inefficient health care delivery by hospitals. To ease the uneven burdenof health care costs on enterprises, pooling for serious diseases has started in several cities on anexperimental basis. The Government is also designing and experimenting with a series of reform optionsincluding expansion of health insurance pools and implementation of various cost containment measures.

- 6 -

2. STRATEGIES FOR REFORM

A. GOVERNMENT'S ECONOMIC REFORM STRATEGIES

2.1 Traditionally, the Government has advanced national reform programs through localexperimentation. This approach is due not only to uncertainties inherent to different, untested reformmodels but also to the great local diversity and autonomy, particularly after the decentralization duringthe last decade. Under the current inter-governmental system, the Government limits its role largely toguidance and coordination, giving local governments latitude to manage local affairs. Most Governmentpolicies are established as general guidelines, which require detailed local rules for implementation. Forissues for which solutions cannot be clearly defined, the Government often encourages local governmentsto experiment with new solutions, identify "best practices", and refine and disseminate them across thecountry as a whole.

2.2 Having succeeded in facilitating fast economic growth through introduction of new managementarrangements and market mechanisms, the Government has recently begun fundamental reforms in fiscal,financial, macroeconomic management, enterprise and labor systems in order to move forward with thenext stage of economic development. Central to these is enterprise reform, as the problems of SOEs andCOEs lie at the root of many difficulties in other areas. Therefore, Government is promoting broad,structural measures to enhance enterprise autonomy and accountability. Extending the managementdecentralization, the Government is promoting corporatization of SOEs, by conversion into shareholdercompanies and exercise of ownership through corporate boards, and reorientation of government agenciesfrom direct interventions and operational controls to regulatory oversights. Beyond these measures toimprove enterprise management, the current strategy to develop a "socialist market economy," officiallyadopted in 1992, calls for more aggressive measures to increase accountability and efficiency of theenterprise sector as a whole. These include measures to even the playing field for enterprises regardlessof ownership status, and hence promote non-state sector enterprises; and those to restructure inefficiententerprises such as leasing or sales of small unprofitable SOEs to better performing enterprises or privateinvestors, and even bankruptcies. Reform measures in other areas, including financial and fiscalmanagement systems, and accelerating of reforms in output and factor markets aim largely at fundamentalreforms in the framework within which enterprises operate so as to facilitate enterprise restructuring.

2.3 The scope and pace of actual enterprise restructuring, however, have remained limited andcautious partly due to the traditional strategy through experimentation but also largely due to concernsover the potential social impact of fundamental restructuring. SOE and COE work force number around100 million and, along with their dependents, represent most of the urban population. Consequently, itis now widely recognized that establishing sustainable housing and social security systems is a crucialprerequisite to broad economic restructuring. As a result, a new reform initiative, Comprehensive PilotReform Program (CPRP) to be launched soon in several selected cities, will combine steps to reformenterprise, labor, housing, and social security systems.

B. BANK GROUP STRATEGIES AND EXPERIENCE

2.4 The main thrust of the Bank Group's assistance strategy for China has been to help facilitateChina's transition from a planned to a market economy, while safeguarding the social safety net and theenvironment, by supporting innovative, flexible approaches to advancing the forefront of reform,particularly in SOEs and their operating environment. As an important part of the Bank Group's

assistance, an extensive series of sector studies has been carried out to define the issues and reformoptions for enterprise, labor, housing, and social security sectors. The relevant sector reports include"Industrial Policies for an Economy in Transition" (Report No. 8312-CHA, 1990), "Reforming SocialSecurity in a Socialist Economy" (Report No. 8074-CHA, 1990), "Urban Housing Reform: Issues andImplementation Options" (Report No. 9222-CHA, 1991), "Reforming the Urban Employment and WageSystem" (Report No. 10266-CHA, 1992), and "Industrial Restructuring: A Tale of Three Cities" (ReportNo. 10479-CHA, 1992). The Bank Group has also supported industrial finance projects in a number oflocalities and a growing number of lending operations to assist municipal and provincial governments inimproving infrastructure planning, pricing, and management.

2.5 The findings of the sector work and earlier industrial lending operations have indicated thatenterprise reform needs to be combined with reforms in the enabling framework, comprising variouselements across the usual sectoral boundaries, including social and management infrastructure. Reflectingthese findings, the Bank Group has been supporting several municipally-based industrial developmentprojects that emphasize reform of the sector infrastructure including technology support and the localgovernment's economic management systems. Realizing the need for even broader reforms, the BankGroup is preparing operations to support reform of enterprises together with other broad economicframeworks. The Bank Group has recently initiated preparation of national operations to support reformsin the financial sector, legal framework, technology transfer, and labor market systems as well as amunicipally-based comprehensive enterprise reform project. The proposed project represents an importantand critical element of this new series of assistance operations.

2.6 However, experiences accumulated through operations to help reform the frameworks forenterprise restructuring are still insufficient; and there have not been any lending operations aimedspecifically at reforming employment benefits systems either in China or elsewhere. The most relevantlessons for the project may therefore be drawn from housing, institutional development, and sectoraladjustment operations supported by the Bank Group world-wide.

2.7 Drawing lessons from housing and housing finance operations supported by the Bank Groupin the last 20 years as well as experiences of industrialized countries, the Bank's Housing Policy Paper(1992) found that performance of the housing sector depends on the pricing and regulatory structure ofthe sector as well as the economy as a whole; in particular, housing finance was found critical as agenerator and regulator of demand. Conversely, the housing sector was shown to have a significantimpact on national fiscal and macroeconomic health. Incorrect pricing of housing and housing loans hascontributed significantly to fiscal deficits and macroeconomic instability in some countries. The HousingPolicy Paper endorses operations involving non-traditional instruments to address broad sectoral andinstitutional issues.

2.8 Experiences with institutional development and sectoral adjustments, however, point outpotential difficulties facing operations that address a broad range of policy and institutional issues andsuggests important lessons to apply. While such operations need to deal with complex sets of interrelatedissues to be effective, the reforms must be carried out in a careful sequence, buttressed by early andvisible benefits for various stake-holders. Careful project preparation and borrower involvement,essential conditions in general, were found to be even more crucial for the policy reform and institutionaldevelopment programs. These lessons have been incorporated in the proposed project design andpreparation.

- 8 -

C. STRATEGIES FOR HOUSING REFORM

Market-Based Housing System

2.9 There is general agreement on the desirability of a market-based housing delivery system whereend users select housing solutions from a wide range of options offered by independent commercialproviders. In such a system, enterprises would not have any direct responsibility for their employees'housing other than providing full, competitive wages. Figure 1 illustrates such a system in contrast withthe current system of housing delivery and finance in typical Chinese cities (Figure l.a) discussed inSection 1.B. Supply and financing of housing, functions now performed mainly by employers in China,would instead be carried out by independent housing consumers, suppliers and financial intermediariesin the market system. In order for commercial suppliers to sell or rent housing without subsidies, salesprices would have to recover all costs and earn profits, while rents would have to be high enough toallow investors to recover costs over the economic life of the housing. Consumers would deal directlywith suppliers to choose housing according to their needs and affordability. As costs of housing assetsare large compared to the homeowner's income or to rental receipts, long-term credit is an essentialingredient of a well-functioning housing market. In order to ensure sustained resource mobilization,financial intermediaries will have to offer competitive returns on deposits and charge interest rates thatcover the cost of funds and their intermediation. Credit risks need to be controlled by strengthening thelegal framework that provides for effective property and mortgage rights. Further, a fully developedhousing finance system should include various institutional channels and resource mobilization instrumentsthat will allow secondary mortgage markets to emerge and encourage the participation of different typesof investors.

Government Strategy to Date

2.10 In order to ease the enterprise burdens and at the same time meet demand for new housing,both of which were growing rapidly in the 1980s under the system, a large number of municipalgovernments adopted programs in mid-1980s to promote individual homeownership by providingenterprise and government subsidies of up to 70 % of purchase prices. It soon became apparent, however,that these programs were financially unsustainable, unable to generate significant housing sales, andinequitable. In view of the worsening problems, a State Council directive in 1988 banning deep discountson housing sales and encouraged experiment with alternative ways toward a view toward commercializinghousing, or establishing a market-based system of housing provision. For a specific model, it selectedtwo small cities of Yantai and Bengbu in 1987 to experiment with substantial but restricted rent and wageincreases and housing finance operation. In 1991 revision of the directive to make it applicable to allcities, the Government retained basic tenets of the 1988 directive, but lacking consensus for a bold reformstrategy, set more gradual targets for rent and wage increases.2.11 Consensus has been established that the current housing system needs to be transformed intoa market-based one, and that commercialization requires raising the currently nominal levels of housingrents to levels covering current and capital costs. In view of low cash incomes of households, however,only gradual rent increases are considered possible initially. As incomes have been rising consistentlyover time, relatively modest increases in the portion of household income spent on housing were expectedto lead to a satisfactory pace of rent increases. This strategy was put into practice in an experiment in1987 involving a small number of cities. A schedule of rent increases was adopted as a part of thenational housing reform program in 1991. Progress to date has been disappointing, however, falling farshort of the modest target for rents to recover current costs plus depreciation (the so-called "3 factors")by 1993. In fact, rents fell in most cities in real terms since economic reform began (Refer to para 1.9).

-9-

Figure 1. Housing Delivery and Finance: Current System In China anda Market-Based System

Fig. 1.a Current Housing System In China

ENTERPRISE BUILDER

HOUSEHOLD BANKS

Key:

,-i Flow of Housing

Ezzz= Flow of Funds

E==* Housing Contributed as Equity

-::. ADvidonds

Fig. 1.b A Market-based Housing System

ENTERPRISE BUILDER

HOUSINGCOMPANY

HOUSEHOLD BANKS

CAPITAL MARKET

- 10 -

2.12 Paralleling the rent increases, another important element of the Government strategy has beenhomeownership promotion. Housing units owned or bought by enterprises are offered to enterpriseemployees at "standard prices," set at cost adjusted for depreciation. Further discounts, thoughdiscouraged, are in fact common in many municipalities. Loans, carrying maturities of up to ten years(but most often about five years), are offered at interest rates that are lower than commonly available onloans of shorter maturities. The combination of low prices and low interest rates, however, has failedto generate significant housing sales to the general public, mainly due to low levels of income and savingsand to disincentives to buy created by low rents.

2.13 The Government has also promoted the creation of "housing funds," partly to supportindividual homeownership and more generally to augment the resources for housing construction. Tomanage the housing funds, local specialized institutions were established in Yantai and Bengbu as partof the 1988 reform experiment. However, in most cities, housing finance is handled by "Real EstateCredit Departments (RECDs)" belonging to local branches of the People's Construction Bank of China(PCBC) or the Industrial and Commercial Bank of China (ICBC). These institutions are described inmore detail in Chapter 4. Most of the funds are deposited by enterprises as part of the welfare reserves.Beginning in 1991, they have been supplemented with "provident funds" contributed equally byindividuals and their employees and kept in individual accounts. This essentially amounts to creating atrust for earmarked funds, with rates for both deposits and loans lower than other prevailing rates.Because the demand for individual loans has been insignificant, most of the housing funds have so farbeen used as short-term loans to enterprises for housing construction or purchase approved by the localgovernment.

2.14 A critical shortcoming of the strategy described above is its inability to bring an end to theenterprise's direct obligations for employee housing. Given that current rents will have to be increased10 to 30 times in real terms to reach commercially viable levels, it is doubtful such a target canrealistically be achieved in gradual steps and be acceptable to consumers. As apparent from the lack ofprogress so far, consumers are likely to resist even gradual rent increases if these are not fullycompensated by income growth. This is because raising the proportion of income spent on rent, asenvisaged in the Government strategy, represents real income reduction, albeit small. The affordabilityanalysis that underlies this approach is fundamentally flawed, as it ignores expenditures incurred byenterprises for employee housing and thus available for compensating wage adjustments when rents arerestructured. In effect, then, the current strategy is geared less toward establishing a market-basedhousing system than to mobilizing more resources for housing, in some cases even increasing theenterprise responsibility for housing. Due to the lack of efficacy of the current strategy, either for truecommercialization or for increased resource mobilization for housing, there is growing discussion amonggovernment and enterprise managers aimed at identifying an effective and feasible alternative strategy.In addition to the experience under the common model of housing reform decribed in the foregoing, moreambitious experiments have been carried out in a few cities. These have shown values and needs ofbolder reforms, but could not be expanded for lack of support and follow-up actions. Such experimentsin Chengdu and Yantai are briefly discussed in Annex 1.

An Alternative Strategy

2.15 An alternative strategy for commercialization of housing would focus on converting the in-kindhousing benefits into cash wages, and setting rents and sale prices at levels which cover at least the fullcost. The rent increases would be large -- in a typical city, about 15 to 20 times the current rents (fromabout Y20 per month to about Y350), compared with average household cash income of about Y900 amonth. However, workers would be fully compensated by wage adjustments and gain more freedom ofchoice. As this strategy redirects the flow of resources that are already available and used in the system,the rent and wage adjustments would be affordable at least at an aggregate level. An effective alternative

- 11 -

strategy, however, would need to have devices to deal with key issues of transition, including the initialabsence of the market-based systems of housing delivery and finance, wage adjustment formulae, andaffordability problems faced by specific individuals and unprofitable enterprises.

2.16 A model of a market-oriented system to effect the transition is illustrated in Figure l.b.Critical elements of the model include:

(a) Autonomous for-profit companies, providing housing directly to consumers, that would takeover housing stock now owned and operated by enterprises;

(b) Commercially viable housing rents and sales prices that would recover the long-run marginalcost of housing;

(c) Cash wage supplements to compensate for rent increases;

(d) Market-oriented long-term mortgage lending operations for owner-occupied and rental housing;and

(e) Policy and regulatory frameworks that allow sustainable operation of the housing managementand finance institutions.

2.17 Housing Management Company. An effective device both to initiate a market-based housingdelivery system and to help the divestiture of enterprise housing would be the creation of joint-stockhousing management companies (HMCs). Several enterprises would join together to create an HMC bycontributing their housing stock as equity capital in return for ownership shares. The HMC wouldadminister this housing stock and also acquire new housing to rent or sell at commercial prices. Suchan HMC would be, in the usual typology of Chinese companies, a collectively-owned enterprise, whichas a class has shown relatively strong autonomy and accountability. Clearly defined ownership rights andcorporate governance structure would help reinforce these characteristics. During the transition, furthermeasures would be required to reinforce incentives for market-based behaviour and to preventcontinuation of ties between enterprise and housing. For example, while shareholders would want anHMC to maximize profits and hence dividend distribution and share values, they would also have othershort-term interests that conflict with the profit objective: to suppress HMC housing rents so as to limittheir wage adjustment burden; and to maximize HMC acquisition of new housing and hence housingsupply to their employees, which could reduce short-term cash flow and even financial stability of theHMC. Therefore, minimum pricing rules and other safeguards would be essential to ensure commerciallyviable behavior.

2.18 Initially, HMC customers would primarily consist of workers employed by the enterprises thatoriginally owned the stock. This is likely not only because the shareholding enterprises would want togive priority to their own employees, but also because commercial rents and prices would not beaffordable to employees of other entities whose wages would not be adjusted. The access to affordablehousing would induce other employers, such as private and joint-venture companies that are profitablebut lack housing, to invest in HMCs by making cash equity contributions. However, as additionalenterprises invest in or create HMCs and provide higher cash wages to their employees, a more openhousing market would emerge, providing wider choice for consumers and greater profit opportunities forHMCs and their shareholders. Again, it would be necessary to ensure that HMCs are not closelyidentified with a few shareholder enterprises and that more HMCs and other housing suppliers enter themarket and compete.

- 12 -

2.19 Finance. Commercial levels of housing rents and high cash wages of individuals would makecommercially priced housing loans for HMCs and individuals feasible. In turn, lenders would be ableto mobilize financial resources from the market without resorting to forced savings or subsidies. Undercurrent market conditions, however, very long maturities, fixed interest rates, or reliance on foreclosuresale would impose undue risks to lenders. The large asset base of existing housing, which is fully paidfor, would provide a large rental income stream as well as a secure collateral for loans. The cash flowwould also allow a HMC to repay loans for new housing over a reasonable maturity shorter than thehousing's economic life, without having to charge extremely high rents on the new housing, which wouldbe necessary if the loan repayments are to be made solely by income from the new housing. Further,the cash flow would be large enough to allow the HMC to pay substantial dividends to shareholders,which would support wage adjustment, especially for enterprises which have made large investments andcontributed a sizeable stock of housing. This financial structure is discussed in more detail in Chapter4 and Annex 4.

2.20 Wages. Compensating for higher costs of renting or buying housing, enterprises wouldprovide cash wage supplements to allow workers to pay higher rents or mortgage payments. Thesupplements would be financed mostly from the savings of housing expenditures that are no longernecessary, supplemented with HMC dividends. As allocation of housing is currently used as a tool toincrease compensation differentials between different groups of workers, the wage adjustmentcompensating for housing rent increases will steepen the current flat wage distribution, and allow it tomore closely reflect job-related characteristics. In principle, the rent increase would be fully compensatedfor most workers. This is necessary to ensure that the workers' real incomes are not reduced; this is alsojustified and affordable as the total amount would not exceed what the enterprises have been paying toacquire and maintain housing. However, it would be important not to tie wage supplements directly andcontinuously to specific housing consumption that would vary with individual employees' needs and time.Therefore, the supplement would be determined on the basis of typical housing occupied by workersholding comparable jobs, not the specific housing unit occupied by a particular individual; and it wouldbe made a part of the comprehensive wage and subject to adjustment as a whole, not according to changesin housing consumption in the future.

2.21 Clearly, there will be winners and losers: those who have lesser housing than others incomparable positions and will now receive a supplement exceeding the rent increase; and those whooccupy disproportionately large housing and now would have to pay rent in excess of the wagesupplement awarded. While the ultimate solution for the latter would be to adjust their housingconsumption, by moving or subletting, transitional relief may be given in the form of an excess allowancethat is phased out, say, in three years. Transitional payments would also be needed for workers whosespouses are employed by enterprises which do not join the new housing system and do not pay a wagesupplement. This type of problem would constitute the largest demand for excess payments, and wouldpose significant problems when the reform covers only part of the city. However, eventual withdrawalof these subsidies would force other enterprises to pay the wage supplement for employees living inhousing not built by them and therefore spur them to join the new system. Such transitional paymentssimply monetize the cross-subsidy provided to the other enterprise and as such would not imposeadditional burdens to the enterprises joining the new system. As the transitional payments are withdrawn,the resources would be used instead to provide wage supplements to participating enterprises' ownworkers who have previously received neither housing nor wage adjustments.

2.22 Regulatory Framework. The proposed new system would require strengthening a numberof legal and regulatory instruments in China, including those governing registration and valuation ofproperty, landlord-tenant relationships, foreclosure, eviction, and condominiums. At present, contractsare commonly used to overcome specific deficiencies in the national legal framework. However, furtherdevelopment of the regulatory framework will become increasingly important as the housing market

- 13 -

develops. In the meantime, local regulations would be needed to strengthen the current framework.Formal regulations aside, it would be difficult to enforce eviction and foreclosure and to apply othermarket disciplines in the housing delivery system in general unless public housing is provided toaccommodate the dispossessed and the poor.

2.23 Beyond Transition. The strategy outlined above focuses on the rental sector for reasonsmentioned in para 2.12 above. However, the strategy would establish commercial levels of rents, highercash wages, and long-term mortgage financing, that would lead to viability of ownership options.Therefore, provisions must be made to allow households, who wish to buy units and can accumulate thenecessary downpayment, to obtain mortgage loans. The success of HMCs would create a viable rentalmarket which would attract further investment from private sources and insurance funds. However, ashomeownership spreads, it would present a more important area of private investment. Because newhousing would increasingly reflect consumers' tastes and budget constraints, the intrusive regulations andguidelines governing housing unit sizes and other related aspects would lose much of its justification andshould be replaced with a set of ordinances to safeguard health, safety, and environmental considerations.

D. SocIAL SECURITY REFORM STRATEGY AND TASKS

2.24 A reformed social and health insurance system is critical to the creation of more efficient laborand enterprise systems in urban China. Such a system would need to be separated from the fortunes ofindividual enterprises, financed in a sustainable and equitable manner, portable, and providing a minimumsafety net. This requires a wide pool to allow redistribution of costs across enterprises and workers andover time, and benefit and contribution formulae that are consistent with each other and workers' needsand means. They would in turn require efficient management organizations that can take over a numberof tasks currently performed by enterprises. The Government is now pursuing reform initiatives andexperiments directed broadly toward these objectives and has made considerable progress, particularlyin pooling retirement pension funds. These initiatives, however, have yet to be consolidated into acoherent and detailed program with specific implementation plans. What is needed at this point is todefine the necessary next steps and schedules, to refine benefit and contribution formulae, and to developa necessary institutional framework and management capacity.

2.25 Benefits and Funding. For various pension and insurance programs, it is important thatbenefit and contribution formulae be defined consistent with the program aims and resources. Forpension reform, the Government is emphasizing individual contributions and encouraging local authoritiesto establish benefit and contribution formulae appropriate for different tiers of retirement income support:the basic social safety net managed publicly, enterprise-based pension schemes, and individual retirementsavings. Further, the Government is also encouraging modest prefunding in view of the growing pensionobligations that may be difficult to meet by the pay-as-you-go system currently used in most pensionschemes other than those for the SOE contract workers. As a near-term task, it would be important todefine at least the first, basic tier of retirement pension linked to changes in effective wages and livingcosts, and define a corresponding contribution requiring workers to pay a share. It would also beimportant to project resource requirements and availability of pension schemes and review variousinvestment options, with a view toward defining a benefit and funding formulae that would be consistentwith each other and sustainable in the long-term.

2.26 The main issue facing the health care system is the rapid escalation of costs. While costcontainment measures would include those to improve efficiency of health care delivery itself, the mostpressing task would be to correct the perverse incentive structure by a better definition of benefits andpayment methods. The Government is supporting experiments in selected cities with alternative healthcare management systems, including for example: a fee-for-service system combined with co-paymentand strong cost control measures; and a capitation system. Results of the experiments are being

- 14 -

disseminated to help other localities formulate new payment and funding systems. It would be importantto introduce co-payment requirements and implement initial cost control measures in the light of theseexperiences, while continuing with further experiments with different strategies in various pricing andmanagement measures.

2.27 In contrast to the considerable reforms in retirement pension and health care systems led bythe Government, programs to provide treatment and compensation for work injury and income andemployment support for the unemployed remain perfunctory and ill-defined, left largely to individualemployers. The Government is now working to better define work injury protection and standardize thebenefits. Protection for labor redundancy is a most serious issue, whose resolution depends on a broadrange of fundamental structural reform policies. Government's current policy is to minimize layoffs bymaking the employing enterprise responsible for finding or creating jobs for the redundant labor, withsome assistance from the government agency supervising the enterprise. Although efforts are under wayto introduce improvements in unemployment insurance and related employment support services, theirsignificance would remain marginal without fundamental decisions on labor and enterprise restructuring.In the meantime, it would be important to clearly define benefit criteria, strengthen the labor informationsystem, and enhance the job training and placement services.

2.28 Pooling. The main thrust of Government reform strategy has been to pool resources forvarious components of social protection, from pension to health insurance, to spread the burden andenhance labor mobility. As described in Chapter 1, most progress has been made in pension pooling:pools for different types of enterprises and workers have been formed in many cities and counties. Theseare to be combined into provincial pools, which have already been formed in several provinces, and thennational pools. Given that there are separate current pools for different types of work units, however,it would be more productive to broaden and consolidate the pooling across different types of workerswithin each city before moving on to pooling over wider geographical areas. Efforts are under way toform insurance pools for health, work injury, and unemployment at city or county level. It would beimportant that such pools cover as wide a proportion of the work force as possible, given experience withthe pension pools.

2.29 Institutional Capacity. Strengthened management and policy analysis capabilities are neededto support the reform tasks, including pooling and establishment of new benefit and contributionformulas. For example, health facility utilization and cost studies are essential to formulating new servicepayment systems and setting health insurance premia. The contribution and benefit formulas for pensions,now being revised, as well as various insurance schemes, must be evaluated and updated periodically withbetter projection of needs and resources.

2.30 To manage pension pools, social insurance agencies (SIAs) have been established under localgovernments. These currently function mainly as clearing houses that collect funds from enterpriseswhose required contribution exceeds the pension costs of their own retirees, and transfer the surplus toenterprises running deficits. Basic pension management tasks remain with each enterprise, including thecollection of contributions, compilation of individual wage histories, calculation and delivery of benefits.For genuine pension pools to function effectively, most of these functions need to be taken over by acentralized management agency. This will bring about substantial economies of scale, particularly if datahandling is computerized. Once a system is established to collect contributions centrally, it could handlethe collection of all contributions and premia for pension, health insurance and other related schemes,although the different schemes would have to be managed separately.

- 15 -

3. THE PROJECT

A. PROJECT BACKGROUND

Project Origin

3.1 The Bank Group has been supporting the Government's search for housing reform models sincethe reform experiment started in 1987. Initial assistance was provided through a series of occasionalpapers and policy seminars and formal sector work ("China: Urban Housing Reform: Issues andImplementation Options," op. cit.), analyzing weaknesses of the existing system as well as recommendingand elaborating on elements necessary for market-based systems. The sector work, delivered in 1991,provided a significant and timely input as the Government held a series of discussions to review theprogress of housing reform experiments begun in 1987 and to define a new national policy frameworkfor housing reform. While accepting the goal of market-based housing system, the Governmentconsidered the steps needed for rapid commercialization of housing well beyond what was consideredfeasible in China at the time and eventually adopted a revised, cautious national housing reform policyincorporating gradual rent increases and other steps, as described in Section 2.C. At the same time,agreement was reached that the Bank Group would help develop an operational model of an alternativestrategy and test it in selected cities prepared to carry out bolder reforms. In view of the Bank Group'sassistance focus on enterprise systems reform, it was decided that the project would also includeassistance for divestiture of enterprise social security burdens, another important enterprise reformconstraint. This component would include modest assistance to responsible central authorities to refineand implement national policy guidelines.

3.2 In late 1991, a Bank Group mission visited several cities in China to explore options for theproject. In view of the far-reaching reforms necessary, it was decided that they would be implementedin municipalities selected competitively on the basis of the following criteria:

(a) a demonstrated willingness and capacity to carry out the fundamental reform strategies asoutlined in Section 2.C;

(b) representativeness in terms of location and population size; and

(c) likely demonstration effect if included under the project.

Project Cities

3.3 The Government selected a short list of fourteen candidate cities, representing a wide rangeof size and location. Among these were several municipalities that had participated in earlier housingreform experiments. After the proposed reform framework was discussed between a Bank Groupidentification mission and the representatives from each of the short-listed municipalities in early 1992,the five municipalities of Beijing, Chengdu, Guanghan, Ningbo, and Yantai were selected. Shanghaimunicipality later joined the list but decided in 1993 not to participate in the project. It would insteadconcentrate on implementing an alternative housing reform program, begun in 1992, which focuses onincreasing housing construction by mobilization of "housing provident funds" (refer to para 2.13) ratherthan by pricing reforms and related measures. Later, Guanghan municipality was unable to participatein the project as it was reluctant to take the major step of raising the rents on the agreed timetable. These

- 16 -

developments were symptomatic of the difficulties involved in commercialization of housing and theconsequent lack of national consensus and demonstrated model on how to proceed with housing reform.

3.4 The four municipalities participating in the project represent a sample of large and medium-sized cities of China: Beijing has about 6 million permanent urban residents, Chengdu 3 million, Ningbo600,000, and Yantai 450,000. It is significant that the cities of Chengdu, Ningbo, and Yantai are amongthe 18 (mostly medium-sized) cities chosen recently for the Government's Comprehensive Pilot ReformProgram to change enterprise, labor, housing, and social security systems. It is also significant thatYantai and Chengdu have carried out reform experiments that involved significant rent increases, housingsale, and new housing management or finance institutions. Although these experiments fell far short ofmarket-based operations, they were significantly bolder, compared with the gradual reforms carried outnationally, so as to demonstrate the value of a transition to a market-based housing system. Chengdu,the capital of Sichuan province (110 million population), also has been active in advancing the reformsin social security. Annex 1 outlines the profiles of the participating cities and their reform programs.

B. OBJECTIVES AND RATIONALE

3.5 Project Objectives. The project will support the implementation of a strategy to develop amarket-based housing system and a robust social safety net, freeing enterprises of parallel responsibilities,and thus helping promote labor mobility, enterprise restructuring and management improvement. Testedand developed in the four selected municipalities, the new models can be replicated in other cities inChina. Features of the models and strategy, discussed in Chapter 2, include: autonomous for-profitcompanies specializing in housing delivery direct to consumers, taking over housing stock owned andoperated by enterprises; commercially viable housing rents and sales prices; cash wage supplements thatcompensate for rent increases; market-oriented long-term mortgage lending operations for owner-occupiedand rental housing; policy and regulatory framework that allows sustainable operation of the housingmanagement and finance institutions; comprehensive pools of retirement pension, health insurance, andemployment services managed centrally by specialized municipal agencies; and enterprises freed ofresponsibility for directly providing and managing worker housing and social security benefits.

3.6 Rationale for Bank Group Involvement. The new systems to be established under the projectwill help increase the efficiency and sustainability of the housing and social security systems, whichrepresent a large and increasing part of the national economy. At the same time, the new systems willease a critical obstacle to urban labor market development and enterprise restructuring. The project willestablish basic frameworks that provide for increased private investment in housing, growth of small andprivate enterprises due to reduced entry costs, as well as continued development of social securitymanagement capacity and related regulations. Thus the project represents a key element of the BankGroup's country assistance strategy, to facilitate China's transition to a market economy by supporting,among others, innovative and flexible approaches to establishing appropriate frameworks for wide-rangingreforms. The Bank Group's involvement and experience in China's reform process and in policy andinstitutional development elsewhere would be helpful in integrating diverse elements of the necessaryframeworks. The transition from a housing finance system dependent on enterprises and forced savingsto one based on market resources would leave an interim funding gap that can be bridged with BankGroup financing.

- 17 -

C. SYSTEMS REFORM ACTIONS

Housing and Wages

3.7 In the four project cities, the strategy to establish a market-based housing system, as describedin Section 2.B above, will be implemented. This would include the following actions, many of whichhave already been implemented:

(a) Several joint-stock Housing Management Companies (HMCs) will be created in each city, withthe housing stock that participating enterprises will contribute as equity capital;

(b) The HMCs will rent and sell housing at prices that recover all costs, initially giving preferenceto employees of participating enterprises;

(c) Participating enterprises will provide cash wage supplements to compensate for the averagerent increases, monetizing the in-kind housing benefit and funded partly by dividends fromHMCs; but the enterprises will no longer provide or maintain housing for their workers;

(d) Participating financial intermediaries (PFIs, two in each city) will mobilize market funds andprovide long-term mortgage loans at competitive rates; and

(e) Regulatory framework governing the definition and enforcement of property rights, includingmortgage and condominium rights, needed to safeguard operation of HMC and mortgagelending will be strengthened.

3.8 Assurances were obtained during negotiations that the project municipalities would carry outtheir respective housing systems reform programs and related technical assistance programs (see paras3.23 and 3. 25) according to time-bound action plans satisfactory to the Bank Group. The housing andwage reforms would start with enterprises that are willing to turn over their housing and join the HMCsystem and able to provide necessary wage adjustments. By April 1993, pre-incorporation conferencesapproved draft charters of at least one HMC in each project city. By appraisal in October 1993, theseHMCs had been formally incorporated, with enterprises pledging housing stock with total floor space ofabout 1.5 million m2. By the time of negotiations, this housing stock had been valued and transferred,and the rents and wages adjusted. While most of the enterprises joining the HMC system will do so byturning over worker housing in return for HMC shares, others with little housing stock will be allowedto join by contributing cash equity. Each HMC is projected to manage between 5,000 and 15,000apartment units. The number of HMCs will increase over time during of the project period, so that by2000, about 20% of the urban enterprise workers of Beijing and Chengdu are expected to be covered,70% of Ningbo's, and virtually the entire population of Yantai. The coverage and schedules of housingreform under the project are summarized in Table 3.1. Rent and wage adjustments are described in theparagraphs below and Annex 2, which have been incorporated in formal plans of action. Mortgagelending arrangements are discussed in Section 3.D below, which will be the basis of re-lendingagreements between the municipalities and PFIs. Institutional, financial and legal frameworks werestrengthened during project preparation, and are discussed in Chapter 4 and Annexes 3 and 8.

3.9 HMCs will charge housing rents and sales prices to recover all costs, including the cost of landlease, plus an allowance for profit. The minimum rents will include all current and capital costs ofhousing, or the so-called eight factors -- current costs of operation and management, depreciation (3%on structure and straight-line depreciation of land lease), return on investment (4-5 %), property and landuse taxes where applicable, insurance, and profits. However, for a limited number of years in Yantaiand Chengdu, the minimum rents for existing housing will cover the so-called five factors -- excluding

- 18 -

profits, insurance, and land use tax (which is not applicable in other cases either) from the full eightfactors (refer to Table 3.1). The basis of rent calculation, for both new and existing housing, is to bethe cost of new housing construction current each year, adjusted for quality and location. Therefore,rents, even at the 5-factor level, will cover the long-run marginal cost of housing. According tocompleted valuations, the housing stock being transferred to the first HMCs is valued on average at 75 %-85 % of the costs of new housing, depending on the city. Although HMCs will be allowed to charge rentshigher than the specified minimum, HMC shareholders, employers of most of the tenants, are initiallylikely to keep rents near the minimum specified levels. As the HMCs begin to cater to a wider publicand the separation between employment and housing provision grows clearer, rents and sales prices areexpected to be set increasingly at market-clearing levels.

TABLE 3.1 SUMMARY OF REFORM ACTION PLANS OF THE FIVE CITIES