world bank documentdocuments.worldbank.org/curated/en/910681468288600904/pdf/multi... · the...

TRANSCRIPT

Document of

The World Bank

FOR OmCIAL USE ONLY

Report No. 7757

PROJECT COMPLETION REPORT

NEPAL

SECOND AND THIRD TELECOMMUNICATIONS PROJECTS

(CREDITS 397-NEP AND 799-NEP)

APRIL 28, 1989

Industry and Energy Operations LivisionCountry Department IAsia Regional Office

Tbis document bas a restricted distribution and may be used by recipients only in the performance ofS * * i- , , . II. , .I

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY UNIT

Napalese Rupee

GOVERNMENT OF NEPAL FISCAL YEAR

July 16 to July 15

ABBREVIATIONS AND ACRONYMS

AMA - Automatic Message AccountingANI - Automatic Number IdentificationDCA - Development Credit AgreementDEL - Direct Exchange LinesHMG/N - His Majesty's Government of NepalIDA - International Development AssociationICB - International Competitive BiddingITU - International Telecommunication UnionJICA - Japanese International Cooperating AgencyHOC - Ministry of CommunicationsNTB - Nepal Telecommunications BoardNTC - Nepal Telecommunications CorporationODA - Overseas Development Age--y of United KingdomPA - Project AgreementSTD - Subscriber Trunk DialingUHF - Ultra High FrequencyUNDP - United Nations Development ProgramUK - UWited KingdomVHF - Very High Frequency

01% WORLO BANK VOR OFFICIAL USR OLYTeK WORLD SANKWmCmgtoa. D.C. 20433

U.S.A.

ode of h00G41opmeim [VA~UU

April 28, 1989

MEMORANDUM TO THE EXECUTIVE DIRECTORS AND THE PRESIDENT

SUBJECT: Project Completion Report on NepalSecond and Third Telecommunications Projects(Credits 397-NEP and 799-NEP)

Attached, for information, is a copy of a report entitled "Project

Completion Report on Nepal - Second and Third Telecommunications Projects

(Credits 397-NEP and 799-NEP)l prepared by the Industry and Energy Operations

Division, Country Department I, Asia Regional Office.

Attachment

This document bza reti disrbutin and may be sed by recipnts o * the peifomanof their officia dutiW& Its contnts may not othrwiso be disau without Wor Dak cuthumA.

FOR OMCIAL USE ONLY

NEPAL

SECOND AND THIRD TELECOMMUNICATIONS PROJECTSCREDITS 397-NEP & 799-NEP

PROJECT COMPLETION REPORT

Table of Contents

Page No.

BASIC DATA SHEETCredit 397-NEP ............ . iiCredit 799-NEP ............ iii

HIGLIGHTS ... i.e..gg..eeegeg..e...g..g.e.....g........eo.. iv

I* INTRODUCTION ...... e.g........e.......... 1Telecommunications Sector I................e...... 1IDAtS Involvement in the Sector ........................... 1

II. PROJECT PREPARATION AND APPRAISAL. .......... ..... cc....... 2

A. Second Telecommunications ProjectPreparation, Apprsisal and Credit Approval .. eeeo.og.e.eeeg 2Project Objectives ......... 2....... 2Project Description ............................. .. - 2Project Costs and Financing ............................... 3Covenants eec ...... ...... o.. g..eecggc. e.g.. 3

B. Third Telecommunications ProjectPreparation, Appraisal and Credit Approval .c........e. 4Project Objectives .. ...................................... 4Project Description 4....................................... 4Project Costs and Financing ............................... 5Covenants ceo...co...e.g..g. cc.........OO..0cc gOOOOOOe c....ccc... 5

This report was prepared by Messrs. J. Miyazaki, Financial Analyst, and D.Joshi, Consultant, of the Asia Technical Department based on informationsupplied by the Nepal Telecommunications Corporation to an IDA mission inFebruary 1988 and data gathered from the Bank's files and records.

This document has a restricted distribution and may be used by recipients only in the performance |of their official duties. Its contents may not otherwise be disclosed without World Bank authorinzatior.

Page No.

III. PROJECT IMPLEMENTATION ............... ........................ 6

A. Second Telecommunications ProjectCredit Effectiveness and Start-up ..... .................... 6Revision of .................P. ..................... ... ..... 6Implementation Schedule 7..................... 7Project Costs *...... ......................... ...... 7Disbursements 8Credit Allocation 9Reporting 10Procurement 10Performance of Consultants, Contractors and Suppliers ..... 12

B. Third Telecommunications ProjectCredit Effectiveness and Start-up 12Revision of P. o j e c t 12Implementation Schedule 12Project Costs .. 13Disbursements 14Credit Allocation 15Reporting 16Procurement 17Performance of Consultants, Contractors and Suppliers 17

IV. OPERATING PERFORMANCE ........................ 18

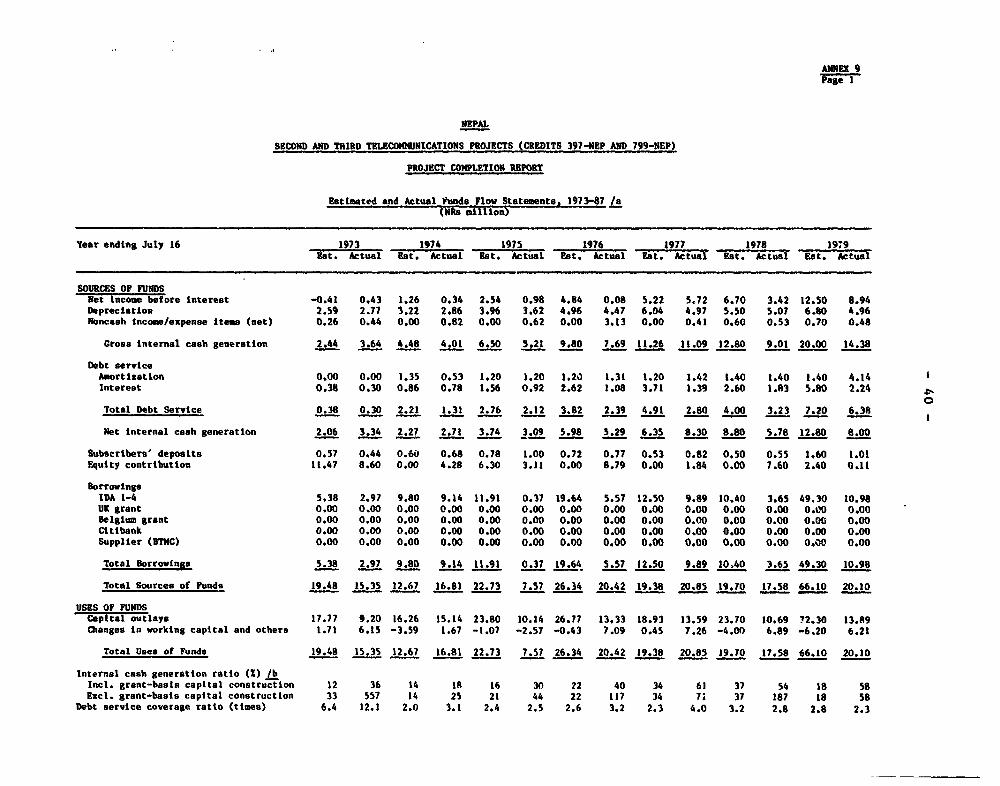

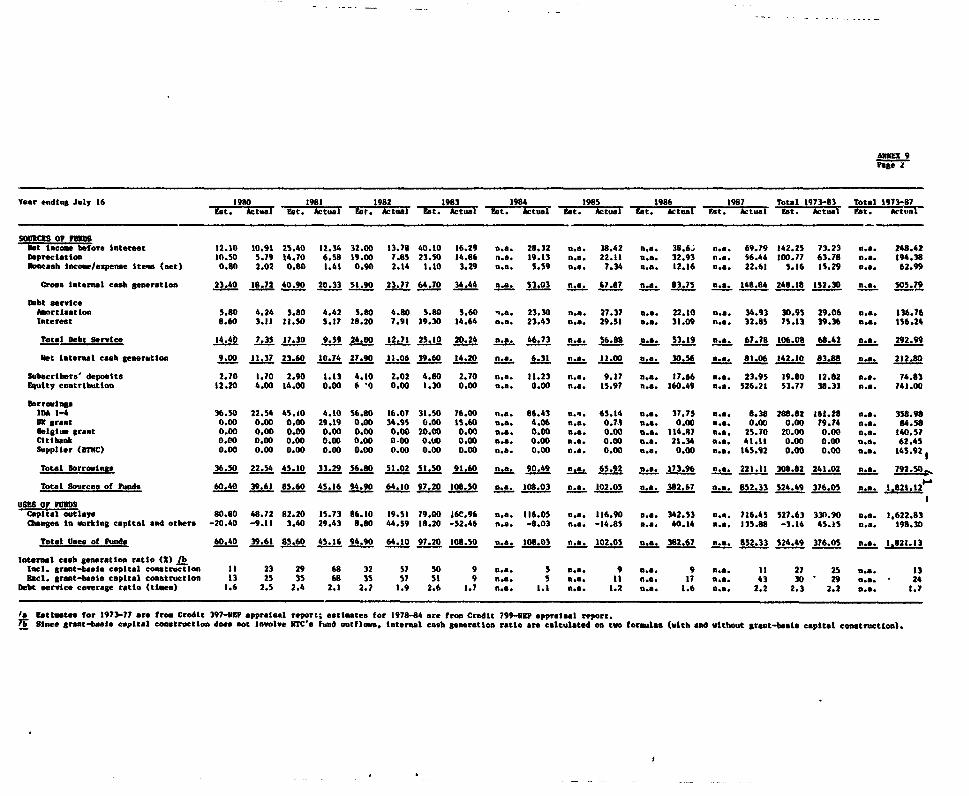

V. FINANCIAL PERFORMANCE.*................... .* .** 19Financial Performance . ......... -..................-. -- 19Financial Position *....* *.**.**@@@-......-.......-.- 20Sources and Uses of Funds ............................. 21Fiscal Impact ............................. < 21

VI. INSTITUTIONAL PERFORMANCE ................. .. .. 6060 21Organization and Management .........-. e..-...--...---.--.-- 21Staff, Recruitment and Training .............................. 22Accounting ................................................... 23Audit ..........0.. ............. .................... 24Billing and Collection ....................................... 24Tariffs ...................................................... 25Compliance with Covenants .................................... 25

VII. PROJECT JUSTIFICATION .............. 25Project Achievements .... 025

Project Spin-off 0.0 26Least Cost Solution . 26Return on Investments 000000000 6600600060006000000600006000000 26

VIII. IDA'S PERFORMANCE...................... ........... 27Overall Performance .......................................... 27

Pase No.

Supervision .............. .... ....................... e.... 28Working Relationship ....................... 28

IX. CONCLUSIONS ............. e..e ....... ...... eeee 28

ANNEXES

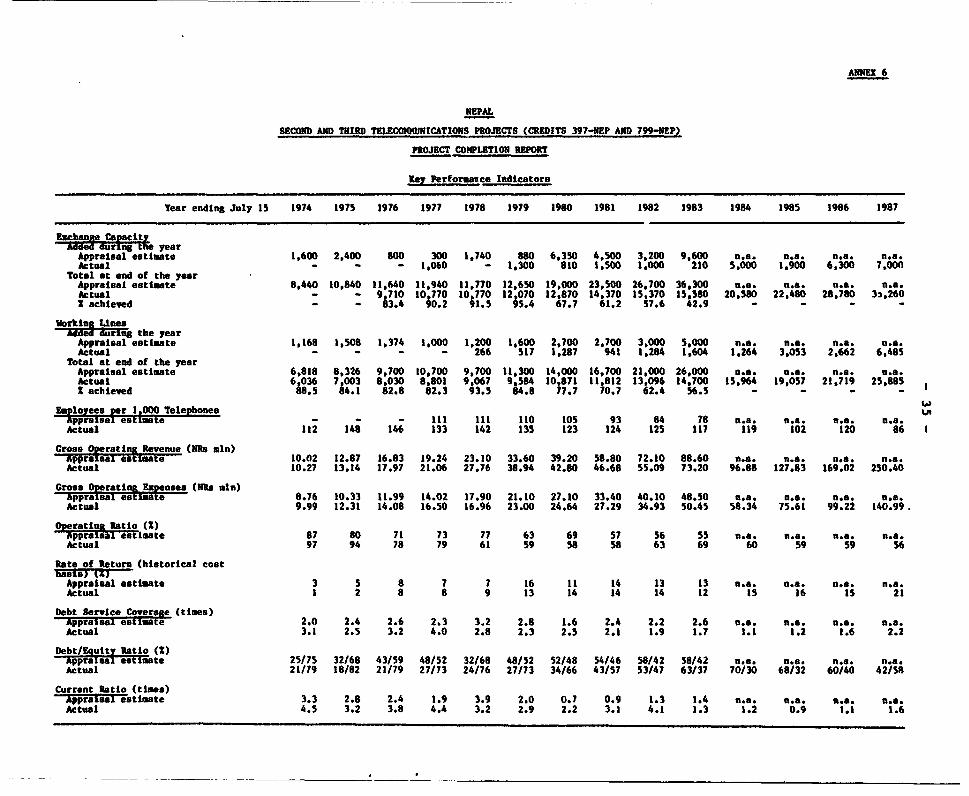

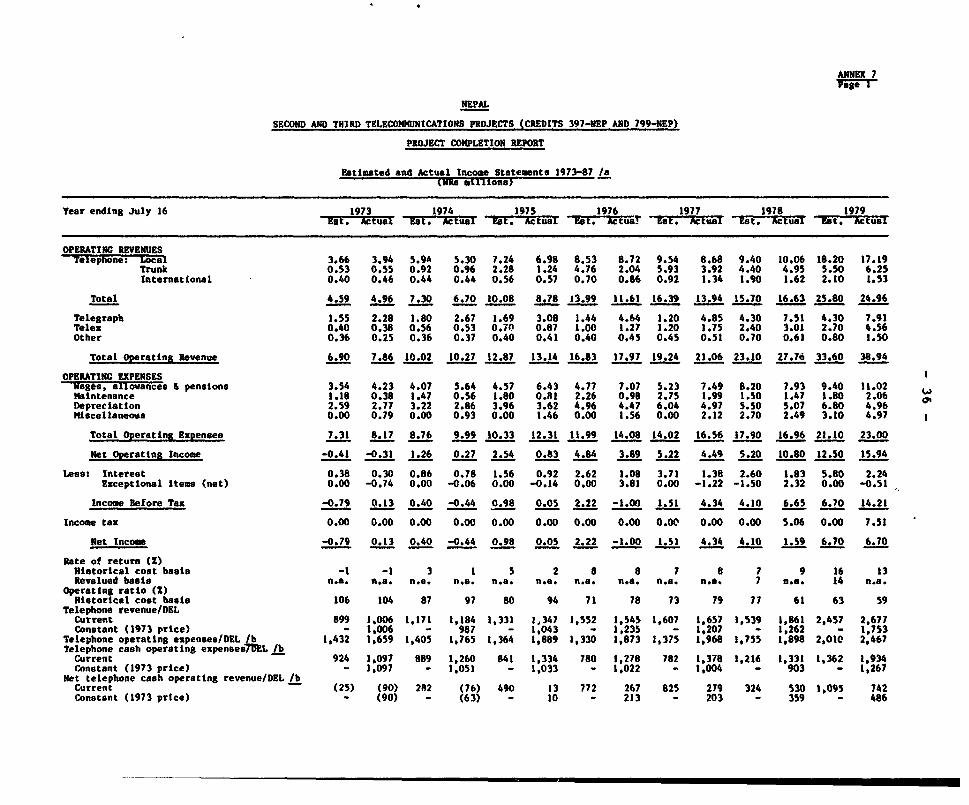

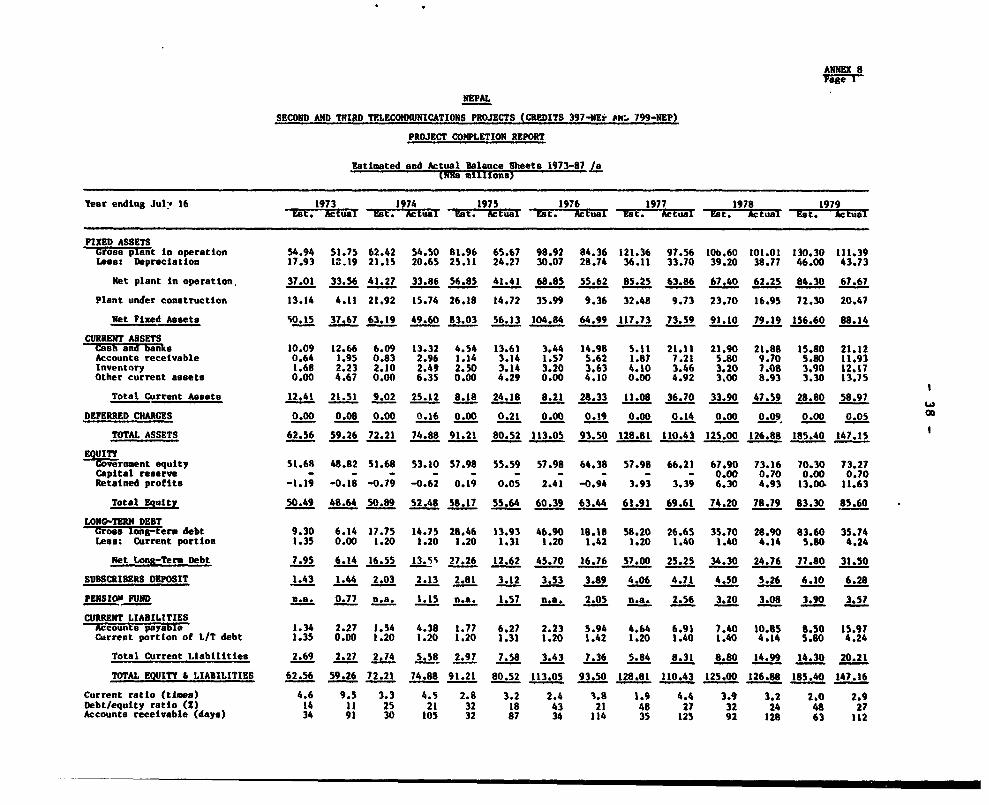

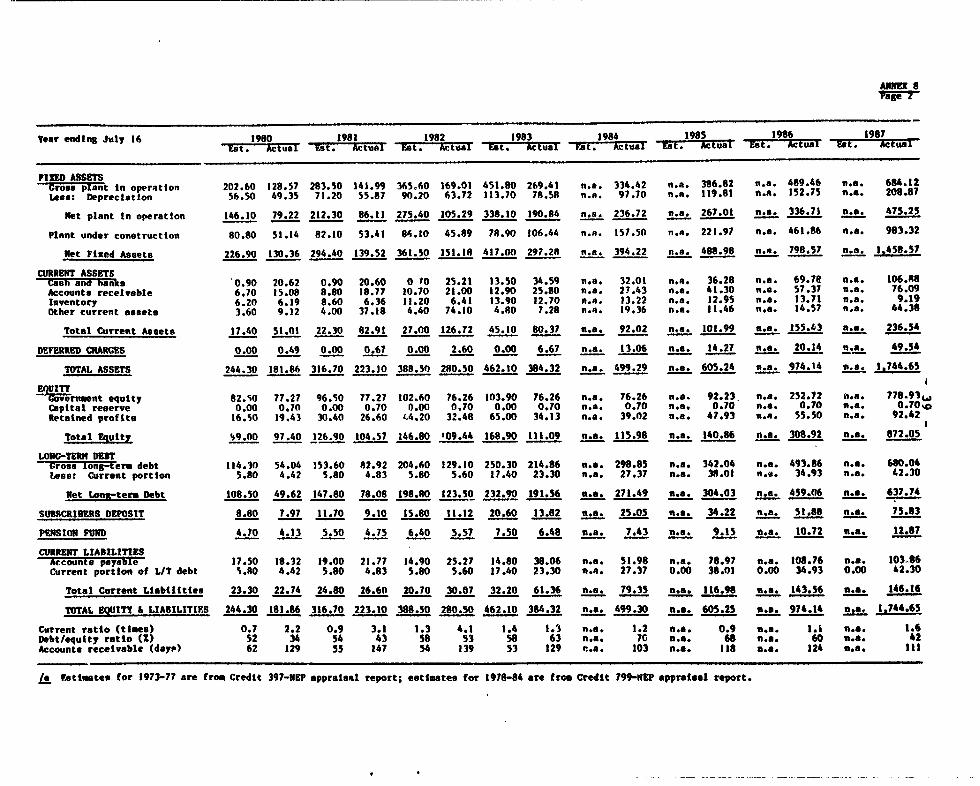

1. Physical Installation...................... .... .. g..... 302. Local Exchange Installations................................ 313. Project Costs...... ............... ...................... 324. Schedule of Credit Disbursements ............................ 335. Credit Allocations and Disbursements........................ 346. Key Performance Indicatorso.................................. 357. Estimated and Actual Income Statements: 1973-87............ 368. Estimated and Actual Balance Sheets: 1973-87............... 389. Estimated and Actual Funds Flow Statemeits: 1973-87........ 4010. Employees and Productivity......... ......... ................ 4211. Summary of Basic Telecommunications Tariffs................. 4312. Compliance with Covenants...........e.......................... 4413. Return on Investments....................................... 45

NEPAL

SECOND AND THIRD TELECOMMUNICATIONS PROJECTSCRD ITS 397-NEP & 799-NEP

PROJECT COMPLETION REPORT

Preface

1. This is a combined Project Completion Report for the Second andThird Telecommunications Projects which were supported by IDA Credits 397- NEPand 799-NEP respectively. The basic data relating to the two credits are asfollows:

Credit 397-NEP Credit 799-NEP

Borrower His Majesty's Government of Nepal (HMG/N)Beneficiary Nepal Telecommunications Board/

Corporation (NTB/NTC)Amount US$ 5.5 million US$ 14.5 millionApproval Date March 16, 1973 May 11, 1978Agreement Date June 26, 1973 August 22, 1978Effectiveness Date September 20, 1973 February 27, 1979Closing Date

Original June 30, 1980 June 30, 1984Actual December 31, 1982 June 30, 1985

2. This report was prepared by the Asia Technical Department based onthe information supplied by NTC co an IDA mission in February 1988 and datagathered from IDA files and other relevant reports.

3. In accordance with the revised procedures for project performanceaudit reporting, this Project Completion Report was read by the OperationsEvaluation Department (OED), but the project was not audited by OED staff.

4. Following standard procedures, OED sent copies of the draft reportto the Borrower and the Executing Agency for their comments; however, nocomments were received.

- il -

PROJECT COKPLtION REPORT BAStC DATA SOHPT

NEPAL, SECOND TKLKOCOP4UtNICATIONS PltJECI (CttDlT 397-Nip)

xIEY PROJECT DATA

Appralqftl k,-t at nttte xpectation current estimate

total Projeet Cost (0I55 Itliton) 7.8t 7.ROOverrun (t) _ (n1)

Loan/Credit A_out (USS mtilton) 5.50 5.50Otebrd )-5Cancelled )Repaid to _

Outetandins to )Cate Physical Coeonents Copetetd 172t679 t2131/83Proportion Completed by Above oate (2) 20tProportion of Tim Underrun or Overrun (2) 80XEconomic 4ate of Return (2) _ t8 __ 13 /aFinanctal PerfOInce Satfactory SatiteactoryInstitutionat Perforsnce Satisfactory

OTHER PROJECT OATA

Ortgtnat Actuat orttm Plan Rvwtsions Est. Actual

First lXntton tn Ftles ot Ttetbte t / I / 02/11/t2Goverrmnt's Applicetion N0 /73Negotiations 03/16773Board Approval 04/Z613toan/Credtt ABreemsnt Date i -7 06/20i73Effectivenese Doate /I 7 09/1/Closing DOat O6/30/80 12!31/82

aornrew His slestv s Govevrment of t1elExecutingt AgeB y

3epal TalQcoMangcans Cororation (N=TC)

Fiscal YTet of Borrower July t6 -July 15Follow-on Project Name Third Telecommuntc4tions Prolect

Loan/Credit Nuabur Credit 799-NE?Aiount (USS .1111ov) 14.50Lean/Credit Agreemnt Date 08/22/18

tlSSt1N DATA

no. of No. of Date ofItem Month. Tsar Days Persons Han-eka Report

tdatifitea-ioePreparationPreappraLeal,60 ~ U7Appraisal tO/720 O

Total 21 6.0

Supervtsion I 7 A 1.0 04/25/74Supervtoson Et 061 7 i .4 0 0912/74Supervcsion tt 075. 07124/75Superviston IV 3 1 0.4 Ti;Sup.cwtdion V _12Supervsteion Vt o576 7 1.0 06/11/16Supervision Vit 7 1 1.0 O1/1l/77Supervteton VIII 11/77 7 tt1.0 ;7Superviston t? 12/78 3 2 01103179Supersiica Ix /b 10793 2 0.9 O1/ 1 0

uprvtstion Xt 0 9 180 Y I 0. 7 soSupeielon KIXtl 04181 2 0.9 04Suprvitston Xltt 1t t 0.4 Supervtion XIV . 3 0.9 01 /7/82

aupetviaon X 07tS_2 202T7Supeevistom XVI 1082 1 0.2 10282Supervision iv:t 12/82 T 2superviston xVttt 04/63 3 t 0.4

Supbtete XU _ _ 4 2 t .2 _8228Superviesio XII -69m____Supervision XI 10/8 2 0.6 10/18/Supervision Xlt 06/84 1 106TiSuperviston tXII 02/85 1 0.2/14/65Supervtitsn XXIttl 10/7S 4 * 1IQ/1/S5Completion 072f/ _2 _1 0.7_

Total 17.

COURT BXCAtUIA;C RAAtS

Mans of Curreny (ebbrevietton) Iuooe(es R

Aptrtell Tear AvTas ES Pxchange Rats: USSt tInteing Ter Averag n Y r 197463 USS1 b N oComplewti peaiU US$198. W SI* 15.20

j. Coebind with the Third Project due to twe diffitculty in seperating the economic banattt Of the tweb projects.

lb Miesione in £979 to 1915 were, coombined aupervision missions for the Second and IbirCd PrO gQCt9.

- iii. -

PROJECT COMPLETION REPOR BASIC OATA SHEET

NFPAL: TIIRD TELECO29WNICATIONS PROJECT (CREItT 799-HEP)

KEY PROWCr DATA

Appratsal Actual orIten exuectation current estimate

Total Project Cost (US$ miltion) 25.56 33.02Underrun ot Overrun (2) - - 29.20

Loan/Credit Amount (Us$ *illton) 14. 50s 14.50Disbureed )14.0CancelledRepaid to )outstanding to )

bate Physical Componnts Completed 12731Pd3 12/31Pruporttion Completed by Above Date (2) IOSProportion of Time Und*rrun or Overrun (2) IOOSEconomIc Rate of Return (2) 1' 13 'iFinanctil Performnce Stisfctor SatitfectorvIntitutitonal Performance Satisfactory

OTHER PROJECT DATA

Original Actual orItem Plan Revitmona Eat. Actual

Firet Mention In Ftles or Timetable I I /1 07/214/75Covern_nt a Application /o/lO/77Negotletions _/47 /:0 0/ 0378Ibard Approval EPP 0 iiLoan/Credit Areement Date r7r77 08/22T8Iffectiveneae Dnte ITT U I 1 mZ79CLoetag Date -730847 T 30785

Borrower Hts Majesty'o Government of HNeo1xecuting Agency Nepal Telecoi nications Corioration (NTC)

Fiscal Year of Borrover July 16- July 15Follow-on Project Name Fourth teleco nteetions ProJect

Credit N"ber Credit 15380-PAmount (U$ million) 22.0Loan/Credit Agreemnt Date April 10., _186

MISSION DATA

No. of No. of Date ofItem Month Y ear D-as Persons Man-eeks Report

Identification _ - - - -/ ' Prepreotion _ - - -?r prsoial _ - - -Appraisl 11/t6 3.6

Total _0 8.6

Supervision t 12/78 6 2 1.7 01/037Supervision 11 lb 10/79 5 2 1.4 01/18180Superviiton tt1 09/a T 1 1.0 09/15180Supervisoln IV 09/81 8 2 2.3 04109/81Superviston V 10181 1.0 1097 8Superviston VI 01182 3 2.7 0317/82Sur rvtiton VII 7 /8 2 1 1.0 07013182Supervieion VIII 10182 1 0. 5 10/2682Superviston tX 12 i82 1.4 12/i711Supervtison X 04/83 8 I.2 05/09/83Supervioson Xt C8/83 2 _____2. 0 08i22183Supervision Ell 10/83 S 2 1.2 -I 07§;MSupervision Xllt 06/84 5 _1 0.14/d4Suparvtelon XIV 02/85 1 0.7 03/14785Supervision XV 10/85 4 3.0 i 10/3r3/6Supervision XVI 05/86 5 2 1.4Superviston XVII 10I86 1 .11510/86Completion _02/8 3 1 0.5 /

Total -3.7

COUNTRY EXCHANGE RATES

Nam of Currency (abbreviation) Rupees ( NR)

Appraisal Year Average 1976 Exchange Rate: US$I - NJ 12.00Interventng Years Average 8 1t ii6 ussi - NB 15.93Completion year 1987 US$1 l H1s 21.60

/e Combined with the Second Project due to the dtfficulty in separating the economic benefits of the tweprojects.

lb ftHiicse In 1979 to 1985 were combined super"ision miestons for the Second and Third Projects and in 1986for the Third and Fourth Projects.

- iv -

NEPAL

SECOND AND THIRD TELECOMMUNICATIONS PROJECTS

CREDITS 397-NEP & 799-NEP

Highlights

i. IDA has been involved in the telecommunications sector in Nepalsince November 1969 when the First Telecommunications Project, Credit 166-NEPfor US$1.7 million was approved. Though its completion was delayed, it wasoverall successful. A major achievement was the creation of the Nepal Tele-communications Corporation (NTC) aa a statutory corporation in June 1975. TheSecond Project, Credit 397-NEP for US$5.5 million, and the Third Project,Credit 799-NEP for US$14.5 million, were approved in April 1973 and May 1978,respectively and are the subject of this Project Complet.ion Report. Bothprojects aimed at further physical and institutional development of the tele-communications sector to improve the availability and quality of local andlong-distance telephone services.

ii. The two projects were overall successful. They made significantcontributions to the development of physical facilities ind improving thequality of the telecommunications services as also towaras the institutionaldevelopment of NTC. The completion of both projects was substantially delayedby about four years. The main contributory factors were: (a) delay in start-up due to delays in design and procurement; (b) break-down of contractnegotiations with the selected bidder of switching equipment for the SecondProject; (c) decision to adopt digital technology long after the start of theThird Project; (d) delay in arranging financing for the uncovered balance ofthe foreign costs of the digital switching and transmission equipment whichwere nearly twice the funds available under the IDA credit for these items;and (e) delay in commissioning of the switching and transmission equipment bythe turn-key contractor.

iii. The two projects eventually achieved their physical targets. Thenumber of working telephone connections increased by over four times. A back-bone of high-capacity modern long-distance network has been established whichwill assist also in penetration of service into rural areas. The introductionof automatic subscriber trunk dialing facility between aitomatic exchangeseliminated the earlier long delays in long-distance call completion due tolack of circuits and manual operation. The provision of the satellite earthstation improved significantly the quality of international telephone servicesand enabled introduction of modern services like facsimile and data.

iv. The actual total costs of Second and Third the projects were higherthan estimated at appraisal by 162 and 90Z respectively in terms of NepaleseRupee and 1X and 382 in terms of US dollar. The large increases in totalcosts in terms of NRs (compared to US dollar) were mainly due to: (a) sub-stantial devaluation of the Nepalese Rupee during the project implementationperiod, and (b) substantial increase in the Third Project costs as a result ofthe high cost of the digital switching equipment which was more than double

the appraisal cost estimates. The higher initial cost of digital equipmentwould be more than compensated in the long-term by the substantial techno-economic benefits of digitalization at the network of the very early stage ofits development; also substantial costs would otherwise have had to beincurred in future in integrating the old technology equipment in a digitalenvironment. The local cost overruns of the two projects were financed by NTCthrough its own funds; the foreign cost overrun of the Third Project wasfinanced by a foreign commercial bank loan.

v. NTC's overall financial performance was generally satisfactorythroughout the project period (FY73-86). NTC's annual rates of return wereconaistently above the covenanted levels except for FY75. The debt servicecovenant was met consistently except in FY84 and FY85. NTC's financialposition and cash flow situation deteriorated during FY83-85, but recoveredsubstantially in FY86 and FY87. Audited financial statements were generallysubmitted 3-4 months later than the covenanted deadline and accountsreceivable were high.

vi. Institutionally, NTC has developed from a Covernment Board dependenton expatriates to fill key management positions into a well-managed publicsector corporation manned entirely by Nepalese. NTC's staff productivity interms of staff employed per 1,000 telephones improved from 172 in FY74 to 86in FY87. NTC is now much better placed institutionally to effectively andefficiently develop, operate and manage the telecommunications ser-7ices inNepal. Some institutional deficiencies exist and these are being addressed byIDA-financed management consultants under the Fourth TelecommunicationsProject approved in April 1986.

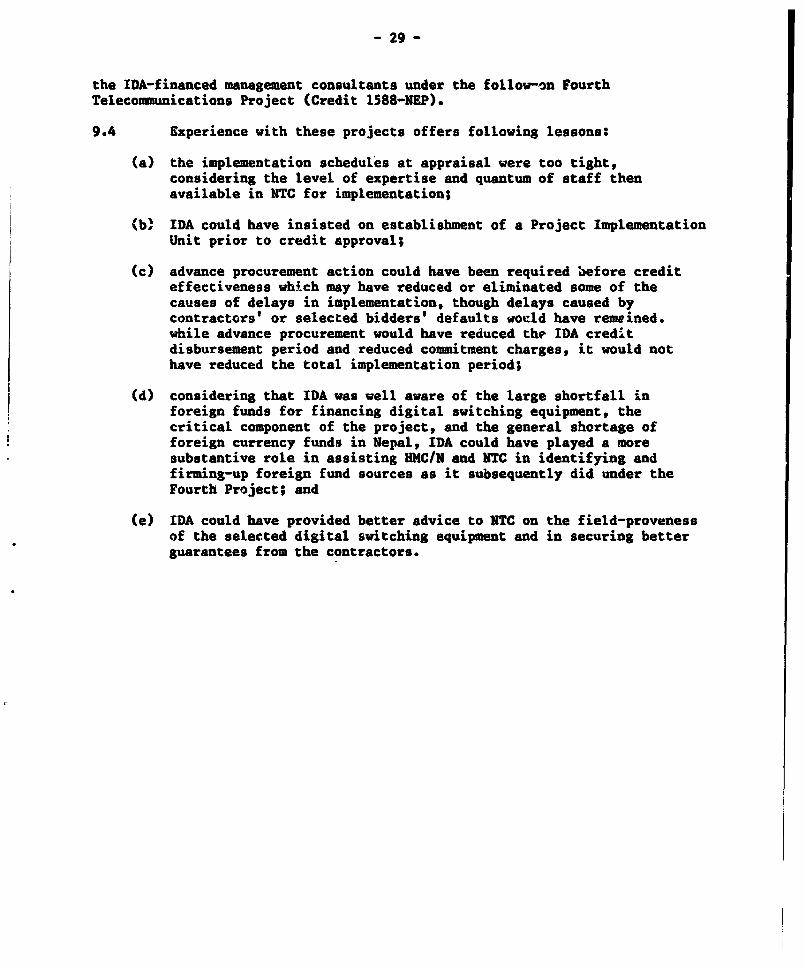

vii. Experience with these projects offers following lessons:

(a) the implementation schedules at appraisal were too tight,considering the level of expertise and quantum cf staff thenavailable in NTC for implementation;

(b) IDA could have insisted on establishment of a Project ImplementationUnit prior to credit approval;

(c) advance procurement action could have been required before crediteffectiveness which may have reduced or eliminated some of thecauses of delays in implementation, though delays caused bycontractors' or selected bidders' defaults would have remained.While advance procurement would have reduced the IDA creditdisbursement period and reduced commitment charges, it would nothave reduced the total implementation period;

(d) considering that IDA was well aware of the large shortfall inforeign funds for financing digital switching equipment, thecritical component of the project, and the general shortage offoreign currency funds in Nepal, IDA could have played a more

- vi -

substantive role in assisting UHC/N and NW'C in identifying andfirming-up foreign fund sources as it subsequently did under theFourth Project; and

(e) IDA could have provided better advice to NTC on the field-provenessof the selected digital switching equipment and in securing betterguarantees from the contractors.

NEPAL

SECOND AND THIRD TELECOMKMUNICATIONS PROJECTSCREDITS 397-NEP & 799-NEP

Project Completion Report

I. INTRODUCTION

Telecommunications Sector

1.1 The authority for the development, operation aid management of thetelecommunications sector in Nepal is vested in the Ministry of Communications(MOC). In 1959, His Majesty's Government of Nepal (HMG/N) established aTelecommunications Department within the Ministry. In October 1968, the NepalTelecommunications Board (NTB) was created and in June 1975, it was convertedinto Nepal Telecommunicaticns Corporation (NTC), a fully government ownedpublic sector corporation.

IDA's Involvement in the Sector

1.2 IDA has been involved in the telecommunications sector in Nepalsince 1969. The first IDA credit to the sector, Credit 166-NEP for US$1.7million, was approved in November 1969. It provided for expansion of localtelephone facilities in Kathmandu, some HF radio systems for the long-distancenetwork and a land-line link to India. A major institutional achievement wasthe creation of NTC (para 1.1). The project was completed in July 1977, fouryears behind schedule. A Project Completion Report was issued in December1977.

1.3 IDA Credit 397-NEP for US$5.5 million for the Second Telecommunica-tions Project and Credit 799-NEP for US$14.5 million for the Third Telecom-munications Project were approved in April 1973 and May 1978 respectively.These projects supported further development of local telephone facilities inKathmandu and other urban areas to meet the growing demand for telephoneconnections, installation of VHF and micro-wave systems in the long-distancenetwork and installation of automatic switching equipment for introduction ofsubscriber trunk dialing (STD) service between automatic exchanges. TheSecond and Third Projects were completed in December 1983 and December 1987respectively and are the subject of this combined Project Completion Report(PCR).

1.4 The PCR is based on data supplied by NTC to the supervision missionsin 1987 and PCR mission in February 1988, and on data collected from the IDAfiles, the appraisal and supervision reports and the legal documents relatingto the two projects and the follow-on Fourth Telecommunications Project(Credit 1588-NEP).

-2-

II. PROJECT PREPARATION AND APPRAISAL

A. Second Telecommunications Project

Preparation, Appraisal and Credit Approval

2.1 No specific request from HAG/N for IDA assistance to the telecom-munications sector is traceable in the IDA files. However, the developmentplans for the proposed Second Telecommunications Project were first preparedby an expatriate staff of the NTB in late 1971. After some discussions withNTB on the proposed large scale use of HF radio systems vis-a-vis microwaveand UHF/VHF radio systems and introduction of subscriber trunk dialing (STD)vis-a-vis manual operator dialing facility in the long-distance network, theSecond Project was appraised in September-October i972. The IDA credit forUS$5.5 million was negotiated between March 12 and 16, 1973, and approved byIDA'S Board of afxecutive Directors on April 26,1973. The credit agreement wassigned on June 20, 1973.

Project Objectives

2.2 The overall project objective was the further development of thetelecommunications facilities started under the First Project.

Project Description

2.3 The main components of the Second Project to be implemented duringFY75-79 were as follows:

(a) installation of 7 automatic and 3 manual exchanges with 7,350 linesand 310 lines capacity respectively; expansion of existing 2automatic exchanges by 1,100 lines; and conversion of 5 manualexchanges (capacity 850 lines) to automatic with 1,450 lines;

(b) expansion of local cable distribution network and installation ofsubscriber terminal equipment to connect about 8,400 newsubscribers;

(c) installation of (i) 2 new microwave radio systems, standby radiochannels on two existing microwave systems and multiplex equipmenton the above systems for 96 speech and 6 VFT channels;

(d) installation of about 250 lines of trunk switching equipment in 6existing exchanges;

(e) installation of one manual telex exchange with 80 lines capacity andprovision of 90 teleprinters;

(f) installation of one international HF radio station;

(g) provision of vehicles, tools, test equipment and training equipment;

-3-

(h) construction of a new headquarters building for NTS; and

(i) provision of consultancy services.

Project Costs and Financing

2.4 The total costs of the project were estimated at NBR 83.2 million(US$7.9 million) including foreign costs of NRs 58.2 million (US$5.5 million).The local costs were to be fully financed by HKG/N and the foreign costs fromthe proceeds of the IDA credit.

Covenants

2.5 In addition to standard IDA covenants, the Development CreditAgreement (DCA) 397-NEP provided for the following:

(a) a subsidiary loan agreement to be signed between HMG/N and NTBwithin six months of the date of the DCA [DCA 3.021;

(b) in the event of NTB being converted into a corporation, HIG/N shallmake available to IDA for comment the rules and regulationsspecifically applicable to such corporation prior to their adoption[DCA 4.04(c)];

(c) HMG/N to cause NTB to adopt measures to improve the performance andproductivity of its employees [DCA 4.051;

(d) by July 16, 1973, NTB to adjust its tariffs to increase itsoperating revenues by a' least 15% and thereafter not reduce itstariffs until the completion of the project [DCA 4.06(a)];

(e) ITB to maintain tariffs at a level adequate to assure a minimum rateof return on average assets in service of at least 5Z in FY75-79 and1OZ thereafter [DCA 4.06(a)];

(f) ITB to maintain debt service coverage ratio of 1.5 times [DCA4.07(a)]; and

(g) NTB to submit audit reports within 5 months of the close of thefiscal year [DCA 4.01].

2.6 The status of compliance with the covenants is discussed inpara. 6.13.

- 4 -

B. Third Telecommunications Project

Preparation, Appraisal and Credit Approval

2.7 No specific HMG/N request for IDA assistance for the Third Projectis traceable in the files but the possibility of IDA assistance for furtherde,elopment of telecommunications Zacilities in Nepal was discussed in Nepalin December 1976 by an IDA supervision mission for the ongoing SecondProject. A Project Brief was issued in February 1977. The project wasprepared by the NTC and was appraised by IDA in November 1977. The IDA Creditfor US$ 14.5 million was negotiated between March 30 and April 5, 1978 andapproved by IDA's Board of Executive Directors on May 11,1978. The creditagreement was signed on August 22,1978.

Project Objectives

2.8 The principal objectives of the Third Project were defined asfollows:

(a) meet about 70Z of the total demand for telephone connections inareas already served, and provide telephone exchanges in 21 newareas and subscriber radio telephone service to 100 rural areas;

(b) automatic long-distance service in all areas served by automaticexchanges; and

(c) improve international telecommunications sw-rvices through provisionof a satellite earth station.

Project Description

2.9 The main components of the Third Project to be implemented duringFY79-83 were as follows:

(a) increase in local telephone exchange capacity by 20,600 linesincluding provision of 10 new automatic and 11 new manual exchanges,and conversion of 6 manual exchanges to automatic;

(b) installation of six 12-channel UHF systems, seven 12- channel VHFsystems and associated multiplex equipment;

(c) installation of subscriber radio telephone facilities to serve 100rural locations;

(d) installation of trunk automatic switching equipment, automaticmessage accounting (AMA) and automatic number identification (ANI)equipment for providing STD service in 19 automatic exchanges areas;

(e) installation of.a small satellite earth station for internationalservices; and

(f) installation of a telex exchange to serve about 400 subscribers.

-5-

Pr.ject Costs and Financing

2.10 The total costs of the project were estimated at NRs 306.8 million(US$25.6 million), including foreign costs of NRs 210.0 million (US$17.5 mil-lion). The local costs were to be financed in full by NTC from its internalresources. Of the foreign costs, US$14.5 million were to be financed from theproceeds of the IDA credit and the balance US$3.0 million (being the estimatedcosts of the telex exchange and the satellite earth station) by the OverseasDevelopment Agency (ODA) of United Kingdom.

Covenants

2.11 Other thar the standard IDA covenants, there were no covenantsspecific to the preject in DCA 799-NEP. Under the Project Agreement (PA), theNTC was required to comply with the following:

(a) employ engineering consultants for design, detailed engineering,preparation of technical specification and bid documents, andevaluation of bids for local and trunk switching equipment, telexexchange and satellite earth station [PA 2.02];

(b) not later than December 31, 1980, carry out an Economic Study of theTelecommunications Sector in Nepal (PA 2.08];

(c) not later than the end of FY79, introduce a commercial accountingsystem [PA 4.01(b)];

(d) submit audit report within six months of the end of each fiscal year[PA 4.021;

(e) maintain tariffs at a level adequate to ensure a rate of return ofat least 8% per annum for FY79 and FY80 end 10% per annum for eachyear thereafter (PA 4.03(a)];

(f) commencing not later than July 15, 1979, review the value of itsassets every 12 months and revalue the assets if the value of theassets is 10% more than their value on July 15, 1977 [PA403(a)]; and

(g) maintain debt service coverage ratio of at least 1.5 times (PA4.04(a)].

2.11 The status of compliance with the covenants is discussed inpara. 6.13.

III. IMPLEMENTATION

A. Second Telecommunications Project

Credit Effectiveness and Start-up

3.1 There being no specific conditions for credit effectiveness, tiecredit was declared effective on the date specified in the DCA, namelySeptember 11, 1973.

3.2 An English translation of a Subsidiary Loan Agreement datedAugust 15, 1974 between the HMG/N and NTB (over eight months behind the datespecified in the DCA) was received by IDA in September 1974 and found to bedeficient in some respects. However, since it was based on a similaragreement in respect of IDA Credit 166-NEP for the First TelecommunicationsProject which IDA had accepted at that time, IDA did not insist on anyamendments. The revision of tariffs required by July 15, 1973 (DCA 4.06(a)]was actually implemented in January 1974. On other items relating to theproject start-up, there was little action in 1974 and 1975, primarily becauseIDA's expectation of the design work being carried out by available expatriatestaff were belied. The actual first steps in the design of the network weretaken only in 1976 after the required experts and consultants became availablein late 1975.

Revision of Project

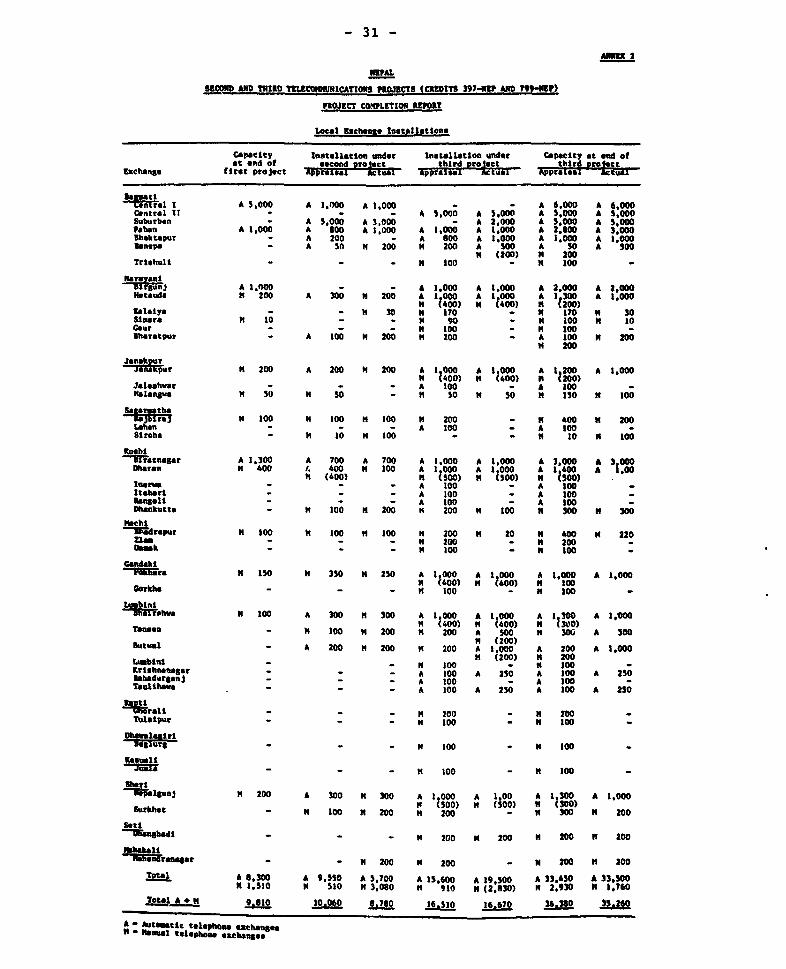

3.3 Annex 1 gives a comparison of the physical installations as plannedand those actually completed. There was no substantive revision of theoverall scope of the project. However, some changes in the type and sizes oftelephone exchanges became necessary (Annex 2) due to delay in project start-up, changes in the demand pattern, the post-appraisal decision to digitalizethe network and combine the procurement of automatic switching equipment forthis and the follow-on Third Project, and the need to provide emergency reliefin some areas. Against 9,550 lines of automatic exchanges proposed atappraisal, only 5,700 lines were installed under this project and the balanceunder the Third Project. On the other hand, against 510 lines of manualexchanges proposed at appraisal, 3,080 lines were installed, most of whichwere subsequently replaced by automatic exchanges under the Third Project asby that time NTC had decided to reduce manual exchanges in the network to theminimum. Total increase in the capacity of automatic exchanges under theSecond and Third Projects was 25,450 lines against appraisal estimate of26,570 lines. Net addition to manual exchanges was only 250 lines under thetwo projects though 3,080 lines were first installed under the Second Projectof which 2,830 lines were replaced under the Third Project.

3.4 The transmission equipment was installed substantially as planned.The long-distance routes on which transmission equipment was installed werenot changed. The reduction in the number of transmission systems (Annex 2)was because of changes in system configuration.

- 7 -

3.5 Two deletions from the project were (a) headquarters building forNTC due to the very low priority allotted by HMG/N to such civil works, and(b) the 600-line PABX for the government agencies which was provided by HMG/Non its own and NTC's services were requested only for its maintenance. Also,due to cost over-runs on other project items, the expansion of telex exchangewas postponed to the Third Project. While the changes in the project detailswere noted and agreed by the IDA supervision missions, no formal revision ofSchedule 2 of the DCA 397-NEP was issued. The reduced local exchangeinstallations under the Second Project reduced the benefits forecast atappraisal from this project. However, the balance lines were installedsimultaneously with similar installations under the Third Project and thusincreased the benefits forecast for that project.

Implementation Schedule

3.6 At appraisal, the project was expected to be completed by July 1979.However, only 20Z of the physical facilities were completed by that date. Amajor portion of the manual exchange expansion was completed in 1980 and 1981and the transmission network in 1981 and 1982. Installation of the automaticexchanges in Kathmandu (for which procurement was combined with similarequipment under the Third Project) was delayed substantially and the exchangewas commissioned in December 1983, completing the project, about four and one-half years behind schedule.

3.7 The delay is attributed mainly to the following:

(a) staff changes at the senior management level and delay in obtainingtechnical assistance for design, detailed engineering and prepara-tion of technical specifications and bid documents after theappraisal expectation of these items being carried out by availableexpatriate staff did not materialize;

(b) delay in procurement of switching equipment as the supplierinitially selected after international competitive bidding (ICB) wasfound during contract negotiations to be unable to comply with theimportant technical requirement of signalling; NTC, with IDAconcurrence, decided to cancel that tender and combine procurementof switching equipment for the Second and the Third projects underone bid;

(c) delay in commissioning of the exchanges by the supplier.

Project Costs

3.8 Annex 3 indicates the estimated and the actual costs of thedifferent components of the project. Table 3.1 below suzmmarizes the totalproject costs in Nepalese Rupees and US dollars. The exchange rate atappraisal was US$l=NRs10.56. In conversion of costs to US dollars, annualexchange variations have been applied which result in proforma exchange rateof US$l=NRs16.06 for the total project costs.

-8-

Table 3.1: TOTAL COSTS OF THE SECOND PROJECT (CREDIT 397-NEP)(millions)

Nsepalese Rupees US Dollarslocal Foreign Total Local Foreign Total

Appraisal estimate 24.97 58.18 83.15 2.36 5.50 7.86Actual 29.43 66.82 96.25 2.42 5.50 7.92Percent increase 18 15 16 3 0 1

3.9 The costs of the civil works were underestimated at appraisal. Theunit costs of the automatic switching equipment and subscriber distributionnetwork were also underestimated, though the increase in total costs wascompensated by reduction in the equipment procured. Teleprinter machineswhich were originally intended to be procured through ICB were procured fromHong Kong using local currency, whereas some vehicles which were intended tobe procured locally were procured through ICB. The increase in total costs interms of NRs is higher than in US$ because of average 52Z reduction in valueof NRs during the project period.

Disbursements

3.10 Annex 4 gives details of the semi-annual cumulative disbursementsand Table 3.2 below gives a comparison of the estimated and actual annualcumulative disbursements of the credit.

Table 3.2: CUMULATIVE DISBURSEMENT OF CREDIT 397-NEP(US$ Million)

IDA Fiscal Appraisal Actual Actual as ZYear estimate of Estimate

1974 0.2 0.0 01975 1.0 0.0 01976 2.7 0.0 01977 4.0 0.0 01978 4.9 0.7 141979 5.5 1.6 291980 - 3.9 711981 - 4.2 761982 - 4.4 80March 31,1983 - 5.5 100

- 9 -

3.11 The credit was closed on December 31, 1982, 30 months after thescheduled date of June 30, 1980. (SAR indicated credit to oe fully disbursedby June 30, 1979.) The credit continued to be disbursed daring the graceperiod and the last disbursement was made on March 31, 19M3. Since the creditwas approved only in April 1973, and considering that :'nsiderable design andengineering work had to be undertaken before procurement could commence, theappraisal estimate of commencement of disbursement during FY74 wasunrealistic. Delay in NTC securing consultants for the design work delayedprocurement and hence the disbursements.

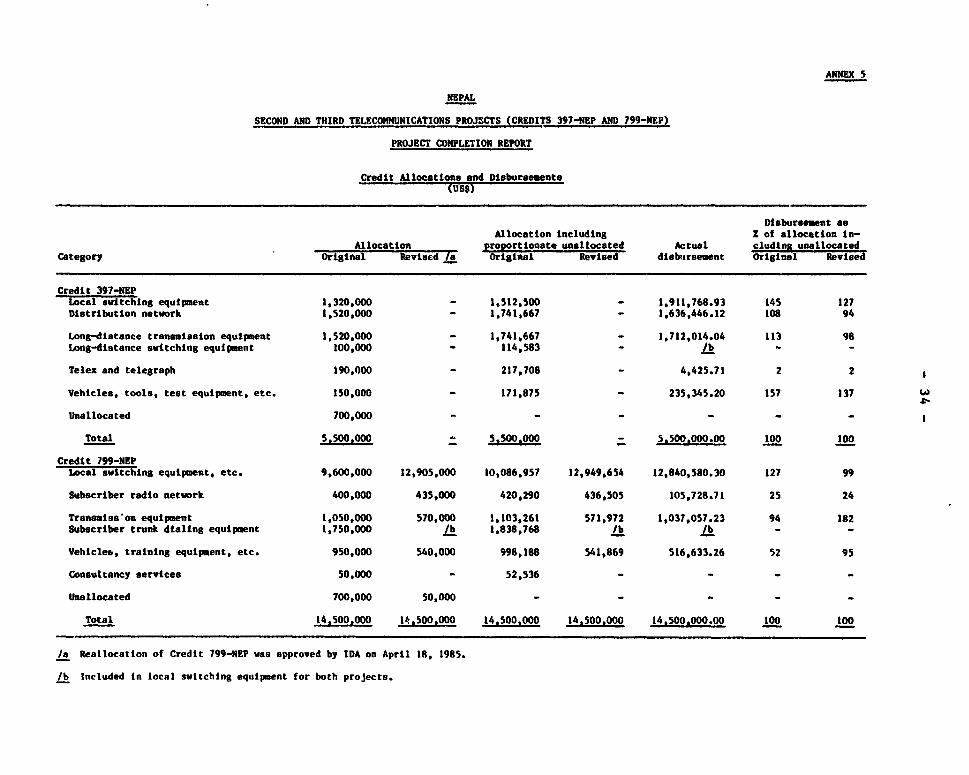

Credit Allocation

3.12 Table 3.3 below indicates the credit allocation and actual dis-bursement against each category. Annex 5 gives a detailed comparison ofcredit allocation (including the unallocated category) and actual disbursementagainst each category. Though there were some changes in project scope andfinancing of goods, no amendment to credit atlocation was issued. Higherdisbursements against categories I(a), I(b) and II(a) were due to higher unitcosts of equipment and higher value of US dollar against other currencies.The long-distance switching equipment in category II(b) was combined withlocal switching equipment and its costs included in category I(a). Incategory III, the procurement of telex exchange was deferred and teleprintersprocured using local currency funds. In category V, vehicles originallyintended to be procured with local funds were procured through ICB using IDAfunds.

- 10 -

Table 3.3: ALLOCATION AND DISBURSEMENT OF CREDIT 397-NEP(US$)

Disbursementas Percent

of AllocationOriginal Actual including

Category Allocation Disbursement Unallocated

I(a) Local 1,320,000 1,911,768.93 127SwitchingEquipment

(b) Distribution 1,520,000 1,636,446.12 94Network andSubscriberNetwork

II(a) Long-distance 1,520,000 1,?12,014.04 98TransmissionEquipment

! (b) Long-distance 100,000SwitchingEquipment

III Telex and telegraph 190,000 4,425.71 2

IV Vehicles, Tools, 150,000 235,345.20 137Test Eqpt.etc.

V Unallocated 700,000 - -

TOTAL 5,500,000 5,500,000.00 100

Reporting

3.13 NTC did not submit any periodic reports on physical implementationduring 1973-77. Thereafter, it submitted combined six-monthly reports for theSecond and the Third Projects. For the ongoing Fourth Project, NTC issubmitting quarterly reports.

Procurement

3.14 Due to changes in the top management personnel of NTB and theinability of the available staff to undertake design and engineering satis-factory to IDA, technical consultants financed by ODA were appointed andstarted work in mid-1976. Orders for the negotiated procurement of switching

- 11 -

equipment for expansion of existing exchanges were placed in February 1976 onfirms in Sweden and India for US$ 602,000 equivalent. Orders for items otLtrthan automatic switching equipment were placed between 1977 and 1979. Forautomatic switching equipment, bids were first invit_d in June 1977 and thesuppliEr was selected with IDA's concurrence in August 1978. However,problems arose during contract negotiations with the selected supplier when heexpressed his inability to meet the important specification requirement ofsignalling. It is not clear hot this aspect was overlooked during evaluationby both NTC and IDA. After consultation with IDA, the bid was declared non-responsive. NTC considered the various alternatives proposed by IDA andfinally accepted IDA's preferred alternative of combining procurement ofswitching equipment for this project with that for the Third Project and thetender was cancelled. At the same time, in consonance with the general worldtrend towards digitalization of telecommunications networks, NTC with full IDAsupport decided to procure only digital switching equipment for both projectsinstead of the analog type proposed earlier.

3.15 Bids for the digital switching equipment were announced in December1980 and received in March 1981. There was substantial delay in the evalua-tion of bids as NTC was evaluating bids for digital equipment for the firsttime. The successful bidder selected by NTC was approved by IDA in February1982. The value of the contract was estimated at approximately US$19.5 mil-lion equivalent (based on the then currency exchange rates) which was far inexcess of the funds (approximately US$9 million) available under the two IDAcredits for this equipment. Securing the financing for the full contractprice became a major issue. A possible alternative of reducing the quantum ofequipment and the scope of the projects was considered, but not accepted,because of acute shortage of available facilities vis-a-vis the pendingdemand. IDA required the NTC and HMG/N to secure financing for the balancecontract price not covered by the available funds in the two IDA creditsbefore signing the contract. However, NTC signed the contract on May 28, 1982before the funding arrangements were in place. Si.:bsequently, HMG/N asiuredIDA that it would cover the balance of US$10.5 million from its own and/orother sources. With this assurance, IDA approved the contract. HMG/N's shareof firancing was reduced from US$10.5 million to US$7.2 million in June 1984when additional funds were all3cated to category 1 of Credit 799-NEP to coverthe contract price. HMG/N was unable to provide even these reduced funds andinstead permitted NTC to finance US$2.2 million from its own funds and securea commercial bank loan for the balance. It was, however, oixteen monthsbefore the commercial bank loan was secured. During this period, for lack ofassurance of payments, the contractor suspended delivery of equipment andservices, which further delayed the installation of the switching andtransmission equipment.

3.16 In summary, the major causes of delay in completion of the projectwere the initial 2-year delay in the start-up of action on procurement, delayin award of contract for the switching equipment and delay in delivery ofequipment by supplier because of non-availability of funds with NTC to pay forit.

- 12 -

Performance of Consultants, Contractors and Suppliers

3.17 Consultants financed by ODA were appointed in late 1975 for designand detailed engineering of the switching equipment; expatriate staff financedthrough the Colombo Plan held key management positions in NTB/NTC till 1978.The performance of the consultants and the expatriate staff was satisfac-tory. The performance of contractors and suppliers was generally satisfactoryexcept for the turn-key contractor for the digital switching equipment. Theperformance of this contractor is discussed in para. 3.32.

B. Third Telecommunications Project

Credit Effectiveness and Start-up

3.18 There were four conditions of effectiveness of the credit, namely(a) signing of the subsidiary loan agreement between HMC/N and NTC;(b) tariffs to be increased substantially by July 16, 1978; (c) employment ofconsultants for design, preparation of technical specification and bid docu-ments, and evaluation of bids for major items for the project; and (d) con-firmation of availability of cofinancing for two project components. Theoriginal effectiveness date (November 20, 1978) was postponed to January 19,1979 and later to February 28, 1979 because of non-compliance with conditions(a) and (d) above, and for lack of formal evidence of compliance with (b) and(c). The credit was declared effective on February 27, 1979.

Revision of Project

3.19 There was no substantive changes in the overall scope of the project(Annex 1) though there were some changes in the types and sizes of localexchanges (Annex 2) and in the transmission systems primarily arising out ofthe post-appraisal decision on technology supported by IDA to digitalize thenetwork (para 3.14).

Implementation Schedule

3.20 At appraisal, the project was expected to be completed by December1983. However, less than 10X of the physical facilities were actuallyinstalled by that date. The project was substantially completed byDecember 31, 1987, four years behind schedule, but some facilities in thedigital exchanges are not yet provided because of non-availability ofsoftware. These are now expected to be introduced in the exchanges only inlate 1989 as the supplier has yet to develep the required software.

3.21 Several factors contributed to the substantial delay in projectimplemwntation. First, there was delay of nearly two years in the start ofprocurement for all items except for small radio systems. For the major itemsof switching and transmission equipment, delay was due to the post-appraisaLdecision of NTC to digitalize the telecommunications network in Nepal. Therewas also delay in securing the services of consultants for design and detailedengineering, and preparation of technical specifications and bid documents forthese items. Second, there was delay in evaluation of bids and selection ofsuccessful bidder. Third, there was delay 4n contract award to the selected

- 13 -

supplier because the funds available under the two IDA credits for these itemswere less than half the contract price. IDA insisted that NTC and HMG/Nguarantee availability of the balance of funds from their own or other sourcesbefore signing the contract. Fourth, HMG/N initially assured IDA that itwould cover the shortfall from its own and/or other sources and this assurancewas accepted by IDA; however, when the time came for actual payments to thecontractor, HMG/N could not provide NTC with the necessary foreign funds.Instead, it authorized NTC to cover the shortfall through its own internalcash generation and the balance through a commercial bank foreign exchangeloan. While NTC acted expeditiously to obtain a foreign commercial bank loan,there was delay in HMG/N's guarantee of the loan. For lack of assurance ofpayment, the contractor suspended delivery of the hardware and software forthe equipment. Fifth, there were substantial initial problems with thefunctioning of the new digital switching equipment due to software defici-encies particularly in respect of interworking of the first digital exchangecommissioned with the existing crossbar exchange. Sixth, while the aupplierhad contracted for the digital remote line units, it was later found that thesoftware for these units had not been developed. The hardware for these unitswas installed at site but it could not be commissioned for lack of software.In addition, the software for several facilities to be provided by the newdigital exchanges and for the operation of the auto-manual special servicespositions was not available due to development delays.

3.22 Because of the poor functioning of the new digitai exchanges bothinternal and in their inter-working with existing exchanges, the quality ofservice to subscribers connected to the new exchanges was initially verypoor. Further, because of traffic problems within the exchanges, NTC couldnot utilize the fulL capacity of the exchanges for subscriber connections tomeet the pending demand though, in some areas this was also due to non-availability of cable distribution network due to delay in its construction byNTC. The malfunctioning of the new digital exchanges also delayed introduc-tion of STD service for long-distance calls. All these affected NTC'srevenues, prolonged subscriber dissatisfaction with the quality of serviceprovided by NTC and, in general, eroded public confidence in NTC's ability todeliver the much-needed telecommunications services.

Projects Costs

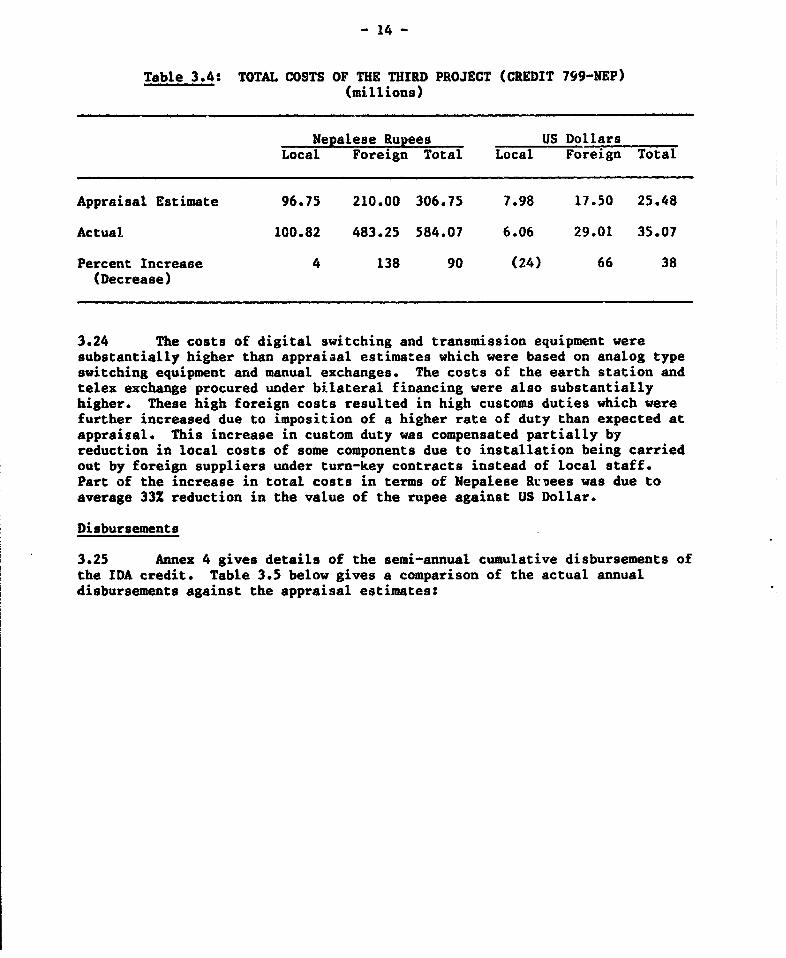

3.23 Annex 3 details the estimated and actual costs of individualcomponents of the project. Table 3.4 below summarizes the total costs inNepalese Rupees and US Dollars. The exchange rate at appraisal wasUS$1=NRsl2.00. In conversion of costs to US$ equivalent, annual exchange ratevariation. were applied which result in a proforma exchange rate ofUS$l=NRs16.60 for the total project costs.

- 14 -

Table 3.4: TOTAL COSTS OF THE THIRD PROJECT (CREDIT 799-NEP)(millions)

Nepalese Rupees US DollarsLocal Foreign Total Local Foreign Total

Appraisal Estimate 96.75 210.00 306.75 7.98 17.50 25.48

Actual 100.82 483.25 584.07 6.06 29.01 35.07

Percent Increase 4 138 90 (24) 66 38(Decrease)

3.24 The costs of digital switching and transmission equipment weresubstantially higher than appraizal estimates which were based on analog typeswitching equipment and manual exchanges. The costs of the earth station andtelex exchange procured under bilateral financing were also substantiallyhigher. These high foreign costs resulted in high customs duties which werefurther increased due to imposition of a higher rate of duty than expected atappraisal. This increase in custom duty was compensated partially byreduction in local costs of some components due to installation being carriedout by foreign suppliers under turn-key contracts instead of local staff.Part of the increase in total costs in terms of Nepalese Rupees was due toaverage 33% reduction in the value of the rupee against US Dollar.

Disbursements

3.25 Annex 4 gives details of the semi-annual cumulative disbursements ofthe IDA credit. Table 3.5 below gives a comparison of the actual annualdisbursements against the appraisal estimates:

- 15 -

Table 3.5: CUYULATIVE DISBURSEMENT OF CREDIT 799-NEP(US$ Million)

IDA Fiscal Appraisal Actual Actual as ZYear estimate of Estimate

1979 0.75 0.00 01980 3.61 0.00 01981 6.55 0.05 11982 11.70 0.63 51983 14.40 4.17 291984 14.50 9.67 671985 - 13.29 92January 22, 1986 - 14.50 100

3.26 The original closing date June 30, 1984 was extended by a year toJune 30, 1985 and the credit was closed that day. IDA however continued todisburse the commicted balance during the grace period which was extended tillthe final disbursement an January 22, 1986. T- delay in disbursement wasmainly due to delayed start-up of procurement civities.

Credit Allocation

3.27 Table 3.6 below gives the original credit allocation, the revisedallocation approved by IDA on April 18, 1985 and final disbursement againsteach category. Annex 5 indicates original and revised allocations includingthe unallocated amount.

- 16 -

Table 3.6: CATEGORYWISE ALLOCATION AND DISBURSEMENT OF CREDIT 799-NEPZUS$ Millions)

Disbursementas Percent

of AllocationOriginal Revised Actual including

Category Allocation Allocation Disbursement Uiiallocated

1. Local Exchange 9.600,000 12,905,000 12,840,580.30 99Equipment andDistributionNetwork

2. Subscriber RadioNetwork 400,000 435,000 105,728.71 24

3(a) Micr3wave 1,050,000 570,000 1,037,057.23 182Radio Systems

3(b) Subscriber 1,750,000 - - -Trunk DialingEquipment

4. Vehicles, Training, 950,000 540,000 516,633.26 95Test Equipment,Tools. etc.

5. Consultancy 50,000 - - -Services

6. Unallocated 700,000 50,000 -

TOTAL 14t500,000 14,500,000 14,500,000.00 100

3.28 The original allocation against category 3(b) was cancelled as theswitching equipment for subscriber trunk dialing formed part of the localexchange equipment under category 1. No expenditure was incurred on con-sultancy services under category 5 under IDA credit as these were financed bythe ODA and Indian Aid grants to HMG/N. In respect of categories 2 and 3(a),the total disbursement was US$ 1,142,785 against revised allocation includingproportionate unallocated of US$ 1,008,477.

Reporting

3.29 NTC submitted regular six-monthly progress reports on physicalimplementation. For the ongoing Fourth Project, NTC is submitting quarterlyreports.

- 17 -

Procurement

3.30 Due to the delay in securing consultants for design, detailedengineering and preparation of technical specifications and bid documents forthe digital switching equipment, the bids for this item were invited inDecember 1980, nearly 14 months after the credit was signed. There wassubsequent delay in evaluation of bids, selection of supplier, award ofcontract, securing financing for the balance of the contract price not coveredby IDA credits, etc. (para. 3.15). For other project items, there was a delayof nearly two years in the issue of bid invitations but there were no specificproblems thereafter in award of contracts. Delays in procurement of otheritems did not materially affect project implementation which was mainlygoverned by the installation and commissioning of the digital switchingequipment and transmission equipment.

Performance of Consultants, Contractors and Suppliers

3.31 As provided under the credit, consultants were provided for design,detailed engineering and preparation of technical specification for (a) theswitching and subscriber trunk dialing equipment, and (b) the satellite earthstation and telex exchange. An expert was provided under the Colombo Plan foritem (a), but his performance was not considered satisfactory by NTC. Afterthe preparation of the bid document, services of an ITU expert were used forbid evaluation. For item (b) above, consultants financed by the ODA wereemployed whose performance was satisfactory. A firm of local consultantsappointed and financed by the Planning Commission of HMG/N, were employed tocarry out the Economic Study of the Telecommunications Sector in Nepal. Thestudy was carried out in 1981, and its draft report was reviewed by IDA. Forthe level of expertise available in Nepal, the report indicated that the studywas well conducted and the type of data collected and their analysis wassatisfactory. IDA offered substantial comments on how the study and itsresults could be further improved. NTC made some use of the findings of thestudy in planning further development of telecommunications services in Nepaland the IDA appraisal mission for the follow-on Fourth Project also used someof the data on rural areas.

3.32 While the performance of the suppliers of other project items wassatisfactory, that of the turn-key contractor for the digital exchanges andtransmission systcms, which formed the backbone of the project, left much tobe desired. This affected substantially the implementation of the projectand, initially, the quality of service from the new equipment was poor. Thedigital exchanges offered by the supplier in response to the bid invitationhad apparentiy not been fully field-proven at that time. Some software (e.g.for remote line units, some facilities in the main exchanges and for auto-manual positions) had apparenitly not been developed before being offered, andnot made available for some years after contract signature. There was arequirement f field-proven equipment in the bid document but there was adifference ot opinion between IDA and the NTC in its interpretation duringevaluation. IDA had initially considered the equipment offered by the bidderselected by NTC for contract award as non-responsive to the field-provenrequirement but subsequently accepted the more loose interpretation applied byNTC and concurred with NTC's award decision. In retrospect, IDA's initial

- 18 -

reaction proved correct. There were also other deficiencies in the hardwareof the equipment offered, such as inadequate protection against high voltagewhich resulted in large number of failures of subscriber cards in the newexchanges. Hardware and software problems in the equipment also precluded NTCfrom loading the first commissioned digital exchange to its full capacity,causing dissatisfaction to the registered applicants on the waiting list andloss of revenue to NTC. While some delay in equipment delivery and commission-ing by the supplier could be attributed to delay by NTC in arranging forfinancing, the overall performance of the contractor for the digital switchingequipment must be judged as unsatisfactory.

IV. OPERATING PERFORMANCE

4.1 Annex 6 lists the key performance indicators relating to the overalloperating performance of NTC. The combined project targets of the Second andthe Third projects were generally achieved, though with substantial delays.In terms of local exchange capacity, 25,450 lines aggregate were installedunder the two projects against the target of 26,570 lines, and 23,920 newconnections were adaed against the aggregate target of 23,233 lines. Theactual number of working lines increased by over three times--from about 7,850lines at end of First Project to over 25,885 lines on completion of the ThirdProject. In addition to the physical growth of the network, the projectscontributed substantially to improvements in the quality of all services-local, domestic long-distance and international--through introduction ofdigital technology in the domestic network and satellite earth station forinternational services. NTC installed some new manual exchanges under theSecond Project to meet urgent demands, but these were later replaced byautomatic exchanges. NTC has since taken a policy decision supported by IDAnot to procure any new manual exchanges, though it may %se some recoveredmanual exchanges in remote rural areas. The domestic long-distance servicebetween automatic exchanges was automatized through STD service. In theinternational sector, land-lines to India and HF radio circuits to othercountries, all of indifferent quality, were replaced by high-grade satellitecircuits and the number of international circuits increased from 17 to 43.

4.2 No data is available on the improvement in call completion rate asno such data were earlier maintained by NTC. Under the Fourth Project,management consultants will propose quality of service parameters fordifferent services, including levels to be attained and methods and proceduresfor their measurements. However, from personal experience of supervisionmissions and their discussions with local public, the service quality hasimproved significantly in both the local and long-distance networks and oninternational calls. In the cable distribution network, introduction ofbetter construction methods, improved fault location and clearance procedures,and the reorganization of the outside plant maintenance department, all withthe assistance of an ITU expert financed by UNDP, have reduced fault incidenceand their duration. As regards international services, due to the multipleincrease in the number of circuits to foreign countries, the delays oninternational telephone and telex calls were substantially reduced. Inaddition, NTC was able to offer new services like facsimile transmission.

- 19 -

4.3 During project implementation, the supervision missions noted thedelays in utilization of available exchange capacities for connection of newlines because of archaic and bureaucratic administrative procedures in NTC forallocation of new lines to waiting applicants and for physical installa-tions. These were streamlined and would be further improved after therecommendations of the management consultants employed under the FourthProject are implemented.

4.4 In summary, while many internal operational problems remain andthese will be identified and addressed by IDA-financed management consultantsunder the Fourth Project, both the availability of facilities and the overalltechnical operational performance of NTC were substantially improved under thetwo projects.

V. FINANCIAL PERFORMANCE

Financial Performance

5.1 The key financial indicators for NTC for the period FY74-87 aregiven in Annex 6 and summarized in Table 5.1 below. Detailed financialstatements are provided in Annexes 7, 8 and 9. The appraisal forecasts wereprepared only up to FY83.

Table 5.1: FINANCIAL PERFORMANCE SUMMARY

FY Ending July 16 1974 1979 1983 1985 1986 1987

Telephone Revenue/DEL (NRs)Current 1,184 2,677 3,422 4,478 5,217 7,248Constant (1973 price) 987 1,753 1,401 1,650 1,615 2,025Telephone Operating Expense/DEL (NRs) 1,765 2,467 3,630 4,318 4,867 5,923Telephone Cash Op. Expense/DEL (NRs)Current 1,260 1,934 2,561 3,055 3,251 3,552Constant (1993 price) 1,051 1,267 1,048 1,126 1,006 992Rate of Return (Z) /a 1 13 12 16 15 21Long-term Debt-to-Equity Ratio (X) 21 27 63 68 60 42Current Ratio (times) 4.5 2.9 1.3 0.9 1.1 1.6Internal Cash Generation Ratio (x) 25 58 9 11 17 43Debt Service Coverage Ratio (times) 3.1 2.3 1.7 1.2 1.6 2.2

/a On historical cost basis.

5.2 UTC's financial performance was generally good over the projectperiod. From FY74 to FY77, its actual telephone revenue per line was almost

- 20 -

the same as the appraisal estimates. Between FY78 and FY83, except FY81 andFY82, the actutl telephone revenue per line was higher than the forecasts.Though the operating expense per line was consistently higher than theappraisal estimates, the rate of its increase (9.5Z per annum during FY73 toFY87) was much smaller than that of telephone revenue (15.1 per annum duringFY73 and FY87). The telephone revenues per line in real terms (1913 prices)increased from NRs 1,488 in FY73 to NRs 1,753 in FY87 as a result of severaltariff increases (para 6.11), but the cash operating expense per line in realterms was maintained at the same level of about NRs 1,000 over the sameperiod.

5.3 The rate of return (on historical cost and after tax before interestbasis) was consistently higher than the covenanted level except for 1975 andmore or less in line with the appraisal estimates despite the fact that NTCbecame liable for income taxes from FY78 which was not anticipated atappraisal. Under the Second Project, NTC was required to maintain a minimumrate of return (on historical cost basis) of 5% in FY75-79 and 10% there-after. The actual rate of return increased from 2% in FY75 to 13Z in FY79.Under the Third Project, NTC was required to revalue its fixed assets and thecovenanted rate was changed to 8Z in FY79 and FY80 and 1OZ thereafter on arevalued basis. IDA had not required NTC to undertake asset revaluation untilFY84 because the book value costs had been considered as reflecting reasonablywell their replacement costs (para. 6.6'. During FY79-84, the actual rate ofreturn on historical (and revalued) basis was consistently above thecovenanted level. Revaluation has not been undertaken until now though itappears to have been necessary from FY85. The actual rate of return (onhistorical cost basis) was 16% in FY85, 15% in FY86 and 21X in FY87.

Financial Position

5.4 NTC's financial position had been generally above expectations untilFY82, reflecting reasonable profitability and a slow growth of long-term debt(and fixed assets) resulting from delays in project implementation. The netlong-term debt-to-equity ratio had been satisfactory and consistently lowerthan the appraisal estimate. At the end of FY82, the ratio was 53/47. Thecurrent ratio was satisfactory and was 4:1 at the end of FY82. However,between FY83 and FY85, the net long-term debt-to-equity ratio increased toabout 70% because fixed assets which were financed by long-term debtincreased, much more substantially during this short period of time than inprevious years. The major factor causing the ratio to increase was the costof digital switching and transmission equipment, procured during this periodand which was substantially higher than appraisal estimate and the increase incost financed by borrowings (para 3.24). While net long term debt increasedby only NRS 117 million in the nine years between FY73 and FY82, it increasedby NRS 181 million only in the years between FY82 and FY85. The current ratiodeclined to 0.9:1 at the end of FY85. However, the capital structure andliquidity position recovered in FY86 and FY87 to a satisfactory level as asubstantial amount of the JICA-funds for a rural project started to be passedon to NTC in the form of HMG/N's equity contributions. The net long-termdebt-to-equity ratio improved to 42/58 at the end of FY87, and the currentratio to 1.6:1.

- 21 -

5.5 The level of accounts receivable was much higher than expectedthroughout the project period. From FY76 to FY80, it averaged about fourmonths and reached 147 days in FY81, compared with the appraisal target of 55days. From FY82 onwards, the trend has been improving, but it was stillequivalent to 111 days in FY87 (para 6.10).

Sources and Uses of Funds

5.6 During FY73-83 (the appraisal estimates are available only up toFY83), the annual funds requirements, and thus total borrowings, were muchless than expected due to delays in project implementation. For the wholeFY73-83 period, the actual three year average net internal cash generation was29% of capital expenditures, and local capital expenditures were covered byinternally generated funds. The ratio was comparable to the appraisalestimate of 30%. However, the internal cash generation ratio declined to 9Zin FY83, 5% in FY84, 11% in FY85 due to hign level of capital expenditure forthese three years. In FY87, the ratio recovered substantially to 43% as aresult of the tariff increase effective October 1986.

5.7 The debt service coverage ratio had been consistently satisfactoryand above the covenanted level of 1.5 times until FY83. Hcwever, the covenant.ias not fulfilled in FY84 and FY85 due to increased debt service amount, butmet in FY86 and FY87 as a result of significant increase in the number oflines connected and the tariff increase in October 1986.

5.8 The actual external financing during FY73-83 consisted of: IDA(56%), onlending of -rant funds (27%), subscriber deposit (4%) and HMG/N(13%), as compared with the appraisal estimates of: IDA (76%), onlending ofgrant funds (5%), subscriber deposit (5%) and HMG/N (14%).

Fiscal Impact

5.9 NTC's operations contributed substantially to government revenues.NTC is required to pay custom duties at 1% for equipment financed by IDAcredit and other concessional funds or 15% for equipment financed by otherforeign sources. IDA credits and other concessionary funds (except the JICAfunds) are onlent from HMG/N to NTC on commercial terms. Also, NTC pays taxesto the government, currently 40% of net incnme before pension provisions. Thenet amount paid by NTC to the government was about NRs. 270 million duringFY79-87.

VI. INSTITUTIONAL PERFORMANCE

Organization and Management

6.1 Arising out of the consultants' recommendations under the FirstTelecommunications Project (Credit 167-NEP), the Nepal TelecommunicationsBoard (NTB) was created in October 1969 as a semi-autonomous agency fordevelopment, operation and management of telecommunications in Nepal. In June1975, legislation was passed converting NTB into a fully government-owned

- 22 -

statutory corporation, NTC. Three expatriate staff financed under the ColomboPlan continued to man key executive positions in NTC till late 1978 when theywere replaced by Nepalese. W4ile NTC legally came into being in mid-1975,internal rules and regulations were not issued till 1979. However, that didnot hold up some gradual internal reorganization within NTC, such as creationof an Internal Audit Section, Training Directerate, International SystemManagement Unit, Project Implementation Unit, Operation and MaintenanceDepartment, Regional Offices, etc. Till mid-1987, NTC was divided into threemain units - engineering, business and administration, and finance andaccounts. In late 1987, appreciating the need for splitting the functions ofplanning and development from those of operation and maintenance, as also theneed to relieve the General Manager as the Chief Executive Officer of routineday-to-day management functions, three positions of Deputy General Managerswere created to take charge of (1) Planning and Development, (2) Operation andMaintenance, and (3) Finance, Business and Personal Administration. Thecreation of these positions and other reorganization measures wereorganizational changes are in the right direction. It is pertinent to notethat the reorganization was initiated by NTC management on its own without anyexternal assistance or pressure. NTC has matured considerably between 1973and 1987, growing from a small Government Board depending on expatriate stafffor key management positions to an independent corporation able to manage itsconsiderably enhanced responsibilities reasonably well. The managementconsultants retained under the Fourth Project are currently reviewing severalinstitutional issues, such as further organizational improvements, strategicplanning process, human resource development, material management, etc. Theirreport is expected in mid 1989 and recommendations will be reviewed with IDA.

Staff, Recruitment and Training

6.2 Under the Third Project, NTC was expected to improve its staffproductivity from 133 staff per 1,000 telephones in 1977 to 78 staff in 1987.The appraisal estimates and actuals achieved annually are given in Annex 10.NTC was able to achieve only a modest improvement of 117 staff per 1,000telephones by 1983, but it improved to 86 staff per *,000 telephones by 1987(against the Fou!th Project target of 92). Between 1977 and 1987, the staffemployed increased on an average 8.6% per annum against 12.5% per annumincrease in telephone lines.

6.3 NTC does not have difficulty in recruiting staff other than forhigher level technical positions, the latter due to lack of candidatesspecifically qualified in telecommunications engineering. For technicalstaff, NTC has a problem of retaining trained experienc.ad staff because ofunattractive levels of renumeration and benefits compared to those in theprivate sector. These problems persisted through the two projects andresulted in large proportion of sanctioned technical posts remainingunfilled. For example, at the end of 1987, 28Z of the sanctioned posts ofengineers and higher level technicians were unfilled. This problem was notedby IDA supervision missions, but no specific action was initiated primarilybecause the renumeration and benefits in NTC are lirked by governmentregulations to those in other state corporations. The issue has now beenreferred to management consultants un.er the Fourth Project as part of theirreview of human rcsource development in NTC.

- 23 -

6.4 During implementation of the Third Project, NTC established a well-equipped Telecommunications Training center for technical staff with ITU/UNDPassistance. The quantum and quality of training in low technology equipmentare adequate for NTC's requirements. For modern high-technology digitalequipment, suppliers were required to provide training in their establishmentsand factories abroad to a few NTC senior engineers and provide an instructorin Nepal to train larger number of technicians in new technology. Appropriatetraining equipment such as a model training exchange was also required to beprovided for the NTC's Telecommunications Training Center. On-the-jobtraining was also received by NTC staff during installation, acceptancetesting and commissioning of new equipment and during the initial period ofmaintenance of the equipmenat by contractor's staff. In summary, the trainingarrangements for technical staff for the equipment provided under the projectswere adequate and satisfactory. The NTC staff are able to operate andmaintain even the sophisticated digital equipment adequately. While there areadequate training arrangements in NTC for the technical staff, there are noprovisions for the finance, accounts and administrative staff nor forrefresher training of technical staff in new technology. The managementconsultants under the Fourth Project will address these deficiencies.

Accounting

6.5 As covenanted under the Third Project, NTC introduced a commercialaccounting system in 1979. Most accounting processes are done manually, andregional technical departments tend to be late in informing the accountoffices about the status of capital work and inventory. Consequently, delaysin account processing often occur. Though the timeliness of the accountingsystem needs to be improved, it produces accurate information and has adequateinternal controls. Computerization of the billing system will be completedafter the management consultants retained under the Fourth Project makespecific recommendations. Such a system will facilitate the timely completionof NTC's financial statements.

6.6 Under the Third Project, NTC was required to revalue its fixedassets in operation for the purpose of rate of return calculations. But,considering that the total book value of NTC's fixed assets in operation hadreflected reasonably well their replacement costs, IDA had not required NTC torevalue its fixed assets until FY84. The continuous devaluacion of theNepalese Rupee, however, has apparently increased the replacement cost of theimported equipment. Currently, the management consultants retained under theFourth Project are assisting NTC in establishing a proper revaluation method.

6.7 Recently, NTC management, which consists mainly of professionalswith engineering background, has placed more emphasis on financial managementand planning. Some evidences are: (a) NTC employed a senior charteredaccountant for the first time in FY87; (b) NTC's FY88 budget presented o theBoard included financial analysis and forecasts for the future which had neverbeen done before; and (c) a financial management/planning wing will be newlyestablished in addition to an accounting wing under the new organizationalstructure which is being put into place.

- 24 -

Audit

6.8 NTC has an internal audit department which carries out audits ofprocedures and financial records and reports to the management twice a year.Until FY79, a local auditing firm had been retained as external auditors.From FY80 onward, two auditing firms based in New Delhi have been serving asexternal auditors. NTC's financial statements have been audited in satisfac-tory manner over the project period. Under the Second Project, NTC had beenrequired to submit its audited statements to IDA within five months of theclose of each fiscal year, which had not been fulfilled. Under the ThirdProject, tne deadline for submission of audited accounts was changed to sixmonths from FY79. However, there were still delays of about four to sixmonths consistently. Delays are due, first, to the late appointment of theexternal auditors, who are appointed by HMG/N for each year and, second, tointernal procedures under which NTC's Board bas to approve draft accountsbefore these are sent for audit. Under the Fourth Project, the covenant waschanged to the effect that unaudited accounts should be submitted to IDAwithin six months of the end of the fiscal year and correspondirg auditaccounts should be submitted two months thereafter. For both FY86 and FY87,unaudited accounts were submitted before the deadline, but audited accountswere still two months late. Recently, NTC started to submit mediumo-termfinancial projections to IDA supervision missions, and this information iswell utilized by its management.

Billing and Collection

6.9 Until 1984, NTC's bills, except for telex services, were preparedmanually. The first new digital telephone exchanges were put into service bymid 1984, and the billing information for the automatic long-distance calls isnow recorded on magnetic tapes which are read by computers. The rest of thebilling system will be computerized after the management consultants makerecommendations by the end of FY88.

6.10 Though the appraisal mission had forecast that the level of accountsreceivable would improve, this did not materialize as discussed in para 5.5.Especially, collection of bills from government subscribers needsimprovement. While private subscribers generally pay promptly to avoid theirservice being cut off, outstanding bills for NTC's services to the governmentare quite high. As of the end of FY1986, the accounts receivable for thegovernment sector were estimated to be about 7 months of billing vis-a-vis twomonths for the private sector. This issue has been addressed under the FourthProject intensively.

6.11 Under the Fourth Project, HMG/N agreed to settle its overduesoutstanding as of July 1985 (about NRs 14 million) in four installments byJuly 1988 and has paid the first three installments so far. In addition, aspecial interministerial committee headed by Secretary of MOC and consistingof representatives from various concerned ministries was established in March1987 to establish new procedures to reduce government arrears in the futureand is currently working on detailed arrangements with various ministries.NTC also appointed three accounting officers for following up the status ofHMG/N's overdues in line with IDA's recommendations. The government arrearsare therefore expected to start to decline from FY88.

- 25 -

Tariffs

6.12 NTC's tariff structure is generally satisfactory. However,introduction of peak/off-peak price differentiation for both local and longdistance calls will be necessary to reduce traffic congestion during peakbusiness hours. A summary of tariff changes during the project period isgiven in Annex 11. Under the Second Project, NTC was required to adjusttariffs by July 1973 so as to increase its gross operating revenues by atleast 15X. This covenant was met in January 1974. Under the Third Project,RTC was required to effect a major tariff increase by July 1978 as a conditionof effectiveness, and tariffs were raised by about 40Z on average in 1978. In1983, tariffs on international services (telephone, telegraph and telex) wereraised. In 1984, installation charges and subscriber deposits for telephoneservices were increased with IDA's support. International telephone tariffswere again raised in 1986. However, other basic local and long distancetelephone tariffs had remained unchanged from 1978 to October 1986. InOctober 1986, all of the domestic telephone tariffs and domestic telex chargeswere raised by about 20% as required under the Fourth Project. At the sametime, long distance call charges were classified by manual and subscribertrunk dialing services.

Compliance with Covenants