wrap c&i pp final report case for recycling food... · final report business case for ... there...

TRANSCRIPT

Final report

Business case for recycling food

grade C&I PP packaging waste

Investigation and preparation of a business case for recycling food grade polypropylene from Commercial & Industrial packaging waste

Project code: IMT003-107 Date: June 2014 Research date: January to March 2014

WRAP’s vision is a world where resources are used sustainably. We work with businesses, individuals and communities to help them reap the benefits of reducing waste, developing sustainable products and using resources in an efficient way. Find out more at www.wrap.org.uk

Document reference: WRAP, 2014, Business Case for Recycling Food Grade C&I PP Packaging Waste, Prepared by Axion Consulting

Document reference: [e.g. WRAP, 2006, Report Name (WRAP Project TYR009-19. Report prepared by…..Banbury, WRAP]

Written by: Keith Freegard, Richard McKinlay, Liz Morrish, Roger Morton and Jessica Stewart

Front cover photography: Used C&I PP buckets ready for recycling at a UK PP recycler

While we have tried to make sure this report is accurate, we cannot accept responsibility or be held legally responsible for any loss or damage arising out of or in

connection with this information being inaccurate, incomplete or misleading. This material is copyrighted. You can copy it free of charge as long as the material is

accurate and not used in a misleading context. You must identify the source of the material and acknowledge our copyright. You must not use material to endorse or

suggest we have endorsed a commercial product or service. For more details please see our terms and conditions on our website at www.wrap.org.uk

Business case for recycling food grade C&I PP packaging waste

Executive summary

WRAP initiated this project because previous research1 2indicated that significant quantities of food grade polypropylene (PP) packaging are used in commercial and industrial (C&I) applications. These end uses may be a useful source of feed material for food grade PP recycling facilities and they may also provide useful end markets for food grade PP recycled from the packaging waste stream. The aim of this project is to establish whether a case can be made for a collection and recycling business for food grade PP derived from C&I sources. Many of the locations in which the target food contact PP packaging waste stream arises are within fast moving, customer service focused sites such as hotels and restaurants. Other places where this waste arises include food manufacturers which, although not directly customer facing, are still under significant pressure to focus on production activities and outputs. Both types of location may have space constraints that affect their ability to segregate multiple waste streams, although from the research undertaken this was not found to be the case in all circumstances. There was a common message that the focus for businesses was on customer service and production of goods rather than waste management. Within these challenging situations the food contact PP packaging waste would have to be segregated, stored and ideally washed separately for collection. Although the recycling plant proposed in this project would not require waste to be washed to accept it as an in feed stream, this would be preferable for extended storage at customer sites where the waste is generated prior to collection. If it is not possible to wash the waste packaging then collections would have to be more frequent due to the environmental health requirements for food manufacture and service areas. Pest control was mentioned frequently as a concern by sector representatives engaged in the research. Regular collections would be required for unwashed food contact packaging, possibly up to twice a week in months where the temperature is higher, in order to minimise the risk of odour and microbial growth. Backhauling of waste by food delivery trucks offers potential for accumulating viable tonnages of food contact PP packaging. There are already some businesses that segregate food contact PP waste packaging and send it for recycling, so this is clearly possible given the right circumstances and appropriate motivation. Where this is happening specialist plastics recyclers are accepting this waste and producing non-food grade recycled PP (rPP) for use in automotive components and packaging products such as paint tubs. A business case for setting up a C&I PP food grade recycling process from scratch has been investigated. The process design is based on a 24 hour operation with 2 tonnes per hour (tph) of feed material. Once uptime efficiency is factored in, the annual throughput of the process is set as 11,290 tonnes per annum. Table 1 shows the infeed specification set for the plant. Although suppliers will be encouraged to provide clean PP, a significant level of contamination has been allowed for.

1 ‘Scoping study into food grade polypropylene recycling’, WRAP, November 2010

2 ‘UK market composition data of polypropylene packaging’, WRAP, July 2012

Business case for recycling food grade C&I PP packaging waste

Table 1 C&I PP plant infeed specification

Feed composition (% by mass)

Food contact PP 62.5%

Ferrous metal 4.0%

Non-ferrous metal 1.0%

Stainless steel 1.0%

Glass/stones 0.5%

>other polymers (i.e. PET, PS, PVC)* 10.0%

Fat and residual contamination 20.0%

Labels/paper 1.0%

*Note: polyethylene terephthalate (PET), polystyrene (PS) and polyvinyl chloride (PVC). An outline process flow diagram was established, with major items of separation equipment identified. A mass balance model was developed for this design in order to calculate the likely yield of food grade rPP and the amount of waste generated. Figure 1 shows the proposed process flow and the results of the mass balance model. Note that 55% of the feed is recovered as food grade PP (of the 62.5% which makes up the feed), giving a yield of 88.4% for the PP present in the feed.

Business case for recycling food grade C&I PP packaging waste

Figure 1 Process flow and mass balance

11290 tpa

Granulator Caustic hot

wash

Rotary vacuum reactor

Gneuss MRS extruder

Sink float Dryer11 16 18 19 21

WasteExtruder

waste

17

Feed

22

Shredder

MagnetEddy current

separator (ECS)

8 10

6

Dry cleaner 14

Fat, residual contamination

and fines

13

Ferrous metal Non-ferrous metal

97

5

Water treatment

Product

Sluice3

15

Solid waste

23

Purge water

20

Heavies

12

Manual sort1

4

HeaviesNon-target

2Chemicals and water

Food grade approved extrusion process

Sortation and washing

909 tpa 165 tpa

430 tpa

125 tpa90 tpa

1650 tpa

689 tpa

657 tpa

334 tpa

6240 tpa

Business case for recycling food grade C&I PP packaging waste

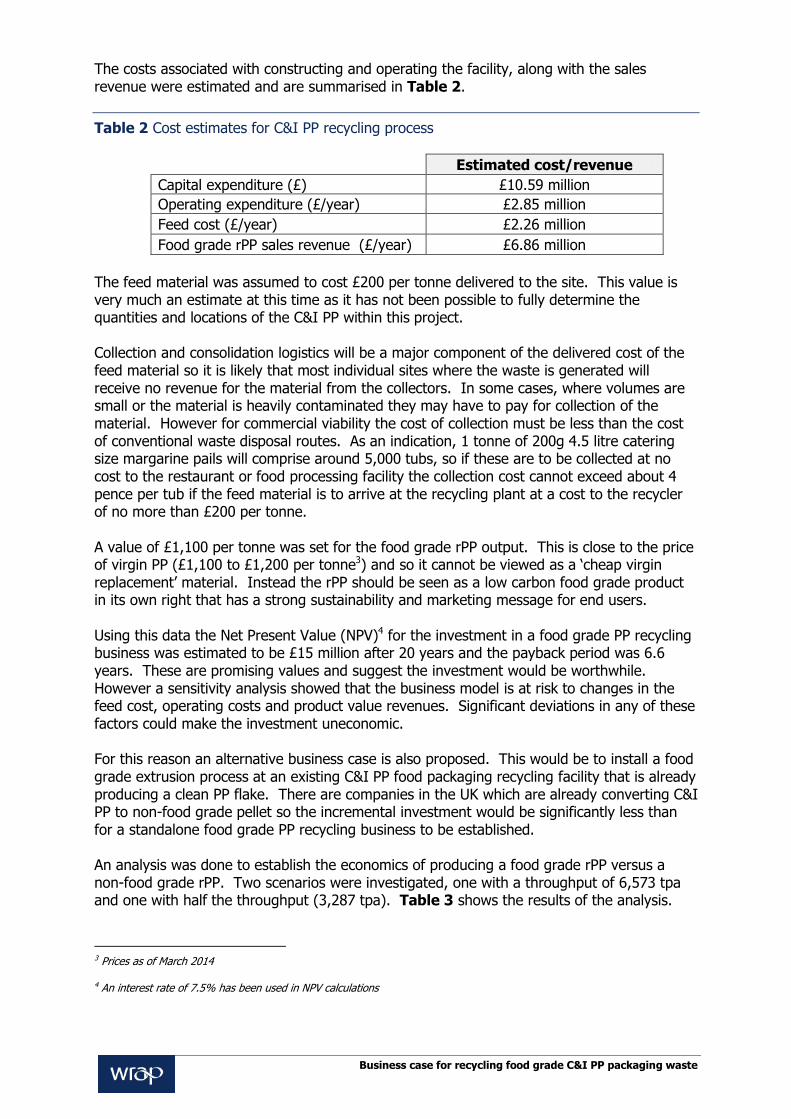

The costs associated with constructing and operating the facility, along with the sales revenue were estimated and are summarised in Table 2.

Table 2 Cost estimates for C&I PP recycling process

Estimated cost/revenue

Capital expenditure (£) £10.59 million

Operating expenditure (£/year) £2.85 million

Feed cost (£/year) £2.26 million

Food grade rPP sales revenue (£/year) £6.86 million

The feed material was assumed to cost £200 per tonne delivered to the site. This value is very much an estimate at this time as it has not been possible to fully determine the quantities and locations of the C&I PP within this project. Collection and consolidation logistics will be a major component of the delivered cost of the feed material so it is likely that most individual sites where the waste is generated will receive no revenue for the material from the collectors. In some cases, where volumes are small or the material is heavily contaminated they may have to pay for collection of the material. However for commercial viability the cost of collection must be less than the cost of conventional waste disposal routes. As an indication, 1 tonne of 200g 4.5 litre catering size margarine pails will comprise around 5,000 tubs, so if these are to be collected at no cost to the restaurant or food processing facility the collection cost cannot exceed about 4 pence per tub if the feed material is to arrive at the recycling plant at a cost to the recycler of no more than £200 per tonne. A value of £1,100 per tonne was set for the food grade rPP output. This is close to the price of virgin PP (£1,100 to £1,200 per tonne3) and so it cannot be viewed as a ‘cheap virgin replacement’ material. Instead the rPP should be seen as a low carbon food grade product in its own right that has a strong sustainability and marketing message for end users. Using this data the Net Present Value (NPV)4 for the investment in a food grade PP recycling business was estimated to be £15 million after 20 years and the payback period was 6.6 years. These are promising values and suggest the investment would be worthwhile. However a sensitivity analysis showed that the business model is at risk to changes in the feed cost, operating costs and product value revenues. Significant deviations in any of these factors could make the investment uneconomic. For this reason an alternative business case is also proposed. This would be to install a food grade extrusion process at an existing C&I PP food packaging recycling facility that is already producing a clean PP flake. There are companies in the UK which are already converting C&I PP to non-food grade pellet so the incremental investment would be significantly less than for a standalone food grade PP recycling business to be established. An analysis was done to establish the economics of producing a food grade rPP versus a non-food grade rPP. Two scenarios were investigated, one with a throughput of 6,573 tpa and one with half the throughput (3,287 tpa). Table 3 shows the results of the analysis.

3 Prices as of March 2014

4 An interest rate of 7.5% has been used in NPV calculations

Business case for recycling food grade C&I PP packaging waste

Table 3 Economics of producing a food grade rPP versus non-food grade at an existing facility

Scenario 1 Scenario 2 Food grade Non-food grade Food grade Non-food grade

Throughput of feed

(tpa) 6,573 6,573 3,287 3,287

Yield of PP after

extrusion 95% 95% 95% 95%

Capital costs £4,789,950 £1,335,9505 £4,789,950 £1,335,950

Operating costs £826,896 £441,289 £478,448 £245,644

Extruder waste

disposal cost £0 £0 £0 £0

Value of washed flake feed

£700 £700 £700 £700

Value of rPP pellet £1,100 £900 £1,100 £900

Net cash flow £1,440,847 £577,552 £655,423 £263,776

Payback period 3.3 2.3 7.3 5.1

NPV £66.5 M £33.2 M £1.0 M £7.0 M

The analysis shows that the smaller scale plant is probably not commercially viable when making either food grade or non-food grade rPP product but it makes more financial sense to produce non-food grade rPP. As throughput increases, the additional margin from food grade rPP means that in the long term it is significantly better to produce a food grade rPP product as the NPV for food grade is double the NPV for non-food grade product. Note that the payback period for the non-food grade product at the higher throughput is shorter than for food grade. This is because the amount of investment required is significantly less. However in the longer term the food grade option generates a lot more cash. The sensitivity analysis shows that this type of investment is also likely to provide a more stable and sustainable business plan. Provided the food grade rPP could be sold for at least £150 per tonne more than non-food grade rPP there would be a benefit in producing food grade. It would therefore be sensible to pursue further the possibility of taking existing clean PP flake from recycling food contact C&I PP and producing food grade rPP. Even if initial tonnages are low, it is possible in the future that household PP packaging could be separated into food and non-food contact fractions, greatly increasing the potential feed to the process in such a facility. The economics rest on being able to obtain a high price for the food grade rPP output, close to that of virgin polymer prices. In order to do this it is proposed that a joint venture between a C&I PP recycler, a packaging converter and retailer or hospitality firm could be a way to progress this business opportunity. It would also be essential to generate interest from end users in the organisations who specify the polymer content of food packaging, such as major food retailers, brand owners

5 A cost of £800,000 has been taken for a non-food grade extruder equivalent to a MAS 90 extruder

Business case for recycling food grade C&I PP packaging waste

and food manufacturers. With confirmed interest in the addition of rPP to their packaging from such parties there would be a strong driver for the waste management and recycling industry to establish the segregation mechanisms and support, the collection infrastructure and the recycling facilities required to enable the production of rPP for food contact packaging.

Business case for recycling food grade C&I PP packaging waste

Contents

1.0 Introduction ................................................................................................. 1 1.1 Background ............................................................................................... 1 1.2 Aims and objectives of the project ............................................................... 1

2.0 Project methodology .................................................................................... 2 3.0 Volumes and availability of food contact PP packaging ............................... 3

3.1 Trade associations ..................................................................................... 3 3.2 Hospitality sector ....................................................................................... 3

3.2.1 Hotels ............................................................................................. 3 3.2.2 Restaurants ..................................................................................... 4 3.2.3 Pub chains....................................................................................... 5

3.3 Retail ........................................................................................................ 5 3.3.1 Supermarkets .................................................................................. 5 3.3.2 Fast-food chains and high street food retailers ................................... 5

3.4 Facilities Management ................................................................................ 6 3.5 Food distribution companies ........................................................................ 6 3.6 Food manufacturers ................................................................................... 7

3.6.1 Sandwich manufacturers .................................................................. 7 3.6.2 Other food manufacturers ................................................................. 8

3.7 Dairies ...................................................................................................... 8 3.8 Waste Management Companies ................................................................... 8

3.8.1 Anaerobic Digestion facilities ............................................................. 8 3.8.2 Waste vegetable oil management companies ..................................... 8 3.8.3 Plastic recycling facilities ................................................................... 9

3.9 Estimate of volumes potentially available ..................................................... 9 3.10 Summary ................................................................................................ 10

4.0 Business case for a polypropylene food grade recycling facility ................. 12 4.1 Infeed specification .................................................................................. 12 4.2 Overview of process and facility ................................................................ 12 4.3 Process mass balance ............................................................................... 14 4.4 Financial viability evaluation ...................................................................... 17

4.4.1 Assumptions and evaluation basis ................................................... 17 4.4.2 Capital expenditure ........................................................................ 18 4.4.3 Operating expenditure .................................................................... 18 4.4.4 Infeed cost and product sales value ................................................. 20 4.4.5 Financial evaluation ........................................................................ 21 4.4.6 Sensitivity analyses ........................................................................ 22

4.5 Summary ................................................................................................ 25 5.0 Business case for production of food grade recycled PP pellet from cleaned flake 26

5.1 Financial evaluation .................................................................................. 26 5.2 Sensitivity analyses .................................................................................. 27 5.3 Summary ................................................................................................ 29

6.0 Conclusions and recommendations ............................................................ 31

List of Figures

Figure 1 Process flow and mass balance ......................................................................... 3 Figure 2 Process flow of C&I PP recycling facility ........................................................... 13 Figure 3 Discounted cash flow (7.5% interest rate) ....................................................... 22

Business case for recycling food grade C&I PP packaging waste

Figure 4 Discounted cash flows for flake processing ....................................................... 27 Figure 5 Closed loop food grade rPP model ................................................................... 30

List of Tables

Table 1 C&I PP plant infeed specification ........................................................................ 2 Table 2 Cost estimates for C&I PP recycling process......................................................... 4 Table 3 Economics of producing a food grade rPP versus non-food grade at an existing facility ........................................................................................................................... 5 Table 4 Infeed specification ......................................................................................... 12 Table 5 Key mass balance results ................................................................................. 16 Table 6 Plant operating basis ....................................................................................... 17 Table 7 Capital expenditure ......................................................................................... 18 Table 8 Operating expenditure ..................................................................................... 18 Table 9 Estimated labour costs ..................................................................................... 19 Table 10 Revenue from sale of by-products and waste disposal ...................................... 19 Table 11 Cost of feed and sales value of rPP ................................................................. 21 Table 12 Sensitivity of NPV when varying feed and product values .................................. 23 Table 13 Sensitivity of NPV when varying capital and operating expenditure .................... 24 Table 14 Sensitivity of NPV when varying operating expenditure and sales value of rPP .... 24 Table 15 Sensitivity of NPV when varying operating expenditure and cost of infeed .......... 25 Table 16 Variables and cost estimates .......................................................................... 26 Table 17 Sensitivity of difference in NPV when varying value of food grade and non-food grade rPP .................................................................................................................... 28 Table 18 Sensitivity of NPV when varying value of food grade rPP and value of cleaned flake .................................................................................................................................. 28 Table 19 Sensitivity of NPV when varying capital and operating expenditures ................... 29

Glossary

AD Anaerobic digestion C&I Commercial & industrial ECS Eddy Current Separator NPV Net Present Value MRF Materials Recovery Facility PE Polyethylene PET Polyethylene terephthalate PP Polypropylene rPP Recycled polypropylene tpa Tonners per annum tph Tonner per hour

Business case for recycling food grade C&I PP packaging waste

Acknowledgements

Axion Consulting and WRAP would like to thank the range of organisations and individuals that participated in and supported the research. Due to the commercially sensitive nature of the information provided the organisations and individuals are not separately acknowledged here.

Business case for recycling food grade C&I PP packaging waste 1

1.0 Introduction 1.1 Background One of WRAP’s objectives is to support UK businesses and individuals to gain value from recycling household mixed plastics waste (pots, tubs, trays and films). Collection of mixed plastics is increasing in the UK, and reprocessing infrastructure must be established to convert this stream into valuable materials. Polypropylene (PP) is a significant polymer in the mixed plastics waste stream and closed loop recycling back into food packaging would enable considerable carbon savings to be realised and is also likely to be the way to generate most commercial value from this material. The household waste rigid plastic packaging stream contains significant quantities of PP pots tubs and trays. Within this household rigid PP material about 60% has previously been in contact with food (poultry trays, cream pots, margarine tubs, etc) and 40% has not (cosmetic pots, detergent bottles, paint pots, etc). An obvious high value end market for recycled PP (rPP) from the household waste stream is to use it back in food contact packaging applications. Technology has been proven to produce food grade rPP678. A key requirement of the food grade certification process for rPP is that 99% of the feed material for the process must previously have been in contact with food. It is not commercially viable to separate food contact from non-food contact PP by hand, so one of the remaining barriers to the recycling of rigid PP packaging waste into food grade materials in the UK is that no automated method for sorting post-consumer PP packaging waste has yet been proven to separate food and non-food contact packaging. WRAP is working separately on developing a sorting system for food contact household packaging9. As a result of the difficulty in developing an automated commercial process to separate food packaging from non-food packaging in the household waste stream WRAP has commissioned this project to investigate the opportunity for producing food grade rPP from segregated Commercial and Industrial (C&I) sources where automated sorting is not required. The concept is that food contact packaging used in a C&I environment could be kept separate from non-food packaging and collected as a separate stream for recycling in a dedicated facility. This could enable the production of food grade rPP sooner, before the development of automated sortation of household rigid PP packaging. 1.2 Aims and objectives of the project The specific objectives of this project were:

Investigate the quantities and sources of post C&I food contact PP packaging waste;

Given the quantities of PP packaging waste potentially available, assess what size of plant

would be required to recycle the waste into food grade PP; and

Prepare a business case for a food grade PP plant that processes post C&I food contact

PP packaging waste.

6 ‘Scoping study into food grade polypropylene recycling’, WRAP, July 2010

7 ‘Food grade decontamination trials of household PP waste’, WRAP, July 2012

8 ‘Further analysis of decontaminated recycled polypropylene (rPP)’, WRAP, July 2013

9 ‘Diffraction gratings for food contact packaging identification’, WRAP, July 2013

Business case for recycling food grade C&I PP packaging waste 2

2.0 Project methodology The project started with a review of existing literature containing data on the volume of PP food contact packaging used and disposed of within the UK. This information was used to contribute to making an estimate of the total tonnage that may be available for a PP food contact recycling plant. A list of potential organisations and stakeholders to contact was identified, from existing contacts and desk based research. These contacts included food manufacture and retail businesses, relevant trade associations and waste management companies. E-mail and telephone enquiries were made to named contacts wherever possible. Each organisation was asked whether they generated food contact PP packaging waste, the type of waste, what food it has been in contact with, the level and type of contamination and how the waste is currently managed. Contacts were also asked whether they would be prepared to segregate food contact PP waste if there was a financial incentive to do so and what complications this would create for them, if any. A leading PP recycler which currently collects C&I PP to produce a non-food grade recyclate was visited in order to understand how this type of waste is collected, handled and processed. A financial model for a new build C&I PP recycling facility was created using Microsoft Excel. The model includes a mass balance along with estimates of the operating and capital expenditure for the process. A sensitivity analysis was conducted to determine how stable the investment would be to changes in feed cost, product value revenue and capital and operating expenditure. The potential benefit of developing an existing C&I PP recycling facility to produce food grade rPP was also investigated.

Business case for recycling food grade C&I PP packaging waste 3

3.0 Volumes and availability of food contact PP packaging This section summarises the discussions held with various representatives and stakeholders from the C&I packaging supply chain. 3.1 Trade associations A number of trade associations were approached to discuss whether they could provide relevant data or if they could send out enquiries to members or suggest relevant members to contact. These were the Industry Council for Research on Packaging and the Environment (INCPEN), the Anaerobic and Biogas Association (ADBA), the Chilled Food Association (CFA) and the British Sandwich Association. One trade association sent out a questionnaire to its members but no responses were received. None of the trade associations contacted were able to provide directly relevant information. Some recommended particular members to contact. Some were also asked for lists of food manufacturers who could be contacted to improve the accuracy of the estimates for arisings of food contact PP waste. They were unable to provide these contacts for data protection reasons. If it had been possible to collect data on PP food contact waste arisings from individual food manufacturing or retail sites, and the total numbers and scale of each type of site, then this data could be extrapolated to estimate total tonnage for the sector. 3.2 Hospitality sector 3.2.1 Hotels Several major hotel chains were able to provide information for this project, either from their head office or from individual hotel sites. Most of these contacts were not sure of the polymer type used in their food containers so it was assumed that buckets and tubs would always be PP where these were mentioned. Some contacts were sure of the plastic type however and could confirm that PP food contact packaging does arise at their hotels, mostly used for mayonnaise and other sauces in their restaurants. At present none of the hotels that were contacted segregate food contact PP waste for collection. The hotel chains contacted did segregate mixed dry recyclables for collection. If the PP containers were cleaned prior to disposal then they could be managed via the mixed recyclables route. However if the containers are not washed out then they are likely to end up the in the general waste stream as the waste management companies have strict criteria on contamination in their recycling streams. Both head office staff and those working at hotel sites stated that implementing mixed recycling had been challenging and further segregation to create a purely food contact PP stream would be difficult. Some hotels have very limited space for additional segregation of recyclable materials and the necessary collection containers but others stated that they did have sufficient space to store the PP separately. In some cases the hotels were already washing out the PP packaging so it could be put into the dry mixed recycling stream and therefore it would be relatively straight forward to create a segregated waste stream of PP for collection where space allowed this. All sites engaged with were concerned about the storage of contaminated packaging waste near food service areas. Some mentioned the potential to use existing dish washing equipment in the kitchens to remove contamination from PP pails.

Business case for recycling food grade C&I PP packaging waste 4

In general hotels did not know how many buckets/containers or what tonnage of PP waste they generate. This was also not something that their waste management companies were able to put a figure on due to the wide range of different materials that make up the dry mixed recycling stream. One hotel was able to estimate the number of 5 litre buckets that they used each week but to calculate this accurately it would be best to engage with the procurement departments and gather data regarding how many containers of food products are purchased annually across the estate. It was not possible to engage with any of the hotel procurement teams during the timescales for this project. Despite the organisational, food safety and storage challenges they face in implementing additional segregation there was interest among most of the hotel groups engaged with in further discussions about future segregation of PP for recycling. Their interest depends on the business case making sense. The model for the proposed plant includes a payment for the PP waste at the gate of the recycling facility. So it should be possible for organisations to consider the costs for segregation and collection of PP waste and the likely revenue for the recovered PP containers and compare these with the current cost or revenue for management of mixed recyclables. 3.2.2 Restaurants A number of restaurant chains were contacted for this project and again, it was clear that they were not aware of the polymer types for items in their waste stream. Waste management companies who deal with restaurant waste were able to provide further information about segregation and handling. Not all restaurants generate suitable waste streams for the proposed PP recycling facility, for example one restaurant chain receives their food products in pouches that are not made of PP. Restaurants generally use food contact PP packaging in the form of buckets and tubs for sauces, coleslaw, potato salad and items such as olives and pickles. Each site would not typically use a large number of such containers per week. If a mixed recycling service was offered at their site they would generally wash the PP containers and manage the waste via this route. Otherwise the containers would be disposed of as general waste. None of the sites contacted are segregating PP containers at present. None of the restaurants were able to estimate the quantity of PP waste that they generate, either in terms of number of containers or weight. In some cases they could probably locate data for their total mixed recycling tonnage but it would not be possible to estimate the PP fraction within this total without carrying out waste composition audits at each site. A major waste management company had experienced issues with contaminated plastic containers in the mixed recycling stream, supporting anecdotal evidence from restaurants that it can be challenging to get staff to wash containers for a variety of reasons, such as the use of temporary staff within restaurants, language barriers and a lack of motivation from often low paid staff. Restaurants also experience seasonal peaks connected with holiday periods. These result in some variation in their waste arisings but more importantly lead to difficulties in ensuring a consistent approach to waste management as temporary staff come and go. The evidence from this research shows that restaurant chains may generate large volumes of PP buckets and tubs across their whole estates but the quantities at individual sites are likely to be small and there is currently no segregation taking place. This means that methods for consolidating economically viable tonnages from multiple sites at low cost must be identified. Space constraints at individual restaurants were cited as the main reason large chains are not currently segregating PP waste. This was closely followed by the ability and desire of staff to wash out containers and segregate them from the general waste stream.

Business case for recycling food grade C&I PP packaging waste 5

Where restaurants are within shopping centres the companies are required to adhere to the waste arrangements of the landlord. One large restaurant chain has mixed recycling facilities at the majority of their sites but no separate PP bucket segregation. Their head office waste manager commented that staff are asked to wash out containers but they are unsure if this is happening in practice. The challenge is to create logistical arrangements to collect the PP waste stream in a few central locations for shipment on to a recycling plant. One restaurant chain use distribution centres and so could consider the use of low cost backhaul from individual sites to their distribution hubs to bulk up their PP waste. 3.2.3 Pub chains Pub chains that were contacted used a range of different waste management models. Some used a single major waste contractor nationally, whereas others employed more piecemeal arrangements using a number of contractors across the country. One chain had an arrangement with a single waste management company who took responsibility for their waste across all sites but used a variety of sub-contractors to deliver the service locally. With this model each site had an arrangement to suit its individual circumstances, taking account of space available for containers and availability of local recycling facilities. The main contractor in this example did not segregate PP packaging waste at any of their sites. Many of their sites were provided with mixed recycling bins but there was no further segregation of the recyclables. Another major chain uses a main waste management contractor for their general waste but backhaul recyclables to their distribution centres. This chain does use a range of PP containers including buckets and tubs for mayonnaise, coleslaw, chutney and ice cream. There is an option for each site to wash and return these items via backhaul with their delivery company, although this is not pushed strongly by the company at the moment. The plastics are then bulked up at a central distribution site and sorted and processed into a mixed plastic stream. The recycling manager at the distribution company said they do not currently receive a lot of PP items in this way but there is potential to increase this if it was promoted more by the company to their sites and staff. This distribution company does collect empty PP vegetable oil tubs which are segregated and so would be suitable for the proposed recycling facility. Individually each pub site generates only a small number of PP items per week and so it would be essential to establish a backhaul model to collect material in commercially viable quantities at each hub. 3.3 Retail 3.3.1 Supermarkets Attempts were made to contact supermarkets but no response was received. Most of the supermarket chains use third party logistics firms to manage their waste and already have quite sophisticated methods in place to backhaul shrink wrap films, cardboard, food waste and vegetable oils to their central distribution centres. Most supermarkets are unlikely to generate significant quantities of food contact PP packaging of the type targeted by this project. 3.3.2 Fast-food chains and high street food retailers Fast-food and other high street food retailers do use food contact PP packaging items, mainly buckets for mayonnaise and sauces. Discussions with this sector indicated that there

Business case for recycling food grade C&I PP packaging waste 6

is a move towards other polymer types for lighter weight and lower cost packaging. One organisation has recently purchased new filling equipment, allowing them to distribute their food in pouches rather than tubs. The waste in this sector is often managed by a single waste contractor offering dry mixed recycling as an option across the chain, so this is where washed items of PP packaging would be placed, with unwashed items going to general waste. Other major fast-food chains use a franchise model where control of waste management is left to the individual franchise owners. One retailer knew that they currently use about 2,000 PP buckets per week but this is the organisation that has recently moved to distribution using pouches so this figure will decrease. Another major fast-food chain mainly uses PP tubs for butter. They estimated that an average site could generate six to ten tubs per week (around 1-2kg/week of PP). In addition they use some sauce bottles made of PP and polyethylene (PE) but they were looking to move to PET to improve recyclability. This chain operates mixed dry recycling at all its sites through a contract with a major waste management company. They have considered backhauling themselves to their depots but would only do this for waste streams with larger volumes or tonnage. Another retailer has central locations where it produces the food to distribute to shops and would be prepared to consider backhaul to accumulate larger volumes of PP waste for collection by a recycler. 3.4 Facilities Management One major Facilities Management company was interviewed for this research. They provide catering facilities as part of their service and were aware of the polymer types in the packaging that they use. The majority of their PP is in the form of items they use to serve customers directly such as containers for salads and yoghurt or muesli pots. They also use some PP buckets for mayonnaise and sauces, but it was estimated that each site will only generate a few of these items per week. The challenge for this organisation is that they operate hundreds of food service sites across the UK and at each site the waste system is under the control of the local client. This means they cannot influence the kind of collection for recycling services available and have to use the existing system on each site. They do not currently operate backhaul collections but they have just completed a significant piece of work to investigate this possibility. This organisation was very clear that hygiene is of great importance and so any items stored for recycling would have to be washed to ensure no problems arose from smell or vermin. More work would have to be done to establish the commercial viability of backhauling waste PP packaging from each site to a central location and to address the practical challenges of washing and storing PP packaging for backhaul collection at a very large number of distributed locations. There would be further challenges in ensuring behaviour change among the staff at each location. 3.5 Food distribution companies A major food distribution company was interviewed for this project. It delivers a wide range of food items to shops, restaurants and hotels, all over the UK. It does not generate a significant amount of PP waste as its business model is to store stocks of items and deliver them out to clients. It has 35 depots in the UK but does not currently take any waste back to these from clients’ sites. There is some waste generated at these depots, mostly out of date and damaged items but there is very little PP among this as the PP packaging is robust.

Business case for recycling food grade C&I PP packaging waste 7

Backhauling of waste is something that it has investigated and costed several times over the past few years but each time it has decided not to proceed as a result of the logistical challenges and perceived contamination risks. It is difficult to load waste onto trucks part way through delivery rounds with multiple drops. The underbelly of a lorry was once modified to trial collecting waste separately from the main load but this reduced the overall capacity of the truck, leading to more journeys and higher costs so was not pursued further. Unfortunately the companies’ sales systems are not set up to allow estimates to be made of the number of particular stock items that are sold nationally and therefore to estimate total volumes of particular packaging types that it distributes and could therefore potentially back haul. Investment by the company would be required in order to generate this data. This established company with high route density and extensive experience of multi-drop logistics to food service establishments still offers good potential to develop a backhaul system for food contact PP packaging. Although it has not seen the benefits of this during previous trials it may be that the prices offered by a dedicated PP recycling facility could make the business plan viable. If backhauling could be shown to be commercially viable for this company and its clients it should be able to accumulate a significant quantity of food contact PP waste. 3.6 Food manufacturers 3.6.1 Sandwich manufacturers Sandwich makers range from small sites making sandwiches for a local area to much larger businesses with multiple sites and nationwide coverage. All the sandwich manufacturers contacted generate PP waste, or could describe items that may be assumed to be PP. This waste is mostly in the form of buckets for a range of food substances including mayonnaise, pickles and sauces in flavours such as peri-peri. There was evidence that some buckets are re-used on site to mix additional ingredients. The sandwich manufacturers were fairly confident in stating the number of buckets that they use and their polymer type. Most were currently washing the items out and many were already segregating the waste for recycling. One sandwich manufacturer sent its plastics to a variety of recyclers and the company that took them was chosen by head office based on the most attractive prices or rebates at the time of collection. Some businesses reported seasonal peaks but some saw steady demand all year. This industry sector repeated the message heard elsewhere during this research that there is a move towards flexible pouches for ingredients such as egg mayonnaise and these often use multi-layer film structures. Several of the smaller companies dispose of their PP containers to general waste due to space constraints and the lack of collection and recycling options. The relatively small number of items that they generate each week means that low cost backhaul would be essential to allow economic collection. One company was very interested in a solution and could segregate its PP packaging but it was clear it would require frequent collections to comply with its hygiene standards. This is an attractive sector that generates the type of waste that the proposed food grade PP recycling plant would need. Larger sandwich manufacturers are already segregating and sending PP to recyclers but this is not being used to produce a food grade rPP. Backhaul

Business case for recycling food grade C&I PP packaging waste 8

logistics using the distribution firms that distribute to the smaller sites will need to be developed in order to access material from the rest of the sector. 3.6.2 Other food manufacturers Other types of food manufacturers interviewed for this project did generate PP waste that would be suitable for the proposed PP recycling facility. This mostly comprised the buckets used for ingredients such as sauces, purees and flavourings but also included some manufacturing rejects for items that were packaged in PP containers. One yoghurt manufacturer knew the overall weekly tonnage for its waste and had quantified the proportion that was plastic but it was unsure of the breakdown by polymer type. Yoghurt is usually packaged in either PP or PS pots. Currently this waste is compacted and landfilled because it is contaminated with food but it appears that it could be suitable for the proposed facility if a separate compactor was set up for PP waste. One food manufacturer disposed of PP with a mixed stream of plastics but stated it could segregate it out separately if required. Another washed and segregated the PP then had it collected by a recycler, receiving a rebate for it. Both of these organisations expressed an interest in the proposed recycling facility and were able to either estimate tonnages for PP alone or for mixed plastics. A pizza manufacturer was able to estimate its annual PP waste volume, although this was only a total of 6 tonnes but it was already washing and segregating this material so it would be an attractive waste stream for the proposed facility. Overall this sector generates PP waste that is attractive for the proposed facility. Segregation is already taking place at some sites so with the right support and collection logistics this should be possible at most food factories. 3.7 Dairies Attempts were made to contact several dairy companies but no response was received. 3.8 Waste Management Companies 3.8.1 Anaerobic Digestion facilities Several operators of anaerobic digestion (AD) facilities for food waste were interviewed. All reported that they take in deliveries of mixed waste and receive only a limited number of loads containing a single type of packaging such as PP. When the food waste is depackaged the residue contains a range of rigid plastics including PE, PET and PP plus some paper, card and plastic films. All stated that it would not be commercially viable at present to extract the PP from the mixed residue stream on its own. Likewise it would be very expensive and often hazardous to extract the PP items by hand at the front end of the process before the depackaging unit. One AD operator is undertaking trials to investigate the make-up of the packaging stream in its in feed, indicating that it is considering the commercial viability of separating the materials within its residue stream. If residue separation processes are developed by the AD operators then this could yield a stream of food contact PP in the future. 3.8.2 Waste vegetable oil management companies There are several companies in the UK which specialise in the distribution of vegetable oils and fats and collection of waste oils. Some have national coverage and some are regional businesses and many are linked to biodiesel processors. They tend to handle cooking oils, butter, margarine and mayonnaise in tubs varying in size between 5 litres and 25 litres.

Business case for recycling food grade C&I PP packaging waste 9

Waste oils may be collected in the same tubs that are used for outward distribution or may be collected in tanks mounted on the delivery truck. One company interviewed for this project shred the tubs at its collection depot in order to access the fats and oils within them, then dispose of the unwashed plastic by delivering it to a plastics recycler. The waste varies depending on what comes in each month from customers and a tonnage for PP was not known, only the total mixed plastics weight. However it is likely that the bulk of the material is injection moulded PP packaging. The company use different recyclers depending on who will give the best deal at the time. The material is stored in a skip and is not heavily contaminated but the residue that remains is greasy. This waste would prove attractive to the proposed facility if some additional segregation could be carried out to produce a pure food contact PP stream. 3.8.3 Plastic recycling facilities Several major plastics recyclers were interviewed for this research. All process PP and two specifically target C&I sources. These businesses were able to estimate tonnages for the waste they receive, adding up to a total of over 7,000 tonnes per year. The PP waste they accept is almost entirely injection moulded PP buckets that have contained food ingredients like mayonnaise, flavourings and sauces. These arrive stacked on pallets, stacked in cages and baled. Ideally these recyclers want to receive the material washed or rinsed. These companies have worked hard over a number of years to build up their customer bases and employ business development teams who source the waste for their facilities. This involves identifying the waste, working with the clients to support effective segregation, washing and storage and then arranging collection to the recycling sites. Contamination is always an issue and this has to be managed carefully with the supplier base to ensure the feed material remains suitable for processing. The recyclers all stated that the export market is a constant threat to their feedstock security. Overseas buyers are less concerned about contamination and their pricing is volatile. They move in and out of the market as prices change, which makes it difficult for UK processors to ensure continuity of supply. The output from these reprocessors at present is non-food grade rPP. It is supplied to a range of moulders to make components for the automotive industry and non-food packaging products such as paint tubs. The food grade PP that is currently sourced would be an attractive feedstock for the proposed facility. These businesses demonstrate that it is possible to operate a business model where PP packaging waste is segregated and transported successfully to a single site for recycling. Any new food grade PP recycler entering the market would compete directly with these processors for its feed material. 3.9 Estimate of volumes potentially available From the data gathered in the initial review of existing reports on supply of waste plastics there is an estimated 20,000 tonnes of PP food contact packaging available in the UK from non-household C&I sources10. In this project an attempt was made to segment the waste sources within this total.

10 WRAP IMT003-102, UK market composition data of polypropylene packaging, July 2012

Business case for recycling food grade C&I PP packaging waste 10

Firstly there were individual businesses that knew they generate plastic food contact packaging waste but did not know the polymer type. From the descriptions of the type of items the proportion of the waste that was PP could be deduced. There were also businesses that knew they generated food contact PP waste but were unsure of the tonnages or even number of items that entered their waste stream. Contacts were sometimes able to describe how the waste was stored. For example they knew they stacked buckets on pallets and the number of pallets they generate. Often they were also able to provide information regarding the size of the containers that made up the waste, for example 10 or 25 litre buckets, and so this enabled a weight to be calculated from an average of such items taken from a range of manufacturers. Although some of the sites and organisations could estimate their waste tonnages care must be taken not to double count material. Several stated that they supply waste PP packaging to a recycling company. Not all were prepared to say who this company was and some stated that the outlet varies depending on who will take the waste or who offers the most competitive price at the time. This means where tonnages were provided by the plastics recyclers it is likely that these figures include some of the other data collected from the waste originators. Two of the plastics recyclers already collect and process around 7,200 tonnes of food contact PP packaging. From figures provided by other sites only small tonnages can be accurately said to have been established as food contact PP. This is not an accurate representation of what is available and further work would need to be done to establish this. 3.10 Summary Lack of awareness around polymer types of specific items was a barrier to estimating accurate tonnages during this work. All contacts were asked to try to identify the polymer type on the items by looking for a ‘number 5’ recycling symbol to designate PP. This was not always possible, as some contacts engaged with did not work where the waste was generated and all were extremely busy. Some large organisations use a single waste management contractor for their whole estate, whereas others are bound by the landlord’s own arrangements on certain sites. Some chains use a wide range of waste management companies depending on the individual site location, meaning the recycling arrangements would vary across each pub or restaurant site. It should still be possible for the parent companies to specify their segregation and collection requirements however. If there was a corporate level desire to segregate food contact PP into a single stream and send it to a recycling facility this could be requested as part of the procurement process for waste management contracts. Where individual sites do generate food contact PP packaging waste there were consistent comments about constraints on space and the need to train and encourage staff to wash out the packaging and segregate it correctly. While it would not always be necessary for the packing to be washed before it was sent to the proposed plant this would reduce yield and increase washing costs for the recycler and would increase food safety and vermin risks for the food processing site. For these reasons the maximum time between collections would probably need to be a week or less, especially during periods of warmer weather. At sites where small volumes of PP are generated this would mean moving very small quantities each week, requiring efficient backhaul logistics to regional distribution centres where the material could be consolidated.

Business case for recycling food grade C&I PP packaging waste 11

There are already several successful businesses collecting food contact PP packaging. All are producing a non-food grade rPP output for use within items such as paint pots. Out of 20,000 tonnes of food grade PP packaging that is believed to be placed on the market each year it is known that such specialist recyclers are capturing over 7,000 tonnes between them. It is likely the total figure for C&I rigid PP is higher than previously estimated as other plastics recyclers are also taking in food contact PP packaging in their mixed loads and this is being used to create non-food grade recyclate. There is a market for this recyclate within other sectors, such as the automotive industry, and this is currently where the food contact PP packaging is going. These businesses have dedicated, specialist business development teams who work with waste producers to establish successful segregation and storage of the PP packaging then manage these accounts closely to ensure the waste their plants receive meets their feed specification. Food manufacturers including sandwich makers are an attractive potential source of waste for the proposed PP food grade recycling facility. They are more aware of their PP waste volumes and are generally currently washing and segregating this material either into an exclusive PP stream or a mixed plastics stream. With a small amount of additional effort mixed plastics could be segregated further to create a PP stream that could be collected and sent to the proposed facility. Currently all organisations interviewed for this project who segregated out the PP into a separate stream were receiving a payment for the material. The potential to obtain a payment for this type of waste should encourage other organisations to investigate backhauling as a solution to gathering PP together in more economically viable volumes. To establish the total tonnages of food contact PP packaging available within the market has proved challenging. Often contacts within industry are not certain of the polymer type of their waste and were unable to state with certainty either the tonnage or number of items that they used within the business as this is not something they have ever attempted to measure. Where individual contacts were able to offer a figure for the number of items this was often established from data held within the purchasing records of their procurement teams. It is recommended that anyone investigating the market for a specific PP recycling project should try to obtain more of this data from the procurement records of their logistics partners.

Business case for recycling food grade C&I PP packaging waste 12

4.0 Business case for a polypropylene food grade recycling facility Based on the market research conducted for this project a business case was developed for the construction and operation of a facility taking in segregated food contact C&I PP and producing a food grade, rPP pellet suitable for injection moulding into new food packaging. 4.1 Infeed specification When designing a recycling process it is vital to establish the composition and format of the feed material. From the research conducted in this project the vast majority of food contact C&I PP is in the form of injected moulded buckets. To ensure that the maximum volumes are recycled it is important for the process to be flexible and allow for reasonably high levels of contamination and non-target material in the stream. Although suppliers of the C&I PP should be encouraged to clean the containers to reduce contamination and therefore improve overall yield, this may not always be possible for some of the reasons discussed in Section 3.0. Table 4 shows the feed composition on which the business case has been based. Material meeting this specification would be accepted into the process. If material is accepted that doesn’t meet this specification as a minimum, then the amount paid to the supplier for the PP would have to be reduced accordingly.

Table 4 Infeed specification

Feed composition (% by mass)

Food contact PP 62.5%

Ferrous metal 4.0%

Non-ferrous metal 1.0%

Stainless steel 1.0%

Glass/stones 0.5%

>other polymers (i.e. PET, PS, PVC) 10.0%

Fat and residual contamination 20.0%

Labels/paper 1.0%

The material would have to be accepted onto site either stacked onto buckets, in cages or baled. It is anticipated that the majority of the PP would be stacked on pallets and fed by hand into the process. If baled it would be possible to break the bales manually. Sufficient space and a comprehensive risk assessment would be required for this approach. 4.2 Overview of process and facility Figure 2 outlines the process flow for the proposed C&I PP food grade recycling facility.

Business case for recycling food grade C&I PP packaging waste 13

Figure 2 Process flow of C&I PP recycling facility

Granulator Caustic hot

wash

Rotary vacuum reactor

Gneuss MRS extruder

Sink float Dryer11 16 18 19 21

WasteExtruder

waste

17

Feed

22

Shredder

MagnetEddy Current

Separator (ECS)

8 10

6

Dry cleaner 14

Fat, residual contamination

and fines

13

Ferrous metal Non-ferrous metal

97

5

Water treatment

Product

Sluice3

15

Solid waste

23

Purge water

20

Heavies

12

Manual sort1

4

HeaviesNon-target

2Chemicals and water

Food grade approved extrusion process

Sortation and washing

Business case for recycling food grade C&I PP packaging waste 14

The process outlined above is one method of separating, cleaning and extruding PP from C&I sources. There are other more highly automated options but they would be more expensive to build and operate and are less likely to be commercially viable at the expected throughput. Material is fed into the process manually, allowing it to be pre-sorted at the same time. This is important as at this stage the manual sorters can remove some of the non-target material and also any non-food contact PP present in the stream, which will help ensure the final product will be food grade. Material is size reduced and contamination removed using a magnet, Eddy Current Separator (ECS), a dry cleaner, hot wash and a sink float separator. The PP will float and contaminants such as stones, metals and heavy plastics such as PET will sink. A hot wash is required as the contamination level is likely to be high and will help to remove the 20% fat and residual waste contamination that is expected in the feed specification. Separation and cleaning processes of this type are well established and used in the UK to produce clean non-food grade PP flake, suitable for extrusion into pellet from C&I food contact PP. At the time of writing there is no established process that enables the production of food grade rPP from the washed flake. The Gneuss MRS extruder and vacuum reactor have been shown in work previously conducted on behalf of WRAP11 to produce a food grade compliant rPP pellet. These units are not currently used together in the UK to produce food grade rPP. The flow sheet only outlines the key separation and processing stages. In reality a significant amount of ancillary equipment and utilities would also be required, such as dust extraction, water treatment, steam generation and cooling water. These have been considered when estimating the capital cost of the process. The process has been designed to work continuously and produce a standard food grade rPP output which is then suitable for compounding to meet specific customer requirements. The rPP would likely be an off-white or grey pellet that may require modification (Melt Flow Index (MFI) adjustment, impact modification, pigmentation, etc) before it is used in the injection moulding of food packaging. Producing the rPP as a commodity food grade polymer rather than a specialised product will initially simplify the business model. However the processor may be able to generate significant extra margin at modest extra cost by formulating the finished polymer to meet specific customer requirements. However this will require them to develop or hire specialist polymer processing skills. 4.3 Process mass balance In order to calculate the amount of waste generated and yield of food grade PP a mass balance model was developed for the outlined process flow shown in Figure 2. Separation efficiencies have been estimated for the various items of equipment based on manufacturer’s feedback and Axion’s in-house knowledge. For the mass balance a feed rate of 2 tonnes per hour (tph) was used as a design basis. This value was chosen as it matches the likely feed supply volume and is towards the lower end of the normal capacity range for commercially available wash plants, magnets, ECS and other recycling process equipment.

11 WRAP IMT003-101, Food grade decontamination trials of household PP waste, July 2012

Business case for recycling food grade C&I PP packaging waste 15

Table 5 shows the calculated compositions of the output streams, the mass flow in tonnes per hour (based on 2 tph of feed) and the yield of each output material. The mass flow is also given in tonnes per annum (tpa) based on 8,000 operating hours and 70% uptime efficiency.

Business case for recycling food grade C&I PP packaging waste 16

Table 5 Key mass balance results

Feed Manually

removed

Sluice

heavies

Ferrous

metal

Non-

ferrous metal

Heavies

(dry cleaner)

Fat, residual contamination

and fines (dry

cleaner)

Sink

float waste

Extruder

waste

Water

treatment waste

Food

grade PP pellet

Stream number 1 2 4 7 9 12 13 17 20 23 22

Composition

Food contact PP 62.5% 15.5% 0.0% 32.2% 27.1% 7.5% 4.1% 10.1% 98.2% 4.8% 100.0%

Ferrous metal 4.0% 2.5% 52.1% 67.8% 0.0% 37.2% 0.0% 2.7% 0.1% 0.0% 0.0%

Non-ferrous metal 1.0% 0.6% 0.0% 0.0% 72.9% 11.6% 0.0% 0.8% 0.0% 0.0% 0.0%

Stainless steel 1.0% 6.2% 27.4% 0.0% 0.0% 10.7% 0.0% 0.3% 0.0% 0.0% 0.0%

Glass/stones 0.5% 0.0% 17.2% 0.0% 0.0% 26.7% 0.0% 0.6% 0.0% 0.0% 0.0%

>1SG polymer 10.0% 62.1% 0.0% 0.0% 0.0% 6.3% 0.0% 83.4% 1.6% 0.8% 0.0%

Fat and residual contamination

20.0% 12.4% 0.0% 0.0% 0.0% 0.0% 91.0% 1.9% 0.0% 91.5% 0.0%

Labels/paper 1.0% 0.6% 3.3% 0.0% 0.0% 0.0% 4.9% 0.2% 0.0% 2.8% 0.0%

Total 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Mass flow (tph)

Food contact PP 1.25 0.03 0.00 0.02 0.01 0.00 0.01 0.01 0.06 0.01 1.11

Ferrous metal 0.08 0.00 0.02 0.05 0.00 0.01 0.00 0.00 0.00 0.00 0.00

Non-ferrous metal 0.02 0.00 0.00 0.00 0.02 0.00 0.00 0.00 0.00 0.00 0.00

Stainless steel 0.02 0.01 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Glass/stones 0.01 0.00 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

>1SG polymer 0.20 0.10 0.00 0.00 0.00 0.00 0.00 0.10 0.00 0.00 0.00

Fat and residual

contamination 0.40 0.02 0.00 0.00 0.00 0.00 0.27 0.00 0.00 0.11 0.00

Labels/paper 0.02 0.00 0.00 0.00 0.00 0.00 0.01 0.00 0.00 0.00 0.00

Total mass flow (tph) 2.00 0.16 0.03 0.08 0.02 0.02 0.29 0.12 0.06 0.12 1.11

Total mass flow (tpa) 11,290 909 165 430 125 90 1650 657 334 689 6240

Yield (% of feed) 100.0% 8.1% 1.5% 3.8% 1.1% 0.8% 14.6% 5.8% 3.0% 6.1% 55.3%

Business case for recycling food grade C&I PP packaging waste 17

The mass balance shows that 55.3% of the feed will be recovered as extruded food grade rPP. This appears low, however the infeed specification contains 62.5% PP, which means the yield on PP is 88%. 4.4 Financial viability evaluation Using the mass balance the financial viability of setting up a food grade C&I recycling facility has been evaluated. The evaluation is based on designing and building the whole process from scratch, including the sorting, washing and extrusion stages. Sorting and washing of packaging PP from C&I sources to make non-food grade polymer is already carried out commercially in the UK by a number of companies. The main difference between this process design and the design of existing C&I PP recycling plants is that it includes a more complex and expensive extruder system. This is required in order to deliver the level of extraction and cleaning needed to make food grade polymer. The commercial analysis in this business case is relatively high level and the costings presented should be taken as preliminary estimates, suitable only to assess the likely viability of a food grade PP process when compared to a non-food grade process. 4.4.1 Assumptions and evaluation basis This high level analysis requires various assumptions in order to carry out the economic evaluation. Table 6 shows the main operating assumptions used. These are based on Axion’s experience of running similar facilities.

Table 6 Plant operating basis

Process throughput (tph) 2.0

Operating hours 8,064

Up-time efficiency 70%

Total operating hours (h/year) 5,645

Annual throughput (tpa) 11,290

Due to the nature of the process continual operation is advisable. This avoids unnecessary downtime for start-up and shut down. The annual throughput of 11,290 tonnes is slightly above the 10,000 tpa of feed material that is believed to be available.

Business case for recycling food grade C&I PP packaging waste 18

4.4.2 Capital expenditure Table 7 shows the estimated capital cost requirements for the process at 2 tph of feed.

Table 7 Capital expenditure

Cost (£)

Equipment purchase cost £5,125,000

Equipment installation £1,537,500

Electricals £512,500

Civil work and steelwork £640,000

Office and Lab setup £550,000

Maintenance and spares inventory £153,750

Engineering design £1,022,250

Insurance of works £95,410

Contingency £954,100

Total capital cost £10,590,510

The most significant element of the capital cost is the cost of purchasing the equipment. It should be noted that over half (£2.85 million) of the equipment cost is attributed to the food grade extrusion process (Genuss MRS extruder and vacuum reactor). A further additional cost for producing a food grade product is the food grade testing laboratory. Sophisticated equipment is required in order to test the product and prove it is food grade (such as a mass spectrometer). A capital cost of £400,000 has been included for purchase of laboratory equipment and set-up. 4.4.3 Operating expenditure Table 8 shows the estimated operating expenditure. This does not include the cost of waste disposal or revenue from by-products which is considered separately.

Table 8 Operating expenditure

Cost (£/year)

Electricity £893,120

Chemicals £93,607

Water discharge and usage £62,405

Maintenance spares £100,000

Office and plant running costs £100,000

Fork lift truck hire £15,600

Labour £1,519,000

Laboratory consumables (£10 per tonne of product) £62,405

Total operating cost £2,846,136

By far the most significant cost is for labour. Table 9 shows the breakdown of the labour costs.

Business case for recycling food grade C&I PP packaging waste 19

Table 9 Estimated labour costs

Role

Number required per shift

Number of shifts

Additional staff on

days Total

Cost per person12

Total cost

Plant Manager 1 1 0 1 £70,000 £70,000

Business Development 4 1 0 4 £50,000 £200,000

Admin/office manager 1 1 0 1 £40,000 £40,000

Office support staff 3 1 0 3 £30,000 £90,000

Shift leader 1 4 0 4 £40,000 £160,000

Maintenance Engineer/electrician

1 4 2 6 £40,000 £240,000

Yard 1 4 1 5 £25,000 £125,000

Operator 3 4 0 12 £25,000 £300,000

Laboratory staff 1 4 1 5 £30,000 £150,000

Manual sorters 2 4 0 8 £18,000 £144,000

Total cost (£/year) £1,519,000

The labour costs for this process that may not be incurred for a non-food grade production process are the business development and laboratory staff. Business development is very important for this process for two reasons:

Staff will be required to identify the sources of the C&I food grade PP and engage with the sites to ensure the correct material is collected in the correct format with minimal contamination; and

The food grade rPP will need end markets which are not yet established. Significant work would be required in order to sell the end product as there is no equivalent material available at this time.

A 24 hour laboratory is required to ensure the products are tested for food grade compliance. This is a more involved process than physical property testing and would require staff with more training and skills. Table 10 shows the cash flow associated with selling the by-products and the cost of disposing of the non-target materials.

Table 10 Revenue from sale of by-products and waste disposal

By-product/waste Tonnage (t/year)

Value (£/t)

Cash flow (£/year)

Ferrous 430 100 £43,002

Non-ferrous 125 600 £75,028

Manually removed 909 -£40 -£36,353

Solid waste (inert) 1246 -£40 -£49,824

Solid waste (including organics) 2340 -£80 -£187,174

Net revenue from waste/by-products -£155,320

12 Costs are cost to the company (inclusive of tax and national insurance) and not just salaries

Business case for recycling food grade C&I PP packaging waste 20

The cost of disposing of the waste is not as significant as the labour or energy costs, and as the wash water is treated on-site this helps to reduce this cost. 4.4.4 Infeed cost and product sales value The cost of infeed material and the sales price of the food grade rPP must be considered. It is highly likely that the feed material would have to be purchased from the producers of the waste. The logistics of collecting material from various sites across the UK and transporting them to a single site has not been evaluated in detail for this project as it will rely on the development of relatively complex backhaul logistics systems. The price of the feed material at the recycling factory gate will have to reflect these likely collection costs. Initially a feed cost of £200 per tonne has been used. This is based on the assumption that the material will match the infeed specification. If material does not meet the specification (for example has too much metal or contamination) then the full £200 per tonne would not be paid. As most of the PP food contact packaging that will form the feed material for this project is likely to be disposed as general waste at present at a cost between £100-£140/tonne to the site operator there is a difference of around £320/tonne between the current disposal cost and the proposed payment at the recycling factory gate. For a typical C&I PP container weight of about 200g this equates to a value of around 6 pence per container for a backhaul logistics operation to move the material from the site where it arises to the recycling factory. The original value of the virgin polymer material within the container will be about 20 pence. The value of the food grade rPP is difficult to estimate as it is not currently produced and there are as yet no proven end markets for the material in food packaging applications. Using rPP in food packaging to substitute virgin polymer will have significant environmental and marketing benefits and the industry as a whole is supportive of the concept. Assuming markets can be found for the food grade rPP, it would be competing with virgin PP polymer. Virgin food grade PP is currently sold at prices in the range £1,100 to £1,200 per tonne13. Large users of the polymer may negotiate a discount on this price. There is no significant difference in cost between food grade and non-food grade virgin polymer. Costs vary more depending on the physical properties of the polymer. A high quality non-food grade rPP that is comparable to virgin, for use in items such as paint pots and storage containers can be sold for 70 to 80% of virgin prices at £800 to £900 per tonne14. The non-food rPP price is lower than the virgin price because buyers perceive less security when using recycled material and insist on a discount. Instead of viewing the food grade rPP as a ‘cheaper’ alternative to virgin, it must be viewed as a valuable product in its own right. This means placing emphasis on the green credentials of the rPP, which, for example, is likely to provide a carbon saving of 60 to 80% over virgin15.

13 Price as of March 2014

14 Price as of March 2014

15 Based on previous carbon foot printing exercises carried out by Axion Consulting

Business case for recycling food grade C&I PP packaging waste 21

The marketing advantage of using the rPP is also significant. A sensible business plan would be to partner with a large packaging converter. Having an assured outlet for the rPP based on the carbon saving and marketing message could allow it to reach prices very close to virgin PP. This has been observed in recent years in the markets for food grade recycled high density polyethylene (HDPE) for milk bottles and food grade recycled PET for both bottles and trays. Recycled food grades for both these polymers currently sell at close to virgin price, sometimes higher. For this reason the value of the of the rPP should be in the region of £1,000 to £1,100 per tonne, which does represent some saving on virgin material but covers the additional cost of processing to a food grade product. This assumes that the supply and the quality of the rPP are consistent and sufficient. For the base case assessment a price of £1,100 per tonne is assumed. The sensitivity analysis in Section 4.4.6 investigates the impact of varying sales prices. Table 11 shows the estimated cost of the feed and estimated sales value for the food grade rPP.

Table 11 Cost of feed and sales value of rPP

Tonnage (t/year)

Value (£/t)

Cash flow (£/year)

Feed 11,300 -£200 -£2,257,920

Food grade rPP pellet 6240 £1100 £6,864,498

4.4.5 Financial evaluation In order to evaluate the commercial viability of the proposed business case two parameters have been calculated:

Net Present Value (NPV): using a 20 year plant lifetime and an interest rate of 7.5%; and

Payback period. Figure 3 shows the base case discounted cash flow for the 20 year lifetime of the plant.

Business case for recycling food grade C&I PP packaging waste 22

Figure 3 Discounted cash flow (7.5% interest rate)

The NPV is calculated to be £15 million over 20 years and the plant has a payback period of 6.6 years. However if the lifetime is lowered to 15 years the NPV is -£9.5 million. This negative NPV shows that the investment would not be profitable if the lifetime of the plant is reduced. This analysis demonstrates that it should be possible to make a business case for production of food grade rPP from C&I sources. This is a relatively simple and preliminary economic analysis and a full engineering and market study would be required to confirm the capital and operating costs and the feed and product values. 4.4.6 Sensitivity analyses Several sensitivity analyses were conducted in order to assess the robustness of the business plan. The effect of varying the key cost parameters on NPV has been considered for simplicity. If the NPV is positive the investment is likely to be economically viable. Table 12 shows how NPV varies with different feed costs and rPP sales values. The box highlighted black shows the base case.

-£12M

-£9M

-£6M

-£3M

£0M

£3M

£6M

0 5 10 15 20

Dis

cou

nte

d c

ash

flo

w

Year