written by vinny clevenger, senior consultant and jay ... · pdf filevinny clevenger and jay...

TRANSCRIPT

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

In This Issue Vol. 16, No. 4

Point ‒ Counterpoint

From the Editor Keith Reagan

Interest rates have to go up!!!

Do they? If so, when will they rise?

What happens if they do not?

In this month’s Bulletin, co-authors Vinny Clevenger and Jay Kollias share their perspectives on these questions and more.

As always, feedback, questions and suggestions on future articles are welcomed.

- Keith Reagan

Questions or Feedback?Contact [email protected]

Point ‒ CounterpointWritten by Vinny Clevenger, Senior Consultant and Jay Kollias, Director of

Financial Analytics

Interest Rates are going to rise! We must prepare for a rising rate cycle! It has been 10 years since short-term rates increased (+400 bps 2004-2006). We then wit-nessed the yield curve flatten, followed by a sharp decline in rates to historically low levels which have held constant for 5 years (and counting).

Over the past five years, many institutions have been extending their asset base just to maintain earnings. One could argue that this asset extension has been funded by an undeniable “surge” of non-maturity deposit inflows onto bank balance sheets.

Long-term fixed rate assets + rate sensitive funding = Exposure to rising rates! And rates have to rise.

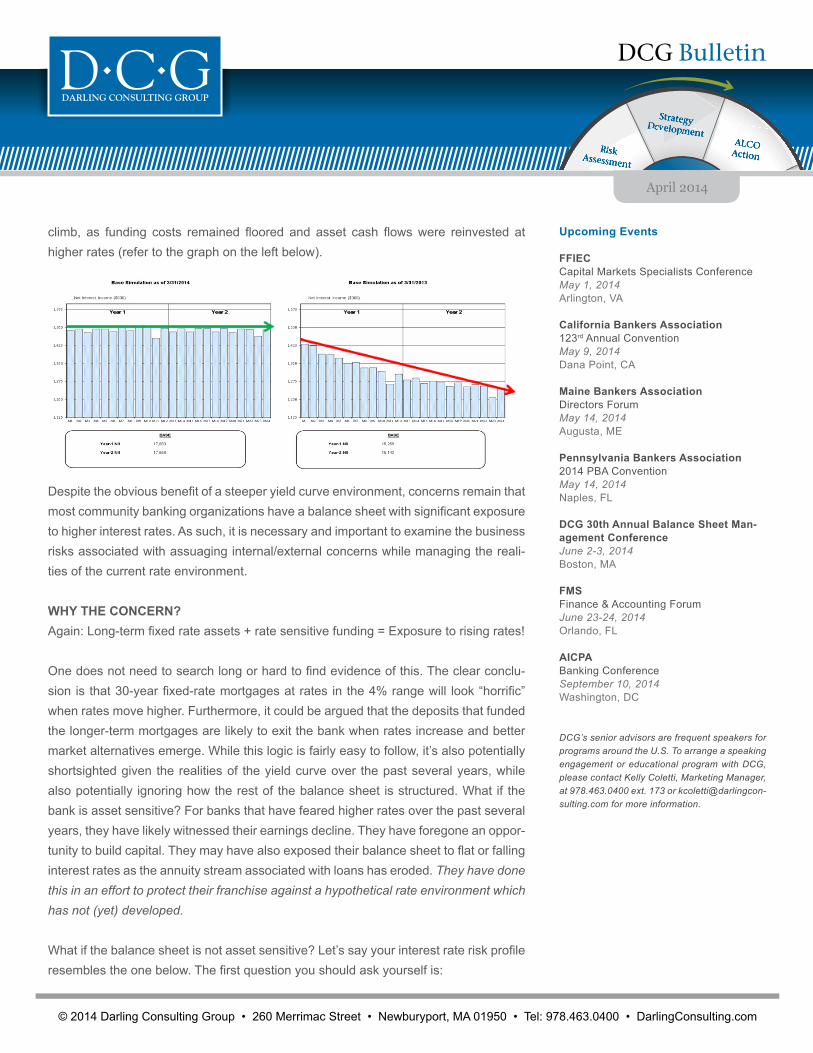

What if interest rates do not rise? It is no secret that regulatory agencies have placed increased emphasis on preparedness for higher interest rates. During the 4th quarter of 2013, both the FDIC and OCC released literature warning of the industry-wide mounting sensitivity to elevated interest rates. Although this concern is certainly warranted…one could easily make the argument that it’s also singularly focused. In fact, if we rewind the clock 12 short months, most would conclude that falling interest rates actually present a greater challenge to levels of net interest income. On April 1, 2013, the 10-year CMT was trading at a paltry yield of 1.61%, and bank margins were under considerable duress (refer to graph on the right below).

The bond market then experienced a considerable sell-off, and industry margins slow-ly improved with the steeper yield curve. Many banks started to see earnings levels

2014? 2015? 2016?

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

Upcoming Events

FFIECCapital Markets Specialists ConferenceMay 1, 2014Arlington, VA

California Bankers Association123rd Annual ConventionMay 9, 2014Dana Point, CA

Maine Bankers AssociationDirectors ForumMay 14, 2014Augusta, ME

Pennsylvania Bankers Association2014 PBA ConventionMay 14, 2014Naples, FL

DCG 30th Annual Balance Sheet Man-agement ConferenceJune 2-3, 2014Boston, MA

FMSFinance & Accounting ForumJune 23-24, 2014Orlando, FL

AICPABanking ConferenceSeptember 10, 2014Washington, DC

DCG’s senior advisors are frequent speakers for programs around the U.S. To arrange a speaking engagement or educational program with DCG, please contact Kelly Coletti, Marketing Manager, at 978.463.0400 ext. 173 or [email protected] for more information.

climb, as funding costs remained floored and asset cash flows were reinvested at higher rates (refer to the graph on the left below).

Despite the obvious benefit of a steeper yield curve environment, concerns remain that most community banking organizations have a balance sheet with significant exposure to higher interest rates. As such, it is necessary and important to examine the business risks associated with assuaging internal/external concerns while managing the reali-ties of the current rate environment.

WHY THE CONCERN?Again: Long-term fixed rate assets + rate sensitive funding = Exposure to rising rates!

One does not need to search long or hard to find evidence of this. The clear conclu-sion is that 30-year fixed-rate mortgages at rates in the 4% range will look “horrific” when rates move higher. Furthermore, it could be argued that the deposits that funded the longer-term mortgages are likely to exit the bank when rates increase and better market alternatives emerge. While this logic is fairly easy to follow, it’s also potentially shortsighted given the realities of the yield curve over the past several years, while also potentially ignoring how the rest of the balance sheet is structured. What if the bank is asset sensitive? For banks that have feared higher rates over the past several years, they have likely witnessed their earnings decline. They have foregone an oppor-tunity to build capital. They may have also exposed their balance sheet to flat or falling interest rates as the annuity stream associated with loans has eroded. They have done this in an effort to protect their franchise against a hypothetical rate environment which has not (yet) developed.

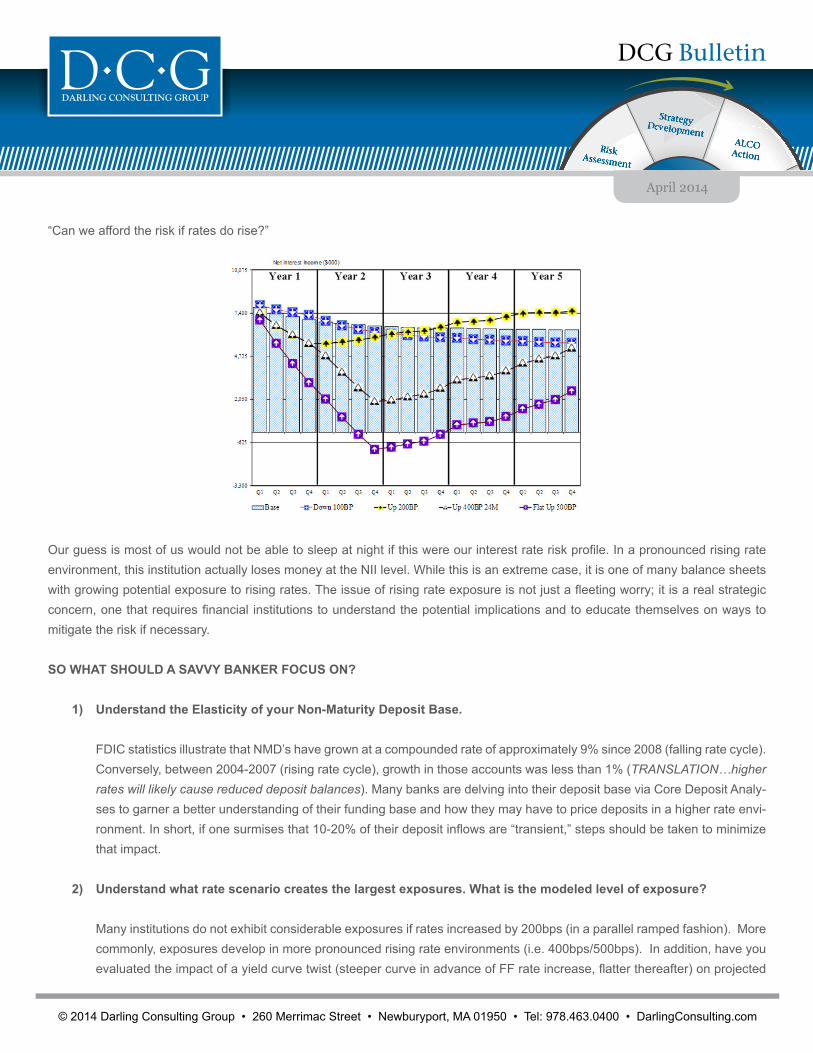

What if the balance sheet is not asset sensitive? Let’s say your interest rate risk profile resembles the one below. The first question you should ask yourself is:

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

“Can we afford the risk if rates do rise?”

Our guess is most of us would not be able to sleep at night if this were our interest rate risk profile. In a pronounced rising rate environment, this institution actually loses money at the NII level. While this is an extreme case, it is one of many balance sheets with growing potential exposure to rising rates. The issue of rising rate exposure is not just a fleeting worry; it is a real strategic concern, one that requires financial institutions to understand the potential implications and to educate themselves on ways to mitigate the risk if necessary.

SO WHAT SHOULD A SAVVY BANKER FOCUS ON?

1) Understand the Elasticity of your Non-Maturity Deposit Base.

FDIC statistics illustrate that NMD’s have grown at a compounded rate of approximately 9% since 2008 (falling rate cycle). Conversely, between 2004-2007 (rising rate cycle), growth in those accounts was less than 1% (TRANSLATION…higher rates will likely cause reduced deposit balances). Many banks are delving into their deposit base via Core Deposit Analy-ses to garner a better understanding of their funding base and how they may have to price deposits in a higher rate envi-ronment. In short, if one surmises that 10-20% of their deposit inflows are “transient,” steps should be taken to minimize that impact.

2) Understand what rate scenario creates the largest exposures. What is the modeled level of exposure?

Many institutions do not exhibit considerable exposures if rates increased by 200bps (in a parallel ramped fashion). More commonly, exposures develop in more pronounced rising rate environments (i.e. 400bps/500bps). In addition, have you evaluated the impact of a yield curve twist (steeper curve in advance of FF rate increase, flatter thereafter) on projected

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

levels of Net Interest Income?

The utility of examining a variety of interest rate scenarios is not only to triangulate the inherent risks which reside in the balance sheet, but also the level of potential exposures can be quantified and then related to the bottom line. NII projec-tions will vary significantly dependent upon the timing, shape and level to which interest rates increase. Management needs to understand the potential impact on earnings in a multitude of rate scenarios and position the balance sheet ac-cordingly. In other words, if your worst case scenario is substantially higher interest rates (but the probability of that event in the near-term is low), then should management pay substantial premiums to insulate future earnings in this scenario? The answer for some is yes while for others it is no.

3) Examine the risk/return tradeoffs associated with positioning the balance sheet for rising rates.

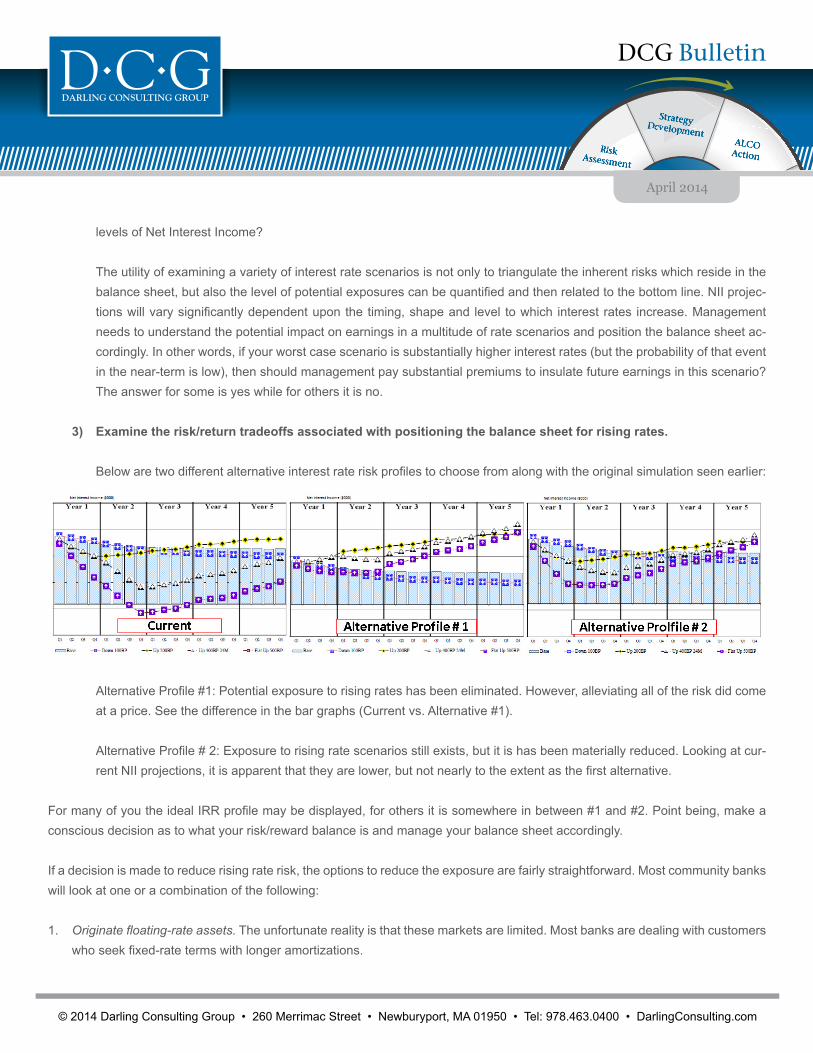

Below are two different alternative interest rate risk profiles to choose from along with the original simulation seen earlier:

Alternative Profile #1: Potential exposure to rising rates has been eliminated. However, alleviating all of the risk did come at a price. See the difference in the bar graphs (Current vs. Alternative #1).

Alternative Profile # 2: Exposure to rising rate scenarios still exists, but it is has been materially reduced. Looking at cur-rent NII projections, it is apparent that they are lower, but not nearly to the extent as the first alternative.

For many of you the ideal IRR profile may be displayed, for others it is somewhere in between #1 and #2. Point being, make a conscious decision as to what your risk/reward balance is and manage your balance sheet accordingly.

If a decision is made to reduce rising rate risk, the options to reduce the exposure are fairly straightforward. Most community banks will look at one or a combination of the following:

1. Originate floating-rate assets. The unfortunate reality is that these markets are limited. Most banks are dealing with customers who seek fixed-rate terms with longer amortizations.

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

2. Sell longer duration assets. The easiest solution for banks with concern for the obvious fact that longer duration assets will cause a perpetual “drag” on earnings is to simply divest those assets. However, with loan demand relatively muted in most markets and investment alternatives remaining unattractive, most banks will retain those assets and assume the interest rate risk.

3. Extend liabilities. Many banks are seriously contemplating liability extension. A very common question today is, “When should we extend liabilities?” The correct answer is that there is no correct answer. No one will successfully time the market and, if they do, it’s a stroke of luck. However, if the bank’s analysis depicts a rate scenario under which management cannot sleep at night, perhaps it’s time to take current earnings off the table. It should be noted that the cost of extension vs. borrowing short is an expensive proposition in a steep yield curve environment. Rates would have to significantly increase for the extension “bet” to pay off. Common on-balance sheet extension options include:

FHLB Advances Community banks are probably most familiar and comfortable with this option. Accessing longer-term funding is as simple as picking up the phone as long as you have available collateral and are a sound financial institution.

Brokered CDsBrokered CDs have long had a negative stigma due to the perceived role they played in the recent and past banking crises. We all know that the use of brokered CDs does not cause loans to go bad, loose underwriting standards does. In reality, brokered CDs have historically been a reliable and relatively inexpensive long-term funding option for institutions that are above “well-capitalized” levels. Recently, call options can be included for little to no premium making the CDs an even more attractive option when contemplating extension.

4. Off-Balance sheet instrument (swaps/caps). Derivatives serve as an effective tool to manage the interest rate risk position of a balance sheet. Unfortunately, they are also treated with disdain by many management teams given the negative connotation associated with them and the fact that they require a complete understanding by all parties (management, board, accountants, etc.) of the inherent risks (counterparty, accounting, etc.).

Not the “D” word! While derivatives require more education, more documentation and more accounting, they are an ef-fective way to hedge against rising rates. If you are truly serious about finding the best and most cost-effective option, you cannot dismiss anything ‒ even if it is outside of your comfort zone. There are myriad options to choose from in the derivatives market. Here are a few of the most common:

Swap: A contract between two parties to exchange interest rate payments on a “notional amount” for a specific period of time in order to replace an undesirable cash flow (e.g. floating rate funding or fixed rate assets).

Forward Swap: An agreement to exchange interest payments, beginning at a future specified date in order to replace an undesirable cash flow.

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

Cap: An option which provides insurance against rising rates where a buyer pays a premium up front and is not ob-ligated to make any additional payments. The buyer receives payments whenever the market rate (usually LIBOR) exceeds a strike price.

Some of the most common on-balance sheet instruments that can be hedged using derivatives are:

Current or future short-term wholesale funding (FHLB, Repos, etc.). Fixed-rate loans (using swaps or back-to-back swaps). Market indexed non-maturity deposits.

Conclusion

The current risk to higher rates (real or perceived) creates a dilemma between managing potential future risks and current earn-ings. Management teams should ask themselves the consequences of their strategic decisions in all rate scenarios ‒ not just rising-rate scenarios. The common refrain that rates “have to go up” has created an environment in which some banks have by-passed opportunities. However, the only guarantee with interest rates is that there are no guarantees. Manage to what is known today, understand the impact on tomorrow if a scenario comes to fruition and have plans in place for that environment.

DCG Bulletin

RiskAssessment

Strategy DevelopmentALCO

Action

© 2014 Darling Consulting Group • 260 Merrimac Street • Newburyport, MA 01950 • Tel: 978.463.0400 • DarlingConsulting.com

April 2014

The 30th Annual Balance Sheet Management Conference

Marriott Long Wharf - Boston, MassachusettsJune 2-3, 2014

Online registration is open. Simply visit DarlingConsulting.com to learn more about how you can benefit from this information-packed conference. Earn up to 13 CPE credits!

As always, this year’s DCG Balance Sheet Management Conference will be filled with timely sessions that are sure to provide a number of strategies for improving the financial performance of your institution, as well as better preparing for your next exam. Monday will feature a general session with Camden R. Fine, president and CEO of the Independent Community Bankers of America® (ICBA). Leading off Tuesday’s program will be a general session conducted by Mark Vit-ner, who is a managing director and senior economist at Wells Fargo, responsible for tracking U.S. and regional economic trends.

We will also be offering our popular core sessions:

Risk/Return Trade-Offs in Balance Sheet Management Measuring and Managing Liquidity Measuring and Managing Interest Rate Risk Developing & Documenting Balance Sheet Management

Strategies

Click here to register. Don’t wait – the event is nearly sold out!

The DCG Bulletin is a regular email publication produced by Darling Consulting Group (DCG). The Bulletin provides essential information, commentary and suggestions to help bankers address strategic and financial management issues and concerns. DCG specializes in education, strategic planning and management tools for financial institutions, helping managers of banks, thrifts and credit unions enhance profitability in today’s dynamic banking environ-ment. Readers may obtain permission for reprinting the contents of the Bulletin for distribution to others by contacting Stephanie Pitman, Marketing & Sales Assistant, at 978.463.0400 ext. 174 or [email protected]. Attribution must be given to DCG for all reprints.