www.theiia.org... what is changing, why it’s changing, and the expected outcomes from the ppf to...

TRANSCRIPT

www.theiia.org

. . . what is changing, why it’s changing,

and the expected outcomes

From the From the PPF PPF

to theto theIIPPFPPF

www.theiia.org

What is a framework?What is a framework?

A framework is a basic skeletal structure for classifying and organizing concepts or various elements.

www.theiia.org

What is the PPF?What is the PPF?

ProfessionalPractices

Framework

www.theiia.org

What is the What is the IIPPF?PPF?

International Professional Practices

Framework

www.theiia.org

PPF and PPF and IIPPFPPF

Both provide a structure for the internal audit profession’s technical guidance.

www.theiia.org

Why the change?Why the change?

Committed to delivering the most qualitative technical guidance for internal audit practitioners all around the world, The IIA wants to be internationally recognized as a trustworthy guidance-setting body.

www.theiia.org

The change ensures:The change ensures:• More Clarity — what is authoritative,

mandatory, and what is neither authoritative nor mandatory.

• More Transparency — throughout the process life cycle, development to maintenance.

• More Timeliness — in issuing guidance.

www.theiia.org

How is the IPPF How is the IPPF different?different?

www.theiia.org

Key DifferencesKey Differences

• Changes of scope and structure

• Development and maintenance process enhancements

www.theiia.org

Scope and StructureScope and Structure

PPF• This framework

organizes all guidance developed and/or endorsed by The IIA.

IPPF• This framework

organizes The IIA’s authoritative guidance.

www.theiia.org

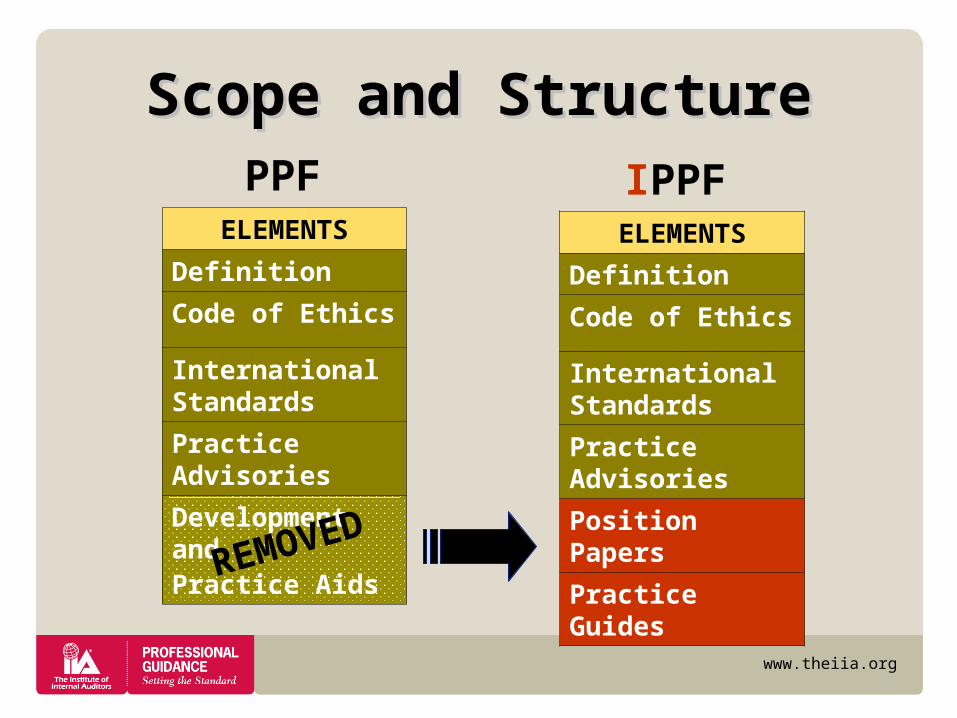

ELEMENTS

Definition

Code of Ethics

International Standards

Practice Advisories

Development and Practice Aids

ELEMENTS

Definition

Code of Ethics

International Standards

Practice Advisories

Position Papers

Practice Guides

PPF IPPF

REMOVED

Scope and StructureScope and Structure

www.theiia.org

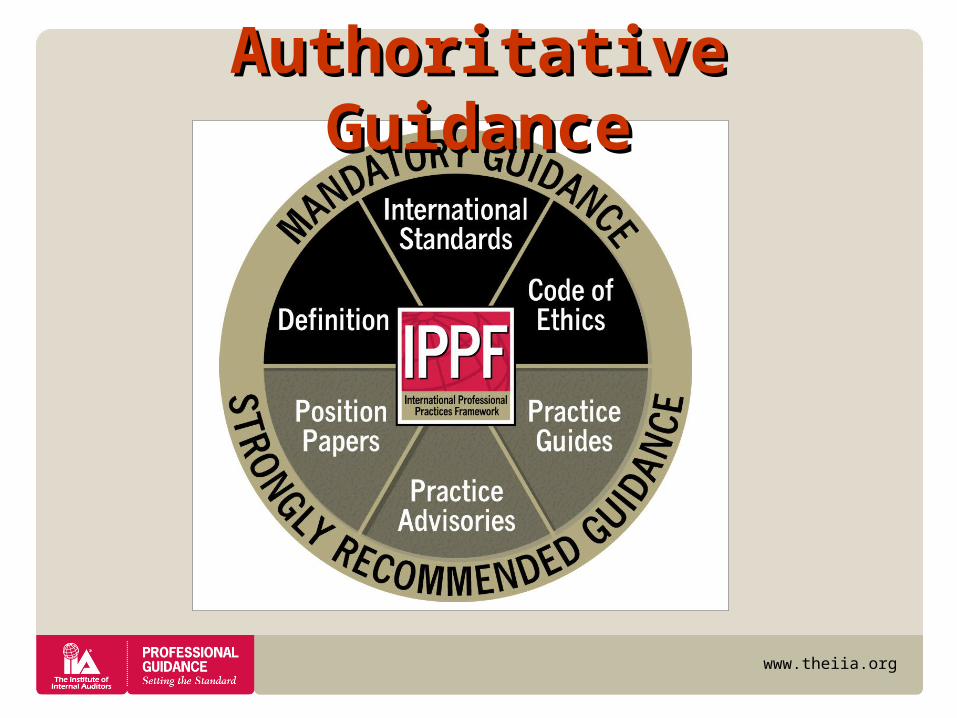

Authoritative Authoritative GuidanceGuidance

www.theiia.org

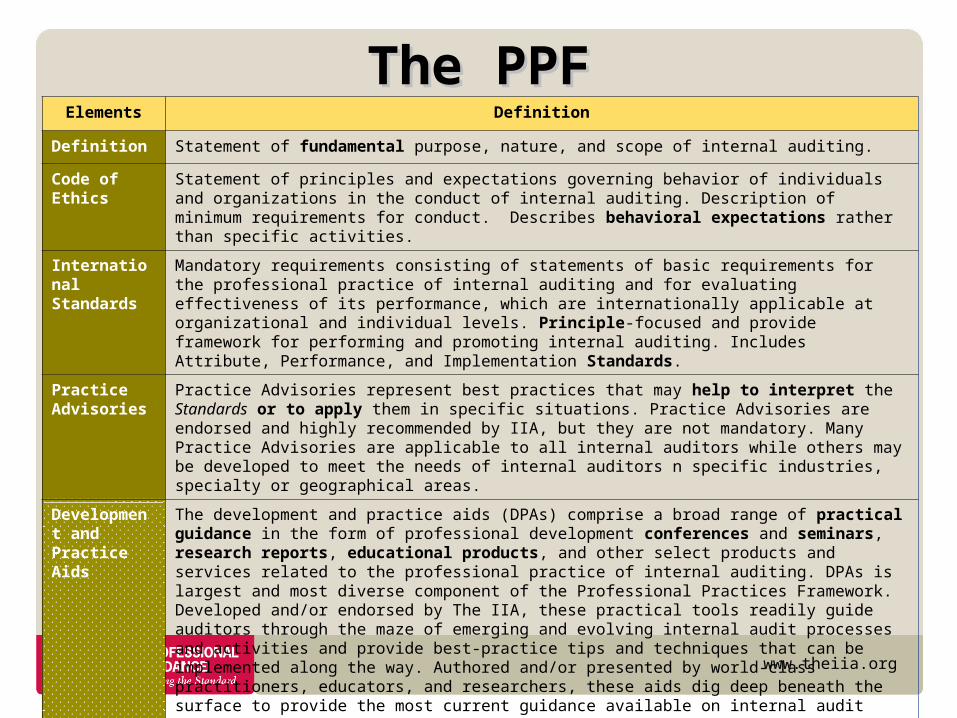

The PPFThe PPFElements Definition

Definition Statement of fundamental purpose, nature, and scope of internal auditing.

Code of Ethics

Statement of principles and expectations governing behavior of individuals and organizations in the conduct of internal auditing. Description of minimum requirements for conduct. Describes behavioral expectations rather than specific activities.

International Standards

Mandatory requirements consisting of statements of basic requirements for the professional practice of internal auditing and for evaluating effectiveness of its performance, which are internationally applicable at organizational and individual levels. Principle-focused and provide framework for performing and promoting internal auditing. Includes Attribute, Performance, and Implementation Standards.

Practice Advisories

Practice Advisories represent best practices that may help to interpret the Standards or to apply them in specific situations. Practice Advisories are endorsed and highly recommended by IIA, but they are not mandatory. Many Practice Advisories are applicable to all internal auditors while others may be developed to meet the needs of internal auditors n specific industries, specialty or geographical areas.

Development and Practice Aids

The development and practice aids (DPAs) comprise a broad range of practical guidance in the form of professional development conferences and seminars, research reports, educational products, and other select products and services related to the professional practice of internal auditing. DPAs is largest and most diverse component of the Professional Practices Framework. Developed and/or endorsed by The IIA, these practical tools readily guide auditors through the maze of emerging and evolving internal audit processes and activities and provide best-practice tips and techniques that can be implemented along the way. Authored and/or presented by world-class practitioners, educators, and researchers, these aids dig deep beneath the surface to provide the most current guidance available on internal audit activities, issues, and approaches.

www.theiia.org

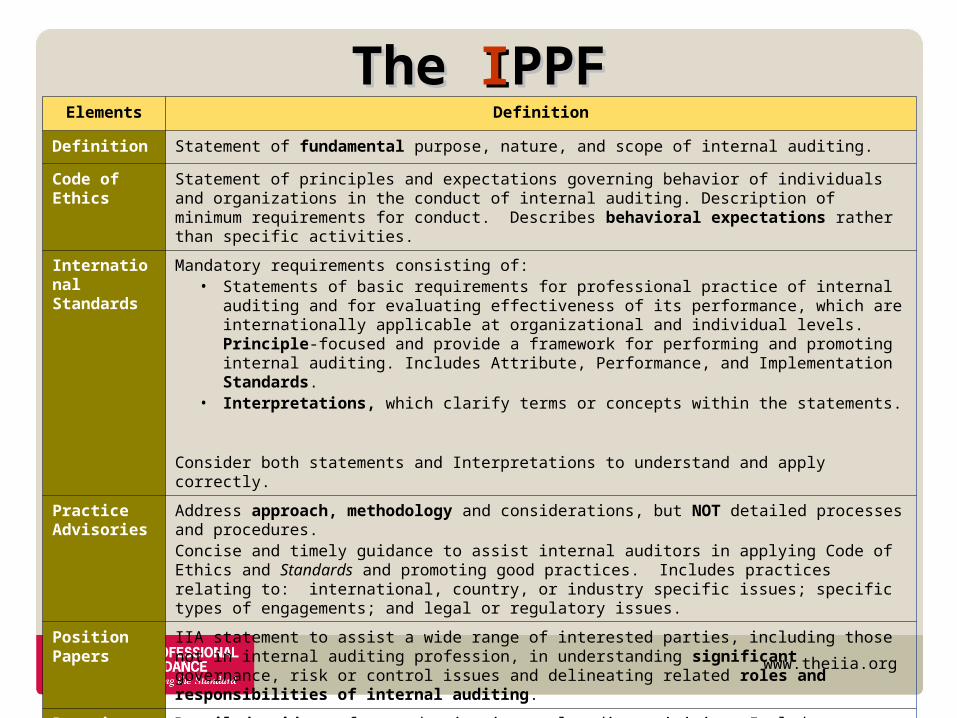

Elements Definition

Definition Statement of fundamental purpose, nature, and scope of internal auditing.

Code of Ethics

Statement of principles and expectations governing behavior of individuals and organizations in the conduct of internal auditing. Description of minimum requirements for conduct. Describes behavioral expectations rather than specific activities.

International Standards

Mandatory requirements consisting of:• Statements of basic requirements for professional practice of internal auditing and for evaluating

effectiveness of its performance, which are internationally applicable at organizational and individual levels. Principle-focused and provide a framework for performing and promoting internal auditing. Includes Attribute, Performance, and Implementation Standards.

• Interpretations, which clarify terms or concepts within the statements.

Consider both statements and Interpretations to understand and apply correctly.

Practice Advisories

Address approach, methodology and considerations, but NOT detailed processes and procedures.Concise and timely guidance to assist internal auditors in applying Code of Ethics and Standards and promoting good practices. Includes practices relating to: international, country, or industry specific issues; specific types of engagements; and legal or regulatory issues.

Position Papers

IIA statement to assist a wide range of interested parties, including those not in internal auditing profession, in understanding significant governance, risk or control issues and delineating related roles and responsibilities of internal auditing.

Practice Guides

Detailed guidance for conducting internal audit activities. Includes detailed processes and procedures, such as tools and techniques, programs, and step-by-step approaches, including examples of deliverables.

The The IIPPFPPF

www.theiia.org

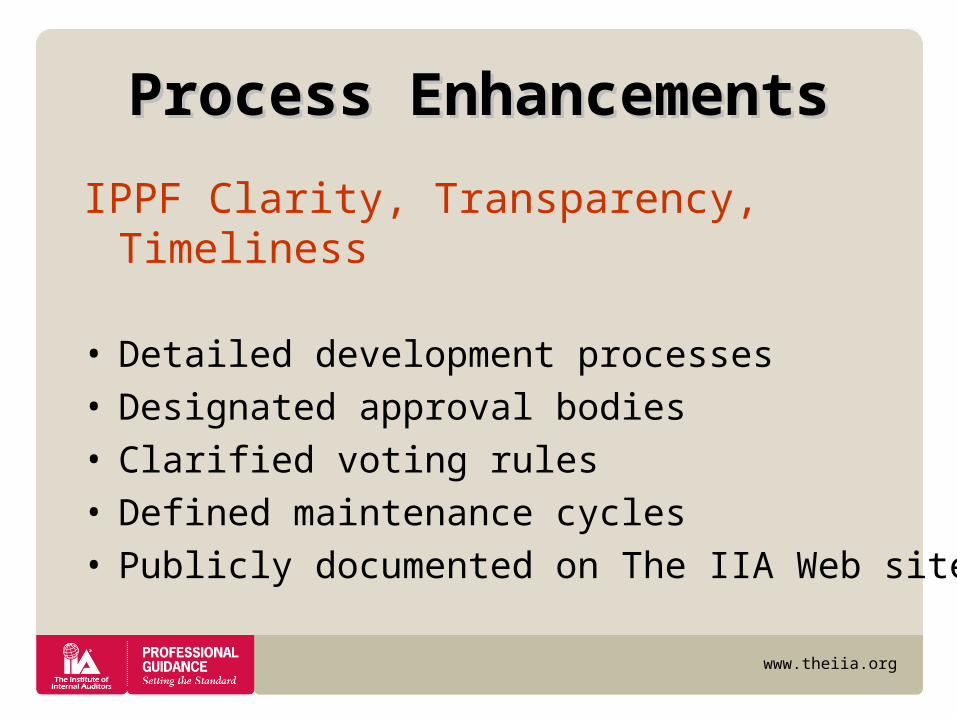

Process EnhancementsProcess Enhancements

IPPF Clarity, Transparency, Timeliness

• Detailed development processes • Designated approval bodies• Clarified voting rules• Defined maintenance cycles• Publicly documented on The IIA Web site

www.theiia.org

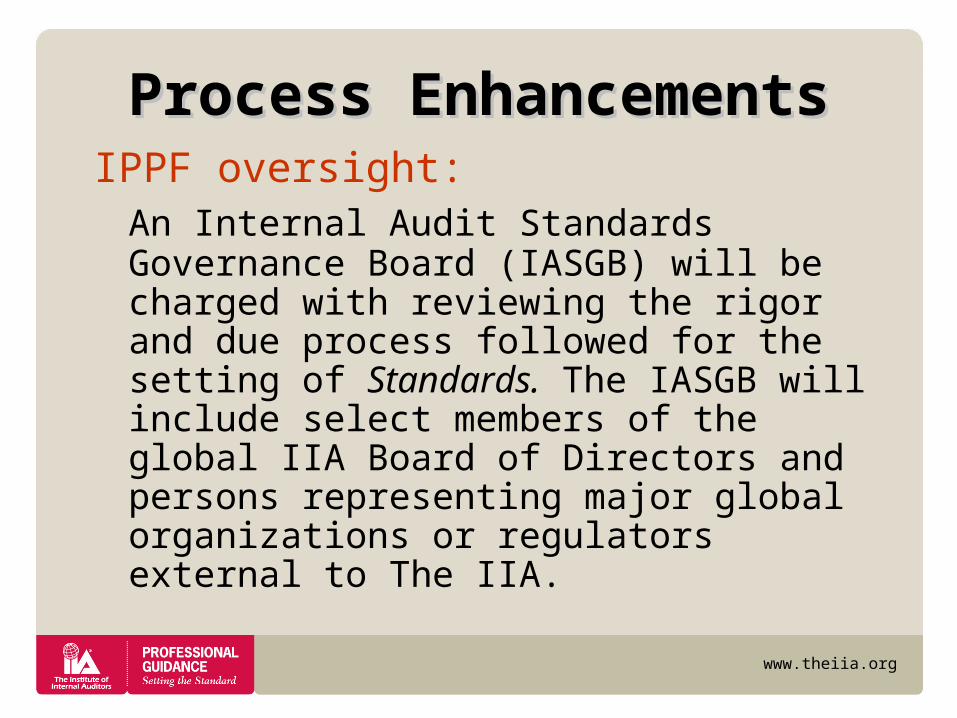

Process EnhancementsProcess EnhancementsIPPF oversight:

An Internal Audit Standards Governance Board (IASGB) will be charged with reviewing the rigor and due process followed for the setting of Standards. The IASGB will include select members of the global IIA Board of Directors and persons representing major global organizations or regulators external to The IIA.

www.theiia.org

Are there any changes Are there any changes to the content?to the content?

www.theiia.org

Content EnhancementsContent Enhancements• Six new Standards.

• Interpretations of existing Standards will enhance the understanding of current requirements.

• A cleansing of existing Practice Advisories will ensure consistency in writing style, tone, and presentation.

www.theiia.org

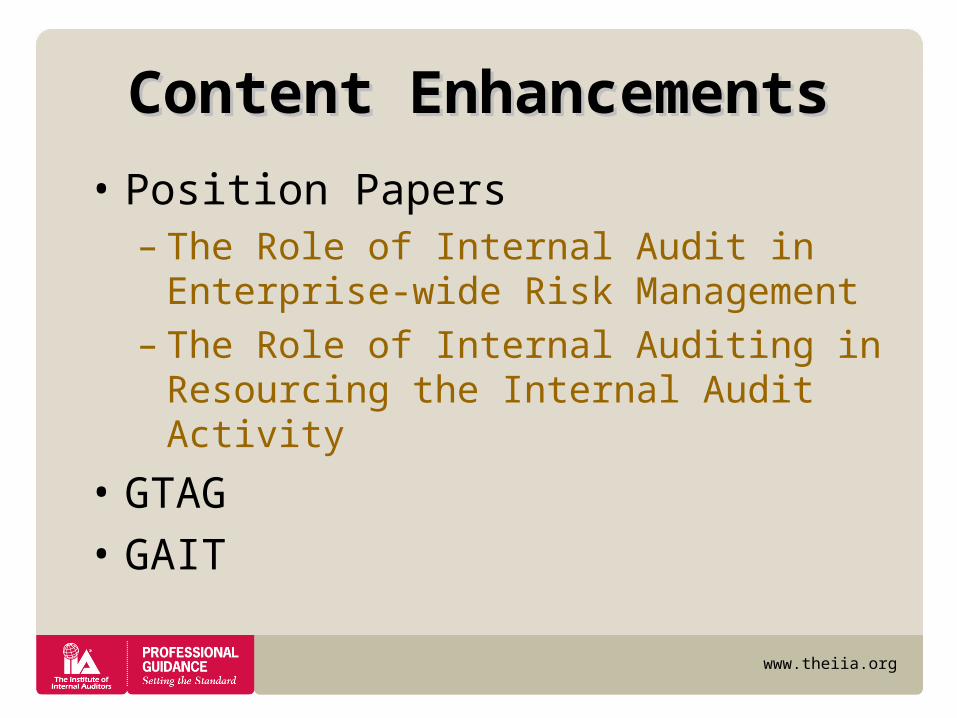

Content EnhancementsContent Enhancements

• Position Papers– The Role of Internal Audit in

Enterprise-wide Risk Management– The Role of Internal Auditing in

Resourcing the Internal Audit Activity

• GTAG• GAIT

www.theiia.org

What will remain What will remain the same?the same?

www.theiia.org

No ChangeNo Change

The Definition of Internal Auditing remains the same and the Code of Ethics had one minor change to ensure consistent grammar.

www.theiia.org

Will a practitioner’s Will a practitioner’s conformance be conformance be

affected?affected?

www.theiia.org

No ChangeNo Change

Conformance with the Standards under the IPPF is equal and identical to conformance under the PPF.

www.theiia.org

IPPF ScheduleIPPF Schedule• Interpretations of the Standards were

exposed the first quarter of 2008.

• The IPPF is scheduled for roll-out simultaneously in English, French, and Spanish, in January of 2009.

• The soft release of the Standards only is October 1st, 2008, to allow a three-month preview before the IPPF is effective.

• IPPF updates will be posted regularly to the Professional Guidance section of The IIA’s Web site.

www.theiia.org

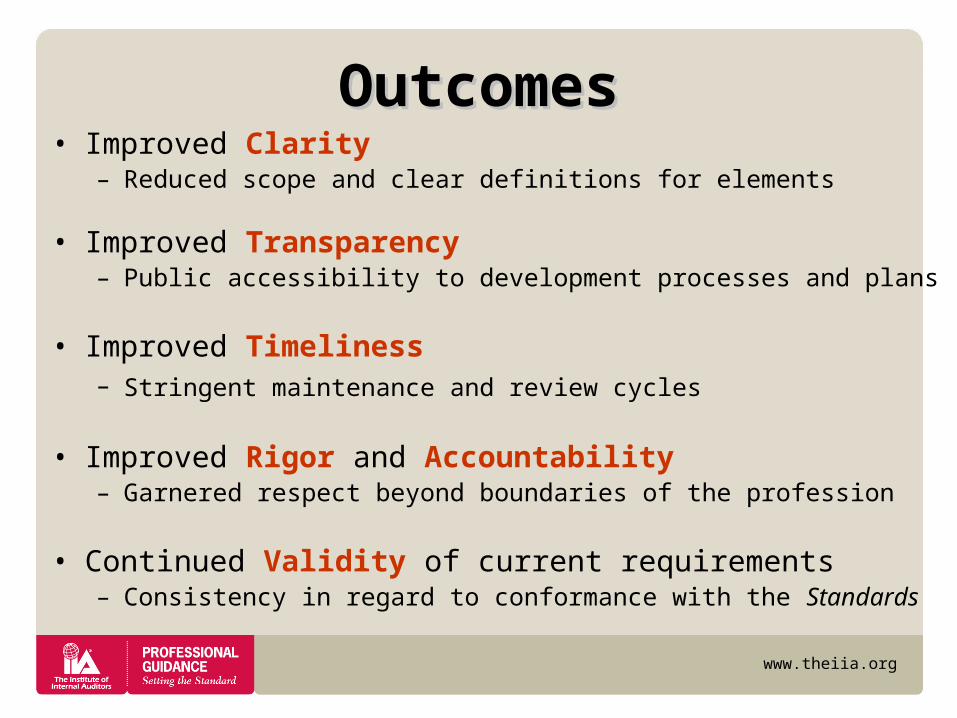

OutcomesOutcomes• Improved Clarity

– Reduced scope and clear definitions for elements

• Improved Transparency– Public accessibility to development processes and plans

• Improved Timeliness– Stringent maintenance and review cycles

• Improved Rigor and Accountability– Garnered respect beyond boundaries of the profession

• Continued Validity of current requirements– Consistency in regard to conformance with the Standards

www.theiia.org

From the From the PPFPPF

INTERNATIONAL

INTERNATIONAL

www.theiia.org

From the From the PPFPPF

to the to the IIPPFPPF

INTERNATIONAL

INTERNATIONAL

QUESTIONS?

www.theiia.org

This presentation was developed by

IIA Global Headquarters.