z-ben advisors april 2016 1 advisors april 2016 2 foreword – a new compeve landscape peter...

TRANSCRIPT

1 Z - B E N A D V I S O R S A p r i l 2 0 1 6

2 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Foreword–Anewcompe..velandscapePeterAlexander,ManagingDirector

To do so, we built a rankings model that directly compares the mainland efforts of more than 100 global investment managers. We assessed their relative strengths and weaknesses across more than three dozen strategic elements that have created, or can create, meaningful business opportunities in the inbound and outbound investment channels and – what we consider to be by far the most important opportunity China will deliver over the next three years – the onshore investment business.

Our findings in brief: US heavyweights, along with established and globalized European players feature prominently due to their ability to offer comprehensive services both to Chinese and global investors. That much we expected. However, we also noted that a number of regional Asian firms score higher than their total AUM might suggest, a reflection of the Mainland’s importance to their strategic plans. Moreover, some of the largest global managers by AUM are notably absent from our top 25 rankings: in most cases, we find this is due to low activity levels in one or more of the business areas we examined.

Here’s our most interesting and, in our view, thought-provoking finding: the top ranked manager in our survey only achieved a score of a little over 50%. We can’t think of a better way to highlight the huge growth potential that China offers even the best-positioned manager. It’s also a score that should fuel determination among firms ranked outside the top 25: China is likely to be the one geography where gains will come in scales large enough to allow good strategists and executors to leapfrog larger competitors.

Every global asset manager recognizes the fact that the Mainland is one of the most under-represented and under-serviced financial markets in the world. That’s changing, but slowly and often in ways that aren’t well-reported or well-recognized. We set out to shed more light on what is being done to penetrate mainland markets and how well those efforts are likely to be rewarded.

3 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Geographyofthetop25

C h i n a r a n k i n g s

UCITS, ’40 Act and Asian hubs

Different regional markets are home to major players in the Mainland, with concentrations coming from the US, UCITS-countries and nearby Asian regional markets.

Firms representing different markets are all present at the top of our competitive rankings. Many of these companies are either already heavyweights in servicing cross-border fund flows globally, or are based in economies that are highly linked to the mainland market through trade or direct investment.

United States

• JP Morgan (#1) • Invesco (#4) • BlackRock (#8) • Prudential Financial (#10) • PineBridge (#15) • Fidelity (#16) • Franklin Templeton (#18) • Goldman Sachs (#19) • Morgan Stanley (#20)

Canada

• BMO (#22)

United Kingdom

• Schroders (#5) • HSBC (#6) • Eastspring (#24)

France

• BNP Paribas (#3) • Societe Generale (#7) • AXA IM (#23)

Germany

• Deutsche AM (#9) • Allianz GI (#14)

Italy

• Eurizon (#12)

Switzerland

• UBS (#2)

Hong Kong

• Value Partners (#13)

Japan

• Nikko AM (#11) • Sumitomo Mitsui (#25)

Korea

• Samsung (#17)

Singapore

• DBS (#21)

4 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Mul.plecapabili.esassessed

C h i n a r a n k i n g s

Onsho re

Ou tbound

I nbound

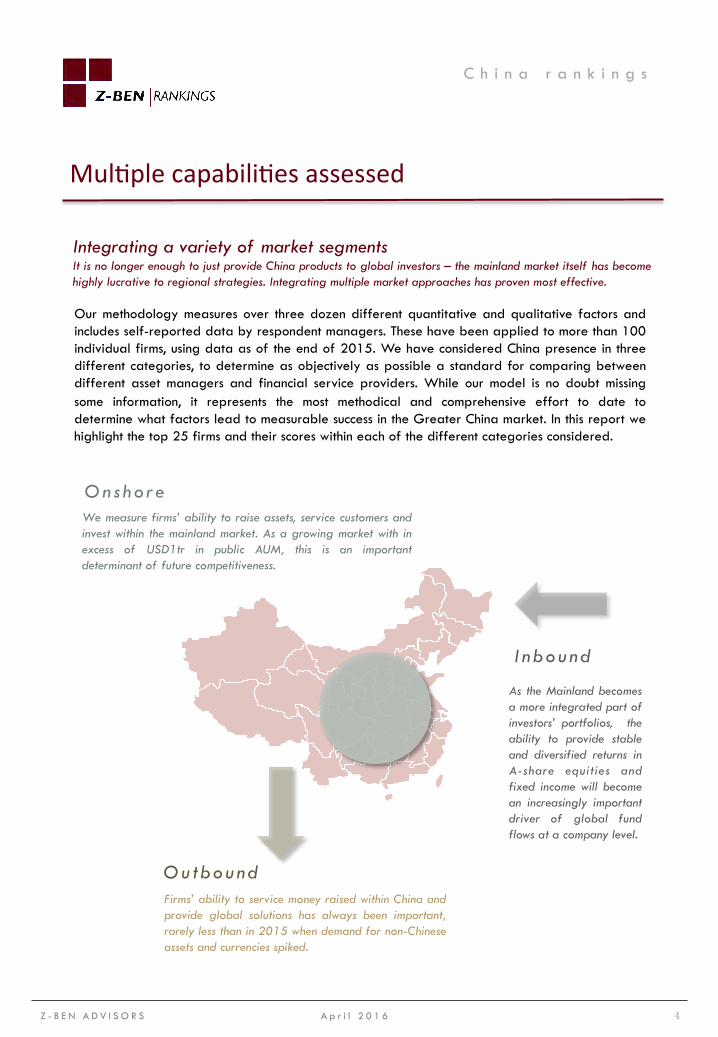

We measure firms’ ability to raise assets, service customers and invest within the mainland market. As a growing market with in excess of USD1tr in public AUM, this is an important determinant of future competitiveness.

As the Mainland becomes a more integrated part of investors’ portfolios, the ability to provide stable and diversified returns in A-share equities and fixed income will become an increasingly important driver of global fund flows at a company level.

Firms’ ability to service money raised within China and provide global solutions has always been important, rarely less than in 2015 when demand for non-Chinese assets and currencies spiked.

Integrating a variety of market segments It is no longer enough to just provide China products to global investors – the mainland market itself has become highly lucrative to regional strategies. Integrating multiple market approaches has proven most effective.

Our methodology measures over three dozen different quantitative and qualitative factors and includes self-reported data by respondent managers. These have been applied to more than 100 individual firms, using data as of the end of 2015. We have considered China presence in three different categories, to determine as objectively as possible a standard for comparing between different asset managers and financial service providers. While our model is no doubt missing some information, it represents the most methodical and comprehensive effort to date to determine what factors lead to measurable success in the Greater China market. In this report we highlight the top 25 firms and their scores within each of the different categories considered.

5 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Rank FirmFinal Index

Score

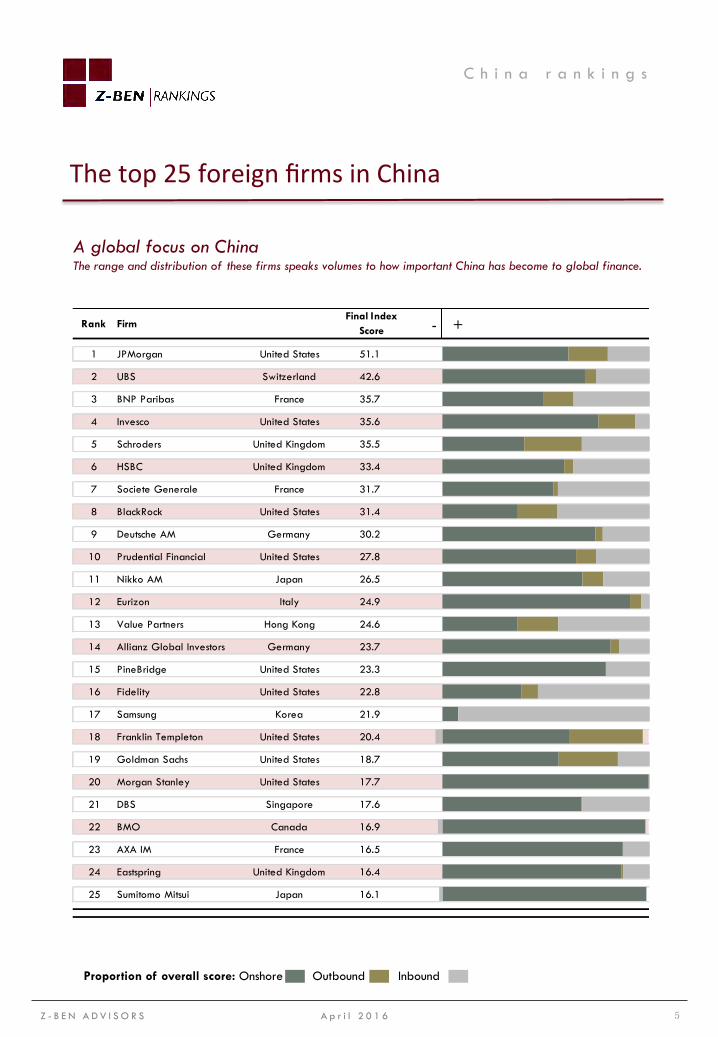

1 JPMorgan United States 51.1

2 UBS Switzerland 42.6

3 BNP Paribas France 35.7

4 Invesco United States 35.6

5 Schroders United Kingdom 35.5

6 HSBC United Kingdom 33.4

7 Societe Generale France 31.7

8 BlackRock United States 31.4

9 Deutsche AM Germany 30.2

10 Prudential Financial United States 27.8

11 Nikko AM Japan 26.5

12 Eurizon Italy 24.9

13 Value Partners Hong Kong 24.6

14 Allianz Global Investors Germany 23.7

15 PineBridge United States 23.3

16 Fidelity United States 22.8

17 Samsung Korea 21.9

18 Franklin Templeton United States 20.4

19 Goldman Sachs United States 18.7

20 Morgan Stanley United States 17.7

21 DBS Singapore 17.6

22 BMO Canada 16.9

23 AXA IM France 16.5

24 Eastspring United Kingdom 16.4

25 Sumitomo Mitsui Japan 16.1

Thetop25foreignfirmsinChina

C h i n a r a n k i n g s

A global focus on China The range and distribution of these firms speaks volumes to how important China has become to global finance.

Proportion of overall score: Onshore Outbound Inbound

- +

6 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Capabili.esindetail

C h i n a r a n k i n g s

Not all firms are focused on building out each set of business lines – some are specializing, typically due to existing overseas strategy. However Z-Ben Advisors believes that the days of focusing on just one business segment are soon over. Only five of the top 25 firms generate over 90% of their score from one category.

Top 10 managers for China onshore business

Top 10 managers for China outbound business

Top 10 managers for China inbound business

Onsho r e Ou tbound Inbound

Mainland China is the first major asset management market to exceed USD1tr in AUM without the support of a defined benefits retirement program.

Total onshore asse t s under management in the Mainland: USD11.5tr

Greater China GDP % of world total

13.84%

Greater China investment % of world total

3.35%

Even if Hong Kong is included; global investors’ allocations to Greater China remain far below what fundamentals suggest is necessary.

Despite acute demand for offshore allocations outside of the Mainland, very few financial firms are positioned to offer products or services.

0.26

3.31

6.25

14.81

19.29

0 5 10 15 20

Offshore

Managed assets

Financial products

Deposits

Property

Chinese investors holdings (USDtr) still exhibit extreme home bias

Rank Firm

1 JPMorgan

2 UBS

3 Invesco

4 Eurizon

5 Deutsche AM

6 HSBC

7 Allianz GI

8 PineBridge

9 Nikko AM

10 Prudential Financial

Rank Firm

1 Schroders

2 JPMorgan

3 Franklin Templeton

4 Invesco

5 BlackRock

6 Principal Global

7 Goldman Sachs

8 BNP Paribas

9 Value Partners

10 Natixis

Rank Firm

1 Samsung

2 Societe Generale

3 BlackRock

4 BNP Paribas

5 HSBC

6 Fidelity

7 Schroders

8 UBS

9 Value Partners

10 JPMorgan

7 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Appendix

C h i n a r a n k i n g s

Time frame Data was collected as of 31st December 2015. Instead of just providing a snapshot of each firm at that point in time, we have also considered factors that analyze a company’s performance throughout the year. Many, but not all, firms also responded to direct surveys which sought data about mandate sizes and numbers.

Onshore business The onshore business focuses on two key areas of mainland presence: joint venture companies and wholly foreign owned entities (WFOEs). The past twelve months has seen a marked increase in the number of firms setting up WFOEs onshore as it will likely be the primary way that most foreign firms conduct business onshore. However, for the time being, this is more of a strategic move for future business growth. Firms with existing joint ventures onshore can benefit economically right now and, as a consequence, we have to consider this as more valuable to a firm’s China strategy in 2015.

Outbound business The outbound business considers the various programs that permit domestic capital to be invested overseas. We also rank the scale of the firm’s subadvisory business.

Inbound business

The inbound business is split into three business lines, covering inbound quota channels and the Greater China fund management business. Here, our rankings consider both AUM and quota size as well as the speed of growth during the calendar year 2015.

Weightings

Each of the three categories is assigned a weighting that is based on its importance to current and future China strategy. As a result, the mainland business score has the highest weighting, followed by the off-to-on business. The on-to-off business has the lowest ranking due to the relative infancy of most outbound programs and the capital outflow controls that were imposed at the end of 2015, which remain in place as of the time of writing. Within each of the three categories, firms are given scores for numerous subcategories, of which each is assigned a weighting based on its importance to the business line.

The rankings model is designed to maintain the same structural format each year and weightings may change based on the evolving nature of foreign firms’ strategy in China and the regulatory environment. These changes would reflect the way that firms view China and are building their strategy.

Scoring structure

The overall score is calculated by summing the weighted scores of the three distinct business lines. The highest possible overall score that any firm can get is 100, which would result from being the highest ranked firm in not only all three categories, but in every subcategory.

Overall Score

Onshore Business Outbound Business Inbound Business

8 Z - B E N A D V I S O R S A p r i l 2 0 1 6

A U T H O R S Neil Flynn Analyst [email protected] Mr. Flynn covers the Greater China investment management industry, specializing in global asset management and capital markets. He leads the research and deliverable production of Z-Ben Advisors’ Greater China Quarterly for clients as well as the annual investment manager rankings report. He also regularly produces reports on fixed income, cross-border investment and alternative assets. Prior to joining Z-Ben Advisors, he worked as a derivatives trader for a global macro hedge fund in London. Mr. Flynn holds an MSc in finance from the University of York. Ivan Shi Director, Research [email protected] As head of the research department, Mr. Shi is responsible for overseeing all of Z-Ben Advisors’ analysis and thought leadership on a variety of topics, including China’s asset management industry, financial institutions, financial markets, macroeconomic and policy developments. During his eight years with Z-Ben Advisors, Mr. Shi has had the opportunity to work extensively on both research and advisory work, where he specializes in examining regulatory developments. Prior to joining the firm, Mr. Shi served as the personal research assistant to American journalist and political commentator, James Fallows, where he spent a year investigating policy and social reforms. Mr. Shi holds a B.A. and M.A. from Shanghai International Studies University. Stephen Baron Deputy Director, Strategic Solutions [email protected] Mr. Baron has broad experience working with clients across various sectors in the financial services space. He has worked closely with clients including banks, hedge funds, prime brokers, asset managers, & custodians amongst others. Mr. Baron came to China in 2009 to undertake his MSc in International Business at Ningbo, Nottingham University after graduating with a Distinction he moved to Beijing to pursue further studies at Tsinghua University. After completing his studies in the middle of 2011 he then moved to Shanghai to join Z-Ben Advisors.

A B O U T Z - B E N A D V I S O R S Z-Ben Advisors is a Shanghai-based consulting firm that helps global financial institutions capitalize on the fast-growing business opportunities presented by the Chinese and Greater China markets. Our business foundation is bottom-up, on the ground research; our services translate that research into actionable intelligence, recommendations and advice. The firm has permanent presences in Hong Kong and New York, with the majority of its staff based on the ground in Shanghai. For more information on Z-Ben Advisors’ 2016 China Rankings: Tel: +86 21 6075 8163 Email: [email protected]

9 Z - B E N A D V I S O R S A p r i l 2 0 1 6

Z-BEN ADVISORS Ltd. (Hong Kong) Two Exchange Square, 39/F 8 Connaught Place Central, Hong Kong SAR

Z-BEN ADVISORS Ltd. (Shanghai, China) 哲奔投资管理咨询(上海)有限公司 Hongjia Tower 25/F 388 Fushan Road Pudong New Area, Shanghai China 200122 +86 21 6075 8155

Disclaimer The contents of the China Rankings (the Product hereafter) are for informational purposes only. The data contained herein is based entirely upon the available information provided in public reports by the locally operating fund managers. The contained information has been verified to the best of Z-Ben Advisors and its re- search affiliate’s ability, but neither can accept responsibility for loss arising from the decisions based upon the product. The Product does not constitute investment advice or solicitation or counsel for investment in any fund or product mentioned thereof. The Product does not constitute or form part of, and should not be construed as, any offer for sale or subscription of any fund or product included herein. Z-Ben Advisors and its re- search affiliate expressly disclaims any and all responsibility for any consequential loss or damage of any kind whatsoever resulting, directly or indirectly, from (a) the use of the Product, (b) reliance on any information contained herein, (c) any error, inaccuracy or omission in any such information or (d) any action resulting therefrom. Disclosure Z-Ben Advisors and its research affiliate currently provides other products and services to some of the firms whose products are included in the Product. Z-Ben Advisors and its research affiliate may continue to have such dealings and may also have other ongoing business dealings with other firms whose products are included in the Product. Copyright The duplication of all or any part of the Product is strictly prohibited under copyright law. Any and all breaches in that law will be prosecuted. No part of the Product may be reproduced, transmitted in any form, electronic or otherwise, photocopied, stored in a retrieval system or otherwise passed on to any person or firm, in whole or in part, with out the prior written consent from Z-Ben Advisors.

10 Z - B E N A D V I S O R S A p r i l 2 0 1 6