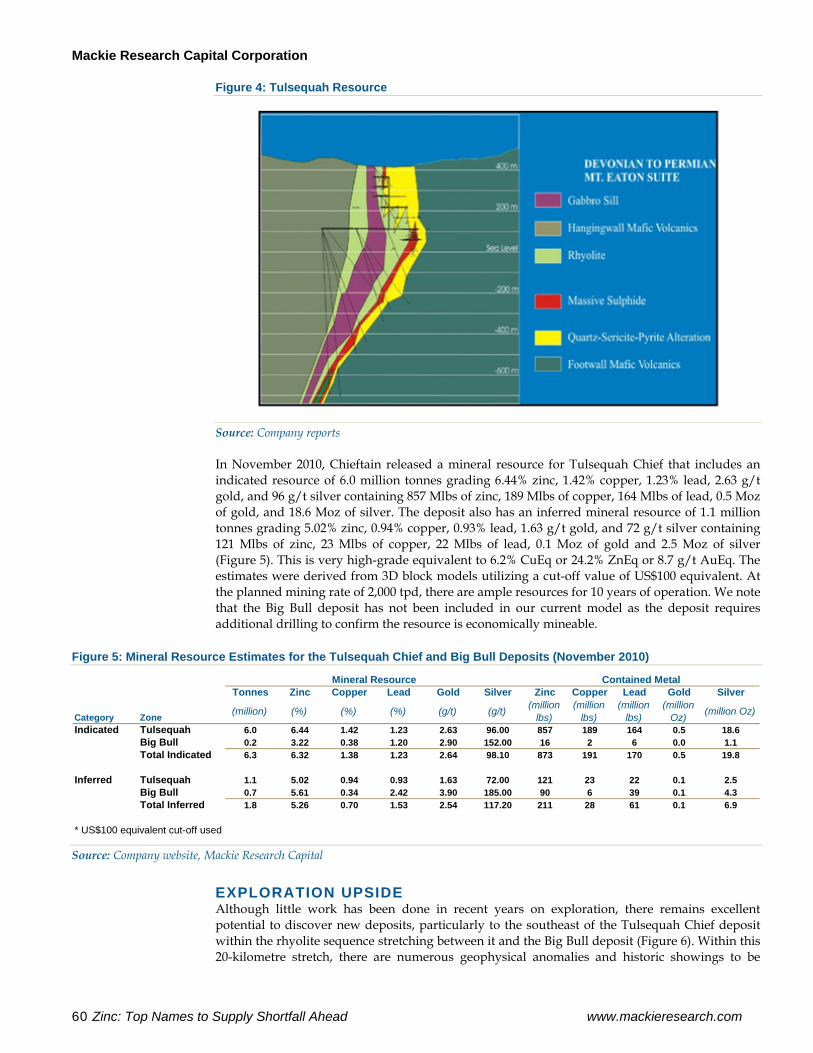

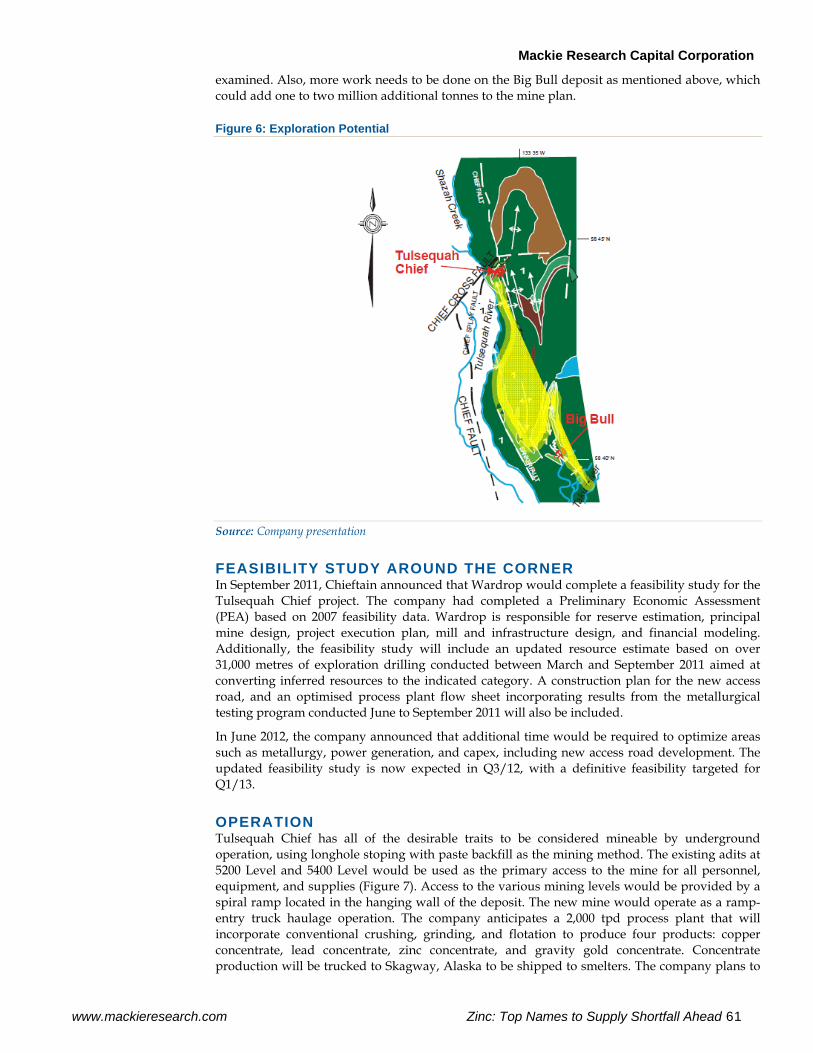

zinc launch_20120816

TRANSCRIPT

MACKIE RESEARCH SERVICE INDEPENDENT THOUGHT GROWTHM A C K I E R E S E A R C H SERVICE INDEPENDENTTHOUGHT GROWTH

M A C K I E R E S E A R C H SERVICE I N D E P E N D E N T

www.mackieresearch.com

16 August 2012 This report has been created by Analysts that are employed by Mackie Research Capital Corporation, a Canadian Investment Dealer. For further disclosures, please see the last pages of this report.

ZincTop Names to the Supply Shor t fa l l Ahead

INITIATING COVERAGE

TREVALI MINING CORP. (TV – TSX) BUY | 12-Month Target: $2.00

Burgeoning Zinc Producer in Established Camps

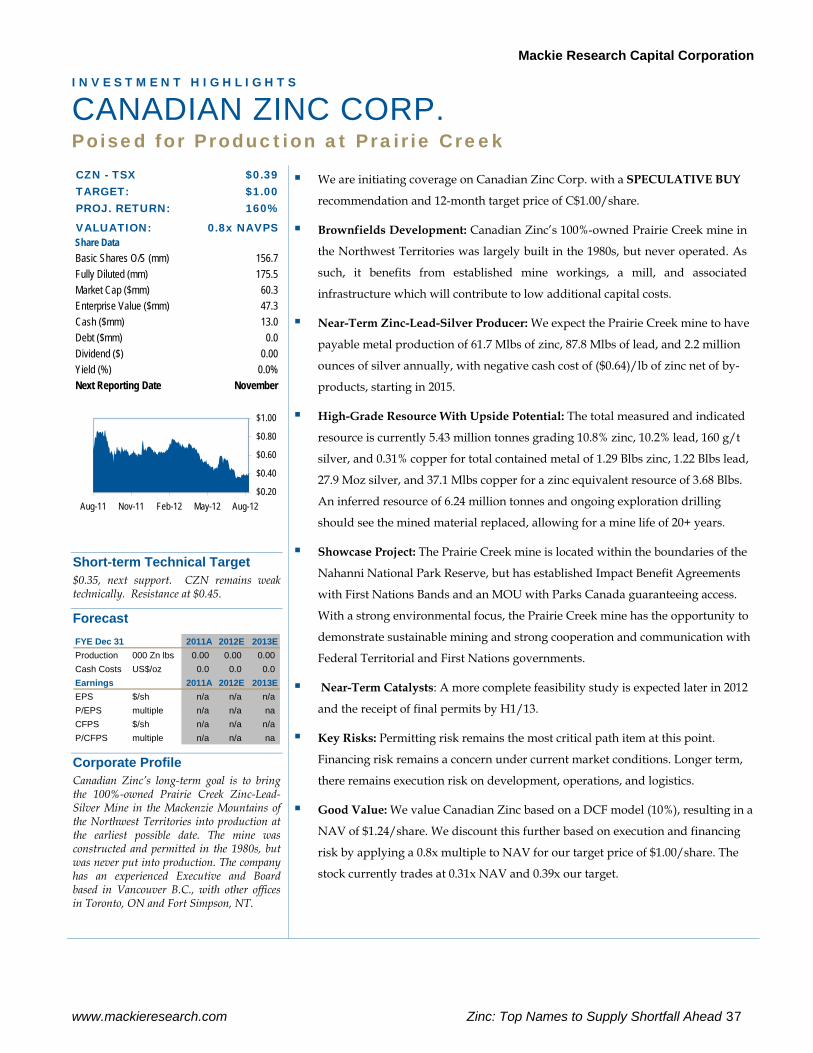

CANADIAN ZINC CORP. (CZN – TSX) SPECULATIVE BUY | 12-Month Target: $1.00

Poised for Production at Prairie Creek

CHIEFTAIN METALS INC. (CFB – TSX) SPECULATIVE BUY | 12-Month Target: $5.50

On the Road to Production

FORAN MINING CORP. (FOM – TSXV) SPECULATIVE BUY | 12-Month Target: $1.20 Growing Polymetallic Project in Saskatchewan

RATHDOWNEY RESOURCES LTD. (RTH – TSXV)

SPECULATIVE BUY | 12-Month Target: $1.25 Adding New Life to an Old Zinc District

MINING, BASE METALS

Matt O’Keefe

Analyst 416.860.8636

Brandon Throop Associate

416.860.7618 [email protected]

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 1

M I N I N G , B A S E M E T A L S

ZINC: TOP NAMES TO SUPPLY SHORTFALL AHEAD

EXECUTIVE SUMMARY The ongoing euro crisis and weak short-term outlook for western economies continue to weigh on equity markets and commodities. However, for the longer-term investor, there are some excellent bargains to be had. Among base metals, zinc is staging for its day in the sun due to very strong fundamentals, growing demand, and stagnating supply. Central to this thesis is the significant amount of supply coming offline within the next two years, creating a shortfall that should become quite material by 2014. In this report, we initiate coverage of five zinc-levered explorers/developers that show excellent value in the base metals space and offer a number of near-term catalysts that should drive their stock prices up in 2012/2013. As a basket, this collection of top names offers good potential for near-term production, attractive valuation, take-over potential, and re-ratings as they move past exploration, development, and production milestones.

Trevali Mining Corp. (TV-TSX) is a burgeoning zinc producer ramping up operations at its Halfmile mine in New Brunswick and on track to build out its Santander mine in Peru. This is one of the few “independent” zinc producers, and although Xstrata and Glencore have significant interests in Trevali’s projects, we see this as the next “go-to” name for zinc, once fully in production. We forecast Trevali to produce 221.8 Mlbs of zinc, 54.9 Mlbs of lead, 850,000 ounces of silver, and 4.6 Mlbs of copper at peak production on a consolidated basis. We rate Trevali a BUY with a 12-month target price of C$2.00/share.

Canadian Zinc Corp. (CZN-TSX) is a brownfields zinc company reviving the built but never operated Prairie Creek zinc-lead-silver mine in the NWT, Canada. Although the project has struggled through rigorous environmental and permitting review for several years, the dedicated team’s hard work should finally come to fruition with its final permits awarded by early 2013. Near-term catalysts, including a more complete feasibility study expected later in 2012, and receipt of final permits in H1/13, should aid in de-risking the project. Once in production, the high-grade Prairie Creek mine will be a significant zinc and silver producer. We rate Canadian Zinc a SPECULATIVE BUY with a 12-month target price of C$1.00/share.

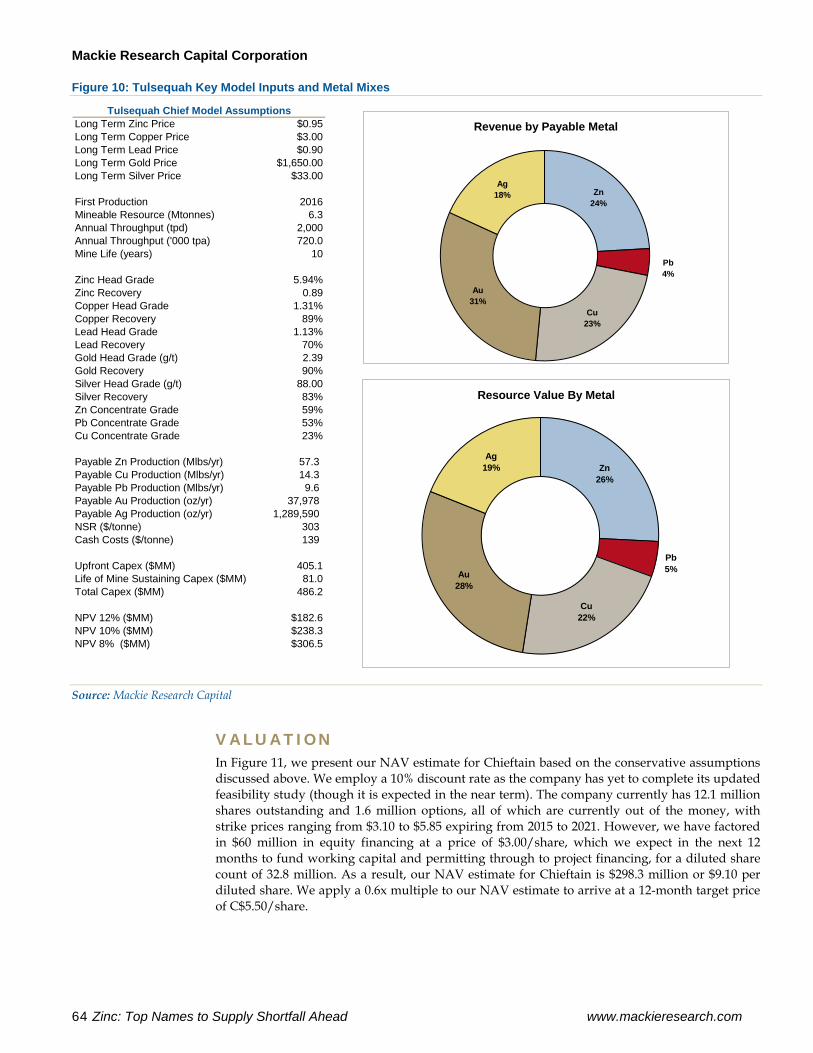

Chieftain Metals Inc. (CFB-TSX) is developing its Tulsequah Chief project in northern B.C. Although this will be a zinc producer, it is technically a polymetallic producer with about equal contributions from zinc, copper, and gold. Tulsequah Chief stands out for its high grades and high expected margins. It is well supported and has several key catalysts in the next 12 months, including an updated feasibility study and approval for a rerouted access road. We rate Chieftain a SPECULATIVE BUY with a 12-month target price of C$5.50/share.

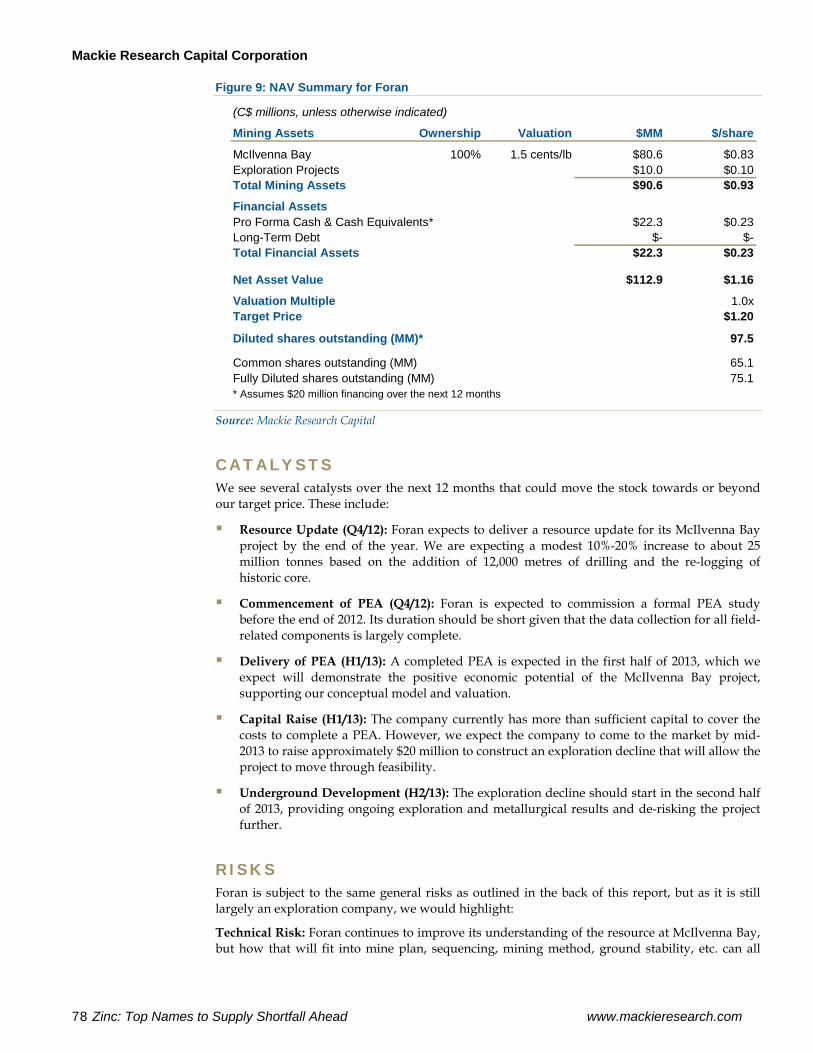

Foran Mining Corp. (FOM-TSXV) is an exploration and development company with a focus on developing its 100%-owned McIlvenna Bay property in east-central Saskatchewan. The deposit hosts a high-grade resource that remains open and continues to grow with subsequent programs. A resource update by the end of 2012 and the completion of a PEA on McIlvenna Bay in the first half of 2013 are near-term catalysts that should see the stock move through our target. We rate Foran Mining a SPECULATIVE BUY with a 12-month target price of C$1.20/share.

Rathdowney Resources Ltd. (RTH-TSXV) is the earliest stage of this group, building out a classic Mississippi Valley deposit within the zinc orefields of southern Poland. Its Olza project is strategically located close to the operating Pomorzany mill and mine, which is near depletion and in search of new ore or a new owner. Rathdowney’s project stands out for its ease of access, established mine infrastructure, and proximity to markets. As part of the Hunter Dickinson Inc. group of companies, Rathdowney has strong marketing, financial and legal resources to draw upon. We rate Rathdowney a SPECULATIVE BUY with a 12-month target price of C$1.25/share.

Mackie Research Capital Corporation

2 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

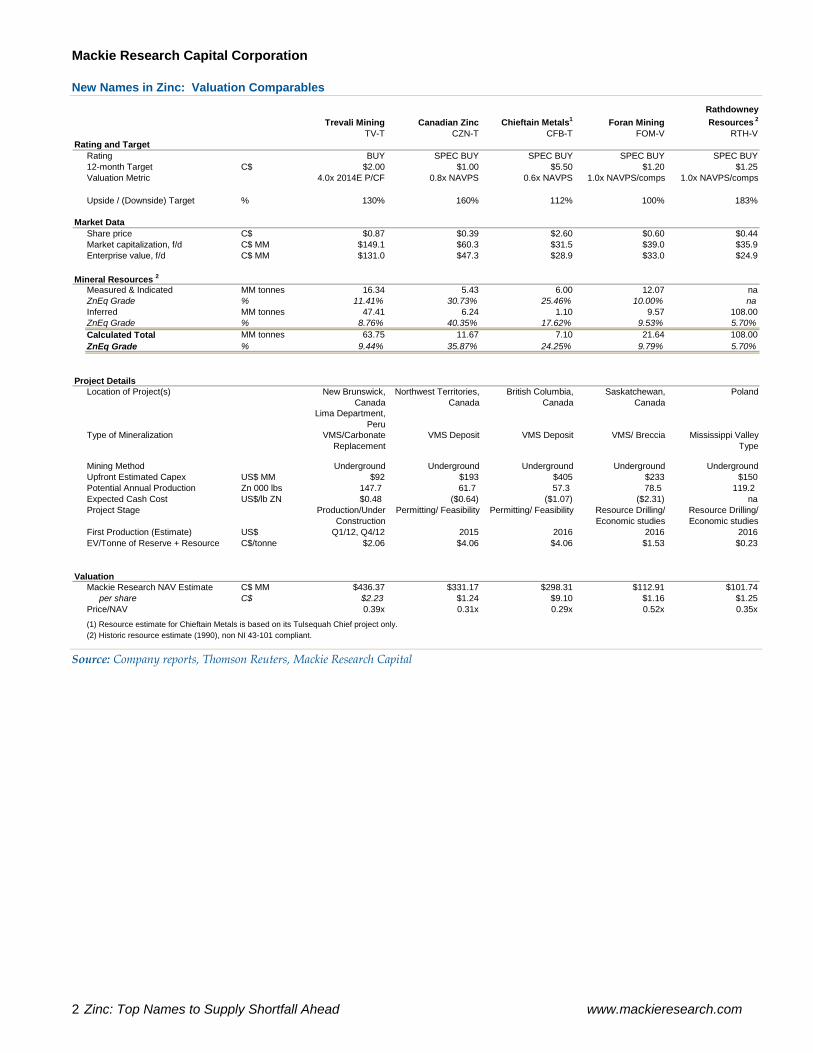

New Names in Zinc: Valuation Comparables

Trevali Mining Canadian Zinc Chieftain Metals1 Foran MiningRathdowney Resources 2

TV-T CZN-T CFB-T FOM-V RTH-VRating and Target

Rating BUY SPEC BUY SPEC BUY SPEC BUY SPEC BUY12-month Target C$ $2.00 $1.00 $5.50 $1.20 $1.25Valuation Metric 4.0x 2014E P/CF 0.8x NAVPS 0.6x NAVPS 1.0x NAVPS/comps 1.0x NAVPS/comps

Upside / (Downside) Target % 130% 160% 112% 100% 183%

Market DataShare price C$ $0.87 $0.39 $2.60 $0.60 $0.44Market capitalization, f/d C$ MM $149.1 $60.3 $31.5 $39.0 $35.9Enterprise value, f/d C$ MM $131.0 $47.3 $28.9 $33.0 $24.9

Mineral Resources 2Measured & Indicated MM tonnes 16.34 5.43 6.00 12.07 naZnEq Grade % 11.41% 30.73% 25.46% 10.00% naInferred MM tonnes 47.41 6.24 1.10 9.57 108.00ZnEq Grade % 8.76% 40.35% 17.62% 9.53% 5.70%Calculated Total MM tonnes 63.75 11.67 7.10 21.64 108.00ZnEq Grade % 9.44% 35.87% 24.25% 9.79% 5.70%

Project DetailsLocation of Project(s) New Brunswick,

CanadaNorthwest Territories,

CanadaBritish Columbia,

CanadaSaskatchewan,

CanadaPoland

Lima Department, Peru

Type of Mineralization VMS/Carbonate Replacement

VMS Deposit VMS Deposit VMS/ Breccia Mississippi Valley Type

Mining Method Underground Underground Underground Underground UndergroundUpfront Estimated Capex US$ MM $92 $193 $405 $233 $150Potential Annual Production Zn 000 lbs 147.7 61.7 57.3 78.5 119.2 Expected Cash Cost US$/lb ZN $0.48 ($0.64) ($1.07) ($2.31) naProject Stage Production/Under

ConstructionPermitting/ Feasibility Permitting/ Feasibility Resource Drilling/

Economic studiesResource Drilling/ Economic studies

First Production (Estimate) US$ Q1/12, Q4/12 2015 2016 2016 2016EV/Tonne of Reserve + Resource C$/tonne $2.06 $4.06 $4.06 $1.53 $0.23

ValuationMackie Research NAV Estimate C$ MM $436.37 $331.17 $298.31 $112.91 $101.74 per share C$ $2.23 $1.24 $9.10 $1.16 $1.25Price/NAV 0.39x 0.31x 0.29x 0.52x 0.35x(1) Resource estimate for Chieftain Metals is based on its Tulsequah Chief project only.(2) Historic resource estimate (1990), non NI 43-101 compliant.

Source: Company reports, Thomson Reuters, Mackie Research Capital

Mackie Research Capital Corporation

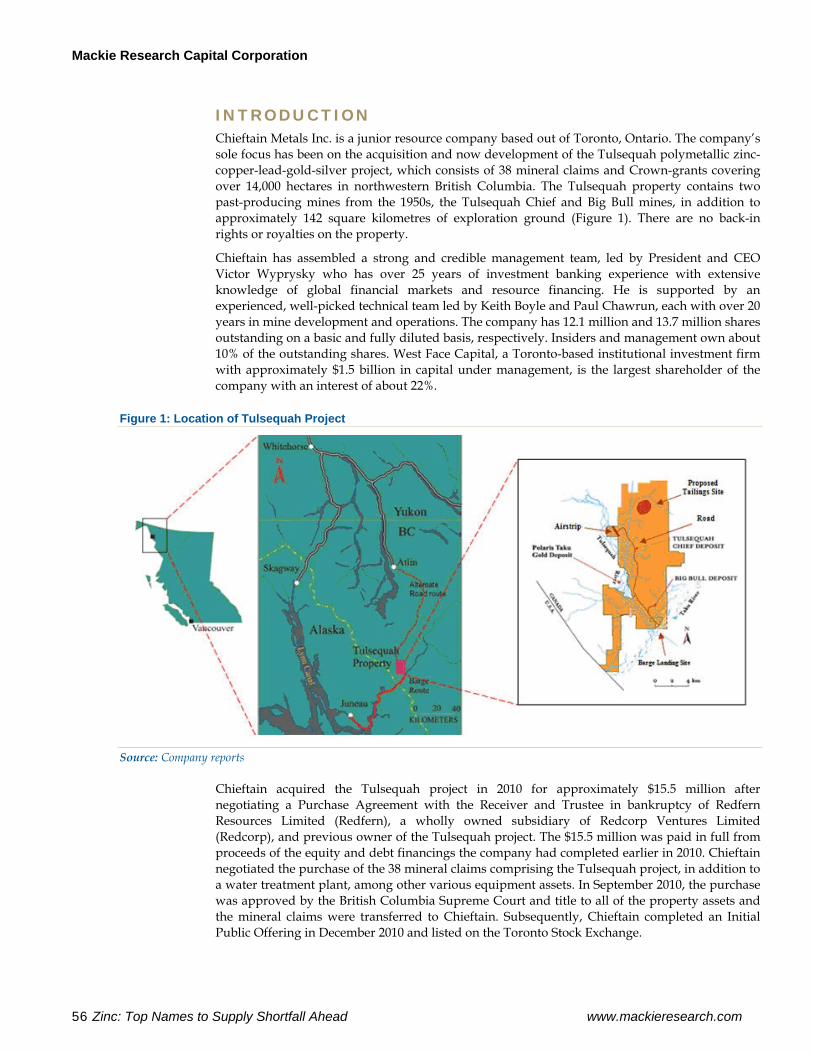

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 3

M I N I N G , B A S E M E T A L S

ZINC: TOP NAMES TO SUPPLY SHORTFALL AHEAD

TABLE OF CONTENTS EXECUTIVE SUMMARY.......................................................................................................................................................................1 THE ZINC MARKET ..............................................................................................................................................................................6

Zinc – Inflection Point Ahead .............................................................................................................................................................6 Don’t Forget Lead.................................................................................................................................................................................9 Zinc & Lead Pricing............................................................................................................................................................................10 Investment Strategy............................................................................................................................................................................12 Initiating Coverage .............................................................................................................................................................................14

TREVALI MINING CORP...................................................................................................................................................................17 Introduction ............................................................................................................................................................................................18

Company Profile.................................................................................................................................................................................18 Consolidated Production Profile.........................................................................................................................................................19 Large Global Resource..........................................................................................................................................................................20 New Brunswick Complex.....................................................................................................................................................................21

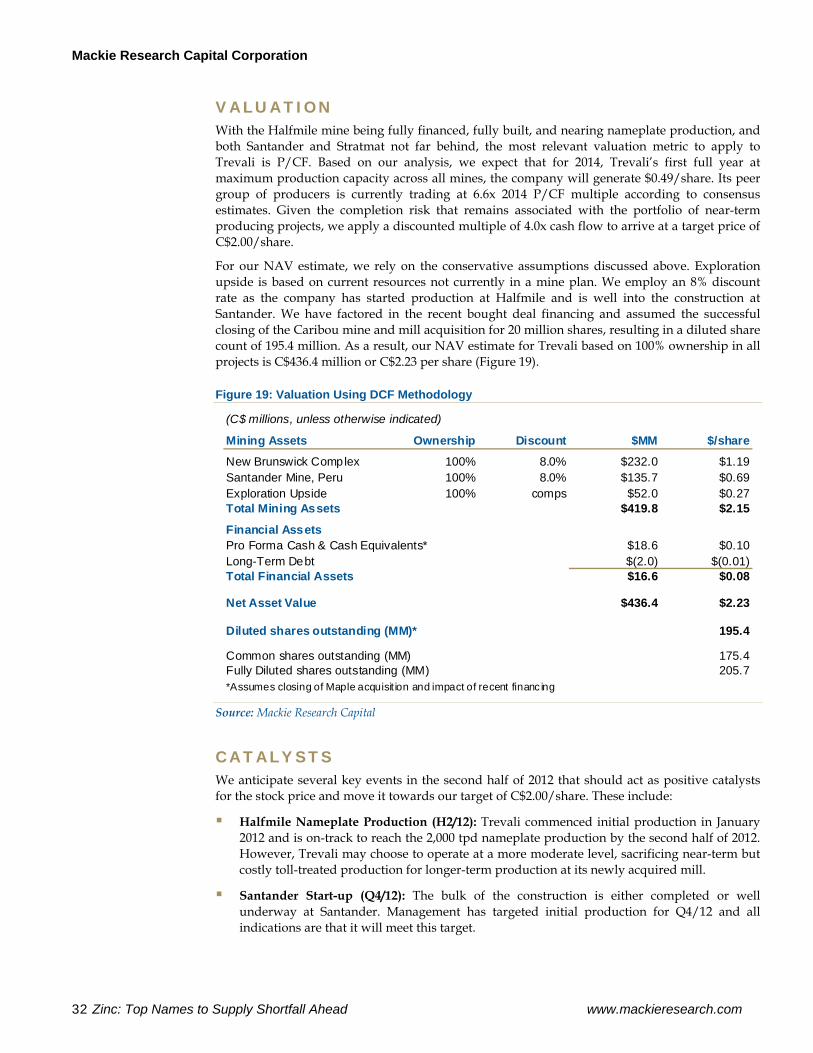

Regional Geology – A Classic Camp................................................................................................................................................21 Resource Estimates .............................................................................................................................................................................22 Halfmile & Stratmat – A Great Start ................................................................................................................................................23 Caribou Mill & Mine Acquisition.....................................................................................................................................................24 Adding Tonnage to the Portfolio......................................................................................................................................................25 New Brunswick Development Plan .................................................................................................................................................25 Project Assumptions...........................................................................................................................................................................26

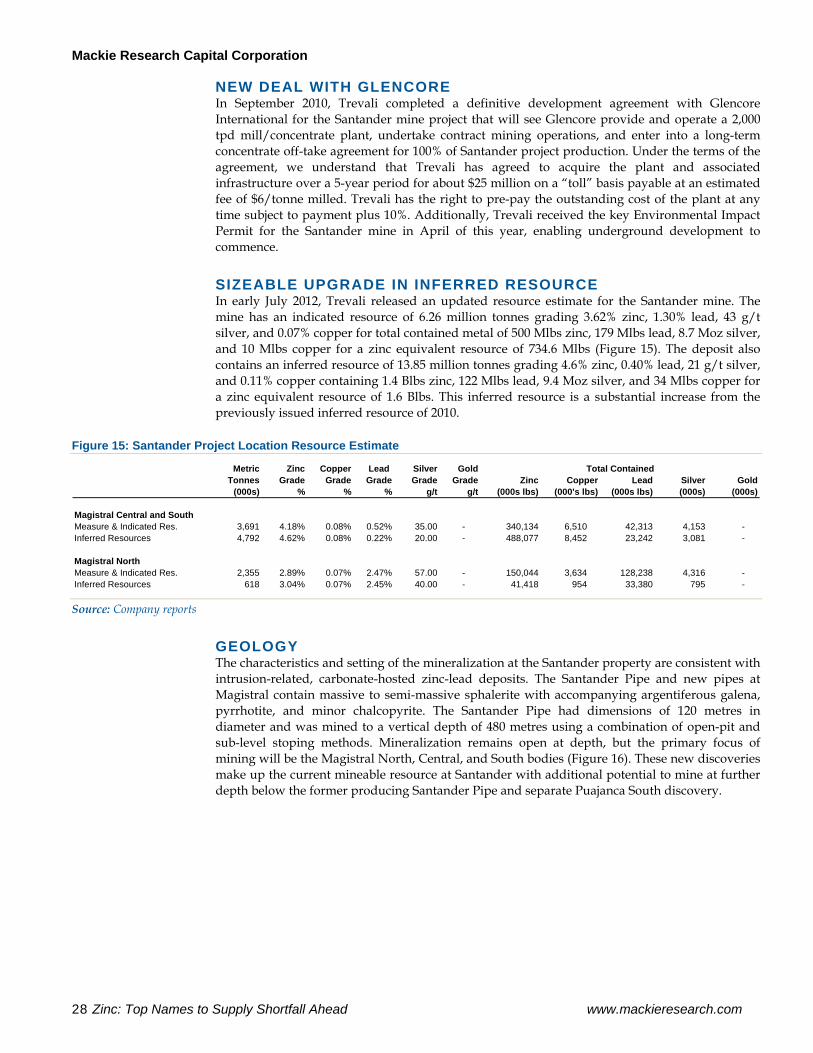

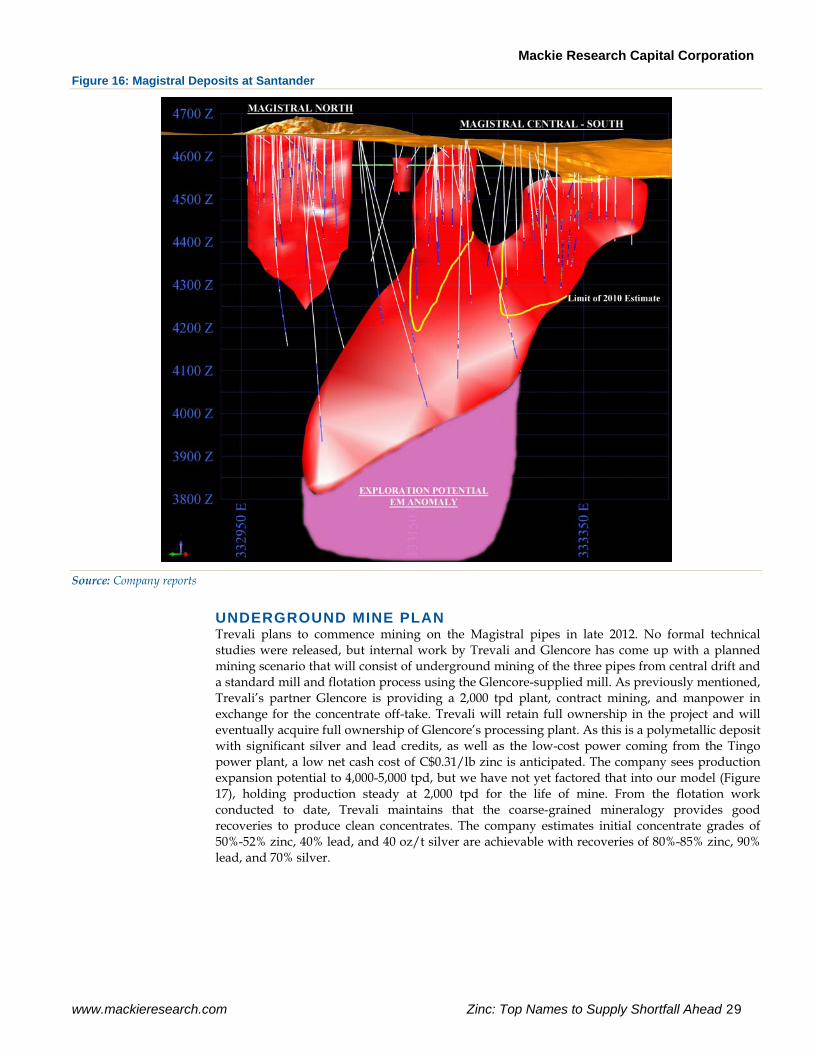

Santander Mine – Peru..........................................................................................................................................................................27 Location & Infrastructure ..................................................................................................................................................................27 History .................................................................................................................................................................................................27 New Deal With Glencore...................................................................................................................................................................28 Sizeable Upgrade in Inferred Resource ...........................................................................................................................................28 Geology ................................................................................................................................................................................................28 Underground Mine plan....................................................................................................................................................................29 Tingo Hydroelectric Plant, Peru .......................................................................................................................................................30 Project Progress & Timeline ..............................................................................................................................................................30

Other Assets............................................................................................................................................................................................31 Huampar Silver Mine, Peru ..............................................................................................................................................................31 Ruttan Copper Mine, Manitoba........................................................................................................................................................31

Valuation.................................................................................................................................................................................................32 Catalysts...................................................................................................................................................................................................32 Risks.........................................................................................................................................................................................................33 Conclusion ..............................................................................................................................................................................................33 Management Team ................................................................................................................................................................................34 CANADIAN ZINC CORP....................................................................................................................................................................37 Company Background ..........................................................................................................................................................................38

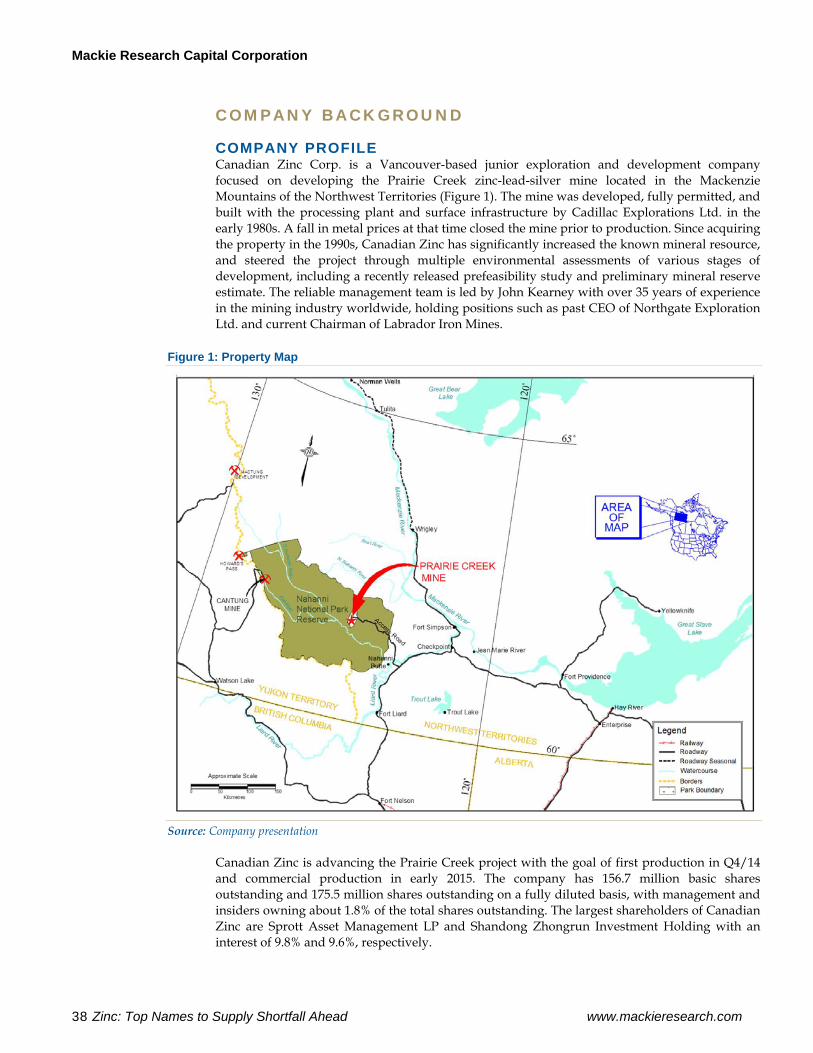

Company Profile.................................................................................................................................................................................38 Prairie Creek Mine ................................................................................................................................................................................39

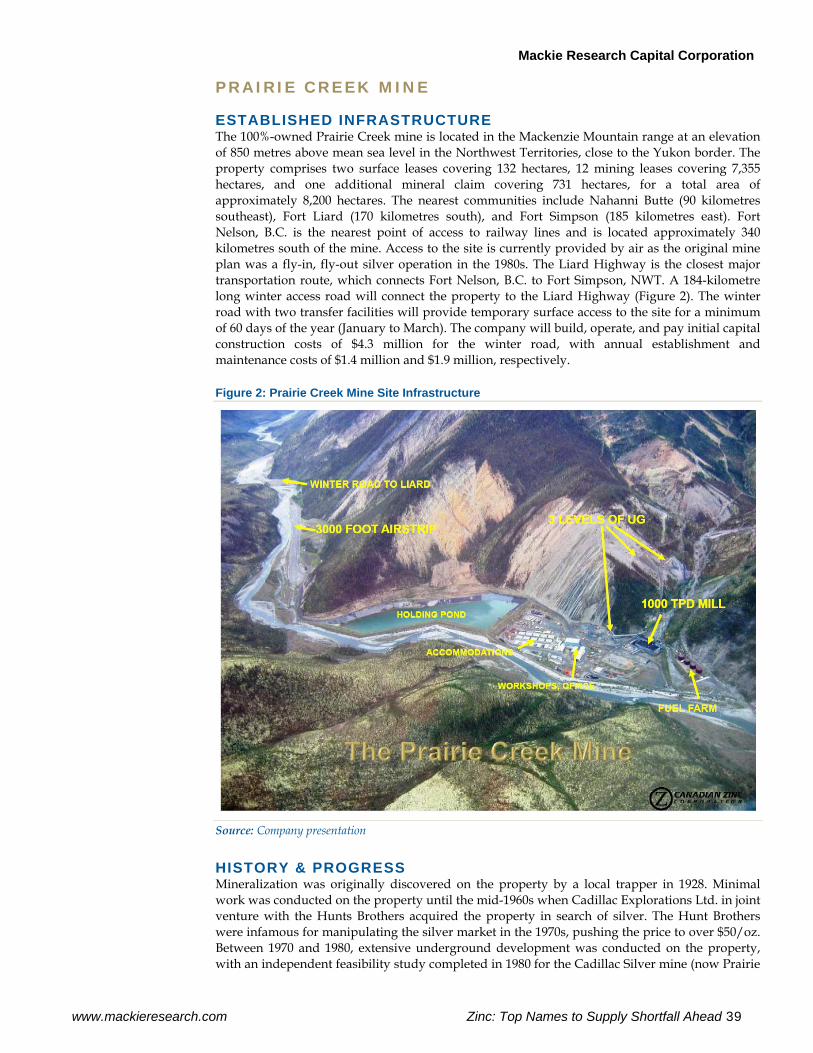

Established Infrastructure .................................................................................................................................................................39 History & Progress .............................................................................................................................................................................39 Government & First Nations Agreements in Place ........................................................................................................................40 Prairie Creek Geology ........................................................................................................................................................................41

Mackie Research Capital Corporation

4 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

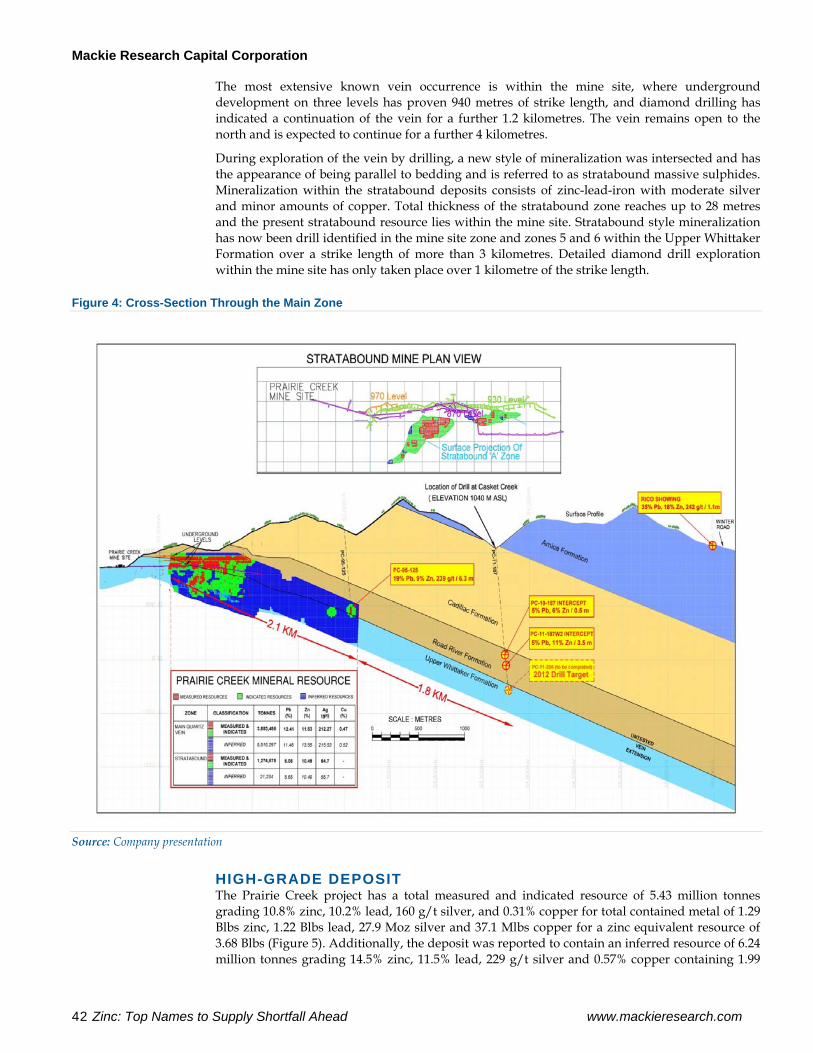

High-Grade Deposit ...........................................................................................................................................................................42 Resource Potential ..............................................................................................................................................................................43 Mine Plan – Mostly Logistics ............................................................................................................................................................44 Water & Waste Management ............................................................................................................................................................46 Project Timeline ..................................................................................................................................................................................46 Permitting ............................................................................................................................................................................................47 Project Assumptions Summary ........................................................................................................................................................47

Other Assets............................................................................................................................................................................................48 Vatukoula Gold Mines .......................................................................................................................................................................48 South Tally Pond (Paragon Minerals Acquisition) ........................................................................................................................49

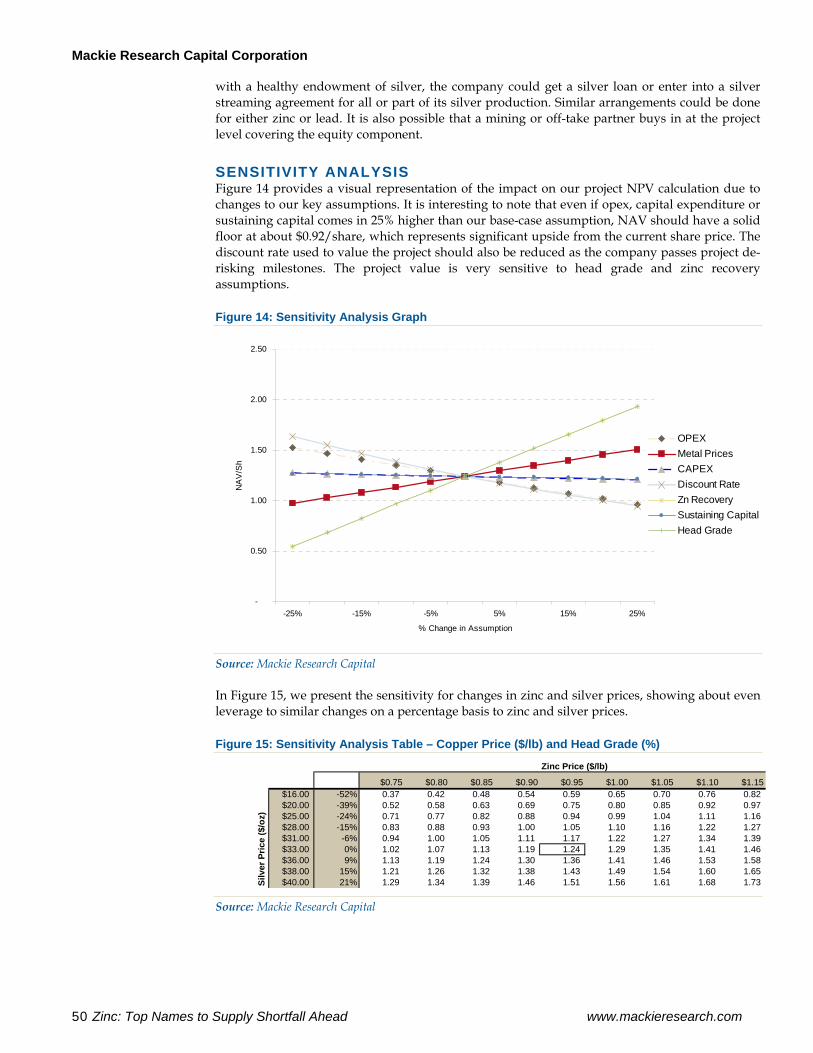

Valuation.................................................................................................................................................................................................49 Financing Assumptions .....................................................................................................................................................................49 Sensitivity Analysis ............................................................................................................................................................................50

Catalysts...................................................................................................................................................................................................51 Risks.........................................................................................................................................................................................................51 Conclusion ..............................................................................................................................................................................................51 Management Team ................................................................................................................................................................................53 CHIEFTAIN METALS INC..................................................................................................................................................................55 Introduction ............................................................................................................................................................................................56 Tulsequah Project ..................................................................................................................................................................................57

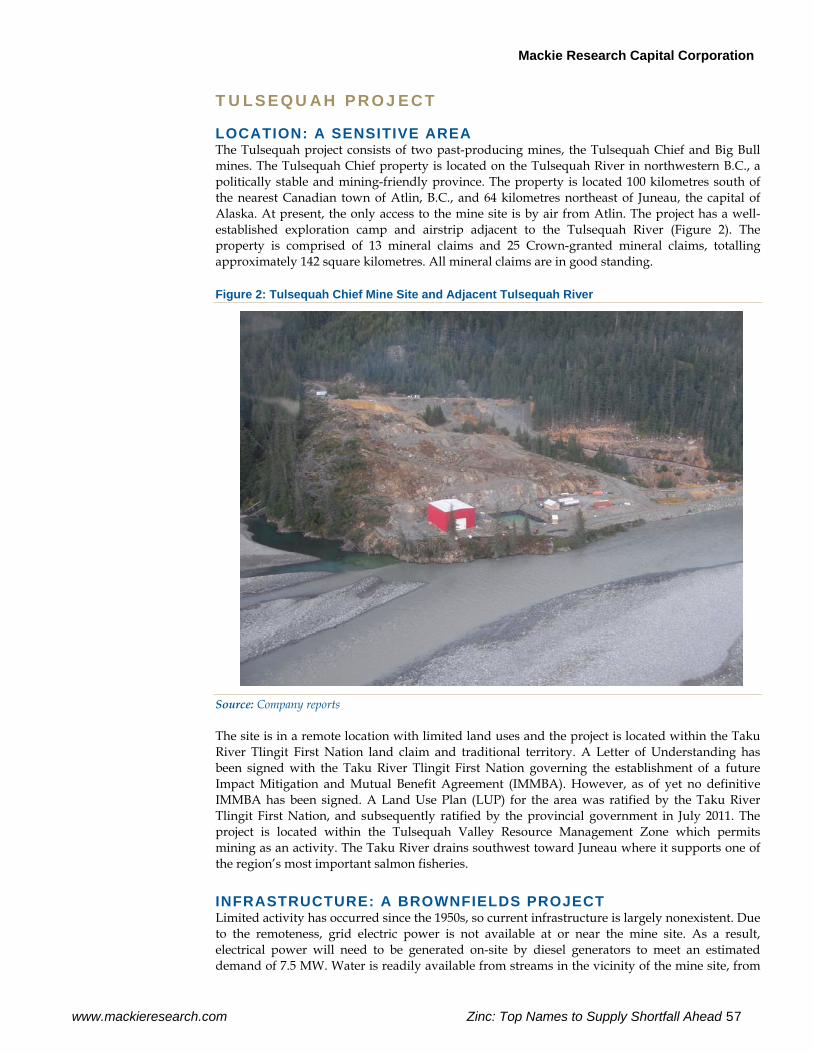

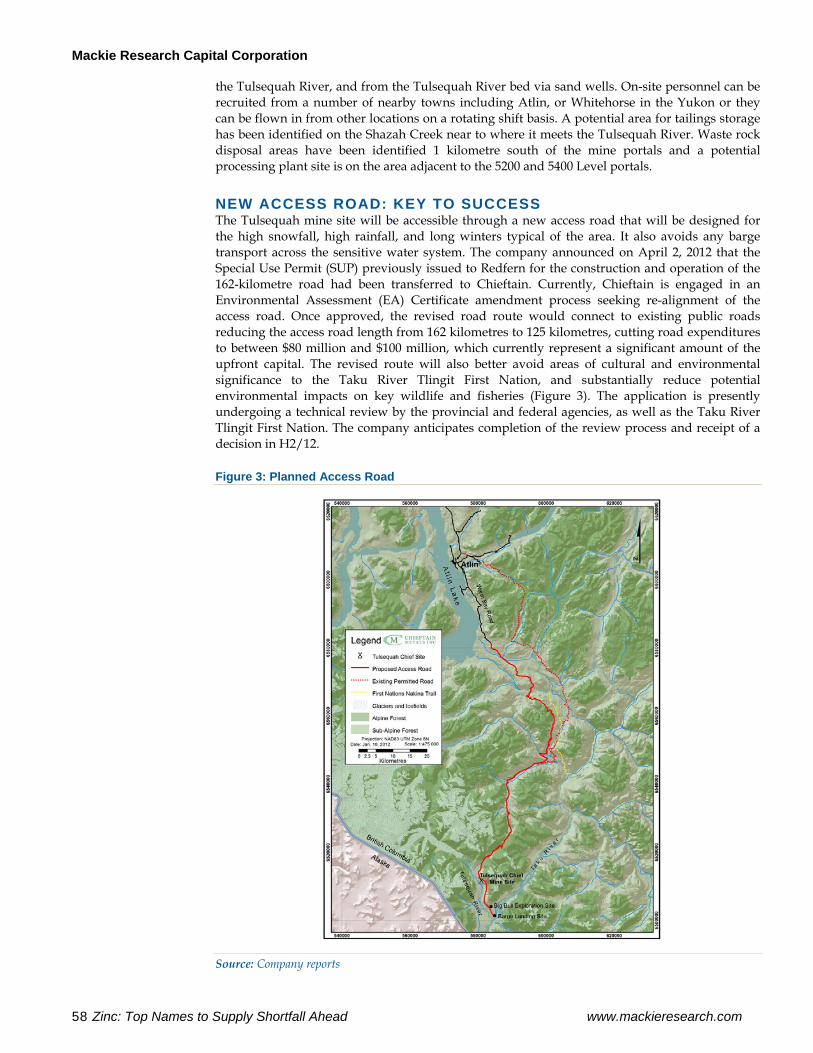

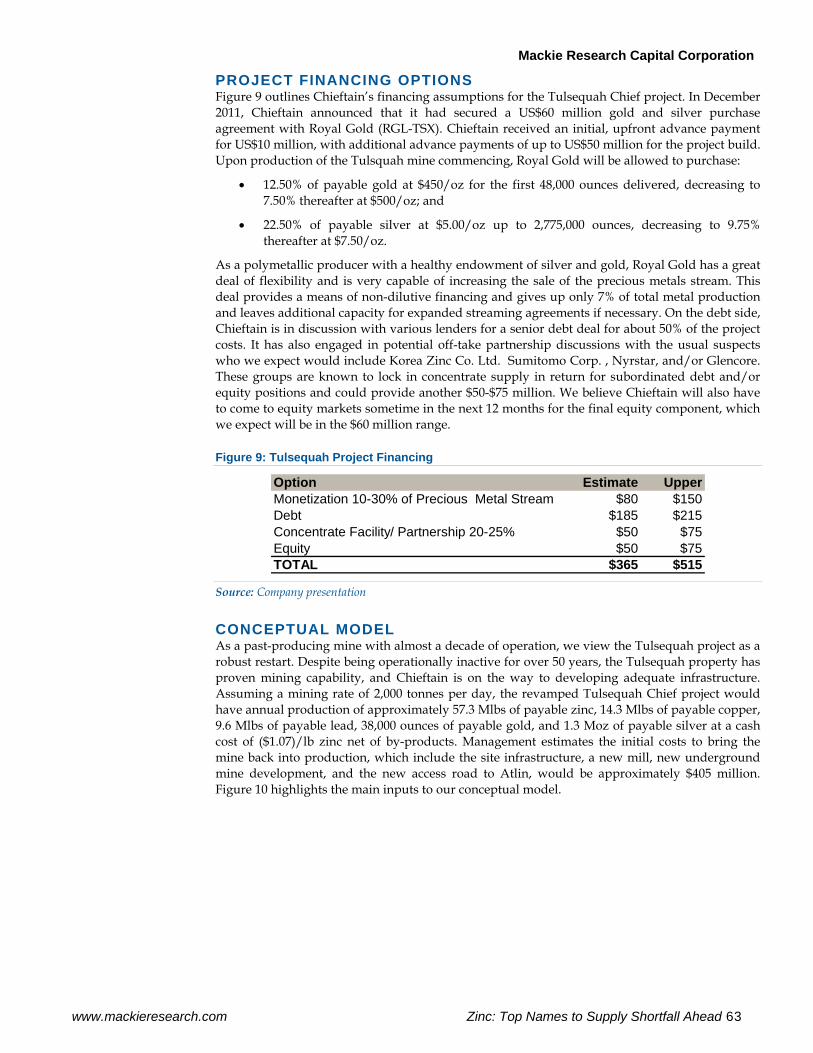

Location: A Sensitive area .................................................................................................................................................................57 Infrastructure: A Brownfields Project ..............................................................................................................................................57 New Access Road: Key to Success....................................................................................................................................................58 History .................................................................................................................................................................................................59 Environmental: Fixing a Leaky Legacy ...........................................................................................................................................59 Resource: High-Grade Polymetallic .................................................................................................................................................59 Exploration Upside.............................................................................................................................................................................60 Feasibility Study Around the Corner...............................................................................................................................................61 Operation .............................................................................................................................................................................................61 Project Timeline ..................................................................................................................................................................................62 Project Financing Options .................................................................................................................................................................63 Conceptual Model ..............................................................................................................................................................................63

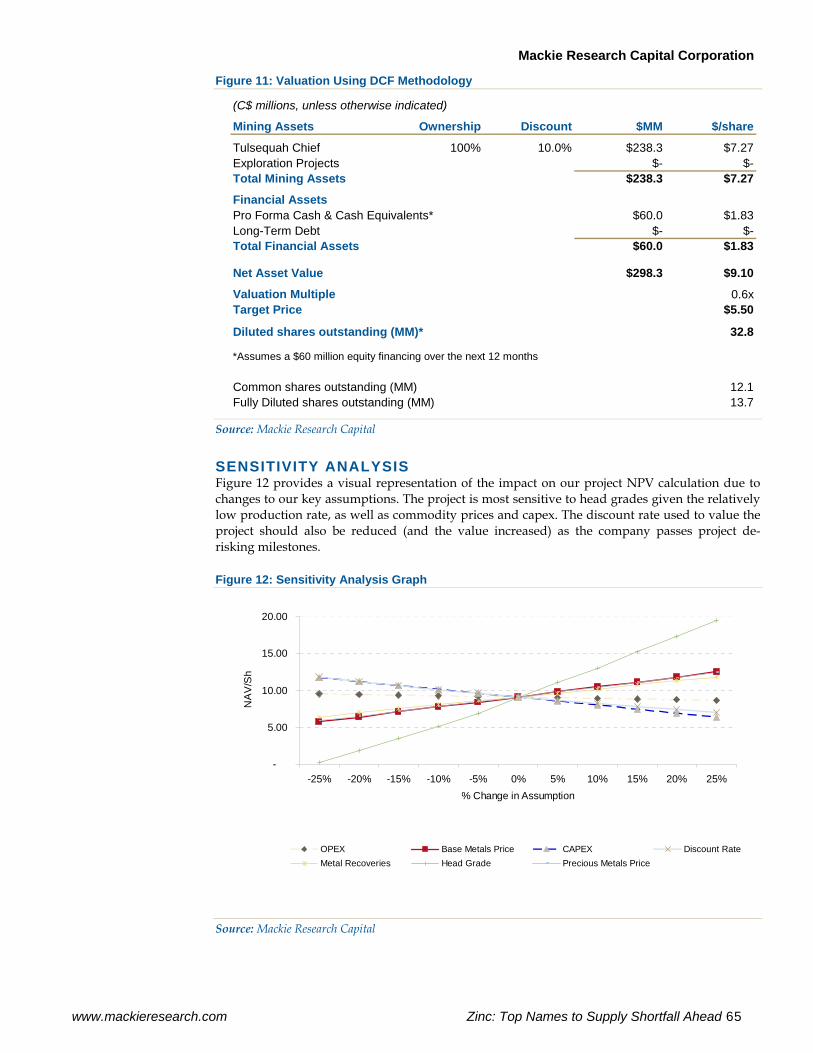

Valuation.................................................................................................................................................................................................64 Sensitivity Analysis ............................................................................................................................................................................65

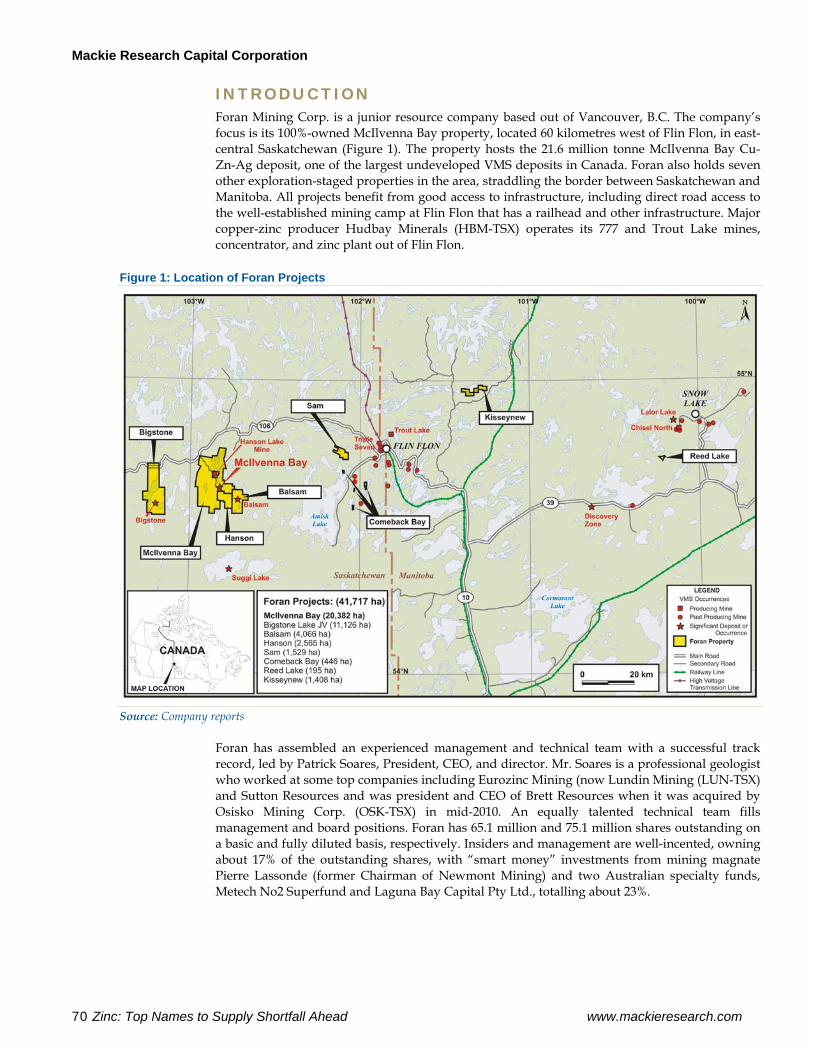

Catalysts...................................................................................................................................................................................................66 Risks.........................................................................................................................................................................................................67 Conclusion ..............................................................................................................................................................................................67 Management Team ................................................................................................................................................................................68 FORAN MINING CORP. .....................................................................................................................................................................69 Introduction ............................................................................................................................................................................................70 McIlvenna Bay Project ..........................................................................................................................................................................71

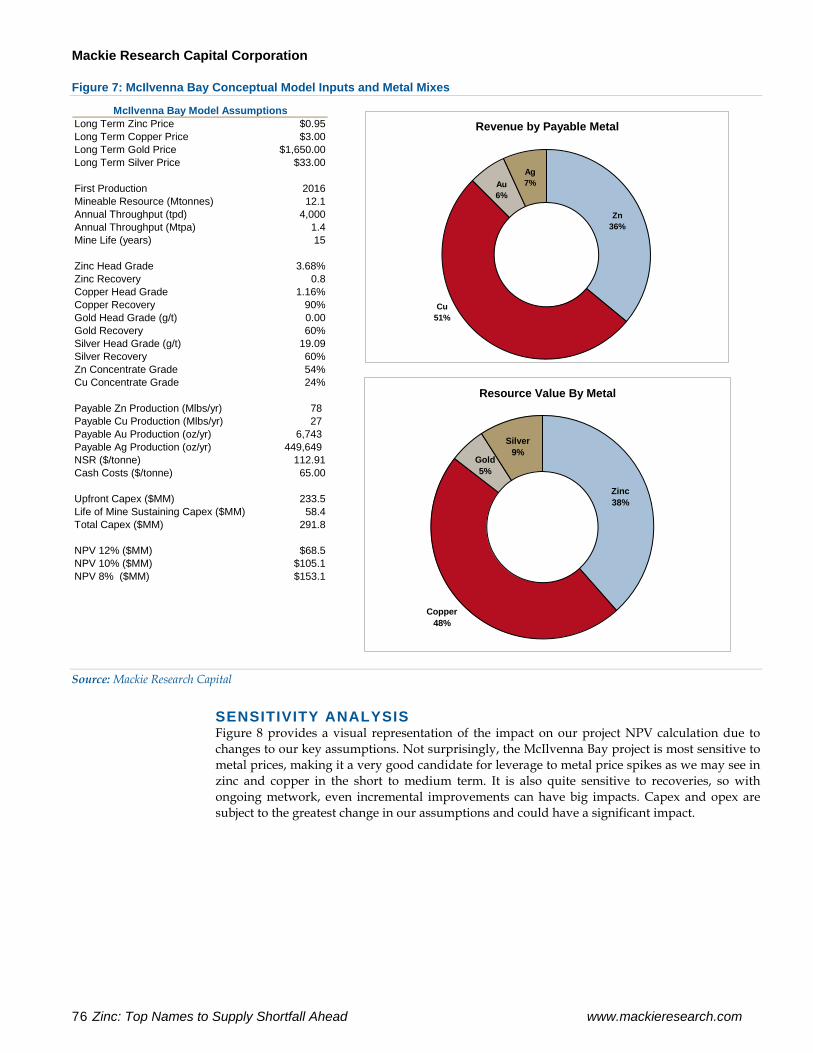

Location & History .............................................................................................................................................................................71 Geology – World-Class VMS Camp.................................................................................................................................................71 McIlvenna Bay Deposit ......................................................................................................................................................................72 Resource & Metallurgy ......................................................................................................................................................................74 Resource Upside .................................................................................................................................................................................74 Conceptual Model – PEA Soon On the Way...................................................................................................................................75 Sensitivity Analysis ............................................................................................................................................................................76

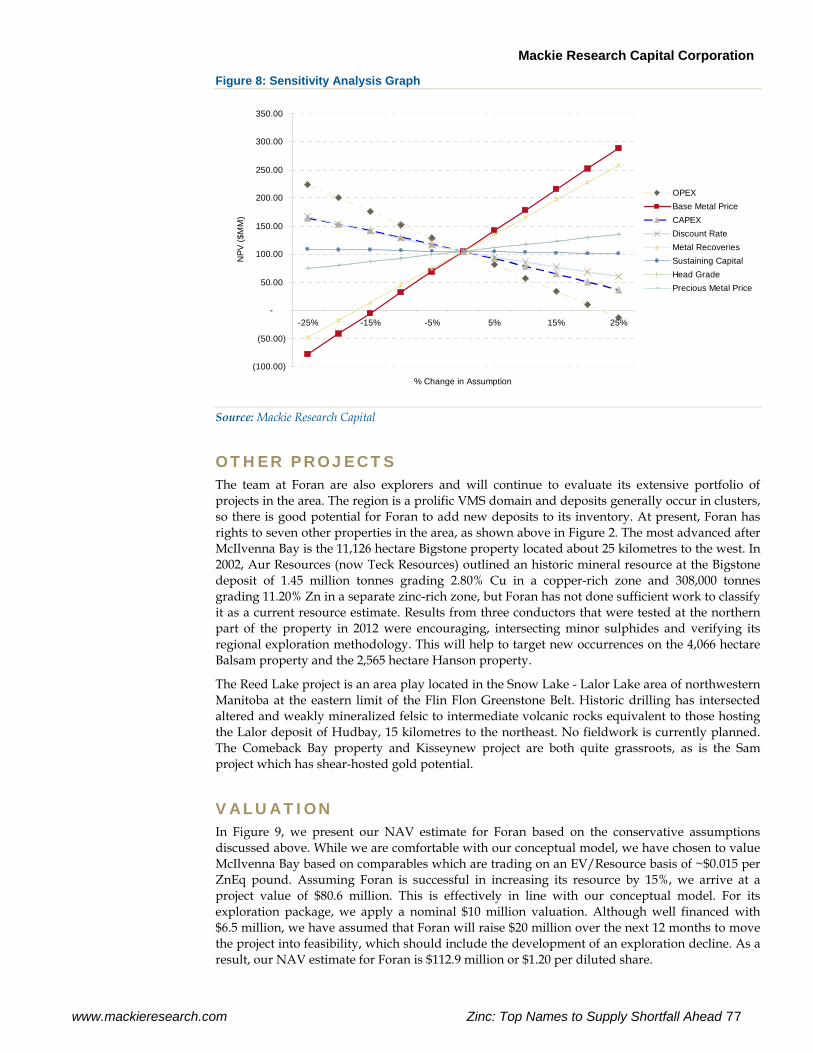

Other Projects .........................................................................................................................................................................................77 Valuation.................................................................................................................................................................................................77 Catalysts...................................................................................................................................................................................................78

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 5

Risks.........................................................................................................................................................................................................78 Conclusion ..............................................................................................................................................................................................79 Management Team & Board ................................................................................................................................................................80 RATHDOWNEY RESOURCES LTD. ................................................................................................................................................83 Introduction ............................................................................................................................................................................................84 Olza Zinc Project - Poland....................................................................................................................................................................85

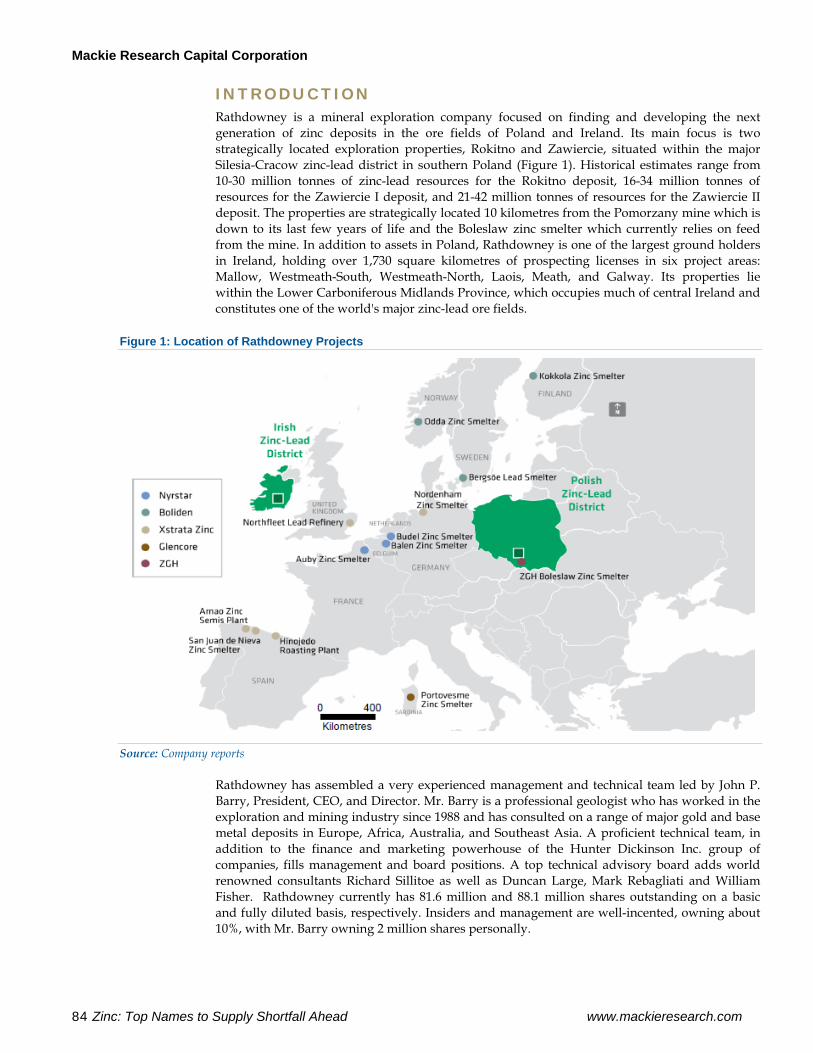

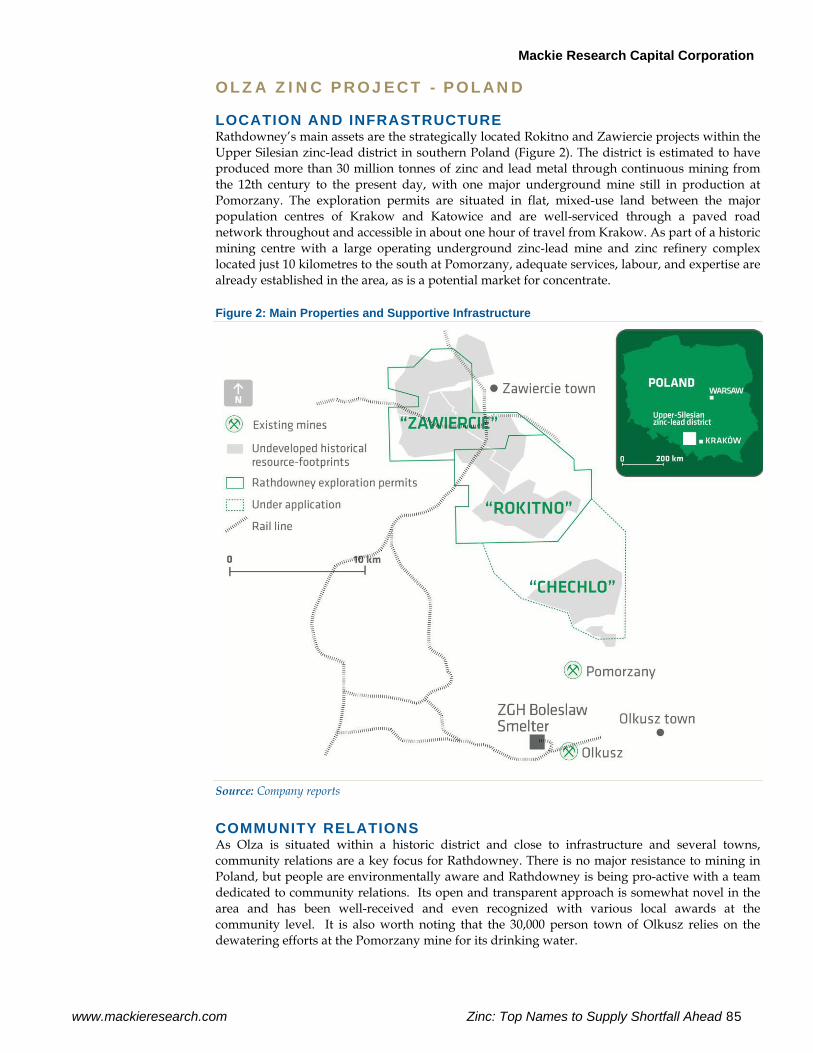

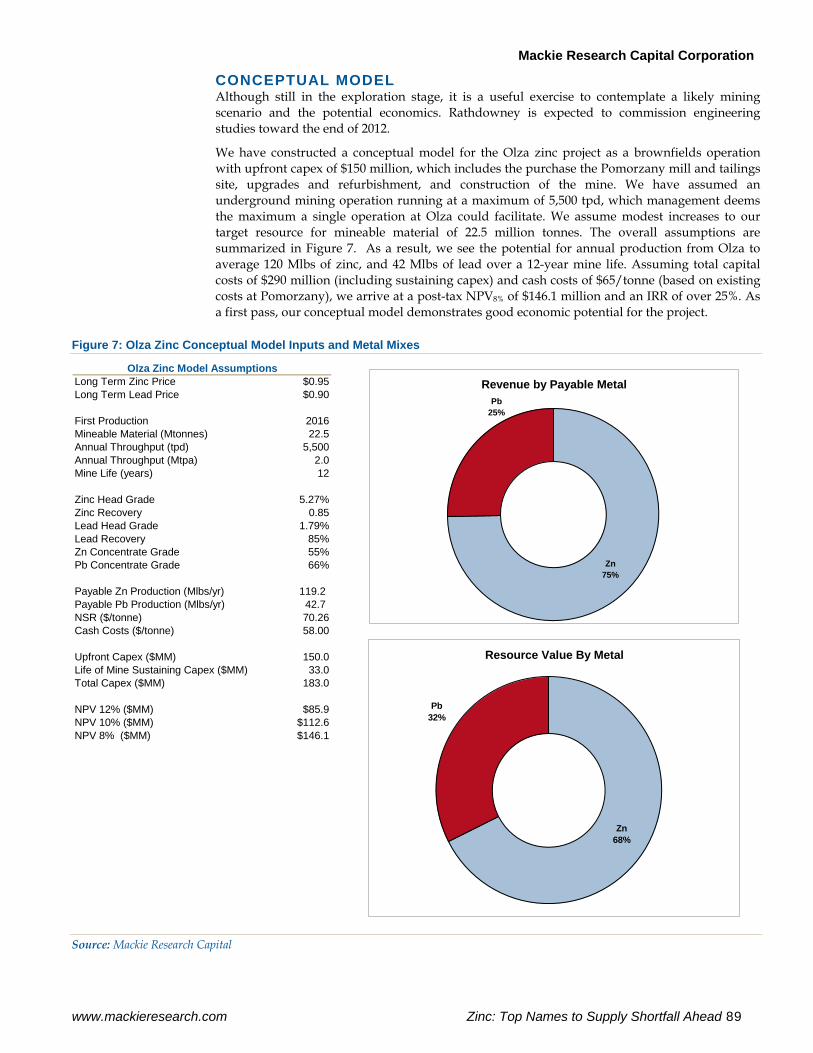

Location And Infrastructure..............................................................................................................................................................85 Community Relations ........................................................................................................................................................................85 History .................................................................................................................................................................................................86 Geology – Classic Mississippi Valley Type.....................................................................................................................................86 Resources – Historic Work Points to Size Potential .......................................................................................................................86 Pomorzany – A Mill & Mine Due to Close......................................................................................................................................88 Conceptual Model ..............................................................................................................................................................................89 Sensitivity Analysis ............................................................................................................................................................................90

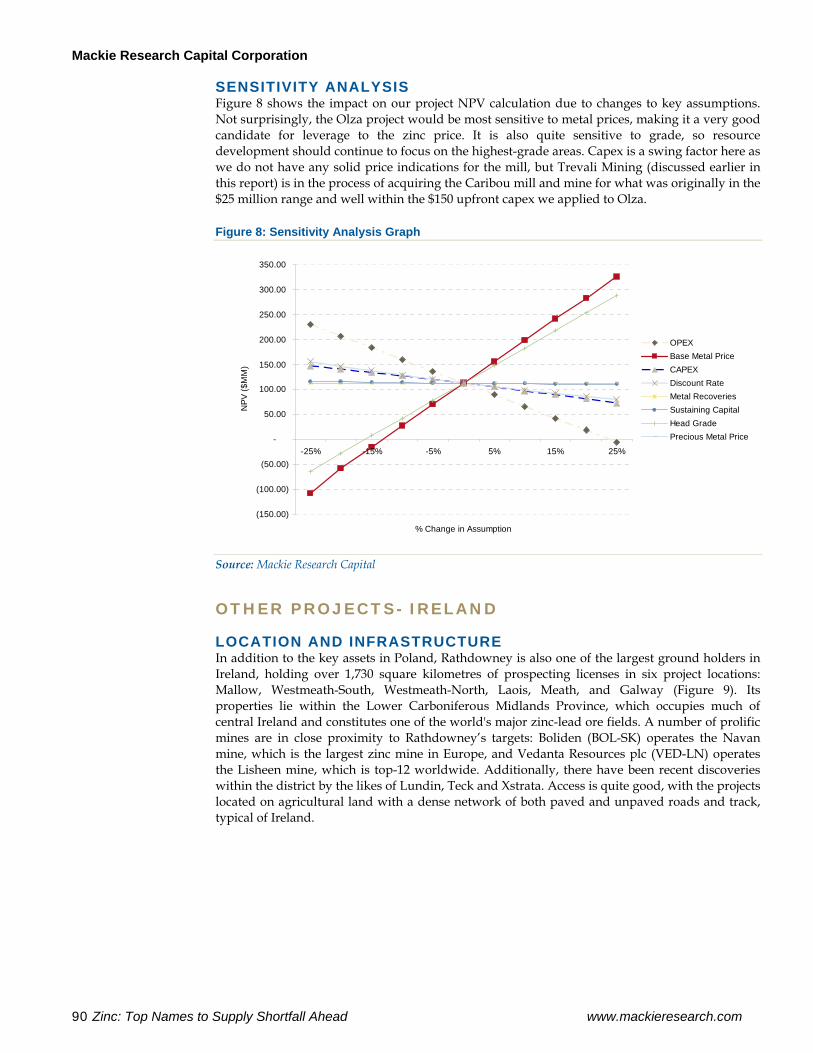

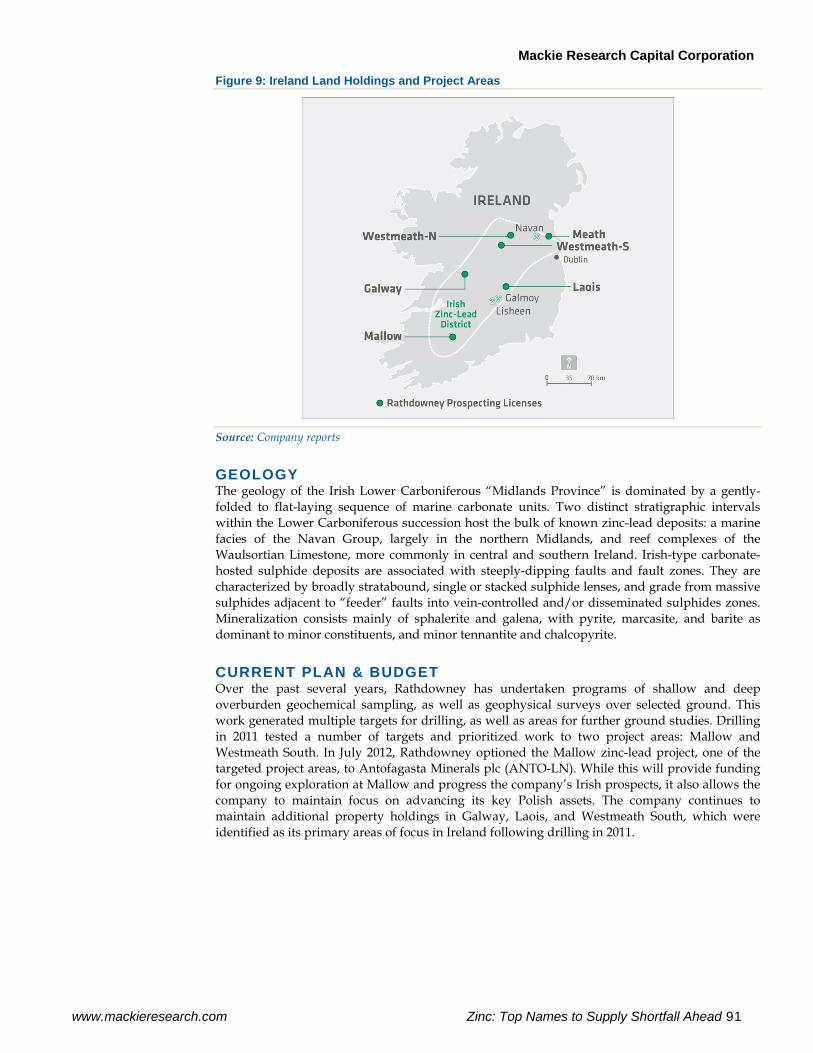

Other Projects- Ireland..........................................................................................................................................................................90 Location And Infrastructure..............................................................................................................................................................90 Geology ................................................................................................................................................................................................91 Current Plan & Budget.......................................................................................................................................................................91

Valuation.................................................................................................................................................................................................92 Catalysts...................................................................................................................................................................................................92 Risks.........................................................................................................................................................................................................93 Conclusion ..............................................................................................................................................................................................93 Management, Technical Team & Board.............................................................................................................................................94 MINING INDUSTRY RISKS ..............................................................................................................................................................96

Commodity Price Risk .......................................................................................................................................................................96 Technical Risk .....................................................................................................................................................................................96 Cost Escalation Risk ...........................................................................................................................................................................96 Financing Risk.....................................................................................................................................................................................96 Regulatory Risk...................................................................................................................................................................................96 Political Risk ........................................................................................................................................................................................96 Exploration Risk..................................................................................................................................................................................96

IMPORTANT DISCLOSURES ...........................................................................................................................................................97 ANALYST CERTIFICATION..............................................................................................................................................................97 Note: All financial figures in this report are in Canadian dollars, unless stated otherwise. Report pricing date: 14-AUG-12

Mackie Research Capital Corporation

6 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

THE ZINC MARKET

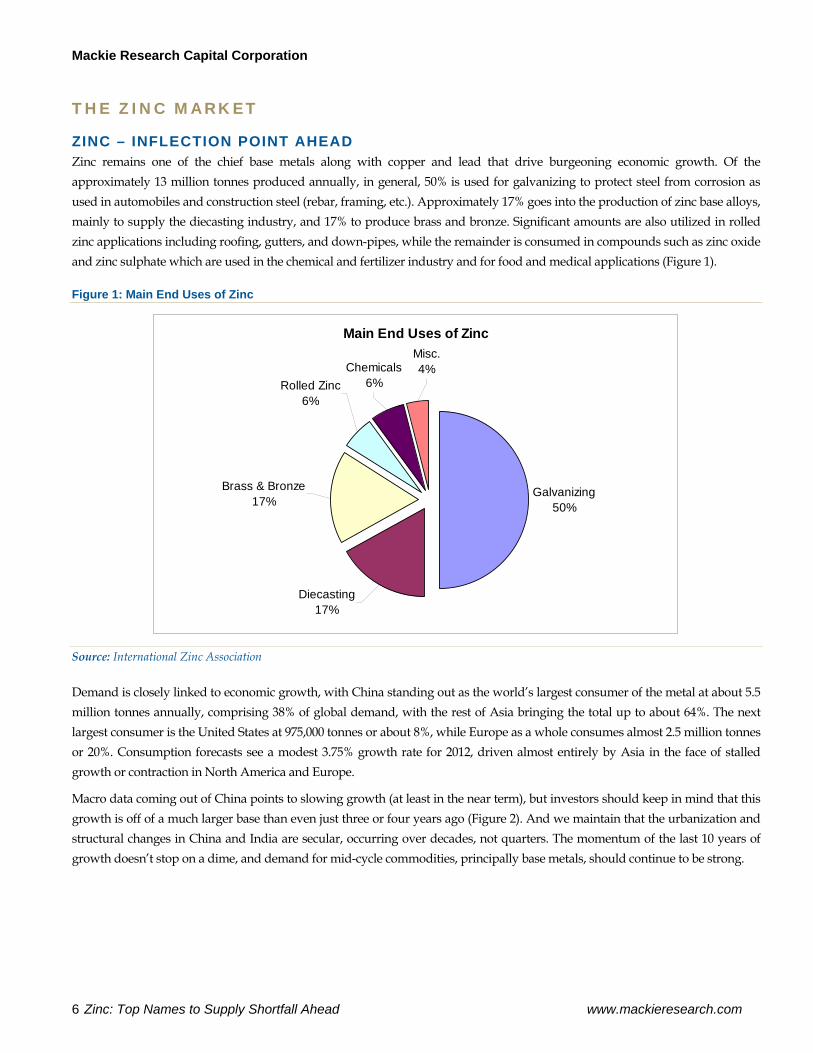

ZINC – INFLECTION POINT AHEAD Zinc remains one of the chief base metals along with copper and lead that drive burgeoning economic growth. Of the approximately 13 million tonnes produced annually, in general, 50% is used for galvanizing to protect steel from corrosion as used in automobiles and construction steel (rebar, framing, etc.). Approximately 17% goes into the production of zinc base alloys, mainly to supply the diecasting industry, and 17% to produce brass and bronze. Significant amounts are also utilized in rolled zinc applications including roofing, gutters, and down-pipes, while the remainder is consumed in compounds such as zinc oxide and zinc sulphate which are used in the chemical and fertilizer industry and for food and medical applications (Figure 1).

Figure 1: Main End Uses of Zinc

Main End Uses of Zinc

Galvanizing50%

Diecasting17%

Misc.4%Chemicals

6%Rolled Zinc6%

Brass & Bronze17%

Source: International Zinc Association

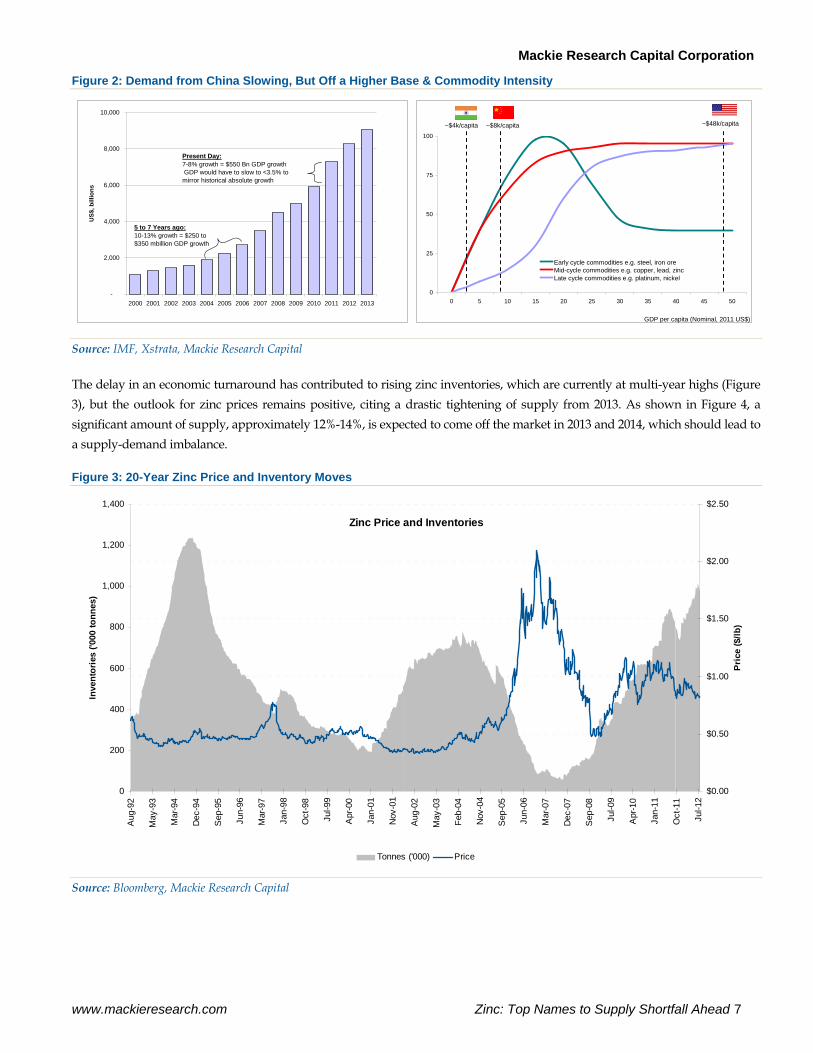

Demand is closely linked to economic growth, with China standing out as the world’s largest consumer of the metal at about 5.5 million tonnes annually, comprising 38% of global demand, with the rest of Asia bringing the total up to about 64%. The next largest consumer is the United States at 975,000 tonnes or about 8%, while Europe as a whole consumes almost 2.5 million tonnes or 20%. Consumption forecasts see a modest 3.75% growth rate for 2012, driven almost entirely by Asia in the face of stalled growth or contraction in North America and Europe.

Macro data coming out of China points to slowing growth (at least in the near term), but investors should keep in mind that this growth is off of a much larger base than even just three or four years ago (Figure 2). And we maintain that the urbanization and structural changes in China and India are secular, occurring over decades, not quarters. The momentum of the last 10 years of growth doesn’t stop on a dime, and demand for mid-cycle commodities, principally base metals, should continue to be strong.

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 7

Figure 2: Demand from China Slowing, But Off a Higher Base & Commodity Intensity

0

25

50

75

100

0 5 10 15 20 25 30 35 40 45 50

Early cycle commodities e.g. steel, iron oreMid-cycle commodities e.g. copper, lead, zincLate cycle commodities e.g. platinum, nickel

~$8k/capita~$4k/capita ~$48k/capita

-

2,000

4,000

6,000

8,000

10,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US$

, bill

ions

GDP per capita (Nominal, 2011 US$)

5 to 7 Years ago:10-13% growth = $250 to $350 mbillion GDP growth

Present Day:7-8% growth = $550 Bn GDP growth GDP would have to slow to <3.5% to mirror historical absolute growth

Source: IMF, Xstrata, Mackie Research Capital

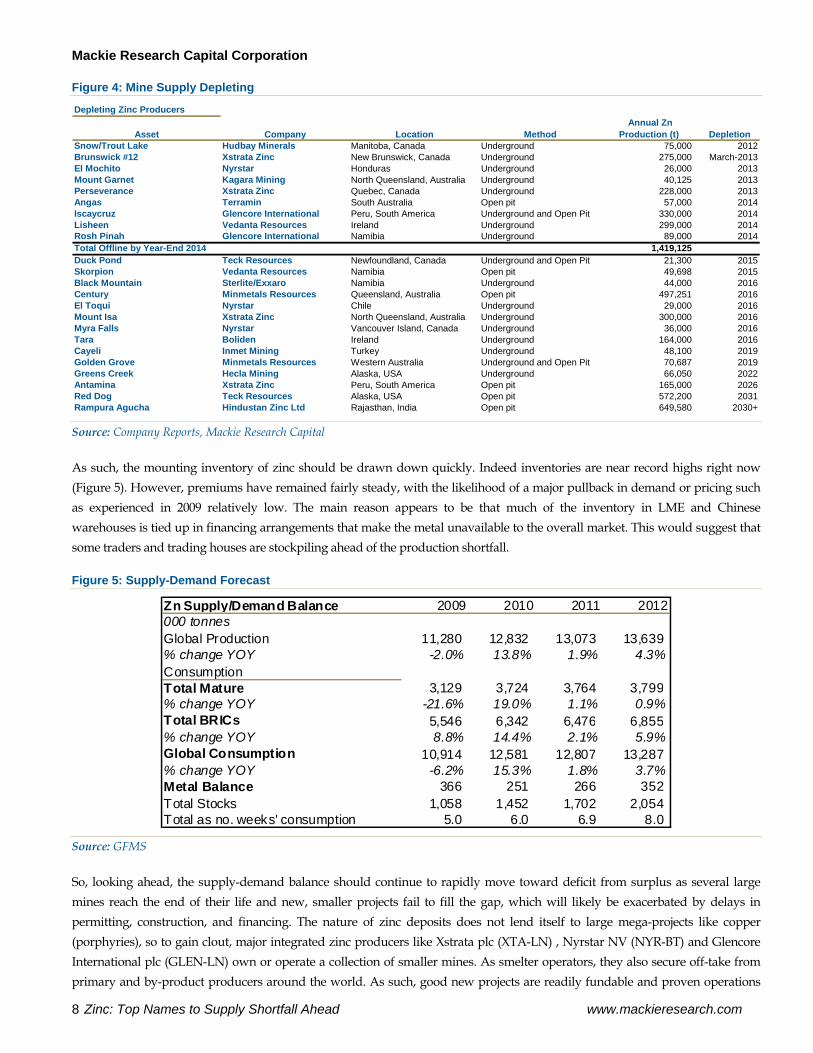

The delay in an economic turnaround has contributed to rising zinc inventories, which are currently at multi-year highs (Figure 3), but the outlook for zinc prices remains positive, citing a drastic tightening of supply from 2013. As shown in Figure 4, a significant amount of supply, approximately 12%-14%, is expected to come off the market in 2013 and 2014, which should lead to a supply-demand imbalance.

Figure 3: 20-Year Zinc Price and Inventory Moves

Zinc Price and Inventories

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

Aug

-92

May

-93

Mar

-94

Dec

-94

Sep

-95

Jun-

96

Mar

-97

Jan-

98

Oct

-98

Jul-9

9

Apr

-00

Jan-

01

Nov

-01

Aug

-02

May

-03

Feb-

04

Nov

-04

Sep

-05

Jun-

06

Mar

-07

Dec

-07

Sep

-08

Jul-0

9

Apr

-10

Jan-

11

Oct

-11

Jul-1

2

Pric

e ($

/lb)

0

200

400

600

800

1,000

1,200

1,400

Inve

ntor

ies

('000

tonn

es)

Tonnes ('000) Price

Source: Bloomberg, Mackie Research Capital

Mackie Research Capital Corporation

8 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

Figure 4: Mine Supply Depleting

Depleting Zinc Producers

Snow/Trout Lake Hudbay Minerals Manitoba, Canada Underground 75,000 2012Brunswick #12 Xstrata Zinc New Brunswick, Canada Underground 275,000 March-2013El Mochito Nyrstar Honduras Underground 26,000 2013Mount Garnet Kagara Mining North Queensland, Australia Underground 40,125 2013Perseverance Xstrata Zinc Quebec, Canada Underground 228,000 2013Angas Terramin South Australia Open pit 57,000 2014Iscaycruz Glencore International Peru, South America Underground and Open Pit 330,000 2014Lisheen Vedanta Resources Ireland Underground 299,000 2014Rosh Pinah Glencore International Namibia Underground 89,000 2014Total Offline by Year-End 2014 1,419,125 Duck Pond Teck Resources Newfoundland, Canada Underground and Open Pit 21,300 2015Skorpion Vedanta Resources Namibia Open pit 49,698 2015Black Mountain Sterlite/Exxaro Namibia Underground 44,000 2016Century Minmetals Resources Queensland, Australia Open pit 497,251 2016El Toqui Nyrstar Chile Underground 29,000 2016Mount Isa Xstrata Zinc North Queensland, Australia Underground 300,000 2016Myra Falls Nyrstar Vancouver Island, Canada Underground 36,000 2016Tara Boliden Ireland Underground 164,000 2016Cayeli Inmet Mining Turkey Underground 48,100 2019Golden Grove Minmetals Resources Western Australia Underground and Open Pit 70,687 2019Greens Creek Hecla Mining Alaska, USA Underground 66,050 2022Antamina Xstrata Zinc Peru, South America Open pit 165,000 2026Red Dog Teck Resources Alaska, USA Open pit 572,200 2031Rampura Agucha Hindustan Zinc Ltd Rajasthan, India Open pit 649,580 2030+

Annual Zn Production (t) Depletion MethodAsset Company Location

Source: Company Reports, Mackie Research Capital

As such, the mounting inventory of zinc should be drawn down quickly. Indeed inventories are near record highs right now (Figure 5). However, premiums have remained fairly steady, with the likelihood of a major pullback in demand or pricing such as experienced in 2009 relatively low. The main reason appears to be that much of the inventory in LME and Chinese warehouses is tied up in financing arrangements that make the metal unavailable to the overall market. This would suggest that some traders and trading houses are stockpiling ahead of the production shortfall.

Figure 5: Supply-Demand Forecast

Zn Supply/Demand Balance 2009 2010 2011 2012000 tonnesGlobal Production 11,280 12,832 13,073 13,639 % change YOY -2.0% 13.8% 1.9% 4.3%ConsumptionTotal Mature 3,129 3,724 3,764 3,799 % change YOY -21.6% 19.0% 1.1% 0.9%Total BRICs 5,546 6,342 6,476 6,855 % change YOY 8.8% 14.4% 2.1% 5.9%Global Consumption 10,914 12,581 12,807 13,287 % change YOY -6.2% 15.3% 1.8% 3.7%Metal Balance 366 251 266 352 Total Stocks 1,058 1,452 1,702 2,054 Total as no. weeks' consumption 5.0 6.0 6.9 8.0

Source: GFMS

So, looking ahead, the supply-demand balance should continue to rapidly move toward deficit from surplus as several large mines reach the end of their life and new, smaller projects fail to fill the gap, which will likely be exacerbated by delays in permitting, construction, and financing. The nature of zinc deposits does not lend itself to large mega-projects like copper (porphyries), so to gain clout, major integrated zinc producers like Xstrata plc (XTA-LN) , Nyrstar NV (NYR-BT) and Glencore International plc (GLEN-LN) own or operate a collection of smaller mines. As smelter operators, they also secure off-take from primary and by-product producers around the world. As such, good new projects are readily fundable and proven operations

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 9

do not last long before being acquired. In the last five years, we have seen several zinc-levered producers be acquired, including Breakwater Resources and Farallon Mining (both acquired by Nyrstar), as well as development projects like Hackett River in Nunavut (discussed further below). Given that the pipeline of projects remains insufficient to meet demand, we would expect to see continued M&A activity driven by cash-rich producers once significantly de-risked.

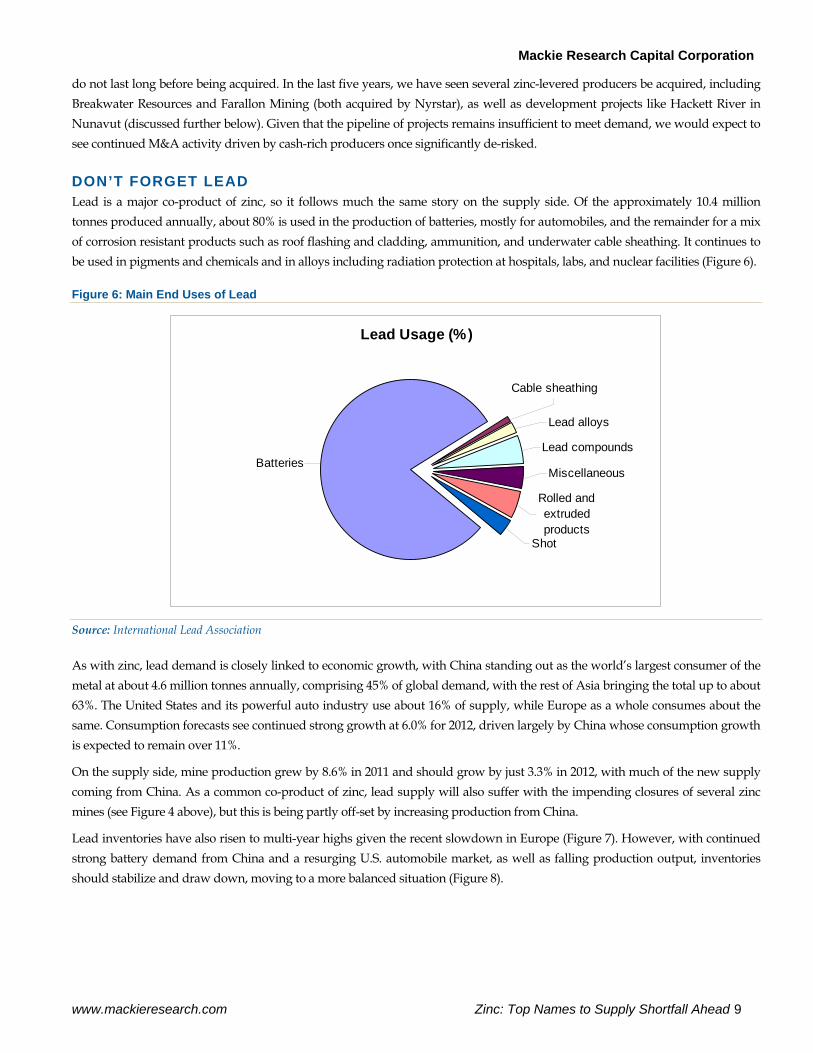

DON’T FORGET LEAD Lead is a major co-product of zinc, so it follows much the same story on the supply side. Of the approximately 10.4 million tonnes produced annually, about 80% is used in the production of batteries, mostly for automobiles, and the remainder for a mix of corrosion resistant products such as roof flashing and cladding, ammunition, and underwater cable sheathing. It continues to be used in pigments and chemicals and in alloys including radiation protection at hospitals, labs, and nuclear facilities (Figure 6).

Figure 6: Main End Uses of Lead

Lead Usage (%)

Rolled and extruded products

Batteries

Lead alloys

Cable sheathing

Lead compounds

Miscellaneous

Shot

Source: International Lead Association

As with zinc, lead demand is closely linked to economic growth, with China standing out as the world’s largest consumer of the metal at about 4.6 million tonnes annually, comprising 45% of global demand, with the rest of Asia bringing the total up to about 63%. The United States and its powerful auto industry use about 16% of supply, while Europe as a whole consumes about the same. Consumption forecasts see continued strong growth at 6.0% for 2012, driven largely by China whose consumption growth is expected to remain over 11%.

On the supply side, mine production grew by 8.6% in 2011 and should grow by just 3.3% in 2012, with much of the new supply coming from China. As a common co-product of zinc, lead supply will also suffer with the impending closures of several zinc mines (see Figure 4 above), but this is being partly off-set by increasing production from China.

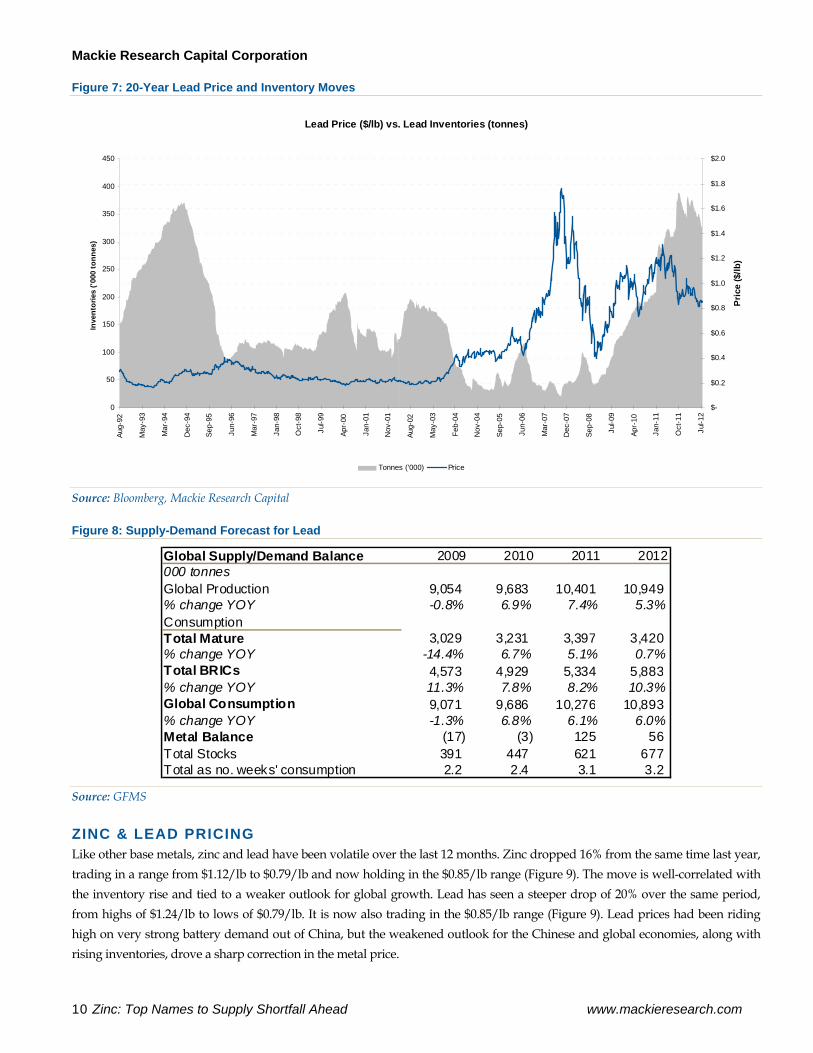

Lead inventories have also risen to multi-year highs given the recent slowdown in Europe (Figure 7). However, with continued strong battery demand from China and a resurging U.S. automobile market, as well as falling production output, inventories should stabilize and draw down, moving to a more balanced situation (Figure 8).

Mackie Research Capital Corporation

10 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

Figure 7: 20-Year Lead Price and Inventory Moves

Lead Price ($/lb) vs. Lead Inventories (tonnes)

$-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

$1.6

$1.8

$2.0

Aug-

92

May

-93

Mar

-94

Dec

-94

Sep-

95

Jun-

96

Mar

-97

Jan-

98

Oct

-98

Jul-9

9

Apr-

00

Jan-

01

Nov

-01

Aug-

02

May

-03

Feb-

04

Nov

-04

Sep-

05

Jun-

06

Mar

-07

Dec

-07

Sep-

08

Jul-0

9

Apr-

10

Jan-

11

Oct

-11

Jul-1

2

Pric

e ($

/lb)

0

50

100

150

200

250

300

350

400

450

Inve

ntor

ies

('000

tonn

es)

Tonnes ('000) Price

Source: Bloomberg, Mackie Research Capital

Figure 8: Supply-Demand Forecast for Lead

Global Supply/Demand Balance 2009 2010 2011 2012000 tonnesGlobal Production 9,054 9,683 10,401 10,949 % change YOY -0.8% 6.9% 7.4% 5.3%ConsumptionTotal Mature 3,029 3,231 3,397 3,420 % change YOY -14.4% 6.7% 5.1% 0.7%Total BRICs 4,573 4,929 5,334 5,883 % change YOY 11.3% 7.8% 8.2% 10.3%Global Consumption 9,071 9,686 10,276 10,893 % change YOY -1.3% 6.8% 6.1% 6.0%Metal Balance (17) (3) 125 56 Total Stocks 391 447 621 677 Total as no. weeks' consumption 2.2 2.4 3.1 3.2

Source: GFMS

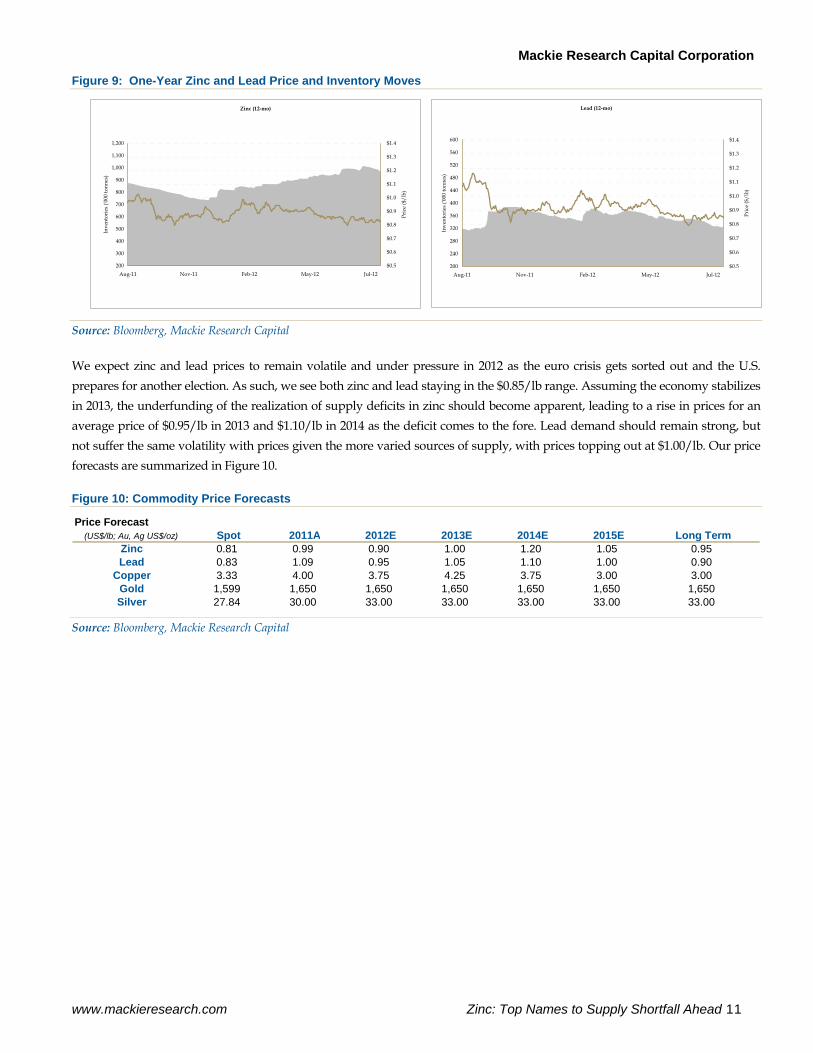

ZINC & LEAD PRICING Like other base metals, zinc and lead have been volatile over the last 12 months. Zinc dropped 16% from the same time last year, trading in a range from $1.12/lb to $0.79/lb and now holding in the $0.85/lb range (Figure 9). The move is well-correlated with the inventory rise and tied to a weaker outlook for global growth. Lead has seen a steeper drop of 20% over the same period, from highs of $1.24/lb to lows of $0.79/lb. It is now also trading in the $0.85/lb range (Figure 9). Lead prices had been riding high on very strong battery demand out of China, but the weakened outlook for the Chinese and global economies, along with rising inventories, drove a sharp correction in the metal price.

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 11

Figure 9: One-Year Zinc and Lead Price and Inventory Moves

Zinc (12-mo)

$0.5

$0.6

$0.7

$0.8

$0.9

$1.0

$1.1

$1.2

$1.3

$1.4

Aug-11 Nov-11 Feb-12 May-12 Jul-12

Pric

e ($

/lb)

200

300

400

500

600

700

800

900

1,000

1,100

1,200

Inve

ntor

ies (

'000

tonn

es)

Lead (12-mo)

$0.5

$0.6

$0.7

$0.8

$0.9

$1.0

$1.1

$1.2

$1.3

$1.4

Aug-11 Nov-11 Feb-12 May-12 Jul-12

Pric

e ($

/lb)

200

240

280

320

360

400

440

480

520

560

600

Inve

ntor

ies (

'000

tonn

es)

Source: Bloomberg, Mackie Research Capital

We expect zinc and lead prices to remain volatile and under pressure in 2012 as the euro crisis gets sorted out and the U.S. prepares for another election. As such, we see both zinc and lead staying in the $0.85/lb range. Assuming the economy stabilizes in 2013, the underfunding of the realization of supply deficits in zinc should become apparent, leading to a rise in prices for an average price of $0.95/lb in 2013 and $1.10/lb in 2014 as the deficit comes to the fore. Lead demand should remain strong, but not suffer the same volatility with prices given the more varied sources of supply, with prices topping out at $1.00/lb. Our price forecasts are summarized in Figure 10.

Figure 10: Commodity Price Forecasts

Price Forecast(US$/lb; Au, Ag US$/oz) Spot 2011A 2012E 2013E 2014E 2015E Long Term

Zinc 0.81 0.99 0.90 1.00 1.20 1.05 0.95Lead 0.83 1.09 0.95 1.05 1.10 1.00 0.90

Copper 3.33 4.00 3.75 4.25 3.75 3.00 3.00Gold 1,599 1,650 1,650 1,650 1,650 1,650 1,650Silver 27.84 30.00 33.00 33.00 33.00 33.00 33.00

Source: Bloomberg, Mackie Research Capital

Mackie Research Capital Corporation

12 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

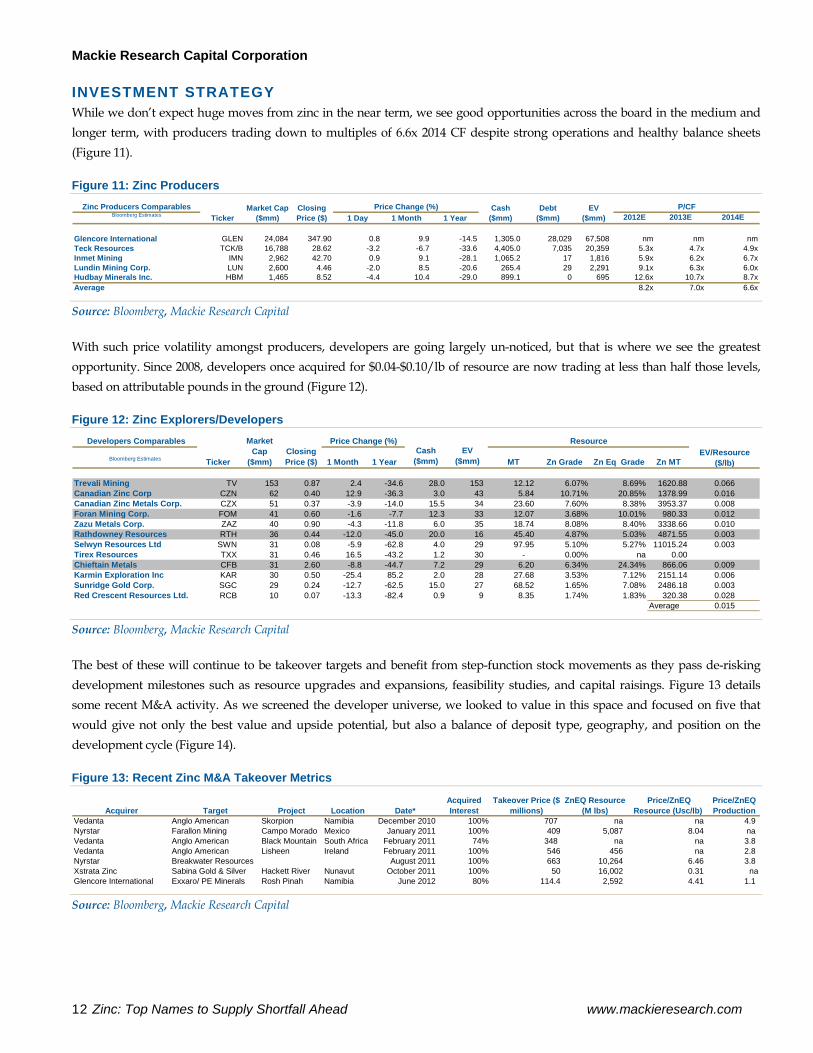

INVESTMENT STRATEGY While we don’t expect huge moves from zinc in the near term, we see good opportunities across the board in the medium and longer term, with producers trading down to multiples of 6.6x 2014 CF despite strong operations and healthy balance sheets (Figure 11).

Figure 11: Zinc Producers Zinc Producers Comparables

Bloomberg Estimates 1 Day 1 Month 1 Year 2012E 2013E 2014E

Glencore International GLEN 24,084 347.90 0.8 9.9 -14.5 1,305.0 28,029 67,508 nm nm nmTeck Resources TCK/B 16,788 28.62 -3.2 -6.7 -33.6 4,405.0 7,035 20,359 5.3x 4.7x 4.9xInmet Mining IMN 2,962 42.70 0.9 9.1 -28.1 1,065.2 17 1,816 5.9x 6.2x 6.7xLundin Mining Corp. LUN 2,600 4.46 -2.0 8.5 -20.6 265.4 29 2,291 9.1x 6.3x 6.0xHudbay Minerals Inc. HBM 1,465 8.52 -4.4 10.4 -29.0 899.1 0 695 12.6x 10.7x 8.7xAverage 8.2x 7.0x 6.6x

P/CFTicker

Market Cap ($mm)

Closing Price ($)

Price Change (%) Cash ($mm)

Debt ($mm)

EV ($mm)

Source: Bloomberg, Mackie Research Capital

With such price volatility amongst producers, developers are going largely un-noticed, but that is where we see the greatest opportunity. Since 2008, developers once acquired for $0.04-$0.10/lb of resource are now trading at less than half those levels, based on attributable pounds in the ground (Figure 12).

Figure 12: Zinc Explorers/Developers Developers Comparables

Bloomberg Estimates 1 Month 1 YearCash

($mm)EV

($mm) MT Zn Grade Zn Eq Grade Zn MTEV/Resource

($/lb)

Trevali Mining TV 153 0.87 2.4 -34.6 28.0 153 12.12 6.07% 8.69% 1620.88 0.066Canadian Zinc Corp CZN 62 0.40 12.9 -36.3 3.0 43 5.84 10.71% 20.85% 1378.99 0.016Canadian Zinc Metals Corp. CZX 51 0.37 -3.9 -14.0 15.5 34 23.60 7.60% 8.38% 3953.37 0.008Foran Mining Corp. FOM 41 0.60 -1.6 -7.7 12.3 33 12.07 3.68% 10.01% 980.33 0.012Zazu Metals Corp. ZAZ 40 0.90 -4.3 -11.8 6.0 35 18.74 8.08% 8.40% 3338.66 0.010Rathdowney Resources RTH 36 0.44 -12.0 -45.0 20.0 16 45.40 4.87% 5.03% 4871.55 0.003Selwyn Resources Ltd SWN 31 0.08 -5.9 -62.8 4.0 29 97.95 5.10% 5.27% 11015.24 0.003Tirex Resources TXX 31 0.46 16.5 -43.2 1.2 30 - 0.00% na 0.00Chieftain Metals CFB 31 2.60 -8.8 -44.7 7.2 29 6.20 6.34% 24.34% 866.06 0.009Karmin Exploration Inc KAR 30 0.50 -25.4 85.2 2.0 28 27.68 3.53% 7.12% 2151.14 0.006Sunridge Gold Corp. SGC 29 0.24 -12.7 -62.5 15.0 27 68.52 1.65% 7.08% 2486.18 0.003Red Crescent Resources Ltd. RCB 10 0.07 -13.3 -82.4 0.9 9 8.35 1.74% 1.83% 320.38 0.028

Average 0.015

Price Change (%) Resource

Ticker

Market Cap

($mm)Closing Price ($)

Source: Bloomberg, Mackie Research Capital

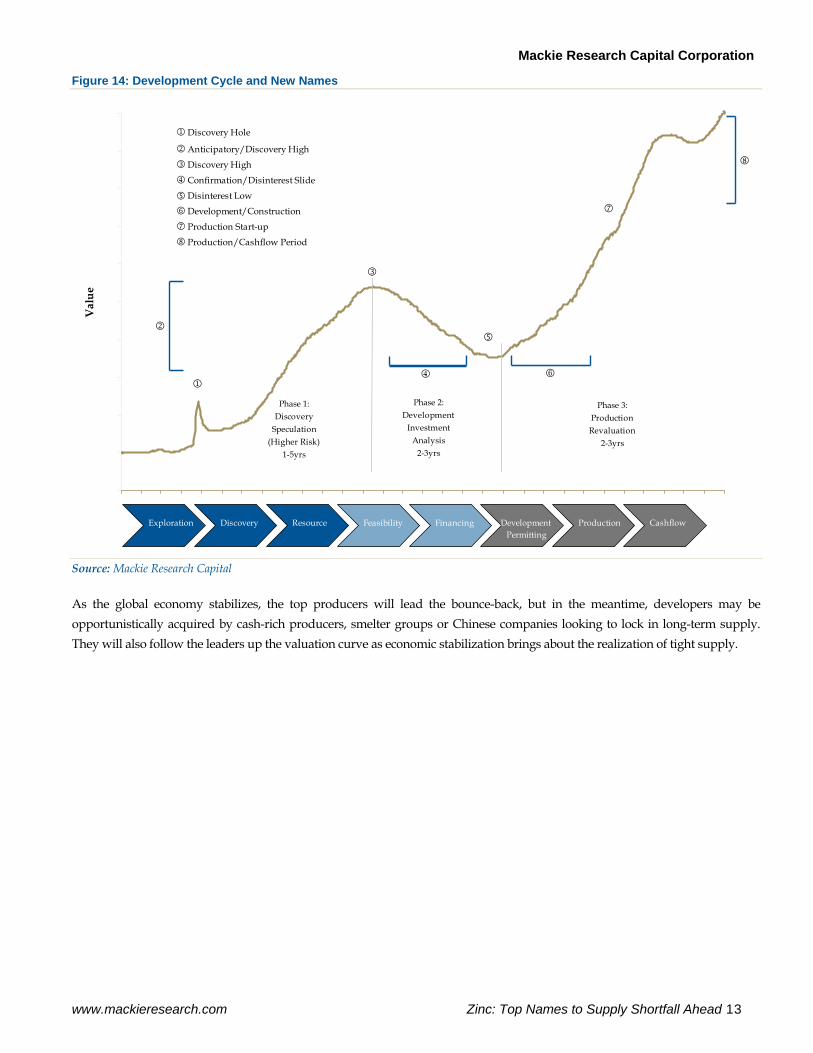

The best of these will continue to be takeover targets and benefit from step-function stock movements as they pass de-risking development milestones such as resource upgrades and expansions, feasibility studies, and capital raisings. Figure 13 details some recent M&A activity. As we screened the developer universe, we looked to value in this space and focused on five that would give not only the best value and upside potential, but also a balance of deposit type, geography, and position on the development cycle (Figure 14).

Figure 13: Recent Zinc M&A Takeover Metrics

Vedanta Anglo American Skorpion Namibia December 2010 100% 707 na na 4.9 Nyrstar Farallon Mining Campo Morado Mexico January 2011 100% 409 5,087 8.04 naVedanta Anglo American Black Mountain South Africa February 2011 74% 348 na na 3.8 Vedanta Anglo American Lisheen Ireland February 2011 100% 546 456 na 2.8 Nyrstar Breakwater Resources August 2011 100% 663 10,264 6.46 3.8 Xstrata Zinc Sabina Gold & Silver Hackett River Nunavut October 2011 100% 50 16,002 0.31 naGlencore International Exxaro/ PE Minerals Rosh Pinah Namibia June 2012 80% 114.4 2,592 4.41 1.1

Price/ZnEQ ProductionAcquirer ProjectTarget Date*

Acquired InterestLocation

Takeover Price ($ millions)

Price/ZnEQ Resource (Usc/lb)

ZnEQ Resource (M lbs)

Source: Bloomberg, Mackie Research Capital

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 13

Figure 14: Development Cycle and New Names

0

1

2

3

4

5

6

7

8

9

10

Val

ue

Phase 1:Discovery

Speculation (Higher Risk)

1-5yrs

Phase 2:Development

Investment Analysis

2-3yrs

Phase 3:ProductionRevaluation

2-3yrs

1

2

3

4

7

8

1 Discovery Hole

2 Anticipatory/Discovery High

3 Discovery High

4 Confirmation/Disinterest Slide Disinterest Low

6 Development/Construction

7 Production Start-up

8 Production/Cashflow Period

6

Exploration Discovery Resource Feasibility Financing Development Permitting

Production Cashflow

Source: Mackie Research Capital

As the global economy stabilizes, the top producers will lead the bounce-back, but in the meantime, developers may be opportunistically acquired by cash-rich producers, smelter groups or Chinese companies looking to lock in long-term supply. They will also follow the leaders up the valuation curve as economic stabilization brings about the realization of tight supply.

Mackie Research Capital Corporation

14 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

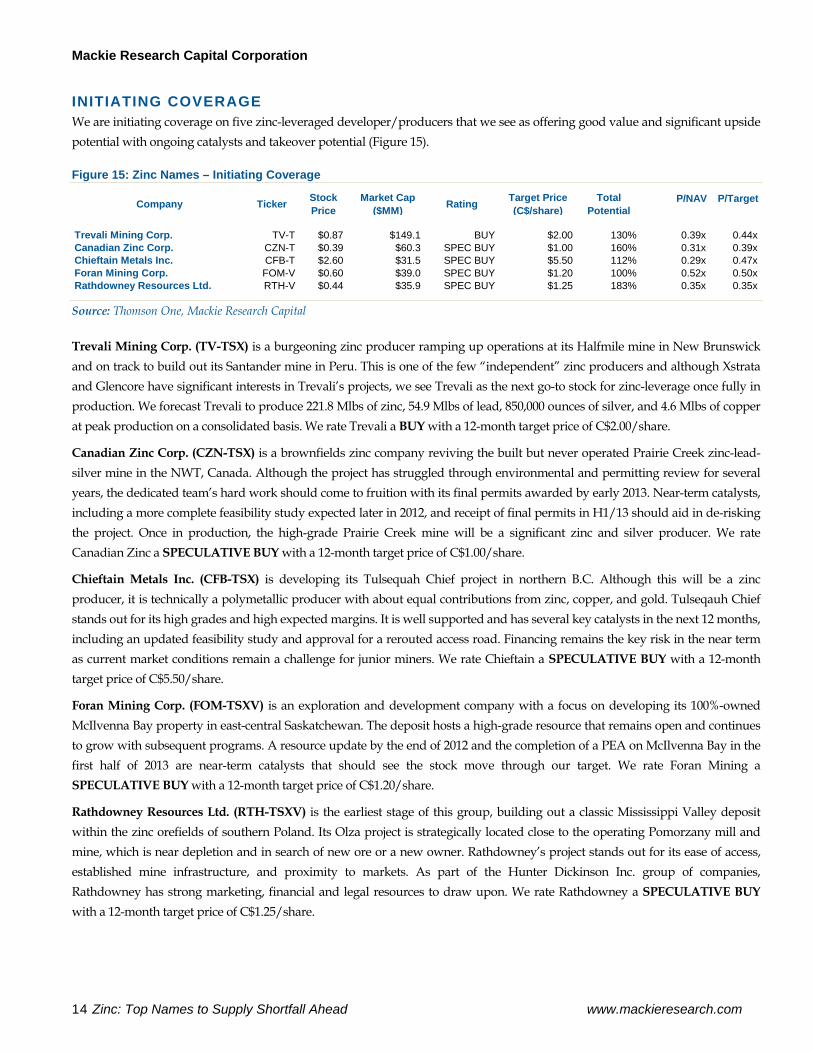

INITIATING COVERAGE We are initiating coverage on five zinc-leveraged developer/producers that we see as offering good value and significant upside potential with ongoing catalysts and takeover potential (Figure 15).

Figure 15: Zinc Names – Initiating Coverage

Company Ticker Stock Price

Market Cap ($MM) Rating Target Price

(C$/share)Total

Potential P/NAV P/Target

Trevali Mining Corp. TV-T $0.87 $149.1 BUY $2.00 130% 0.39x 0.44xCanadian Zinc Corp. CZN-T $0.39 $60.3 SPEC BUY $1.00 160% 0.31x 0.39xChieftain Metals Inc. CFB-T $2.60 $31.5 SPEC BUY $5.50 112% 0.29x 0.47xForan Mining Corp. FOM-V $0.60 $39.0 SPEC BUY $1.20 100% 0.52x 0.50xRathdowney Resources Ltd. RTH-V $0.44 $35.9 SPEC BUY $1.25 183% 0.35x 0.35x Source: Thomson One, Mackie Research Capital

Trevali Mining Corp. (TV-TSX) is a burgeoning zinc producer ramping up operations at its Halfmile mine in New Brunswick and on track to build out its Santander mine in Peru. This is one of the few “independent” zinc producers and although Xstrata and Glencore have significant interests in Trevali’s projects, we see Trevali as the next go-to stock for zinc-leverage once fully in production. We forecast Trevali to produce 221.8 Mlbs of zinc, 54.9 Mlbs of lead, 850,000 ounces of silver, and 4.6 Mlbs of copper at peak production on a consolidated basis. We rate Trevali a BUY with a 12-month target price of C$2.00/share.

Canadian Zinc Corp. (CZN-TSX) is a brownfields zinc company reviving the built but never operated Prairie Creek zinc-lead-silver mine in the NWT, Canada. Although the project has struggled through environmental and permitting review for several years, the dedicated team’s hard work should come to fruition with its final permits awarded by early 2013. Near-term catalysts, including a more complete feasibility study expected later in 2012, and receipt of final permits in H1/13 should aid in de-risking the project. Once in production, the high-grade Prairie Creek mine will be a significant zinc and silver producer. We rate Canadian Zinc a SPECULATIVE BUY with a 12-month target price of C$1.00/share.

Chieftain Metals Inc. (CFB-TSX) is developing its Tulsequah Chief project in northern B.C. Although this will be a zinc producer, it is technically a polymetallic producer with about equal contributions from zinc, copper, and gold. Tulseqauh Chief stands out for its high grades and high expected margins. It is well supported and has several key catalysts in the next 12 months, including an updated feasibility study and approval for a rerouted access road. Financing remains the key risk in the near term as current market conditions remain a challenge for junior miners. We rate Chieftain a SPECULATIVE BUY with a 12-month target price of C$5.50/share.

Foran Mining Corp. (FOM-TSXV) is an exploration and development company with a focus on developing its 100%-owned McIlvenna Bay property in east-central Saskatchewan. The deposit hosts a high-grade resource that remains open and continues to grow with subsequent programs. A resource update by the end of 2012 and the completion of a PEA on McIlvenna Bay in the first half of 2013 are near-term catalysts that should see the stock move through our target. We rate Foran Mining a SPECULATIVE BUY with a 12-month target price of C$1.20/share.

Rathdowney Resources Ltd. (RTH-TSXV) is the earliest stage of this group, building out a classic Mississippi Valley deposit within the zinc orefields of southern Poland. Its Olza project is strategically located close to the operating Pomorzany mill and mine, which is near depletion and in search of new ore or a new owner. Rathdowney’s project stands out for its ease of access, established mine infrastructure, and proximity to markets. As part of the Hunter Dickinson Inc. group of companies, Rathdowney has strong marketing, financial and legal resources to draw upon. We rate Rathdowney a SPECULATIVE BUY with a 12-month target price of C$1.25/share.

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 15

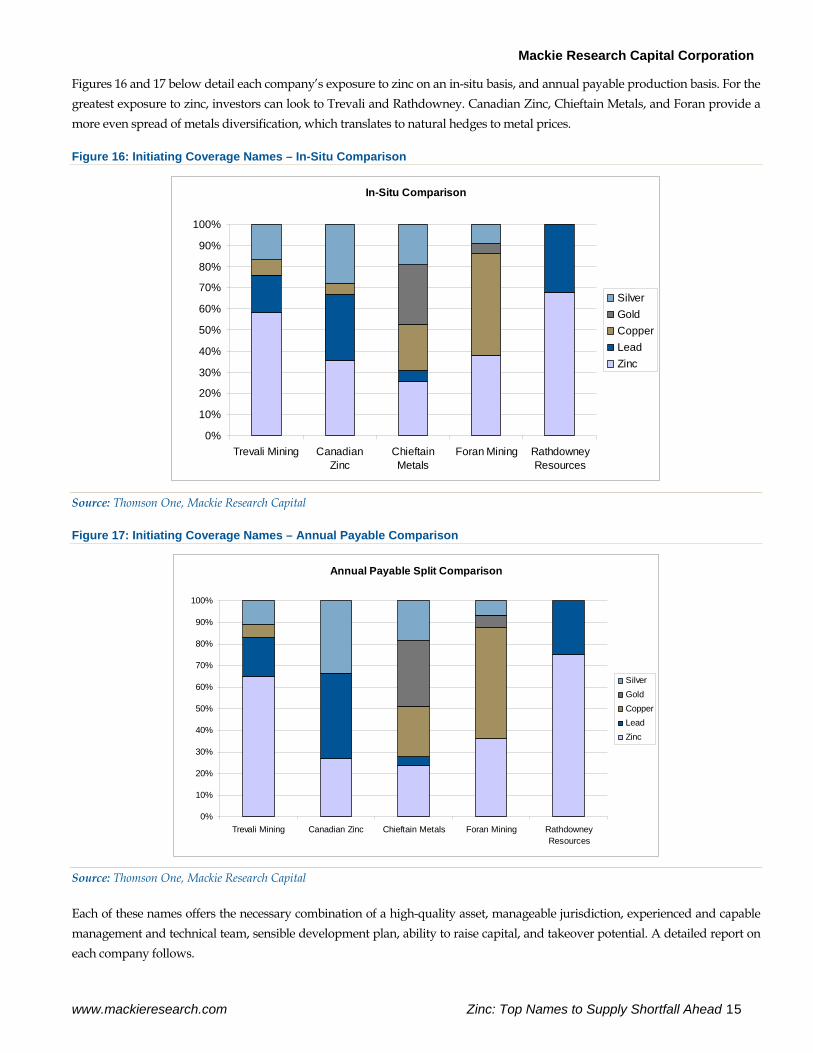

Figures 16 and 17 below detail each company’s exposure to zinc on an in-situ basis, and annual payable production basis. For the greatest exposure to zinc, investors can look to Trevali and Rathdowney. Canadian Zinc, Chieftain Metals, and Foran provide a more even spread of metals diversification, which translates to natural hedges to metal prices.

Figure 16: Initiating Coverage Names – In-Situ Comparison

In-Situ Comparison

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Trevali Mining CanadianZinc

ChieftainMetals

Foran Mining RathdowneyResources

SilverGoldCopperLeadZinc

Source: Thomson One, Mackie Research Capital

Figure 17: Initiating Coverage Names – Annual Payable Comparison

Annual Payable Split Comparison

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Trevali Mining Canadian Zinc Chieftain Metals Foran Mining RathdowneyResources

SilverGoldCopperLeadZinc

Source: Thomson One, Mackie Research Capital

Each of these names offers the necessary combination of a high-quality asset, manageable jurisdiction, experienced and capable management and technical team, sensible development plan, ability to raise capital, and takeover potential. A detailed report on each company follows.

Mackie Research Capital Corporation

16 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

This page left intentionally blank.

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 17

I N V E S T M E N T H I G H L I G H T S

TREVALI MINING CORP. Burgeoning Zinc Producer in Established Mining Camps

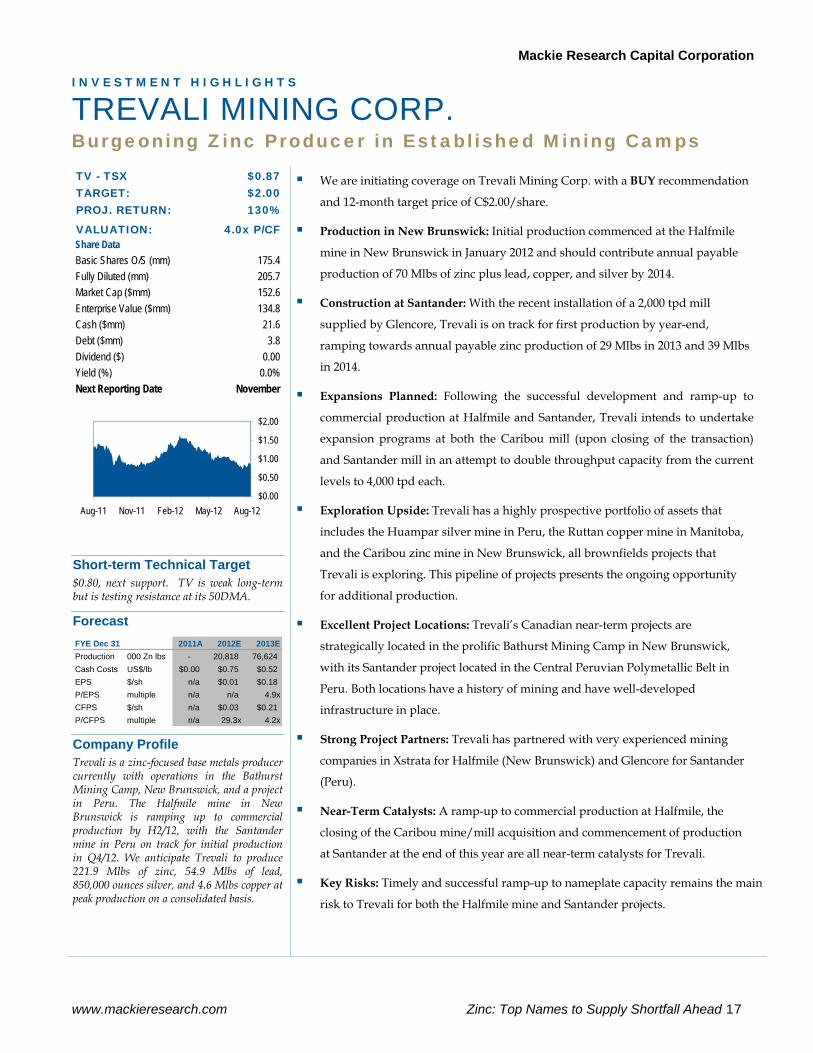

TV - TSX $0.87TARGET: $2.00PROJ. RETURN: 130%

VALUATION: 4.0x P/CFShare DataBasic Shares O/S (mm) 175.4Fully Diluted (mm) 205.7Market Cap ($mm) 152.6Enterprise Value ($mm) 134.8Cash ($mm) 21.6Debt ($mm) 3.8Dividend ($) 0.00Yield (%) 0.0%Next Reporting Date November

$0.00

$0.50

$1.00

$1.50

$2.00

Aug-11 Nov-11 Feb-12 May-12 Aug-12

Short-term Technical Target $0.80, next support. TV is weak long-term but is testing resistance at its 50DMA.

Forecast FYE Dec 31 2011A 2012E 2013EProduction 000 Zn lbs - 20,818 76,624 Cash Costs US$/lb $0.00 $0.75 $0.52EPS $/sh n/a $0.01 $0.18P/EPS multiple n/a n/a 4.9xCFPS $/sh n/a $0.03 $0.21P/CFPS multiple n/a 29.3x 4.2x

Company Profile Trevali is a zinc-focused base metals producer currently with operations in the Bathurst Mining Camp, New Brunswick, and a project in Peru. The Halfmile mine in New Brunswick is ramping up to commercial production by H2/12, with the Santander mine in Peru on track for initial production in Q4/12. We anticipate Trevali to produce 221.9 Mlbs of zinc, 54.9 Mlbs of lead, 850,000 ounces silver, and 4.6 Mlbs copper at peak production on a consolidated basis.

We are initiating coverage on Trevali Mining Corp. with a BUY recommendation

and 12-month target price of C$2.00/share.

Production in New Brunswick: Initial production commenced at the Halfmile

mine in New Brunswick in January 2012 and should contribute annual payable

production of 70 Mlbs of zinc plus lead, copper, and silver by 2014.

Construction at Santander: With the recent installation of a 2,000 tpd mill

supplied by Glencore, Trevali is on track for first production by year-end,

ramping towards annual payable zinc production of 29 Mlbs in 2013 and 39 Mlbs

in 2014.

Expansions Planned: Following the successful development and ramp-up to

commercial production at Halfmile and Santander, Trevali intends to undertake

expansion programs at both the Caribou mill (upon closing of the transaction)

and Santander mill in an attempt to double throughput capacity from the current

levels to 4,000 tpd each.

Exploration Upside: Trevali has a highly prospective portfolio of assets that

includes the Huampar silver mine in Peru, the Ruttan copper mine in Manitoba,

and the Caribou zinc mine in New Brunswick, all brownfields projects that

Trevali is exploring. This pipeline of projects presents the ongoing opportunity

for additional production.

Excellent Project Locations: Trevali’s Canadian near-term projects are

strategically located in the prolific Bathurst Mining Camp in New Brunswick,

with its Santander project located in the Central Peruvian Polymetallic Belt in

Peru. Both locations have a history of mining and have well-developed

infrastructure in place.

Strong Project Partners: Trevali has partnered with very experienced mining

companies in Xstrata for Halfmile (New Brunswick) and Glencore for Santander

(Peru).

Near-Term Catalysts: A ramp-up to commercial production at Halfmile, the

closing of the Caribou mine/mill acquisition and commencement of production

at Santander at the end of this year are all near-term catalysts for Trevali.

Key Risks: Timely and successful ramp-up to nameplate capacity remains the main

risk to Trevali for both the Halfmile mine and Santander projects.

Mackie Research Capital Corporation

18 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

INTRODUCTION

COMPANY PROFILE Trevali Mining Corp. is a Vancouver-headquartered, zinc-focused base metals miner currently advancing two polymetallic zinc deposits in Canada and Peru towards commercial production (Figure 1). In Canada, Trevali owns the Halfmile zinc-lead-silver mine and Stratmat polymetallic deposit located in the Bathurst Mining Camp of northern New Brunswick. Additionally, the company owns the past-producing Ruttan copper-zinc mine in Manitoba. Halfmile commenced production in January 2012 and is presently ramping up to a production capacity of 2,000 tpd. To move away from the current toll treatment arrangement with Xstrata, Trevali recently entered into a definitive combination agreement to acquire the Caribou milling and mine complex located in close proximity to Halfmile and Stratmat. The deal should close by year-end, with management forecasting in-house milling by mid-2013.

In Peru, Trevali owns the Santander zinc-lead-silver mine and the past-producing Huampar silver mine, both of which are located in the Central Peruvian Polymetallic Belt. Mine construction is currently on track at Santander, with initial production anticipated from the Magistral deposits at the end of 2012. Trevali anticipates a production ramp-up to 2,000 tpd in 2013. The company also owns the Tingo run-of-river hydroelectric generating facility in Peru, located 17 kilometres from its Santander mine. Trevali plans a significant upgrade of the facility, with the goal of providing cheap power for operations at Santander.

Figure 1: Trevali Project Locations (North and South America)

Source: Company presentation

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 19

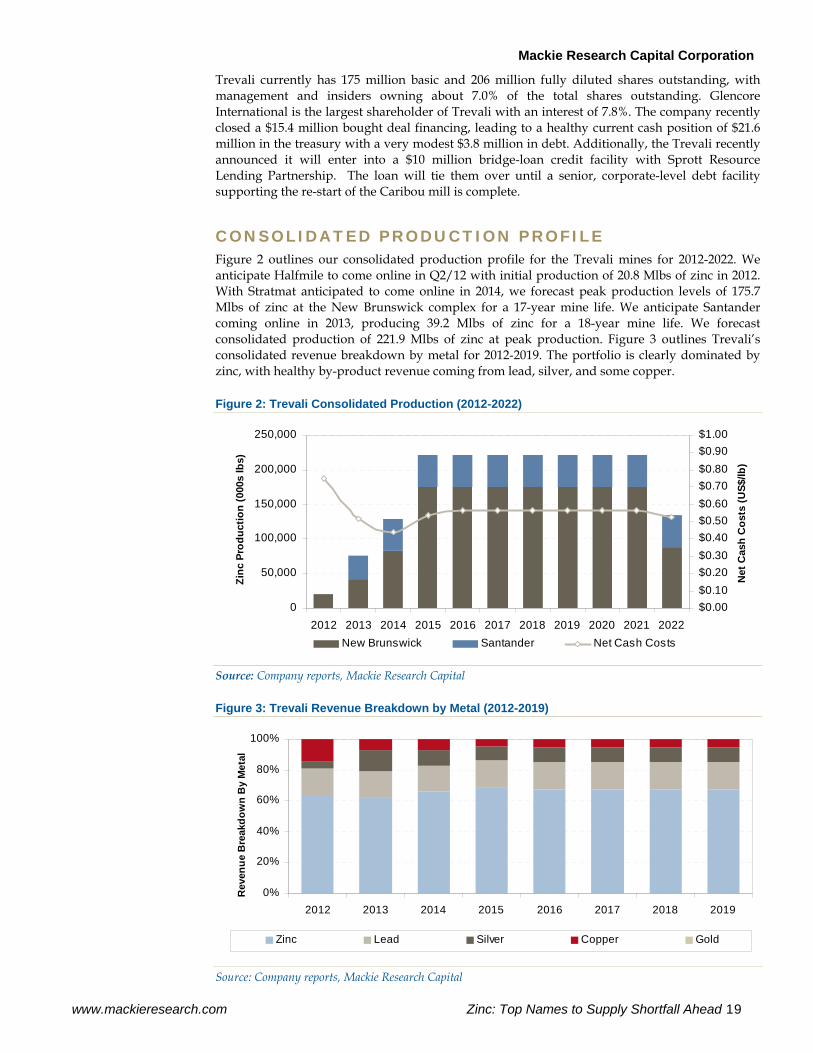

Trevali currently has 175 million basic and 206 million fully diluted shares outstanding, with management and insiders owning about 7.0% of the total shares outstanding. Glencore International is the largest shareholder of Trevali with an interest of 7.8%. The company recently closed a $15.4 million bought deal financing, leading to a healthy current cash position of $21.6 million in the treasury with a very modest $3.8 million in debt. Additionally, the Trevali recently announced it will enter into a $10 million bridge-loan credit facility with Sprott Resource Lending Partnership. The loan will tie them over until a senior, corporate-level debt facility supporting the re-start of the Caribou mill is complete.

CONSOLIDATED PRODUCTION PROFILE Figure 2 outlines our consolidated production profile for the Trevali mines for 2012-2022. We anticipate Halfmile to come online in Q2/12 with initial production of 20.8 Mlbs of zinc in 2012. With Stratmat anticipated to come online in 2014, we forecast peak production levels of 175.7 Mlbs of zinc at the New Brunswick complex for a 17-year mine life. We anticipate Santander coming online in 2013, producing 39.2 Mlbs of zinc for a 18-year mine life. We forecast consolidated production of 221.9 Mlbs of zinc at peak production. Figure 3 outlines Trevali’s consolidated revenue breakdown by metal for 2012-2019. The portfolio is clearly dominated by zinc, with healthy by-product revenue coming from lead, silver, and some copper.

Figure 2: Trevali Consolidated Production (2012-2022)

0

50,000

100,000

150,000

200,000

250,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Zinc

Pro

duct

ion

(000

s lb

s)

$0.00$0.10$0.20$0.30$0.40$0.50$0.60$0.70$0.80$0.90$1.00

Net

Cas

h C

osts

(US$

/lb)

New Brunswick Santander Net Cash Costs

Source: Company reports, Mackie Research Capital

Figure 3: Trevali Revenue Breakdown by Metal (2012-2019)

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016 2017 2018 2019

Rev

enue

Bre

akdo

wn

By

Met

al

Zinc Lead Silver Copper Gold

Source: Company reports, Mackie Research Capital

Mackie Research Capital Corporation

20 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

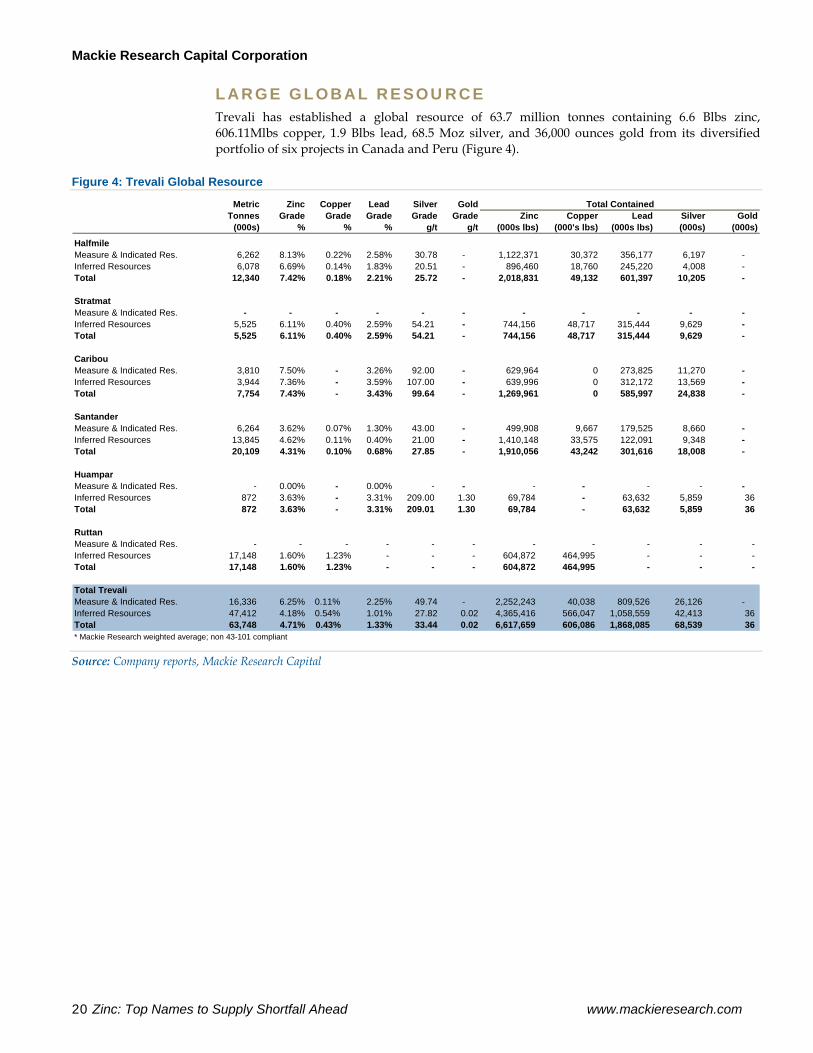

LARGE GLOBAL RESOURCE Trevali has established a global resource of 63.7 million tonnes containing 6.6 Blbs zinc, 606.11Mlbs copper, 1.9 Blbs lead, 68.5 Moz silver, and 36,000 ounces gold from its diversified portfolio of six projects in Canada and Peru (Figure 4).

Figure 4: Trevali Global Resource

Metric Zinc Copper Lead Silver GoldTonnes Grade Grade Grade Grade Grade Zinc Copper Lead Silver Gold

(000s) % % % g/t g/t (000s lbs) (000's lbs) (000s lbs) (000s) (000s)

HalfmileMeasure & Indicated Res. 6,262 8.13% 0.22% 2.58% 30.78 - 1,122,371 30,372 356,177 6,197 - Inferred Resources 6,078 6.69% 0.14% 1.83% 20.51 - 896,460 18,760 245,220 4,008 - Total 12,340 7.42% 0.18% 2.21% 25.72 - 2,018,831 49,132 601,397 10,205 -

StratmatMeasure & Indicated Res. - - - - - - - - - - - Inferred Resources 5,525 6.11% 0.40% 2.59% 54.21 - 744,156 48,717 315,444 9,629 - Total 5,525 6.11% 0.40% 2.59% 54.21 - 744,156 48,717 315,444 9,629 -

CaribouMeasure & Indicated Res. 3,810 7.50% - 3.26% 92.00 - 629,964 0 273,825 11,270 - Inferred Resources 3,944 7.36% - 3.59% 107.00 - 639,996 0 312,172 13,569 - Total 7,754 7.43% - 3.43% 99.64 - 1,269,961 0 585,997 24,838 -

SantanderMeasure & Indicated Res. 6,264 3.62% 0.07% 1.30% 43.00 - 499,908 9,667 179,525 8,660 - Inferred Resources 13,845 4.62% 0.11% 0.40% 21.00 - 1,410,148 33,575 122,091 9,348 - Total 20,109 4.31% 0.10% 0.68% 27.85 - 1,910,056 43,242 301,616 18,008 -

HuamparMeasure & Indicated Res. - 0.00% - 0.00% - - - - - - - Inferred Resources 872 3.63% - 3.31% 209.00 1.30 69,784 - 63,632 5,859 36 Total 872 3.63% - 3.31% 209.01 1.30 69,784 - 63,632 5,859 36

RuttanMeasure & Indicated Res. - - - - - - - - - - - Inferred Resources 17,148 1.60% 1.23% - - - 604,872 464,995 - - - Total 17,148 1.60% 1.23% - - - 604,872 464,995 - - -

Total TrevaliMeasure & Indicated Res. 16,336 6.25% 0.11% 2.25% 49.74 - 2,252,243 40,038 809,526 26,126 - Inferred Resources 47,412 4.18% 0.54% 1.01% 27.82 0.02 4,365,416 566,047 1,058,559 42,413 36 Total 63,748 4.71% 0.43% 1.33% 33.44 0.02 6,617,659 606,086 1,868,085 68,539 36 * Mackie Research weighted average; non 43-101 compliant

Total Contained

Source: Company reports, Mackie Research Capital

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 21

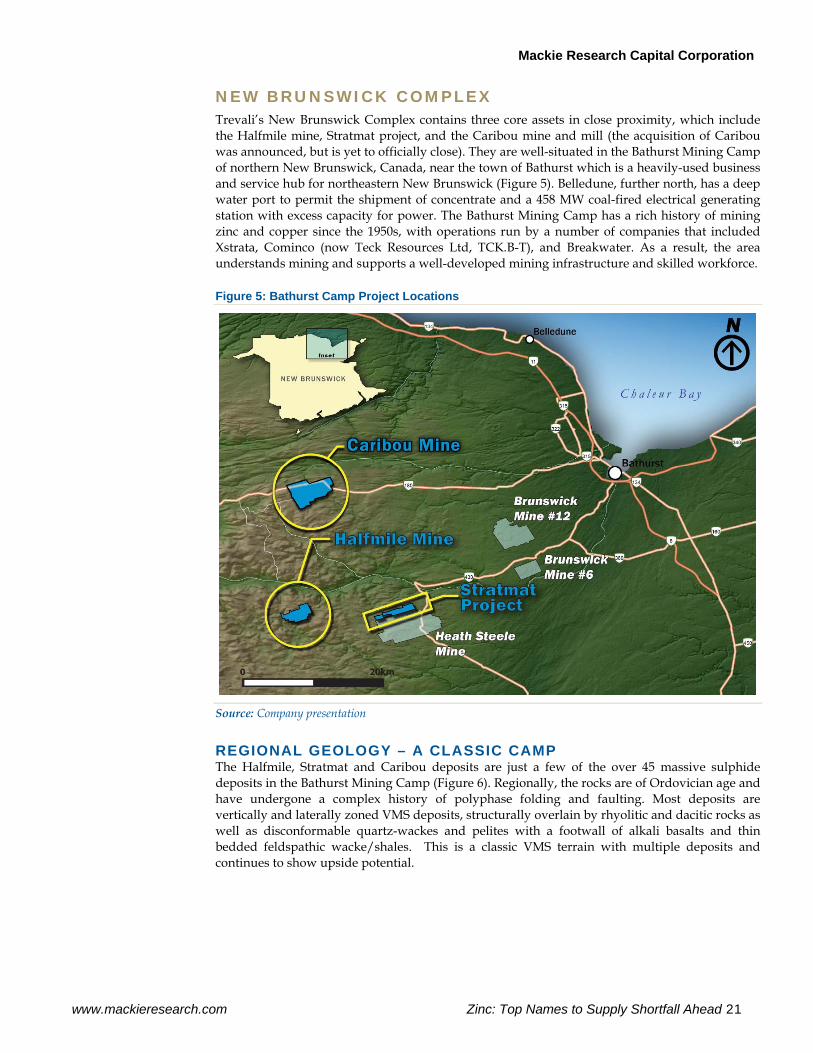

NEW BRUNSWICK COMPLEX Trevali’s New Brunswick Complex contains three core assets in close proximity, which include the Halfmile mine, Stratmat project, and the Caribou mine and mill (the acquisition of Caribou was announced, but is yet to officially close). They are well-situated in the Bathurst Mining Camp of northern New Brunswick, Canada, near the town of Bathurst which is a heavily-used business and service hub for northeastern New Brunswick (Figure 5). Belledune, further north, has a deep water port to permit the shipment of concentrate and a 458 MW coal-fired electrical generating station with excess capacity for power. The Bathurst Mining Camp has a rich history of mining zinc and copper since the 1950s, with operations run by a number of companies that included Xstrata, Cominco (now Teck Resources Ltd, TCK.B-T), and Breakwater. As a result, the area understands mining and supports a well-developed mining infrastructure and skilled workforce.

Figure 5: Bathurst Camp Project Locations

Source: Company presentation

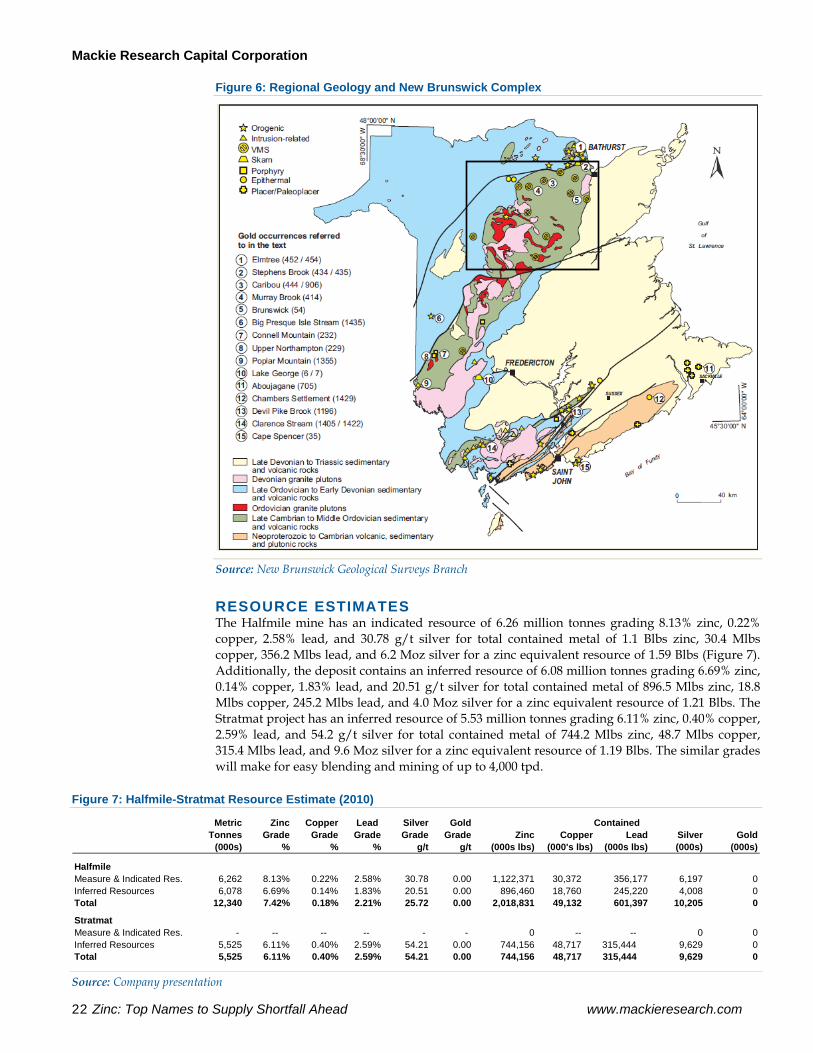

REGIONAL GEOLOGY – A CLASSIC CAMP The Halfmile, Stratmat and Caribou deposits are just a few of the over 45 massive sulphide deposits in the Bathurst Mining Camp (Figure 6). Regionally, the rocks are of Ordovician age and have undergone a complex history of polyphase folding and faulting. Most deposits are vertically and laterally zoned VMS deposits, structurally overlain by rhyolitic and dacitic rocks as well as disconformable quartz-wackes and pelites with a footwall of alkali basalts and thin bedded feldspathic wacke/shales. This is a classic VMS terrain with multiple deposits and continues to show upside potential.

Mackie Research Capital Corporation

22 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

Figure 6: Regional Geology and New Brunswick Complex

Source: New Brunswick Geological Surveys Branch

RESOURCE ESTIMATES The Halfmile mine has an indicated resource of 6.26 million tonnes grading 8.13% zinc, 0.22% copper, 2.58% lead, and 30.78 g/t silver for total contained metal of 1.1 Blbs zinc, 30.4 Mlbs copper, 356.2 Mlbs lead, and 6.2 Moz silver for a zinc equivalent resource of 1.59 Blbs (Figure 7). Additionally, the deposit contains an inferred resource of 6.08 million tonnes grading 6.69% zinc, 0.14% copper, 1.83% lead, and 20.51 g/t silver for total contained metal of 896.5 Mlbs zinc, 18.8 Mlbs copper, 245.2 Mlbs lead, and 4.0 Moz silver for a zinc equivalent resource of 1.21 Blbs. The Stratmat project has an inferred resource of 5.53 million tonnes grading 6.11% zinc, 0.40% copper, 2.59% lead, and 54.2 g/t silver for total contained metal of 744.2 Mlbs zinc, 48.7 Mlbs copper, 315.4 Mlbs lead, and 9.6 Moz silver for a zinc equivalent resource of 1.19 Blbs. The similar grades will make for easy blending and mining of up to 4,000 tpd.

Figure 7: Halfmile-Stratmat Resource Estimate (2010)

Metric Zinc Copper Lead Silver GoldTonnes Grade Grade Grade Grade Grade Zinc Copper Lead Silver Gold

(000s) % % % g/t g/t (000s lbs) (000's lbs) (000s lbs) (000s) (000s)

HalfmileMeasure & Indicated Res. 6,262 8.13% 0.22% 2.58% 30.78 0.00 1,122,371 30,372 356,177 6,197 0Inferred Resources 6,078 6.69% 0.14% 1.83% 20.51 0.00 896,460 18,760 245,220 4,008 0Total 12,340 7.42% 0.18% 2.21% 25.72 0.00 2,018,831 49,132 601,397 10,205 0

StratmatMeasure & Indicated Res. - -- -- -- - - 0 -- -- 0 0Inferred Resources 5,525 6.11% 0.40% 2.59% 54.21 0.00 744,156 48,717 315,444 9,629 0Total 5,525 6.11% 0.40% 2.59% 54.21 0.00 744,156 48,717 315,444 9,629 0

Contained

Source: Company presentation

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 23

HALFMILE & STRATMAT – A GREAT START Trevali’s New Brunswick properties were heavily explored by Xstrata Zinc and its predecessor companies at intervals since the 1960s. In particular, extensive exploration activity occurred during the 1980s and 1990s when the Heath Steele and Stratmat mines were in production. In 2008, Kria Resources (now Trevali) entered into an agreement with Xstrata Zinc whereby Kria had the right to gain 100% ownership of the Stratmat and Halfmile projects by:

Paying US$18,000,000 (completed)

Issuing units worth a total of C$7,000,000 (completed).

Xstrata maintains the first right and option to purchase all or any portion of the concentrate off-take, as well as a 2% Net Smelter Return (NSR) royalty. In 2010, Kria produced a Preliminary Economic Assessment (PEA) on the Halfmile-Stratmat properties, as well as various resource estimates between 2008 and 2011. In April 2011, Trevali completed a friendly business combination with Kria whereby Trevali acquired all of the issued and outstanding shares of Kria in a stock swap at a rate of 0.2 Trevali shares for every Kria share, providing an acquisition value of $44 million. Upon completion, Trevali was provided with 100% ownership of the Halfmile-Stratmat deposits.

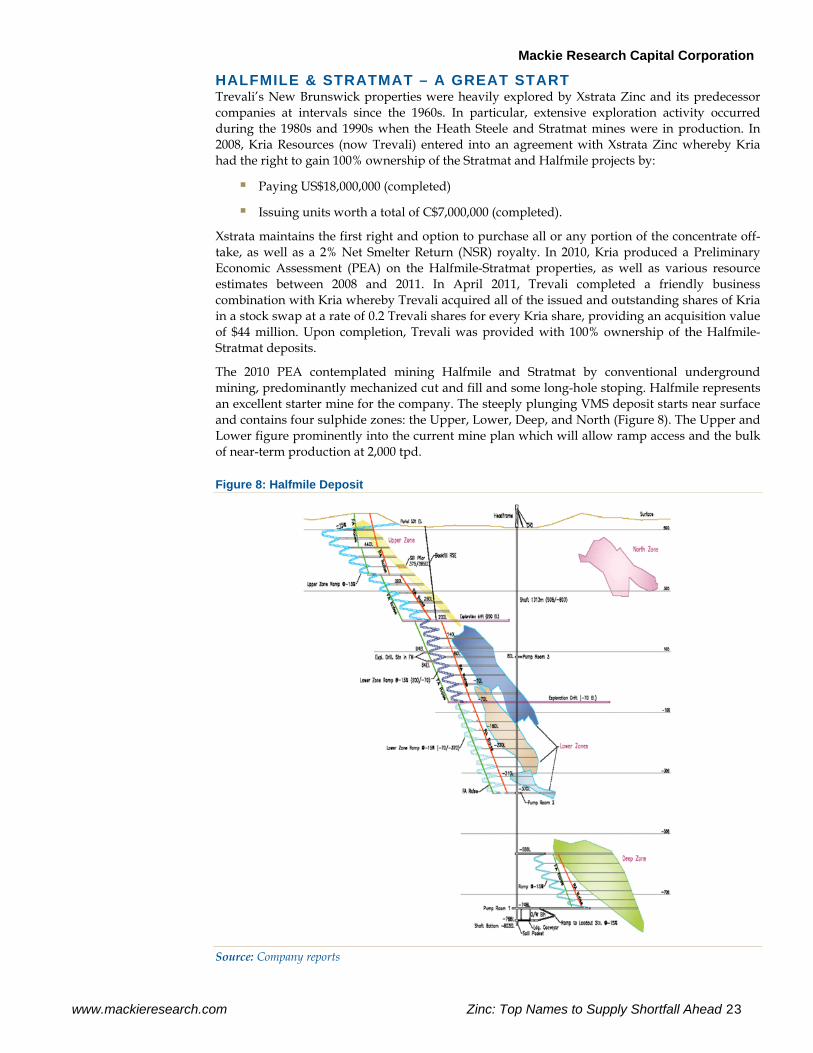

The 2010 PEA contemplated mining Halfmile and Stratmat by conventional underground mining, predominantly mechanized cut and fill and some long-hole stoping. Halfmile represents an excellent starter mine for the company. The steeply plunging VMS deposit starts near surface and contains four sulphide zones: the Upper, Lower, Deep, and North (Figure 8). The Upper and Lower figure prominently into the current mine plan which will allow ramp access and the bulk of near-term production at 2,000 tpd.

Figure 8: Halfmile Deposit

Source: Company reports

Mackie Research Capital Corporation

24 Zinc: Top Names to Supply Shortfall Ahead www.mackieresearch.com

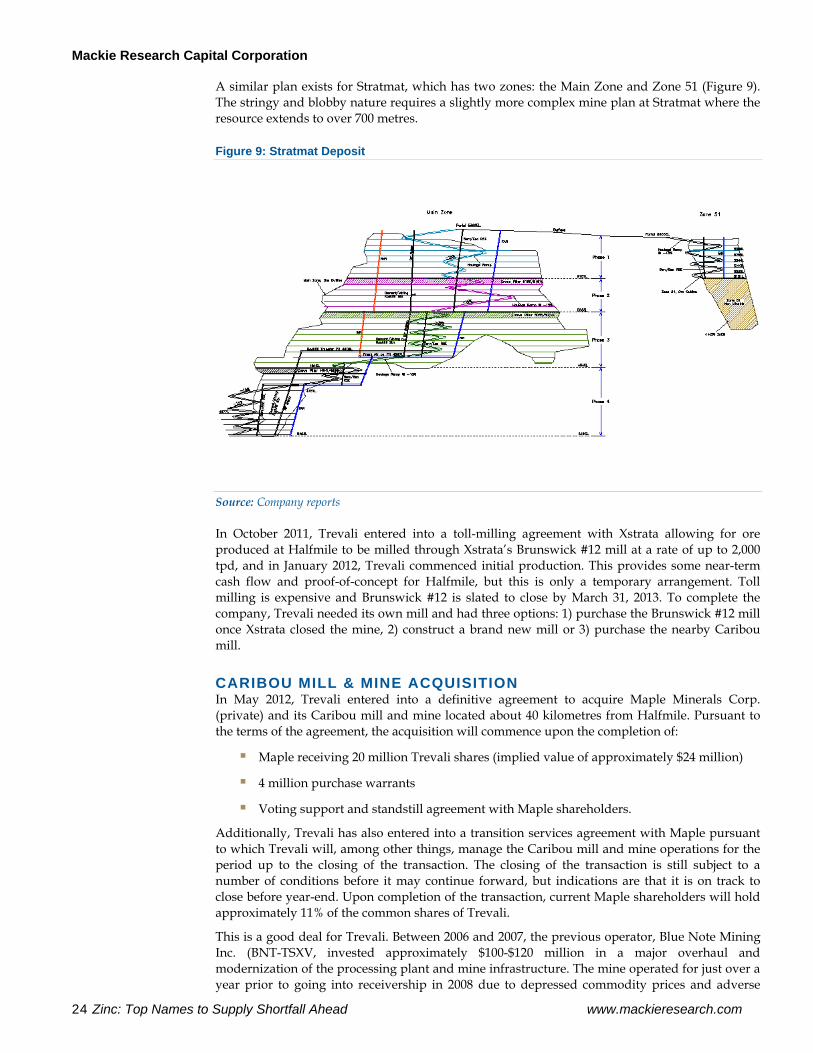

A similar plan exists for Stratmat, which has two zones: the Main Zone and Zone 51 (Figure 9). The stringy and blobby nature requires a slightly more complex mine plan at Stratmat where the resource extends to over 700 metres.

Figure 9: Stratmat Deposit

Source: Company reports

In October 2011, Trevali entered into a toll-milling agreement with Xstrata allowing for ore produced at Halfmile to be milled through Xstrata’s Brunswick #12 mill at a rate of up to 2,000 tpd, and in January 2012, Trevali commenced initial production. This provides some near-term cash flow and proof-of-concept for Halfmile, but this is only a temporary arrangement. Toll milling is expensive and Brunswick #12 is slated to close by March 31, 2013. To complete the company, Trevali needed its own mill and had three options: 1) purchase the Brunswick #12 mill once Xstrata closed the mine, 2) construct a brand new mill or 3) purchase the nearby Caribou mill.

CARIBOU MILL & MINE ACQUISITION In May 2012, Trevali entered into a definitive agreement to acquire Maple Minerals Corp. (private) and its Caribou mill and mine located about 40 kilometres from Halfmile. Pursuant to the terms of the agreement, the acquisition will commence upon the completion of:

Maple receiving 20 million Trevali shares (implied value of approximately $24 million)

4 million purchase warrants

Voting support and standstill agreement with Maple shareholders.

Additionally, Trevali has also entered into a transition services agreement with Maple pursuant to which Trevali will, among other things, manage the Caribou mill and mine operations for the period up to the closing of the transaction. The closing of the transaction is still subject to a number of conditions before it may continue forward, but indications are that it is on track to close before year-end. Upon completion of the transaction, current Maple shareholders will hold approximately 11% of the common shares of Trevali.

This is a good deal for Trevali. Between 2006 and 2007, the previous operator, Blue Note Mining Inc. (BNT-TSXV, invested approximately $100-$120 million in a major overhaul and modernization of the processing plant and mine infrastructure. The mine operated for just over a year prior to going into receivership in 2008 due to depressed commodity prices and adverse

Mackie Research Capital Corporation

www.mackieresearch.com Zinc: Top Names to Supply Shortfall Ahead 25

global financial conditions. The acquisition of the Caribou mine and milling complex has a number of benefits to Trevali. Of particular importance is that Trevali receives ownership of a modern 3,000 tpd concentrate processing plant including a metallurgical and geochemical laboratory and permitted tailings treatment facility. Further benefits include the addition of a former producing mine (Caribou) to the company’s already promising portfolio, which Trevali believes remains open for expansion at depth and along strike.

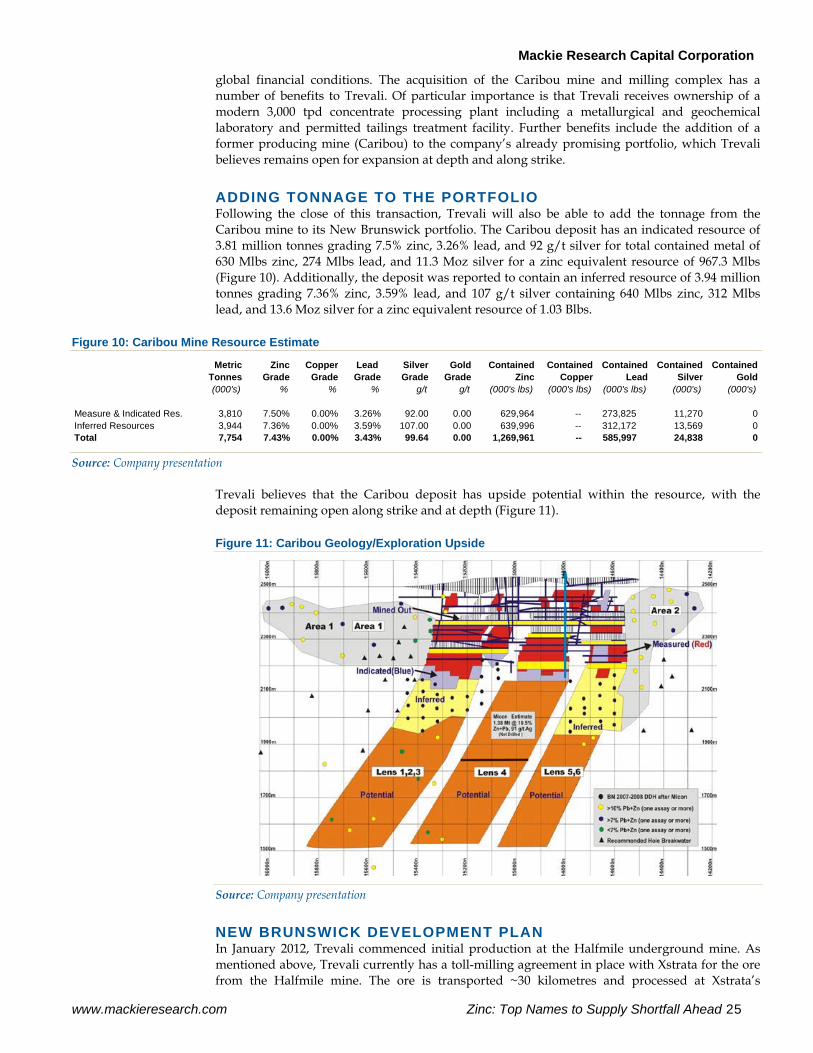

ADDING TONNAGE TO THE PORTFOLIO Following the close of this transaction, Trevali will also be able to add the tonnage from the Caribou mine to its New Brunswick portfolio. The Caribou deposit has an indicated resource of 3.81 million tonnes grading 7.5% zinc, 3.26% lead, and 92 g/t silver for total contained metal of 630 Mlbs zinc, 274 Mlbs lead, and 11.3 Moz silver for a zinc equivalent resource of 967.3 Mlbs (Figure 10). Additionally, the deposit was reported to contain an inferred resource of 3.94 million tonnes grading 7.36% zinc, 3.59% lead, and 107 g/t silver containing 640 Mlbs zinc, 312 Mlbs lead, and 13.6 Moz silver for a zinc equivalent resource of 1.03 Blbs.