© copyright 2006 ims/glc all rights reserved. page 1 the state of open source in higher...

TRANSCRIPT

Page 1© Copyright 2006 IMS/GLCAll Rights Reserved.

The State of OpenSource in Higher

Education:Time for aReality Check?

June 2006

– Rob Abel– CEO, IMS Global Learning Consortium– office: +1.407.792.4164– mobile: +1.407.687.7255– skype: rob_abel– [email protected]– http://www.imsglobal.org/

Page 2© Copyright 2006 IMS/GLCAll Rights Reserved.

“It is not the strongest species that survive, nor the most intelligent, but

the ones who are most responsive to change”

- Charles Darwin

Page 3© Copyright 2006 IMS/GLCAll Rights Reserved.

Who Will Win?

Traditional CommercialApplications

Traditional CommercialApplications

Open Source ApplicationsOpen Source Applications

Community Source ApplicationsCommunity Source Applications

HigherEducationEnterpriseSoftwareApplications

HigherEducationEnterpriseSoftwareApplications

Page 4© Copyright 2006 IMS/GLCAll Rights Reserved.

Collaborative Research*

• Online Learning• Open Source• Digital Content• Vendor Satisfaction

*Join IMS LILF to subscribe

Page 5© Copyright 2006 IMS/GLCAll Rights Reserved.

Agenda• Overall Purpose: Discussion about the progress of community source from a business perspective

• Results of industry survey through a market leadership lens

• Summary thoughts• Call to action for the IMS Global Learning Consortium

*Note: There will be discussion topics throughout the presentation- active participation is expected

Page 6© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey Results Agenda• Survey background• Issue #1- What level of penetration of open source applications constitutes success?

• Issue #2- Do the open source initiatives have what it takes to succeed as application products in the higher education market?

• Issue #3- What is the level of expectation regarding open source and is this good or bad?

Page 7© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey Background

• Conducted Fall and early Winter 2005-6• Respondents were CIOs or others claiming

responsibility for evaluating open source products

• Sought to target all levels of engagement in open source (including none)

• Took a broad view - including open source-enabled products - Luminis, Academus

• Sought to target all types of institutions• U.S. focused, but did not exclude outside

U.S.• 195 completed surveys, 30 partially

completed• 15 minutes average time to completion

Page 8© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey Sponsors

• Sun Microsystems• Sungard SCT• Unicon• Alliance for Higher Education Competitiveness

Page 9© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey is Reopened

• A rolling open survey with periodic report outs

• Participants receive the report• We will notify you when its been 12

months since your last completion• Click on link under “participate” at:

http://www.a-hec.org/open_source_state.html

Page 10© Copyright 2006 IMS/GLCAll Rights Reserved.

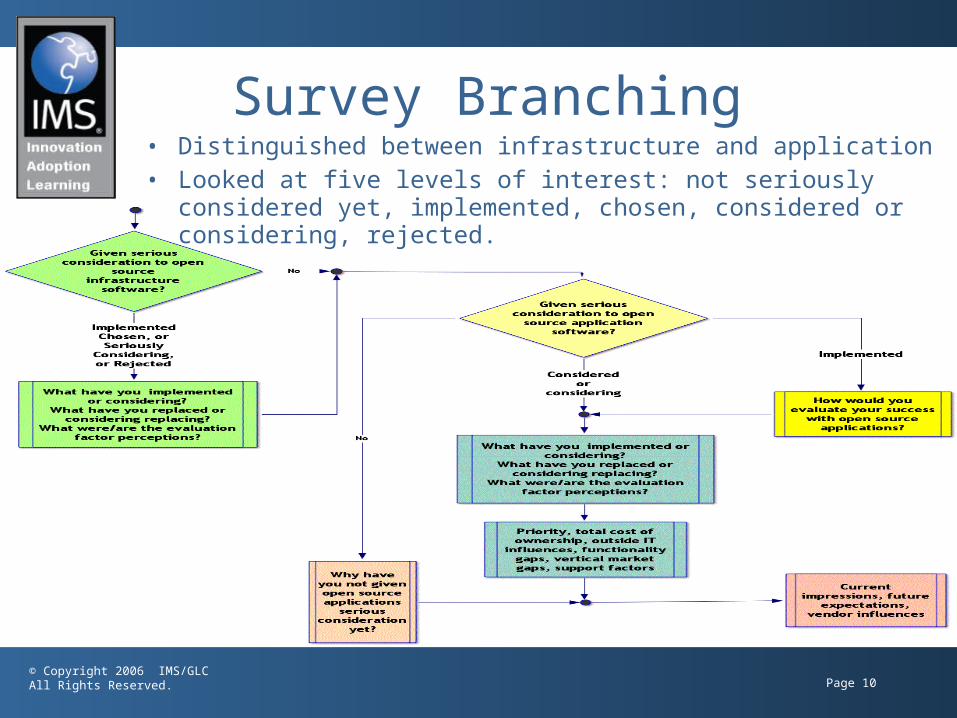

Survey Branching• Distinguished between infrastructure and

application• Looked at five levels of interest: not seriously

considered yet, implemented, chosen, considered or considering, rejected.

Page 11© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey Results Agenda• Survey background• Issue #1- What level of penetration of open source applications constitutes success?

• Issue #2- Do the open source initiatives have what it takes to succeed as application products in the higher education market?

• Issue #3- What is the level of expectation regarding open source and is this good or bad?

Page 12© Copyright 2006 IMS/GLCAll Rights Reserved.

Discussion Topic

• Issue #1- What level of penetration of open source applications constitutes success?

• How will community source know when it has succeeded?

• What are the successes so far?• What is the proof?

Page 13© Copyright 2006 IMS/GLCAll Rights Reserved.

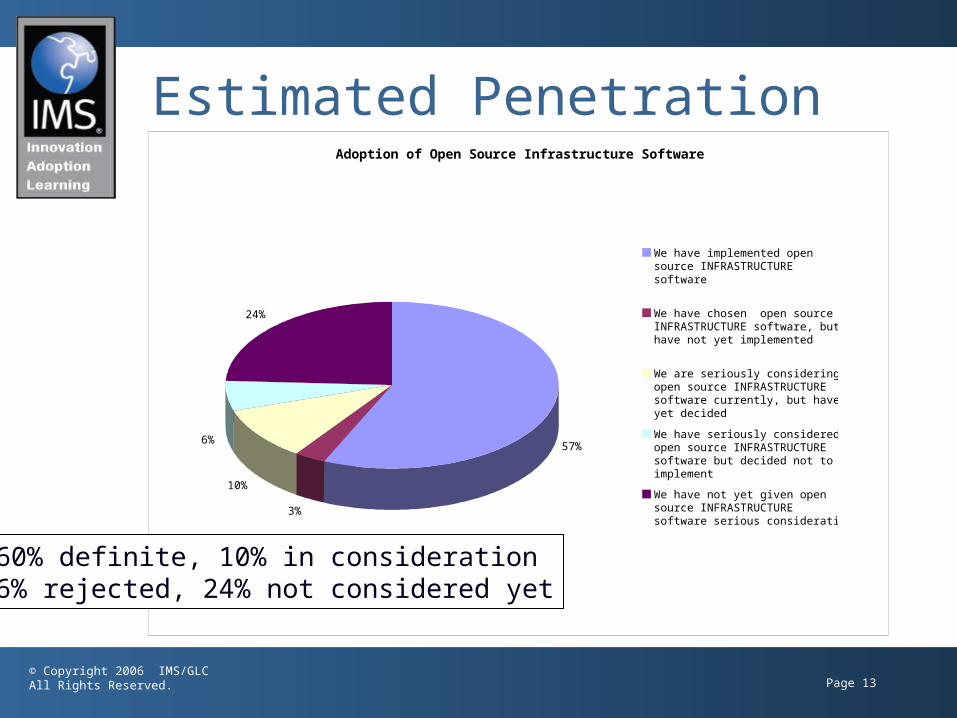

Estimated PenetrationAdoption of Open Source Infrastructure Software

57%

3%

10%

6%

24%

We have implemented opensource INFRASTRUCTUREsoftware

We have chosen open sourceINFRASTRUCTURE software, buthave not yet implemented

We are seriously consideringopen source INFRASTRUCTUREsoftware currently, but have notyet decided

We have seriously consideredopen source INFRASTRUCTUREsoftware but decided not toimplement

We have not yet given opensource INFRASTRUCTURE software serious consideration

60% definite, 10% in consideration6% rejected, 24% not considered yet

Page 14© Copyright 2006 IMS/GLCAll Rights Reserved.

Estimated PenetrationAdoption of Open Source Application Software: All Institutions

34%

8%

16%

8%

34%

We have implemented open sourceAPPLICATION software

We have chosen open sourceAPPLICATION software, but have not yetimplemented

We are seriously considering open sourceAPPLICATION software currently, buthave not yet decided

We have seriously considered opensource APPLICATION software butdecided not to implement

We have not yet given open sourceAPPLICATION software seriousconsideration

42% definite, 16% in consideration8% rejected, 34% not considered yet

Page 15© Copyright 2006 IMS/GLCAll Rights Reserved.

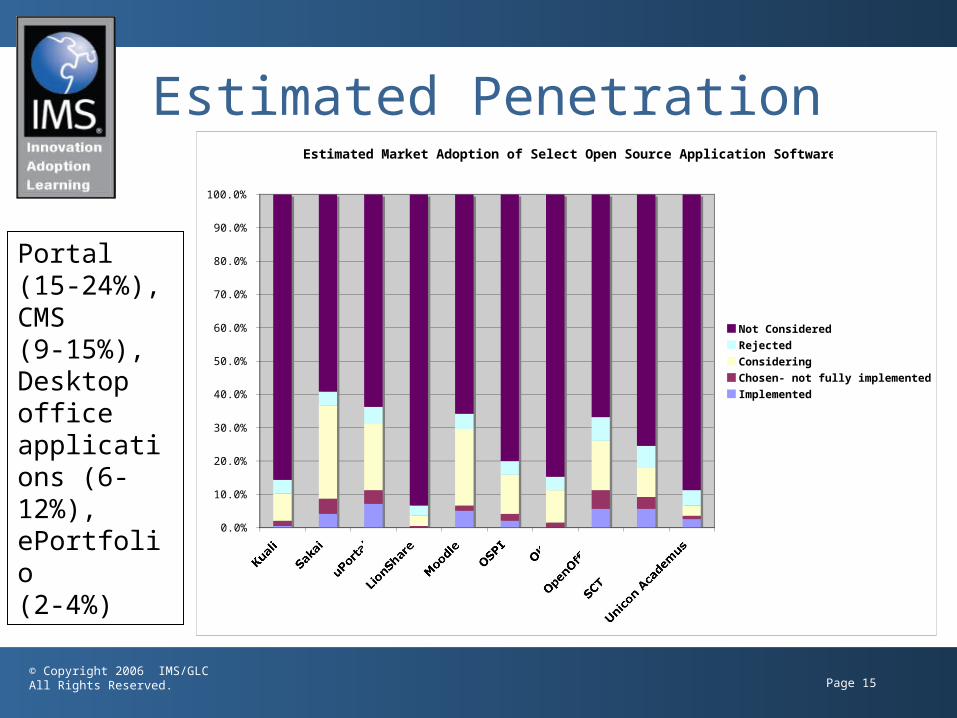

Estimated Penetration

Portal (15-24%), CMS (9-15%), Desktop office applications (6-12%), ePortfolio (2-4%)

Estimated Market Adoption of Select Open Source Application Software

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Kuali SakaiuPortal

LionShareMoodle

OSPI OKI

OpenOfficeSCT Luminis

Unicon Academus

Not Considered

Rejected

Considering

Chosen- not fully implemented

Implemented

Page 16© Copyright 2006 IMS/GLCAll Rights Reserved.

Estimated PenetrationAdoption of Open Source Application Software by Operating

Budget: Six Levels

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

We haveimplemented open

sourceAPPLICATION

software

We have chosen open source

APPLICATIONsoftware, but have

not yetimplemented

We are seriouslyconsidering open

sourceAPPLICATION

software currently,but have not yet

decided

We have seriouslyconsidered open

sourceAPPLICATIONsoftware but

decided not toimplement

We have not yetgiven open source

APPLICATIONsoftware serious

consideration

< $20m

$20-50m

$50-100m

$100-200m

$200-500m

>$500m

Page 17© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey Results Agenda• Survey background• Issue #1- What level of penetration of open source applications constitutes success?

• Issue #2- Do the open source initiatives have what it takes to succeed as application products in the higher education market?

• Issue #3- What is the level of expectation regarding open source and is this good or bad?

Page 18© Copyright 2006 IMS/GLCAll Rights Reserved.

Some Data Points

• Blackboard market cap: $788 million• eCollege market cap: $532 million (one of

Forbes 100 hot growth companies)• Estimated market value of Sungard Higher Ed:

$1.5 billion• Datatel, Oracle/Peoplesoft, Jenzabar: $$

• Discussion question: How does this compare to the resources of open source and community source initiatives?

• Discussion question: Do resources matter?

Page 19© Copyright 2006 IMS/GLCAll Rights Reserved.

Discussion Topic• Issue #2- Do the open source initiatives have what it takes to succeed as application products in the higher education market?

• Why did Blackboard, WebCT, and eCollege succeed?

Page 20© Copyright 2006 IMS/GLCAll Rights Reserved.

Priority of Open SourceInstitutional Priority of Open Source Applications

Compared to Other IT Initiatives

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

Very low priority Low priority Average priority High priority Very high priority

Page 21© Copyright 2006 IMS/GLCAll Rights Reserved.

Top IT Issues Today• Security and identity management• Funding IT• Administrative/ERP/information systems

• Disaster recovery/business continuity• Faculty development, support, and training

• Source: Educause• http://www.educause.edu/ir/library/pdf/eqm0622.pdf

Page 22© Copyright 2006 IMS/GLCAll Rights Reserved.

TCO ConclusionsExperience or Analysis of Total Cost of Ownership of Open Source Applications

26%

30%

27%

5%

2%

10%

Significantly lower (50% or less)cost than competing commercialapplications

Somewhat lower cost (51% to 80%)than competing commercialapplications

About the same cost (81% to 119%)as competing commercialapplications

Somewhat higher cost (120% to149%) than competing commercialapplications

Significantly higher (150% or more)cost than competing commercialapplications

Have no idea

56% TCO advantage7% TCO disadvantage

Page 23© Copyright 2006 IMS/GLCAll Rights Reserved.

Outside InfluencersEncouragement of Open Source Applications from Outside IT

Strongly Disagree19%

Disagree33%

Maybe18%

Agree22%

Strongly Agree8%

30% outside IT influence

Page 24© Copyright 2006 IMS/GLCAll Rights Reserved.

Influencers Outside IT:Those Respondents that Felt There Was Influence from Outside IT

4%8%

4%

24%

33%

27% The president

The provost or VP academic affairs

Chief financial officer or VPadministration

Deans or department leaders

Faculty leaders

Other

Who?

57% faculty or department leaders16% institutional leaders

Page 25© Copyright 2006 IMS/GLCAll Rights Reserved.

Reasons for ConsideringDrivers for Considering Open Source Application Software

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

EnhancedFunctionality

IntegrationFramework

Customization Unique Needs ofHigher

Education

Platform forResearch

CommercialVendor Lock-In

Strongly Agree

Agree

Maybe

Disagree

Strongly Disagree

CustomizationLock-inUnique needs

Page 26© Copyright 2006 IMS/GLCAll Rights Reserved.

Survey Results Agenda• Survey background• Issue #1- What level of penetration of open source applications constitutes success?

• Issue #2- Do the open source initiatives have what it takes to succeed as application products in the higher education market?

• Issue #3- What is the level of expectation regarding open source and is this good or bad?

Page 27© Copyright 2006 IMS/GLCAll Rights Reserved.

Discussion Topic• Issue #3- What is the level of expectation regarding open source and is this good or bad?

• What are the most important expectations that have been created concerning community source?

• Are these being fulfilled?

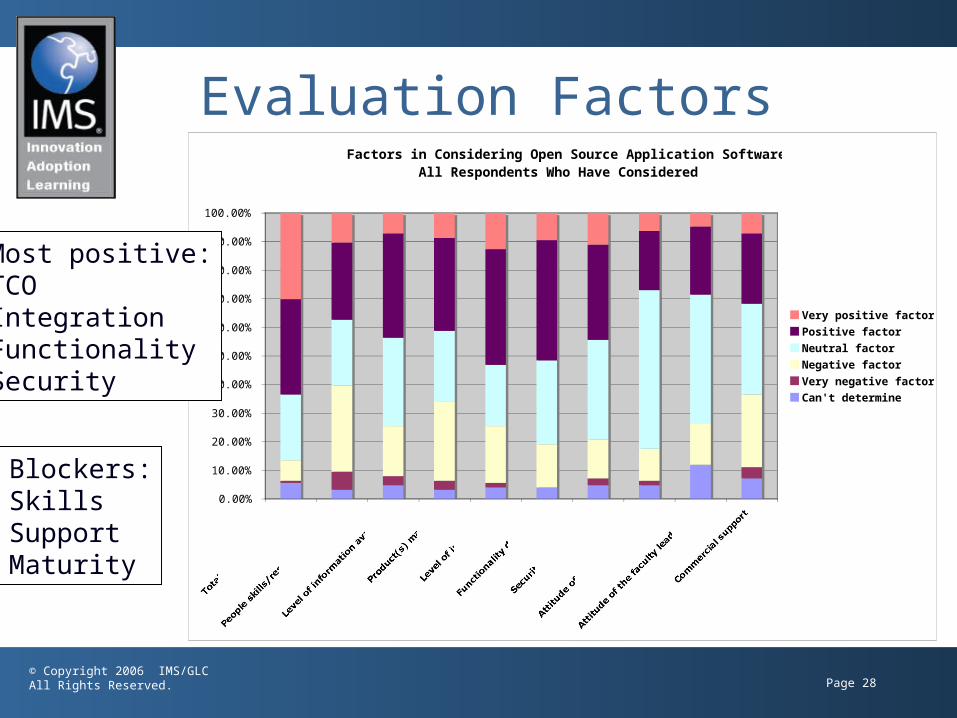

Page 28© Copyright 2006 IMS/GLCAll Rights Reserved.

Evaluation FactorsFactors in Considering Open Source Application Software:

All Respondents Who Have Considered

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Total cost of ownership

People skills/resources requiredLevel of information available

Product(s) maturityLevel of integration

Functionality differenceSecurity level provided

Attitude of the administrationAttitude of the faculty leadership

Commercial support

Very positive factor

Positive factor

Neutral factor

Negative factor

Very negative factor

Can't determine

Most positive:TCOIntegrationFunctionalitySecurity

Blockers:SkillsSupportMaturity

Page 29© Copyright 2006 IMS/GLCAll Rights Reserved.

Skills IssuesAvailability of IT Resources to Support Open Source:

All Respondents

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Our institution has the breadth anddepth of IT resources to supportDEVELOPMENT of open source

products

Our institution has the breadth anddepth of IT resources to support

IMPLEMENTATION of open sourceproducts

Our institution has the breadth anddepth of IT resources to support

the USAGE of open source products

Strongly Agree

Agree

Maybe

Disagree

Strongly Disagree

Don't Know

Page 30© Copyright 2006 IMS/GLCAll Rights Reserved.

Commercial SupportMore Likely to Implement Open Source if Backed by Commercial Vendor: By

Operating Budget

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

Less Than $100M Greater Than $100M

Strongly Agree

Agree

Neutral

Disagree

Strongly Disagree

Page 31© Copyright 2006 IMS/GLCAll Rights Reserved.

Perceived Maturity Impression of Select Open Source Applications: All Respondents

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

SakaiuPortal

OSPI OKI

Lionshare

KualiMoodle

OpenOfficeSCT Luminis

Unicon Academus

A viable, proven product that couldbe considered by an institution likeours now

A viable product that could beconsidered by an institution like oursin a year or two

A new initiative that is worthwatching but is not ready for primetime in the near future

An initiative I have heard of butdoes not seem relevant to aninstitution like ours

Never heard of it

Page 32© Copyright 2006 IMS/GLCAll Rights Reserved.

Successes of Open SourceSuccess Achieved With Open Source Application Software:

All Respondents Who Have Implemented

41.54%33.85%

23.08%

38.46%

21.54%32.31%

15.38%21.54%

12.31%

36.92%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Total cost of ownership

User satisfaction

Support from the presidents officeResponsiveness to institutional needs

Meeting project schedulesEnhanced functionality

Collaboration with other institutions

Achieving an institution-wide infrastructure

Facilitation of IT research

Creating a platform for innovation

Very Successful

Somewhat Successful

Not Sure Yet

Somewhat Unsuccessful

Very Unsuccessful

Not A Goal

Most:TCOResponsivenessInnovationSatisfactionFunctionality

Page 33© Copyright 2006 IMS/GLCAll Rights Reserved.

Considering Now . . . Estimated Market Adoption of Select Open Source Application Software

8.2%

28.1% 19.9%

3.1%

23.0%

11.7%9.7%

14.8%

8.7%

3.1%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Kuali SakaiuPortal

LionShareMoodle

OSPI OKI

OpenOfficeSCT Luminis

Unicon Academus

Not Considered

Rejected

Considering

Chosen- not fully implemented

Implemented

Page 34© Copyright 2006 IMS/GLCAll Rights Reserved.

Future Expectations Three-Year Prediction of Pervasiveness of Open Source

Applications:

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

< $20m $20-50m $50-100m $100-200m $200-500m >$500m

Pervasive

Substantial

One or Two Products in Use

Occasional Consideration

None

Page 35© Copyright 2006 IMS/GLCAll Rights Reserved.

Agenda• Overall Purpose: Discussion about the progress of community source from a business perspective

• Results of industry survey through a market leadership lens

• Summary thoughts • Call to action for the IMS Global Learning Consortium

*Note: There will be discussion topics throughout the presentation- active participation is expected

Page 36© Copyright 2006 IMS/GLCAll Rights Reserved.

Summary Thoughts• Open source applications have clearly emerged as a factor in the higher education market

• It’s difficult to see how open source can rival the innovation of commercial products going forward given the focus on cost as the key value proposition (but it is possible)

• Commercial CMS’s created a strong pull from underserved users that drove an IT decision - can IT drive open source applications?

Page 37© Copyright 2006 IMS/GLCAll Rights Reserved.

Agenda• Overall Purpose: Discussion about the progress of community source from a business perspective

• Results of industry survey through a market leadership lens

• Summary thoughts• Call to action for the IMS Global Learning Consortium

*Note: There will be discussion topics throughout the presentation- active participation is expected

Page 38© Copyright 2006 IMS/GLCAll Rights Reserved.

IMS Global LearningConsortium

• In service to the community of organizations and individuals enhancing learning worldwide

• IMS/GLC is a global, nonprofit, member organization that provides leadership in shaping and growing the learning industry through community development of standards, promotion of innovation, and research into best practices

Page 39© Copyright 2006 IMS/GLCAll Rights Reserved.

IMS and the Global Tech Industry

Investing in

LearningInnovation

Page 40© Copyright 2006 IMS/GLCAll Rights Reserved.

IMS and Global Education

Leaders inLearning

Page 41© Copyright 2006 IMS/GLCAll Rights Reserved.

IMS Open Source Objectives

• Separate truth from fiction• Address efficient return across commercial and grant funding through interoperability standards and projects

• Research and document best practices

• Explore the connection between open source and key learning industry challenges

Page 42© Copyright 2006 IMS/GLCAll Rights Reserved.

IMS Open Source Actions• Open source activities at annual conference June 19-22– Moodle, Sakai, Blackboard, Angel, Microsoft, IBM, Open University, etc.

• New working group on Integrated Learning Architectures partnering with UBC open source SOA group, among others

• This research - your involvement and support welcome . . .

Page 43© Copyright 2006 IMS/GLCAll Rights Reserved.

Participate: Support IMS!• Join IMS! New Member Levels Available!

–http://www.imsglobal.org/joinims.html

• Annual Conference: June 19-22, Hosted by Indiana U:

–http://www.imsglobal.org/altilab2006/

Page 44© Copyright 2006 IMS/GLCAll Rights Reserved.

Open Source Workshop• Special Workshop (Thursday, 22 June) Integrating Open

Source, Commercial, and In-House Solutions to Deliver Online Learning Solutions

• Workshop Themes: * How integration can happen. * How standards support an integrated approach. * Relevant IMS specifications. * Typical customer requirements. * Making fit for purpose choices. * Real user case studies.

• 10:00 - 10:10 Introduction * Joel Greenberg, Chair of EIN, Director of Strategic Development Learning & Teaching Solutions, The Open University

• 10:10 - 10:40 The Vendor View: * Microsoft - Chris Moffatt, Senior Program Manager, Education Products Group, Microsoft * Blackboard/WebCT - Chris Vento, Senior Vice President - Technology & Product Development, Blackboard * Angel Learning - Ray Henderson, Chief Products Officer, Angel Learning

• 10:40 - 11:00 The Open Source View: * Moodle - Martin Dougiamas, Moodle Founder and Lead Developer, Executive Director of Moodle Pty Ltd * Sakai - Charles Severance, Sakai Foundation Board Member, Chief Architect, University of Michigan

• 11:15 - 11:35 The User View: * The Open University - Jason Cole, Product Development Manager, Learning and Teaching Solutions, The Open University * The University of Wisconsin - Dirk Herr- Hoymann, eLearning System Architect, University of Wisconsin-Madison, DoIT

• 11:35 - 1:30 Developing User Guidelines Agreeing on on-going collaborative activities • 1:30 Workshop Closes

Page 45© Copyright 2006 IMS/GLCAll Rights Reserved.

Summit Panel• Wednesday, 21 June• Open Source: Win-Lose, Win-Win, or Lose-Lose for the

Learning Industry? New open source applications in the learning market have been explored with great interest as a potential way to provide the education industry with the customization, control, and stability. Hear about new research on the adoption of open source in higher education and join the debate on what business issues open source

addresses and whether it is a positive or negative influence on the learning industry. • Chris Vento, Senior Vice President Technology & Product Development,

Blackboard • Chris Moffatt, Senior Program Manager, Teaching & Learning Technologies

Team, Microsoft • Joel Greenberg, Ph.D., Director of Strategic Development Learning &

Teaching Solutions, The Open University • Mike King, Director, Market Development, IBM Education Industry • Brad Wheeler, Ph.D., Indiana University Chief Information Officer & Indiana

University-Bloomington Dean of IT, IU

• Moderator: Rob Abel, CEO, IMS Global Learning Consortium, Inc.

Page 46© Copyright 2006 IMS/GLCAll Rights Reserved.

Additional Resources• What’s Next in Learning Technology in Higher Education webinar– http://lecture.horizonwimba.com/launcher.cgi?channel=ims_2006_0517_1403_03

• Educational Pathways recent coverage of IMS– http://www.edpath.com