jerry rhinehart, cic, clu, chfc, rhu panama city, fl top five uses of life insurance

TRANSCRIPT

Jerry Rhinehart, CIC, CLU, ChFC, RHU

Panama City, FL

Top Five Uses of Life InsuranceTop Five Uses of Life Insurance

1 Advantages of Life Insurance

2 Create an Estate

3 Fund a Business Transfer

4 Pay off the Home Mortgage

5 Key Person Insurance

6 “Tax-Free” Retirement Replacement

Learning Objectives

1

Please note the

DISCLAIMER

2

3

Tax Advantages

The Advantages of Life Insurance

Taxation of Life Insurance The Premiums are Not

Deductible

4

Death benefit free of income tax

Benefit will be in Estate of Owner

Gifted policy could result in Gift Tax

Cash Values grow Tax Deferred –

FIFO

Example of First In, First Out — FIFO

Cash Value 15,000

Paid Premiums 10,000

Example of First In, First Out — FIFO

Cash Value 15,000

Paid Premiums 10,000

Gain 5,000

The Advantages of Life Insurance

3

Tax Advantages

Benefit Advantages

Relationship Advantages

What (and how important) is Relationship in our business?

As the agent you want to Build A Wall around your clients. This is especially important for a P/C agent.

Working with an Insured (life) or a Beneficiary should lead to

additional sales … including P/C.

Why Should Your Agency Why Should Your Agency Sell Life Insurance?Sell Life Insurance?

Life Insurance Fact-Finder

Questioning is the basic foundation for selling

4

Life Insurance Fact-Finder

Go gather data...

… and then try to sell them something! 5

Life Insurance Fact-Finder

5

Life Insurance Fact-Finder

5

Emotional Selling

Questioning (70% - 30% rule)

Life Insurance Fact-Finder

followed by...

Life Insurance Fact-Finder

L&H L&H questionnaire questionnaire (pages 27-30)(pages 27-30)

Create an Estate

What is “an estate”?

Life Insurance Can Be Used To...

7

Create an Estate

What is “an estate”?

Life Insurance Can Be Used To...

7

$100,000$300,000

CashResidenceMutualsQ-PlansBusiness

A View of Your “Stuff”

$3,000,000$1,000,000

$250,000

$4,650,0008

What Makes Up Your Estate?

Everybody has an estate

_________. Everybody’s estate

is either __________ … or it is

_________. ___________ can

solve either problem.

8

Losses That Can Impair an Estate

7

Property Losses

Casualty Losses

Disability

Death

Loss of Employment

What Type of Life

Insurance is Best for this

Need? 7

Term Insurance

7

Great for Temporary Needs!

Return of Premium (ROP) TermHow to sell ROP using the “TWO ACCOUNTS”

concept

Return of Premium (ROP) TermHow to sell ROP using the “TWO ACCOUNTS”

conceptBrad Walton - Nearest Age 38 – Pref Plus / Non-Tob$1,000,000 Level Term

Lincoln Benefit Life Insurance Company

TrueTerm 30 Year Level TrueTerm 30 Year Level ROP

$1,390 Annual ($122 per mo) $2,410 Annual ($211 per mo)

Death Benefit - $1,000,000 Death Benefit - $1,000,000

30 Years - $41,700 Total Prem 30 Years - $72,300 Total Prem

Cash returned at Age 68? Cash returned at Age 68?

- 0 - $72,300

Permanent Insurance

7

Great for Long-Term Needs!

Whole Life

Universal Life

Variable Life or VUL

“you gotta have the piece of

paper”

Create an Estate

Fund a Business Transfer

Life Insurance Can Be Used To...

9

“you gotta have the piece of

paper”

Create an Estate

Fund a Business Transfer

Life Insurance Can Be Used To...

9

What the Remaining Owners Really Want!

Full Control of the Business

Minimum Payment for the Business

No Interference from the Deceased Heirs

A Smooth and Prompt Transfer

Continuing Line of Credit

The Cost of Borrowing

10

To borrow the money and buy-out the heirs will be extremely

burden- some … and expensive

No partner – lost expertise

How much profit do you have to earn to pay back the bank?

Death Disability Termination

10

Key Provisions of a

Death Disability Termination Pre-arranged Price / Formula First Right of Refusal

10

Key Provisions of a

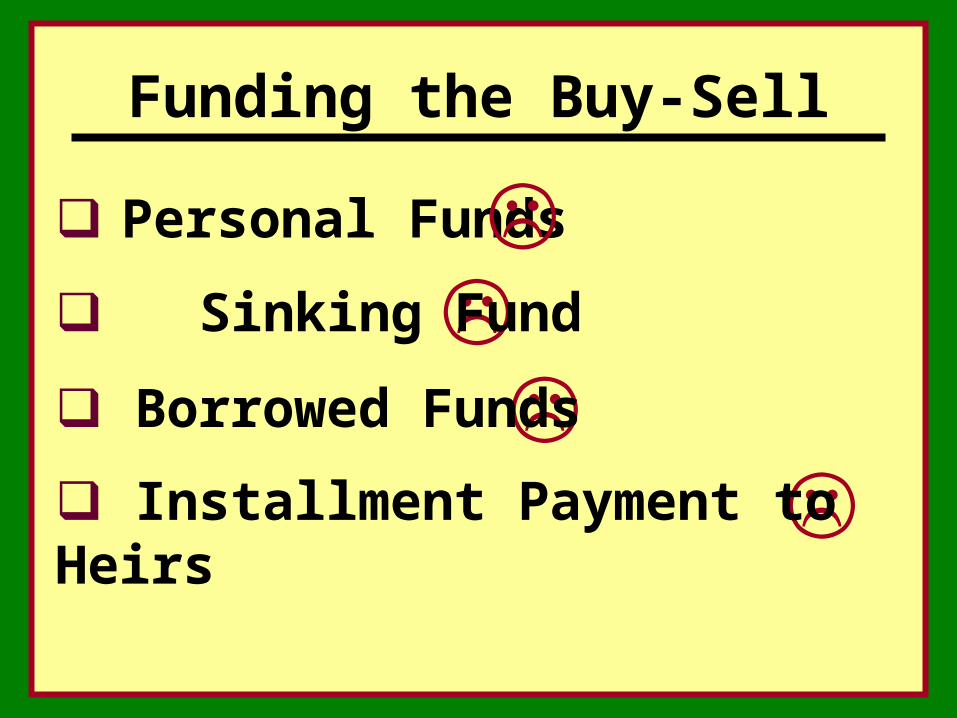

Funding the Buy-Sell

Personal Funds

Sinking Fund

Installment Payment to Heirs

Borrowed Funds

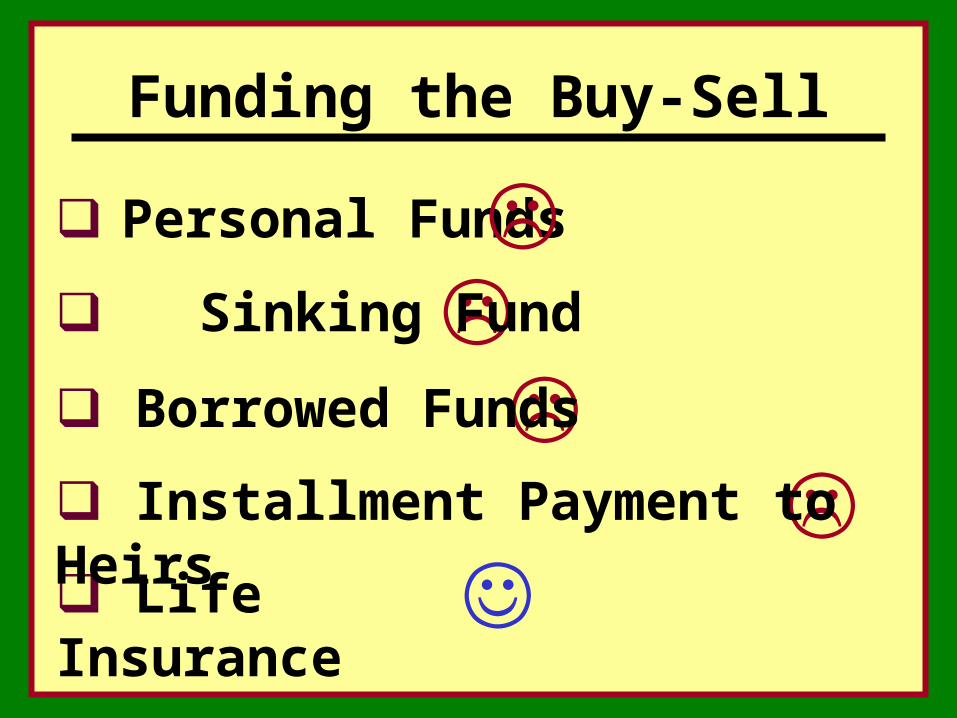

Funding the Buy-Sell

Personal Funds

Sinking Fund

Life Insurance

Installment Payment to Heirs

Borrowed Funds

11

Examine the “Key Point” on Page 11

What is your Role as the Agent Concerning the Buy-Sell

Process?

12

1 – Understand the Basics

2 – Know how life insurance

fits

3 – Motivate your client to take

action

What Type of Life

Insurance is Best for this

Need? 11

Permanent or Term Insurance

11

Term Insurance

Permanent Life Insurance or

First-to-Die Life

Create an Estate

Fund a Business Transfer

Pay off the Home Mortgage

Life Insurance Can Be Used To...

13

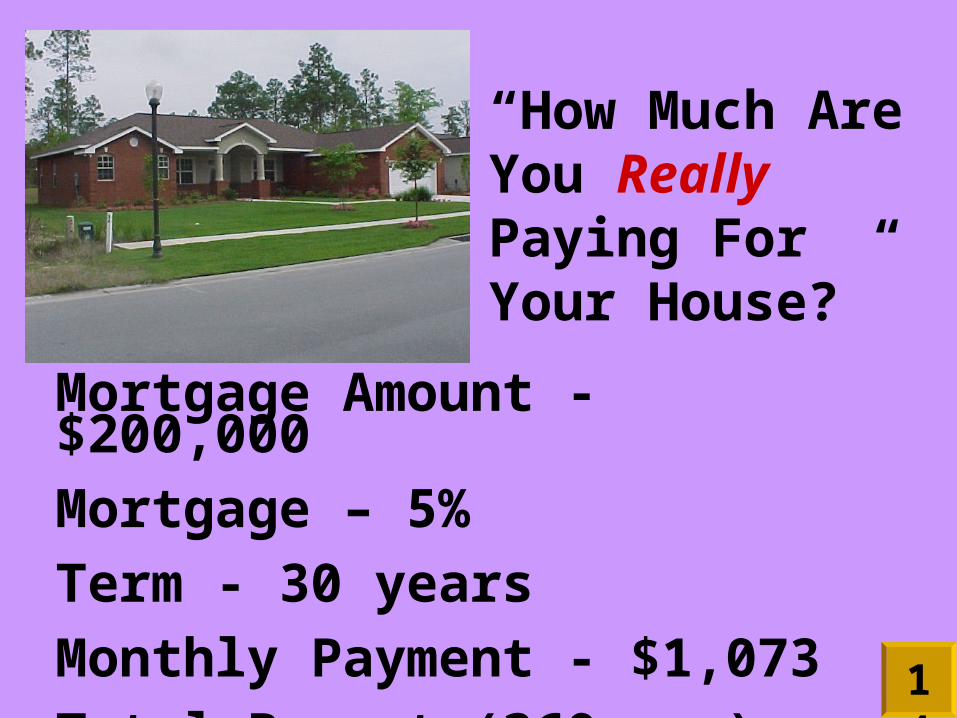

Mortgage Amount - $200,000Mortgage – 5%Term - 30 yearsMonthly Payment - $1,073Total Payout (360 mo.) - $386,280

“How Much Are You Really Paying For Your House?”

14

Mortgage Amortization Calculators

14

How do we find our “Mortgage Pay-off”

prospects? All New Homeowner’s Applications

All New Commercial Property Insurance Applications

Talk with your Realtor friends

Check the Real Estate closing at the Court House

What Type of Life

Insurance is Best for this

Need? 13

Permanent or Term Insurance

11

Term Insurance / Joint Decreasing

13

Permanent or Term Insurance

11

Term Insurance / Joint Decreasing

Permanent Life with Term Rider for Spouse – Cash

Value for Future Payoff13

Create an Estate

Fund a Business Transfer

Pay off the Home Mortgage

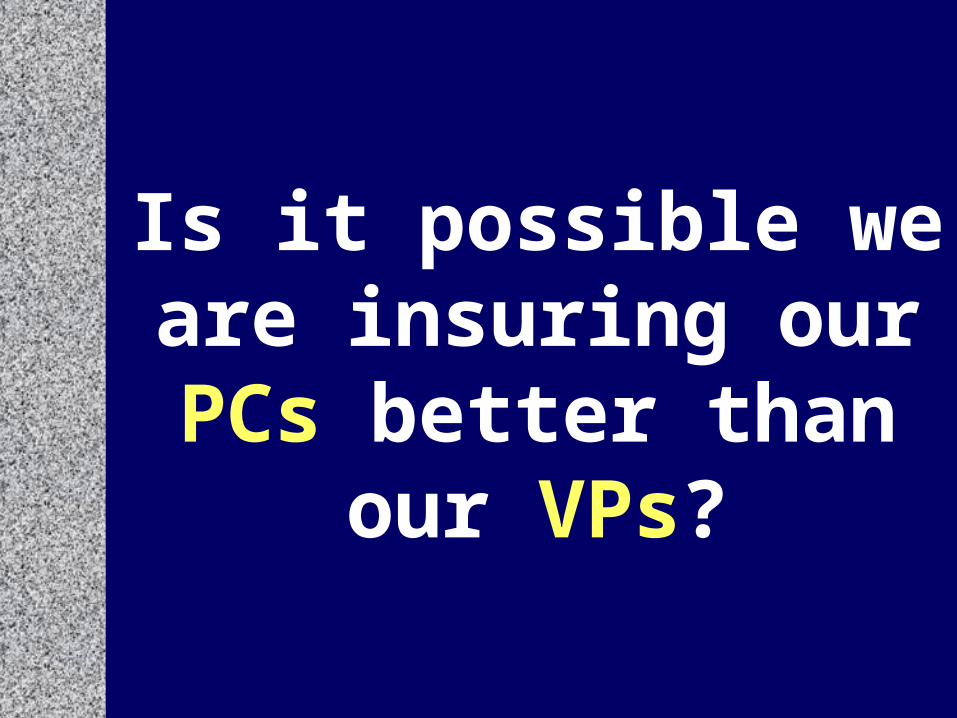

Key Person Insurance

Life Insurance Can Be Used To...

15

Is it possible we are insuring our PCs better than

our VPs?

A Natural Sale for the P/C

Agent

Insuring the Key Person

Use the Comparison of

“Key Equipment”

Insuring the Key Person

15

Various Methods for Valuation

Earnings Approach

Replacement Approach

Present Value Method

Seat-of-the-Pants Method

Insuring the Key Person

16

What Type of Life

Insurance is Best for this

Need? 15

Type of Insurance

11

Term Insurance

UL / VUL / WL with Other Person Term Riders

15

Create an Estate

Fund a Business Transfer

Pay off the Home Mortgage

Key Person Insurance

Create a “Tax-Free” Retirement Fund Replacement For Loved-Ones

Life Insurance Can Be Used To...

17

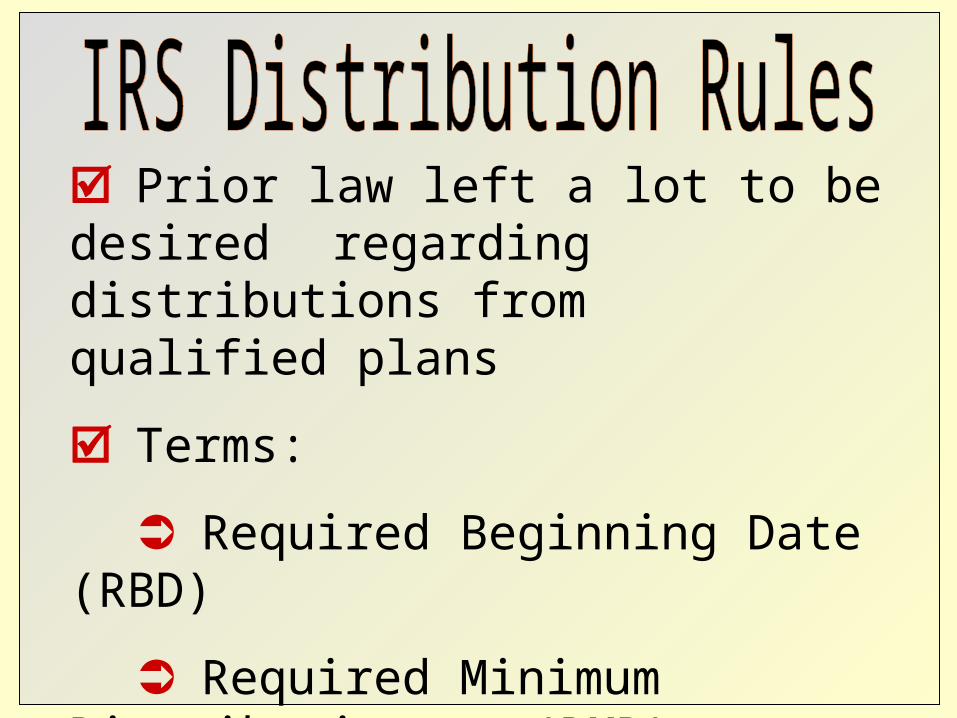

Prior law left a lot to be desired regarding distributions from

qualified plans

Terms:

Required Beginning Date (RBD)

Required Minimum Distribution (RMD)

The date when a participant MUST begin taking their retirement money

IRAs – required at 70½

Non-IRAs – normally at 70½, but later is possible

A Roth IRA has no RBD for the account holder

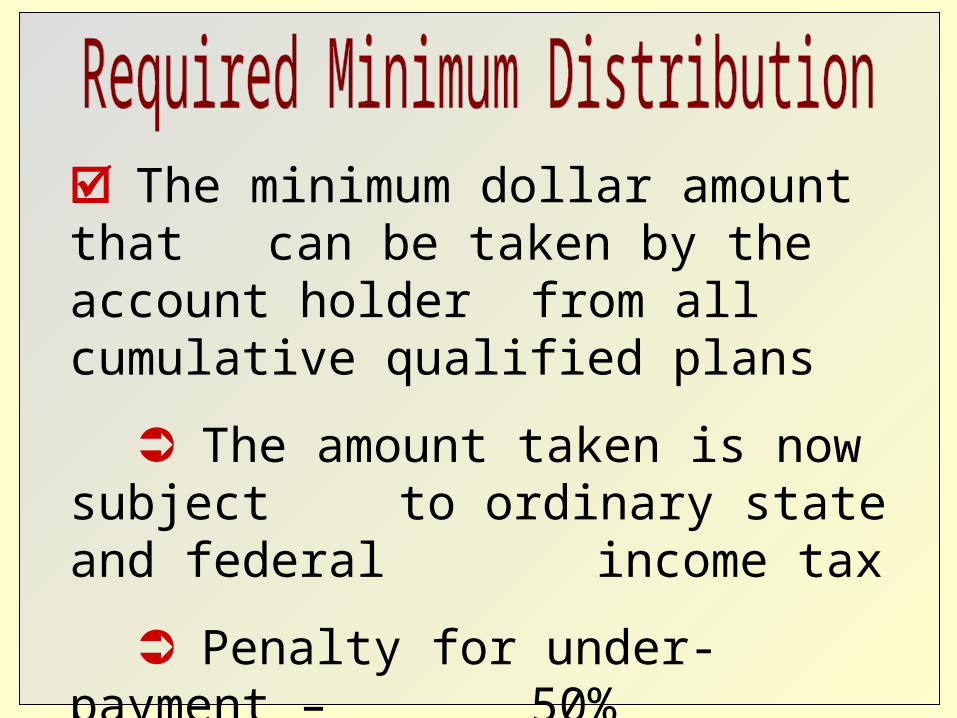

The minimum dollar amount that can be taken by the account holder from all cumulative qualified plans

The amount taken is now subject to ordinary state and federal income tax

Penalty for under-payment – 50%

This year the account holder’s RMD was $40,000 … but took nothing.

The financial institution is required to “rat” you out! Now look what happens with the IRS:

This year the account holder’s RMD was $40,000 … but took nothing.

The financial institution is required to “rat” you out! Now look what happens with the IRS:

$20,000 penalty… that really

hurts!

18

Roll-Under … Now What is That?

Using Annuities and Life Insurance to greatly increase the ultimate payout ...

and with possible tax advantages.

- Take a distribution from all Q-Plans (maybe rolling to an annuity) and use to pay for life insurance.

- All payout will be income-tax (and estate tax) free when received by the beneficiaries … but only if the kids are NOT the beneficiaries of

the qualified plans!

18

Roll-Under … How Does It Work? Bob currently has his 3 children listed as

beneficiary of his $1.5 million in the Q-Plans

Bob – age 70 – qualifies for a $1.5 million life policy ($42,000 annual premium). (ILIT owns, pays and beneficiary)

Bob “rolls” all his Qualified money into an annuity and takes @$65,000 annually (taxable = @ $42,000 after-tax)

Bob names his favorite charity the beneficiary of his Qualified Annuity

18

Roll-Under … How Does It Work? Upon Bob’s death … the charity receives the

remainder value of his annuity and his estate receives a tax deduction on his last tax return.

The kids receive NONE of the Q-Plan proceeds nor do they have any tax liability on these

proceeds.

Upon Bob’s death … the ILIT receives the $1.5 free of any tax.

Upon Bob’s death … each child receives – from the ILIT – $500,000 free of any tax.

Using Life Insurance at Older Ages

20

Pro’s and Con’s

What Type of Life

Insurance is Best for this

Need? 19

Permanent or Term Insurance

11

Term Insurance

Permanent Life

WL - UL - VUL

19

- Charitable Gifting Uses

21

State Road 5021

State Road 5021

State Road 50

3%$7,500

21

Can You Deduct the

Premium?

Gifting Issues

Ownership / Beneficiary

Issues21

Permanent

Permanent Life

WL - UL - VUL

Existing Policies no longer needed??

22

- Pension Payout Protection

23

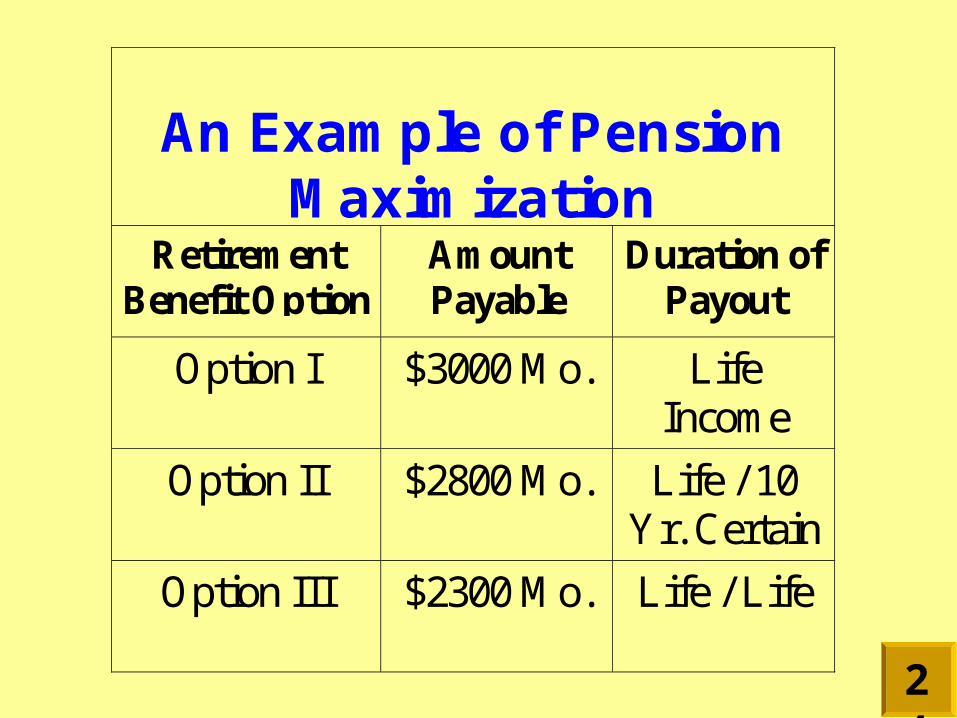

An Example of PensionMaximization

RetirementBenefit Option

AmountPayable

Duration ofPayout

Option I $3000 Mo. LifeIncome

Option II $2800 Mo. Life / 10Yr. Certain

Option III $2300 Mo. Life / Life

24

Permanent

Permanent Life

WL - UL - VUL

Existing Policies??

23

- Equalize Inheritance

25

26

Using Life Insurance to Equalize an Inheritance

Dad owns business - $1,000,000 value

Daughter active in the business - being groomed to take it over

Son - not involved in the business

Dad dies - 50/50 to each child

26

Using Life Insurance to Equalize an Inheritance

Dad owns business - $1,000,000 value

Daughter active in the business - being groomed to take it over

Son - not involved in the business

Dad dies

- 50/50 to each child

26

Using Life Insurance to Equalize an Inheritance

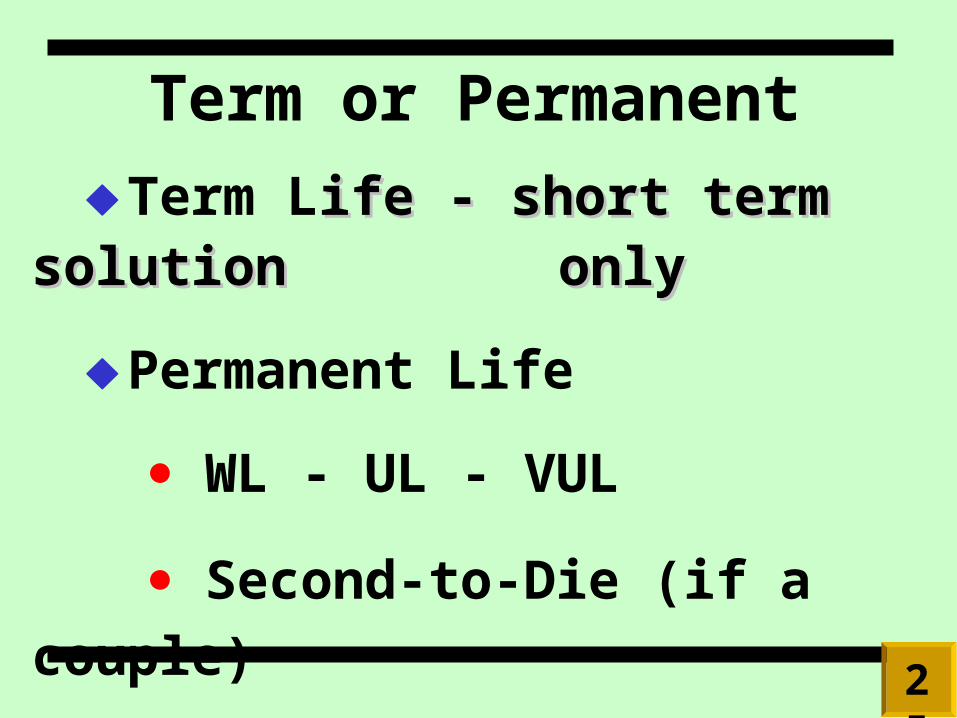

Term or Permanent

Term Life - short term solution ife - short term solution onlyonly

Permanent Life

WL - UL - VUL

Second-to-Die (if a couple)

25

Top Five Life Top Five Life Insurance NeedsInsurance Needs

Jerry RhinehartJerry Rhinehart

Panama City, FLPanama City, FL