© the mcgraw-hill companies, inc., 2008 mcgraw-hill/irwin chapter 14 regulating the financial...

TRANSCRIPT

© The McGraw-Hill Companies, Inc., 2008McGraw-Hill/Irwin

Chapter 14

Regulating the Financial System

14-2

Regulating the Financial System:The Big Questions

1. What are the sources and consequences of financial fragility?

2. What is the role of the government in the financial system?

3. How does financial regulation and supervision work?

14-3

Regulating the Financial System:Roadmap

• Runs, Panics & Financial Crises

• The Government Safety Net

• Regulation and Supervision

14-4

Financial Crisis

• Since the 1970s:– 93 Countries– 117 system-wide crises– 51 smaller disruptions– No part of the world has been spared

14-5

Size of Financial Crisis vs. Change in GDP Growth

14-6

Bank Runs, Bank Panics, and Financial Crises

• Sources of Bank Runs:– Promise depositors withdrawal on demand– First come, first served

• Suppose depositors lose confidence?• Concern over insolvency can lead to

illiquidity.• Bank run can be the result of both real

and imagined problems

14-7

Bank Panics

• Run on a single bank can turn into a system-wide panic.

• Asymmetric information:Can’t distinguish good from bad banks.

• Concern about one bank can create panic about all banks.

14-8

Bank Panics

• Cyclical downturns are associated with bank panics

• Look at the period prior to the Federal Reserve, 1871-1913– Eleven business cycles– Bank panics during 7 recessions– No panics without recessions.

14-9

The Government Safety Net:Why?

• Depositor protection – Government is obligated to protect small

deposits unable to judge the soundness of financial institutions

• Protect customers from exploitation– Large institutions can raise prices

• Ensure financial stability– System is inherently unstable

14-10

The Government Safety Net:Unique Role of Depository Institutions

• We rely heavily on depository institutions (banks) for access to the payments system

• If banks disappeared, we would have a difficult time making payments

• Furthermore, banks are prone to runs• The result is that banks receive a

disproportionate amount of the attention of regulators

14-11

The Government Safety Net:Component Parts

• Lender of Last Resort

• Deposit Insurance

• Regulation

• Supervision

• Examination

14-12

• The SIPC insures investors from fraud

• If a brokerage firm fails and you don’t receive the securities you purchased, you are insured

• The SIPC does NOT insure you against making poor investments

14-13

The Government Safety Net:Lender of Last Resort

• Lend to solvent but illiquid banks

• Can authorities tell the difference?

14-14

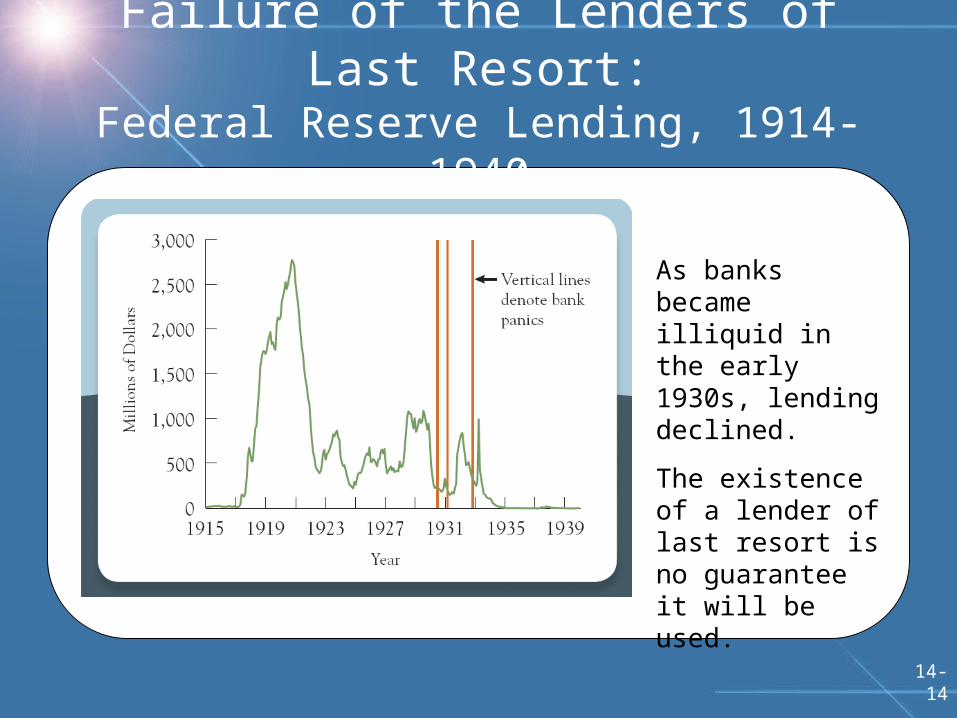

Failure of the Lenders of Last Resort:Federal Reserve Lending, 1914-1940

As banks became illiquid in the early 1930s, lending declined.

The existence of a lender of last resort is no guarantee it will be used.

14-15

• On Nov 20, 1985 there was a software error at Bank of New York

• Made payments without receiving funds

• Borrowed $23 billion

• Success of Lender of Last Resort:Problem at one bank didn’t become a system-wide crisis

14-16

The Government Safety Net:Deposit Insurance

• Means depositors (liability holders) are indifferent to the risk taken by the bank’s managers

• Creates moral hazard

14-17

“Each depositor insured to $100,000.”

• Insurance covers individuals

• Accounts at different banks are insured separately

• Retirement savings are insured separately and have a higher limit, currently $250,000

14-18

The Government Safety Net:The Problems it Creates

• Creates moral hazard• Before deposit insurance banks had debt

to equity of 4 to 1, today it is 13 to 1

• Too-big-to-fail policy– Care more about the largest institutions.– Gives banks an incentive to become large and

then take on too much risk.

14-19

• Higher levels of deposit insurance are associated with more risk-taking at banks.

• Explicit deposit insurance may make financial crises more likely

14-20

Regulation

• Banks have more than one regulator

• Creates regulatory competition

14-21

Regulation:Who Regulations Whom?

14-22

Regulation

• Restrictions on competition– Greater competition leads to more risk to survive.

• Asset holding restrictions– Can’t hold stocks,

• Minimum capital requirements– Capital acts as buffer, has to be big enough.

• Disclosure requirements– Allows regulators and financial markets to assess

quality of the institution

14-23

Supervision and Examination

• Regular visits from examiners

• Check that loan collateral exists

• Evaluate past-due loans to see that banks write them off

• Rate banks (CAMELS)

14-24

• Global competition requires global rules• If one bank can hold less capital than

another, it will have an advantage• The Basel Accord tries to make bank

regulation more uniform across countries• Recent changes are improving the system,

but the details are complex

© The McGraw-Hill Companies, Inc., 2008McGraw-Hill/Irwin

Chapter 14

End of Chapter