0 annet aris sviaz-expocomm day of mass communication may10, 2011 strategic outloook for media:...

Post on 18-Dec-2015

219 views

TRANSCRIPT

1

Annet Aris

SVIAZ-Expocomm

Day of Mass Communication

May10, 2011

Strategic outloook

for media:

technology,

economy, content

Copyright 2011 Annet Aris. No part of it may be circulated, quoted, or reproduced for distribution without prior written approval from Annet Aris. This material was used by Annet Aris during an oral presentation; it is not a complete record of the discussion.

2

Is the digitization of media a blessing or a curse?

Blessings Curses

More consumer value: transparency, access, choice, own contribution

Higher advertising „Return on Investment“: better targeting, measuring, performance based pricing

Lower costs: production,distribution, storage

Lower willingness to pay, piracy

Exponential growth of advertising inventory

Winner takes it all?

Source: Annet Aris

For discussion

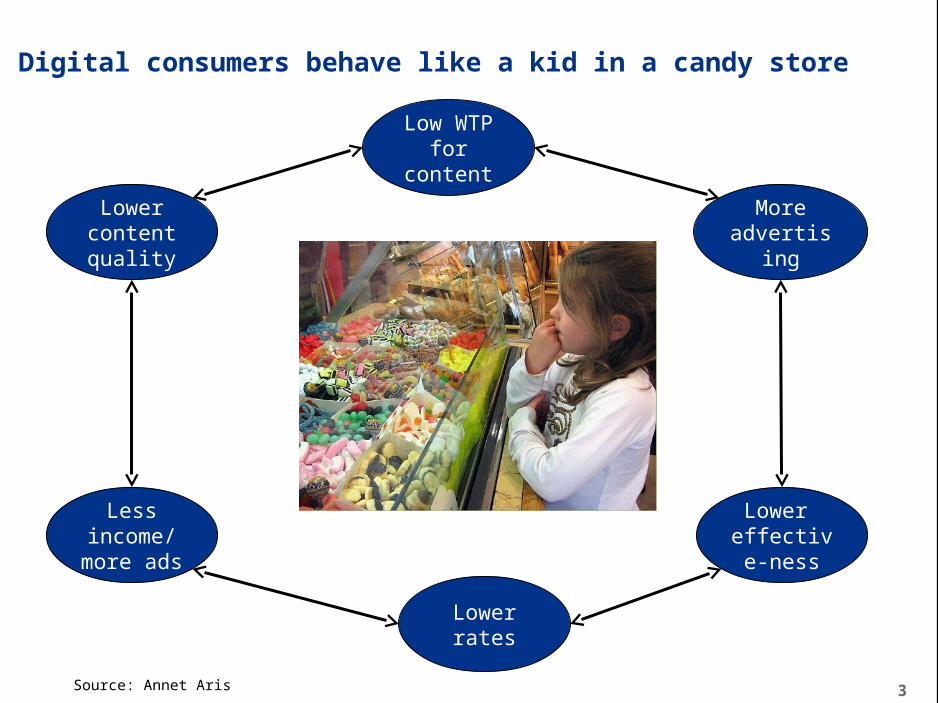

Digital consumers behave like a kid in a candy store

3

Lower rates

More advertising

Lower effective-

ness

Low WTP for content

Less income/

more ads

Lower content quality

Source: Annet Aris

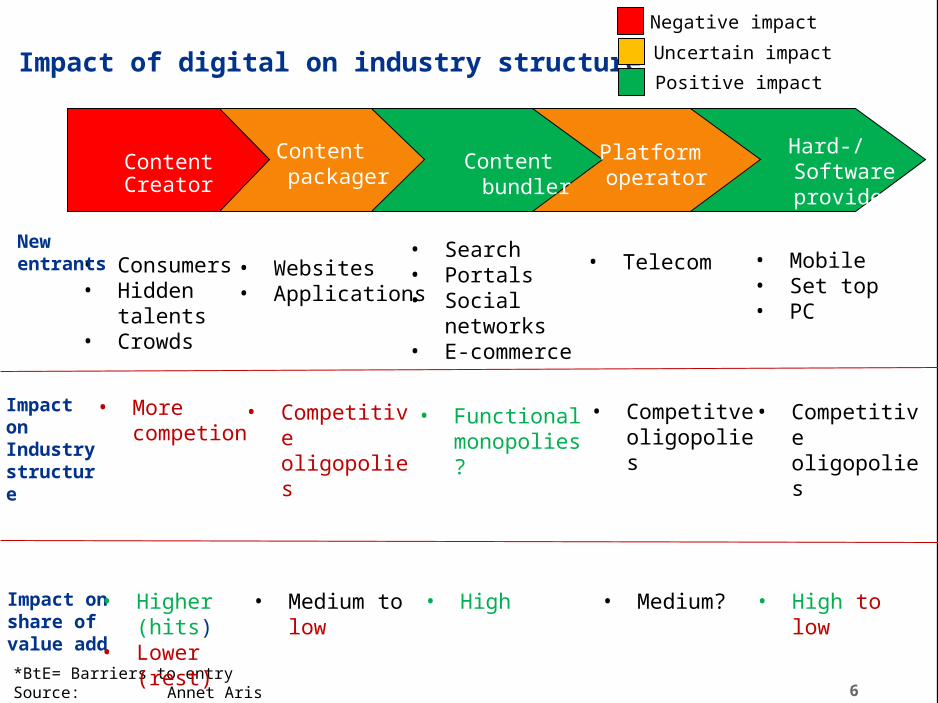

Impact of digitization on industry structure

4

Key characteristics• No competition• High barriers to entry• High profitability• Low consumer benefits

Monopoly OligopolyPerfect competition

• Limited competition• Medium barriers to entry• Profitability depends on

industry conduct• Medium to high consumer

benefits

• High competition• Low Barriers to entry• Low profitability• Medium to high consumer

benefits

Examples • US telco’s/cable co’s• US local newspapers

• TV broadcasters• German magazines• Music majors

• Independent TV producers

• Free lance journalists• Book publishing

Impact digitization

Source: Annet Aris

5

• Pay TV• Cable operators• (Retailers)

• Terrestial• Satelitte• Cable

Industry structure in the analogue media world

Exam-ples

Source: Annet Aris

• TV • Game console

• TV channels• Newspapers/

magazines• Music majors• Book publishers• Game publishers• Radio channels

• Artists• TV/Movie

Producers• Sport

associations• Journalists

Content CreatorContent packager Platform operator

Content bundlerHard-/ Software

provider

Industry structure

• Mostly competion

• Some oligopoly Hollywood)

• Monopoly for owners of hit rights

• Mostly well behaved oligopolies

• BtE: distribution scarcity, purchasing power

• Monopoly or competitve oligopoly

• Some competion between small retailers

• Monopolies or oligopolies

• BtE: investment in infrastructure

• Competitive oligopolies

• BtE: IP, investment in production facitlities

Share of value add

• High (hits)• Low (rest)

• High to medium • High to low • High to medium• Medium to low

6

• Search• Portals• Social

networks• E-commerce

• Telecom

Impact of digital on industry structure

*BtE= Barriers to entrySource: Annet Aris

• Mobile• Set top• PC

• Websites• Applications

• Consumers• Hidden

talents• Crowds

Content CreatorContent packager Platform operator

Content bundlerHard-/ Software

provider

Impact on Industry structure

• More competion

• Competitive oligopolies

• Functional monopolies?

• Competitve oligopolies

• Competitive oligopolies

Impact on share of value add

• Higher (hits)• Lower (rest)

• Medium to low

• High • Medium? • High to low

Negative impact

Positive impact

Uncertain impact

New entrants

7

• Pay TV• Cable

operators

• Portal• Search

• Mobile operators

• Terrestial• Satelitte• Cable

• ISP‘s

• Telco‘s• FVNO

• Mobile operators

• MVNO‘S

Convergence of platforms leads to vertical integration

Video

Inter-net

Fixed Line voice

MobileVoice

Source: Annet Aris

• TV • Set top box

• PC• Game consoles

• Telephone manufacturers

• Mobile phone manufacturers

• TV channels• Free• Pay

• Content sites

• Mobile operators

• TV/Movie Producers

• Sport associations

• Webeditors• Users

• User

• User• Mobile

content developers

Content Creator Content packager

Platform operator

Content bundlerHard-/ Software

provider

• Pay TV• Cable

operators

• Portal

• Mobile operators

• Terrestial• Satelitte• Cable

• ISP‘s

• Telco‘s• FVNO

• Mobile operators

• MVNO‘S

• TV channels• Free• Pay

• Content sites

• Mobile operators

• TV/Movie Producers

• Sport associations

• Webeditors• Users

• User

• User• Mobile

content developers

8

Convergence drives integration

Video

Inter-net

Fixed Line voice

MobileVoice

Source: Annet Aris

• TV • Set top box

• PC• Game consoles

• Telephone manufacturers

• Mobile phone manufacturers

Content Creator Content packager

Platform operator

Content bundlerHard-/ Software

provider

• Pay TV• Cable

operators

• Portal

• Mobile operators

• Terrestial• Satelitte• Cable

• ISP‘s

• Telco‘s• FVNO

• Mobile operators

• MVNO‘S

• TV channels• Free• Pay

• Content sites

• Mobile operators

• TV/Movie Producers

• Sport associations

• Webeditors• Users

• User

• User• Mobile

content developers

9

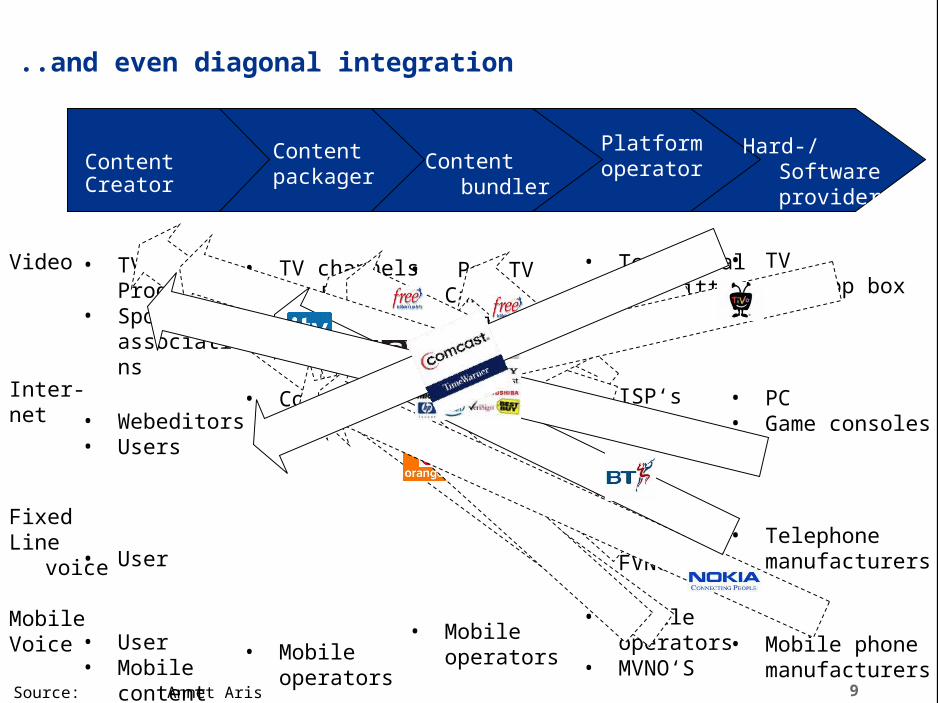

..and even diagonal integration

Video

Inter-net

Fixed Line voice

MobileVoice

Source: Annet Aris

• TV • Set top box

• PC• Game consoles

• Telephone manufacturers

• Mobile phone manufacturers

Content Creator Content packager

Platform operatorContent bundler

Hard-/ Software provider

10

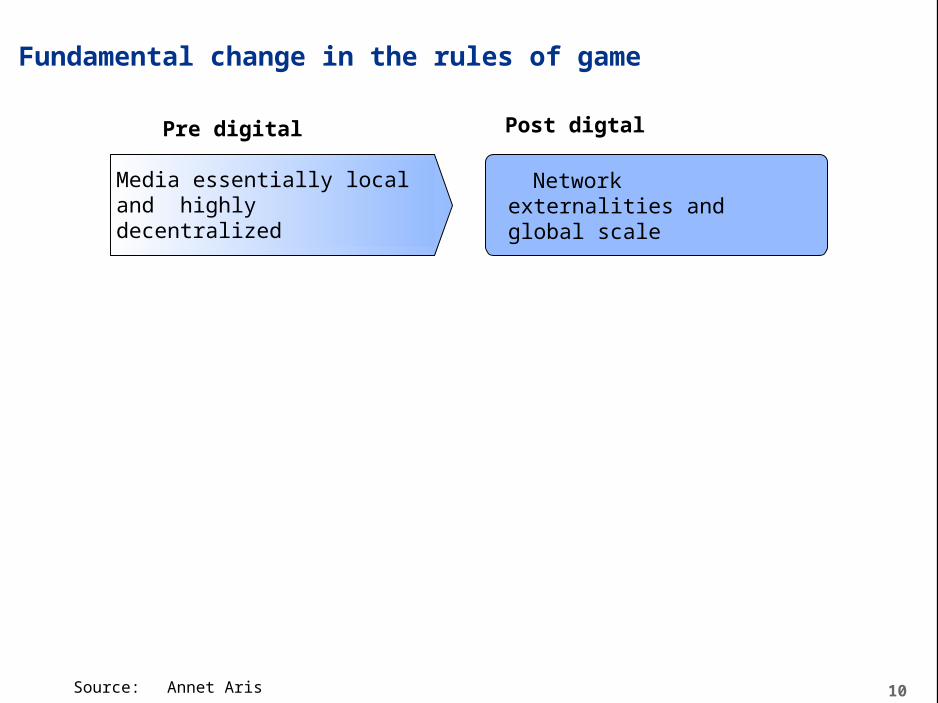

Media essentially local and highly decentralized

Network externalities and global scale

Pre digital Post digtal

Fundamental change in the rules of game

Source:Annet Aris

Apple’s ecosystem

11

Apps

iBooks

AdsiTunes

account

iTunes account

Google creates major network benefits through systematic learning

12Adwords Adsense Admob

ContinuousExperimenting and

Learning !

Network effect

Cost effectSource: Annet Aris

13

Mass marketing Customer lifetime value

Media essentially local and highly decentralized

Succes increasingly driven by network externalities and global scale

Pre Internet Post Internet

Fundamental change in the rules of game

Source:Annet Aris

Company based competition Ecosystem based competition

Exposure based advertising Marketing ROI

14

Media in the future: who will

win?

When we are not careful:

nobody!

IMPLICATIONS FOR MEDIA COMPANIES

• Less is more: prevent the negative content/advertising spiral, go for high impact content and advertising

• Focus more on how to grow the digital pie together rather than on how to share the pie

• Don’t reinvent the wheel: Learn and create own network effects (content communities?)

• Innovate not only content and medium but also business models, dare to take risks based on your consumer insights..

• Build the right capabilities for a volatile world (people, organization)

15