1 federal office of private insurance philipp keller research & development düsseldorf, 16...

Post on 21-Dec-2015

212 views

TRANSCRIPT

1

Federal Office of Private Insurance

Philipp Keller

Research & Development

Düsseldorf, 16 January 2007

Der Schweizer Solvenztest und Risk Management

2

Overview

Risk and Capital Management

Internal Models

Economic Balance Sheet

Scenarios

Limit SystemGroup

Diversification

Responsibilities

Valuation

Risk Based Supervision

Risk Mitigation and Transfer

3

Contents

•Principles-Based Supervision•Swiss Solvency Test Methodology•Market Consistent Valuation• Internal Models•Scenarios•Risk and Capital Management•Outlook

Risk and Capital Management

Internal Models

Economic Balance Sheet

Scenarios

Limit SystemGroup

Diversification

Responsibilities

Valuation

Risk Based Supervision

Risk Mitigation and Transfer

4

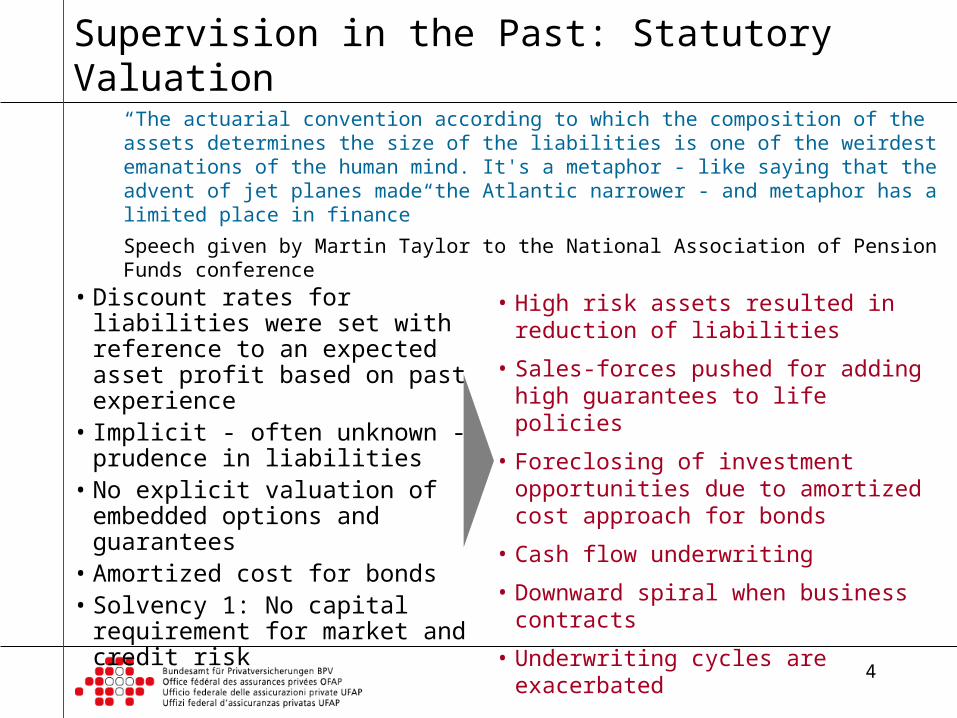

Supervision in the Past: Statutory Valuation

• Discount rates for liabilities were set with reference to an expected asset profit based on past experience

• Implicit - often unknown - prudence in liabilities

• No explicit valuation of embedded options and guarantees

• Amortized cost for bonds• Solvency 1: No capital

requirement for market and credit risk

• High risk assets resulted in reduction of liabilities

• Sales-forces pushed for adding high guarantees to life policies

• Foreclosing of investment opportunities due to amortized cost approach for bonds

• Cash flow underwriting

• Downward spiral when business contracts

• Underwriting cycles are exacerbated

“The actuarial convention according to which the composition of the assets determines the size of the liabilities is one of the weirdest emanations of the human mind. It's a metaphor - like saying that the advent of jet planes made the Atlantic narrower - and metaphor has a limited place in finance”

Speech given by Martin Taylor to the National Association of Pension Funds conference

5

Correlation between Solvency 1 and SST

Risk bearing capital / target capital

Sol

ven

cy 1

rat

io

Nonlife

correlation -0.178

Risk bearing capital / target capital

Sol

ven

cy 1

rat

io

correlation 0.56

Life

The correlation between the Solvency 1 ratio and the SST solvency ratio is 0 for nonlife and approx. 0.5 for life (based on provisional data from field test 2006)

6

Rules- vs. Principles-Based Supervision

Underlying most arguments against the free market is a lack of belief in freedom itself, Milton Friedman

Regulator A system promoting a free and liberal market

The market decides which companies succeed or fail

A system trying to define and micro-manage the

insurance market

Rule Based Approach Principles Based Approach

The “5-year plan” approach to regulation

The complexity grows over time, the system needs to be adapted continuously to new products

The system needs to promote competition, punish collusion and create a level playing field via risk based capital requirements and transparency

Regulator

Liberal Insurance Market

Dirigistic Insurance Market

Regulation: A system of laws, decrees, rules, principles, implicit and explicit conventions and expectations, incentives, rewards and punishments, etc.

7

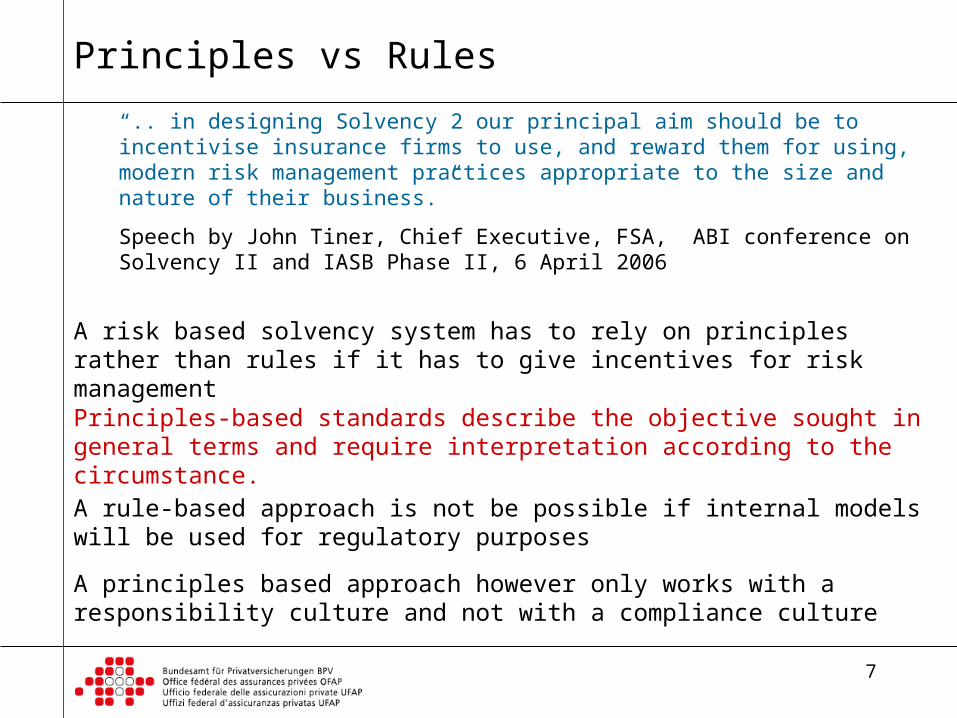

Principles vs Rules

“.. in designing Solvency 2 our principal aim should be to incentivise insurance firms to use, and reward them for using, modern risk management practices appropriate to the size and nature of their business.”

Speech by John Tiner, Chief Executive, FSA, ABI conference on Solvency II and IASB Phase II, 6 April 2006

A risk based solvency system has to rely on principles rather than rules if it has to give incentives for risk management

Principles-based standards describe the objective sought in general terms and require interpretation according to the circumstance.

A rule-based approach is not be possible if internal models will be used for regulatory purposes

A principles based approach however only works with a responsibility culture and not with a compliance culture

8

Elements of Supervision

Board of Directors

Actuarial Profession

Supervisor

Accounting Profession

Risk Management

Senior Management

Internal Audit

Responsible Actuary

Professional guidance and enforcement of code of conduct

Direct supervision and check that oversight responsibilities are implemented

Principles based supervision will depend on a web of relationships between the company, professional bodies and the supervisor

For a liberal, principles based approach to function, all have to see to it that the system of checks and balances works

Indirect supervision to ascertain that professional standards are defined and in-line with regulatory expectations

Implications for supervision: closer contact and dialogue with the board, professional bodies and all relevant functions within the company

9

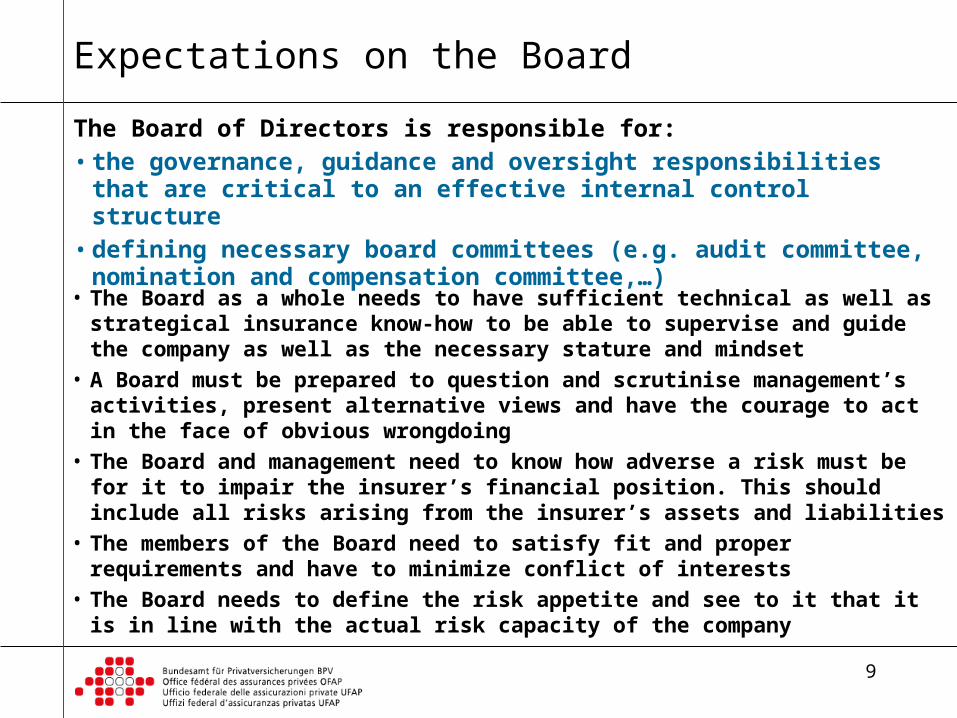

Expectations on the Board

The Board of Directors is responsible for:• the governance, guidance and oversight responsibilities that

are critical to an effective internal control structure• defining necessary board committees (e.g. audit committee,

nomination and compensation committee,…)

• The Board as a whole needs to have sufficient technical as well as strategical insurance know-how to be able to supervise and guide the company as well as the necessary stature and mindset

• A Board must be prepared to question and scrutinise management’s activities, present alternative views and have the courage to act in the face of obvious wrongdoing

• The Board and management need to know how adverse a risk must be for it to impair the insurer’s financial position. This should include all risks arising from the insurer’s assets and liabilities

• The members of the Board need to satisfy fit and proper requirements and have to minimize conflict of interests

• The Board needs to define the risk appetite and see to it that it is in line with the actual risk capacity of the company

10

Elements of Supervision

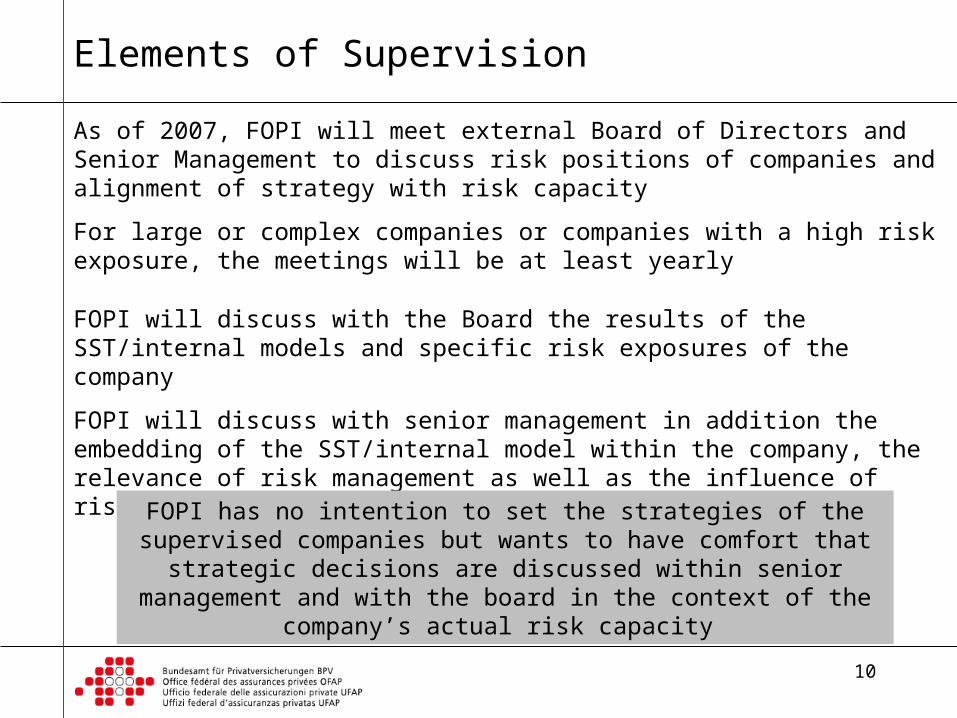

FOPI will discuss with the Board the results of the SST/internal models and specific risk exposures of the company

FOPI will discuss with senior management in addition the embedding of the SST/internal model within the company, the relevance of risk management as well as the influence of risk on the strategic

As of 2007, FOPI will meet external Board of Directors and Senior Management to discuss risk positions of companies and alignment of strategy with risk capacity

For large or complex companies or companies with a high risk exposure, the meetings will be at least yearly

FOPI has no intention to set the strategies of the supervised companies but wants to have comfort that strategic decisions are discussed within senior management and with the board

in the context of the company’s actual risk capacity

11

Contents

•Principles-Based Supervision•Swiss Solvency Test Methodology•Market Consistent Valuation• Internal Models•Scenarios•Risk and Capital Management•Outlook

Risk and Capital Management

Internal Models

Economic Balance Sheet

Scenarios

Limit SystemGroup

Diversification

Responsibilities

Valuation

Risk Based Supervision

Risk Mitigation and Transfer

12

Swiss Solvency Test: Principles1. All assets and liabilities are valued market

consistently

2. Risks considered are market, credit and insurance risks

3. Risk-bearing capital is defined as the difference of the market consistent value of assets less the market consistent value of liabilities, plus the market value margin

4. Target capital is defined as the sum of the Expected Shortfall of change of risk-bearing capital within one year at the 99% confidence level plus the market value margin

5. The market value margin is approximated by the cost of the present value of future required regulatory capital for the run-off of the portfolio of assets and liabilities

6. Under the SST, an insurer’s capital adequacy is defined if its target capital is less than its risk bearing capital

7. The scope of the SST is legal entity and group / conglomerate level domiciled in Switzerland

8. Scenarios defined by the regulator as well as company specific scenarios have to be evaluated and, if relevant, aggregated within the target capital calculation

Defi

nes O

utp

ut

9. All relevant probabilistic states have to be modeled probabilistically

10. Partial and full internal models can and should be used. If the SST standard model is not applicable, then a partial or full internal model has to be used

11. The internal model has to be integrated into the core processes within the company

12. SST Report to supervisor such that a knowledgeable 3rd party can understand the results

13. Public disclosure of methodology of internal model such that a knowledgeable 3rd party can get a reasonably good impression on methodology and design decisions

14. Senior Management is responsible for the adherence to principles

Defi

nes H

ow

-to

Tra

nsp

are

ncy

13

Swiss Solvency Test: Basic Equations

Most capital models consist of two basis components:• A valuation V(.) is a mapping from the space of financial

instruments (assets and liabilities) in R:

V: A * L R, where A * L is the space of all assets and liabilities

• A risk measure rm(.) of a random variable (e.g. VaR, TVaR,…)

SCR = - rm( AC(1) – AC(0) )

Available capital at time t: random variable

Available capital at time 0: known

AC(t) = V(A(t))-V(L(t)), t=0,1

Valuation: Market consistent Risk Measure: Expected Shortfall

For the SST:

14

Market Value Margin

Available capital SCR: Required capital

for 1-year risk

Discounted best estimate of liabilities

Free capital

Market consistent value of liabilities

Market value of assets

Cost of Capital Margin

Market value of the replicating portfolio

The Economic Balance Sheet

The market consistent (economic) balance sheet

15

Risk as Change of Available Capital

Year 0

Best estimate of liabilities

Market Value Margin

Available Capital

Market value of assets

Catastrophes

Claims

Revaluation of liabilities due to new information

New business during one year

Change in market value of assets

Economic balance sheet at t=0 (deterministic)

Economic balance sheet at t=1 (stochastic)

Probability density of the change of available capital

Average value of available capital in the 1% ‚bad‘ cases = TailVaR = -SCR

Probability < 1%

Year 1

Market consistent value of liabilities

Risk quantification via standard models or internal modelsAvailable capital changes

due to random events

16

Standard vs. Internal Models

Risk Quantification:

•Using standard models for life, P&C and health companies, if the standard models capture the risk the companies are exposed to appropriately

•Using internal models for reinsurers, insurance groups and conglomerates and all companies for which the standard model is not appropriate (e.g. if they write substantial business outside of Switzerland)

The use of an internal model is the default option, the standard models can only be used if they adequately quantify the company‘s risks

17

Market Consistent Valuation

Market Consistent Value of Liabilities: Best Estimate + MVM:

= market value (if it exists); or

= value of a replicating portfolio of traded financial instruments + cost of capital margin for remaining basis risk as a proxy for the MVM

Replicating portfolio: a portfolio of financial instruments which are traded in a deep, liquid market, with cash flow characteristics matching either the expected cash flows of the policy obligations or, more generally, matching the cash flows of the policy obligations under a number of financial market scenarios (IAIS Structure Paper)

Simple version (replication of expected cash flows): Replicating portfolio consists of government bonds, MVM does not contain credit risk component

Complex version (replication of cash flows under a number of financial market scenarios): Replicating portfolio consists of government and corporate bonds, swaps and other derivatives to capture payouts of embedded options and guarantees. MVM contains credit risk component, but basis risk is generally smaller than under the simple replicating portfolio

18

Market Consistent Valuation: Life

•The complexity in a group setting becomes daunting

•The management options/strategy of the company rsp. group needs to be modeled over a long time horizon

•Current discussions with industry: Which simplifications are acceptable

Review of models: Supervisors need to have comfort that the management rules correspond to the actual strategy; the requirements on the technical sophistication of companies increases massively

The theoretically correct method implies the use of multi-year risk models for the whole group taking into account management options per legal entity as well as intra-group capital transfers over the whole duration of the run-off

Profit participation features: The market consistent value of life portfolios containing substantial profit participation features necessitates - in theory – the calculation of the economic and statutory position of the company over the whole run-off of the company.

19

SST Standard Models

Scenarios

Standard Models or Internal Models

Mix of predefined and company specific scenarios

Target Capital SST Report

Market Consistent Data

Market Risk

Credit Risk

Life

P&C

Market Value Assets

Risk Models Valuation Models

Best Estimate Liabilities

MVM

Output of analytical models (Distribution)

Health

Aggregation Method

20

Contents

•Principles-Based Supervision•Swiss Solvency Test Methodology•Market Consistent Valuation• Internal Models•Scenarios•Risk and Capital Management•Outlook

Risk and Capital Management

Internal Models

Economic Balance Sheet

Scenarios

Limit SystemGroup

Diversification

Responsibilities

Valuation

Risk Based Supervision

Risk Mitigation and Transfer

21

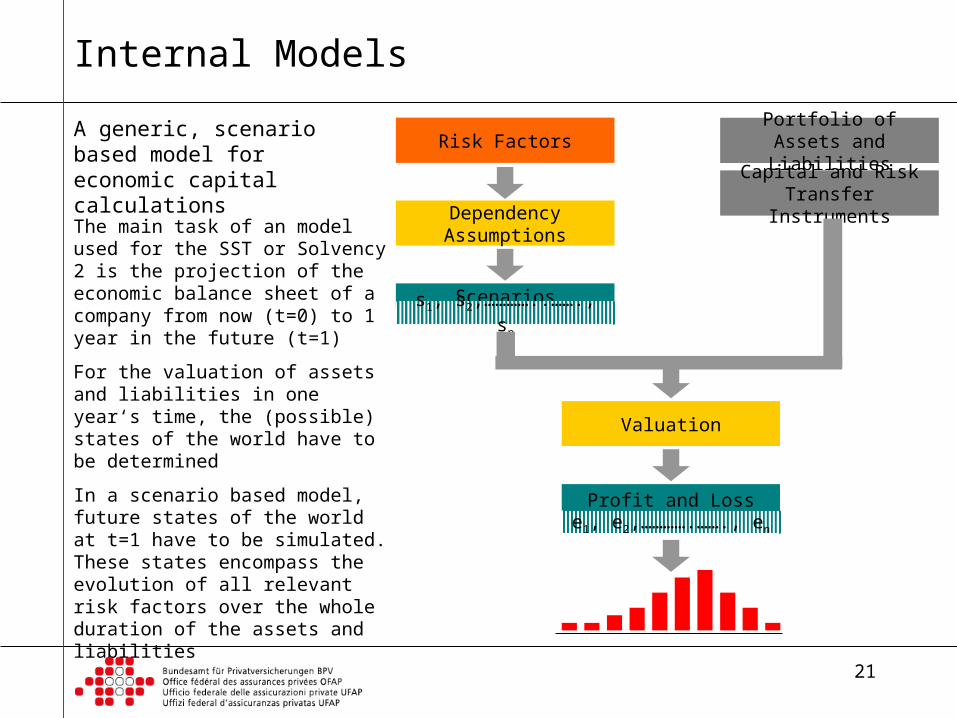

Internal Models

Risk FactorsPortfolio of Assets

and Liabilities

Capital and Risk Transfer InstrumentsDependency

Assumptions

Scenarios

Profit and Loss

Valuation

s1, s2,…………..……., sn

e1, e2,………….……., en

A generic, scenario based model for economic capital calculations

The main task of an model used for the SST or Solvency 2 is the projection of the economic balance sheet of a company from now (t=0) to 1 year in the future (t=1)

For the valuation of assets and liabilities in one year‘s time, the (possible) states of the world have to be determined

In a scenario based model, future states of the world at t=1 have to be simulated. These states encompass the evolution of all relevant risk factors over the whole duration of the assets and liabilities

22

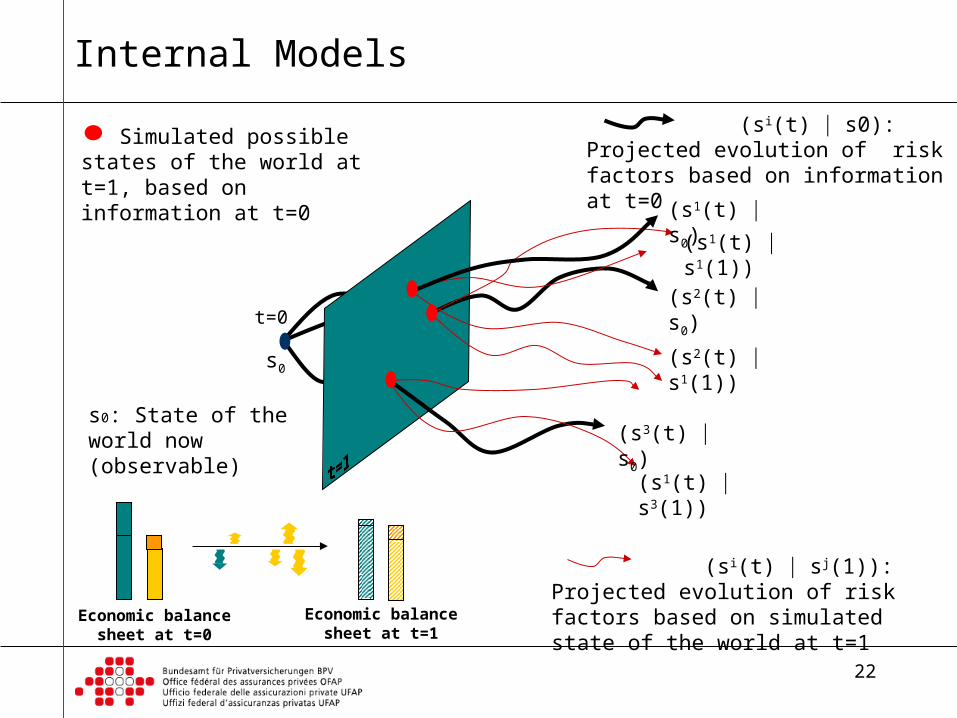

Internal Models

s0: State of the world now (observable)

t=0

s0

(s1(t) s0)

(s2(t) s0)

(s3(t) s0)

(s1(t) s1(1))

(s2(t) s1(1))

(s1(t) s3(1))

Simulated possible states of the world at t=1, based on information at t=0

(si(t) sj(1)): Projected evolution of risk factors based on simulated state of the world at t=1

(si(t) s0): Projected evolution of risk factors based on information at t=0

Economic balance sheet at t=0

Economic balance sheet at t=1

23

Internal Models

The valuation of the economic balance sheet now (t=0) depends on the state of the world now as well as the projection of the risk factors (e.g. the possible evolution of the state of the world) from now until the run-off of assets and liabilities. Risk factors are company specific (interest rates, FX rates, mortalities, catastrophes, etc.)

The valuation of the economic balance sheet in 1 year depends on the simulated states of the world at t=1 as well as projections of the risk factors given the simulate states of the world at t=1

Insurance model are substantially more complex conceptually than most bank models due to the long time horizon of liabilities. The long time horizon makes model not just more difficult to calibrate but qualitatively different from 10 day VaR engines or Basel 2 type credit risk models used by banks.

To make the calculations tractable, most models use simplifications (e.g. using only the expected risk free interest rate for discounting, assuming steady states for the evolution of risk factors etc.). It is then important, that the company is aware of the simplifications and the underlying assumptions

24

Internal Models: Applications

Risk FactorsPortfolio of Assets and

Liabilities

Capital and Risk Transfer InstrumentsDependency

Assumptions

Scenarios

Profit and Loss

Valuation

s1, s2,…………..……., sn

e1, e2,………….……., en

Different valuations (economic, statutory,…) to assess risks for relevant metrics

Analysis of the impact of capital and risk instruments on P&L (e.g. reinsurance, contingent capital,…)

Different risk measures (VaR, TailVaR,…) for various confidence levels to capture risk

Specific scenarios allow detailed analysis of underlying causes of a company‘s risk exposure

Setting of limit systemsCapital allocation

Analysis of liquidity constrains

Impact of changes in mixture of assets and liabilities for ALM, product development, exploring business opportunities, etc.

Analysis of the value of the firm for different investors (policy holders, share holders, bond holders, etc.)

25

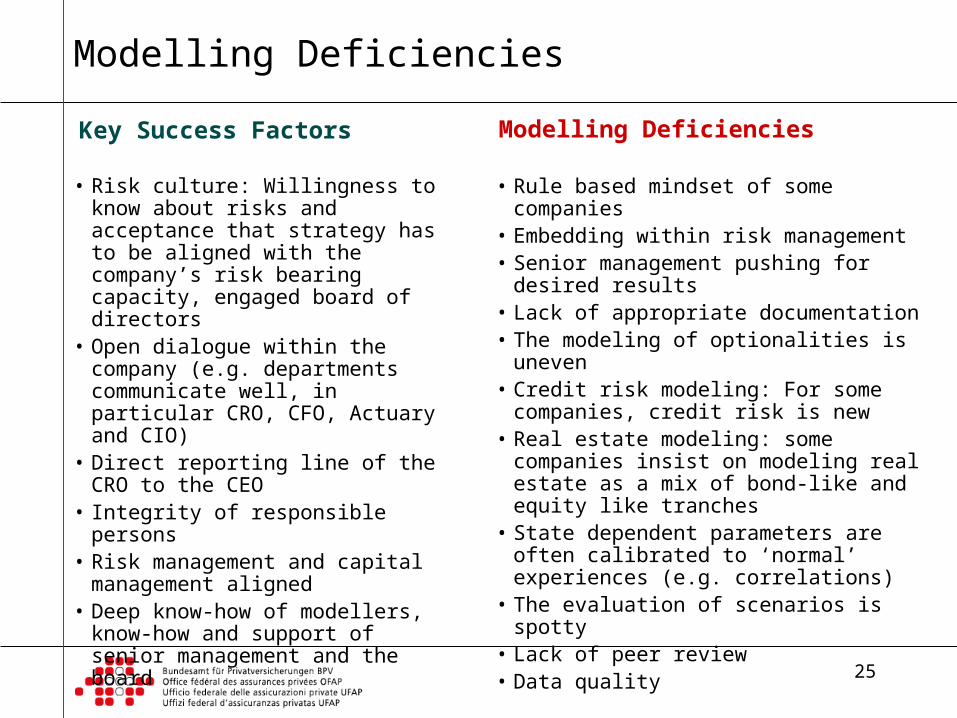

Modelling Deficiencies

• Rule based mindset of some companies• Embedding within risk management• Senior management pushing for desired

results• Lack of appropriate documentation• The modeling of optionalities is uneven• Credit risk modeling: For some

companies, credit risk is new• Real estate modeling: some companies

insist on modeling real estate as a mix of bond-like and equity like tranches

• State dependent parameters are often calibrated to ‘normal’ experiences (e.g. correlations)

• The evaluation of scenarios is spotty• Lack of peer review • Data quality

• Risk culture: Willingness to know about risks and acceptance that strategy has to be aligned with the company’s risk bearing capacity, engaged board of directors

• Open dialogue within the company (e.g. departments communicate well, in particular CRO, CFO, Actuary and CIO)

• Direct reporting line of the CRO to the CEO

• Integrity of responsible persons• Risk management and capital

management aligned• Deep know-how of modellers,

know-how and support of senior management and the board

Key Success Factors Modelling Deficiencies

26

Contents

•Principles-Based Supervision•Swiss Solvency Test Methodology•Market Consistent Valuation• Internal Models•Scenarios•Risk and Capital Management•Outlook

Risk and Capital Management

Internal Models

Economic Balance Sheet

Scenarios

Limit SystemGroup

Diversification

Responsibilities

Valuation

Risk Based Supervision

Risk Mitigation and Transfer

27

Scenarios

Company specific scenarios: Allow senior management and the board to have an informed discussion on strategic decisions

For supervisors, the quality of company specific scenarios is a good indication on the quality of the company’s risk management

Predefined scenarios: Allow the analysis of the risk exposure of the company

For supervisors, they allow a discussion with senior management and the board on the actual risk exposure of the company

Both company specific and predefined scenarios are important tools for supervisors to assess the quality of risk management and the company’s internal processes. They are the basis of an informed dialog of supervisors with senior management and the board of directors

28

Risk Concentrations

• The knowledge about the limitation of risk concentrations is an essential part of risk management

• Insurers need to formulate and evaluate scenarios to identify and quantify its main risk concentrations

• The identification of risk concentrations has to encompass the whole spectrum of risks, and should not be limited to exposures to counterparty only

• Senior management and the board of directors have to be informed on the risk concentrations and the company’s strategy aligned

• The insurer then has to put into place an effective limit system

Scenarios Risk Concentrations

Risk Management

Internal Models

Senior Management

Board of DirectorsStrategy

Limit System

29

Contents

•Principles-Based Supervision•Swiss Solvency Test Methodology•Market Consistent Valuation• Internal Models•Scenarios•Risk and Capital Management•Outlook

Risk and Capital Management

Internal Models

Economic Balance Sheet

Scenarios

Limit SystemGroup

Diversification

Responsibilities

Valuation

Risk Based Supervision

Risk Mitigation and Transfer

30

Risk Management

Warren Buffett‘s three key principles for running a successful insurance business:

February 28, 2002, Warren E. Buffett

• They accept only those risks that they are able to properly evaluate (staying within their circle of competence) and that, after they have evaluated all relevant factors including remote loss scenarios, carry the expectancy of profit. These insurers ignore market-share considerations and are sanguine about losing business to competitors that are offering foolish prices or policy conditions.

• They limit the business they accept in a manner that guarantees they will suffer no aggregation of losses from a single event or from related events that will threaten their solvency. They ceaselessly search for possible correlation among seemingly-unrelated risks.

• They avoid business involving moral risk: No matter what the rate, trying to write good contracts with bad people doesn't work. While most policyholders and clients are honorable and ethical, doing business with the few exceptions is usually expensive, sometimes extraordinarily so.

31

Risk Management

The Need for Probabilistic Thinking

For a risk culture to develop, senior management, the board and supervisors must be able to understand the probabilistic nature of the world

Example: A CRO hedges the risk of interest rates falling since the company is short in duration. Interest rates then increase and the hedge expires worthless. Senior management then criticizes the CRO for „destroying“ profit

Example: A CRO models the exposure to hurricane risk according to industry best-practice but the actual loss is a multiple of the predicted loss. The supervisor then assume wrong-doing and an intentional optimistic assumption to minimize required regulatory capital

In insurance, reality can – and often will be – different from prediction. While only one of the possible outcomes will be realized, there nevertheless are many a-priori potentialities, which the company and risk management have to consider

32

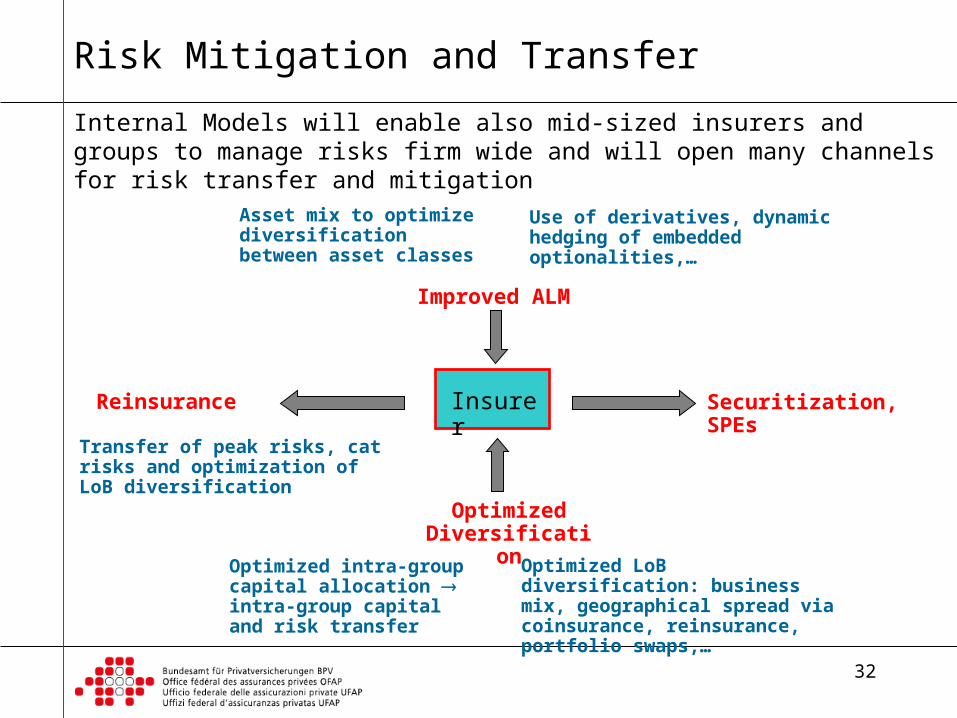

Risk Mitigation and Transfer

Optimized LoB diversification: business mix, geographical spread via coinsurance, reinsurance, portfolio swaps,…

Asset mix to optimize diversification between asset classes

Improved ALM

Securitization, SPEs

Optimized intra-group capital allocation intra-group capital and risk transfer

Use of derivatives, dynamic hedging of embedded optionalities,…

Insurer

Transfer of peak risks, cat risks and optimization of LoB diversification

Internal Models will enable also mid-sized insurers and groups to manage risks firm wide and will open many channels for risk transfer and mitigation

Reinsurance

Optimized Diversification

33

Impressions from the Industry

… Zusammen mit aussenstehenden Aktuaren haben wir die notwendigen, aufwendigen Arbeiten frühzeitig in Angriff genommen und erachten sie als Fitnesstest. Zudem sehen wir die Chance, optimale Beurteilungsgrundlagen für unsere neue Rückversicherungslösung zu erhalten. Die bisherigen Zwischenresultate bestätigen die gute Solvabilität und Risikofähigkeit der emmental.

Geschäftsbericht 2005, Emmental Versicherung

“For our risk and investment strategy we need to be able to quantify the cash flow structure and the risk bearing capacity of our portfolios. For this the SST is a good (although in many aspects still to be modified and enhanced) basis. In addition, we can use the SST to test capital requirements for alternative investment strategies. As we have not yet an equally well suited internal model, the SST is for us of great benefit. We see it as an integral part within our ALM process.”

Comment by René Bühler from the “National Versicherung

“[The SST] produces a lot of interesting data, and we now know more about the company and understand its business better. Most important of all, however, is that we are now sure we have enough reserves, and we know that the reserves could in fact be smaller.“

Interview with Patrizio Polesana, Metzgerversicherung in ‚Life and Pension Magazine‘

34

Management of Group Diversification

MCR

MCRSCR

MCR

SCR

SCR

The SCRs of a group‘s legal entities can be optimized using capital and risk transfer instruments

The amount of optimization available to the group depends on the definition of the MCR

Legal Entity 2

Legal Entity 1

Legal Entity 3

Capital and risk transfer instruments (CRTI) allow allocation and down-streaming of diversification between different legal entities of a group

35

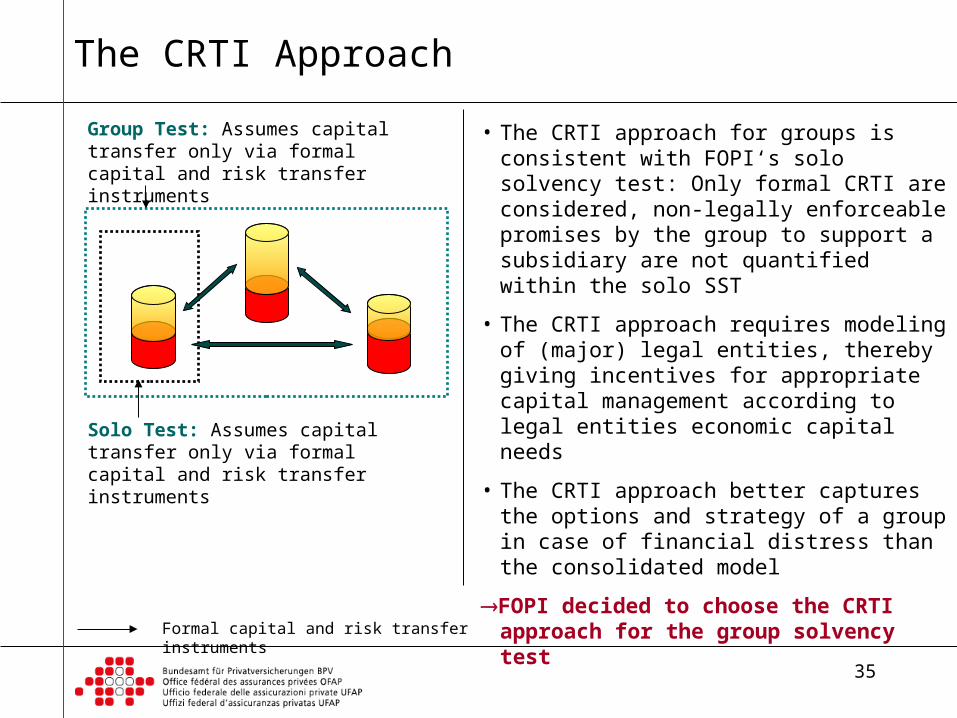

The CRTI Approach

Solo Test: Assumes capital transfer only via formal capital and risk transfer instruments

Group Test: Assumes capital transfer only via formal capital and risk transfer instruments

Formal capital and risk transfer instruments

• The CRTI approach for groups is consistent with FOPI‘s solo solvency test: Only formal CRTI are considered, non-legally enforceable promises by the group to support a subsidiary are not quantified within the solo SST

• The CRTI approach requires modeling of (major) legal entities, thereby giving incentives for appropriate capital management according to legal entities economic capital needs

• The CRTI approach better captures the options and strategy of a group in case of financial distress than the consolidated model

FOPI decided to choose the CRTI approach for the group solvency test

36

CRTI Approach: Risks

The risk of a subsidiary for the parent company is emanating from the change in economic value of the subsidiary and – potentially – from CRTI which will be implemented during a time horizon of one year

A L A L

Subsidiary Parent

A L A L

A L A L

No CRTI in place: The subsidiary is in default, the economic value of the subsidiary for the parent is zero. The CRTI approach takes into account the legally limited liability structure: The model assumes that in case of financial distress, the group will not support a subsidiary if no CRTI are in place

An insolvency protection guarantee from the parent to the subsidiary is in place: The subsidiary is in run-off, the value of the subsidiary for the parent is zero and capital is further depleted due to payout of guarantee

Economic value of subsidiary as asset of the parent

Missing capital of subsidiary is replenished with assets from the parent

Subsidiary ParentAdverse event impacting the subsidiary’s balance sheet, subsidiary is insolvent

37

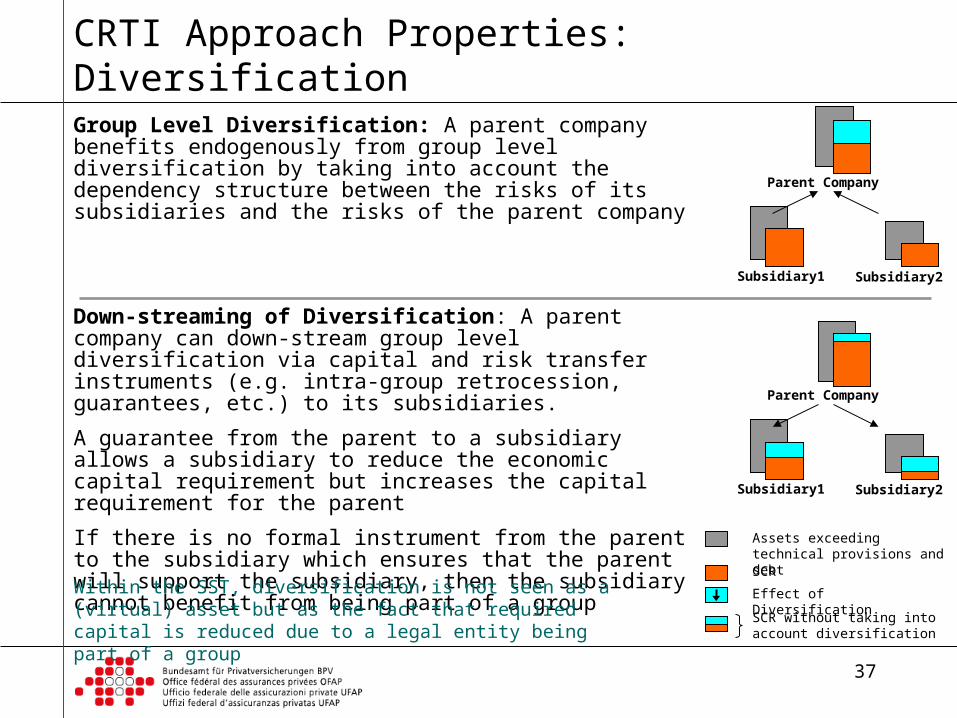

CRTI Approach Properties: Diversification

Group Level Diversification: A parent company benefits endogenously from group level diversification by taking into account the dependency structure between the risks of its subsidiaries and the risks of the parent company

Down-streaming of Diversification: A parent company can down-stream group level diversification via capital and risk transfer instruments (e.g. intra-group retrocession, guarantees, etc.) to its subsidiaries.

A guarantee from the parent to a subsidiary allows a subsidiary to reduce the economic capital requirement but increases the capital requirement for the parent

If there is no formal instrument from the parent to the subsidiary which ensures that the parent will support the subsidiary, then the subsidiary cannot benefit from being part of a group

Subsidiary1 Subsidiary2

Parent Company

Subsidiary1 Subsidiary2

Parent Company

Within the SST, diversification is not seen as a (virtual) asset but as the fact that required capital is reduced due to a legal entity being part of a group

Assets exceeding technical provisions and debtSCR

Effect of Diversification

SCR without taking into account diversification

38

Contents

•Principles-Based Supervision•Swiss Solvency Test Methodology•Market Consistent Valuation• Internal Models•Scenarios•Risk and Capital Management•Outlook

39

Outlook

• A consistent quantification of all risks will demand that many functions within a company work together: actuaries, underwriter, claims managers, RI specialists, CROs, CIOs, CFOs,…

• An economic view of business will demand deeper quantitative skills• Companies will have to optimize their economic performance

optimization of asset liability mismatch, coherent reinsurance programs, securitization of risks, optimization of diversification via coinsurance, geographical spread, etc.

• Mid-sized companies might become being squeezed between smaller, specialized and nimble insurers and large, well diversified insurance groups

• Large companies will have to optimize their risk and capital allocation to maximize diversification

Consequences of an economic and risk based view:

Prediction is very difficult, especially about the future

Niels Bohr

40

Outlook

Main issues:• Group Diversification: Will group level diversification be recognized

or do local supervisors insist on full (physical) capitalization of all legal entities in their territory?

• Legacy Regulation: Will implicit prudence margins, limits on investment, eligibility of assets be replaced with an economic view of risk and transparency or will the old prudence driven approach with supervision coexist with the risk-based solvency framework?

• Internal Models: Will supervisors accept that company-specific risk-based solvency will entail to a certain degree the subjective assessment of re/insurers of their risk exposure or will supervisors prefer to achieve comparability of calculation steps via standard-models rather than comparability of results via internal models?

Whether a pervasive risk culture can develop and lead to an innovative, thriving insurance market depends not only on the re/insurance market, but also on how future regulation will be implemented

41

Outlook

The success of principles based supervision will depend crucially on:

• Trust and an open and informed dialog between the industry and the supervisor

• Development of a responsibility culture the willingness to do the right thing rather than purely complying with a minimal set of rules

• Adequate self-governance of the industry and relevant professional associations (actuaries, accountants,…)

The ultimate responsibility for ascertaining adherence to principles lies with the supervisor but a principles based supervisory framework will depend on devolving responsibility for implementing the principles away from the supervisor to the board of directors, senior management and professional organizations

I believe we are on an irreversible trend toward more freedom and democracy - but that could change

Dan Quayle