1 © supply chainge management ltd. 2008 intensive savings delivery programmes

TRANSCRIPT

1 © supply chainge management ltd. 2008

Intensive Savings Delivery Programmes

2 © supply chainge management ltd. 2008

Intensive Savings Programmes (as an interim manager)

Petro-chemicals

Pan-European Post Acquisition Purchasing Synergies

NOVA acquired four large chemical plants from Shell - giving £ 500m turnover

Replaced McKinsey’s role in previous acquisitions

Led first pan-European supplier conference & intensive negotiation programme

1 year assignment Delivered synergy target in 12 weeks. Exceeded annual savings target too Substantially exceeded client’s expectationsAwarded 2 “applause!” awards & offered the permanent role

Polymer compounding industry Client wanted a review of a selection of spend categories Identified global suppliers using supplier industry research tools incl. India Launched global RFQs and engaged with suppliers Re-negotiated categories based upon global quotations Delivered annual savings target 7% (> £ 400k) in 8 weeks (brand new industry entirely unsupported)

Substantially exceeded client’s expectations Contract extended Invited to examine supply chain improvement opportunities.

3 © supply chainge management ltd. 2008

Pan-European Purchasing Synergies Programme

March April May J une J uly August September October

Resource Requirements • DJ• Analyst/ Indirect Buyer (F/ T 6 months)• Material Technologist (P/ T 6 months -> ongoing)•SAP Purchasing Rep. (F/ T)

Note: this programme does not address $ 0.7m freight opportunities.

Shell Acquisition PurchasingChange ManagementProgramme

Ongoing operational line management roles

Resource Requirements

Project 1a: Raw Materials Synergies - IntensiveDJ (F/ T)+ Analyst (F/ T) + support from NA PS raw matl. leaders

Project 1b: Raw Materials Synergies (ongoing material rationalisation focus) Material Technologist (P/ T)

Project 2: Pallets & Octoboxes Packaging Consultant

Project 3: Pan European Indirect Spend Analysis DJ (F/ T) Analyst/ Indirect Buyer (F/ T) (Global synergies ??)

Programme Management DJ20th March Meeting (Formal Launch ?)

Review Review Review Review J U/ DP/ LH/ DJ & Team

Pan - European Purchasing Operations Management DJ (P/ T) / TBD

Org. Developments

Project 5: SAP (Purchasing) ImplementationDJ (P/ T) & SAP Purchasing Rep. (F/ T)

Systems/ structure review

Project 4: Strategic Pan European Purchasing projects e.g. MRO

Key: Changes from presentation in week 2

Week28/ 2

Week6/ 3

Week20/ 3

Week13/ 3

Week27/ 3

Week3/ 4

Week10/ 4

Week17/ 4

Week24/ 4

Week1/ 5

Week8/ 5

Week15/ 5

Resource Allocation Confirmed (J U)

Consolidate/ Validate Data (Analyst)

Identify Supplier Long Lists by Category – Kompass (DJ )

Prepare for Supplier Meeting (Associate)

Pittsburgh Launch (DJ )

European Launch (DJ )

Launch RFPs to potential suppliers & analysis of quotes (DJ )

Preparation of Presentations “Big Bang” (DJ )

Supplier Communication Day “Big Bang” & subsequent meetings

Preparation of RFQs & nego. dates for current supply base (DJ )

Negotiation Tactics Planning (DJ )

First Round Negotiations (DJ )

Second Round Negotiations (DJ )

Measure Savings (Analyst)

Implement Savings at Sites (Analyst)

Purchasing: Intensive European Synergies (PIES)

Week21/ 5

European Site Meetings (DJ )

DJ 50% availability

Booked holidays & Bank Holidays

??

Helen wants to visit European Sites

Carefully designed & well executed processes...

Project 1a

Process Manual Input Report Data Preparation Stored DataMerge

Predefined Process

Multi-document Manual Process

Create

“Fax- shot”

Spend Data Analysis (from

European Purchasing &/ or

Logistics teams)

Current (2000):

prices

projected volumes

contract details

Continuously

Update Information

& Input

“Fax-shot”(- NA &?)

Eur. Vols by Item

To next page

Obtain Supplier

Databases

Auto send

“Fax-shot”

Supplier

Databases

Merge

“Fax-shot”

to Suppliers

Advise on

Database Selection“Identify

Potential

Suppliers”

PIES Team

“Get the Data Right”

Analyst

Leaders

Technologist

Purchasing: Intensive European Synergies (PIES)Project 1a

Produce RFQ

Material Specifications (from Technology)

Create Supplier European Email Address Book by Category – including existing Eur. & NA suppliers

Specs. vs. volume data

Email RFQs

Email Address Book by

Category

Merge

RFQs to Suppliers

PIES TeamProcess Manual Input Report Data Preparation Stored Data

MergePredefined

Process Multi-document Manual Process

Obtain Information

& Input

Obtain & harmonise specs and volumes

Analyst

Leaders

Technologist

“Responses from

Potential Suppliers

RFQ

Kick Off Communication (by Phone?)

Spend/ Volume Spreadsheet

Create &Email RFQs

Individual Kick-off Communications

Purchasing: Intensive European Synergies (PIES)

Project 1a

Quotation Spreadsheet

Process Manual Input Report Data Preparation Stored Data MergePredefined Process

Multi-document Manual Process

Quotes from

Suppliers

Develop Negotiation

Strategy

Input Quotation Data to

Spreadsheet

Negotiation Priorities

Negotiations for each Material

Contract

Local Copies of Contracts

Copies of contract details to sites

Distribute

Current (2000): prices volumes contract details

MeasureSavings

Reports: 1.Progress 2.Savings

Priorities forMaterial Rationalisation/

Standardisation & SubstitutionNeed an

inspection activity here ?

PIES Team

Analyst

Leaders

Technologist

Negotiation Strategies Negotiation

Update Contracts

Select Suppliers for Negotiation

Measure Savings

Purchasing: Intensive European Synergies (PIES)

4 © supply chainge management ltd. 2008

Prioritising Negotiation Programmes Focus by Supplier

ow

Bottleneck / Collaborative

Strategic

Leverage / Opportunist

Routine / Transactional

Value / Expenditure HiLoLo

Hi

Supply Market Risk / Challengeow

Chance of Success HiLoLo

Hi

Proportion ofProject Spend

Start Here

Start Here

Kraljic

Output: Added focus on highest priority supplierse.g. some suppliers may supply several lower value systems not picked up in key sub-systems

Also need to understand risk (quality, lead time/liquidated damages etc.)

Opportunities for e-auction ?

5 © supply chainge management ltd. 2008

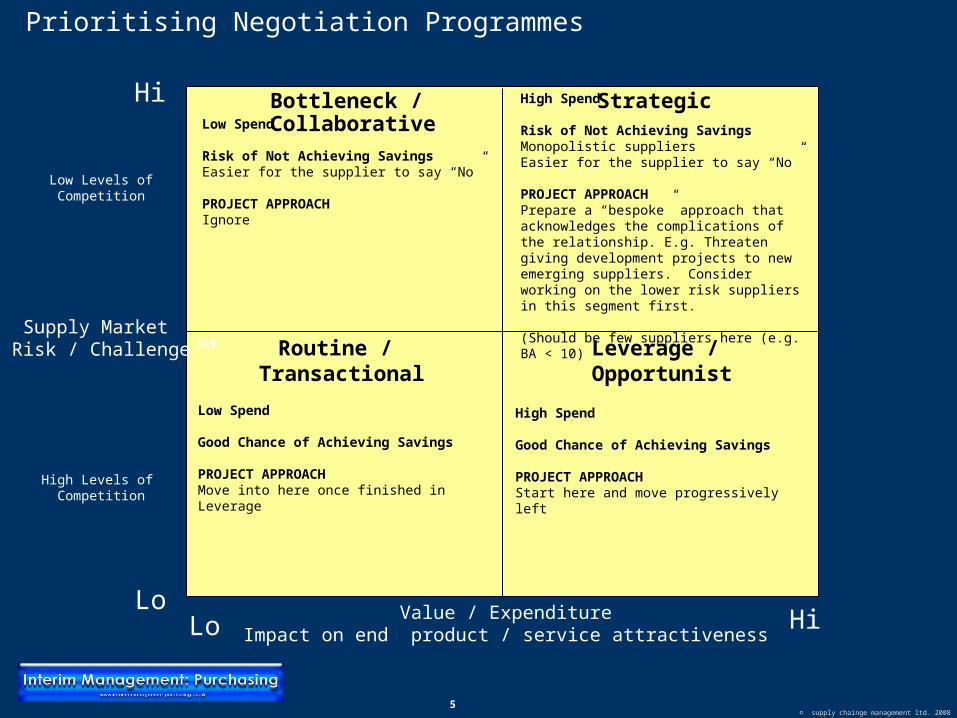

Prioritising Negotiation Programmes

ow

Bottleneck / Collaborative

Strategic

Leverage / Opportunist

Routine / Transactional

High Spend

Risk of Not Achieving SavingsMonopolistic suppliersEasier for the supplier to say “No”

PROJECT APPROACHPrepare a “bespoke” approach that acknowledges the complications of the relationship. E.g. Threaten giving development projects to new emerging suppliers. Consider working on the lower risk suppliers in this segment first.

(Should be few suppliers here (e.g. BA < 10)

Value / ExpenditureImpact on end product / service attractiveness

HiLoLo

Hi

Low Levels ofCompetition

Supply Market Risk / Challenge

High Levels of Competition

Low Spend

Risk of Not Achieving SavingsEasier for the supplier to say “No”

PROJECT APPROACHIgnore

High Spend

Good Chance of Achieving Savings

PROJECT APPROACHStart here and move progressively left

Low Spend

Good Chance of Achieving Savings

PROJECT APPROACHMove into here once finished in Leverage

6 © supply chainge management ltd. 2008

Value Where’s the value in the entire system?

Use the BoM Structure Focus on the Pareto value

Cascade the target prices through the major sub-systems & components What are the drivers of these prices Sanity check

Risk (e.g. delivery and quality)

Where’s the risk in the entire system Use the logistics plan Focus on the pareto long lead time sub-systems ?

What are the drivers of these lead times ? “Real” lead times?

Elapsed time vs. op time ratio

Can we buy ourselves time? (Same for quality and other risks)

Output: Added focus on key sub-systems/components

Prioritising Negotiation Programmes (cont)

Focus by Sub-system

7 © supply chainge management ltd. 2008

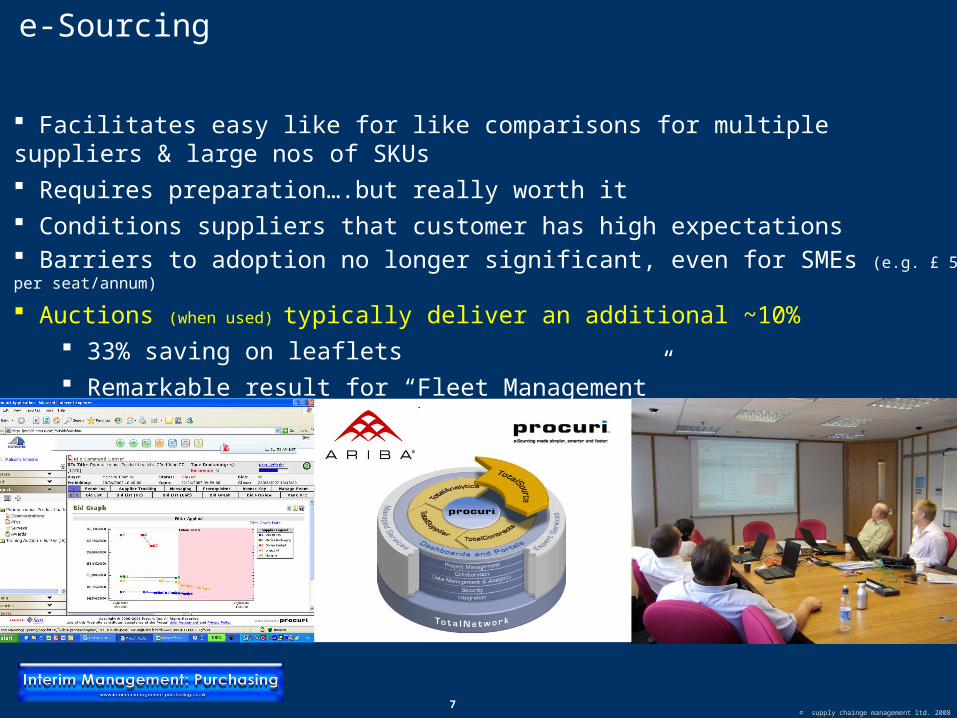

e-Sourcing

Facilitates easy like for like comparisons for multiple suppliers & large nos of SKUs Requires preparation….but really worth it Conditions suppliers that customer has high expectations Barriers to adoption no longer significant, even for SMEs (e.g. £ 5k per seat/annum)

Auctions (when used) typically deliver an additional ~10% 33% saving on leaflets Remarkable result for “Fleet Management”

8 © supply chainge management ltd. 2008

Managing Supplier Conditioning Co-ordinated multi-media campaign (PR/Comms support?)

14

© supply chainge management ltd. 2008

Managing Supplier Conditioning

The Merger &

NUI Claims

Projected Movement of Ex CGU

Claims to NUI Product Set

0102030405060708090

100

J F M A M J J A S O N D J F M A M J J A S O N D J F MNow%

• Interim solution in place to cope with growth

The Programme

• ~50 projects

• £ 2 bn + of influenceable costs across:

Motor

Legal Services

Property Repair

Replacement Goods

Loss Adjusting Services

As market leaders we need to

develop a market leading value

chain for Loss Adjustment

Services

We need to think

fundamenta

lly differently…

• loss adjusters

…to deliver better results for

• NUI

• policy-holders

• corporate partners

Fees

Settlement

Year 0

NUI

Costs

It’s not simply about

incremental fee reductions…

Step Change

Year 1

Settlement

Fees

NUI

Costs

Continuous Improvement

SettlementSettlement

Year 2Year 3

Fees

FeesNUI

Costs

NUI

Costs

Year 0Year 1

Year 2Year 3

Continuous Improvement

We must also deliver

more value to policy-holders…

Improved Service

NU Branded Delivery

Etc.

To do this we must first be able to

measure value and total cost…

Fees

Settlement

NUI

Costs

Some indicators

of value that we measure…

Satisfaction With Claims Handling

LA Co. 1LA Co. 2 LA Co. 3 LA Co. 4 LA Co. 5

100 %

No opinion

Satisfied

V. Satisfied

Dissatisfied

V. Dissatisfied

%

Satisfaction With Claims Settlement

LA Co. 1 LA Co. 2 LA Co. 3 LA Co. 4 LA Co. 5

No opinion

Satisfied

V. Satisfied

Dissatisfied

V. Dissatisfied

%

100 %

Advocacy : Propensity to Recommend

PossiblyProbably

Definitely

No/unlikely

%

100 %

LA Co. 1 LA Co. 2 LA Co. 3 LA Co. 4 LA Co. 5

Loyalty - Propensity to Renew

Possibly

Probably

Definitely

%

100 %

LA Co. 1 LA Co. 2 LA Co. 3 LA Co. 4 LA Co. 5

“What key characteristics of

our value chain really

cause or drive value

to policy-holders ?”

As a policy holder -

what’s important to

me?

We also need to measure total

cost…

Household Segment

Fees

Settlement

NUI

Costs

Jewellery

Brown & W hite GoodsCarpets

Others

1. Economies of Scale

(e.g. consortium buy)

2. value chain Architecture

- “High St.” wholesalers vs.

- Direct wholesalers vs.

- Manufacturers

-3. Others ?

Cost Drivers:

B&W Goods ?

Example

Detail

e.g.

Property

e.g.

Contents

Other

NUI

Costs

Loss Adjusters Costs (Direct Labour ?)

Back Office (In

direct Labour ?)

O’heads & Profit

“What key characteristics

of our value chain really

cause or drive the

total cost ?”

13

© supply chainge management ltd. 2008

Re-contractingResearchingRationalisation

The Three R’s in “PIES”...

Re-contracting...

With existing suppliers in recognition of NOVA

Chemicals’ new market position globally.

Is focused around a detailed Request for Quotation

(RFQ) and a single “follow-on meeting.”

The Shell team will be involved.* raw material and packaging

Re-contracting with Supplier X During the Huntsman acquisition Existing supplier at some NOVA Chemicals sites

Embraced Re-contracting Result: growth from $ 0.8m to $ 3.7m > 450%

Researching... Runs in parallel with Re-contracting Using intensive wide area faxed Requests For

Proposal* (RFP) to test market prices Examining new supply opportunities with both:

- approved suppliers - unapproved suppliers.* less detailed than the RFQ sent to existing suppliers

70% ...

...of acquisitions fail** to meet the objectives published to the investment community

PurchasingIntensiveEuropeanSynergies(PIES)

“PIES”

The Huntsman Acquisition... January 1st last year 7 styrenics sites acquired Synergies of $65m* targeted over 3 years

Synergies of $30m* achieved in year 1

Purchasing Team achieved synergy targets

Consolidation of volumes & suppliers is on-going

* all synergies, not just Purchasing

The Shell Acquisition... February 1st this year European revenues of $500m

4 plants on 3 sites acquired € 32m spend and 46 suppliers - raw materials

€ 9m spend and 30 suppliers - packaging

Rationalisation... Begins after Re-contracting and Researching

Is an on-going programme to consolidate the

global supply chain- Suppliers create opportunities- Purchasing & Technology teams prioritise

qualification programme

NOVA Chemicals’ Expectations...

Re-contracting retro-active to Feb 1st.

Reduce NOVA Chemicals total cost of

ownership year on year hereafter

- process productivities at NOVA Chemicals

- supplier material productivities- supplier process productivities

- supplier managed consignment stocks

- etc. Add value to NOVA Chemicals’ customers.

NOVA Chemicals’ Expectations...

Nominate a leader* to own the relationship during

Re-contracting Ensure you give us this person’s contact details

today#

Assign necessary resources Validate RFQ details, complete & return it promptly

Maintain the sense of urgency to complete

Re-contracting in one meeting following RFQ

Have the decision maker there

* responsible for pan-European sales (?)

# See Gordon O’Kell Tel: +44 (0)161 776 5545 Fax: +44 (0) 161 776 5541

Benefits of Engagement... Potential for increased volumes for pro-active

suppliers during Rationalisation Alignment with a global styrenics leader

Cement the relationship as we continue to grow

Managing Supplier ConditioningLetters from CPO /CFO / CEO etc.

Standard Presentation Packs / Supplier Conferences

Phone calls• Purchasing• Logistics• Supplier Quality

Emails

Website / Webinars

Meetings

XX% savings

needed…

“Introduction of auctions”

“Global Sourcing Initiative”

“Lean Supplier

Interventions”

“SupplierRationalisation

”

9 © supply chainge management ltd. 2008

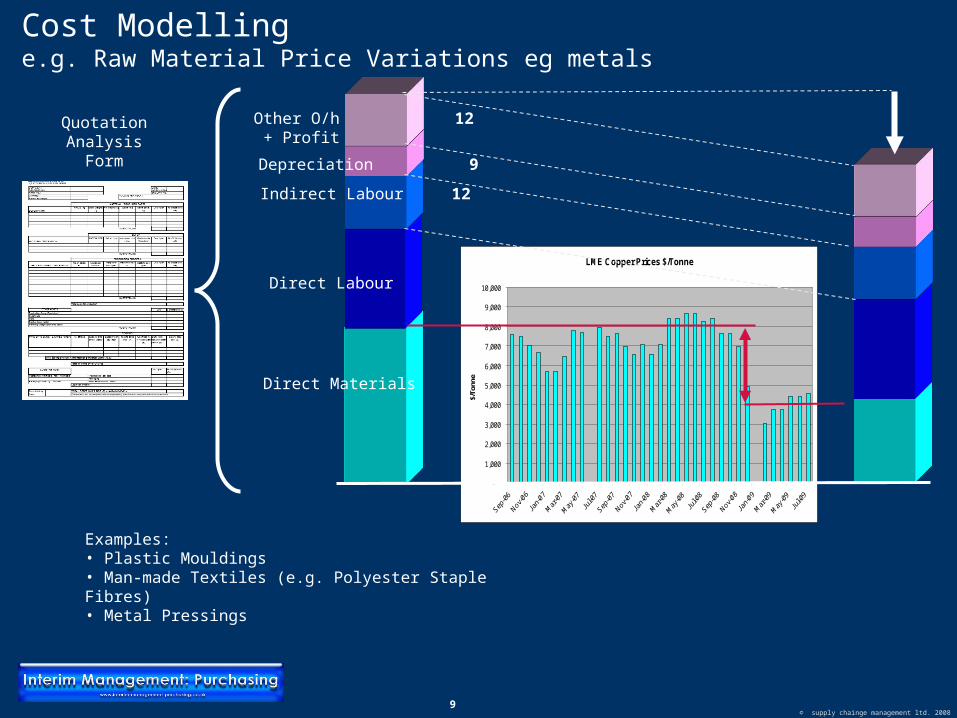

Direct Materials 45

Cost Modellinge.g. Raw Material Price Variations eg metals

Direct Labour 22

Indirect Labour 12

Depreciation 9

Other O/h 12 + Profit

LME Copper Prices $/Tonne

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

$/To

nne

22.5

22

12

9

12

QuotationAnalysis

Form

Examples:• Plastic Mouldings• Man-made Textiles (e.g. Polyester Staple Fibres)• Metal Pressings

10 © supply chainge management ltd. 2008

Direct Materials 45

Cost Modelling Volume Increases / Decreases – say 2x volume

Direct Labour 22

Indirect Labour 12

Depreciation 9

Other O/h 12 + Profit

45

22

6 4.5

6

QuotationAnalysis

Form

Example:• Right-sourcing of electrical control systems categories:

• pressings• turned and prismatic machining• coil winding• moulding• plating

Modelling effects on fixed costs & ROCEROCE Target 25% - achieved 41%

Before Volume After

22xx

149© supply chainge management ltd. 2008

Competitivenessof In-House ProcessTechnologies

Best in Class

Worst in Class

Importance to Business’ Competitive Advantage

HighLow

Make

Outsource

Pan-European SolonoidManufacturer Process technology road maps

Product technology road maps

Identify core / non core processes

Model allocation of remaining fixed costs

TUPE employees and transfer capital equipment

Consolidate plants

Dispose of assets (land, buildings etc)

Outsourced Turning

Milling

Grinding

Presswork

Retained Coining (high tolerance presswork)

Copper Coil Winding

Assembly

Multi-disciplinary Team Strategic Make vsBuy Concept Design: ~ 3 months

Target: ROCE > 25%Design: ROCE = 41%

Strategic Make vs. Buy: Case Example 1

11 © supply chainge management ltd. 2008

What Information is Available for Cost Modelling?

E.g. If volume effects are key opportunity:

What’s known about the split between direct and indirect costs?

What’s known about volume changes? Our volume changes by line Total volume changes by line

Possible sources of information: QUAFs Database Hosts (e.g. volume increases)

Published accounts Category Manager’s knowledge Questionnaires (RFIs / eRFIs) Org charts SQA Audits Other touch points:

Supplier Management Team Logistics

Factory gate monitoring Lean re-engineering diagnostics

12 © supply chainge management ltd. 2008

Database Hosts

Web based pay as you go service No training required Largest source for immediate intelligence

gathering 40,000 sources Journals and Periodicals 20,000+ licensed news sources 13 languages 163 countries

2000 global newspapers Newswires, Associated Press, PR Newswire, AAP

Newsfeed, Datamonitor Newswire, US News, PA Newswires & FinancialWire

Hundreds of UK regional newspapers

Information on > 46,000,000 companies Creditreform Companies, Directory of Corporate Affiliations

Executive Directories, Dun and Bradstreet, Hoover's Company Profiles, Investext, Bundesanzeiger, Mergent, Hoppenstedt and Worldscope International Company Profiles, ICC Directory of UK Companies, ICC Financial Analysis Reports and ICC Full-Text Quoted Company Annual Reports.

13 © supply chainge management ltd. 2008

198

© supply chainge management ltd. 2008

What are the three key learnings/ takeaways from this negotiation?

1. 2.3.

Who were today’s participantsName

Position

Role Exhibited in Negotiation

SUPPLIER: __________________________

What facts or information did we learn today?

1. 2.

3.4.5.6.7.8.

Key decision makers not included today that we need to ensure are included in future

negotiations?Name

Position

Post Negotiation Evaluation

McKinsey Negotiation Process Team based negotiation

Synergistic: “X heads are better than one” Tag-team approach to questions Variety of styles / role playing Rules of engagement - maverick s can derail progress Value of consensus in identifying & validating SWOTs

Rigorous planning Objectives SWOTs Role playing

Formal debriefs to close the loop Back to planning the next negotiation

199

© supply chainge management ltd

. 2008

199

Based on today’s discussion, what negotiation tactics do you recommend we use in the 2nd

interview?1. 2.

How would you classify the tone of today’s

negotiation?

1

5

3

Hostile, Non-

cooperative

Enthusiastic

SUPPLIER: __

________

________

________

Based on your first meeting, what response do you

anticipate from the supplier?

1

7

4

No Savings

Likely

Reach Stretch

Target

Attain Realistic

Target

What are the specific next steps we need to take before the next negotiation?

Next Step

Team Member Ownership

Post Negotiation Evaluations (cont).

200

© supply chainge management ltd. 2008

200

•Product characteristics / runability•New product development

• Innovating packaging / logistics•Global coverage / capability

•Flexibility to customer product requirements•Total cost of ownership reduction

mentality•Other

•Overall Rating

Supplier-Specific Strengths & Weaknesses

Internal Expectations (Strengths & Weaknesses)

Weakness

Strength1 2

34 51 2

34 51 2

34 51 2

34 51 2

34 51 2

34 51 2

34 5

1 23

4 5

14 © supply chainge management ltd. 2008

Contract ModelsStructuredprocess to develop bespoke contracts from standard models…

Generic Contract Frameworks• Direct Goods (e.g. Raw Materials & Packaging)• Indirect Goods • Services (e.g. Development Services)• Capital Equipment• etc.

(available on intranet) (Legal)

Risk Evaluation

• Risk• Scale of Likely Impact• Probability of Occurrence• Prevention• Mitigating Action• etc

(Purchasing & Internal Customer)

Contract ManagementProcedure, Guidelines & Standard Forms

(available on intranet)

BespokedSchedule/s

• Commercial Specification • Service Level Agreement• Prices & Incentivisation• etc.

(Purchasing & Legal)

Guidelines for Drafting Comprehensive

Purchasing Specifications

--including Service Level -Agreements (SLAs)

-(available on intranet)- (Purchasing)

(Legal & Purchasing)

Bespoke Contract

To be used for invitation to tender (ITT) & contract

negotiation.

Examples of good practisebecome future

standards

Purchasing to become a key interface between budget holders, to facilitate the

evaluation of risk and specify requirements including

target service levels and Legal (Sheila)

On-line Contract Repository

Signed contracts to scanned & be held in .pdf form on a central

Server i.e. accessible to Legal, Purchasing, etc. with change

control procedure.

Have contract models been established?

Have they been set up as “non negotiable” ?

Risks ?