1 valuation of cash flow streams: company valuation global financial management campbell r. harvey...

TRANSCRIPT

1

Valuation of Cash Flow Streams: Company Valuation

Global Financial Management

Campbell R. HarveyFuqua School of Business

Duke [email protected]

http://www.duke.edu/~charvey

2

Overview

Stocks and stock markets Valuation:

» Use present value formula Dividend growth models

» Applications» Extensions

Financial ratios» Dividend yields» P/E multiples

Discounted cash flow models (DCF)

3

Common Stock Stockholders are owners of the firm. Stockholders are residual claimants. Stockholders have the right to:

» vote at company meetings» dividends and other distributions» sell their shares

Stockholders benefit in two ways:» dividends» capital gains

Stock is issued by public corporations to finance investments. Stock is initially issued in the primary market (IPOs and

secondary offerings). Stock is traded in the secondary market on organized

exchanges.

4

World Stock Markets

New York Tokyo London Frankfurt Paris

Johannesburg Sydney Stockholm Amsterdam Switzerland

Mexico Canada Brussels Hong Kong Singapore

5

International Stock Market Indices

Value Net Chg Pct ChgUKX FT-SE 100 Index 4207.70 10.20 0.24CAC CAC 40 INDEX 2425.10 17.33 0.71DAX DAX INDEX 3001.37 8.05 0.26IBEX IBEX 35 INDEX 5470.23 85.41 1.58MIB30 MILAN MIB30 INDEX 18485.00 344.00 1.89BEL20 BEL20 INDEX 2006.79 8.22 0.41AEX AMSTERDAM EXCHANGES INDX 670.08 0.53 0.07SMI SWISS MARKET INDEX 4019.89 12.79 0.31NKY NIKKEI 225 INDEX 18090.03 -54.30 -0.29HSI HANG SENG STOCK INDEX 13856.40 25.72 0.18AS30 ASX ALL ORDINARIES INDX 2435.50 -0.80 -0.03STI SING: STRAITS TIMES INDU 2244.21 23.84 1.07TS300 TSE 300 Index 6136.39 32.73 0.53MEXBOL MEXICO BOLSA INDEX 3741.87 40.04 1.08

Value on January 17, 1997, Change relative to previous day

6

U. S. Stock MarketsMajor U. S. Stock Exchanges

New York Stock Exchange (NYSE) American Stock Exchange (AMEX) Over-The-Counter (OTC)

» National Association of Securities Dealers (NASDAQ)

U. S. Stock Market Value Net Chg Pct Chg

INDU DOW JONES INDUS. AVG 6795.37 30.00 0.44SPX S&P 500 INDEX 773.68 3.92 0.50CCMP NASDAQ COMB COMPOSITE IX 1349.49 9.02 0.67

Other Indices NYSE Composite Russell 2000 Wilshire 5000 Value Line

7

Transactions Involving Stocks

Buy Savings motive Expect stock to

appreciate in value Long position

Sell Liquidity needs Expect stock to decline

in value

Short Sell Sell stock without first owning it. Borrow stock from your broker

with the promise to repay it at some later date.

Sell the borrowed stock. Repurchase it at a later date to

repay your broker. Responsible for all dividends and

other distributions while short the stock.

8

Stock Valuation

The price an investor is willing to pay for a share of stock depends upon:» Magnitude and timing of expected future dividends.» Risk of the stock.

The stock’s discount rate, re, is the rate of return investors can expect to earn on securities with similar risk.

9

Shareholders require a rate of return re for buying a share. They buy for

P0 and sell after one year for P1 and receive dividends D1:

The next buyer also sells after one year:

The same holds for P2. Continuing gives:

Share price = PV of dividends

Why short-termists are long-termists

PD P

re0

1 1

1

P

D P

rP

D

r

D P

re e e1

2 20

1 2 221 1 1

P

D

r

D

r

D

re e e

01 2

23

31 1 1

...

10

Assumption: Dividends grow at a constant rate g for ever:

Then:

Issues: » constant growth» g < re.

» Is this a real or a nominal calculation?

The “Constant Growth” Formula

D D g D D g D g D gt tt t

2 1 1 11

01 1 1 1 ( ) ( ) ... ( ) ( ),

PD

r

D g

r

D g

r

D

r ge e

t

et

e0

1 12

11

1

1

1

1

1

1

( )

( )... ...

Share PriceProspective Dividend per Share

Required return - growth rate

11

Simplifying the Dividend Discount Model

Constant Dividends

Then the pricing relation simplifies to:

» Stock similar to perpetual bond If dividends are constant, then we have that:

Required return on equity = Dividend yield

g D D D 0 1 2 ...

PD

rr

D

Pee0

0

12

Constant Dividends: An Example

Consider a company that pays a dividend of:

$3 per share in bad years (Probability = 50%)

$15 per share in good years (Probability = 50%)» Required rate of return is 18%» What is the share price?

E Div

P

( ) . * $3 . * $15 $9

$9

.$50

0 5 0 5

0 180

13

Constant Dividends:RJR Nabisco Preferred Stock

RJR Nabisco has a preferred stock outstanding » annual dividend of $2.50 per share.» Securities with similar risk are expected to return 9.6%

– what is the price of the preferred stock?

PD

re0

50

0 09604 $2.

.$26.

14

Constant Growth:Duke Power Common Stock

Duke Power currently pays a dividend of $2.04 per share.» Demand for electric power is growing at 4% per year,» Inflation averages 3% per year,» Duke Power expects its profits and dividends to grow at about

7% per year.» Stockholders require a 12% rate of return

– what is the market price of Duke Power’s common stock?

P0

2 04 1 07

0 12 0 0766

. ( . )

. .$43.

P gD

r ge0

01

15

Valuation with Growing Dividends

An Example: Valuation of GM

Generally, companies have growing dividends on stocks, hence apply general formula:

Consider data for GM:» Number of shares: 855,820» Market capitalization $42.051bn» Historic dividend $1.50 per share» Your forecast: $1.60

– What valuation do you obtain for GM, depending on g and r?

PD

r ge0

1

16

Valuation of GM

Alternative valuations:

Example:

855,820,000*$1.60=$1.37bn

MCAPD

r g

bnbnGM

GM GM

1997 37

0 09 0 0523

$1.

. .$34.

Return/Growth 3% 4% 4.50% 5% 6% 7%7% 34.23 45.64 54.77 68.47 136.93 -8% 27.39 34.23 39.12 45.64 68.47 136.939% 22.82 27.39 30.43 34.23 45.64 68.4710% 19.56 22.82 24.90 27.39 34.23 45.6411% 17.12 19.56 21.07 22.82 27.39 34.2312% 15.21 17.12 18.26 19.56 22.82 27.39

17

Valuing a BusinessA Hybrid Approach

Sometimes equity analysts have knowledge about the immediate, but not the distant future» Dividend forecasts for immediate future (2-5 years)» Assume constant growth for distant future (>5 years)» How do you change the model?

Dividends

Value

18

Modify the Growth Model

The formula for a T-year horizon can be written as:

Apply the growth model to the price in T:

Then the current value of the share is:

P

D

r

P

rt

ett

t T T

eT0 1 1 1

PD

r gTT

e

1

P

D

r

g

r

D

r gt

ett

t T

eT

T

e0 1 1

1

1

19

Valuing a Business

Consider a company with cash flows from operations of $1 million for the most recent year.

The company’s cash flows are expected to grow at a rate of 10% for the next 5 years and at a constant rate of 5% thereafter.

To generate this increase in cash flows, the company is required to reinvest 50% of its cash flows for the first 5 years and 25% of its cash flows thereafter.

Given the risk of the business, the required rate of return is 15%.

What is the value of the business?

20

Valuing a Business (cont.)

Present value= CF(1)+...+CF(5)=0.48+0.45+0.43+0.42+0.40=2.18

Year 1 Year 2 Year 3 Year 4 Year 5OperatingCash Flows

1.10 1.21 1.33 1.46 1.61

New CapitalInvestment

-0.55 -0.61 -0.67 -0.73 -0.81

Net CashFlow (Div)

0.55 0.60 0.66 0.73 0.80

PresentValue

0.48 0.45 0.43 0.42 0.40

21

Valuing a Business

Value of dividends over the first 5 years is $2.18. Value of business at the end of the 5th year:

Value of the Business:

P

D

r ge5

6 161 1 0 25 105

015 0 0568

. . .

. .$12.

P0 51868

11548 $2.

$12.

.$8.

22

Another Application:Estimating the required return on equity

Holders of stock receive returns in two forms:» Dividend payouts» Capital gains (stock appreciation P1-P0)

Note:» The required rate of return is not equal to the dividend yield» The expression is in terms of the prospective yield, not the historic

yield

rD

P

P P

Pe 1

0

1 0

0

23

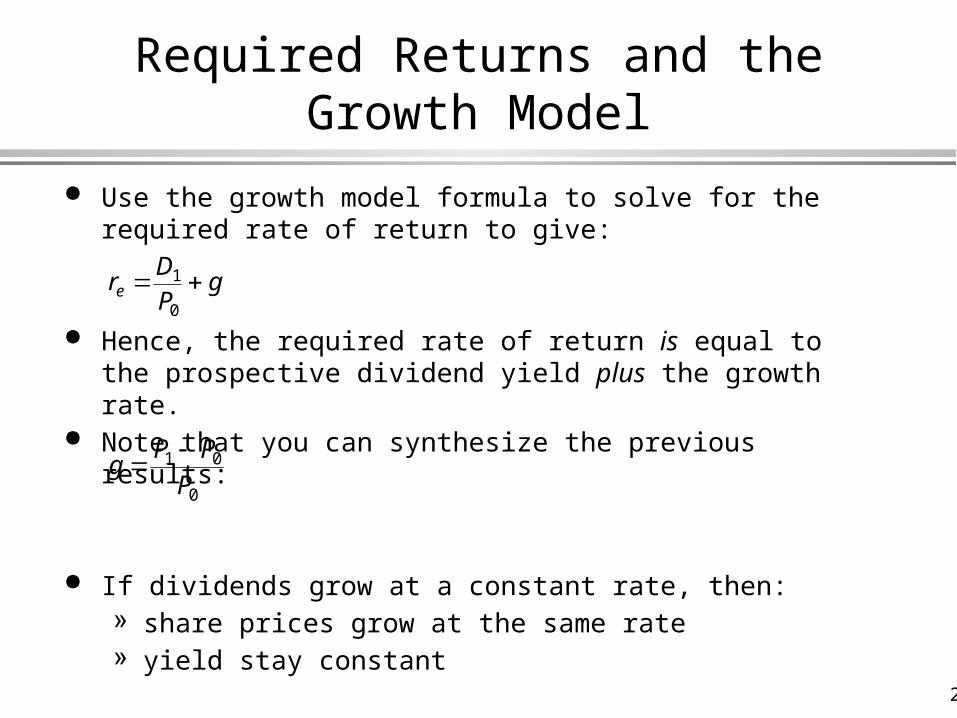

Required Returns and the Growth Model

Use the growth model formula to solve for the required rate of return to give:

Hence, the required rate of return is equal to the prospective dividend yield plus the growth rate.

Note that you can synthesize the previous results:

If dividends grow at a constant rate, then:» share prices grow at the same rate» yield stay constant

rDP

ge 1

0

gP P

P 1 0

0

24

Next year’s EPS: E1

Payout ratio:

P/E-ratio: P0/E1

Earnings yield: E1/P0

The we obtain the following results:

» Which assumptions do you have to make in order to argue that stocks with a low P/E multiple are undervalued?

Another view: P/E-ratios

DE

1

1

D EP

E r g

rE

Pg

e

e

1 10

1

1

0

*

25

P/E Ratios and Growth

You can use the expression for the historic yield to infer the growth rate:

Consider auto industry:

gr D P

D Pe

0 0

0 01

Required return Yield

1 Yield

Chrysler Ford GMMCAP 24.671 38.152 42.051No. of shares ('000) 713500 1186000 855820Share Price 34.58 32.17 49.14Dividend p. share 1.3 1.43 1.5Dividend Yield 3.76% 4.45% 3.05%EPS 2.78 3.58 7.28P/E ratio 6.78 10.1 7.8

26

Growth rate in the Auto Industry

Infer growth rate in the auto industry

Example:

Returns Implied growth ratesChrysler Ford GM

9% 5.05% 4.36% 5.77%10% 6.01% 5.32% 6.74%11% 6.98% 6.28% 7.71%12% 7.94% 7.23% 8.68%13% 8.91% 8.19% 9.65%14% 9.87% 9.15% 10.62%15% 10.83% 10.11% 11.59%

g turnFord Re. .

.. .

12%

0 12 0 0445

1 04450 0723 7 23%

27

Summary

Stocks and equity securities can be valued by using present value techniques» The discounting horizon does not depend on the investment

horizon of individual investors in the stock market Investors are compensated through cash dividends and through

capital gains» Required returns on equity are generally not equal to the

dividend yield, but to the dividend yield plus the growth rate P/E-ratios should be used with caution:

» Depends on simplifying assumptions

28

Issues in Capital Budgeting: Investment

How should capital be allocated? » Do I invest / launch a product / buy a building / scrap /

outsource...» Should I acquire / sell / accept offer for company or division?» How should the capital budgeting process be organized?

Which choices should I make?» make or buy» which distribution channel

29

Issues in Capital Budgeting: Financing

Choose between financing alternatives» How should I finance this deal?» Should I change my capital structure?» Lease or buy?

Risk Management» Hedging» Taking a view

30

Discounted Cash FlowsA Tool For Rational Decision Making

What can be an object of capital budgeting procedures?» There must be a choice - choose a base case and an

alternative. (Do nothing/status quo)

Identify incremental cash flows from project» Treat as incremental cash flows to shareholder

Calculate the value of the project.» Taking into account timing and risk» Aggregate cash flows into one single number

Show that doing all and only projects which have positive net present value maximizes the value of the firm.

31

Estimating Relevant Cash Flows

The relevant cash flows for evaluating a new investment project are the incremental cash flows contributed by the project.

Incremental = Firm’s CFs - Firm’s CFs

Cash Flows with Project without Project

Only Incremental Cash Flows are Relevant.

» Include all incidental effects, including project interactions.» Don’t forget to include investment in working capital. » Forget about sunk costs.» Include all opportunity costs (e.g., land used to construct a

new plant).» Beware of allocated overhead expenses.

32

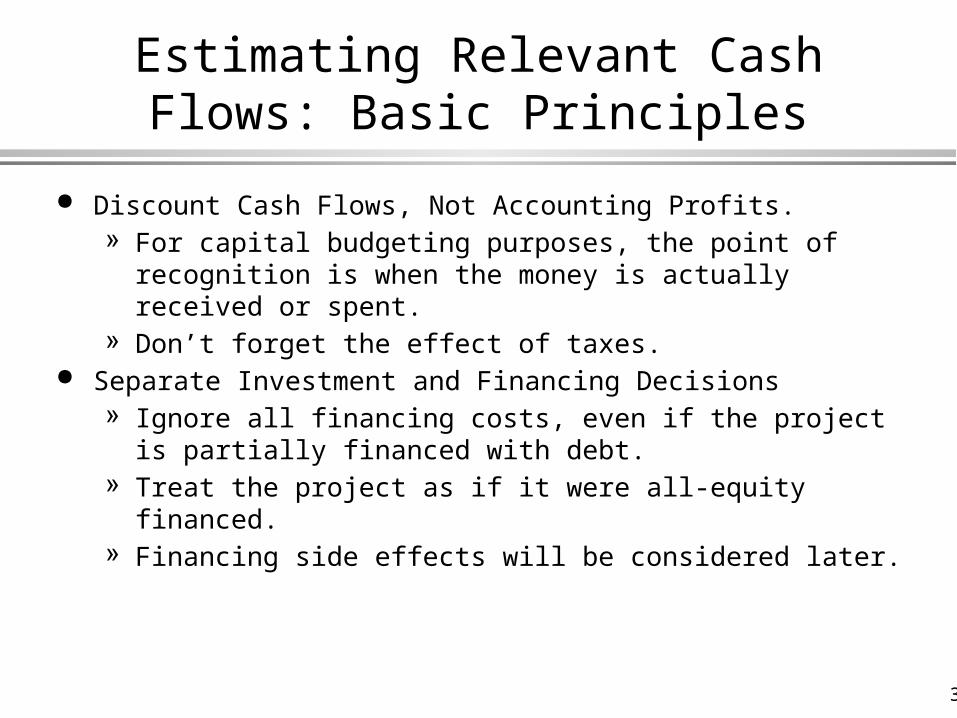

Estimating Relevant Cash Flows: Basic Principles

Discount Cash Flows, Not Accounting Profits.» For capital budgeting purposes, the point of recognition is when

the money is actually received or spent.» Don’t forget the effect of taxes.

Separate Investment and Financing Decisions» Ignore all financing costs, even if the project is partially financed

with debt.» Treat the project as if it were all-equity financed.» Financing side effects will be considered later.

33

Depreciation

Depreciation is a non-cash expense that only affects cash flows through its tax effect.

Assets are depreciated down to their estimated salvage values. Any removal costs associated with old equipment are expensed

immediately. Sales tax, delivery costs, and installation are regarded as part of the

cost of the new asset for depreciation purposes. Removal costs of the old asset are not regarded as part of the cost

of the new asset and are expensed immediately. If an asset is later sold for an amount above (below) its book value,

the excess is taxable (deductible).

34

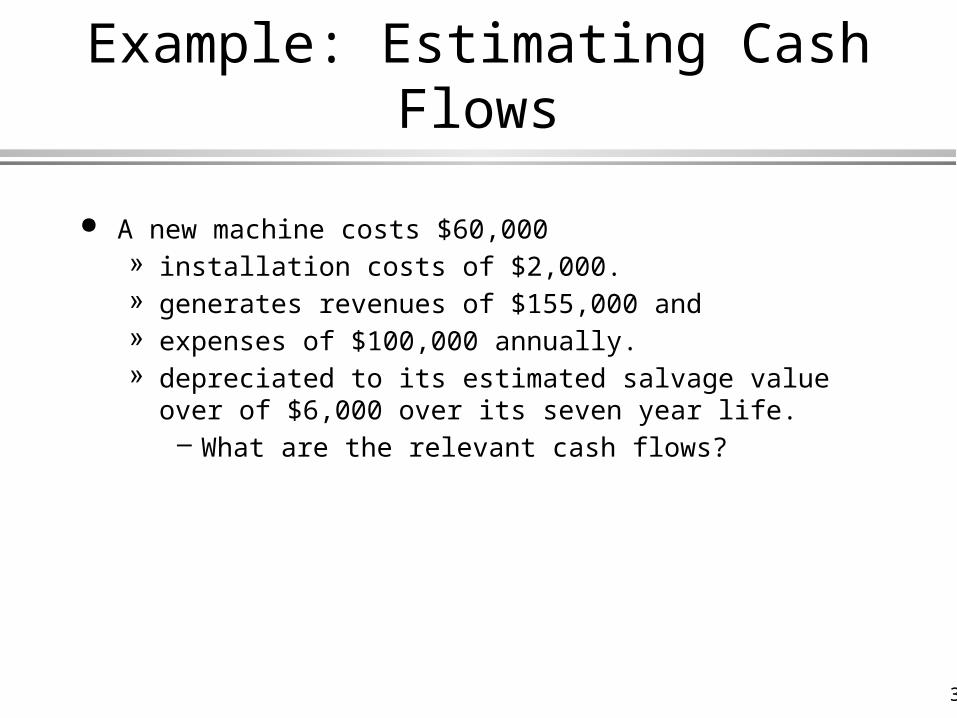

Example: Estimating Cash Flows

A new machine costs $60,000 » installation costs of $2,000.» generates revenues of $155,000 and » expenses of $100,000 annually.» depreciated to its estimated salvage value over of $6,000

over its seven year life.– What are the relevant cash flows?

35

Compute Cash Flows

Year 0 1 ... 7Revenues 155,000 ... 155,000Expenses -100,000 ... -100,000Depreciation -8,000 ... -8,000Taxable Income 47,000 ... 47,000Tax 15,980 ... 15,980

Step 1: Compute Tax cash flows

Year 0 1 ... 6 7Revenues 155,000 ... 155,000 155,000Expenses -100,000 ... -100,000 -100,000Tax -15,980 ... -15,980 -15,980Cost of Machine -62,000Salvage 6,000Net Cash Flow -62,000 39,020 ... 39,020 45,020

Step 2: Compute Cash Flows

36

Cash Flow and Accounting Numbers:How to Value a Company

The value of the firm is the present discounted value of all net cash flows accruing to all security holders (debt and equity).

Define:

The capital cash flow of period t CCF(t) is the net cash flow received by all security holders of the firm combined:

CCF = EBIT

- (EBIT - Interest)*T

- Depreciation & Amortization

- Change in working capital

- Capital Expenditure

+ Asset Sales

37

Since Net Income = (1 - T)*(EBIT - Interest) we have the alternative definition:

CCF = Net Income+ Interest- Depreciation & Amortization- Change in working capital- Capital Expenditure+ Asset Sales

Then we can value a company as:

where r is the company’s cost of capital.

Capital Cash Flows

VCCF t

r tt( )

( )

( )0

11

38

Summary and Preview

Most investment and financing problems can be analyzed as capital budgeting problems

Focus is on cash flows, not accounting numbers» Use accounting numbers, remove non-cash flow charges like

depreciation– However, depreciation has tax consequences– Taxes are cash flows

Capital budgeting always focuses on decisions, hence» Include all cash flow consequences affected by a decision

On the agenda: Take into account the time value of money Use single criterion to evaluate project

» NPV, compare with IRR, payback Account for risk, inflation, and taxes