2010 investors' meeting presentation - são paulo

TRANSCRIPT

Banco PINE specializes in the corporate sector, offering its clients a complete range of financial products and services

August - 2010August - 2010

B PINEBanco PINE2Q10

Presentation

Agenda

Highlights and Results

B i SBusiness StrategyBusiness OpportunitiesCross-Selling OpportunitiesAgility in Granting CreditOrganizational StructureHuman ResourcesThe Current Scenario and Future Prospects

Corporate Governance and SharesCorporate GovernanceMain CommitteesMain CommitteesShareholders’ StructureShareholders’ ProfileDividendsSocial ResponsibilitySocial ResponsibilityRating upgrade by FitchEvents and Highlights of the PeriodBanco PINE

3/32Investor Relations | August - 2010

Highlights and Results

HighlightsMain indicators improvement: profitability, credit and funding

Operating Income (R$ Million)

75.2% 26.2%

Δ QuarterΔ 12M

65.8%

Δ 6MNet Income (R$ Million)

63.3% 18.0%Δ QuarterΔ 12M

57.1%Δ 6M

Corporate Loan Portfolio(R$ Million)

Δ QuarterΔ 12M Δ 6M

108 3 65.8

56.3% 7.5%16.4%

34.5 47.9

60.4 65.3

108.3

21.8 30.2 35.6 41.9

2Q09 1Q10 2Q10 1H09 1H10

3,068 3,416 4,118 4,462 4,794

J 09 S 09 D 09 M 10 J 10 2Q09 1Q10 2Q10 1H09 1H10 2Q09 1Q10 2Q10 1H09 1H10

Efficiency RatioROAE

Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

Total Deposits+ Agribusiness Letter of Credit (R$ Million)

-650 bps -600 bps

Δ QuarterΔ 12M

-310 bps

Δ 6M

680 bps 260 bps

Δ QuarterΔ 12M

580 bps

Δ 6MCredit (R$ Million)

66.0% 5.6%

Δ TriΔ 12M5.1%Δ 6M

40.0% 39.5%

33 5%

39.3%

36.2%11.1%15.3%

17.9%

10.5%

16.3%

1,917 2,302

3,029 3,013 3,183

5/32Investor Relations | August - 2010

33.5%

2Q09 1Q10 2Q10 1H09 1H102Q09 1Q10 2Q10 1H09 1H10Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

EarningsConsistent income growth in the last quarters, as a result of selective credit portfolio increase and cross-selling strategycross selling strategy

ROAE

Even during the globalfinancial crisis, ROAEmaintained a minimum of 10%

7.1%

3% 7.9%

% 6.3%

260 bps increase in thequarter

17

9.9%

10.1

%

11.1

%

11.3

%

10.7

% 15. 1

13.2

%

10.5

%

10.8

% 1 6

Net Income (R$ Thousand)

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 2H08 1H09 2H09 1H10

76

Gradual and consistent incomegrowth in post-crisis periodNet Income 18% up in thequarter 33

,429

,821

,070

,800

,068

,148

30,1

71

35,6

05

53,2

50

41,8

70

43,2

16 65,7

7

6/32Investor Relations | August - 2010

quarter

19,

20,

21 22 21, 3

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 2H08 1H09 2H09 1H10

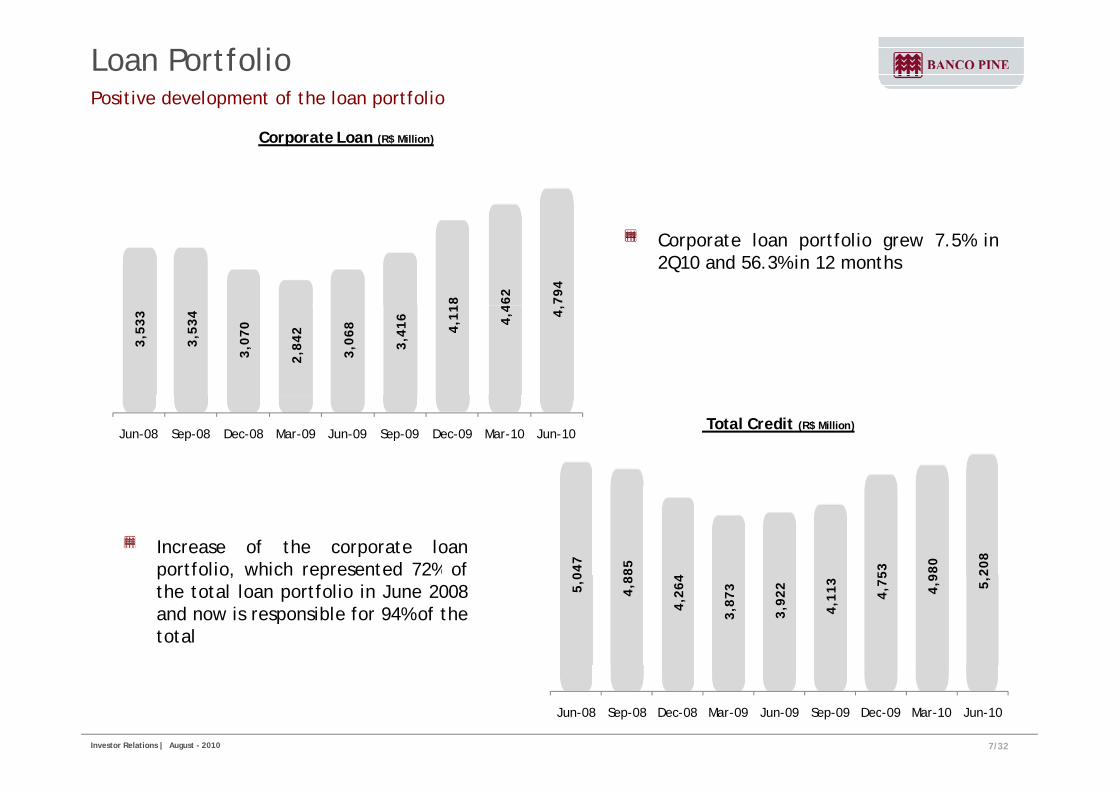

Loan PortfolioPositive development of the loan portfolio

Corporate Loan (R$ Million)

Corporate loan portfolio grew 7.5% in2Q10 and 56.3% in 12 months

8 462

,794

3,53

3

3,53

4

3,07

0

2,84

2

3,06

8

3,41

6

4,11 4,

4 4,

Total Credit (R$ Million)Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

Increase of the corporate loanportfolio, which represented 72% of 04

7

85

4 53

980

208

portfolio, which represented 72% ofthe total loan portfolio in June 2008and now is responsible for 94% of thetotal

5,0

4,8

4,26

4

3,87

3

3,92

2

4,11

3

4,75 4,9 5,2

7/32Investor Relations | August - 2010

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

Loan Portfolio ProfileBanco PINE operates in the major sectors of the economy, with product diversity and regional distribution that mirrors the GDP’s

Loan Portfolio by Region

distribution that mirrors the GDP s

South 12%

Loan Portfolio by SectorNortheast

10%

A i l

Construction7% Financial

Institutions Meat packing

Southeast66%

Mid-West10%

Northeast2%

Electric and Renewable

Energy

Agriculture8%

Institutions6%

Meat packing5%

Vehicles and Parts5%

Working Capital

Loan Portfolio by Product

Energy11% Transportation

and Logistics4%

Pharmaceutical 58% BNDES onlendings

9%

Resolution 2770 1%

Infrastructure13%

and Cosmetic3%

Foreign Trade3%

Metallurgy3%

Trade Finance14%

Sugar and Ethanol

15%

3%Specialized

Services2%

Foodstuffs2%

Healthcare2%

Other11%

8/32Investor Relations | August - 2010

Guarantees18%

Loan Portfolio QualityThe coverage of the overdue portfolio reached 214.7% in June 2010

D-H Overdue Credit Portfolio/ Total Credit

Credit Portfolio Quality – June 2010

1 6% 1 7%

A, 49.6%1.6% 1.7%

1.3%

0.7% 0.7% 0.7%

M 09 J 09 S 09 D 09 M 10 J 10B, 18.9%

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

Overdue Credit Portfolio/ Total Credit

AA, 26 3%

C, 3.5%

D-E, 0.4%26.3%F-H, 1.3% 1.8% 1.7%

1.5%

0.8% 0.7% 0.7%

9/32Investor Relations | August - 2010

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

FundingBanco PINE maintains diversified funding sources

T l F di Total Funding (R$ Million)

Multilateral Organizations

4,39

6

4,31

1

3,77

2

,656

,701

3,87

5

4,55

3

4,65

5

4,89

0

US$28.9 Million US$33.5 Million

3 3 3 3

US$30.2 Million US$50.9 MillionUS$20.0 Million

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

229 296 508 24

29 26 27

229

Funding Mix (R$ Million)

Subordinanted Debt

1,119 1,005 552

440 351 268 288

429

663 713 642

576

586 521 541 467 554

496 382 306 275

242 447 160 144 147

156 143 127 142

229 296 508 29

35 35 29

27 Borrowings and Onlendings

Funds from Acceptance and

2,354 2,148 1,462 1,553

1,917 2,302

3,029 3,013 3,183

1,005

959 832 679

552 Securities IssuedTrade Finance / Cayman

Loan Assignments

10/32Investor Relations | August - 2010

1,462 ,

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

Total Deposits

Funding and Loan Portfolio Maturities In 2Q10, the average term of funding was 18 months, compared with 13 months for the loan portfoliop

R$ Million

Loan Portfolio + Cash Position From 3 to 5 years

Funding(1)

From 3 to 12 monthsR$1,675

From 1 to 3 years

R$1,069 From 3 to 5

yearsR$250

From 1 to 3 years

R$1,185

yearsR$299

More than 5 yearsR$661

More than 5 yearsR$76

No MaturityR$36

From 3 to 12 Up to 3 months

(includes Cash)

R$2,557

Up to 3 months R$1,244

From 3 to 12 monthsR$1,465

(1) Excluding Shareholders’ Equity

11/32Investor Relations | August - 2010

Capital Adequacy Ratio (BIS)BIS ratio was 18.5% in June, which demonstrates a comfortable capital base. The growth rate reflects the approval of subordinated debt as Tier IIreflects the approval of subordinated debt as Tier II

BIS Ratio

Subordinated NotesJoint Bookrunners

Public OfferingFebruary / 2010

16.5

%

15.6

%

19.3

%

18.6

%

19.3

%

17.2

%

15.6

%

14.9

%

18.5

%

Joint Bookrunners

Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10

US$125 Million

p p

Equity (R$ thousand) BIS Ratio (%)

Tier I 854,041 14.6%

Tier II 228,230 3.9%

12/32Investor Relations | August - 2010

BIS Ratio 1,082,271 18.5%

Consistent and Consolidated StrategyBanco PINE is a commercial bank focused on delivering a full set of financial services to corporations

We will intensify our focus on companies, closely follow our client portfolio and endeavor to meet theird iftl d i li d ll ff id f d t th t i thneeds swiftly and in a personalized manner as well as offer a wide range of products that increase the

potential for cross-selling opportunities (Press Release 4Q08 – Page 2)

Our strategy is not only working capital and trade finance, but a strategy to service a company in a cross-selling amplified ( ) The type of client chosen is focused on a comprehensive strategy for deliveringselling amplified (...) The type of client chosen is focused on a comprehensive strategy for deliveringmultiple products (Conference Call 2Q09)

We are and will be a commercial credit bank, this is our vocation, it is our DNA (Conference Call 2Q09)

Our goal is to offer a wide range of products that meet the needs of our clients, and also optimize ourcapital use, therefore increasing our per-client profitability (Conference Call 3Q09)

These two parts, putting more capital to work and cross-selling strategy, will make ROAE 2010 closer to 15%These two parts, putting more capital to work and cross selling strategy, will make ROAE 2010 closer to 15%(Conference Call 3Q09)

We are optimistic and believe in a growth tendency and recovery for the next quarters (Conference Call4Q09)

As we said since the end of 2008, the Bank successfully reinforced its strategy of cross-selling financialinstruments (Conference Call 4Q09)

13/32Investor Relations | August - 2010

Business Strategy

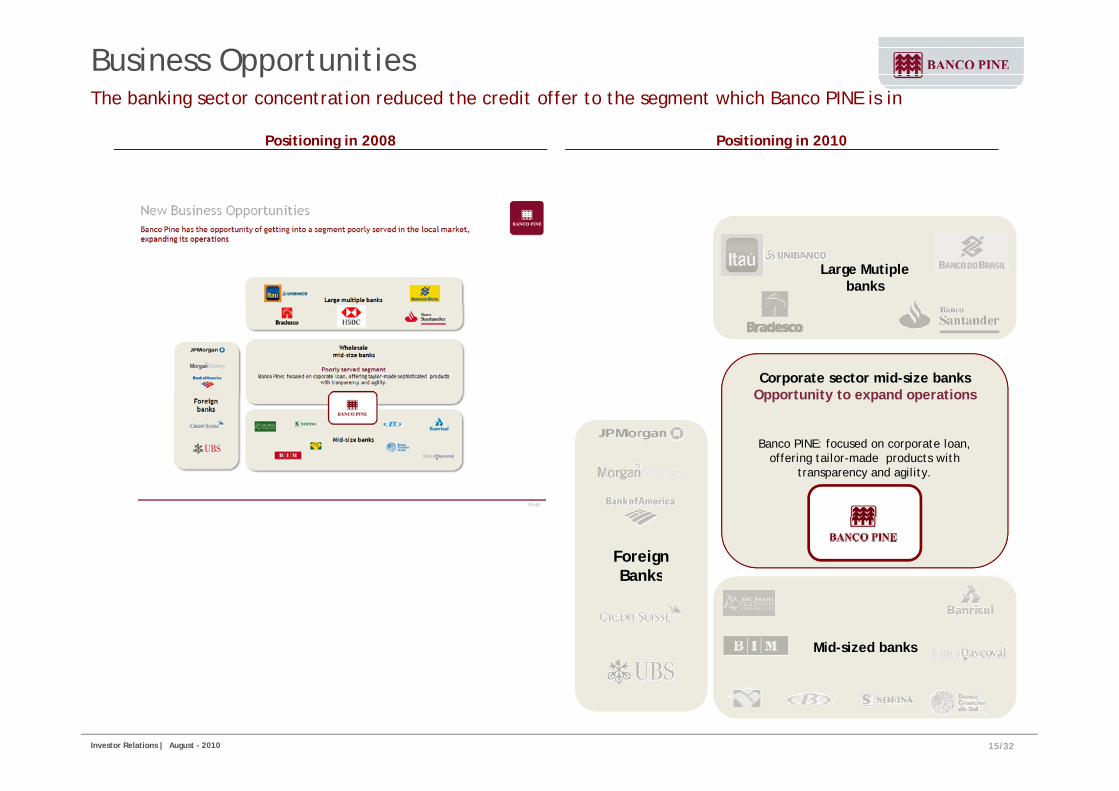

Business OpportunitiesThe banking sector concentration reduced the credit offer to the segment which Banco PINE is in

Positioning in 2008 Positioning in 2010

Large Mutiple banks

Large Mutiple banks

Corporate sector mid-size banks Opportunity to expand operations Opportunity to expand operations

Banco PINE: focused on corporate loan, offering tailor-made products with

transparency and agility.

Foreign Banks

Foreign Banks

Mid-sized banksMid-sized banks

BanksBanks

15/32Investor Relations | August - 2010

Cross-selling OpportunitiesFinancial instruments diversity for the diverse needs of our clients

Challenges :

L i t t t & l

Challenges :

L i t t t & l

Capital optimization:

Selective loan portfolio growth

Capital optimization:

Selective loan portfolio growth

Lower interest rates & lower volatility

Lower interest rates & lower volatility Cross-selling:

More products per client

Cross-selling:

More products per client

Corporate

Loans

Loans

Overdraft accounts

Foreign Exchange / Trade Finance

Exports

ACC/ACE

Letter of Credit

Onlending

FINAME

Automatic

Guarantees

Bidding

Public tenders

Treasury

(Sales Desk)

Currencies

Investments

Local Currency

CDB/ RDB

Government Bonds

PINE Investimentos

Underwriting and Syndicated Loans

Private EquityDiscounts

Compror/Vendor

Linked Collection

Letter of Credit

Documentary Collection

Prepayment

Imports

Letter of Credit

Manufacturer

Agribusiness

Others

EXIM

Pre-shipping

Performance

Credit/Financial Institutions

Rates

Commodities

Equities

Macro Advisory

FIDC (Receivables Investment Funds)

CDI (Interbank Deposit Certificate)

LCA (Agribusiness)

q y

Credit Funds

Advisory

Letter of Credit

Advance Payments

Documentary Collection

Spot Foreign Exchange

pp g

Special Pre-shipping

Post-shipping

Automatic BNDES

FINEM

( g )

Credit Funds

Private Equity

Foreign Currency

CD -Certificate of Deposit

Foreign currency loans and investments

Loans (2,770)

Foreign Lending

Demand Deposit Accounts

Eurobonds

Custody Account

Money Market

16/32Investor Relations | August - 2010

Foreign Investments

Accounts

Time Deposit

Private Equity

Cross-selling OpportunitiesDiversity of financial instruments for the diverse needs of our customers

Credit products in local and foreign currencyLoans

Funding products in local and foreign currencyLocal deposits

Credit and Funding Products

LoansOverdraft accountsDiscountsBNDES onlendingGuarantees

Local depositsDouble index CDBLCA (Agribusiness Letters of Credit)/LCIBNDES onlendingFIDC and Credit funds

Compror/VendorACC/ACEExport Pre-paymentFinimp

Senior and subordinated local financial notesTime DepositsCD – Certificate of DepositEurobonds

Letter of Credit2,770 onlending

Subordinated notes2,770 onlending

Clients’ Sales Desk PINE Investimentos

Products for mitigating market risk mismatchesCurrencies, Commodities, Interest andIndex derivatives:

Credit StructuringSyndicated Loans

Third-parties Asset ManagementIndex derivatives:NDFOptionsSwapsStructured Options

Third-parties Asset ManagementCredit FundsPrivate Equity Funds

Corporate ServicesMergers & Acquisitions

17/32Investor Relations | August - 2010

pFX Financial Advisory

Agility in Granting Credit72-hour process in average; credit analysis may be concluded within 1 business day in special cases

CREDIT COMMITTEEStrong origination team

Presentation of proposals to the

Chief Credit Officer

Close relationship to clients and business with highrenewal ratio among clients

Cross-selling of credit products and financialproposals to the Committee

roce

ss

Platform and

and Credit Analystsg p

services

Diligent and complete credit analysis

Credit analysis, visits to clients, data

Issue of opinion

ctro

nic

Pr Regional Superintendents

Expertise and flexibility in credit structuring

Close monitoring of borrowers’ credit evolution

Reports on credit

,update, interaction with internal research team and issue of opinion

Ele

Credit AnalystAgile credit decision-making process

Management of receivables portfolio risks andcollaterals quality

Reports on credit visits and loan transactions structuring

Sales OfficerEfficient loan process, documentation andcontrols

18/32Investor Relations | August - 2010

Simple structure and flat hierarchy

Organizational Structure

Board of Directors

Internal AuditorsTikara Yoneya

Internal AuditorsTikara Yoneya

External AuditorsDeloitte

External AuditorsDeloitte

Noberto PinheiroChairman

Noberto Pinheiro Jr.Vice-Chairman

Maurizio MauroIndependent Member

Fernando AlbinoExternal Member

Mailson da NóbregaIndependent Member

Operating RisksOperating Risks

Sidney VenezianiSérgio MachadoAlcindo Itikawa

Sidney VenezianiSérgio MachadoAlcindo Itikawa

Fiscal CouncilCEONoberto N. Pinheiro Jr.

CEONoberto N. Pinheiro Jr.

Operating Risks& Compliance

Operating Risks& Compliance

Pine InvestimentosGustavo JunqueiraPine InvestimentosGustavo Junqueira

Control and Market/Liquidity Risk

Control and Market/Liquidity Risk Financial & Products

N b t Z i t JFinancial & Products

N b t Z i t JCorporate Sales

Cli B t lhCorporate Sales

Cli B t lhCredit Risk & Research

G b i l Chi tCredit Risk & Research

G b i l Chi tCorporate Operations

Uli Al t illCorporate Operations

Uli Al t illGustavo JunqueiraGustavo Junqueira q ySusana Waldeck

q ySusana WaldeckNorberto Zaiet Jr.Norberto Zaiet Jr.Clive BotelhoClive Botelho Gabriela ChisteGabriela ChisteUlisses AlcantarillaUlisses Alcantarilla

Corporate• Loan Portfolio

R$4.8 billion• 950 Clients

Corporate Credit• Analysis and granting

of credit• Credit risk monitoring

Treasury• Local• International• Sales Desk

Market and liquidity RiskHuman Resources

Credit StructuringCredit FundsFinancial Advisory

Corporate Processing and FormalizationL l

950 Clients• São Paulo• Ribeirão Preto• São José do Rio Preto• Rio de Janeiro• Curitiba• Porto Alegre• Belo Horizonte

Credit risk monitoring and analysis by sector

Sales Desk

Funding• Local• International

International• Cayman• Trade Finance

AccountingControlling Department

Private EquityDistribution

Legal

19/32Investor Relations | August - 2010

• Belo Horizonte• Recife

Trade Finance

Macro ResearchProductsInvestor Relations

Human ResourcesBanco PINE’s employees are its main assets

Performance Management and RecognitionCulture based on meritocracy100% of employees profit sharing eligibleSemiannual individual performance evaluation

QualificationMonitoring the potential of each employeeThe Bank provides continuous training actionsPINE University: programs to encourage the development, with incentives for language coursesand short-duration, graduate, MBA programs, among other

Compensation and BenefitsMeritocracy : semiannual bonus programs aligned to the Bank's strategy, by encouraging cross-selling

20/32Investor Relations | August - 2010

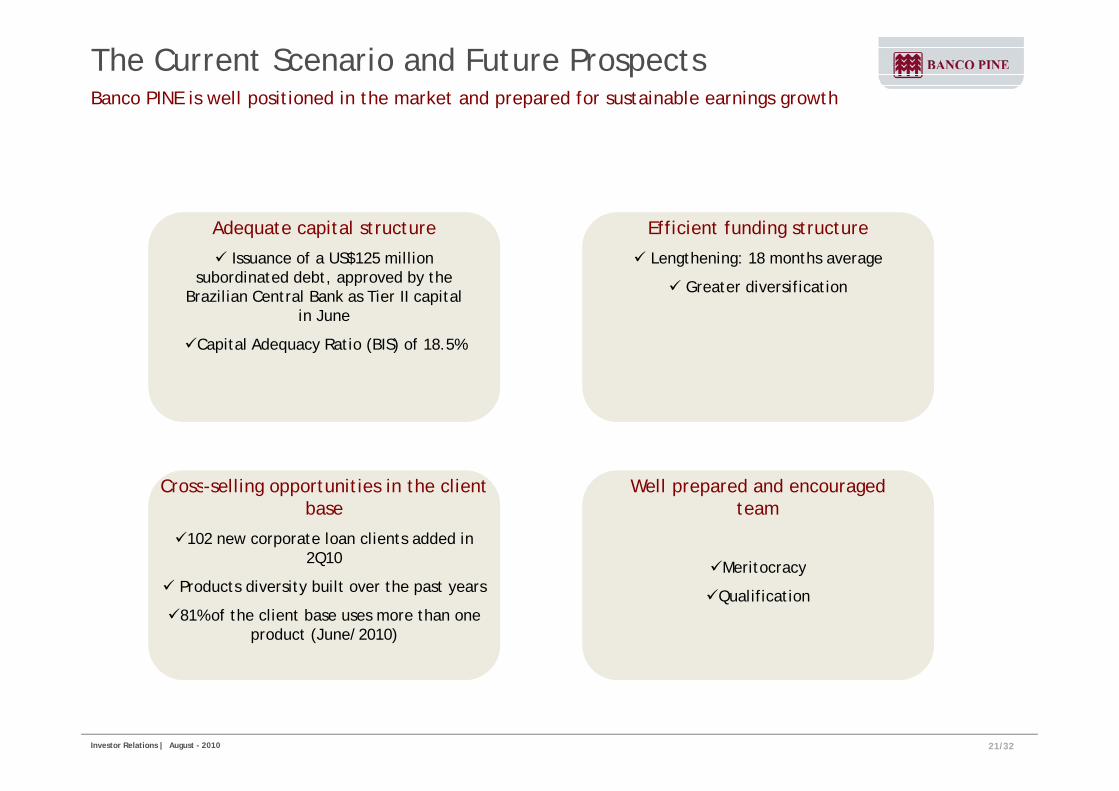

The Current Scenario and Future Prospects Banco PINE is well positioned in the market and prepared for sustainable earnings growth

Adequate capital structure

Issuance of a US$125 million subordinated debt, approved by the

Brazilian Central Bank as Tier II capital

Efficient funding structure

Lengthening: 18 months average

Greater diversification

in June

Capital Adequacy Ratio (BIS) of 18.5%

Well prepared and encouraged Cross selling opportunities in the client Well prepared and encouraged team

Meritocracy

Cross-selling opportunities in the client base

102 new corporate loan clients added in 2Q10 y

QualificationProducts diversity built over the past years

81% of the client base uses more than one product (June/2010)

21/32Investor Relations | August - 2010

Corporate Governance and Governance and

Shares

Corporate GovernanceBanco PINE adopts the best corporate governance practices

Two independent members and one external member in theBoard of Directors

Mailson Ferreira da Nóbrega: Finance Minister of BrazilClear PoliciesClear Policies Performance

MonitoringPerformanceMonitoring

Mailson Ferreira da Nóbrega: Finance Minister of Brazilfrom 1988 to 1990Maurizio Mauro: CEO of Booz Allen Hamilton and GrupoAbrilFernando Albino de Oliveira: ex-director of CVM andpartner of Albino Advogados Associados

Settlement ofResponsibilitiesSettlement of

ResponsibilitiesAlignment of

Internal PoliciesAlignment of

Internal Policies

partner of Albino Advogados Associados

São Paulo Stock Exchange Level 1 of Corporate Governance

C li ithC li ith

Fiscal Council

100% l i h f ll h h ld i l diRisk ManagementRisk Management

Compliance withLegislation and

interests

Compliance withLegislation and

interests

100% tag along rights for all shareholders, including non-voting shares

Arbitration procedures for fast settlement of litigation

23/32Investor Relations | August - 2010

Main CommitteesBanco PINE believes that the use of the best corporate governance practices substantially enhancesits business‟ outcome

Main decisions are taken by committees: Board of Directors and a structure of specific committeesNon-stop exchange of knowledge and informationT

its business outcome

Transparency

Board ofBoard ofBoard ofDirectorsBoard ofDirectors

Fiscal CouncilFiscal CouncilAudit

S tAudit

S tSupportCommittee

SupportCommittee

ExecutiveCommitteeExecutive

Committee

TreasuryCommitteeTreasury

Committee

National andForeign Funding

National andForeign Funding CreditCredit RetailRetail

Complianceand Basel

Complianceand Basel

PINE Investimentos

PINE InvestimentosCommittee

(ALCO)Committee

(ALCO)Products

CommitteeProducts

CommitteeCommitteeCommittee CommitteeCommittee

DelinquencyC ittDelinquencyC itt

RiskCommittee

RiskCommittee

PerformanceEvaluation

PerformanceEvaluation Ethics

C ittEthics

C ittIT

C ittIT

C itt

HumanResources

HumanResources

InvestimentosCommittee

InvestimentosCommittee

24/32Investor Relations | August - 2010

CommitteeCommitteeCommitteeCommittee CommitteeCommittee CommitteeCommitteeCommitteeCommittee

Ownership StructureOn July 1, BM&FBovespa granted Banco PINE’s request for an extension of the deadline for complying with the minimum free-float requirementcomplying with the minimum free float requirement

Base: 07/30/2010Base: 07/30/2010

Common Preferred Total %

Noberto Nogueira Pinheiro 45,443,872 14,490,556 59,934,428 70.2%

Management - 2,631,243 2,631,243 3.1%

Free Float - 20,768,595 20,768,595 24.3%

Subtotal 45,443,872 37,890,394 83,334,266 -

Treasury 2 074 839 2 074 839 2 4% Treasury - 2,074,839 2,074,839 2.4%

Total 45,443,872 39,965,233 85,409,105 100.0%

The Bank shall maintain at least 24.3% free float until January 10, 2011

Should free float exceed 24.3% at any time before January 10, 2011, the Bank will notpermit a reduction of this level

25/32Investor Relations | August - 2010

Shareholders’ ProfileShareholders' profile change since the crisis

2007IPO

F i IForeign Investors

78.4%Foreign Investors

78.4%

InstitucionalInstitucional

39.7% 39.5%

39.5%

39.8%40.5%

41.0%42.0% 41.6% 41.7%

39 3%

40.7%40.3% 40.1% 40.1% 39.6%

39.8%

Foreign Investors

InstitucionalInvestors12.9%

InstitucionalInvestors12.9%

37.8%38.3% 38.4% 38.5%

39.3%38.6% 38.4% 38.2% 38.1% 38.0%

37.3%

Institutional Investors

Individuals8.7%

Individuals8.7% 21.1%

21.9% 21.5% 21.4% 21.5% 21.4%20.9%

20.4%21.1% 20.8%

19.9%20.4%

21.0%

Individuals

Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10

26/32Investor Relations | August - 2010

The Price/Book Value multiple was 1.17x on August 20, 2010The Price/Book Value multiple was 1.17x on August 20, 2010

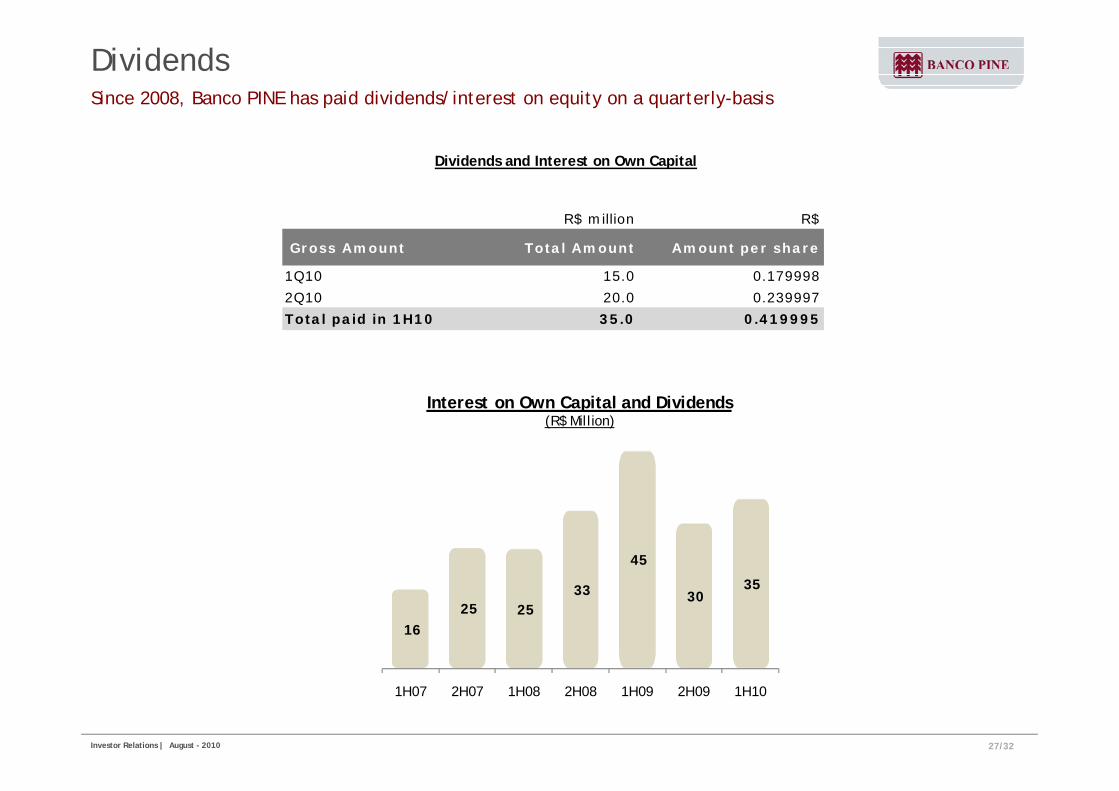

DividendsSince 2008, Banco PINE has paid dividends/interest on equity on a quarterly-basis

Dividends and Interest on Own Capital

R$ million R$ R$ million R$

Gross Amount Total Amount Amount per share

1Q10 15.0 0.179998

2Q10 20.0 0.239997

l d d d

Total paid in 1H10 35.0 0.419995

Interest on Own Capital and Dividends (R$ Million)

45

16 25 25

33 30 35

27/32Investor Relations | August - 2010

1H07 2H07 1H08 2H08 1H09 2H09 1H10

Social ResponsibilityBanco PINE supports and promotes the Brazilian culture

SocialCasa HopeInstituto Alfabetização Solidária

CultureA Cidade e a Rosa: retrospective of the artistPaulo Von Poser

Instituto Sedes SapientiaeInstituto Casa da Providência Paisagem e Olhar (Landscape and View):

featuring watercolors of the biodiversity of theRainforest

SportsMinas Tênis Clube: training program forathletesPasse de Mágica: created in 2004 by MagicP l d B f B ili b k tb ll

Embarcações (Typical Vessels of the Brazilian Coast):registers the beauty of vessels from north to south of Brazil

Paula and Branca, former Brazilian basketballplayers, to offer basketball instruction forchildrenProjeto Rede Atletismo Novos Talentos:(New Talent Athletics Network Project)

i i f hl d l d dResponsible Credit

training program for athletes developed andmaintained by the Aquarela Foundation

Green Building

“Lists of Exceptions”: the Bank does not finance – withmultilateral organizations lines - projects or those organizationsthat damage the environment, are involved in illegal laborpractices or produce, sell or use products, substances or

ti iti id d j di i l t i tactivities considered prejudicial to society.

System of environmental monitoring, financed by the IADB andcoordinated by FGV, and internally-produced sustainabilityreports for corporate loans.

28/32Investor Relations | August - 2010

Rating upgrade by FitchConsistent performance and credit quality

On May 24, Fitch Ratings, one of the main international ratings agencies, raised PINE's ratings as follows:

Long-Term Local and Foreign Currency IDR from “B+” to “BB-”National Long-Term rating from “A-(bra)” to “A(bra)”National Short-Term rating from “F2(bra)” to “F1(bra)”Individual rating from “D” to “C/D”

The agency attributed the improvement in ratings due to the following factors :

Bank's consistent performance during the global financial crisisAdequate credit qualityConsistent risks and credit manageFavorable capitalization ratiosp

According to the agency, “the Bank’s rating reflects its agility in adapting to economic volatility, itsstrategy of consistently managing risks and balance sheet adjustments”.

Additionally, "since the second half of 2009, Pine resumed focus on Corporate credit growth (...) and alsoexpanded revenues from cross-selling with the Treasury, addressed to its customers, and services financialadvisory”.

29/32Investor Relations | August - 2010

Market recognition

Events and Highlights of the Period

Banco PINE is one of the top 15 banks in Brazil in terms of Corporate Loans, according to the 2010edition of Melhores e Maiores, from Exame magazine

Banco PINE was considered the Best Commercial Bank in Brazil by World Finance Banking AwardsThe award was created by British magazine World Finance. Among the factors analyzed were:

l f l d f l h d fl b l d h dsolutions for clients and optimization of relationships, innovation and flexibility and staying aheadof the competition.

30/32Investor Relations | August - 2010

Banco PINEPioneering spirit, solid and transparent, with the agility that companies need

The first Brazilian bank of itssize to go public

One of the 15 largest banks inCorporate loans, noted for itsCorporate loans, noted for itsgood management during thecrisis

Cl ibl dClear, accessible andconsistent information

31/32Investor Relations | August - 2010

Investor Relations

Norberto Zaiet Júnior

CFO

Clive Botelho

Corporate Sales Executive Vice-president

Nira Bessler

Head of Investor Relations

Alejandra Hidalgo

Investor Relations Analyst

Phone: +55-11-3372-5553 / 5552

www bancopine com br/irwww.bancopine.com.br/ir

32/32Investor Relations | August - 2010

This presentation contains forward-looking statements relating to the prospects of the business, estimates for operating and financial results, and those related to growth prospects of Banco Pine. These aremerely projections and, as such, are based exclusively on the expectations of Banco Pine’s management concerning the future of the business and its continued access to capital to fund the Company’sbusiness plan. Such forward-looking statements depend, substantially, on changes in market conditions, government regulations, competitive pressures, the performance of the Brazilian economy and theindustry, among other factors and risks disclosed in Banco Pine’s filed disclosure documents and are, therefore, subject to change without prior notice.